Embed Size (px)

Citation preview

Tax avoidance and firm value:evidence from China

Xudong Chen, Na Hu and Xue WangThe School of Accounting, Southwestern University of Finance and Economics,

Chengdu, China, and

Xiaofei TangThe School of Business Management,

Southwestern University of Finance and Economics, Chengdu, China

Abstract

Purpose – The purpose of this study is to examine whether corporate tax avoidance behaviorincreases firm value in Chinese context. A large number of studies conduct their designs on theconsumption that tax avoidance represents wealth transfer from government to enterprises andtherefore enhances firm value. This study argues that, contrast to developed countries, tax avoidancedoes not necessarily add value to opaque Chinese firms relative to transparent counterparts due tohigher agency costs.

Design/methodology/approach – Using a large sample of Chinese listed-firms data for the period2001-2009 and fixed effects regression model, this study examines the relation between tax avoidanceand firm value. A series of robustness checks are conducted to alleviate the concern of endogeneity.

Findings – The authors find that tax avoidance behavior increases agency costs and reduces firmvalue. The authors further find that information transparency interacts with corporate tax avoidance,moderating the relation between tax avoidance and firm value. Investors in China react negatively tocorporate tax avoidance behavior, but this negative reaction could be mitigated by informationtransparency. The results are robust to a series of alternative treatments, including varied measures,first-order differential approach and 2SLS.

Originality/value – The results suggest that tax avoidance does not necessarily increase firm value,part of gains are encroached by self-serving managers. Moreover, investors in China downplaythe significance of tax avoidance, although corporate information transparency could soften theirnegative tone.

Keywords Tax avoidance, Firm value, Information transparency

Paper type Research paper

1. IntroductionTax avoidance is an important corporate strategy (Cai and Liu, 2009; Hanlon andHeitzman, 2010). Traditionally, it is believed that corporate tax avoidance representswealth transfer from government to corporations and should enhance firm value.Nevertheless, tax avoidance is not costless. Direct costs include implementation cost,reputation loss and potential punishment, etc. Agency theorists argue that taxavoidance activities are also intertwined with corporate governance issues. Opaque tax

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/2040-8749.htm

The authors appreciate the anonymous reviewers for their constructive comments andsuggestions. The study is supported by the National Natural Science Foundation of China(No. 70972146; No. 71372209), Humanities and Social Science Research Project of Ministry ofEducation (09YJAZH078), Research Fund of Southwestern University of Finance and Economics,and the Fundamental Research Funds for the Central Universities.

Received 13 September 2013Revised 17 November 2013

Accepted 24 December 2013

Nankai Business ReviewInternational

Vol. 5 No. 1, 2014pp. 25-42

q Emerald Group Publishing Limited2040-8749

DOI 10.1108/NBRI-10-2013-0037

Tax avoidanceand firm value

25

planning activities camouflage managerial rent diversion and reduce firm value (Desaiand Dharmapala, 2006; Desai et al., 2007). Thus, whether a firm engages in taxavoidance depends on whether benefits outweigh costs. This paper extends the taxavoidance literature by examining the effect of tax avoidance on firm value in Chineseunique institutional setting. We expect the relation of tax avoidance and firm valuevaries with different levels of corporate governance.

Whether tax avoidance creates firm value is an important but under studiedresearch question. Current empirical evidence on investors’ reactions to tax avoidanceis mixed. The research on information content of tax avoidance suggests that incometax expense is an indicator of corporation profitability. Tax avoidance reduces theinformation content of income tax expense (Hanlon et al., 2005; Ayers et al., 2009). Desaiand Dharmapala (2009) find that the overall effect of corporate tax avoidance activitieson firm value is not significantly different from zero. The effect is positive only forthose firm-years with high levels of institutional ownership. They argue that corporatetax avoidance has two competing effects on firm value. While it constitutes a wealthtransfer from government to shareholders, the agency conflicts between managers andoutside shareholders increase the likelihood of managerial diversion which is a minusof firm value. Hanlon and Slemrod (2009) examine the market reactions to news abouttax shelter involvement. They find limited evidence on cross-sectional variations ofmarket reaction. Wang (2010) finds that investors place a value premium on taxavoidance, but the price premium decreases as corporate opacity increases.Presumably, the inconsistency of research findings may be partly due to differentselection of factors of interest, which have varying effects on current and future cashflows and ultimate firm value, and partly due to differences in sample selections andresearch perspectives. For the former reason, in particular, tax avoidance can imposedirect and indirect changes on current or future cash flows. For instance, directchanges include that tax avoidance can increase cash flows through saving taxwhereas it is also associated with higher agency costs (increasing managementcompany-paid consumption, the building of “personal empire”, etc.). On the other hand,aggressive tax avoidance complicates business transactions, leading to poorerinformation transparency and lower firm value in an indirect way. Overall, the neteffect of tax avoidance on firm value is an empirical question. The emergence ofdominant influencing factor depends on specific business operating environment andinstitutional background.

In this paper, we examine the effect of tax avoidance on firm value in Chineseinstitutional environment because listed companies in China suffer serious agencyproblems due to imperfect corporate governance mechanism. Thus, China is aninteresting setting to test the agency theory explanations of why tax avoidance doesnot necessarily increase firm value.

Recent research suggests that information transparency, defined as the availability offirm-specific information to those users outside publicly-traded firms, can function aseffective corporate governance to mitigate interest conflicts among stakeholders(Armstrong et al., 2010). Prior studies show that information transparency can directlycontribute to economic performance by disciplining corporate insiders in better selectionof investments, more efficient management of assets in place, and reduced expropriationof minority shareholders’ wealth (Bushman and Smith, 2003). Business decision makingrelies on quality and quantity of information, thus information transparency could shift

NBRI5,1

26

current and future cash flows through influencing management decision making.Domestic research suggests that information transparency plays a key role in enhancingthe efficiency of management compensation contract (Wang and Zhang, 2009) andshaping securities analyst forecast characteristics (Fang, 2007). Zhang et al. (2009) findthat there is a U-shaped relation between information transparency and firm marketvalue. In our case, we are wondering if information transparency plays a moderatingrole in the relation of tax avoidance and firm value by alleviating agency severity.

With 20 years of development of Chinese capital market, listed companies havemade great efforts in building information disclosure, assessment and ratingmechanism. In this study, in addition to collecting a large sample of 4,104 firm-yearobservations from 2001 to 2009, we also obtain annual information disclosure ratingindex of listed firms compiled by Shenzhen Stock Exchange (SZSE), trying to examinethe interaction effects of tax avoidance and corporate transparency on firm value asmeasured by Tobin’s q. We find that tax avoidance is negatively and significantlyassociated with firm value. In addition, more tax avoidance activities are related tohigher agency costs, as measured by the ratio of period expenses to sales. Ourempirical results also show that tax avoidance behavior only enhances firm value inmore transparent listed companies. All three hypotheses are supported. Our uniquefinding is inconsistent with conclusions based on US data. We argue that since firmvalue is determined by the discounted value of current and future cash flows.Intuitively, not only can tax avoidance change current or future cash flows directly, butit also can shift cash flows indirectly by influencing management decision making. Theemergence of dominant effect depends on the equilibrium of multiple interacting forces,including institutional arrangement and operating environment.

This paper contributes to the agency literature on corporate tax avoidance inChinese capital market setting. To our best knowledge, it provides the first piece ofevidence regarding shareholder reaction to Chinese listed firms’ tax avoidance andoffers insights into corporate governance. Our results show that, first, agency costs andother non-tax costs are relatively high in China; second, investors in China do not placevalue premium on tax avoidance for these kind of activities could cover managementrent-seeking behavior. Finally, information transparency can offset the negativeimpact of tax avoidance on firm value, that is, tax avoidance is more likely to bring ingains for transparent firms than opaque counterparts.

The rest of the paper proceeds as follows. Section 2 reviews literature and developsempirical hypotheses. Sample selection and research design are presented in Section 3.The empirical model and variable definition are presented in Section 4, and report theempirical results and discussions in Section 5, and robustness checks are discussedin Section 6.

2. Literature review and hypotheses developmentTax avoidance is broadly defined as the reduction in a firm’s explicit tax liabilities(Dyreng et al., 2008). Under this broad definition, tax avoidance represents a continuumof tax planning strategies where perfectly legal activities are at one end and moreaggressive activities would be closer to the other end (Hanlon and Heitzman, 2010).

Different disciplines differ in research perspectives regarding how and why corporateincome tax influences firm value. Finance literature focuses on the impact of debt-as-taxshield on financing decisions (Kemsley and Nissim, 2002; Cooper and Nyborg, 2006).

Tax avoidanceand firm value

27

Economists explore how illegal tax shield influences firm value (Hanlon and Slemrod,2009) and how agency theory can account for tax avoidance on firm value (Desai andDharmapala, 2009). Accounting researchers tend to examine how tax avoidance wouldshape financial statements and value relevance of taxation information (Hanlon et al.,2005; Ayers et al., 2009). So far, there is lack of a comprehensive conceptual framework tointegrate research findings across disciplines. Traditionally, tax avoidance is viewed astax-saving method, and there is no other economic incentive other than saving tax.By contrast, agency theorists argue that tax issues are interwoven with corporategovernance because of widespread agency problems. It is impossible to study taxavoidance in a vacuum. In practice, the real purpose for management to engage in taxavoidance is to complicate and obfuscate the transaction process, which providesmanagers with shelter for self-serving behavior (Desai et al., 2007). Anecdotal evidencealso supports their view. In the 1990s, Enron leveraged structured financing transactionsto evade tax and manipulate earnings, which ultimately led to its failure.

Empirical research on the effect of tax avoidance on firm value is mixed. Desai andDharmapala (2009) find that tax avoidance is likely to increase value for well-governedfirms but it is not the case for poorly-governed firms. But other research findings areinconsistent. Hanlon and Slemrod (2009) examine market reaction to application of taxshield. On average, stock prices are falling at announcement, but the cross-sectionvariation is small and only significant to the retailing industry. Wang (2010) finds thattransparent firms are more aggressive to avoid tax than their opaque counterparts.She also finds investors react positively to tax avoidance but firm value decreases astransparency is decreasing.

How to account for the inconsistency of research findings? Theoretically, it ispresumed that tax avoidance behavior provides corporations with more free cash floweither in the short run or in the long run, which directly increases firm value, and thetax avoidance itself will shift cash flows indirectly by influencing managementdecision making. Practically, the complexity and ambiguity of tax avoidance allowmanagers to pipe the gains into themselves, which would reduce current and futurecash flows. In addition, according to classic agency theory, the free cash flow derivingfrom tax avoidance would lead to the occurrence of company-paid consumption andthe building of “personal empire”, which will shrink future cash flow and decrease firmvalue. Moreover, aggressive tax avoidance behavior is associated with administrativepunishment and subsequent reputation loss, which also decreases future cash flow andfirm value. Other indirect effects of tax avoidance include opaque financial information(Balakrishnan et al., 2011), increasing probabilities of earnings management (Desai,2005; Frank et al., 2009) and rising cost of capital (Lambert et al., 2007). Overall, webelieve that the relation of tax avoidance and firm value is an empirical question.The emergence of dominant effect is dependent on a variety of factors, including theinstitutional arrangement and operating environment, and the ultimate impact is theequilibrium result of all involving forces.

Domestic empirical studies are primarily focused on tax avoidance behaviordeterminants. For example, Wu (2009) examines the effects of state ownership andfavorable tax treatment on corporate tax liabilities. He finds that corporate taxliabilities increase with the proportion of state ownership, and state ownership imposesa heavier tax burden on firms without favorable tax treatment than firms withfavorable tax treatment. Zeng and Zhang (2009) argue that in districts with strong

NBRI5,1

28

taxation enforcement, the agency costs will be lower, and the tunneling and relatedparty transactions will be fewer for majority shareholders, thus they believe taxationenforcement can function as an external corporate governance mechanism. Li and Xu(2013) find that enterprises with more political connections engage in more taxavoidance behavior. Current Chinese literature could not explain why corporate taxavoidance behavior differs, which is the exact void we are trying to fill.

As far as Chinese institutional environment is concerned, Chen and Zhu (2007)conclude that the governance mechanism of Chinese listed firms has obviousdrawbacks, such as government intervention, poor investor legal protection,controlling of major shareholders, loose supervision from state-owned banks and theabsence of external CPA governance. These flaws intensify two kinds of agencyproblems. One is between shareholders and managers, and the “owner absence” causesmore severe agency problems in China; the other is between controlling shareholdersand minority shareholders. The controlling shareholders can dominate personnelarrangements for board of directors and top management, and engage tunnelingthrough related party transaction. Jiang et al. (2010) find that tunneling has tax effectas well, and it leads to firm value loss in the long run. Zeng and Zhang (2009) suggest inareas with strong taxation enforcement, controlling shareholder is less likely toexpropriate assets and conduct related party transactions. They view taxationenforcement as corporate governance mechanism. Using financial data of large andmedium-sized enterprises released by the Bureau of National Statistics, Zheng et al.(2013) examine the corporate governance issues of non-listed firms. Their researchsuggests that the improvement of the external legal environment significantly reducesagency costs for non-listed firms, and taxation enforcement can partially serve ascorporate governance. As for the information content of tax expense, corporate incometax expense can be viewed as an indicator of profitability (Chen and Yuan, 2004) andhas explanatory power of annual stock return (Wang and Dai, 2013).

Given Chinese institutional setting, the agency perspective may better explain therelation between tax avoidance and firm value. H1 and H2 are put forward as follows:

H1. Ceteris paribus, tax avoidance behavior is negatively associated with firmvalue.

H2. Ceteris paribus, tax avoidance behavior increases corporate agency costs.

Based on agency perspective on tax avoidance, firm governance is an importantdeterminant of the valuation of purported corporate tax savings. The direct effect oftax avoidance is to increase the after-tax value of the firm, and these effects arepotentially offset, particularly in poorly governed firms, by increasing opportunitiesfor managerial rent diversion. Thus, the net effect on firm value should be greater forfirms with stronger governance institutions.

The foregoing analysis illustrates that information transparency interacts with taxavoidance. Facing the threat of severe agency problems, information transparencyhelps to mitigate agency conflicts among all stakeholders (Armstrong et al., 2010), toadjust market value by shifting current and future cash flows through changingmanagement decision making (Lambert et al., 2007), and to discipline corporateinsiders in better selection of investments, more efficient management of assets inplace, and less expropriation of minority shareholders’ wealth (Bushman and Smith,2003). On the other hand, transparency makes the business operations more revealing

Tax avoidanceand firm value

29

to government, weakening the capability of avoiding tax. Hence, informationtransparency is a well-suited variable to test the propositions of agency theory.

Transparency and openness are challenging to Chinese companies. Studies based onChina indicate that information transparency can improve the manager compensationcontract efficiency (Wang and Zhang, 2009), and shape securities analysts’ forecastingcharacteristics (Fang, 2007). Zhang et al. (2009) argue that information transparency isa double-edged sword, and there is a U-shaped relationship between informationtransparency and firm market value. We expect that information transparencymoderates the relation of tax avoidance and firm value. H3 is proposed as follows:

H3. Relative to opaque counterparts, tax avoidance increases firm value fortransparent firms.

3. Sample selection and research design(1) Sample selectionOur sample consists of firms that were listed on the SZSE over the period 2001-2009,primarily because the information disclosure rating index of SZSE started from 2001and only SZSE provides such disclosure rating index for firms listed in SZSE.We exclude target firms in the financial industry since they have unique accountingrequirements and regulatory environment. We obtain a sample of 4,104 uniquefirm-year observations. Financial accounting data is obtained from CSMAR database,and tax rate data are sourced from RESSET financial research database.

(2) Measures of tax avoidanceIn accounting literature, there is a lack of consensus on tax avoidance measure.Generally, tax avoidance can be measured from three dimensions, and each measurecaptures different aspects of the construct. The first two are based on book-taxdifferences (BTD). We calculate the Manzon and Plesko (2002) BTD as follows:

Current Income tax ¼ Income tax expenseþ ðEnding deferred income tax liabilities2 Beginning deferred income tax liabilitiesÞ2 ðEnding deferred income tax assets2 Beginning deferred income tax assetsÞ

BTD ¼ Profit before tax2Minority shareholder interests2 ðCurrent Income tax expense=tax rate2 Changes in the amount caused by making up losses for prior periodsÞ

The second way to measure tax avoidance is proposed by Desai and Dharmapala(2006). This measure focuses on BTD that cannot be explained by variations in totalaccruals. We denote this measure by TS as follows:

BTDi;t ¼ b1TAi;t þ mi þ 1i;t

TSi;t ¼ mi þ 1i;t

where:

TA ðTotal accrualsÞ ¼ Total income 2 Cash flows from operating activities

NBRI5,1

30

Both measures are widely adopted in following research, such as Chen et al. (2010). Totalbook-tax gap reflects both temporary and permanent BTD in tax avoidance; however, itmakes no distinction between real operating activities and tax shelter transactions, andthis gap is influenced by corporate earning management as well. To reduce the impact ofearning management, Desai and Dharmapala (2006) construct an empirical measure ofcorporate tax avoidance – the component of the book-tax gap not attributable toaccounting accruals. These two indicators can complement each other.

Recent studies adopt firms’ effective tax rates (ETRs) to measure tax avoidance aswell. However, ETR do not distinguish the difference among tax avoidance,government tax preference, or taxation lobbying activities (Hanlon and Heitzman,2010). In China, local governments adopt various tax preference policies to attractinvestments[1], which lead to lower effective rate than statutory rate. Thus, usingeffective rate to measure tax avoidance in China could be misleading. Chinese listedcompanies disclose actual statutory tax rate (e.g. 24, 15, and 7.5 percent) in the notesto financial statements, so it is more accurate to measure tax avoidance using thedifference between actual statutory tax rate and effective tax rate. However, thisindicator may also be affected by different tax rates applied to parent company andits subsidiaries, especially different consolidation rules for book and tax purposes. Thegreater the difference is, the higher the degree of tax avoidance is. Our ETR valuesare truncated within 0-1, and the actual statutory tax rate is obtained from RESSETdatabase. We denote the difference between ETR and adaptable tax rate by ETR_D asfollows:

ETR ¼ Income tax expense=Pre-tax income; ETR [ ½0; 1�

ETR_D ¼ Actual statutory tax rate2 Effective tax rate

It is worth noting that, rather than focusing on extreme tax-shielding transactions, weaim to examine the general impact of tax avoidance on firm value, and thus adopt abroad definition of tax avoidance which is suitable to our research objectives.

(3) Measures of information transparencyInformation transparency plays a central role in the efficient allocation of resources inthe economy. SZSE started rating the information disclosure level of public firms listedon SZSE since 2001. Tracking the information disclosure behavior of each listed firmin one year, SZSE annually evaluates the information disclosure features in terms ofcompliance, accuracy, timeliness and completeness, and ranks each firm at four levelsclassified as excellent, good, acceptable and unacceptable. Consistent with recentstudies, we employ the annual rating by SZSE as the proxy variable of informationtransparency. Wang and Zhang (2009) and Fang (2007) indicate informationtransparency can improve the manager compensation contract efficiency, and play animportant role in reducing the information asymmetry and lowering agency cost byusing the SZSE information transparency ranking in the Chinese capital market.

4. Empirical model and variable constructionIn the preceding analysis, we raise three questions: would tax avoidance decreasevalues for firms with poor corporate governance? If it is the case, is it because highagency costs exist in poorly-governed firms? Would information transparency provide

Tax avoidanceand firm value

31

a buffer for declining firm value resulted from tax avoidance? To shed light on thesequestions, three models are specified as follows, corresponding to three hypotheses:

qi;t ¼ a0 þ a1TaxAggi;t þ a2PPE i;t þ a3DEBT i;t þ a4ROAi;t þ a5SIZE i;t

þ a6NOLi;t þ a7GROWTH i;t þ a8BETAi;t þ a9YEARi;t þ 1i;tð1Þ

AgencyCosti;t ¼ a0 þ a1TaxAggi;t þ a2PPE i;t þ a3DEBT i;t þ a4ROAi;t

þ a5SIZE i;t þ a6GROWTH i;t þ a7YEARi;t þ 1i;tð2Þ

qi;t ¼ a0 þ a1TaxAggi;t þ a2Transi;t þ a3ðTaxAggi;t *Transi;tÞ þ a4TransSQi;t

þ a5PPE i;t þ a6DEBT i;t þ a7ROAi;t þ a8SIZE i;t þ a9NOLi;t

þ a10GROWTH i;t þ a11BETAi;t þ a12YEARi;t þ 1i;t

ð3Þ

Following Zhang et al. (2009), we add a quadratic term of Trans in model (3) given the“U-shape” relation of information transparency and firm value for Chinese listedfirms. In all three models, where a0 refers to constant interception, a1-a12 arecoefficients, 1 represents residual error.

Dependent variablesTobin’s q (q) is used to represent firm value. Since there are two classes of shares inChinese listed companies, tradable shares and non-tradable shares, we adopt anaverage discount factor 0.45 for non-tradable shares according to Yang et al. (2008) anddefine Tobin’s q as follows:

q ¼ ðMarket value of tradable sharesþMarket value of non-tradable shares*0:45þ Book value of liabilitiesÞ=Total assets:

Following Zheng et al. (2013), we use two ratio variables to measure agency costs: theratio of sales to total assets (STA), and the ratio of period expenses to sales (OETS):

STA ¼ Sales=Total assets

OETS ¼ ðSelling expense þ General administrative expenseþ Financing expenseÞ=Sales

Independent variablesTaxAgg is the tax avoidance variable, and we use three ways to measure taxavoidance: BTD, TS and ETR_D as defined above. We expect a negative coefficient a1.

Trans is the proxy viable for corporate transparency. This ordered variable is codedas 4, 3, 2 and 1 for excellent, good, acceptable and unacceptable rating based on SZSEassessment of corporate information disclosure level.

TaxAgg*Trans is the interaction term of tax aggressiveness and transparency toexamine the moderating role of accounting information quality on tax avoidance andfirm value, and we expect a positive coefficient a3 for this interaction.

NBRI5,1

32

Control variablesWe include firm size (SIZE), return on assets (ROA), fixed assets (PPE), capitalstructure (DEBT), loss carryforwards (NOL), sales growth rate (GROWTH), and risk(BETA) in the regression model as control variables because prior studies show thatthey are related to firm value (Desai and Dharmapala, 2009). Year dummy is alsoincluded to control for year fixed effects. All variables (not including TS, Trans,BETA) are winsorized at the 1 and 99 percentiles. The control variables are defined as:

PPE ¼ (Net PP&E þ Net investment in real estate)/Beginning total assets.

DEBT ¼ (Short term loans þ Notes payable þ Long termliabilities[2])/Beginning total assets.

ROA ¼ Total profits/Beginning total assets.

SIZE ¼ LN (Total assets).

GROWTH ¼ (Current operating revenue 2 Prior operating revenue)/Beginningoperating revenue.

NOL ¼ Losses carryforwards/Beginning total assets.

BETA ¼ Stock market risk, sourced from CSMAR database.

YEAR ¼ Year dummy variable.

Estimation methodWe expect that the level of tax avoidance varies across years and sectors of theeconomy. To capture these effects, we adjust the standard errors for heteroskedasticityand time-series correlation by using robust standard errors clustered at the firm level(Petersen, 2009). We also use regression with Driscoll-Kraay standard errors, and weuse fixed effect model following the Hausman test result (x 2 ¼ 153). Most corporatefinance studies suffer endogeneity issues (Roberts and Whited, 2011), thus fixed effectmodel is employed to alleviate the concern of endogeneity.

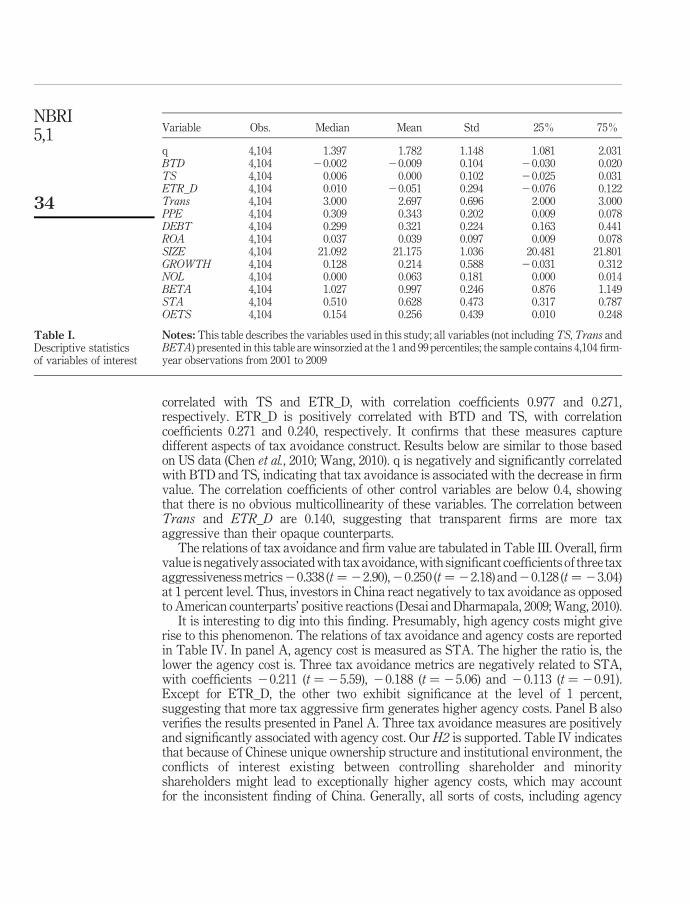

5. Empirical results and discussionsThe descriptive statistics of main variables of interest are reported in Table I. Themean and median of Tobin’s q are 1.782 and 1.397, respectively, whereas the mean andmedian of BTD are 20.009 and 20.002, respectively. These numbers indicate that inChinese institutional environment the accumulated BTD are negative as opposed topositive BTD based on US data. The result is similar to Tang and Firth (2011),suggesting that tax law is more conservative on expense recognition than accountingprinciples in China. The mean and median values for TS are 0 and 0.006, respectively.As for the residual error of fixed effect estimation, it cannot be viewed as the taxavoidance amounts during various years, and it properly reflects the changes oftax avoidance activities related to time variables (Desai and Dharmapala, 2006). Themean and median values of ETR_D are 20.051 and 0.01, while the mean and medianvalues of Trans are 2.697 and 3, indicating that more than half sample firms achieve“good” information disclosure rating.

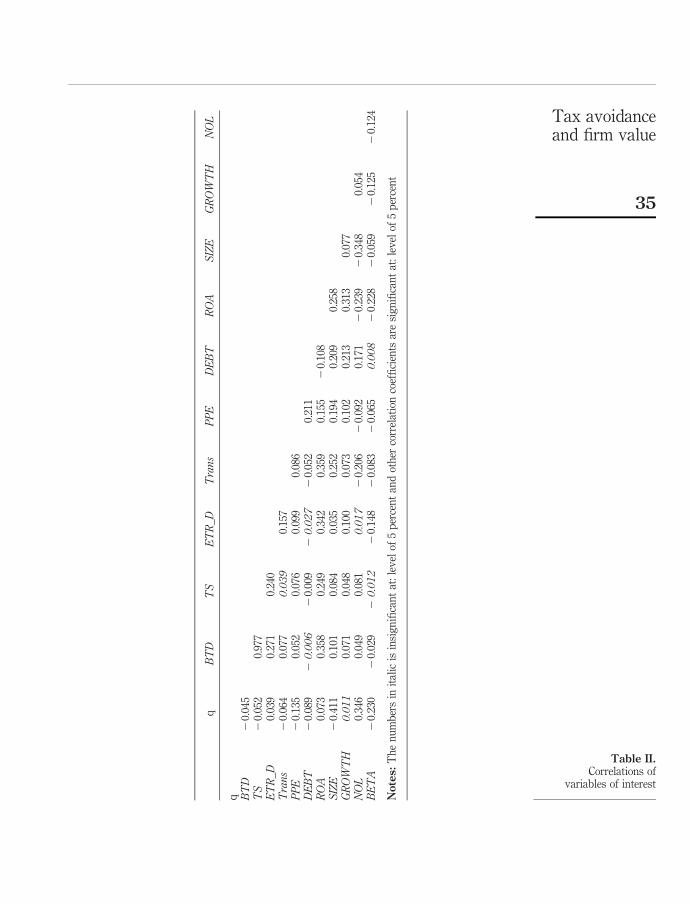

Table II presents correlations among the main variables of interest. Correlationsamong three tax avoidance measures are significant at the 0.05 level. BTD is positively

Tax avoidanceand firm value

33

correlated with TS and ETR_D, with correlation coefficients 0.977 and 0.271,respectively. ETR_D is positively correlated with BTD and TS, with correlationcoefficients 0.271 and 0.240, respectively. It confirms that these measures capturedifferent aspects of tax avoidance construct. Results below are similar to those basedon US data (Chen et al., 2010; Wang, 2010). q is negatively and significantly correlatedwith BTD and TS, indicating that tax avoidance is associated with the decrease in firmvalue. The correlation coefficients of other control variables are below 0.4, showingthat there is no obvious multicollinearity of these variables. The correlation betweenTrans and ETR_D are 0.140, suggesting that transparent firms are more taxaggressive than their opaque counterparts.

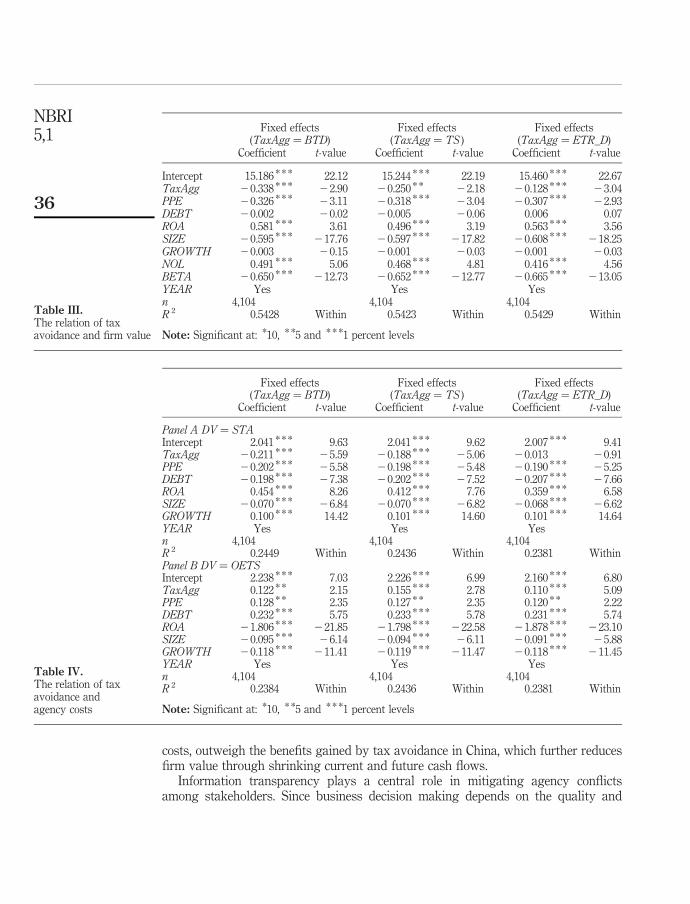

The relations of tax avoidance and firm value are tabulated in Table III. Overall, firmvalue is negatively associated with tax avoidance, with significant coefficients of three taxaggressiveness metrics20.338 (t ¼ 22.90),20.250 (t ¼ 22.18) and20.128 (t ¼ 23.04)at 1 percent level. Thus, investors in China react negatively to tax avoidance as opposedto American counterparts’ positive reactions (Desai and Dharmapala, 2009; Wang, 2010).

It is interesting to dig into this finding. Presumably, high agency costs might giverise to this phenomenon. The relations of tax avoidance and agency costs are reportedin Table IV. In panel A, agency cost is measured as STA. The higher the ratio is, thelower the agency cost is. Three tax avoidance metrics are negatively related to STA,with coefficients 20.211 (t ¼ 25.59), 20.188 (t ¼ 25.06) and 20.113 (t ¼ 20.91).Except for ETR_D, the other two exhibit significance at the level of 1 percent,suggesting that more tax aggressive firm generates higher agency costs. Panel B alsoverifies the results presented in Panel A. Three tax avoidance measures are positivelyand significantly associated with agency cost. Our H2 is supported. Table IV indicatesthat because of Chinese unique ownership structure and institutional environment, theconflicts of interest existing between controlling shareholder and minorityshareholders might lead to exceptionally higher agency costs, which may accountfor the inconsistent finding of China. Generally, all sorts of costs, including agency

Variable Obs. Median Mean Std 25% 75%

q 4,104 1.397 1.782 1.148 1.081 2.031BTD 4,104 20.002 20.009 0.104 20.030 0.020TS 4,104 0.006 0.000 0.102 20.025 0.031ETR_D 4,104 0.010 20.051 0.294 20.076 0.122Trans 4,104 3.000 2.697 0.696 2.000 3.000PPE 4,104 0.309 0.343 0.202 0.009 0.078DEBT 4,104 0.299 0.321 0.224 0.163 0.441ROA 4,104 0.037 0.039 0.097 0.009 0.078SIZE 4,104 21.092 21.175 1.036 20.481 21.801GROWTH 4,104 0.128 0.214 0.588 20.031 0.312NOL 4,104 0.000 0.063 0.181 0.000 0.014BETA 4,104 1.027 0.997 0.246 0.876 1.149STA 4,104 0.510 0.628 0.473 0.317 0.787OETS 4,104 0.154 0.256 0.439 0.010 0.248

Notes: This table describes the variables used in this study; all variables (not including TS, Trans andBETA) presented in this table are winsorzied at the 1 and 99 percentiles; the sample contains 4,104 firm-year observations from 2001 to 2009

Table I.Descriptive statisticsof variables of interest

NBRI5,1

34

qBTD

TS

ETR_D

Trans

PPE

DEBT

ROA

SIZE

GROWTH

NOL

q BTD

20.

045

TS

20.

052

0.97

7ETR_D

0.03

90.

271

0.24

0Trans

20.

064

0.07

70.039

0.15

7PPE

20.

135

0.05

20.

076

0.09

90.

086

DEBT

20.

089

20.006

20.

009

20.027

20.

052

0.21

1ROA

0.07

30.

358

0.24

90.

342

0.35

90.

155

20.

108

SIZE

20.

411

0.10

10.

084

0.03

50.

252

0.19

40.

209

0.25

8GROWTH

0.011

0.07

10.

048

0.10

00.

073

0.10

20.

213

0.31

30.

077

NOL

0.34

60.

049

0.08

10.017

20.

206

20.

092

0.17

12

0.23

92

0.34

80.

054

BETA

20.

230

20.

029

20.012

20.

148

20.

083

20.

065

0.008

20.

228

20.

059

20.

125

20.

124

Notes:

Th

en

um

ber

sin

ital

icis

insi

gn

ifica

nt

at:

lev

elof

5p

erce

nt

and

oth

erco

rrel

atio

nco

effi

cien

tsar

esi

gn

ifica

nt

at:

lev

elof

5p

erce

nt

Table II.Correlations of

variables of interest

Tax avoidanceand firm value

35

costs, outweigh the benefits gained by tax avoidance in China, which further reducesfirm value through shrinking current and future cash flows.

Information transparency plays a central role in mitigating agency conflictsamong stakeholders. Since business decision making depends on the quality and

Fixed effects(TaxAgg ¼ BTD)

Fixed effects(TaxAgg ¼ TS )

Fixed effects(TaxAgg ¼ ETR_D)

Coefficient t-value Coefficient t-value Coefficient t-value

Intercept 15.186 * * * 22.12 15.244 * * * 22.19 15.460 * * * 22.67TaxAgg 20.338 * * * 22.90 20.250 * * 22.18 20.128 * * * 23.04PPE 20.326 * * * 23.11 20.318 * * * 23.04 20.307 * * * 22.93DEBT 20.002 20.02 20.005 20.06 0.006 0.07ROA 0.581 * * * 3.61 0.496 * * * 3.19 0.563 * * * 3.56SIZE 20.595 * * * 217.76 20.597 * * * 217.82 20.608 * * * 218.25GROWTH 20.003 20.15 20.001 20.03 20.001 20.03NOL 0.491 * * * 5.06 0.468 * * * 4.81 0.416 * * * 4.56BETA 20.650 * * * 212.73 20.652 * * * 212.77 20.665 * * * 213.05YEAR Yes Yes Yesn 4,104 4,104 4,104R 2 0.5428 Within 0.5423 Within 0.5429 Within

Note: Significant at: *10, * *5 and * * *1 percent levels

Table III.The relation of taxavoidance and firm value

Fixed effects(TaxAgg ¼ BTD)

Fixed effects(TaxAgg ¼ TS )

Fixed effects(TaxAgg ¼ ETR_D)

Coefficient t-value Coefficient t-value Coefficient t-value

Panel A DV ¼ STAIntercept 2.041 * * * 9.63 2.041 * * * 9.62 2.007 * * * 9.41TaxAgg 20.211 * * * 25.59 20.188 * * * 25.06 20.013 20.91PPE 20.202 * * * 25.58 20.198 * * * 25.48 20.190 * * * 25.25DEBT 20.198 * * * 27.38 20.202 * * * 27.52 20.207 * * * 27.66ROA 0.454 * * * 8.26 0.412 * * * 7.76 0.359 * * * 6.58SIZE 20.070 * * * 26.84 20.070 * * * 26.82 20.068 * * * 26.62GROWTH 0.100 * * * 14.42 0.101 * * * 14.60 0.101 * * * 14.64YEAR Yes Yes Yesn 4,104 4,104 4,104R 2 0.2449 Within 0.2436 Within 0.2381 WithinPanel B DV ¼ OETSIntercept 2.238 * * * 7.03 2.226 * * * 6.99 2.160 * * * 6.80TaxAgg 0.122 * * 2.15 0.155 * * * 2.78 0.110 * * * 5.09PPE 0.128 * * 2.35 0.127 * * 2.35 0.120 * * 2.22DEBT 0.232 * * * 5.75 0.233 * * * 5.78 0.231 * * * 5.74ROA 21.806 * * * 221.85 21.798 * * * 222.58 21.878 * * * 223.10SIZE 20.095 * * * 26.14 20.094 * * * 26.11 20.091 * * * 25.88GROWTH 20.118 * * * 211.41 20.119 * * * 211.47 20.118 * * * 211.45YEAR Yes Yes Yesn 4,104 4,104 4,104R 2 0.2384 Within 0.2436 Within 0.2381 Within

Note: Significant at: *10, * *5 and * * *1 percent levels

Table IV.The relation of taxavoidance andagency costs

NBRI5,1

36

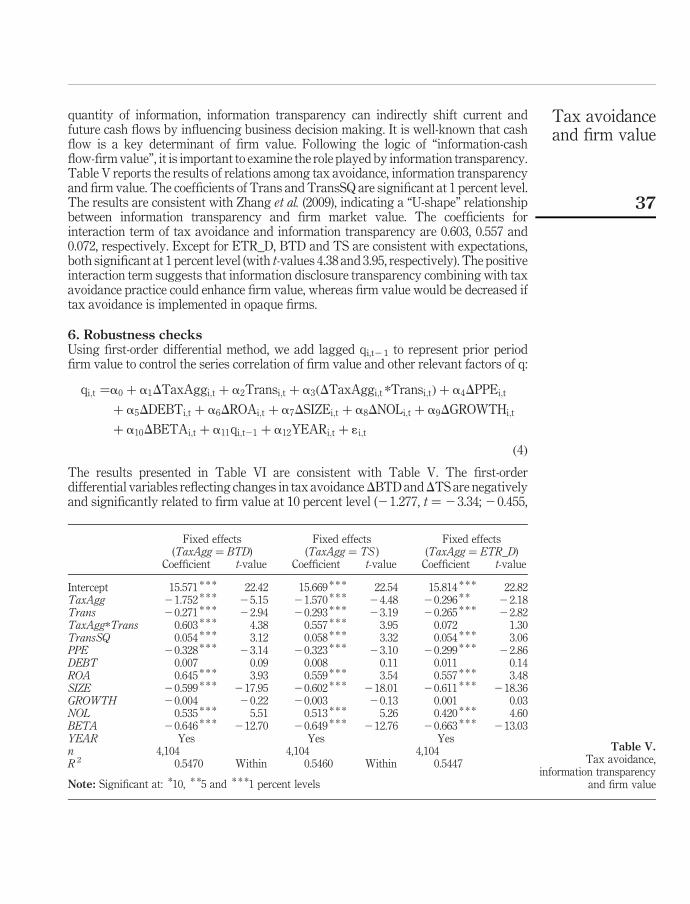

quantity of information, information transparency can indirectly shift current andfuture cash flows by influencing business decision making. It is well-known that cashflow is a key determinant of firm value. Following the logic of “information-cashflow-firm value”, it is important to examine the role played by information transparency.Table V reports the results of relations among tax avoidance, information transparencyand firm value. The coefficients of Trans and TransSQ are significant at 1 percent level.The results are consistent with Zhang et al. (2009), indicating a “U-shape” relationshipbetween information transparency and firm market value. The coefficients forinteraction term of tax avoidance and information transparency are 0.603, 0.557 and0.072, respectively. Except for ETR_D, BTD and TS are consistent with expectations,both significant at 1 percent level (with t-values 4.38 and 3.95, respectively). The positiveinteraction term suggests that information disclosure transparency combining with taxavoidance practice could enhance firm value, whereas firm value would be decreased iftax avoidance is implemented in opaque firms.

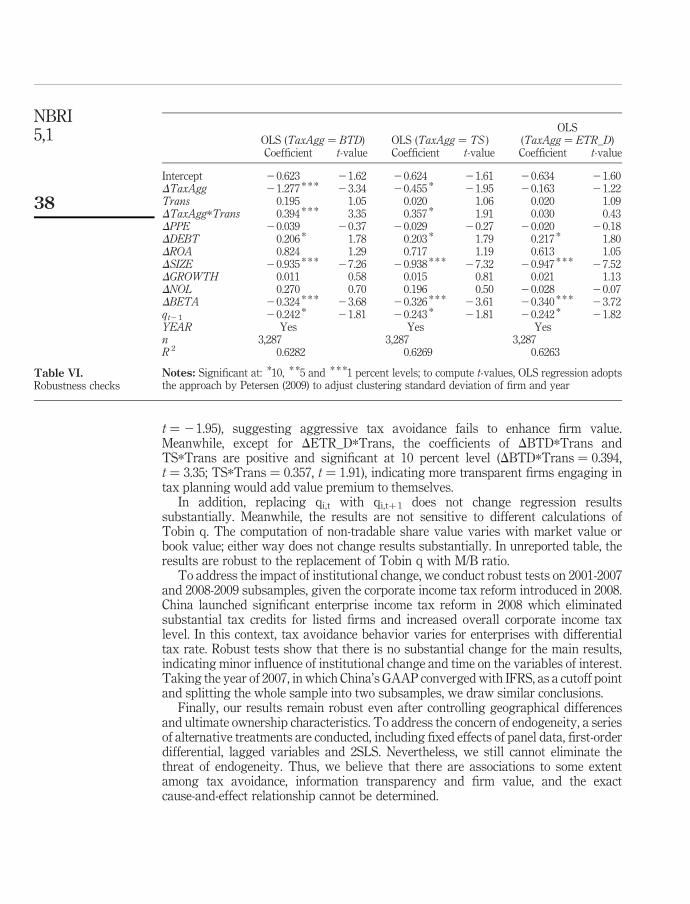

6. Robustness checksUsing first-order differential method, we add lagged qi,t21 to represent prior periodfirm value to control the series correlation of firm value and other relevant factors of q:

qi;t ¼a0 þ a1DTaxAggi;t þ a2Transi;t þ a3ðDTaxAggi;t *Transi;tÞ þ a4DPPEi;t

þ a5DDEBTi;t þ a6DROAi;t þ a7DSIZEi;t þ a8DNOLi;t þ a9DGROWTHi;t

þ a10DBETAi;t þ a11qi;t21 þ a12YEARi;t þ 1i;t

ð4Þ

The results presented in Table VI are consistent with Table V. The first-orderdifferential variables reflecting changes in tax avoidanceDBTD andDTS are negativelyand significantly related to firm value at 10 percent level (21.277, t ¼ 23.34; 20.455,

Fixed effects(TaxAgg ¼ BTD)

Fixed effects(TaxAgg ¼ TS )

Fixed effects(TaxAgg ¼ ETR_D)

Coefficient t-value Coefficient t-value Coefficient t-value

Intercept 15.571 * * * 22.42 15.669 * * * 22.54 15.814 * * * 22.82TaxAgg 21.752 * * * 25.15 21.570 * * * 24.48 20.296 * * 22.18Trans 20.271 * * * 22.94 20.293 * * * 23.19 20.265 * * * 22.82TaxAgg*Trans 0.603 * * * 4.38 0.557 * * * 3.95 0.072 1.30TransSQ 0.054 * * * 3.12 0.058 * * * 3.32 0.054 * * * 3.06PPE 20.328 * * * 23.14 20.323 * * * 23.10 20.299 * * * 22.86DEBT 0.007 0.09 0.008 0.11 0.011 0.14ROA 0.645 * * * 3.93 0.559 * * * 3.54 0.557 * * * 3.48SIZE 20.599 * * * 217.95 20.602 * * * 218.01 20.611 * * * 218.36GROWTH 20.004 20.22 20.003 20.13 0.001 0.03NOL 0.535 * * * 5.51 0.513 * * * 5.26 0.420 * * * 4.60BETA 20.646 * * * 212.70 20.649 * * * 212.76 20.663 * * * 213.03YEAR Yes Yes Yesn 4,104 4,104 4,104R 2 0.5470 Within 0.5460 Within 0.5447

Note: Significant at: *10, * *5 and * * *1 percent levels

Table V.Tax avoidance,

information transparencyand firm value

Tax avoidanceand firm value

37

t ¼ 21.95), suggesting aggressive tax avoidance fails to enhance firm value.Meanwhile, except for DETR_D*Trans, the coefficients of DBTD*Trans andTS*Trans are positive and significant at 10 percent level (DBTD*Trans ¼ 0.394,t ¼ 3.35; TS*Trans ¼ 0.357, t ¼ 1.91), indicating more transparent firms engaging intax planning would add value premium to themselves.

In addition, replacing qi,t with qi,tþ1 does not change regression resultssubstantially. Meanwhile, the results are not sensitive to different calculations ofTobin q. The computation of non-tradable share value varies with market value orbook value; either way does not change results substantially. In unreported table, theresults are robust to the replacement of Tobin q with M/B ratio.

To address the impact of institutional change, we conduct robust tests on 2001-2007and 2008-2009 subsamples, given the corporate income tax reform introduced in 2008.China launched significant enterprise income tax reform in 2008 which eliminatedsubstantial tax credits for listed firms and increased overall corporate income taxlevel. In this context, tax avoidance behavior varies for enterprises with differentialtax rate. Robust tests show that there is no substantial change for the main results,indicating minor influence of institutional change and time on the variables of interest.Taking the year of 2007, in which China’s GAAP converged with IFRS, as a cutoff pointand splitting the whole sample into two subsamples, we draw similar conclusions.

Finally, our results remain robust even after controlling geographical differencesand ultimate ownership characteristics. To address the concern of endogeneity, a seriesof alternative treatments are conducted, including fixed effects of panel data, first-orderdifferential, lagged variables and 2SLS. Nevertheless, we still cannot eliminate thethreat of endogeneity. Thus, we believe that there are associations to some extentamong tax avoidance, information transparency and firm value, and the exactcause-and-effect relationship cannot be determined.

OLS (TaxAgg ¼ BTD) OLS (TaxAgg ¼ TS )OLS

(TaxAgg ¼ ETR_D)Coefficient t-value Coefficient t-value Coefficient t-value

Intercept 20.623 21.62 20.624 21.61 20.634 21.60DTaxAgg 21.277 * * * 23.34 20.455 * 21.95 20.163 21.22Trans 0.195 1.05 0.020 1.06 0.020 1.09DTaxAgg*Trans 0.394 * * * 3.35 0.357 * 1.91 0.030 0.43DPPE 20.039 20.37 20.029 20.27 20.020 20.18DDEBT 0.206 * 1.78 0.203 * 1.79 0.217 * 1.80DROA 0.824 1.29 0.717 1.19 0.613 1.05DSIZE 20.935 * * * 27.26 20.938 * * * 27.32 20.947 * * * 27.52DGROWTH 0.011 0.58 0.015 0.81 0.021 1.13DNOL 0.270 0.70 0.196 0.50 20.028 20.07DBETA 20.324 * * * 23.68 20.326 * * * 23.61 20.340 * * * 23.72qt21 20.242 * 21.81 20.243 * 21.81 20.242 * 21.82YEAR Yes Yes Yesn 3,287 3,287 3,287R 2 0.6282 0.6269 0.6263

Notes: Significant at: *10, * *5 and * * *1 percent levels; to compute t-values, OLS regression adoptsthe approach by Petersen (2009) to adjust clustering standard deviation of firm and year

Table VI.Robustness checks

NBRI5,1

38

7. Conclusions and implicationsThis paper examines whether tax avoidance behavior enhances firm value in Chineseinstitutional setting. While the traditional view of corporate tax avoidance suggests thatshareholder value should benefit from tax avoidance activities, an agency perspective oncorporate tax avoidance provides a more nuanced prediction. Specifically, corporategovernance should be an important determinant of the valuation of purported corporatetax savings. While tax avoidance per se should increase the after-tax firm value, thiseffect is potentially offset, particularly in poorly governed firms, by increasingprobabilities of rent diversion provided by tax shelters. China is a country where theunique institutional arrangements make corporate agency problems more severe thanmost western countries. Using the data of Chinese listed companies for the period2001-2009, we find that the increases in tax avoidance tend to reduce the level of firmvalue. Tax avoidance behavior does more harm than good to investors in China. After 20years of development of the Chinese capital market, listed companies have made greatefforts in improving corporate governance, including enhancing information disclosuretransparency. In this paper, we also find that corporate transparency interacts with taxavoidance and acts as the moderator variable between tax avoidance and corporatevalue. The negative relation between tax avoidance and firm value is attenuated inwell-governed firms. Taken as a whole, investors in China do not place value premiumon tax avoidance because this kind of activity could camouflage manager rent-seekingbehavior. In other words, investors in China downplay the significance of tax avoidance,although information transparency could soften their negative tone.

One limitation of our study is that we focus on examining the general economicconsequences of tax avoidance in the Chinese institutional context, and we do not explorehow specific institutional characteristics shape domestic corporate tax avoidancebehavior, so we leave these questions for future research. The policy implications of thispaper indicate that the characteristics of the taxation system in one country, such as thestructure of rates and the status of enforcement, will shape managerial actions as well asthe severity of agency problems. Tax avoidance does not simply represent wealthtransfer from government to shareholders, but it also means part of gains might be pipedinto self-serving managers. Hence, improving corporate governance and strengtheningtax enforcement can bring in more tax revenue and shareholder wealth.

Notes

1. In China, National Taxation Bureau (Guoshuiju) and provincial bureaus (Dishuiju) areresponsible for collecting central taxes and local taxes separately. Right now, corporateincome tax is classified as a central tax and thus is collected by the National TaxationBureau and its branches in all provinces. Tax policies are widely used in local governments,especially in coastal regions of China to attract more investments, such as establishingeconomic development zone and granting tax credit and preference for high-tech firms, etc.

2. If the amount of long-term liabilities is zero, we use non-current liabilities instead.

References

Armstrong, C.S., Guay, W.R. and Weber, J.P. (2010), “The role of information and financialreporting in corporate governance and debt contracting”, Journal of Accounting andEconomics, Vol. 22 Nos 2/3, pp. 179-234.

Tax avoidanceand firm value

39

Ayers, B.C., Jiang, J. and Laplante, S.K. (2009), “Taxable income as a performance measure:the effects of tax planning and earnings quality”, Contemporary Accounting Research,Vol. 26 No. 1, pp. 15-54.

Balakrishnan, K., Blouin, J. and Guay, W. (2011), “Does tax aggressiveness reduce financialreporting transparency?”, available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id¼1792783 (accessed 30 September 2013).

Bushman, R.M. and Smith, A.J. (2003), “Transparency, financial accounting information, andcorporate governance”, Economic Policy Review, Vol. 9 No. 1, pp. 65-87.

Cai, H. and Liu, Q. (2009), “Competition and corporate tax avoidance: evidence from Chineseindustrial firms”, The Economic Journal, Vol. 119, April, pp. 1-32.

Chen, K.C.W. and Yuan, H. (2004), “Earnings management and capital resource allocation:evidence from China’s accounting-based regulation of rights issues”, The AccountingReview, Vol. 79 No. 3, pp. 645-665.

Chen, S., Chen, X., Cheng, Q. and Shevlin, T. (2010), “Are family firms more tax aggressive thannon-family firms?”, Journal of Financial Economics, Vol. 95 No. 1, pp. 41-61.

Chen, X. and Zhu, H. (2007), Corporate Governance in Transition Economies, TsinghuaUniversity Press, Beijing.

Cooper, I.A. and Nyborg, K.G. (2006), “The value of tax shields IS equal to the present value oftax shields”, Journal of Financial Economics, Vol. 81 No. 1, pp. 215-225.

Desai, M.A. (2005), “The degradation of reported corporate profits”, Journal of EconomicPerspectives, Vol. 19 No. 4, pp. 171-192.

Desai, M.A. and Dharmapala, D. (2006), “Corporate tax avoidance and high-powered incentives”,Journal of Financial Economics, Vol. 79 No. 1, pp. 145-179.

Desai, M.A. and Dharmapala, D. (2009), “Corporate tax avoidance and firm value”, Review ofEconomics and Statistics, Vol. 91 No. 3, pp. 537-546.

Desai, M.A., Dyck, A. and Zingales, L. (2007), “Theft and taxes”, Journal of Financial Economics,Vol. 84 No. 3, pp. 591-623.

Dyreng, S.D., Hanlon, M. and Maydew, E.L. (2008), “Long-run corporate tax avoidance”,The Accounting Review, Vol. 83 No. 1, pp. 61-82.

Fang, J. (2007), “Information disclosure transparency and analyst forecasts of Chinese listedfirms”, The Journal of Financial Research, Vol. 6, pp. 136-149 (in Chinese).

Frank, M.M., Lynch, L.J. and Rego, S.O. (2009), “Tax reporting aggressiveness and itsrelation to aggressive financial reporting”, The Accounting Review, Vol. 84 No. 2,pp. 467-496.

Hanlon, M. and Heitzman, S. (2010), “A review of tax research”, Journal of Accounting andEconomics, Vol. 50 Nos 2/3, pp. 127-178.

Hanlon, M. and Slemrod, J. (2009), “What does tax aggressiveness signal? Evidence from stockprice reactions to news about tax shelter involvement”, Journal of Public Economics, Vol. 93Nos 1/2, pp. 126-141.

Hanlon, M., Laplante, S.K. and Shevlin, T. (2005), “Evidence for the possible information loss ofconforming book income and taxable income”, Journal of Law & Economics, Vol. 48 No. 2,pp. 407-442.

Jiang, G., Lee, C.M.C. and Yue, H. (2010), “Tunneling through intercorporate loans: the Chinaexperience”, Journal of Financial Economics, Vol. 98 No. 1, pp. 1-20.

Kemsley, D. and Nissim, D. (2002), “Valuation of the debt tax shield”, Journal of Finance, Vol. 57No. 5, pp. 2045-2073.

NBRI5,1

40

Lambert, R.A., Leuz, C. and Verrecchia, R.E. (2007), “Accounting information, disclosure, andthe cost of capital”, Journal of Accounting Research, Vol. 45 No. 2, pp. 385-420.

Li, W. and Xu, Y. (2013), “Political status and tax avoidance”, The Journal of Financial Research,Vol. 3, pp. 114-129 (in Chinese).

Manzon, G.B.J. and Plesko, G.A. (2002), “The relation between financial and tax reportingmeasures of income”, Tax Law Review, Vol. 55, pp. 175-214.

Petersen, M.A. (2009), “Estimating standard errors in finance panel data sets: comparingapproaches”, Review of Financial Studies, Vol. 22 No. 1, pp. 435-480.

Roberts, M.R. and Whited, T.M. (2011), “Endogeneity in empirical corporate finance”, availableat: http://papers.ssrn.com/sol3/papers.cfm?abstract_id¼1748604

Tang, T.Y. and Firth, M. (2011), “Can book-tax differences capture earnings management and taxmanagement? Empirical evidence from China”, The International Journal of Accounting,Vol. 46, pp. 175-204.

Wang, J. and Zhang, Q. (2009), “Information transparency and manager compensationeffectiveness: evidence from Chinese securities market”, Nankai Business Review, Vol. 5,pp. 94-100 (in Chinese).

Wang, X. (2010), “Tax avoidance, corporate transparency, and firm value”, available at:http://papers.ssrn.com/sol3/papers.cfm?abstract_id¼1716474

Wang, X. and Dai, D. (2013), “The information content of income tax item in consolidatedfinancial statements”, The Journal of Shanxi University of Finance and Economics, Vol. 2,pp. 116-124 (in Chinese).

Wu, L. (2009), “State ownership, preferential tax, and corporate tax burdens”, Economic ResearchJournal, Vol. 10, pp. 109-120 (in Chinese).

Yang, D., Wei, Y. and Ye, J. (2008), “The effects of split share structure on the empirical capitalmarket research in China and the corrections”, Economic Research Journal, Vol. 3, pp. 73-87(in Chinese).

Zeng, Y. and Zhang, J. (2009), “Does taxation have a governance role?”, The Management World(Monthly), Vol. 3, pp. 143-151 (in Chinese).

Zhang, B., Fan, Z. and Pan, J. (2009), “Information transparency and corporate performance –from endogeneity perspective”, The Journal of Financial Research, Vol. 2, pp. 169-184(in Chinese).

Zheng, Z., Yin, H. and Hu, B. (2013), “The effectiveness of corporate governance of non-listedfirms – evidence from Chinese manufacturing large and medium-sized enterprises”,The Journal of Financial Research, Vol. 2, pp. 142-155 (in Chinese).

Further reading

Cheng, C.S.A., Huang, H., Li, Y. and Stanfield, J. (2012), “The effect of hedge fund activism oncorporate tax avoidance”, The Accounting Review, Vol. 87 No. 5, pp. 1493-1526.

Chyz, J. (2012), “Personally tax aggressive executives and corporate tax aggressiveness”,available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id¼1985558 (accessed30 September 2013).

Gai, D. and Hu, G. (2012), “The tradeoff between tax avoidance and financial reporting costs –evidence from China corporate income tax reform in 2008”, The Journal of AccountingResearch, Vol. 3, pp. 20-25 (in Chinese).

Graham, J.R. and Tucker, A.L. (2006), “Tax shelters and corporate debt policy”, Journal ofFinancial Economics, Vol. 81 No. 3, pp. 563-594.

Tax avoidanceand firm value

41

Hanlon, M. (2003), “What can we infer about a firm’s taxable income from its financialstatements?”, National Tax Journal, Vol. 56 No. 4, pp. 831-863.

Jensen, M.C. and Meckling, W.H. (1976), “Theory of the firm: managerial behavior, agency costsand ownership structure”, Journal of Financial Economics, Vol. 3 No. 4, pp. 305-360.

Lambert, R.A. (2001), “Contracting theory and accounting”, Journal of Accounting & Economics,Vol. 32 Nos 1-3, pp. 3-87.

Lang, M. and Maffett, M. (2010), “Economic effects of transparency in international equitymarkets: a review and suggestions for future research”, Foundations and Trends inAccounting, Vol. 5, pp. 175-241.

Lv, W. (2011), “Agency cost, tax planning and market value: a case study on j company”, NankaiBusiness Review, Vol. 4, pp. 138-148 (in Chinese).

Rego, S.O. and Wilson, R. (2012), “Equity risk incentives and corporate tax aggressiveness”,Journal of Accounting Research, Vol. 50 No. 3, pp. 775-810.

Slemrod, J. (2004), “The economics of corporate tax selfishness”, National Tax Journal, Vol. 57No. 4, pp. 877-899.

Ye, K. (2006), “Earnings management and income tax expense: a study on book-tax difference”,China Accounting Review, Vol. 4 No. 2, pp. 205-224 (in Chinese).

Yu, L. and Li, C. (2010), “The tax decentralization reform and corporate tax avoidance”,The Journal of Xiamen University (Social Science Edition), Vol. 4, pp. 123-130 (in Chinese).

NBRI5,1

42

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints