Embed Size (px)

Citation preview

Supercharge Your Collection Strategy with CL Collections™

CL Collections™

Executive Summary

The Strategic Value of Collections

Best Practices in Collections

Collection Phases

How Automation Can Optimize Collection

Implementing Collection Processes

How CL Collections™ Can Supercharge Your Collections Strategy

Summary

Contents

3

4

5

6

7

8

9

11

Executive Summary

3 | Cloud Lending Solutions

CL Collections™

The primary objective of collections is to generate a positive return for the organization by converting potential losses into revenue. Most organizations leave this potential revenue on the table as collections is often viewed as a secondary or nonexistent activity. In any economy, collections will always be a part of a good end-to-end lending model. Combining collections revenue with stricter regulatory laws implicates that it is even more important than ever to have a mature, grounded collections strategy.

A significant challenge that lenders face today is striking the right balance between risk and reward. An imbalance in the risk/reward dynamic creates business stress, unprofitability, and loss of market share. The strength of an organization’s collection operation can impact the level of risk a lender can carry in its loan portfolio. A strategic and robust collection operation allows better loan portfolio management and operations. It cultivates a better customer engagement process and long term relationships.

The collection strategies adopted and implemented by banks and financial institutions also impact the brand and reputation of the businesses, impacting the overall profitability.

With the needs of the brand, customer experience, risk and bottom-line revenue, an adept collection strategy becomes pertinent for loan recovery and profitable portfolio management for organizations’ overall growth and customer relationship management.

An e�ective in-house collection strategy can increase revenue up to 15 percent* and decrease collection costs up to 25** percent through the more e�ective use of resources and sta�. In addition, implementing a collections strategy has shown to reduce default rates, protect the bottom line, find “lost” customers, and maintain customer relationships.

Following the 2008 financial crisis and the subsequent recession, consumers retreated heavily on debt. Growth rates in debt began to accelerate around 2012 and in 2016 about 90 percent of new debt came from auto and student loans, according to a Schlagenhauf and Ricketts report. CardHub calculates that the average American has about $7,879 in credit card debt. These rising Non-performing assets (NPA) are a concern for banks, fintechs, large financial institutions,regulators, and federal auditors likewise.

Mehlin, Lisa. “Collections: Leverage Analytics to Collect More, Increase Unit Yields and Spend Less to Do So.” PowerPoint presentation. First Data 2007 Fall Forum, October 9-11, 2007.

Ibid

*

**

Be it a business owner, accounts receivable manager, or the individual responsible for recovering your company’s unpaid debt, debt collection is pivotal for the profitability of the company. A poorly planned or executed collection strategy can contribute to poor cash flow, risk revenue, and impact growth. Therefore, the strategy for delinquent consumer and business-to-business debt needs to be one of the foremost action items in business planning.

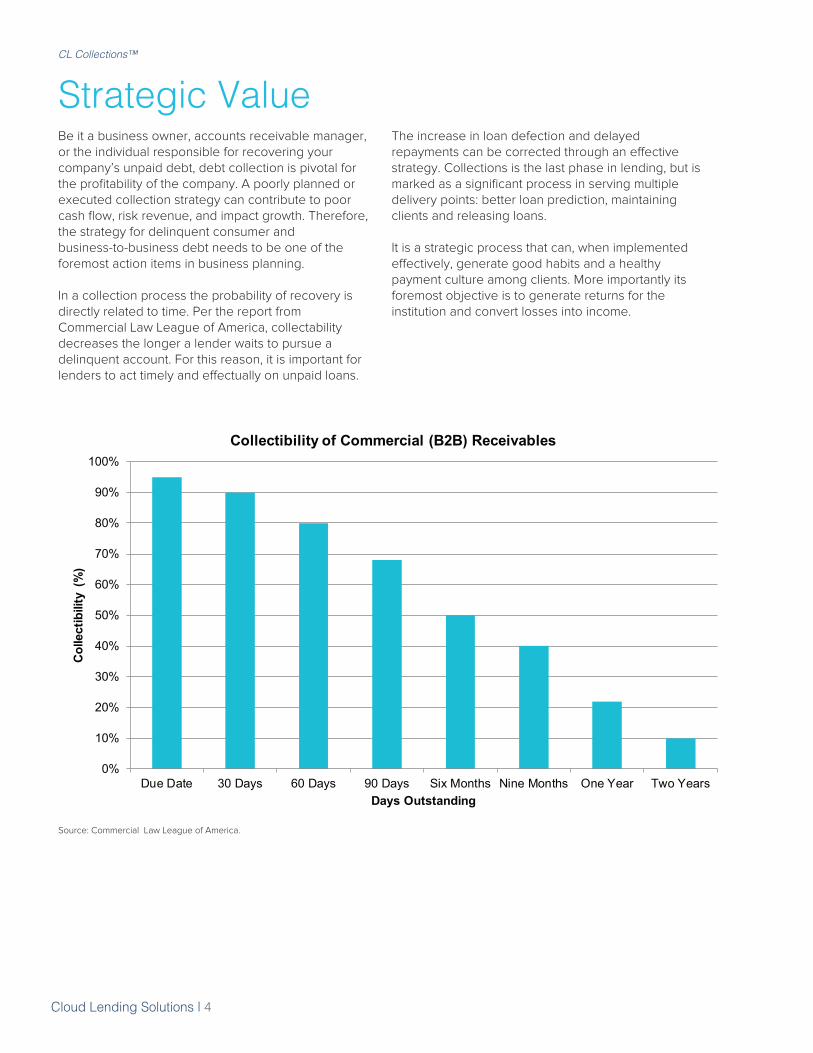

In a collection process the probability of recovery is directly related to time. Per the report from Commercial Law League of America, collectability decreases the longer a lender waits to pursue a delinquent account. For this reason, it is important for lenders to act timely and e�ectually on unpaid loans.

The increase in loan defection and delayed repayments can be corrected through an e�ective strategy. Collections is the last phase in lending, but is marked as a significant process in serving multiple delivery points: better loan prediction, maintaining clients and releasing loans.

It is a strategic process that can, when implemented e�ectively, generate good habits and a healthy payment culture among clients. More importantly its foremost objective is to generate returns for the institution and convert losses into income.

Strategic Value

Cloud Lending Solutions | 4

CL Collections™

Source: Commercial Law League of America.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Due Date 30 Days 60 Days 90 Days Six Months Nine Months One Year Two Years

Colle

ctib

ility

(%)

Days Outstanding

Collectibility of Commercial (B2B) Receivables

Align collections strategies with organizational strategies

Collection strategy should not be in isolation, rather it should be part of the overall organizational strategy. If organizational strategies are focused on a proactive customer experience with automation and an omnichannel experience, then the collection strategy needs to be proactive as well. When strategies are aligned the e�orts required in collection are reduced substantially and customer satisfaction and quality of engagement improve considerably.

In the wake of increasing debt trends and stricter regulatory laws from the FTC (Federal Trade Commission), Consumer Financial Protection Bureau (CFPB) and the Fair Debt Collections Practices Act (FDPCA), it is more important than ever to have a mature, grounded collections strategy. Adhering to the contact compliance requirements as per FDCPA, state laws and the Unfair, Deceptive or Abusive Acts or Practices (UDAAP) standard is not just recommended but is mandatory. A collection contact strategy should be flexible and considerate of customer preferences, while maintaining strict compliance with consumer protection regulations, including the Telephone Consumer Protection Act (TCPA). With regulators closely monitoring and employing a strict reign over the financial process, it becomes pertinent that collection processes are compliant and adhere to the subjected regulations.

Creating a streamlined workflow for the collection process is a significant step. For example, defining an activity matrix with automation for routine tasks and allowing more focus on value-added activities can optimize the collection process and create a more robust system. The automation of routine activities can aid in reducing cost and improving service delivery. Automated decisioning can eliminate bias and manual error, making the collection process objective and data driven. The time, e�ort and investment saved on that account can be utilized for more customer-focused operations.

Use data analytics to improve decision making

Streamline collections workflows and decisioning

As part of an end-to-end lending strategy, it is important that the collections solution is integrated with core lending systems as well as other productivity tools such as dialers, SMS and email systems. A service-oriented architecture enables a collection system integrated with other operational systems to be more configurable, easier to implement and highly flexible.

Service-oriented architecture (SOA)

With the advent of cloud technologies, the process of collection decision making can be improved measurably. By leveraging technologies like big data, machine learning, and 3rd party collection scoring models, strategies can align with predictive models to predict the ability to pay. Predictive modeling enables better risk analysis, more accurate delinquency probability and bad loan prediction. The predictive models can additionally create borrowers’ behavior profile which can aid in predicting future behavior and create a contact strategy for potential loss mitigation or settlement o�ers.

Customer-centric focus

The collection process should not be viewed as organizationally focused , rather the collection strategy should be designed with a customer centric approach to delivering better results. Customer-centric approaches include targeted customer communications and multiple borrower payment approaches to improve the customer experience and reduces collection cost. Additional approaches include maintaining a single source of record to track client interactions and ensure quality information to drive workflows, help ensure regulatory compliance and support agent-customer interactions.

Compliant collection process

Best Practices in Collection

5 | Cloud Lending Solutions

CL Collections™

In evaluating the the value and approaches in debt collection, it is important to look at the general phases in the collection process. As we established earlier, time is the most important factor in collections. The quicker the collections, the lower the costs and losses. The following collection phases are integral in well planned collection strategy.

Collection Phases

Cloud Lending Solutions | 6

CL Collections™

Customer, loan and payment data is important in evaluating and managing borrowers. Segmentation data

is used to define and execute a customer-centric collection strategy. Loans by region, value, asset type,

loan type and language as well as predictive and scoring models can all be used to run targeted, automated

communications, define queue priorities, and manage workload.

A written demand is the next route for contacting customer through a mailed notice for payment due. The written letter contains the details of the debt, expected payment date, and further consequences in case of missed payment. Written demand can be included and automated as part of an early-stage collection strategy.

If the negotiation doesn’t lead to any satisfactory agreement, a debt collection agency can be

consulted or the outstanding debt sold.

Driven by customer segment and contact strategy. E�ective collections should be focused on early contact using automation for early-stage self-cure collections, to be followed up with, the late-stage in-house collection e�orts.

Self Cure: By definition, self-cure represents the borrower being prompted into taking action on their own via automated communication through text, email or letter. This early-stage phase in a collections process has the lowest costs and highest returns. This might be as simple as a reminder that a bill is past-due, but can include communications that are the first steps to legal actions.

The negotiated end of the collection process between the borrower and lender. The debt is settled based upon agreement between the borrower and lender. Note, this is di�erent from debt restructure, for example, where new loan terms may be negotiated.

Phase 1

Phase 2

Phase 3

Phase 4

Phase 5

SEGMENTATION

WRITTEN DEMAND

CONTACT

SETTLEMENT IN FULL

DEBT COLLECTION AGENCY/SALE

In-house collections: In this late-state collection phase, specialized sta� is used to contact borrowers and work out payment. Data intelligence, workload management, work queues, recovery management and support systems are most important for e�cient implementations.

7 | Cloud Lending Solutions

CL Collections™

How Automation Can Optimize Collections

1

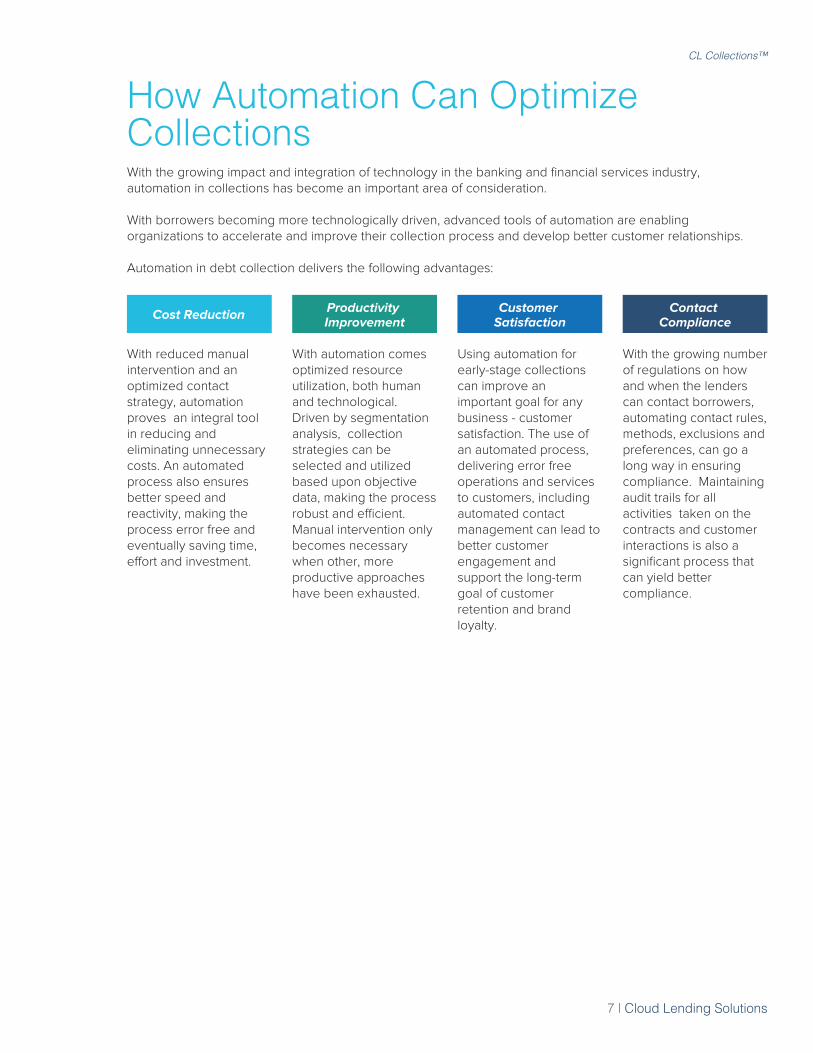

With the growing impact and integration of technology in the banking and financial services industry, automation in collections has become an important area of consideration.

With borrowers becoming more technologically driven, advanced tools of automation are enabling organizations to accelerate and improve their collection process and develop better customer relationships.

Automation in debt collection delivers the following advantages:

With reduced manual intervention and an optimized contact strategy, automation proves an integral tool in reducing and eliminating unnecessary costs. An automated process also ensures better speed and reactivity, making the process error free and eventually saving time, e�ort and investment.

With automation comes optimized resource utilization, both human and technological. Driven by segmentation analysis, collection strategies can be selected and utilized based upon objective data, making the process robust and e�cient. Manual intervention only becomes necessary when other, more productive approaches have been exhausted.

Using automation for early-stage collections can improve an important goal for any business - customer satisfaction. The use of an automated process, delivering error free operations and services to customers, including automated contact management can lead to better customer engagement and support the long-term goal of customer retention and brand loyalty.

With the growing number of regulations on how and when the lenders can contact borrowers, automating contact rules, methods, exclusions and preferences, can go a long way in ensuring compliance. Maintaining audit trails for all activities taken on the contracts and customer interactions is also a significant process that can yield better compliance.

4

Cost ReductionProductivity Improvement

Customer Satisfaction

Contact Compliance

Cloud Lending Solutions | 8

CL Collections™

Implementing Collection Processes

IMPLEMENTING COLLECTION PROCESSES

Single System of Record

Segmentation

With the advent of fintech in lending process, collections can be more precise, streamlined and data driven. Automation in collections is very productive, can increase accuracy, and reduce cost. Still, the significance of an e�ective and e�cient implementation of collection process should be of the highest priority.

In a practical collection process, having access to a 360° view of the customer is important. A single system of record increases transparency and clarity in the decision making and improves the ability to support automated, customer-centric collection strategies.

Contact ManagementAutomated contact management helps in maintaining

compliance with appropriate laws. A contact management system can ensure better tracking of logged complaints,

monitor complaint status, and manage contact preferences along with communication thresholds. It can also help in

automating and setting up payment arrangements, collecting payments, tracking promise to payments.This helps in the long

run by ensuring better customer service delivery and relationship management.

Segmenting customers based upon loan type, region, language, asset type and loan value or even a wider set of variables including

payment history, credit data, default rate, and credit bureau

score, helps in defining a targeted strategy. This creates a

better alignment of the contact strategy and higher collection

rates.

Automated StrategyUsing workflow tools allows for the automation of the collection strategy. Workflows are created based on the segmentation data to ensure the correct approach is used by customer to optimize collections. Workflows can define automated processes to implement required notifications or to e�ciently manage time and workload for the collections team.

Workload ManagementCollector’s workload needs to be optimized on a daily basis. This is primarily done through managing assignments and reassignments

in work queues. A collector’s workload, sta�ng changes,

collection surges, cross-queue, permanent as well as temporary assignments, are all factors that

need to be managed.

Managing a typical extended collection process does not have to be expensive or labor intensive. With the focus on optimizing and automating the collection process, tangible returns can be achieved.

Lenders need a technology solution for automating and organizing their collection strategies that keeps track of delinquencies and o�ers visibility into the collection process.

CL Collections™ is a customer-centric collections application that enables lenders to define and automate collection strategies, optimize customer interaction across channels, lower risk and reduce technical and operational costs. With CL Collections you can track customer interactions, set priorities and optimize workloads. CL Collections can be used independently or as part of Cloud Lending Solutions’ end-to-end loan, leasing and marketplace solutions.

CL Collection is a solution used to manage both early and late stage collection process:

Manage early stage collection: E�ective contact management integrated in CL Collection system ensures consistent communications based on contact preferences and communication thresholds. It o�ers a self-cure option to the borrower prompting them to taking action via automated communication through text, email or letter.

Manage late stage collections: CL Collection implements data intelligence, workload management, work queues and support systems through managing assignments and reassignments taking into account acollector’s workload, sta�ng changes and surges.

CL Collections™

How CL Collections™ Can Supercharge Your Collections Strategy

9 | Cloud Lending Solutions

Key Features in CL Collections include:

Collection Strategies

Queue Management

CL Collections allows for the configuration of automated collection emails, queue assignments, dunning letters and SMS communications defined for a lender’s entire portfolio or by customer segment. Collection strategies are used in CL Collection to manage the workflow for both contact automation and collector queues.

Collection queues can be setup for in a number of di�erent ways. Collectors can be individually assigned to queues on a fixed, temporary or permanent bases. Delinquent contracts can be assigned to a queue based on any criteria such as loan type, size or collectability and executed as part of a collection strategy workflow based upon criteria such as days delinquent.

Contact automation defines what actions, whether emails or SMS are to be executed when and on what conditions

Work queues are assigned and managed by specific action criteria in a collection strategy. Work queues are used by collectors to prioritize collections using the collector’ dashboard

Collection Strategies

Configuration

Reporting

Service Oriented Architecture

CollectorDashboard

Queue Management

Workload Management

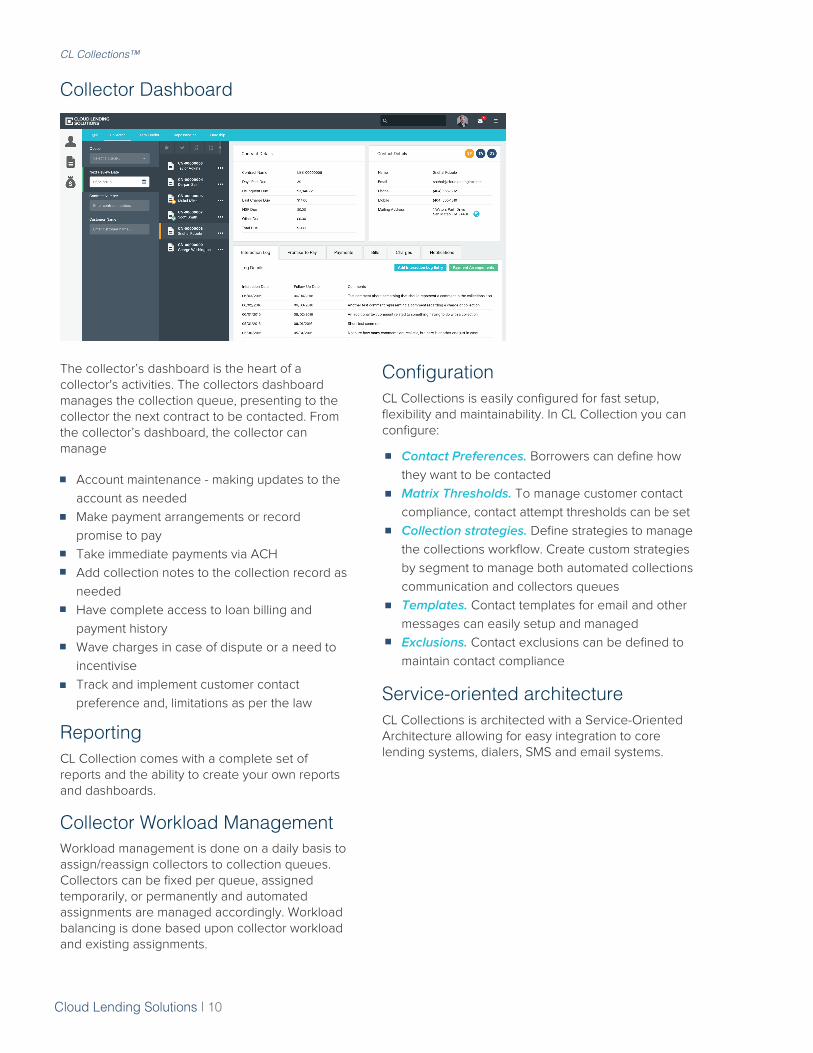

CL Collections is architected with a Service-Oriented Architecture allowing for easy integration to core lending systems, dialers, SMS and email systems.

Service-oriented architecture

CL Collections™

Collector Dashboard

Cloud Lending Solutions | 10

The collector’s dashboard is the heart of a collector's activities. The collectors dashboard manages the collection queue, presenting to the collector the next contract to be contacted. From the collector’s dashboard, the collector can manage

ReportingCL Collection comes with a complete set of reports and the ability to create your own reports and dashboards.

Workload management is done on a daily basis to assign/reassign collectors to collection queues. Collectors can be fixed per queue, assigned temporarily, or permanently and automated assignments are managed accordingly. Workload balancing is done based upon collector workload and existing assignments.

Account maintenance - making updates to the

account as needed

Make payment arrangements or record

promise to pay

Take immediate payments via ACH

Add collection notes to the collection record as

needed

Have complete access to loan billing and

payment history

Wave charges in case of dispute or a need to

incentivise

Track and implement customer contact

preference and, limitations as per the law

CL Collections is easily configured for fast setup, flexibility and maintainability. In CL Collection you can configure:

Configuration

Contact Preferences. Borrowers can define how

they want to be contacted

Matrix Thresholds. To manage customer contact

compliance, contact attempt thresholds can be set

Collection strategies. Define strategies to manage

the collections workflow. Create custom strategies

by segment to manage both automated collections

communication and collectors queues

Templates. Contact templates for email and other

messages can easily setup and managed

Exclusions. Contact exclusions can be defined to

maintain contact compliance

Collector Workload Management

Automated collection strategies reduces cost and e�ort

Complete record of billing and collection interactions eliminate servicing errors

Configurable collection strategies reduces cost and e�ort

Benefits

Benefits$

CL Collections™

A successful collection strategy relies heavily on using technology to achieve a customer-centric and compliant collection process. With the focus on streamlining collections and lowering costs, financial organization are updating their collection processes to achieve these better returns.

CL Collections™ is designed to meet these collection challenges with a technology strategy that supports best practices by supporting organizational objectives through the ability to configure collection strategies directly in the system.

Through CL Collections Single System of Record, data analytics and segmentation can be used to dive a customer-centric collection process along with a collector-centric approach to dashboards, collector queues and workload management functions.

Through the highly configurable architecture, customer contact compliance can be supported along with the ability to configure and automate a large number of customer interactions. Through a service-oriented architecture, CL Collections, it is easy to integrate with core systems or other productivity tools.

To learn more about CL Collections visit www.cloudlendinginc.com

Summary

11 | Cloud Lending Solutions

Contact preferences support contact compliance

Streamline customer interaction improving customer experience

About Cloud Lending Solutions

+1-(650) 918-0499 | [email protected] | www.cloudlendinginc.com | Social Media

Cloud Lending Solutions is a financial services technology company o�ering a cloud-based, end-to-end lending platform to deliver

innovation to the global lending community. Unlike legacy technology platforms that are expensive to maintain and prevent agile

response to market conditions, Cloud Lending Solutions’ clients take back control of their business by quickly implementing, extending,

and digitizing the entire lending lifecycle. Cloud Lending Solutions’ single system of record is the market leading cloud solution supporting

both consumer and commercial lending that scales for the needs of lenders of all sizes. Clients include banks, traditional finance

companies, online lenders, and marketplace platforms.