Embed Size (px)

Citation preview

The innovation imperative

The rapid pace of change in technology and its adoption is fundamentally altering the entire value chain – from what arouses customer interest in the first place to how the completed sale is paid for and settled. Innovation and disruption are not new topics. However, what is new are the immediacy and the magnitude with which they have hit the Australian banking system between the eyes in 2014. Technological change has been an integral component of the banking landscape for many decades, but when we draw all the lines together, 2014-15 is the years that there has been awakening in the banking system to the change required to leap into a new digital banking future.

Digital Disruption*

Disruption is occurring outside the banking industry at a rapid pace. In areas such as payments global players such as Google Wallet, Apple Pay, Square and Amazon are having a significant impact. Locally, we have seen the emergence of Fin Techs and startups such as P2P lender SocietyOne, payment provider Tryo Payments and foreign exchange platform provider OzForex. Disruption brings a validation for banks to disrupt themselves or defend the value.

Disrupting oneself can bring benefits of cost reduction in using the platforms and partners of highest value. For example, cloud services or startups providing non-core services like security and video ATMs. Disruption also brings the opportunity for banks to leverage other ecosystems or create their own, much like eBay which does not compete with bricks and mortar retailers but gives them another channel by listing on eBay. One of the banks could enable a peer to peer payment service for Facebook users to use globally.

Facebook drives a significant amount of mobile app downloads that banks can embrace to drive their businesses. Thirteen million people in Australia engage with Facebook every month and 11 million engage each day. The majority of bank customers and prospects return to the platform 14 times per day on average. This immense engagement provides a canvas for the banks to efficiently connect with all of these people to drive results.

Consider the objective of increasing the average product per customer. Then consider the fact that a very high proportion of bank customers are looking at Facebook on a smartphone 14 times per day on average. This may provide the single most effective opportunity to connect customer data with the Facebook audience to drive an increase in product adoption and share of wallet.

The major disrupting areas will be:

Cloud Mobile Social Media Customer Analytics

* Source - pwc.com.au 1

What are the IT demands?

Life has never been simple for IT leaders, but these days, complexity is shifting into high gear. The demands on IT are more intense than ever. While many organizations express basic satisfaction with their own IT departments, new hurdles face IT executives as business units are demanding more value from the function. Banks are pressing IT executives for gains from transformational technologies like cloud computing, and they want IT to help turn growing stores of corporate data into information assets that support growth and guide innovation. And all this is playing out in a more challenging IT environment as competitors wield new technologies to wrest competitive gains and shape new product offerings.

Coping with competitive demands:

Technology, undeniably, is changing competitive dynamics. It is actually a double-edged sword: IT is both a competitive weapon and a source of disruption when used by competitors. Bank IT executives say their companies are most vulnerable to two technology-enabled threats: rising customer expectations and significant changes in delivery costs. As companies begin to consider a return to growth, two other concerns leapt up: the emergence of new products or services from competitors and competitors’ development of new offerings outside their current scope.

Managing the future:

Banks IT department cite new demands and expanded mandates related to two increasingly important technology-based innovations: integrating data and analytics more completely into business decisions, and taking greater advantage of emerging cloud computing platforms. Business intelligence and analytics are changing the way banks make decisions. Bank management says the business processes and decisions within their spheres of influence are becoming more data driven. They also believe this trend is spreading more broadly throughout the bank. Banks who have incorporated data and analytics into their decision making say the most significant benefits are the discovery of new insights, significantly improved projections of future performance, and faster decision making. Despite optimism about the rising use of data in decision making, bank management also highlight a number of barriers to expanding adoption.

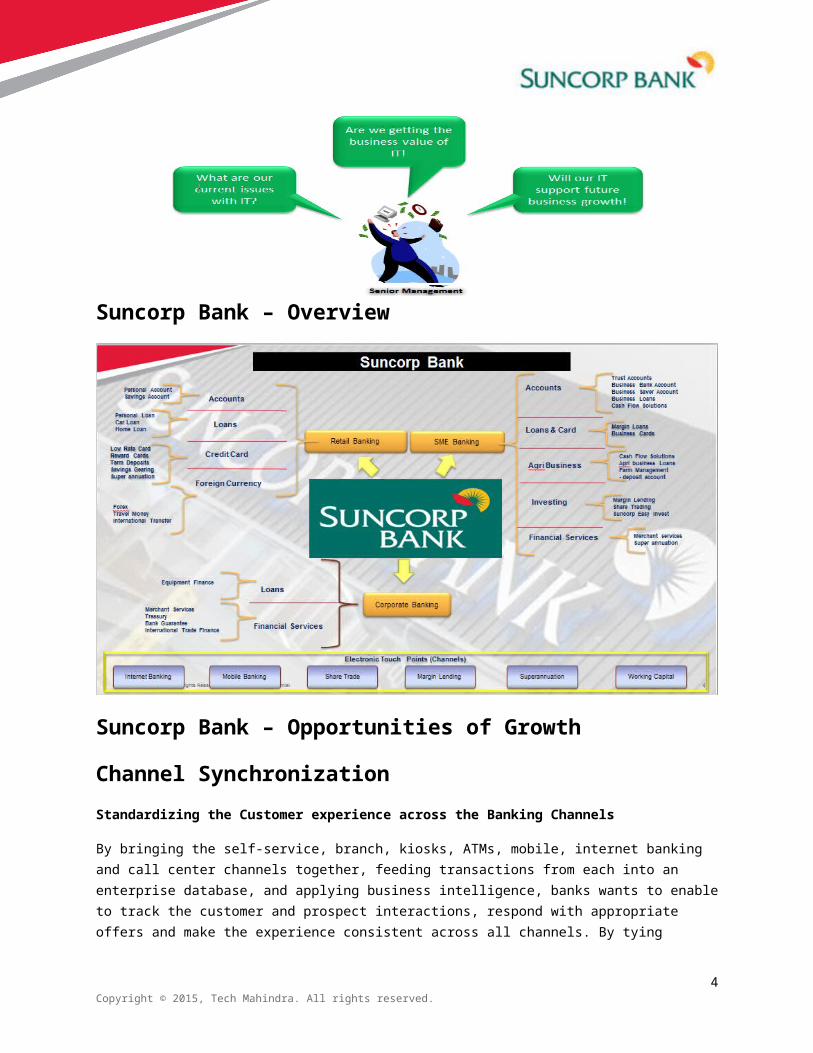

Suncorp Bank – Overview

2Copyright © 2015, Tech Mahindra. All rights reserved.

Suncorp Bank – Opportunities of Growth

Channel Synchronization

Standardizing the Customer experience across the Banking Channels

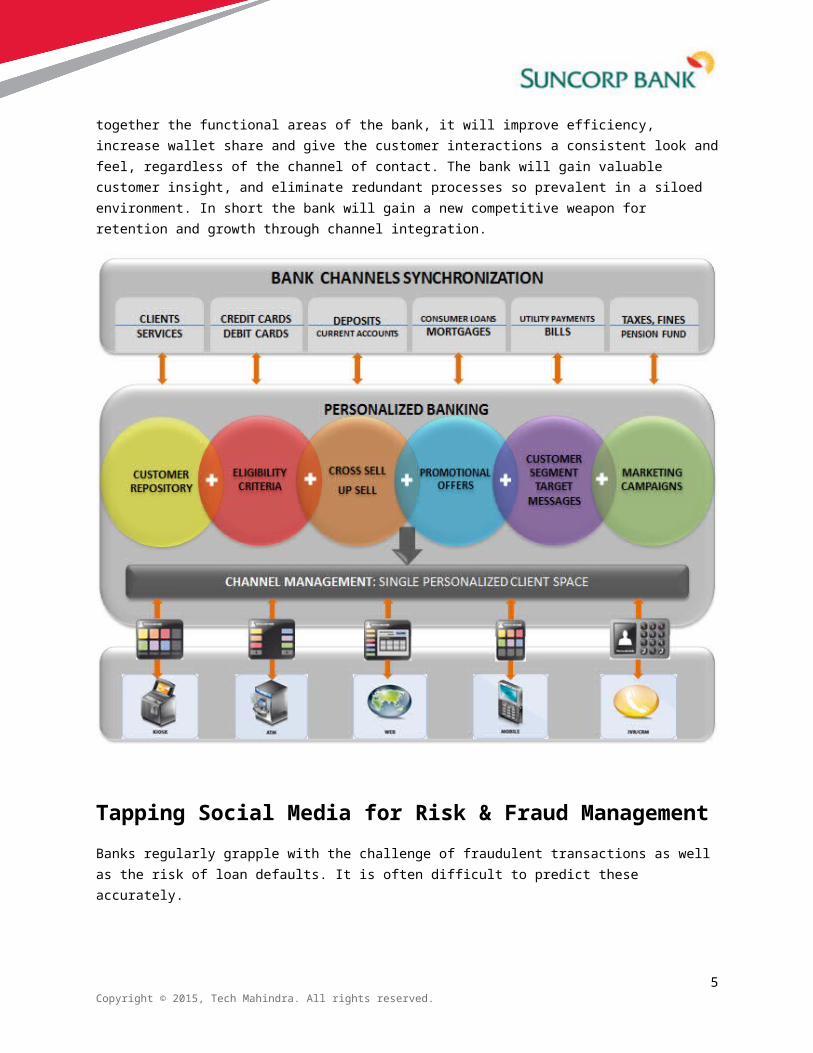

By bringing the self-service, branch, kiosks, ATMs, mobile, internet banking and call center channels together, feeding transactions from each into an enterprise database, and applying business intelligence, banks wants to enable to track the customer and prospect interactions, respond with appropriate offers and make the experience consistent across all channels. By tying together the functional areas of the bank, it will improve efficiency, increase wallet share and give the customer interactions a consistent look and feel, regardless of the channel of contact. The bank will gain valuable customer insight, and eliminate redundant processes so prevalent in a siloed environment. In short the bank will gain a new competitive weapon for retention and growth through channel integration.

3Copyright © 2015, Tech Mahindra. All rights reserved.

Tapping Social Media for Risk & Fraud Management

Banks regularly grapple with the challenge of fraudulent transactions as well as the risk of loan defaults. It is often difficult to predict these accurately.

Social media, used the right way, can be a very useful ally here. By engaging with customers on social media and developing a better understanding of the customer’s social transactions and behavioural patterns, the bank puts itself in a much better position to predict the risk of loan default as also the possibility of a fraudulent transaction.

4Copyright © 2015, Tech Mahindra. All rights reserved.

Social Media Tapping – Sentiment Analysis

Customers are spending increasingly more time on social media, consuming and creating data, connecting, airing views forming groups. Tapping into these data streams can help Suncorp bank identify customer preferences, test new products, and create better targeted products.

This requires the ability to analyze a large volume of unstructured data, through multiple data streams. Traditional tools fail to cope with the variety, volume and velocity of social data. The BI platform first creates a context using traditional data then overlays social profile data on top of it followed by continuous social streaming data. This delivers highly accurate contextual sentiment analysis ideal for quick sentiment capture as well as behavioural targeting.

5Copyright © 2015, Tech Mahindra. All rights reserved.

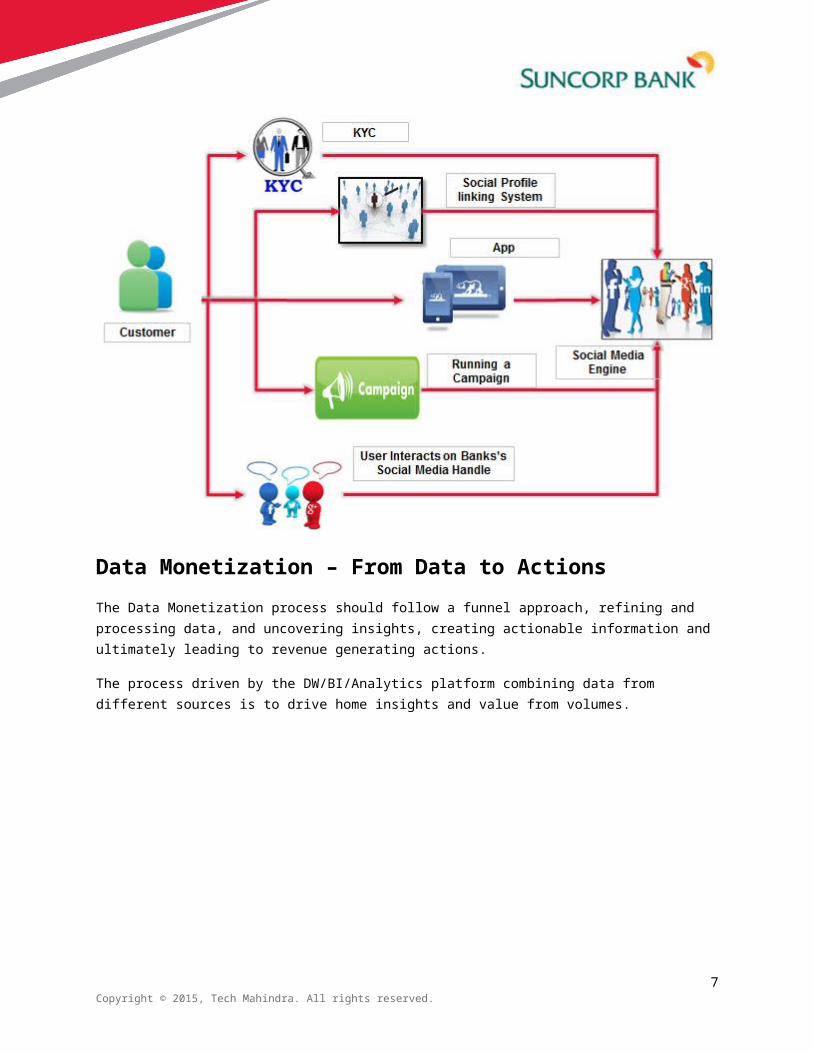

Data Monetization – From Data to Actions

The Data Monetization process should follow a funnel approach, refining and processing data, and uncovering insights, creating actionable information and ultimately leading to revenue generating actions.

The process driven by the DW/BI/Analytics platform combining data from different sources is to drive home insights and value from volumes.

6Copyright © 2015, Tech Mahindra. All rights reserved.

7Copyright © 2015, Tech Mahindra. All rights reserved.