Embed Size (px)

Citation preview

The EU clothing market in 2008: Opportunities for Colombian

manufacturersSam Anson

Economist and editorTextiles Intelligence

April 21-22, 2008

Textiles Intelligence

Contents• About Textiles Intelligence and the IAF – 5 mins• Map of the EU and list of member states – 5 mins• Key EU imports of clothing –buyers’ preferences, import trends, markets for

lingerie and swimwear – 35 mins• Key competitive factors when supplying the EU market: demand driven

factors – 30 mins• Coffee break – 15 mins• Key competitive factors when supplying the EU market: supply driven factors

– 15 mins• Case study: H&M – 5 mins• Emerging sectors: Performance fabrics and apparel and home textiles – 10

mins• Recommendations – 10 mins• Q&A – 20 mins

Textiles Intelligence

About Textiles Intelligence• International provider of independently

researched reports on the international fibre, textile and clothing markets

• Formed as a spin off from the Economist Intelligence Unit (EIU), part of the Economist Group

• Publishes four subscription-based publications– Textile Outlook International– Global Apparel Markets– Technical Textiles Markets– Performance Apparel Markets Textiles

Intelligence

Subscription reportsTextile Outlook

InternationalTechnical Textile

MarketsPerformanceApparel Markets

Global ApparelMarkets

25% discount for all conference delegates Textiles

Intelligence

The International Apparel Federation and Global Apparel Markets

Textiles Intelligence

• The IAF is a worldwide knowledge network that collects and disseminates information, statistical, benchmarking and otherwise, on developments in apparel design, manufacturing, distribution, sourcing, trade and technology.

• politically neutral global association• open to entrepreneurs and executives from the apparel chain

worldwide. • Members include national clothing associations and companies

whose core business is sourcing, designing, development, manufacturing, distribution, and retailing of apparel products.

• Associate members include educational institutions and companies that supply textiles, accessories, equipment, technology, and services to the apparel industry.

The International Apparel Federation and Global Apparel Markets

Textiles Intelligence

• The mission of the IAF is to develop business contacts which foster dialogue, and knowledge exchange between individuals active in the world apparel value chain:

• for the betterment of business practices • for the promotion of the international image of the apparel business • for the advancement of technology and the promotion of its' use • for the encouragement of innovation and new ways of thinking • for the growth of apparel trade worldwide • for the improvement of social, health and safety, and environmental

conditions relating to the apparel chain worldwide, and • for the advancement of apparel related education and training. • Annual conference. 2008 conference is in Mastricht, Netherlands

The International Apparel Federation

Textiles Intelligence

The International Apparel Federation

Textiles Intelligence

• If you have any questions regarding the IAF, please contact

Mrs. Nadia van StadenPR & CommunicationsP.O.Box 428, 3700 AK ZEIST, The NetherlandsE_ [email protected]_ +31 30 - 232 09 08F_ +31 30 - 232 09 99

Over 50% discounts

Textiles Intelligence

15 Individual reports referred to in this presentation:

Significant discount for delegates:• Buy World Textile and Apparel Trade and

Production Trends for US$495 (normal price US$1,030 each)

• Buy any other report for US$295 each• Buy 5 or more reports for US$195 each• Buy 10 or more reports for US$95 each

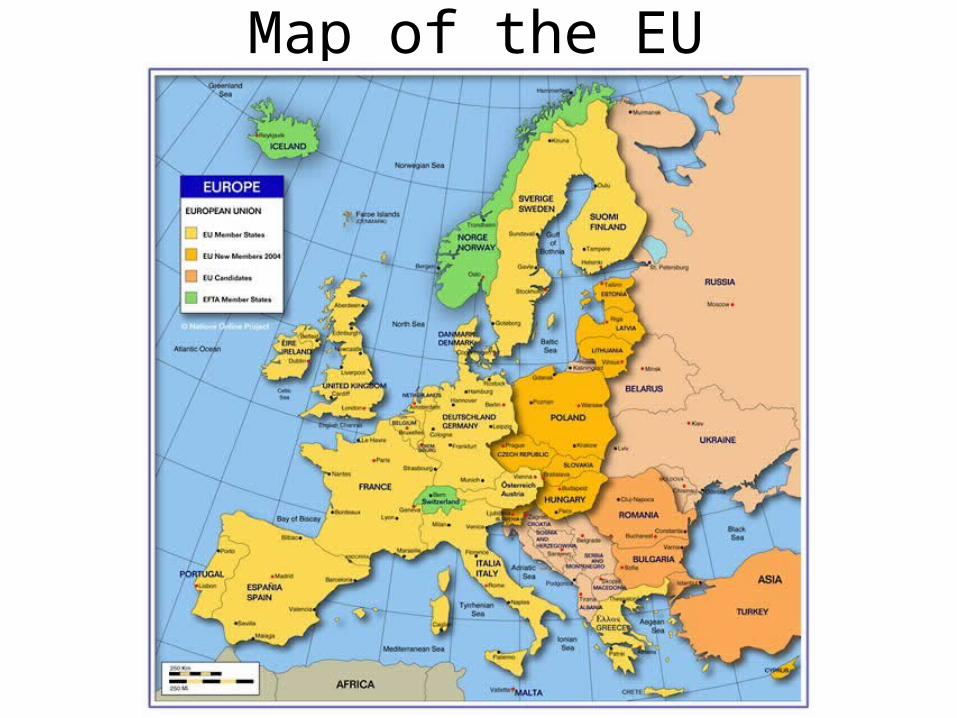

Map of the EU

15. Latvia16. Lithuania17. Luxemberg18. Malta19. Netherlands20. Poland21. Portugal22. Romania23. Solvakia24. Slovenia25. Spain26. Sweden27. United Kingdom

EU member states1. Austria2. Belgium3. Bulgaria4. Cyprus5. Czech Republic6. Denmark7. Estonia8. Finland9. France10. Germany11. Greece12. Hungary13. Ireland14. Italy

The EU market in 2006

• EU clothing imports were worth US$141 bn, or 45% of world trade in 2006

• Almost half of the EU’s clothing come from inside the EU

• More than 200 countries supplied the EU in 2006• Countries in N and S America produced just 1.3% of

the EU’s clothing in 2006• Many EU firms are outsourcing manufacturing

operations to lower cost locations abroadTextiles Intelligence

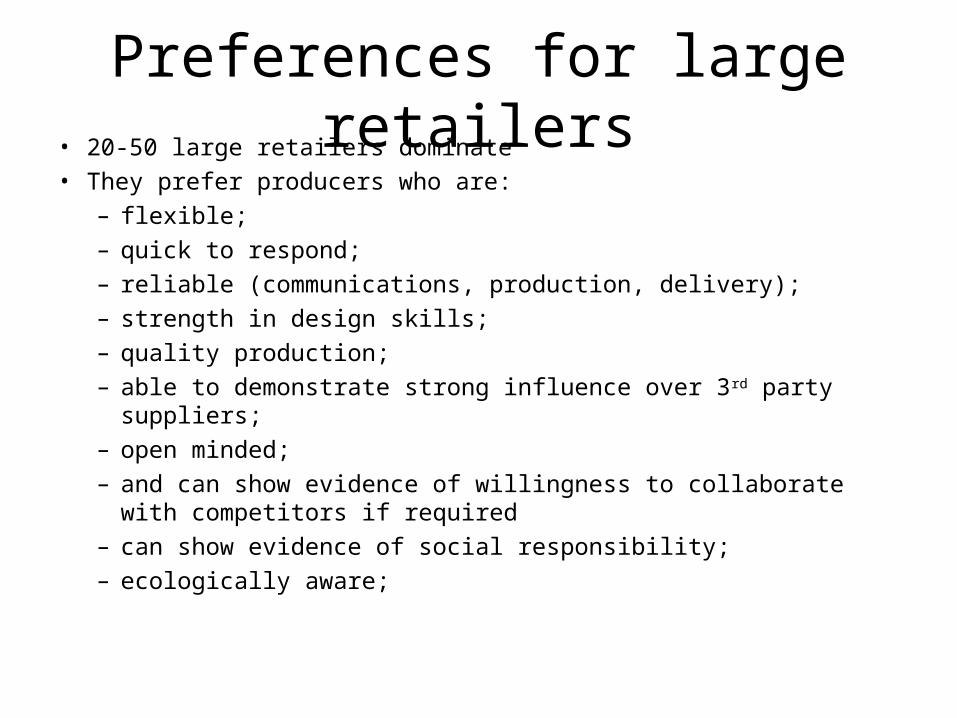

Preferences for large retailers• 20-50 large retailers dominate• They prefer producers who are:

– flexible;– quick to respond;– reliable (communications, production, delivery);– strength in design skills;– quality production;– able to demonstrate strong influence over 3rd party suppliers;– open minded;– and can show evidence of willingness to collaborate with competitors if

required– can show evidence of social responsibility;– ecologically aware;

Brief history of EU trade:2000-07

Textiles Intelligence

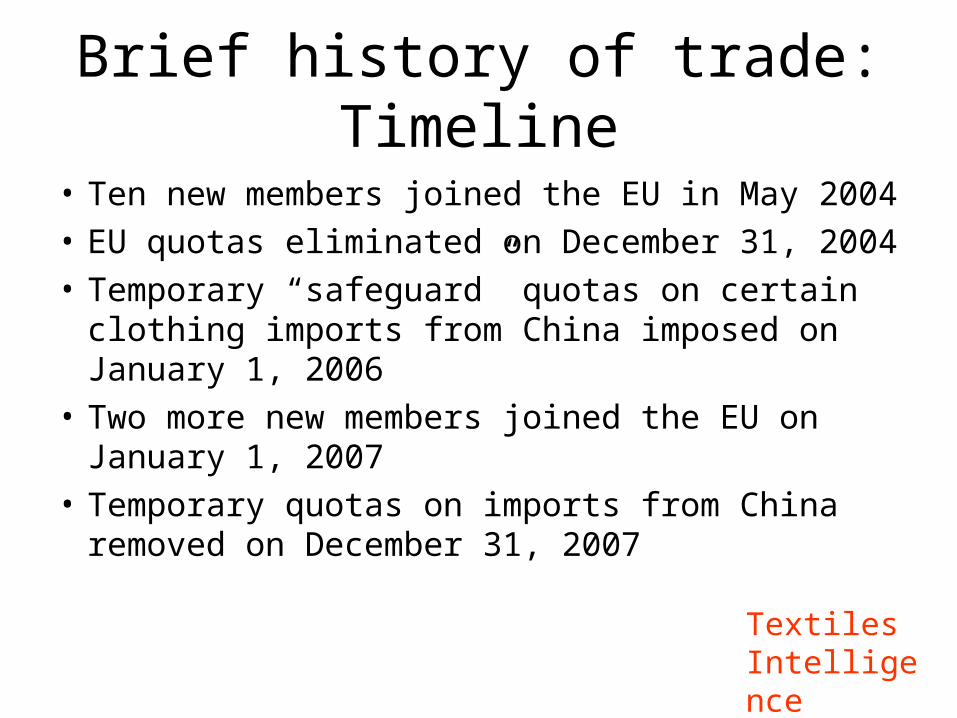

Brief history of trade: Timeline

• Ten new members joined the EU in May 2004• EU quotas eliminated on December 31, 2004• Temporary “safeguard” quotas on certain

clothing imports from China imposed on January 1, 2006

• Two more new members joined the EU on January 1, 2007

• Temporary quotas on imports from China removed on December 31, 2007 Textiles

Intelligence

EU25 before quota elimination

Textiles Intelligence

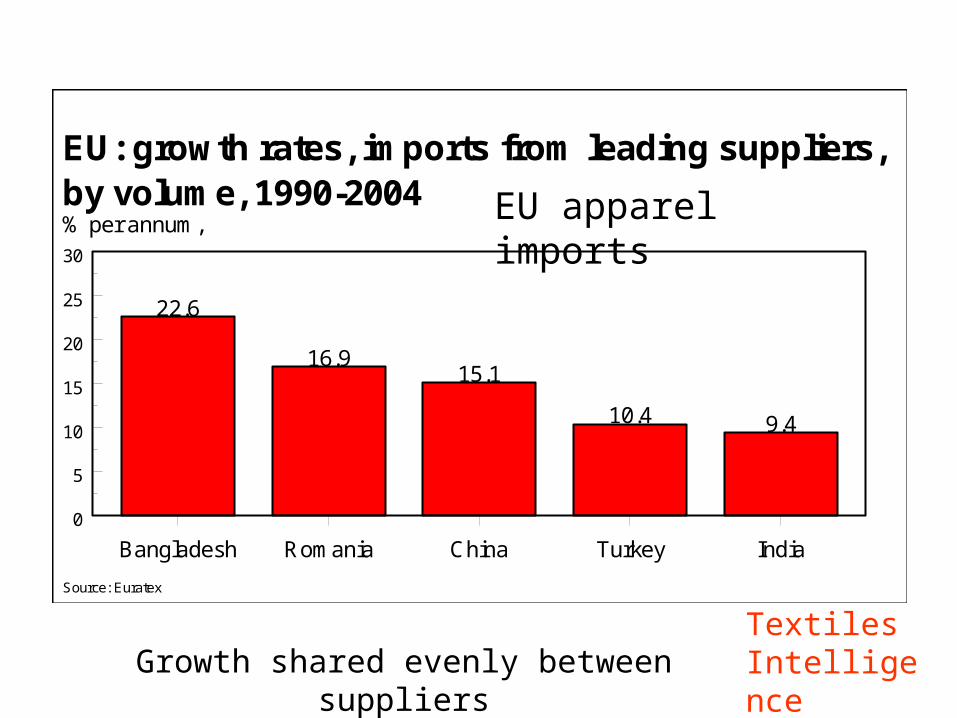

EU: growth rates, imports from leading suppliers, by volume, 1990-2004

Source: Euratex

Bangladesh Romania China Turkey India0

5

10

15

20

25

30

22.6

16.915.1

10.4 9.4

% per annum, EU apparel imports

Growth shared evenly between suppliersTextiles Intelligence

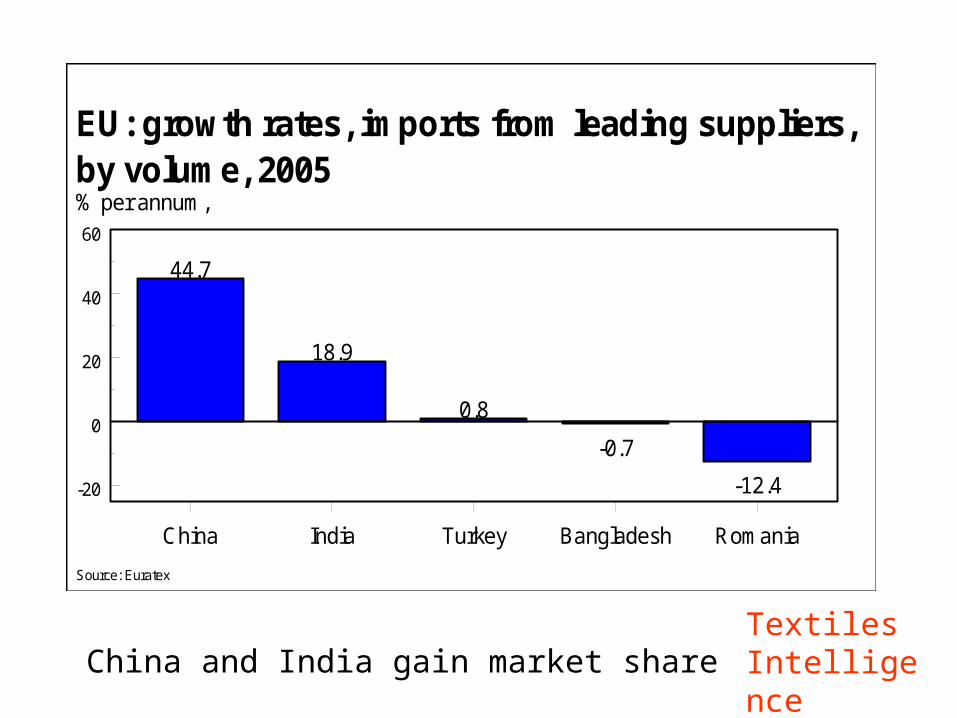

EU25 imports in 2005 (after quota elimination)

Textiles Intelligence

EU: growth rates, imports from leading suppliers, by volume, 2005

Source: Euratex

China India Turkey Bangladesh Romania

-20

0

20

40

60

44.7

18.9

0.8

-0.7

-12.4

% per annum,

Textiles IntelligenceChina and India gain market share

How did China cope with safeguard quotas introduced in EU in 2006?

Textiles Intelligence

Let’s look at the six clothing categories covered by China

safeguard quotas

Textiles Intelligence

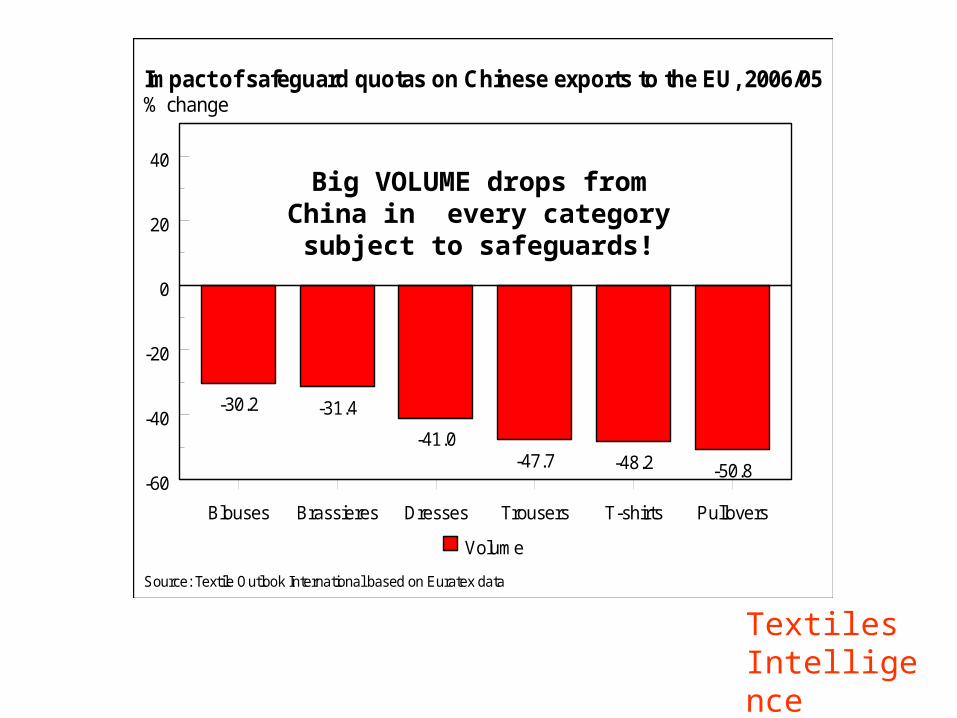

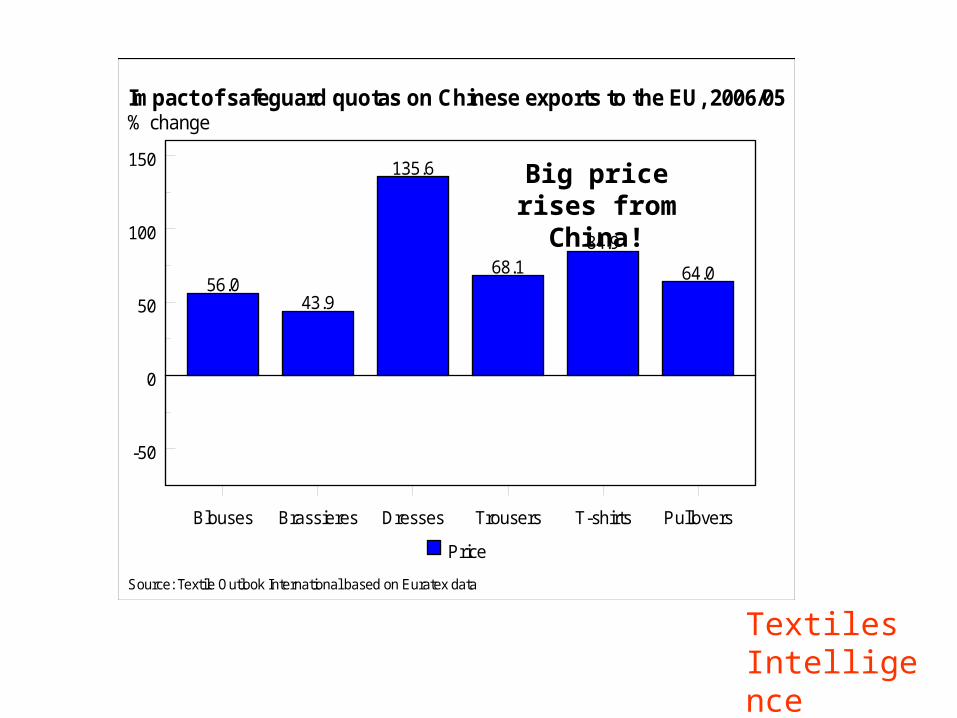

Impact of safeguard quotas on Chinese exports to the EU, 2006/05

Source: Textile Outlook International based on Euratex data

Blouses Brassieres Dresses Trousers T-shirts Pullovers

-60

-40

-20

0

20

40

-30.2 -31.4

-41.0-47.7 -48.2 -50.8

% change

Volume

Big VOLUME drops from China in every category subject to

safeguards!

Textiles Intelligence

Impact of safeguard quotas on Chinese exports to the EU, 2006/05

Source: Textile Outlook International based on Euratex data

Blouses Brassieres Dresses Trousers T-shirts Pullovers

-50

0

50

100

150

56.043.9

135.6

68.184.9

64.0

% change

Price

Big price rises from China!

Textiles Intelligence

How did Vietnam, a competing country, respond to China’s

quotas?

Textiles Intelligence

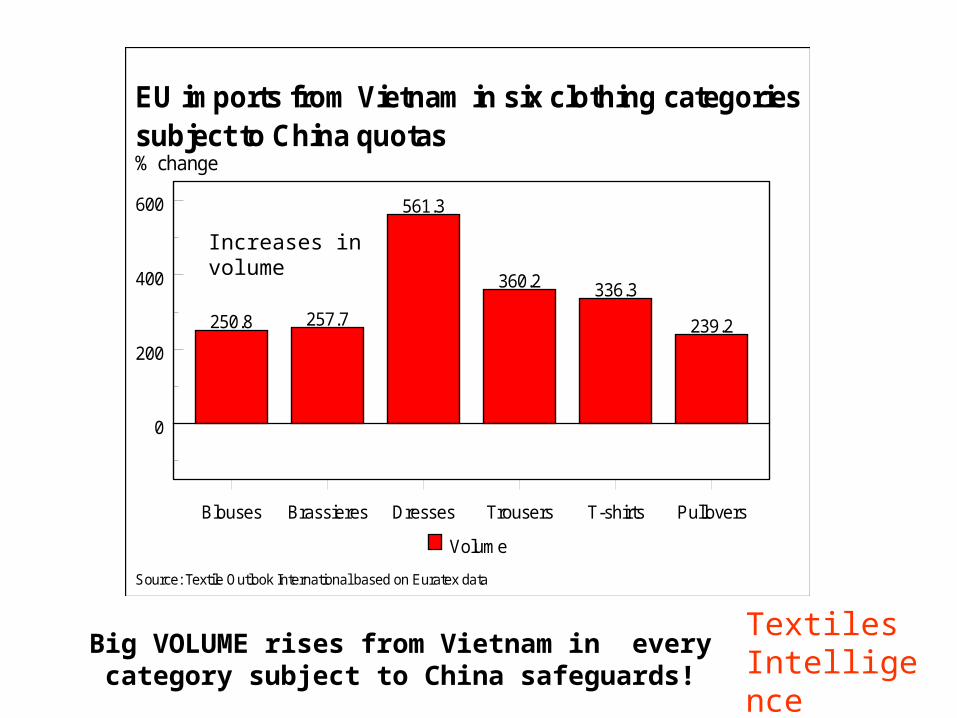

EU imports from Vietnam in six clothing categoriessubject to China quotas

Source: Textile Outlook International based on Euratex data

Blouses Brassieres Dresses Trousers T-shirts Pullovers

0

200

400

600

250.8 257.7

561.3

360.2 336.3

239.2

% change

Volume

Big VOLUME rises from Vietnam in every category subject to China safeguards!

Increases in volume

Textiles Intelligence

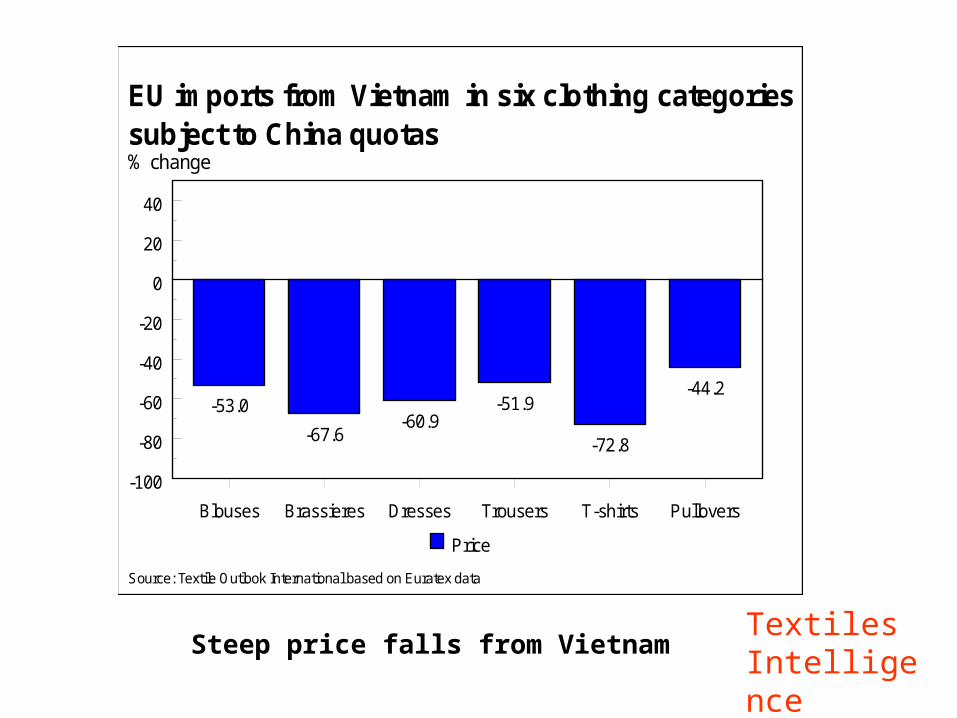

EU imports from Vietnam in six clothing categoriessubject to China quotas

Source: Textile Outlook International based on Euratex data

Blouses Brassieres Dresses Trousers T-shirts Pullovers

-100

-80

-60

-40

-20

0

20

40

-53.0

-67.6-60.9

-51.9

-72.8

-44.2

% change

Price

Steep price falls from VietnamTextiles Intelligence

Nearby suppliers

Textiles Intelligence

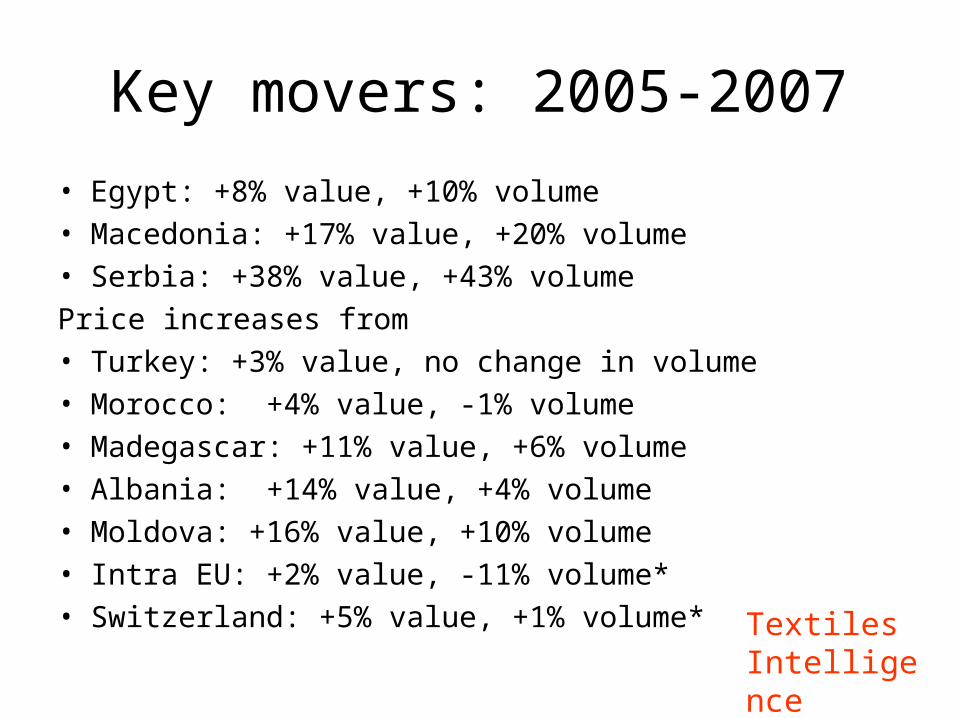

Key movers: 2005-2007

• Egypt: +8% value, +10% volume• Macedonia: +17% value, +20% volume• Serbia: +38% value, +43% volumePrice increases from• Turkey: +3% value, no change in volume• Morocco: +4% value, -1% volume• Madegascar: +11% value, +6% volume• Albania: +14% value, +4% volume• Moldova: +16% value, +10% volume• Intra EU: +2% value, -11% volume*• Switzerland: +5% value, +1% volume* Textiles

Intelligence

High volume Asian suppliers

Textiles Intelligence

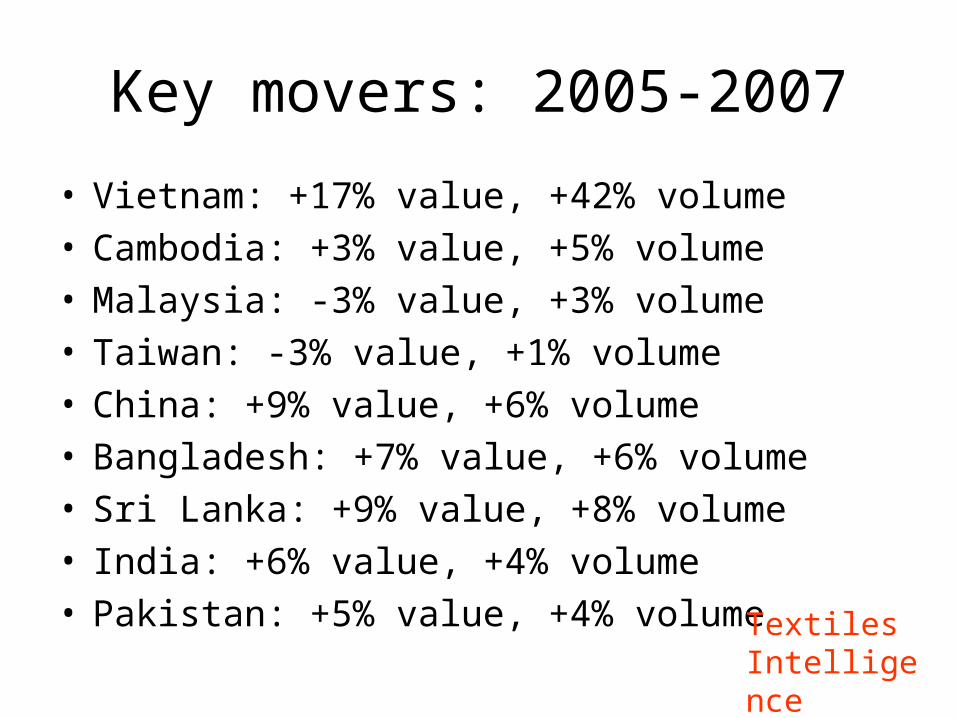

Key movers: 2005-2007

• Vietnam: +17% value, +42% volume• Cambodia: +3% value, +5% volume• Malaysia: -3% value, +3% volume• Taiwan: -3% value, +1% volume• China: +9% value, +6% volume• Bangladesh: +7% value, +6% volume• Sri Lanka: +9% value, +8% volume• India: +6% value, +4% volume• Pakistan: +5% value, +4% volume Textiles

Intelligence

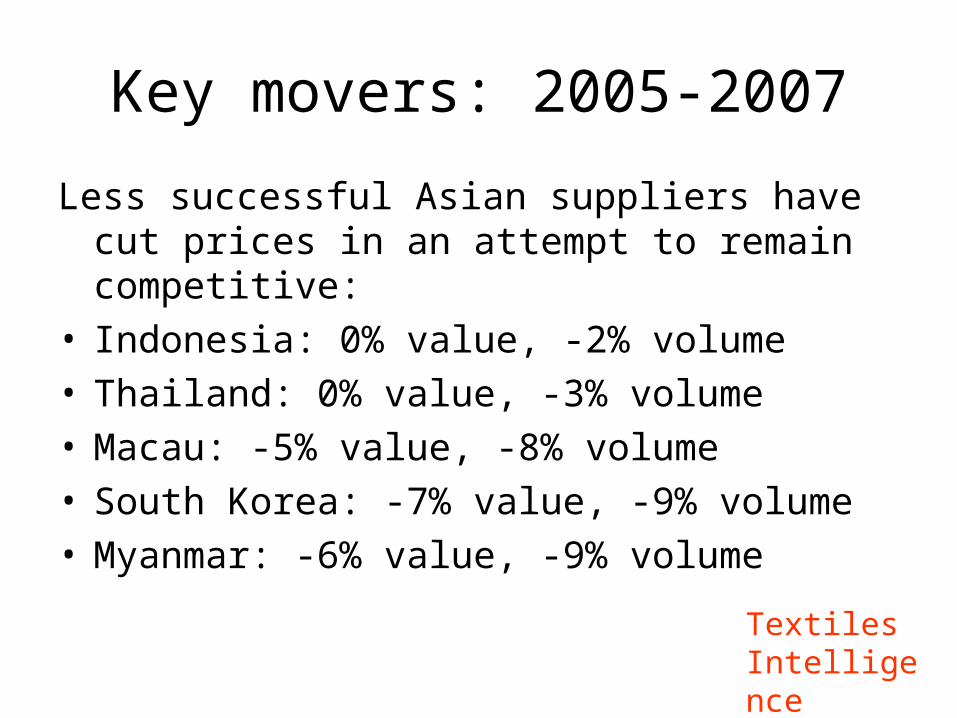

Asian suppliers which are cutting prices in order to compete

Textiles Intelligence

Key movers: 2005-2007

Less successful Asian suppliers have cut prices in an attempt to remain competitive:

• Indonesia: 0% value, -2% volume• Thailand: 0% value, -3% volume• Macau: -5% value, -8% volume• South Korea: -7% value, -9% volume• Myanmar: -6% value, -9% volume

Textiles Intelligence

Key suppliers to the EU market in 2007

Textiles Intelligence

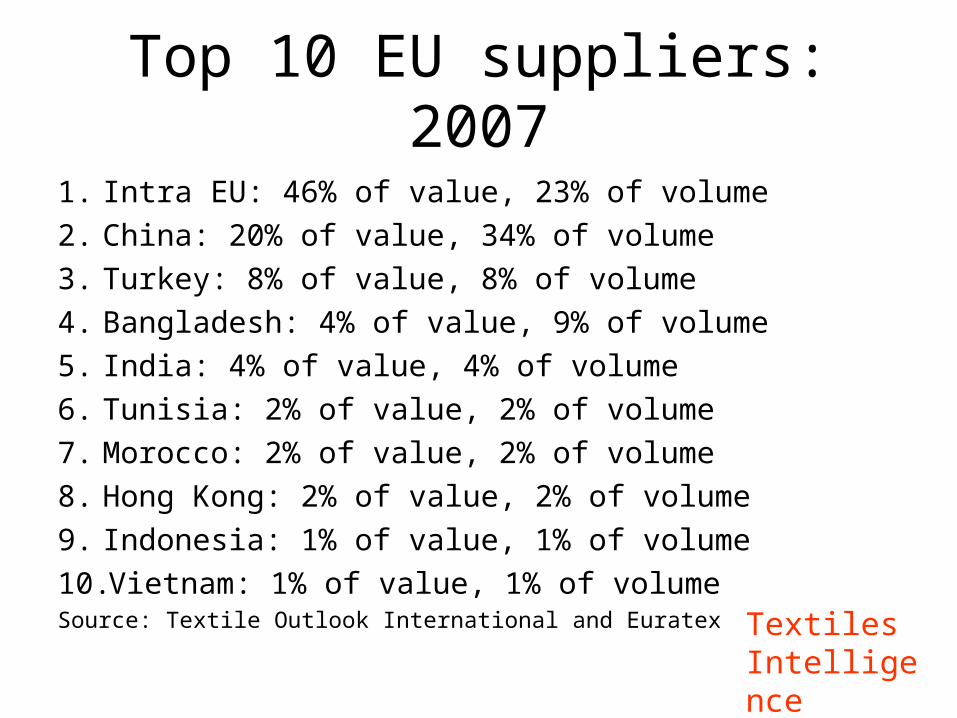

Top 10 EU suppliers: 2007

1. Intra EU: 46% of value, 23% of volume2. China: 20% of value, 34% of volume3. Turkey: 8% of value, 8% of volume4. Bangladesh: 4% of value, 9% of volume5. India: 4% of value, 4% of volume6. Tunisia: 2% of value, 2% of volume7. Morocco: 2% of value, 2% of volume8. Hong Kong: 2% of value, 2% of volume9. Indonesia: 1% of value, 1% of volume10. Vietnam: 1% of value, 1% of volumeSource: Textile Outlook International and Euratex Textiles

Intelligence

Key suppliers of T-shirts and cotton trousers in 2006

Textiles Intelligence

Top 10 T-shirt suppliers

1. Turkey 27%2. Bangladesh 17%3. China 12%4. India 10%5. Mauritius 3%6. Morocco 3%7. Hong Kong 3%8. Tunisia 2%9. Thailand 2%10. Romania (now EU) 2% Textiles

Intelligence

Top 10 suppliers of cotton trousers

1. Turkey 15%2. China 15%3. Bangladesh 12%4. Tunisia 9%5. Romania (now EU) 9%6. Hong Kong 7%7. Morocco 7%8. Pakistan 4%9. India 3%10. Indonesia 2% Textiles

Intelligence

For more information:

For more information on international trade in textiles and clothing, please see:

• “Trends in EU imports of textiles and clothing”, once a year in Textile Outlook International,

• “Trends in US imports of textiles and clothing” - once a year in Textile Outlook International,

• “World trade in textiles and clothing” - once a year in Textile Outlook International,

• “World textile and apparel trade and production trends” – twice a year in Textile Outlook International.

• “Clothing Trade and Trade Policy” – four times aYear in Global Apparel Markets Textiles

Intelligence

EU lingerie market

Textiles Intelligence

European markets for lingerieLow end basic products

Source: Marks & Spencer

Key facts• Worth US$11.3 bn in 2005 (56% bras, 29% briefs)• Germany is the largest market, followed by Italy, the

UK, France, and Spain.• Consumption of items of lingerie per woman rose by

12-13% during 1994-2005 • Average price of bras was US$17.58 per item in 2005.• Italy has highest average prices, followed by Spain,

France, Germany and the UK.

Textiles Intelligence

Key facts• Flurry of merger and acquisition activity, culminating with the

divestment by Sara Lee of its European branded intimate apparel business to Dim Branded Apparel (DBA) in February 2006 and its UK-based Courtaulds private label apparel business in May 2006.

• Future prospects for brands in the bra business appear reasonable.• Briefs market is becoming intensely competitive as sales of

multipacks in supermarkets exert downward price pressure on suppliers and other retailers.

• Nightwear is an important part of the lingerie market• Source: Textile Outlook International – European market for

lingerie

EU swimwear market

Textiles Intelligence

European markets for swimwear

One-piece swimsuit Two-piece bikini

Key facts• Worth US$3.11 bn in 2005.• Forecast to reach US$3.16 bn by 2012. • Innovative and unique designs are very important factors• Italy had the highest sales and highest prices in 2005 and it was

the only country in Europe to experience price increases in swimwear during the year

• Prices are expected to fall in all countries except Italy, Germany and Spain.

• Major differences in cultures between countries –the all in one swimsuit is more popular than the 2-piece bikini.

• Italy is the largest market, followed by Germany, France, the UK and Spain.

Textiles Intelligence

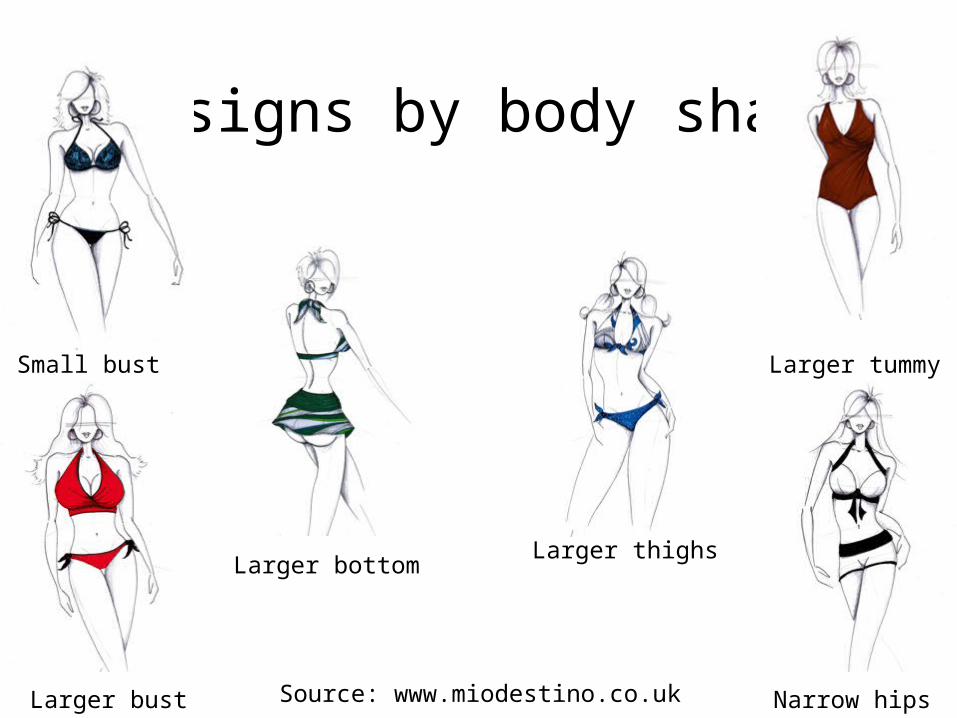

Key factsMain Trends:• Many different styles and designs including

functional designs to help improve wearer’s figure - tummy tuck, cover up – as well as different lines for different body shapes.

• Source: Textile Outlook International – European market for swimwear

Textiles Intelligence

Designs by body shape

Small bust

Larger bust

Larger bottomLarger thighs

Larger tummy

Narrow hipsSource: www.miodestino.co.uk

Key factors when supplying the EU clothing market

Textiles Intelligence

Key competitive factors in supplying the EU market

Market driven factors:• Knowledge of the market

– EU trade policy: under heavy pressure to constant reform from many lobbying groups

– Target customers: largest and fastest growing retailers – keep abreast of their financial performance and sourcing strategy

– Understanding that the EU market is the fastest changing market in the world, mainly driven by oversupply from Asia, extreme fashion trends and increasingly celebrity activity - “gossip” and “styles”

– Understanding sizing, pricing and seasonality is a very important asset

Key competitive factors in supplying the EU market

Market driven factors:• Current socio-economic trends:

– Eco-friendly production– Corporate social responsibility

• Emerging high value sectors: Home textiles and Performance Apparel

Textiles Intelligence www.textilesintelligence.com

EU Market: Key political and commecial lobbying groups

• Key decision-making bodies in EU:– The European Commission– The Council of Ministers– The European Parliament– The European Committee for Standardisation

• Brussels-based industry associations– Euratex– Eurocoton– IWTO (wool) Textiles

Intelligence

EU Market: Key political and commecial lobbying groups

• Key commerce based associations:– AEDT–The European Association of Fashion

Retailers;– Eurocommerce– The Foreign Trade Association (FTA)

• Workers’ representations– European Trade Union Federation

Textiles Intelligence

Sizing

Textiles Intelligence

Sizing– Sizing varies from one EU country to another. All are very

different from USA and LatAm.– EU initiative to standardise sizing but it’s a long way off.

PricingPricing• Prices have fallen for clothing across the board.• Low and Mid priced clothing is very popular and comes from

Asia. However, weak in flair and creativity for design. Quality is generally acceptable, however.

• Low and Mid priced clothing is sold mainly by supermarkets and large high street retailers and basic department stores.

• Much high priced clothing is still produced within the EU but retailers are looking for new suppliers abroad as there is pressure on margins due to high cost of labour, rising energy costs and slow EU economic growth.

• High priced clothing is sold by luxury department stores,independent boutiques, own brand stores and via the internet.

EU markets are traditionally very seasonal.Temperatures and climates vary massively from one country to

another.Southern med countries – hot dry summers, cool but not cold

winters. Sometimes flash rain and thunder storms throughout the year.

North European countries are characterised by cold and wet winters, variable springs, hot summers with unpredictable rain and pleasant autumns.

High end retailers focus on the 2 traditional collections a year.Mid and low end retailers are blurring collections with many

having 6 or more collections a year to encourage a new and fresh attitude to clothing.

Seasonality

Selling via the internet

Textiles Intelligence

Selling via the internet

Textiles Intelligence

• Volume and value of clothing sales via the internet is growing fast.

• Time-poor cash-rich consumers are shopping from home for convenience.

• Established retailers also sell online.• Most established catalogue sales channels are now

done online• The biggest retailers have exclusive websites while

resellers and agents collaborate.• Some stores offer free delivery.

Selling via the internet

Textiles Intelligence

• Internet sales is characterised by:• High % of returns which can be resold as shoppers

cannot try the clothes on before they buy• Lower prices due to lower overheads for retail

space, advertising, staff etc• High levels of cooperation between competitors.• Very low margins for agents and resellers.

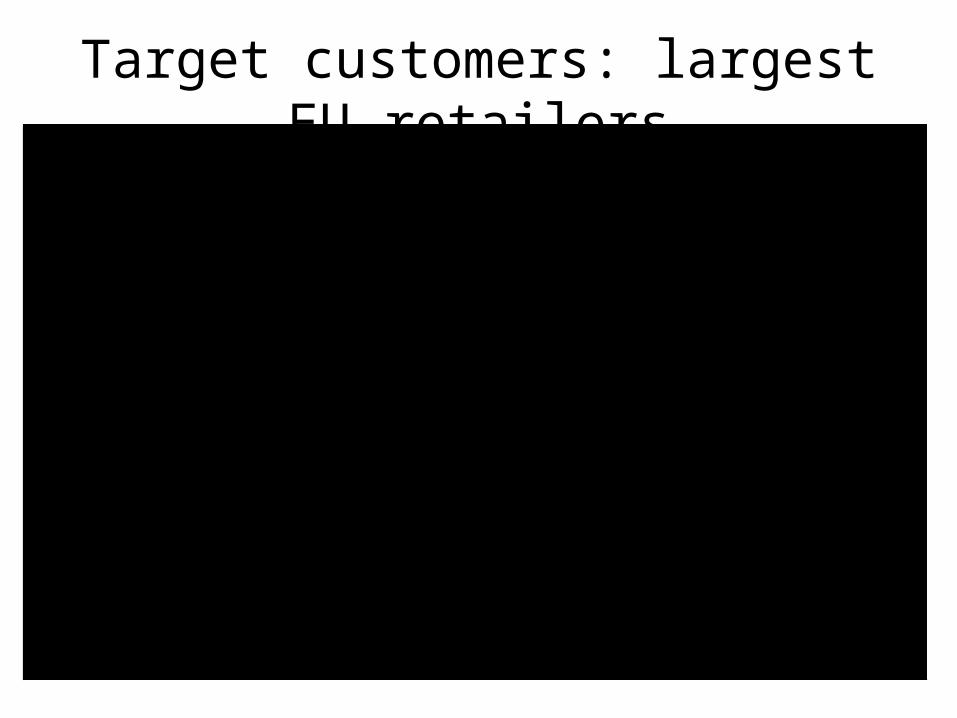

Target customers: largest EU retailersCompany Country Turnover Turnover Profit Stores

2007 2006 2007Inditex Spain 11,181 9,196 1,850 3,131H&M Sweden 10,166 9,105 2,274 1,420C&A Belgium 7,640 na na 1,100M&S UK 7,193 6,586 na >500Next UK 6,615 6,256 1,023 1,095Arcadia Group UK NA 3,565 606 >2,500Asda UK 3,525Esprit Holdings Hong Kong 2,993 2,645 611 >500Primark UK 2,637 2,026 373 160Benetton Italy NA 2,408 246 5,100Mango Spain NA 1,000The Peacock Group UK 1,104 987 na 540Monsoon UK 7,100 977 na naFrench Connection UK 485 495 na naCortefiel Spain 1,100New Look UK na na na 315

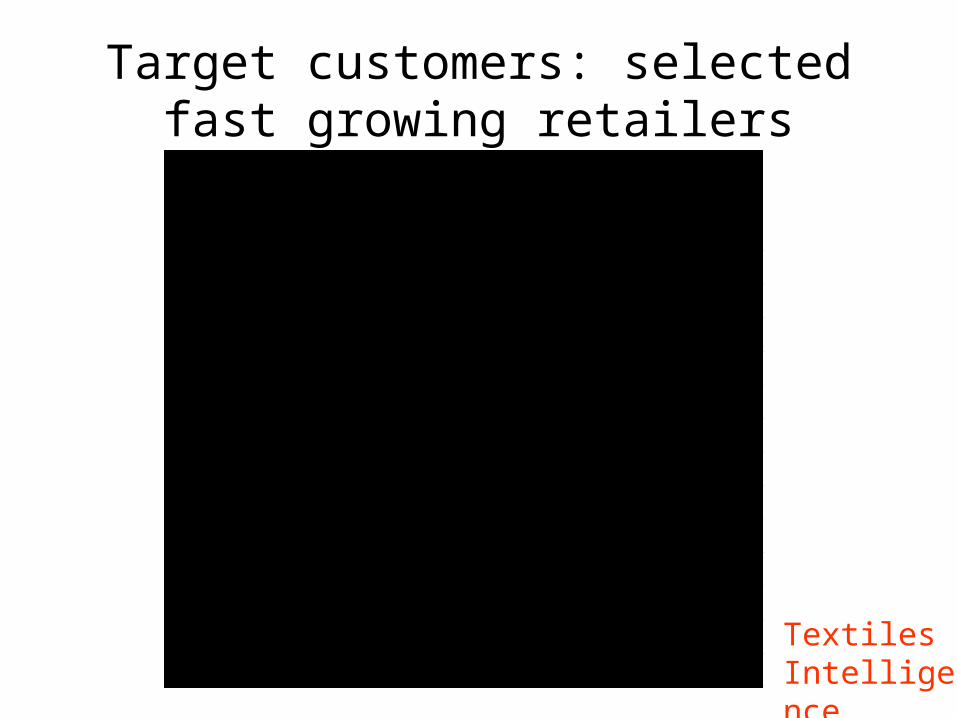

Target customers: selected fast growing retailers

Rank Company Y/Y growth%

1 Primark UK 30.14 The Peacock Group UK 30.15 H&M Sweden 11.76 Mango Spain 10.07 Monsoon UK 626.88 M&S UK 9.29 Benetton Italy NA10 Next UK 5.711 Arcadia Group UK n/s12 French Connection UK -2.013 C&A Belgium NA14 New Look UK NA15 Cortefiel Spain na16 Asda UK na

Textiles Intelligence

Fast growing retailers: The importance of supermarkets in EU clothing retailing

• Supermarkets growing share of UK and EU clothing market

• In UK, Asda and Tesco are in the top 10 largest clothing retailers

• Supermarkets are using convenience, existing distribution, large customer base – online delivery within 24 hours

• Supermarkets are looking to expand range of clothing to higher value added goods

• Reward cards create loyalty Textiles IntelligenceFor more information see “Apparel business update”, Global

Apparel Markets every 3 months

Fast growing retailers: The importance of supermarkets in EU clothing retailing

Textiles IntelligenceFor more information see “Apparel business update”, Global

Apparel Markets every 3 months

Fast growing retailers: The importance of supermarkets in EU clothing retailing

Textiles IntelligenceFor more information see “Apparel business update”, Global

Apparel Markets every 3 months

Tesco’s home page

For more information see “Apparel business update”, GlobalApparel Markets every 3 months

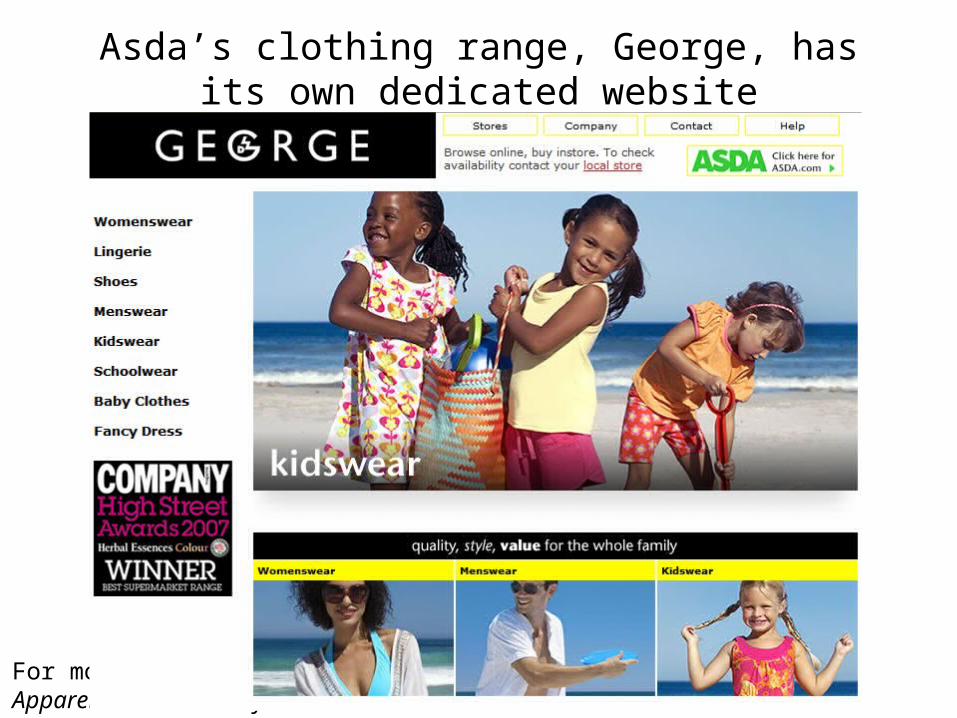

Asda’s clothing range, George, has its own dedicated website

For more information see “Apparel business update”, GlobalApparel Markets every 3 months

Understanding the speed of change of fashion trends

• Good sources of information include:– Global Apparel Markets (a one-stop shop);– The International Apparel Federation;– Just style;– www.iamfashion.blogspot.com– Fashion trade press;– Financial Times;– Fashion supplements to EU tabloid papers;– Major retailer’s websites. Textiles

Intelligence

Spring/Summer collections 2007 vs 2008

2007

Textiles Intelligence

2008

www.iamfashion.blogspot.com

Spring/Summer collections 2007 vs 2008

2007

Textiles Intelligence

2008

www.iamfashion.blogspot.com

Spring/Summer collections 2007 vs 2008

2007

Textiles Intelligence

2008

www.iamfashion.blogspot.com

Major EU fabric fairs

• EU fabric fairs remain important events for high quality fabrics for suppliers to the EU

• Spinners and fabric manufactures have met Asian competition with innovative designs, high quality, fast turnaround times and superior customer service (see later)

• Demand is growing fastest for eco-friendly products – organic cotton and natural dyes

• However, in recent times, Chinese trade fairs have become more important for buyers Textiles

Intelligence

Major EU fabric fairs

• Munich Fabric Start, Germany• Tissu Premier, Lille, France• Milano Unica, Milan, Italy• Texworld, for non-European Textile

Producers, Paris, France• Première Vision Pluriel, Paris, FranceFor more information see “Fabric and Apparel trends and fairs”

in Textile Outlook International twice a year and in GlobalApparel Markets once a year Textiles

Intelligence

Socio-economic trends: Green textiles and clothing

• Green textiles and clothing is becoming an increasingly important factor in the EU market in terms of production and consumers

• Eco labels and official certification– EU Eco label– Organic Cotton

• Retailers’ initiativesFor more information see “Green textiles and clothing” in Textile Outlook

International and “Organic cotton” in Global Apparel Markets

Textiles Intelligence

Socio-economic trends:Corporate social responsibility

• Social responsibility – “giving back to society”:– Worker incentives– Schools– Child care– Charitable donations– Facilities for workers (exercise, restaurants) – Environmental responsibility– Charity donations– Local civil projects – schools, water supply, hospitals,

orphanages Textiles Intelligence

Home textiles

Source: John Lewis Partnership

Emerging sectors: Home textiles• Home textiles include:

– Bathroom textiles– Bedding– Cushions and cushion covers– Table linen– Window dressings (curtains, drapes etc)

• Bedding and window dressings are largest sub sectors – 72% of UK market and 75% of German market

• EU import market was worth Euro5.3 bn in 2006. UK is by far largest market in EU.

• Key suppliers were Turkey (15%), Pakistan (12%), China (11%), India (9%), Portugal (8%), Germany (5%), Belgium (4%), France (3%), Poland (3%), Czech Republic (3%), Italy (2%)

Textiles Intelligence

Emerging sectors: Home textiles

• Common fibres include: Cotton, linen, silk, wool, modacrylic, nylon, acetate, acrylic, polyester, rayon

• Key growth areas:– Innovative functional fabrics

• temperature regulation, odour management, antibacterial coatings, phase change materials, easy care, stain resistance, flame retardancy, fragrance encapsulation, cosmeo textiles, anti-static

– Eco friendly fibres and fabric,– Simple designs are popular in EU market

For more information please see report on “Developments inHome textiles” in Textile Outlook International Sep-Oct 2006 Textiles

Intelligence

Emerging sectors: Performance apparel

• Performance apparel:– Waterproof breathable fabrics;– Temperature regulating fabrics;– Compression clothing;– Antimicrobial technology;– Ultra violet protection;– Insect repellent;– Flame retardent;– Personal protective equipment;– Anti odour;– Anti-static technology

Textiles Intelligence

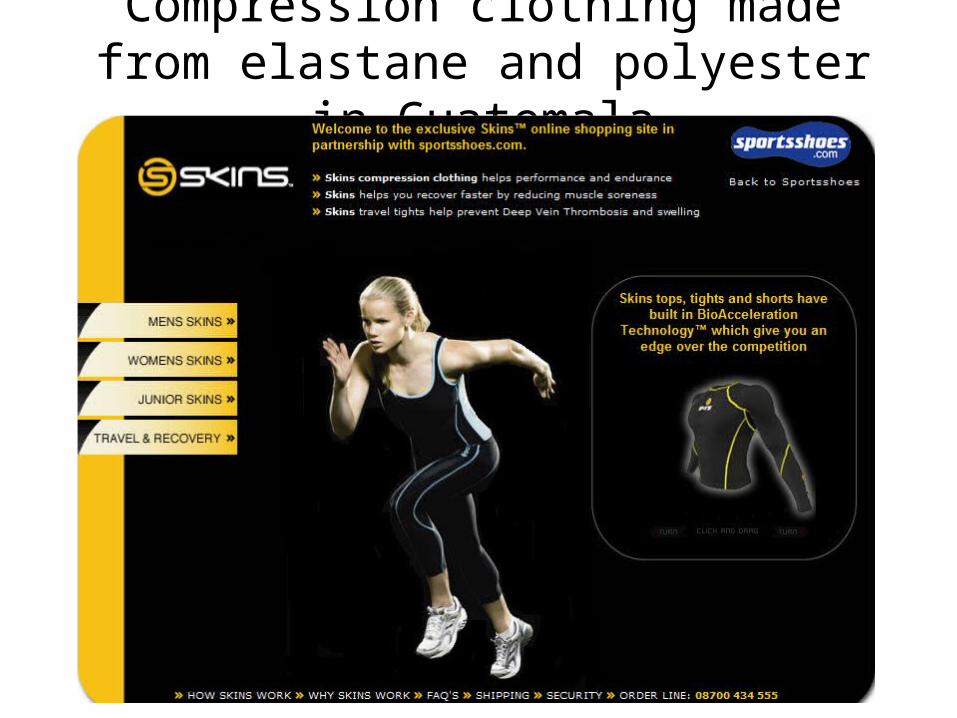

Compression clothing made from elastane and polyester in Guatemala

Trends in sourcing strategies: a case study on H&M

H&M has reacted to:• Highly competitive market• Removal of quotas has meant there’s a situation of

over supply• Fast changing consumer tastes• Heavy influence by media• Large retailers with strong brands have the best

knowledge of the market and the majority of control

Textiles Intelligence

Trends in sourcing strategies: a case study on H&M

• H&M is one of the world’s largest and fastest growing clothing retailers

• Pioneer of fast fashion– Fast fashion refers to the speed at which a retailer

is able to spot a trend on the catwalk and have it available, at an affordable price in the shops

• Achieves this with efficiency and flexibility throughout its supply chain

Textiles Intelligence

Trends in sourcing strategies: a case study on H&M

• H&M has strong knowledge of fashion and is adept at anticipating trends

• This makes it popular with consumers, , especially women, who want to have the most up-to-date fashion items

• It has grown at a formidable rate, despite challenging economic conditions

Textiles Intelligence

Trends in sourcing strategies: a case study on H&M

• H&M’s strategy:– Centralised key functions of design, buying and

logistics;– Decentralised decision making for all other

aspects;– Third party manufacturers;– Regional distribution centres, or “hubs”; – Celebrity endorsement; and– Hi-tech communication technology. Textiles

Intelligence

Trends in sourcing strategies: a case study on H&M

• H&M aims to produce “fashion and quality at the best price” through:– creative designers – Strict quality control– Few middlemen– Buying in large volumes– Comprehensive market knowledge– An extensive supplier portfolio– Efficient distribution Textiles

Intelligence

Trends in sourcing strategies: a case study on H&M

• Corporate social and environmental responsibility– H&M has established a reputation for social and

environmental awareness– All suppliers must adhere to the company’s code

of conduct• Forced and child labour• Full Audit Programme• Environmental legislation on handling of chemicals,

waste management and water treatment Textiles Intelligence

Trends in sourcing strategies: a case study on H&M

• Outlook:– Store expansion will be focused on USA, Europe

and Japan – 1,500 stores at end 2007;– Product diversification – household textiles and

men’s shoes and maybe performance apparel

For more info please see Profile of H&M: pioneer of fast fashion in Textile Outlook International Jul-Aug 2007

Textiles Intelligence

Key competitive supply factorsSupply driven factors to enhance competitiveness in a fast

changing and unpredictable market:• Low labour cost• Relative value of exporting currency• Manufacturing efficiency and quality• Collaboration with local competitors and third parties• Short lead times vs distance to market• Flexibility and responsiveness to clients’ needs• Building of long term relationships with customers• Competitive investment climate with competing countries

(including trade policy and investment incentives)

Textiles Intelligence

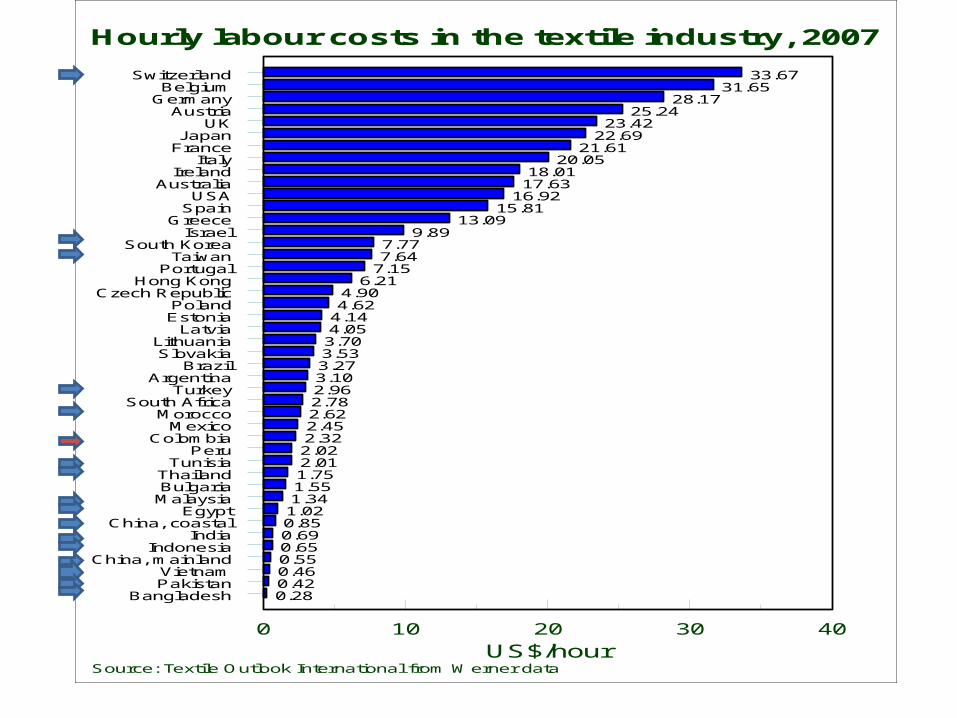

Labour costs in competing countries

Textiles Intelligence

Hourly labour costs in the textile industry, 2007

Source: Textile Outlook International from Werner data

SwitzerlandBelgium

GermanyAustria

UKJapan

FranceItaly

IrelandAustralia

USASpain

GreeceIsrael

South KoreaTaiwan

PortugalHong Kong

Czech RepublicPolandEstonia

LatviaLithuaniaSlovakia

BrazilArgentina

TurkeySouth Africa

MoroccoMexico

ColombiaPeru

TunisiaThailandBulgariaMalaysia

EgyptChina, coastal

IndiaIndonesia

China, mainlandVietnamPakistan

Bangladesh

0 10 20 30 40

33.6731.65

28.1725.24

23.4222.69

21.6120.05

18.0117.63

16.9215.81

13.099.89

7.777.64

7.156.21

4.904.62

4.144.053.703.533.273.102.962.782.622.452.322.022.011.751.551.341.020.850.690.650.550.460.420.28

US$/hour

Relative value of exporting currency

Textiles Intelligence

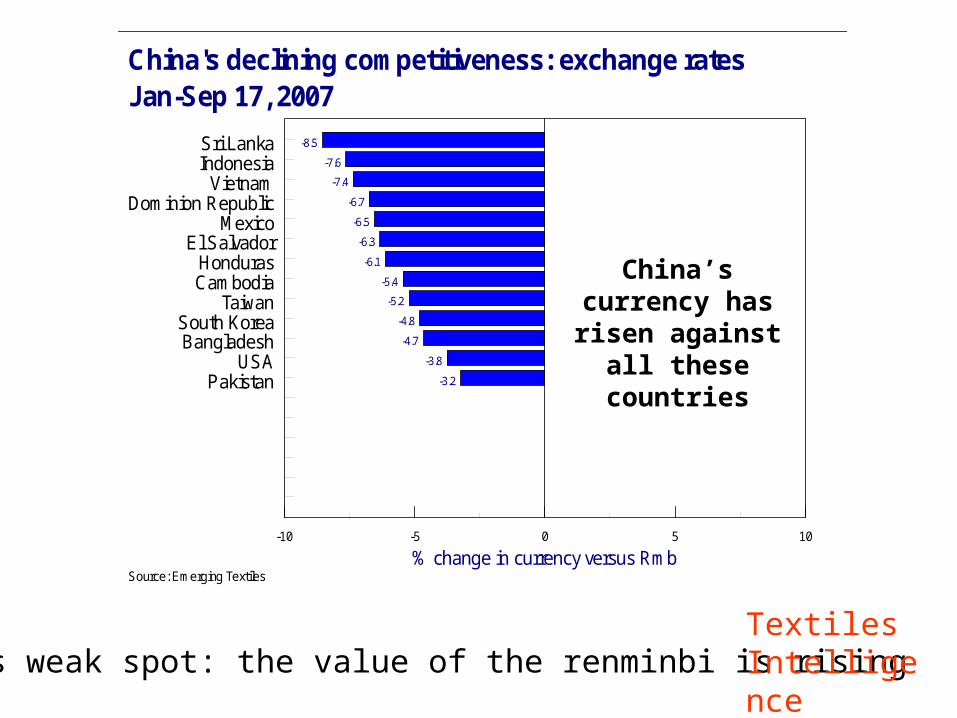

China's declining competitiveness: exchange ratesJan-Sep 17, 2007

Source: Emerging Textiles

Sri LankaIndonesia

VietnamDominion Republic

MexicoEl Salvador

HondurasCambodia

TaiwanSouth KoreaBangladesh

USAPakistan

-10 -5 0 5 10

-8.5

-7.6

-7.4

-6.7

-6.5

-6.3

-6.1

-5.4

-5.2

-4.8

-4.7

-3.8

-3.2

% change in currency versus Rmb

China’s currency has risen against

all these countries

China’s weak spot: the value of the renminbi is risingTextiles Intelligence

Manufacturing efficiency and quality

Buyers look for:• Low operating costs;• Implementation of total quality management systems;• Investment in good quality machinery, perhaps on a modular

basis;• Removal of expensive and unnecessary gadgetry• Machinery which has been designed for low labour costs• Worker incentive schemes for efficiency and quality• Efficient strategy for fabric sourcing and 3rd party services

Textiles Intelligence

Collaboration with local competitors and third party suppliers

Buyers are also impressed with:• Evidence of collaboration with competitors • Evidence of development of specialist production “hubs” or

“clusters”• Evidence of influence over third party suppliers (accessories,

finishing, labels etc)• Efficient capital markets in country • Efficient logistics and communication methods• Strong knowledge of foreign markets

Textiles Intelligence

Other factors

• Short lead times: Speed to market and up-to-date fashion items allows retailers to keep a competitive edge

• Modern Information Technology methods which is compatible with buyers encourages EU customers to do business:– Product Lifecycle Management (PLM);– Three dimensional design and visualisation software;– Virtual fabric samples and catwalk technology;– Radio Frequency Identification labels;

• Collaboration and relationship building with local logistics companies and those in EU can help optimise shipping times

Textiles Intelligence

Flexibility and responsiveness to customer needs

• EU market is changing very fast• Retailers want manufacturers who are flexible and quick to

respond• No sooner has one trend, fashion or “social phase” been

implemented in a product range, a new one is on its way• Flexibility is key to win business in terms of:

– Order size – small versus large;– Quick response – turn around a design in days;– Blurring of conventional seasons;– Integration of emerging products at short notice – lifestyle products,

performance coatings, garment decoration– Incorporation of celebrity “fads” can make a quick buck Textiles

Intelligence

Building long term relationships with suppliers and customers

• EU customers have knowledge of market and knowledge of clothing manufacture

• EU customers don’t have knowledge of suppliers and third parties in less developed countries

• EU customers can keep abreast of changes in trends and have exceptional ability in design and innovation

• EU customers need help from suppliers in terms of producing clothing at low cost quickly and with minimum returns

• Out of a portfolio of 130+ suppliers, retailers have a focus on three or four producers which they have a long term win-win relationship with

For more information, see “Strategies for manufacturers in The post quota era to 2015” in Textile Outlook International Textiles

Intelligence

Recommendations• Use Colombia’s political and social situation to your advantage• If capacity is underutilised, consider collaborating with competitors to

streamline operations and improve efficiency• Create a databook containing key operational performance statistics in

english to put on your website and give to EU customers (see ACI – Agencia de cooperacion y inversion- for template)

• “Shout” about your competitive advantages and achievements through the international textile and clothing press

• Consider establishing a full time press representative to generate and receive press releases

• Collect impressive statistics about your company’s achievements and send the information via press releases to the international community

Textiles Intelligence

Recommendations• Read the textile and clothing business-to-business press every

day to learn what’s going on and to decide your target countries and customers.

• Use internationally-recognised terminology• Update websites in English • List company’s strengths (technology, quality, social

responsibility) in an obvious place. • Update marketing and sales brochures regularly and make sure

the English is well translated• Many large retailers have strict requirements for safety, ecology

and treatment of employees. EU certification in these aspects can be a business winning advantage

Textiles Intelligence

Thank you

Questions and Answers?

Textiles Intelligence