Embed Size (px)

Citation preview

HARRY E. BLOUNT [email protected]

415-274-5452

The HDD Industry Transformed: New Risks and Opportunities Emerge

February 13, 2007February 13, 2007February 13, 2007February 13, 2007

Lehman Brothers does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this email communication.

Customers of Lehman Brothers in the United States can receive independent, third-party research on the company or companies covered in this report, at no cost to them, where such research is available. Customers can access this independent research at www.lehmanlive.com or can call 1-800-2-LEHMAN to request a copy of this research.

Investors should consider this communication as only a single factor in making their investment decision

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 39

Harry E. Blount, [email protected]

415-274-5452

Public Company Research Coverage

EnterpriseHardware

Storage Services

Enterprise Storage

Dot Hill

EMC

NTAP

TechnologyDistribution

Arrow

Avnet

Ingram

Tech Data

Storage Networking

Brocade

Emulex

QLogic

Disk Drives and Tape

Quantum

Seagate

WDC

Consumer Hardware

Apple

Dell

HP

Dell

HP

IBM

Sun

Akamai

Equity Research Excellence

Ranked #1 in 2003, 2004, 2005, and 2006 All-America Survey.

# 3#1

Institutional Investor

1

Harry E. Blount, [email protected]

415-274-5452

Agenda

� Industry Report Card

� Share Shifts

� Competitive Analysis and Outlook

� Where Should HDD Stocks Be Valued?

2

Harry E. Blount, [email protected]

415-274-5452

Industry Report Card

2006 Was a Pretty Good Year

3

Harry E. Blount, [email protected]

415-274-5452

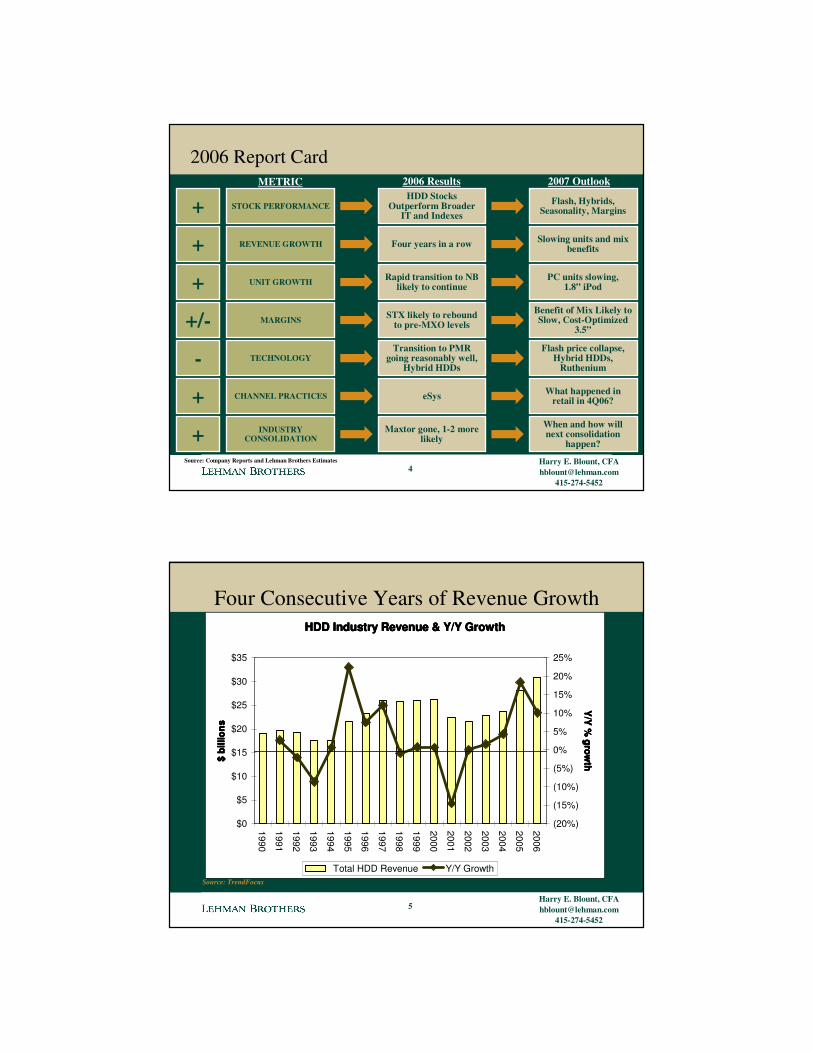

2006 Report Card

Rapid transition to NB likely to continueUNIT GROWTH PC units slowing,

1.8” iPod

STX likely to rebound to pre-MXO levelsMARGINS

Benefit of Mix Likely to Slow, Cost-Optimized

3.5”

Transition to PMR going reasonably well,

Hybrid HDDsTECHNOLOGY

Flash price collapse, Hybrid HDDs,

Ruthenium

Four years in a rowREVENUE GROWTH Slowing units and mix benefits

METRIC 2006 Results 2007 OutlookHDD Stocks

Outperform Broader IT and Indexes

STOCK PERFORMANCE Flash, Hybrids, Seasonality, Margins

CHANNEL PRACTICES What happened in retail in 4Q06?eSys

INDUSTRY CONSOLIDATION

When and how will next consolidation

happen?Maxtor gone, 1-2 more

likely

+

-

+

+

+

+

+/-

Source: Company Reports and Lehman Brothers Estimates4

Harry E. Blount, [email protected]

415-274-5452

Four Consecutive Years of Revenue GrowthHDD Industry Revenue & Y/Y GrowthHDD Industry Revenue & Y/Y GrowthHDD Industry Revenue & Y/Y GrowthHDD Industry Revenue & Y/Y Growth

$0

$5

$10

$15

$20

$25

$30

$35

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

$ bi

llion

s$

billi

ons

$ bi

llion

s$

billi

ons

(20%)

(15%)

(10%)

(5%)

0%

5%

10%

15%

20%

25%

Y/Y

% grow

thY

/Y %

growth

Y/Y

% grow

thY

/Y %

growth

Total HDD Revenue Y/Y Growth

5

Source: TrendFocus

Harry E. Blount, [email protected]

415-274-5452

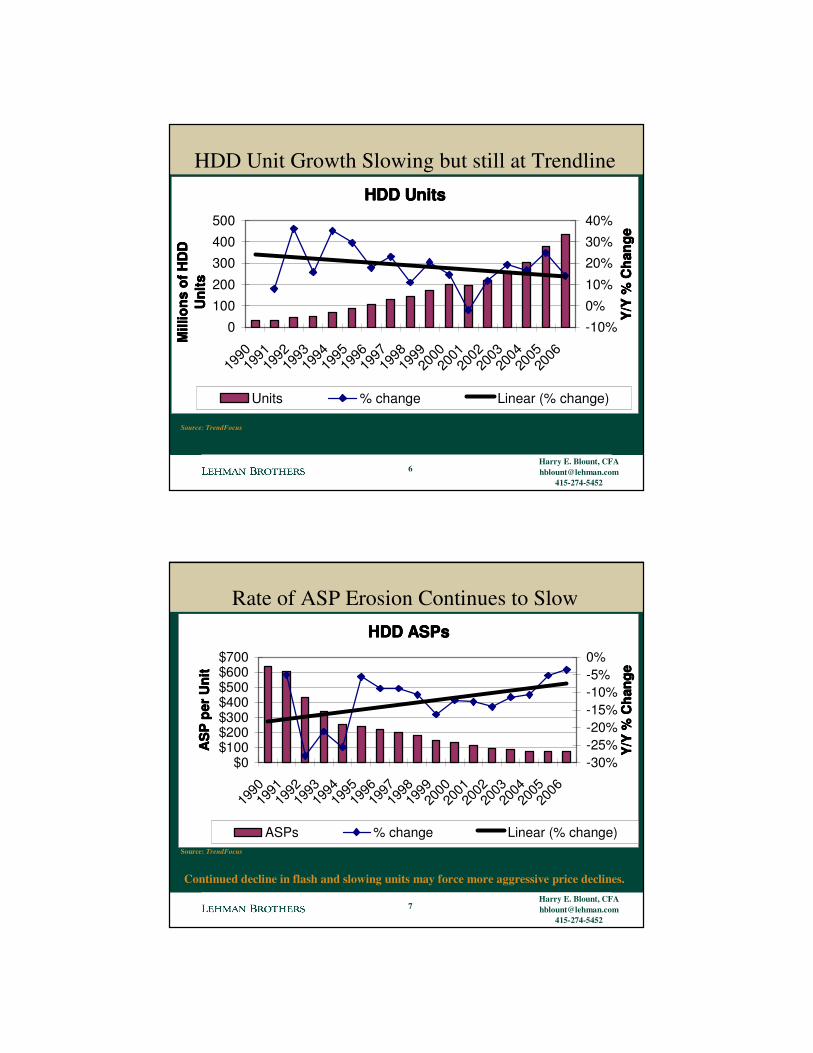

HDD Unit Growth Slowing but still at Trendline

Source: TrendFocus

HDD UnitsHDD UnitsHDD UnitsHDD Units

0

100

200

300

400

500

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Mill

ions

of H

DD

M

illio

ns o

f HD

D

Mill

ions

of H

DD

M

illio

ns o

f HD

D

Uni

tsU

nits

Uni

tsU

nits

-10%

0%

10%

20%

30%

40%

Y/Y

% C

hang

eY

/Y %

Cha

nge

Y/Y

% C

hang

eY

/Y %

Cha

nge

Units % change Linear (% change)

6

Harry E. Blount, [email protected]

415-274-5452

Rate of ASP Erosion Continues to Slow

Source: TrendFocus

HDD ASPsHDD ASPsHDD ASPsHDD ASPs

$0$100$200$300$400$500$600$700

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

AS

P p

er U

nit

AS

P p

er U

nit

AS

P p

er U

nit

AS

P p

er U

nit

-30%-25%-20%-15%-10%-5%0%

Y/Y

% C

hang

eY

/Y %

Cha

nge

Y/Y

% C

hang

eY

/Y %

Cha

nge

ASPs % change Linear (% change)

Continued decline in flash and slowing units may force more aggressive price declines.

7

Harry E. Blount, [email protected]

415-274-5452

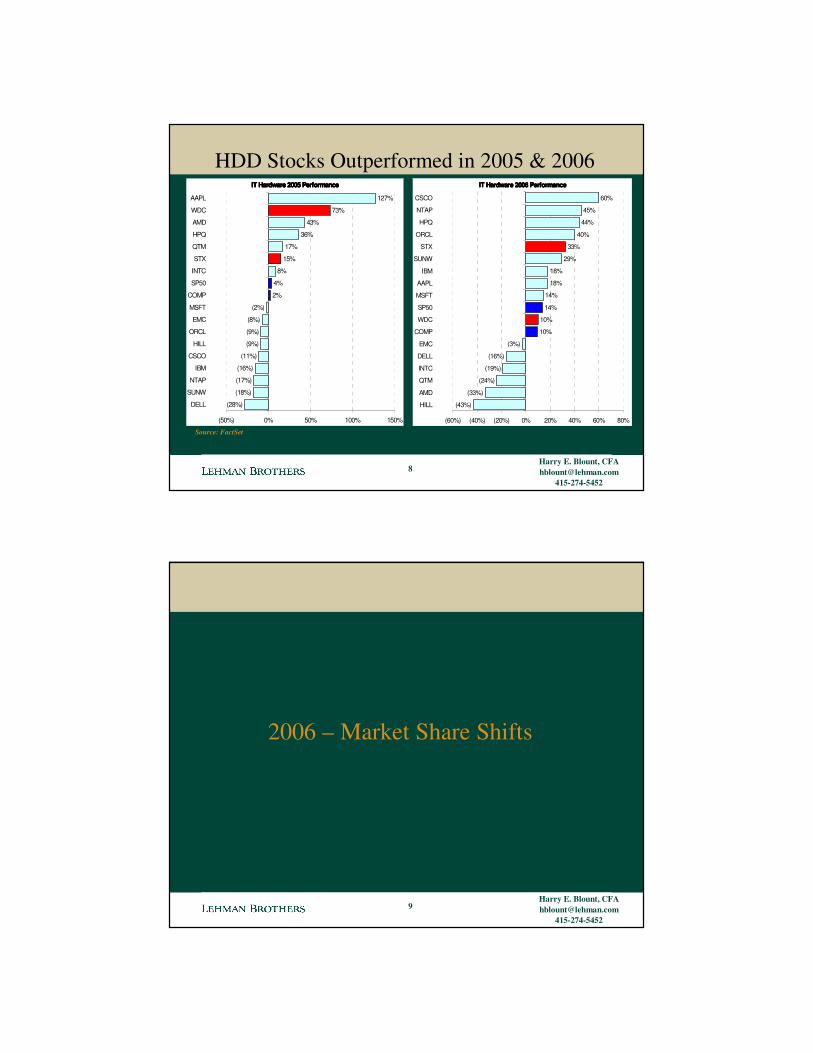

HDD Stocks Outperformed in 2005 & 2006IT Hardware 2005 PerformanceIT Hardware 2005 PerformanceIT Hardware 2005 PerformanceIT Hardware 2005 Performance

73%

15%

8%

4%

2%

(2%)

43%

36%

17%

(8%)

(9%)

(9%)

(11%)

(16%)

(17%)

(18%)

(28%)

127%

(50%) 0% 50% 100% 150%

DELL

SUNW

NTAP

IBM

CSCO

HILL

ORCL

EMC

MSFT

COMP

SP50

INTC

STX

QTM

HPQ

AMD

WDC

AAPL

IT Hardware 2006 PerformanceIT Hardware 2006 PerformanceIT Hardware 2006 PerformanceIT Hardware 2006 Performance

45%

29%

18%

18%

14%

14%

44%

40%

33%

10%

10%

(3%)

(16%)

(19%)

(24%)

(33%)

(43%)

60%

(60%) (40%) (20%) 0% 20% 40% 60% 80%

HILL

AMD

QTM

INTC

DELL

EMC

COMP

WDC

SP50

MSFT

AAPL

IBM

SUNW

STX

ORCL

HPQ

NTAP

CSCO

Source: FactSet

8

Harry E. Blount, [email protected]

415-274-5452

2006 – Market Share Shifts

9

Harry E. Blount, [email protected]

415-274-5452

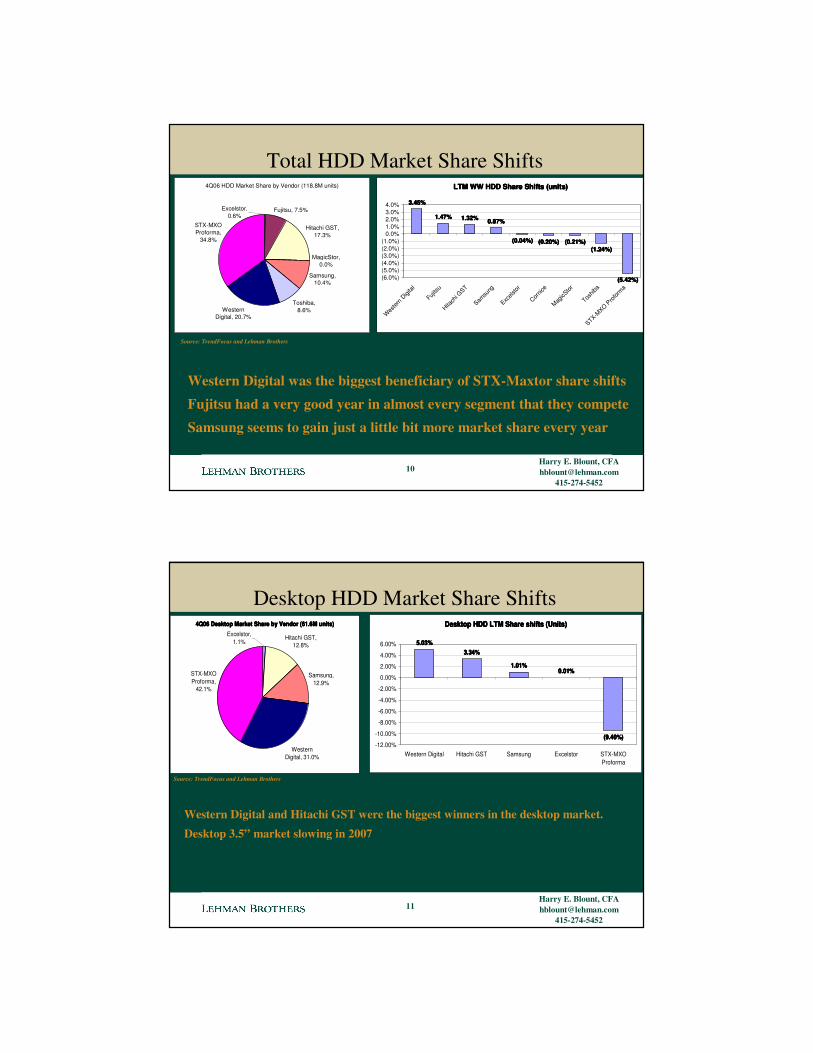

Total HDD Market Share Shifts

Source: TrendFocus and Lehman Brothers

LTM WW HDD Share Shifts (units)LTM WW HDD Share Shifts (units)LTM WW HDD Share Shifts (units)LTM WW HDD Share Shifts (units)

3.45%3.45%3.45%3.45%

1.47%1.47%1.47%1.47% 1.32%1.32%1.32%1.32% 0.87%0.87%0.87%0.87%

(0.04%)(0.04%)(0.04%)(0.04%) (0.20%)(0.20%)(0.20%)(0.20%) (0.21%)(0.21%)(0.21%)(0.21%)(1.24%)(1.24%)(1.24%)(1.24%)

(5.42%)(5.42%)(5.42%)(5.42%)(6.0%)(5.0%)(4.0%)(3.0%)(2.0%)(1.0%)

0.0%1.0%2.0%3.0%4.0%

Wes

tern D

igital

Fujitsu

Hitach

i GST

Samsu

ng

Excels

tor

Cornic

e

MagicS

tor

Toshib

a

STX-MXO P

rofor

ma

4Q06 HDD Market Share by Vendor (118.8M units)

Fujitsu, 7.5%

Hitachi GST, 17.3%

MagicStor, 0.0%

Samsung, 10.4%

Toshiba, 8.6%Western

Digital, 20.7%

STX-MXO Proforma,

34.8%

Excelstor, 0.6%

Western Digital was the biggest beneficiary of STX-Maxtor share shiftsFujitsu had a very good year in almost every segment that they competeSamsung seems to gain just a little bit more market share every year

10

Harry E. Blount, [email protected]

415-274-5452

Desktop HDD Market Share Shifts

Source: TrendFocus and Lehman Brothers

Desktop HDD LTM Share shifts (Units)Desktop HDD LTM Share shifts (Units)Desktop HDD LTM Share shifts (Units)Desktop HDD LTM Share shifts (Units)

5.03%5.03%5.03%5.03%3.34%3.34%3.34%3.34%

1.01%1.01%1.01%1.01%0.01%0.01%0.01%0.01%

(9.40%)(9.40%)(9.40%)(9.40%)-12.00%

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

Western Digital Hitachi GST Samsung Excelstor STX-MXOProforma

4Q06 Desktop Market Share by Vendor (61.6M units)4Q06 Desktop Market Share by Vendor (61.6M units)4Q06 Desktop Market Share by Vendor (61.6M units)4Q06 Desktop Market Share by Vendor (61.6M units)

Hitachi GST, 12.8%

Samsung, 12.9%

Western Digital, 31.0%

STX-MXO Proforma,

42.1%

Excelstor, 1.1%

Western Digital and Hitachi GST were the biggest winners in the desktop market.Desktop 3.5” market slowing in 2007

11

Harry E. Blount, [email protected]

415-274-5452

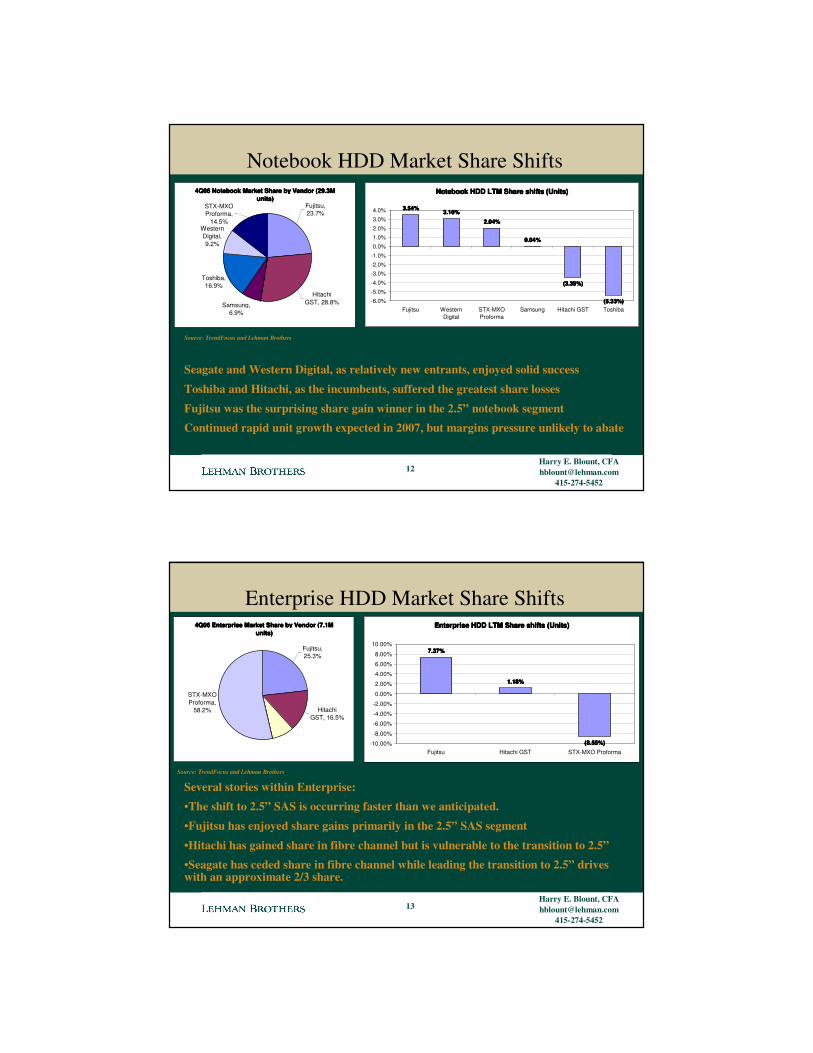

Notebook HDD Market Share Shifts

Seagate and Western Digital, as relatively new entrants, enjoyed solid success

Toshiba and Hitachi, as the incumbents, suffered the greatest share losses

Fujitsu was the surprising share gain winner in the 2.5” notebook segmentContinued rapid unit growth expected in 2007, but margins pressure unlikely to abate

Source: TrendFocus and Lehman Brothers

Notebook HDD LTM Share shifts (Units)Notebook HDD LTM Share shifts (Units)Notebook HDD LTM Share shifts (Units)Notebook HDD LTM Share shifts (Units)

3.54%3.54%3.54%3.54%3.10%3.10%3.10%3.10%

2.04%2.04%2.04%2.04%

0.04%0.04%0.04%0.04%

(3.39%)(3.39%)(3.39%)(3.39%)

(5.33%)(5.33%)(5.33%)(5.33%)-6.0%

-5.0%

-4.0%

-3.0%-2.0%

-1.0%

0.0%

1.0%2.0%

3.0%

4.0%

Fujitsu WesternDigital

STX-MXOProforma

Samsung Hitachi GST Toshiba

4Q06 Notebook Market Share by Vendor (29.3M 4Q06 Notebook Market Share by Vendor (29.3M 4Q06 Notebook Market Share by Vendor (29.3M 4Q06 Notebook Market Share by Vendor (29.3M units)units)units)units)

Samsung, 6.9%

Toshiba, 16.9%

Western Digital, 9.2%

Hitachi GST, 28.8%

Fujitsu, 23.7%

STX-MXO Proforma,

14.5%

12

Harry E. Blount, [email protected]

415-274-5452

Enterprise HDD Market Share Shifts

Several stories within Enterprise:•The shift to 2.5” SAS is occurring faster than we anticipated.

•Fujitsu has enjoyed share gains primarily in the 2.5” SAS segment

•Hitachi has gained share in fibre channel but is vulnerable to the transition to 2.5”•Seagate has ceded share in fibre channel while leading the transition to 2.5” drives with an approximate 2/3 share.

Source: TrendFocus and Lehman Brothers

Enterprise HDD LTM Share shifts (Units)Enterprise HDD LTM Share shifts (Units)Enterprise HDD LTM Share shifts (Units)Enterprise HDD LTM Share shifts (Units)

7.37%7.37%7.37%7.37%

1.18%1.18%1.18%1.18%

(8.55%)(8.55%)(8.55%)(8.55%)-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Fujitsu Hitachi GST STX-MXO Proforma

4Q06 Enterprise Market Share by Vendor (7.1M 4Q06 Enterprise Market Share by Vendor (7.1M 4Q06 Enterprise Market Share by Vendor (7.1M 4Q06 Enterprise Market Share by Vendor (7.1M units)units)units)units)

STX-MXO Proforma,

58.2% Hitachi GST, 16.5%

Fujitsu, 25.3%

13

Harry E. Blount, [email protected]

415-274-5452

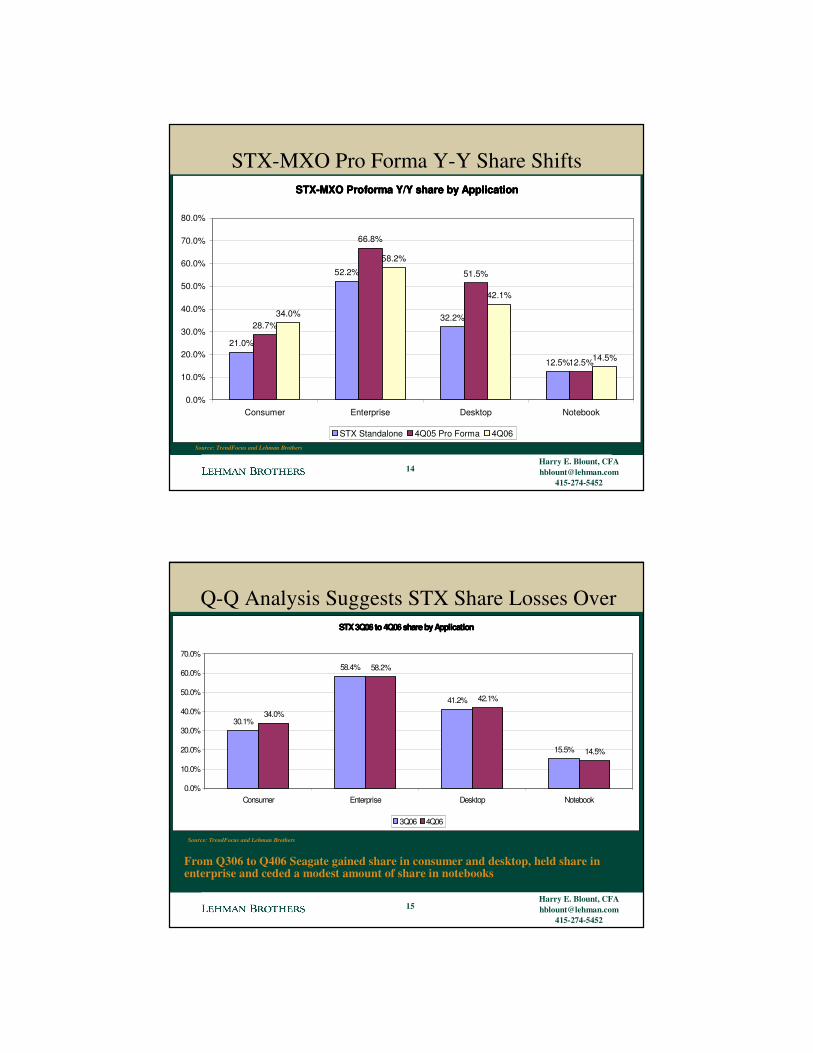

STX-MXO Pro Forma Y-Y Share Shifts

Source: TrendFocus and Lehman Brothers

STX-MXO Proforma Y/Y share by ApplicationSTX-MXO Proforma Y/Y share by ApplicationSTX-MXO Proforma Y/Y share by ApplicationSTX-MXO Proforma Y/Y share by Application

21.0%

52.2%

32.2%

12.5%

28.7%

66.8%

51.5%

12.5%

34.0%

58.2%

42.1%

14.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Consumer Enterprise Desktop Notebook

STX Standalone 4Q05 Pro Forma 4Q06

14

Harry E. Blount, [email protected]

415-274-5452

Q-Q Analysis Suggests STX Share Losses Over

Source: TrendFocus and Lehman Brothers

STX 3Q06 to 4Q06 share by ApplicationSTX 3Q06 to 4Q06 share by ApplicationSTX 3Q06 to 4Q06 share by ApplicationSTX 3Q06 to 4Q06 share by Application

30.1%

58.4%

41.2%

15.5%

34.0%

58.2%

42.1%

14.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Consumer Enterprise Desktop Notebook

3Q06 4Q06

From Q306 to Q406 Seagate gained share in consumer and desktop, held share in enterprise and ceded a modest amount of share in notebooks

15

Harry E. Blount, [email protected]

415-274-5452

Competitive Analysis

16

Harry E. Blount, [email protected]

415-274-5452

FujitsuFujitsu 4Q06 % of Shipments by Application (8.9 units)Fujitsu 4Q06 % of Shipments by Application (8.9 units)Fujitsu 4Q06 % of Shipments by Application (8.9 units)Fujitsu 4Q06 % of Shipments by Application (8.9 units)

Enterprise, 20.2%

Notebook, 78.0%

Consumer Electronics,

1.8%

Fujitsu 4Q06 % of Shipments by Form Factor (8.9 units)Fujitsu 4Q06 % of Shipments by Form Factor (8.9 units)Fujitsu 4Q06 % of Shipments by Form Factor (8.9 units)Fujitsu 4Q06 % of Shipments by Form Factor (8.9 units)

2.5", 83.8%

3.5", 16.2%

Source: TrendFocus, Lehman Brothers and Company Reports

Strength/Opportunity Vulnerability/Challenge

Early Move into 2.5” Enterprise SASHitachi uncertainty Alternative to Seagate in enterprise

Notebook exposure – share and marginsWestern Digital entrance into enterpriseLack of scale (30M units in 2006)

17

Harry E. Blount, [email protected]

415-274-5452

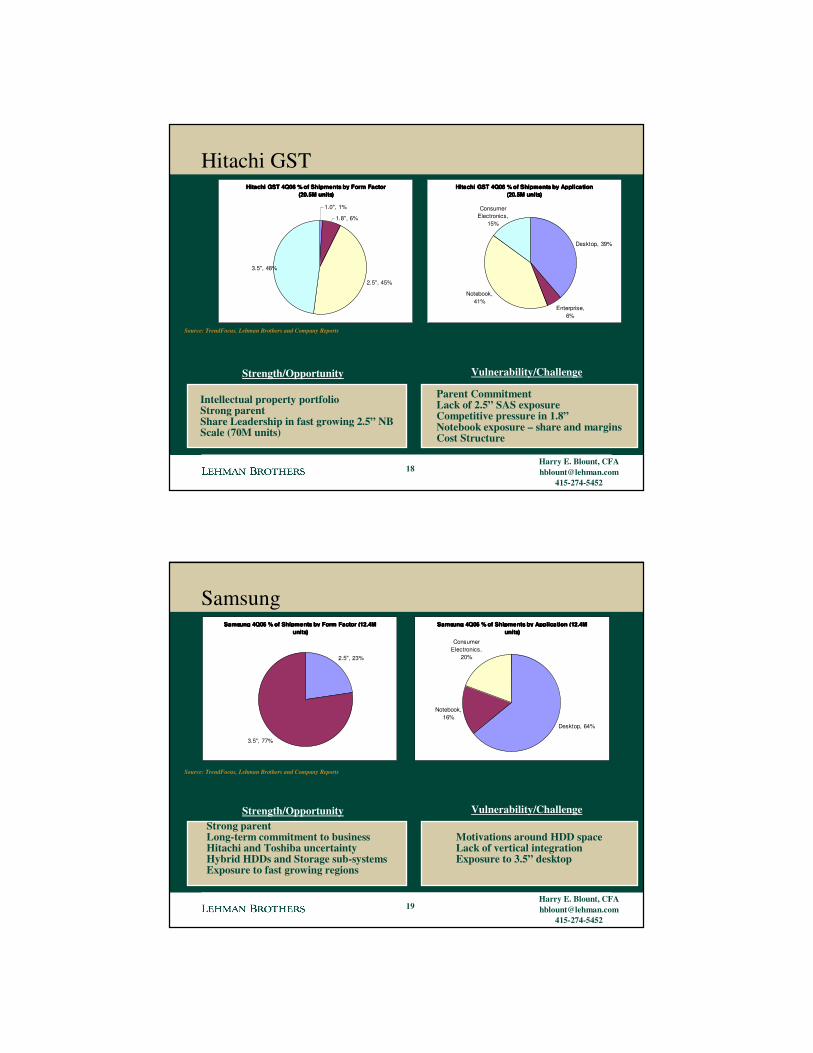

Hitachi GSTHitachi GST 4Q06 % of Shipments by Application Hitachi GST 4Q06 % of Shipments by Application Hitachi GST 4Q06 % of Shipments by Application Hitachi GST 4Q06 % of Shipments by Application

(20.5M units)(20.5M units)(20.5M units)(20.5M units)

Desktop, 39%

Enterprise, 6%

Notebook, 41%

Consumer Electronics,

15%

Hitachi GST 4Q06 % of Shipments by Form Factor Hitachi GST 4Q06 % of Shipments by Form Factor Hitachi GST 4Q06 % of Shipments by Form Factor Hitachi GST 4Q06 % of Shipments by Form Factor (20.5M units)(20.5M units)(20.5M units)(20.5M units)

1.0", 1%

1.8", 6%

2.5", 45%

3.5", 48%

Source: TrendFocus, Lehman Brothers and Company Reports

Strength/Opportunity Vulnerability/Challenge

Intellectual property portfolioStrong parentShare Leadership in fast growing 2.5” NBScale (70M units)

Parent CommitmentLack of 2.5” SAS exposureCompetitive pressure in 1.8”Notebook exposure – share and marginsCost Structure

18

Harry E. Blount, [email protected]

415-274-5452

SamsungSamsung 4Q06 % of Shipments by Application (12.4M Samsung 4Q06 % of Shipments by Application (12.4M Samsung 4Q06 % of Shipments by Application (12.4M Samsung 4Q06 % of Shipments by Application (12.4M

units)units)units)units)

Desktop, 64%

Notebook, 16%

Consumer Electronics,

20%

Samsung 4Q06 % of Shipments by Form Factor (12.4M Samsung 4Q06 % of Shipments by Form Factor (12.4M Samsung 4Q06 % of Shipments by Form Factor (12.4M Samsung 4Q06 % of Shipments by Form Factor (12.4M units)units)units)units)

2.5", 23%

3.5", 77%

Source: TrendFocus, Lehman Brothers and Company Reports

Strength/Opportunity Vulnerability/ChallengeStrong parentLong-term commitment to businessHitachi and Toshiba uncertaintyHybrid HDDs and Storage sub-systemsExposure to fast growing regions

Motivations around HDD spaceLack of vertical integrationExposure to 3.5” desktop

19

Harry E. Blount, [email protected]

415-274-5452

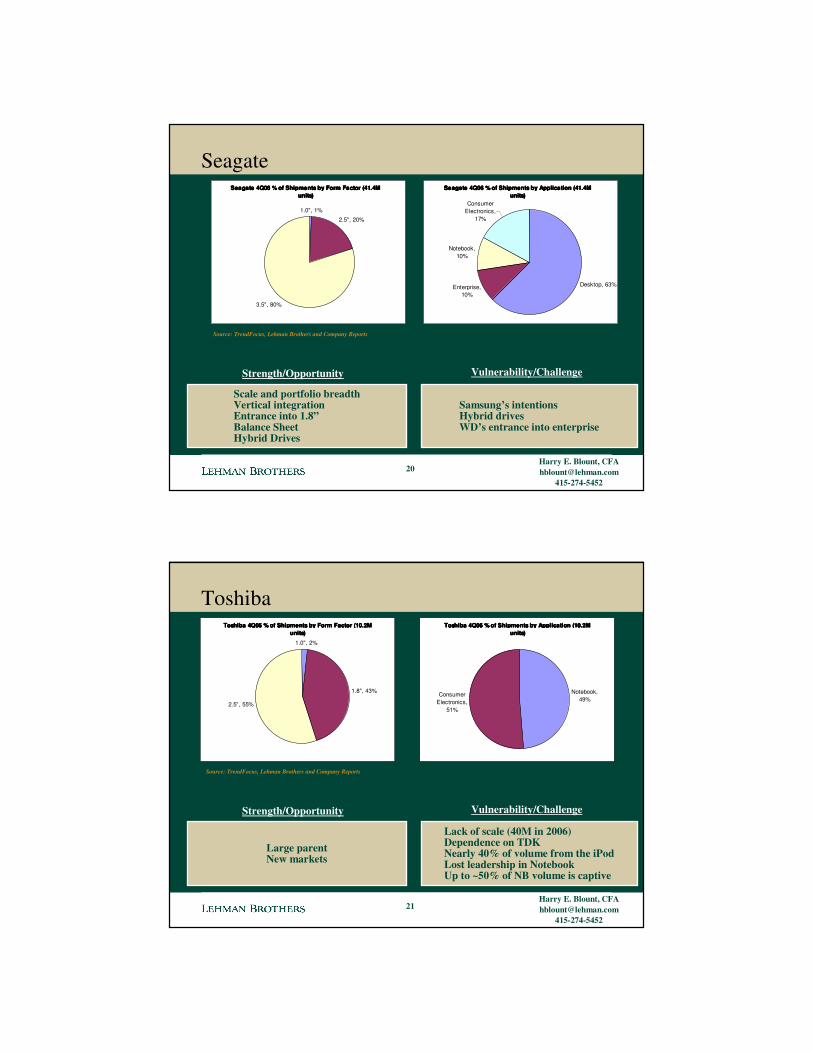

SeagateSeagate 4Q06 % of Shipments by Application (41.4M Seagate 4Q06 % of Shipments by Application (41.4M Seagate 4Q06 % of Shipments by Application (41.4M Seagate 4Q06 % of Shipments by Application (41.4M

units)units)units)units)

Desktop, 63%Enterprise, 10%

Notebook, 10%

Consumer Electronics,

17%

Seagate 4Q06 % of Shipments by Form Factor (41.4M Seagate 4Q06 % of Shipments by Form Factor (41.4M Seagate 4Q06 % of Shipments by Form Factor (41.4M Seagate 4Q06 % of Shipments by Form Factor (41.4M units)units)units)units)

1.0", 1%

2.5", 20%

3.5", 80%

Source: TrendFocus, Lehman Brothers and Company Reports

Strength/Opportunity Vulnerability/Challenge

Scale and portfolio breadthVertical integrationEntrance into 1.8”Balance SheetHybrid Drives

Samsung’s intentionsHybrid drivesWD’s entrance into enterprise

20

Harry E. Blount, [email protected]

415-274-5452

ToshibaToshiba 4Q06 % of Shipments by Application (10.2M Toshiba 4Q06 % of Shipments by Application (10.2M Toshiba 4Q06 % of Shipments by Application (10.2M Toshiba 4Q06 % of Shipments by Application (10.2M

units)units)units)units)

Notebook, 49%

Consumer Electronics,

51%

Toshiba 4Q06 % of Shipments by Form Factor (10.2M Toshiba 4Q06 % of Shipments by Form Factor (10.2M Toshiba 4Q06 % of Shipments by Form Factor (10.2M Toshiba 4Q06 % of Shipments by Form Factor (10.2M units)units)units)units)

1.0", 2%

1.8", 43%

2.5", 55%

Source: TrendFocus, Lehman Brothers and Company Reports

Strength/Opportunity Vulnerability/Challenge

Large parentNew markets

Lack of scale (40M in 2006)Dependence on TDKNearly 40% of volume from the iPodLost leadership in NotebookUp to ~50% of NB volume is captive

21

Harry E. Blount, [email protected]

415-274-5452

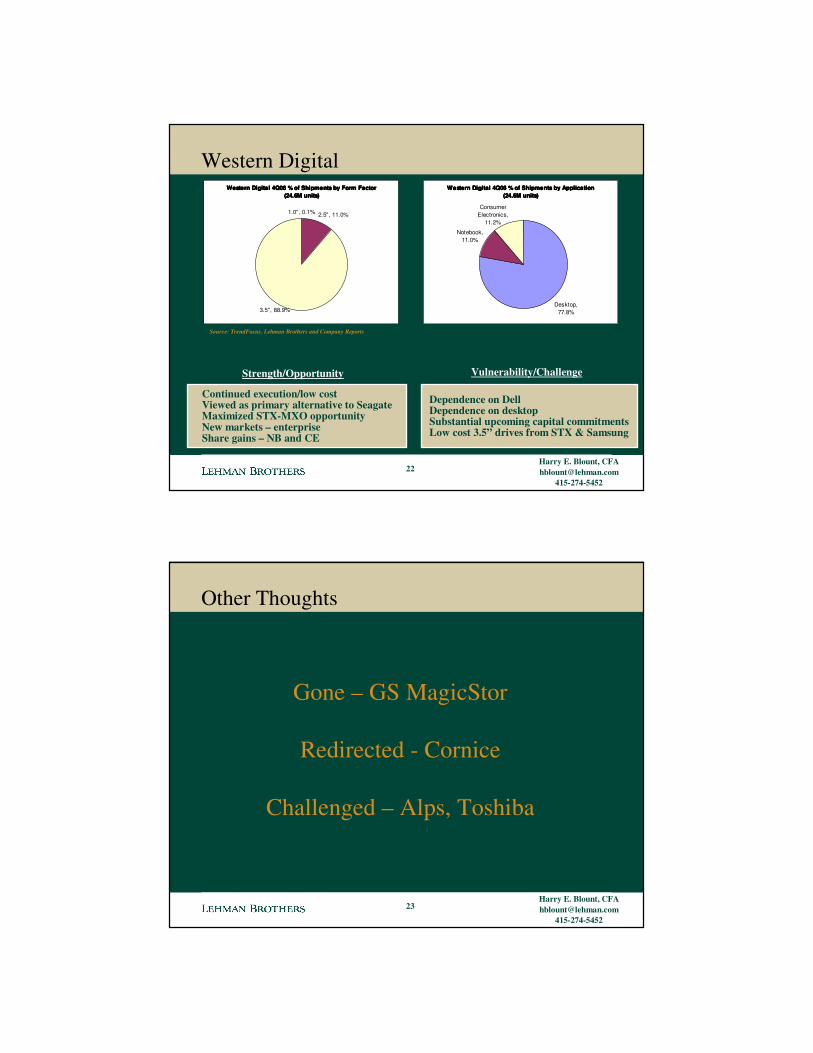

Western DigitalWestern Digital 4Q06 % of Shipments by Application Western Digital 4Q06 % of Shipments by Application Western Digital 4Q06 % of Shipments by Application Western Digital 4Q06 % of Shipments by Application

(24.6M units)(24.6M units)(24.6M units)(24.6M units)

Desktop, 77.8%

Notebook, 11.0%

Consumer Electronics,

11.2%

Western Digital 4Q06 % of Shipments by Form Factor Western Digital 4Q06 % of Shipments by Form Factor Western Digital 4Q06 % of Shipments by Form Factor Western Digital 4Q06 % of Shipments by Form Factor (24.6M units)(24.6M units)(24.6M units)(24.6M units)

1.0", 0.1% 2.5", 11.0%

3.5", 88.9%

Source: TrendFocus, Lehman Brothers and Company Reports

Strength/Opportunity Vulnerability/Challenge

Continued execution/low costViewed as primary alternative to SeagateMaximized STX-MXO opportunityNew markets – enterpriseShare gains – NB and CE

Dependence on DellDependence on desktopSubstantial upcoming capital commitmentsLow cost 3.5” drives from STX & Samsung

22

Harry E. Blount, [email protected]

415-274-5452

Gone – GS MagicStor

Redirected - Cornice

Challenged – Alps, Toshiba

Other Thoughts

23

Harry E. Blount, [email protected]

415-274-5452

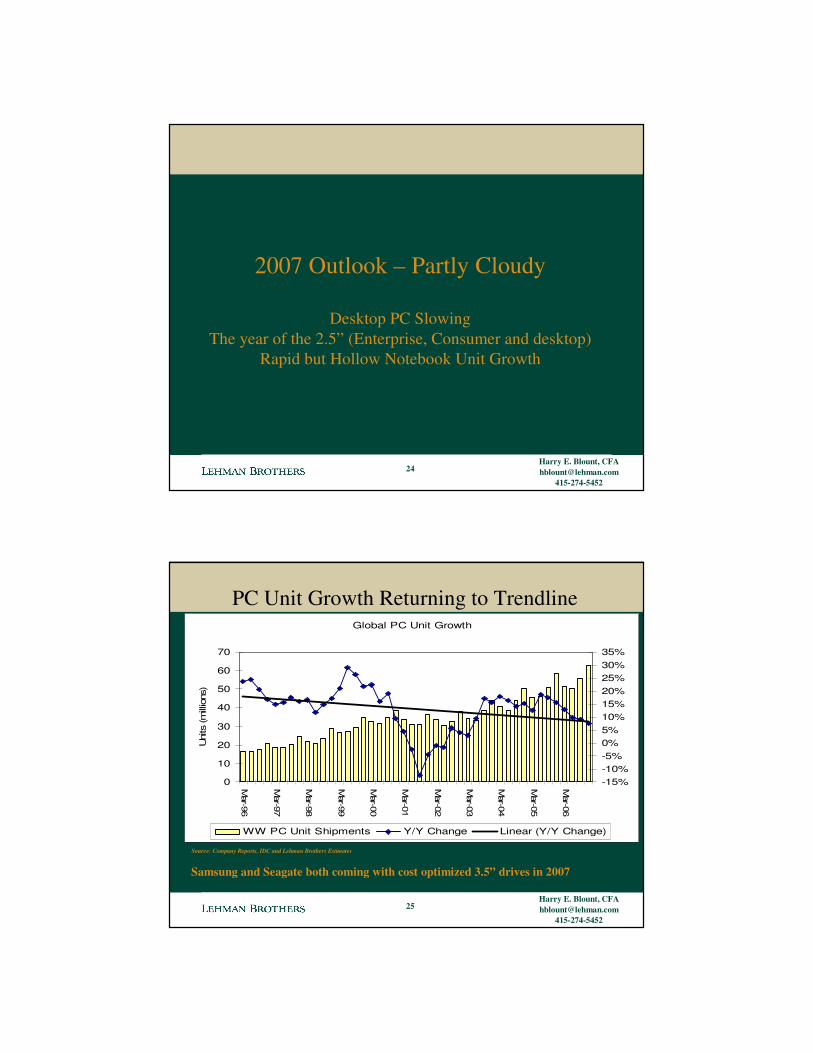

2007 Outlook – Partly Cloudy

Desktop PC SlowingThe year of the 2.5” (Enterprise, Consumer and desktop)

Rapid but Hollow Notebook Unit Growth

24

Harry E. Blount, [email protected]

415-274-5452

PC Unit Growth Returning to Trendline

Source: Company Reports, IDC and Lehman Brothers Estimates

Global PC Unit Growth

0

10

20

30

40

50

60

70

Mar-96

Mar-97

Mar-98

Mar-99

Mar-00

Mar-01

Mar-02

Mar-03

Mar-04

Mar-05

Mar-06

Uni

ts (m

illio

ns)

-15%-10%-5%0%5%10%15%20%25%30%35%

WW PC Unit Shipments Y/Y Change Linear (Y/Y Change)

25

Samsung and Seagate both coming with cost optimized 3.5” drives in 2007

Harry E. Blount, [email protected]

415-274-5452

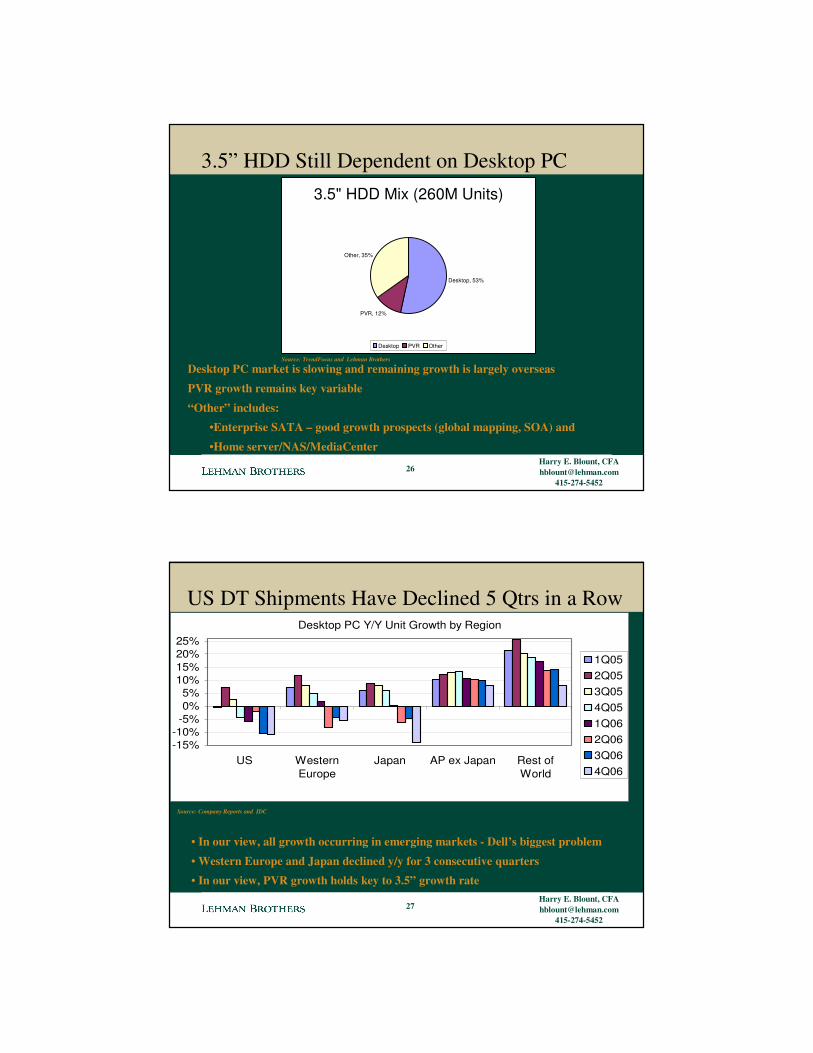

3.5” HDD Still Dependent on Desktop PC

Source: TrendFocus and Lehman Brothers

Desktop PC market is slowing and remaining growth is largely overseas

PVR growth remains key variable

“Other” includes: •Enterprise SATA – good growth prospects (global mapping, SOA) and

•Home server/NAS/MediaCenter

3.5" HDD Mix (260M Units)

Desktop, 53%

PVR, 12%

Other, 35%

Desktop PVR Other

26

Harry E. Blount, [email protected]

415-274-5452

US DT Shipments Have Declined 5 Qtrs in a Row

Source: Company Reports and IDC

Desktop PC Y/Y Unit Growth by Region

-15%-10%-5%0%5%

10%15%20%25%

US WesternEurope

Japan AP ex Japan Rest ofWorld

1Q052Q053Q054Q051Q062Q063Q064Q06

• In our view, all growth occurring in emerging markets - Dell’s biggest problem

• Western Europe and Japan declined y/y for 3 consecutive quarters• In our view, PVR growth holds key to 3.5” growth rate

27

Harry E. Blount, [email protected]

415-274-5452

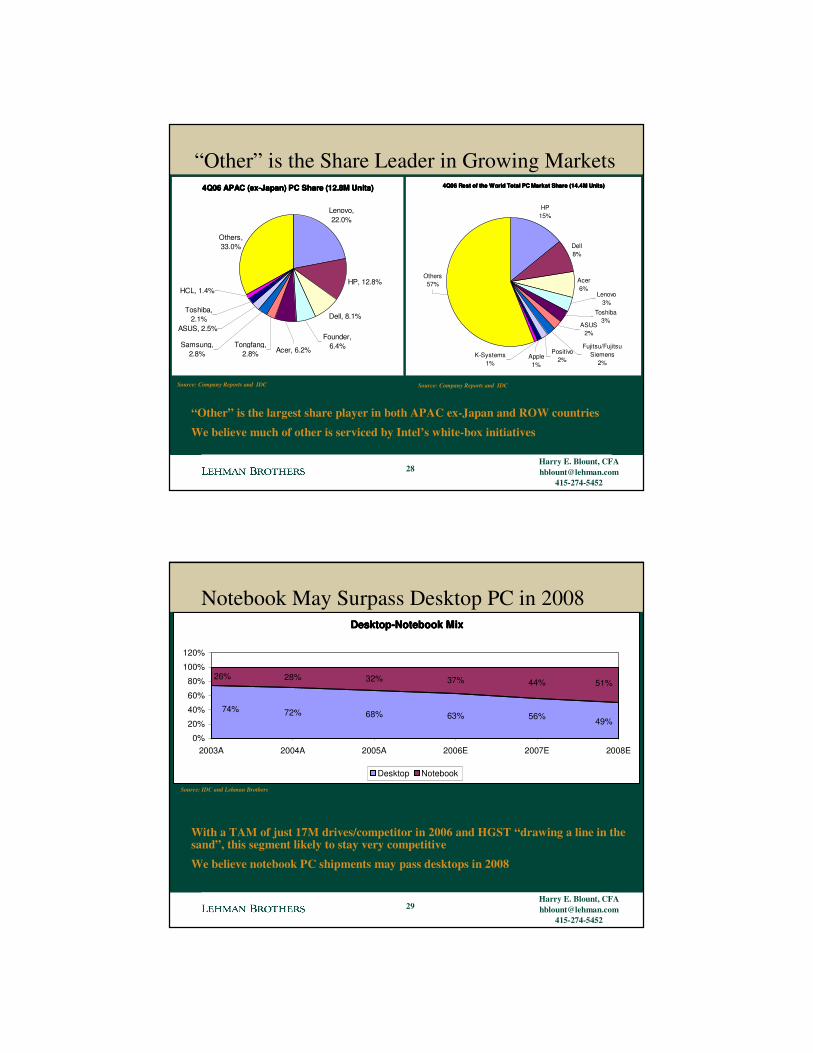

“Other” is the Share Leader in Growing Markets

Source: Company Reports and IDC

4Q06 APAC (ex-Japan) PC Share (12.8M Units)4Q06 APAC (ex-Japan) PC Share (12.8M Units)4Q06 APAC (ex-Japan) PC Share (12.8M Units)4Q06 APAC (ex-Japan) PC Share (12.8M Units)

Lenovo, 22.0%

HP, 12.8%

Dell, 8.1%

Founder, 6.4%

Others, 33.0%

HCL, 1.4%

Toshiba, 2.1%

ASUS, 2.5%

Acer, 6.2%Tongfang,

2.8%Samsung,

2.8%

4Q06 Rest of the World Total PC Market Share (14.4M Units)4Q06 Rest of the World Total PC Market Share (14.4M Units)4Q06 Rest of the World Total PC Market Share (14.4M Units)4Q06 Rest of the World Total PC Market Share (14.4M Units)

HP15%

Dell8%

Acer6%

Others57%

Positivo2%Apple

1%K-Systems

1%

Fujitsu/Fujitsu Siemens

2%

ASUS2%

Toshiba3%

Lenovo3%

Source: Company Reports and IDC

“Other” is the largest share player in both APAC ex-Japan and ROW countries

We believe much of other is serviced by Intel’s white-box initiatives

28

Harry E. Blount, [email protected]

415-274-5452

Notebook May Surpass Desktop PC in 2008

Source: IDC and Lehman Brothers

With a TAM of just 17M drives/competitor in 2006 and HGST “drawing a line in the sand”, this segment likely to stay very competitive

We believe notebook PC shipments may pass desktops in 2008

Desktop-Notebook MixDesktop-Notebook MixDesktop-Notebook MixDesktop-Notebook Mix

72% 68% 63%

28% 32% 37% 44%

74%56% 49%

26%51%

0%

20%

40%

60%

80%

100%

120%

2003A 2004A 2005A 2006E 2007E 2008E

Desktop Notebook

29

Harry E. Blount, [email protected]

415-274-5452

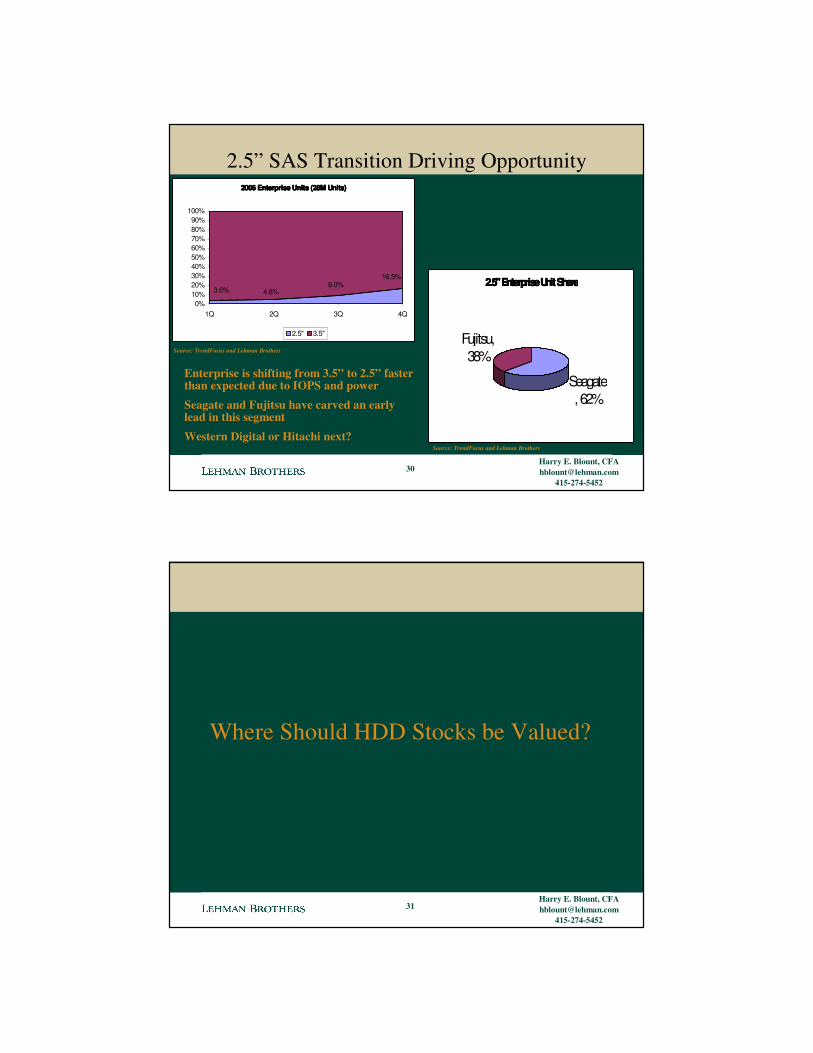

2.5” SAS Transition Driving Opportunity

Source: TrendFocus and Lehman Brothers

Enterprise is shifting from 3.5” to 2.5” faster than expected due to IOPS and powerSeagate and Fujitsu have carved an early lead in this segmentWestern Digital or Hitachi next?

2006 Enterprise Units (28M Units)2006 Enterprise Units (28M Units)2006 Enterprise Units (28M Units)2006 Enterprise Units (28M Units)

16.5%9.0%

4.8%3.6%

0%10%20%30%40%50%60%70%80%90%

100%

1Q 2Q 3Q 4Q

2.5" 3.5"

2.5" Enterprise Unit Share2.5" Enterprise Unit Share2.5" Enterprise Unit Share2.5" Enterprise Unit Share

Seagate, 62%

Fujitsu, 38%

Source: TrendFocus and Lehman Brothers

30

Harry E. Blount, [email protected]

415-274-5452

Where Should HDD Stocks be Valued?

31

Harry E. Blount, [email protected]

415-274-5452

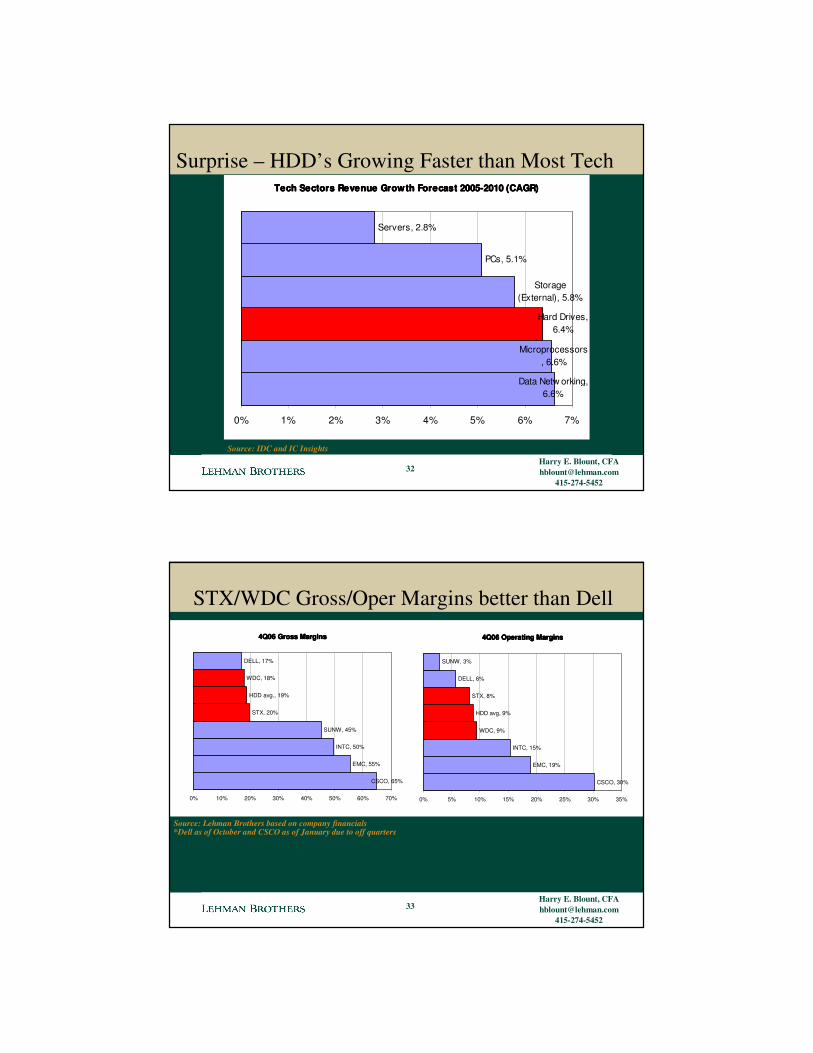

Surprise – HDD’s Growing Faster than Most Tech

Source: IDC and IC Insights

Tech Sectors Revenue Growth Forecast 2005-2010 (CAGR)Tech Sectors Revenue Growth Forecast 2005-2010 (CAGR)Tech Sectors Revenue Growth Forecast 2005-2010 (CAGR)Tech Sectors Revenue Growth Forecast 2005-2010 (CAGR)

Data Netw orking, 6.6%

Microprocessors, 6.6%

Hard Drives, 6.4%

Storage (External), 5.8%

PCs, 5.1%

Servers, 2.8%

0% 1% 2% 3% 4% 5% 6% 7%

32

Harry E. Blount, [email protected]

415-274-5452

STX/WDC Gross/Oper Margins better than Dell

Source: Lehman Brothers based on company financials*Dell as of October and CSCO as of January due to off quarters

4Q06 Gross Margins4Q06 Gross Margins4Q06 Gross Margins4Q06 Gross Margins

CSCO, 65%

EMC, 55%

INTC, 50%

SUNW, 45%

STX, 20%

HDD avg., 19%

WDC, 18%

DELL, 17%

0% 10% 20% 30% 40% 50% 60% 70%

4Q06 Operating Margins4Q06 Operating Margins4Q06 Operating Margins4Q06 Operating Margins

CSCO, 30%

EMC, 19%

INTC, 15%

WDC, 9%

HDD avg, 9%

STX, 8%

DELL, 6%

SUNW, 3%

0% 5% 10% 15% 20% 25% 30% 35%

33

Harry E. Blount, [email protected]

415-274-5452

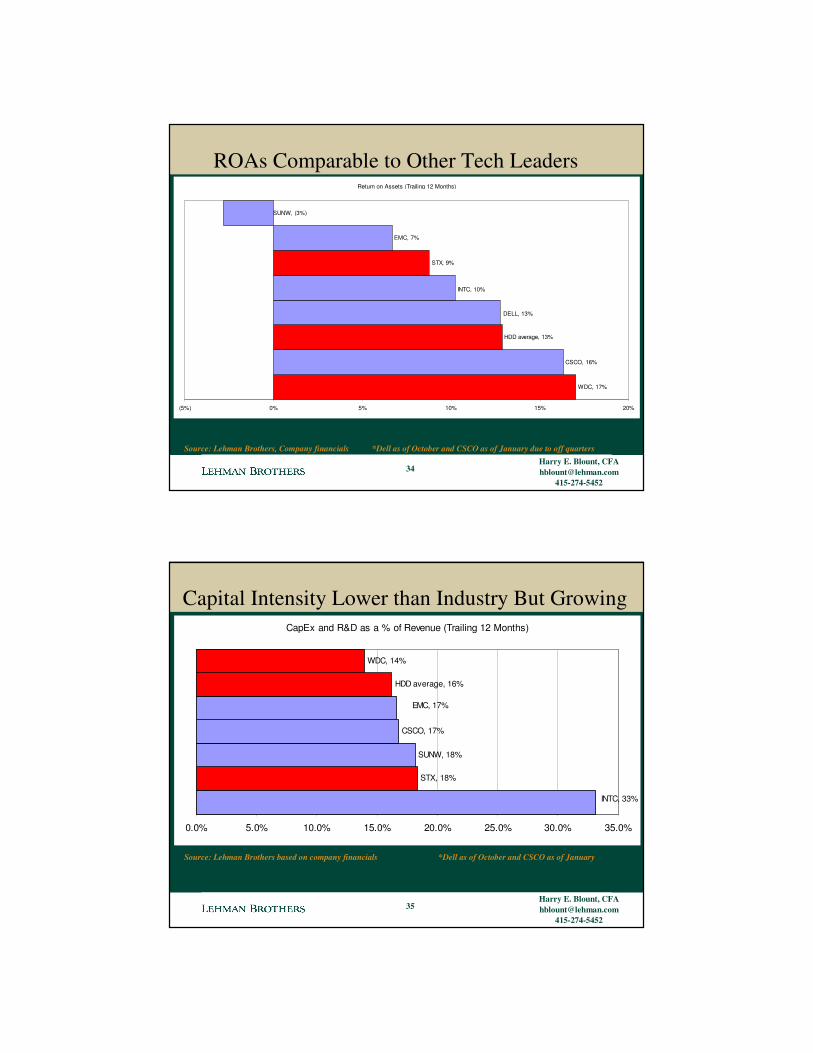

ROAs Comparable to Other Tech Leaders

Source: Lehman Brothers, Company financials *Dell as of October and CSCO as of January due to off quarters

Return on Assets (Trailing 12 Months)

CSCO, 16%

HDD average, 13%

EMC, 7%

WDC, 17%

SUNW, (3%)

DELL, 13%

INTC, 10%

STX, 9%

(5%) 0% 5% 10% 15% 20%

34

Harry E. Blount, [email protected]

415-274-5452

Capital Intensity Lower than Industry But Growing

Source: Lehman Brothers based on company financials *Dell as of October and CSCO as of January

CapEx and R&D as a % of Revenue (Trailing 12 Months)

STX, 18%

SUNW, 18%

CSCO, 17%

WDC, 14%

INTC, 33%

HDD average, 16%

EMC, 17%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0%

35

Harry E. Blount, [email protected]

415-274-5452

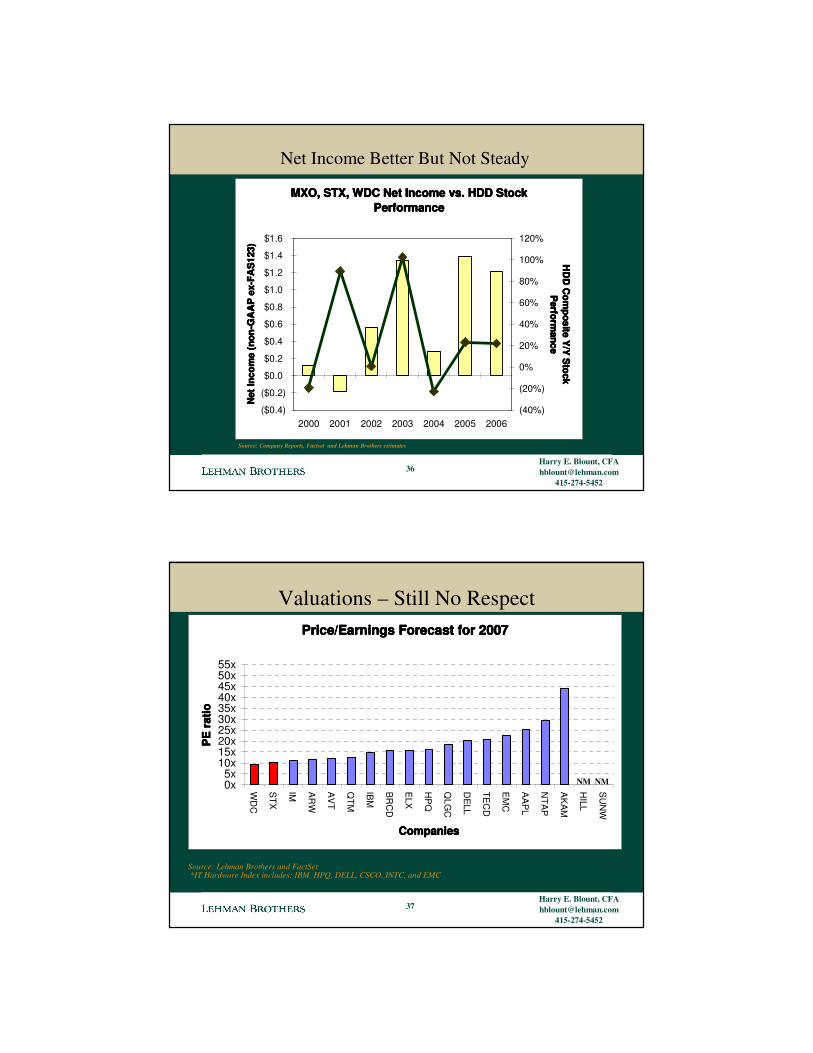

Net Income Better But Not Steady

MXO, STX, WDC Net Income vs. HDD Stock MXO, STX, WDC Net Income vs. HDD Stock MXO, STX, WDC Net Income vs. HDD Stock MXO, STX, WDC Net Income vs. HDD Stock Performance Performance Performance Performance

($0.4)

($0.2)

$0.0

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

$1.6

2000 2001 2002 2003 2004 2005 2006

Net

Inco

me

(non

-GA

AP

ex-

FAS

123)

Net

Inco

me

(non

-GA

AP

ex-

FAS

123)

Net

Inco

me

(non

-GA

AP

ex-

FAS

123)

Net

Inco

me

(non

-GA

AP

ex-

FAS

123)

(40%)

(20%)

0%

20%

40%

60%

80%

100%

120%H

DD

Com

posite Y/Y

Stock

HD

D C

omposite Y

/Y S

tock H

DD

Com

posite Y/Y

Stock

HD

D C

omposite Y

/Y S

tock P

erformance

Perform

anceP

erformance

Perform

ance

Source: Company Reports, Factset and Lehman Brothers estimates

36

Harry E. Blount, [email protected]

415-274-5452

Valuations – Still No Respect

Source: Lehman Brothers, IDC, and First Call

Source: Lehman Brothers and FactSet*IT Hardware Index includes: IBM, HPQ, DELL, CSCO, INTC, and EMC

Price/Earnings Forecast for 2007Price/Earnings Forecast for 2007Price/Earnings Forecast for 2007Price/Earnings Forecast for 2007

0x5x

10x15x20x25x30x35x40x45x50x55x

WD

C

STX

IM AR

W

AV

T

QTM

IBM

BR

CD

ELX

HP

Q

QLG

C

DE

LL

TEC

D

EM

C

AA

PL

NTA

P

AK

AM

HILL

SU

NW

CompaniesCompaniesCompaniesCompanies

PE

rat

ioP

E r

atio

PE

rat

ioP

E r

atio

37

NM NM

Harry E. Blount, [email protected]

415-274-5452

THANK YOU! – QUESTIONS

Please let me know if you would like to be added to my distribution list for the

following publications:

Weekly - In Blount TermsMonthly - IT Hardware Monthly

38

Harry E. Blount, [email protected]

415-274-5452

Analyst Certification and Important Disclosures

Analyst Certification:I, Harry Blount, hereby certify (1) that the views expressed in this research email accurately reflect my personal views about any or all of the subject securities or issuers referred to in this email and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this email.

Important DisclosuresLehman Brothers does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this email communication.

Customers of Lehman Brothers in the United States can receive independent, third-party research on the company or companies covered in this report, at no cost to them, where such research is available. Customers can access this independent research at www.lehmanlive.com or can call 1-800-2-LEHMAN to request a copy of this research.

Investors should consider this communication as only a single factor in making their investment decision.

The analysts responsible for preparing this report have received compensation based upon various factors including the Firm’s total revenues, a portion of which is generated by investment banking activities.

Stock price and ratings history charts along with other important disclosures are available on our disclosure website at www.lehman.com/disclosures And may also be obtained by sending a written request to: LEHMAN BROTHERS CONTROL ROOM, 745 SEVENTH AVENUE, 19TH FLOOR NEW YORK, NY 10019

39

Harry E. Blount, [email protected]

415-274-5452

Important Disclosures (continued)Mentioned Stocks

2-EW / PositiveUSD$27.90 MSFTMICROSOFT

3-UW / Neutral1373 (JP)6770.TALPS2-EW / PositiveUSD$19.30 INTCINTEL CORP

3-UW / Neutral9660 (JP)6762.TTDK1-OW / NeutralUSD$19.08 IMINGRAM MICRO

2-EW / Positive820 (JP)6501.THITACHI2-EW / NeutralUSD$91.57 IBMINTL BUS MACHINE

3-UW / Positive727 (JP)6502.TTOSHIBA1-OW / NeutralUSD$38.73 HPQHEWLETT-PACKARD

2-EW / Neutral566,000 (KR)5930.KSSAMSUNG2-EW / NeutralUSD$3.54 HILLDOT HILL SYSTEMS

2-EW / Positive804 (JP)6702.TFUJITSU2-EW / NeutralUSD$13.51 EMCEMC CORP

2-EW / NeutralUSD$18.51 WDCWESTERN DIGITAL 2-EW / NeutralUSD$17.46 ELXEMULEX CORP

3-UW / NeutralUSD$36.76 TECDTECH DATA CP 2-EW / NeutralUSD$23.15 DELLDELL INC

2-EW / NeutralUSD$6.07 SUNWSUN MICROSYSTEMS 1-OW / PositiveUSD$25.32 CSCOCISCO SYSTEMS

1-OW / NeutralUSD$25.08 STXSEAGATE1-OW / NeutralUSD$9.04 BRCDBROCADE COMM SYS

1-OW / NeutralUSD$34.77 AVTAVNET INC

2-EW / NeutralUSD$2.40 QTMQUANTUM DLT 2-EW / NeutralUSD$37.52 ARWARROW ELECTRONIC

2-EW / NeutralUSD$17.32 QLGCQLOGIC CORP 2-EW / PositiveUSD$14.37 AMDADVANCED MICRO DEVICES

1-OW / PositiveUSD$16.63 ORCLORACLE CORP 2-EW / NeutralUSD$48.22 AKAMAKAMAI TECH INC

1-OW / NeutralUSD$37.75 NTAPNETWORK APPLIANCE 1-OW / NeutralUSD$85.91 AAPLAPPLE INC

RatingRecent PriceTickerName RatingRecent PriceTickerName

40

Harry E. Blount, [email protected]

415-274-5452

Important Disclosures (continued)Other Material Conflicts:

Lehman Brothers International (Europe), Seoul branch is a liquidity provider of equity linked notes for Samsung.

Guide to Lehman Brothers Equity Research Rating System

Our coverage analysts use a relative rating system in which they rate stocks as 1-Overweight, 2- Equal weight or 3-Underweight (see definitions below) relative to other companies covered by the analyst or a team of analysts that are deemed to be in the same industry sector (“the sector coverage universe”). To see a list of companies that comprise a particular sector coverage universe, please go to www.lehman.com/disclosures.

In addition to the stock rating, we provide sector views which rate the outlook for the sector coverage universe as 1-Positive, 2-Neutral or 3-Negative (see definitions below). A rating system using terms such as buy, hold and sell is not the equivalent of our rating system. Investors should carefully read the entire research report including the definitions of all ratings and not infer its contents from ratings alone.

41

Harry E. Blount, [email protected]

415-274-5452

Important Disclosures (continued)Stock Rating

1-Overweight - The stock is expected to outperform the unweighted expected total return of the sector coverage universe over a 12-month investment horizon.

2-Equal weight - The stock is expected to perform in line with the unweighted expected total return of the sector coverage universe over a 12-month investment horizon.

3-Underweight - The stock is expected to underperform the unweighted expected total return of the sector coverage universe over a 12-month investment horizon.

RS-Rating Suspended - The rating and target price have been suspended temporarily to comply with applicable regulations and/or firm policies in certain circumstances including when Lehman Brothers is acting in an advisory capacity on a merger or strategic transaction involving the company.

Sector View

1-Positive - sector coverage universe fundamentals are improving.

2-Neutral - sector coverage universe fundamentals are steady, neither improving nor deteriorating.

3-Negative - sector coverage universe fundamentals are deteriorating.

Distribution of Ratings:

Lehman Brothers Equity Research has 1994 companies under coverage.

41% have been assigned a 1-Overweight rating which, for purposes of mandatory disclosures, is classified as a Buy rating, 39% of companies with this rating are investment banking clients of the Firm.

41% have been assigned a 2-Equal weight rating which, for purposes of mandatory disclosures, is classified as a Hold rating, 28% of companies with this rating are investment banking clients of the Firm.

13% have been assigned a 3-Underweight rating which, for purposes of mandatory disclosures, is classified as a Sell rating, 22% of companies with this rating are investment banking clients of the Firm.

42

Harry E. Blount, [email protected]

415-274-5452

Important Disclosures (continued)This material has been prepared and/or issued by Lehman Brothers Inc., member SIPC, and/or one of its affiliates (“Lehman Brothers”) and has been approved by Lehman Brothers International (Europe), authorized and regulated by the Financial Services Authority, in connection with its distribution in the European Economic Area. This material is distributed in Japan by Lehman Brothers Japan Inc., and in Hong Kong by Lehman Brothers Asia Limited. This material is distributed in Australia by Lehman Brothers Australia Pty Limited, and in Singapore by Lehman Brothers Inc., Singapore Branch. (“LBIS”). Where this material is distributed by LBIS, please note that it is intended for general circulation only and the recommendations contained herein does not take into account the specific investment objectives, financial situation or particular needs of any particular person. An investor should consult his Lehman Brothers’ representative regarding the suitability of the product and take into account his specific investment objectives, financial situation or particular needs before he makes a commitment to purchase the investment product. This material is distributed in Korea by Lehman Brothers International (Europe) Seoul Branch. This document is for information purposes only and it should not be regarded as an offer to sell or as a solicitation of an offer to buy the securities or other instruments mentioned in it. No part of this document may be reproduced in any manner without the written permission of Lehman Brothers. With the exception of disclosures relating to Lehman Brothers, this research report is based on current public information that Lehman Brothers considers reliable, but we make no representation that it is accurate or complete, and it should not be relied on as such. In the case of any disclosure to the effect that Lehman Brothers Inc. or its affiliates beneficially own 1% or more of any class of common equity securities of the subject company, the computation of beneficial ownership of securities is based upon the methodology used to compute ownership under Section 13(d) of the United States' Securities Exchange Act of 1934. In the case of any disclosure to the effect that Lehman Brothers Inc. and/or its affiliates hold a short position of at least 1% of the outstanding share capital of a particular company, such disclosure relates solely to the ordinary share capital of the company. Accordingly, while such calculation represents Lehman Brothers’ holdings net of any long position in the ordinary share capital of the company, such calculation excludes any rights or obligations that Lehman Brothers may otherwise have, or which may accrue in the future, with respect to such ordinary share capital. Similarly such calculation does not include any shares held or owned by Lehman Brothers where such shares are held under a wider agreement or arrangement (be it with a client or a counterparty) concerning the shares of such company (e.g. prime broking and/or stock lending activity). Any such disclosure represents the position of Lehman Brothers as of the last business day of the calendar month preceding the date of this report. This material is provided with the understanding that Lehman Brothers is not acting in a fiduciary capacity. Opinions expressed herein reflect the opinion of Lehman Brothers and are subject to change without notice. The products mentioned in this document may not be eligible for sale in some states or countries, and they may not be suitable for all types of investors. If an investor has any doubts about product suitability, he should consult his Lehman Brothers representative. The value of and the income produced by products may fluctuate, so that an investor may get back less than he invested. Value and income may be adversely affected by exchange rates, interest rates, or other factors. Past performance is not necessarily indicative of future results. If a product is income producing, part of the capital invested may be used to pay that income. © 2007 Lehman Brothers. All rights reserved. Additional information is available on request. Please contact a Lehman Brothers entity in your home jurisdiction. Lehman Brothers policy for managing conflicts of interest in connection with investment research is available at www.lehman.com/researchconflictspolicy. Ratings, earnings per share forecasts and price targets contained in the Firm's equity research reports covering U.S. companies are available at www.lehman.com/disclosures.Complete disclosure information on companies covered by Lehman Brothers Equity Research is available at www.lehman.com/disclosures.

43

Harry E. Blount, [email protected]

415-274-5452

Public Appearance DisclosuresLehman Brothers Inc. and/or an affiliate has received compensation for investment banking services from the following companies within the past 12 months, and the following companies are or during the past 12 months have been investment banking clients of Lehman Brothers Inc. and/or an affiliate:

• Apple Inc • Brocade Systems

• EMC Corp • Dot Hill Systems

• Hewlett-Packard • IBM

• Intel Corp • Microsoft

• Seagate

Lehman Brothers Inc has received non-investment banking related compensation from the following companies within the last 12 months and the following companies are or during the last 12 months have been non-investment banking clients (securities related services) of Lehman Brothers Inc:

• Apple Inc. • Advanced Micro Devices

• Brocade Systems • Cisco Systems

• Dell Inc. • EMC Corp

• Dot Hill Systems • Hewlett Packard

• IBM • Ingram Micro

• Intel Corp • Microsoft

• Network Appliance • Oracle

• Quantum • Seagate

• Sun Microsystems • Western Digital

Lehman Brothers Inc. and/or its affiliate beneficially owns 1% or more of any class of common equity securities of the following companies as of the end of the last month:

• Akamai Tech • Advanced Micro

• Brocade Systems • Network Appliance

• QLogic • Tech Data

44