Embed Size (px)

Citation preview

The GlobalOil & Gas Market:

DYNAMICS OF STRUCTURING

THE INTEGRATEDMEDIA MIX

An Independent Research Study Conducted by Martin Akel & Associates; Sponsored by PennWell Corporation

DETERMINE ...

A. Respondents’ status as decision makers in the oil and gas industry.

RESEARCH OBJECTIVES

2

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

DETERMINE ...

A. Respondents’ status as decision makers in the oil and gas industry.

B. Challenges faced by decision makers and their use of technology to address challenges.

RESEARCH OBJECTIVES

3

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

DETERMINE ...

A. Respondents’ status as decision makers in the oil and gas industry.

B. Challenges faced by decision makers and their use of technology to address challenges.

C. Trends in the environment for branding new oil and gas technology.

RESEARCH OBJECTIVES

4

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

DETERMINE ...

A. Respondents’ status as decision makers in the oil and gas industry.

B. Challenges faced by decision makers and their use of technology to address challenges.

C. Trends in the environment for branding new oil and gas technology.

D. The dynamics of team decision making for new oil and gas technology.

RESEARCH OBJECTIVES

5

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

DETERMINE ...

A. Respondents’ status as decision makers in the oil and gas industry.

B. Challenges faced by decision makers and their use of technology to address challenges.

C. Trends in the environment for branding new oil and gas technology.

D. The dynamics of team decision making for new oil and gas technology.

E. How decision makers are branded about suppliers, products & systems.

RESEARCH OBJECTIVES

6

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

DETERMINE ...

A. Respondents’ status as decision makers in the oil and gas industry.

B. Challenges faced by decision makers and their use of technology to address challenges.

C. Trends in the environment for branding new oil and gas technology.

D. The dynamics of team decision making for new oil and gas technology.

E. How decision makers are branded about suppliers, products & systems.

F. Decision makers’ engagement with today’s array of media.

RESEARCH OBJECTIVES

7

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

DETERMINE ...

A. Respondents’ status as decision makers in the oil and gas industry.

B. Challenges faced by decision makers and their use of technology to address challenges.

C. Trends in the environment for branding new oil and gas technology.

D. The dynamics of team decision making for new oil and gas technology.

E. How decision makers are branded about suppliers, products & systems.

F. Decision makers’ engagement with today’s array of media.

G. The degree to which decision makers are engaged with professional publications.

RESEARCH OBJECTIVES

8

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

DETERMINE ...

A. Respondents’ status as decision makers in the oil and gas industry.

B. Challenges faced by decision makers and their use of technology to address challenges.

C. Trends in the environment for branding new oil and gas technology.

D. The dynamics of team decision making for new oil and gas technology.

E. How decision makers are branded about suppliers, products & systems.

F. Decision makers’ engagement with today’s array of media.

G. The degree to which decision makers are engaged with professional publications.

H. Trends in engagement with event and digital media.

RESEARCH OBJECTIVES

9

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

DETERMINE ...

A. Respondents’ status as decision makers in the oil and gas industry.

B. Challenges faced by decision makers and their use of technology to address challenges.

C. Trends in the environment for branding new oil and gas technology.

D. The dynamics of team decision making for new oil and gas technology.

E. How decision makers are branded about suppliers, products & systems.

F. Decision makers’ engagement with today’s array of media.

G. The degree to which decision makers are engaged with professional publications.

H. Trends in engagement with event and digital media.

I. The complementary roles of different media in the product adoption process.

RESEARCH OBJECTIVES

10

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

11

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

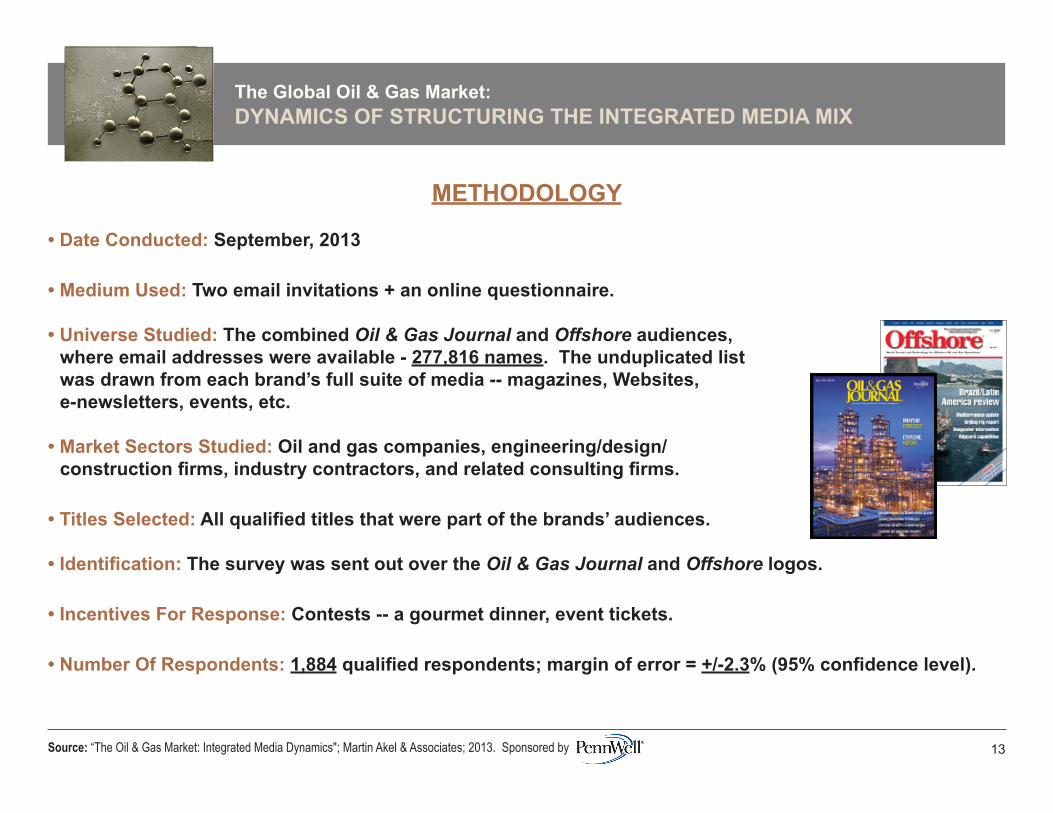

Methodology

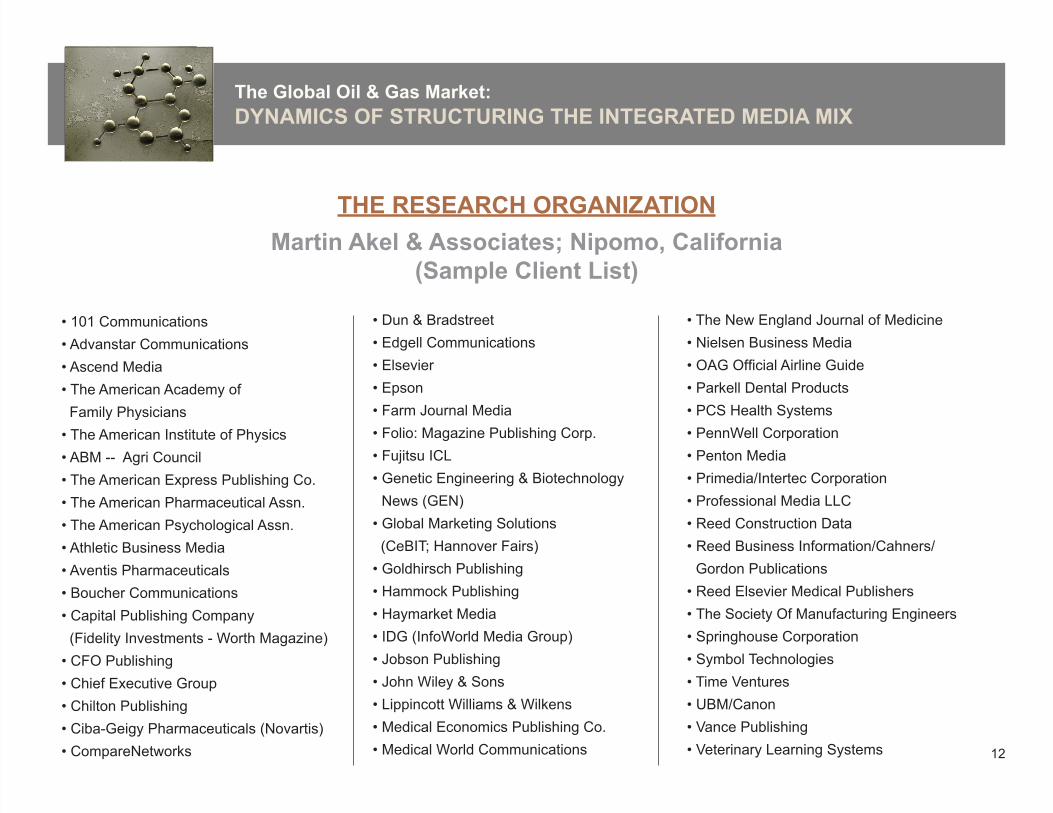

THE RESEARCH ORGANIZATIONMartin Akel & Associates; Nipomo, California

(Sample Client List)

12

• 101 Communications• Advanstar Communications• Ascend Media• The American Academy of Family Physicians• The American Institute of Physics• ABM -- Agri Council • The American Express Publishing Co.• The American Pharmaceutical Assn.• The American Psychological Assn.• Athletic Business Media• Aventis Pharmaceuticals• Boucher Communications• Capital Publishing Company (Fidelity Investments - Worth Magazine)• CFO Publishing• Chief Executive Group• Chilton Publishing• Ciba-Geigy Pharmaceuticals (Novartis)• CompareNetworks

• Dun & Bradstreet• Edgell Communications• Elsevier • Epson• Farm Journal Media• Folio: Magazine Publishing Corp.• Fujitsu ICL• Genetic Engineering & Biotechnology

News (GEN)• Global Marketing Solutions (CeBIT; Hannover Fairs)• Goldhirsch Publishing• Hammock Publishing• Haymarket Media• IDG (InfoWorld Media Group)• Jobson Publishing• John Wiley & Sons• Lippincott Williams & Wilkens• Medical Economics Publishing Co.• Medical World Communications

• The New England Journal of Medicine• Nielsen Business Media• OAG Official Airline Guide• Parkell Dental Products• PCS Health Systems• PennWell Corporation• Penton Media• Primedia/Intertec Corporation• Professional Media LLC• Reed Construction Data• Reed Business Information/Cahners/

Gordon Publications• Reed Elsevier Medical Publishers• The Society Of Manufacturing Engineers• Springhouse Corporation• Symbol Technologies• Time Ventures• UBM/Canon• Vance Publishing• Veterinary Learning Systems

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

• Date Conducted: September, 2013

• Medium Used: Two email invitations + an online questionnaire.

• Universe Studied: The combined Oil & Gas Journal and Offshore audiences, where email addresses were available - 277,816 names. The unduplicated list was drawn from each brand’s full suite of media -- magazines, Websites, e-newsletters, events, etc.

• Market Sectors Studied: Oil and gas companies, engineering/design/ construction firms, industry contractors, and related consulting firms.

• Titles Selected: All qualified titles that were part of the brands’ audiences.

• Identification: The survey was sent out over the Oil & Gas Journal and Offshore logos.

• Incentives For Response: Contests -- a gourmet dinner, event tickets.

• Number Of Respondents: 1,884 qualified respondents; margin of error = +/-2.3% (95% confidence level).

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 13

METHODOLOGY

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

A. Respondents’Status as

Decision Makersin the

Oil & GasIndustry

14

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

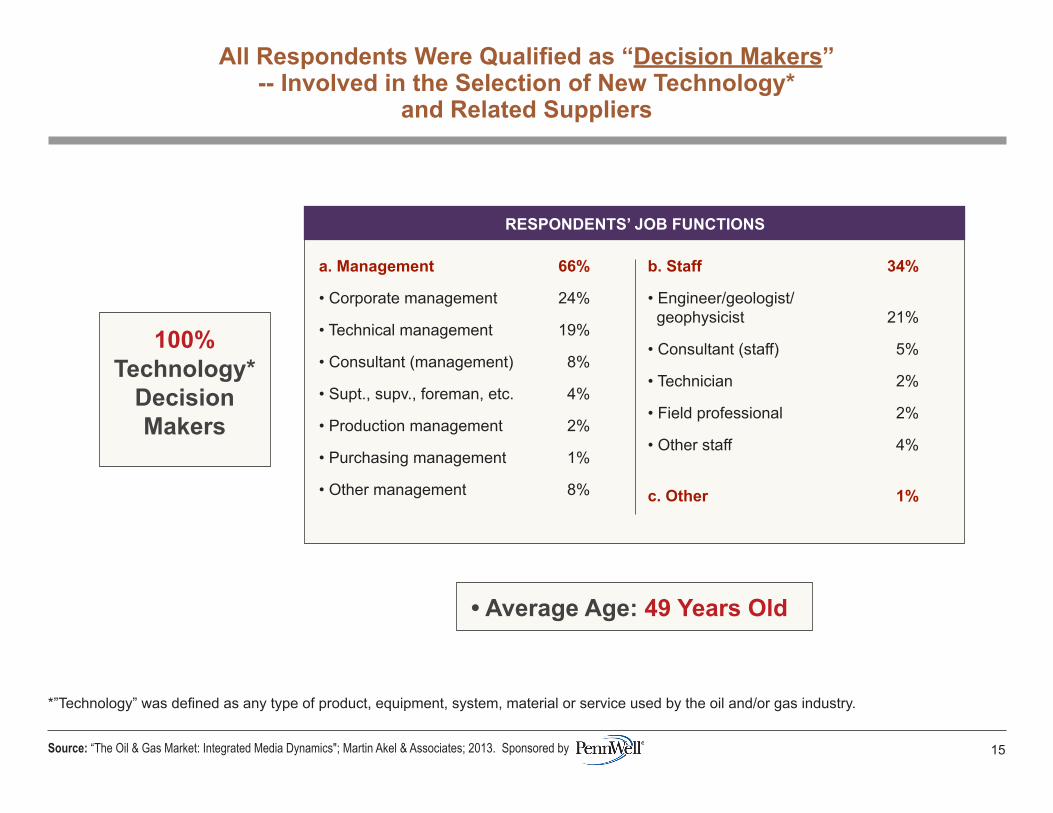

All Respondents Were Qualified as “Decision Makers”-- Involved in the Selection of New Technology*

and Related Suppliers

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 15

RESPONDENTS’ JOB FUNCTIONS

*”Technology” was defined as any type of product, equipment, system, material or service used by the oil and/or gas industry.

100%Technology*

DecisionMakers

a. Management 66%

• Corporate management 24%

• Technical management 19%

• Consultant (management) 8%

• Supt., supv., foreman, etc. 4%

• Production management 2%

• Purchasing management 1%

• Other management 8%

b. Staff 34%

• Engineer/geologist/ geophysicist 21%

• Consultant (staff) 5%

• Technician 2%

• Field professional 2%

• Other staff 4%

c. Other 1%

• Average Age: 49 Years Old

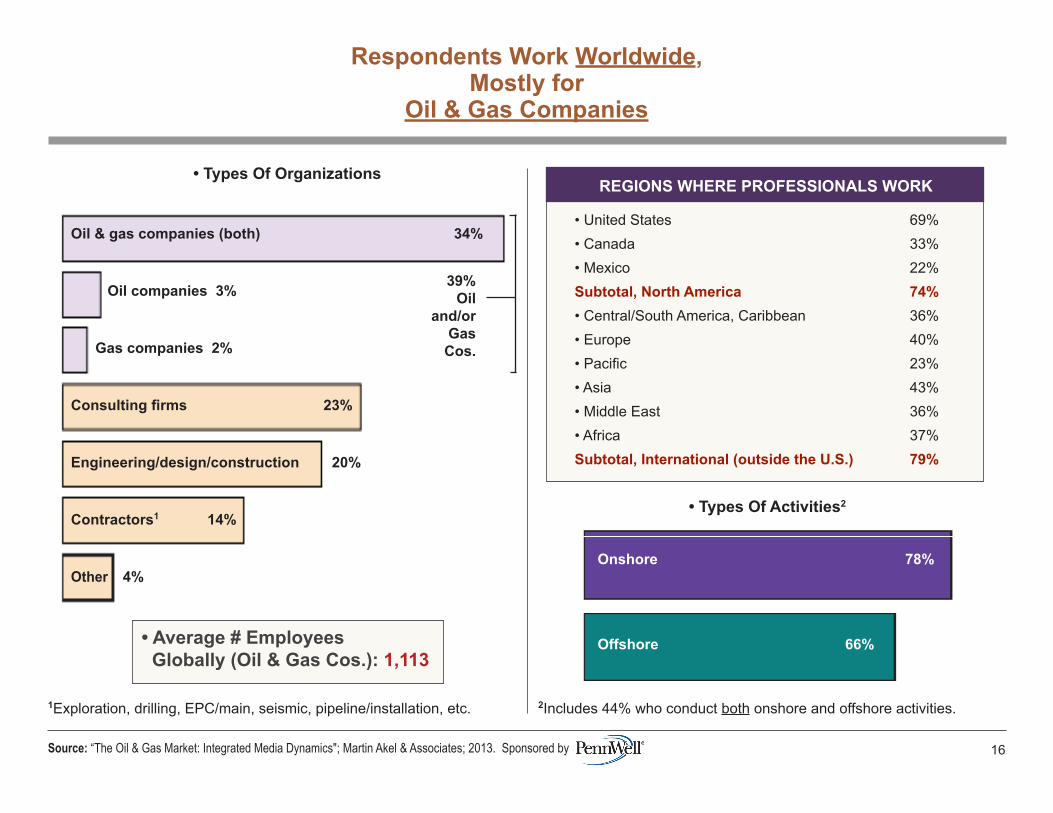

Oil & gas companies (both) 34%

Oil companies 3%

Gas companies 2%

Consulting firms 23%

Engineering/design/construction 20%

Contractors1 14%

Other 4%

REGIONS WHERE PROFESSIONALS WORK

• Types Of Organizations

Respondents Work Worldwide,Mostly for

Oil & Gas Companies

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 16

• Average # Employees Globally (Oil & Gas Cos.): 1,113

1Exploration, drilling, EPC/main, seismic, pipeline/installation, etc.

• United States 69%• Canada 33%• Mexico 22%Subtotal, North America 74%• Central/South America, Caribbean 36%• Europe 40%• Pacific 23%• Asia 43%• Middle East 36%• Africa 37%Subtotal, International (outside the U.S.) 79%

• Types Of Activities2

2Includes 44% who conduct both onshore and offshore activities.

39%Oil

and/orGasCos.

Onshore 78%

Offshore 66%

Examples of CompaniesParticipating in this Study

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 17

• Amec Oil & Gas• Anadarko Petroleum Corp.• Aurora Gas, LLC• Belize Natural Energy, Ltd.• Berger Geosciences, LLC• BP• Canyon Offshore Inc.• Chesapeake Energy• Chevron Australia Pty Ltd• CNX Gas Co. LLC• ConocoPhillips• Diamond Offshore Drilling• DOF Subsea• DTE Pipeline Company• Eastern Oil and Gas Company• Enbridge Pipelines Inc.• Encana Oil & Gas• Essar Oil Ltd.• ExxonMobil• FSI Energy• Genesis Pipeline• Geophysical Pursuit, Inc.• GT Gas LLC• Halliburton Energy Services

• Pegasus Oil & Gas• PEMEX• Persian Offshore• Petrobras• Petroleum Development Oman LLC• Petronas• Qatar Petroleum• QEP Energy• Red Oak Petroleum Corp• RNK Energy• ROO Iraq• RPS Energy• Saipem• Sanjel Canada Ltd.• Saudi Aramco• Shell• South Texas Petroleum, LLC• Suncor Energy• T-C Oil Company, LLC• Technip France• The Eastland Oil Company• TransCanada• Transocean• Valero Energy Corp.

• Hess• Husky Energy• Icon Oil and Gas• IntecSea• Keen Oil Company LLC• Kiewit Offshore Services• Kuwait Oil Company• LUKOIL Engineering• Marathon Oil• MarkWest Energy Partners• Nabors Alaska Drilling• NalcoChampion• National Oilwell Varco• Noble Drilling• Northern Offshore• Norton Engineering Consultants• Occidental Petroleum• Oil & Natural Gas Corporation Ltd.• Oil States Industries, Inc.• Onesubsea• Ophir Energy• Origin Energy• OSM Offshore AS• Pace Global, Siemens

• All respondents are technology decision makers in the global oil and/or gas industries ... and their activities reflect both the onshore and offshore market sectors.

• Respondents are therefore well qualified to comment on the industry’s challenges, trends in relationships with suppliers, and on today’s media engagement patterns.

CONCLUSIONS:

A. Respondents’ Status as Decision Makersin the Oil & Gas Industry

18

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

B. ChallengesFaced;

the Use ofTechnologyto AddressChallenges

19

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

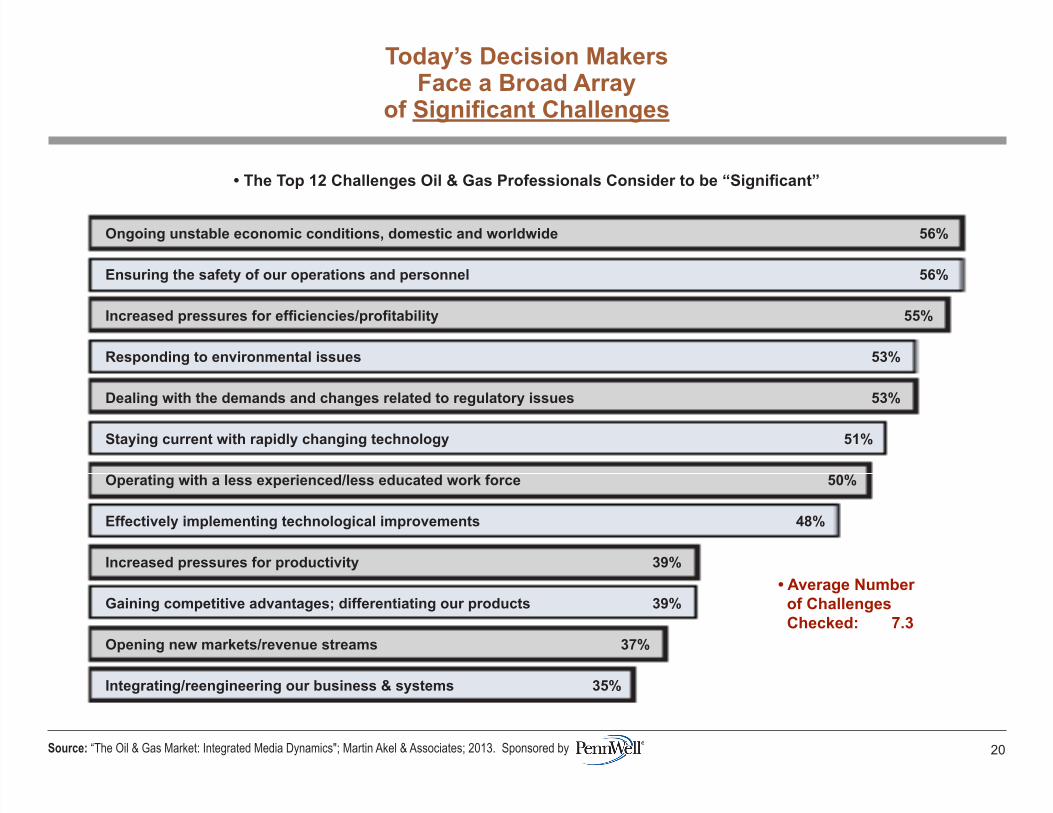

Today’s Decision MakersFace a Broad Array

of Significant Challenges

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 20

• The Top 12 Challenges Oil & Gas Professionals Consider to be “Significant”

Ongoing unstable economic conditions, domestic and worldwide 56%

Ensuring the safety of our operations and personnel 56%

Increased pressures for efficiencies/profitability 55%

Responding to environmental issues 53%

Dealing with the demands and changes related to regulatory issues 53%

Staying current with rapidly changing technology 51%

Operating with a less experienced/less educated work force 50%

Effectively implementing technological improvements 48%

Increased pressures for productivity 39%

Gaining competitive advantages; differentiating our products 39%

Opening new markets/revenue streams 37%

Integrating/reengineering our business & systems 35%

• Average Number of Challenges Checked: 7.3

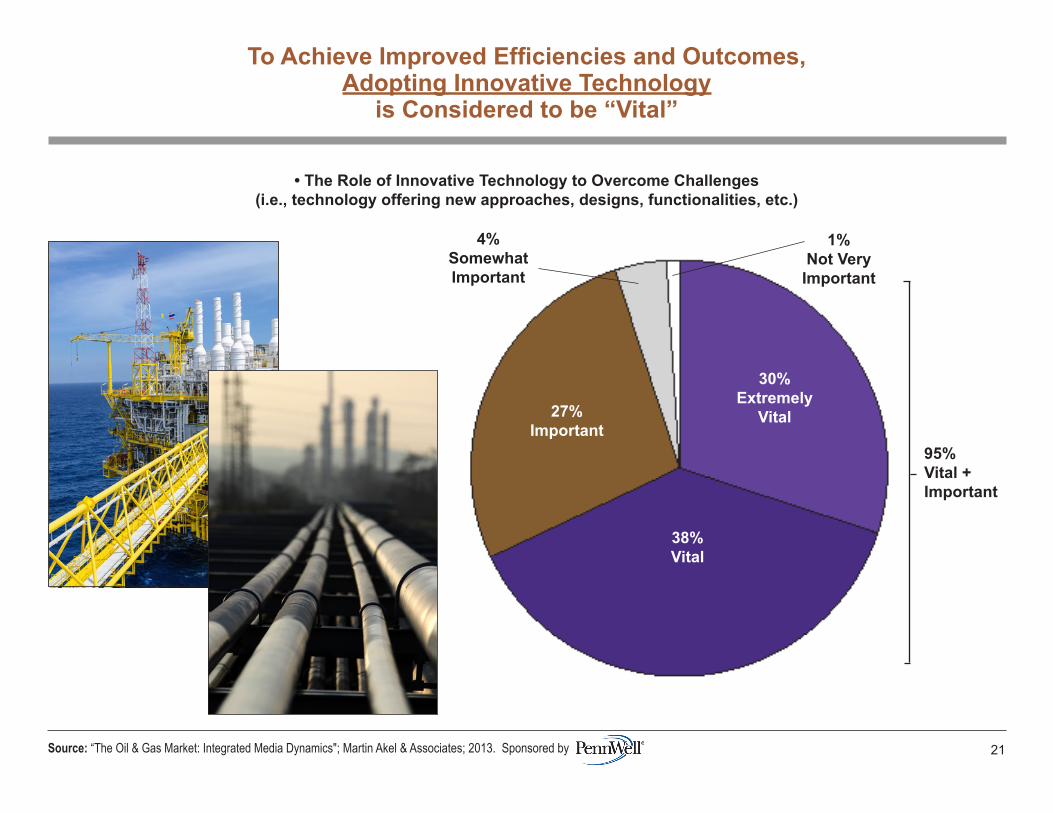

To Achieve Improved Efficiencies and Outcomes,Adopting Innovative Technology

is Considered to be “Vital”

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 21

• The Role of Innovative Technology to Overcome Challenges(i.e., technology offering new approaches, designs, functionalities, etc.)

95%Vital +Important

4%SomewhatImportant

30%Extremely

Vital

38%Vital

27%Important

1%Not VeryImportant

• Those who make decisions on products and systems face a wide range of challenges. And most are relying on new technology to help overcome those issues.

• This positive market condition can be advantageous to suppliers who can:

- Effectively position their brands as solutions.

- Establish and maintain strong brand relationships with key buyers.

CONCLUSIONS:

B. Challenges Faced;the Use of Technology to Address Challenges

22

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

C. Trends in theEnvironmentfor BrandingProducts and

Systems

23

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

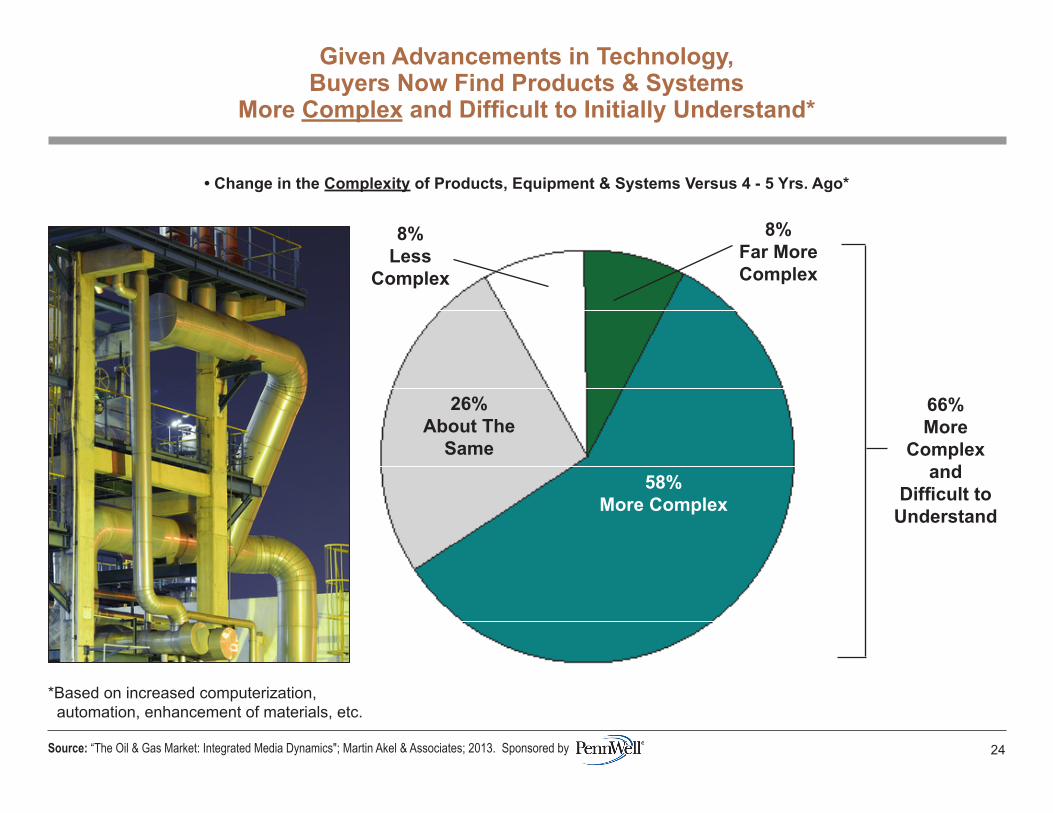

• Change in the Complexity of Products, Equipment & Systems Versus 4 - 5 Yrs. Ago*

Given Advancements in Technology,Buyers Now Find Products & Systems

More Complex and Difficult to Initially Understand*

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 24

*Based on increased computerization, automation, enhancement of materials, etc.

58%More Complex

26%About The

Same

8%Less

Complex

66%More

Complexand

Difficult toUnderstand

8%Far MoreComplex

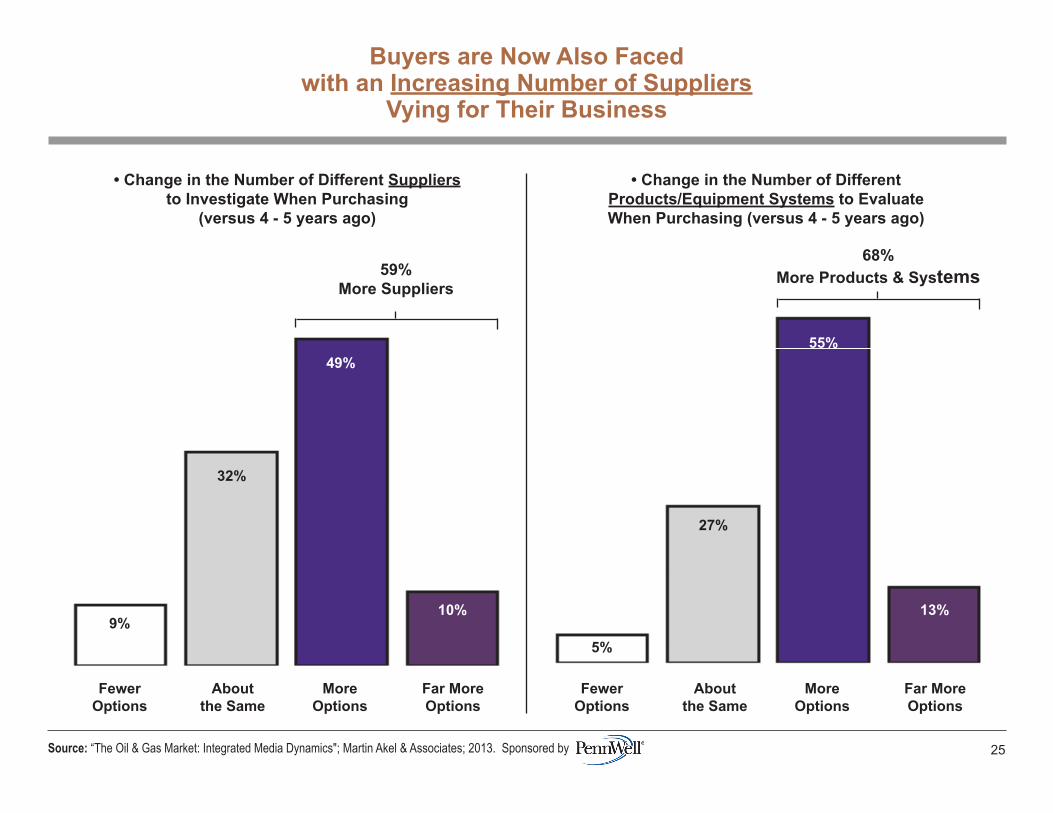

• Change in the Number of Different Suppliersto Investigate When Purchasing

(versus 4 - 5 years ago)

Buyers are Now Also Facedwith an Increasing Number of Suppliers

Vying for Their Business

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 25

• Change in the Number of DifferentProducts/Equipment Systems to EvaluateWhen Purchasing (versus 4 - 5 years ago)

59%More Suppliers

FewerOptions

Aboutthe Same

MoreOptions

Far MoreOptions

9%

32%

49%

10%

68%More Products & Systems

FewerOptions

Aboutthe Same

MoreOptions

Far MoreOptions

5%

27%

55%

13%

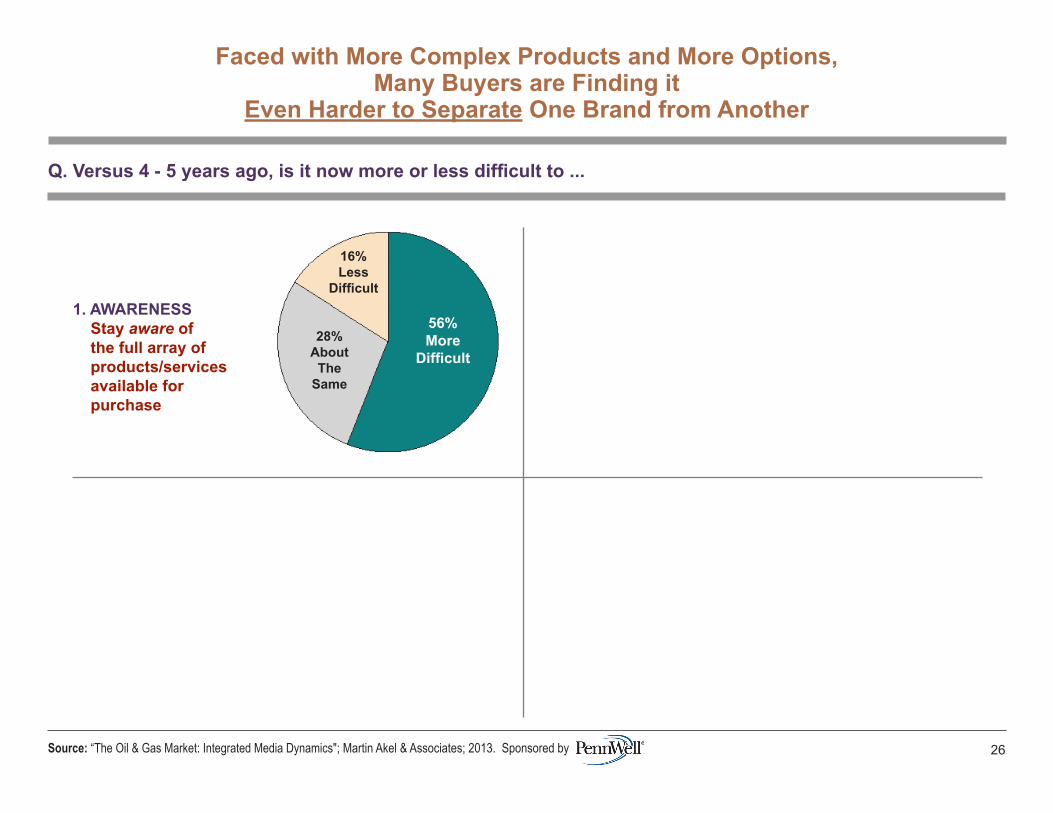

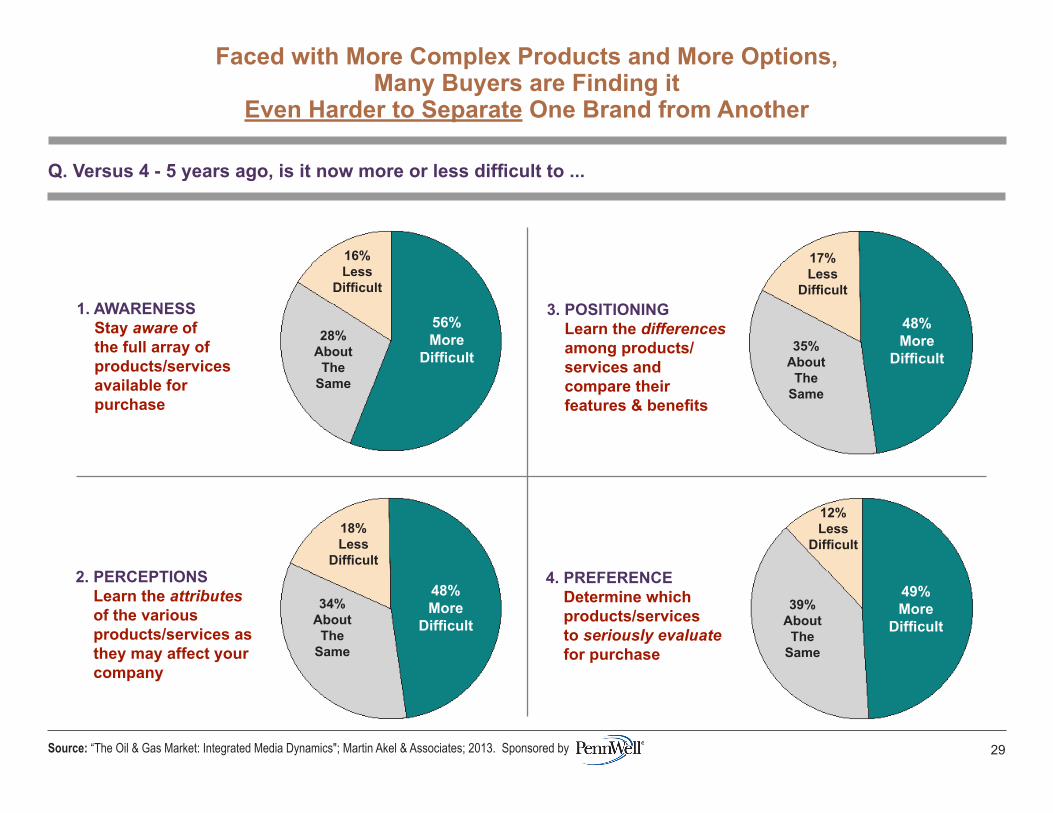

Faced with More Complex Products and More Options,Many Buyers are Finding it

Even Harder to Separate One Brand from Another

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 26

Q. Versus 4 - 5 years ago, is it now more or less difficult to ...

1. AWARENESS Stay aware of the full array of products/services available for purchase

56%More

Difficult28%

AboutThe

Same

16%Less

Difficult

Faced with More Complex Products and More Options,Many Buyers are Finding it

Even Harder to Separate One Brand from Another

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 27

Q. Versus 4 - 5 years ago, is it now more or less difficult to ...

1. AWARENESS Stay aware of the full array of products/services available for purchase

56%More

Difficult28%

AboutThe

Same

16%Less

Difficult

2. PERCEPTIONS Learn the attributes of the various products/services as they may affect your company

48%More

Difficult34%

AboutThe

Same

18%Less

Difficult

Faced with More Complex Products and More Options,Many Buyers are Finding it

Even Harder to Separate One Brand from Another

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 28

Q. Versus 4 - 5 years ago, is it now more or less difficult to ...

1. AWARENESS Stay aware of the full array of products/services available for purchase

56%More

Difficult28%

AboutThe

Same

16%Less

Difficult

2. PERCEPTIONS Learn the attributes of the various products/services as they may affect your company

48%More

Difficult34%

AboutThe

Same

18%Less

Difficult

3. POSITIONING Learn the differences among products/ services and compare their features & benefits

48%More

Difficult35%

AboutThe

Same

17%Less

Difficult

Faced with More Complex Products and More Options,Many Buyers are Finding it

Even Harder to Separate One Brand from Another

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 29

Q. Versus 4 - 5 years ago, is it now more or less difficult to ...

1. AWARENESS Stay aware of the full array of products/services available for purchase

56%More

Difficult28%

AboutThe

Same

16%Less

Difficult

2. PERCEPTIONS Learn the attributes of the various products/services as they may affect your company

48%More

Difficult34%

AboutThe

Same

18%Less

Difficult

3. POSITIONING Learn the differences among products/ services and compare their features & benefits

48%More

Difficult35%

AboutThe

Same

17%Less

Difficult

4. PREFERENCE Determine which products/services to seriously evaluate for purchase

49%More

Difficult39%

AboutThe

Same

12%Less

Difficult

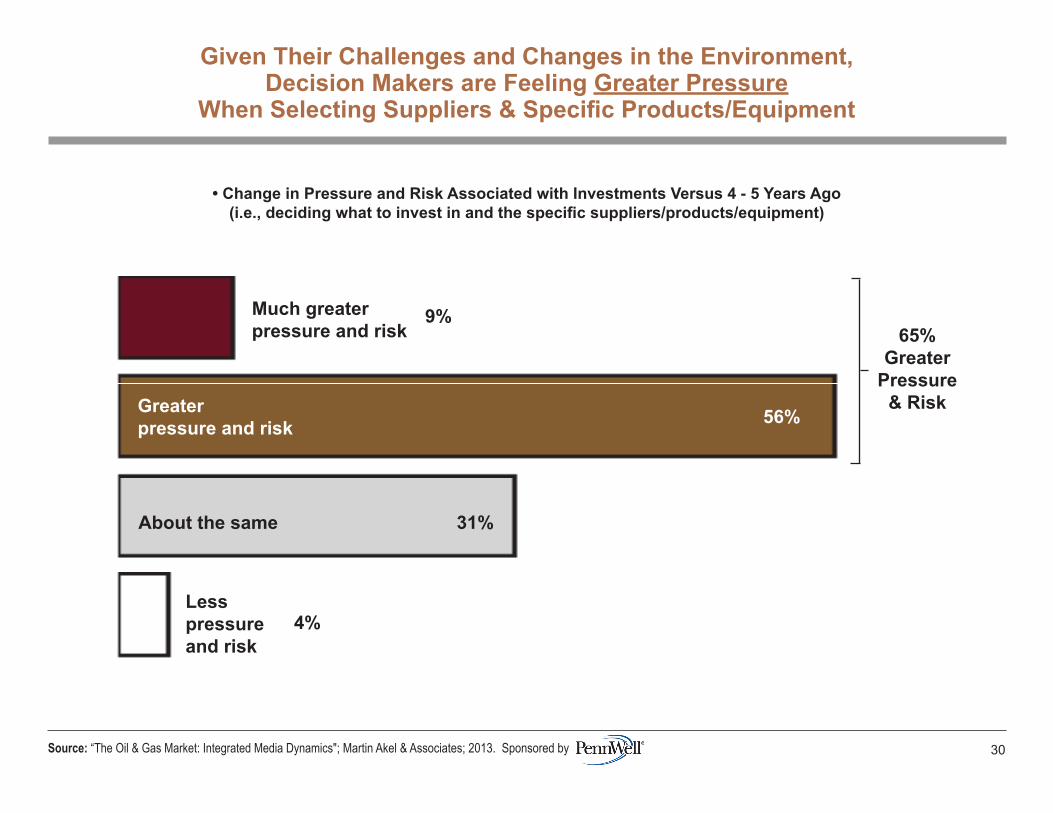

• Change in Pressure and Risk Associated with Investments Versus 4 - 5 Years Ago(i.e., deciding what to invest in and the specific suppliers/products/equipment)

Much greaterpressure and risk

Greaterpressure and risk

About the same 31%

Less pressure and risk

9%

56%

65%Greater

Pressure & Risk

4%

Given Their Challenges and Changes in the Environment,Decision Makers are Feeling Greater Pressure

When Selecting Suppliers & Specific Products/Equipment

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 30

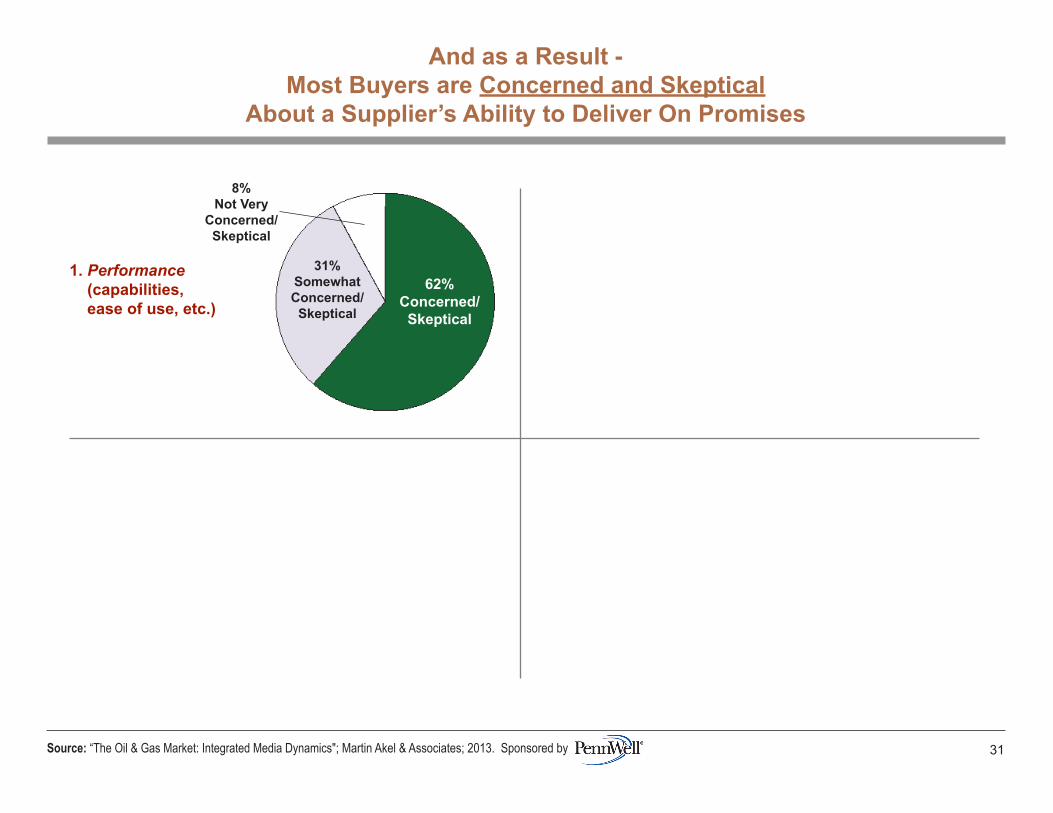

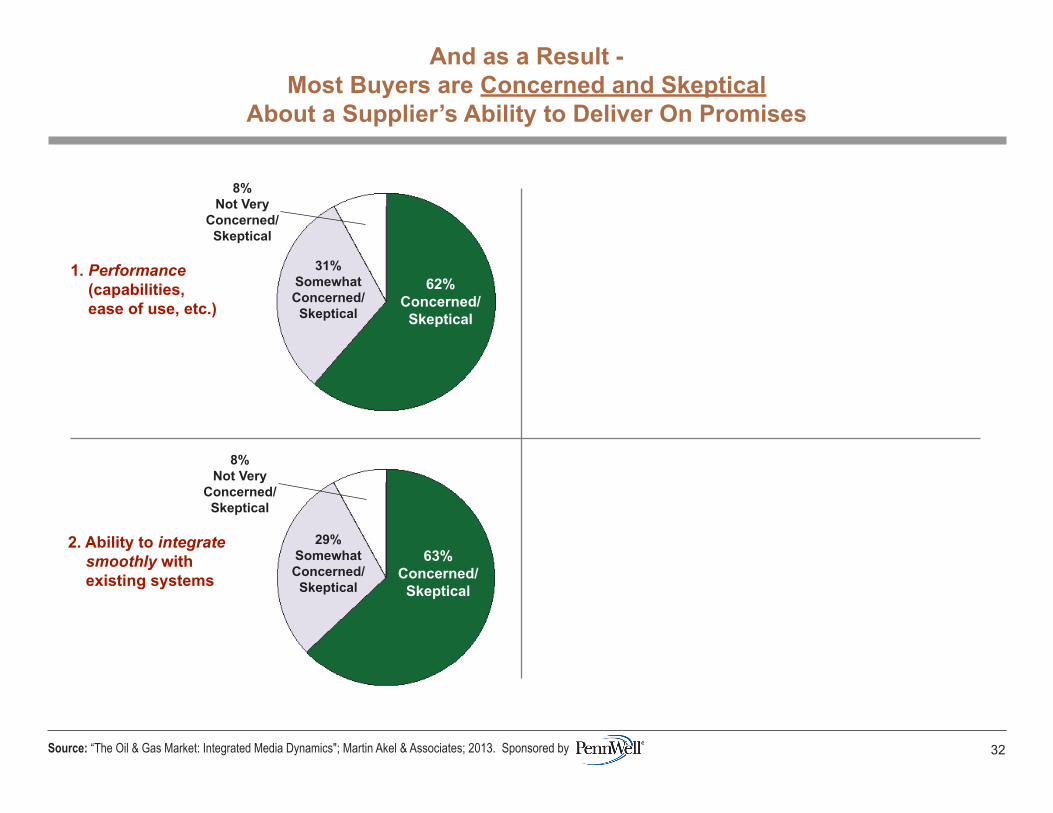

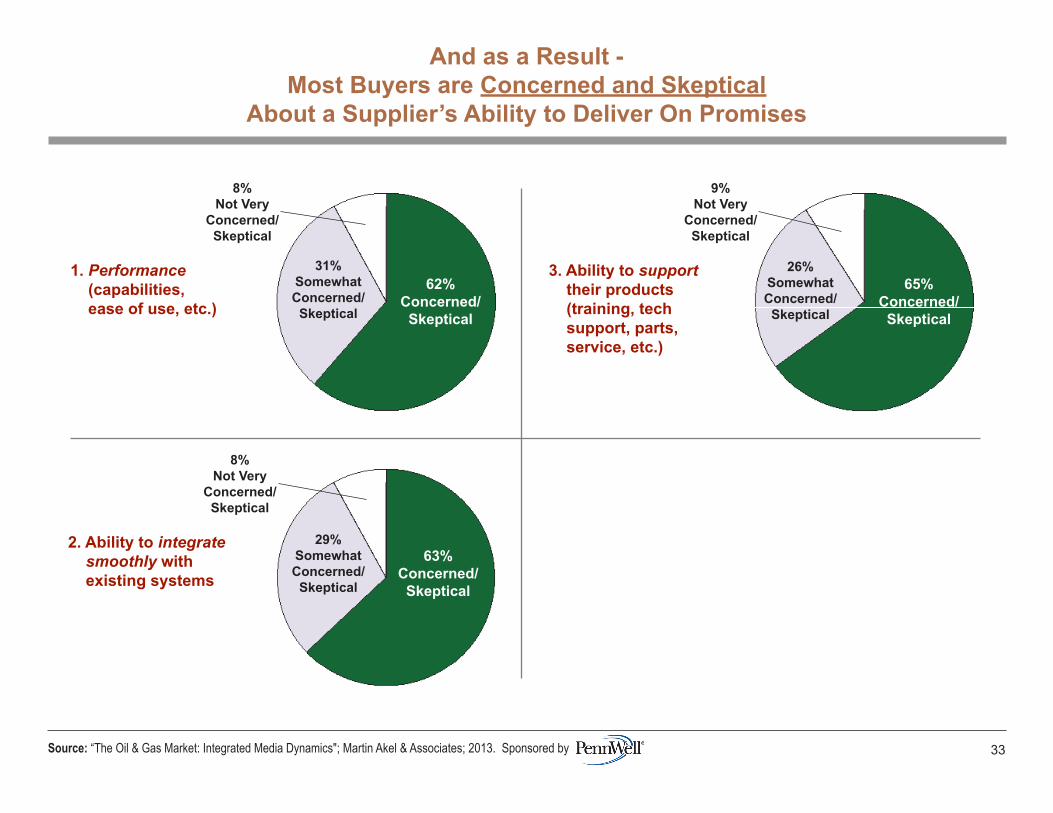

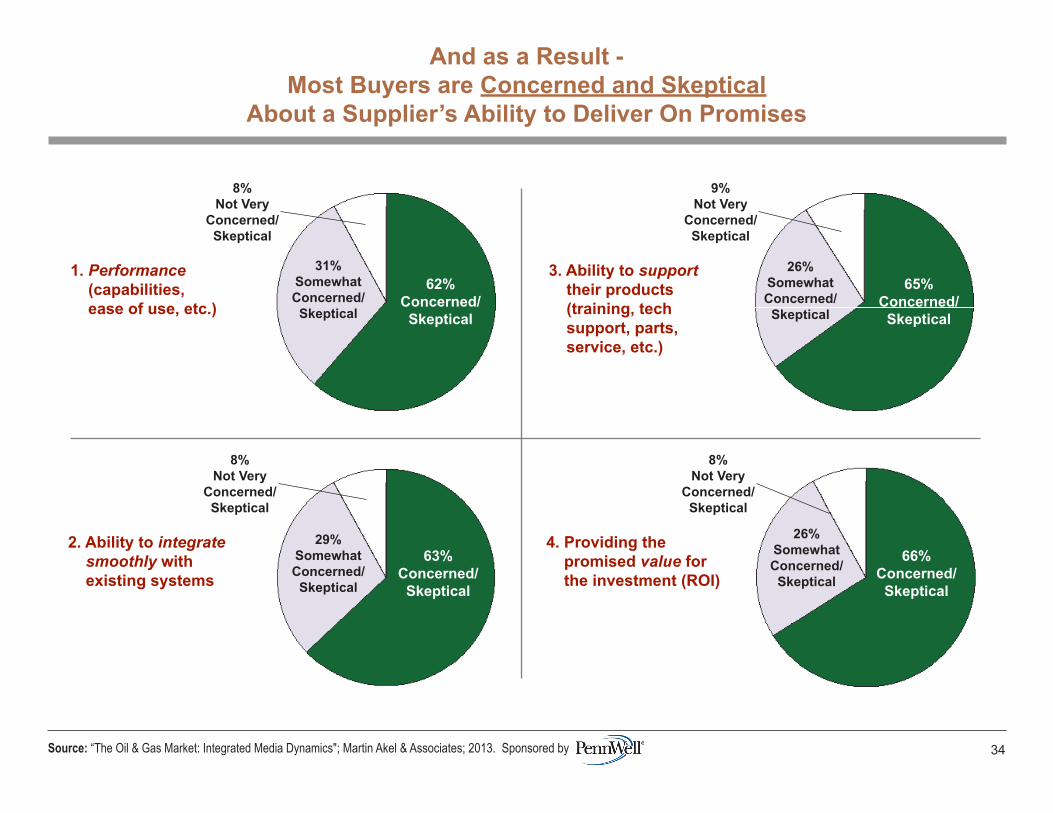

1. Performance (capabilities, ease of use, etc.)

62%Concerned/Skeptical

31%SomewhatConcerned/Skeptical

8%Not Very

Concerned/Skeptical

And as a Result -Most Buyers are Concerned and Skeptical

About a Supplier’s Ability to Deliver On Promises

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 31

1. Performance (capabilities, ease of use, etc.)

62%Concerned/Skeptical

31%SomewhatConcerned/Skeptical

8%Not Very

Concerned/Skeptical

2. Ability to integrate smoothly with existing systems

63%Concerned/Skeptical

29%SomewhatConcerned/Skeptical

8%Not Very

Concerned/Skeptical

And as a Result -Most Buyers are Concerned and Skeptical

About a Supplier’s Ability to Deliver On Promises

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 32

1. Performance (capabilities, ease of use, etc.)

62%Concerned/Skeptical

31%SomewhatConcerned/Skeptical

8%Not Very

Concerned/Skeptical

2. Ability to integrate smoothly with existing systems

63%Concerned/Skeptical

29%SomewhatConcerned/Skeptical

8%Not Very

Concerned/Skeptical

3. Ability to support their products (training, tech support, parts, service, etc.)

65%Concerned/Skeptical

26%SomewhatConcerned/Skeptical

9%Not Very

Concerned/Skeptical

And as a Result -Most Buyers are Concerned and Skeptical

About a Supplier’s Ability to Deliver On Promises

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 33

1. Performance (capabilities, ease of use, etc.)

62%Concerned/Skeptical

31%SomewhatConcerned/Skeptical

8%Not Very

Concerned/Skeptical

2. Ability to integrate smoothly with existing systems

63%Concerned/Skeptical

29%SomewhatConcerned/Skeptical

8%Not Very

Concerned/Skeptical

3. Ability to support their products (training, tech support, parts, service, etc.)

65%Concerned/Skeptical

26%SomewhatConcerned/Skeptical

9%Not Very

Concerned/Skeptical

4. Providing the promised value for the investment (ROI)

66%Concerned/Skeptical

26%SomewhatConcerned/Skeptical

8%Not Very

Concerned/Skeptical

And as a Result -Most Buyers are Concerned and Skeptical

About a Supplier’s Ability to Deliver On Promises

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 34

Buyers Have Also Made Significant Changes in Their Relationshipswith Suppliers ... Especially in Requiring Vendors

to Provide Greater Proof of Performance

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 35

• Changes Buyers Have Made in Relationships with Suppliers (Versus 4 - 5 Years Ago)

Now require suppliers to provide, up front, greater proof of performance 60%

The evaluation of suppliers & technology is now more rigorous and analytical 59%

Now require suppliers to offer more support (tech support, maintenance, etc.) 58%

Now require suppliers to be more accountable for their technology 57%

Now require suppliers to stay more involved after the sale (implementing, training, consulting, etc.) 55%

Now make more objective decisions about technology & brands (performance, ROI, etc.) 51%

Have a more businesslike relationship with suppliers (rely less on personal attributes) 47%

Now require suppliers to develop more customized solutions to their situations 46%

Now require suppliers to provide more info. on total cost of ownership 43%

Measure the ROI more closely after implementation 31%

93%Have ChangedRelationshipsWith Suppliers

Buyers Remarked on the ForcesDriving Changes in Relationships with Suppliers

An Evolving, More Competitive Oil & Gas Market:

• “Producing from more difficult and complex fields.”- Engineer/Geologist/Geophysicist, Oil & Gas Company

• “No more easy oil, pressure to produce more, produce faster, do it all more profitably.”- Consultant to the Oil & Gas Industry

• “More competitiveness, higher pressure on time and costs.”- Manager, Engineering/Design/Construction Company

Unsatisfactory Past Experiences With Suppliers:

• “Having performance fail to meet expectations.”- Corporate Manager, Contractor

• “Integrity, failure of the product, poor follow-up.”- Engineer/Geologist/Geophysicist, Consulting Firm

• “Require more transparent exchange of information from suppliers.”- Manager, Engineering/Design/Construction Company

• “Past failures. Determination to not repeat them.”- Engineer/Geologist/Geophysicist, Oil & Gas Company

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 36

Buyers Remarked on the ForcesDriving Changes in Relationships with Suppliers

Availability Of More Suppliers; Competition Among Suppliers:

• “More supplier options, more product and services options.”- Technical Manager, Engineering/Design/Construction Company

• “They know I have options now! More competitive!”- Corporate Manager, Consulting Firm

• “Driving force is availability of better products in the market.”- Technical Manager, Oil & Gas Company

The Need For Greater Accountability:

• “Less “good ol’ boy” used in the selection process and more hard data and tough negotiations.”- Technical Manager, Consulting Firm

• “Greater transparency to upper management, board of directors, investment community.”- Purchasing Manager, Oil Company

• “More oversight and a higher level of integrity is expected.”- Engineer/Geologist/Geophysicist,Contractor

• “Performance and profitability drive a more rigorous evaluation of product/technology.”- Engineer/Geologist/Geophysicist, Oil & Gas Company

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 37

Buyers Remarked on the ForcesDriving Changes in Relationships with Suppliers

The Need For ROI/Cost Savings:

• “Corporate requiring more price bench marking instead of continuing with existing vendor.”- Engineer/Geologist/Geophysicist, Oil & Gas Company

• “Less personal and more businesslike as ROI is a major portion of our concern.”- Consultant, Oil & Gas Company

• “Less relationship and more performance.”- Corporate Manager; Consulting Firm

Environmental/Safety Issues:

• “Greater stress on environmental impact, safety, and cost consciousness.”- Corporate Manager; Consulting Firm

• “Safety is the biggest driving force behind the changes in relationships.”- Engineer/Geologist/Geophysicist, Oil & Gas Company

• “The industry can no longer rely on plausible deniability with respect to impact on the population and environment. We are dealing with a more informed, concerned and activist population who will no longer tolerate the laissez-faire attitude of the industry.”

- Corporate Manager, Contractor

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 38

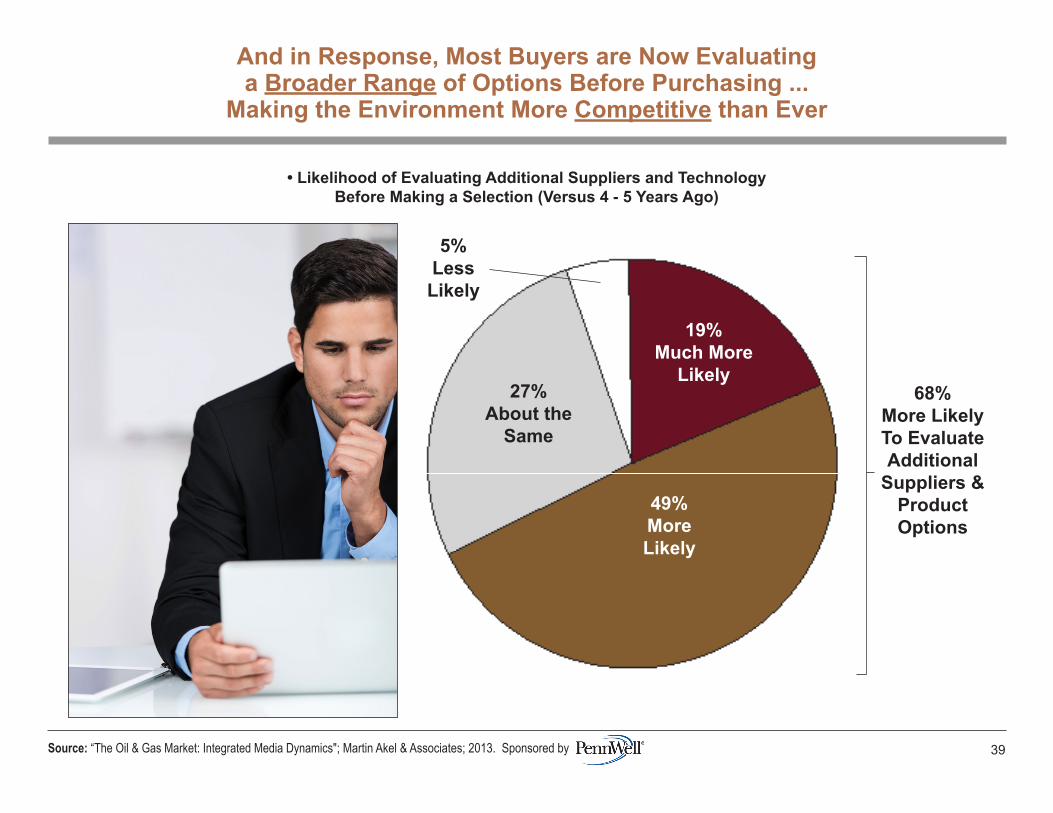

68%More LikelyTo EvaluateAdditional

Suppliers &ProductOptions

And in Response, Most Buyers are Now Evaluatinga Broader Range of Options Before Purchasing ...

Making the Environment More Competitive than Ever

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 39

• Likelihood of Evaluating Additional Suppliers and TechnologyBefore Making a Selection (Versus 4 - 5 Years Ago)

19%Much More

Likely

49%MoreLikely

27%About the

Same

5%Less Likely

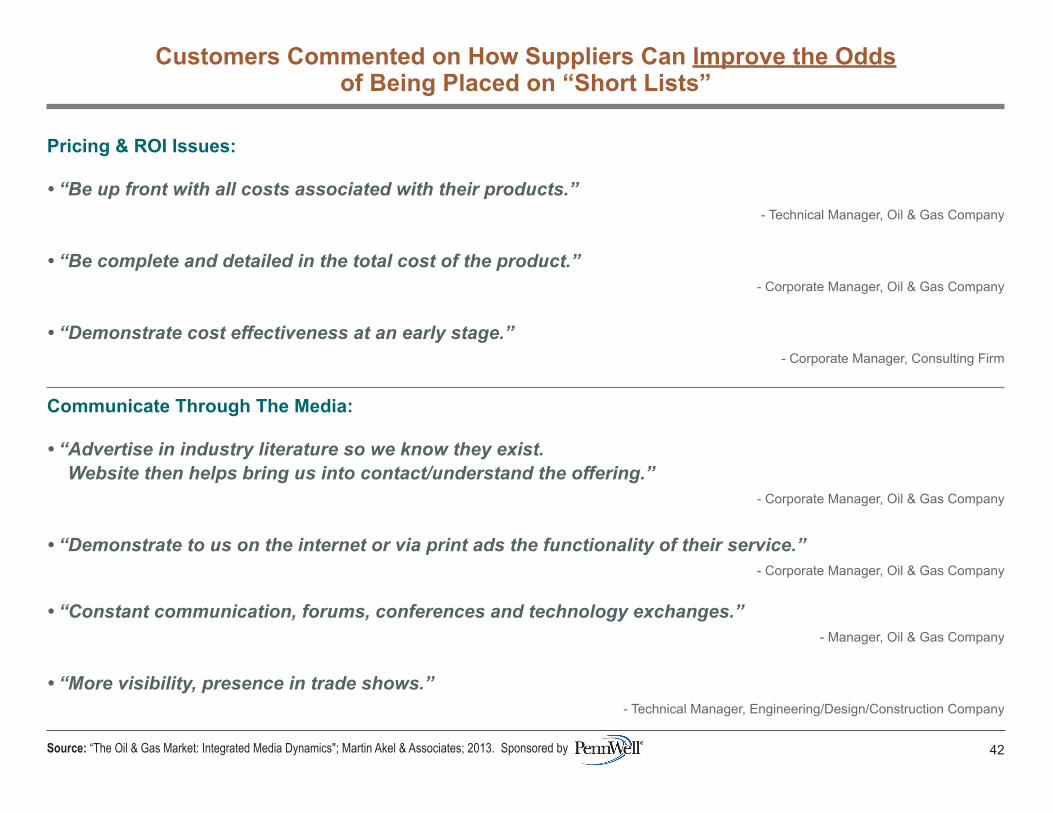

Customers Commented on How Suppliers Can Improve the Oddsof Being Placed on “Short Lists”

Be Honest:

• “Be honest and transparent about the technology and the ROI! Less sales pitch more integrity.”- Corporate Manager, Oil & Gas Company

• “Don’t oversell/embellish, don’t promise what you can’t deliver.”- Technical Manager, Oil & Gas Company

• “Show professionalism, not being a ‘car salesman’ just interested in selling the product.”- Engineer/Geologist/Geophysicist, Oil & Gas Company

Provide Proof Of Performance:

• “More factual data, less puff and fluff.”- Corporate Manager, Consulting Firm

• “Offer sound evidence of product quality and demonstrate it adds value.”- Engineer/Geologist/Geophysicist, Consulting Firm

• “Proof of concepts in real operational environment.”- Technical Manager, Oil & Gas Company

• “Demonstrate that the technology performs as described and integrates well.”- Consultant, Oil & Gas Company

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 40

Customers Commented on How Suppliers Can Improve the Oddsof Being Placed on “Short Lists”

Operate As A Partner:

• “Become a partner with the company rather than merely a vendor.”- Technical Manager, Oil & Gas Company

• “Be more supportive and display more ownership.”- Superintendent, Supervisor, Foreman, Oil & Gas Company

• “Demonstrate ability to line its mission and values with those of our clients.”- Engineer/Geologist/Geophysicist; Engineering/Design/Construction Company

Provide Relevant Case Histories:

• “Document successful application of their technology.”- Engineer/Geologist/Geophysicist, Oil & Gas Company

• “Demonstrate knowledge of our business/operations.”- Consultant, Oil & Gas Company

• “Demonstrate the merits of their technology by making case histories available.”- Engineer/Geologist/Geophysicist, Consulting Firm

• “Historical success!”- Corporate Manager, Consulting Firm

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 41

Customers Commented on How Suppliers Can Improve the Oddsof Being Placed on “Short Lists”

Pricing & ROI Issues:

• “Be up front with all costs associated with their products.”- Technical Manager, Oil & Gas Company

• “Be complete and detailed in the total cost of the product.”- Corporate Manager, Oil & Gas Company

• “Demonstrate cost effectiveness at an early stage.”- Corporate Manager, Consulting Firm

Communicate Through The Media:

• “Advertise in industry literature so we know they exist. Website then helps bring us into contact/understand the offering.”

- Corporate Manager, Oil & Gas Company

• “Demonstrate to us on the internet or via print ads the functionality of their service.”- Corporate Manager, Oil & Gas Company

• “Constant communication, forums, conferences and technology exchanges.”- Manager, Oil & Gas Company

• “More visibility, presence in trade shows.”- Technical Manager, Engineering/Design/Construction Company

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 42

• Buyers now find products more difficult to understand and differentiate from one another. They’re more skeptical about suppliers’ promises, and have altered their relationships with vendors. And more suppliers are now vying for their business.

• The result -- buyers are now evaluating a larger number of choices before making decisions.

• Therefore, to bring brands to market in a more businesslike, competitive environment, it’s imperative that suppliers work even harder to establish, maintain and differentiate their brands.

CONCLUSIONS:

C. Trends in the Environmentfor Branding Products and Systems

43

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

D. The Dynamicsof Team

Decision Makingfor New Technology

44

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

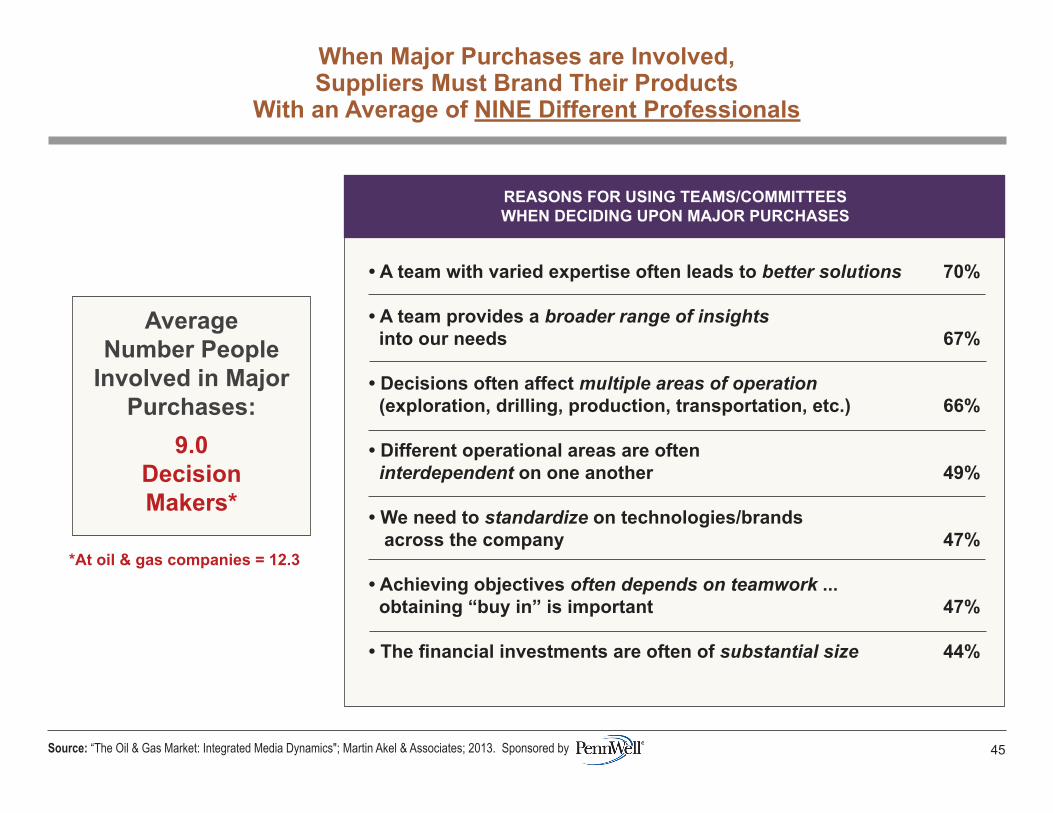

When Major Purchases are Involved,Suppliers Must Brand Their Products

With an Average of NINE Different Professionals

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 45

REASONS FOR USING TEAMS/COMMITTEESWHEN DECIDING UPON MAJOR PURCHASES

9.0DecisionMakers*

AverageNumber People

Involved in MajorPurchases:

• A team with varied expertise often leads to better solutions 70%

• A team provides a broader range of insights into our needs 67%

• Decisions often affect multiple areas of operation (exploration, drilling, production, transportation, etc.) 66%

• Different operational areas are often interdependent on one another 49%

• We need to standardize on technologies/brands across the company 47%

• Achieving objectives often depends on teamwork ... obtaining “buy in” is important 47%

• The financial investments are often of substantial size 44%

*At oil & gas companies = 12.3

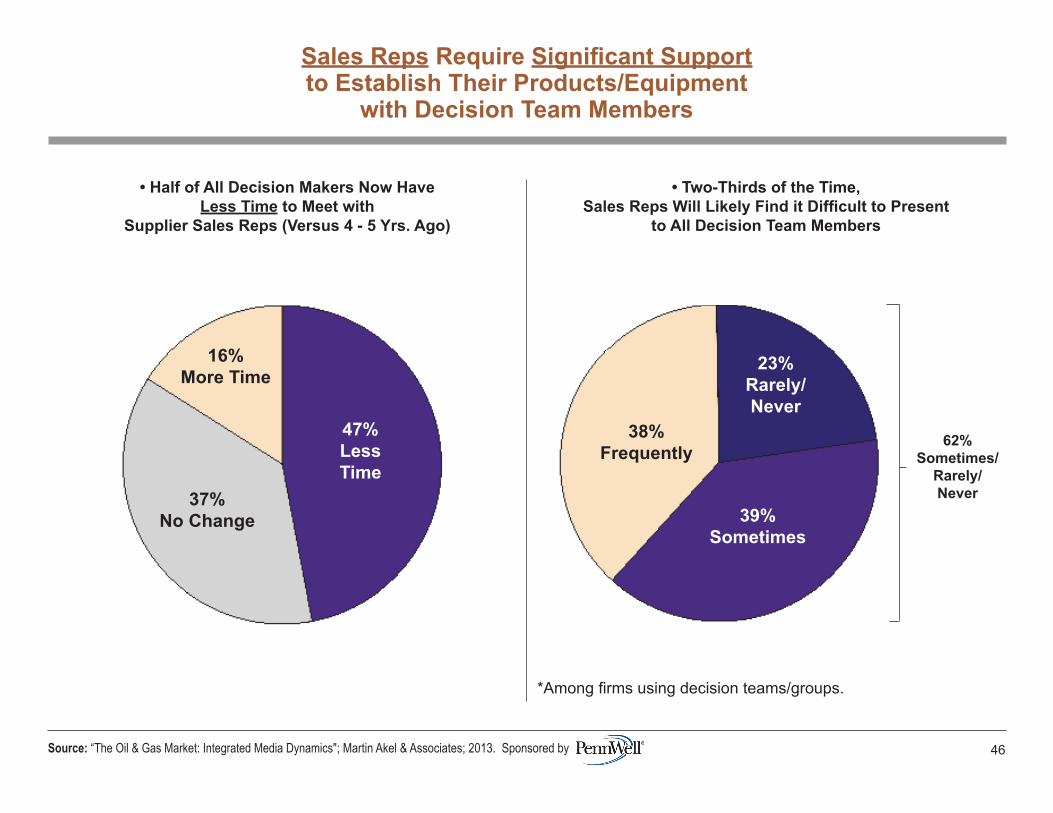

• Half of All Decision Makers Now HaveLess Time to Meet with

Supplier Sales Reps (Versus 4 - 5 Yrs. Ago)

Sales Reps Require Significant Supportto Establish Their Products/Equipment

with Decision Team Members

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 46

• Two-Thirds of the Time,Sales Reps Will Likely Find it Difficult to Present

to All Decision Team Members

62%Sometimes/

Rarely/Never

39%Sometimes

38%Frequently

23%Rarely/Never

*Among firms using decision teams/groups.

47%LessTime

16%More Time

37%No Change

• Virtually all firms use a team approach to making major purchasing decisions.

• Yet, sales reps often cannot call on all those involved in the selection of suppliers. In fact, the majority of buyers now have even less time to meet with reps.

• Therefore, in an era when it’s even more imperative to maintain and differentiate brands, suppliers must look beyond their own sales teams to achieve those objectives.

CONCLUSIONS:

D. The Dynamics ofTeam Decision Making for New Technology

47

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

E. How Buyersare Branded AboutSuppliers, Products

and Systems

48

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

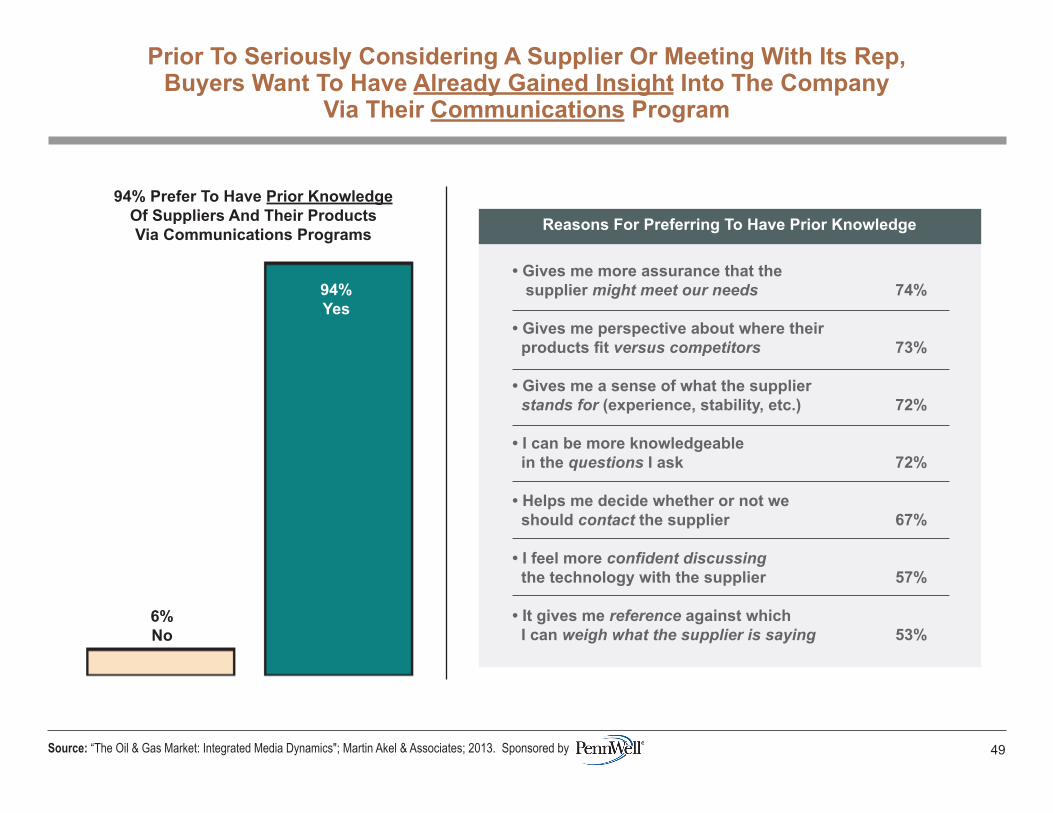

Prior To Seriously Considering A Supplier Or Meeting With Its Rep,Buyers Want To Have Already Gained Insight Into The Company

Via Their Communications Program

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 49

94% Prefer To Have Prior KnowledgeOf Suppliers And Their ProductsVia Communications Programs

94%Yes

6%No

Reasons For Preferring To Have Prior Knowledge

• Gives me more assurance that the supplier might meet our needs 74%

• Gives me perspective about where their products fit versus competitors 73%

• Gives me a sense of what the supplier stands for (experience, stability, etc.) 72%

• I can be more knowledgeable in the questions I ask 72%

• Helps me decide whether or not we should contact the supplier 67%

• I feel more confident discussing the technology with the supplier 57%

• It gives me reference against which I can weigh what the supplier is saying 53%

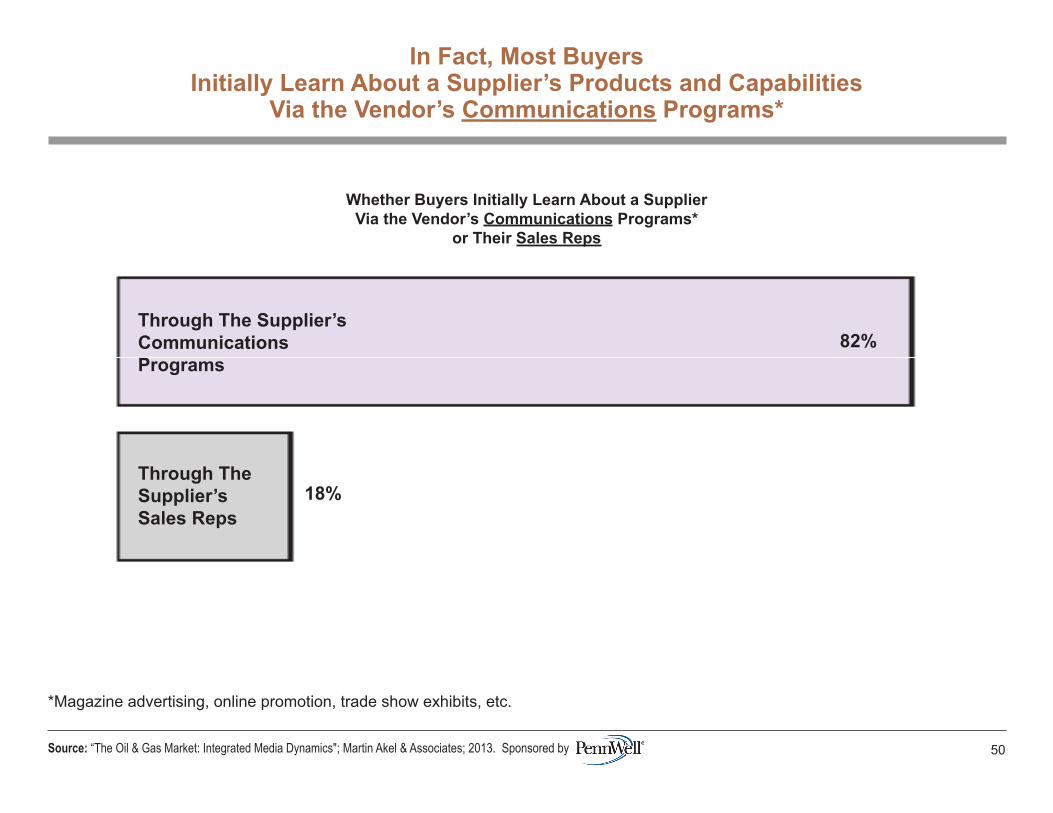

Whether Buyers Initially Learn About a SupplierVia the Vendor’s Communications Programs*

or Their Sales Reps

Through The Supplier’sCommunicationsPrograms

82%

Through The Supplier’sSales Reps

18%

In Fact, Most BuyersInitially Learn About a Supplier’s Products and Capabilities

Via the Vendor’s Communications Programs*

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 50

*Magazine advertising, online promotion, trade show exhibits, etc.

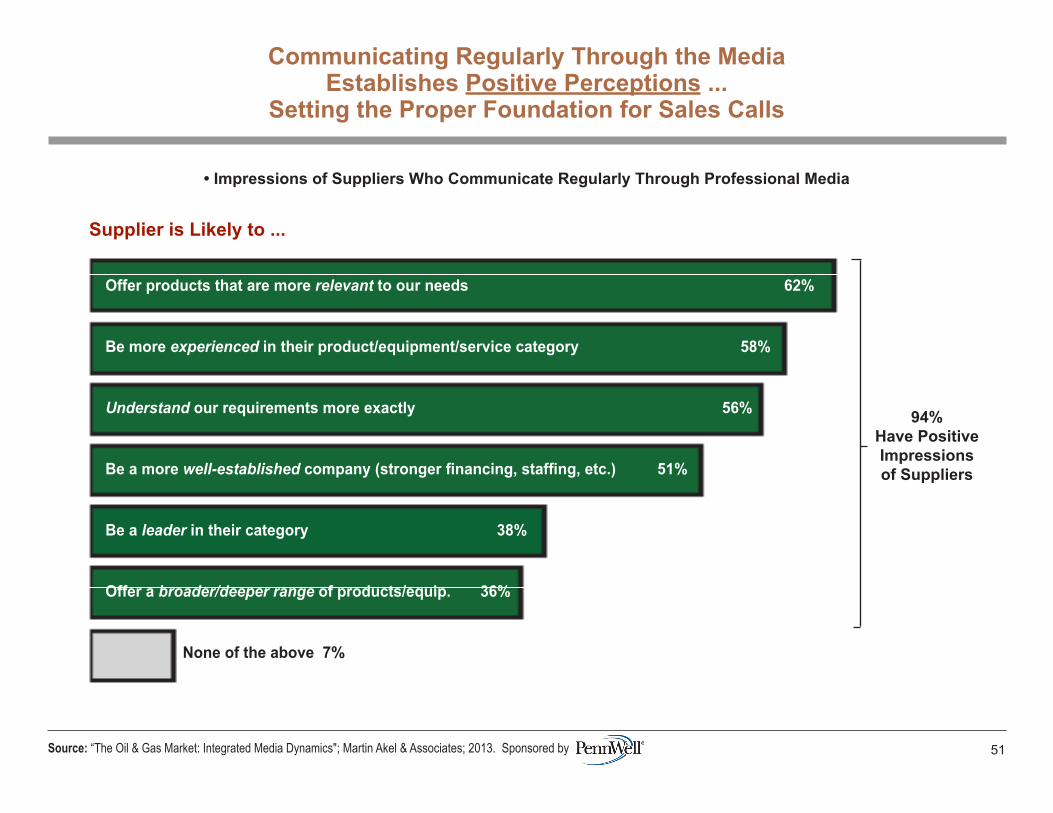

Communicating Regularly Through the MediaEstablishes Positive Perceptions ...

Setting the Proper Foundation for Sales Calls

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 51

94%Have PositiveImpressionsof Suppliers

• Impressions of Suppliers Who Communicate Regularly Through Professional Media

Supplier is Likely to ...

Offer products that are more relevant to our needs 62%

Be more experienced in their product/equipment/service category 58%

Understand our requirements more exactly 56%

Be a more well-established company (stronger financing, staffing, etc.) 51%

Be a leader in their category 38%

Offer a broader/deeper range of products/equip. 36%

None of the above 7%

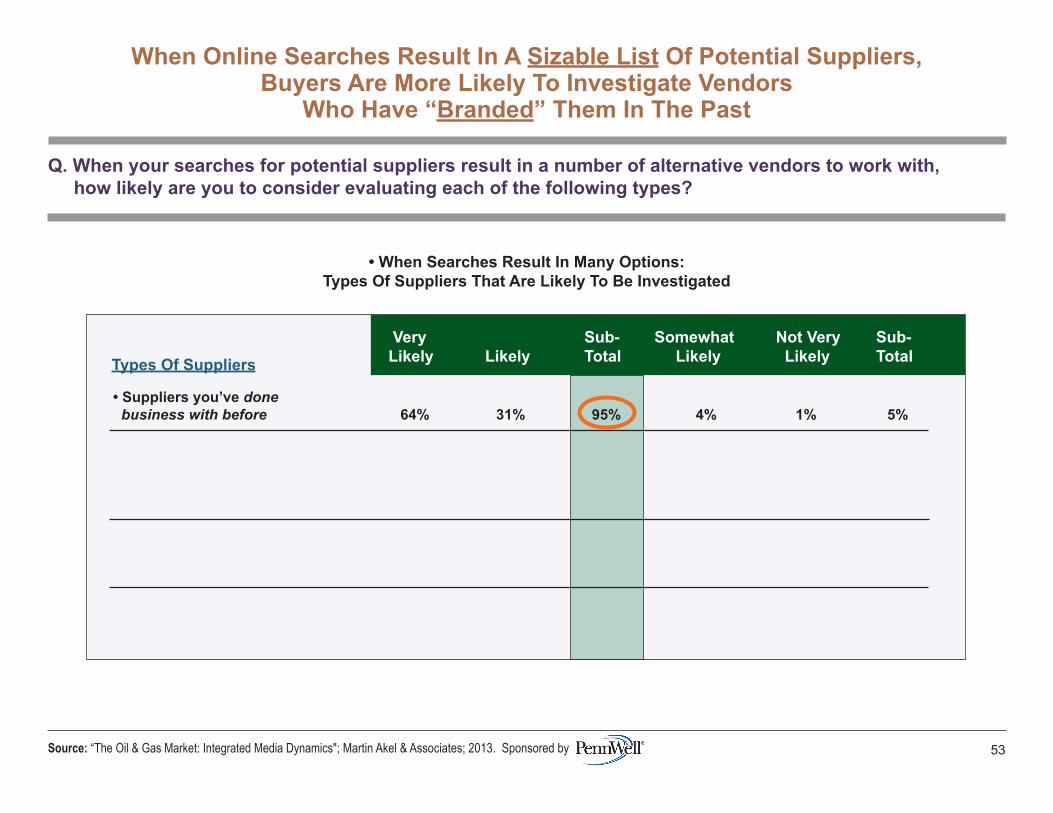

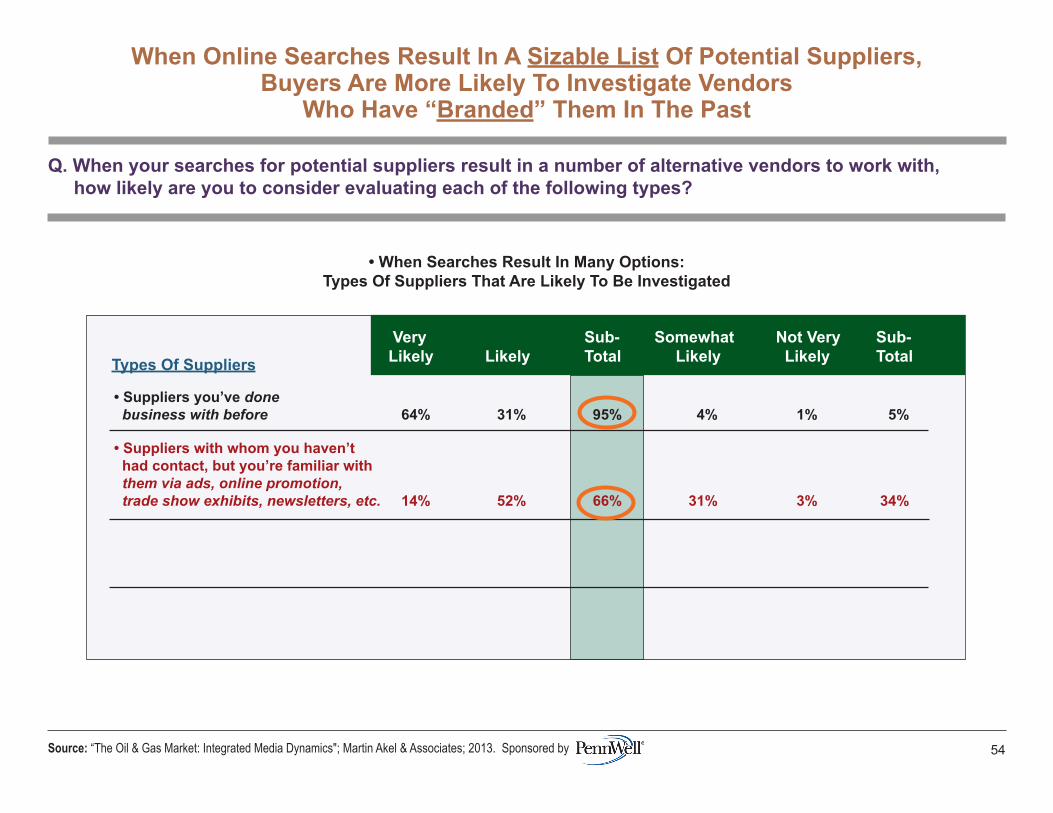

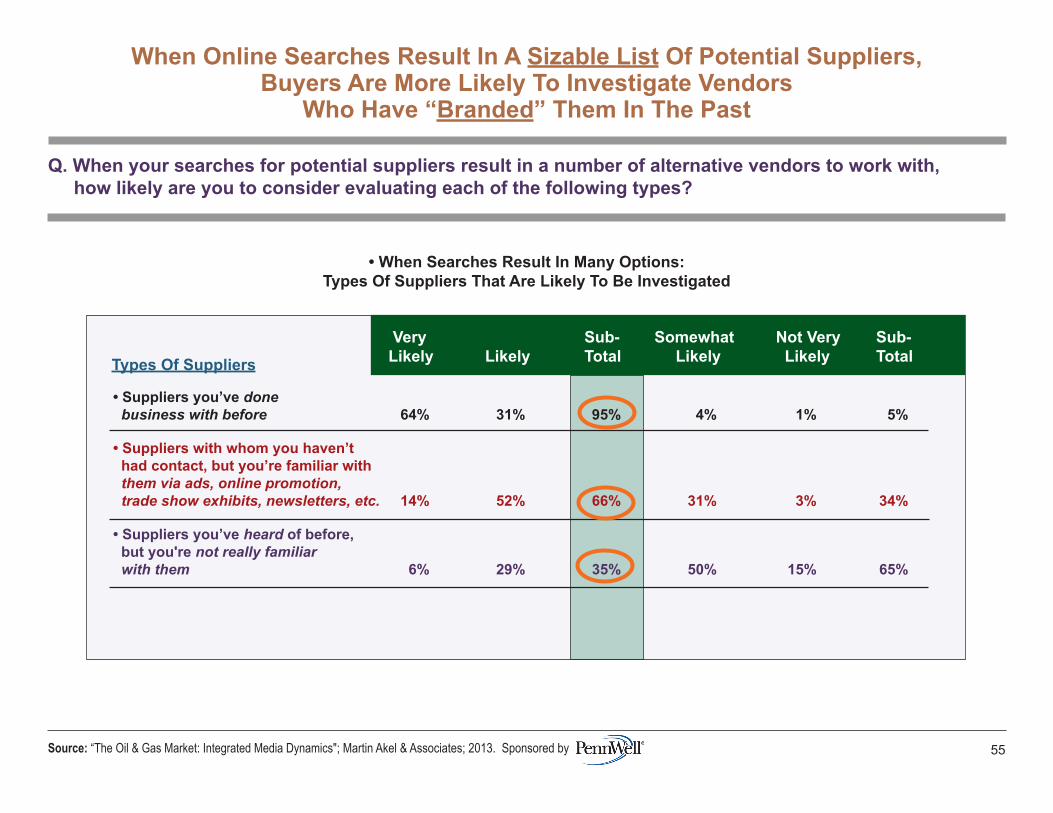

Q. When your searches for potential suppliers result in a number of alternative vendors to work with, how likely are you to consider evaluating each of the following types?

• When Searches Result In Many Options:Types Of Suppliers That Are Likely To Be Investigated

Very Sub- Somewhat Not Very Sub-Likely Likely Total Likely Likely TotalTypes Of Suppliers

When Online Searches Result In A Sizable List Of Potential Suppliers,Buyers Are More Likely To Investigate Vendors

Who Have “Branded” Them In The Past

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 52

• Suppliers you’ve done business with before

• Suppliers with whom you haven’t had contact, but you’re familiar with them via ads, online promotion, trade show exhibits, newsletters, etc.

• Suppliers you’ve heard of before, but you're not really familiar with them

• Suppliers who offer the products/ equipment you’re seeking, but you’ve never heard of them

Q. When your searches for potential suppliers result in a number of alternative vendors to work with, how likely are you to consider evaluating each of the following types?

• When Searches Result In Many Options:Types Of Suppliers That Are Likely To Be Investigated

Very Sub- Somewhat Not Very Sub-Likely Likely Total Likely Likely TotalTypes Of Suppliers

When Online Searches Result In A Sizable List Of Potential Suppliers,Buyers Are More Likely To Investigate Vendors

Who Have “Branded” Them In The Past

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 53

• Suppliers you’ve done business with before 64% 31% 95% 4% 1% 5%

Q. When your searches for potential suppliers result in a number of alternative vendors to work with, how likely are you to consider evaluating each of the following types?

• When Searches Result In Many Options:Types Of Suppliers That Are Likely To Be Investigated

Very Sub- Somewhat Not Very Sub-Likely Likely Total Likely Likely TotalTypes Of Suppliers

When Online Searches Result In A Sizable List Of Potential Suppliers,Buyers Are More Likely To Investigate Vendors

Who Have “Branded” Them In The Past

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 54

• Suppliers you’ve done business with before 64% 31% 95% 4% 1% 5%

• Suppliers with whom you haven’t had contact, but you’re familiar with them via ads, online promotion, trade show exhibits, newsletters, etc. 14% 52% 66% 31% 3% 34%

Q. When your searches for potential suppliers result in a number of alternative vendors to work with, how likely are you to consider evaluating each of the following types?

• When Searches Result In Many Options:Types Of Suppliers That Are Likely To Be Investigated

Very Sub- Somewhat Not Very Sub-Likely Likely Total Likely Likely TotalTypes Of Suppliers

When Online Searches Result In A Sizable List Of Potential Suppliers,Buyers Are More Likely To Investigate Vendors

Who Have “Branded” Them In The Past

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 55

• Suppliers you’ve done business with before 64% 31% 95% 4% 1% 5%

• Suppliers with whom you haven’t had contact, but you’re familiar with them via ads, online promotion, trade show exhibits, newsletters, etc. 14% 52% 66% 31% 3% 34%

• Suppliers you’ve heard of before, but you're not really familiar with them 6% 29% 35% 50% 15% 65%

Q. When your searches for potential suppliers result in a number of alternative vendors to work with, how likely are you to consider evaluating each of the following types?

• When Searches Result In Many Options:Types Of Suppliers That Are Likely To Be Investigated

Very Sub- Somewhat Not Very Sub-Likely Likely Total Likely Likely TotalTypes Of Suppliers

When Online Searches Result In A Sizable List Of Potential Suppliers,Buyers Are More Likely To Investigate Vendors

Who Have “Branded” Them In The Past

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 56

• Suppliers you’ve done business with before 64% 31% 95% 4% 1% 5%

• Suppliers with whom you haven’t had contact, but you’re familiar with them via ads, online promotion, trade show exhibits, newsletters, etc. 14% 52% 66% 31% 3% 34%

• Suppliers you’ve heard of before, but you're not really familiar with them 6% 29% 35% 50% 15% 65%

• Suppliers who offer the products/ equipment you’re seeking, but you’ve never heard of them 7% 21% 28% 39% 33% 72%

• As marketers seek to maintain brand relationships and differentiate their products, ongoing communications programs are essential:

- Buyers want to have been previously educated via communications programs.

- Suppliers who communicate regularly earn positive impressions among buyers.

- And suppliers who effectively “brand” decision makers via communications programs, are far more likely to be evaluated during the purchasing process ... i.e., far more likely to generate sales leads.

• Therefore, to bring products to market in a more formidable environment, it’s in the supplier’s best interests to invest in marketing programs targeting key buyers.

CONCLUSIONS:

E. How Buyers are BrandedAbout Suppliers, Products and Systems

57

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

F. The Engagementof DecisionMakers with

Today’sArray of Media

58

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

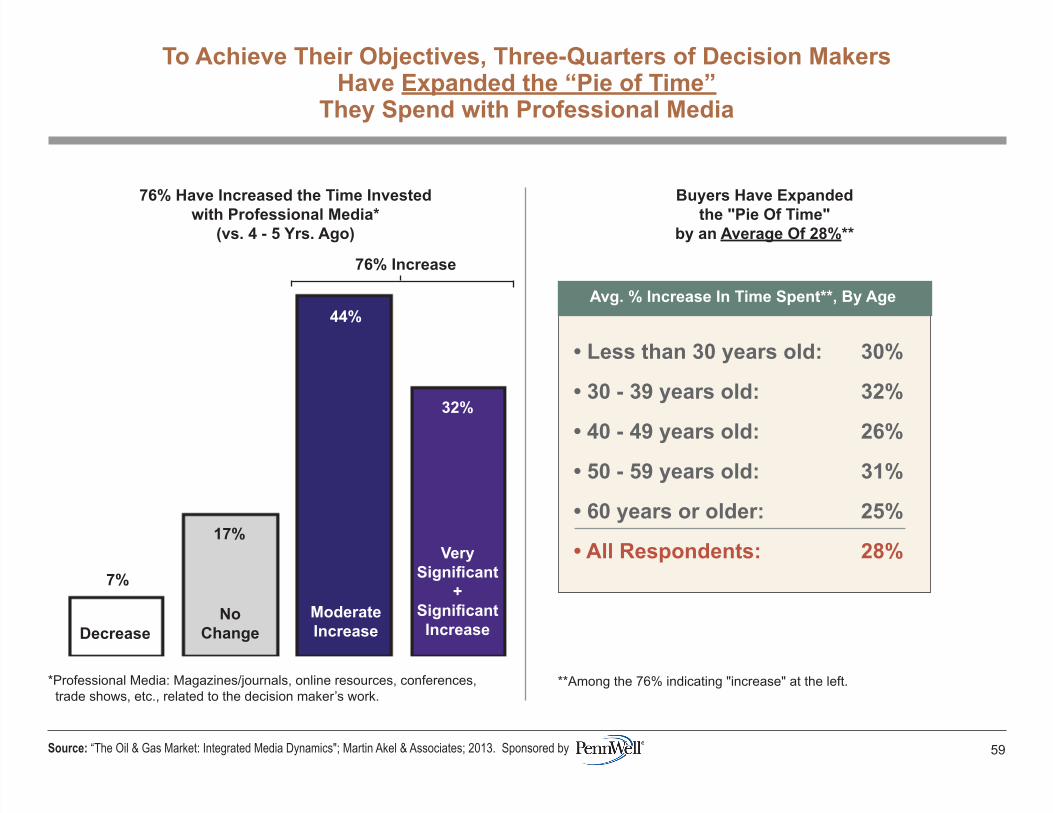

To Achieve Their Objectives, Three-Quarters of Decision MakersHave Expanded the “Pie of Time”

They Spend with Professional Media

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 59

76% Have Increased the Time Investedwith Professional Media*

(vs. 4 - 5 Yrs. Ago)

Avg. % Increase In Time Spent**, By Age

*Professional Media: Magazines/journals, online resources, conferences, trade shows, etc., related to the decision maker’s work.

32%

44%

VerySignificant

+SignificantIncrease

ModerateIncrease

NoChange

17%

Decrease

7%

76% Increase

Buyers Have Expandedthe "Pie Of Time"

by an Average Of 28%**

**Among the 76% indicating "increase" at the left.

• Less than 30 years old: 30%

• 30 - 39 years old: 32%

• 40 - 49 years old: 26%

• 50 - 59 years old: 31%

• 60 years or older: 25%

• All Respondents: 28%

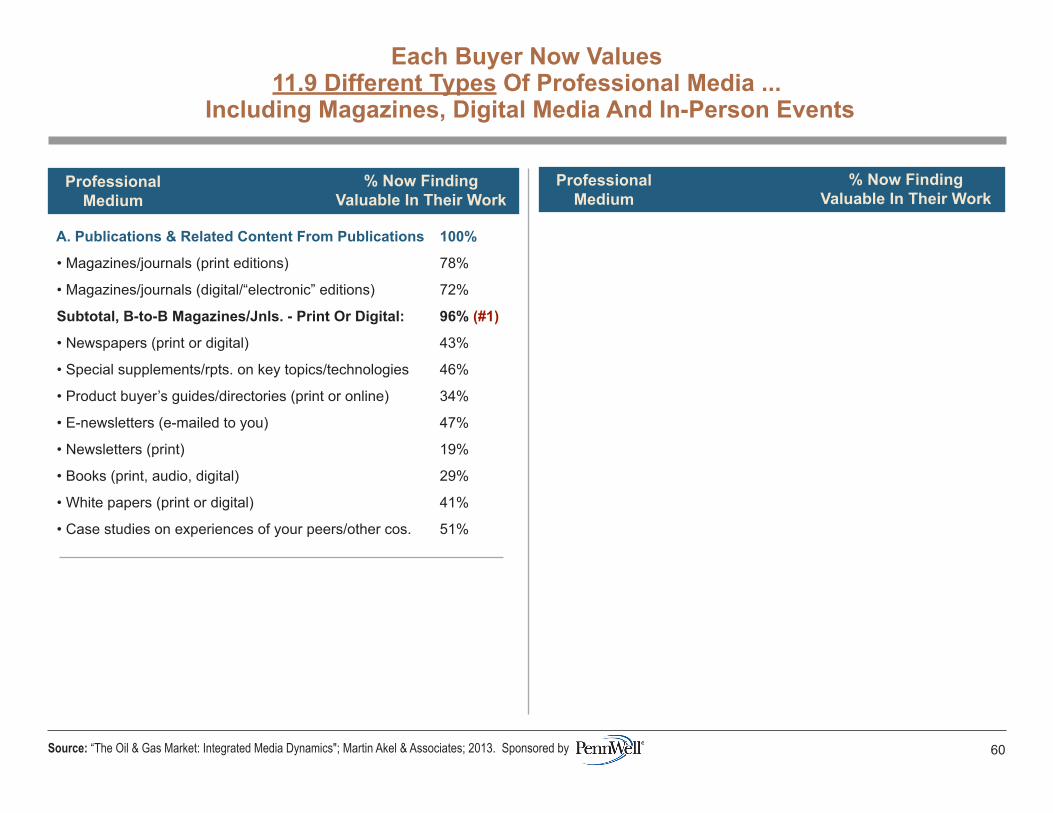

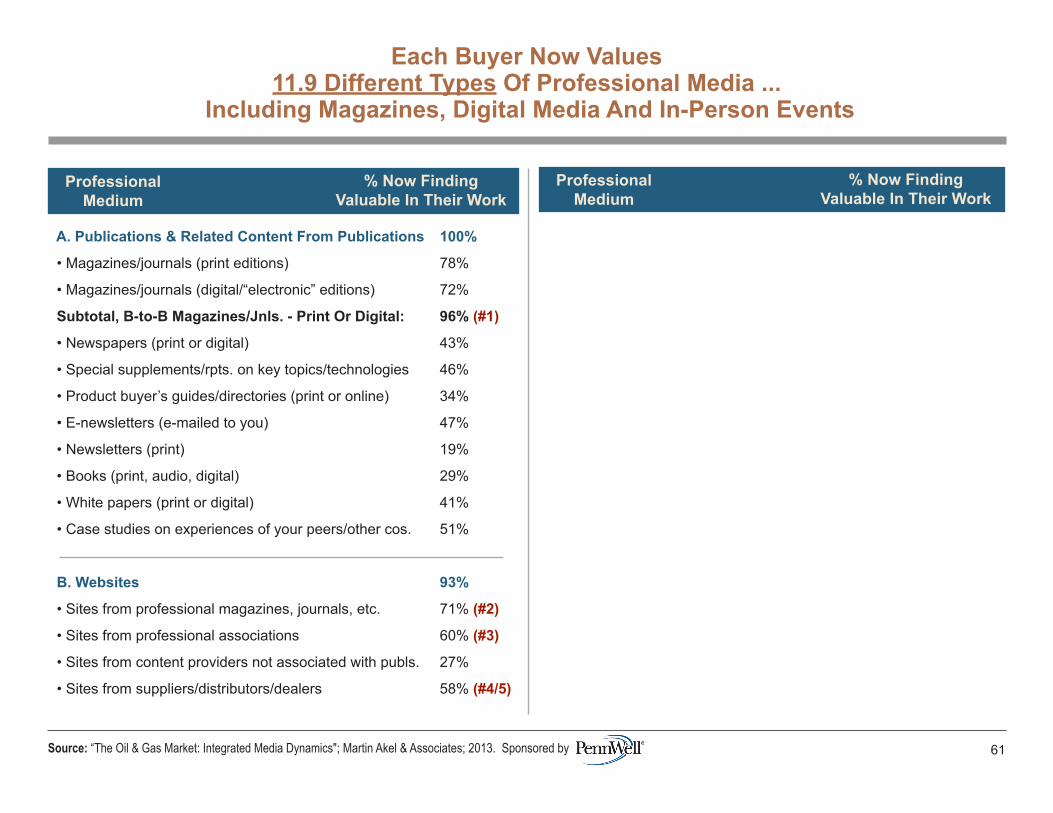

A. Publications & Related Content From Publications 100%

• Magazines/journals (print editions) 78%

• Magazines/journals (digital/“electronic” editions) 72%

Subtotal, B-to-B Magazines/Jnls. - Print Or Digital: 96% (#1)

• Newspapers (print or digital) 43%

• Special supplements/rpts. on key topics/technologies 46%

• Product buyer’s guides/directories (print or online) 34%

• E-newsletters (e-mailed to you) 47%

• Newsletters (print) 19%

• Books (print, audio, digital) 29%

• White papers (print or digital) 41%

• Case studies on experiences of your peers/other cos. 51%

Each Buyer Now Values11.9 Different Types Of Professional Media ...

Including Magazines, Digital Media And In-Person Events

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 60

ProfessionalMedium

% Now FindingValuable In Their Work

ProfessionalMedium

% Now FindingValuable In Their Work

A. Publications & Related Content From Publications 100%

• Magazines/journals (print editions) 78%

• Magazines/journals (digital/“electronic” editions) 72%

Subtotal, B-to-B Magazines/Jnls. - Print Or Digital: 96% (#1)

• Newspapers (print or digital) 43%

• Special supplements/rpts. on key topics/technologies 46%

• Product buyer’s guides/directories (print or online) 34%

• E-newsletters (e-mailed to you) 47%

• Newsletters (print) 19%

• Books (print, audio, digital) 29%

• White papers (print or digital) 41%

• Case studies on experiences of your peers/other cos. 51%

B. Websites 93%

• Sites from professional magazines, journals, etc. 71% (#2)

• Sites from professional associations 60% (#3)

• Sites from content providers not associated with publs. 27%

• Sites from suppliers/distributors/dealers 58% (#4/5)

Each Buyer Now Values11.9 Different Types Of Professional Media ...

Including Magazines, Digital Media And In-Person Events

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 61

ProfessionalMedium

% Now FindingValuable In Their Work

ProfessionalMedium

% Now FindingValuable In Their Work

A. Publications & Related Content From Publications 100%

• Magazines/journals (print editions) 78%

• Magazines/journals (digital/“electronic” editions) 72%

Subtotal, B-to-B Magazines/Jnls. - Print Or Digital: 96% (#1)

• Newspapers (print or digital) 43%

• Special supplements/rpts. on key topics/technologies 46%

• Product buyer’s guides/directories (print or online) 34%

• E-newsletters (e-mailed to you) 47%

• Newsletters (print) 19%

• Books (print, audio, digital) 29%

• White papers (print or digital) 41%

• Case studies on experiences of your peers/other cos. 51%

B. Websites 93%

• Sites from professional magazines, journals, etc. 71% (#2)

• Sites from professional associations 60% (#3)

• Sites from content providers not associated with publs. 27%

• Sites from suppliers/distributors/dealers 58% (#4/5)

Each Buyer Now Values11.9 Different Types Of Professional Media ...

Including Magazines, Digital Media And In-Person Events

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 62

ProfessionalMedium

% Now FindingValuable In Their Work

ProfessionalMedium

% Now FindingValuable In Their Work

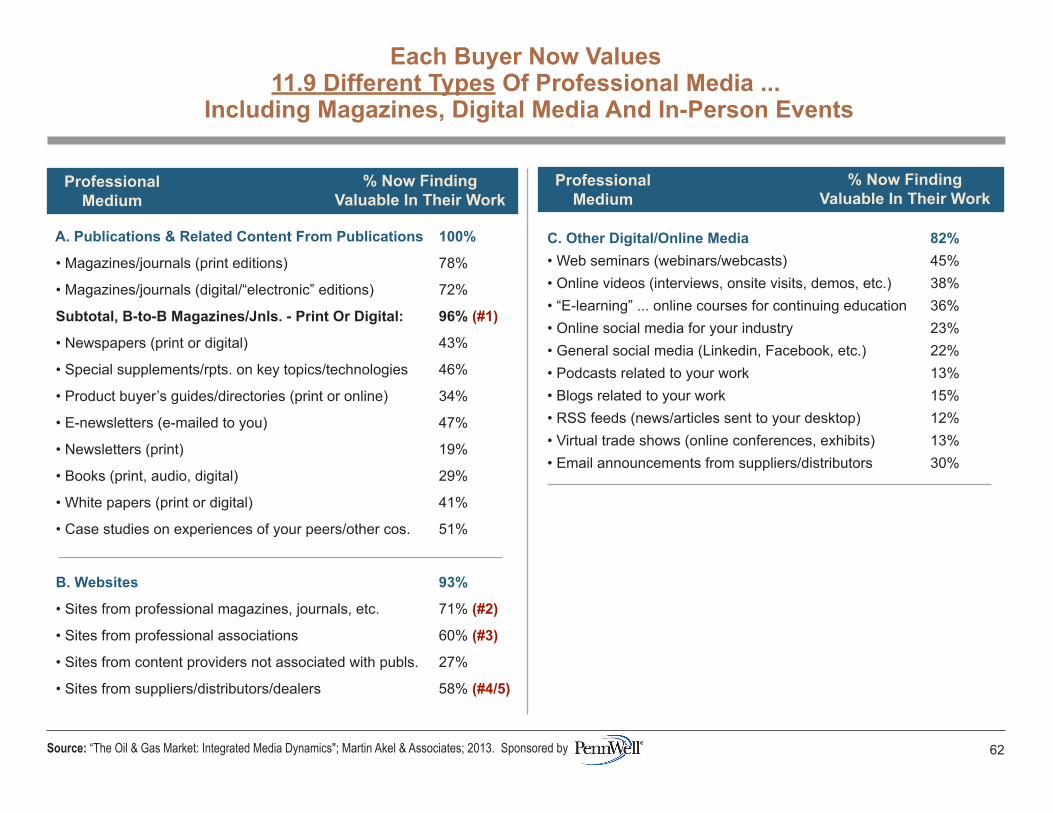

C. Other Digital/Online Media 82%• Web seminars (webinars/webcasts) 45%• Online videos (interviews, onsite visits, demos, etc.) 38%• “E-learning” ... online courses for continuing education 36%• Online social media for your industry 23%• General social media (Linkedin, Facebook, etc.) 22%• Podcasts related to your work 13%• Blogs related to your work 15%• RSS feeds (news/articles sent to your desktop) 12%• Virtual trade shows (online conferences, exhibits) 13%• Email announcements from suppliers/distributors 30%

A. Publications & Related Content From Publications 100%

• Magazines/journals (print editions) 78%

• Magazines/journals (digital/“electronic” editions) 72%

Subtotal, B-to-B Magazines/Jnls. - Print Or Digital: 96% (#1)

• Newspapers (print or digital) 43%

• Special supplements/rpts. on key topics/technologies 46%

• Product buyer’s guides/directories (print or online) 34%

• E-newsletters (e-mailed to you) 47%

• Newsletters (print) 19%

• Books (print, audio, digital) 29%

• White papers (print or digital) 41%

• Case studies on experiences of your peers/other cos. 51%

B. Websites 93%

• Sites from professional magazines, journals, etc. 71% (#2)

• Sites from professional associations 60% (#3)

• Sites from content providers not associated with publs. 27%

• Sites from suppliers/distributors/dealers 58% (#4/5)

Each Buyer Now Values11.9 Different Types Of Professional Media ...

Including Magazines, Digital Media And In-Person Events

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 63

ProfessionalMedium

% Now FindingValuable In Their Work

ProfessionalMedium

% Now FindingValuable In Their Work

C. Other Digital/Online Media 82%• Web seminars (webinars/webcasts) 45%• Online videos (interviews, onsite visits, demos, etc.) 38%• “E-learning” ... online courses for continuing education 36%• Online social media for your industry 23%• General social media (Linkedin, Facebook, etc.) 22%• Podcasts related to your work 13%• Blogs related to your work 15%• RSS feeds (news/articles sent to your desktop) 12%• Virtual trade shows (online conferences, exhibits) 13%• Email announcements from suppliers/distributors 30%

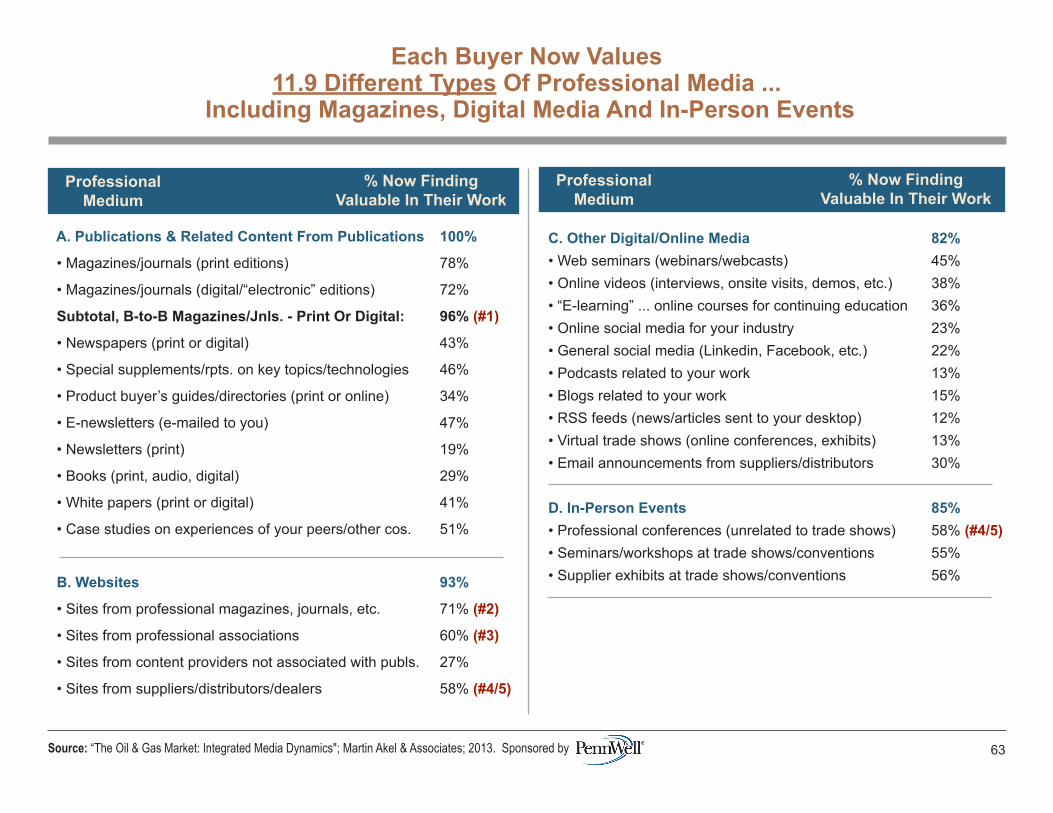

D. In-Person Events 85%• Professional conferences (unrelated to trade shows) 58% (#4/5)• Seminars/workshops at trade shows/conventions 55%• Supplier exhibits at trade shows/conventions 56%

A. Publications & Related Content From Publications 100%

• Magazines/journals (print editions) 78%

• Magazines/journals (digital/“electronic” editions) 72%

Subtotal, B-to-B Magazines/Jnls. - Print Or Digital: 96% (#1)

• Newspapers (print or digital) 43%

• Special supplements/rpts. on key topics/technologies 46%

• Product buyer’s guides/directories (print or online) 34%

• E-newsletters (e-mailed to you) 47%

• Newsletters (print) 19%

• Books (print, audio, digital) 29%

• White papers (print or digital) 41%

• Case studies on experiences of your peers/other cos. 51%

B. Websites 93%

• Sites from professional magazines, journals, etc. 71% (#2)

• Sites from professional associations 60% (#3)

• Sites from content providers not associated with publs. 27%

• Sites from suppliers/distributors/dealers 58% (#4/5)

Each Buyer Now Values11.9 Different Types Of Professional Media ...

Including Magazines, Digital Media And In-Person Events

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 64

ProfessionalMedium

% Now FindingValuable In Their Work

ProfessionalMedium

% Now FindingValuable In Their Work

C. Other Digital/Online Media 82%• Web seminars (webinars/webcasts) 45%• Online videos (interviews, onsite visits, demos, etc.) 38%• “E-learning” ... online courses for continuing education 36%• Online social media for your industry 23%• General social media (Linkedin, Facebook, etc.) 22%• Podcasts related to your work 13%• Blogs related to your work 15%• RSS feeds (news/articles sent to your desktop) 12%• Virtual trade shows (online conferences, exhibits) 13%• Email announcements from suppliers/distributors 30%

D. In-Person Events 85%• Professional conferences (unrelated to trade shows) 58% (#4/5)• Seminars/workshops at trade shows/conventions 55%• Supplier exhibits at trade shows/conventions 56%

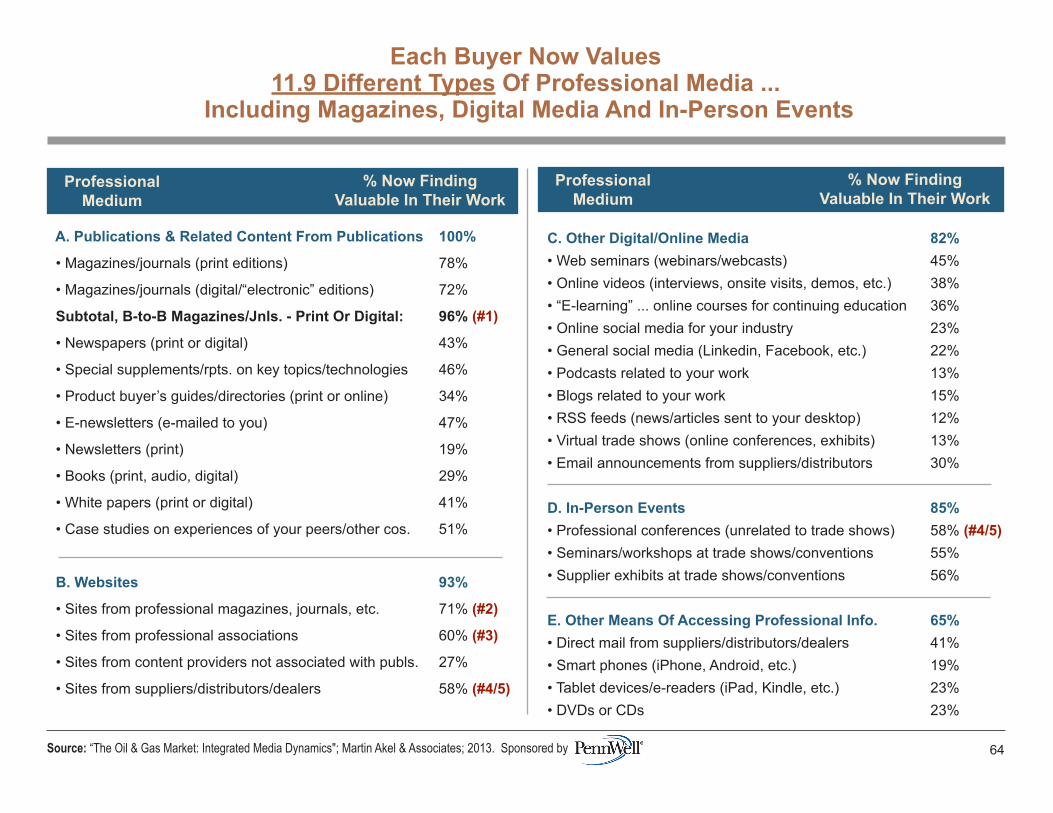

E. Other Means Of Accessing Professional Info. 65%• Direct mail from suppliers/distributors/dealers 41%• Smart phones (iPhone, Android, etc.) 19%• Tablet devices/e-readers (iPad, Kindle, etc.) 23%• DVDs or CDs 23%

Average Number of Typesof Media Valued - by Age

• Less than 30 years old: 11.2

• 30 - 39 years old: 11.5

• 40 - 49 years old: 12.4

• 50 - 59 years old: 12.1

• 60 years or older: 12.0

• All Respondents: 11.9

Each Buyer Now Values11.9 Different Types Of Professional Media ...

Including Magazines, Digital Media And In-Person Events

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 65

• Buyers have expanded the time they spend with professional information ... and are now engaged with an average of 11.9 different media.

• They have not abandoned “traditional” media. In fact 96% read professional magazines.

• Therefore, as marketer’s seek to move products through the brand adoption process, it’s in their best interests to utilize the full range of media ... constructing a mix that includes

publications, digital and face-to-face events.

CONCLUSIONS:

F. The Engagement of Decision Makerswith Today’s Array of Media

66

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

G. The Degree to Which Buyers

are Engaged withProfessionalPublications

67

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

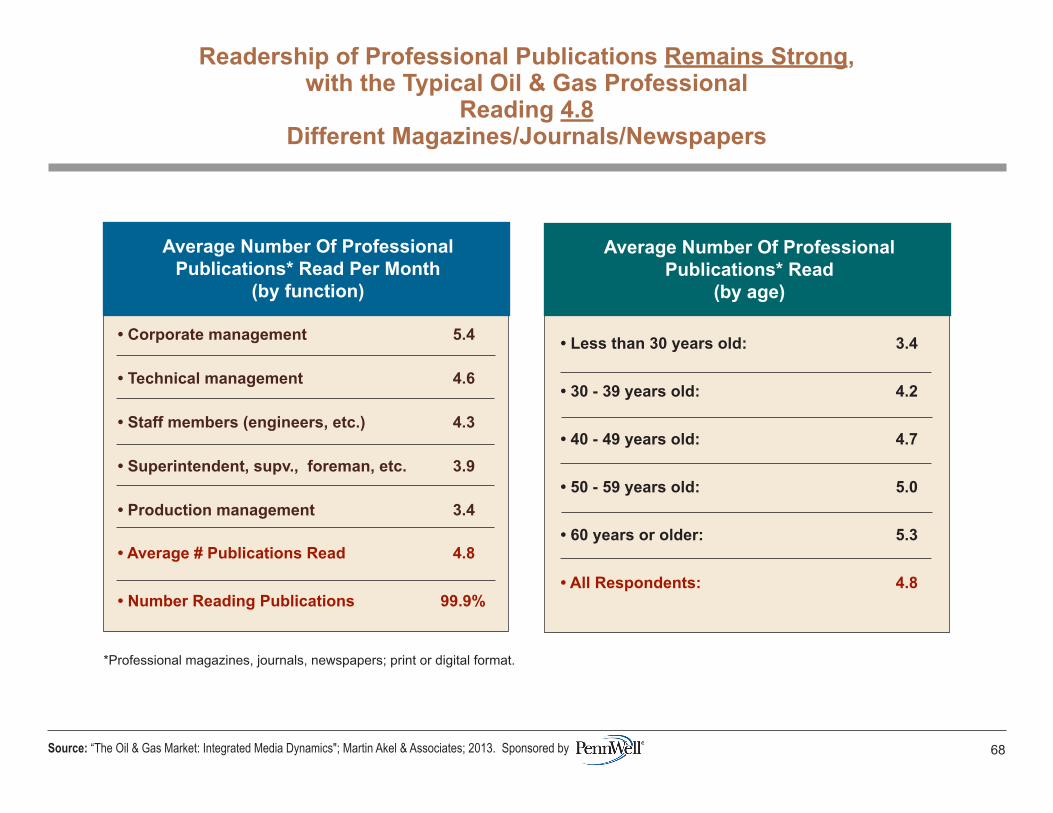

Readership of Professional Publications Remains Strong,with the Typical Oil & Gas Professional

Reading 4.8Different Magazines/Journals/Newspapers

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 68

• Corporate management 5.4

• Technical management 4.6

• Staff members (engineers, etc.) 4.3

• Superintendent, supv., foreman, etc. 3.9

• Production management 3.4

• Average # Publications Read 4.8

• Number Reading Publications 99.9%

Average Number Of ProfessionalPublications* Read Per Month

(by function)

*Professional magazines, journals, newspapers; print or digital format.

Average Number Of ProfessionalPublications* Read

(by age)

• Less than 30 years old: 3.4

• 30 - 39 years old: 4.2

• 40 - 49 years old: 4.7

• 50 - 59 years old: 5.0

• 60 years or older: 5.3

• All Respondents: 4.8

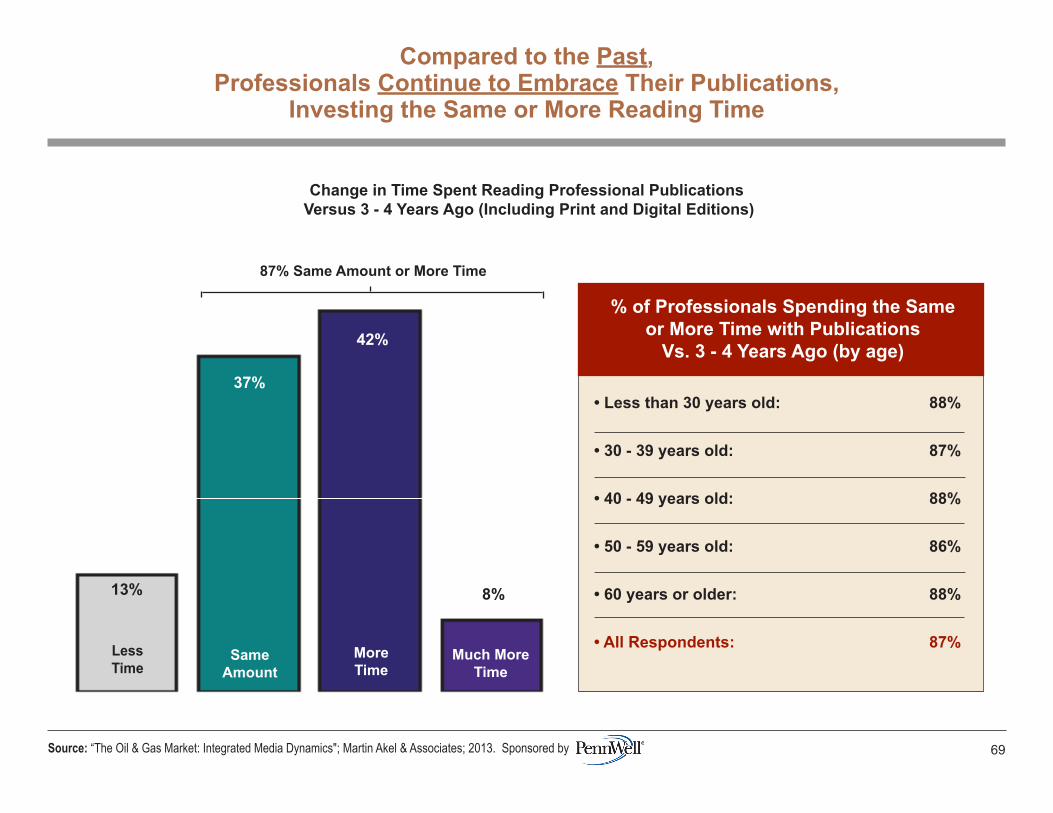

Change in Time Spent Reading Professional Publications Versus 3 - 4 Years Ago (Including Print and Digital Editions)

87% Same Amount or More Time

8%

SameAmount

MoreTime

LessTime

13%

Much MoreTime

Compared to the Past,Professionals Continue to Embrace Their Publications,

Investing the Same or More Reading Time

42%

37%

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 69

% of Professionals Spending the Sameor More Time with Publications

Vs. 3 - 4 Years Ago (by age)

• Less than 30 years old: 88%

• 30 - 39 years old: 87%

• 40 - 49 years old: 88%

• 50 - 59 years old: 86%

• 60 years or older: 88%

• All Respondents: 87%

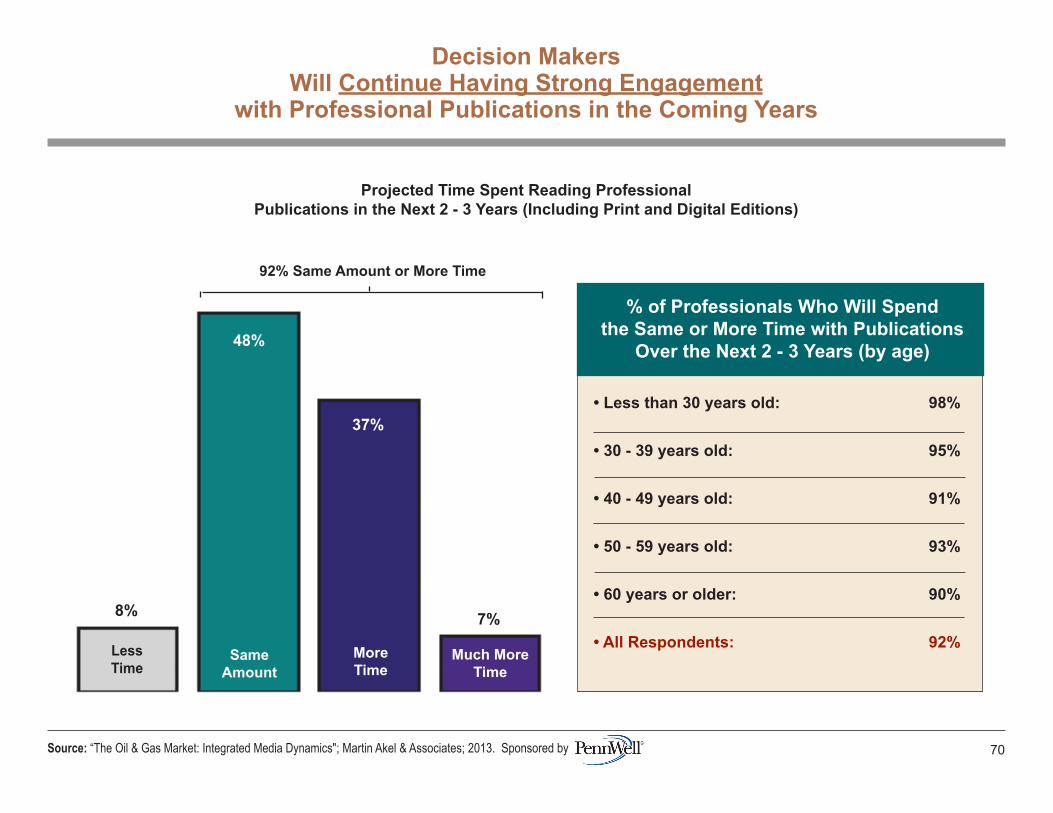

Projected Time Spent Reading ProfessionalPublications in the Next 2 - 3 Years (Including Print and Digital Editions)

92% Same Amount or More Time

7%

SameAmount

MoreTime

LessTime

8%

Much MoreTime

Decision MakersWill Continue Having Strong Engagement

with Professional Publications in the Coming Years

37%

48%

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 70

% of Professionals Who Will Spendthe Same or More Time with Publications

Over the Next 2 - 3 Years (by age)

• Less than 30 years old: 98%

• 30 - 39 years old: 95%

• 40 - 49 years old: 91%

• 50 - 59 years old: 93%

• 60 years or older: 90%

• All Respondents: 92%

I spend a lot of time on a computer; print is a welcome change 61%

They’re portable; can read them at work, at home, in transit, etc. 60%

They’re tangible; I enjoy physically thumbing through them 55%

They’re convenient; I can reach for and get into them quickly 53%

They’re are a reliable way to be updated periodically 49%

They’re very visual, bringing information to life 47%

They offer random access; I can quickly flip to any article 44%

It’s easy to save for reference; can remove articles/ads 36%

I can write notes on them, highlight items, etc. 36%

Not desirable 9%

Nine of Ten ProfessionalsContinue to Read Print Publications ...

for a Wide Range of Reasons

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 71

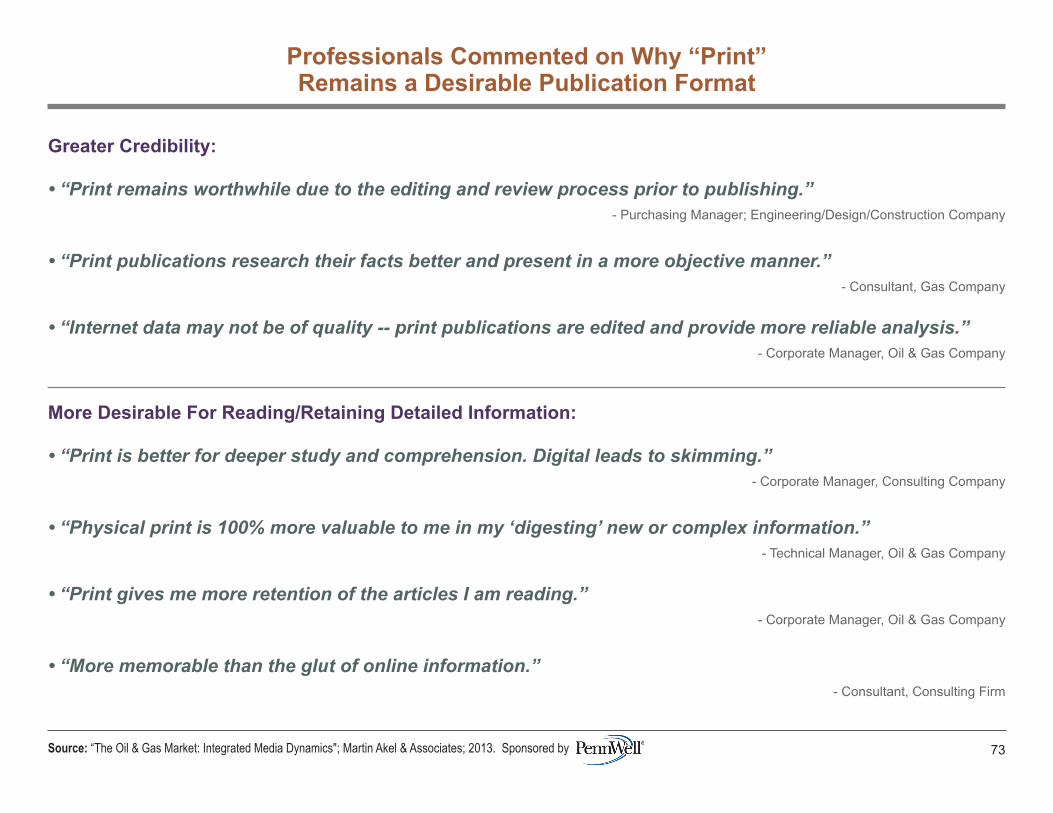

Print Publicationsare Desirable:

• 91%

Professionals Commented on Why “Print”Remains a Desirable Publication Format

Tangibility:

• “They are a tangible thing in our digital age. Everything is digital now, print is a nice change.”- Superintendent, Supervisor, Foreman, Oil & Gas Company

• “I prefer the tactile experience of thumbing through the pages. It feels less like work.”- Superintendent, Supervisor, Foreman, Oil & Gas Company

• “It is nice to touch something.”- Superintendent, Supervisor, Foreman, Oil & Gas Company

A Welcome Alternative To Computers:

• “I receive so much electronic information. Would rather get away from reading on a screen.”- Engineer/Geologist/Geophysicist, Engineering/Design/Construction Company

• “Need a rest from a computer screen, easier to pick out relevant detail.”- Corporate Manager, Oil & Gas Company

• “Print publications are a welcome change from the computer and are portable.”- Consultant; Contractor

• “Print remains worthwhile because digital versions are often a pain to read.”- Consultant, Consulting Firm

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 72

Professionals Commented on Why “Print”Remains a Desirable Publication Format

Greater Credibility:

• “Print remains worthwhile due to the editing and review process prior to publishing.”- Purchasing Manager; Engineering/Design/Construction Company

• “Print publications research their facts better and present in a more objective manner.”- Consultant, Gas Company

• “Internet data may not be of quality -- print publications are edited and provide more reliable analysis.”- Corporate Manager, Oil & Gas Company

More Desirable For Reading/Retaining Detailed Information:

• “Print is better for deeper study and comprehension. Digital leads to skimming.”- Corporate Manager, Consulting Company

• “Physical print is 100% more valuable to me in my ‘digesting’ new or complex information.”- Technical Manager, Oil & Gas Company

• “Print gives me more retention of the articles I am reading.”- Corporate Manager, Oil & Gas Company

• “More memorable than the glut of online information.”- Consultant, Consulting Firm

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 73

Alerts me to potential solutions (products/systems/services) 77%

Alerts me to new suppliers in the market 66%

Helps position individual suppliers in my mind 57%

Alerts me to changes at suppliers 53%

Provides information to request/access more details 48%

Offers continuing education on technologies 47%

Time is short; it’s a quick way to stay current 35%

Do not look at ads 6%

Professionals Continue to Embrace Magazine Advertisingas a Way to Discover

Technological Solutions and Which Suppliers to Contact

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 74

After purchasing, keeps me up-to-date on the supplier 24%

Value MagazineAdvertisements:

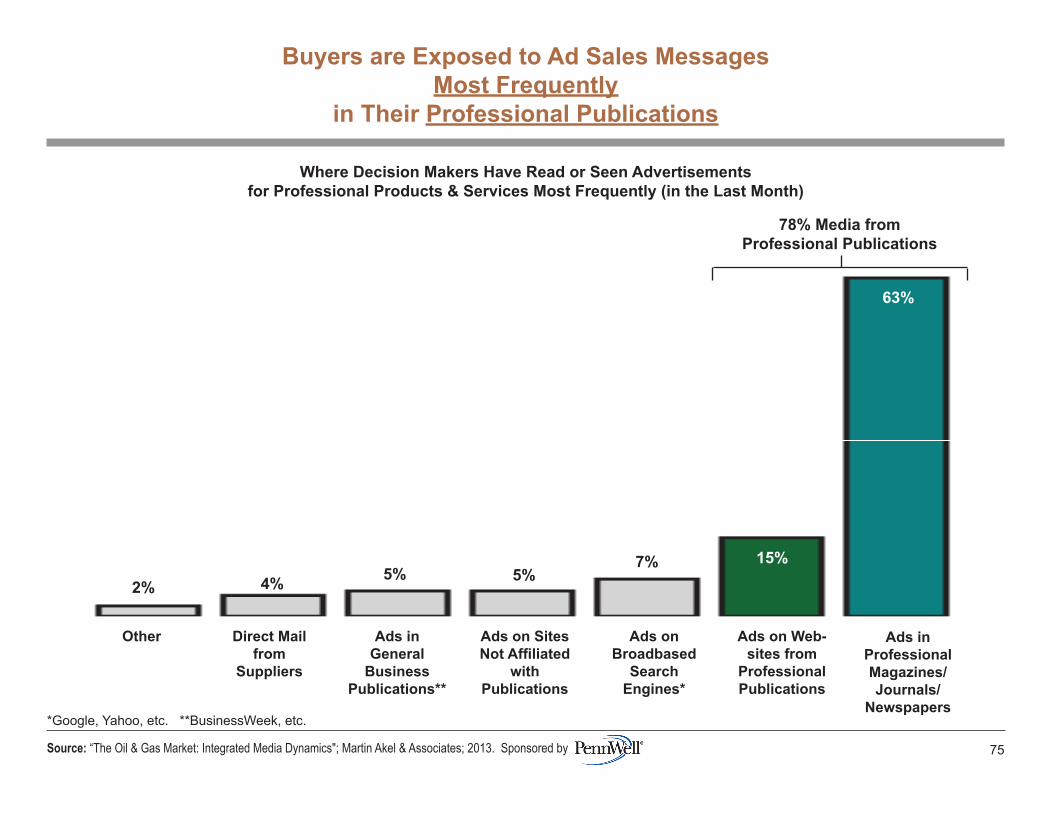

• 94%

Buyers are Exposed to Ad Sales MessagesMost Frequently

in Their Professional Publications

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 75

78% Media fromProfessional Publications

Ads inProfessional Magazines/Journals/

Newspapers

Ads on Web-sites from

Professional Publications

Direct Mail from

Suppliers

Ads onBroadbased

SearchEngines*

Ads on Sites Not Affiliated

withPublications

Ads inGeneral

BusinessPublications**

Other

*Google, Yahoo, etc. **BusinessWeek, etc.

63%

15%7%4% 5%5%

2%

Where Decision Makers Have Read or Seen Advertisementsfor Professional Products & Services Most Frequently (in the Last Month)

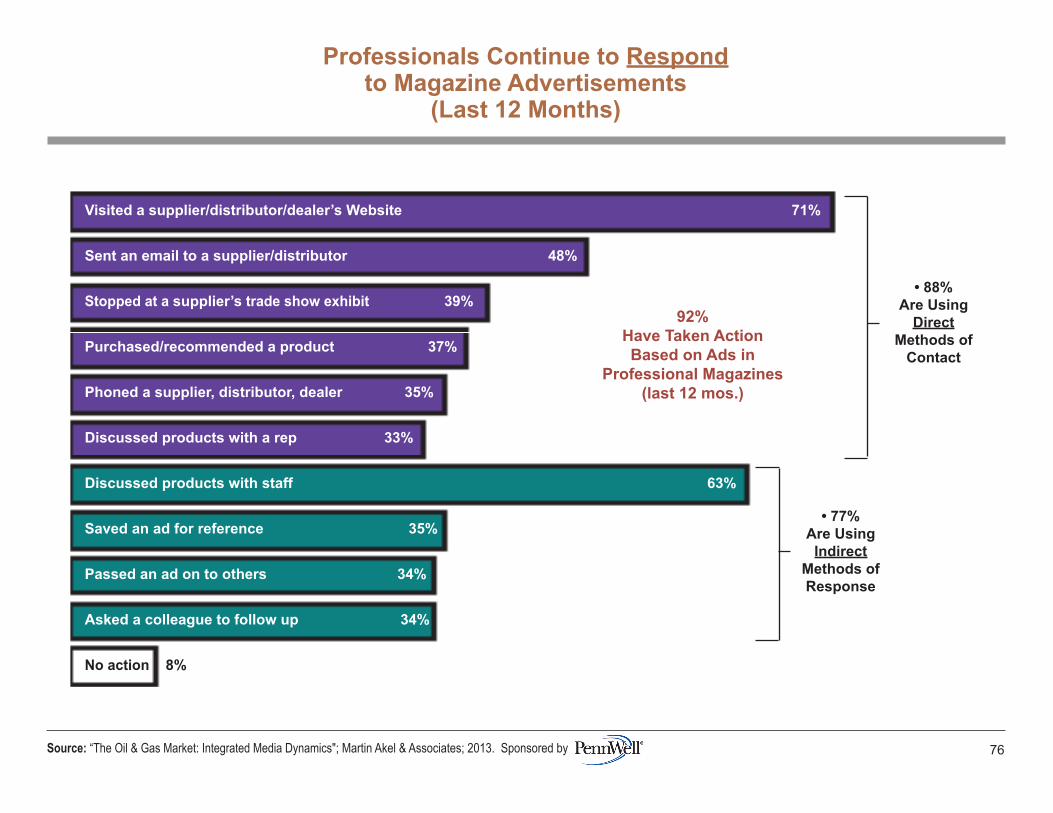

Visited a supplier/distributor/dealer’s Website 71%

Sent an email to a supplier/distributor 48%

Stopped at a supplier’s trade show exhibit 39%

Purchased/recommended a product 37%

Phoned a supplier, distributor, dealer 35%

Discussed products with a rep 33%

Discussed products with staff 63%

Saved an ad for reference 35%

Passed an ad on to others 34%

Asked a colleague to follow up 34%

No action 8%

Professionals Continue to Respondto Magazine Advertisements

(Last 12 Months)

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 76

• 88%Are Using

DirectMethods of

Contact

• 77%Are UsingIndirect

Methods ofResponse

92%Have Taken ActionBased on Ads in

Professional Magazines(last 12 mos.)

Given Their Needs for New Technology,the Level of Response to Publication Advertising

Remains Strong

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 77

Change in Professionals’ Overall Response to Ads in Professional Publications(Versus 4 - 5 Years Ago)

4%Respond Much More

Frequently

97% Responding with the Same or Greater Frequency

Respond MoreFrequently

45%

No Change

48%

3%Respond Less

Frequently

• Virtually all professionals continue reading their magazines and journals ... including those in print format. Readership into the future will remain strong.

• Decision makers also value magazine advertising content and continue to respond to ads.

• Therefore -- despite the opinions of some marketers, magazine advertising remains a highly effective medium for moving buyers through the brand adoption process.

CONCLUSIONS:

G. The Degree to Which Buyers are Engaged withProfessional Publications

78

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

H. Trends inEngagement

with Event andDigital Media

79

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

79

Both Event and Digital MediaWill Experience Substantial Growth

within the Oil & Gas Market

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 80

Significant Sub- No Significant Sub- Increase Increase Total Change Decrease Decrease Total

Change in Usage/Readership:Next 2 - 3 Years

(continued)

a. In-Person Event Media

• Supplier exhibits at trade shows 7% 32% 39% 52% 8% 2% 10%

• In-person conferences 6% 33% 39% 51% 9% 1% 10%

b. Digital Media

• Websites from publications; other industry-related portals 13% 46% 59% 40% 1% 0% 1%

• White papers on new technology 9% 42% 51% 45% 3% 1% 4%

• Webinars/webcasts 9% 39% 48% 46% 5% 1% 6%

• Online videos 8% 40% 48% 46% 5% 1% 6%

Significant Sub- No Significant Sub- Increase Increase Total Change Decrease Decrease Total

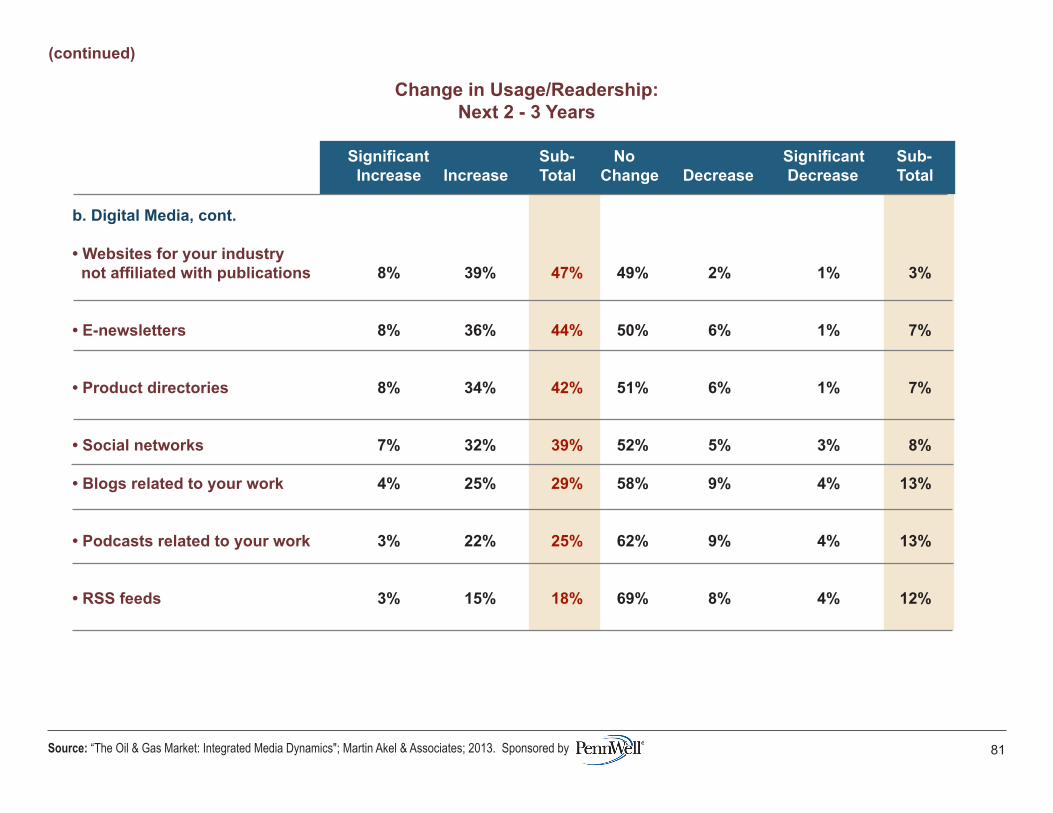

(continued)

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 81

Change in Usage/Readership:Next 2 - 3 Years

b. Digital Media, cont.

• Websites for your industry not affiliated with publications 8% 39% 47% 49% 2% 1% 3%

• E-newsletters 8% 36% 44% 50% 6% 1% 7%

• Product directories 8% 34% 42% 51% 6% 1% 7%

• Social networks 7% 32% 39% 52% 5% 3% 8%

• Blogs related to your work 4% 25% 29% 58% 9% 4% 13%

• Podcasts related to your work 3% 22% 25% 62% 9% 4% 13%

• RSS feeds 3% 15% 18% 69% 8% 4% 12%

• Event and digital media will be increasingly embraced by industry professionals.

• Therefore, marketers can select from a range of digital and event media to complement other components in their marketing program.

• However, as they structure their programs, it’s important for marketers to understand the roles of different media in the product adoption process (see the next section).

CONCLUSIONS:

H. Trends in Engagementwith Event and Digital Media

82

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

I. TheComplementary

Rolesof Different Media

in the ProductAdoption Process

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

83

• Articles and ads in your professional publications (print and/or digital) 57% 66% 2.4

• Websites from professional publications 10% 35% 3.9

• Search results from broadbased search engines (Google, Yahoo, etc.) 8% 15% 4.7

• Sales reps from suppliers/distributors/dealers 5% 9% 5.1

• Conferences (in-person) 5% 16% 4.7

• Trade show exhibits (in-person or “virtual”) 4% 12% 4.7

• Websites from suppliers/distributors/dealers 4% 16% 4.5

• E-newsletters 4% 13% 4.9

• Websites for your field not affiliated with publications 2% 9% 5.2

• Direct mail from suppliers 1% 4% 5.6

• Product directories, buyer’s guides, etc. (hardcopy or online) 1% 5% 5.4

% Mentioning % Mentioning Average As #1 As #1 Or 2 Score*

Where Buyers are Initially Branded(Respondents Ranked Top 5 Media)

Medium

*The closer to “1.0”, the more the medium is likely to be the one where respondents first become aware of products and suppliers.

Where BuyersFirst Become Aware of and Form Impressions

About New Products and Suppliers ...

Top 5 Resources Where Decision Makers First Become Aware of and Form ImpressionsAbout Most New Products and Suppliers for the Oil & Gas Industry

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 84

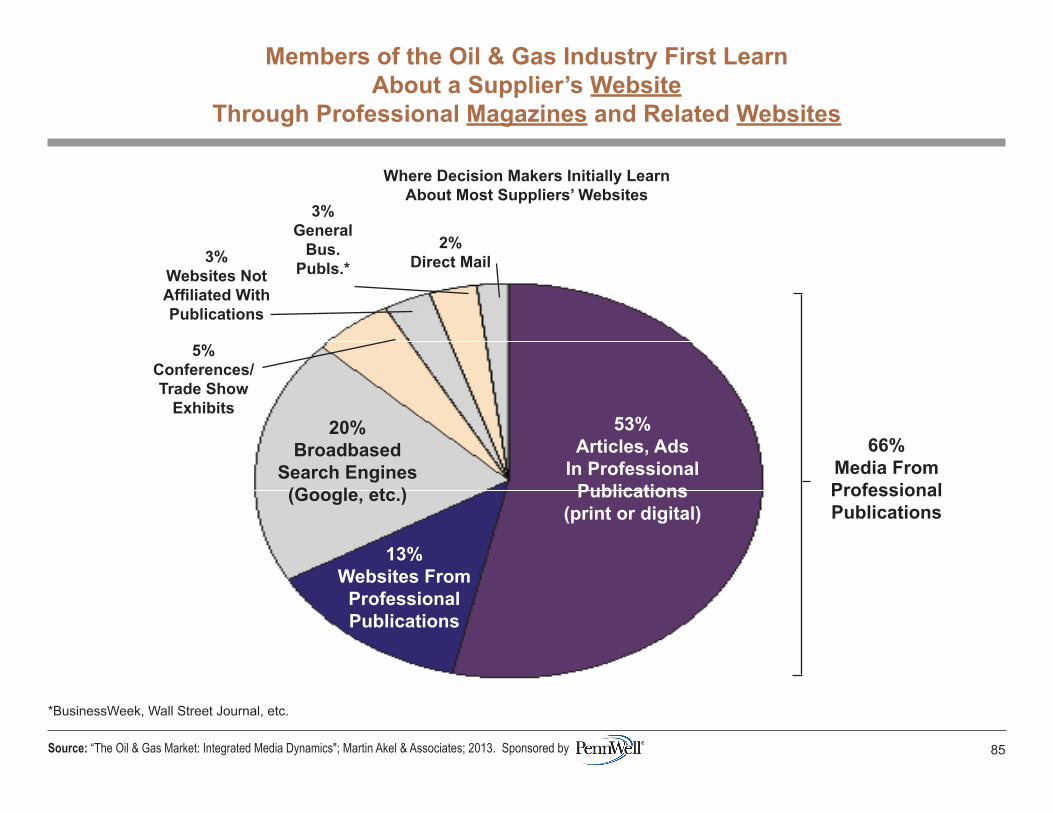

53%Articles, Ads

In ProfessionalPublications

(print or digital)

20%Broadbased

Search Engines(Google, etc.)

13%Websites From

ProfessionalPublications

3%Websites NotAffiliated WithPublications

66%Media FromProfessionalPublications

5%Conferences/Trade Show

Exhibits

3%General

Bus.Publs.*

2%Direct Mail

Members of the Oil & Gas Industry First LearnAbout a Supplier’s Website

Through Professional Magazines and Related Websites

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 85

Where Decision Makers Initially LearnAbout Most Suppliers’ Websites

*BusinessWeek, Wall Street Journal, etc.

86

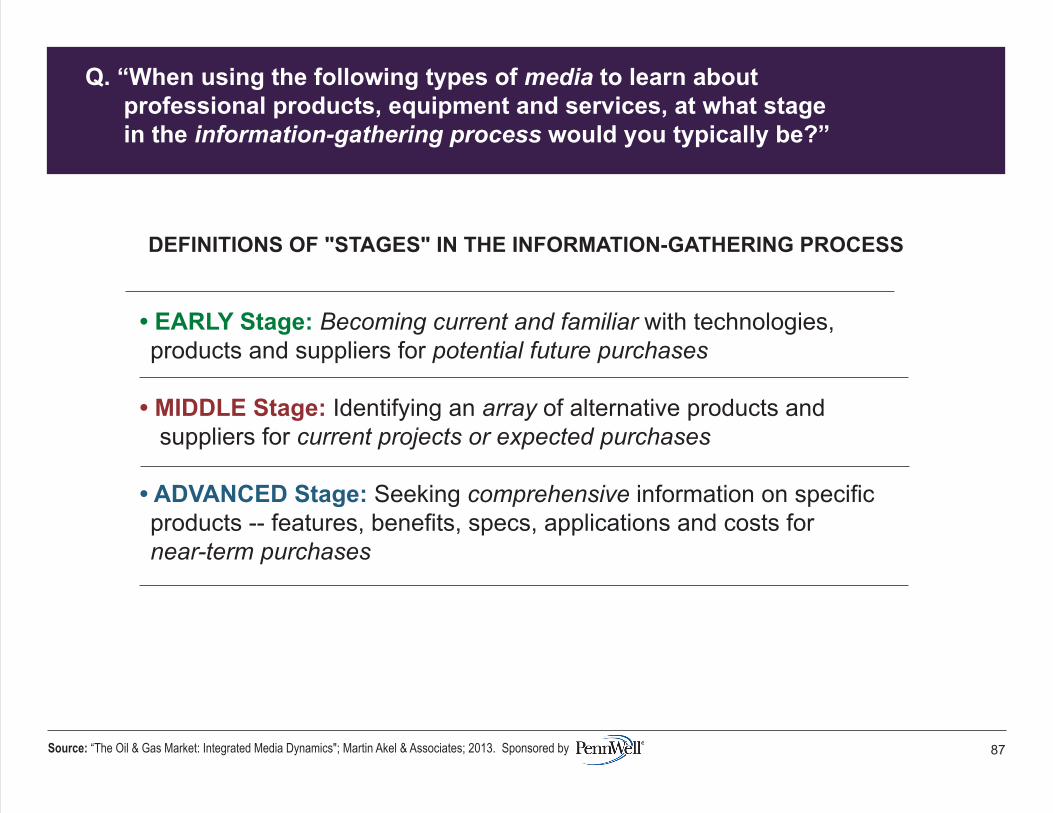

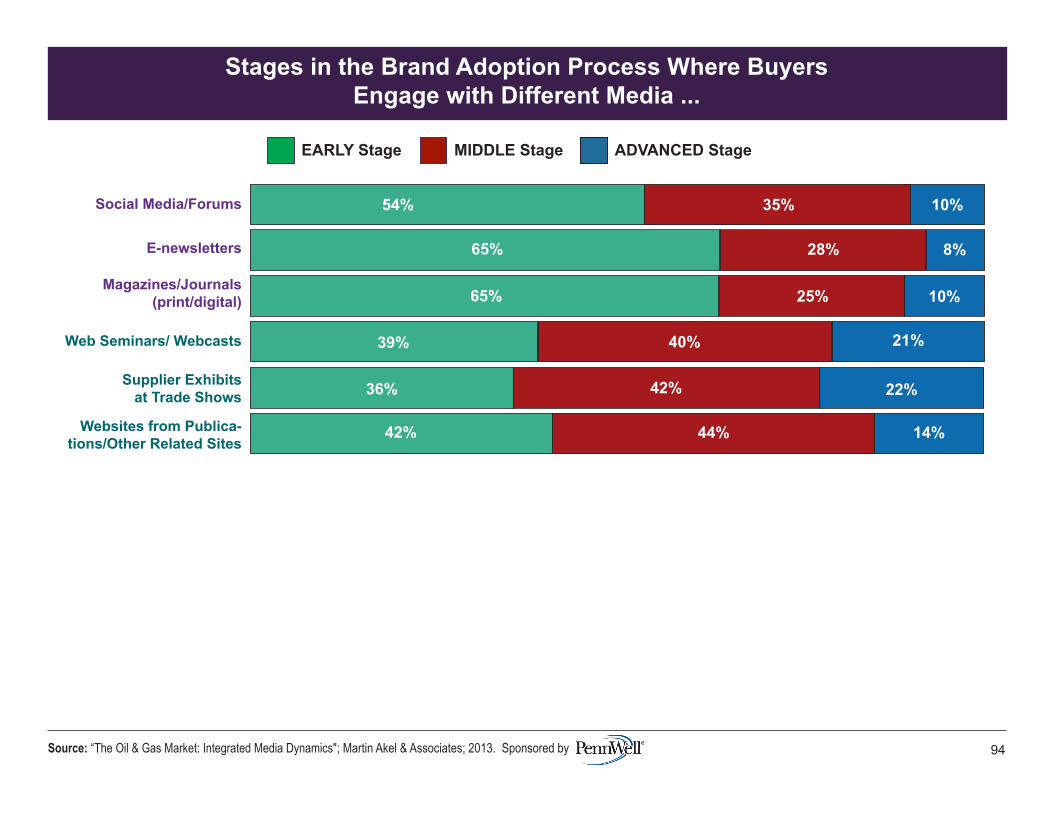

Stages in theBrand Adoption ProcessWhere Buyers Engagewith Different Media ...

DEFINITIONS OF "STAGES" IN THE INFORMATION-GATHERING PROCESS

• EARLY Stage: Becoming current and familiar with technologies, products and suppliers for potential future purchases

• MIDDLE Stage: Identifying an array of alternative products and suppliers for current projects or expected purchases

• ADVANCED Stage: Seeking comprehensive information on specific products -- features, benefits, specs, applications and costs for

near-term purchases

Q. “When using the following types of media to learn about professional products, equipment and services, at what stage in the information-gathering process would you typically be?”

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 87

*Those containing technology-related articles and news, buyer’s guides, product reviews, etc.

ProfessionalMedia

1. Buyer’s Guides/Directories (print/digital)

2. E-Newsletters

3. Face-To-Face Conferences/Seminars

4. Magazines/Journals/Newspapers (print & digital)

5. Online Community Groups/Social Media/Forums

6. Online Videos About Technologies/Products

7. Supplier Exhibits At Trade Shows

8. Web Seminars/Webcasts

9. Websites from Publications/Other Industry-Related Sites*

10. Websites from Specific Suppliers

11. White Papers/Case Histories/Reports on New Technology

EARLY MIDDLE ADVANCED Stage Stage Stage

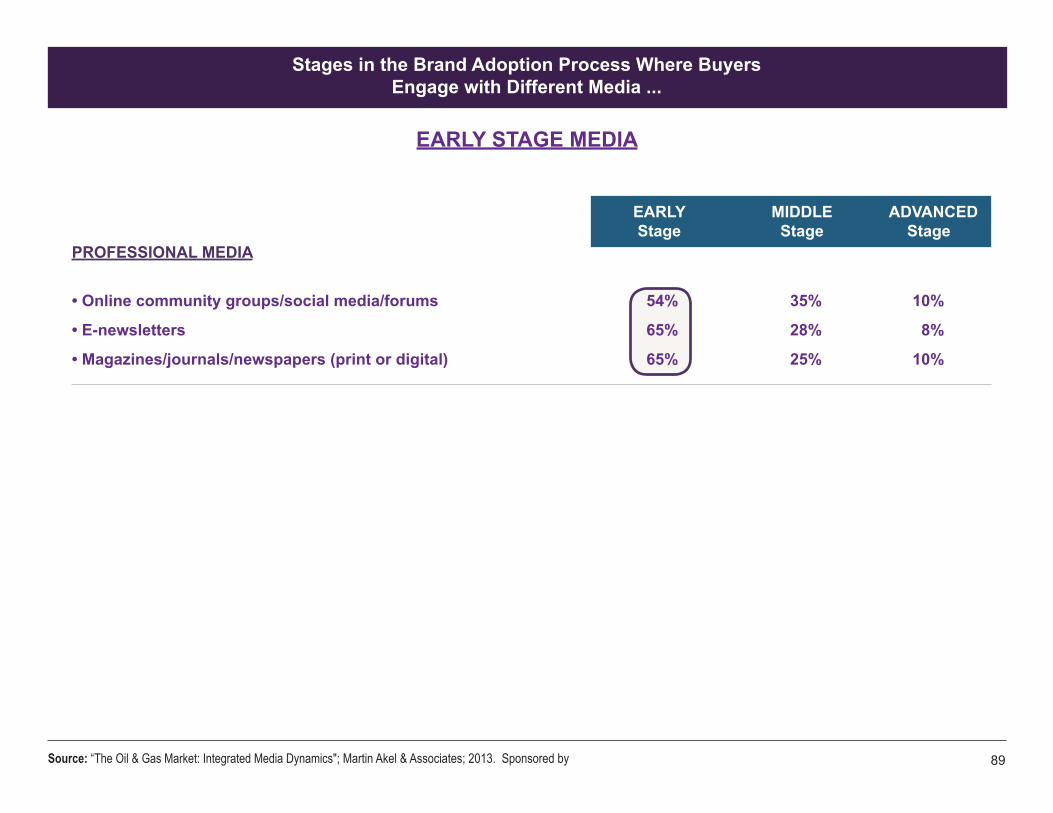

Stages in the Brand Adoption Process Where BuyersEngage with Different Media ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 88

Stages in the Brand Adoption Process Where BuyersEngage with Different Media ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by

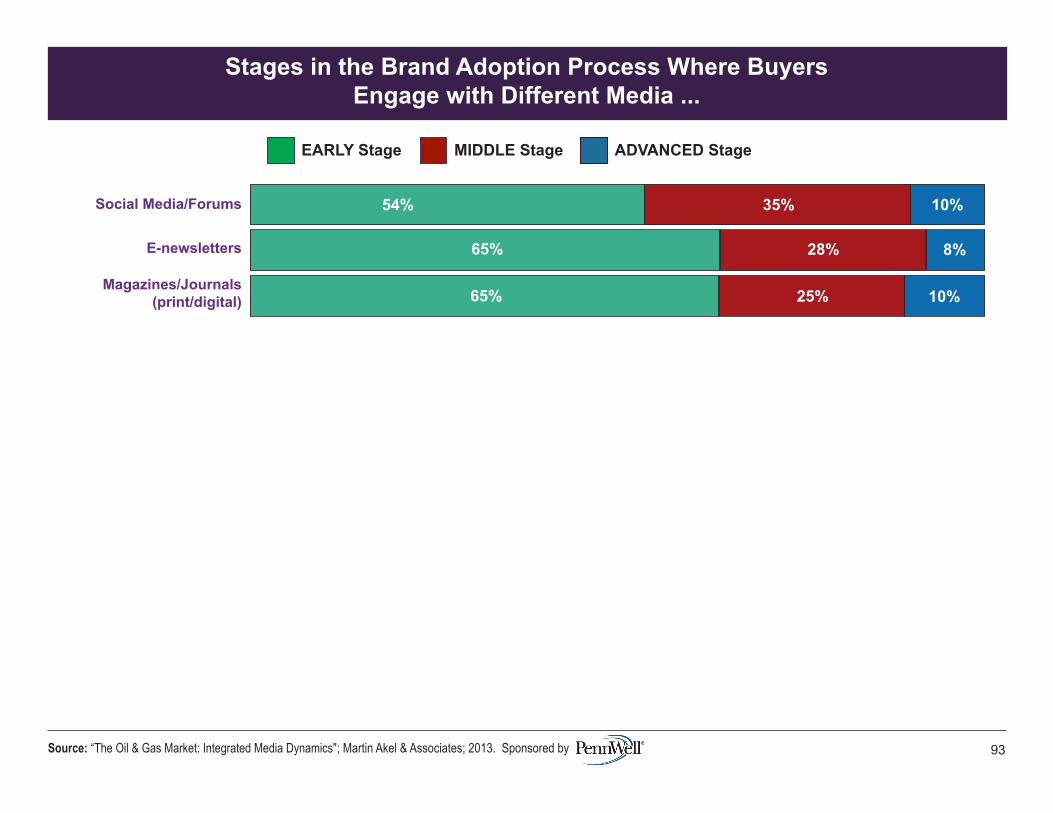

EARLY STAGE MEDIA

EARLY MIDDLE ADVANCED Stage Stage Stage

PROFESSIONAL MEDIA

• Online community groups/social media/forums 54% 35% 10%

• E-newsletters 65% 28% 8%

• Magazines/journals/newspapers (print or digital) 65% 25% 10%

89

Stages in the Brand Adoption Process Where BuyersEngage with Different Media ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by

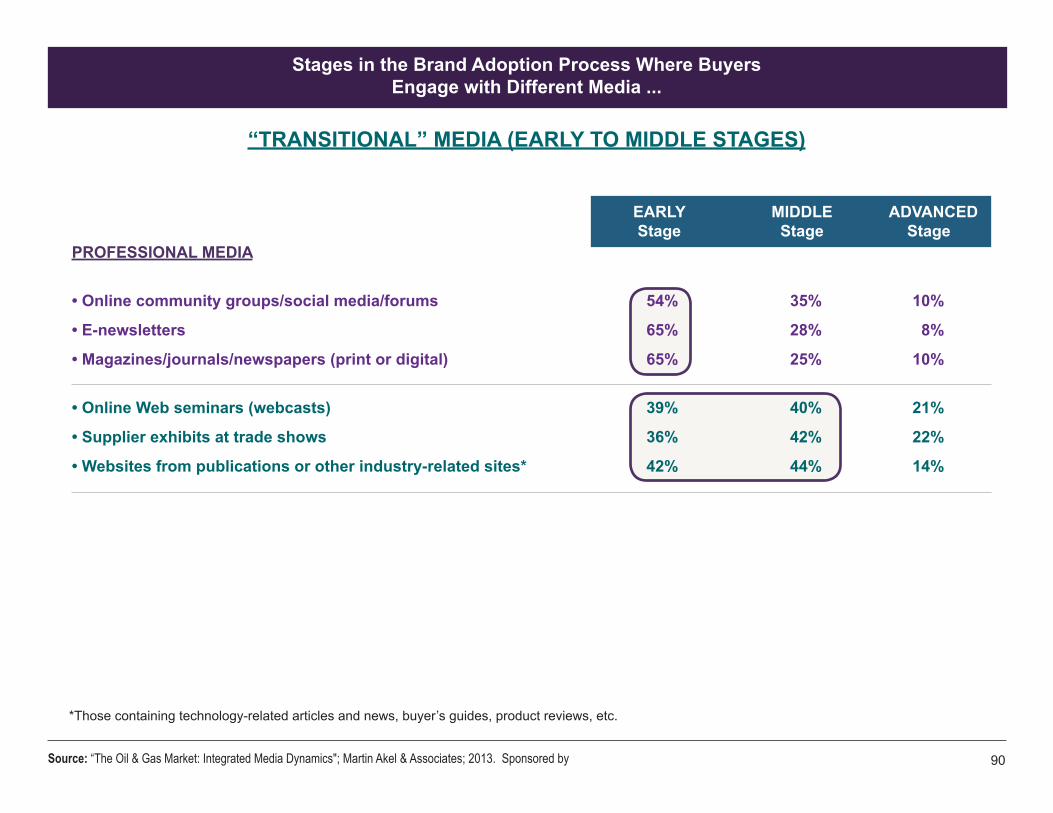

“TRANSITIONAL” MEDIA (EARLY TO MIDDLE STAGES)

EARLY MIDDLE ADVANCED Stage Stage Stage

*Those containing technology-related articles and news, buyer’s guides, product reviews, etc.

PROFESSIONAL MEDIA

• Online community groups/social media/forums 54% 35% 10%

• E-newsletters 65% 28% 8%

• Magazines/journals/newspapers (print or digital) 65% 25% 10%

• Online Web seminars (webcasts) 39% 40% 21%

• Supplier exhibits at trade shows 36% 42% 22%

• Websites from publications or other industry-related sites* 42% 44% 14%

90

Stages in the Brand Adoption Process Where BuyersEngage with Different Media ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by

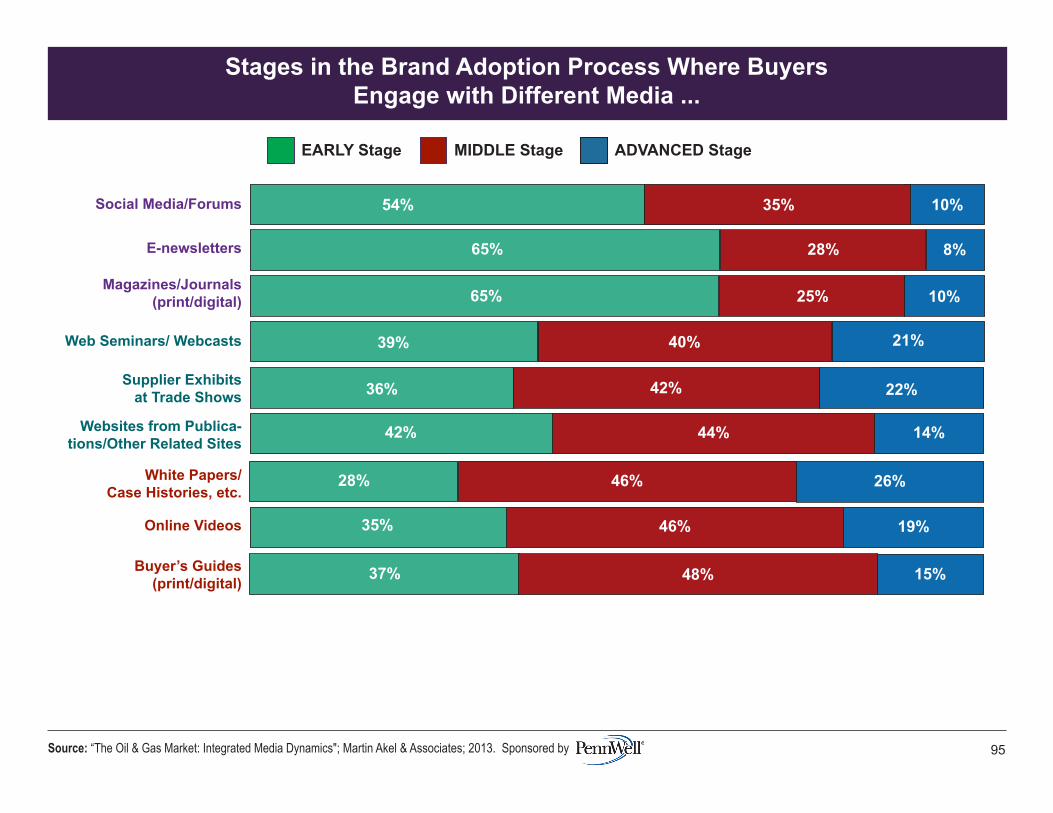

MIDDLE STAGE MEDIA

EARLY MIDDLE ADVANCED Stage Stage Stage

*Those containing technology-related articles and news, buyer’s guides, product reviews, etc.

PROFESSIONAL MEDIA

• Online community groups/social media/forums 54% 35% 10%

• E-newsletters 65% 28% 8%

• Magazines/journals/newspapers (print or digital) 65% 25% 10%

• Online Web seminars (webcasts) 39% 40% 21%

• Supplier exhibits at trade shows 36% 42% 22%

• Websites from publications or other industry-related sites* 42% 44% 14%

• White papers/case histories/special reports on new technologies 28% 46% 26%

• Online videos about technologies/products 35% 46% 19%

• Buyer’s guides/directories (print or digital) 37% 48% 15%

91

Stages in the Brand Adoption Process Where BuyersEngage with Different Media ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by

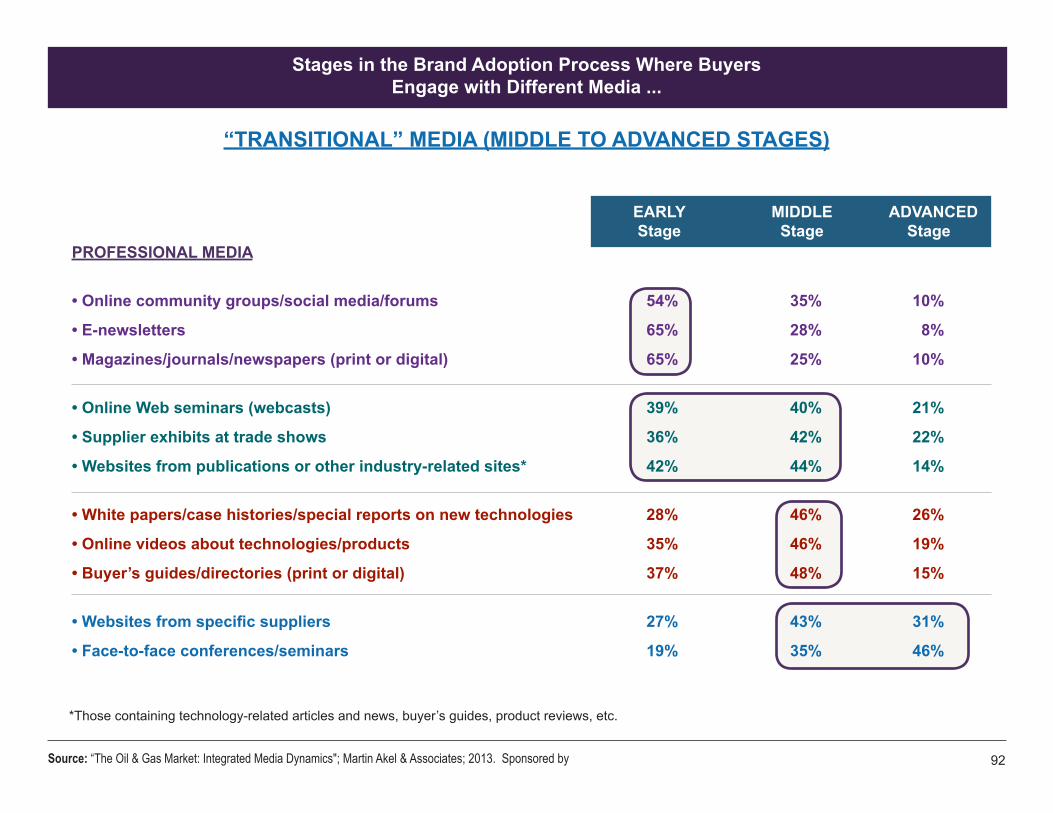

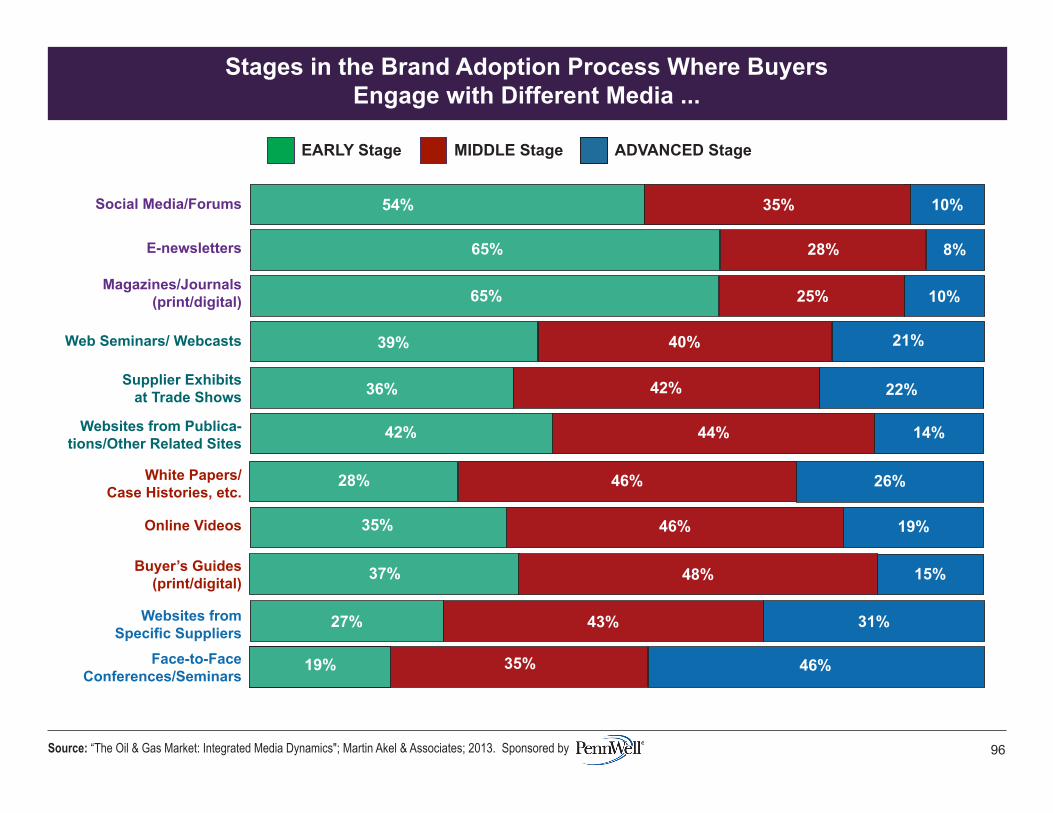

“TRANSITIONAL” MEDIA (MIDDLE TO ADVANCED STAGES)

EARLY MIDDLE ADVANCED Stage Stage Stage

*Those containing technology-related articles and news, buyer’s guides, product reviews, etc.

PROFESSIONAL MEDIA

• Online community groups/social media/forums 54% 35% 10%

• E-newsletters 65% 28% 8%

• Magazines/journals/newspapers (print or digital) 65% 25% 10%

• Online Web seminars (webcasts) 39% 40% 21%

• Supplier exhibits at trade shows 36% 42% 22%

• Websites from publications or other industry-related sites* 42% 44% 14%

• White papers/case histories/special reports on new technologies 28% 46% 26%

• Online videos about technologies/products 35% 46% 19%

• Buyer’s guides/directories (print or digital) 37% 48% 15%

• Websites from specific suppliers 27% 43% 31%

• Face-to-face conferences/seminars 19% 35% 46%

92

EARLY Stage MIDDLE Stage ADVANCED Stage

Magazines/Journals(print/digital)

8%28%E-newsletters

54% 10%35%Social Media/Forums

65% 25% 10%

65%

Stages in the Brand Adoption Process Where BuyersEngage with Different Media ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 93

EARLY Stage MIDDLE Stage ADVANCED Stage

Supplier Exhibitsat Trade Shows

Web Seminars/ Webcasts

Websites from Publica-tions/Other Related Sites

36% 22%42%

39% 40%

42% 14%44%

Magazines/Journals(print/digital)

8%28%E-newsletters

54% 10%35%Social Media/Forums

65% 25% 10%

21%

65%

Stages in the Brand Adoption Process Where BuyersEngage with Different Media ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 94

EARLY Stage MIDDLE Stage ADVANCED Stage

Supplier Exhibitsat Trade Shows

35% 46% 19%

Web Seminars/ Webcasts

46% 26%

Websites from Publica-tions/Other Related Sites

36% 22%42%

White Papers/Case Histories, etc.

39% 40%

Online Videos

42% 14%44%

Buyer’s Guides(print/digital)

Magazines/Journals(print/digital)

8%28%E-newsletters

54% 10%35%Social Media/Forums

65% 25% 10%

21%

15%37%

65%

Stages in the Brand Adoption Process Where BuyersEngage with Different Media ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 95

28%

48%

EARLY Stage MIDDLE Stage ADVANCED Stage

Supplier Exhibitsat Trade Shows

35% 46% 19%

Web Seminars/ Webcasts

46% 26%

Face-to-FaceConferences/Seminars

27% 43% 31%Websites fromSpecific Suppliers

46%35%

Websites from Publica-tions/Other Related Sites

36% 22%42%

White Papers/Case Histories, etc.

39% 40%

Online Videos

42% 14%44%

Buyer’s Guides(print/digital)

Magazines/Journals(print/digital)

8%28%E-newsletters

54% 10%35%Social Media/Forums

65% 25% 10%

21%

15%37%

19%

65%

Stages in the Brand Adoption Process Where BuyersEngage with Different Media ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 96

28%

48%

The Level to WhichDecision Makers are Branded ...

Single VersusMultiple Media

97

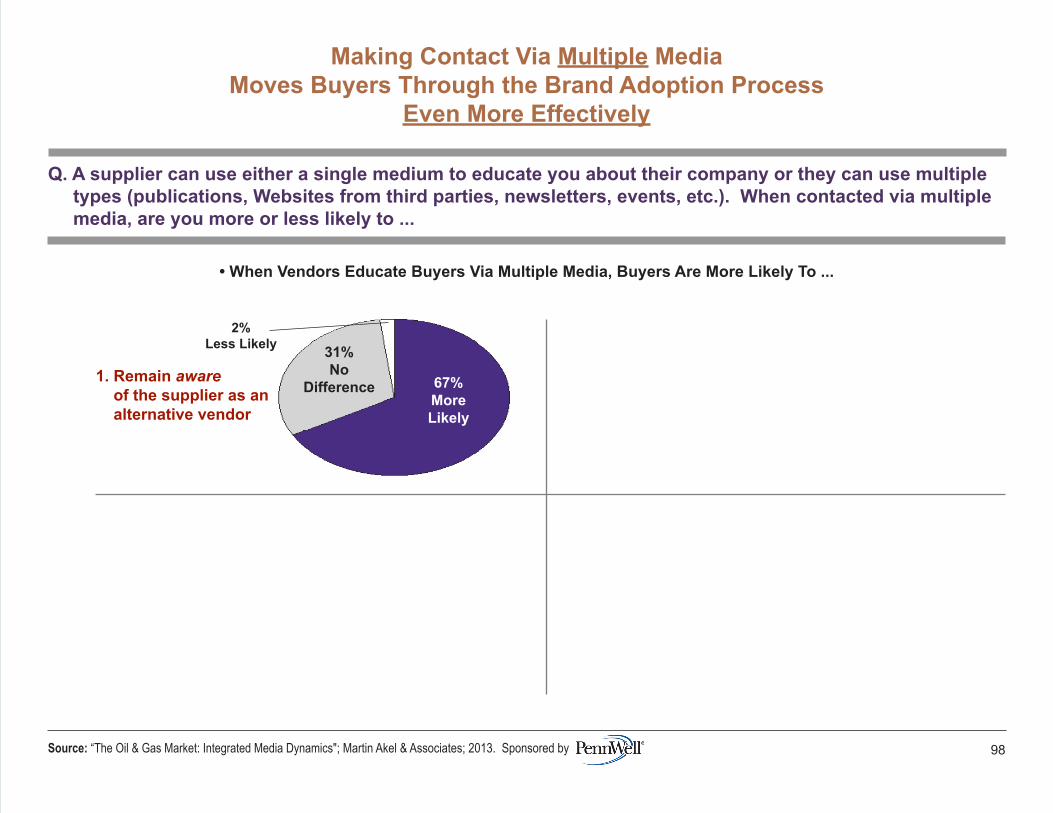

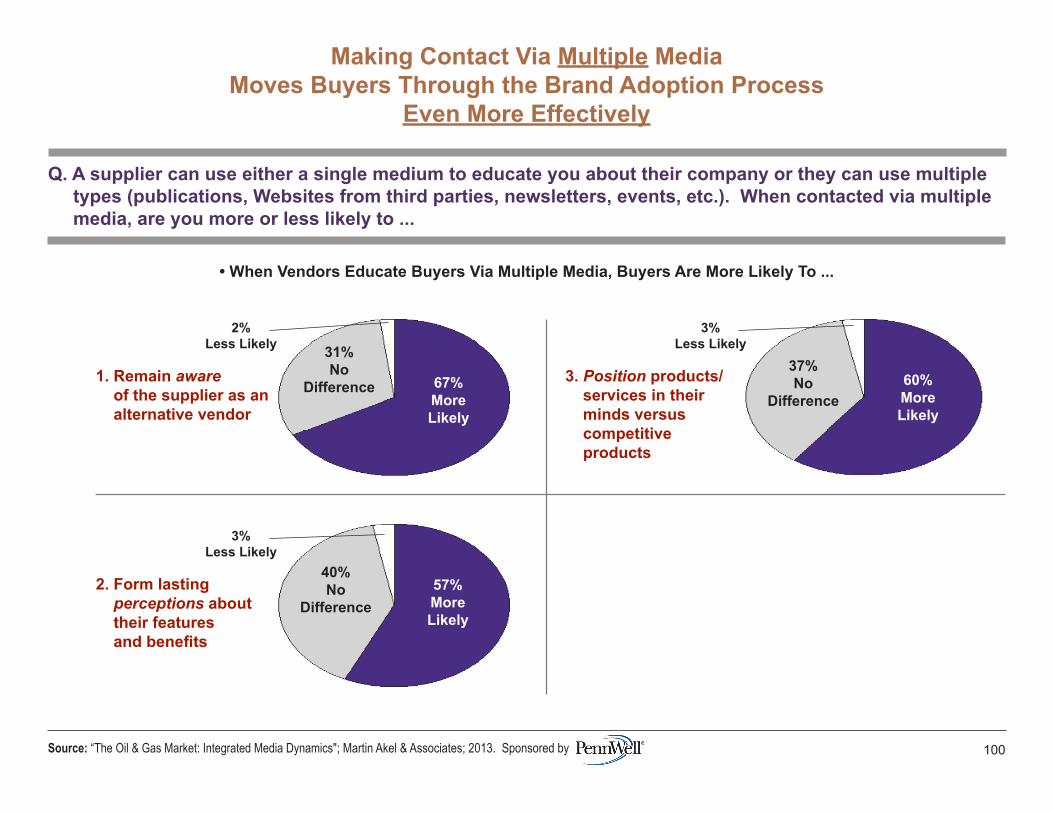

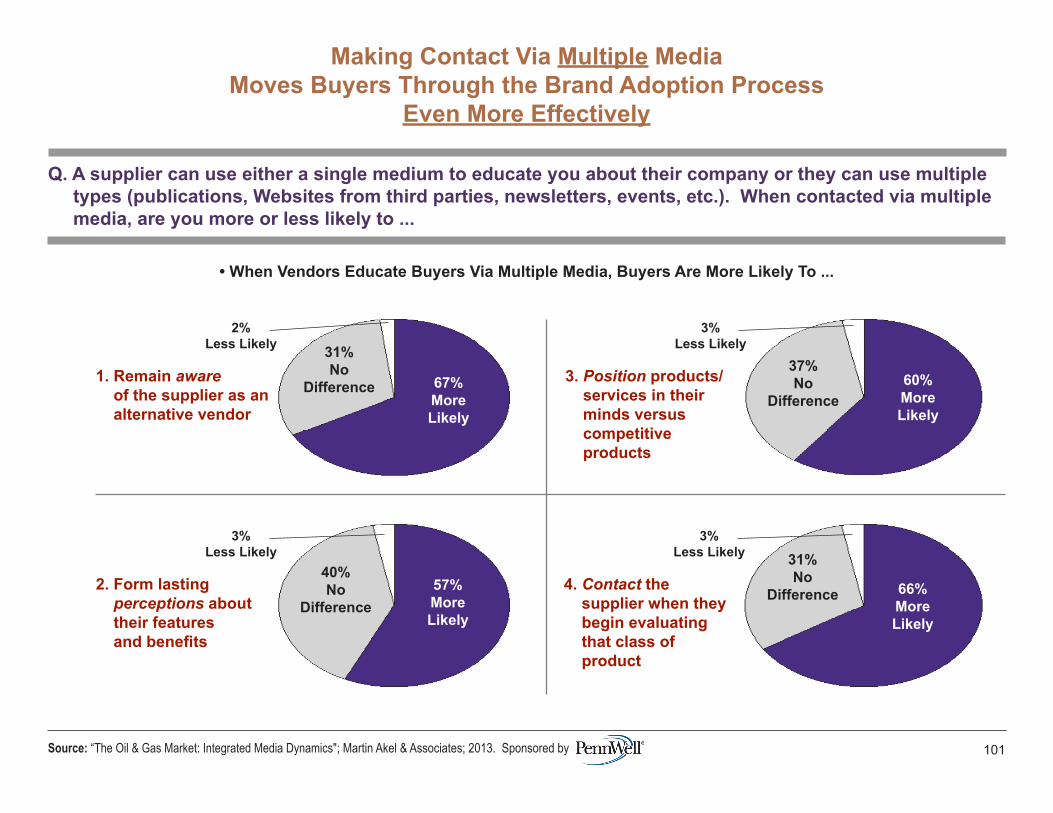

• When Vendors Educate Buyers Via Multiple Media, Buyers Are More Likely To ...

1. Remain aware of the supplier as an alternative vendor

67%MoreLikely

31%No

Difference

2%Less Likely

Making Contact Via Multiple MediaMoves Buyers Through the Brand Adoption Process

Even More Effectively

Q. A supplier can use either a single medium to educate you about their company or they can use multiple types (publications, Websites from third parties, newsletters, events, etc.). When contacted via multiple media, are you more or less likely to ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 98

• When Vendors Educate Buyers Via Multiple Media, Buyers Are More Likely To ...

1. Remain aware of the supplier as an alternative vendor

67%MoreLikely

31%No

Difference

2%Less Likely

2. Form lasting perceptions about their features and benefits

57%MoreLikely

40%No

Difference

3%Less Likely

Making Contact Via Multiple MediaMoves Buyers Through the Brand Adoption Process

Even More Effectively

Q. A supplier can use either a single medium to educate you about their company or they can use multiple types (publications, Websites from third parties, newsletters, events, etc.). When contacted via multiple media, are you more or less likely to ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 99

• When Vendors Educate Buyers Via Multiple Media, Buyers Are More Likely To ...

1. Remain aware of the supplier as an alternative vendor

67%MoreLikely

31%No

Difference

2%Less Likely

2. Form lasting perceptions about their features and benefits

57%MoreLikely

40%No

Difference

3%Less Likely

3. Position products/ services in their minds versus competitive products

60%MoreLikely

37%No

Difference

3%Less Likely

Making Contact Via Multiple MediaMoves Buyers Through the Brand Adoption Process

Even More Effectively

Q. A supplier can use either a single medium to educate you about their company or they can use multiple types (publications, Websites from third parties, newsletters, events, etc.). When contacted via multiple media, are you more or less likely to ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 100

• When Vendors Educate Buyers Via Multiple Media, Buyers Are More Likely To ...

1. Remain aware of the supplier as an alternative vendor

67%MoreLikely

31%No

Difference

2%Less Likely

2. Form lasting perceptions about their features and benefits

57%MoreLikely

40%No

Difference

3%Less Likely

3. Position products/ services in their minds versus competitive products

60%MoreLikely

37%No

Difference

3%Less Likely

4. Contact the supplier when they begin evaluating that class of product

66%MoreLikely

31%No

Difference

3%Less Likely

Making Contact Via Multiple MediaMoves Buyers Through the Brand Adoption Process

Even More Effectively

Q. A supplier can use either a single medium to educate you about their company or they can use multiple types (publications, Websites from third parties, newsletters, events, etc.). When contacted via multiple media, are you more or less likely to ...

Source: “The Oil & Gas Market: Integrated Media Dynamics"; Martin Akel & Associates; 2013. Sponsored by 101

• When multiple media are used, marketing objectives are achieved far more effectively.

• Publications continue to be the primary medium to initiate relationships with buyers.

• As buyers gather intelligence about their options, additional media drive them further into the adoption process, giving them an ever-deeper understanding of ...

- What individual suppliers and products stand for. - How they’re positioned versus competitive products. - The specific suppliers to put on their list for contact and serious evaluation.

• In short - different media contribute different strengths to the mix ... they perform complementary roles in the adoption process.

CONCLUSIONS:

I. The Complementary Roles of Different Mediain the Product Adoption Process

102

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

KEY TAKEAWAYSAbout Structuring the Integrated Media Mix

Targeted at Oil & Gas Professionals

The Global Oil & Gas Market:DYNAMICS OF STRUCTURING THE INTEGRATED MEDIA MIX

103

KEY TAKEAWAYS ...

1. Faced with a broad array of challenges, professionals are relying heavily on new technology to offer solutions.