Embed Size (px)

Citation preview

TEXAS STATEWIDE TELEPHONE COOPERATIVE, INC.FCC CHANGES TO PART 32 –

What You Need to Know

Presented by Wade Wilson, C.P.A.

Bolinger, Segars, Gilbert & Moss, L.L.P.

8215 Nashville Ave. ; Lubbock, Texas 79423

806-747-3806 www.bsgm.com

2017 Accounting, Marketing & Customer Service Conference

Test of Your Attention to Detail

Bolinger, Segars, Gilbert & Moss, L.L.P. 2

Bolinger, Segars, Gilbert & Moss, L.L.P. 3

:ØComplete the FCC’s proceeding to review its Part 32

Uniform System of Accounts (USOA) to consider: v Ways to minimize the compliance burdens on carriers v Ensure the FCC retains access to the information it needs to

fulfill its regulatory duties.

Bolinger, Segars, Gilbert & Moss, L.L.P. 4

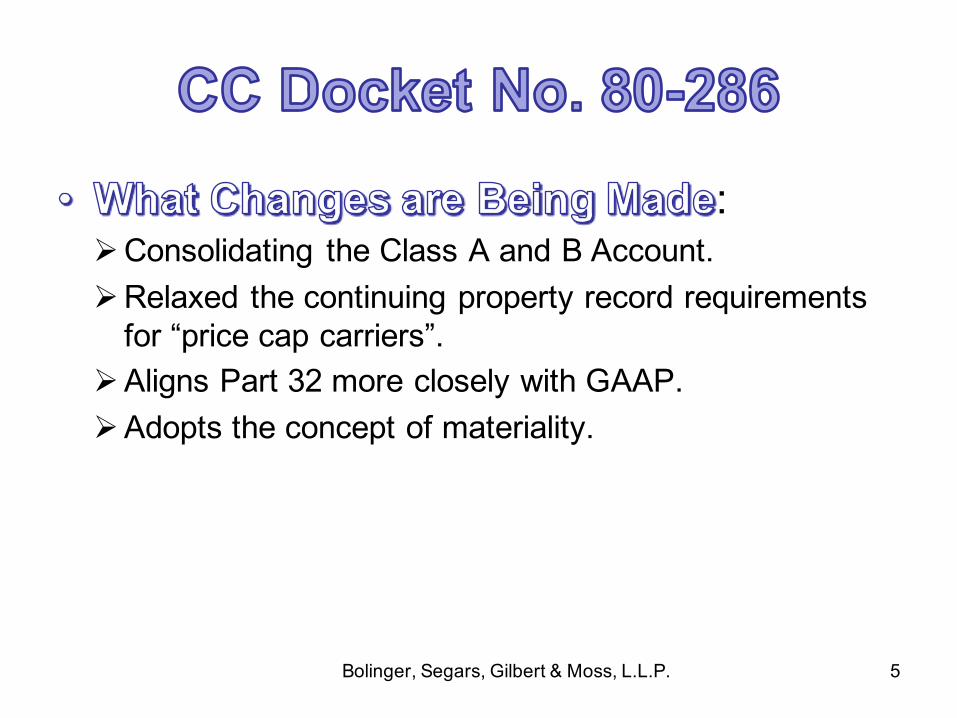

:ØStreamline and eliminate outdated accounting rules no

longer needed.ØReduce the cost burden of outdated regulatory

requirements.ØReducing compliance cost allows carriers to better

allocate resources toward expanding modern networks.

Bolinger, Segars, Gilbert & Moss, L.L.P. 5

:ØConsolidating the Class A and B Account.ØRelaxed the continuing property record requirements

for “price cap carriers”.ØAligns Part 32 more closely with GAAP.ØAdopts the concept of materiality.

Bolinger, Segars, Gilbert & Moss, L.L.P. 6

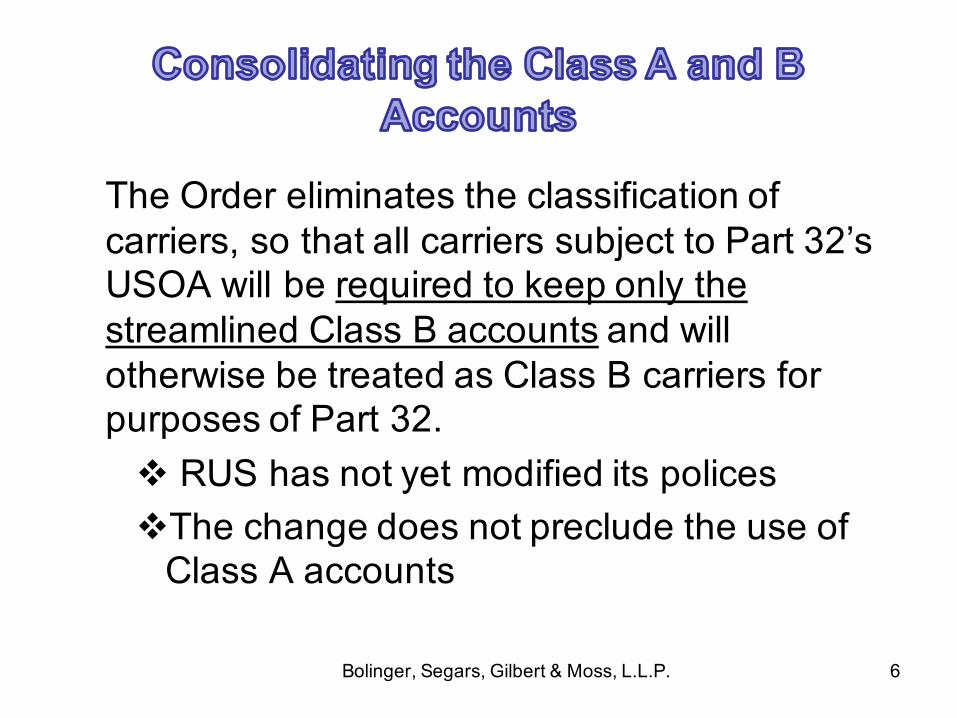

The Order eliminates the classification of carriers, so that all carriers subject to Part 32’s USOA will be required to keep only the streamlined Class B accounts and will otherwise be treated as Class B carriers for purposes of Part 32.v RUS has not yet modified its policesvThe change does not preclude the use of

Class A accounts

Bolinger, Segars, Gilbert & Moss, L.L.P. 7

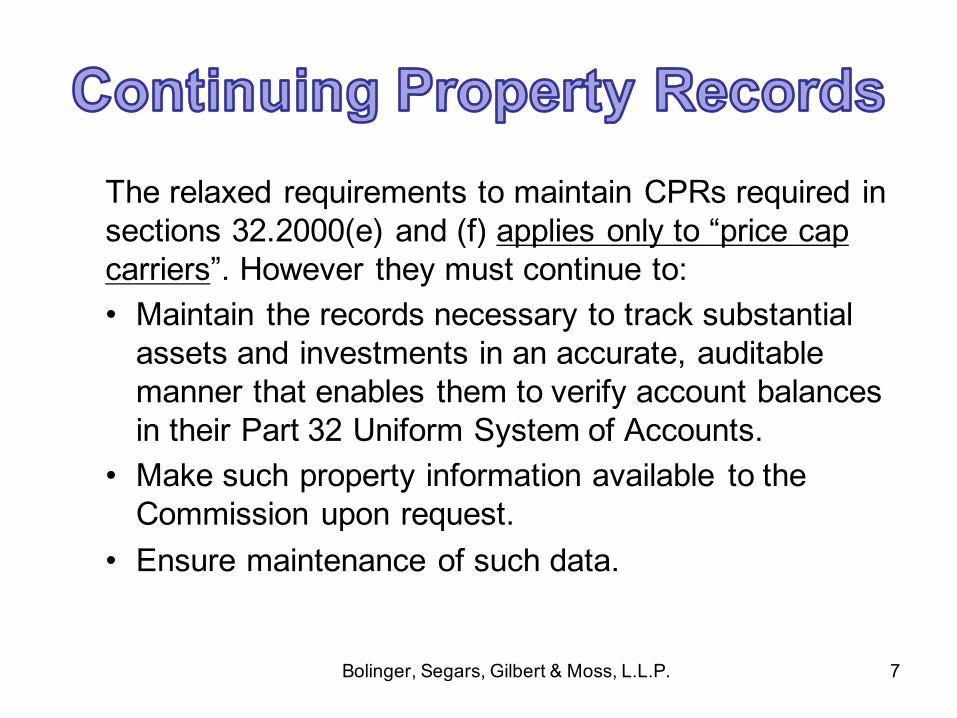

The relaxed requirements to maintain CPRs required in sections 32.2000(e) and (f) applies only to “price cap carriers”. However they must continue to:• Maintain the records necessary to track substantial

assets and investments in an accurate, auditable manner that enables them to verify account balances in their Part 32 Uniform System of Accounts.

• Make such property information available to the Commission upon request.

• Ensure maintenance of such data.

Bolinger, Segars, Gilbert & Moss, L.L.P. 8

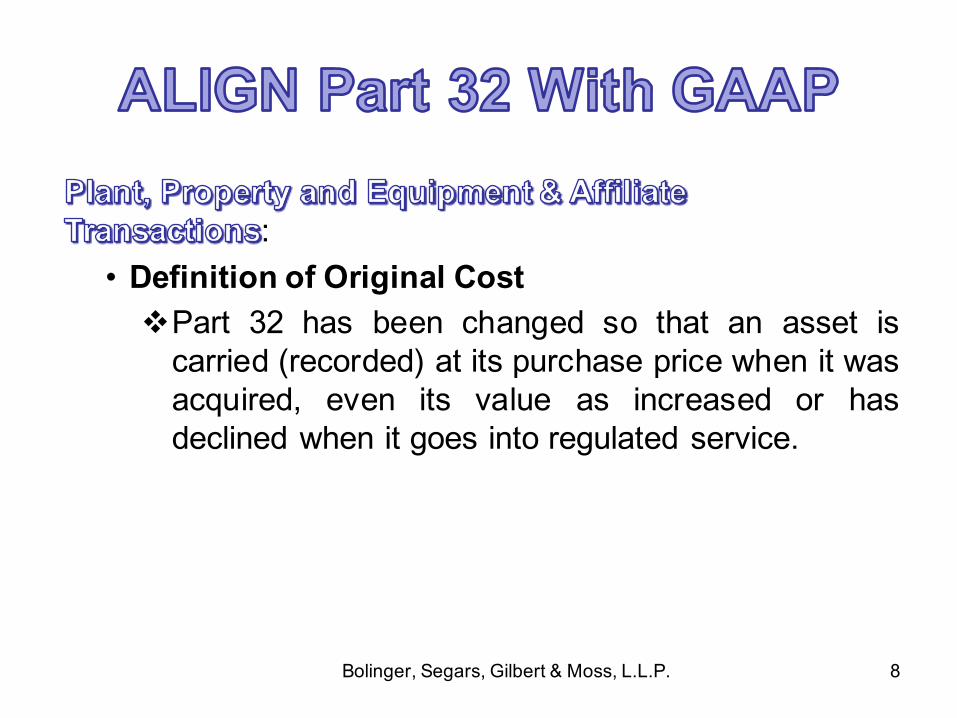

:• Definition of Original Cost

vPart 32 has been changed so that an asset iscarried (recorded) at its purchase price when it wasacquired, even its value as increased or hasdeclined when it goes into regulated service.

Bolinger, Segars, Gilbert & Moss, L.L.P. 9

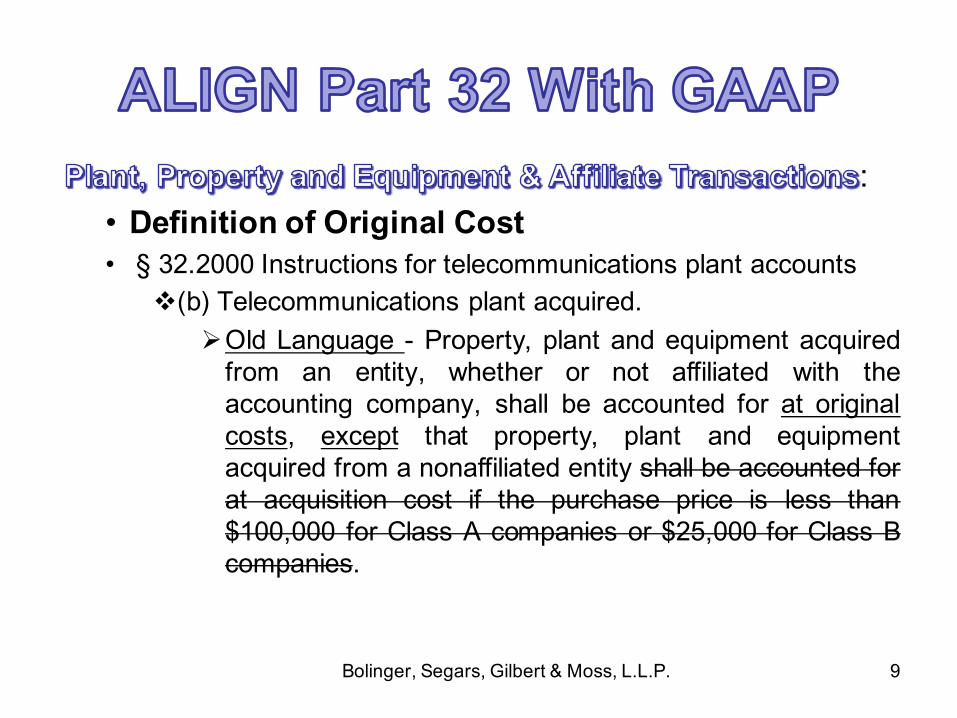

:• Definition of Original Cost• § 32.2000 Instructions for telecommunications plant accounts

v(b) Telecommunications plant acquired.ØOld Language - Property, plant and equipment acquired

from an entity, whether or not affiliated with theaccounting company, shall be accounted for at originalcosts, except that property, plant and equipmentacquired from a nonaffiliated entity shall be accounted forat acquisition cost if the purchase price is less than$100,000 for Class A companies or $25,000 for Class Bcompanies.

Bolinger, Segars, Gilbert & Moss, L.L.P. 10

:

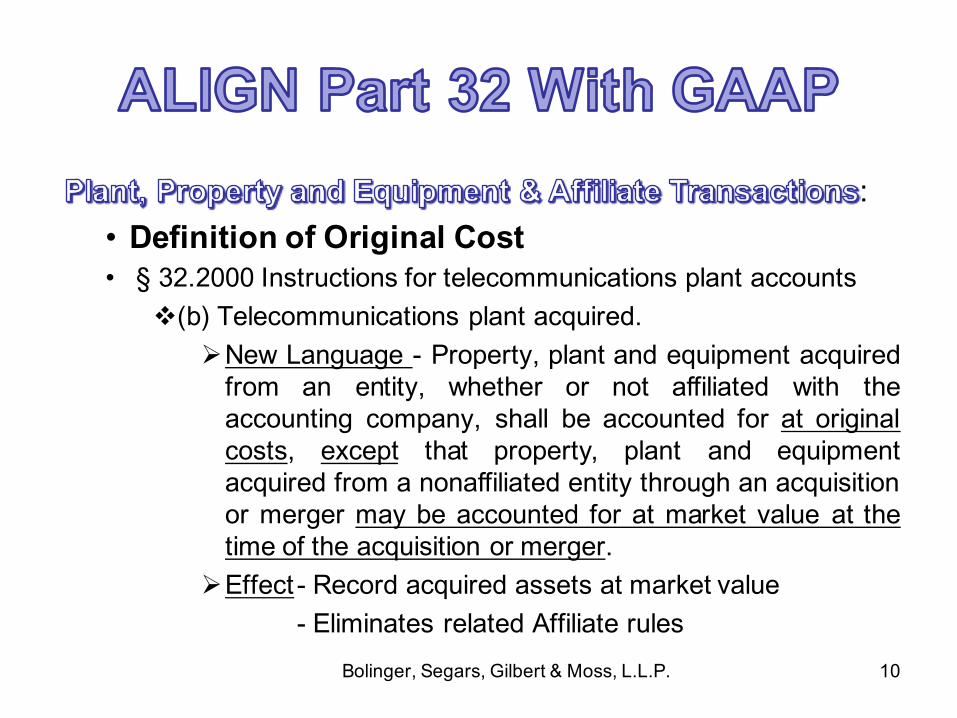

• Definition of Original Cost• § 32.2000 Instructions for telecommunications plant accounts

v(b) Telecommunications plant acquired.ØNew Language - Property, plant and equipment acquired

from an entity, whether or not affiliated with theaccounting company, shall be accounted for at originalcosts, except that property, plant and equipmentacquired from a nonaffiliated entity through an acquisitionor merger may be accounted for at market value at thetime of the acquisition or merger.

ØEffect - Record acquired assets at market value- Eliminates related Affiliate rules

Bolinger, Segars, Gilbert & Moss, L.L.P. 11

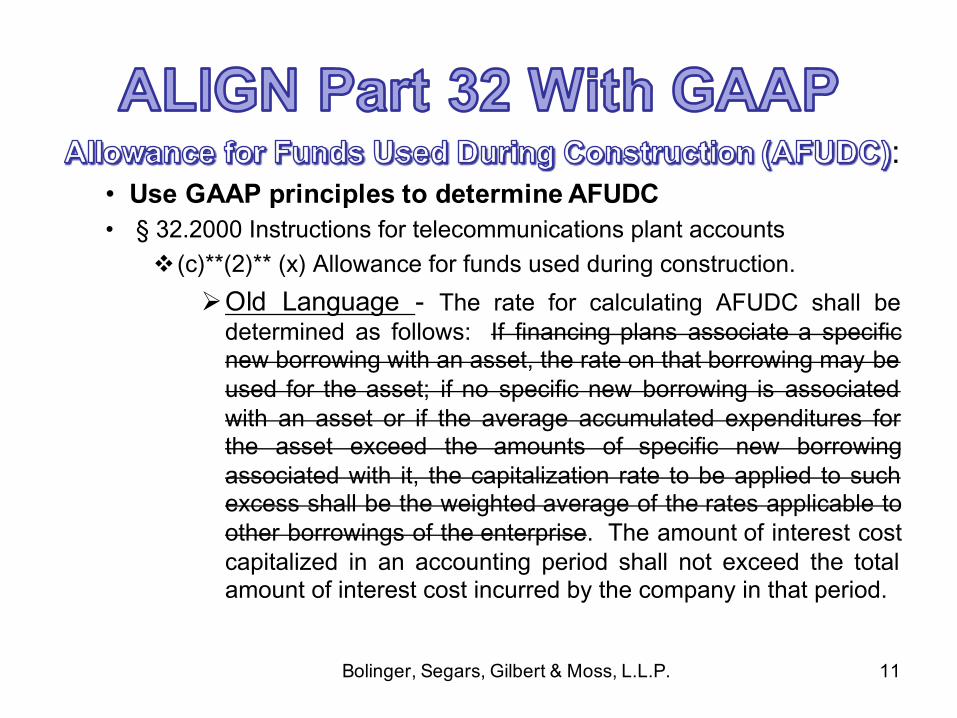

:• Use GAAP principles to determine AFUDC • § 32.2000 Instructions for telecommunications plant accounts

v (c)**(2)** (x) Allowance for funds used during construction.

ØOld Language - The rate for calculating AFUDC shall bedetermined as follows: If financing plans associate a specificnew borrowing with an asset, the rate on that borrowing may beused for the asset; if no specific new borrowing is associatedwith an asset or if the average accumulated expenditures forthe asset exceed the amounts of specific new borrowingassociated with it, the capitalization rate to be applied to suchexcess shall be the weighted average of the rates applicable toother borrowings of the enterprise. The amount of interest costcapitalized in an accounting period shall not exceed the totalamount of interest cost incurred by the company in that period.

Bolinger, Segars, Gilbert & Moss, L.L.P. 12

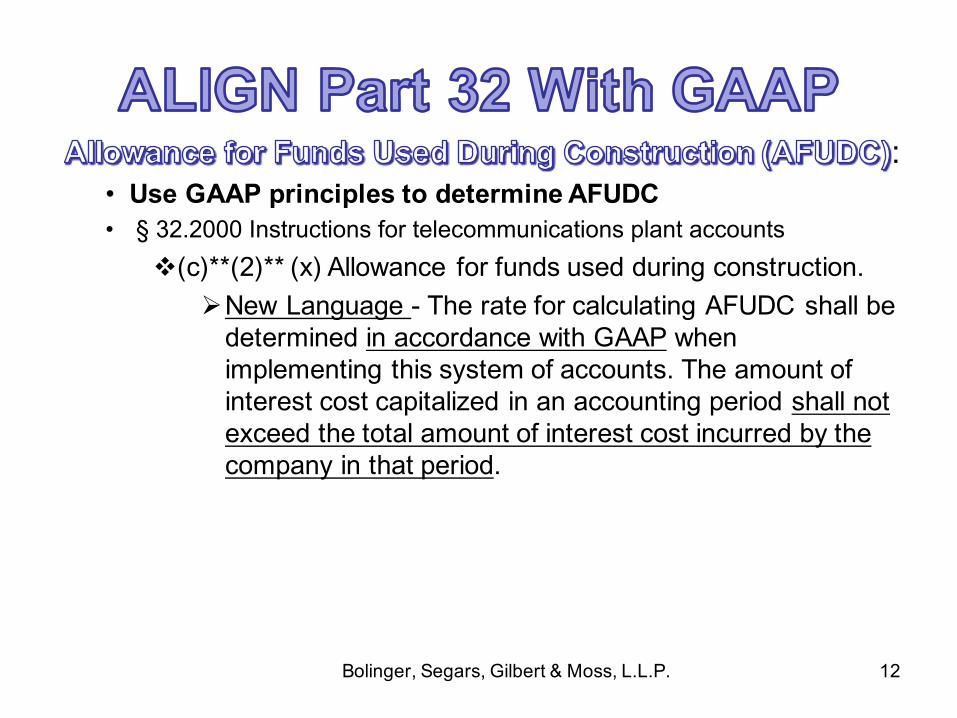

:• Use GAAP principles to determine AFUDC• § 32.2000 Instructions for telecommunications plant accounts

v(c)**(2)** (x) Allowance for funds used during construction.ØNew Language - The rate for calculating AFUDC shall be

determined in accordance with GAAP when implementing this system of accounts. The amount of interest cost capitalized in an accounting period shall not exceed the total amount of interest cost incurred by the company in that period.

Bolinger, Segars, Gilbert & Moss, L.L.P. 13

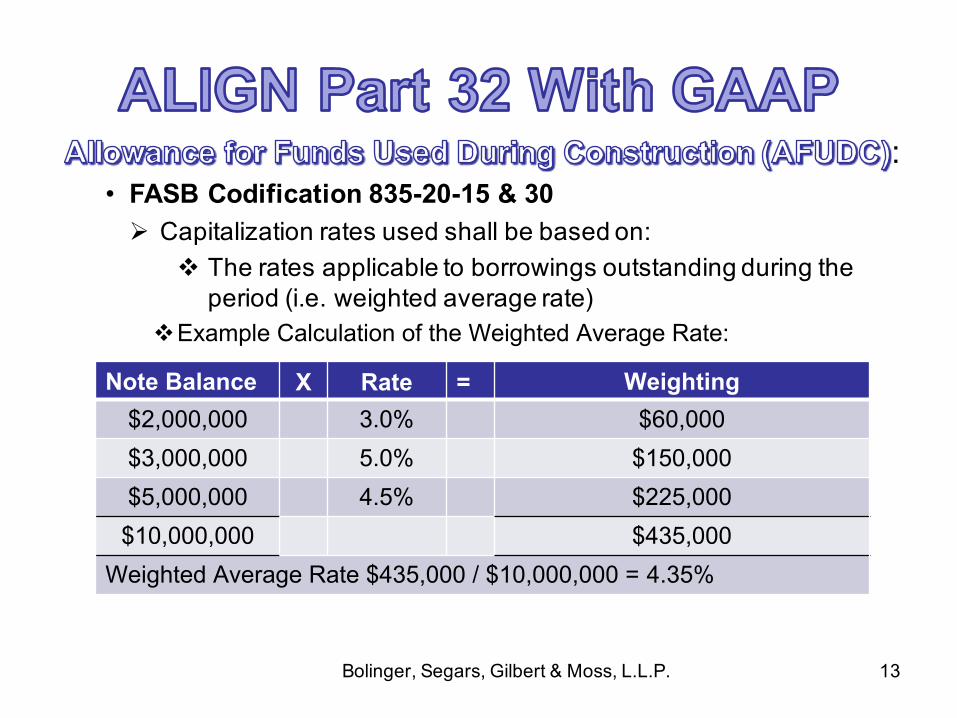

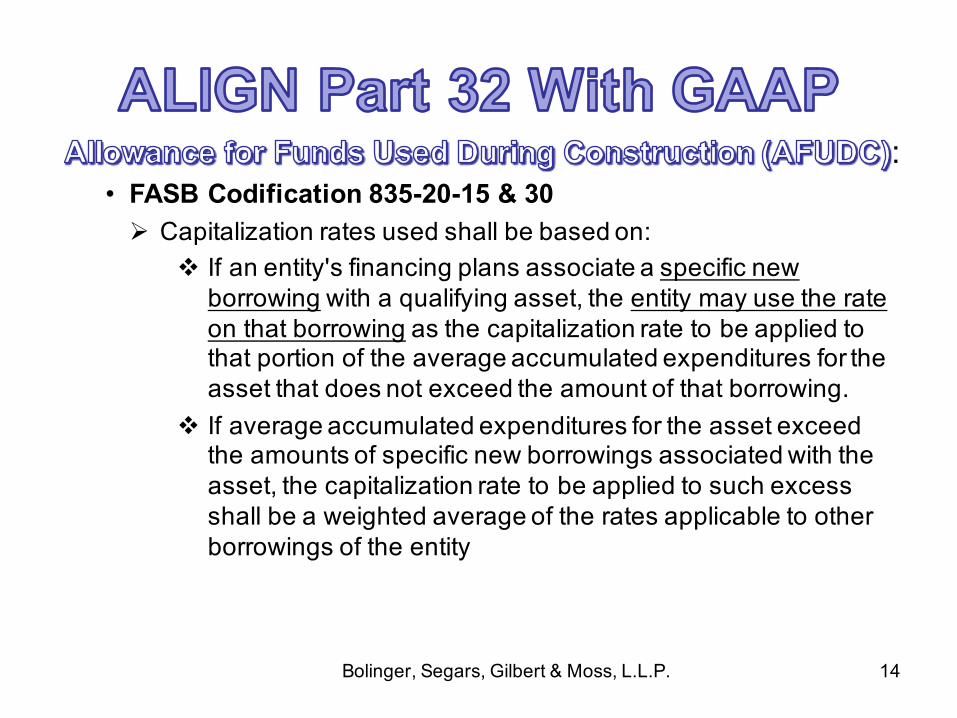

:• FASB Codification 835-20-15 & 30Ø Capitalization rates used shall be based on:

v The rates applicable to borrowings outstanding during the period (i.e. weighted average rate)

vExample Calculation of the Weighted Average Rate:

Note Balance X Rate = Weighting$2,000,000 3.0% $60,000

$3,000,000 5.0% $150,000

$5,000,000 4.5% $225,000

$10,000,000 $435,000

Weighted Average Rate $435,000 / $10,000,000 = 4.35%

Bolinger, Segars, Gilbert & Moss, L.L.P. 14

:• FASB Codification 835-20-15 & 30Ø Capitalization rates used shall be based on:

v If an entity's financing plans associate a specific new borrowing with a qualifying asset, the entity may use the rate on that borrowing as the capitalization rate to be applied to that portion of the average accumulated expenditures for the asset that does not exceed the amount of that borrowing.

v If average accumulated expenditures for the asset exceed the amounts of specific new borrowings associated with the asset, the capitalization rate to be applied to such excess shall be a weighted average of the rates applicable to other borrowings of the entity

Bolinger, Segars, Gilbert & Moss, L.L.P. 15

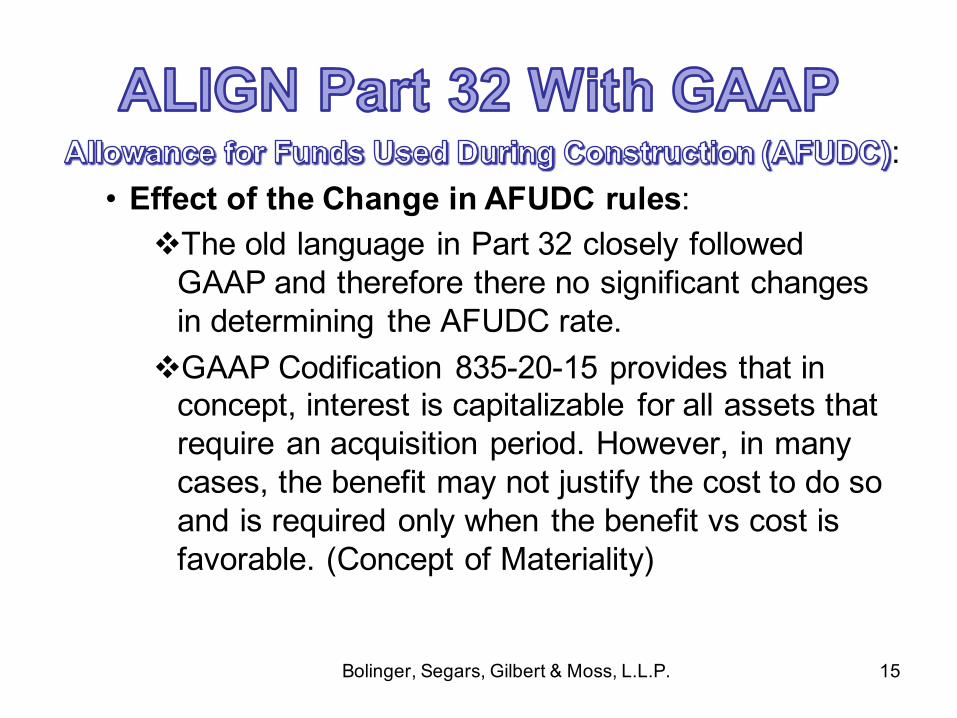

:• Effect of the Change in AFUDC rules:

vThe old language in Part 32 closely followed GAAP and therefore there no significant changes in determining the AFUDC rate.

vGAAP Codification 835-20-15 provides that in concept, interest is capitalizable for all assets that require an acquisition period. However, in many cases, the benefit may not justify the cost to do so and is required only when the benefit vs cost is favorable. (Concept of Materiality)

Bolinger, Segars, Gilbert & Moss, L.L.P. 16

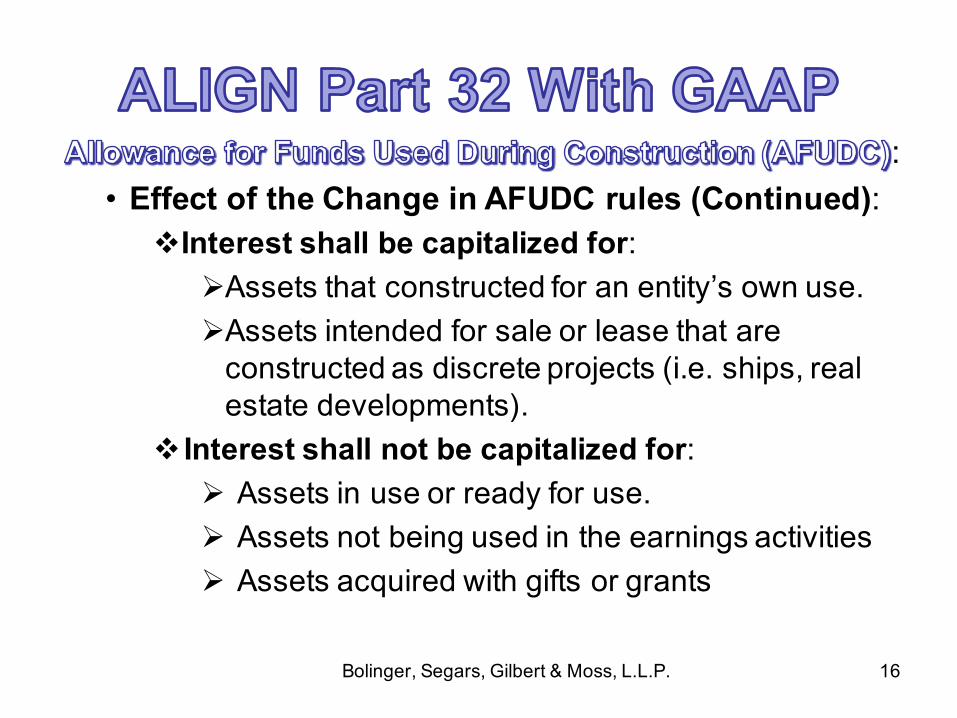

:• Effect of the Change in AFUDC rules (Continued):

vInterest shall be capitalized for:ØAssets that constructed for an entity’s own use.ØAssets intended for sale or lease that are

constructed as discrete projects (i.e. ships, real estate developments).

v Interest shall not be capitalized for:Ø Assets in use or ready for use.Ø Assets not being used in the earnings activitiesØ Assets acquired with gifts or grants

Bolinger, Segars, Gilbert & Moss, L.L.P. 17

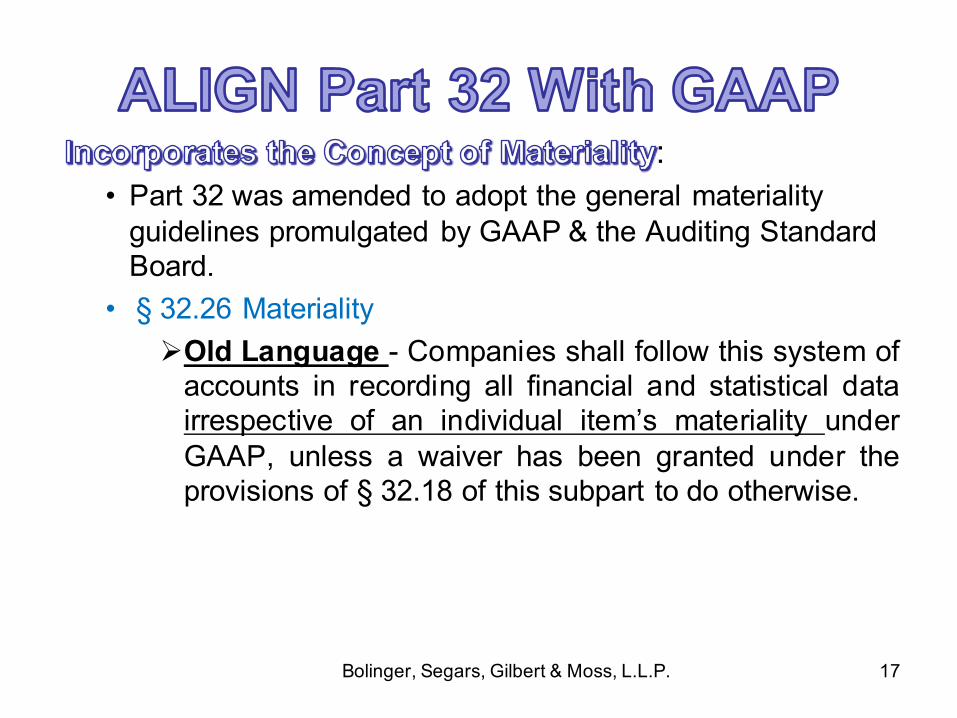

:• Part 32 was amended to adopt the general materiality

guidelines promulgated by GAAP & the Auditing Standard Board.

• § 32.26 MaterialityØOld Language - Companies shall follow this system of

accounts in recording all financial and statistical datairrespective of an individual item’s materiality underGAAP, unless a waiver has been granted under theprovisions of § 32.18 of this subpart to do otherwise.

Bolinger, Segars, Gilbert & Moss, L.L.P. 18

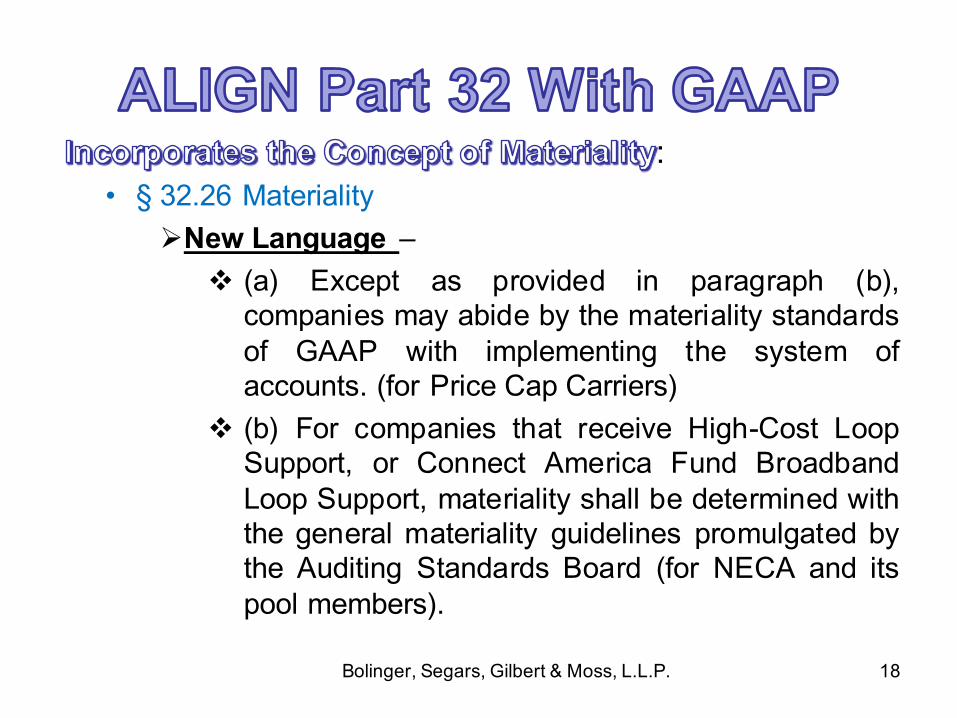

:• § 32.26 Materiality

ØNew Language –v (a) Except as provided in paragraph (b),

companies may abide by the materiality standardsof GAAP with implementing the system ofaccounts. (for Price Cap Carriers)

v (b) For companies that receive High-Cost LoopSupport, or Connect America Fund BroadbandLoop Support, materiality shall be determined withthe general materiality guidelines promulgated bythe Auditing Standards Board (for NECA and itspool members).

Bolinger, Segars, Gilbert & Moss, L.L.P. 19

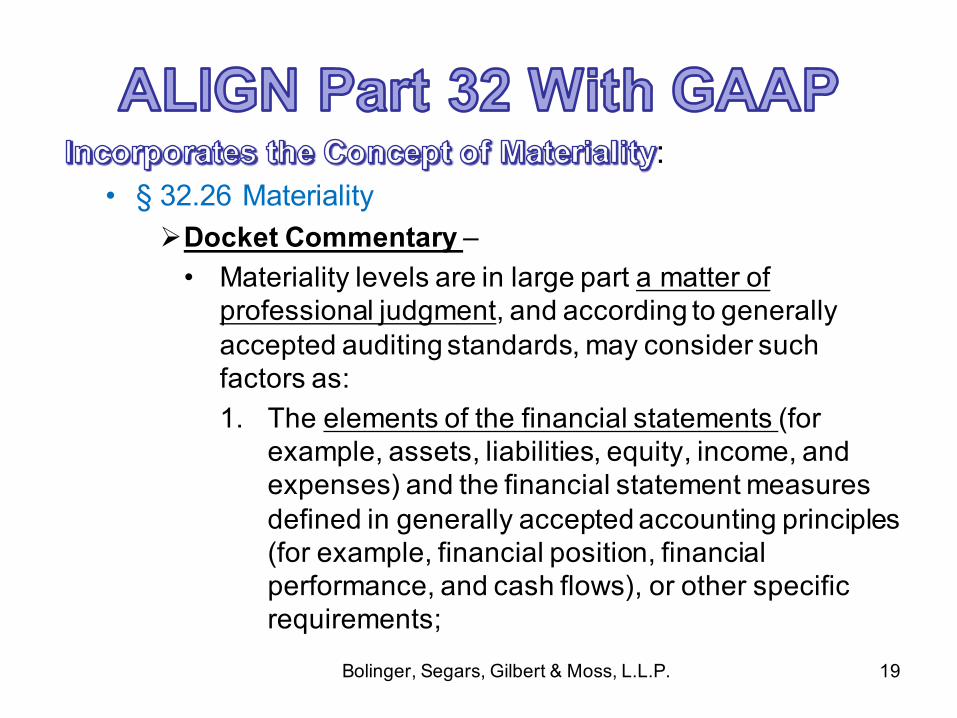

:• § 32.26 Materiality

ØDocket Commentary –• Materiality levels are in large part a matter of

professional judgment, and according to generally accepted auditing standards, may consider such factors as:1. The elements of the financial statements (for

example, assets, liabilities, equity, income, and expenses) and the financial statement measures defined in generally accepted accounting principles (for example, financial position, financial performance, and cash flows), or other specific requirements;

Bolinger, Segars, Gilbert & Moss, L.L.P. 20

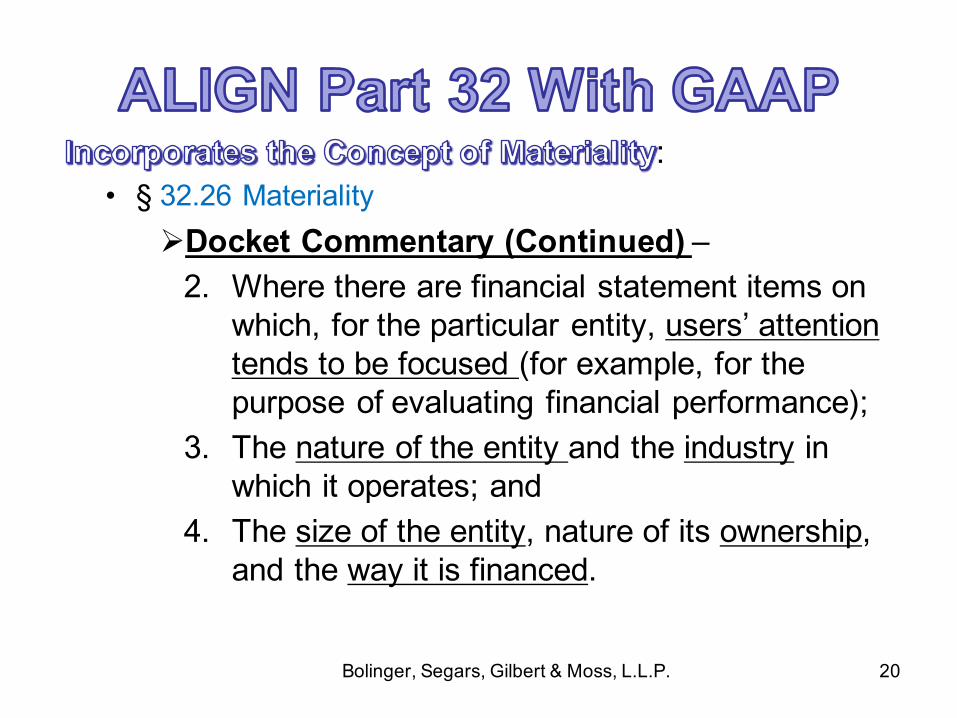

:• § 32.26 Materiality

ØDocket Commentary (Continued) –2. Where there are financial statement items on

which, for the particular entity, users’ attention tends to be focused (for example, for the purpose of evaluating financial performance);

3. The nature of the entity and the industry in which it operates; and

4. The size of the entity, nature of its ownership, and the way it is financed.

Bolinger, Segars, Gilbert & Moss, L.L.P. 21

:• § 32.26 Materiality

ØDocket Commentary (Continued) –• Because independent auditors are required to

undertake assessments of materiality and risk in all audit engagements, their judgment can and should be relied upon when determining materiality levels for purposes of regulatory reporting and review).

Bolinger, Segars, Gilbert & Moss, L.L.P. 22

:• Auditing Standards

ØMateriality is a concept that is judged in light of the expected range of reasonableness of the information.

ØThe misstatements is material if the magnitude misstatement - individually or when aggregated with other misstatements - is such that a reasonable person using the presentation would be influenced by the inclusion or correction of the individual assertion. The relative rather than absolute size of an misstatement may determine whether it is material in a given situation.

Bolinger, Segars, Gilbert & Moss, L.L.P. 23

:• Auditing Standards (Continued) -

ØMateriality as a whole - reduce to an appropriately low level the probability that the aggregate of uncorrected and undetected misstatements exceeds materiality for the financial statements as a whole.

ØPerformance Materiality - refers to the amount or amounts set by the auditor at less than the materiality level or levels for particular classes of transactions, account balances, or disclosures.

Bolinger, Segars, Gilbert & Moss, L.L.P. 24

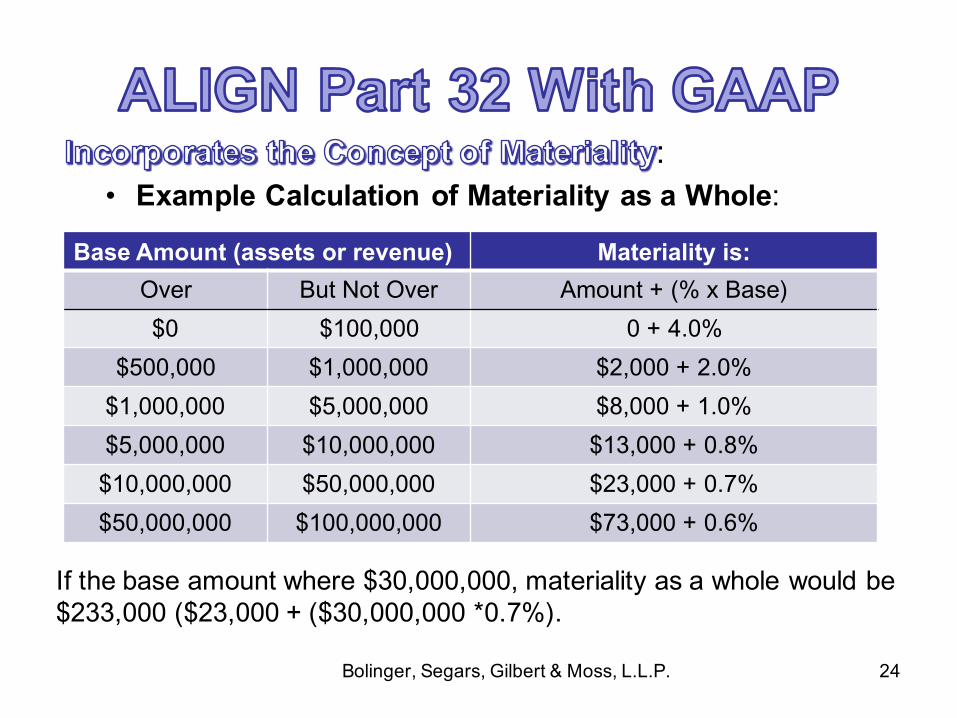

:• Example Calculation of Materiality as a Whole:

Base Amount (assets or revenue) Materiality is:Over But Not Over Amount + (% x Base)

$0 $100,000 0 + 4.0%

$500,000 $1,000,000 $2,000 + 2.0%

$1,000,000 $5,000,000 $8,000 + 1.0%

$5,000,000 $10,000,000 $13,000 + 0.8%

$10,000,000 $50,000,000 $23,000 + 0.7%

$50,000,000 $100,000,000 $73,000 + 0.6%

If the base amount where $30,000,000, materiality as a whole would be $233,000 ($23,000 + ($30,000,000 *0.7%).

Bolinger, Segars, Gilbert & Moss, L.L.P. 25

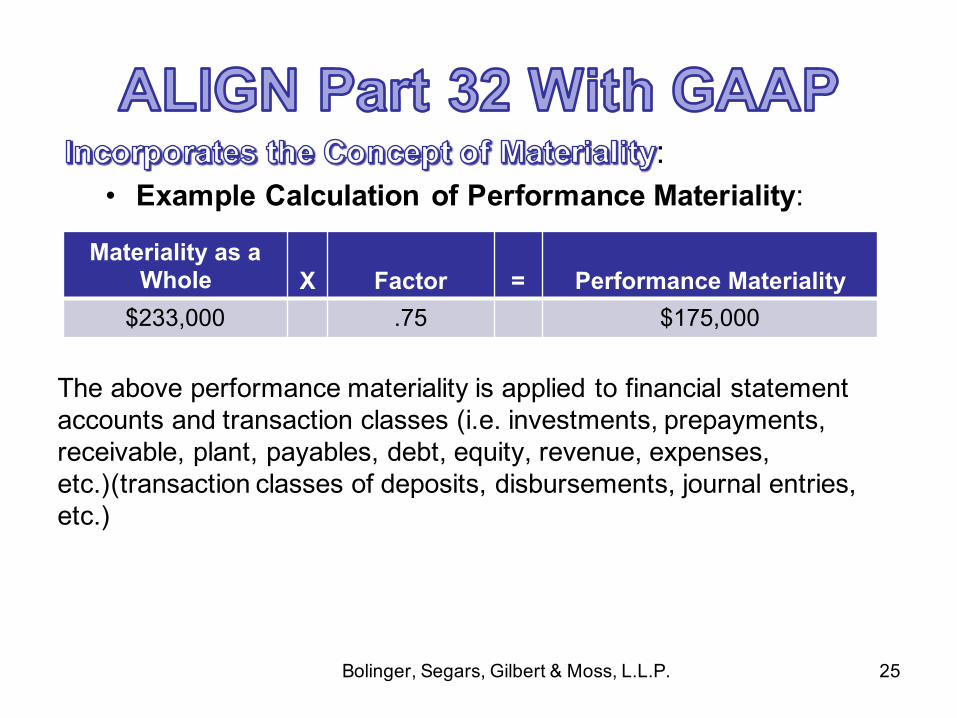

:• Example Calculation of Performance Materiality:

Materiality as a Whole X Factor = Performance Materiality

$233,000 .75 $175,000

The above performance materiality is applied to financial statement accounts and transaction classes (i.e. investments, prepayments, receivable, plant, payables, debt, equity, revenue, expenses, etc.)(transaction classes of deposits, disbursements, journal entries, etc.)

Bolinger, Segars, Gilbert & Moss, L.L.P. 26

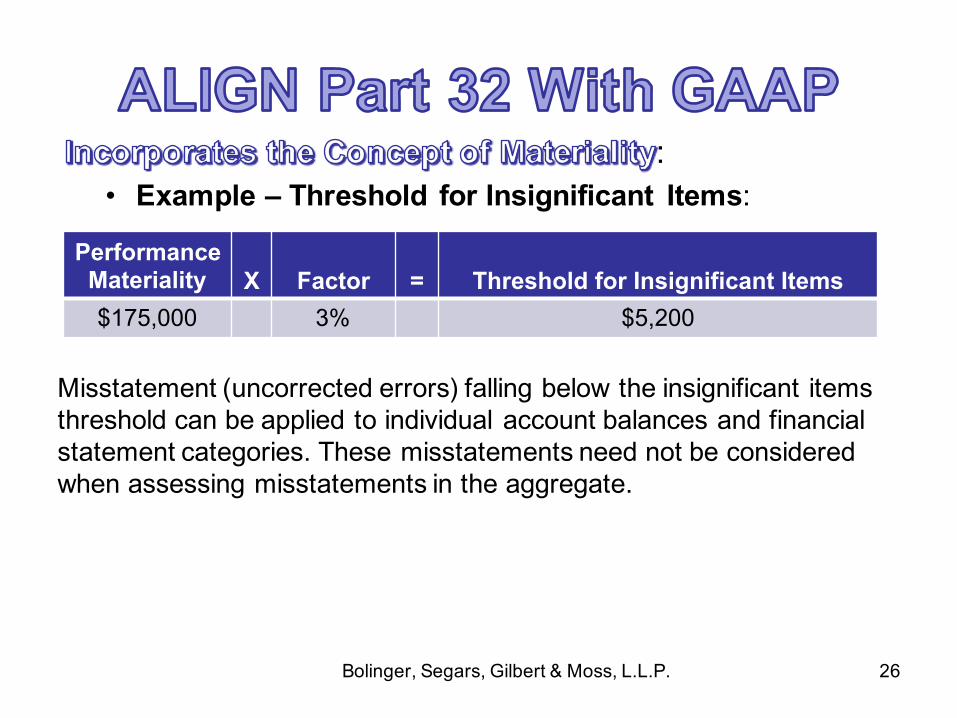

:• Example – Threshold for Insignificant Items:

Performance Materiality X Factor = Threshold for Insignificant Items$175,000 3% $5,200

Misstatement (uncorrected errors) falling below the insignificant items threshold can be applied to individual account balances and financial statement categories. These misstatements need not be considered when assessing misstatements in the aggregate.

Bolinger, Segars, Gilbert & Moss, L.L.P. 27

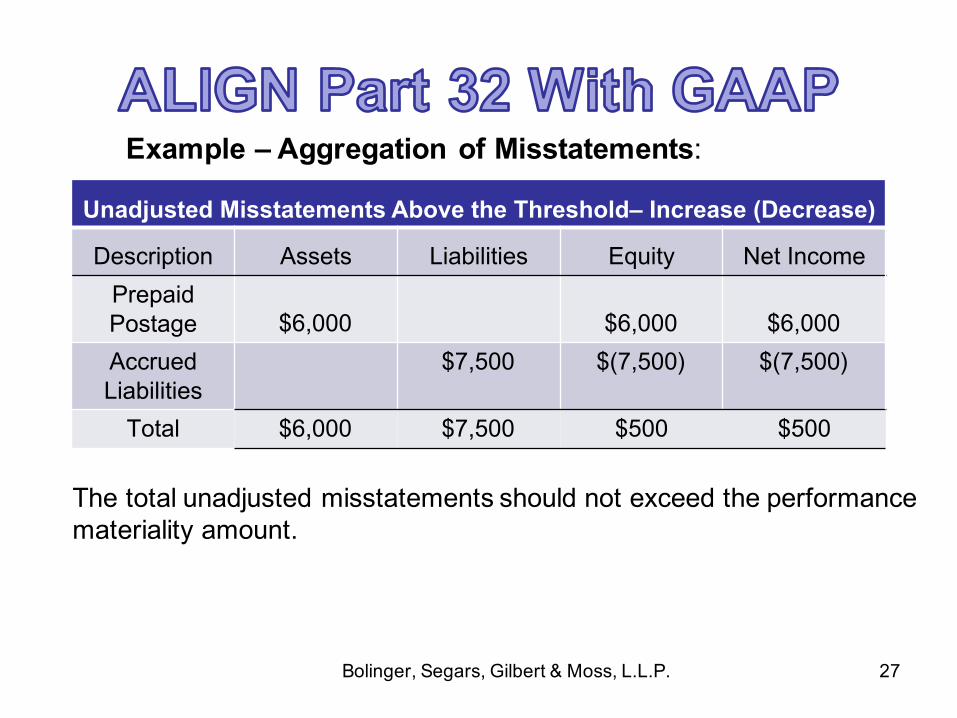

Example – Aggregation of Misstatements:

Unadjusted Misstatements Above the Threshold– Increase (Decrease)

Description Assets Liabilities Equity Net Income

PrepaidPostage $6,000 $6,000 $6,000

Accrued Liabilities

$7,500 $(7,500) $(7,500)

Total $6,000 $7,500 $500 $500

The total unadjusted misstatements should not exceed the performance materiality amount.

Bolinger, Segars, Gilbert & Moss, L.L.P. 28

:• Applications:

v Reduce amount of time spent on accounting for and tracking immaterial prepayments and accruals.

v Discontinue recording AFUDC on minor work orders.v Reduce amount of time and effort on accounting for

items that the cost of doing so does not justify the benefit received and will not result in misleading the user of the financial statements.

v May be used in responding to immaterial findings in USAC compliance audits.

Bolinger, Segars, Gilbert & Moss, L.L.P.29

The information in this presentation is limited to an overview of the topics being presented. Due to the limited time we have together and the complexity of specific facts and circumstances present in actual transactions and their related effects on the proper accounting treatment, the material and opinions expressed today should not be used without full consideration of all relevant authoritative accounting guidance and full analysis of the specific facts and circumstances present in an actual transaction.