Embed Size (px)

Citation preview

The Pittsburgh Economy

Challenges and Innovations

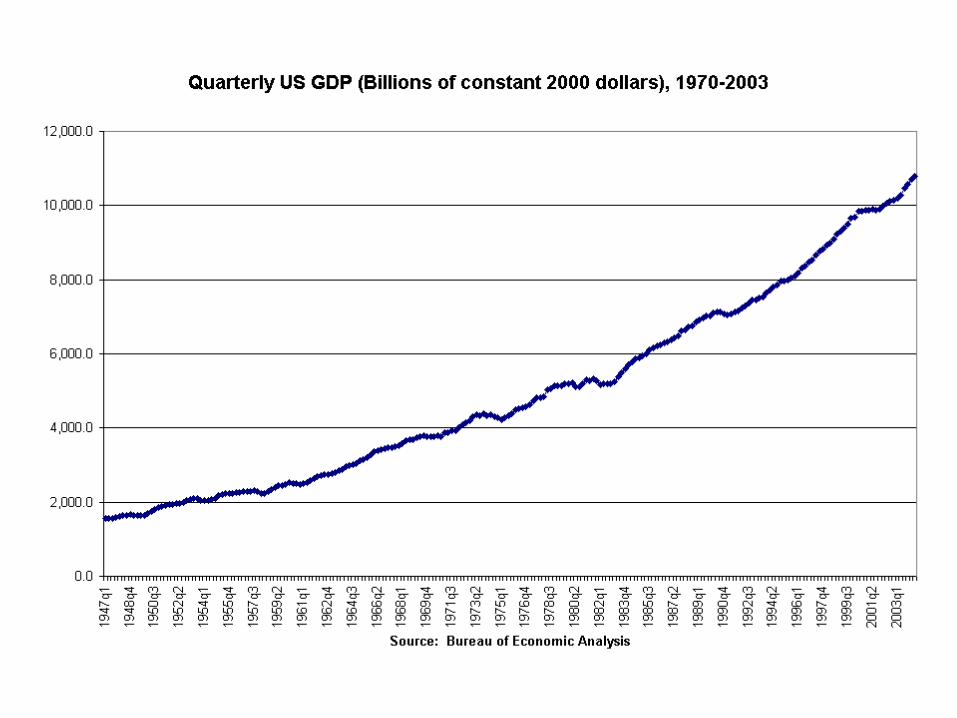

Corporate Profits

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

2001-I 2001-II 2001-III 2001-IV 2002-I 2002-II 2002-III 2002-IV 2003-I 2003-II 2003-III 2003-IV 2004-I 2004-II

Source: U.S. Bureau of Economic Analysis

Bill

ion

s o

f D

olla

rs

Corporate profits have increased by more than $395 Billion!

Bush signed the tax cut bill on June 7, 2001

Jobs Created vs. Jobs Needed

122,000

124,000

126,000

128,000

130,000

132,000

134,000

136,000

138,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

2001 2002 2003 2004

Source: US Bureau of Labor Statistics

Th

ou

san

ds

of

Job

s

Actual Needed

Jobs created in 2004 have narrowed the jobs gap to more than 5.1 million jobs, down from a 7 million jobs deficit in 2003.

Key Points

Details on the transition Resources and programs Defining cluster connections Effective cluster policy

Initial Development Efforts

Smoke and Flood Control– 1907 – Chamber of Commerce– 1911 – Pittsburgh Industrial Development

Corporation

Rebuild Industrial Infrastructure– 1956 Pennsylvania Governor George Leader

created PA Industrial Development Authority

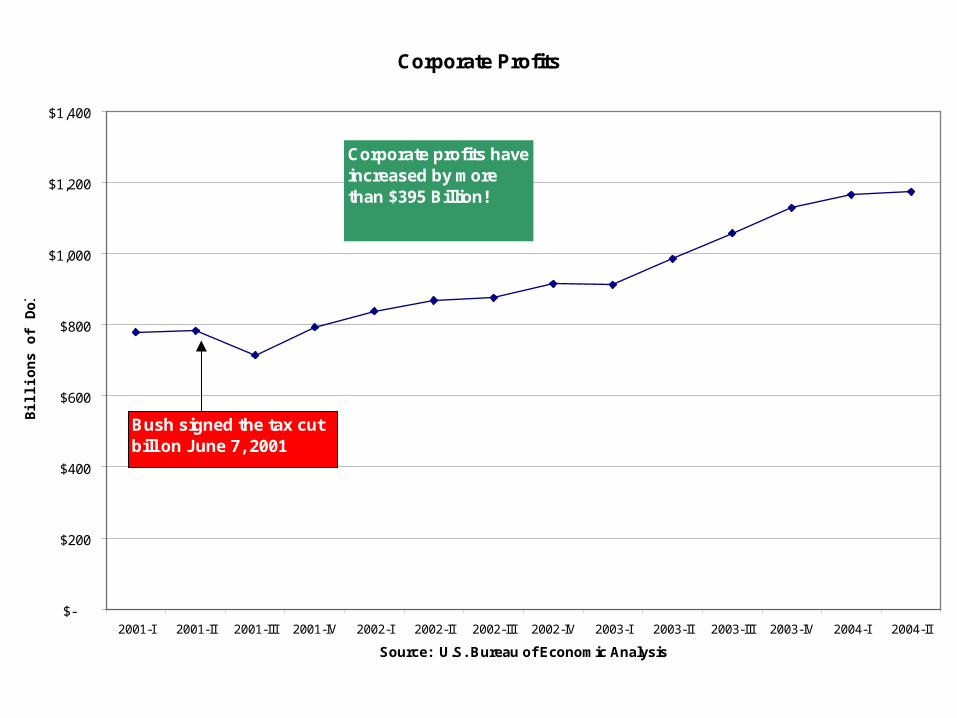

Change in Manufacturing, 1967-1992

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

Estab

lishm

ents

Emplo

yees

Tota

l Pay

roll

Produ

ction

Em

ploye

es

Produ

ction

Hou

rs

Produ

ction

Wag

es

Value A

dded

Capita

l Exp

endit

ures

Cost o

f Mat

erial

s

Value

of S

hipm

ent

Estim

ated

Pro

fit*

Restructuring

Change in Manufacturing

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

1958-1967 1967-1977 1977-1987 1987-1992

Establishments

Employees

Total Payroll

Recovery

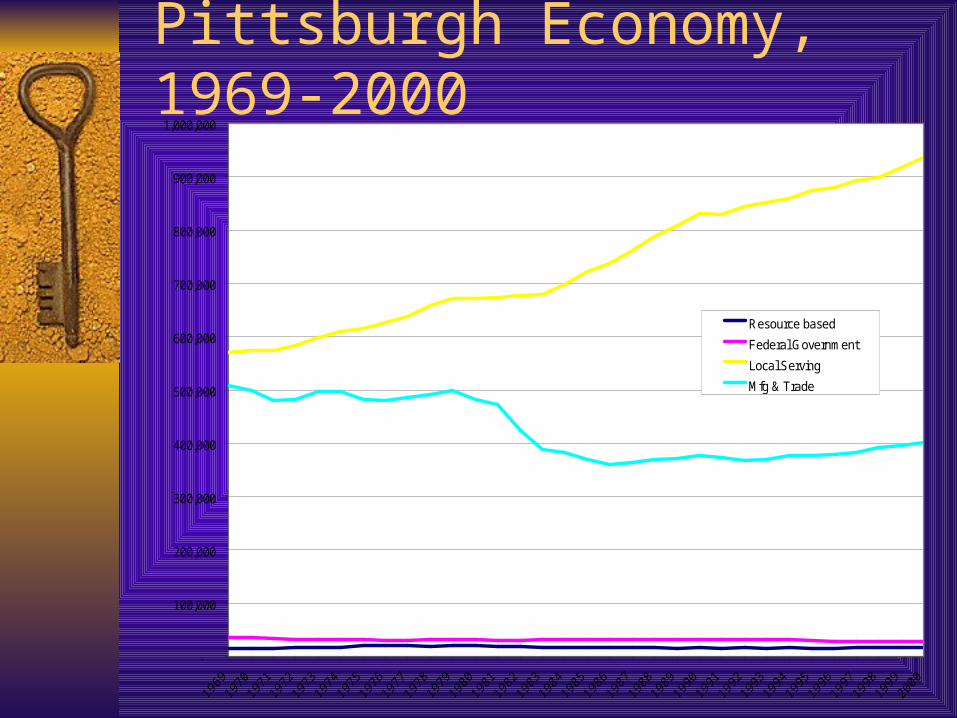

Pittsburgh Economy, 1969-2000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Resource based

Federal Government

Local Serving

Mfg & Trade

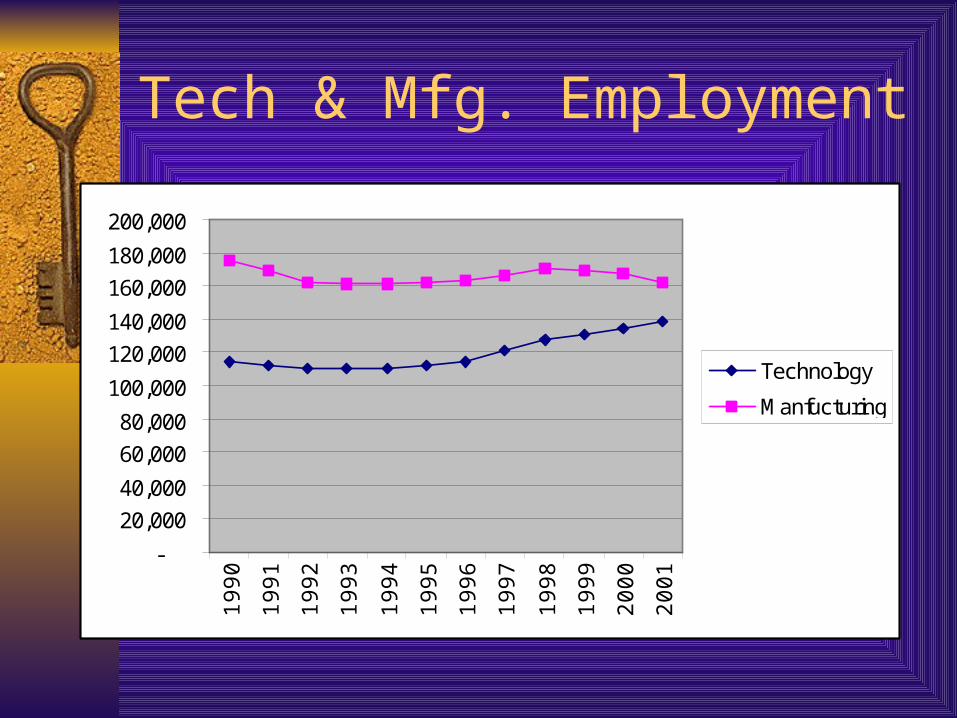

Tech & Mfg. Employment

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,00019

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Technology

Manfucturing

TimelineStrategic Role 1983 1987 1988 1994 1996 1998 1999 2000 2001 2002 2003Biomedical Pittsburgh

Biomedical Development Corporation

Pittsburgh Tissue Engineering Iinitiative

LaunchCyte Limbach Center McGowan Institute Pittsburgh Life Sciences Greenhouse

Pittsburgh NMR Center for Biomedical Research

Entrepreneurship Pittsburgh Seed Fund

PantherlabWorks

The Enterprise Corporation

General Pittsburgh Regional Alliance

Information Technology Pittsburgh Digital Greenhouse

Idea Foundry Robotics Foundry

Manufacturing SPIRC (Catalyst Connection)

Pittsburgh Gateways

Technology Pittsburgh High Technology Council (PHTC)

Ben Franklin Technology Center (Innovation Works) Innovation Works

1980s Development Focus

Legacy of Big Steel Technology

– Materials, instruments, environmental Research and Development

– Bio-medical technology, information technology

Services– Finance– Healthcare

Team PA

SMC

Tech/ExtensionServices

Site Selection

Assistance

Finance & Incentives

Site DevelopmentCornerstone

Special Init. Workforce&

Talent

PRA

Cornerstone

RIDC

Permits andRegulatoryAssistance

PRA/WFC

PTC

WIB

IDC/URA

DCED / GAT

Catalyst

SPC

PRA

Cornerstone

Special Init.

RIDC

Commercial Real Estate

Catalyst

Special Init.

Networking& Industry

Info.

PTC

PRA

County/ Cornerstone

Navigators Marketing/Prospecting

PRA

Special Init.Catalyst

GAT

IW

Team PA

GAT

IW

Industry Legend

All

Spike

Technology

Special Initiatives

Manufacturing

Start-ups

EAN

Comm R.E.

Chamber

SBDCs

Business & Mgmt

Consulting

IW

Special Init.

Catalyst

Identify Needs

Identify Prospects

Services Overview

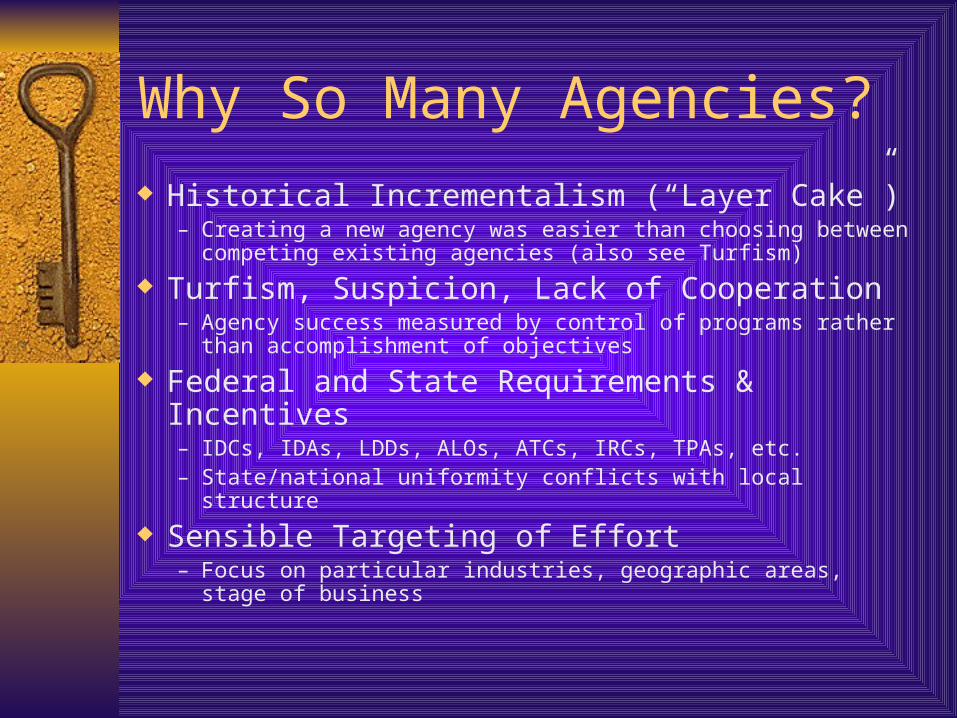

Why So Many Agencies?

Historical Incrementalism (“Layer Cake”)– Creating a new agency was easier than choosing between

competing existing agencies (also see Turfism)

Turfism, Suspicion, Lack of Cooperation– Agency success measured by control of programs rather than

accomplishment of objectives

Federal and State Requirements & Incentives– IDCs, IDAs, LDDs, ALOs, ATCs, IRCs, TPAs, etc.– State/national uniformity conflicts with local structure

Sensible Targeting of Effort– Focus on particular industries, geographic areas, stage of business

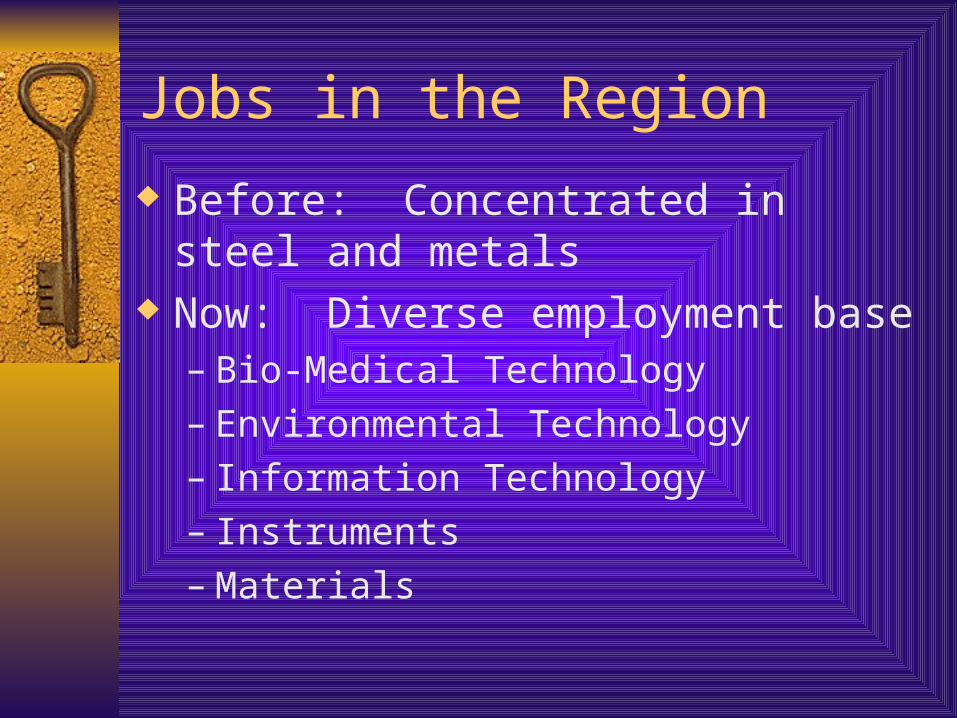

Jobs in the Region

Before: Concentrated in steel and metals Now: Diverse employment base

– Bio-Medical Technology– Environmental Technology– Information Technology– Instruments– Materials

1994-1998 Pittsburgh Region New Business Starts Per 10,000 Employees

0

2

4

6

8

10

12

14

16

1994 1995 1996 1997 1998

Year

To

tal

Sta

rts

Per

10,

000

Em

plo

yees

Source: Dun and Bradstreet, Bureau of Labor Statistics

Our rate of business starts is falling.

Business Creation

Small Business Development

Business Plans – Small Business Development Centers (SBDCs)– University of Pittsburgh– Chrysler Center, Duquesne University– St. Vincent College

Marketing– Don Jones Center

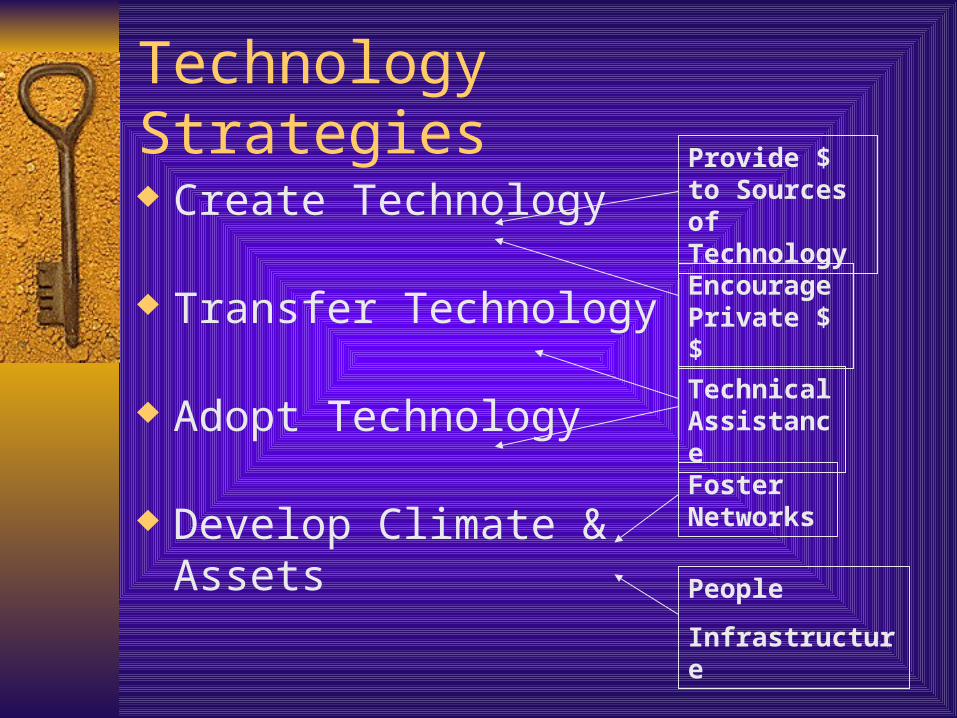

Technology Strategies

Create Technology

Transfer Technology

Adopt Technology

Develop Climate & Assets

Provide $ to Sources of TechnologyEncourage Private $$

Foster Networks

Technical Assistance

People

Infrastructure

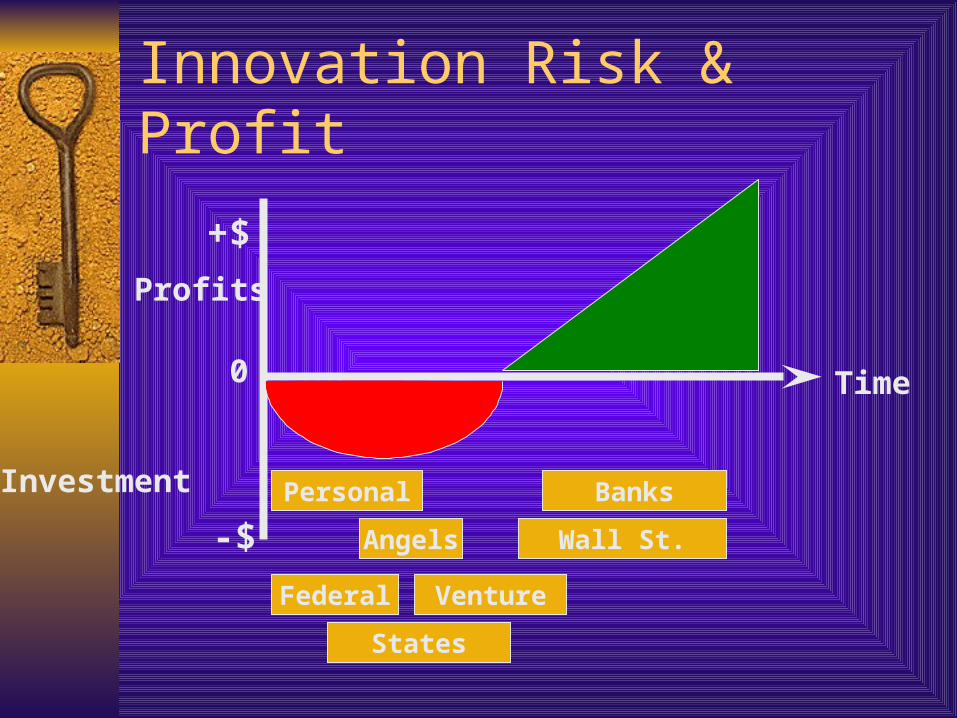

Innovation Risk & Profit

Time

+$

0

-$

Profits

Investment Personal

Federal

Banks

Angels

Venture

Wall St.

States

Finance For Startups

Federal– SBIR – Small Business Innovation Research– SBICs – Small Business Investment Companies

State– Opportunity Grants (PA)– Ben Franklin Partners – Innovation Works

Venture Capital

Innovation Works

A Pennsylvania Ben Franklin Partner Max of $100,000 for prototype and proof of

concept (x3) Max of $300,000 for market entry Equity investments up to $500,000 Disburse $1.5M per quarter Quarterly cycle, 60-90 day turn-around

BFP Impacts, 1983-1992

$-

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

$35,000,000

$40,000,000

$45,000,000

$50,000,000

Bio Info Tech Devices Env Tech Materials Chem & Ind Automation

Cu

rren

t D

olla

rs

-

100

200

300

400

500

600

700

Job

s

Technology Funds Technology Jobs

Pittsburgh Venture Investment

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Source: Thomson Financial VenturEconomics/NVCA

Inve

stm

ent

($ M

)

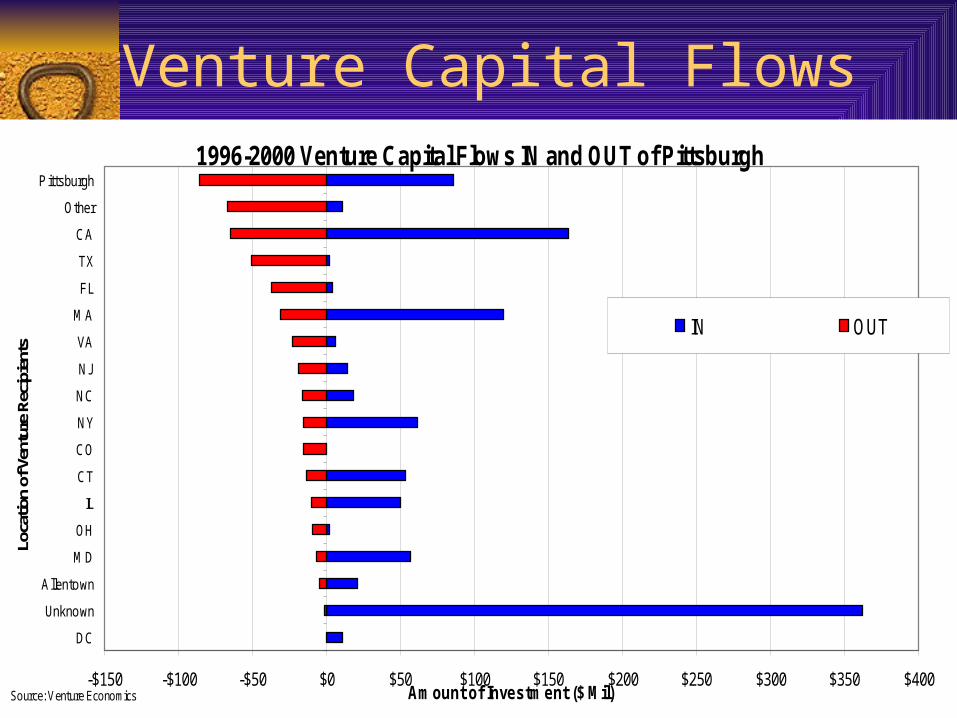

1996-2000 Venture Capital Flows IN and OUT of Pittsburgh

-$150 -$100 -$50 $0 $50 $100 $150 $200 $250 $300 $350 $400

DC

Unknown

Allentown

MD

OH

IL

CT

CO

NY

NC

NJ

VA

MA

FL

TX

CA

Other

P ittsburgh

Loca

tion

of V

entu

re R

ecip

ient

s

Amount of Investment ($ Mil)

IN OUT

Source: Venture Economics

Venture Capital Flows

Catalyst Connection A Pennsylvania Industrial Resource Center and NIST

Manufacturing Extension Partner Catalyst Connection provides customized consulting

services to small and medium-sized manufacturers– Financial

– Information Technology

– Lean Manufacturing

– Market Development

– Quality Systems

– Web Enhancement

– Workforce

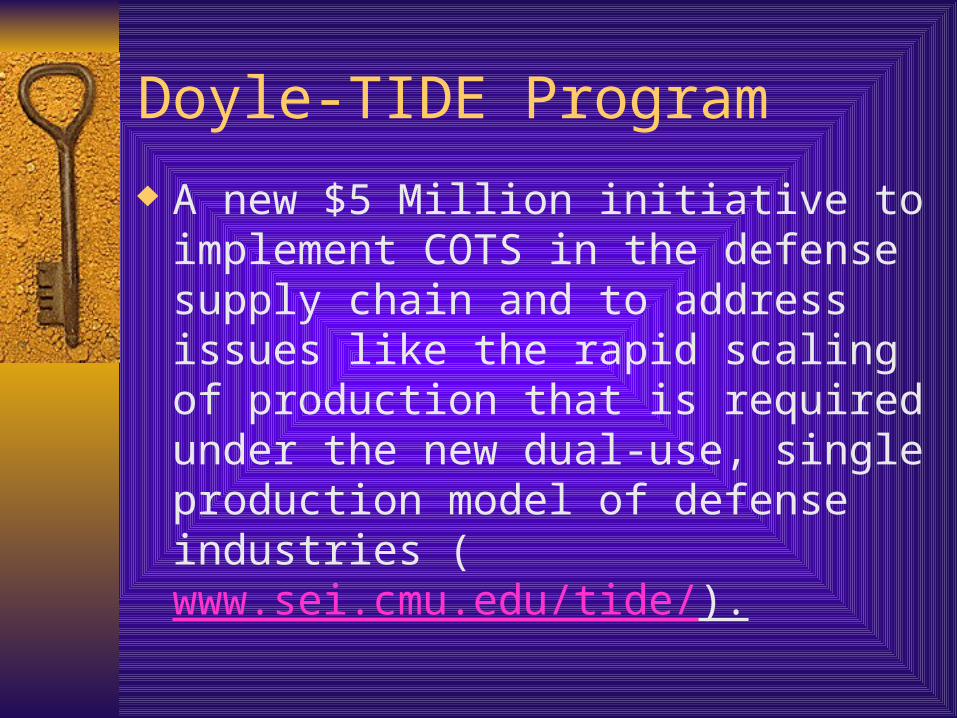

Doyle-TIDE Program

A new $5 Million initiative to implement COTS in the defense supply chain and to address issues like the rapid scaling of production that is required under the new dual-use, single production model of defense industries (www.sei.cmu.edu/tide/).

The transition from manufacturing to Life Sciences

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

ManufacturingHealth & Life Sciences

Life Science Employment

-

50,000

100,000

150,000

200,000

250,000

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

Research & Testing Labs

Drug Distribution

Electronics, Instruments & Devices

Metals

Plastic & Glass

Chemicals & Drugs

Textiles & Filters

Health Services

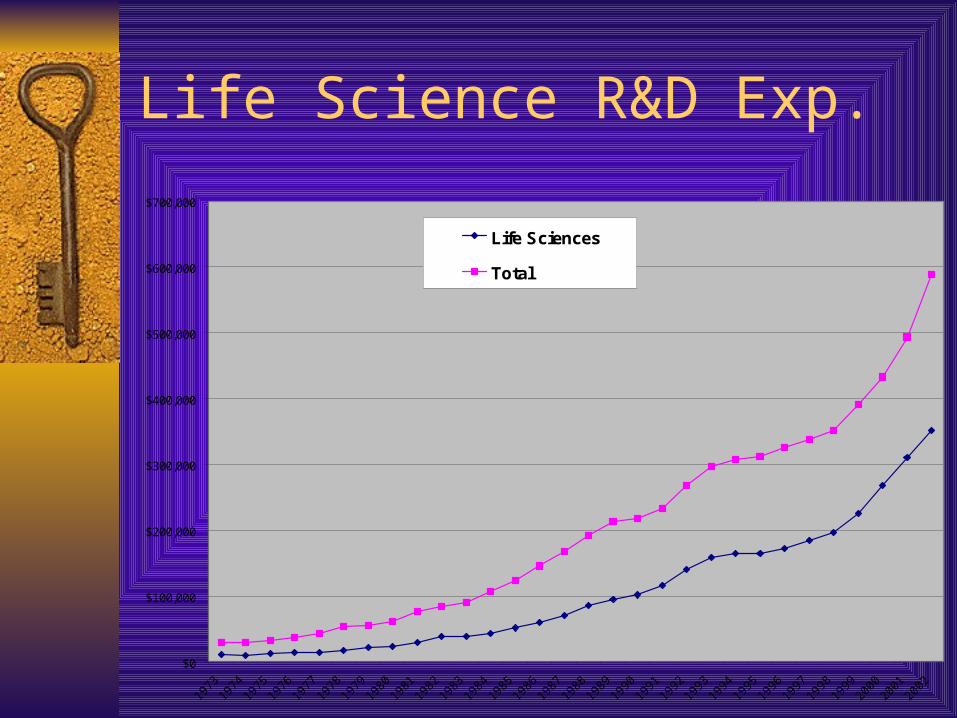

Life Science R&D Exp.

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Life Sciences

Total

Pittsburgh’s areas of strengthEmployment Growth in Life Sciences, 2001-2002

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

Health Services Instruments and Devices Medical Equipment andSupplies

Pharmaceuticals Research

Life Science Clusters

Per

cen

t C

han

ge

Pittsburgh United States

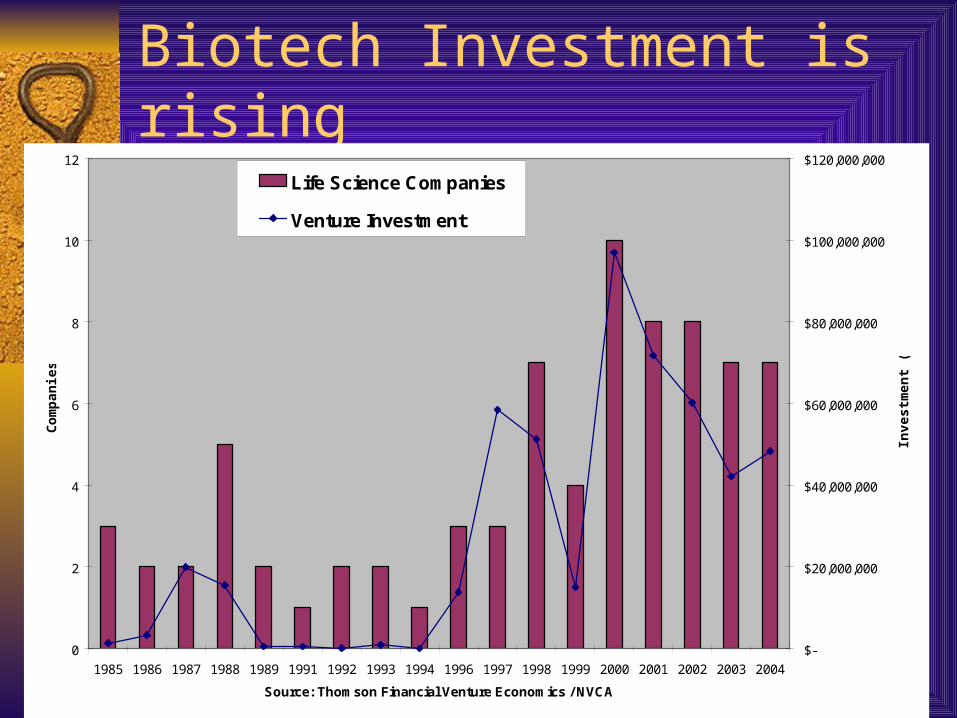

Biotech Investment is rising

0

2

4

6

8

10

12

1985 1986 1987 1988 1989 1991 1992 1993 1994 1996 1997 1998 1999 2000 2001 2002 2003 2004

Source: Thomson Financial Venture Economics / NVCA

Co

mp

anie

s

$-

$20,000,000

$40,000,000

$60,000,000

$80,000,000

$100,000,000

$120,000,000

Inve

stm

ent

($)

Life Science Companies

Venture Investment

Biotech Convergence

IT joining a new wave of Biotech Leverages Region’s Life Sciences R&D Center for Biomedical Informatics

(University of Pittsburgh) Pittsburgh Tissue Engineering Initiative BioVenture / Life Sciences Greenhouse

Human Capital and Amenities

Tech / Innovative Industries Growing Knowledge worker in high demand Areas with skilled labor attract good jobs Knowledge workers can choose their location Amenities / Quality of life become more important Education and Training are critical

– Highly competitive markets

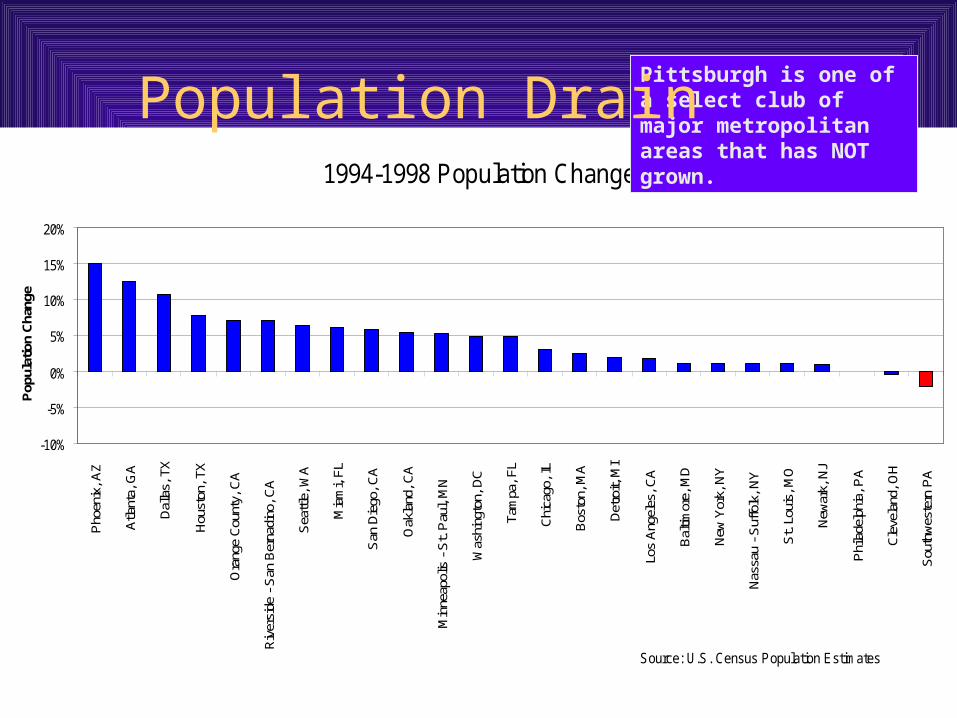

1994-1998 Population Change

-10%

-5%

0%

5%

10%

15%

20%

Pho

enix

, AZ

Atla

nta,

GA

Dal

las,

TX

Hou

ston

, TX

Ora

nge

Cou

nty,

CA

Riv

ersi

de -

San

Ber

nadi

no, C

A

Sea

ttle,

WA

Mia

mi,

FL

San

Die

go, C

A

Oak

land

, CA

Min

neap

olis

- S

t. P

aul,

MN

Was

hing

ton,

DC

Tam

pa, F

L

Chi

cago

, IL

Bos

ton,

MA

Det

roit,

MI

Los

Ang

eles

, CA

Bal

timor

e, M

D

New

Yor

k, N

Y

Nas

sau

- Suf

folk

, NY

St.

Loui

s, M

O

New

ark,

NJ

Phi

lade

lphi

a, P

A

Cle

vela

nd, O

H

Sou

thw

este

rn P

A

Pop

ulat

ion

Cha

nge

Source: U.S. Census Population Estimates

Pittsburgh is one of a select club of major metropolitan areas that has NOT grown.

Population Drain

People Do Matter

Region continues to lose population, albeit slowly

PSU study shows that disproportionate share of losses are young, well-educated

Push for amenities is in full swing Chicken and Egg –

– Jobs bring people OR– People attract job

What attracts them?

High quality, high paying jobs at cool companies still #1

Depth of job opportunity in local market Quality of life

– Coolness– Amenities – music, outdoor activities, culture– Diversity (or perceived openness to it)

The End

Thank you