Embed Size (px)

Citation preview

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 1/59

NRHQ Commercial 1

WorkshopOn

Commercial Competency Building

AtRihand STPS

On15 March 2008

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 2/59

NRHQ Commercial 2

Program Outline

1. Presentation on Tariff Formulations

2. Presentation on Reform Status in Uttar Pradesh

3. Sharing of CRMS Outputs

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 3/59

NRHQ Commercial 3

Presentation

On

Tariff Formulations

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 4/59

NRHQ Commercial 4

Backgroundof

Tariff Determination

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 5/59

NRHQ Commercial 5

SEBs Section 59 of Electricity (Supply) Act, 1948 provides that --

“The Board shall, after taking credit for any subvention from the State Government under section 63, carry on its operations under this Act and adjust its tariffs so as to ensure that the total revenues in any year of account

shall, after meeting all expenses properly chargeable to revenues, including operating, maintenance and management expenses, taxes (if any) on income and profits, depreciation and interest payable on all debentures, bonds and loans leave such surplus as is not less than three per cent or such higher percentage, as the State Government may, by notification in the Official Gazette, specify in this behalf, of the value of the fixed assets of the Board in

service at the beginning of such year.”

LICENSEES

Schedule VI of Electricity(Supply) Act, 1948 specifies basis for determinationof tariff by the licensees.

STATUTORY PROVISIONS FOR TARIFF OF DIFFERENT UTILITIES

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 6/59

NRHQ Commercial 6

Sixth-schedule of Electricity (Supply) Act - 1948

Return Assets acquired before 1956 - 7%Assets acquired between 1956 - 15.10.1991 - RBI rate + 2%Assets acquired after 15.10.91 - RBI rate + 5%

Capital Base considered for this purpose is sum of:The original cost of fixed assets available for useThe cost of intangible assetsThe original cost of works in progress

Working capitalAmount of compulsory investments

LessAccumulated depreciationAmount of loan advanced by the BoardAmount of any debentures issued by the licenseesAmount of any loans approved by the state governmentAmount of any cash deposit by the consumersAmount standing to the credit of the tariff and dividend control reserveAmount carried forward in the accounts of the licensee fordistribution to the consumers

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 7/59

NRHQ Commercial 7

GENERATING COMPANIES (Prior to ERC Act / EA 2003)

Section 43A(2) of Electricity (Supply) Act provides that --“ The tariff for the sale of electricity by a Generating Company to the

Board shall be determined in accordance with the norms regarding operation and the Plant Load Factor as may be laid down by the Authority and in accordance with the rates of depreciation and reasonable return and such other factors as may be determined, from time to time, by the Central Government, by notification in the Official Gazette.

Provided that the terms, conditions and tariff for such sale shall, in respect of a Generating Company, wholly or partly owned by the Central Government, be such as may be determined by the Central Government and in respect of a Generating Company wholly or partly owned by one

or more State Governments be such as may be determined, from time to time, by the government or governments concerned.”

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 8/59

NRHQ Commercial 8

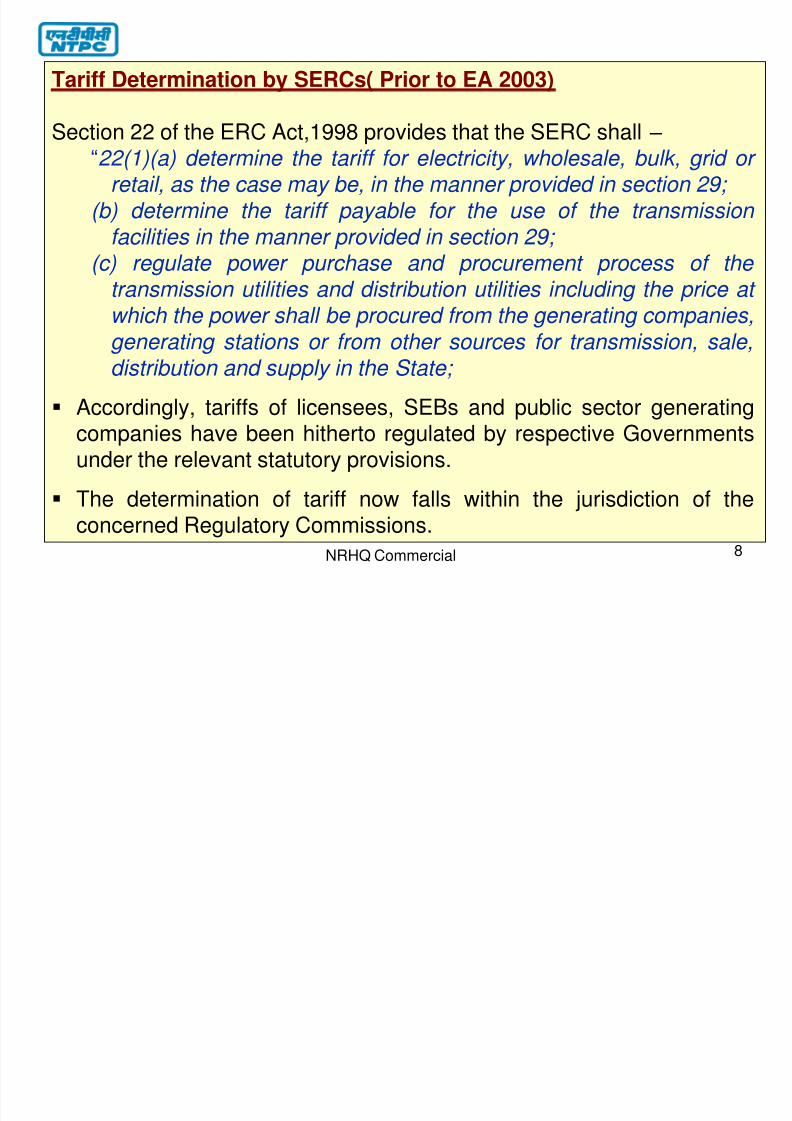

Tariff Determination by SERCs( Prior to EA 2003)

Section 22 of the ERC Act,1998 provides that the SERC shall – “22(1)(a) determine the tariff for electricity, wholesale, bulk, grid or

retail, as the case may be, in the manner provided in section 29; (b) determine the tariff payable for the use of the transmission

facilities in the manner provided in section 29; (c) regulate power purchase and procurement process of the

transmission utilities and distribution utilities including the price at which the power shall be procured from the generating companies,generating stations or from other sources for transmission, sale,distribution and supply in the State;

Accordingly, tariffs of licensees, SEBs and public sector generatingcompanies have been hitherto regulated by respective Governmentsunder the relevant statutory provisions.

The determination of tariff now falls within the jurisdiction of theconcerned Regulatory Commissions.

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 9/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 10/59

NRHQ Commercial 10

Tariff Determination by CERC (Electricity Act 2003) – Contd.

Section 86 (1) of the EA-2003 provides that -- “The State Commission shall discharge the following functions, namely: - (a) determine the tariff for generation, supply, transmission and wheeling of electricity, wholesale, bulk or retail, as the case may be, within the State:

Providing that where open access has been permitted to a category of consumers under section 42, the State Commission shall determine only the wheeling charges and surcharge thereon, if any, for the said category of

consumers; (b) regulate electricity purchase and procurement process of

distribution licensees including the price at which electricity shall be procured from the generating companies or licensees or from other sources through agreements for purchase of power for distribution and supply within the

State” Section 63 of the EA-2003 provides that -- “Notwithstanding anything

contained in section 62, the Appropriate Commission shall adopt the tariff if such tariff has been determined through transparent process of bidding in accordance with the guidelines issued by the Central Government.”

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 11/59

NRHQ Commercial 11

Single part based on MOU1982 – 85

Mutual Negotiation

Two part- GOI NotificationOn 30.03.1992

ABTCERC

Evolution of Tariff

Single part based on BPSA1985 – 87

Mutual Negotiation

Umpire Award1987-1992

Tariff Regulation (K P Rao)1997-01CERC

Tariff Regulation 2001-04

CERC

Tariff Regulation 2004-09CERC

Two part- K P Rao

1992 – 97GOI

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 12/59

NRHQ Commercial 12

Single-part Tariff based on MOU (1982 – 85 )

• First unit of Singrauli was synchronised on 13.02.1982

• MOU for Tariff was signed for Singrauli in 1982, Korba in 1984,

Ramagundam in 1984 & Farakka in1985• Norms adopted were as follows:

Norms Singrauli Korba

Gen level for full FC recovery 5000 5000

Stabilisation Period 12 months 12 months

APC 10% 10%

Depreciation 3.5% 3.5%

O&M Expenses 2.25% of current capital cost@ Rs. 7500 per kw

2.25% of current capitalcost @ Rs. 8000 per kw

SHR 2750 kcal / kwh 2750 kcal / kwh

RoE As notified by GoI As notified by GoI

IoL 12.5% 13%

Specific oil consumption 12 ml /kwh 12 ml /kwh

Tariff 31.12 paisa / kwh + FPA 34.5 paisa / kwh + FPA

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 13/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 14/59

NRHQ Commercial 14

Cost of electricity = Fixed Cost / Gen. at 5000 / 5500 hrs

= ‘ X ’ p / kwh This rate was used even if generation was higher than5000/5500 kwh / kw / yr

Demerits

Collection of fixed charges above the actual fixed charges.

GENCOs started dumping power even when frequency was high.

SEBs found that total cost to be paid to GENCOs was higher than the marginal cost of

their station.

Led to sharp difference between CGs & SEBs on who should back down.

Discouraged Merit Order Operation

Single- Part Tariff

Prolonged discussions were held in 1988 but consensus could notbe reached

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 15/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 16/59

NRHQ Commercial 16

Two-part Tariff - K.P.Rao (1992 – 97)

• Norms adopted ( Continued…)

– Stabilisation period – 1 year

– Generation level for full FC recovery• During Stabilisation period -

ER – 3500 hrs ; Other Regions – 4000 hrs

• After Stabilisation period –

ER – 5000 hrs ; Other Regions – 5500 hrs

– Incentive @ 1 paisa per kwh for each 1% rise in PLF

• During Stabilisation period -

ER – 4000 hrs; Other Regions – 4500 hrs

• After Stabilisation period –

ER – 5500 hrs; Other Regions – 6000 hrs

– O&M Charges - 2.5% of current capital cost escalated @ 10% per year.

– Working Capital –

• O&M expenses – 1 month

• Fuel Expenses – 1 month

• Coal Stock – Not exceeding 15 days for pit-head, 30 days for non-pithead

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 17/59

NRHQ Commercial 17

Two-part Tariff - K.P.Rao (1992 – 97)

Norms Other Regions Eastern region

Ist year Thereafter Ist year ThereafterSp.Oil (ml/kwh) -200 / 500 MW 5 3.5 15 10 , 8

APC (%) - 200 (with / w/o CT)

-500 TDBFP / MDBFPWith CT

10 / 10.5

8.75 / 9.75

+ 0.5

9 / 9.5

7.5 / 9

+ 0.5

12 / 12.5

10.75/11.75

+ 0.5

10 / 10.5

8.5 / 10

+ 0.5

SHR (Kcal/Kwh) – 200 /500MW

With MDBFP

2600

2560

2500

2460

2800

2740

2700

2640

Fixed Cost of SEB A for the year = AFC x EA / TE

EA = Energy drawn by SEB A in a particular year

TE = Total Energy generated in the year

AFC = Annual Fixed Cost to be paid based on annual availability

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 18/59

NRHQ Commercial 19

Umpire Award (1987-1992)

• During the interim period (1987 -1992), GoIthrough Cabinet approval constituted 5 Umpires inthe 5 Regions

– ER – A.K.Shah

– WR- A.K.Shah

– SR – D.V.Kapoor

– NR - T.L.Shankar

– NER – Eswaran• The report of the Umpire came out in 1995-96

and effected subsequent adjustment in tariff

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 19/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 20/59

NRHQ Commercial 21

Umpire Award (1987-1992)

Norms

Working capital

• O&M – one month• Fuel – one month

• Coal stock – 15 days for pit head – 30 days for non pit head

• .Oil stock – Average maintained over preceding two yearslimited to 60 days

• Spares – Inventory covering one year requirement• Receivables – 60 days

• Interest Rate – Bank CC rate• Variable charge – At actual• Deemed generation not allowed for Tx and fuel constraint• Incentive rate as per K P Rao• Excise duty, Cess etc allowed

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 21/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 22/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 23/59

NRHQ Commercial 24

Different Tariff Structures

50 %

100 %

FIXED

CHARGES

62.8 % 68.5 %

P LF / AVAILABILITY

INCENTIVE

80% 100%

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 24/59

NRHQ Commercial 25

CERC TARIFF REGULATIONS 2001

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 25/59

NRHQ Commercial 26

Return on Equity

Return on equity is computed on the equity component ofcapital cost of the project considering the approved debt :

equity ratio.

For the purpose of tariff, capital cost adopted is the amount

capitalised on year to year basis as per audited accounts.Equity component of the capital cost is worked out based

on the approved debt:equity ratio which is 50:50 for earlier

stations and 70:30 for the new projects.

Rate of return of 16% is applied to the equity component ofthe capital cost worked out as above.

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 26/59

NRHQ Commercial 27

GENERALRegulation came into force w.e.f. 1-4-2001, and remained in force for

a period of 3 years• Applicable where the capital cost-based tariff• Capital cost of the project shall be broken up into stages and by

distinct units forming part of the project. The common facilities shallbe apportioned on the basis of the installed capacity of the units

• Recovery of Income Tax and Foreign Exchange Rate Variationshall be done directly by the utilities from the beneficiaries withoutfiling a petition before the Commission

• Tariff revisions during the tariff period on account of capitalexpenditure within the approved project cost incurred during the

tariff period may be entertained by the Commission only if suchexpenditure exceeds 20% of the approved cost. In all cases, wheresuch expenditure is less than 20%, tariff revision shall beconsidered in the next tariff period.

Tariff Regulation 2001-04

Norms were only ceiling norms

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 27/59

NRHQ Commercial 28

FERV

• Extra rupee liability towards interest payment and loan repaymentactually incurred, in the relevant year shall be admissible; providedit directly arises out of foreign exchange rate variation and is notattributable to Utility or its suppliers or contractors. Every utility shallfollow the method as per the Accounting Standard- 11(Eleven) as

issued by the Institute of Chartered Accountants of India tocalculate the impact of exchange rate variation on loan repayment.

• Any foreign exchange rate variation to the extent of the dividendpaid out on the

permissible equity contributed in foreign currency, subject to theceiling of permissible return shall be admissible. This as and whenpaid, may be spread over the twelve-month period in arrears.

Tariff Regulation 2001-04

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 28/59

NRHQ Commercial 29

Norms• Target Availability 80%

• Target PLF for incentive 77%• Depreciation

Coal based – 3.6% and Gas – 6%

• Advance Against Depreciation has been limited to 1/12th of theloan amount less depreciation

• Return on Equity 16%• Stabilization period commencing from the date of commercialoperation shall be reckoned as follows:

(a) Thermal (coal/lignite) station - 180 days(b) Open cycle gas and Naphtha based station - 90 days(c) Combined cycle gas and Naphtha based station - 90 days

• Interest on loan capital shall be computed on the outstandingloans, duly taking into account the schedule of repayment, as perthe financial package approved by the Authority or an appropriateindependent agency, as the case may be

Tariff Regulation 2001-04

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 29/59

NRHQ Commercial 30

Norms

Operation and Maintenance expenses for the existing stations of NTPC which

have been in operation for 5 years or more in the base year of 1999-2000, shallbe derived on the basis of actual O&M expenses, excluding abnormal O&Mexpenses, if any, for the years 1995-96 to 1999-2000 duly certified by thestatutory auditors.

The average of actual O&M expenses for the years 1995-96 to 1999-2000considered as O&M expenses for the year 1997-98 shall be escalated twice atthe rate of 10 percent per annum to arrive at O&M expenses for the base year1999-2000

The Base O&M expenses for the year 1999-2000 shall be further escalated atthe rate of 6 percent per annum to arrive at permissible O&M expenses for therelevant year.

For plants commissioned during the tariff period (2001-02 to 2003-04), the BaseO&M expenses shall be fixed at 2.5 percent of actual capital cost as approvedby the Authority or an appropriate Independent agency, as the case may be, inthe year of commissioning and shall be subject to an annual escalation of 6 percent per annum from the subsequent year.

Tariff Regulation 2001-04

T iff R l ti 2001 04

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 30/59

NRHQ Commercial 31

Norms• The escalation factor of 6 percent per annum shall be used to revise the base

figure of O&M expenses. A deviation of the escalation factor computed from

the actual inflation data that lies within 20 percent of the above notifiedescalation factor of 6 percent (which works out to be 1.2 percentage points oneither side of 6 percent) shall be absorbed by the utilities/beneficiaries. In otherwords if the escalation factor computed from the observed data lies in therange of 4.8 to 7.2 percent, this variation should be absorbed by the utilities.

• Any deviations beyond this limit shall be adjusted on the basis of the actual

escalation factor arrived at by applying a weighted price index of CPI forindustrial workers (CPI_IW) and an index of select components of WPI(WPIOM)

• The escalation of yearly expenses from the published data for the tariff periodshall be computed as follows:

0.4 x INFLCPI + 0.6 x INFLWPIOMwhere:INFLCPI = Annual Average Inflation in CPI_IWINFLWPIOM = Annual Average Inflation in WPIOM

Tariff Regulation 2001-04

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 31/59

NRHQ Commercial 32

Interest on working capital

Elements of Working Capital

O&M expenses for one month

Fuel expenses for one month at normative generation level

Fuel stock - coal 15 days for pit head stations

30 days for non-pit head stations

Secondary fuel oil stock of 60 days

Spares inventory for one year consumption

Receivables – 2 months

Bank CC Rate is taken

Income Tax is pass through and payment wasenvisaged through tax escrow account

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 32/59

NRHQ Commercial 33

Incentive• An incentive shall be allowed to be recovered @ 50% of the fixed

cost/kWh at normative PLF for generation between normative PLF andup to 90% PLF, subject to a ceiling of 21.5 paise/kWh.

• For generation beyond 90% PLF, incentive shall be allowed to berecovered @ 50% of the incentive payable as above.

Development Surcharge

• Development Surcharge of 5% on every bill for Fixed Charges raisedby it in respect of generation at regional level. The DevelopmentSurcharge shall not be payable for plants operating exclusively within a

State which has been discontinued by CERC

Tariff Regulation 2001-04

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 33/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 34/59

NRHQ Commercial 35

CERC TARIFF REGULATIONS 2004

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 35/59

NRHQ Commercial 36

Tariff Regulations 2004-09

• CERC Terms and Conditions of Tariff Regulations 2004came into force on 01.04.2004 for a period of 5 years.

• Applicable in all cases where tariff is to be determined by

Commission based on capital cost

• Commission shall adopt the tariff if arrived throughcompetitive bidding process as per GoI Guidelines

• Operation Norms specified under these regulations areceiling norms – – Improved norms may be mutually agreed by generator

and beneficiary for determination of tariff

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 36/59

NRHQ Commercial 37

Tariff Regulations 2004-09

Application for Tariff Determination – Provisional Tariff• Applicable from date of commercial operation

• Application in advance of anticipated date of

project completion• Based on audited capital expenditure actuallyincurred up to the date of application or earlierdate

– Final Tariff• Based on actual capital expenditure incurred up to

the date of commercial operation certified bystatutory auditor

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 37/59

NRHQ Commercial 38

Tax on income from core business

– Tax on income from core business shall be computed as anexpense and recovered from the beneficiaries.

– Benefits of tax-holiday shall be passed on to beneficiaries

– Corporate Tax liability shall be distributed amongst all generatingstations on the basis of Estimated annual generating station-wise Profit Before Tax

– Income tax allocated to thermal generating stations shall becharged to beneficiaries in the proportion of Annual fixedcharges

– Tax liability shall be estimated and intimated to beneficiaries twomonths before starting of each year

– Any Under / Over recoveries of tax shall be adjusted annually onthe basis of income-tax assessment

– Tax escrow mechanism shall be maintained by beneficiaries forfacilitating payment and refund of income-tax

Tariff Regulations 2004-09

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 38/59

NRHQ Commercial 39

Extra Rupee Liability:• Extra rupee liability towards loan repayment and interest payment

corresponding to normative / actual foreign loan shall be permissible

if it arises out of FERV and is not attributable to the generating

company

• Recovery of FERV by Generating company shall be made

– On a year to year basis

– Directly without making any application before the Commission

Deviations from Specified Norms:

• Overall per unit Tariff determined over entire life of plant on basis of

norms in deviation does not exceed the tariff on basis of specified

norms.

Tariff Regulations 2004-09

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 39/59

NRHQ Commercial 40

Tariff comprises of two parts-

Annual Capacity (Fixed) Charges –

• Return on equity (ROE)

• Interest on Loan

• Depreciation including Advance Against Depreciation

• O&M Expenses

• Interest on Working Capital Energy (Variable) Charges -

• Fuel cost

Tariff for Thermal Generating Stations

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 40/59

NRHQ Commercial 41

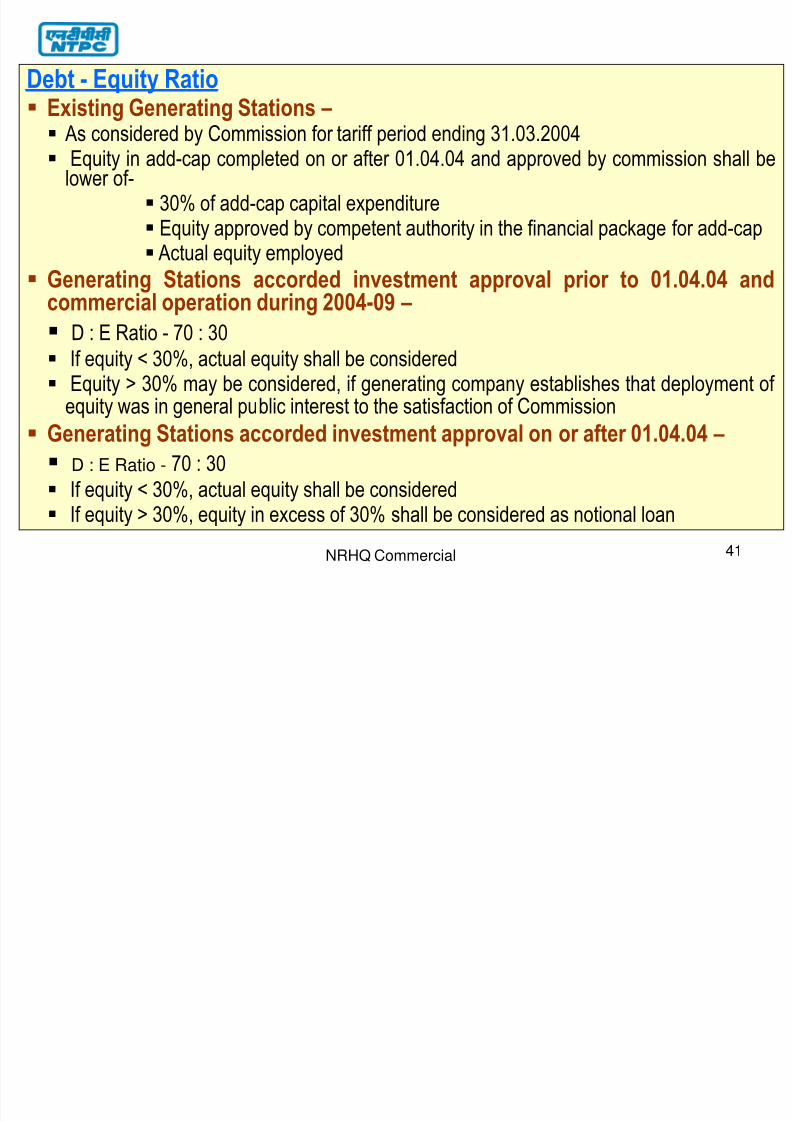

Debt - Equity Ratio Existing Generating Stations –

As considered by Commission for tariff period ending 31.03.2004 Equity in add-cap completed on or after 01.04.04 and approved by commission shall belower of-

30% of add-cap capital expenditure Equity approved by competent authority in the financial package for add-cap Actual equity employed

Generating Stations accorded investment approval prior to 01.04.04 andcommercial operation during 2004-09 – D : E Ratio - 70 : 30

If equity < 30%, actual equity shall be considered Equity > 30% may be considered, if generating company establishes that deployment of

equity was in general public interest to the satisfaction of Commission Generating Stations accorded investment approval on or after 01.04.04 –

D : E Ratio - 70 : 30

If equity < 30%, actual equity shall be considered If equity > 30%, equity in excess of 30% shall be considered as notional loan

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 41/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 42/59

NRHQ Commercial 43

Additional Capitalisation-• Capital expenditure (within the original scope of work) actually incurred from

cod and up to cut-off date, may be admitted, subject to prudence by Commission,in cases as under – • Deferred liabilities• Works deferred for execution• Procurement of initial spares within original scope of work• On account of change of law• Liabilities to meet award of arbitration or compliance of order or decree of

court• Capital expenditure incurred after cut-off date may be admitted for-

• Deferred liabilities (within original scope of work)• Deferred Works relating to ash pond or ash handling system• Necessary for efficient and successful operation of plant but not included inoriginal project cost

• On account of change of law• Liabilities to meet award of arbitration or compliance of order or decree ofcourt

• Expenditure on minor items like tools & tackles, PCs, ACs, Refrigerators, Fans,Coolers, TV, Heat convectors, Mattresses, etc. bought after cut-off date shall not be considered for capitalisation

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 43/59

NRHQ Commercial44

Additional Capitalization (Contd.)

• Any Capital expenditure on account of – • Committed liabilities / Deferred expenditure on techno-economic grounds

(within original scope of works) shall be serviced in the normative debt equityratio.

• Replacement of old assets shall be considered after writing off the grossvalue of the assets from the project cost

• New works not in original scope of works shall be serviced in the normativedebt equity ratio.

• R&M and life extension shall be serviced at normative debt equity ratio after

writing off the original amount of the replaced assets from the original projectcost

• Impact of additional capitalisation in tariff revision may be consideredtwice in a tariff period including revision of tariff after the cut off date

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 44/59

NRHQ Commercial45

Return on Equity • 14% per annum post tax

• Return on Equity invested in foreign currency

• Shall be allowed up to the prescribed limit in the same

currency

• Shall be paid in Indian rupees on the exchange rate on

the due date of billing

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 45/59

NRHQ Commercial46

Interest on loan• Interest on loan shall be computed

• Loan-wise as per the debt-equity ratio adopted for tariff • By applying weighted average actual interest rate

• Outstanding loan (as on 01.04.2004) shall be computed as Gross loan minus cumulativerepayment (as admitted on 31.3.2004)

• Repayment shall be on normative basis. • Commission has further said that during the period of moratorium, depreciation recovery

shall be treated as loan repayment while working out interest on loan.

• Generating company shall make efforts to refinance loans as long as it results in net benefitto the beneficiaries. Cost associated with such refinancing of loan shall be borne bybeneficiaries

• Generating company shall not make any profit on account of interest on loan and refinancingof loan

• The generating company may swap loans having a floating rate of interest with loans havingfixed rate of interest or vice-versa at its own cost and gains / losses as aresult shall accrue tothe generating company. Beneficiaries shall be liable to pay interest for loans originallycontracted

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 46/59

NRHQ Commercial47

Depreciation • Depreciation shall be allowed up to a maximum of 90% of the historical capital cost

(excluding the cost of land)

• Based on straight line method at. rates (weighted avg.) prescribed as under-

• 3.6% for coal based stations

• 6% for gas based station

• On repayment of loan, remaining depreciation shall be spread over balance useful life

Advance Against Depreciation (AAD)• AAD permitted only if Cumulative repayment up to a particular year exceeds

cumulative depreciation up to that year

• AAD shall be lower of the following

• Loan repayment in a year (Limited to 1/10th of loan amount ) minus depreciationallowed in that year

• Difference between cumulative repayment and cumulative depreciation up to theyear

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 47/59

NRHQ Commercial48

Interest on working capitalWorking capital comprises of -

• Fuel Cost-Coal based stations - 1½ month for pit head and 2 months for non-pit headcorresponding to target availability

Gas based Stations – Cost of fuel for 1 month

• Secondary Fuel-Coal based stations – Cost of secondary fuel oil for 2 monthsGas based Stations – Cost of Liquid fuel for ½ month.

• O&M expenses - For 1 month

• Spares – 1% of historical capital cost escalated @ 6% p.a from COD.

• Receivables – For 2 months(Earlier provisions for stock of coal & oil were on normative stock or actual whichever is lower. Now ithas been provided on normative basis.)

• Rate of Interest on working capital – Short-term PLR of SBI as on 01.04.2004 or 1st April of the year of cod of generating station, whichever is later.

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 48/59

NRHQ Commercial49

O&M Expenses

Coal based stations (for 2004-05)- For 200/210/250 MW - Rs.10.4 lacs / MW

- For 500 MW and above - Rs. 9.36 lacs / MW

Gas based stations (for 2004-05)

- For Stations with warranty spares - Rs. 5.2 lacs / MW

- For Stations without warranty spares - Rs. 7.8 lacs / MW

Escalation – 4% per year

Talcher TPS – Average of actual O&M expenses of 5 yrs( From 1998-99

to 2002-03) escalated @ 4% per year to arrive at O&M expenses

provision for 2004-05Tanda TPS – Average of actual O&M expenses of 3 years (From 2000-01

to 2002-03) escalated @ 4% per year to arrive at O&M expenses

provision for 2004-05

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 49/59

NRHQ Commercial50

Target Availability for recovery of Full Capacity charges

• All Thermal generating Stations - 80 %• Talcher TPS – 75%

• Tanda TPS – 60%( Recovery of capacity charges below the level of targetavailability shall be on pro rata basis.)Target Plant Load factor for Incentive• All Thermal Generating Stations – 80%• Talcher TPS – 75%• Tanda TPS – 60%

Operating Norms

Operating Norms

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 50/59

NRHQ Commercial51

Operating Norms

Gross Station Heat Rate –

• Coal Based- 200 / 210 / 250 MW - 2500 kcal/kwh (same as earlier)

- 500 MW & Above - 2450 kcal/kwh (reduced by 50 kcal/kwh). (In case of MDBFP, Heat rate will be reduced by 40 kcal/kwh.)

(For generating stations having combination of 200 and 500 MW sets, Normative

Station heat rate shall be weighted avg. heat rate)- Talcher TPS -3100 Kcal / Kwh , Tanda TPS – 3000 Kcal/ kwh

• Gas Based- Gandhar / Faridabad / Kayamkulam GPS - 2000 kcal/kwh

- Dadri / Anta / Kawas GPS - 2075 kcal/kwh

- Auraiya GPS - 2100 kcal/kwh

- Future gas based stations (COD on or after 01.04.2004)

Advanced class machines - 1850 kcal/kwh

Conventional machines - 1950 kcal/kwh

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 51/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 52/59

NRHQ Commercial53

Stabilisation Period180 days for coal based & 90 days for gas basedstations allowed only up to 31.03.2006.

No relaxed norms for target availability have beenallowed during stabilisation period.

Coal LossesLanded cost of coal shall be computed considering transit

loss of-

Generating Stations CERC Norm Pit Head 0.3%

Non Pit Head 0.8%

Operating Norms

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 53/59

NRHQ Commercial54

Other Provisions

• Provision regarding actual or norm whichever is lower has beendeleted. It will provide efficiency gain from future stations.

Commercial Operation Date

• Earlier regulation stipulated a period of 180 days between

synchronisation of a coal unit and its commercial operation.

• This provision has been deleted. It is a welcome change.

Development Surcharge• 5% of fixed charges for regional stations has been deleted

UI CHARGES

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 54/59

NRHQ Commercial55

UI CHARGES (07. 01.08)

Average Frequency of timeblock (Hz)

UI Rate ( paisa per kwh)

50.5 hz & above 0.0

50.5 - 50.48 hz 8.0

49.80 - 49.78 Hz 298

Below 49.02 Hz 1000

Each 0.02 Hz step is equivalent to 8 p / kwh in the 50.5 -49.8 Hz freq. range and 18.0 p /kwh in the 49.8 -49.0 Hz

freq range Provided that in case of generating stationswith coal or lignite firing and stations burning only APMgas, UI rate shall be capped at 406 paise per kWh whenactual generation exceeds the scheduled generation.

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 55/59

NRHQ Commercial56

UI Charges

0

200

400

600

800

1000

1200

4 9

4 9

. 8

5 0

. 5

Freqency (Hz.)

R a t e ( P / U n i t )

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 56/59

NRHQ Commercial57

UI Charges

0

50

100

150

200250

300

350

400450

4 9

4 9

. 7

4 9

. 8

5 0

. 5

Freqency (Hz.)

R a t e ( P

/ U n i t )

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 57/59

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 58/59

NRHQ Commercial59

Interest on difference in Provisional & Final Tariff –

• Where the provisional tariff charged exceeds the final tariff, thegenerating company shall pay simple interest @ 6% per annum,computed on a monthly basis on the excess amount so charged from thedate of payment of payment of such excess amount and up to the date ofadjustment

• Where the provisional tariff charged is less than the final tariff, thebeneficiaries shall pay simple interest @ 6% per annum, computed on amonthly basis on the deficit amount from the date on which final tariff willbe applicable up to the date of billing such deficit amount

• The excess / deficit amount along with simple interest @ 6% shall beadjusted within three months of the order failing which the defaultingentity / beneficiary shall be liable to pay penal interest at rate as may bedecided by Commission

8/2/2019 Tariff Formulations

http://slidepdf.com/reader/full/tariff-formulations 59/59

60