Embed Size (px)

Citation preview

Struggling To Model Upside For Verisk|Must Read Mar. 29, 2016 8:45 AM ET

by: Lester Goh

Summary• Carnage in the energy/metals/mining sector is not isolated to the sector

itself. There are usually spillover effects, which have yet to fully play out.• While worries regarding the Verisk's energy/metals/mining exposure is

probably overblown, current valuation multiples require a very clear path to growth, which simply is not there, in my view.

• Verisk sports a solid deleveraging story going forward, though other sources of growth are unclear and harder to pin down.

• Until there is more visibility on growth, the current price is too big of an ask.

Thesis

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | Se… Page 1 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

Thanks to the current low oil environment, firms that even have an inkling of exposure to the oil & gas industry or the metals and mining industries (which have been suffering from commodity oversupply in recent years) have seen their shares fall drastically, in anticipation of the forthcoming spill-over effects.

Prima facie, Verisk Analytics's (NASDAQ:VRSK) ("Verisk", "VRSK", or the "Company") acquisition of Wood MacKenzie, which sells to the energy, metals & mining industries, appears ill-timed given the depression in oil prices and the commodity oversupply situation in the metal & mining industries. The market appears unconcerned regarding the Company's exposure to these sectors and I agree with its assessment.However, considering the fact that Verisk's free cash flow to equity multiple is approaching 30x, there needs to be a very clear path to growth to justify the current price. Put simply, there is a bear case to be made here, but it's not the Company's energy, metals & mining exposure.While the Company appears to sport a rather solid deleveraging story going forward, other sources of levered free cash flow growth are less clear. Specifically, with the continued improvement in insurance premium pricing, bulls may be

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | Se… Page 2 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

modeling robust growth for Verisk's insurance segments, counting on this trend to drive future growth. Yet, recent management commentary suggests that this may be a smaller driver going forward than expected.With the growth story being hard to pin down, it is difficult to justify going long Verisk at current prices, in my view. Even if we are extremely lenient and extrapolate recent growth numbers into the future, it is still hard to justify the current multiple, and this also serves to highlight the lack of any reasonable upside to the stock.Quick background to Verisk's businessesAs a quick reminder, Verisk's (and Wood MacKenzie's) offerings are unique in the data analytics in that they stem from proprietary sources. Some players in the space use publically available data, but Verisk takes it one step further by aggregating proprietary data from its customers. This is possible because insurers are required to periodically collect and report data to regulators, and Verisk's statistical agent services makes this a walk in a park for insurers. These unique data assets differentiate Verisk from the competition.The difference between Verisk and Wood Mac is simply the verticals they serve - Wood Mac serves energy, and Verisk serves insurance, healthcare, payments, amongst others. Additionally, some firms only focus on one leg of the insurance process - pricing risk, for example - while Verisk offers a comprehensive offering, catering to everything from predicting loss to selecting and pricing risk to loss prevention, and finally to fraud prevention.The business model itself is characterized by highly recurring revenue thanks to the presence of multi-year contracts, economies of scale (data collection costs are <2% of revenue), and significant barriers to entry (mainly proprietary data) ensuring the sustainability of fat margins.For further information, I recommend reading through the Company's most recent investor presentation.The bad: energy, metals & mining

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | Se… Page 3 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

The Company has exposure to energy, metals & mining, sectors where things have been a little scary, to be kind. The overarching concern is that low commodity prices would result in reduced customer spending (this is playing out now) and could possibly cause customers to refrain from using Verisk's solutions.Since the price of oil begun declining from ~$100/bbl, analysts covering the Company have been very worried (evident from numerous related questions posed on recent earnings calls) about whether the VRSK would suffer from this, and to what extent, due to the Wood Mac acquisition (added ~$200m in revenues and ~$100m in EBITDA, which represents ~10% of VRSK's overall sales and EBITDA).It is fairly easy to see that concerns regarding the Company's metals & mining exposure are overblown. Metals & mining revenue was ~4% of Wood Mac's revenue (source: 2015 investor day, slide 66), and a de minimis amount with respect to consolidated revenue.The real concern is energy, which is ~44% of Wood Mac sales. Admittedly, this is only ~5% of sales and presumably a similar percentage of EBITDA (margins are very similar across all sub-segments), but if one takes into account the nearly ~30x levered free cash flow multiple that Verisk currently trades at, a meaningful drop in ~5% of EBITDA could result on the Company whiffing on analyst estimates going forward. A growth story with cracks is not a pretty sight.Wood Mac has been reporting fairly decent results throughout fiscal 2015, but 4Q results certainly gave analysts covering the stock a fright as sales turned negative (declining 1% y/y), prompting no less than three questions from analysts in the subsequent Q&A regarding the subsidiary. This came as a surprise to me for a few reasons, as Wood Mac was not what I was worried about.Wood Mac's offerings are deeply embedded in customer workflows - much like Verisk. For example, say an E&P customer is looking to develop its oil reserves. It would need to review its regional assets and filter for the projects that would provide the highest return, understand the potential for upside, supply & demand dynamics, valuation, capital expenditures, timing of cash flow, risks, and asset-specific issues (location, etc.).

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | Se… Page 4 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

At every step of this process, the customer would need to consult Wood Mac's data sets to aid him in his decision-making. Clearly, to customers, Wood Mac is mission-critical - management supports this by highlighting a large customer on the call who heavily relies on Verisk's solutions to go about their day-to-day decision. Even if customers are paring back their spending, they would still need to periodically utilize Wood Mac's products to re-evaluate the situation. Such a level of embeddedness essentially suggests that customers have to go out of business before they stop using Wood Mac.Readers may say: well, they are going out of business. There is an important nuance here though. The players that are going out of business (i.e. headed into bankruptcy) in the energy sector are primarily smaller players with weak balance sheets.Wood Mac's significant customer concentration (top 10% accounts for nearly a quarter of sales) and leading market position (#1 or #2 in market share) implies that its customers are predominantly larger players. While larger players are undoubtedly experiencing some difficulty (they are certainly not totally immune to large fluctuations in commodity prices), their situation is not life-threatening - their relatively stronger balance sheets would allow them to ride it out, in stark contrast to the smaller players. In short, energy is clearly not really the issue at hand here.Deleveraging story is solid, but other sources of growth is less soAs a result of the Wood Mac acquisition, Verisk levered up its balance to 3x+ net debt/EBITDA. The metric has come down quite a bit - currently it is just south of 3x.Management has an explicit target to de-lever to 2.5x by year-end 2016, and likely would reduce debt further going into 2017 and beyond. The Company has guided ~$130m in interest expense for 2016, which implies a ~4.1% average rate on ~$3.16b of gross debt.Assuming the entirety of levered free cash flow (~$450m) is allocated to debt paydown, interest expense would decrease by ~$19m (~$130m - [~$3.16b - ~$0.45b] * 0.041), driving ~4% levered free cash flow growth. As a reference, utilizing the entirety for share repurchases instead, would drive ~3.3% levered free

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | Se… Page 5 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

cash flow growth (~5.7m shares repurchased, assuming average purchase price of $80). Thus, it seems fairly clear that management would favor the debt paydown route.Debt paydown cannot be the only source of growth though. To justify the near-30x levered free cash flow multiple, one would need 25%+ total growth. In other words, pro forma for debt paydown, where is the other 20% growth going to come from?It is unlikely to stem inorganically. The Company has already made 6 acquisitions in the past two years (including a very large one - Wood Mac) - management likely has their hands full with integration. Their commitment to debt paydown also suggests that there would be minimal free cash flow left over to make incremental acquisitions.

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | Se… Page 6 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

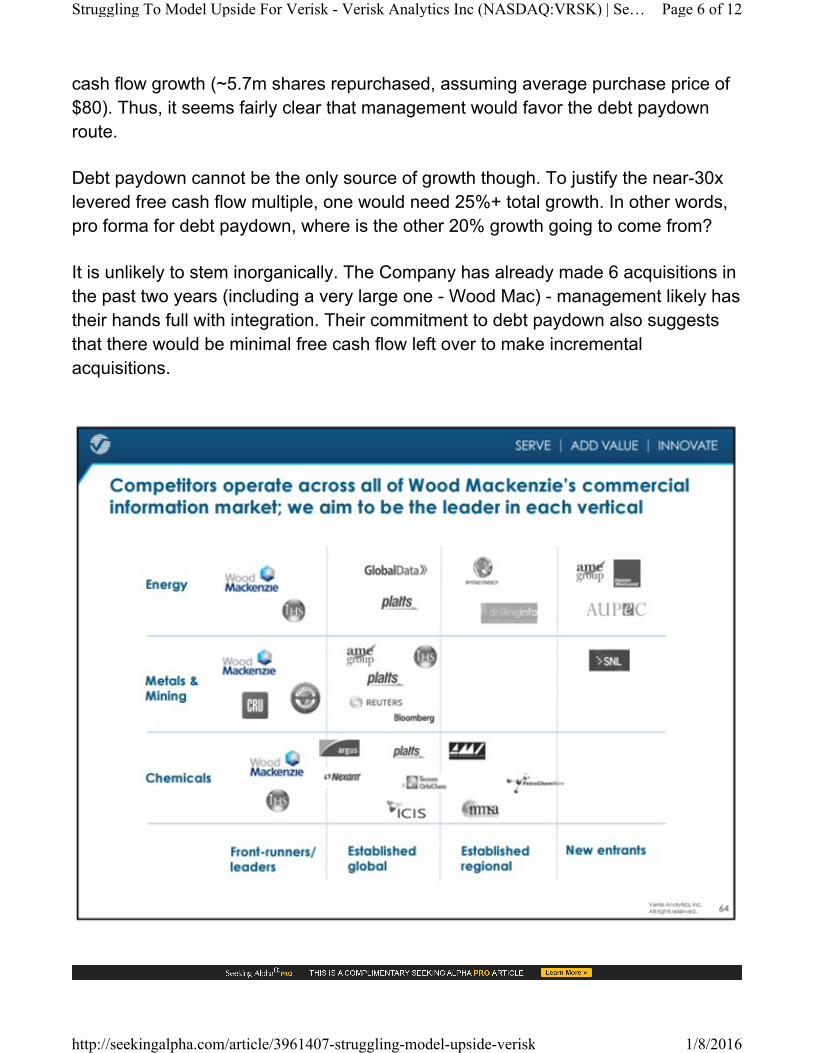

Source: Verisk's December Investor PresentationLongs betting on continued incremental acquisitions is a misguided thesis, in my view. Further, this is a space dominated by a few large players (as seen above), so a huge acquisition is probably not something you should be counting on.Most of the large players are subsidiaries of larger corporations (e.g. Reuters, Bloomberg and Platts - a subsidiary of McGraw-Hill) whose data services are integrated with other financial offerings (e.g. Bloomberg Terminal), making an acquisition very unlikely - it would not be wise for Verisk to stray away from its core competency. Smaller players tend to focus on their own regional markets (as they should, given the enormous barriers to entry into larger markets) and would not move the needle much even assuming management wants to acquire them. So where is growth going to come from?Bulls point to the improving insurance premium pricing environment as the main driver. This (the focus on insurance premium pricing) is unsurprising given insurance accounts for ~55% of sales and EBITDA.Longs support this story by citing a 'hard' pricing environment, which is characterized by strong pricing trends. From 2004-2011, the P&C industry at large operated in a 'soft' environment. Beginning in 2012 or so, pricing trends have improved substantially and are likely to continue due to the fact that some players have exited the industry and thus reducing capital capacity (e.g. CNA Financial and Mercury General have exited commercial auto).Notably, these cycles ('soft' and 'hard' pricing environments) tend to last for years as it takes time for 1) new competitors to be attracted to a strong pricing environment, and 2) for capacity to ramp up - increases in capacity do not happen overnight, even if new entrants have poor underwriting standards. Stated simply, there still appears to be a lot of steam left in the insurance premium pricing engine going forward.The bull thesis is quite a simple one. In recent years, Verisk has begun signing multi-year agreements with its insurance customers where pricing is fixed at the beginning of the contract. Unsurprisingly, this coincided with the better pricing environment. Put simply, longs expect the bulk of the outstanding contracts still linked to the poor pricing environment to be re-negotiated, allowing Verisk to increase overall pricing and drive revenue growth.

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | Se… Page 7 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

Verisk's insurance segments have been growing in the high single-digits lately. If we are very kind and very aggressively assume that:1) this growth stemmed purely from price increases through contract re-pricing (growth due to price requires no incremental costs and thus falls directly to the net income line, while growth through new customer acquisition would require incremental opex/COGS),2) no additional working capital investment needed (purely cash sales, no incremental account receivables),3) a 30% tax rate, and4) 8% insurance segment growth,this would add ~13% to levered free cash flow growth. Basically, my assumptions are for no friction between top line growth and levered free cash flow growth, with taxes being the only exception.[Math: ~$2b in sales * 0.55 * 0.08 * (1-0.3) = ~$62m or ~13% of 2015 levered free cash flow].The high single-digit growth in insurance segments in recent years have likely been quite significantly (though probably not wholly, as I aggressive assume above) driven by contract pricing re-negotiations and this particular tailwind is unlikely to be that pronounced going forward, as 1) the low-hanging fruit has likely been plucked already and 2) management's cautious commentary indicating so (emphasis mine):

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | Se… Page 8 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

Yeah. So we, I think we have shared with you in the past that sort of the mix of revenue sources in that part of the business has changed, where it used to be that most every customer was being priced according to a two-year look back on premiums. But we're now at a point where more than 50% of what we do in RA is on multi-year agreements, not related at all to what was happening in the premiums two years prior.And then with respect to the rest of our customer base, where we still do reference premiums from two years before, just want to remind you that there are three terms in the pricing algorithm and premium is only one of the three. And we have complete freedom with respect to the other two, which is mill rate and the flat fees. And so the actual, literal effect of what is going on in the premium environment is actually very muted at this point."Source: 4Q 2015 Earnings Call Transcript

But even if we are very kind and are willing to tack on this ~13% to the ~4% growth stemming from debt paydown, we would still fall significantly short of the ~25% total growth needed to justify the current multiple.

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | Se… Page 9 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

Growth is unlikely to stem from non-insurance segments as they are either too small (financial services), growing too slowly (property), flat (energy & other specialized), or declining (healthcare, possibly energy). As such, they would likely drag down the overall levered free cash flow growth rate of the enterprise. There are margin headwinds as well - chief of which is increased personnel costs - the Company announced that it is stepping up its hiring (personnel costs are ~50% of total expenses).Management mentioned a promising initiative on the call. Specifically, Wood Mac announced a commercial alliance with Thomson Reuters' Eikon platform. The basic idea seems to be as follows: provide Eikon users (i.e. paying subscribers) with a 'teaser' of Wood Mac products (primarily oil supply chain data and research reports) and over time persuade them to pay for the full thing. The press release provides a decent background of the agreement.The deal is a win for Reuters as their news reporters can provide more comprehensive insight, and a win for Verisk as it opens up an additional sales channel. There was no mention of the duration of the agreement, but given the win-win situation I noted, it seems likely that the deal will be in place for a long time.It is hard to see this deal backfiring on Verisk given that the Company is merely providing a 'teaser' of its offerings, not the entire thing (which provides way more value). As the agreement involves simply syncing Wood Mac's data with the Eikon feed, it is difficult to imagine problems with integration. The alliance is very much analogous to the 'freemium' model that most tech companies utilize. There are not many ways that one can lose with this model. The principal way that I can identify is that if the 'free' products are more than enough to satisfy customers' needs, making it unlikely for them to pay for premium products. As noted, this is not the case for Wood Mac.This initiative is promising if we take management's word that this particular sales channel extends their reach to customers they were largely not serving. However, even if this statement is true, growth from this area is unlikely to materialize in coming quarters. Reason being: Wood Mac's (and Verisk's for the matter) sales cycles are inherently long due to their level of embeddedness into the customers' workflow. It thus takes many years to convince potential customers to come on board.

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | S… Page 10 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

At nearly 30x free cash flow to equity and with the growth story largely unclear, risks are weighted to the downsideVerisk has next to no attributes that make it a compelling long. Growth due debt paydown is grossly insufficient. Even heroic assumptions with regard to the largest segment - insurance, is not enough, and it appears foolish to expect non-insurance segments to punch above their weight given their small size or mediocre growth rates. Extrapolating recent results to the future could probably justify the current multiple, but that also serves to highlight the absence of upside.While Verisk is inherently a wonderful business, the current price is simply too big of an ask - shares would certainly be more attractive if there is a significant pullback. A wonderful business does make sense at a fair price, but the current price is anything but fair, in my view.Shorting would probably be difficult, given the lack of clear catalysts; you would be shorting based almost solely on valuation, which does not tend to work out. Avoiding or exiting a long position seems the prudent choice here.Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.Additional disclosure: The author's reports contain factual statements and opinions. He derives factual statements from sources which he believes are accurate, but neither they nor the author represent that the facts presented are accurate or complete. Opinions are those of the the author and are subject to change without notice. His reports are for informational purposes only and do not offer securities or solicit the offer of securities of any company. Mr. Goh ("Lester") accepts no liability whatsoever for any direct or consequential loss or damage arising from any use of his reports or their content. Lester advises readers to conduct their own due diligence before investing in any companies covered by him. He does not know of each individual's investment objectives, risk appetite, and time

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | S… Page 11 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016

horizon. His reports do not constitute as investment advice and are meant for general public consumption. Past performance is not indicative of future performance.

Struggling To Model Upside For Verisk - Verisk Analytics Inc (NASDAQ:VRSK) | S… Page 12 of 12

http://seekingalpha.com/article/3961407-struggling-model-upside-verisk 1/8/2016