Embed Size (px)

Citation preview

INDUSTRY REPORT

A supplement to Shopper Marketing magazine

The New Aisle: Emerging Trends in Online Grocery Shopping

Packaged goods marketers need no longer wait to see if consumers will embrace the concept of online grocery shopping. They already have. There’s no dismissing the fact that consumers are starting to view online purchases as a viable option for meeting their packaged goods needs — not to replace brick-and-mortar stores, but to supplement and improve their previous shopping behavior. Sales totals are admittedly low at this stage: Online shoppers spent $8.7 billion on health & personal care products and $4.4 billion on food and beverages in 2011, according to the U.S. Department of Commerce. Overall, online shopping represented about $12 billon during the year, or roughly 2% of all CPG sales, according to The Nielsen Co. But one-third of consumers already buy grocery products online, according to proprietary research commissioned by Integrated Marketing Services, the shopper marketing arm of Advantage Sales & Marketing. They’re buying across all product categories. And it’s not just Gen Y Millennials weaned on digital technology who are making the purchases, but also members of the Gen X and Baby Boomer generations who are finding convenience and the perception of better deals online.

PRESENTS:

“As retailers have built

out their presence ...

we’ve seen the lines

between the online

shopper and traditional

shopper begin to blur.”– Kristin Wonzen,

Director of Marketing, E-Commerce, Clorox Co.

12P2P_CDM_IntegratedPaper.indd 1 5/15/12 8:58 AM

2

“We’re at the dawn, both for consumers and for CPGs,” says Elizabeth Fogerty, vice president of insights and strategy development at Integrated, Norwalk, CT. “It’s time to test and learn, because the choices we’re facing are many and varied.” “E-commerce is now a channel for consumer products,” says Kristin Wonzen, director of marketing, e-commerce for Clorox Co. “We’re seeing real material sales out there for some of our products, and it’s growing faster than any other channel we have.” While no one expects a sudden, massive migration to online grocery shopping in the next few years (the revolutionary shifts in consumer behavior sparked elsewhere by digital technology likely won’t take place here), consumers are steadily embracing the notion of buying groceries online — shampoo, detergent, soup and soda, if not bananas and lettuce as well. Retailers and product marketers, meanwhile, are developing strategies for catering to grocery shoppers

who may very well prefer to avoid parking lots and checkout lines, or who might simply be happy to eliminate store trips from their busy schedules. “The expansive opportunities in the e-commerce space have us excitedly working on a long-term strategy,” says Kelly Downey, Unilever’s vice president, strategic growth channels. Increasingly, CPG marketers are actively helping traditional retail partners move into the digital space while also stepping up collaborative activity with leading e-tailers. As often has been the case in the world of digital shopper marketing, the trickle of e-commerce collaboration seen in 2011 turned into a steady wave of activity in the first half of 2012. And that wave will continue to grow. Grocery retailers, who until recently had dabbled in e-commerce almost begrudgingly, are now making it a strategic goal. In addition, strategies that initially focused

on supplementing the physical store by emphasizing broader selections and slow-moving inventory unworthy of shelf space now are expanding to cover any item in the warehouse. “This is brand new for us,” Dollar General chief executive officer Rick Dreiling admitted in fall 2011, as the retailer launched e-commerce capabilities.

“We do know there’s demand for it. But I just don’t know enough yet about what it’s going to generate.”

A New TackUntil recently, most digital shopper marketing activity focused on driving sales to bricks-and-mortar stores. With ever-more consumers using digital tools to inform their store choices and purchase decisions, marketers have adopted various methods of reaching shoppers during pre-trip, planning mode. The idea has been to influence their decisions before they get to the store. However, near the end of 2011, the Path to Purchase Institute observed marketers acknowledging that consumers don’t always make it to the store, and therefore beginning to more openly employ tactics that directly drive online sales. To cite just a few recent examples:

MeanAmount

Monthly Spending Patterns Q: How much money do you spend on groceries in a typical month for your household?

Source: Integrated Marketing Services, 2012

Share ofTotal

Boomers Gen X Gen Y

(n = 203) (n = 200) (n = 200)

$418$473

$413

Online3%

In-Store97%

Online4%

In-Store96%

Online6%

In-Store94%

INDUSTRY REPORT

12P2P_CDM_IntegratedPaper.indd 2 5/15/12 8:58 AM

• InMarch,UnileveractivateditsNationalCollegiateAthletic Association sponsorship by staging a brand showcase on Target.com that leveraged various basketball-themed assets to promote the Dove Men+Care portfolio. The webpage contained two noteworthy marketing messages that were not present one year earlier, when Unilever and Target joined for a similar promotion. The first was a call to

“get free shipping on all Dove Men+Care products.” The second was a link to immediately buy those products online.

• Thatsamemonth,AholdUSA-ownedhomedelivery service Peapod placed coded transit ads on Philadelphia train platforms that let commuters shop for groceries in the morning and schedule a home delivery for later that day. “We want to make it easier to grocery shop anywhere, anytime

— even while waiting for the train,” Peapod chief operating officer Mike Brennan said.

• Amongnumerousaccount-specificoverlaysfortheApril 2012 launch of Tide Pods, Procter & Gamble teamed with Dollar General for a co-op FSI in Sunday newspapers that offered a free sample of the new product with purchase of “anything” on dollargeneral.com.

Ahold’s Plan to Reshape RetailExecutives at Ahold USA want to reconstruct the supermarket business to give 21st century shoppers three options for stocking their pantries: buying groceries at the supermarket in the traditional way, ordering them online for home delivery, or ordering them online for pick-up at the store or elsewhere. “The average customer is going to employ all three options at different times,” chief commercial and development officer James McCann said last fall, as the company announced its long-term strategic plans. “Moms tell us it’s more efficient to pick up groceries at the store than to wait at home two hours for a delivery.” Shoppers who are willing to wait at home can avail themselves of Peapod, the Internet-based home delivery service that Ahold acquired in 2000. Operating in 12 East Coast and Midwest states, Peapod has roughly $450 million in annual sales and gives Ahold an operational leg up on competitors who have to build such distribution services from scratch. (There are good reasons why Walmart and Amazon haven’t expanded their respective home delivery services beyond the initial test markets.) Ahold plans to align Peapod with its 750 brick-and-mortar stores to create a network of pick-up locations, creating a “fulfillment factory” that caters both to shoppers willing to pay extra for the full convenience of home delivery (Peapod charges $6.96 to $9.95, depending on ticket size) and those seeking cheaper options. “Home delivery serves a niche, but most families can’t afford it,” McCann said. “If we can get prices to the same as in stores, we are going to see huge increases” in online orders, he predicted. The retailer plans to test a number of “click-and-collect” business models in 2012 and roll out the concepts that work best in 2013. Its first “Curbside Pick-Up” service opened at a new Stop & Shop in Chelmsford, MA, last November. (A free introductory offer is billed as a “$4.95 value.”)

3

12P2P_CDM_IntegratedPaper.indd 3 5/15/12 8:58 AM

4

• LastNovember,H.J.HeinzintroducedHeinz Tomato Ketchup with Balsamic Vinegar to the world by making the new SKU available exclusively through the brand’s Facebook page for direct-to-home delivery. The initiative was explained as a way to gauge consumer interest in the product before attempting a rollout to retail outlets. In early 2012, the product became available at two retailers: Walmart and Amazon.

“Two years ago, the vast majority of our work was only focused on driving in-store sales. Today, everyone [still] wants the opportunity to engage with shoppers, but they also want to offer that ‘buy’ button,” says Greg Murtaugh, chief executive officer of Triad Retail Media, a digital agency that develops brand advertising for CPGs on traditional retailer sites such as walmart.com and cvs.com. Triad also is helping e-tailing giant eBay move into the packaged goods arena. “Shoppers have gone beyond shopping across channels to discovering brands across media,” says Valerie Bernstein, vice president, client services at Integrated. “And when you consider that the center of gravity for discovery/info gathering has shifted toward digital

Goliath vs. GoliathAlthough Amazon.com is keeping its plans close to the vest (the company declined to be interviewed for this report), it’s been well reported that the “category-killer killer” has set its sights intently on the CPG marketplace. That’s why the e-tailer that began life in 1995 as the “world’s largest bookstore” acquired Quidsi and its Diapers.com and Soap.com operations in 2011; continues to experiment with an “Amazon Fresh” delivery service in hometown Seattle, WA; serves as a fulfillment house for P&G’s direct-sales ventures on Facebook; and offers the most comprehensive pages of CPG product information available anywhere. Since the company doesn’t break out sales figures, it’s not quite clear how big a player Amazon already is; packaged goods were a portion of the $17.3 billion in “electronics and other general merchandise” it sold in 2011. (A recent Reuters story quoted an Amazon executive stating that 4% of customers buy packaged goods; a recent Advertising Age article indicated that Amazon was among the top five U.S. accounts for P&G’s Pampers.) By comparison, Walmart.com generates an estimated $8 billion in total online sales, with packaged goods a relatively new endeavor for the operation. Hiding behind all the flashy benefits of the Amazon Prime loyalty program (such as instant access to movies and e-books) is free two-day shipping, a feature that eliminates one key drawback to online grocery shopping: waiting a long time for your Tide, Dove or Cottonelle to arrive. Membership costs $79 annually. LikeAmazonFresh,WalmarttoGoisahomedeliveryservice that the retailing giant has been testing in the San Jose, CA, market since April 2011. But Walmart.com has something that Amazon.com does not: 3,868 U.S. stores that can be used as delivery points or fulfillment centers for online orders. The retailer also recently introduced a self-explanatory “Homefree” service that mails shelf-stable grocery orders of at least $45 in three to five days; shoppers also can opt for same day/next day pickup at a store.

INDUSTRY REPORT

12P2P_CDM_IntegratedPaper.indd 4 5/15/12 8:58 AM

5

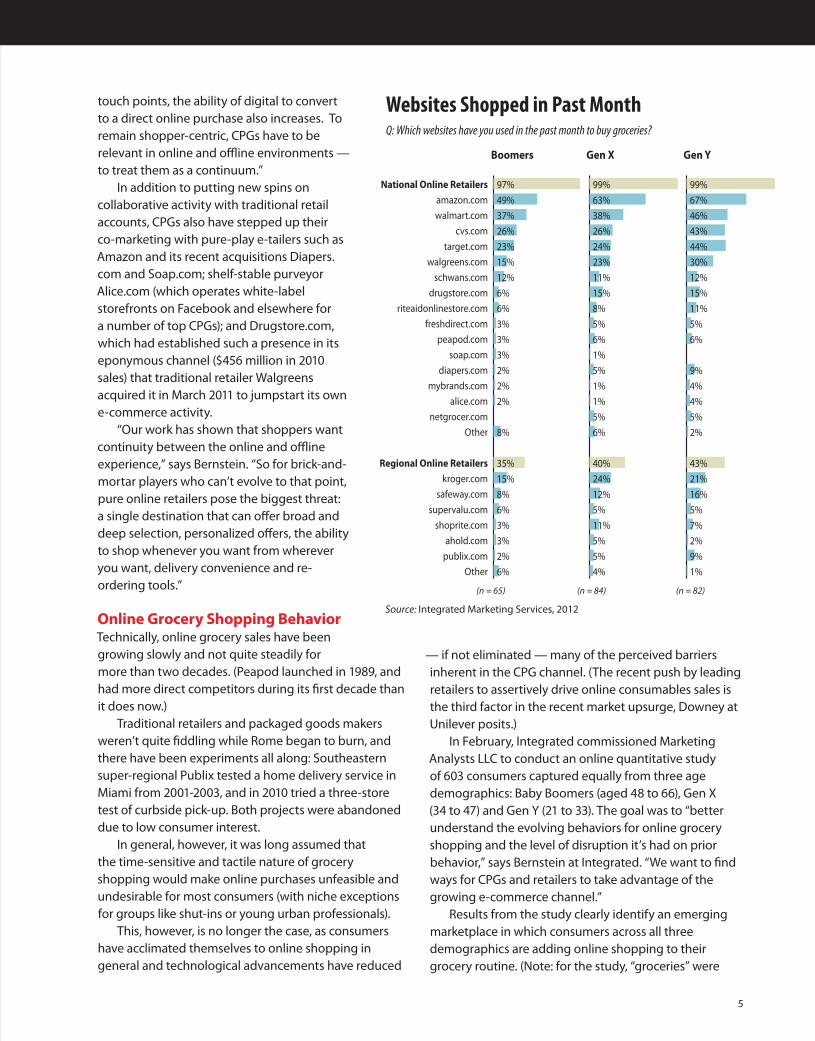

touch points, the ability of digital to convert to a direct online purchase also increases. To remain shopper-centric, CPGs have to be relevant in online and offline environments — to treat them as a continuum.” In addition to putting new spins on collaborative activity with traditional retail accounts, CPGs also have stepped up their co-marketing with pure-play e-tailers such as Amazon and its recent acquisitions Diapers.com and Soap.com; shelf-stable purveyor Alice.com (which operates white-label storefronts on Facebook and elsewhere for a number of top CPGs); and Drugstore.com, which had established such a presence in its eponymous channel ($456 million in 2010 sales) that traditional retailer Walgreens acquired it in March 2011 to jumpstart its own e-commerce activity. “Our work has shown that shoppers want continuity between the online and offline experience,” says Bernstein. “So for brick-and-mortar players who can’t evolve to that point, pure online retailers pose the biggest threat: a single destination that can offer broad and deep selection, personalized offers, the ability to shop whenever you want from wherever you want, delivery convenience and re-ordering tools.”

Online Grocery Shopping BehaviorTechnically, online grocery sales have been growing slowly and not quite steadily for more than two decades. (Peapod launched in 1989, and had more direct competitors during its first decade than it does now.) Traditional retailers and packaged goods makers weren’t quite fiddling while Rome began to burn, and there have been experiments all along: Southeastern super-regional Publix tested a home delivery service in Miami from 2001-2003, and in 2010 tried a three-store test of curbside pick-up. Both projects were abandoned due to low consumer interest. In general, however, it was long assumed that the time-sensitive and tactile nature of grocery shopping would make online purchases unfeasible and undesirable for most consumers (with niche exceptions for groups like shut-ins or young urban professionals). This, however, is no longer the case, as consumers have acclimated themselves to online shopping in general and technological advancements have reduced

— if not eliminated — many of the perceived barriers inherent in the CPG channel. (The recent push by leading retailers to assertively drive online consumables sales is the third factor in the recent market upsurge, Downey at Unilever posits.) In February, Integrated commissioned Marketing AnalystsLLCtoconductanonlinequantitativestudyof 603 consumers captured equally from three age demographics: Baby Boomers (aged 48 to 66), Gen X (34 to 47) and Gen Y (21 to 33). The goal was to “better understand the evolving behaviors for online grocery shopping and the level of disruption it’s had on prior behavior,” says Bernstein at Integrated. “We want to find ways for CPGs and retailers to take advantage of the growing e-commerce channel.” Results from the study clearly identify an emerging marketplace in which consumers across all three demographics are adding online shopping to their grocery routine. (Note: for the study, “groceries” were

National Online Retailers

amazon.com

walmart.com

cvs.com

target.com

walgreens.com

schwans.com

drugstore.com

riteaidonlinestore.com

freshdirect.com

peapod.com

soap.com

diapers.com

mybrands.com

alice.com

netgrocer.com

Other

Regional Online Retailers

kroger.com

safeway.com

supervalu.com

shoprite.com

ahold.com

publix.com

Other

Websites Shopped in Past Month Q: Which websites have you used in the past month to buy groceries?

Source: Integrated Marketing Services, 2012

97%

49%

37%

26%

23%

15%

12%

6%

6%

3%

3%

3%

2%

2%

2%

8%

35%

15%

8%

6%

3%

3%

2%

6%

99%

63%

38%

26%

24%

23%

11%

15%

8%

5%

6%

1%

5%

1%

1%

5%

6%

40%

24%

12%

5%

11%

5%

5%

4%

99%

67%

46%

43%

44%

30%

12%

15%

11%

5%

6%

9%

4%

4%

5%

2%

43%

21%

16%

5%

7%

2%

9%

1%

Boomers Gen X Gen Y

(n = 65) (n = 84) (n = 82)

12P2P_CDM_IntegratedPaper.indd 5 5/15/12 8:58 AM

6

broadly defined for respondents as any items that can be purchased in a typical supermarket, including health & beauty aids, over-the-counter medicine, household cleaners, paper goods and other non-edible products.) To be clear, the overwhelming majority of grocery trips and purchases are still taking place in brick-and-mortar stores. As noted earlier, about one-third of respondents said they buy online in a given month, and typically for only one or two purchase occasions; those same shoppers are making 16 to 18 trips per month to supermarkets, supercenters/mass merchants, drugstores and dollar stores. That, of course, leaves two-thirds of consumers who still conduct all their grocery shopping in a physical store. This online shopper is a newbie: Baby Boomers and Gen Xers have been shopping online for less than two years on average; Gen Y has been doing it for only a year (a disparity that might reflect their recent entry into the market as they leave home and start their own households). These shoppers spend between 3% and 6% of their monthly budgets online, with the rest being rung up in the aforementioned brick-and-mortar channels. That means they are spending roughly $13 to $25 of their $400 to $500 totals online, which implies little more than a handful of items being purchased each month, and explains why most respondents said their primary online mission is a fill-in trip. However, the fact that one-third of consumers already are making grocery purchases online is significant, especially since many are shopping in categories that aren’t yet viewed as digitally viable by many CPGs. (See Category-LevelBehavioronpage9.)

Also noteworthy is the fact that, contrary to what is commonly assumed, Baby Boomers are nearly as likely to be shopping online as Millennials. “This isn’t a case of Gen Y leading the charge online and Baby Boomers sticking with the traditional store,” notes Fogerty. “When we first started to move into this space, we saw that the typical online shopper was exactly whom you would expect it to be: young, tech-savvy, and looking for that ‘long tail’ item,” explains Wonzen.

Swinging with Schwan’sAmazon. Walmart. CVS. Target. Walgreens. And Schwans?

Known better nationally for such frozen-aisle staples as Freschetta, Red Baron and Mrs. Smith’s, the Schwan Food Co. originated as an ice cream home delivery business in Western Minnesota in 1952 (18 years before it initiated retail distribution). And despite the company’s success at retail since then, the Schwan’s Home Service division still thrives as a national e-tailer, delivering its frozen foods to 2.3 million customers through a fleet of 5,300 vehicles and a direct-mail business (via UPS) that encompasses the 48 contiguous states. (Next-day delivery rates start at a pretty steep $61.95; standard ground charges run from $4.95 to $14.95.) In 2010, Schwans.com recorded $1 million in sales in one day for the first time.

INDUSTRY REPORT

Don't have to wait in line to check out

Save money/better deals

Can order any time of day or night

Saving time

Ease of ordering online

Controlling impulse purchases

Can find items can't get in local stores

Don't have to load groceries into car

Way to shop when busy

Don't have to get out of the car

Don't have to shop with the kids

Better variety/more choices

Not having to do a disliked task/chore

Shop more thoroughly

Advantages to Shopping Online Q: Please rank the three benefits to shopping online that are of the most value to you.

Source: Integrated Marketing Services, 2012

29%

26%

23%

22%

15%

15%

15%

15%

12%

8%

6%

6%

3%

2%

30%

32%

23%

23%

13%

11%

13%

12%

8%

4%

8%

10%

6%

6%

20%

43%

9%

29%

11%

6%

16%

11%

16%

4%

12%

13%

5%

4%

Boomers Gen X Gen Y

(n = 65) (n = 84) (n = 82)

12P2P_CDM_IntegratedPaper.indd 6 5/15/12 8:58 AM

7

“However, as retailers have built out their presence with upgraded sites, expanded category selection and more convenient delivery options, we’ve seen the lines between the online shopper and traditional shopper begin to blur.”

Popular DestinationsNational websites are the most common shopping destination, followed by retailers offering store pickup or local delivery. Most CPGs probably wouldn’t need more than one guess to pick the two most popular online destinations for grocery, although they might get the order wrong: Amazon.com topped Walmart.com as the most common website for grocery shopping across all age groups, and by pretty significant margins. More noteworthy might be the popularity of drugstore websites. CVS.com trailed only the big two in popularity, and was visited by more respondents than Target.com in two age groups (only Gen Yers visited the mass merchant more). Walgreens rounded out the top five as the only other retailer to be cited by as many as 20% of respondents, and Drugstore.com was also high on the list. The low penetration levels for traditional supermarkets is understandable, since most have yet to make any formidable pushes for online sales. Many chains currently offer little more than online ordering for perimeter-department fare like deli platters and birthday cakes, options that Alec Newcomb, MyWebGrocer’s chief strategy officer, calls “e-commerce light.” But the fact that the 242-store ShopRite chain trails only the big three of Kroger, Safeway and Supervalu in terms of online trips might illustrate what a little forward thinking might do. The retailer has been actively working to influence online shopping behavior for several years now, and 56 stores recently began offering home delivery for online orders. Aside from Amazon, pure-play e-tailers and home delivery services also have yet to gain significant penetration, according to the study (see chart on page 5). But that largely reflects their scale: Peapod currently covers 12 states in two regions, while FreshDirect operates only in the New York City market. Meanwhile, Schwans.com has its own unique story (see “Swinging with Schwans” on page 6). For the most part, these online grocery “trips”

represent a reduction in store visits, which implies that brick-and-mortar retailers are losing sales — although respondents say their store visits have actually increased at a faster rate than online trips over the last three years. That reflects the general industry trend toward fewer pantry-loading stock-up trips and more, smaller fill-ins. “Among Boomers and Gen X, brick-and-mortar trips are being cannibalized by online shopping. But for Gen Y, online occasions are more incremental,” notes Fogerty.

“This means we need to understand how to win with Gen Y in the online space — now, while we can influence their behavior.”

Trip DriversThe desire for financial savings and shopping convenience are the primary reasons consumers are shopping online for groceries. However, the greatest advantage cited by respondents is one that has influenced trip decisions for decades: not having to wait in a checkout line. “Nothing feels more like wasting time than waiting, being at the mercy of the human element

INDUSTRY REPORT

Review paper copies of store circulars

Clip/organize paper coupons

Prepare a list from scratch

Check my cupboards/pantry

Search and download coupons online

Look at recipes/ plan meals from books or files

Review store circulars online

Look at recipes/ plan meals online

Reference my old shopping lists

Reference my online order

Browse the retailer's website

Nothing, I do nothing to prepare

Shopping Preparation Habits, In-Store vs. OnlineQ: Please indicate what sort of preparation you do before shopping for groceries in-store and online.

Source: Integrated Marketing Services, 2012

Online (n = 65)In-Store (n = 202)

6%

9%

31%

45%

20%

8%

29%

12%

9%

22%

42%

15%

47%

51%

54%

64%

39%

22%

38%

19%

12%

4%

23%

10%

49%

50%

66%

75%

34%

22%

32%

15%

10%

2%

15%

5%

14%

12%

24%

36%

23%

12%

30%

18%

15%

18%

48%

18%

18%

15%

29%

28%

29%

20%

28%

24%

20%

16%

33%

23%

32%

38%

49%

59%

33%

27%

22%

34%

13%

3%

16%

11%

Online Boomers Gen X Gen YIn-Store

Online (n = 84)In-Store (n = 200)

Online (n = 82)In-Store (n = 199)

Online shoppers are LESS likely than in-store shoppers to...

Online shoppers are MORE likely than in-store shoppers to...

12P2P_CDM_IntegratedPaper.indd 7 5/15/12 8:58 AM

8

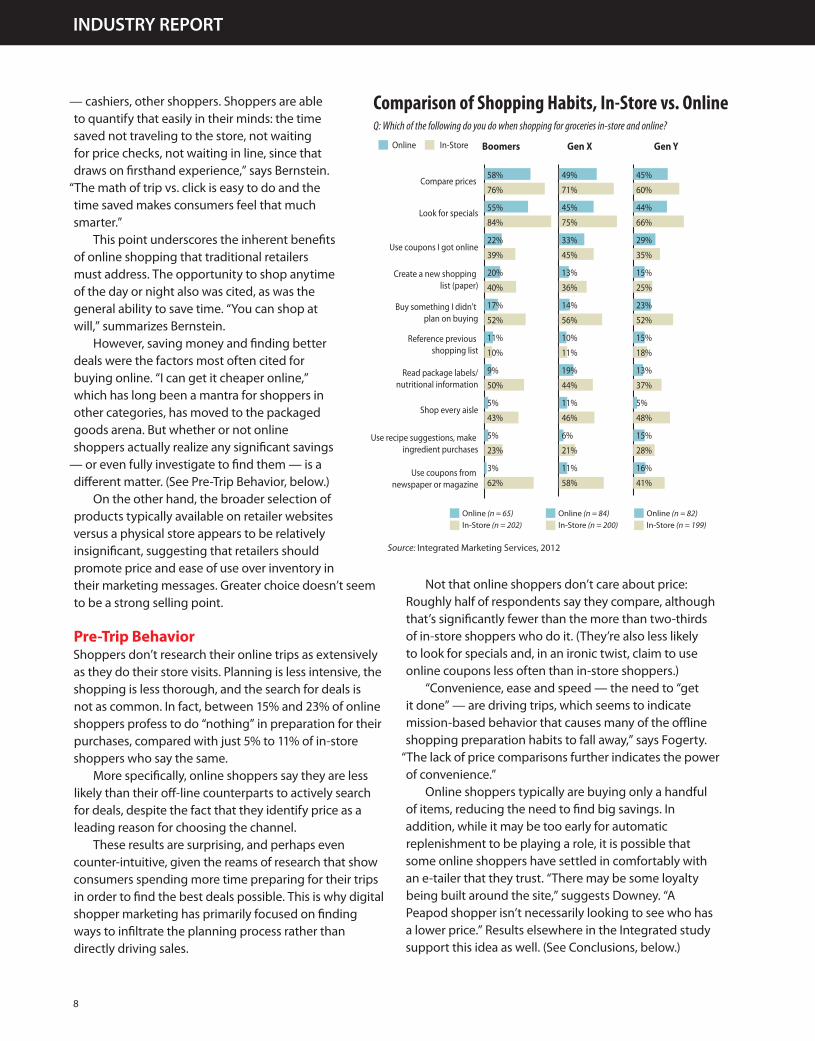

— cashiers, other shoppers. Shoppers are able to quantify that easily in their minds: the time saved not traveling to the store, not waiting for price checks, not waiting in line, since that draws on firsthand experience,” says Bernstein.

“The math of trip vs. click is easy to do and the time saved makes consumers feel that much smarter.” This point underscores the inherent benefits of online shopping that traditional retailers must address. The opportunity to shop anytime of the day or night also was cited, as was the general ability to save time. “You can shop at will,” summarizes Bernstein. However, saving money and finding better deals were the factors most often cited for buying online. “I can get it cheaper online,” which has long been a mantra for shoppers in other categories, has moved to the packaged goods arena. But whether or not online shoppers actually realize any significant savings

— or even fully investigate to find them — is a different matter. (See Pre-Trip Behavior, below.) On the other hand, the broader selection of products typically available on retailer websites versus a physical store appears to be relatively insignificant, suggesting that retailers should promote price and ease of use over inventory in their marketing messages. Greater choice doesn’t seem to be a strong selling point.

Pre-Trip BehaviorShoppers don’t research their online trips as extensively as they do their store visits. Planning is less intensive, the shopping is less thorough, and the search for deals is not as common. In fact, between 15% and 23% of online shoppers profess to do “nothing” in preparation for their purchases, compared with just 5% to 11% of in-store shoppers who say the same. More specifically, online shoppers say they are less likely than their off-line counterparts to actively search for deals, despite the fact that they identify price as a leading reason for choosing the channel. These results are surprising, and perhaps even counter-intuitive, given the reams of research that show consumers spending more time preparing for their trips in order to find the best deals possible. This is why digital shopper marketing has primarily focused on finding ways to infiltrate the planning process rather than directly driving sales.

Not that online shoppers don’t care about price: Roughly half of respondents say they compare, although that’s significantly fewer than the more than two-thirds of in-store shoppers who do it. (They’re also less likely to look for specials and, in an ironic twist, claim to use online coupons less often than in-store shoppers.) “Convenience, ease and speed — the need to “get it done” — are driving trips, which seems to indicate mission-based behavior that causes many of the offline shopping preparation habits to fall away,” says Fogerty.

“The lack of price comparisons further indicates the power of convenience.” Online shoppers typically are buying only a handful of items, reducing the need to find big savings. In addition, while it may be too early for automatic replenishment to be playing a role, it is possible that some online shoppers have settled in comfortably with an e-tailer that they trust. “There may be some loyalty being built around the site,” suggests Downey. “A Peapod shopper isn’t necessarily looking to see who has a lower price.” Results elsewhere in the Integrated study support this idea as well. (See Conclusions, below.)

Compare prices

Look for specials

Use coupons I got online

Create a new shopping list (paper)

Buy something I didn't plan on buying

Reference previous shopping list

Read package labels/nutritional information

Shop every aisle

Use recipe suggestions, make ingredient purchases

Use coupons from newspaper or magazine

Comparison of Shopping Habits, In-Store vs. OnlineQ: Which of the following do you do when shopping for groceries in-store and online?

Source: Integrated Marketing Services, 2012

Online (n = 65)In-Store (n = 202)

58%

55%

22%

20%

17%

11%

9%

5%

5%

3%

76%

84%

39%

40%

52%

10%

50%

43%

23%

62%

49%

45%

33%

13%

14%

10%

19%

11%

6%

11%

71%

75%

45%

36%

56%

11%

44%

46%

21%

58%

45%

44%

29%

15%

23%

15%

13%

5%

15%

16%

60%

66%

35%

25%

52%

18%

37%

48%

28%

41%

Online Boomers Gen X Gen YIn-Store

Online (n = 84)In-Store (n = 200)

Online (n = 82)In-Store (n = 199)

INDUSTRY REPORT

12P2P_CDM_IntegratedPaper.indd 8 5/15/12 8:58 AM

9

Category-Level BehaviorThe development of an online marketplace for packaged goods has come in gradual stages, with most marketers having already accepted the fact that e-commerce is suitable for:

• non-foodssuchashousehold,babycareandhealth& beauty products. (The success of niche e-tailers like Diapers.com and Drugstore.com attests to this.)

• recurringpurchases,especiallyproductsboughtinbulk like diapers, laundry detergent, pet food and paper towels. (Some believe e-tailers already have surpassed supermarkets in diaper sales.)

• sociallysensitiveproductssuchasadultundergarments, weight-loss tools or sexual aids.

However, online shoppers also are buying food and beverages — and in greater numbers than for the above non-foods categories, in some cases. And more startling is the fact that some survey respondents claimed to only buy online. While these online-only shoppers are admittedly few in number (about 50 respondents across the three demographics), the fact that any consumers already claim to satisfy all their food and beverage needs online is an eye opener. Even Tim Dorgan, vice president-managing director of Peapod Interactive, says that it’s

“rare to get 100%” of a customer’s spend. It’s only here at the category level that the behavior of Baby Boomers, Gen Xers and Gen Yers starts to differentiate to any significant level. For instance, Gen Yers are almost three times as likely as Boomers to buy all their food online, and Gen Xers are three times as likely to purchase all their household goods. There also are some categories (frozen, bakery, produce) in which no Baby Boomers are making online purchases, whereas the X and Y generations are buying across all of them. (See chart, page 10.) Fogerty again takes special notice of Gen Y, among which roughly one-third of online shoppers claim to have dispensed with stores altogether. “Engaging and understanding the purchase preferences of this burgeoning segment is critical to the future,” she advises.

Barriers to ConversionConversely, it will be welcome news to traditional retail marketers that not everyone is ready to abandon the store: Of the two-thirds of respondents who have yet to shop online, about 22% said they haven’t because they “enjoy grocery shopping in the store.” Surprisingly, more Gen Yers made this claim than their older, store-raised counterparts.

The most common barrier to adoption, however, is the one that has long been assumed to be the key obstacle for online grocery shopping: 30% of holdouts said they prefer to select their own items rather then leave it up to someone else. Elsewhere, about 14% of respondents said they find online shopping too expensive and don’t like paying extra fees for delivery. Otherwise, the identified barriers are related more to the Internet as a whole (supplying personal information, having difficulty with the process) than with grocery shopping in particular. That suggests that it’s only a matter of time before the practice becomes more widely adopted, as shoppers become more comfortable with the medium and technology continues to improve. “Consumers are becoming more and more comfortable with it,” notes Dorgan at Peapod, where shoppers are largely using the service for stock-up trips that span all fresh, frozen and dry grocery categories. Price barriers also are going away, partly due to consumer feedback but also because of an increase in competitive positioning. Delivery charges are declining and more e-tailers are offering “free shipping” at relatively low purchase thresholds (as low as $25 at many sites). “When it comes to home essentials, we still trudge off to the store, load up the cart, and haul a trunk-load of stuff out of the parking lot. Why? Because no one has come up with an efficient, cost-effective way to buy these goods online,” explains the website of Alice.com, which claims to have launched to solve that very problem (and provides free shipping for all orders of $40 or more).

Conclusions:The dawn of online grocery shopping is here. While many consumers still might not be ready to buy online, and although most will continue to do the vast majority of their shopping at traditional stores for a long time to come, the multi-channel era has arrived in the packaged goods world. In the future, “Consumers will choose how they want to shop today,” says Peapod’s Dorgan. It might be a store one day, and a computer, smartphone or tablet (or whatever else comes along) the next. Here’s what marketers should do to prepare:

Start Yesterday: A wait-and-see approach is no longer an option. Marketers need to get out ahead of the trend or risk being left behind as the marketplace shifts. “You need to walk into your boss and say, ‘I need more resources.’ We’re going to have to adapt and

12P2P_CDM_IntegratedPaper.indd 9 5/15/12 8:58 AM

10

change our strategies,” says Newcomb at MyWebGrocer, which manages the websites and related digital marketing activity for 115 supermarket chains.

“Otherwise, you’ll be giving up on loyal shoppers.” New shopping behaviors could easily lead consumers to different choices if the retailers and brands they’re familiar with don’t make themselves readily available online. Although it has an advantageous domain name, Diapers.com may never have enjoyed such success if Walmart, Kroger, Walgreens and other traditional retailers had already been online solving the needs of new-age moms. Earlier this year, e-tailing start-up Dollar Shave Club posted a video on YouTube, and 48 hours later had 12,000 consumers signed up to receive replacement razor blades each month for $10 or less. So CPGs need to be defensive as well. “Digital is the great equalizer,” says Newcomb.

Don’t Fear Cannibalization: Just make sure you’re the one doing the eating. The rise of online grocery shopping won’t increase overall consumer demand for packaged goods products, but it could very well lead to dramatic shifts in consumer loyalty for specific retailers and brands. At this stage, the group most at risk is brick-and-mortar stores, which will have to adopt e-commerce strategies to ensure that loyal shoppers remain so as they migrate online. Walmart took a big step in this direction last February, when it began crediting store managers for the online sales generated within their territories. How the sale is made no longer matters. “That changes the game,” says Downey. It might not be too obvious to say that e-tailing also broadens the footprint. “E-commerce allows us to reach

… customers who live outside our 35-state market area,” Dreiling said last fall. The same holds true for CPGs, in two ways. First, they must defend their existing market share while looking for opportunities to attract new customers by establishing a strong presence online (where they often are freed from historic constraints like distribution, shelf slotting and store environments). Second, they must embrace a new retail landscape that requires both broader collaborative

activity with traditional partners (who need e-commerce help) and new players (who’ll need marketplace and marketing assistance). The digital elephant in the room is direct sales. E-commerce does make it possible for product marketers to skip the allowance-charging, discount-demanding, brand-agnostic retail channel entirely, although doing so would require some structural transformations that CPGs might be loathe to undertake. And, no shopper would likely relish a path to purchase that requires her to shop brand-by-brand or company-by-company for every transaction. “At the end of the day, it is about the consumer experience, and many consumers would prefer to shop at a site where they can fill up their basket and get free shipping. This is harder to do at a company- or brand-specific site,” says Wonzen. “Also, I would challenge the notion that selling direct to consumers is more profitable. When you add up the technology, fulfillment and traffic- driving costs for a direct site, it is not a given that it will be more profitable than selling through online retailers.”

Cut to the chase: Digital shopper marketing has been proven to drive CPG sales all the way to the brick-and-mortar store. Marketers can easily and effectively

All Food & Beverage

Beverages

Canned/Packaged Items

Condiments/Sauces

Snacks

All Personal Care

Cosmetics

Health & Beauty

OTC Meds

Personal Care

All Household Products

Paper/Plastic

Cleaning Products

Pet Food

Laundry Care

Online Grocery Purchases, By Category Q: Indicate whether you buy each item online exclusively, in-store exclusively, or in both places.

Source: Integrated Marketing Services, 2012

Boomers Gen X Gen Y

Online only Both Online and In-Store

(n = 65) (n = 84) (n = 82)

12% 80%

5% 52%

6% 43%

6% 43%

3% 45%

14% 74%

9% 48%

2% 55%

2% 45%

3% 25%

5% 58%

3% 45%

2% 45%

0% 40%

0% 38%

19% 64%

8% 29%

7% 36%

5% 30%

6% 35%

20% 65%

12% 31%

7% 54%

8% 33%

7% 29%

17% 65%

10% 40%

8% 44%

8% 40%

10% 44%

32% 63%

15% 34%

13% 35%

11% 33%

9% 41%

23% 64%

11% 40%

15% 44%

7% 26%

10% 29%

21% 61%

20% 34%

11% 43%

4% 33%

10% 40%

INDUSTRY REPORT

12P2P_CDM_IntegratedPaper.indd 10 5/15/12 8:58 AM

Digital ImpulsesApparently, display ads are no match for P-O-P displays: Nearly two-thirds of Boomers and Gen Xers say they’re less likely to make impulse purchases while buying groceries online than they are in a store. However, 20% and 26%, respectively, say they’re more likely. The impetuousness of youth proves true, however. Among Gen Yers, only 46% say they’re less likely to buy unplanned items, while 30% are inclined to buy more. This suggests that digital marketers have some work to do when it comes to driving impulse buys — especially since there already are many automated, targeted tactics at their disposal. “That’s what Amazon does so well, drive impulse purchases with their recommendations,” says Bernstein at Integrated. Launchedyearsagoandnowemulatedwidely,Amazon.comhasagreattacticinitsrecommendations,whichoffer shoppers other ideas derived from their own purchase and browsing history as well as the company’s universal database (“Customers who bought this item also bought …”). Based on results from the survey, however, the e-tailer’s tendency to bombard shoppers with a vast amount of product information might be overkill in the CPG world. With pre-set shopping lists and automatic replenishment now possible, heretofore “planned” purchases can become transactions that are no longer even considered, which is great for time-starved shoppers but potentially lethal for impulse-heavy CPG categories.

provide any and all the information a shopper needs as she moves along the path to purchase. But no matter what other communications it may encompass, a sound strategy needs to include a clear, direct path to online purchase as well. “Any good website page, if it doesn’t have a bin and a ‘buy it now’ option, then it is incomplete,” said April Carlisle, leader of Procter & Gamble North America’s Shopper Marketing Center of Excellence, while speaking at a recent industry conference. “That is a stated strategy for P&G.” MyWebGrocer’s Newcomb hypothesizes about placing “shop now” buttons linking to a retail partner alongside branded recipes on a third-party culinary site. Shoppers looking for meal solutions are aided in their quest, as are those inspired to buy related products immediately. Until all traditional retailers establish e-commerce capabilities (assuming they will), CPGs will need to adjust their efforts accordingly, providing store-driving tactics and/or direct sales levers as the circumstances dictate.

“We want to create programs that can do both,” says Downey. “Our two primary audiences — our customers and consumers — demand that.”

11

Better prices

Free shipping/no delivery charges

Exclusive online offers

Same-day service

Better product selection

More convenient delivery options

Better qualityproduce/meat/bakery

Easier online ordering process

More convenient pickup locations

Better customer service

More user-friendly websites

Incentives for Future Online Grocery Spending Q: Which of the following would entice you to do more grocery shopping online?

Source: Integrated Marketing Services, 2012

78%

75%

55%

51%

49%

43%

38%

37%

26%

25%

25%

76%

76%

54%

52%

48%

43%

37%

40%

27%

24%

33%

71%

79%

56%

65%

54%

51%

51%

46%

50%

39%

40%

Boomers Gen X Gen Y

(n = 65) (n = 84) (n = 82)

Break down the barriers: In addition to serving as an obstacle for non-shoppers, delivery charges and other extra online fees are a hindrance for consumers who already are online: three-fourths of online shoppers in

12P2P_CDM_IntegratedPaper.indd 11 5/15/12 8:58 AM

The Path to Purchase Institute is a global organization of brand marketers, retailers, agencies and manufacturers focused on improving retail marketing strategy worldwide. The Institute serves the needs of its membership by providing information, research, education and training, networking opportunities, trade publications and a trade show designed to further the understanding, acceptance and effectiveness of in-store marketing. For more information, go to www.p2pi.org.

Founded in 2000, Integrated Marketing Services is the full-service promotions agency within Advantage Sales&MarketingLLCspecializinginshoppermarketing,eventmarketing,technicalbrands,in-storedemos,and more. From insights to execution, Integrated offers leading brands and retailers expertise specifically designed to influence buyer behavior and drive sales. After all, the point is purchase. For more information, visit www.INmarketingservices.com.

the Integrated study said their elimination would be an enticement to buy more (see chart on page 11). The general perception that prices are cheaper online won’t persist if consumers continue to encounter extra fees (especially after state-level online sales taxes become commonplace). Price is extremely important, therefore. But with many online shoppers wanting lower prices but not necessarily taking the time to find them, marketers might not have to give away the store (so to speak) to satisfy the desire. And convenience might be a better message to convey: The value proposition may be improved more by offering free two-day shipping or same-day store pickup than bydangling10%offofthereceipt.(Lackofimmediacy,another classic obstacle to online grocery shopping, is rapidly going the way of the telephone landline.)

Play to your strengths: Despite the ubiquitous presence of behemoths old and new (Walmart and Amazon), smaller retailers still have a great opportunity to retain their loyal shoppers and gain new ones. Localretailers“havesomehugeadvantages.Theyareembedded partners in the community,” says Newcomb. In the Integrated survey, “a name I know and trust” was the most commonly cited influence on website selection, and the only one identified by more than 50%ofrespondentsinallthreeagegroups.(“Lowestprices” finished a distant second, and product selection was even farther behind.) Retailers with an established reputation should build on that rather than letting it be usurped online.

Promote: Awareness about online shopping opportunities was high in the Integrated survey. But media advertising and email marketing were among the lowest factors in determining a shopping destination. “On the national level, you could argue that the retailer’s overall marketing is giving a halo to site selection, and that’s why you see large players such as Walmart.com, CVS.com and Target.com rise to the top for usage. They’re awareness levels are that much higher,” suggests Bernstein. “And, they have a larger overall

INDUSTRY REPORT

user base from which to increase conversion to grocery purchases — not unlike Amazon. It will be interesting to see if regional grocery players will push harder for their shopper segments to adopt dual online/offline behaviors, or if they’ll risk losing trips to dot-com competitors.” “This is not a common behavior for many consumers to consider,” says Downey, advising that retailers need to

“scream” about the option being available.

The future of online grocery shopping is not guaranteed: While about half of survey respondents said they’ll likely continue ordering groceries online over the next three years, about 20% said they probably won’t. And roughly as many say they hope to decrease their online spending as say they plan to increase it. That means retailers and product marketers have to improve the online shopping experience not only to attract new shoppers, but also to retain the ones already there. Gen Y is just becoming a true grocery demographic, and its members have a preference and aptitude for digital technology that make online shopping a natural fit. But as the Integrated study shows, Gen Xers and even Baby Boomers are not too old to learn new digital tricks, making it vital for retailers and CPGs to consider their needs, too, as they develop online strategies. What’s needed most is a digital shopping experience that’s aligned with the brick-and-mortar experience, to make the transition seamless in the minds of shoppers. “The message is clear. While the emergence of e-commerce is certainly underway, there is work to be done by e-tailers and CPGs alike,” says Fogerty. “CPGs have an opportunity to help retailers build an online experience that strengthens their off-line experience. Building credibility for retailer websites, and then ensuring that those sites deliver against their promises, will be critical.” Understanding that online shoppers exhibit different behaviors than their offline counterparts — at least for now — is also vital. CPGs and retailers must learn how to effectively engage the digital shopper and drive her to purchase — wherever that purchase may take place.

12P2P_CDM_IntegratedPaper.indd 12 5/15/12 8:58 AM