Embed Size (px)

Citation preview

Risk Management Practices of the Hong Kong

Insurance Industry Survey 2011

The Actuarial Society of Hong Kong

Investment & Risk Management Committee, ASHK

26 June 2012

2

1st industry wide survey conducted in 2008 during the crisis, covering

a comprehensive scope. Companies demonstrated an increasing

importance towards risk management concept while were still finding

their ways through new approaches.

2 years since then with SII introduced and August 2011 US

downgrade plus European debt issues have aroused another new

situation which is often said to be worse than 2008. 2nd survey to be

conducted on similar questions and more specific scopes.

Let’s see where the industry is at now……

Background

3

Part 1: Risk Management Overview

Part 2 : Regulatory Impact

Part 4 : Interest Rate and Equity Risk, the latest “crisis”

Part 5 : Currency Risk

Part 6 : Stress testing and overall Wrap Up

Part 3 : Capital Risk

Table of Content

4

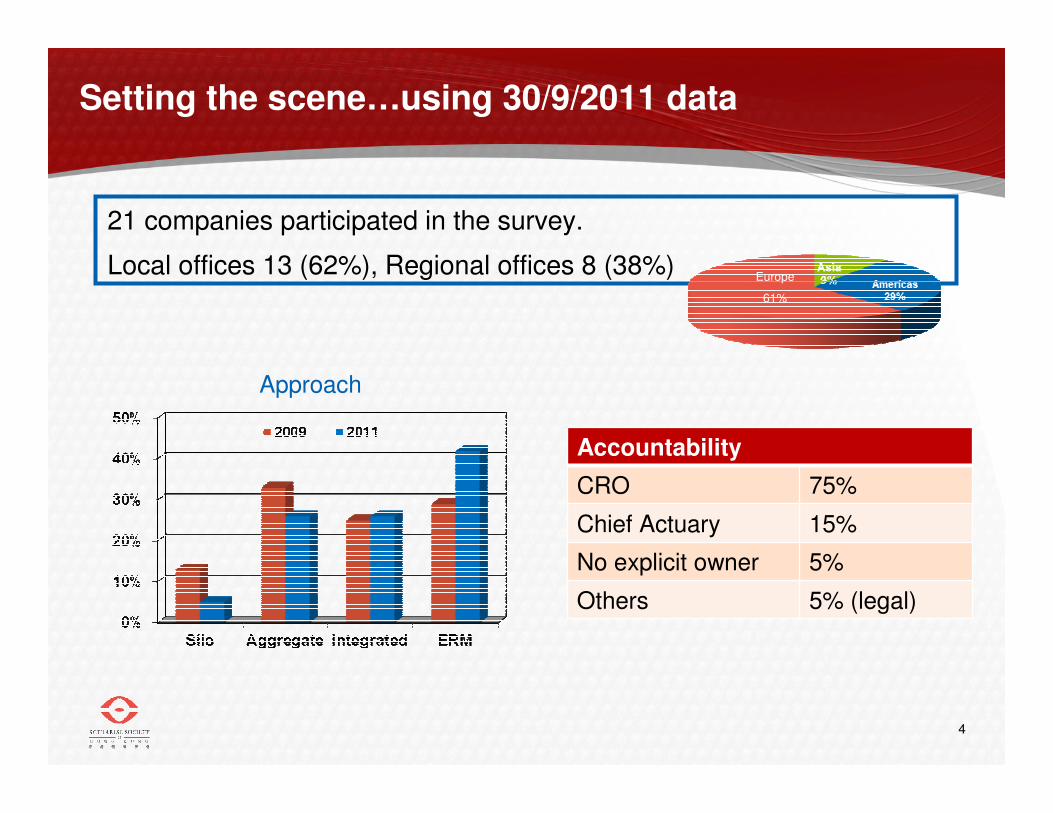

Setting the scene…using 30/9/2011 data

21 companies participated in the survey.

Local offices 13 (62%), Regional offices 8 (38%)

Approach

Accountability

CRO 75%

Chief Actuary 15%

No explicit owner 5%

Others 5% (legal)

Europe

61%

5

Asset and liability positions (local offices only)

(rounded to the nearest %) 2011 2009

Corporate bond 49% 62%

Government bond 23% 11%

Equities (and fund) 10% 11%

Cash / money market 14% 9%

Mortgage / ABS 2% 2%

Policy loans 1% 2%

Real estate 0% 1%

Hedge funds 0% 0%

Others * 1% 2%

Asset class holding Product portfolio

* Other loans and account receivables

6

Key risks to company

Respondents asked to rank 1st to 3rd (1st scores 3, 2nd scores 2, 3rd scores 1)

0

5

10

15

20

25

30

35

40

45

50

Interest rate Equity Credit Liquidity Operational Reputation Capital vol /

level

Regulatory Others

One year ago

Current

Currency, insurance risks

7

Risk management program - Drivers

Respondents asked to rank 1st to 3rd (1st scores 3, 2nd scores 2, 3rd scores 1)

0

5

10

15

20

25

30

35

40

45

50

Head office

requirements

Good business

practice

Regulations GFC impact Shareholders'

need

Rating agency Manage

complex risk

exposures

Competitive

advantage

One year ago Current

8

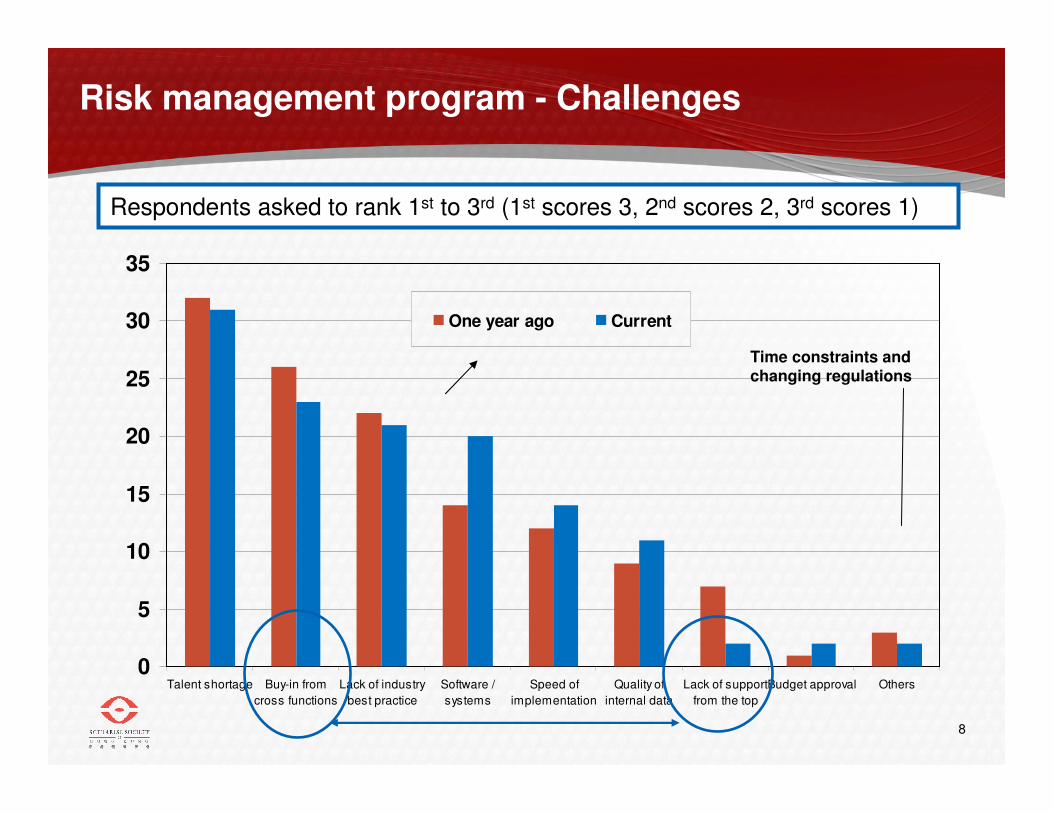

Risk management program - Challenges

Respondents asked to rank 1st to 3rd (1st scores 3, 2nd scores 2, 3rd scores 1)

0

5

10

15

20

25

30

35

Talent shortage Buy-in from

cross functions

Lack of industry

best practice

Software /

systems

Speed of

implementation

Quality of

internal data

Lack of support

from the top

Budget approval Others

One year ago Current

Time constraints and changing regulations

9

Satisfactory level to internal capabilities

Risk management components: Most Least

Framework and governance structure ☺☺☺☺ ☺☺☺☺ ☺☺☺☺

Definition of risk appetites and risk limits ☺☺☺☺ ���� ����

Risk indicators and identification

Risk measurement and quantification ☺☺☺☺ ☺☺☺☺

Internal / external risk reporting and disclosure ���� ���� ����

Internal education and communication of risk policies

Linking senior management remuneration to risk performance ����

10

Alignment of Risk to Strategy

No explicit alignment

1. ERM forms part of strategic planning

2. Integration of risk appetite into business decision process

Closely integrated

11

Part 1: Risk Management Overview

Part 2 : Regulatory Impact

Part 4 : Interest Rate and Equity Risk, the latest “crisis”

Part 5 : Currency Risk

Part 6 : Stress testing and overall Wrap Up

Part 3 : Capital Risk

Table of Content

12

Concerns over regulatory risks

Move up in risk priority No change Less important

60% 35% 5%

Areas of regulatory changes in concern, in order (tick all apply): Most important

1. Local country regulations – capital requirements43%

2. Local country regulations – reserving methodology

3. Local regulators communication / transparency / structure

4. Capital – volatility imposed by economic balance sheet50%

5. Capital – level required by Solvency II

6. Overall tighter scrutiny on distribution, marketing, disclosure 7%

7. Treatment of residual margin and discount rate with IFRS

13

What are the concerns over regulatory risks?

0

2

4

6

8

10

12

14

16

18

20

Inhouse talent

shortage

Uncertainty makes

planning difficult

Pace of change is

distracting

Model risks related to

new rules

Impact on profitability

and competitiveness

Heavy costs of

implementation

One year ago Current

Tick all that apply – sum of responses

14

Views on Solvency II…

European Companies Non Solvency II Practitioners

Top 3 challenges to Solvency II implementation to date

1. Build capacity and flexibility to cope with potential surprises from further guidance

2. Devise detail action plans to define key stakeholders’ role, work flow and procedures

3. Develop adequate subject matter resources

15

Part 1: Risk Management Overview

Part 2 : Regulatory Impact

Part 4 : Interest Rate and Equity Risk, the latest “crisis”

Part 5 : Currency Risk

Part 6 : Stress testing and overall Wrap Up

Part 3 : Capital Risk

Table of Content

16

Capital measures – what is everyone using now?

Others include Local, ICA, S&P

� Majority using at least 2 capital measures.

� Most popular combination -Solvency I & RBC/EC.

17

Capital measures – what is everyone thinking now?

Rank importance (1-3)

18

Capital measures – what is everyone thinking in 5 years time?

Rank importance (1-3)

19

Capital calculation – RBC / EC / Solvency II SCR

Measures Key survey results

Implementation 50% with “5+ years”

Frequency 73% with “Quarterly”

Time horizon 86% with “1 year”

VaR or CTE 75% with “VaR alone”

Satisfaction level (1 = “Not at all” and 5 = “Very”)

53% with “3”; 33% with either “4” or “5”

20

Capital calculation – Benefits

Provides uniform, clear, comparableand transparentquantification and presentation of different type of risks

Allows risk management to be embedded in the

business decision process

Risk-based and under economic basis regardless of accounting rules

Allows easier communication with senior management

Transparency of risks as the measures set out explicitly the capital requirement for the various risks considered. This provides management with a better view of the key risks.

RBC / EC / Solvency II SCR

RBC / EC / Solvency II SCR

21

Capital calculation – Weakness

Lack full understanding and adoption of the measure

RBC / EC / Solvency II SCR

RBC / EC / Solvency II SCR

Resource constraint

May contradict the result under accounting basis

Lacking credible calibration of the required shocks to use (due to lack of

data, various possible calibration approaches, etc)

Reliance on historical data to estimate parameters for probability distributions, and

that the model distribution may not fit reality

Large risk charge on equities, and overly complicatedmethodology which makes it difficult to understand changes and extremely difficult to communicate and explain to management

Correlation is subjective

22

Capital regime and reserving basis

Q1: Do you consider a need to review the reserving basis if HK is to move to RBC

regime?

Q2: What is your view on when, if ever, Hong Kong should move to a RBC regime?

75%

23

Capital requirement volatility

Q3: Should volatility of capital requirement (the risk thereof) be a consideration

when designing a regulatory capital base? 1 to 5 with 1 = “Not at all” and 5 =

“Very agree”.

24

Capital regime uncertainties

The greatest hurdles when moving towards RBC regime

� Long-term products require long-maturity assets to reduce asset and liability mismatch risk, butmarket lack credible HK yield curve.

� Acceptance of industry to penalise current accepted practices (e.g. ALM mismatch) is difficult.

� Equity (subject to higher risk charge) would be less attractive to invest thus par products would be penalised.

� Lack of resources and skills to build and implement RBC for both regulator and insurance players.

� Subject to capital availability in the market.

� Multiple solvency requirements for international insurance companies.

� Only change capital requirement but keep the reserving basis unchanged� Should consider both under RBC-type capital regime.

� Require stochastic modelling capability, calibration of shocks, consistent methodology and transparent reporting.

� Lack of historical data to set management action and dynamic policyholder behavior.

25

Part 1: Risk Management Overview

Part 2 : Regulatory Impact

Part 4 : Interest Rate and Equity Risk, the latest “crisis”

Part 5 : Currency Risk

Part 6 : Stress testing and overall Wrap Up

Part 3 : Capital Risk

Table of Content

26

Liability Management: Existing Portfolio

Responses on Product Management

• Unprofitable products likely to be closed as of last survey• Resort to dividend mechanisms• More inclined to develop new products

68%

87%

69%

54%

66%

20%

32%

13%

31%

46%

34%

80%

0% 25% 50% 75% 100%

2010

Adj Dividend rates 2011

2010

Develop new products 2011

2010

Closing certain products 2011

Yes No

200920092009201120112011

27

Liability Management: New Products

Relative change to / intention to change the product mix of new business sales

Decrease No change Increase

Pure risk / health 0% 35% 65%

Participating products 28% 56% 17%

Non-participating products 24% 59% 18%

Investment linked (with guarantees) 40% 60% 0%

Investment linked (without guarantees) 12% 41% 47%

Non-life / Others 0% 94% 6%

• Move away from guaranteed products• Move more towards risk products• Move more towards investment linked products

28

Management of assets

CashGov’t bond

Corp bond

EquitiesReal

EstatePolicy Loan

Hedge funds

MBS/ ABS

Increased 30% 33% 30% 0% 30% 6% 12% 0%

No change 70% 62% 55% 67% 65% 88% 82% 82%

Decreased 0% 5% 15% 33% 5% 6% 6% 18%

Responses to the sovereign crisis

Yes:79% No:21%

Asset management arrangement

10%

Shift to In-house

No Change : 85%

More dynamic asset allocation

Shift to Outsource

5%

29

Actions for Unforeseeable Future Events

Non-Guaranteed

Products

Unit-linked

Products

Dynamic allocation in

the investment process

Intention to increase

78% 83% 50%

No change 22% 17% 50%

30

Part 1: Risk Management Overview

Part 2 : Regulatory Impact

Part 4 : Interest Rate and Equity Risk, the latest “crisis”

Part 5 : Currency Risk

Part 6 : Stress testing and overall Wrap Up

Part 3 : Capital Risk

Table of Content

31

Currency Mismatch Risk

No

80.0%

Materiality of HKD Currency Mismatch

Do your company use separate duration measurement for different currency?

Immaterial 64%

Somewhat sizeable

23%

Significant and should be dealt with

14%

32

Level of Currency Mismatch Reserve

33

Changes since 2008 financial crisis

No

80.0%

No

46.3%

No 13.3%

34

Instruments use to manage currency exposures

No

80.0%

No

46.3%

No 13.3%

• Participants can select more than one instrument in the survey

35

Managing and taking currency risks

No

80.0% No

46.3%

No 13.3%

Number of instruments used for managing currency risks

Do your company use asset managers to profit from taking currency risks explicitly?

Use Four Types7%

Use One Type43%

Using Two Types36%

Using Three Types14%

No95%

Yes5%

36

Part 1: Risk Management Overview

Part 2 : Regulatory Impact

Part 4 : Interest Rate and Equity Risk, the latest “crisis”

Part 5 : Currency Risk

Part 6 : Stress testing and overall Wrap Up

Part 3 : Capital Risk

Table of Content

37

Purpose of Stress Testing

What type of risks are covered?

20 out of 21 companies perform stress testing / 12 local and 8 regional offices

• Other risks covered in stress testing are: implied volatility risk, credit spread risk and expense risk

38

Purpose of Stress Testing (cont’d)

Importance of risks vs. risks covered in stress testing

80%

40%

15%20%

5%

100% 95%

80%

60%

40%

0%

20%

40%

60%

80%

100%

Interest rate risk Equity risk Credit risk Operational risk Liquidity risk

Risk typesThe 3 most important risks seen by companies Covered in stress testing

39

Drivers of Stress Testing

70% 75%90%

30% 25%10%

0%

20%

40%

60%

80%

100%

Regulator - local Regulator - group Internal risk

management

Yes No

40

Frequency of Stress Testing

6% 5%

12% 28%

55%6%

5%82%

66%

20%

15%

0%

20%

40%

60%

80%

100%

Regulator - local Regulator - group Internal risk management

One-off

Irregular

Annually

Bi-annually

Quarterly

Monthly

41

Frequency of Stress Testing (cont’d)

How often do we perform stress testing for internal risk

management in relation to asset portfolio size?

25%

45%

75%33%

22%

0%

20%

40%

60%

80%

100%

<$50 billion >=$50 billion

Asset portfolio size

Irregular

Annually

Quarterly

Monthly

42

Measurements/ Risk Metrics used

Other risk metrics that we have used are: MCEV(EEV), Embedded Value, new business strain, experience variance, liquidity cover

80%

65% 60%

30%

20%

35% 40%

70%

0%

20%

40%

60%

80%

100%

Statutory

Solvency ratio &

Capital

Economic

Capital

IFRS profit Statutory profit

No

Yes

43

Time horizon of stress testing performed

Snapshot on

current position

only

30%

Projected 1 year

15%Projected 3-4 years

30%

Projected 5 years

20%

Not

provided

5%

40%

20%

67%

20%

33%

20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

<$50 billion >=$50 billion

Asset portfolio size

Snapshot on current position only Projected 1 year

Projected 3-4 years Projected 5 years

Time Horizon used in Stress Testing

44

Types of modelling used

50%

20%

85%

15%

30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Deterministic Stochastic

With dynamic policyholder behaviour Without dynamic policyholder behaviour Yes No

45

Types of modelling used (cont’d)

Choice of model type in relation to location of head office

Deterministic

25%

Stochastic

17%

Deterministic +

Stochastic

58%

Deterministic

38%

Stochastic

12%

Deterministic +

Stochastic

50%

European Companies Non Solvency II Practitioners

46

Key takeaways (1)…

• Regulatory

– General concern over regulatory capital, and how regulators react to current (still) volatile market

– Seem overall agreement that RBC is the way to go but not all companies are prepared for the requirements

– A portion of non-European based insurers to catch up on sophisticated modeling?

– Believe in implementation of SII?

• Product strategy

– Moving towards risk products and less guarantees, health an apparent trend

– At current economic condition, illustrated yields set PRE? Affordable level? How to manage going forward given the smaller room….

– Dilemma: competition reactions drive behavior and strategy?

47

Key takeaways (2)…

• ALM and profit enhancement

– Cautious and gone / going through significant de-risking

– Variations in currency risk management – 1/3 said mismatch sizable!

– Are we still relying on the peg?

• Industry attitude and mindset to ERM

– Multiple perspectives and acquainted with process, more buy-in from the top

– Still uncertainty around internal and external disclosures

– Overall a good sign to industry

Risk Management Practices of the Hong Kong

Insurance Industry Survey 2011

The Actuarial Society of Hong Kong

Presenters:

Ms. Ka-Man Wong / Mr. Peter Fang / Mr. Steve Tong / Mr. Andrew Siu

26 June 2012

Thank you – Q&A