Embed Size (px)

Citation preview

The Innovative Insurer

by the Digital Insurer Network

A write up of the 2016 face-to face meeting

April 21st and 22nd

Paris Innovation Center

Copyright © 2016 Accenture All rights reserved. 2

In 2014 the Digital Insurer Network first met to

focus on the urgent need for insurers to transform

and digitize in order to compete with new market

entrants

In 2015 we looked at the adaptive insurer,

discussing the concept of human value in a digital

environment and considering how insurers can

keep up

Now, in 2016, we looked at the innovative insurer,

considering

• How insurers can get ahead of the competition

• How to play within a larger ecosystem

• How to manage and operationalize innovation

The Digital Insurer Network Journey

Copyright © 2016 Accenture All rights reserved. 3

Jocely AubryAON - France

Richard BeavenSwinton – UK

Michael Blix TryggHansa – Sweden

Valerie BompardSogecap – France

Christophe de CacquerayCovea – France

Frank CoolerIntrasurance – Netherlands

Dr. Nils ReichAXA – Germany

Øivind Skallerud Gjensidige – Norway

Fred SlikkerIntrasurance – Netherlands

Frank van WesselDelta Lloyd – Netherlands

Juha ViljakainenOP Vakuutus – Finland

Lukas VogtSanitas – Switzerland

Paul WishmanLV= - UK

Ian Gandy Esure – UK

Cyril HaiounBNP Paribas Cardif – France

Alex KoslowskiRoyal London – UK

Nisse Jakob KrenchelAlm.Brand – Denmark

Demetrio Migliorati Banca Mediolanum – Italy

Lee NoonLV= - UK

Anssi OkkonenIf P&C Insurance - Finland

Attendees

Copyright © 2016 Accenture All rights reserved. 4

Speakers

Stuart BaldwinThe Positive Company – UK

Rachel BartonAccenture – UK

Tara BrownAccenture – UK

Ana Maria GiménezSigFox – France

Stephane GuinetKAMET– France

Dan HarrisFjord - UK

Laetitia JaySigFox – France

Jean-Marc LazardOpenDataSoft - UK

Peter SanyTM Forum - Switzerland

Calogero ScibettaEverledger - UK

Colin SlomanAccenture - UK

Emmanuel Viale Accenture - France

Copyright © 2016 Accenture All rights reserved. 5

Accenture Hosts / Facilitators

Piercarlo GeraGlobal Managing Director: Distribution & Marketing Services

Jean-Francois Gasc Managing Director: Strategy EALA

Roy Jubraj Managing Director: Digital & Innovation

Thomi Meyer Managing Director: Insurance EALA [email protected]

Edwin van der OuderaaManaging Director: Financial Services Digital EALA

Copyright © 2016 Accenture All rights reserved. 6

Day One

Bringing the Ecosystem to Life

Copyright © 2016 Accenture All rights reserved. 7

…began by exploring interesting technology demos and

introducing ourselves

We then reflected on the past year, looking at disruptive

customer trends and technologies

Dan Harris, Rachel Barton and Emmanuel Viale shared

their views on customer, technology and market trends

Case studies and start-up leaders Leanne Kemp, Scott

Walcheck and Laetitia Jay provided insight as to how

insurance will look by 2026

We looked at how Google, Santander and Apple play

across multiple ecosystems and POV about the

opportunities for insurance

At the end of the day Peter Sany introduced us to TM

Forum’s approach to ecosystems

The journey on day one…

Copyright © 2016 Accenture All rights reserved. 8

What will the implications be for

customer and employee strategy

when virtual reality is mass

market?

Enables remote attendees to sit

in a virtual meeting room together

Digital sales and service functions

to support face-to-face client

interactions

What will employees expect in

terms of the technologies they

can use at work in the future?

How can technology enable

workers to be more customer

centric?

Analytics transformed into art

creates amazing visuals

How can the visualisation of data

be used to drive new insights and

change behaviours?

We began by exploring technology demos and the

art of the possible

Virtual Reality Employee Enablement Data Visualisation

Copyright © 2016 Accenture All rights reserved. 9

BlockchainOffers the potential to revolutionise insurance with

distributed databases and smart contracts

3D Printer and ScannerCollects data on the shape, measurements and

appearance of a real-world object which can then

be printed as a 3D objectt

We began by exploring technology demos and the

art of the possible

How can Blockchain drive transparency and

honesty? What is the impact on data security?

Could Blockchain drive automation and faster

claims processing?

What does this mean for how products are insured?

Who is liable if 3D printing goes wrong? Which

insurance products could be impacted? How can

this technology impact claims documentation?

Copyright © 2016 Accenture All rights reserved. 10

“One could be the solution to the other”

Newspapers Crowd-sourcing

“A cat has more

than one life so fail

fast and you can

still go on.”

Pets

“Connected health

and home

insurance are

moving together as

everything

becomes more

connected”

Internet of

Things

Analytics Sportswear

“Opportunity to improve fitness data”

“We’re exploring

robo-advisor

opportunities right

now”

Robotics

We then introduced ourselves and started considering the impact

of key disruptors

Copyright © 2016 Accenture All rights reserved. 11

Key Trends Key Products

We then introduced ourselves and started considering the impact

of key disruptors

Crowd-sourcing

Internet

of Things Analytics

Robotics

Automation

Personalisation Gamification

Blockchain Platfom Economy

Sharing

Economy

Virtual Reality

Sportswear

Flood Protection

Books

Bicycles

Toothbrush

Delivery Services

Television

Car Insurance

Copyright © 2016 Accenture All rights reserved. 12

Since we last met…

How do you lead change… before you have to change?

In more detail, we delved into the key customer and technology

disruptions from the past 12 months

Copyright © 2016 Accenture All rights reserved. 13

Sure lets you purchase travel insurance

on your phone just as your flight is

about to take off

We considered some of the key facts

In January a new cellphone store

opened in Japan manned exclusively by

robots

2015 saw Nepal’s biggest earthquake in

81 years. Within 24 hours crowd-

sourced volunteers had made 3 million

edits to google map sand 7 million

people had checked in safe on

FacebookB2B customers are more and more

demanding: 76% have higher service

expectations & 73% are more price

sensitive than ever before. Yet only

14% of B2B insurers are considered

leaders in customer experience

Humana Cue sends you reminders in

line with your health stats

Most of us would like premiums set

according to driving patterns

Last year BLP law firm began recruiting

robots last year. They processed 100

days of legal work. in less than 2

seconds

Last year 300 hours of youtube video

were uploaded; 51,000 Apple apps

were downloaded; 1,041,666 Vine

videos were played; 4,166,667

facebook posts were liked EVERY

MINUTE

Amazon Pantry and Morrison’s

partnered in February to deliver fresh

and frozen groceries to Amazon Prime

customers in less than an hour

Last year TalkTalk’s data was breached

3 times in 2015 at a cost of £60million

and 100,000 customers

2/3 of drivers would love their car

insurer to let us know when our children

are driving dangerously… or to that “off

limits” location

87% of millennials have no contents

insurance

Last year the top 5 insurtech start-ups

achieved $2.5bn in funding (Zhongan –

931m; OscarHealth – 728m ; Zenefits –

584m ;Gusto – 136m;Clover – 135m)

Snapcash have now introduced money

transfers by photo…and soon we’ll be

booking Lyft taxis through Facebook

Chat

Oscar Health you up to local doctors

and sending out nurses when you need

them

Copyright © 2016 Accenture All rights reserved. 14

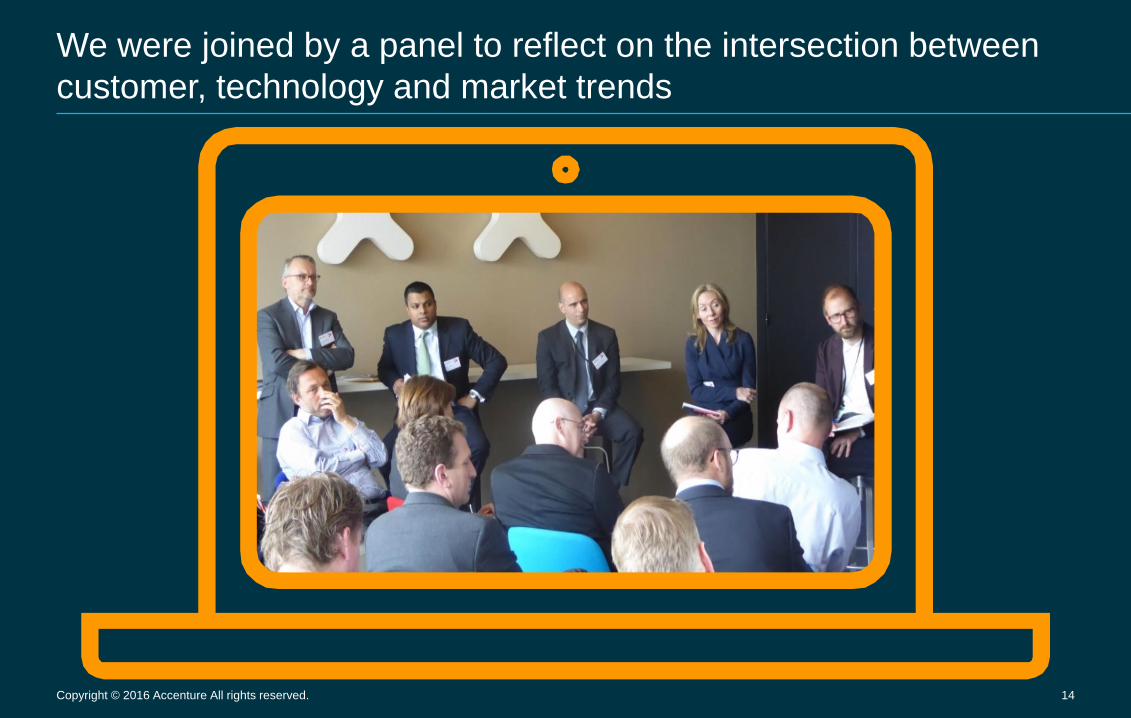

We were joined by a panel to reflect on the intersection between

customer, technology and market trends

Copyright © 2016 Accenture All rights reserved. 15

And we reflected on how these made us feel

“Could peer to peer be

a new business model

for us?”

“If customers don’t feel the

value add, it will be offered by

someone else”

“Who is really going to win the battle? the

small competitors are usually in it for the

exit strategy but the big non-traditional

competitors – now, that's scary”

“Now that data is readily-available, for how much

longer will customers need insurers to analyse risk?”

“There is an opportunity to

modernize but the large

insurance companies don’t

know how to do it”

“We’re going to see large

organisations joining up with

others to deliver new customer

propositions”

“The challenge is – how do you make it relevant to all customers?

Lots of sexy stuff but many of our customers are still terrified by

aggregators that have been around for 20 years”

“The first thing is

getting the

housekeeping up to

scratch…then we

can look at the

ideas that push the

boat out”

“A lot is happening and it is

difficult to know where to

place bets”

“Our value is being re-

questioned. For example if

car accidents are reduced

by automation, what is the

new proposition for car

insurance?”

“Expectations are liquid. Once you have

experienced something great once, you never

want to go back”

“The consumer isn’t interested in

tech… they are interested in

outcomes”

“Technology is speeding up but our industry is not keeping pace”

“New entrants

are my biggest

fear”

“Not just about pricing any

more. Could the answer be

replacing products with

services? Or is it something

else?”

“We might have the trust of customers but other

incumbents like Amazon already have trust too so

why would customers keep coming to us over them?”

“Customers especially trust financial

services with data but will the experience

be aligned with the trust…. Trust alone is

not enough!”

“Is technology making

insurance obsolete? We

need to ask who we are”

“Data strategies are still risky

for big firms – we can’t lose

the customers trust”

Copyright © 2016 Accenture All rights reserved. 16

Copyright © 2016 Accenture All rights reserved. 17

There were a number of key takeaways

We need to determine what the solid monetisable propositions are in

order to ensure that innovation produces ROI

Partnerships, modulation and ecosystems are increasingly important

As we integrate technologies into our strategies, we need to ensure

that they are easy to use

Data privacy and the right to be forgotten are going to become bigger

challenges for organisations

Experience and service design needs to be understood by the people

who work with the customers every day

Employee experiences are as important as customer experiences

Technology, artificial intelligence and millennial expectations are making

liquid workforces a reality

When attracting millennials, there is likely to be a tipping point where

salary once again becomes as important as the experience

Copyright © 2016 Accenture All rights reserved. 18

Dan Harris, from Fjord Living Services, talked to us about

emerging customer trends

What are the most interesting trends from the past year?“Organisational design has been a very important factor in the

growth of businesses in recent years. Companies like Walmart have

really integrated design thinking into their ecosystems.

The two key trends that we see at the moment are “B2WE” and

“design from within”. We need to start thinking about how we can

use design as a common language that spans across vertices in our

organisations and how we can make our businesses more agile. As

employee expectations increase, we need to focus on how we can

make their experiences in the work space at least as digital as their

experiences at home and as customers.

Right now we are seeing the first 4G companies and they are

asking three big questions:

• How do you bring design into an organisation?

• How do you go about innovation and designing new products?

• How do you revolutionise the employee experience?”

Copyright © 2016 Accenture All rights reserved. 19

Rachel Barton, EALA Head of Advanced Customer

Strategy at Accenture, talked to us about market forces

How can Insurers gain advantage in a disruptive environment?“We have looked at a number of key trends already from digital to the changing customer

to the wider ecosystem play. The digital economy will soon be worth four trillion dollars and,

to reap the benefits, we need to understand how we will engage with customers of the

future. To do so, we need to be thinking about wider ecosystem trends.

In the current climate it is not easy to earn an additional dollar. To gain an advantage, we

need to be thinking about how we can collaborate and what partnership models we can

achieve. How do we pop up in other ecosystems in order to ensure that we are appearing

at just the right moment in the customer’s digital journey? How do we make our

propositions more interesting and differentiated?

Partnership strategy will be an important answer to these questions but many are nervous

about travelling into different ecosystems because of digital trust. It is important to think

about what data we are using to inform our customer service and who is using, selling and

monetising this data?

Another issue is deciding how to make the right investment. Most propositions fail and only

50% of those that break even deliver a non-negligible ROI. Therefore it is crucial to

understand the value levers that sit behind propositions. How do we determine what the

solid monetisable proposition is as we navigate through the landscape?”

Copyright © 2016 Accenture All rights reserved. 20

Emmanuel Viale, from Accenture Technology Labs,

talked to us about the latest technology trends

What technology poses the greatest threat to traditional insurance

business models?

There are a number of exciting technologies emerging. They key

challenge will lie in integrating these technologies in a “simple to

use” way, whilst taking into account what is best for the customer

and what the user experience will be. The two biggest trends in

insurance right now are Blockchain and data security.

Blockchain has already seen a lot of investment in the banking

sector and we are now seeing traction in insurance. How will you

make Blockchain simple to use and hide the fact that behind a

simple customer journey sits a complicated infrastructure?

Data Privacy will become a bigger concern. Any data exchanged

between partners will need to be encrypted and the right to be

forgotten is going to become a bigger issue for all technology.

We constantly need to consider how we use technologies;

whether we are using technology for a major disruption or a

minor innovation.

Copyright © 2016 Accenture All rights reserved. 21

How do you build an internal capability? Do you put

people in a war room? And how do you train

leadership to drive this agile organisation?

How would an organisation manage design from

within?

Do they need to outsource to a consultancy?

Dan Harris

Experience and service designs are built around the

customers so empathy regarding what customers value

and what motivates them is critical. This means that we

need to work alongside people who observe customers on

a daily basis; asking questions is not enough. The “why?”

for the customer needs to be answered internally. This

helps us to build into the service the thing that is missing

from the product: emotion. For example when someone is

applying for a mortgage, they don’t just care about the

money to buy a house, they will remember the emotions

they felt in the process. For us, success is when the

experience feels unexpected. With great design customers

are asking “why are you doing this for us? What’s the

trick?” Right now customers don’t expect services that wrap

around their lives, but one day they will, then there will

need to be a new way to delight them.

And we had some questions for the panel

Dan Harris

A year ago I would have struggled to think of 5 forward thinking

people in an organisation who would get this. Now I can find 50.

There has been a big change and we have seen a shift in our

people. Now they are asking “How can you get me to stay?”

and it is a question of retaining and utilising talent.

Rachel Barton

Recently I have been working with Lego who are a very

innovative company. They hire extremely creative people who

spend their time playing with toy guns (seriously!) The difficulty

however is knowing how to make sense of all their ideas. They

need to be grounded in something that you can make money

from and you need to make sure that the best ideas make it

through the pipeline and get actioned. So the question to make

innovation work is – how do you create an environment where

you can design and fail but that also has a structure as well?

You need to balance a certain unpredictability and diversity of

sources and resources but at the same time you can’t launch

500 new propositions every year. You need to launch

propositions in a very specific way based on customers and

their needs and you need to pick out the best bits.

Copyright © 2016 Accenture All rights reserved. 22

How do you create a liquid

workforce?

How do you attract talent?

Emmanuel Viale

60% of the workforce will likely be

contracted in 5 to 10 years and we

expect millennials to have twenty

careers. Technology is making it easier

to enable a liquid workforce, maybe

too easy. Artificial Intelligence is now

easier to work with as it becomes

more mature and there are other

options such as crowdsourcing.

Technology can also help to onboard

non-traditional talent whether this be

data scientists or connected cars.

However you need a clear strategy

backed by leadership to sit behind this.

And we had some questions for the panel

Rachel Barton

There is a high expectation of fluidity

but at the same time millennials will be

the first generation to be poorer than

their parents. There will need to be a

resetting at some point. Very high

expectations of life might seem to be

the key driver right now and money

might not be seen as a key driver but

there will be a tipping point where

money becomes important again.

Dan Harris

It is blended. We have partnerships

through the Accenture Colleagues.

The role as a designer is shifting to

creating a concept for the client to

work on in an organised partnership.

There is a design thinking concept and

a design doing. Fjord has its own go-

to-market approach.

The young generation is keen to

work in new structures with

flexible working hours, greater

collaboration, data sharing and

less hierarchy. How do you attract

young talent and accommodate

greater flexibility and

collaboration?

At Fjord are you working with

start-ups?

Copyright © 2016 Accenture All rights reserved. 23

Next, we launched ten years into the future…. To discover that

insurance as we know it today no longer exists…

Each of us was tasked with finding out what had happened…

Copyright © 2016 Accenture All rights reserved. 24

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: Internet of Things - Laetitia Jay, CMO & Ana Maria Gimenez,

Partnerships Director • Founded in 2009, Sigfox is a French company

that builds wireless networks using an ‘ultra-

narrow band’ signal that passes freely through

solid objects, to connect low-energy objects to

the ‘Internet of Things’, with the long-term goal

of "having petabytes of data produced by

billions of everyday objects

• Provides the opportunity for preventative

maintenance of assets – rather than waiting for

something to break down or go wrong before

making a claim

• Applies not only in the consumer market, but in

every business or industry

Insurance in 10 years will be usage

centric…

…And will blend into our lives

Key Takeaways

Key risks

• Will we need insurance at all in the future?

• Some risks may disappear – particularly

predictable risks - creating a need for

insurers to come up with new value

propositions

• We need to shift from being customer centric

to business centric

Key opportunities

• Ability to use data to provide pre-emptive

insurance / solutions

• Opportunity to provide customers with an

effortless experience

• Receive immediate, accurate information

about an accident

• Use of personal information to provide new

services

• Do we create pools of similar people with

similar risks?

Copyright © 2016 Accenture All rights reserved. 25

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: Blockchain - Leanne Kemp, CEO Key Takeaways

• Risk of disintermediation and the

potential for completely new insurance

models

• Can regulation keep pace with the

technology?

• Can technology keep the trust of

consumers?

• Opportunities in all high value / luxury

products e.g. wine, art diamonds

• Opportunities for back-end proficiencies

• Collaboration is required to share the

risk and potential for “Co-insurance”

• Everledger was founded in March 2015 and

funded through the Barclays TechStars

FinTech accelerator

• Everledger uses blockchain technology to

provide new methods of financing and

insuring diamonds using smart contracts

• Their vision is that blockchain can provide

the technology to eliminate fraud and

protect high value items (beyond diamonds)

by proving provenance rather than relying

on paper certificates or receipts

• There is an opportunity for entirely new

market places to open up – particularly

around wealth management and financing

of these assets - once provenance, proof of

ownership and certification have been

established

“We will see closely aligned partnerships

being forged between insurers, re-insurers,

commercial and retail banking - and that’s

the really exciting part of this technology

as it matures”

“When you start to bring smart contracts

and distributed ledgers into place it’s

absolutely clear any transaction is about

both finance and insurance”

Interconnected Financial Services

The two most important questions in any

business transaction are “How do I ensure

something is covered from risk and how do

I ensure I can buy it?

Copyright © 2016 Accenture All rights reserved. 26

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: Cloud & Mobile – Scott Walchek, CEO

“Things are enablers for experiences –

with Trov you are protecting your lifestyle”

Key Takeaways

Key Risks

• Potential of fraud

• Micro insurance pricing has new kinds of

risks linked with this policy – how do you

make decisions in seconds?

Key Opportunities

• Automation of the claims process

• A bridge to a new generation

• Consumers have a new type of

relationship with material things

• Prepaid risk mitigation is needed and

possible

• Trov is the cloud for your things, letting

you insure the things you want on

demand from your phone

• Trōv is both a data collection app and a

digital insurance platform all rolled into

one

• Launching this year, Trov will provide “on

demand protection for the things you

love, exactly when you want, just from

your phone”

• Allows you to link email receipts, snap

photos of items or receipts, add your

home with GPS, auto insure your car

using VIN as well as search a product

database to add items

“We find that the millennial generation

increasingly values control and

convenience over price”

Copyright © 2016 Accenture All rights reserved. 27

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: P2P & The Sharing Economy – Case StudiesKey Takeaways

Key Risks

• Could create exclusion

• Variety across the value chain

• Too early to know if it’s going to succeed

• Power to kill the existing model of

insurance

Key Opportunities

• Provides a balance between regulation

and capital which could drive innovation

• Risk responsibility is shifted to the

customer

• P2P model could complement the

traditional model to close the gap on

customer expectations

• Peer-to-peer (P2P) is a set of practices

and models that, through technology and

community, allow individuals and

companies to gather together to diversify

and mutualise common risks

• In a certain way, P2P insurance takes

insurance back to its roots

• P2P aims to eliminate traditional frictions

in insurance markets: Incomplete

markets, asymmetric information, moral

hazard, intermediation and processing

costs and a lack of transparency

• 2015 saw 16 P2P start ups launch –

more than in the previous 5 years

combined, the majority (14) in the US

and the UK

Bought by Many

“Together, our members are making

insurance companies listen”

Guevara

“Old insurance is rubbish, use Guevara”

Lemonade

”We’ve redesigned insurance from the

ground up to make it honest, instant and

delightful”

Copyright © 2016 Accenture All rights reserved. 28

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: P2P & The Sharing Economy – Case Studies

Copyright © 2016 Accenture All rights reserved. 29

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: P2P & The Sharing Economy – Case Studies

Copyright © 2016 Accenture All rights reserved. 30

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: P2P & The Sharing Economy – Case Studies

Copyright © 2016 Accenture All rights reserved. 31

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: P2P & The Sharing Economy – Case Studies

Copyright © 2016 Accenture All rights reserved. 32

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: P2P & The Sharing Economy – Case Studies

Copyright © 2016 Accenture All rights reserved. 33

We broke into groups to understand the future of the insurance

industry from the viewpoint of insurtech start-up leaders

Topic: P2P & The Sharing Economy – Case Studies

You had your own examples

Copyright © 2016 Accenture All rights reserved. 34

Having watched the video, we

realised that there is a “Long road

ahead”….”but [that]we don't have to

take the journey alone”

We were reminded to forget about

regulation: “Some of the great things

that companies like Uber achieve is

because they don’t care about

regulation; they’re just thinking about

the customer. They are doing it and

asking for forgiveness later… So I

want you to forget all about

regulation”

Next, we explored the possibilities offered by entering new

ecosystems

Copyright © 2016 Accenture All rights reserved. 35

And we considered some key facts

Apple don’t just make computers & iPods,

they exist to let their customers challenge the

status quo

40% of financial services innovations have

been launched by non-banking start-ups

Tesla has done away with patents in a bid to

accelerate the advent of sustainable

transport

64% of insurers plan to engage new partners

in the insurance industry 43% plan to engage

with partners, or aquire start-ups outside the

insurance industry

By 2020…

• The world will be filled with 1 trillion

connected sensors

• 80million US jobs will have been replaced

by artificially intelligent machines

• Global Internet traffic will be 64 times

larger than in 2005

67% of insurance customers would consider

purchasing insurance products from non-

insurance providers

Lego has an ‘open innovation’ platform which

invites users to design and upload product

ideas with the possibility of the designs being

made into reality

Amazon were never just a bookseller, they

exist to make the customer’s life easier. 35%

of Amazon’s revenue is generated by its

personalised customer recommendation

engine

Copyright © 2016 Accenture All rights reserved. 36

And considered examples of leading

ecosystem players

Copyright © 2016 Accenture All rights reserved. 37

And considered examples of leading

ecosystem players

Apple Pay contactless payments – partnerships

with retailers and over 140 financial institutions

• Why? Provides an effortless payment transaction for

the customer

• Benefits: For retailers – access to customer data and

a quick and convenient method of payment for

customers – apps integrated into Apple pay have seen

checkout rates double.

• Wider ecosystem impact: Payments and messaging

are merging – Facebook are trialling payments

through its messenger app, Google are trialling

attaching payments through Gmail

Apple Music Launched in 2015 –

after acquisition of Beats Electronic & Music

• Why? – “Empowers artists and music lovers to create

curated experiences that forge seamless relationships

between people and the music they love”

• The overall intent of Apple Music is to grow, nurture

and sustain careers, while more specifically shaping

one shared conversation around music.

• Benefits: $9.99 a month – acquired 10 million users in

the first month, already half the market share of

market leader Spotify (which took 6 years to reach

10m)

• Wider ecosystem impact: A response to other

streaming services e.g. Spotify

Partnership with Hermez to reinvent the

iWatch as a fashion accessory

• Why? There was a sense that technology was

going to move onto the body,” says Alan Dye,

who runs Apple’s human interface group. With

the ultimate goal being to ‘free people from their

phones’.

• Benefits: luxury watch industry generates more

than $20 billion a year in revenue

• Apple received almost 1 million Apple Watch

pre-orders in the US during the initial 6 hours of

the pre-order period on April 10, 2015

• The Apple watch is the market leader in

smartwatches, with 66% market share

• Wider ecosystem impact: Other players follow

suit; Samsung, Pebble, AndroidWear creating

their own versions of smartwatches

Copyright © 2016 Accenture All rights reserved. 38

And considered examples of leading

ecosystem players

Apple Care is Apple’s tech support division. The service and support product is Apple Care Protection Plan

• Why? To provide ongoing support for software and hardware issues

• Benefits: Customers purchase Protection Plans to extend the 1 year coverage and 90 day tech support that comes as standard for any new Apple

product. In Q1 of 2015 Apple Care revenue increased by 26%.

• Wider ecosystem impact: Third party warranty providers try to compete but struggle to offer the premium services and understanding of the Apple

operating systems. Because Apple makes the hardware, the operating system, and many applications, Apple products are truly integrated systems.

Only AppleCare products give you one-stop service and support from Apple experts, so most issues can be resolved in a single call.

Connect to Apple OS while driving

• Why? Apple have partnerships with many car

manufacturers including Volvo, Ferarri, Mercedes Benz

and General Motors to enable users to connect an

iPhone while driving and get directions, make calls,

send and receive messages and listen to music using

voice and the built in display

• Benefits: Independent dealers report that the feature

draws in customers and helps to close the deal in selling

new cars.

• Wider ecosystem impact: Tim Cook, CEO, explained,

"It is a part of the ecosystem. And so just like the App

Store is a key part of the ecosystem, and iTunes and all

of our content is key, and the services we provide from

messaging to Siri and so forth, having something in the

automobile is very important. It's something that people

want. And I think that Apple can do this in a unique way,

and better than anyone else.”

Open development platform to harness the power

of the crowd of developers

• Why? – to provide a greater range of software and

services to the customer, ‘ecosystem of services’ is a

barrier to switching for customers

• Benefits: The App Store has more than 1.5 million

apps and more than 100 billion copies of apps have been

downloaded

• Wider ecosystem impact: Android have 82% market

share but lower end of the market

Launched in 2011, iCloud gives users the option

to upgrade their storage levels to premium packages.

• In 2016 Apple made a deal with Google to use the Google Cloud Platform for some

iCloud services.

• Why? Provides a platform for users to backup their photos, contacts, documents –

adding to the ecosystem and becoming a more integral part of the customers life

• Benefits: As of February 2016 iCloud had 782 million users

Copyright © 2016 Accenture All rights reserved. 39

And considered examples of leading

ecosystem players

Copyright © 2016 Accenture All rights reserved. 40

And considered examples of leading

ecosystem players

Youtube: Acquired in 2006 for $1.65bn

• Why? – To “Complement Google’s mission to organise the world’s information”. New

revenue stream, huge potential for YouTube to grow and be extremely profitable for

Google.

• Benefits: Google expand product offering and make billions of dollars in advertising

revenue and Youtube got the funding, technology and expertise to

dominate the video sharing market

Android: In July 2005, Google acquired Android

Inc. for at least $50 million.

• Why? – To enter the mobile phone market

• Effect on wider ecosystem: Strong market position

for the phones and the operating systems Android

phones now make up 84% of the mobile market.

60.99% of the market share of mobile operating

systems.

Google Maps: First developed in 2005, Google Maps

has become an integral ecosystem within the wider

Google world.

• Why? - Google brand becomes more integrated in

consumers everyday lives. Provides a free useful

service that benefits customers and therefore drives

loyalty. Also uses smart partnerships – Uber and Zagat

are just two strategic partnerships, all designed to keep

the user within Google’s ecosystem.

• Benefits - For Google - You can search for a restaurant,

read reviews, book a table, find the route and hail and

Uber all in the application meaning the user never has to

leave Google. For partners – access to a platform used

by over a billion people

• Effect on wider ecosystem - Apple created its own

maps product as a response, and pre-loaded it to

iPhones and iPads

Driverless Cars - part of Google’s X programme –

started in 2009

• Why? - Potential revenue stream for Google in the

future

• Effect on wider ecosystem - Industry still in infancy

stages as driverless cars aren’t on the market yet but

already many other companies are investing in R&D

technology, including Bosch, Tesla and Uber, who

partnered with Carnegie Mellon University to launch a

research centre to develop driverless car technology

and expects to launch a driverless fleet by 2030.

Copyright © 2016 Accenture All rights reserved. 41

And considered examples of leading

ecosystem players

Google Flights: Google Flights is an online flight

booking service which facilitates the purchase of

airline tickets through third party suppliers.

• Why? – Expand Google brand and become more

integrated in consumers everyday lives. Provides a free

useful service that benefits customers and therefore can

start to build a connection with the brand

• Benefits - For the user it has additional features that

other competitors don’t, enhanced filtering options and

gamified aspects such as the “I’m feeling lucky” button

which allows spontaneous travellers to find a cheap

destination to fly to. For Google it directs more traffic

through their website.

• Effect on wider ecosystem - There was no immediate

change in the price of stocks for Priceline, Expedia, or

Travelzoo in response to the opening of Google Flights

Nexus: Mobile phones and tablets launched as flagship Android products, including those made with Motorola, LG and HTC

• Why? – They want to provide users with the ‘total user experience’ – they make the phone, create the software, sell it through their outlets and users use Google

Accounts to maintain their information, providing Google with more customer data.

• Effect on Wider Ecosystem - Created partnership opportunities within the industry, the Nexus line of products have been created in partnership with LG,

Motorola, HTC and Huawei. Can undercut competitors products such as $399 Moto X Pure with the $379 Nexus 5X, which has the added benefit of a fingerprint

sensor and matches the Moto X with a highly rated camera capable of 4K video

• Benefits - Google can show off capabilities of Android operating system, new revenue streams and access to more customer data through customers using

google accounts to store their information

Google Express offers same day or overnight

delivery from a numver of popular stores

• Why? – Google said a major goal of the initiative is

to add more utility to product search advertisements

on Google.com. On Amazon, you search for a product

and can buy it immediately. On Google, that hasn’t

been the case hence the launch of Google Express

• Benefits - The consumer benefits from the

convenience of shopping local stores all in one place

and Google improves its product search capabilities,

directs more traffic to its website and begins to take on

huge market players like amazon.

• Effect on Wider Ecosystem - Don’t have their own

warehouses like main competitor Amazon so they are

positioning themselves more as an ally, they collect

the items from local stores and make the deliveries. It

is $95 a year for membership which is slightly

undercutting amazon.

Copyright © 2016 Accenture All rights reserved. 42

And considered examples of leading

ecosystem players

Launched in 2009, GV is Google’s

venture-capital arm providing funding to

technology companies. They have

invested in over 300 companies, from

Uber to 23andMe to #slack

• Why? – Financial gain, they get a return from

the companies that they invest in, which brings

additional revenue streams.

• Benefits - For the start-ups and other

companies (in addition to the funding), they get

access to the ‘world’s best technology and

talent’ at Google. As of 2015, GV had $1.5bn in

assets and has expanded out of the USA to

Europe.

NEST: Purchased NEST for

$3.2bn in 2014 to provide

connected home devices to

customers

• Why? - To feed in to the

growing IoT movement and

position Google as a provider

of these services. Also, to get

more data on consumers and

the way they live their lives

• Benefits - For Google:

Building on an established

company and position Google

as the ‘master of the home’,

For Nest: Access to Google’s

scale and expertise to grow

their product

Google Fibre: High speed internet in a number of US cities, a solo venture

• Why? - As a test-bed for other Google services, and as an additional revenue stream

• Benefits - For Google it s a testbed for new products and with 29,000 subscribers it

has generated $12.8m revenue,

• Effect on wider ecosystem - Genuine threat to media as offer really fast and

comprehensive service to customers. Response from other broadband providers –

AT&T Gigapower rollout (cheaper cost, more speed) and C-Spire created a similar

ecosystem in Mississippi

Android Pay lets you pay in-store or in an app via your cards

stored on your account. Achieved through partnerships with

retailers (such as Lego, Nike and McDonalds), you can now

use it in over a million stores in the USA.

Why? - Direct competitor to Apple Pay

• Effect on wider ecosystem - Offers another channel for payment

and provides similar service as Apple Pay on Android phones (which

make up over 80% of the market)- Apply Pay no longer have the

monopoly.

• Benefits - For users, it is an easy way to pay for goods

or apps, for retailers it offers another way for customers

to pay, for Google it provides more data and also keeps

up competition with Apple and for banks it gives their

clients easy access to their accounts

Crisis Response: Crisis Response provides an open

platform for people to use in times of need or crises (e.g.

Japan tsunami)

• Why? - To help people in times of need, good CSR PR

• Effect on wider ecosystem - Leads more people to donation

pages so helps increase funding for crisis charities.

• Benefits - No revenue stream for Google but good PR,

consumers benefit from increased access to information and

charities receive more donations and awareness

Copyright © 2016 Accenture All rights reserved. 43

And considered examples of leading

ecosystem players

Copyright © 2016 Accenture All rights reserved. 44

London based innovation lab that collaborates

and partnership with start-up companies in Fin-

Tech; investing £100 million since 2014

• Why? To help drive innovation in the financial service

market. The fund is part of the Santander Group’s

broader innovation agenda, in which we help FinTech

companies grow from a very early stage (i.e. seed) to

a more mature stage.

• Benefits: Investing and forging partnerships with

competitors/start-ups that may ultimately create

something innovative in terms of customer experience

or operations. Santander bring the capabilities of the

Eurozone’s largest bank by market capitalisation

while start-ups bring agility, innovation and a fresh

perspective.

• Wider ecosystem impact: Santander Innoventures

portfolio includes payments specialist iZettle; mobile

payment provider MyCheck; and Cyanogen, an

android operating system experts.

Referral arrangement which will see Santander

proactively refer small business customers

looking for a loan to Funding Circle, where they

are better placed to help

• Why? Rather than leave customers who do not

qualify for a loan with Santander to work it out

themselves, Santander actively refer these people to

Funding Circle for financial help, extending the

ecosystem beyond just a product provider

• Benefits: Builds customer relationships and trust and

positions Santander as an advice provider rather than

just a source of finance

• Wider ecosystem impact: H&R Block and Sage

announced a similar partnership with Funding Circle

in 2015

And considered examples of leading

ecosystem players

Copyright © 2016 Accenture All rights reserved. 45

Partnership with TFL to provide access to

bicycles across London (replaced Barclays as the

sponsor)

• Why? To increase brand awareness. “More local

sponsorships show how we help people on a day to

day business and that it’s not just about money but

about helping people get on in life.” Keith Moor, CMO,

Santander. Santander has cycle champions across its

London branches who offer help to customers and

advice on how to use the scheme. They were also out

on the streets during the Tube strike giving people

maps of the docking stations.

• Benefits: Speaking to Marketing Week, CMO Keith

Moor said the brand has seen an uptick in brand

scores, particularly among those that use the

Santander Cycles scheme in London. Figures that

show 67% associate Santander with the scheme.

• Winder ecosystem impact: The deal with Transport

for London is part of a wider sponsorship strategy at

Santander that has seen the brand use its Formula

One tie-up to drive brand awareness globally and

then more local deals to help consumers “get under

the skin of the brand”

Santander have created an international network

of partner universities

• Why? Santander been working with Universities

since 2007 and are now partnered with 77

universities across the UK and with over 1,200

universities partners in 20 countries across the world;

offering tailor-made funding packages and initiatives

• Benefits: Increase brand awareness and customer

loyalty, specifically with students who are a potentially

high value future customer

And considered examples of leading

ecosystem players

Copyright © 2016 Accenture All rights reserved. 46

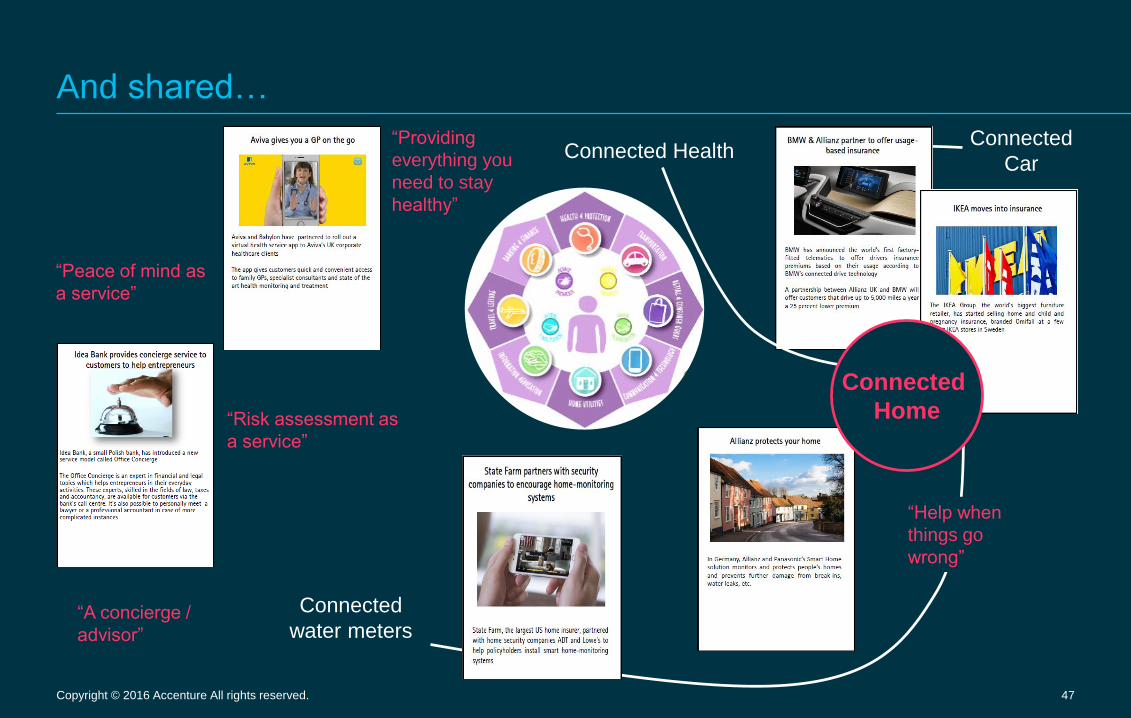

Inspired by other industries, we broke into groups to consider

what a new ecosystem for an insurer could look like

Copyright © 2016 Accenture All rights reserved. 47

Connected

water meters

Connected

CarConnected Health

“Help when

things go

wrong”

“Peace of mind as

a service”

“Risk assessment as

a service”

“Providing

everything you

need to stay

healthy”

“A concierge /

advisor”

And shared…

Connected

Home

Copyright © 2016 Accenture All rights reserved. 48

Embedded

insurance

Carpooling

“Multi-modal

mobility

insurance”

“Mobility

service”Pay as

you drive

“Carpools for

catastrophes”

Self driving

cars

Platinum

SLA’s

… our ideas

Copyright © 2016 Accenture All rights reserved. 49

About TM Forum• TM Forum was created by its members for its members

to connect via an ecosystem platform

• It launched 28 years ago with just ten telco companies. It

has now expanded to include players from multiple

industries including Google and Alibaba

• TM forum helps organisations to engage with relevant

players through APIs, contracts, partnerships and

standards supported within the platform

• Everyone in the TM Forum gets access to and learns

from all the projects that the network members work on

together

Key Takeaways

Peter Sany, introduced us to TM Forum’s ecosystem platform over

a fireside discussion

TM Forum Case Studies

“The future for insurance will be a form of collaboration

involving partners from lots of different areas”

“You can’t solve everything yourself. Take the

autonomous car for example – the car manufacturer

needs to connect with the city infrastructure, the

pedestrian infrastructure and the communication

provider – all connected by a digital backbone!”

“Forget about the regulators – Uber might have had to

withdraw from 4 or 5 cities, perhaps - but how many

markets are they still in? Hundreds!”

Copyright © 2016 Accenture All rights reserved. 50

The forum has 20 executive-level

members at present , each committing 2-

3 hours per month, and is managed by

TM Forum.

Members have access to: • Knowledge from the top global insurers

• Long-lasting Insurance thought leadership

• Partners from the wider insurance ecosystems

• Digital transformation and platform technology expertise

• Academia

Members have the opportunity to:• Build peer-to-peer relationships with counterparts around the world

• Guide the research agenda for the Smart Insurance Think Tank

• Drive innovation through Catalyst proof-of-concept projects

• Enhance their company’s digital value proposition to customers,

partners, shareholders, etc

• Drive best practice creation (e.g. maturity models, open data

platform, crowdsourcing and linking data, data analytics)

• Position their company as a world leader through all TM Forum

channels

• Be invited as a keynote speaker for TM Forum events

We considered the potential for insurers to partner with the Smart

Insurance Forum which is currently being built

Smart

Insurance

Leaders1

Digital

Ecosystem

Players2

Consultancies

and

Suppliers3

2x Co-Chair

Smart

Insurance

Think Tank

Group1 Rotating Chair

Copyright © 2016 Accenture All rights reserved. 51

Day Two

Managing & Operationalising Innovation

Copyright © 2016 Accenture All rights reserved. 52

The journey on day two…

… began with a recap of day one and inspiration for

innovating like a start-up

Tara Brown, Stuart Baldwin and Stephane Guinet then came

together to talk to us about preparing for and managing

disruption, implementing ideas and building an innovative

workforce

Next we questioned the insurance orthodoxies that are

holding us back

We then thought about the skills, supply chain, technologies

and employee experience that will be critical for our

workforce in the future with Colin Sloman

Finally we wrapped up and considered our key takeaways

from the previous two days

Copyright © 2016 Accenture All rights reserved. 53

We started by watching a video to remind us of what we had

learnt on day one

Copyright © 2016 Accenture All rights reserved. 54

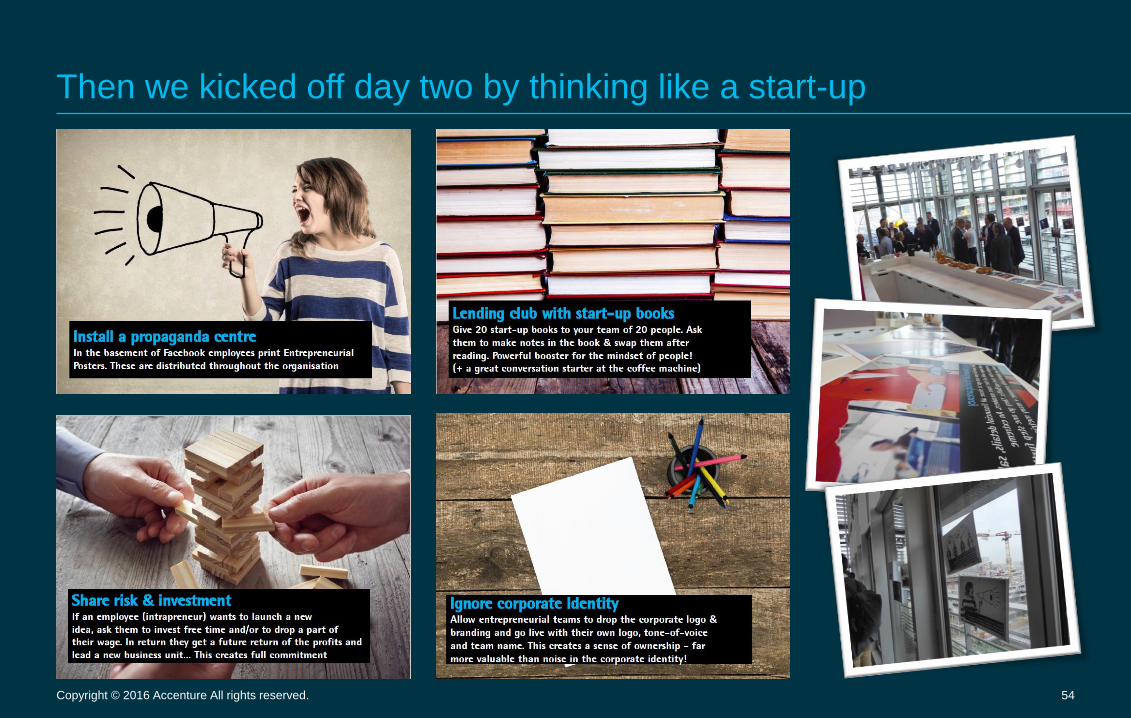

Then we kicked off day two by thinking like a start-up

Copyright © 2016 Accenture All rights reserved. 55

We considered how we can make our organisations more

innovative with a panel of experts

Copyright © 2016 Accenture All rights reserved. 56

There were a number of key takeaways

Innovation does not stop with ideation: It also involves implementation and

dissemination

Leadership needs to make it clear that innovation is important and funding won't be

cut

Leaders need to not only manage tasks but also focus on making a difference to

culture in order to get the best out of their employees. Ten years from now we want

the way that we lead people to stimulate creativity

Culture-change needs to be driven by leaders and innovators need to work within

the organisational aims and needs in order to achieve buy-in

Employees need to be empowered to treat every decision as if it were there own

business

Everyone needs to be trained to question regulation

It is important to consider which elements of innovation are achieved internally and

which are better achieved through partnerships and platforms

You can’t afford not to take risks!

Copyright © 2016 Accenture All rights reserved. 57

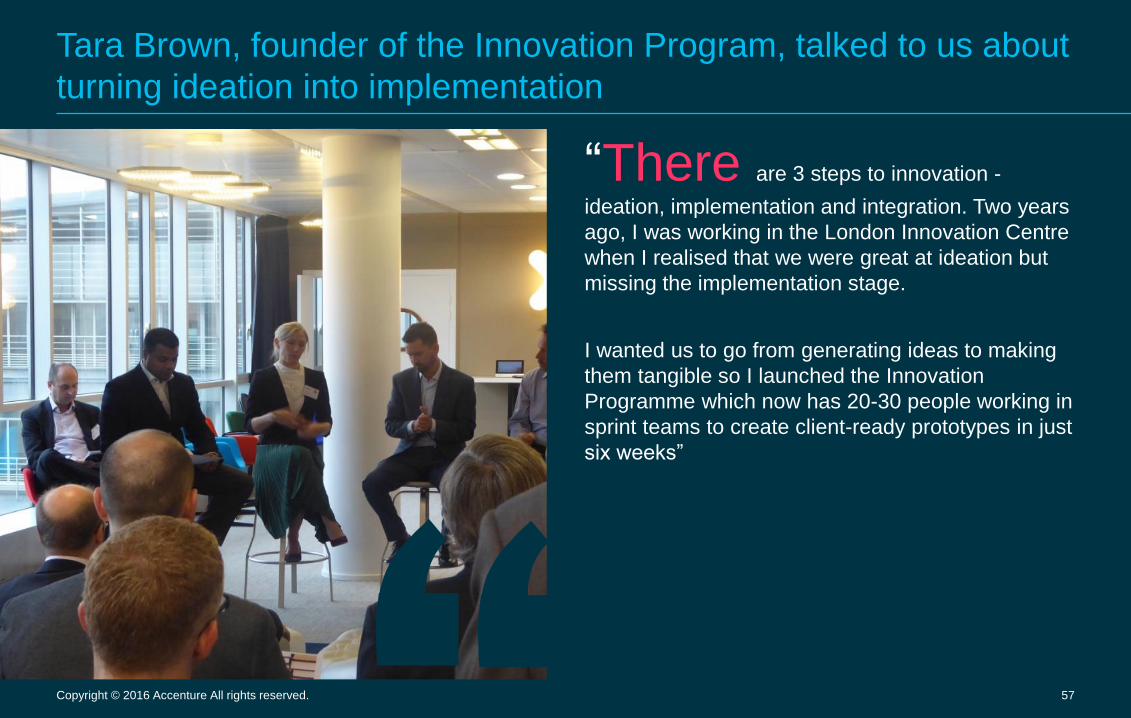

“There are 3 steps to innovation -

ideation, implementation and integration. Two years

ago, I was working in the London Innovation Centre

when I realised that we were great at ideation but

missing the implementation stage.

I wanted us to go from generating ideas to making

them tangible so I launched the Innovation

Programme which now has 20-30 people working in

sprint teams to create client-ready prototypes in just

six weeks”

Tara Brown, founder of the Innovation Program, talked to us about

turning ideation into implementation

Copyright © 2016 Accenture All rights reserved. 58

“My aim is to help companies to live

big and make employees love their work. We need

to be as good at innovating people as we are at

innovating products. The direct line manager is the

key to better, happier employees and more

successful, innovative companies. Leaders need

not to only manage tasks but to set us up to grow.

I am driven by how kids think. They have an

openness and confidence that will be hard to keep

hold of in the future. “

Stuart Baldwin, from The Positive Company, considered how to

unleash a happier, more engaged workforce

Copyright © 2016 Accenture All rights reserved. 59

“AXA realised that our business will not

survive if we do not change dramatically so we

created two labs in San Francisco and Shanghai to

connect with interesting start-ups from outside our

organisation.

We need a new way to approach the future and

need to be less risk averse - failure is part of the

innovation process and should be celebrated. In a

large organisation it is too easy to say “No” – we

need a different mind-set.

I lead Kamet – a £100m incubator which initially is

100% funded by AXA. This has the remit and

decision-making autonomy to develop and create

real, tangible propositions which have the potential

to cannibalise and break the traditional business

model at AXA”

Stephane Guinet, CEO of Kamet, talked to us about preparing for

and managing disruption

Copyright © 2016 Accenture All rights reserved. 60

And we had plenty of questions for the panel

HOW DO WE CHANGE MIND-SETS?

REGULATION

FUNDING

WHERE DO WE START?

GENERATING BUY-IN

BUSINESS MODELS

Copyright © 2016 Accenture All rights reserved. 61

A Question of Getting Started

How did you get started and how do you fund your

innovation programs?

Tara Brown

The Innovation Programme is funded by R&D tax credits

for Accenture across all industries. We began by

determining what we would define success as and what the

criteria was for funding. We then trained the team,

generated ideas and created a funnel. We later built the

team out further.

For each project, we undergo two sprints of two weeks to

build out a design. We are flexible about where the project

takes us.

Once we have created something for one industry, we can

think about how we can apply it to other industries too.

We’re constantly looking for new experiences and skills, for

example considering what the new exciting technologies

are or how we can run hackathons.

How do you get CEOs and leaders to embrace

innovation when they are focused on delivering

what their shareholders ask them to do,

rationalising profits and cutting costs?

Tara Brown

You need buy in from leadership and the people who will

eventually be using whatever you create. Innovations are

difficult to diffuse in a company if there is no need for them

in the first place so you need to give leaders and users a

say in what it is and how it is used from the beginning… It

also makes sense to tell your innovation team what leaders

want to do and to let them come up with ideas that help

them to achieve it.

We make sure that we are coming up with something very

tangible, taking into account challenges, effectiveness and

cost-effectiveness. There is also no point bringing in jazzy

new things for the sake of it - you need to be fixing an

existing pain.

Stephane Guinet

Innovation needs to come from the top if you want your

company as a whole to embrace it. It needs to be ingrained

in top management and to then be diffused down to

strategy, HR, Business Development etc.

Copyright © 2016 Accenture All rights reserved. 62

A Question of People

How do we make our people more innovative?

Tara BrownWhen everyone has their day jobs it's hard to say “now be more

innovative” without having a structure. This is why we split our

program out as a mini rotation (a mini sabbatical within your normal

role)… We have also learnt that innovation works so much better

when you bring different people with different knowledge together

Stuart BaldwinHere today we have brilliant thinkers and thought leaders around

technology, process and ideas. We need the same thing around

people. Ten years from now we want the way people are led to

stimulate creativity. How do we do this? Every manager in a company

needs to think about how they'll alter behaviour each day rather than

just thinking about all the tasks they need to get done.

There are six core skills that leaders need to draw out in people in

order to drive performance: Optimism, Purpose, Focus, Questions,

Impact and Creativity. We need to make an impact with our

behaviours, change the stories that employees tell themselves about

the past, drive our people with a real sense of purpose and

encourage them to “give it a go”.

How do you build a more innovative culture within

your organisation in a world full of Gantt charts?

Roy JubrajIn Accenture we have a deep culture to drive out activity and

engagement. We gave people tools like Yammer (and internal

collaboration software) to get juices flowing and to drive collaboration.

We then allowed these to grow organically and we let our employees

drive the agenda.

Stuart BaldwinHumans are driven by two desires: pleasure and pain avoidance.

93% of what we are doing is looking for things that will kill us and

therefore 93% of what we think about is irrelevant. That’s the sticking

point but we can coach people’s stories and psychology to change

the way they feel.

Stephane GuinetWe need employees to be empowered to treat every decision as if it

were their own company. I’m not a boss; I’m a coach and peer. My

people can call me whenever they want my opinion but if I have put

them in a position then I want them to make the decisions … At AXA

employees can partner to come up with new ideas. The best ideas

are voted for. The problem is then execution. We need to empower

and help navigate people to execute these ideas.

Copyright © 2016 Accenture All rights reserved. 63

A Question of Business Models

What have you learnt about innovative business

models?

Stephane Guinet

We can never modernise fast enough but, even if we could,

this is not enough. If we really want to drive customer value

we need to work with other people. The models of the

future need to be more transparent, more collaborative and

aligned with the interests of the customer.

When you are a large organisation you need certain

processes in place and this is not compatible if you want to

create real innovation. Sometimes a separate start-up is

the answer because when we are dealing with a large

organisation, often you need to build something that is

sufficiently mature before the large organisation will

recognise it and react to it. Then the large organisation can

integrate this into the core and build on it.

How do we get organisations to invest appropriately

in R&D?

Roy Jubraj

We shouldn’t just be looking at discretionary funding in a

separate pocket. Funding should be critical to the core of

the business. When things get tough, funding tends to be

cut around innovation. Leadership needs to make it clear

that innovation is important and funding won't be

cut. Quarterly metrics around innovation need to be put in

place.

Tara Brown

The more we change people’s culture and mind-set, and

the more you create in this space, the easier it will get and

the better firms will be at challenging these things.

Copyright © 2016 Accenture All rights reserved. 64

A Question of Regulation

Regulation is a whole new areas of pain and fear

for my company. How do we balance start-up

culture against risk culture?

Roy Jubraj

It’s all about interpretation. Risk Committees often interpret regulation as

being worse than it actually is. This creates a culture where you can’t try

anything new. You need a culture of education to get people challenging

the status quo and asking why. If you are doing something that is not

benefiting customers and is not the right approach people need to be

asking “why are we doing this?”

Stephane Guinet

There is a culture element here. The risk committee is paid to say no. They

need to be incentivized not to say no but to help the business go forwards.

The question should be “if this were your own money would you spend it?”

Stuart Jubraj

The Romans were very fond of stoicism. They would look at all the risks

and problems and neutralise them by imaging the very worst that could

happen and being comfortable with it. Then they would ask “What's the

best that could happen? And how do we make this happen?”

Tara Brown

Our most important relationship is with the compliance and risk teams. We

need to understand what is the worst that can happen and how do we

avoid that.

How can we be innovative when everyone is

concerned about their personal accountabilities? The

beauty of start-ups is that they have a different

mentality and are less concerned about what might

happen…

Roy Jubraj

A start-up still has huge risks. They are playing with someone else’s

money and need to legitimise everything that they do.

Stuart Baldwin

We have to think about the risk in not taking risks. This reminds me of

the well known joke where someone says “What is the point in

training my people if they'll just get good and leave?” The real risk is,

“what if I don’t train my people, they’re bad at their job and they stay”.

The same could be applied to innovation. “What’s the point of

innovative ideas if they’ll just be taken?” I have friends who work for

What If Innovation. Their philosophy after ten years experience is that

actually you just need to try something - “Just do it!”

Tara Brown

Richard Branson said “Train them well enough that they want to go,

but treat them well enough that they choose to stay”.

Copyright © 2016 Accenture All rights reserved. 65

And we had some comments to share

“Have we used tax credits for innovation?

Yes, but in the wrong way! They sit in

finance but we need to think about how we

drag them out of finance and use them to

fund innovation differently”

“Sometimes bad ideas come

up and people say “ah, this is

innovation!” – we need to

filter these ides”

“Is insurance a freestanding

natural product by itself… Or

should it be embedded in

something else?”

“We had nothing going live and

we were losing momentum so we

changed the structure completely.

We used the crowd to identify the

best way to do the execution”

”The culture needs to come from the top so that the company

as a whole can embrace it. It needs to be ingrained in top

management. In our company the chairman doesn’t even

have a smartphone. He doesn’t even use a PC on a daily

basis. When you email him his EA prints out the email”

“The way we do innovation right now is too

incremental and not disruptive enough. We tried

to fast-track ideas but that wasn’t enough. We

need to work out an investment strategy and we

want to take ideas through to implementation. We

have run a Dragon’s Den competition and started

providing start-up kits”

Copyright © 2016 Accenture All rights reserved. 66

Next, we thought about how orthodoxies can act as barriers to

innovation

Copyright © 2016 Accenture All rights reserved. 67

Regulators

won’t let us

changeTechnology

is expensive

Insurance

is sold not

bought

Actuaries are

needed (and

they can’t party)

Most people

want to buy

insurance

annually

We can’t do it

because the

intermediaries

don’t like it

Our people

don’t have

the skills

We are a

customer

business

Insurance will

get disrupted

by someone

else/ we are on

the defence

People

Need

Insurance

We know

better than

the

customer

The most

important thing

is to guarantee

performance

for the next

month

We are an

industry of

followers who

don’t believe in

first-mover

advantage

Legacy

systems stop

us from

innovating

If I’ve tried it

and it didn’t

work, it won’t

work again

Insurance

needs to be

assessed on

the past

Bigger is

better

Middle-aged

straight white

blokes run

insurance best

We will not

get disrupted

because we

are regulated

Claimants

want to

defraud the

company

We don’t

trust our

customers

Only we can

do insurance

because it is

complicated

Innovation &

disruption

only comes

from start-

ups

One day the

UK

automotive

market will

make money

Digitalisation is

the problem of

the Chief

Information

Officer (not the

Chief Investment

Officer)

We can’t

be loved

The only way

to get things

done is a multi-

year multi-

million-dollar

projectResults of

the past

can predict

the future

And we thought about the orthodoxies that are holding us back

Copyright © 2016 Accenture All rights reserved. 68

Colin Sloman then introduced us to how the workforce might look

in the future

Copyright © 2016 Accenture All rights reserved. 69

How do we create a digital workforce when only 2% of graduates

want to work in insurance?

Copyright © 2016 Accenture All rights reserved. 70

We considered some key ideas

Top Coder splits

projects into bite

sized pieces that

are offered to its

worldwide

community of

developers

Spotify divides its staff

into constantly

changing “squads” –

each one run like a

business in its own

right. Autonomy is

given at every level to

avoid decision-making

bottlenecks

Beyond verbal is a

software that can

detect 400 variations

in human moods. This

can be integrated into

call centres to help

staff understand and

react to human

emotions

Audi uses analytics

to turn customer

response to product

features into real-

time alterations to

products

GE uses sensor-

based analytics to

report on its

machinery in real-

time and develop

predictive

maintenance

algorithms

35% of jobs are at

risk of automation

over the next 20

years

Microsoft is

using

gamification to

identify more

bugs during

testingRio Tinto has a

workerless mine in

Australia –

autonomous trucks,

excavators and drills

are controlled by

remote operators,

hundreds of

kilometres away

3,200,000

workers in

Japan are

robots

EE use coding

schools t improve

the digital literacy

of their

employees

1/3 of the US

workforce are

currently

freelancers and

over 40% will be

freelancers by

2020

Uber has 160,000

contractors but

just 2000

employees – a

ratio of 80:1

Lego

crowdsources new

product ideas that

over users can

vote on – the

creator receives

1% of royalties

The CEO of

Salesforce often

participates in

conversation threads

to keep up to date on

the thinking of his

workforce and to

establish a presence

amongst staff

70% of CEOs believe

their presence on

social media has a

positive impact on

business results but

75% have no

engagement plan or

strategy

7-Eleven places

ordering decisions

directly in the

hands of 200, 000

sales people

Copyright © 2016 Accenture All rights reserved. 71

“There is so much change

with the ratio of contractors

to workers at 80:1”

“We need transparency,

knowledge sharing and

total collaboration”

“We need to forget hierarchies and

structures. You have your go to guys -

That's what a social network view of the

organisation looks like”

“How do we personalise

the experience for multiple

generations all working

together?”

“The future of HR will be to be

absent and let managers create

a personalised experience”

“We really need to think about where we

automate, where we use AI and where we

use people to create the greatest value”

“How could we use facial recognition

to understand the impact of our

leaders on employees?”

“How can we use insights and

analytics to build a 360 degree

view of the employee?”

“Work should not just be a place

you earn money, it should be

something you do for yourself”

“HR needs to become more like

marketing, understanding segments,

offers, products and how to engage

particular employees”

“We need to filter data

into information to make

it accessible”

“Need to lose the attitude of

I am what I know and I lose

my power if I share this”

“Leaders need to be open to ideas, not selective

about where ideas come from and they need to

besupportive of testing, trying and engaging”

“Leaders need to change

the orthodoxy of ‘what I

know is what works best’”

“Leadership needs

to introduce the

change”

The Workforce

of the FutureLeadership

& Skills

Employee

Experience

Technology

Enablers

Talent &

Supply

Chain

And we reflected on what we need to think about to prepare our

workforces for the future

Copyright © 2016 Accenture All rights reserved. 72

We broke into groups to think about the roles that the future will

create or change

Copyright © 2016 Accenture All rights reserved. 73

Empathy

Collaboration

Unafraid of

confrontation

Visualise

data

And we designed new roles, skills and capabilities that our

organisations might need

Copyright © 2016 Accenture All rights reserved. 74

And we determined which of these would make up the high value,

scarce talent composing the critical workforce

Scarce

Low

Value

Plentiful

High

Value

Copyright © 2016 Accenture All rights reserved. 75

Inspired by some examples, we then considered innovative ways to

attract and retain, develop and enable this talent

Copyright © 2016 Accenture All rights reserved. 76

Inspired by some examples, we then considered innovative ways

to attract, retain and develop this talent

Reverse

mentoring

Don’t employ

them! (in the traditional sense)

Give space

to meditate

Provide inspiration

We don’t need

an office Create an

under 35

shadow board

Give the

freedom to

pick projects

Focus on

behaviours

not values

Offer global opportunities

Copyright © 2016 Accenture All rights reserved. 77

“You can say you want to be data driven,

but unless you can get something to the

front line, it’s like saying you want to lose

weight by looking at fitness apps”

“Jobs and titles go away –

instead you have a role that

might change regularly”“We need to change the

language of the

company”

“We need to shape our talent

management to align with our

customer vision”

“Do we need a culture

design specialist?”“The way you treat

customers is key for

business – so there is still a

role for a claims agent at the

moments of truth”

“A claims agent is a customer

empathiser – they should be

empowered”

“We need people with

empathy, design skills and

creativity”

“Culture and leadership is

our big challenge” “We will have to reinvent ourselves

several times over our career”

“Data and technology are possible,

but are you actually executing what

is critical for the customer?”

And shared our thoughts as a group

Copyright © 2016 Accenture All rights reserved. 78

Finally, we wrapped up and reflected on the past two days

Copyright © 2016 Accenture All rights reserved. 79

“The balance of

different topics was

great – it feels more

rounded than just

another discussion

about the latest

technology trends”

“There are so many messages – I

need more time to digest them all”

“A lot of what was shared

here will shape my thinking

over the next 12 months”

“We really started to

think about how we

operationalise these

ideas”

“It’s a great group of people

coming together and that

allows you to really get

beneath the surface”

“Speaking to Trov was great as

you could see it live…it felt real.

That’s what really resonated –

I’d like to see more of that in the

next session”

“I take so many notes when I come to the

DIN – 15-20 pages, That just shows how

interesting it is!”

“Day 1 felt very fast paced and

today felt more reflective.. To

me that was right”

We shared our thoughts on the past 24 hours

Copyright © 2016 Accenture All rights reserved. 80

“The pace of change

always amazes me –

it’s moving so fast”

“25 years ago insurance