Embed Size (px)

DESCRIPTION

March 2013 edition

Citation preview

1

Volume 21, Issue 1

2

FROM THE EDITOR The Financial Bulletin

Money Matters Club IBS,Hyderabad Established—2005

Editorial Enquiries Contact

Contact No

Advisor

Faculty Co-ordinator

Student Co-ordinator &

Editor

Advertising Contacts

Money Matters Club

+919948564613,

+919573462013

Dr V Narendra

Dr. S Vijayalaxmi

Kanchan Kumar Roy

Vikas Singh

+9573462013

Can we help?

For any enquiries ,subscription and

advertisement

email us @ [email protected]

You can log into

http://moneymattersclub.weebly.com/

All rights reserved.

Money Matters Club, The official Finance

Club of IBS Hyderabad.

Visit us at for further

information.

Dear Readers

We congratulate the winner of the “Article of the month”

award, Chandra Sekhar from ABV- Indian Institute of

Information Technology and Management Gwalior, M.P

for his article “Micro credit in modernizing Agriculture:

Indian Perspective” .

The March edition holds a lot of interesting articles to read

Where at one side we tried to analyze the Budget 2013, Is

taxing the super-rich justified? On the other side we also

get to know about the Mergers and De-mergers and its im-

pact and also the Fed bonds impact. We also discussed

about the micro credits impact in India.

Go through this brilliant collection of articles from the best

minds of Indian B-schools and find out lots of interesting

facts.

Newsletter Editor

Kanchan Kumar Roy

3

The Financial Bulletin March 2013

CONTENTS

04 Budget 2013 –by Aditya Chordia

SCIT 2012-2014

08 MERGERS &

ACQUISITIONS: EVALUATION

OF SYNERGIES -by Prakarsh Jain, Rohit Gambhir S P Jain

School of Global Management, Dubai-

Singapore

13 Micro credit in modernizing

Agriculture: Indian Perspective -by Chandra Sekhar ABV - Indian Institute of

Information Technology & Management,

Gwalior

16 Taxing the Super-rich – A

costly move! –by Nitin Bhat, Infosys

20 Emerging Market shines over

Euro zone -by Kunal Sanghvi

SIMSREE

27 Bank Consolidation: An

Overhyped Idea? -by Aarzoo sharma,

Krupa shah MET institute of management

Mumbai University

32 Impact of Fed Bond Buying on

the Economy –by Yogesh Athale,

SIMSREE

04 E-Commerce Effervescence

4

BUDGET 2013 In the current scenario, I am sure nobody would

be ready to take on the job of Finance minister of

India. Considering all the corruption scams, policy

inaction and growing inflation which has been the

headlines of the UPA II regime for the past 5 years.

And here comes a Harvard business graduate to

present his 8th budget as a Finance minis-

ter....Welcome Mr. P Chidambaram (Let’s call him

PC). The three big issues that might have been

troubling PC prior to announcing the budget is as

follows:

The widening fiscal deficit

i.e. the difference between

income and expenditure.

PC had promised prior the

budget that he would try to

keep the fiscal deficit to

5.3%.

The decelerating growth combined with an ever

rising inflation.

Finally the rising current account deficit i.e. the

difference between exports and imports due to

rising imports of oil and gold.

Prior to the budget, India was already facing a

threat of downgrade from the Standard and Poor

rating agency which would have seriously affected

the foreign inflows. PC also had to keep in mind

that this is the last budget before the general

elections and hence he had to present a fairly

populist budget but at the same time it also had to

be economically viable for India in the face of

rising uncertainty. Keeping all these points in

consideration below mentioned are the some of

the important decisions taken in the budget 2013.

Fiscal Deficit

PC beat his own estimate of keeping fiscal deficit

to 5.3% by bringing down the number to 5.2%.

But this was largely possible because of a huge

reduction in the planned expenditure (money

used for investment in various sectors for

development of the

country). So basically PC cut

down the expenditure by a

huge margin and with a little

help from the recent

decisions like de-regulation

of diesel prices and capping

the LPG helped in bringing

down the fiscal deficit.

Also PC has aimed to bring down the fiscal deficit

to 4.8% in the coming fiscal year. This reduction is

predicted based on huge ambitious targets like

bringing down the subsidies to fuel, increased tax

collections, spectrum allocation and huge funds

collected from the disinvestment in PSU’s. Of the

above only the target from disinvestments seems

achievable and the tax collections target seems

achievable provided the economy grows at 6.2-

6.3% in the next fiscal.

GST (Goods and Service tax) & DTC (Direct tax

5

code)

PC mentioned that the government has set a

deadline for bringing in DTC and the bill would be

brought in the parliament at the end of the budget

session.

As far as GST is concerned, PC mentioned there is no

deadline as such because it depends on how fast all

the state ministers can come to a conclusion over a

common model and compensation. But PC has set

aside 9000cr (compensation for year 2010-11) for

GST and requested all the state ministers to come a

conclusion as early as possible. It is estimated that

the introduction of GST would add at least 1.5% to

the existing GDP.

Direct benefit transfer (DBT)

The flagship programme of UPA for the forthcoming

elections “Direct benefit transfer” as per PC is on

right tracks and some modifications here and there

are required. According to PC, there are 3 pillars for

DBT:

A digitized beneficiary list.

Bank accounts for all beneficiaries.

Aadhaar card.

As per PC, the digitized beneficiary list is almost

ready and once the list is ready, bank accounts for

all beneficiaries will be opened and Aadhaar is

doing the catch-up work. PC also mentioned that

the food and fertilizers benefit would be kept out of

the current DBT as they are complicated and some

work needs to be done.

Taxing Super rich

PC has proposed to charge a surcharge of 10% for

those earning more than 1 crore and the

surcharge for a domestic firm earning more than

10 crore has been increased to 10% from 5%.

Though he has mentioned that this surcharge

would be valid only for one year. Nearly 49500

people earn more than 1 crore as per

government estimates. Really this number

baffles me!!!!! (Only 49000...come on yaar)

The government has increased excise duty on

SUV’s to 30%. Cigarettes and mobile phones

also attract more taxes. There has been an

increase in customs duty for luxury cars and

bikes. Also import duty of used cars has been

increased to 125% from 100% which curbs the

import of luxury second hand cars. Even A/C

restaurants have to pay more as part of their

service tax.

Energy & Manufacturing

Electricity is set to become costlier as duty will be

charged on imported coal (be it stem coal or

bituminous coal) with 2% custom duty and 2%

CVD (countervailing duty—a duty that is applied

to offset subsidized export from another

country).

Also to revive the manufacturing sector,

government has planned an investment

allowance of 15% over an investment of 100

crores for all investments in plant & machinery

in the coming two years. PC has also raised the

custom duty on electronics goods which is a

positive sign for the local electronic

6

manufacturing units.

Incubators

PC mentioned in his budget speech that funding will

be given to incubators on college campuses. Also

the corporate sector’s investment in such

incubators will be considered as CSR (Corporate

social responsibility). The corporate’s will be more

than happy to invest in such incubators as they are

interested in giving funding to entrepreneur’s.

Real estate

The government has proposed that a 25 lakh home

loan will get tax deduction of an additional one lakh

tax deduction on interest payments for the first

year. Overall a person taking a home loan of 25 lakh

will get tax deduction of 2.5lakh.

This step surely augurs well for the real estate sector

as it has been reeling under low demand from the

customers. But the real estate sector feels that

there are very few homes available at that rate and

hence this step wouldn’t make any significant

difference to their prospects. Instead the real estate

sector expected some perks on the premium home

side rather than the affordable home section.

Foreign investment

The government has proposed a 20% tax on profits

distributed through buyback of shares (government

felt many firms instead of distributing profit

through dividends opted for the route of buyback of

shares). Also there has been an increase on tax on

royalties, companies pay to their parents abroad to

25% from 10%.

Also PC has clearly stated the difference between FII

(Foreign institutional investment) and FDI

(Foreign direct investment). Any foreign

institution having more than 10% stake will be

considered as FDI and less than 10% will be

considered as FII. This step has left many foreign

institutions to change their holding pattern in

the Indian organizations. Also PC has stated that

along with tax certificates, a beneficiary

certificate is also necessary to avoid double

taxation.

These decisions have spooked the foreign

investors from investing their funds in the Indian

economy.

Women Power

PC has allocated nearly 2000crores for the

women and child development ministry and

1000crores for the “Nirbhaya fund” in honour of

the Delhi gang-rape victim to promote women’s

safety.

But Congress has faced to pass the bill which

reserves 33% of the seats for women in

Parliament as though it has been passed by

Rajya sabha, it has still not been cleared in the

Lok Sabha. All these steps clearly indicate

Congress is trying to woo the second largest

base of voters.

Also PC has proposed to open an All-women bank

which will lend specifically to women

entrepreneurs and women self-help groups. It

will also be managed completely by women.

Health care

Universal health coverage (UHC) one of the

7

flagship programmes of UPA takes a back seat and 21,239 crores have been allocated for National

Health mission (NHM). Also allocation for the Integrated Child development services has been increased

11.7% to 17,700 crores. Allocation to the Ministry of drinking water and sanitation was increased to

15,260 crores from 14,000 crores.

But the health care industry feels there has been only a marginal increase in the budget allocated to them

when compared with the previous year. Also the experts feel that the government is not concerned

about the health of the people.

Education

The education sector has been allocated roughly 65,000 cr, an increase of 7% from that of the current

fiscal year. Major portion of this budget goes to Sarva Shiksha Abhiyan (SSA) which is entrusted with

implementing the Right to education act.

Also 1000cr have been set aside by PC for a scheme in which 1 million students will get Rs.10,000 each on

completing skills training course.

CONCLUSION

Considering the current scenario, it has been a satisfactory budget and let’s hope that the country rises to

a growth of 6% plus. It’s achievable provided the investment cycle improves which has been stagnant

due to various bottlenecks. Moreover everybody can’t be made happy in a budget!!!!!!.

Aditya Chordia

SCIT 2012-2014

8

I purchase companies, split them into small arms, and sell them off; it’s worth more than the whole one

of it, explicated by the corporate acquirer, in the movie, Pretty Woman, which displays a company

acquired through uncongenial bid and thereon striped-off its assets, entirely disregarding the decades of

sweat-work seated by its holders. This is what actually happens in cutthroat environment and therefore

a need arises for a guard to take care of the interest from third party interference. To mitigate this

problem, there are laws across globe that are in place, dealing with mergers and acquisitions. Hence,

one thing stands clear, before doing any number-crunching and other planning; we have to consider if

systems are in place to follow the law of the land.

Mergers & acquisitions has been big part of the corporate world since decades. It deals with conjoining

entities for gaining various operational/financial benefits.

From the capital market viewpoint, the promulgation of merger sends a strong message, such that the

company is moving forward in the business and probable increase in the market capitalization. The main

aim of M&A is to create positive synergy effects in business.

“One plus One makes Three” - this statement represents the main philosophy behind M&A.

Merger and Acquisitions are used as synonyms, but they mean slightly different.

Merger: Blend of two or more companies, dealt by offering the stockholders securities in the

acquiring company in exchange for the surrender of their stock.

Acquisition: The target company ceases to exist and the acquirer continues to trade its own shares.

Acquisitions can be either friendly or unfriendly; it depends on the accordance of the

target company.

Synergy: A concept that the value and performance of two companies combined will be greater

than the sum of the separate individual parts.

Introduction

The Words

MERGERS & ACQUISITIONS:

EVALUATION OF SYNERGIES

9

Following would give us clarity on the above:

Inorganic Growth: Organic is limited to the stand-alone growth of the company, whereas, merger/

acquisition leads to immediate growth in size and market capitalisation/valuation.

Acquiring intellectual capital/technology

Tax considerations and Overcoming government policies

Restructuring the business

Cost reduction and efficiency leverage

Capital optimization

To top it all, the overarching reason for a decision on merger and acquisition taken by a company is the

synergy it would provide.

The synergy provided by an event of M&A can be calculated on estimating the value of the company to

be acquired. There are various methods of doing so; some of them are as follows:

Discounted Cash-Flow Analysis:

This method involves discounting the expected future cash flow to the present value in order to derive an

estimated value of the company. The terminal value too, is taken into consideration, which is discounted

to perpetuity.

Assets Based Valuation:

A method wherein valuation is based on the assets and liabilities of the company. It plays an important

role where companies have large investments in fixed assets to generate earnings. It is also a sought out

approach by companies that are “worth more dead than alive.”

Comparable Company Analysis:

The analyst first defines a set of other companies that are similar to the target company. This may include

companies within the target’s primary industry or in similar industries.

Why Merger and Acquisition ?

Valuation

10

A company’s enterprise value is the market value of its debt and equity to cash flows, enterprise value to

EBITDA, to EBIT and to sales. The equity can also be valued using equity multiples.

Other considerations:

Brand Valuation

Relative Valuation: Price Earnings Ratios, P/B Ratio, Tobin Q, Price to Sales Ratio

Valuation of combined firm should be greater than the value of companies on stand-alone basis.

Creating value of the enterprise that exceeds the cost of acquisition is the primary objective of the

management based on which the market pays-off or punishes the shareholders of a combined company.

When employed on to valuation and other deal theories, synergy would mean, the companies win, in

which the seller receives an acquisition deal premium and the buyer realizes shareholders value. The

fundamental and the only palpable justification, which appeals to the owners and management of the

company, is the synergy that an M&A would provide and therefore, the centering is on identifying and

tracking synergy.

A chiseled and crystal-clear approach to synergies, gives rise in the probability of achieving the objectives.

Such an approach would involve:

Prototyping-Synergies

Synergy Identification and Validation: For preparing, a deal model the company that is acquiring would

need to validate assumptions that are sensitive to the deal. When it comes to an auction process, the

amount of information to reveal or not to reveal is completely in the hands of the seller. Hence due

diligence is extremely essential to identify and authenticate value drivers.

To prototype synergies, assumptions are based on information, which is target provided and using public

data. The corporate development and finance teams develop these assumptions. Hence, higher the level

of detailing in the initial assumptions would be of relevance to negotiate approval process.

Many companies face challenges when they are approaching diligence in the form of unraveling, what

could be wrong with the target company. To overcome this challenge a more efficient approach would

be to break down risk areas and important value drivers.

Prior to realizing synergies from an acquisition, it is essential that the synergy assumptions are identified

and validated by the functional units. Once the functional units have ownership of the numbers and the

Probing Synergies

11

same are verified by experts the credibility of the synergy estimates go up. Synergies are easier to realize

if the acquirer has a good understanding of the business, he is acquiring. In general, cost synergies are

more successful than revenue synergies. This could be true because cost synergies-reduce headcount,

overhead reduction, etc. involve lesser variables and rely less on subjective variables as compared to

revenue synergies.

Companies face possible risks if they don’t validate the synergies with the functional owners. Firstly,

inaccurate estimates have a higher chance of occurrence with no validation from functional owners.

Secondly, a chance of shortfall in synergy increases once the deal is completed. Hence, vetting these

costs and including these numbers in the overall valuation is extremely critical to create a realistic

model.

Carrying-Out

Challenges of Synergy Realization: The most common reason for acquisitions not realizing their full

potential lies in weak execution. This in turn hampers the ability to create shareholder wealth through

acquisitions.

Factors that play a key role in realizing synergies from a deal depend on the type of synergy target. For

cost synergies the management’s tone and supervision is critical. The revenue synergies are more about

aligning efforts through combination of technical knowledge.

Transparency: Transparency is extremely essential to maximize synergy realization. The company that is

being acquired should have a clear link to its internal and external financial statements. This is important

information that stakeholders can use to authenticate value creation. In addition, management’s

commitment is extremely essential to the successful creation of synergies.

Talent Retention: Another essential factor for realizing synergies is the retention of talent that would

help maximize the benefits from the integration of the acquirer and the company being acquired.

Certain companies use financial incentives to retain certain key members of the firm until the synergy

realization is maximized.

Integration: Certain companies make an error in judgment by delaying integration and underestimating

its complexity. To avoid making this error companies should focus on accelerating the transition, prepare

for day one and at the same time establish leadership on all levels. More importantly, the company

should manage the integration as a business process.

12

Tracking-Synergies

It is simple, if your operating profit is good, then its working well for you. The focus is on tracking if the

actual income, sales/gross receipts, and the spending budget and see if that makes sense. More often

than not, the first few years’ performance is solid because that is something, which is the near future,

and that we have an integration team for, but we really have a hard time tracking it beyond a certain

point of time. The bottom line and typically the revenue lag a little bit behind. Usually, we never get the

sales synergies as we expect it to be.

Comparing this with the prototyping is the basic that we are to undertake. Companies in present times

also track non-financial metrics such as employee and customer retention.

Preeminent practises make us conclude that the success of the deal puts emphasis on:

Synergy-tracking

Deal-process

Measuring Share-holder value

“Mergers are like speed-dating. There is a short chronology involved in making a vital decision that would

lead to union. The company acquired shows off its colours, and you need to differentiate between

fascination and a perfect match.”

Leveraging operations, human-resources, and tools that rapidly and accurately track synergies is

indispensable to an effective M&A. These elements may not vouch value creation, but without these, a

dealmaker’s chance for success diminishes substantially.

Conclusion

Prakarsh Jain

S P Jain School of Global Management,

Dubai-Singapore

Rohit Gambhir

S P Jain School of Global Management, Dubai

-Singapore

13

Micro credit in modernizing Agriculture: Indian Perspective

Microcredit (MC) has become a buzz word among

the development practitioner. Term 'microcredit'

means providing very poor families with very small

loans to help them engage in productive activities or

develops their tiny businesses. Agriculture is a

major contributor to India Gross Domestic Product

(14.6% - 2013) and small-scale farmers play a

dominant role in this contribution but their

productivity and growth are hindered by limited

access to credit

facilities. Agriculture is

the most important

sector of the country

because the main

policies of output

growth, poverty

alleviation, social justice and equity are best served

in this sector. The participation of commercial banks

was negligible in agricultural loans. Farmers’ level of

income was low and they were hesitant to use

technology. Therefore, agriculture Micro credit

policy aimed at increasing the flow of institutional

credit at reasonable rate of interest to agriculture

sector. The cooperative credit structure was

strengthened by reorganizing and merging weak

societies with strong societies. Credit institutions

can be categorized into three groups: first one is

Formal Financial Institutions: such as Commercial

banks, Microfinance Banks, Development Finance

Institutions (DFIs), and State Government –owned

Credit Institutions. Second one is Semi-Formal

Financial Institutions: such as Non-governmental

Organizations –Microfinance Institutions (NGOs –

MFIs) and the last and Third one is Cooperative

Societies. Agricultural credit specifically involves

enjoying control over the use of money, goods

and services in the present in the exchange for a

promise to repay at a future date. With

agricultural credit, a lender forgoes the use of his

money or its equivalent in the present by

extending credit to a

borrower who

promises to repay on

terms specified in the

loan agreement. Many

microcredit policies

had seen launched in

India with the

objectives of providing microcredit to the rural

poor farm households. Microcredit has also been

acknowledged as one of the prime strategies to

achieve the Millennium Development Goals

(MDGs). Access to adequate financial services

enables small-holder farmers to procure

productive assets, reduce their vulnerability to

external shocks and increased production

efficiency. Microcredit involves the supply of

loans, savings and other basic financial services to

the poor farm households. The small-holder

farmers require diverse range of financial

instruments to meet working capital requirement,

build assets, stabilize consumption and shield

14

themselves against risks. In practice, microcredit is

much more than disbursement, management and

collection of small amount of loans. It recognizes

the peculiar challenges of

micro enterprises and their

owners. It also recognizes the

inability of the rural farm

households to provide

tangible collateral and thus

promotes collateral

substitution. Farmers,

especially rural farm

households are constrained

by credit from both formal

and informal sources. As the microcredit revolution

spreads the rural farm households are seen as

micro-entrepreneurs with no collateral to pledge

but with a business world to conquer with the help

of micro credit. Financial services are needed by the

rural farm households to improve their wellbeing

through the upgrading of their farms and small

scale businesses for positive impact on their

livelihood. Judicious use of credit to acquire

productive resources will not only lead to on farm

capitalization but will also increase the production

efficiency of the farmers. The objective was to

promote agricultural development by modernizing

agriculture. The most common approach involved

direct government intervention via state-owned

development banks and direct donor intervention

in credit markets with favorable terms and

conditions like soft interest rates or lenient

guarantees. The factors that hinder the

development of financial services made accessible

to family agriculture are numerous and have been

well identified. In order to develop agricultural

finance, different kinds of innovations regarding

products and services as well as institutional

aspects are very important. The challenge is two-

fold: improve financial inclusion through better

outreach of marginalized populations as well as

financial services that fit the diversity of financial

needs. Other solutions to promote efficient,

sustainable and accessible financial services for

smallholder farmers are being found in terms of

institutional organization such as portfolio

diversification between urban and rural

borrowers or between agricultural activities and

less risky economic activities within rural areas in

order to mitigate risk.

With the help of some approach /character

reference we can improve the situation of rural

financial services generally in developing

countries like Financial Sector Reform which is

essential to restructure the financial sector aiming

at eliminating financial market distortions,

restoring the health of the existing financial

15

institutions. Rural Finance which should be set up to design better operational procedures to improve

staff and management performance to install adequate management information systems for use by the

local farmer. Formal Financial Sector and Informal Financial Intermediaries can be used to reduce their

information costs to link rural savings mobilization with credit and to facilitate loan supervision and loan

recovery and also provide marketing loans which can be guaranteed by the government to contracted

input dealers or traders. On the other hand Cooperatives and Role of government used to strengthening

the business character of these organizations by providing adequate training marketing, financial

management, accounting and auditing. Therefore, the government should take the responsibility of

shifting the operation of informal cooperatives to formal cooperatives so that they will stand the chance

of equal status and financial support.

Last but certainly not the least I have concluded that Micro credit helps to modernize production in

agriculture and place farmers in a proper position to employ mechanized equipment that can lead to

increased agricultural productivity. Increased credit could accelerate rural development, reduce income

disparities and create income increases that would improve welfare.

Chandra Sekhar

ABV - Indian Institute of Information Technology &

Management, Gwalior

16

Taxing the Super-rich – A costly move!

Until a few days back, with the budget around the

corner, taxing the superrich seemed to be the gossip

of the town. With an ominously increasing fiscal

deficit, this move would aim at improving direct tax

revenues, simultaneously giving an upward boost to

our Tax/GDP ratio. Populists and generalists

supported this view; however the economists came

out against it vehemently. While the former were of

the opinion that marginal tax rates should increase

as incomes rose, leading to greater tax collections,

the latter argued that this move would have a

detrimental effect on the economy due to increased

incidences of tax evasions. Both arguments had their

merits in place, what mattered was the cost at which

the benefits

would be accrued.

Pre-liberalization,

India had an un-

friendly tax re-

gime, unfavorable

on all terms with

the common man.

In 1970-71, the

personal income tax had 11 tax brackets with the tax

rates progressively rising from 10 per cent to 85 per

cent. In the decades that followed, marginal taxes

were progressively reduced from the astronomical

levels of 85% to less than 40%. Post liberalization, in

1997-98, income tax brackets were defined at 10%,

20% and 30% and haven’t changed since. Post-

independence, though the government had noble

intentions of increasing the country’s revenues,

sky-rocketing tax rates led to large scale tax

evasion, increased incidences of smuggling and

emergence of underground black markets. This

counteractive sway of high tax rates became the

raison d’ etre for steady decline in tax rates to

their current levels.

Fast forward to 2013 January, the government

was faced with quite the opposite situation. The

economy has an untamable tiger, the rising fiscal

deficit. High disposable incomes and low Tax/GDP

ratio as compared to other developing countries

forced to government to rethink the prevailing

marginal tax

rates. Table 1

details the

marginal tax

rates and the

Tax/GDP ratio

of some of the

developing

and developed

countries of

the world. A quick scan tells us that India has the

lowest Tax/GDP ratio among countries having

similar/greater marginal tax rates.

For a country with one of the lowest marginal tax

rates, this is an indicative of the low levels of fiscal

jurisprudence among the masses. Other factors

which can be attributed to this anomaly are:

Country Marginal Tax Rate Tax/GDP ratio (%)

UK 50% 39

Brazil 28% 34.4

Australia 50% 30.8

Japan 50% 28.3

US 40% 26

China 45% 17

India 30% 10.3

17

1. High poverty levels and low disposable in-

comes

2. Inability of the govt. to capture the earnings

of SME’s/proprietary firms across the

country

3. High tax exemptions to certain sectors like

agriculture

The finance minister was treading on thin ice when

he presented this year’s budget. Among others,

fiscal consolidation, reeling inflation, contain-

ing fiscal deficit and tax reforms were some of the

key expectations from the common man. The fi-

nance minister did manage to live up to the expec-

tations of the common man by proposing appro-

priate measures to bring the economy back on

tracks. The bone of contention was on the issue of

taxing the superrich. The finance minister offered

his two cents by main-

taining the marginal

tax rates as it, while

imposing an additional

10% surcharge on indi-

vidual and corporate

incomes rising above 1

crore rupees. Given the

large number of con-

cessions and exemp-

tions available, the

number of tax-paying entities falling in this range is

small. The Minister himself provides a figure of a

paltry 42,800 individuals who qualify. With

due considerations to economic implications, the

finance minister expects this move to add about

180 billion rupees to the revenue base. This move

makes the most economic sense for the following

reason. The surcharge of 10% on the highest tax

bracket of 30%, translates to an effective tax rate

of 33.99% (with education cess included). Such

individuals were so far taxed at 30.90 % for

incomes exceeding 10, 00,000 rupees. Under the

new tax regime, such individuals

will have to pay the new tax of just 33.99% on

income exceeding 10 times their sum. For

individuals with such high incomes, this increase in

tax is too small an incentive to launder the excess

money in the hope of tax evasion. They might as

well as end up paying it rather than being

questioned about a suspicious tax evading deal.

The costs associated with tax avoiding money

laundering activities

are far higher than the

benefits of being tax

complaint. This will

ensure a greater ratio

of tax compliance thus

boosting the tax

collections of the

government.

Other than the one

reason mentioned in

the above paragraph, there are quite a few

economic implications entailing higher taxes for

the superrich. They also serve as reasons why the

superrich should not be taxed extra. Any tax

regime needs to give due considerations to these

points, failing which the myopic vision of

18

increasing revenue will cloud the greater evil of tax

evasion.

The classical Laffer curve explanation : The

Laffer curve is a representation of the relationship

between possible rates of taxation and the resulting

levels of government revenue. It illustrates the

concept of taxable income elasticity—i.e., taxable

income will change in response to changes in the

rate of taxation. It postulates that no tax revenue

will be raised at the extreme tax rates of 0% and

100% and that there must be at least one rate

where tax revenue would be a non-zero maximum.

The "economic effect" assumes that the tax rate will

have an impact on the tax base itself. At the

extreme of a 100% tax rate, the government

theoretically collects zero revenue because

taxpayers change their behavior in response to the

tax rate: either they have no incentive to work or

they find a way to avoid paying taxes. Thus, the

"economic effect" of a 100% tax rate is to decrease

the tax base to zero.

This theory also subtly hints that as the tax rate

crosses the optimal tax rate where the tax revenue

is maximum; imposing any additional taxes will act

as a negative incentive for citizens to pay taxes.

Thus, citizens of such economies resort to money

laundering measures to avoid taxes from the

government. Increasing taxes acts as a disincentive

for tax compliance and causes tax avoidance. (The

tax rate t* is an indicative value varying across

economies.)

Historical failure : In the past, India has had a

disastrous experience by levying exorbitant taxes

on the rich. At its zenith, taxes were more than

90% which achieved unintended objectives of

massive tax evasion and erosion of national

character. As per Laffer, there was no incentive

whatsoever for any individual to part with so

much of earnings with the government. This led

to large scale unaccounted cash transactions, thus

fuelling a massive black market economy.

Historically, there is not a single instance where

taxing the superrich has worked as a solution to

increase tax revenues. Similar problems, albeit on

a much compounded scale can be expected in

case similar tax regimes are adopted.

Burdening the honest tax payer : In the past,

the honest tax payer has always been haunted by

the image of the vicious tax official waiting to

wring every last penny out of people’s pockets.

More often than not, the IT department knocks

down the doors of individuals and corporates who

religiously pay their taxes. Be it a regular salaried

job individual or a reputed MNC entering India

through an acquisition, they are harassed and

interrogated about their supposedly suspicious

transactions, the IT dept. turns a nelson’s eye

towards sectors like liquor, real-estate, education

where massive tax evasion is prevalent. Such

incidences have eroded the faith of the tax

system in the eyes of the so-called-rich, who

continue to look for greener pastures outside the

Indian economy.

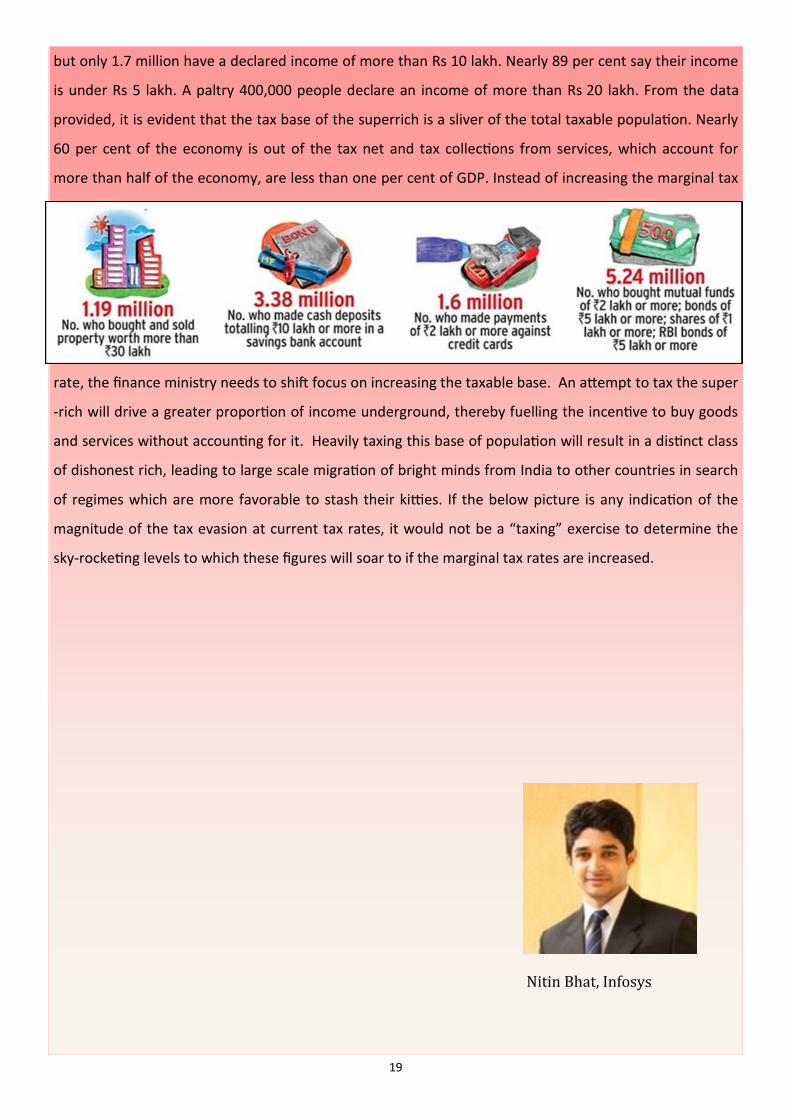

The dishonest rich: According to the Ministry

of Finance, India has nearly 35 million taxpayers,

19

but only 1.7 million have a declared income of more than Rs 10 lakh. Nearly 89 per cent say their income

is under Rs 5 lakh. A paltry 400,000 people declare an income of more than Rs 20 lakh. From the data

provided, it is evident that the tax base of the superrich is a sliver of the total taxable population. Nearly

60 per cent of the economy is out of the tax net and tax collections from services, which account for

more than half of the economy, are less than one per cent of GDP. Instead of increasing the marginal tax

rate, the finance ministry needs to shift focus on increasing the taxable base. An attempt to tax the super

-rich will drive a greater proportion of income underground, thereby fuelling the incentive to buy goods

and services without accounting for it. Heavily taxing this base of population will result in a distinct class

of dishonest rich, leading to large scale migration of bright minds from India to other countries in search

of regimes which are more favorable to stash their kitties. If the below picture is any indication of the

magnitude of the tax evasion at current tax rates, it would not be a “taxing” exercise to determine the

sky-rocketing levels to which these figures will soar to if the marginal tax rates are increased.

Nitin Bhat, Infosys

20

Emerging Market shines over Euro zone

EXECUTIVE SUMMARY:

The emerging markets have become favorable destination for investments for its resilient nature and

improved policies. Before European crisis, emerging economies have been attracting investments from

European Union (EU). Post crisis absolute quantum of inflows from EU into emerging markets have

reduced considerably. However momentum is sustained because of bilateral treaties and aggressive

entrepreneurial environment in emerging economies. Globalization made EU crisis affect emerging

countries and the domestic demands in the emerging economies were not as strong enough to fill the

demand shortfall that Euro zone created. During the East Asian crisis, emerging countries lacked

countercyclical measures and policies. Since then many financial reforms with strong institutional

architecture started attracting investors.

1. INVESTMET ACROSS BORDERS

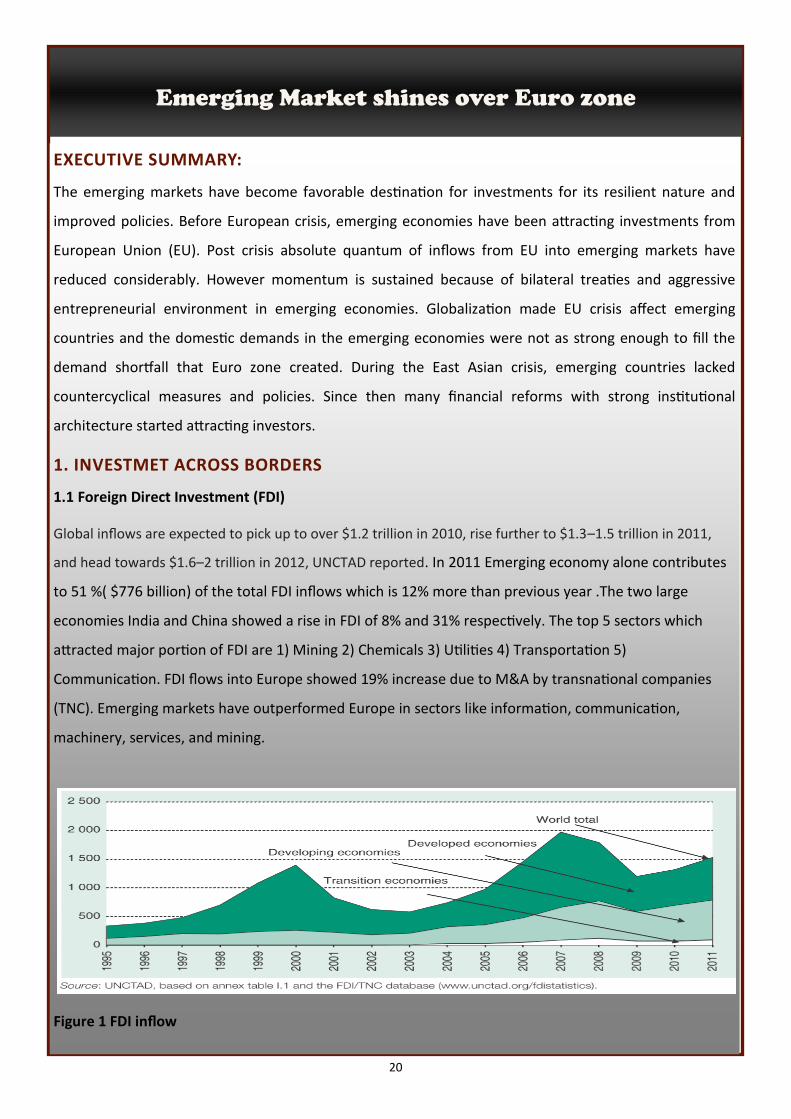

1.1 Foreign Direct Investment (FDI)

Global inflows are expected to pick up to over $1.2 trillion in 2010, rise further to $1.3–1.5 trillion in 2011,

and head towards $1.6–2 trillion in 2012, UNCTAD reported. In 2011 Emerging economy alone contributes

to 51 %( $776 billion) of the total FDI inflows which is 12% more than previous year .The two large

economies India and China showed a rise in FDI of 8% and 31% respectively. The top 5 sectors which

attracted major portion of FDI are 1) Mining 2) Chemicals 3) Utilities 4) Transportation 5)

Communication. FDI flows into Europe showed 19% increase due to M&A by transnational companies

(TNC). Emerging markets have outperformed Europe in sectors like information, communication,

machinery, services, and mining.

Figure 1 FDI inflow

21

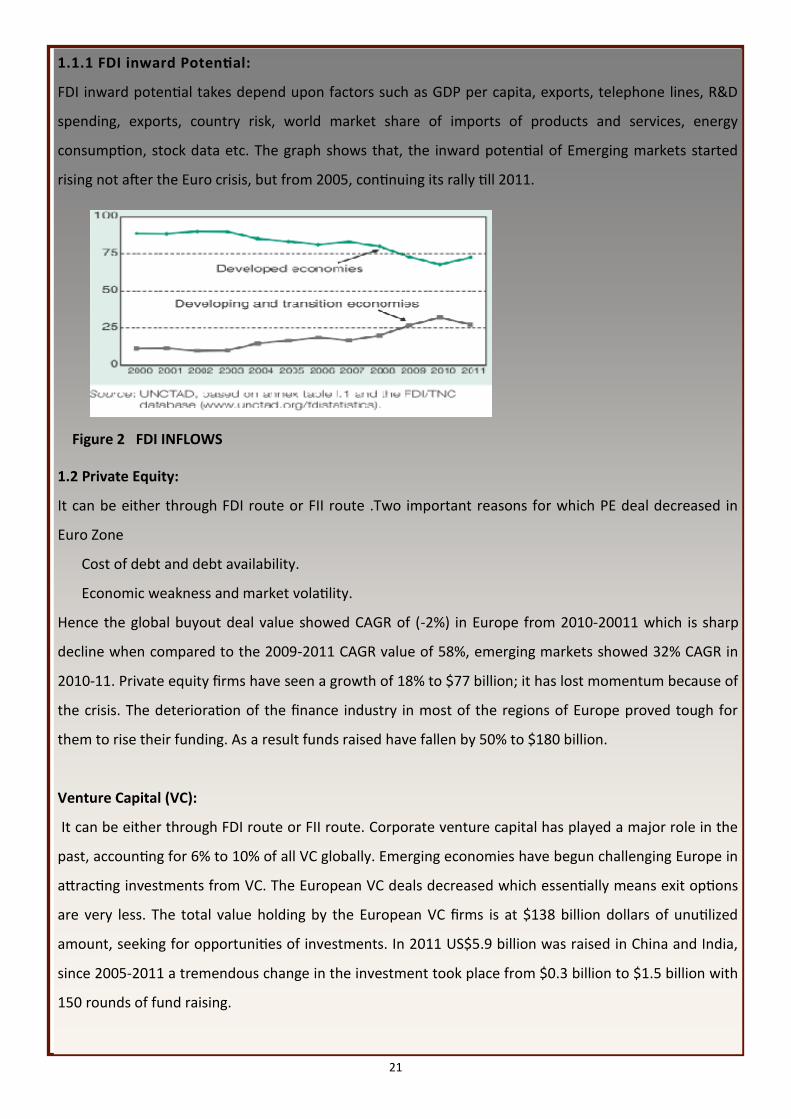

1.1.1 FDI inward Potential:

FDI inward potential takes depend upon factors such as GDP per capita, exports, telephone lines, R&D

spending, exports, country risk, world market share of imports of products and services, energy

consumption, stock data etc. The graph shows that, the inward potential of Emerging markets started

rising not after the Euro crisis, but from 2005, continuing its rally till 2011.

Figure 2 FDI INFLOWS

1.2 Private Equity:

It can be either through FDI route or FII route .Two important reasons for which PE deal decreased in

Euro Zone

Cost of debt and debt availability.

Economic weakness and market volatility.

Hence the global buyout deal value showed CAGR of (-2%) in Europe from 2010-20011 which is sharp

decline when compared to the 2009-2011 CAGR value of 58%, emerging markets showed 32% CAGR in

2010-11. Private equity firms have seen a growth of 18% to $77 billion; it has lost momentum because of

the crisis. The deterioration of the finance industry in most of the regions of Europe proved tough for

them to rise their funding. As a result funds raised have fallen by 50% to $180 billion.

Venture Capital (VC):

It can be either through FDI route or FII route. Corporate venture capital has played a major role in the

past, accounting for 6% to 10% of all VC globally. Emerging economies have begun challenging Europe in

attracting investments from VC. The European VC deals decreased which essentially means exit options

are very less. The total value holding by the European VC firms is at $138 billion dollars of unutilized

amount, seeking for opportunities of investments. In 2011 US$5.9 billion was raised in China and India,

since 2005-2011 a tremendous change in the investment took place from $0.3 billion to $1.5 billion with

150 rounds of fund raising.

22

1.4 Trading Volume:

The debt and equity market of emerging markets has showed a positive trend since 2005.

Figure 3: Debt and Equity Flows

Debt Instruments:

From the recent quarter of 2012, among the instruments traded across the world Brazilian

instruments, according to EMTA (Emerging Market Trade Association) making $250 billion

turnover a 34% increase from $187 billion previous year. Followed by Mexican debt instrument,

with a turnover of $230 billion an 8% increase and then Russian instrument in 3rd position with

turnover $ 130 billion. The total debt instruments of Emerging markets contribute to $1.43 trillion

a decline of 17% although this is a sign of volatility and many investors followed buy and hold

strategy expecting future returns.

CDS: CDS also traded at $218 billion for this quarter 2012, main reason being China’s slowdown in the

second quarter and a marginal improvement in Euro zone.

Bond Issuance: Emerging markets issued bonds and raised more than $300 billion and it was due to

investors’ belief about emerging markets as well as high yield on bonds

Funds: Emerging markets have attracted more than $21 billion in debt funds according to EPFR global

source data released.

Corporate issuance has touched $255 billion.

1.5 Exit opportunities:

When VC investors evaluate the exit possibilities for emerging markets, they look at only two routes

Selling to Private Equity Firms

IPO

Since the emerging markets like Brazil, India, China, Mexico showed a positive trend in IPO and private

equity investments; emerging markets are safe and attractive haven for Venture Capitalist and PE

23

investors to enter and exit.

2. HOW INVESTORS VALIDATE INVESTMENT DECISIONS?

2.1 Credit Rating of Country

The credit rating of a country gives a broad perspective about the country’s economic and political sce-

nario. With the rating for almost all Emerging markets remain stable to positive except for Egypt due to

political turmoil .For India; S&P rated B with negative outlook due to political and economic slowdown.

On the other hand European Union which was hit by the crisis was given a higher rating except for

Greece still the outlook for countries are negative.

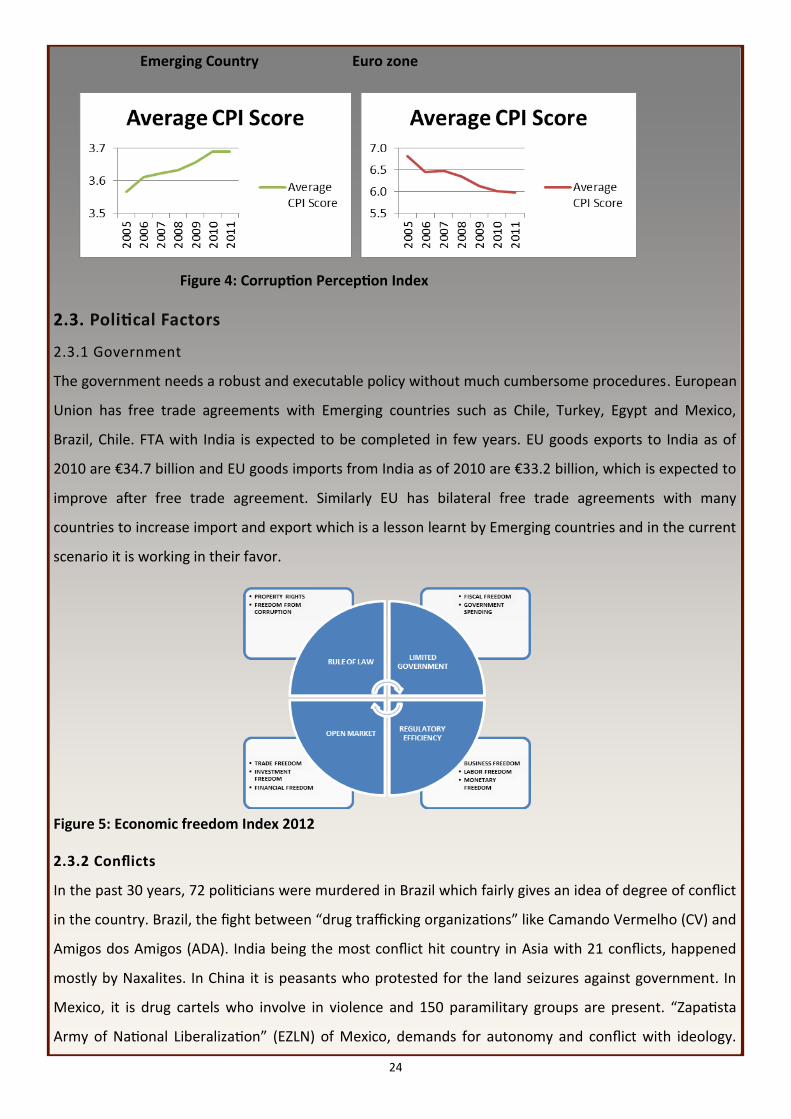

2.2 Corruption

One of the important reasons for Euro zone crisis is corruption in Greece. India’s case of 2G spectrum

allocation, common wealth games scam, coal allocation scam. China, Mexico, Brazil, Russia are not an

exception. Investors started demanding safety and security for their efforts as part of the policy reforms

in order to invest, hence with increase in corruption decrease in investors’ interest to invest.

2.2.1 Corruption Perception Index (CPI) Ranks

Germany 14,Ireland 19,Chile 22,France 25, Spain 31, Portugal 32, Turkey 61, Italy 69, Greece 80, India 95,

Indonesia 100,Mexico 100, Egypt 112, Russia 143. Most of the European countries scored better rankings

in the CPI index. But in the past seven years “Corruption Perception Index Ranking” of the Emerging

markets and Euro zone is shown below.

Country Moody's/Outlook Fitch/Outlook S&P/Outlook

Emerging Brasil Baa2/Stable BBB/Stable BBB/Stable

Turkey Ba1/Positive BB+/Positive BB+/Positive

Russia Baa1/Stable BBB/Positive BBB/Stable

Mexico Baa1/Stable BBB/Stable BBB/Stable

Indonesia Baa3/Stable BBB-/Stable BB+/positive

India Baa3/Stable BBB-/Stable BBB-/Negative

Egypt B-/Under Review B+/Negative B/Negative

Chile

China Aa3/Positive A+/Stable AA-/Stable

European France Aaa/Negative AAA/Stable AA+/Negative

Italy Baa2/Negative A-/Negative BBB+/Negative

Germany Aaa/Negative AAA/Stable AAA/Negative

Ireland Ba1/Negative BBB+/Negative BBB+/Stable

Portugal Ba3/negative BB+/Negative BB/Negative

Greece C/Substantial Risk CCC/Negative CCC/Stable

Credit rating July 2012

24

Emerging Country Euro zone

Figure 4: Corruption Perception Index

2.3. Political Factors

2.3.1 Government

The government needs a robust and executable policy without much cumbersome procedures. European

Union has free trade agreements with Emerging countries such as Chile, Turkey, Egypt and Mexico,

Brazil, Chile. FTA with India is expected to be completed in few years. EU goods exports to India as of

2010 are €34.7 billion and EU goods imports from India as of 2010 are €33.2 billion, which is expected to

improve after free trade agreement. Similarly EU has bilateral free trade agreements with many

countries to increase import and export which is a lesson learnt by Emerging countries and in the current

scenario it is working in their favor.

Figure 5: Economic freedom Index 2012

2.3.2 Conflicts

In the past 30 years, 72 politicians were murdered in Brazil which fairly gives an idea of degree of conflict

in the country. Brazil, the fight between “drug trafficking organizations” like Camando Vermelho (CV) and

Amigos dos Amigos (ADA). India being the most conflict hit country in Asia with 21 conflicts, happened

mostly by Naxalites. In China it is peasants who protested for the land seizures against government. In

Mexico, it is drug cartels who involve in violence and 150 paramilitary groups are present. “Zapatista

Army of National Liberalization” (EZLN) of Mexico, demands for autonomy and conflict with ideology.

25

Comparatively Euro zone had lesser conflicts and ranked better in conflict barometer

2.4 Economic Factors

2.4.1. Microeconomic factors include demand for product, labor force, skill sets, and labor laws and

wage (both compulsory wage rate proposed by Government and general wage demand)

2.4.2 Macroeconomic factors include volatility in inflation rate, exchange rate, interest rates and tax rate

Main macroeconomic indicators are GDP, Industrial production and trade balance, current account

balance, unemployment rate.

2.4.2.1 Industrial Production, Current Account surplus/deficit: Europe has showed a positive trend in

industrial production though it is marginal 0.6%, while India posted a yearly average of 6.8%, and China

9.4%, Mexico with 4% .Industrial production for Emerging economy slipped because of weak demand

from the Euro area. In India exports grown by 2% in contrast to 21% increase. India has current account

deficit of 4.3 %( % of GDP) which is lowest since economic crisis of 1991.Brazil showed a sharp bounce

back in exports hence trade deficit decreased. Russia bounced back to 5.5% of GDP. The whole of Euro

area showed a current account deficit of 0.6% of GDP

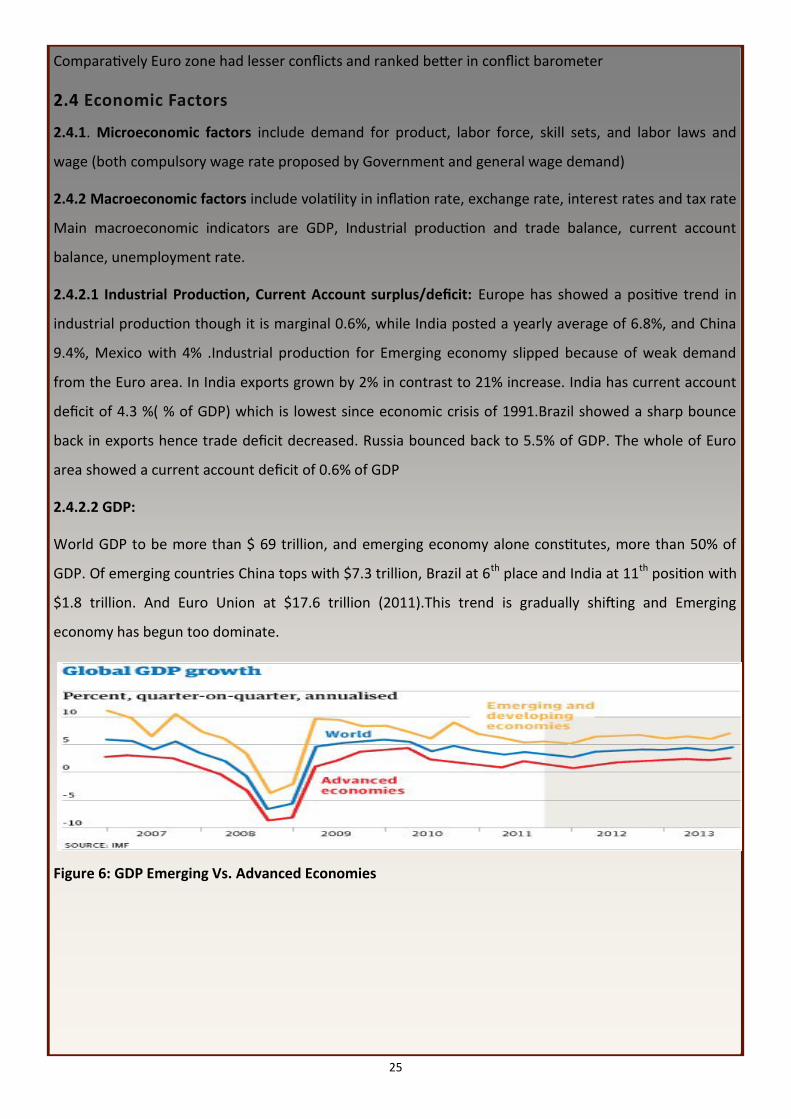

2.4.2.2 GDP:

World GDP to be more than $ 69 trillion, and emerging economy alone constitutes, more than 50% of

GDP. Of emerging countries China tops with $7.3 trillion, Brazil at 6th place and India at 11th position with

$1.8 trillion. And Euro Union at $17.6 trillion (2011).This trend is gradually shifting and Emerging

economy has begun too dominate.

Figure 6: GDP Emerging Vs. Advanced Economies

26

2.4.2.3 Unemployment Rate:

The unemployment rate of Euro zone has reached a new high of 11.6%, whereas emerging markets are

at around 5.9%.

2.4.2.4 Inflation Rate (Wholesale Price Index)

Annual inflation rate for the Europe Union is estimated to be 2.5% including all items such as food, alco-

hol, tobacco, energy, non energy industrial goods. Compared to countries such as Germany (2%), France

(1.9%), Spain (3.5%), Portugal (2.9%), China (1.9%), Mexico (4.77%), Brazil (5.28%), Russia (6.6%), India

has the highest inflation rate of around 7.8%.

3. CONCLUSION

Investors looking at emerging economy favorably because of rapid industrialization , high economic

growth, marked improvement in Infrastructure, aggressive business environment, connectivity,

education (Employable population), Information Technology, technological advancements, resilience to

crisis like situation, improvement in quality of life . Since emerging markets not only believe in

investments from across boundaries but create a “self economy” environment, this is to meet our own

demand hence many emerging markets are not much affected by crisis situation. Although investments

across these markets partially declined due to cautious move by investors to withhold investments and

partially due to reduced demand from Euro Zone. Few demerits such as weak legal and institutional

frameworks/systems, unpredictable tax regimes, transfer and convertibility risk, volatile operating

environment- social /political investors hamper investment. But merits of emerging market such as policy

reforms in such a way to remain resilient, lesser intense domestic shocks, aggressive entrepreneurial

environment overcome the demerits, making the emerging markets a favorable destination for investors

Kunal Sanghvi

SIMSREE

27

BANK CONSOLIDATION:AN OVERHYPED IDEA ?

INTRODUCTION

Consolidation in the banking industry is one of the

most crucial issues facing the Indian financial

sector at present. The logic of consolidation in

Indian banks is twofold. First, it is generally

accepted that India has too many banks of national

spread and it will help the cause of a strong banking

industry to reduce the number of banks through

permitting greater consolidation in the industry.

Secondly, going forward, increasing globalization in

financial sector and opening up of Indian banking

industry progressively to the foreign banks will

require Indian banks to be globally competitive

wherein size of the banks will be one of the most

important dimensions.

The Raghuram Rajan Committee, in general, has

recommended to encourage, but not force,

consolidation amongst Public Sector Banks (PSBs).

The Committee has observed that given the

fragmented nature of the Indian banking system

and the small size of the typical bank, some

consolidation may be in order for banks that aim

to play on a larger stage.

The reasons for consolidation in India are the

following:

Basel Norms: Basel III requires banks to meet

tougher and higher capital adequacy

norms such as capital allocation towards

operational risk, in addition to credit and

market risks. According to the Reserve

Bank of India‟s report on “ Currency and

Finance „‟ released on September 4, 2008,

the banking sector would require an

additional capital of Rs 5,68,744 cr in the

next five years. This is based on the

assumption that banks would maintain

Capital –to Risk –weighted Assets ratio

(CRAR) at 12. 5%. Over the next five years,

28

PSBs would require Rs 3,69,115 cr (64.9% of

total requirements , old private sector banks

Rs 23,319 cr (4.1%). New private sector

banks Rs 113,180 cr (19.9%), and foreign

banks Rs 63,131 cr(11.1%). To maintain the

51 per cent minimum government share,

PSBs cannot collect additional capital

directly from the public and with this view it

promotes bank mergers. Consolidation may

be a route for smaller banks to infuse funds

to strengthen their capital base.

Fragmented Size

It is felt that India has many commercial

banks that are very small. That is of the 53

domestic

banks (both

public and

private ), the

size of 16

banks at end

March 2007

individually

was less than

0.5 percent of

size of the

banking sector. Indian banking industry is

highly skewed and almost 67 banks have a

less than 2.0% market share in India. There

should be a small number of large banks

rather than a large number of small banks so

that Indian banks could keep up with the

growing balance sheets of large Indian

companies and play a role in big takeover .

To Attain Global Competitiveness: Indian

banks are not able to compete globally in

terms of fund mobilization, credit

disbursal, investment and rendering of

financial services. The main reason behind

it is the size of the industry. In 2008, there

was only one Indian lender - SBI, at eighth

place among the top 25 Asian banks.

Industrial and Commercial Bank of China,

the biggest Asian bank and the world’s

eighth biggest bank, is four times bigger

than SBI, both in terms of tier-I capital as

well as assets. Another recent study

„Report on Currency and Finance‟ released

by the RBI reveals that

the combined assets of

the five largest Indian

banks - SBI, ICICI Bank,

Punjab National Bank,

Canara Bank and Bank of

Baroda are just about

half the asset size of the

largest Chinese bank,

Bank of China. The bank

is 3.6 times larger than

SBI in terms of assets, branches and

profits.

Indian banking industry

The banking industry in India has been in the

process of transformation and consolidation ever

since 1961. The Banking Regulation Act, 1949

empowers the regulator with the approval of the

29

government to amalgamate weak banks with

stronger ones. Majority of the mergers in India have

been crafted to bail out weak banks to safeguard

depositors’ interest and to protect the financial

system. The report of the Committee on Banking

Sector Reforms (the Second Narasimham Committee

- 1998), however, discouraged this practice. It

recommended a multi-tier banking system with

existing banks to merge into 3-4 international banks

at the topmost level, 8-10 national banks engaged in

universal banking at the next level and local and rural

bank confined.

Following are the existing strengths and weaknesses

of the Indian banking system and potential

opportunities and threats if it undertakes

consolidation by M&A as an avenue of inorganic

growth.

Strengths

Liquidity:. Banks are required to keep a

stipulated proportion of their total demand

and time liabilities in the form of liquid assets

which affect their liquidity position. RBI has

been easing the requirements with several

rounds of reduction in the Statutory Liquidity

Ratio (SLR) and Cash Reserve Ratio (CRR).

Sound banking systems: The banking system in

India has generally been stable and sound in

terms of growth, asset quality and

profitability. It is because of healthy, prudent

and well capitalized policies and practices

implemented by the RBI from time to time.

Weaknesses

Competition from foreign banks: Foreign

banks will be soon allowed to spread their

business in India which will create intense

competition for Indian banks. The RBI

Report on Currency and Finance presents

the view that mergers are the only way to

face competition from foreign banks.

High level of fragmentation: There is a high

level of fragmentation, especially among

cooperative banks, as compared to some

of the advanced economies of the world,

which poses a serious threat to their

profitability and viability in conducting

business.

Lack of product differentiation: The financial

products offered by banks in India are

similar across the industry with no

distinctive features, thereby leading to

unhealthy competition.

Low penetration: There is an uneven

distribution of banking services in the

country. It is limited to few customer

segments and geographies only. There is a

need for banks to open branches at these

locations and establish connectivity with

the help of a core banking solution.

Opportunities

Advanced technology: New generation

private sector banks and foreign banks are

technologically more advanced in terms of

management information systems,

delivery mechanisms, etc. These systems

30

and processes require substantial

investments which may be possible after

consolidation.

Basel norms: Basel III requires banks to meet

tougher and higher capital adequacy norms

such as capital allocation towards operational

risk, in addition to credit and market risks.

Many Indian banks, especially public sector

banks, cooperative banks and regional rural

banks are unprepared for this

implementation due to capital inadequacy.

Cost cutting: Many branches and ATMs of various

banks are congregated in the same areas

leading to pointless outlay on premises,

manpower and maintenance facilities.

Consolidation may lead to redeployment and

rationalization of such infrastructure, human

resources and other administrative facilities

thereby undercutting the cost factor.

Enlarged customer base: The combined

customer base may increase the volume of

business. The enhanced rural branch network

may lead to increase in microfinance activities

and lending to the agriculture sector. M&A

may be a far-sighted conclusion to increase

the market share.

Geographical spread: Banks can diversify the risk

of concentrated lending through mergers.

They can also have a greater market access

thereby widening the deposit base. The RBI

has imposed strict licensing norms for

opening of new branches and hence via

consolidation, the acquirer will have access to

ready physical infrastructure.

Product diversification: Merger creates the

opportunity to cross-sell products and

leverage alternative delivery channels. Old

generation banks can merge with the new

generation private sector banks and

foreign banks to diversify their credit

profile. They can sell technology-based

innovative products.

Threats

Alignment of technology: The technology

infrastructure, system platforms, network

architecture, database vendors and IT-

enabled synergies should be compatible in

banks desiring to merge. Most of the

public sector banks are at different stages

of technology implementation. It would

pose a stiff challenge to such merging

entities to integrate their technology and

working platforms.

Customer dissatisfaction: The change in the

nature and quality of financial products

may dissatisfy the customers, even if the

products are better. In some cases

customers may be deterred by the

acquiring company for various reasons

which may affect brand loyalty of the

combined entity.

Integration of people: The acquirer bank may

have to absorb the entire workforce of

the target bank which may push up the

wage cost. It also requires the integration

31

of the heterogeneous work cultures. The

varied aspects of the work environment, if

not handled properly, may lead to

resentment and shrinkage in productivity.

Marginalization of small customers: Larger enti-

ties may neglect small customers and concen-

trate on affluent customers or High Net worth

Individuals (HNIs).

Regulatory hurdles: Some of the legal barriers

need to be removed to make PSBs, which still

control about 68 per cent of the Indian

banking sector, active participants in the

consolidation process.

Rise of monopolistic structures: They may give

rise to monopolistic structures and lower

competition. Monopolistic entities may

charge higher fees for services rendered in

case there is no effective competition. The

motive should be to increase the size but not

in isolation.

CONCLUSION

The benefits of consolidation far outweigh its

drawbacks. The major gains from merger are the

increase in size of the banks, the strengthening of the

performance of the banks, effective absorption of

new technologies, capability to meet the demand for

sophisticated products and services, strengthening of

risk management systems and the ability to arrange

funding for major development works. Consolidation

leads to cost reduction and revenue enhancement. It

enhances the reach of the banks to the underserved

segment and also reduces the cost of intermediation.

The changing regulatory environment has paved

the way for foreign banks to enter Indian market

with their huge capital reserves, skilled personnel

and cutting edge technology. Mergers will enable

Indian banks to compete effectively with these

foreign banks by enhancing their capital reserves

and improving their operational efficiency and

distribution efficiency.

Aarzoo sharma

MET institute of management

Mumbai University

Krupa shah

MET institute of management

Mumbai University

32

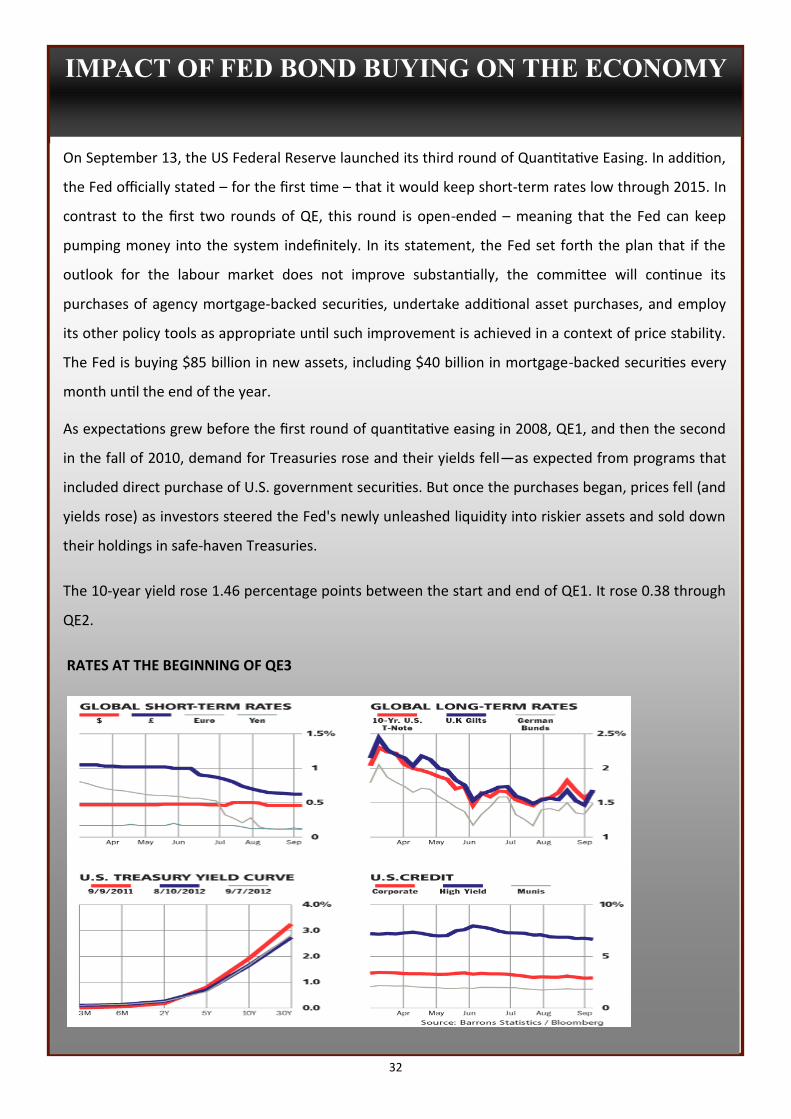

IMPACT OF FED BOND BUYING ON THE ECONOMY

On September 13, the US Federal Reserve launched its third round of Quantitative Easing. In addition,

the Fed officially stated – for the first time – that it would keep short-term rates low through 2015. In

contrast to the first two rounds of QE, this round is open-ended – meaning that the Fed can keep

pumping money into the system indefinitely. In its statement, the Fed set forth the plan that if the

outlook for the labour market does not improve substantially, the committee will continue its

purchases of agency mortgage-backed securities, undertake additional asset purchases, and employ

its other policy tools as appropriate until such improvement is achieved in a context of price stability.

The Fed is buying $85 billion in new assets, including $40 billion in mortgage-backed securities every

month until the end of the year.

As expectations grew before the first round of quantitative easing in 2008, QE1, and then the second

in the fall of 2010, demand for Treasuries rose and their yields fell—as expected from programs that

included direct purchase of U.S. government securities. But once the purchases began, prices fell (and

yields rose) as investors steered the Fed's newly unleashed liquidity into riskier assets and sold down

their holdings in safe-haven Treasuries.

The 10-year yield rose 1.46 percentage points between the start and end of QE1. It rose 0.38 through

QE2.

RATES AT THE BEGINNING OF QE3

33

The Fed is weighing the costs and benefits of its bond purchases. It has a dual mandate: to both

maximize employment and maintain low inflation.

The central bank has pledged to keep the target range for the Federal Funds rate at 0 to 1/4 percent

until the national unemployment rate falls to at least 6.5%, and as long as inflation stays in line with

its 2% target. It anticipates that exceptionally low levels for the federal funds rate are likely to be

warranted at least through mid-2015.

On Feb 26, 2013 Chairman Ben Bernanke stood behind the Federal Reserve's low-interest-rate

policies and sought to reassure members of Congress that the central bank has a handle on the risks.

Bernanke told members of the House Financial Services Committee that the Fed's bond purchases are

needed to boost a still-weak economy and that they have helped create jobs for average Americans.

The bond purchases are intended to lower long-term interest rates. That encourages more borrowing

and spending, which generates growth. However, continually pumping more money into the financial

system, the bond purchases could ignite inflation.

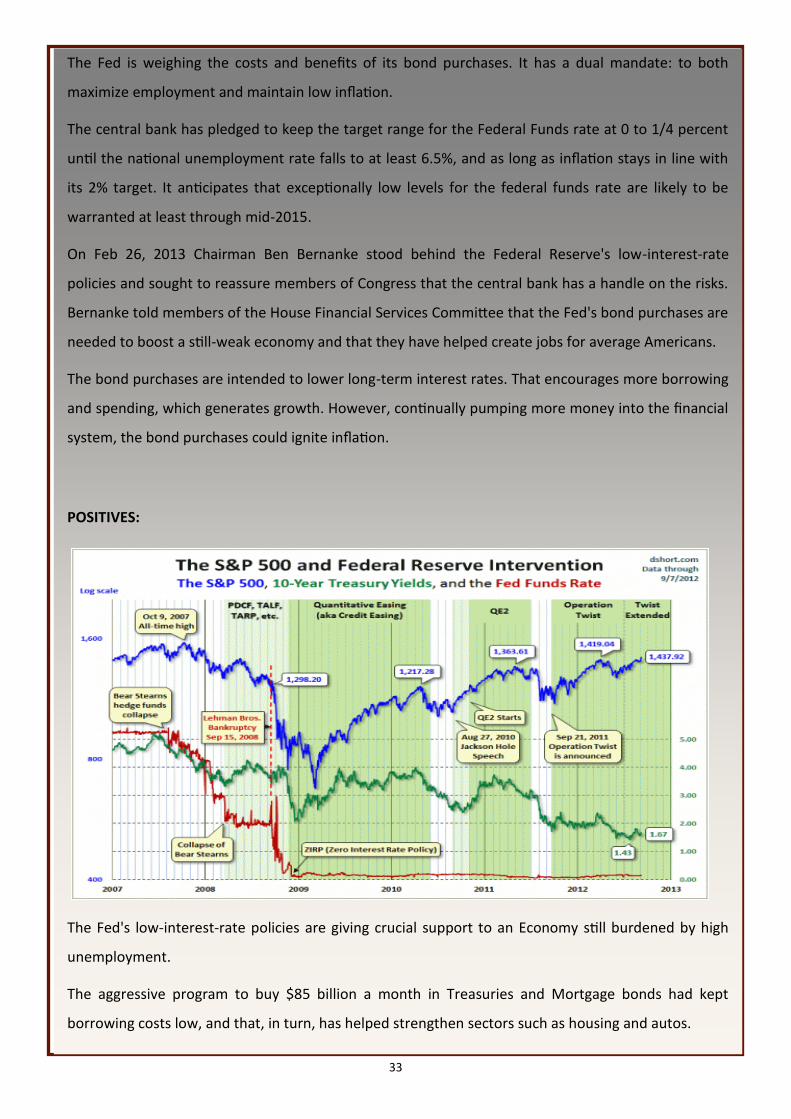

POSITIVES:

The Fed's low-interest-rate policies are giving crucial support to an Economy still burdened by high

unemployment.

The aggressive program to buy $85 billion a month in Treasuries and Mortgage bonds had kept

borrowing costs low, and that, in turn, has helped strengthen sectors such as housing and autos.

34

The Fed estimates are that its policy in recent months has helped create many private-sector jobs.

People are able to buy houses at very low mortgage rates, refinancing at low mortgage rates. People

are able to get car loans at low rates.

The low borrowing costs have boosted demand, and that has helped to lift home prices, making

homeowners feel more financially secure.

US FISCAL CLIFF AND SEQUESTRATION

In the United States, the fiscal cliff was the sharp decline in the federal budget deficit that could have

occurred beginning in early January 2013 due to increased taxes and reduced spending as required by

previously enacted laws. The deficit—the amount by which government spending exceeds its

revenue—was projected to be reduced by roughly half in 2013. The Congressional Budget Office

(CBO) had estimated that the fiscal cliff would have likely led to a mild recession with higher

unemployment in 2013, followed by strengthening in the labour market with increased economic

growth.

Under the fiscal-cliff scenario, some major programs like Social Security, Medicaid, federal pay

(including military pay and pensions) and veterans' benefits would have been exempted from the

spending cuts. Discretionary spending for federal agencies and cabinet departments would have been

reduced through broad cuts referred to as budget sequestration.

Instead, the American Taxpayer Relief Act of 2012 (ATRA) largely eliminated the revenue side of the

fiscal cliff by implementing a higher deficit and a smaller increase compared to the previously enacted

laws. ATRA eliminated much of the tax side of the fiscal cliff while the reduction in spending due to

budget sequestration was delayed for two months.

The raise in revenue contained in the act came from: increased marginal income and capital gains tax

rates relative to their 2012 levels for annual income over $400,000 ($450,000 for couples); a phase-

out of certain tax deductions and credits for those with incomes over $250,000 ($300,000 for

couples); an increase in estate taxes relative to 2012 levels on estates over $5 million; and expiration

of payroll tax cuts (a 2% increase for most taxpayers earning under approximately $110,000). None of

these changes would expire.

Around 2 am EST on January 1, 2013, the U.S. Senate passed this compromise bill by a margin of

89–8. At about 11 pm that evening, the U.S. House of Representatives passed the same legislation

without amendments by a vote of 257–167.U.S. President Barack Obama signed it into law the next

day. However, the budget sequestration was only delayed and the debt ceiling was not changed,

leading to further debate during early 2013.

35

In addition to the income tax rates and spending cuts, the package includes rise in inheritance taxes

from 35% to 40% after the first $5m for an individual and $10m for a couple.

However, President Obama is expected to order the highly-anticipated, much-dreaded

"sequestration" - an across-the-board set of budget cuts totaling $1.2 trillion from defense and

non-defense spending over the course of the next ten years. The administration has been vehement

in its calls for Congress to find a way to avert the legally-mandated package.

The cuts may result in hundreds of thousands of lost jobs, crippling losses for the nation's public

education system, defense cuts that would leave the country unprepared for future military

engagements, and a number of day-to-day inconveniences, like long lines at the airport and the

shuttering of some public parks.

As sequestration officially becomes law of the land, however, its impacts won't immediately be clear.

Despite warnings of an economic turndown, cuts for 2013 may be rolled out over the next several

months, triggering a government slowdown that will hit different agencies with various degrees of

speed and impact as time goes on. And its toll, whatever it ends up being, will likely be drawn out and

murky, with sources nearly unidentifiable to the average voter.

According to the Budget Control Act of 2011, sequestration will cut $85 billion from the federal

budget in the remainder of the 2013 fiscal year, slashing about $1.1 trillion more over the next

decade. The White House has recently released a slew of memos detailing what they believe those

cuts would look like on both a state and program level:

The Office of Management and Budget (OMB) has calculated that sequestration will require an annual

reduction of roughly 5 percent for nondefense programs and roughly 8 percent for defense programs.

However, given that these cuts must be achieved over only seven months instead of 12, the effective

percentage reductions will be approximately 9 percent for nondefense programs and 13 percent for

defense programs.

These large and arbitrary cuts will have severe impacts across the government.

NEGATIVES

Unemployment remains high at around 7.9% and job creation has been weak even with all the

stimulus the Fed has provided, although Inflation has been low and contained.

36

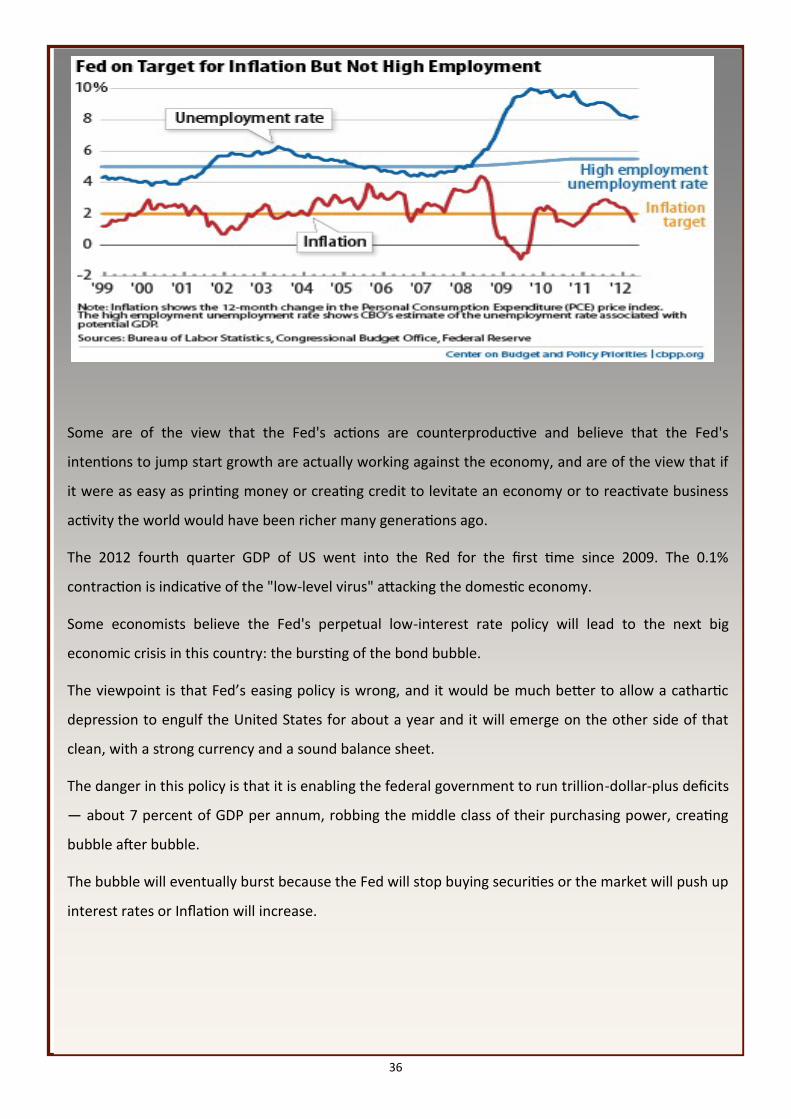

Some are of the view that the Fed's actions are counterproductive and believe that the Fed's

intentions to jump start growth are actually working against the economy, and are of the view that if

it were as easy as printing money or creating credit to levitate an economy or to reactivate business

activity the world would have been richer many generations ago.

The 2012 fourth quarter GDP of US went into the Red for the first time since 2009. The 0.1%

contraction is indicative of the "low-level virus" attacking the domestic economy.

Some economists believe the Fed's perpetual low-interest rate policy will lead to the next big

economic crisis in this country: the bursting of the bond bubble.

The viewpoint is that Fed’s easing policy is wrong, and it would be much better to allow a cathartic

depression to engulf the United States for about a year and it will emerge on the other side of that

clean, with a strong currency and a sound balance sheet.

The danger in this policy is that it is enabling the federal government to run trillion-dollar-plus deficits

— about 7 percent of GDP per annum, robbing the middle class of their purchasing power, creating

bubble after bubble.

The bubble will eventually burst because the Fed will stop buying securities or the market will push up

interest rates or Inflation will increase.

37

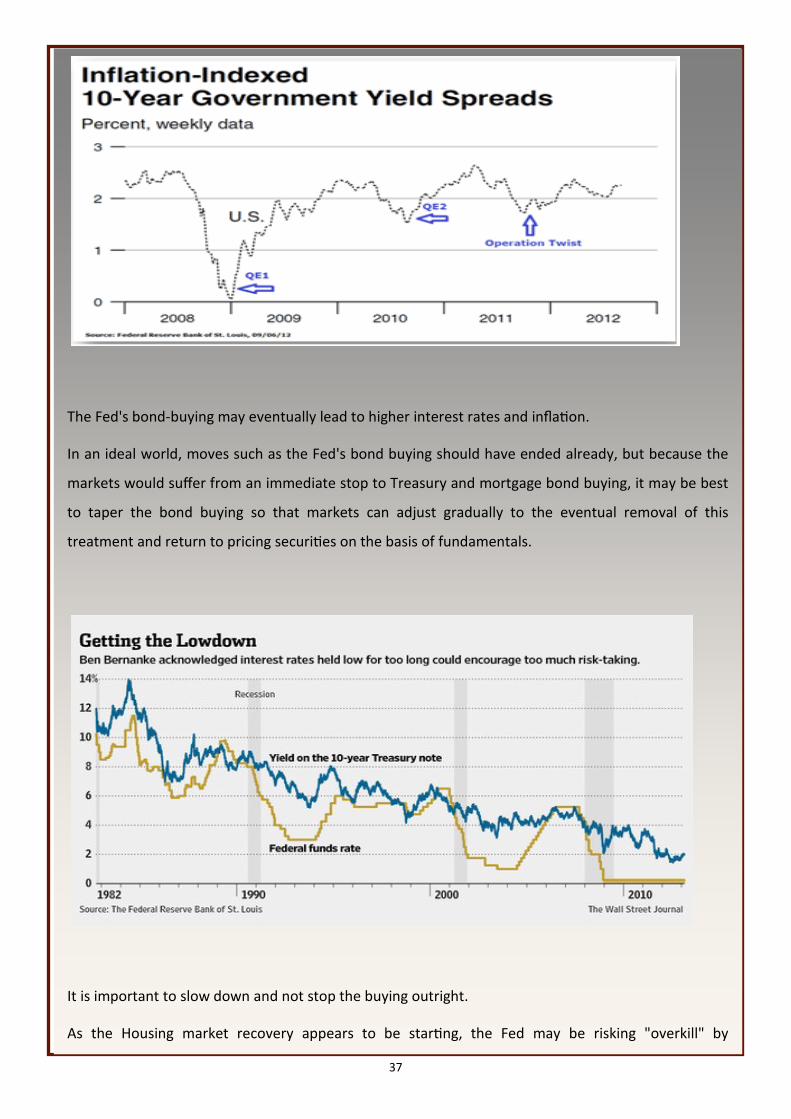

The Fed's bond-buying may eventually lead to higher interest rates and inflation.

In an ideal world, moves such as the Fed's bond buying should have ended already, but because the

markets would suffer from an immediate stop to Treasury and mortgage bond buying, it may be best

to taper the bond buying so that markets can adjust gradually to the eventual removal of this

treatment and return to pricing securities on the basis of fundamentals.

It is important to slow down and not stop the buying outright.

As the Housing market recovery appears to be starting, the Fed may be risking "overkill" by

38

continuing to buy the bonds that support that sector.

The wealth effect of Fed stimulus has been unbalanced. Main Street does not seem to have been

impacted to the same degree as Wall Street

Also, Huge market gains seen under recent rounds of Fed interventions may be illusions. Credit is

super-abundant and stock market behavior is conditioned not so much by the fundamental

performance of its underlying companies but by increasing Money being pumped into the Economy.

Ultimately, it appears Fed policy right now may be counterproductive to its goals.

The Fed's legal mandate to promote maximum sustainable job growth may turn out to be a bad idea

as it draws the central bank into political issues it naturally wants to avoid.

The fears a rapidly rising interest-rate environment might cause the Fed to lose money are overdone

due to the way the central bank accounts for its holdings, but there is a concern that the Congress

might forget how much money the Fed has returned to the Treasury in the form of excess profits over

recent years.

When it eventually comes time to raise rates and tighten monetary policy, the difficulty of exiting will

be much more difficult than the theoreticians believe.

Conclusion:

While the measures taken by the Fed seem to be right taking into account the current economic

conditions, only time will tell whether these decisions prove right impact in the Long term.

Yogesh Athale

SIMSREE

39

To subscribe for a personal copy do write us and

keep contributing your articles @

Send feedback at [email protected]

“Beyond the realms of Finance”

MONEY MATTERS CLUB

All Rights reserved, Money Matters Club, The official Finance Club of

IBS Hyderabad

http://moneymattersclub.weebly.com/