Embed Size (px)

Citation preview

Corporate presentation 2017 1

Corporate presentation 2017AGRANA Beteiligungs-AG

S U G A RS TA R C HF R U I TThe natura l upgrade

Corporate presentation 2017 2

OVERVIEW

About us

AGRANA-products in daily life

Strategy

Production sites

Group- & ownership structure

History

Financials

Investment

Segment SUGAR

Segment STARCHSegment FRUIT

Research & Development

Sustainability

Economic footprint

Business figures 2016|17

Outlook

1

2

3

4

5

6

7 15

12

13

9

10

11

8

14

16

Corporate presentation 2017 3

ABOUT US

We refine agricultural raw materials, turning them into a range of different industrial products to supply local producers as well as large multinational companies active in the food processing industry, in particular

We also serve the end-consumer market in the Sugar segment with country-specific brands such as „Wiener Zucker“ in Austria

AGRANA FACTS

8,900employees

57production

sites2.6 €bn

revenue

Leading

SUGAR SUPPLIERIn Central, Eastern & South-Eastern Europe

Major manufacturer of customer-specific

STARCHPRODUCTS

World market leaderin the production of

FRUITPREPARATIONS

Corporate presentation 2017 4

WE ALL CONSUME AGRANA (PRODUCTS)STRATEGIC POSITIONING B2B

At the beginning there is always agriculture…

AGRANA refines agricultural raw

materials...

AGRANA supplies the Big Names...

We all consume AGRANA every

day...

confectionery, beverage, fermentation industries, food retailers; paper,

textile, pharmaceutical industries; feed industry; dairy, ice-cream, bakery

industries and many more

Corporate presentation 2017 5

AT A GLANCEAGRANA-PRODUCTS IN DAILY LIFE

SUGAR STARCH FRUIT

for consumers: „Wiener Zucker“ (20%) for food producers:

e.g. for pastries, confectionery, dairy products, preserves, drinks etc. (80%)

as food ingredients, e.g. forsauces, potato products etc. as child and infant food for cosmetic products for technical applications, e.g.

for paper finishing as animal feeds for bioethanol

fruit preparations in dairyproducts, ice-cream, in baked goods or as fruitdecoration fruit juice concentrates in

soft drinks and alcoholicbeverages

Corporate presentation 2017 6

STRATEGYREFINING OF AGRICULTURAL RAW MATERIALS

SUGARCENTRAL & EASTERN EUROPE

FRUITGLOBAL

STARCHEUROPE

SynergiesUse synergies between business segments to position the Group optimally for the increasingly volatile operating environment in the segments

Customer- and market-oriented growth in CEE and

Southeastern Europe

Organic growth, and adding value by tailor-made products

Customer- and market-oriented global growth

Capital marketA long-term asset for shareholders

Investors & Customers Balance of risk, exchange of know-how between the segments, cost savings through synergies

Corporate presentation 2017 7

57 PRODUCTION SITES WORLDWIDEINTERNATIONAL PRODUCTION MEETS INT. CUSTOMERS

Austria

Czech Rep.

Hungary*Romania

Slovakia

Bosnia-Herzegovina Bulgaria

SUGAR7 sugar beet plants2 raw sugar refineries & Instantina plant

Countries with production sitesMain marketsStarch plantsBioethanol plants

Beet sugar plantsRaw sugar refinery

Countries with plantsOther markets

* Also with refiningactivities

FRUIT28 fruit preparation plants and14 fruit concentrate plants

Distribution centre Potential Growth RegionsCountries with production sites

STARCH5 starch plants (incl. 2 bioethanol plants)

Corporate presentation 2017 8

AGRANA IS PROCESSING 10 MILLION TONNES OF RAW MATERIALS

6.70.2

1.9

0.3 0.9

Beet Raw sugar Grain Potato Fruits

Including 50% of the JVs HUNGRANA and STUDEN

million tonnes

Corporate presentation 2017 9

AGRANA IS SELLING 5.4 MILLION TONNES OF HIGH-QUALITY PRODUCTS

2.2

2.4

0.8

Sugar Starch Fruit

Including 50% of the JVs HUNGRANA and STUDEN

million tonnes

1.3 m tonnes of core products Sugar Sugar speciality products (Quota and non-quota sugar)

0.9 m tonnes of by-products + other Feedstuffs & fertilisers Molasses, beet pulp…

1.2 m tonnes of core products Native starches Modified starches Saccharification products Alcohol and ethanol

0.7 m tonnes of by-products Feedstuffs & fertilisers Proteins (incl. DDGS / ActiProt©) Corn germ / mash

0.5 m tonnes of other products Soy Dried beet pulp

0.7 m tonnes of core products Fruit preparations (dairy and non-dairy Fruit juice concentrates Other juice core products (NFC, fruit

wine

0.07 m tonnes of by-products/other Particularly pomace Natural flavours, beverage bases

Sugar 41%Sugar 41%Starch 45%Starch 45%

Fruit 14%Fruit 14%

Corporate presentation 2017 10

GROUP STRUCTURE

AGRANA Internationale Verwaltungs-& Asset Management GmbH

AGRANA Stärke GmbHAGRANA Zucker GmbH

42 sites5,761 employees1,155.5 €m revenue

10 sites2,135 employees671.9 €m revenue

5 sites974 employees733.9 €m revenue

57 sites8,870 employees2.6 €bn revenue

FRUITSUGAR STARCH

AGRANA Beteiligungs-AG

Corporate presentation 2017 11

OWNERSHIP STRUCTURE

~78.4%

TOTAL: 15,622,244 shares

Z & SZucker und Stärke

Holding AG

ZBG

Südzucker

RübenproduzentenBeteiligungs-GmbH

Raiffeisen-HoldingNÖ-Wien

~50%

~70%

~30%

~10% ~50%

~2.7%1

~18.9%

1 directly held by Südzucker

Corporate presentation 2017 12

HISTORYOUR

1988 1989 1990 1991 2012 201320082003 2010 - 2011 2014

FOUNDINGof AGRANA Beteiligungs-AG

PARTNER-SHIPwith Germany‘sSüdzucker AG

INITIAL PUBLIC OFFERING (IPO)of AGRANA Beteiligungs-AG

OPENINGOf the bioethanol facility in Pischelsdorf|Austria

MERGERof AGRANA JuiceHolding GmbH andYbbstaler Juice AustriaGmbH and the launchof the new brandAUSTRIA JUICE

OPENINGof the new AGRANAResearch & Innovation Center (ARIC) in Tulln|Austria

50% ACQUISITIONIn the Hungarian cornstarch und Isoglucose millHUNGRANA

DEVELOPMENTof the third businesssegment, Fruit, with theareas of fruitpreparations and fruitjuice concentrates

OPENINGof the wheat starch plant in Pischelsdorf|Austria

EXPANSIONof the company‘s presencein the area of fruitpreparations in the MiddleEast and Africa with plantsin Cairo|Egypt andJohannesburg|South Africa

EXPANSION of the Sugar andStarch segments by means ofacquisitions in Bosnia-Herzegovina, Bulgaria, Romania, Slovakia, Czech Republic andHungary

EXPANSIONof the company‘s presence in the area of fruit

preparations with a fourth US-plant in Lysander|USA

2015

OPENINGof packagingstock andlogistics hub in Kaposvár|HU

2016 2017

EXPANSIONof market position in South Americathrough theacquisition of 100% ofthe share in Main Process S.A., a producer of fruitpreparations in Buenos Aires

EXPANSIONOf market position in Asia through theacquisition of theIndian fruit processingplant SAIKRUPA FruitProcessing Pvt. Ltd.

Corporate presentation 2017 13

SOLID ECONOMIC GROWTHSINCE 1988

Revenue EBIT

355.8

24.7

467.6684.6

866.4

2,026.3

42.276.8

34.6

CAGR Revenue: 7.0 % CAGR EBIT: 6.9 %

€m

15.0

2,561.3

172.4

Annual growth rates:2,841.7

166.9

Corporate presentation 2017 14

STEADY DIVIDEND POLICY

4.00

3.00

2.00

1.00

0

€

*Dividend proposal to the AGM on 7 July 2017: € 4.00 per share

0

20

40

60

80

100

120

140

AGRANA share price Dividend per share

Performance (10 July 1991 – 23 May 2017): AGRANA +119.09% (last: € 101.90)

*

Corporate presentation 2017 15

REVENUE-, EBIT- AND MARGIN DEVELOPMENT

2009-2017

REVENUE

EBIT-MARGIN

EBIT

* The prior-year data have been restated under IAS 8.

1.989,2 2.165,9

2.577,6

3.065,92.841,7

86,9

128,6

231,0 217,9166,9

121,7 129,0 172,4

2.493,5 2.477,6

4,4 %

9,0 %7,1 %

5,9 % 5,2 %

in M

io. €

5,9 % 4,9 %

2.561,3

6,7 %

Corporate presentation 2017 16

INVESTMENT DEVELOPMENT

*equity-method

SUGARSTARCHFRUITGROUP

25.355.9 43.1 34.5 46.1

23,3

29.3

59.1

35.0

13.7

28.257,6

42.5

34.8

51.8

43.0

41.7 33,8

0

20

40

60

80

100

120

140

160

2011|12 2012|13 2013|14 2014|15* 2015|16* 2016|17*

€m

149.8

97.1

130.0

91.2

116.0 114.7

Corporate presentation 2017 17

INVESTMENT OVERVIEW2016|17

46.1

23.3

28.257.6

41.733.8

2015|16 2016|17

Sugar Starch Fruit

116.0 2016|17

SUGAR General overhaul of the high-bay warehouse in Tulln, Austria Renewal of the fresh water treatment in Tulln, Austria Construction of the pelleted dried beet bagging station in

Leopoldsdorf, Austria

STARCH Expansion of corn processing in Aschach, Austria Expansion of starch saccharification facilities in Aschach, Austria Construction of a new maltodextrin spray drying plant in Aschach,

Austria

FRUIT Construction of a third production line in Lysander, New York, USA Installation of a bag-in-box packaging in Botkins, Ohio, USA Installation of a new production line in Mitry-Mory, France

€m

114.7

GROUP

Corporate presentation 2017 18

SUGARSEGMENT

18

Corporate presentation 2017 19

SUGAR SEGMENT

Sugar: is obtained from sugar beet without any additives pure, natural product

is a natural provider of energy as part of a balanced diet

AGRANA: market leader in Austria and top provider in Eastern and South-Eastern Europe

Close partnerships with sugar beet growers: AGRANA offers wide range of advice on growing sugar beet

End-consumer-market is served with country-specific brands

Europe’s largest producer of organic sugar: ‘Wiener Bio Kristall- und Staubzucker’: sugar made

from organically grown Austrian beet

Corporate presentation 2017 20

AGRANA SUGARBENEFIT FROM THE STRONG MARKET POSITION IN CEE AND SEE

7 SUGAR PLANTS AND2 RAW SUGAR REFINERIES

Austria

Czech Rep.

Hungary*

Romania

Slovakia

Bosnia-Herzegovina

Bulgaria

Beet sugar plants

Raw sugar refinery

Countries with plants

Other markets

* Also with refining activities

Distribution centre

Corporate presentation 2017 21

SUGAR SEGMENT

Maintenance of regional products…

....and specialty products

Corporate presentation 2017 22

STARCHSEGMENT

Corporate presentation 2017 23

STARCH SEGMENT

Processing and refinement of top-quality corn, wheat and potatoes to create a variety of different, highly refined starch products

Manufacture of products made of valuable raw materials at the highest quality level, using modern, environmentally friendly methods

Starch and special starch products (e.g. organic and GMO free starch) to numerous industrial sectors: food and beverage industries baby food industry paper and paper processing industry textile industry construction chemicals industry pharmaceutical and cosmetic industries

Corporate presentation 2017 24

MARKET POSITIONSTARCH SEGMENT

Austrian production sites: potato starch factory in Gmünd|AUT corn starch plant in Aschach|AUT Bioethanol & wheat starch plant in

Pischelsdorf|AUT

AGRANA Stärke GmbH: operational management and coordination of international holdings in Hungary and Romania

Focus on highly refined speciality products Innovative, customer-driven products supported

by application advice Leading position in organic and in GMO-free

starches for the food industry Bioethanol business: part of the Starch segment

STARCH

5 starch plants (incl. 2 bioethanol plants)

Countries with production sites

Main markets

Starch plants

Bioethanol plants

Corporate presentation 2017 25

FRUITSEGMENT

Corporate presentation 2017 26

FRUIT SEGMENT Processing of fruit in the gentlest way possible,

applying state-of-the-art production processes. Refinement of fruit into top quality fruit preparations and fruit juice concentrates

fruit juice concentrate business: operated by AUSTRIA JUICE (formerly Ybbstaler) as a joint venture between AGRANA and RWA (Raiffeisen Ware Austria AG)

AGRANA Fruit … is the global market leader in producing fruit

preparations for the dairy, baking and ice-cream industries

is a leading producer of fruit juice concentrates in Europe and

has established a global presence based on its production facilities and international sales activities

Corporate presentation 2017 27

28 FRUIT PREPARATION PLANTS &14 FRUIT JUICE CONCENTRATE PLANTS

Potential Growth Regions

Countries with production sites

MARKET POSITIONFRUIT SEGMENT

World Market Leader in Fruit preparations: global market share > 30%

Currently: Europe: stagnating market’s sales volumes of fruit

preparations in Europe at a high absolute level good market growth rates in the Asia-Pacific region

Most important producer of fruit juice concentrates in Europe (AUSTRIA JUICE)

Additional customer portfolio and new markets Optimisation measures taken in previous years show

their positive effects

FRUIT PREPARATIONS

FRUIT JUICE CONCENTRATES

Corporate presentation 2017 28

FRUIT PREPARATION – WHAT IS IT ABOUT?

+ =

… most important ingredient of fruit preparations Frozen (IQF or block) Aseptic Purees Concentrates

… sweetens and supports taste anddurability Crystal sugar Liquid sugar (syrup) Other sweeteners

create a good mouth-feel and prevent emulsions

Pectins Starch Guar, Xanthan, …

optional flavors and coloursfor an even fruitier taste and an intense colour

THICKENERS

FRUIT SUGAR FRUIT PREPARATIONS

Corporate presentation 2017 29

RESEARCH & DEVELOPMENTAGRANA RESEARCH & INNOVATION CENTER

Bundling of all R&D activities at ARIC in Tulln|AUT

Synergies in crossdivisional research topics:Clean Label / Nutrition / Sweeteners / Flavors

Networking with other research institutions

Aim: to secure and actively shape the company’s success in the future through innovations: product innovations innovations related to our processes and production

technology

State-accredited testing unit for yield and quality evaluation of sugar beets

Specialised R&D expertise is also made available to third parties

AGRANA Research & Innovation Center (ARIC)

Corporate presentation 2017 30

AGRANA‘S UNDERSTANDING OF SUSTAINABILITY

utilise almost 100% of our raw materials and employ low-emission technologies to protect the environment,

respect all our stakeholders and the communities where we operate,

engage in long-term partnerships.

At AGRANA, we …

Balance of economic, environmental and social responsibility

Corporate presentation 2017 31

AGRANA‘S CORE SUBJECTS ALONG THE VALUE CHAIN

Labour practices and human rights of employees

Product responsibility

and sustainable products

Compliance and business

conduct

Social engagement

Environmental and energy aspects of production

Environmental and social

criteria in the sourcing of agricultural

raw materials

Sustainability Reporting:Acc. to GRI integrated in AGRANA‘s annual reports since 2012|13

Corporate presentation 2017 32

SUSTAINABLE AGRICULTURE INITIATIVE (SAI)

ENVIRONMENTAL AND SOCIAL CRITERIA IN THE SOURCING OF AGRICULTURAL RAW MATERIALS

SAI is an initiative of stakeholders of the food industry, founded in 2002 by Nestlé, Unilever and Danone.

SAI develops principles and practices of sustainable agriculture

SAI‘s 2 major tools to document sustainable environmental and social practices in the agricultural value chain Farm Sustainability Assessment (FSA) Benchmarking Tool for international certification

standards & national legislation

AGRANA has been a member of SAI since 2014 and uses the FSA questionnaire to assess contract growers and the benchmarking tool in all its business segments

Farm Sustainability Assessment (FSA) & Benchmarking Tool

FSA is a questionnaire (applicable worldwide), that enables agricultural producers to assess the status of their operations in terms of environmentally and socially sustainable production (112 questions on farm management, soil and nutrient management as well as plant protection).

The benchmarking tool compares requirements of internat. certification standards with the requirements of the FSA-questionnaire

Corporate presentation 2017 33

SUSTAINABILITY AT AGRANAMEASURES IN THE CORE BUSINESS

• 2014: Introduction of an energy-management-system in all Austrian production plants and certification according to ISO 50001; CEE sites as of 2015|16

• Low temperature dryers installed at the Tulln & Leopoldsdorf site, both Austria, have saved more than 100,000 tonnes CO2equ. since their installation in 2011|12

• Target: energy-self-sufficient in terms of figures of the sugarplant Kaposvár|HU

The Kaposvár sugar plant in Hungary generated about 30 million cubicmetres of biogas from beet pulp in the 2016|17 financial year. This wouldhave been sufficient for the site:

to cover 80% of its primary energy requirement for the 2016|17 beetcampaign, or

60% of its total primary energy needs for beet processing and therefining of raw sugar

about 8.3 million cubic metres of the biogas produced at the facilitywere refined by the biogas upgrading plant installed in 2015 intoapproximately 4.9 million cubic metres of biomethane for feeding intothe local natural gas grid and this was equivalent to the annual heatingrequirement of about 1,950 single-family homes

ENERGY EFFICIENCYTargets 2020|21

Sugar (baseline 2013|14):

• 5% reduction of direct energy / tonne of core- & by-products

Starch (baseline 2013|14): • 50 GWh (all measures

summed up) reduction of energy consumption until 2020|21

Fruit (baseline 2014|15):• 6.8% reduction of total

energy consumption / tonne of fruit preparation (baseline 2013|14)

• Hold energy use per tonne of fruit juice concentrate & by-products constant at 2014|15 baseline

Corporate presentation 2017 34

SUSTAINABILITY AT AGRANAMEASURES IN THE CORE BUSINESS

Almost complete (98.6 to 99.9%) of raw materials use in all segments through the efficient use of raw materials technical innovations and product development (main & by-products)

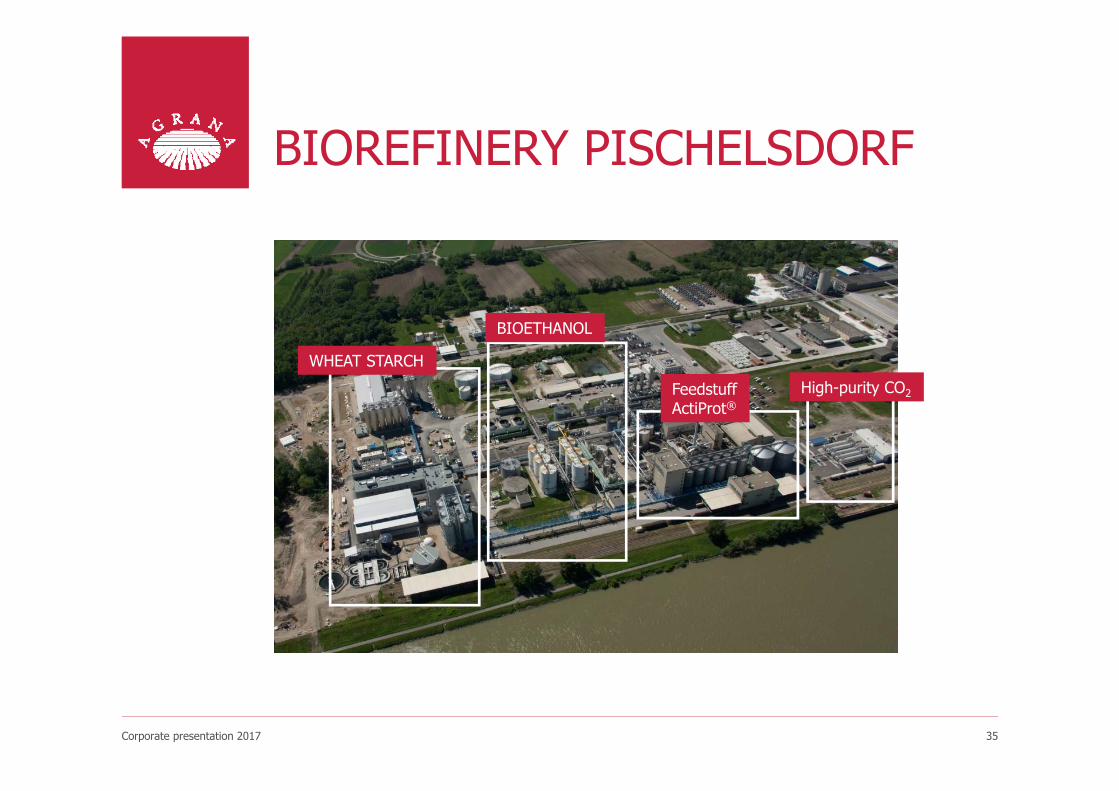

Biorefinery Pischelsdorf|AUT: Integration of 2013 opened wheat starch plant and the bioethanol facility 100% grain utilization resource efficiency

„ZERO-WASTE“-PRINCIPLE

Corporate presentation 2017 35

BIOREFINERY PISCHELSDORF

WHEAT STARCH

BIOETHANOL

FeedstuffActiProt®

High-purity CO2

Corporate presentation 2017 36

100% UTILISATION OF RAW MATERIALS ENVIRONMENTAL AND ENERGY ASPECTS OF PRODUCTION

WHEAT

WHEAT + CORN

roller-mill

Starch-factory

Fermenterhammer-mill

Ethanol-plant

WHEAT BRAN

A-WHEAT STARCH

WHEAT GLUTEN

BIOETHANOL

ACTIPROT®

BIOGENIC CO2

B+C -Starch

Wheat-Starch-Products1

2

3

4

approx. 105,000 t

approx. 55,000 t

approx. 23,500 t

up-to 240,000m³

„WITH ONE RAW MATERIAL TO FOUR PRODUCTS“

approx. 180,000 t

approx. 100,000 t

Corporate presentation 2017 37

AGRANAS ECONOMIC FOOTPRINT

Study carried out by “Economica”

Calculation of the economic impact of AGRANA's business operations according to the companies understanding of sustainability, as a balance of economic, environmental and social aspects

Methodology: Input-Output Analysis

Based on data of the 2014|15 financial year

Gross value-added: the gross value added calculates the amount that is available to remunerate the production factors of labour (wages and salaries) and capital (profit, interest on borrowed capital and deductions).

Direct effects: Include that value of gross value creation or employment that is earned directly in the enterprise under consideration or generates jobs.

Indirect effects: Come into existence through the advance services interfaces of the observed enterprise in other sectors (e.g. a clinic requires advance services medications, electricity, etc., through which the final demand in the pharmaceutical industry and the electricity economy are stimulated and then in turn need advance services, etc.).

Induced effects: The jobs created and/or secured in the direct or indirect effect generate income that is then spent again by the workers (above all for consumption). This promotes ultimate demand in the respective sectors (especially retail).

Multipliers: Represent the extent to which the total effects exceed the original direct effect. A multiplier is calculated as the sum of the total value added divided by the direct economic value added generated by AGRANA.

Corporate presentation 2017 38

RESULTS ECONOMIC FOOTPRINTAGRANA-GROUP

511

142

975

8,708 30,970

direct indirect + induced

Gross value-added (business operations): in €m

Employment effects (business operations):

Gross value-added (investment):in €m

Employment effects (investments):

€ 172 m

40,000 jobs

4,622 jobs

€ 1.5 bn

Macroeconomically relevant!

Share of the Austrian GDP: • Direct effect: around 0.2% • Total effect: around 0.5%

Gross value-added multiplier:

Every Euro of gross value-addedgenerated by AGRANA, created upto two additional euros of value-added in other companies.

Employment multiplier:

Corporate presentation 2017 39

GROSS VALUE-ADDED (GVA) EFFECTSAGRANA GROUP (BUSINESS OPERATIONS)

Gross value-added effects of the AGRANA Group‘s business operations by segment in €m, 2014|15

510.6

840.9

133.8 1,485.3

The largest single contribution (58%) is made by the Fruit segment

The largest economic lever expressed as the multiplier, is also found in the Fruit segment.

Multiplier:• Sugar: 2.85

• Starch: 2.69

• Fruit: 3.03

Corporate presentation 2017 40

EMPLOYMENT EFFECTSAGRANA GROUP (BUSINESS OPERATIONS)

Employment effects of the AGRANA Group‘s businessoperations by segments, (heads), 2014|15

39,678

8,708

29,103

1,867

The largest contribution to the employment effects is made by the Fruit segment because of the global presence and the employment model.

The larger economic levers, are however found in the Starch and Sugar segments. Multiplier:

• Sugar: 5.52

• Starch: 5.81

• Fruit: 3.95

Corporate presentation 2017 41

BUSINESS FIGURES2016|17

Corporate presentation 2017 42

REVENUE BY SEGMENT2016|17 VS PRIOR YEAR

672.6 721.61,083.4

2,477.6

671.9733.9

1,155.5

2,561.3

0

1.000

2.000

3.000

Reve

nue

in €

m

2015|162016|17 2015|16 2016|17 2015|162016|17 2015|162016|17

SUGARSTARCHFRUITGROUP

27.2%

29.1%

43.7%

2015|16

26.2%

28.7%

45.1%

2016|17

Corporate presentation 2017 43

EBIT BY SEGMENT2016|17 VS PRIOR YEAR

4.3

65.958.8

129.0

24.4

76.2 71.8

172.4

0

50

100

150

200

EBIT

in €

m

2015|162016|17 2015|162016|17 2015|162016|17 2015|162016|17

3.3%

51.1%

45.6%

2015|16

14.2%

44.2%

41.6%

2016|17

6.2%3.6%

10.4%EBIT margin

5.4%

0.6%

9.1%

SUGARSTARCHFRUITGROUP

Corporate presentation 2017 44

CONSOLIDATED INCOMESTATEMENT

€m (condensed) 2016|17 2015|16 Change

Revenue 2,561.3 2,477.6 +3,4%

EBITDA1 235.2 192.0 +22,5%

Operating profit before except. items and results of equity-accounted JV 150.8 107.5 +40.3%

Share of results of equity-accounted JV 30.6 24.5 +24.9%

Exceptional items (9.0) (3.1) -190.3%

EBIT 172.4 129.0 +33.6%

EBIT margin 6.7% 5.2% +1.5pp

Net financial items (17.9) (24.5) +26.9%

Profit before tax 154.5 104.4 +48.0%

Income tax expense (36.6) (23.5) -55.7%

Profit for the period 117.9 80.9 +45.7%

Attributable to shareholders of the parent 111.3 82.7 +34.6%

Earnings per share € 7.132 € 5.82 +22.5%

1 EBITDA represents operating profit before exceptional items, results of equity-accounted joint ventures, and operating depreciation and amortisation.

2 EPS is calculated on the basis of 15,622,244 outstanding shares at the balance sheet date (29 Feb 2017)

Corporate presentation 2017 45

CONSOLIDATED BALANCE SHEET€m (condensed) 2016|17 2015|16 Change

Non-current assets 1,135.3 1,027.7 +10.5%

Current assets 1,346.1 1,213.9 +10.9%

Non-current assets held for sale 0.0 1.6 -100,0%

Total assets 2,481.4 2,243.2 +10.6%

Equity 1,411.9 1,200.1 +17.6%

Non-current liabilities 296.6 378.7 -21.7%

Current liabilities 772.9 664.4 +16.3%

Total equity and liabilities 2,481.4 2,243.2 +10.6%

Equity ratio 56.9% 53.5% +3.4pp

Net debt 239.9 405.8 -40.9%

Gearing 17.0% 33.8% -16.8pp

Corporate presentation 2017 46

CONSOLIDATED CASH FLOW STATEMENT

€m (condensed) 2016|17 2015|16 Change

Operating cash flow before changes in working capital 258.0 225.9 +14.2%

Changes in working capital 31.8 (73.7) +143.1%

Total of interest paid/received and tax paid (34.0) (50.3) +32.4%

Net cash from operating activities 255.8 101.9 +151.0%

Net cash (used in) investing activities (171.5) (19.9) -761.8%

Net cash (used in) financing activities 9.3 (163.6) +105.7%

Net (decrease)/increase in cash and cash equivalents 93.6 (81.6) +214.7%

Corporate presentation 2017 47

ANALYSIS OF NET FINANCIAL ITEMS

€m 2016|17 2015|16 Change

Net interest expense (10.2) (8.4) -21.4%

Currency translation differences (1.2) (13.5) +91.1%

Share of results of non-consolidated subsidiaries and outside companies

0.6 0.03 +1,900.0%

Other financial items (7.1) (2.6) -173.1%

Total (17.9) (24.5) +26.9%

Corporate presentation 2017 48

OUTLOOK

AGRANA

Corporate presentation 2017 49

OUTLOOK

2017|18

AGRANA expects Group revenue to increase slightly and operating profit (EBIT) to increase significantly for the 2017|18 financial year.

Total investment in the three business segments, at about € 140 million, will significantly exceed depreciation of about € 90 million.

Corporate presentation 2017 50

DISCLAIMER

This presentation is being provided to you solely for your information and may not be reproduced or further distributed to any other person or published, in whole or in part, for any purpose. This presentation comprises the written materials/slides for a presentation concerning AGRANA Beteiligungs-AG (“Company”) and its business.

This presentation does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any shares in the Company, nor shall it or any part of it form the basis of, or be relied on in connection with, any contract or investment decision.

This presentation includes forward-looking statements, i.e. statements that are not historical facts, including statements about the Company's beliefs and expectations and the Company's targets for future performance are forward-looking statements. These statements are based on current plans, estimates and projections, and therefore investors should not place undue reliance on them. Forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update publicly any of them in light of new information or future events.

Although care has been taken to ensure that the facts stated in the presentation are accurate, and that the opinions expressed are fair and reasonable, the contents of this presentation have not been verified by the Company no representation or warranty, express or implied, is given by or on behalf of the Company any of its respective directors, or any other person as to the accuracy or completeness of the information or opinions contained in this presentation. Neither the Company nor any of its respective members, organs, representatives or employees or any other person accepts any liability whatsoever for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection therewith.