Embed Size (px)

DESCRIPTION

Telecommunication Regulatory Authority Investing In Infrastructure Telecom & ICT Opportunity 13 April 2008. ألاقتصاد والأعمال Al- Iktissad Wal-Aamal Conference. www.tra.gov.om. Overview. Market Profile. Market Statistics. Market Forces. Challenges & Solutions. - PowerPoint PPT Presentation

Citation preview

Telecommunication Regulatory AuthorityInvesting In Infrastructure Telecom & ICT Opportunity13 April 2008

أالقتصاد واألعمالAl-Iktissad Wal-Aamal

Conference

www.tra.gov.om

Overview

Market Profile.

Market Statistics.

Market Forces.

Challenges & Solutions.

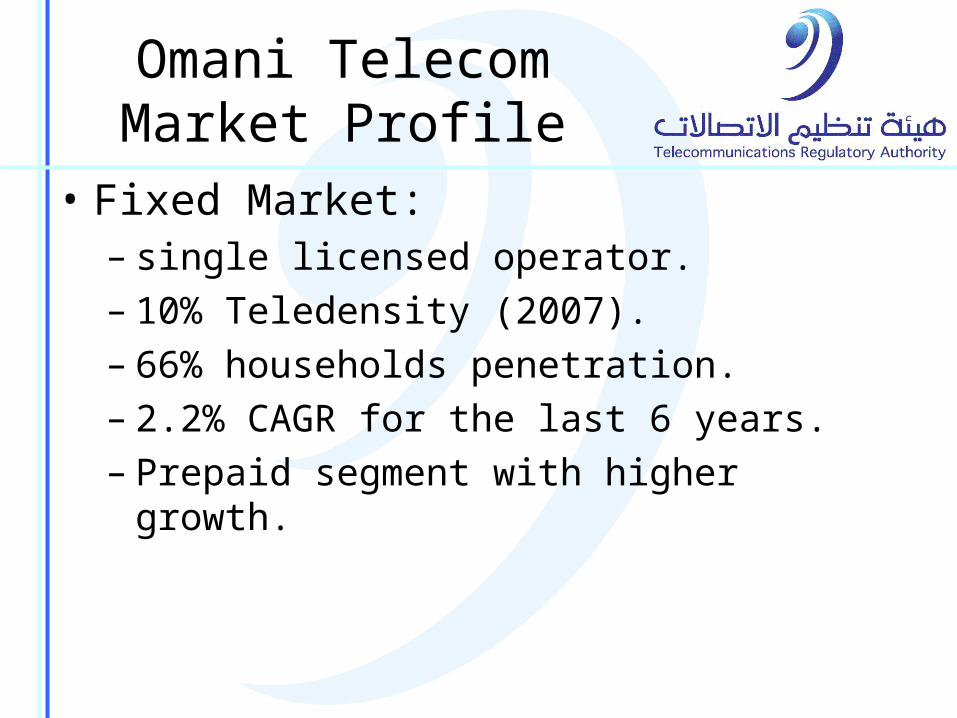

Omani Telecom Market Profile

• Fixed Market:– single licensed operator.– 10% Teledensity (2007).– 66% households penetration.– 2.2% CAGR for the last 6 years.– Prepaid segment with higher growth.

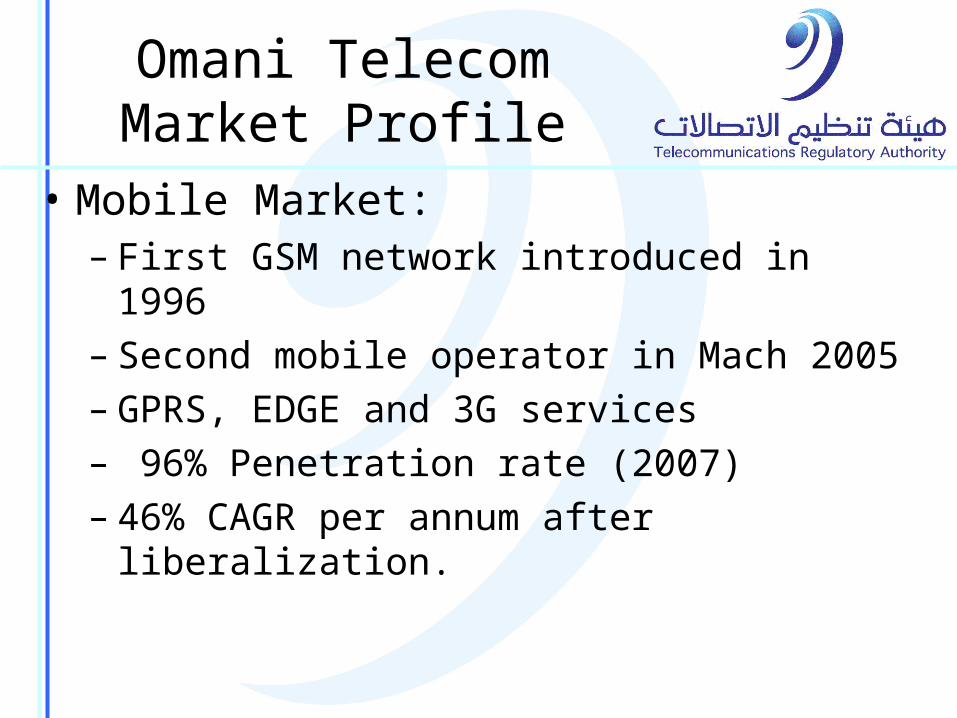

Omani Telecom Market Profile

• Mobile Market:– First GSM network introduced in 1996– Second mobile operator in Mach 2005– GPRS, EDGE and 3G services– 96% Penetration rate (2007)– 46% CAGR per annum after liberalization.

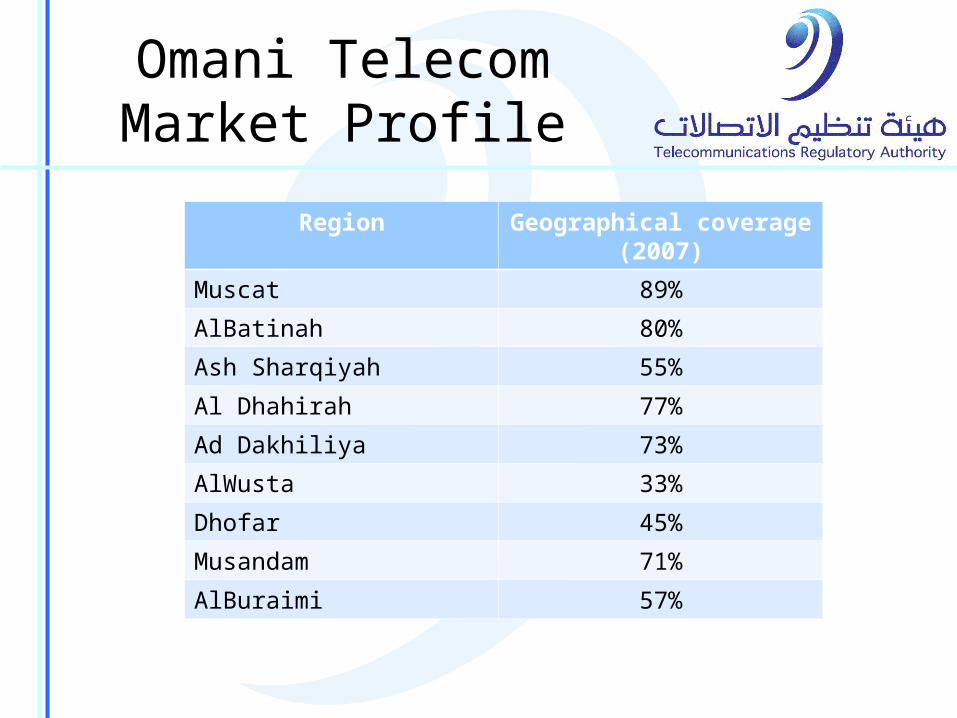

Omani Telecom Market Profile

Region Geographical coverage (2007)

Muscat 89%

AlBatinah 80%

Ash Sharqiyah 55%

Al Dhahirah 77%

Ad Dakhiliya 73%

AlWusta 33%

Dhofar 45%

Musandam 71%

AlBuraimi 57%

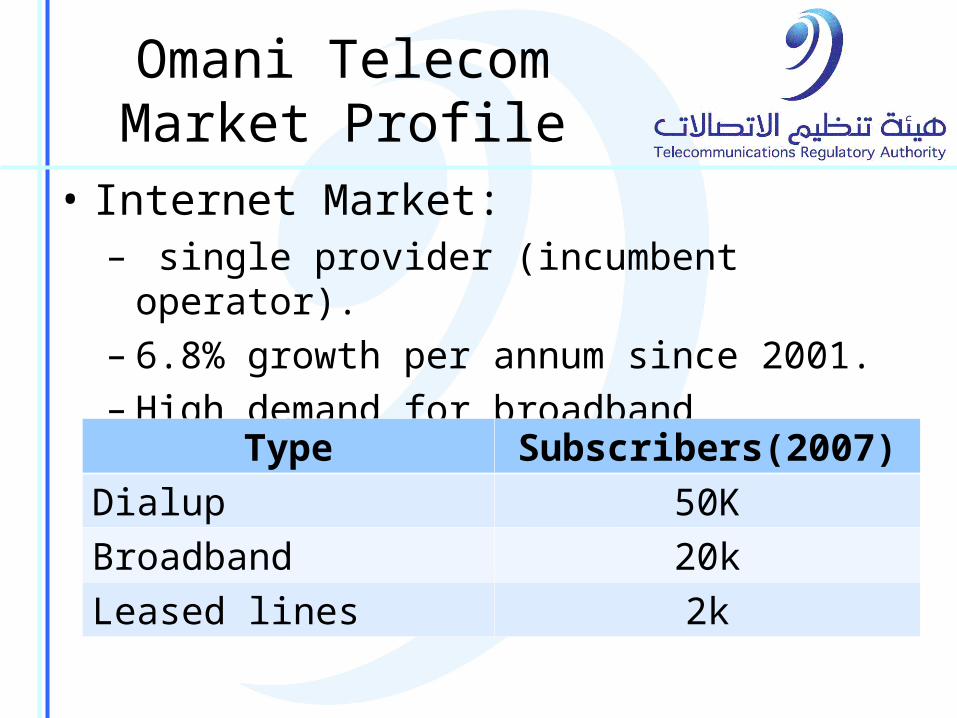

Omani Telecom Market Profile

• Internet Market:– single provider (incumbent operator).– 6.8% growth per annum since 2001.– High demand for broadband services.

Type Subscribers(2007)

Dialup 50K

Broadband 20k

Leased lines 2k

Omani Telecom Market Profile

•Requirement in the legal frame work in the telecom act (Article 38 of the telecom act)

•Government USO Initiative

•Pilot project for the first phase to be auctioned, might not be economic viable and might attract subsidies according to the telecom act article 39.

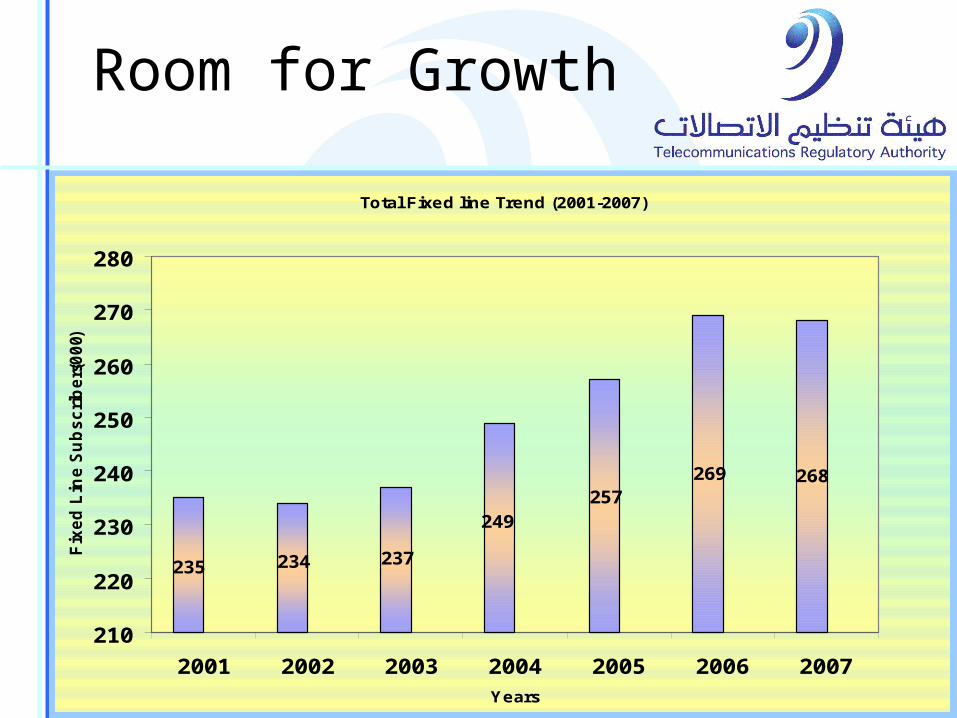

Room for Growth

Total Fixed line Trend (2001-2007)

235 234 237

249257

268269

210

220

230

240

250

260

270

280

2001 2002 2003 2004 2005 2006 2007Years

Fix

ed

Lin

e S

ub

sc

rib

ers

(00

0)

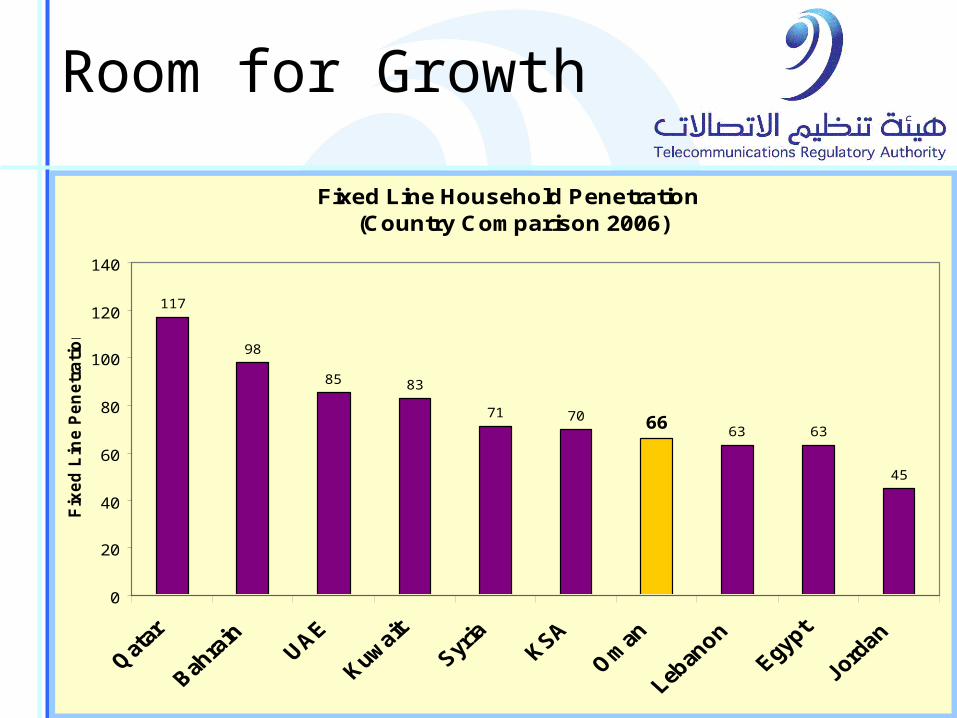

Room for Growth

Fixed Line Household Penetration (Country Comparison 2006)

117

98

85 83

71 7063 63

45

66

0

20

40

60

80

100

120

140

Fix

ed

Lin

e P

en

etr

ati

on

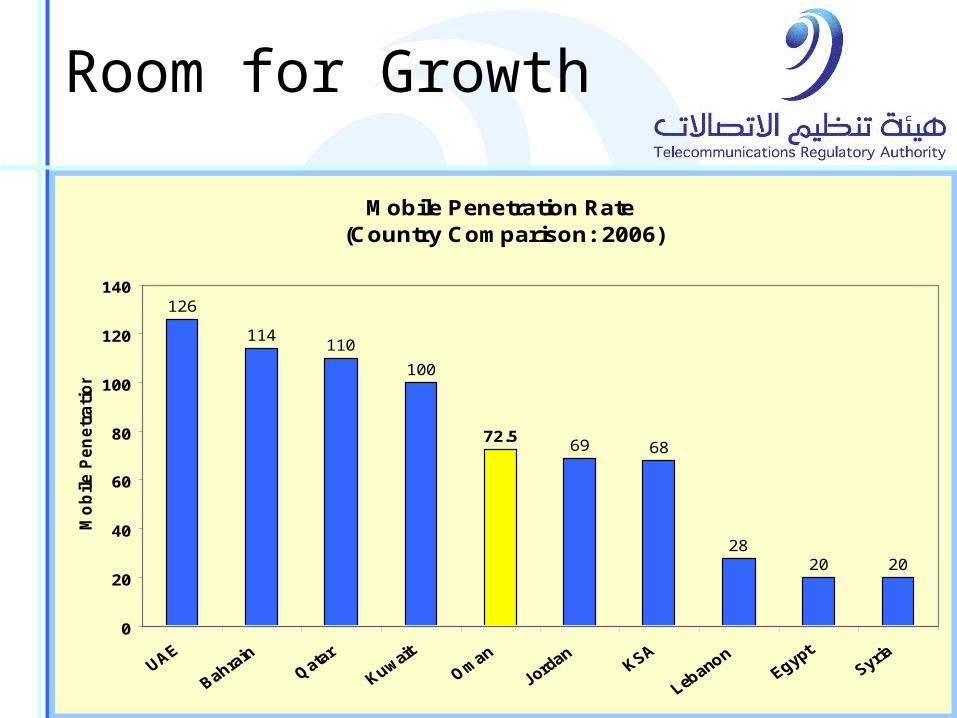

Room for Growth

Mobile Penetration Rate (Country Comparison: 2006)

126

114110

100

69 68

2820 20

72.5

0

20

40

60

80

100

120

140

Mo

bil

e P

en

etr

ati

on

Room for Growth

Internet Subscribers Trend (2002-2007)

4852

48 49

64

70

0

10

20

30

40

50

60

70

80

2002 2003 2004 2005 2006 2007

Years

Inte

rne

t S

ub

sc

rib

ers

, 00

0

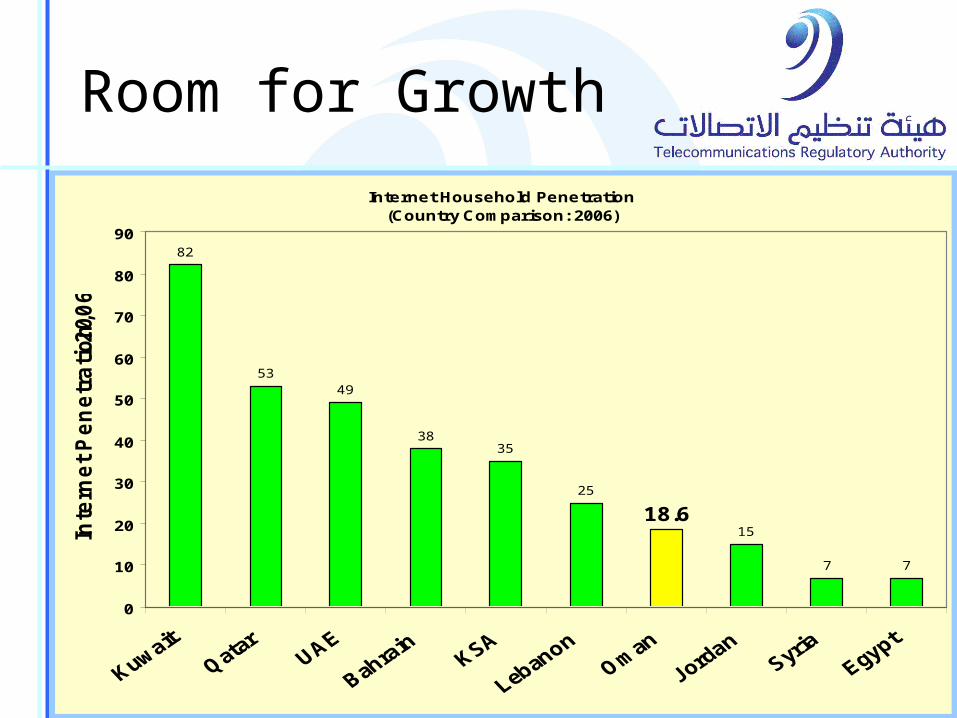

Room for Growth

Internet Household Penetration(Country Comparison: 2006)

82

5349

3835

25

15

7 7

18.6

0

10

20

30

40

50

60

70

80

90

Inte

rne

t P

en

etr

ati

on

, 2

00

6

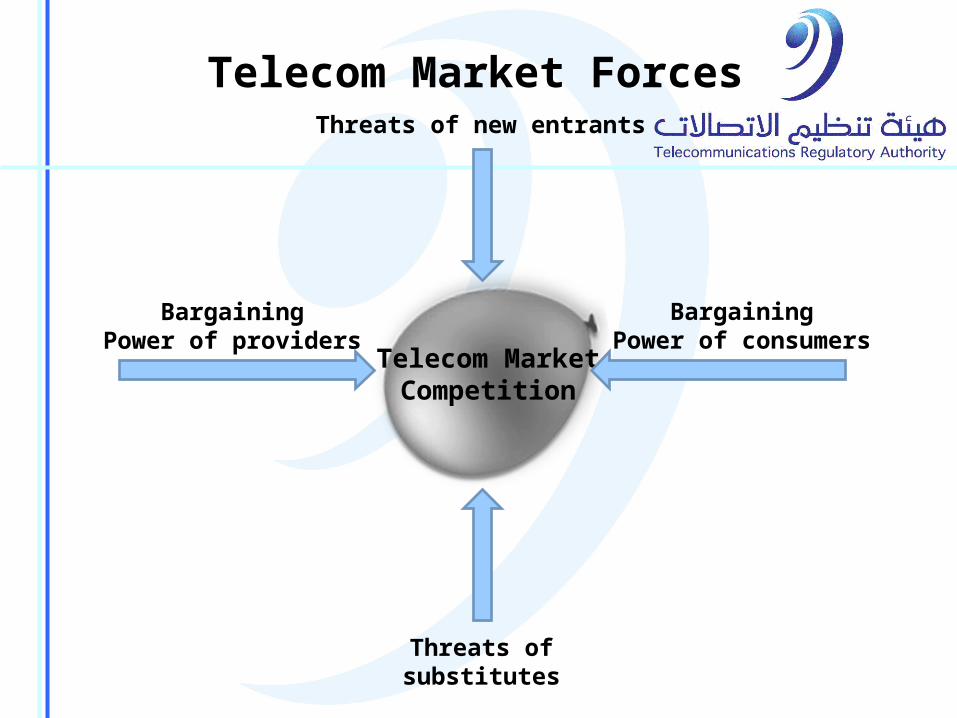

Threats of new entrants

BargainingPower of consumers

Threats ofsubstitutes

BargainingPower of providers

Telecom Market Forces

Telecom MarketCompetition

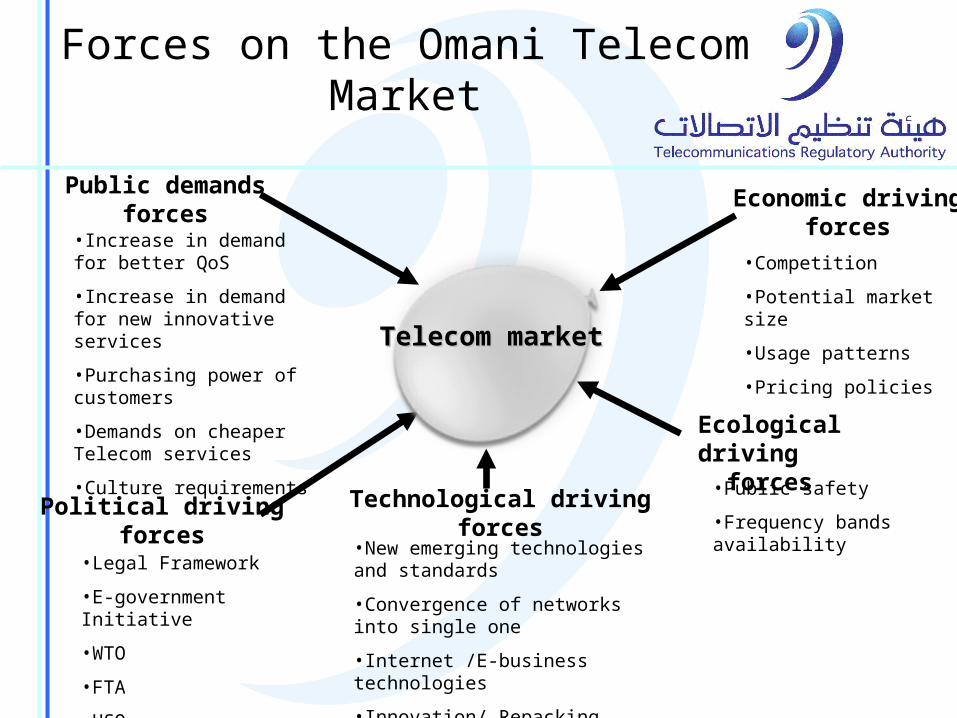

Forces on the Omani Telecom Market

Public demandsforces

Technological drivingforces

Ecological driving forces

Political drivingforces

Economic drivingforces•Increase in demand for better

QoS

•Increase in demand for new innovative services

•Purchasing power of customers

•Demands on cheaper Telecom services

•Culture requirements

•Legal Framework

•E-government Initiative

•WTO

•FTA

•USO

•Competition

•Potential market size

•Usage patterns

•Pricing policies

•Public safety

•Frequency bands availability•New emerging technologies and

standards

•Convergence of networks into single one

•Internet /E-business technologies

•Innovation/ Repacking

Telecom marketTelecom market

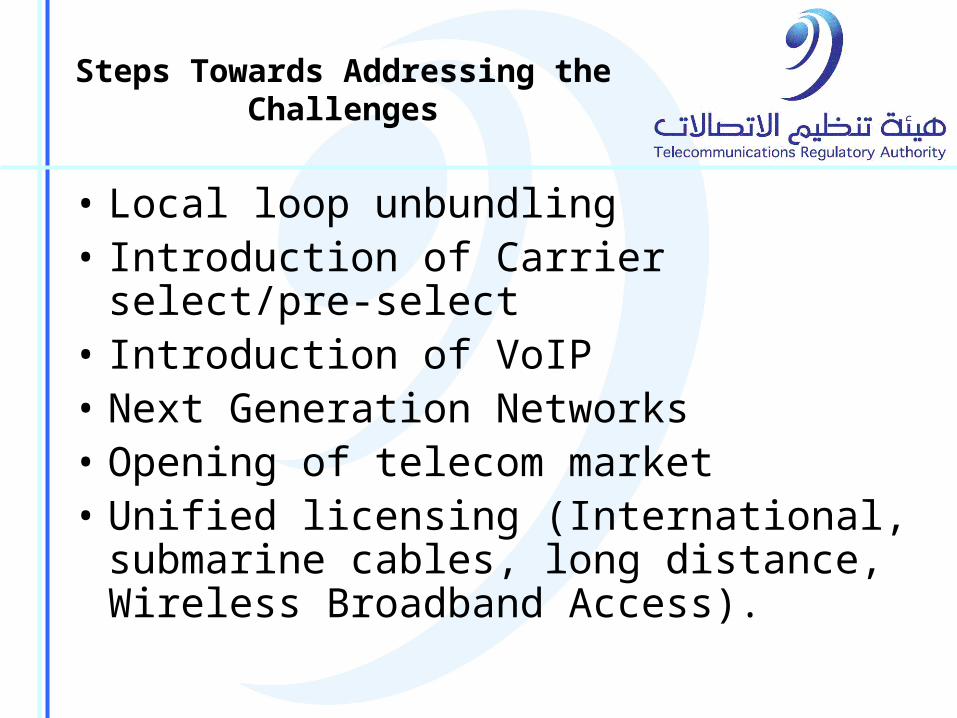

Steps Towards Addressing the Challenges

• Local loop unbundling• Introduction of Carrier select/pre-

select• Introduction of VoIP• Next Generation Networks• Opening of telecom market• Unified licensing (International,

submarine cables, long distance, Wireless Broadband Access).

Challenges to the new entrant

Challenges

Capital requirements

Economies of scale

Product differentiation

Brand performance/customer loyalty

Access to distribution channels

Cost advantages of the Incumbent

Expected retaliation

Legislation/government action

Threats of Substitutes

Challenges

Offer competitive product mix for subscribers to lure from respective competitor

Demonstrate high perceived QoS

Tendency of subscribers to switch to new provider

Consumer disposable income