Embed Size (px)

Citation preview

.'

Project 81307 No. 29August 1986

THE ECONOMETRICS OFMODELS WITH RATIONAL EXPECTATIONS

Benny Lee

,

CONTENTS

Summary

1. Introduction

2. Non-rational Expectation Models in Economics

3. The Rational Expectations Hypothesis

3.1 Properties of Muthian rationality3.2 Applications of rational expectations in economics

4. Statistical Identification

4.1 Models with current expectations4.2 Models with future expectations and other

complications

5. Estimation Problems

6. Hypothesis Testing

7. The Lucas Critique of Conventional EconometricPolicy Evalu~tion

8. Conclusion

References

THE ECONOMETRICS OF MODELS WITH RATIONAL EXPECTATIONS

Benny Lee

SUMMARY

Muth's (1961) paper has triggered off the so-called Rational Expectations

revolution in economics research. The rational expectations approach in

modelling economic behaviour has the merit of formalising expectations

according to coherent economic principles rather than ad hoc assumptions

such as those which extrapolate from the past. The hypothesis that

expectations and model structure are interdependent has, however, posed

serious problems for econometricians attempting to identify, estimate,

test and simulate models with rational expectations. Furthermore, it may

not in general be possible to infer empirically whether it is the model

structure or.the rationality hypothesis that has been refuted by the data.

This paper is a review of various econometric problems associated with

models employing rational expectations, with a discussion of possible ways

of overcoming them.

Helpful comments from Brian Fisher, John Spriggs, Steve Beare and other

colleagues at BAE are gratefully acknowledged. The author is, however,

responsible for any error that remains.

1

1. INTRODUCTION

Economics is concerned with human behaviour reacting to both current and

anticipated events. Rational economic decisions are made under conditions

w~ich are partly unknown to the decision makers. In econometric models,

anticipated events are usually represented in the form of unobservable

expectations variables. While it may be convenient to leave the nature of

expectations formation vague when developing economic theories,

quantitative policy evaluation and forecasting have to be based on exact

representation of the expectation variables. This connection becomes more

critical as conflicting forecasts are produced by econometric models using

different expectations assumptions. A notable example is the debate on the

effectiveness of countercyclical policy in the macroeconomics literature

(Sargent and Wallace 1976; Lucas and Sargent 1978).

Before the introduction of Muth's (1961) rational expectations

hypothesis, econometricians made ad hoc assumptions and used simple proxy

variables to replace the unobservable expectations variables in their

econometric models. These proxies could be data from futures markets,

sample surveys, predictions from time series models, econometric model

forecasts and/or the actual values (assuming perfect foresight). With the

introduction of the rational expectation hypothesis, econometricians can

now integrate the specification of both model structure and expectations

formation. One result is to complicate the identification and estimation

of the model. The conventional tool-kit, which originated from the Cowles

Commission (Fisher 1966) and emphasises exclusion restrictions (for

example, that, to distinguish a demand equation from a supply equation,

certain variables should occur in one of the equations), is no longer

adequate.

The object of this paper is to bring together the various

contributions in the literature and to make them more accessible to

economists who wish to familiarise .themselves with the topic. In

section 2, non-rational expectation approaches in economics are reviewed.

Section 3 is a recapitulation of the concept of rational expectations and

of· its manifestations in dif~erent contexts. Sections 4 and 5,

respectively, deal with the identification problem of models with rational

expectations and the problem of estimating these models. In sections 6

2

and 7, respectively, problems of hypothesis testing and policy evaluation

are discussed. ConcluSions and directions for further research are given

in section 8.

2. NON-RATIONAL EXPECTATION MODELS IN ECONOMICS

Expectations, in economics, are essentially forecasts of the future values

of economic variables. It should be noted that, being the personal

judgments of particular individuals, they are essentially subjective.

Usually, an expectation should better be characterised by a probability

distribution than by a single predicted value. However, provided that the

models are linear and stochastic, there is no loss of generality in

summarising the expectation by the mean of the distribution.

Keynes (1936, p.47) stressed that expectations playa major role in

influencing economic decisions. While accepting that expectations are

likely to be revised in the light of new information, Keynes argued that

there may be no explicit mechanism through which individuals assess and

revise an expectation. Thus, in short-run analysis, expectations are

assumed to be exogenously determined. Comparative static analyses of the

behaviour of current endogenous variables are then conducted, conditional

on exogenous shifts in expectations.

The ways in which expectations have been formalised in economics can

be traced through the familiar cobweb model. The essence of this model is

the delay between the formation of production plans and their realisation.

Formally, the system can be written in three simple equations.

d- I3pqt = a t

s y o eqt = + Pt

d sqt = qt

(demand)

(supply)

(market equilibrium)

where p~is some expectation of the price at time t.

3

To close the model, we need an additional equation to describe how p~

is determined in terms of other variables in the model. The cobweb model

imposes the simple hypothesis of naive prediction:

(1) = (naive expectation)

Substituting this equation in the model and solving for the reduced

form:

( 2) Pt = CLi,x - 0 p8" t-l,

which is clearly a non-homogeneous difference equation of order one. The

price variable oscillates over time and mayor may not converge to a

constant equilibrium value, depending on the size of 0113.

Empirically, the cobweb model does not attract much support (see Coase

and Fowler 1935).

TO improve upon the naive expectation assumption, Metzler (1941)

introduced the idea of extrapolative expectations, on the ground that

future expectations should be based not only on the past level of an

economic variable, but also on its direction of change. That is:

( 3)e

p =t

(extrapolative expectation)

where 'a' is called the coefficient of extrapolation.

If a > 0, the direction of the past trend is expected to be

maintained, whereas if a < 0, the direction is expected to be reversed.

For a = 0, the expectation is identical to the naive expectation. The

choice-of the coefficient of extrapolation depends upon the underlying

economic structure of the model. Again, there is little empirical support

for this model.

4

A similar mechanism of expectation formation, usually attributed to

Cagan (1956) or Nerlove (1958) has been based on the assumption that

agents revise their expectations each period according to their previous

expectation errors. That is:

( 4) (adapt I ve expectation)

where 'b' is called the coefficient of adaptation. If b = 1, this reduces

to the naive expectation model. By repeated substitution, it can be shown

that:

<X>

= b E (l_b)i P .. t-,-11=0

This expression has a finite value if and only if 0 < b < 1.

Note that this equation is a specialised version of a general linear

model called, in the time series literature, the autoregressive moving

average model (see Box and Jenkins 1970). This model is suitable for any

series that is stationary (not explosive), and yields the best linear

predictor one step ahead if the only information available is the past

history of the variable (see Granger and Newbold 1973, ch.4).

This type of model has been used successfully in empirical economics

for the past two decades. However, the approach is being criticised as at

best weakly rational because of its backward-looking nature and its

neglect of other information on the economic structure.

3. THE RATIONAL EXPECTATIONS HYPOTHESIS

In an attempt to explain changes in the level of business activity, Muth

(1961) pointed out that the dynamic character of price determination is

very sensitive to the way expectations are influenced by the actual course

of events. He pointed out that fixed expectational formulae fail to allow

for change in expectations when the structure of the system changes.

The basic rationale of the rational expectations hypothesis (REH) is

that rational individuals should not make systematic errors. This idea

makes sense, in that individuals will usually learn from their mistakes

5

and eventually discover the true structure of the underlying system. Thus,

the errors should simply be random movements due to uncertainty and should

tend to cancel each other on average.

In the absence of uncertainty, the REH reduces to the special case of

perfect foresight, because the equilibrium solution of the system is then

uniquely determined. The problem then is w:,ether individuals know the true

structure of the system. Muth did not address this problem; he conjectured

that 'expectations of firms tend to be distributed, for the same

information set, systematically about the prediction of the theory'. If

the theory is wrong and the prediction proves to be inaccurate, then an

REH model cannot be reduced to perfect foresight, even without

uncertainty, unless the rational individuals respecify the model until its

systematic errors are removed. However, for the purpose of empirical

analysis we assume that the prediction of the theory represented in the

form of an econometric model is the true value. In other words, we accept

as the maintained hypothesis that the model is a true description of the

system; rational expectations are then the mathematical expectations

implied by the model conditional on the information available at the time

when expectations must be formed.

3.1 Properties of Muthian Rationality

Let At denote the information set available at time t. This set

includes knowledge of the structure of the model, government policies in

operation and the past history of relevant economic variables. Also, let

y~+k denote the rational expectation at time t of the value of the variable

y at time t+k, and E(Yt+k!At) = Et Yt+k denote the mathematical

expectation of the variable y at time t+k conditional on the information

available at time t. Then, for linear models, the rational expectation y~+k

is defined as E(Yt+kIAt) = Et Yt+k' and has the following properties.

Property (i): Time consistency

6

that is, individuals have no basis for predicting how they will change

their expectations about future values of a variable.

Property (ii): Unbiasedness

where u . =t+1

expectation,

At. That is,

component St

available at

y .- EtYt . is the forecast error of the rationalt+1 +1and St is some subset at time t of the full information set

the forecasting error is uncorrelated with each and every

of the information set At' and therefore no information

the time when expectations are formed may be used

systematically to improve forecasting errors if expectations are rational.

Property (iii): Forecast error unpredictability

The forecast error is serially uncorrelated, with mean zero:

( 7)t '" s

that is, previous forecast errors contain no information about how utwill deviate from its mean value.

Property (iv): Orthogonality

The forecast error is uncorrelated with any information that is

available:

.. ( 8)

that is, the rational expectations forecast cannot be further improved

upon with available information.

Note: In what follows we shall call E lY the current rational. t- t

expectation and E y .(i~l) the future rational expectation.t t+1

7

3.2 Applications of Rational Expectations in Economics

Microeconomic theory is concerned with the existence and optimality of

competitive equilibrium. The Arrow-Debreu model of markets with

uncertainty (Debreu 1959) assumes that 'markets are complete', which is

basically equivalent to assuming certainty. Such a model has been found to

be unrealistic. Radner (1982) analyses the introduction of information and

expectations in models of sequences in incomplete markets. Under the REH,

traders enter the market with different non-price information but use the

market prices to make revisions of their individual models. In

equilibrium, not only are prices determined so as to equate supply and

demand, but individual economic agents correctly perceive the true

relationship between the non-price information received by the market

participants and the resulting equilibrium market prices. A market in

which such a RE equilibrium exists is termed 'informationally efficient'.

Assuming that there is only a finite number of states of initial

information, the concept of REH requires that each trader know the

relationship between initial information and equilibrium prices.

Futia (1979) considered a special case in which there is a market for

a single commodity, the excess supply equations are linear and the

underlying information signals are stationary Gaussian processes. He

established that there exists a symmetric RE equilibrium if and only if

each trader makes as good a conditional prediction of the next period's

price as if he has the pooled information of all traders. This model leads

to an equilibrium theory of stochastic business cycles.

Work on public prediction equilibrium and the 'efficient market

hypothesis' has been done by Jordan (1980) and by Border and Jordan

(1979). Muth's (1961) classic paper used the REH to demonstrate that the

cobweb theorem of price fluctuation is consistent with longer mean cycle

lengths than those implied by extrapolative and non-RE hypotheses.

The popularity of the REH among macroeconomists is primarily due to

the seeming failures of Keynesian macroeconomics in the 1970s, when

stagnation and persistent inflation created a receptive environment for

new ideas.

8

Shiller (1978) and Kantor (1979) have reviewed applications of REH

where the concept is justified as equivalent to profit maximising

expectations for individual agents. If information were free, only the

limits of the Heisenberg uncertainty principle could prevent the REH from

being equivalent to the assumption of perfe~t foresight. Though

information can be acquired only at som~ cost, arbitrage may nevertheless

lead to behaviour corresponding to Muthian rationality.

Sargent and Wallace (1976) used REH and the aggregate supply equation

of Lucas (1972) to provide theoretical support for the controversial

Phelp-Friedman 'invariance' proposition of a vertical Phillips curve

that is, that neither monetary nor fiscal policy has any effect on

unemployment. They also explained why a large proportion of macroeconomic

models typically fail tests for structural change if they ignore rational

expectations.

Lucas's (1976) criticism of the use of conventional econometric

modelling for policy evaluation goes right to the heart of existing

econometric practice. As decision rules are likely to change when the

economic environment changes, simulations using existing models can

provide no useful information as to the actual consequences of alternative

economic policies. REH explicitly exposes this difficulty. However, to

handle models incorporating the concept of REH, the conventional

econometric techniques of identification, estimation, hypothesis testing

and policy simulation are nO longer adequate. The following sections will

deal with each of these problems in turn.

4. STATISTICAL IDENTIFICATION

The 'identification problem' in econometric theory is that of inferring

the structure of a system from information about a reduced-form model. The

classic example of an identification problem arises in demand and supply

analysis. From price and quantity data alone, it is impossible to

determine either the supply or demand curve. Additional information about

the system is needed to estimate the separate demand and supply relations.

In the aggregate supply literature, the problem takes the form of

inability to discriminate between models for which the invariance

9

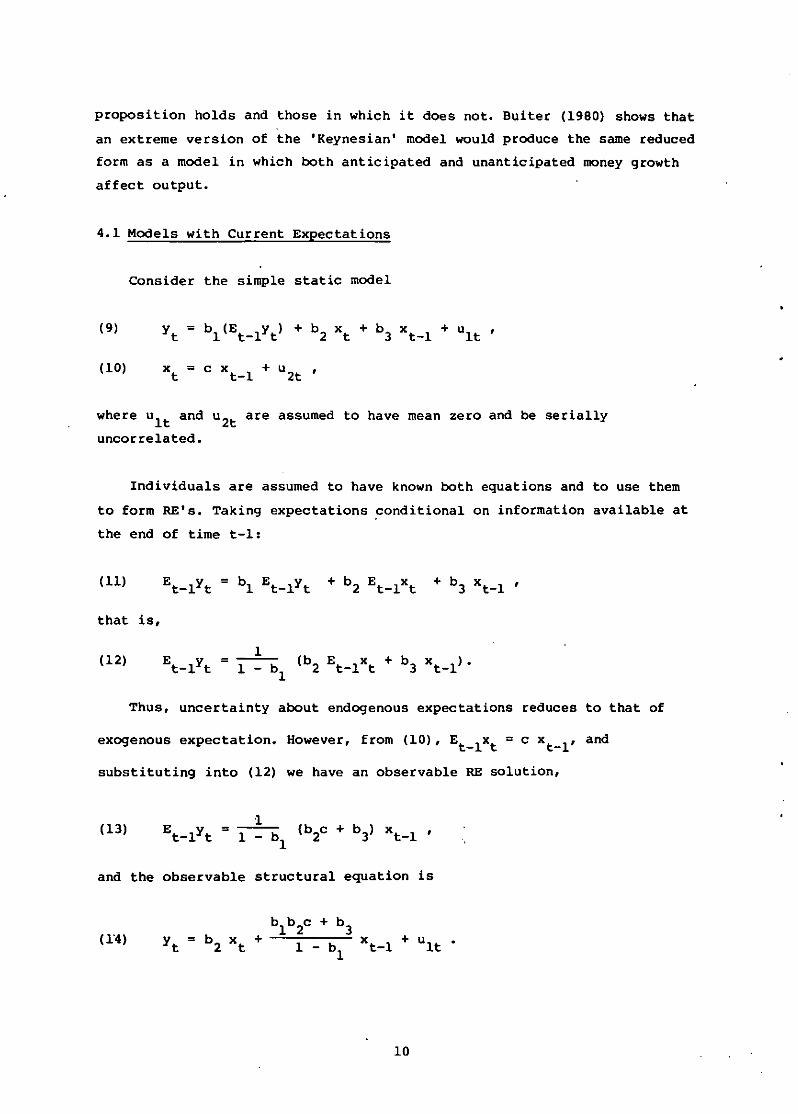

proposition holds and those in which it does not. Buiter (1980) shows that

an extreme version of the 'Keynesian' model would produce the same reduced

form as a model in which both anticipated and unanticipated money growth

affect output.

4.1 Models with Current Expectations

Consider the simple static model

where ul t and u2t are assumed to have mean zero and be serially

uncorrelated.

Individuals are assumed to have known both equations and to use them

to form RE's. Taking expectations conditional on information available at

the end of time t-l:

( 11) Et-lYt = bl Et_lyt + b2 Et_lXt+ b

3x

t_l,

that is,

(12) Et-lYt1

(b2 Et_lXt + b3 xt_l)·= 1 - b1

Thus, uncertainty about endogenous expectations reduces to that of

exogenous expectation. However, from (10), Et_lXt = c xt_l' and

substituting into (12) we have an observable RE solution,

(13)

and the observable structural equation is

(H)

10

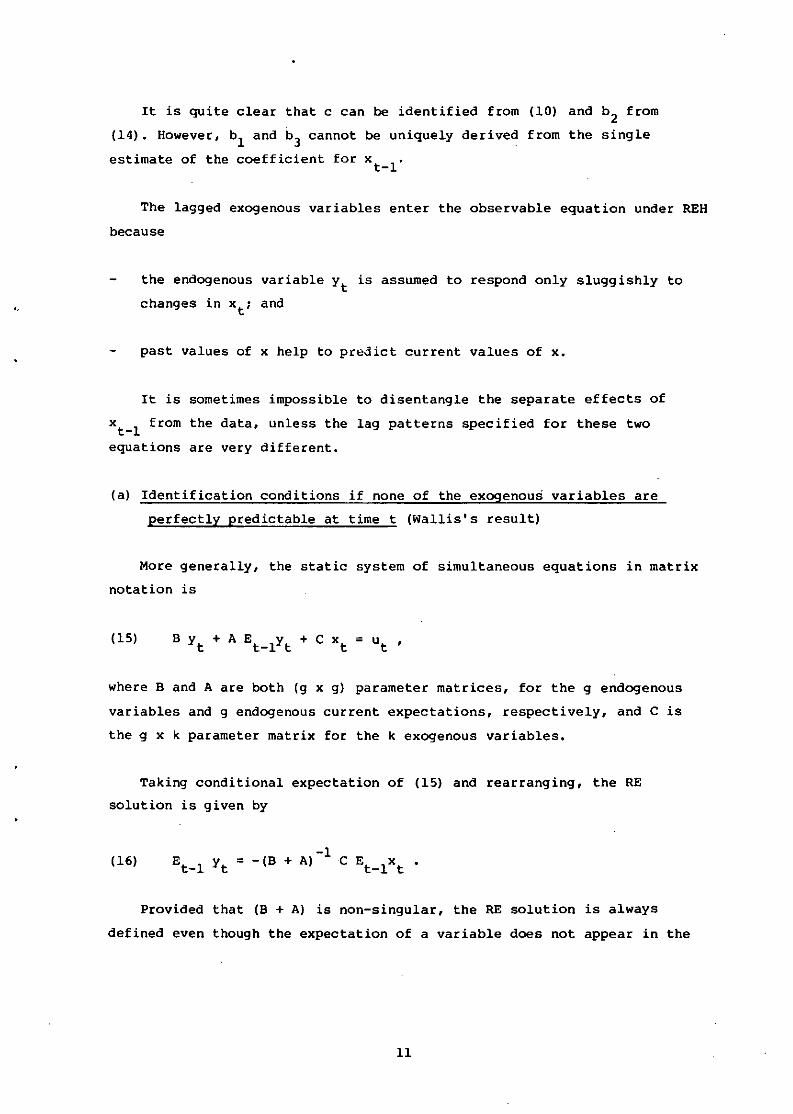

It is quite clear that c can be identified from (10) and

(14). However, bl and b3

cannot

estimate of the coefficient for

be uniquely derived from the

xt-l

b2

from

single

<,

The lagged exogenous variables enter the observable equation under REH

because

the endogenous variable Yt is assumed to respond only sluggishly to

changes in xt; and

past values of x help to predict current values of x.

It is sometimes impossible to disentangle the separate effects of

x 1 from the data, unless the lag patterns specified for these twot-equations are very different.

(a) Identification conditions if none of the exogenous variables are

perfectly predictable at time t (Wallis's result)

More generally, the static system of simultaneous equations in matrix

notation is

where B and A are both (g x g) parameter matrices, for the g endogenous

variables and g endogenous current expectations, respectively, and C is

the g x k parameter matrix for the k exogenous variables.

Taking conditional expectation of (15) and rearranging, the RE

solution is given by

(16)-1= -(B + A)C Et_lX

t

Provided that (B + A) is non-singular, the RE solution is always

defined even though the expectation of a variable does not appear in the

11

model. Substituting (16) into (15), one obtains the observable reduced

form,

where

-1 -1= B A(B + A) C,

-1= -B C,

-1v = B ut t .

However, the unobservable reduced form is given by

(18) Yt = III Et-lYt + I12 xt + vt '

where

-1 -1III = -B A and II2 = -B C.

Furthermore, taking conditional expectation,of (18) and substituting

back into (18), the alternative observable reduced form is:

Comparing (17) and (19):

Let 0 be a column vector .containing the r (~2g + k) structural

parameters of (B, A, C) that are not known a priori (and suppose there are

only h«g) endogenous expectations, so that g - h columns of A are nUll) 1

let P be the column vector containing the 2gk elements of observable

reduced form coefficients (PI' P2). Then the necessary and sufficient

condition for local identifiability of the structural parameters is that

the Jacobian matrix J = dp/do has rank r, the number of structural

parameters to be estimated (see, for example, Rothenberg 1973).

12

o·

"

e

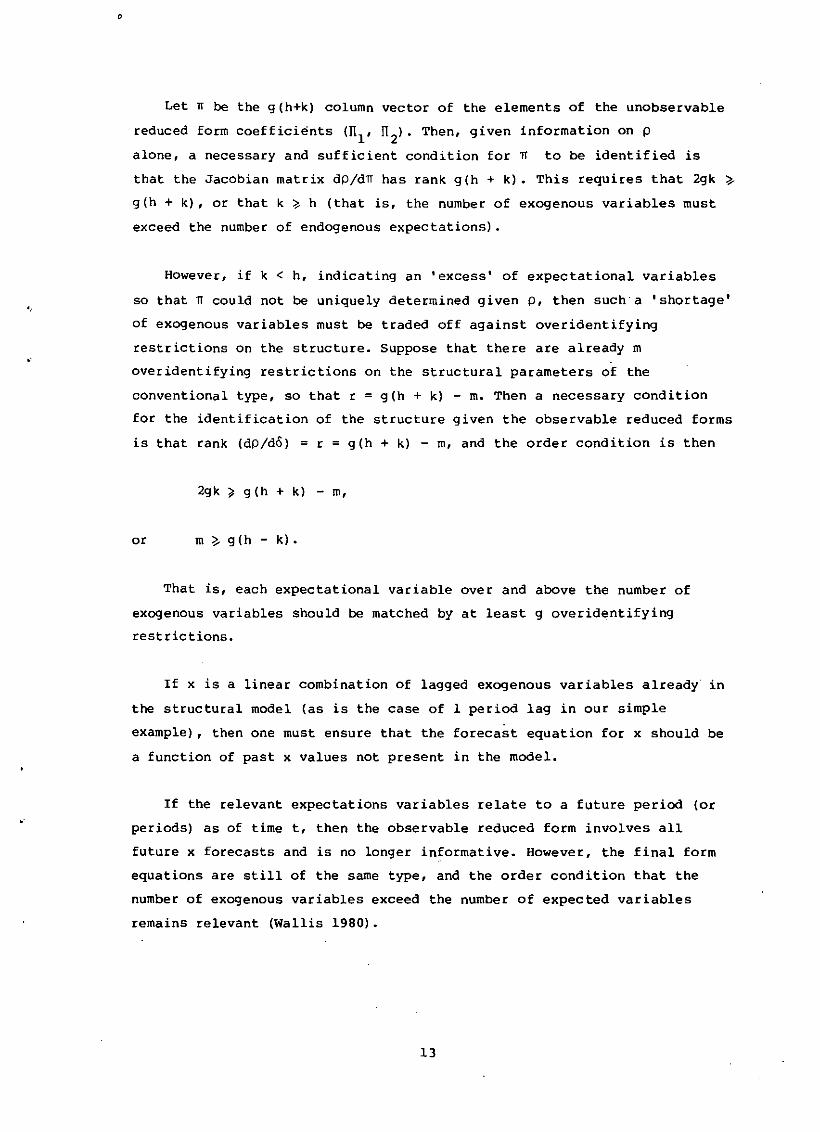

Let TI be the g(h+k) column vector of the elements of the unobservable

reduced form coefficients (TIl' TI2).

Then, given information on p

alone, a necessary and sufficient condition for TI to be identified is

that the Jacobian matrix dP/dTI has rank g(h + k). This requires that 2gk ~

g(h + k), or that k ~ h (that is, the number of exogenous variables must

exceed the number of endogenous expectations).

However, if k < h, indicating an 'excess' of expectational variables

so that TI could not be uniquely determined given P, then such·a 'shortage'

of exogenous variables must be traded off against over identifying

restrictions On the structure. Suppose that there are already m

over identifying restrictions on the structural parameters of the

conventional type, so that r = g(h + k) - m. Then a necessary condition

for the identification of the structure given the observable reduced forms

is that rank (dP/do) = r = g(h + k) - m, and the order condition is then

2gk " 9 (h + k) - m,

or m ~ g(h - k).

That is, each expectational variable over and above the number of

exogenous variables should be matched by at least 9 overidentifying

restrictions.

If x is a linear combination of lagged exogenous variables already in

the structural model (as is the case of 1 period lag in our simple

example), then one must ensure that the forecast equation for x should be

a function of past x values not present in the model.

If the relevant expectations variables relate to a future period (or

periods) as of time t, then the observable reduced form involves all

future x forecasts and is no longer informative. However, the final form

equations are still of the same type, and the order condition that the

number of exogenous variables exceed the number of expected variables

remains relevant (Wallis 1980).

13

(b) Identification conditions if some of the exogenous variables

are perfectly predictable (for example, time trends, seasonal

dummy variables)

Although Wallis (1980, p.S6) did point out that the effect of a 'fixed

regression' assumption, in which x t is treated as known, is to remove

the identifiability of the model because the observable reduced form could

not be estimated, he did not consider the case where identification can be

achieved by extra restrictions on the structural parameters. Pesaran

(1981) and Wegge and Feldman (1983) pursued the problem independently and

obtained rank and order conditions for current RE models under these

circumstances.

k) selection matrix such that

Returning to equations

(x l t' x 2t)· Suppose x 2t is

= x 2t' and let S be a (k x

sXt = [:It(15) and (16), let x

tbe

perfectly predictable so

partitioned into

that

The restricted reduced

PI + P2

= (B + A)-lC,

-1form (17) becomes, using P2 = -B C Sand

( 20)

and the unrestricted reduced form becomes

Assuming there are m restrictions on the 2g + k unknown elements of

the ith row of (A, B, C) and no restrictions on the covariance matrix for

simplicity, the ith row is said to be identified if non-trivial unique

solution can be derived from the following relationships:

b' Jl + c' S = 0,1(?2) (b' + a') ~ + c· = 0,

a' 4> + b' 4> + c" 4> = 0,a b c

14

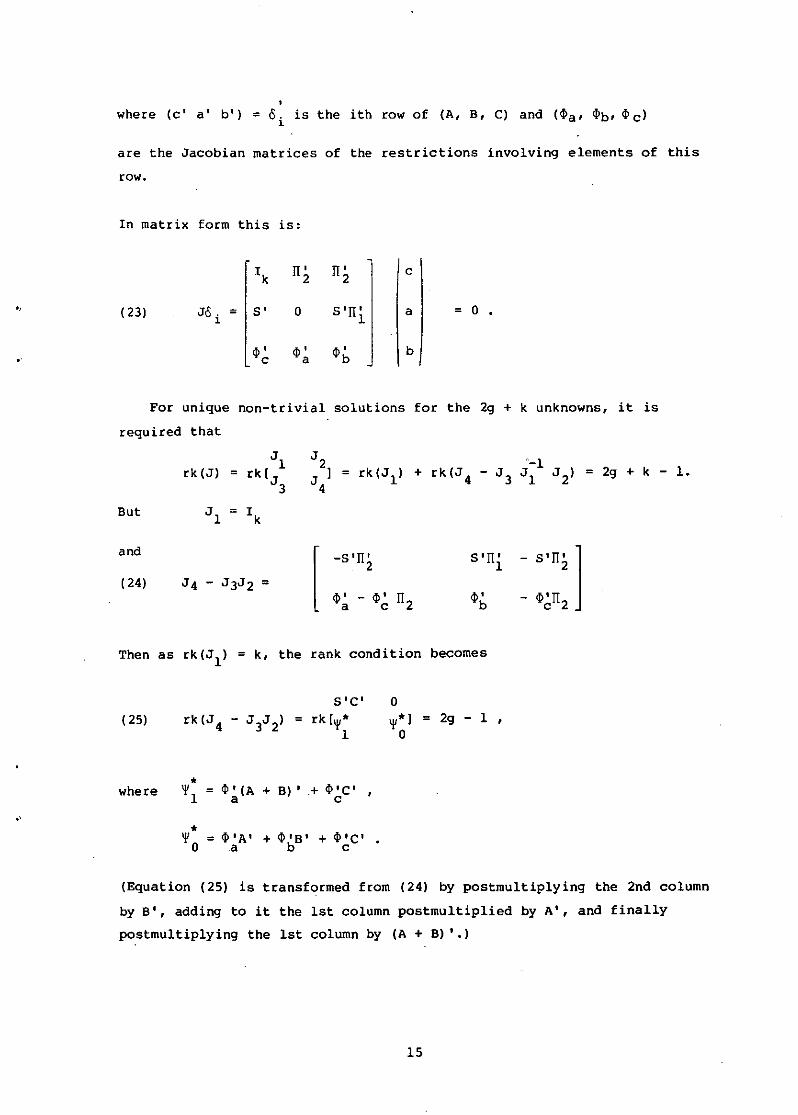

"

,where (c' a' b'l = '\ is the ith row of (A, B, C) and (<I>a' <l>b' <l>cl

are the Jacobian matrices of the restrictions involving elements of this

row.

In matrix form this is:

I k II' II' c2 2

( 23) J8 i = S' a S 'n ' a = a .1

<I> ' <1>' <1>' bc a b

For unique non-trivial solutions for the 2g + k unknowns, it is

required that

Jl

J 2 + rk(J 4 - J 3'-1

2g+k-1.rk (Jl = rkl J J ] = rk(Jl) Jl

J 2) =3 4

But J l = Ik

and

[_sIn' S'I1' - ,orr; ]2 1

(24) J4 - J3J2 =<1>' - <1>' I1 2

<1>' <I>'I1a c b c 2

Then as rk(Jl) = k, the rank condition becomes

( 25)S'C'

= rk ['1'*1

a'1'*] = 2g - 1 ,

a

where*

'1'1 = <1>' (A + B) , .+ <I>'C'a c

*'1'0 = ~'A' + ¢ IB' + <I>'c'

a b c

(Equation (25) is transformed from (24) by postmultiplying the 2nd column

by B', adding to it the 1st column postmultiplied by A', and finally

postmultiplying the 1st column by (A + B) '.)

15

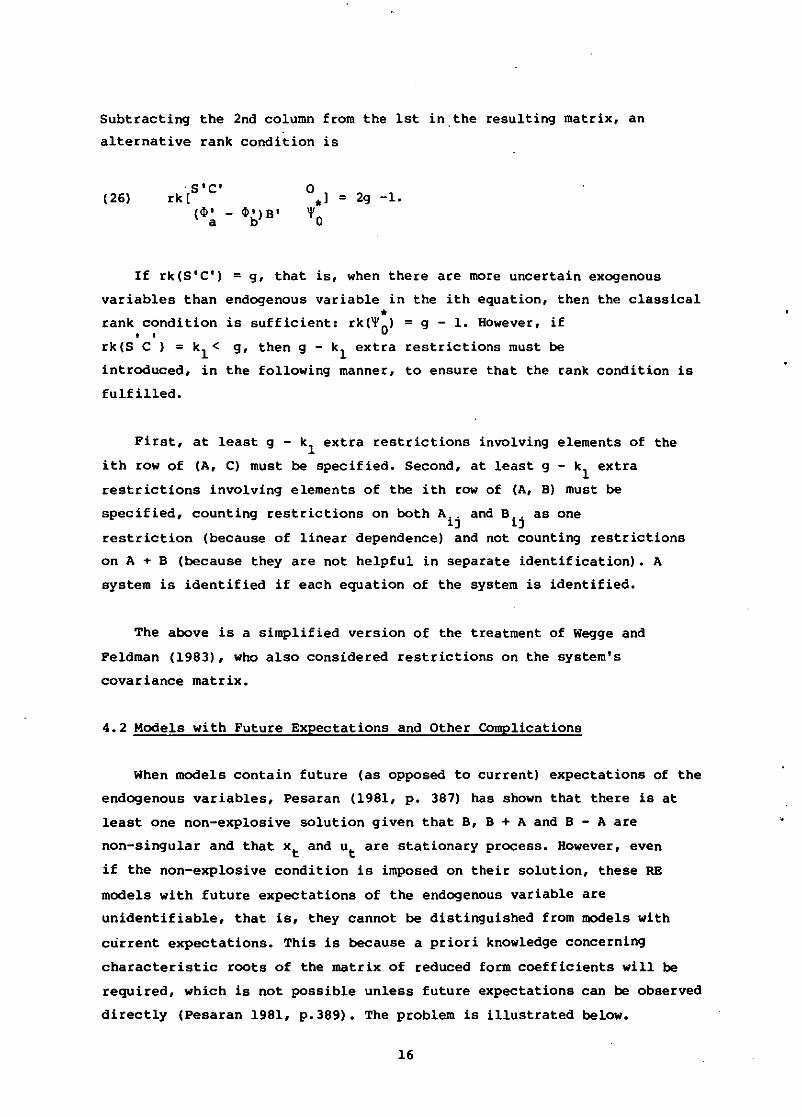

Subtracting the 2nd column from the 1st in,the resulting matrix, an

alternative rank condition is

( 26)

If rk(S'C') = g, that is, when there are more uncertain exogenous

variables than endogenous variable in the ith equation, then the classical•rank condition is sufficient: rk(~O) = g - 1. HOwever, if, ,

rk (S C ) = kl < g, then g - kl extra restrictions must be

introduced, in the following manner, to ensure that the rank condition is

fulfilled.

First, at least g - kl extra restrictions involving elements of the

ith row of (A, C) must be specified. Second, at least g - kl

extra

restrictions involving elements of the ith row of (A, B) must be

specified, counting restrictions on both A.. and B.. as one1) 1)

restriction (because of linear dependence) and not counting restrictions

on A + B (because they are not helpful in separate identification). A

system is identified if each equation of the system is identified.

The above is a simplified version of the treatment of Wegge and

Feldman (1983), who also considered restrictions on the system's

covariance matrix.

4.2 Models with Future Expectations and Other Complications

When models contain future (as opposed to current) expectations of the

endogenous variables, Pesaran (1981, p. 387) has shown that there is at

least one non-explosive solution given that B, B + A and B - A are

non-singular and that xt and ut are stationary process. However, even

if the non-explosive condition is imposed on their solution, these RE

models with future expectations of the endogenous variable are

unidentifiable, that is, they cannot be distinguished from models with

current expectations. This is because a priori knowledge concerning

characteristic roots of the matrix of reduced form coefficients will be

required, which is not possible unless future expectations can be observed

directly (Pesaran 1981, p.389). The problem is illustrated below.

16

"

.'

(a) Single equation models with future expectation

Identification of models with future RE starts from finding their

reduced forms. For the most part, these models are systems of linear

stochastic difference equations in which agents' views about the future

enter in a specific way. If these expectations are formed adaptively, the

problem of finding a reduced form is equivalent to finding the solution to

a standard difference equation. But when expectations are assumed to be

rational, the search for a reduced form is transformed into a rather more

complicated search for a fixed point. Suppose that expectations of future

variables can be written as linear functions of available information. One

can calculate the reduced form using standard techniques, and the reduced

form can be used to forecast the same variables that agents were

interested in. The model is solved when the forecasts of agents match

those of the reduced form.

Since RE models are 'expectational difference equations', special

techniques are needed to find the reduced-form solution with the fixed

point property of REH. There is a wide range of techniques suggested in

the literature to deal with the problem. One can find •state-space'

technique in Lucas (1972), 'operator' methods in Sargent (1979) and Wallis

(1980), 'methods of undetermined coefficients' in time domain in Muth

(1961) and Aoki and Canzoneri (1979), and 'forward' and 'backward'

solutions in Blanchard (1979). However, these techniques are basically of

two kinds: one transforms an expectational difference equation into

another ordinary difference equation; the other transforms the

expectationa1 difference equation into a system of non-linear algebraic

equations. All of them tend to go too far toward obtaining closed form

solutions and are often intractable or conceal the existence and

uniqueness problems •

Whiteman (1983) proposes a simplified version of the method of

'undetermined coefficients in the frequency domain' which was due to

Saracoglu and Sargent (1978) and Futia (1981). In comparison with the

standard techniques, this technique is simpler computationally due to the

availability of existing algorithms for power spectrum estimation. The

technique could be used in conjunction with a maximum likelihood procedure

for estimating the parameters of the expectational difference equation

under the cross-equation restrictions of RE.

17

For the purpose of illustration it is necessary only to consider the

simple future expectation model,

where xt

is an exogenous stationary stochastic process having the Wold

representation:

00

xt

= 1: a. e t .j=O J -J

where a (L)

such that:

00

= 1: a.j=o J

Lj is the polynomial in terms of the lag operators L

nL e

t= e t 0

-n

Many models appearing in the literature could be transformed to this1

simple form with appropriate restrictions on the parameters.

(1) For example, Muth's inventory speculative model contains current andfuture expectations as well as a lagged dependent variable:

Define: Zt = Yt - S Yt-l1

Then the model can be written as:

a-as

o1 -as

That is, if S A + 8S= 1 _ as' then the left hand side is simply Zt O

8Now define wt = Zt - 1 -as Et_lZt

8so that Etwt+l = (1 - 1 -as ) EtZt+l

Substituting back for EtZt+l:a

wt = 1 - as -5

which has the same form as (27)0

18

"

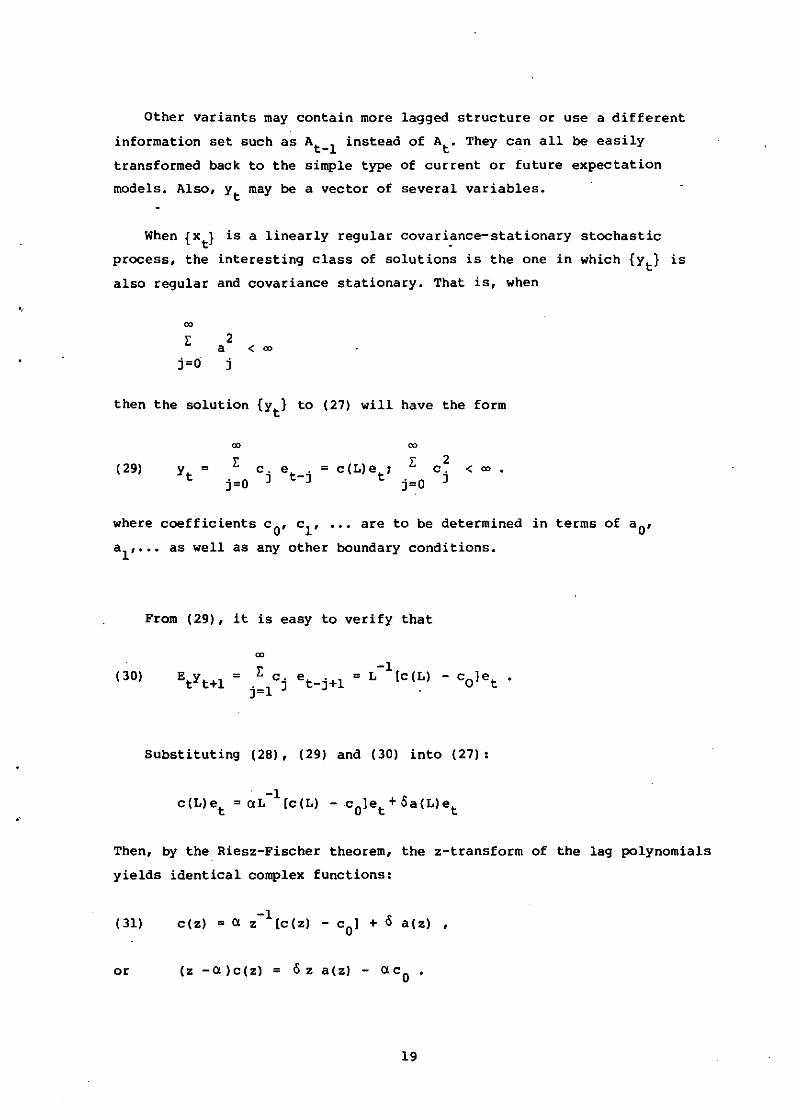

Other variants may contain more lagged structure or use a different

information set such as At_l instead of At' They can all be easily

transformed back to the simple type of current or future expectation

models. Also, Yt may be a vector of several variables.

When {Xt} is a linearly regular covariance-stationary stochastic

process, the interesting class of solutions is the one in which {Yt} is

also regular and covariance stationary. That is, when

'" 2a < co

j=O j

then the solution {Yt} to (27) will have the form

( 29)

cc

I:

j=Oc. e

t.

J -J

co

I:

j=O

2c.

J<00.

where coefficients cO' c l' ••• are to be determined in terms of aD,

a l, ••• as well as any other boundary conditions.

From (29), it is easy to verify that

00

(30) I: c.j=l J

.'

SUbstituting (28), (29) and (30) into (27):

Then, by the Riesz-Fischer theorem, the z-transform of the lag polynomials

yields identical complex functions:

( 31) c (z)-1=Q z [c(z) - cOl + 6 a(z) ,

or (z -Q )c(z) = 6 z a(z) - QC O •

19

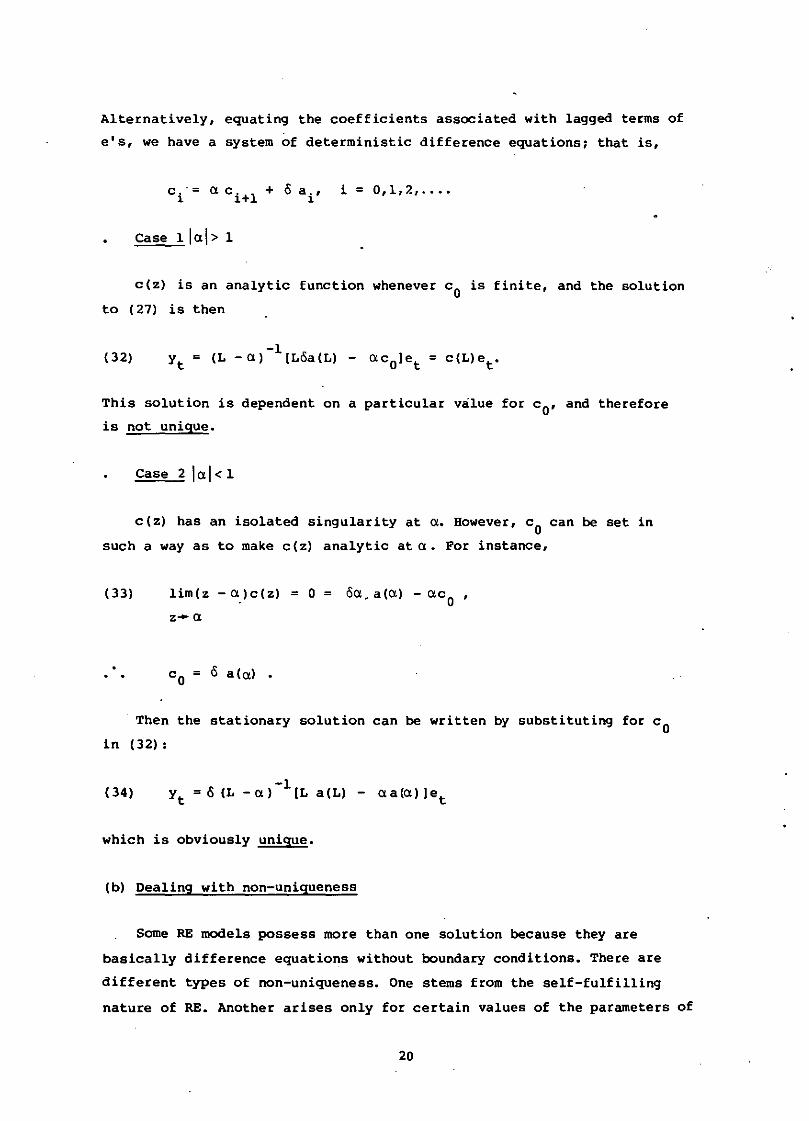

Alternatively, equating the coefficients associated with lagged terms of

e's, we have a system of deterministic difference equationsl that is,

case llal> 1

c(z) is an analytic function whenever Co is finite, and the solution

to (27) is then

( 32)

This solution is dependent on a particular value for cO' and therefore

is not unique.

Case 2 lal < 1

c(z) has an isolated singularity at a. However, Co can be set in

such a way as to make c(z) analytic at a. For instance,

(33) lim(z - a )c(z) = 0 = ca. ala) - ac O '

z-a

c = c ala) •o

Then the stationary solution can be written by sUbstituting for Coin (32):

( 34)-1

Yt = C (L - a ) [L a (L) - a a (a) )e t

which is obviously unique.

(b) Dealing with non-uniqueness

Some RE models possess more than one solution because they are

basically difference equations without boundary conditions. There are

different types of non-uniqueness. One stems from the self-fulfilling

nature of RE. Another arises only for certain values of the parameters of

20

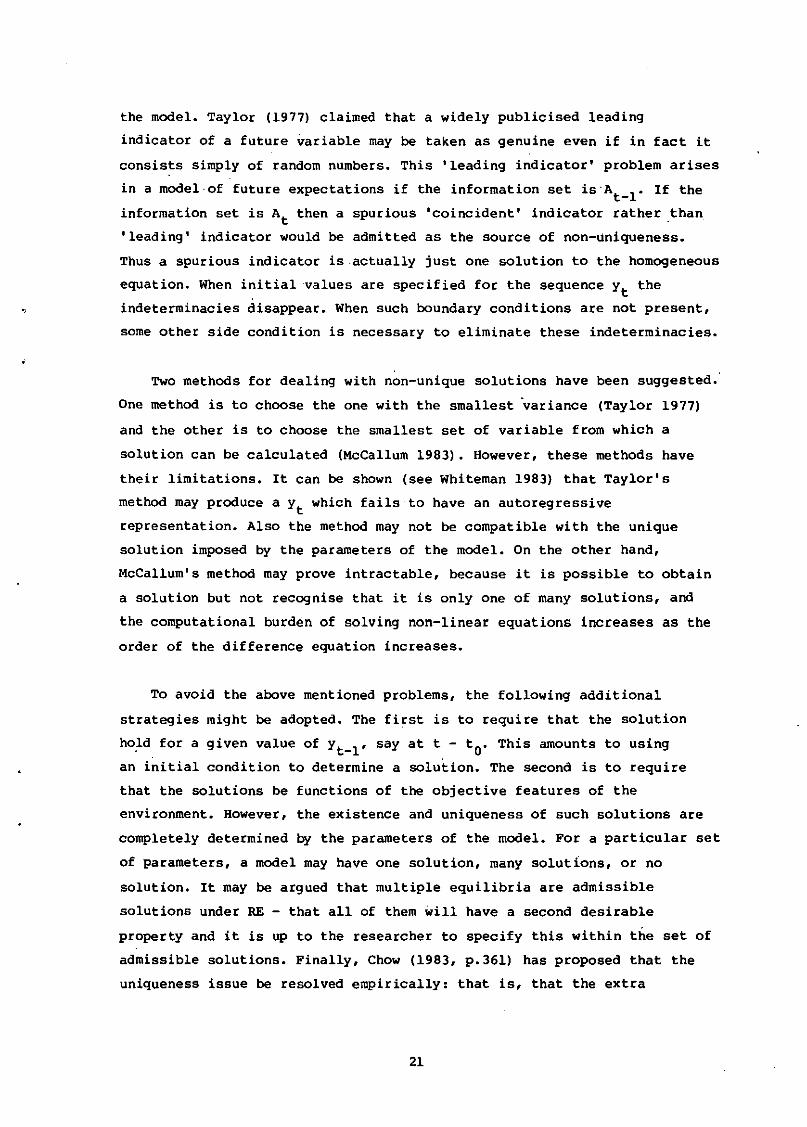

the model. Taylor (1977) claimed that a widely publicised leading

indicator of a future variable may be taken as genuine even if in fact it

consists simply of random numbers. This 'leading indicator' problem arises

in a model-of future expectations if the information set is-At_l•

If the

information set is At then a spurious 'coincident' indicator rather than

'leading' indicator would be admitted as the source of non-uniqueness.

Thus a spurious indicator is-actually just one solution to the homogeneous

equation. When initial values are specified for the sequence Yt the

indeterminacies disappear. When such boundary conditions are not present,

some other side condition is necessary to eliminate these indeterminacies.

Two methods for dealing with non-unique solutions have been suggested.

One method is to choose the one with the smallest variance (Taylor 1977)

and the other is to choose the smallest set of variable from which a

solution can be calculated (McCallum 1983). However, these methods have

their limitations. It can be shown (see Whiteman 1983) that Taylor's

method may produce a Yt which fails to have an autoregressive

representation. Also the method may not be compatible with the unique

solution imposed by the parameters of the model. On the other hand,

McCallum's method may prove intractable, because it is possible to obtain

a solution but not recognise that it is only one of many solutions, and

the computational burden of solving non-linear equations increases as the

order of the difference equation increases.

To avoid the above mentioned problems, the following additional

strategies might be adopted. The first is to require that the sOlution

hold for a given value of Yt-l' say at t - to' This amounts to using

an initial condition to determine a solution. The second is to require

that the solutions be functions of the objective features of the

environment. However, the existence and uniqueness of such solutions are

completely determined by the parameters of the model. For a particular set

of parameters, a model may have one solution, many solutions, or no

solution. It may be argued that multiple equilibria are admissible

solutions under RE - that all of them will have a second desirable

property and it is up to the researcher to specify this within the set of

admissible solutions. Finally, Chow (1983, p.361) has proposed that the

uniqueness issue be resolved empirically: that is, that the extra

21

parameter be estimated from the data. This procedure serves to highlight

the non-uniqueness of RE solutions rather than concealing the problem.

(c) General identification conditions with future expectations

Consider the general linear models of the form:

(35) B Y + A E Y +t t t+l

pE

i=O

where future expectations are assumed to be formed rationally using the

current information set At. Note that replacing At by At_lmay have

.only minor effects for the identification of the system (35). B and A are

parameter matrices defined as at (15).

If B is non-singular. the unobservable reduced form of (35) may be

written as:

where

D = _B-1A

If there are only h «g) endogenous expectations, then rank(A) =rank(D) = h. Assuming all the h non-zero characteristic roots of D to be

distinct. there exists a non-singular square matrix P of order g so that D

has the canonical form D = P A p-l. where A = diag(Al •••••Ah. 0, ... r I)

with the h roots as its non-zero diagonal elements. Let Yt = p-1Yt1

wt = p-1Wt. The system (36) can then be written as:

the ith row of (37) being

(37a) Y =A.Ey +wti 1 t t+l.i ti

22

i = 1,2, ... h

(37b) i ::: h+ 1, ••. 9

Note that (37a) has the same form as (27). Dropping the subscript i a

general solution for the ith equation in (37a) may be written (see

Appendix of Pesaran 1981) as:

(38) m t

t-lE

j=l

where mt is a martingale process, that is, Etmt +l = mt•

Due to the presence of mt, there will be an infinite number of

solutions to choose from, unless a priori restrictions are placed on the

Yt process. To obtain solutions, it may be plausible to require Yt to

be non-explosive. This can be done by requiring that B + A and B·- A are

non-singular ,(for example, Wallis 1980, p.59; Revankar 1980, footnote 13).

However, it can be shown that for the model to have at least one

non-explosive solution, a priori knowledge concerning those roots of the

matrix D that lie within and those that lie outside the unit circle will

be required. This information will· not, normally, become available unless

structural parameters can be identified and estimated.

Suppose it is known that the roots of D lie within the unit circle

jA!<l. The stationary solutions are (Pesaran 1981, p.388):

ro

E Ai -Yt = EtWt +jj=O

or Yt = wt .

Stacking these relations

the original space:

ro

(39) Yt = E Dj

EtWt +jj=O

for A to 0

for A = 0

into a g x 1 vector and transforming back to

which is the familiar 'forward solution' (Shiller 1978,.p.29-33).

23

Assuming the ut are non-autocorrelated:

( 40)-1= -B

PL c.

i=O 1j = 0

-1 P= -B L

i=Oj > 0

( 41)

Thus. the chosen stable solution of Yt becomes:

00

Dj P -1

Yt = - L L B C. EtXt +j_i + vtj=O i=O 1

P 00

= L /:'. Xt . + L Dj/:,EtXt +j + vt •

j=O J -J j=l 0

where

( 41a) j = 0.1.2•••• p

It is now clear that the structural parameters enter the reduced form

in a highly non-linear way. and that Yt depends upon all the future

expectations of the exogenous variables.

Assuming that all future expectations of the exogenous variables are

known. the RE models with future expectations are identified if and only

if. for given future expectations of the endogenous variables Etyt +l•their underlying structures are identified. However. the more likely

situation is that the EtXt +j are not known. The identification will

then critically depend upon the nature of the xt

process.

Suppose xt has an autoregressive representation of order q. Then the

best linear predictor of xt +j conditional on the information set At

may be written as:

( 42)q-lL

i=O

24

j = 1.2 ••••

Substituting into (41), the observable reduced form of the RE model

becomes:

q-l(43) Yt

= r IT. xt

_i

+ vti=O 1

where 00

IT = (j + r oj (j b ..i i j=O

0 1)

00

oj(j( 44) = r b .. = OH.j=l 0 1) 1

where 00j-l

H. = E n (j 0 b ..1 j=l 1)

and (j . are given by (41a) •1

Rewrite relations. (44) as:

(45) B. IT. + C. + AG. = 01 1 1 1

B. IT. + AM. = 01 1 1

where

eej-l

H. = z n (jObi j,1 j=l

pj-i-l -1G. = H. - r 0 B C.

1 1 j=i+1 )

i::;;:O,l, ••• p

i = p + 1, •.. , q-l

i=O,l, ,p

i = p+l, ,q-l

i = 0,1, ... ,q-l

i=O,l, ... ,p

and both are independent of C. (i = 0,1, •.• , q-l).1

Suppose there are m linear homogeneous restrictions on the

coefficients of the 1st equations in the form:

( 46) o'<I>=b'<I>b+C'<I> + +c'<I> +a'<I> =0,o cO '" p cp a

where 0' = (b', cO' .~. , cp' a') is the 1st row of the g x [2g + k(p+l»)

25

'r~l ojni pnijujiJadUe

: asmo:)sc'

Combining (45) and (46) we can write the system of kq + m equations in

the 2g + k(p+l) unknown structural parameters in matrix form:

<l>b TIO TIl ••• TIp-l TIp

.o':~:

<l>cp 0"---- 0 I k<l>a Go Gl Gp_l Hp

TIpH" • 'TIq-l

o 0

o 0

H ••• HpH q-l

For the structural parameters 6 to be uniquely determined given

estimates of the reduced-form coefficients and of the prior restrictions,

we must have:

(47) rank (J) = 2g + k (pH) - 1,

which implies the following order conditions:

( 48a)

(48b)

Notes:

kq + m ~ 2g + k (pH) - 1,

q > p+l.

When q ~ p, the models with current or future expectations are

observationally equivalent to those without expectations, and when

q = p+l, the RE model with futures expectations cannot be

distinguished from those with current expectations (Pesaran 1981,

p. 392) •

When q < p+2, even in the case of single-equation models (g = 1), at

least one homogeneous restriction (m ~ 1) will be needed if the

parameters are to be identified (Pesaran, p.394). (That is, if p = 0,

the exogenous variables should have an AR(2) process when there are no

homogeneous restrictions on the parameters.)

26

If q ~. p+2 and k (q-p-l) < g, then the necessary condition is that qk

exceeds the number of variables included in that equation less 1

(Pesaran, p.394).

If q~. p+2 and k (q-p-l) ~ g, the necessary condition for

identification could be investigated simply by treating all the

expectation variables as if they were observable and exogenously given

(Pesaran, p.394). This becomes the classical condition for

identification, that there should be at least g - 1 independent linear

restrictions on the parameters of that equation (m ~ g-l).

5. ESTIMATION PROBLEMS

It is well known that, when structural equations are overidentified,

'full information' methods such as 3SLS will be more efficient than

'limited information' methods such as 2SLS. Since many of the RE

restrictions are cross-equation, it might seem natural to use full

information methods. However, estimation by full information methods is

very sensitive to model misspecification and incorrect restrictions. Thus,

many researchers prefer limited information methods so as to hedge against

these problems.

Another issue in the estimation of models with RE is that proxies for

anticipated and unanticipated variables have to be constructed in the form

of predictors or residuals from an estimated equation. For instance,

Anderson et al. (1976) and Duck et al. (1976) used predictors of ARMA

models to replace anticipation variables. Barro (1977) and Sheffrin (1979)

proxied unanticipated quantities with the residuals of the one-period

predictions. To overcome possible inconsistency in the resulting

estimates, Wickens (1982) and Mccallum (1976a) considered the 'errors in

variables' method and Wallis (1980) proposed a three-step method. The

latter two approaches will be examined below in reverse order.

Wallis (1980) considered estimation of model (15) assuming that the

structure is identified.

The three-step method of Wallis comprises

27

~

Step 1: Estimate Et_lxt by x t' from the exogenous process

conditional on the past history of all variables in the system,

~ ~

Step 2: Given that xt = xt + et, the observable reduced'form at

(19) becomes

(49)

~

which can be estimated consistently by OLS to obtain the predictions Yt'

Step 3: Apply 2SLS to the structural equations ,after Et_1Yt in~

(15) has been replaced by Yt'

Pagan (1984, p.230) demonstrated that while the coeffigients estimated

by Wallis are consistent, the estimated covariance matrix is generally

inconsistent. However, if Et-1Yt is to be replaced by the actual~

values, Yt' with Yt included among the set of predetermined variables

in the reduced form, the resulting estimated covariance matrix is

consistent while the parameter estimates are unaffected.

McCallum (1976a) used the actual value Yt as a proxy for the

expectations variable Et-lyt, Such a substitution induces an 'errors

in variables' problem, since Yt is now a stochastic regressor which is

correlated with the augmented disturbance term. Note that the RE

forecasting errors consist of both shocks due to exogenous variables and

reduced-form disturbances, and therefore are contemporaneously correlated

with the exogenous variables. Thus, instrumental variables are required

for both Yt

and xt in order to obtain consistent estimates for the

equation. This approach suffers from perfect multicollinearity if the

structural equation consists of the endogenous variable and its own RE

simultaneously. Furthermore, current exogenous variables can no longer be

used as instruments due to correlation with the error term, and the

identification condition is now more stringent.

One advantage of McCallum's approach is that one can now do without

specifying and estimating the autoregressive model for the exogenous

variables, In fact, consistent estimates are now obtained by a single

application of the method of instrumental variables.

28

For a dynamic model involving future expectation of endogenous

variables, the use of actual values as proxies can. also be applied

(Mccallum 1976b). But this approach must be sUbject to further

identifiability problems in large systems (Wallis 1980 p.68).

With regard to non-linear models, there has been relatively little

research done. Fair and Taylor (1983) have investigated a full information

estimation method for a nonlinear model. However, the solution procedure,

-based on the Gauss-Siedel algorithm, was found to be extremely expensive

to use. Hansen and Singleton (1982) have developed and applied -a limited

information estimator for non-linear models.

6. HYPOTHESIS TESTING

Restricting attention to linear models, the implication of the RE

hypothesis is that the expectation assessed by the market equals the

conditional expectation using all available past information. That is:

which implies that

(50)

The error of market expectation has zero mean and is uncorrelated with any

past information.

A form of the RE model that has been used extensively in empirical

work is:

(51)

This model has been used to study the rationality of interest rate and

inflation forecasts in the bond market and many other applications in the

efficient-market literature (for example, Dornbusch 1976, Frenkel 1981).

It was also used to display the policy ineffectiveness proposition by

Sargent and Wallace (1975), Barro (1979) and Grossman (1979). Lagged terms

29

have also been included in the model, to capture dynamics (see Shiller

1980, Bernanke 1982). The hyPOthesis of rationality implies thate e

Et_l Yt = Yt and Et_l xt = xt' whereas the hypothesis of neutrality (or

policy

lagged

ineffectiveness) implies thateterms of xt are also zero).

o = 0 (and that the coefficients of

To be able to test the hyPOthesis of

linear forecasting model for xt•

Suppose

where

rationality, we need to specify a

that

zt-l

= a column vector of variables used to forecast xt

which are

available at t-l,

Y = a column vector of coefficients,

ut = serially uncorrelated errors.

Taking expectation of equation (52) conditional on information available

at t-l:

,(53) Et_ l xt = Zt_l Y*

and, substituting into equation (51),

( 54)

If the y-equation is a reduced form so that all the right-hand side

variables are exogenous and are uncorrelated with the error term, then OLS

will yield consistent estimates of S. An identification problem exists if

Zt_l includes only lagged values of xt while equation (53) is a

distributed lag of x in the model (see Sargent 1976). This is the case

illustrated in section 4.1 above.

30

If the model is unidentified, then a model with 6 = 0 is

observationally equivalent to that with 6 # o. To avoid this problem, the

researcher must ensure that either (a) there is no distributed lag of x in

the y-equation or (b) the forecasting model for x includes lagged values

of at least one other variable besides x which does not enter the

y-equation as a separate variable. If the equation is identified, then a

test of rationality is equivalent to a test of the equality of the

coefficients Y estimated in (52) and (54). This cross-equation restriction

y =y. can be tested by the likelihood ratio statistic:2

that is, by

comparing the maximum likelihood function of the system (52) and (54)

estimated jointly, with and without imposing the cross-equation

restriction.

The hypotheses both of rationality (Y =Y*) and of neutrality (6 = 0)

can be tested as a joint hypothesis. However, neutrality has meaning only

if we have a theory of expectation such as the RE hypothesis. Thus, the

test of the rationality hypothesis assuming neutrality would not 'yield

useful inform~tion.

Note that the test may be rendered invalid if relevant variables are

omitted from the model and if the 'error terms are serially correlated. On

the other hand, it is known that the addition of irrelevant variables to a

model only has the disadvantage of a potential decrease in power of the

test (that is the latter becomes less likely to reject the null

hypothesis, if it is untrue) and will not result in invalid inference.

Thus, in cases of doubt, it is advisable to consider less restrictive

models.

eSpecification of Yt may be important for generating reliable tests of

of the models. For example, tests of market efficiency have often assumed

that y~, the equilibrium nominal return on a security, is constant. Despite

its being a crude model of market equilibrium, many such empirical studies

fail to reject the efficient market model (the rationality hypothesis). The

(2) The likelihood ratio statistic is defined as -2 In A where A is theratio of the maximum likelihood value of the restricted to that of theunrestricted model: in large samples, this ratio follows a chi-squaredistribution with a degree of freedom equal to the number of restrictionsimposed.

31

reason is that as the variation of y~ is small relative to

the spec if ication of y will have little impact on tests of

market model (see Nelson and Schwert 1977).

ethat of Yt - Yt'

the efficient

Proponents of the policy ineffectiveness proposition usually emphasise

deviations of output from the 'natural rate' in their model. In this case,

the variation in y~ (removing its trend, if any) is small relative

to the variation in Yt - y~. Tests of the policy ineffectivenesse

proposition are then insensitive to the specification of the model for Yt'

the natural rate.

~

variable in the model and K t ~ Zt_l Y as the anticipated variable: these

estimates are substituted in (54), which is then estimated by OLS (see

Barro 1977, 1979: Wallis 1980). This two-step procedure will still yield

In many studies, the forecasting equation for K in (52) is first~ ,~

estimated by OLS, and the residuals ut ~ K t - Zt_l Yare then

calculated. The residuals are subsequently used as the unanticipated, ~

consistent estimates. However, it does not generate valid test statistics

because the standard errors of the parameters will be underestimated. This

will lead to rejecting neutrality more often than will a valid test (see

Pagan 1984).

Abel and Mishkin (1979) have demonstrated that a test of rationality

y ~ y* using this two-step procedure, for a model in which only

contemporary unanticipated Kt

appear in the y-equation, is

asymptotically equivalent to the test that Zt does not 'Granger-cause'

Yt (see Granger and Newbold 1977, ch.7). This can be shown by writing

the system with 0 ~ 0 as:

( 55)

Instead of testing the cross-equation restriction Y ~ Y*, one can write

the y-equation in the fo~m:

32

( 56)

where e = B (Y-y*) .

Thus, a test for Y = y* is equivalent to testing e = o.

In the two-step procedure, Y is estimated by OLS in the regression of

x on z 1 so that the OLS residuals will be orthogonal to Zt 1.t t- -

Thus a test for e = 0 could simply be based on the regression:

( 57)

Often, Yt is specified as a stationary process with an ARMA

representation. Suppose it is represented by an AR(p) so that:

(58)e p

Yt = E a. Yt-i.i=l 1

Substituting into the y-equation with Y = Y* or e = 0 and taking

conditional expectation, we have:

( 59)p

i:l a i Yt-i·

That is, the optimal linear forecast for Yt

does not benefit from

the use of other information beside past y's. Hence, a regression of the

form:

PE

i=la. Y + Z a + W

t1 t-i t-l

would have an estimated a not significantly different from zero. This is

the well-known Granger-causality test that z does not help predict y if

the past history of y has already been taken into account (Sargent 1981).

With regard to the effects of specifying the list of variables

included in Zt_l' it is useful to note that inclusion of irrelevant

33

predetermined variables will not lead to inconsistent parameter estimates

but will, in general, reduce the power of tests. On the other hand,

excluding relevant variables from Zt_l will lead to inconsistent

estimates of y. Even in this case, however, any rejection of the

constraint y = y. in (55) indicates a failure of rationality or of

neutrality, since a rejection of this constraint indicates that

Z 'Granger-causes' y. This shows that Luca~'s (1972) conjecture that tests

of neutrality cannot be conducted when there is a change in policy regime

(that is, new variables included in Zt_l) is not always correct.

Nevertheless, the change in policy regime could alter the variances of the

error terms and thus induce serial correlation or heteroscedasticity,

rendering the tests invalid.

Sargent (1973, 1976) pointed out that the Granger-causality tests are

valid tests of neutrality (0 = 0) and rationality (that is, Y = y.) ife(a) lagged values of xt - xt do not enter the y-equation (60) or (b) the

error term et is serially uncorrelated. The result breaks down if there

are lagged surprises (x t - x~) in (55) because the lagged OLS residuals

from the x-equation are not orthogonal to Zt_l. The Granger causality

test will no longer be a test of the hypotheses of rationality and/or

neutrality. In this case, the only valid test will be generated by

estimating both the x-equation and the y-equation jointly with and without

imposing the cross-equation restrictions and using the likelihood ratio

test.

Startz (1983) has considered Wald-type tests for the cross-equation

restr ictions.

7. THE LUCAS' CRITIQUE OF CONVENTIONAL ECONOMETRIC POLICY EVALUATION

The conventional approach to econometric policy evaluation is to take an

estimated model assuming an invariant structure. The implied reduced form

from the model is then used to predict the behaviour of the endogenous

variables under alternative specifications of the future values of policy

instruments (exogenous variables). Lucas (1976) criticises such

comparisons of alternative policy rules on the ground that the 'structure'

of econometric models - hence the implied reduced form - is not invariant

to changes in policy. For such comparisons to be meaningful, it is

34

•

necessary to assume that the nature of the economic system's reponse is

unaltered when substantial shifts in key variables occur.

Sims (1980) has also defined a structural model as one in which the

parameters can be treated as fixed over the relevant range of potential

changes in the policy rule. Some parameters of a model could be made

structural through the use of REH while other parameters were made

structural by assumption.

If adaptive expectations were used, then the coefficients of

expectation would not be policy-invariant and hence would not' be

structural. The shortcoming with these expectational assumptions is the

failure to take full account of agents' reaction to the policies

formulated. The 'problem is characteristic of both policy simulation and

formal optimal control techniques, each of which is based on the reduced

form model in which expectations are formed by fixed-coefficient

distributed lag structures. Since these lag structures show no direct

relationship to government policy, the mechanisms generating expectations

are inconsistent with those that take account of this policy.

Attempts to revise the methodology along the lines suggested by Lucas

appear to have been frustrated by the Sargent and Wallace proposition of

policy ineffectiveness under REH. However, when it was discovered that the

negative result relied heavily on a specialised structure rather than on

REH as such, the Lucas criticism was finally accepted as being

constructive rather than destructive.

The modern approach would now distinguish an underlying economic

structure incorporating the REH from a forecasting mechanism for the

exogenous policy rule which is allowed to change as policy changes.

The contribution of the Lucas critique tq econometric methodology is

now recognised as a breakthrough comparable to that of the Cowles

Commission who, in the 1950s, suggested that in policy analysis structural

simultaneous equations rather than single-equation reduced forms should be

modelled, to avoid bias. More care should now be devoted to modelling

expectations that are consistent with the model structure.

35

8. CONCLUSION

The rational expectations hypothesis takes into account the important case

of endogenous expectations formation, as was foreshadowed by Keynes in his

General Theory. While the hypothesis has generally been accepted as being

more plausible than the ad hoc approach in forming expectations, RE models

cannot guarantee to deliver unique solutions and replicate the real world.

However, if the real world is characterised by expectational confusion,

then the RE model reveals this problem and thus leads to better policies

which avoid it.

Regarding the problem of identification, economists cannot implement

the RE solution unless the structural parameters can be disentangled from

economic data. Even if the parameters are identified, individuals may have

begun from an incorrect view of the economy, forming mistaken expectations

which cause the RE model to fail to replicate reality. However, if

individuals do not make perceivable errors in forecasting the future, then

the RE hypothesis is a convenient assumption with which to begin the

analysis of endogenous expectations formation.

The idea that policy changes may induce revision of individuals'

behaviour dates back to Marschak (1953). Macroeconomic analysis of

stabilisation policy· should recognise that individuals' expectations are

endogenous, depending on the operation of government policies, as pointed

out by Lucas. What remains to be studied is how to capture more accurately

the constraints which intertemporal decision makers actually face, and to

model more realistically the information they can acquire when forming

expectations (see Blanchard 1981).

This new mode of thinking among economists has led to SUbstantial

progress in the analysis of bond and foreign exchange markets. BY

emphasising the dangers of ad hoc expectations rules, the RE approach has

encouraged a more general reconsideration of the micro foundation of

macroeconomics •

. Most of the early empirical literature uses 'limited information'

estimation of equations. Since REH imposes precise cross-equation

restrictions, this information concerning the full system should be

36

imposed a priori to obtain more efficient es~imates and more powerful

tests. The Lucas problem must also be addressed. A forecast or simulation

should involve a series of iterations until the evolution of the economy

is consistent with the expectations the model assumes.

Further insights concerning rational expectations theory may be found

in the works of Taylor (1985), Begg (1982), Mishkin (1983) and Sheffrin

(1983).

37

REFERENCES

Abel, A. and F.S. Mishkin (1979),On the Econometric Testing of Rationality

and Market Efficiency, Chicago Report No. 7933, University of Chicago.

Anderson, G.J., Pearce, I.F. and Trivedi, P.K. (1976), 'Output, expected

demand and unplanned stocks' in I.F. Pearce et al. (eds) , A Model of

Output, Employment, Wages and Prices in the United Kingdom, Cambridge

University Press, Cambridge.

Aoki, M. and Canzoneri, M. (1979), 'Reduced forms of rational expectations

models', The Quarterly Journal of Economics 93, 59-71.

Barro, R.J. (1977), 'Unanticipated money growth and unemployment in the

United States', American Economic Review 67, 101-15.

___ (1979) ,'Unanticipated money growth and unemployment in the United

States: reply'. American Economic Review 69, 1004-9.

Begg, D.K.H. (1982), The Rational Expectations Revolution in

Macroeconomics, Philip Allan, Oxford.

Bernanke, B. (1982), The financial collapse as a direct cause of the Great

Depression. Stanford University Graduate School of Business, California

(unpubli shed) •

Blanchard, O.J. (1979), 'Backward and forward solutions for economies with

rational expectations', American Economic Review 69, 114-8.

___ (1981), 'Output, the stock market, and interest rates', American

Economic Review 71, 132-43.

Box, G.E.P. and Jenkins, G.M. (1970), Time Series Analysis, Forecasting

and Control, Holden Bay, San Francisco.

Border, K.C. and Jordan, J.S. (1979), 'Expectations equilibrium with

expectations based on past data', Journal of Economic Theory 22, 395-406.

38

•Suiter, W.H. (1980), Real effects of anticipated and unanticipated money:

some problems of estimation and hypothesis testing. Working Paper No.

601, National Bureau of Economic Research, Cambridge, Massachusetts.

Cagan, P. (1956), 'The monetary dynamics of hyper-inflation' in M.

Friedman (ed.), Studies in the Quantity Theory of Money, University of

Chicago Press, Chicago.

Chow, G.C. (1983), Econometrics, McGraw-Hill, New York.

Coase, R.H. and Fowler, R.F. (1935), 'Bacon production and the pig cycle

in Great Britain', Economica, 2, 142-67.

Debreu, G. (1959), Theory of Value, Wiley, New York.

Dornbusch, R. (1976), 'Expectations and exchange rate dynamics', Journal

of Political Econo~ 84, 1161-76.

Duck, N., Parkin, M., Rose, D. and Zis, G. (1976), 'The determination of

the rate of change in wages and prices in the fixed exchange rate world

economy, 1956-1971' in M. Parkin and G. zis (eds) , Inflation in the

World Economy, Manchester University Press, Manchester, United Kingdom.

Fair, R. and Taylor, J.B. (1983), 'Solution and maximum likelihood

estimation of dynamic non-linear rational expectations models',

Econometrica 51, 1169-85.

Fisher, F.M. (1966), The Identification Problem, McGraw-Hill, New York.

Frenkel, J.A. (1981), 'The collapse of purchasing power parity during the

1970s', European Economic Review 16, 145-65.

Futia, C.A. (1981) 'Rational expectations in stationary linear models',

Econometrica 49, 171-92.

Granger, C.W.J. and Newbold, P. (1977), Forecasting Economic Time Series

Academic Press, New York.

39

Grossman, J. (1979), 'Nominal demand policy and short-run fluctuations in

unemployment and prices in the United States', Journal of Political

Economy 87, 1063-85.

Hansen, L.P. and Singleton, K.J. (1982), 'Generalised instrumental

variables estimation of non-linear rational expectations models',

Econometrica 50, 1269-86.

Jordan, J.S. (1980), 'On the predictability of economic events',

Econometrica 48, 955-86.

Kantor, B. (1979), 'Rational expectations and economic thought', Journal of

Economic Literature 17, 1422-41.

Keynes, J.M. (1936) The General Theory of Employment Interest and Money,

Macmillan, London.

Lucas, R.E. (1972), 'Expectations and the neutrality of money', Journal of

Economic Theory 4, 103-4.

___ (1976), 'Econometric policy evaulation: a critique', in K. Brunner and

A.H. Meltzer (eds) , The Phillips Curve and Labour Markets,

Carnegie-Rochester Conference Series, No.1, North Holland, New York,

19-46.

___ and Sargent, T.J. (1978), 'After Keynesian macro-economics' in After

the Phillips Curve: Persistence of High inflation and High Unemployment,

Federal Reserve Bank of Boston, Massachusetts.

Marschak, J. (1953), 'Economic measurements for policy and prediction',

W.C. Hood and T.C. Koopmans (eds) , Studies in Econometric Methods, Yale

University Press, Connecticut.

Metzler, L. (1941), 'The nature and stability of inventory cycles', Review

of Economics and Statistics 3, 113-29.

40

"

.'

Mccallum, B.T. (1976a), 'Rational expectations and the estimation of

economists' models: an alternative procedure', International Economic

Review 17, 484-90.

(1976b), 'Rational expectations and the natural rate hypothesis: some

consistent estimates', Econometrica 44, 43-52.

___ (1983), 'On non-uniqueness in rational expectations: an attempt at

perspective', Journal of Monetary Economics II, 139-68.

Mishkin, F.S. (1983) A Rational Expectations Approach to Macroeconometrics,

National Bureau of Economic Research Monograph, University of Chicago

Press, Chicago.

Muth, J.F. (1961), 'Rational expectations and the theory of price

movements', Econometrics 29, 315-35.

Nelson, C.R. and Schwert, G.w. (1977), 'Short term interest rates as

predictors of inflation: on testing the hypothesis that the real rate is

constant', American Economic Review 67, 475-86.

Nerlove, M. (1958), 'Adaptive expectations and cobweb phenomena', Quarterly

Journal of Economics 72, 227-40.

Pagan, A. (1984), 'Econometric issues in the analysis of regressions with

generalised regressors', International Economic Review 25, 221-48.

pesaran, M.H. (1981), 'Identification of rational expectations models',

Journal of Econometrics 16, 375-98.

Radner, R. (1982), 'Equilibrium under uncertainty', in K.J. Arrow and

M.D. Intriligator (eds), Handbook of Mathematical Economics, Vol. II,

North Holland, Amsterdam.

Revankar, N.S. (1980), 'Testing of the rational expectations hypothesis',

Econometrica 48, 1347-63.

41

Rothenberg R.J. (1973), Efficient Estimation with A Priori Information,

Cowles Foundation Monograph No. 23, Yale University press, Connecticut.

Saracoglu,·R. and Sargent, T.J. (1978), 'seasonality and portfolio balance

under rational expectations', Journal of Monetary Economics 4, 435-54.

Sargent, T.J. (1973), 'Rational expectations, theoretical rate of interest,

and the natural rate of unemployment', Brookings Papers on Economic

Activity 2, 429-72.

___ (1976), 'The observational equivalence of natural and unnatural rate

theories of macroeconomics', Journal of Political Economy 84, 631-640.

___ (1979), Macroeconomic Theory, Academic Press, New York.

___ (1981), 'Interpreting economic time series', Journal of Political

Economy 89, 213-48.

___ and Wallace, N. (1975), 'Rational expectations, the optimal monetary

instrument and the optimal money supply rule', Journal of Political

Economy 83, 241-54.

___ and (1976), 'Rational expectations and the theory of economic

policy', Journal of Monetary Economics 2, 169-83.

Sheffrin, S. (1979), 'Unanticipated monetary growth and output

fluctuations', Economic Inquiry 17, 1-13.

___ (1983), Rational Expectations, Cambridge University Press, United

Kingdom.

Shiller R.J. (1978), 'Rational expectations and the dynamic structure of

macroeconomic models', Journal of Monetary Economics 4,1-44.

___ (1980), 'Can the Fed control real interest rates?' in S. Fisher (ed.) ,

Rational Expectations and Economic Policy, University of Chicago Press,

Chicago.

42

•

,

•

•

Sims, C.A. (1980), 'Macroeconomics and reality', Econometrica 48, 1-48.

Startz, R. (1983), 'Testing rational expectations by the use of

overidentifying restrictions', Journal of Econometrics 23; 343-51.

Taylor, J.B. (1977), 'On conditions for unique solutions in stochastic

macroeconomic models with price expectations', Econometrica 45, 1377-86.

(1985), 'New econometric techniques for macroeconomic policy

evaluation' in Z. Griliches and M.D. Intriligator (eds), Handbook of

Econometrics, Vol. 3, North Holland, Amsterdam.

Wallis, K.F. (1980), 'Econometric implications of the rational expectations

hypothesis', Econometrica 48, 49-72.

Wegge, L.L. and M. Feldman (1983), 'Identifiability criteria for

Muth-rational expectations models', Journal of Econometrics 21, 245-54.

Whiteman, C.H. (1983), Linear Rational Expectations Models: A Users Guide,

University of Minnesota Press, Minneapolis.

Wickens, M.R. (1982), 'The efficient estimation of econometric models with

rational expectations', Review of Economic Studies 49, 55-68 •

43