Embed Size (px)

Citation preview

Strategies to Accelerate Growth in the Steel Sector

Peter J. ScottManaging PartnerHeadwall Partners LLC

March 13, 2017

Steel Volume Growth

Indexed Apparent U.S. Steel Consumption(1)

(1) Defined as TTM total steel mill product shipments + imports – exports – semifinished steel product imports, indexed to 1/1/2007 = 100

Source: AISI

0%

50%

100%

150%

200%

77%

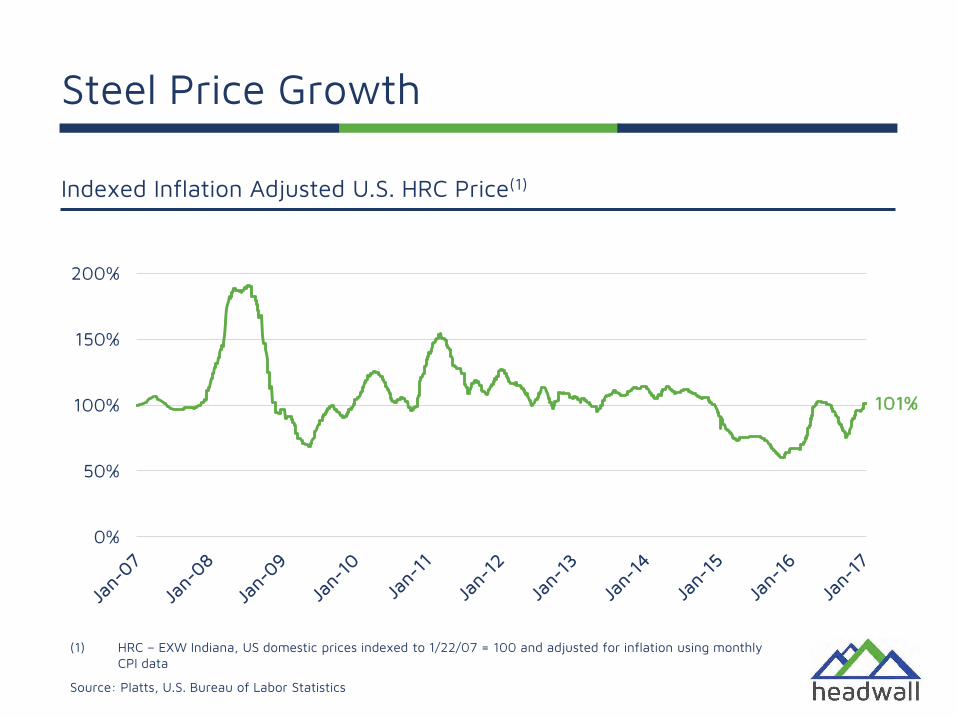

Steel Price Growth

0%

50%

100%

150%

200%

Indexed Inflation Adjusted U.S. HRC Price(1)

(1) HRC – EXW Indiana, US domestic prices indexed to 1/22/07 = 100 and adjusted for inflation using monthly CPI data

Source: Platts, U.S. Bureau of Labor Statistics

101%

Steel Spread Growth

0%

50%

100%

150%

200%

Indexed Inflation Adjusted U.S. Steel Spread(1)

(1) Spread = (HRC – EXW Indiana, US domestic prices less Shredded Midwest US – delivered, US domestic prices), indexed to 1/22/07 = 100 and adjusted for inflation using monthly CPI data

Source: Platts, U.S. Bureau of Labor Statistics

98%

0%

50%

100%

150%

200%Steel Index

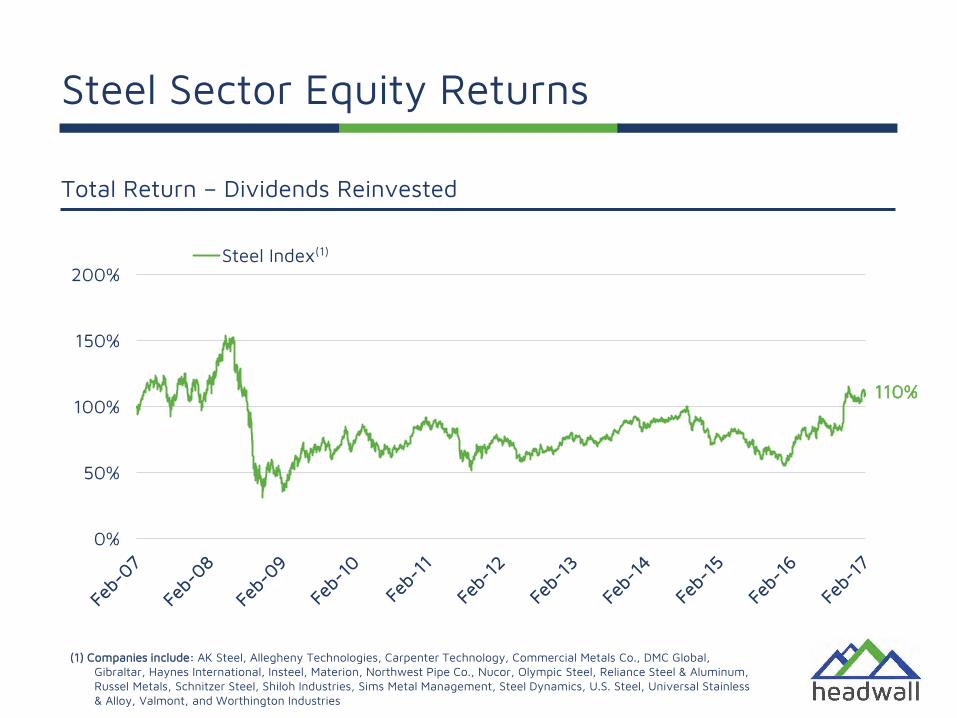

Steel Sector Equity Returns

Total Return – Dividends Reinvested

(1) Companies include: AK Steel, Allegheny Technologies, Carpenter Technology, Commercial Metals Co., DMC Global, Gibraltar, Haynes International, Insteel, Materion, Northwest Pipe Co., Nucor, Olympic Steel, Reliance Steel & Aluminum, Russel Metals, Schnitzer Steel, Shiloh Industries, Sims Metal Management, Steel Dynamics, U.S. Steel, Universal Stainless & Alloy, Valmont, and Worthington Industries

(1)

110%

0%

50%

100%

150%

200%

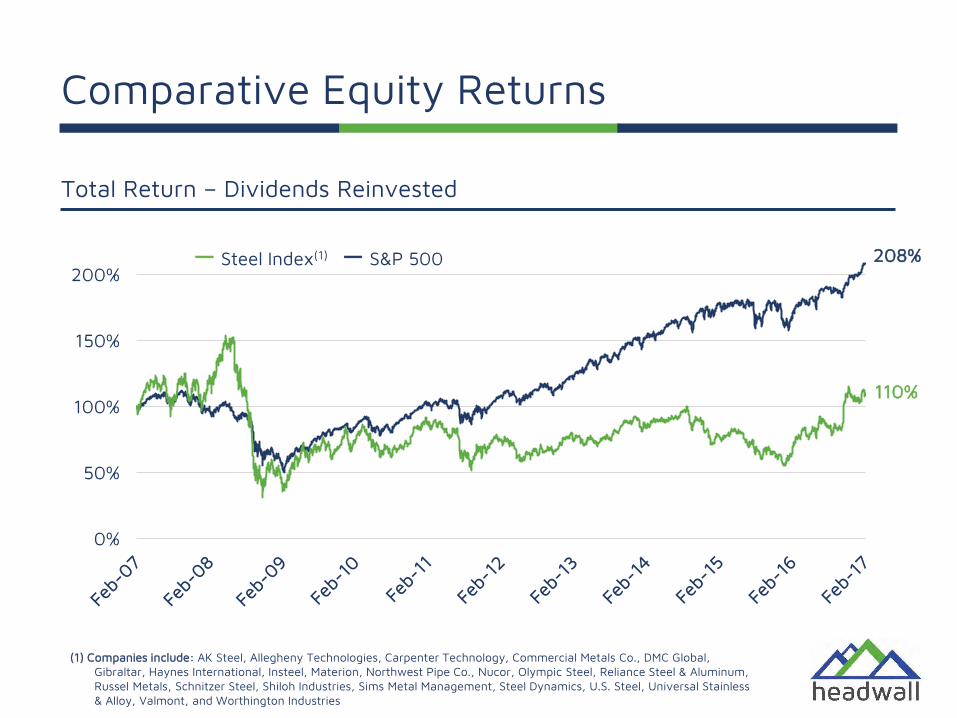

Comparative Equity Returns

Total Return – Dividends Reinvested

(1) Companies include: AK Steel, Allegheny Technologies, Carpenter Technology, Commercial Metals Co., DMC Global, Gibraltar, Haynes International, Insteel, Materion, Northwest Pipe Co., Nucor, Olympic Steel, Reliance Steel & Aluminum, Russel Metals, Schnitzer Steel, Shiloh Industries, Sims Metal Management, Steel Dynamics, U.S. Steel, Universal Stainless & Alloy, Valmont, and Worthington Industries

208%

110%

一 Steel Index(1) 一 S&P 500

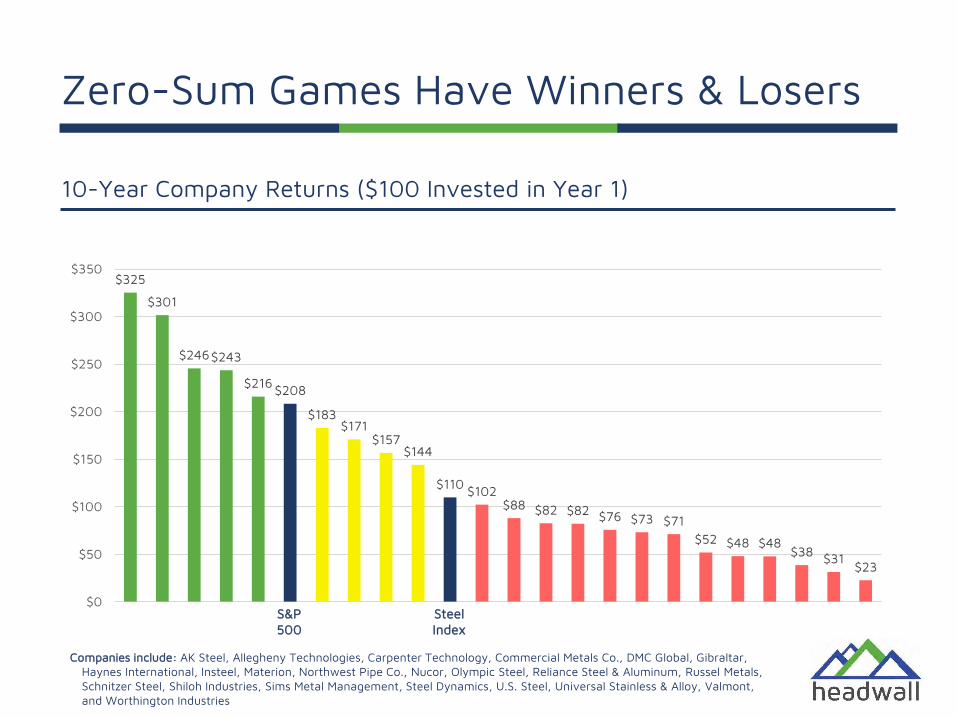

Steel – A Zero-Sum Game?

Zero-sum Game:

A competition in which one person’s gain is equivalent to another’s loss, so the net change in wealth is zero.

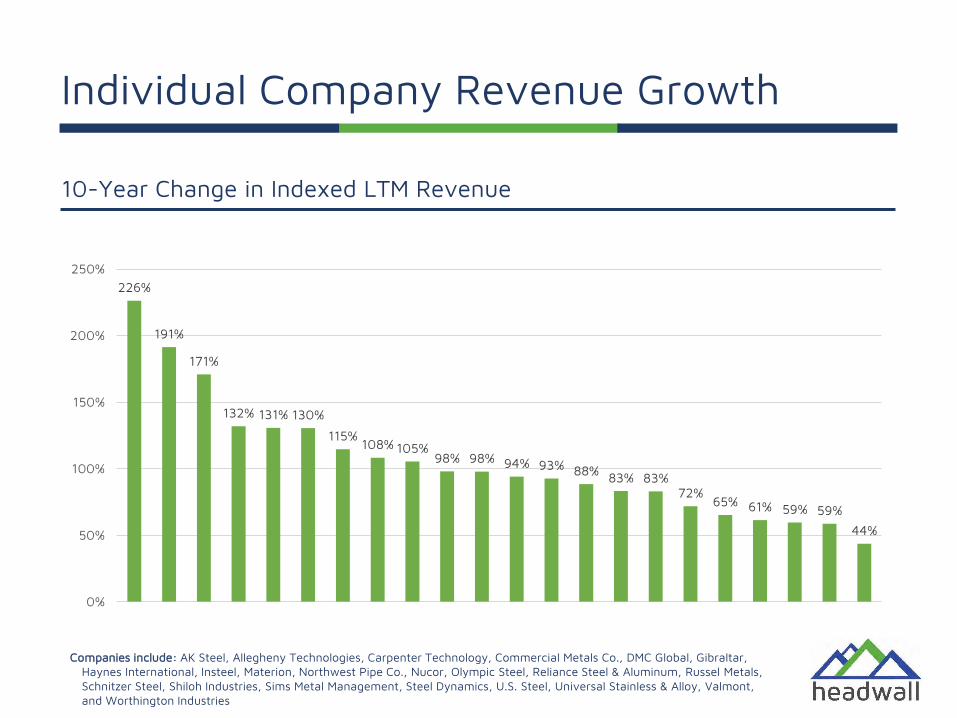

Individual Company Revenue Growth

10-Year Change in Indexed LTM Revenue

Companies include: AK Steel, Allegheny Technologies, Carpenter Technology, Commercial Metals Co., DMC Global, Gibraltar, Haynes International, Insteel, Materion, Northwest Pipe Co., Nucor, Olympic Steel, Reliance Steel & Aluminum, Russel Metals, Schnitzer Steel, Shiloh Industries, Sims Metal Management, Steel Dynamics, U.S. Steel, Universal Stainless & Alloy, Valmont, and Worthington Industries

226%

191%

171%

132% 131% 130%

115%108% 105%

98% 98% 94% 93% 88% 83% 83%72%

65% 61% 59% 59%

44%

0%

50%

100%

150%

200%

250%

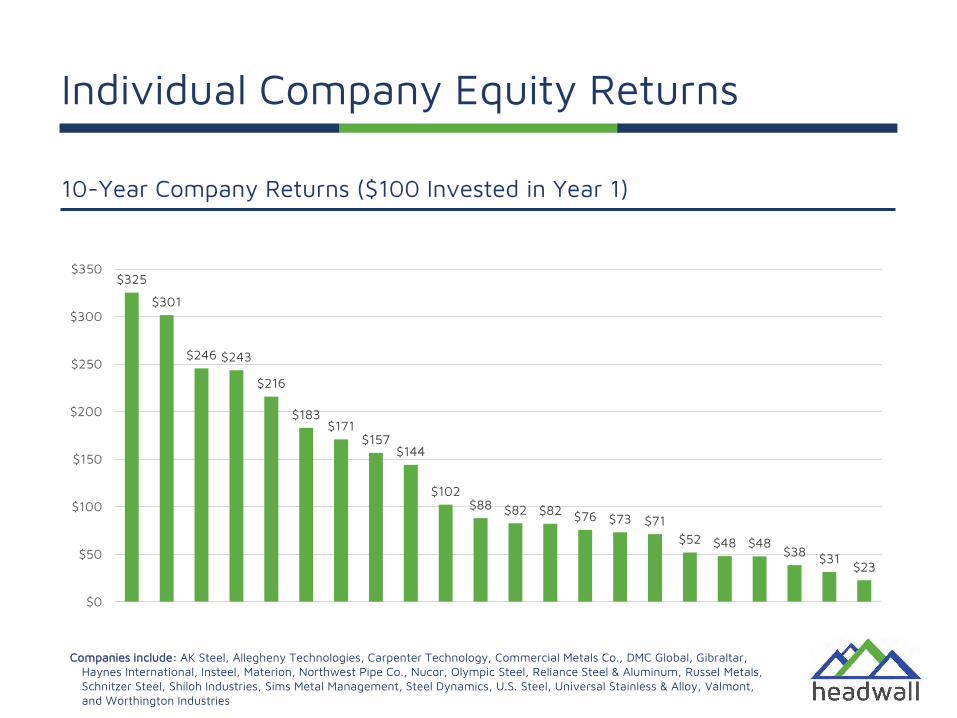

Individual Company Equity Returns

10-Year Company Returns ($100 Invested in Year 1)

Companies include: AK Steel, Allegheny Technologies, Carpenter Technology, Commercial Metals Co., DMC Global, Gibraltar, Haynes International, Insteel, Materion, Northwest Pipe Co., Nucor, Olympic Steel, Reliance Steel & Aluminum, Russel Metals, Schnitzer Steel, Shiloh Industries, Sims Metal Management, Steel Dynamics, U.S. Steel, Universal Stainless & Alloy, Valmont, and Worthington Industries

$325

$301

$246 $243

$216

$183$171

$157$144

$102$88 $82 $82 $76 $73 $71

$52 $48 $48$38 $31

$23

$0

$50

$100

$150

$200

$250

$300

$350

10-Year Company Returns ($100 Invested in Year 1)

Companies include: AK Steel, Allegheny Technologies, Carpenter Technology, Commercial Metals Co., DMC Global, Gibraltar, Haynes International, Insteel, Materion, Northwest Pipe Co., Nucor, Olympic Steel, Reliance Steel & Aluminum, Russel Metals, Schnitzer Steel, Shiloh Industries, Sims Metal Management, Steel Dynamics, U.S. Steel, Universal Stainless & Alloy, Valmont, and Worthington Industries

$325

$301

$246$243

$216 $208

$183$171

$157$144

$110 $102$88 $82 $82 $76 $73 $71

$52 $48 $48$38 $31

$23

$0

$50

$100

$150

$200

$250

$300

$350

Steel Index

S&P 500

Zero-Sum Games Have Winners & Losers

Strategic Growth Tactics

Strategic Growth:

A business tactic to increase sales by any one of several courses, including:

(i) market penetration(ii) geographic expansion (iii) product development(iv) market development (v) acquisitions or business combinations

What are Management Teams Doing?

Survey:• N.A. steel sector Chairmen, CEOs, and CFOs

• Steel mills, steel processors, service centers, scrap, other

• Broad size range (under $500mm to more than $5bn)

• Public, family owned, PE owned

• Topics:

‒ Trump Administration policies

‒ Growth expectations

‒ Sources of strategic growth

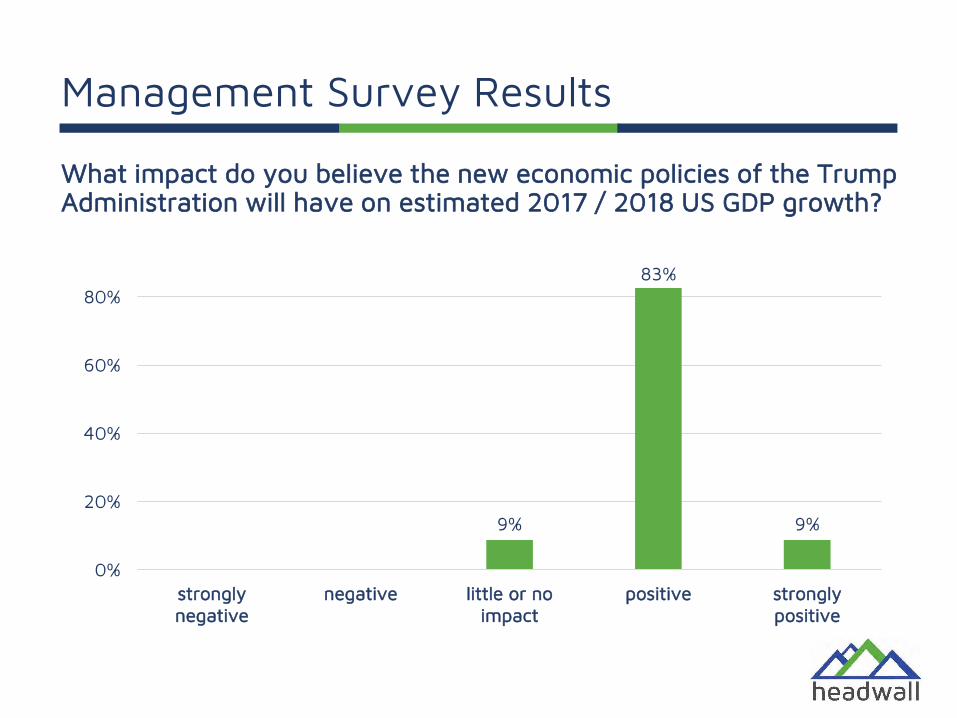

What impact do you believe the new economic policies of the Trump Administration will have on estimated 2017 / 2018 US GDP growth?

9%

83%

9%

0%

20%

40%

60%

80%

stronglynegative

negative little or noimpact

positive stronglypositive

Management Survey Results

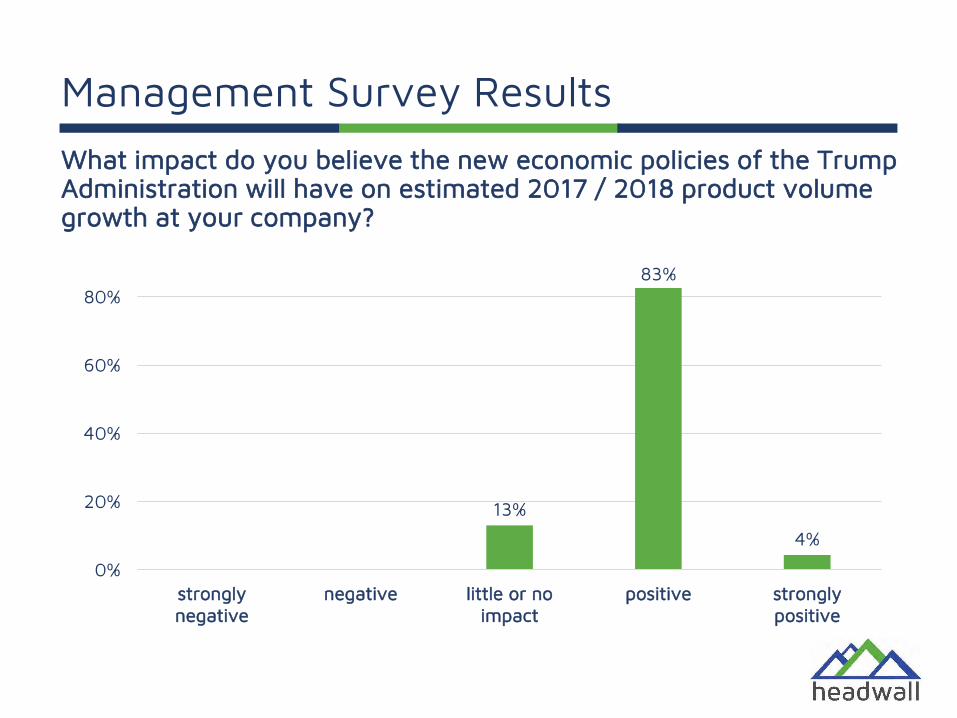

What impact do you believe the new economic policies of the Trump Administration will have on estimated 2017 / 2018 product volume growth at your company?

13%

83%

4%

0%

20%

40%

60%

80%

stronglynegative

negative little or noimpact

positive stronglypositive

Management Survey Results

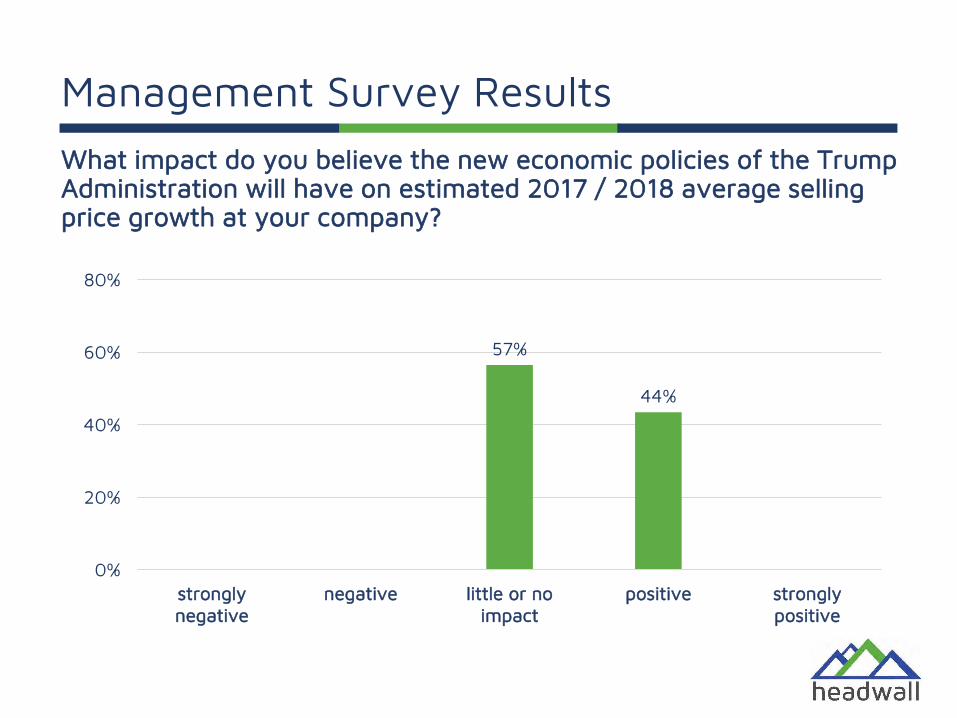

What impact do you believe the new economic policies of the Trump Administration will have on estimated 2017 / 2018 average selling price growth at your company?

57%

44%

0%

20%

40%

60%

80%

stronglynegative

negative little or noimpact

positive stronglypositive

Management Survey Results

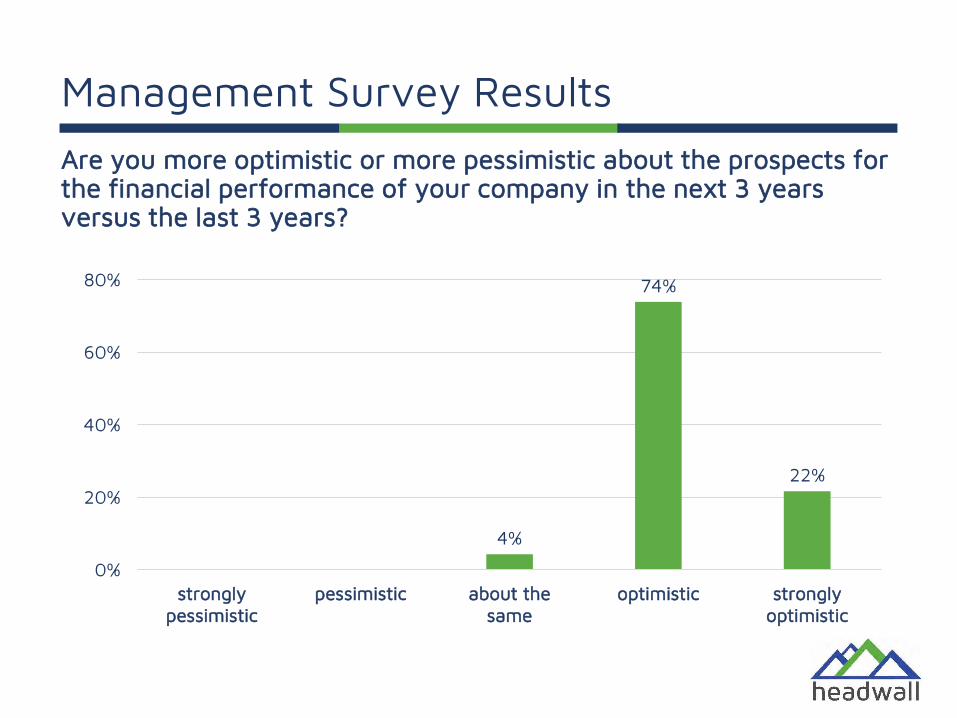

Are you more optimistic or more pessimistic about the prospects for the financial performance of your company in the next 3 years versus the last 3 years?

4%

74%

22%

0%

20%

40%

60%

80%

stronglypessimistic

pessimistic about thesame

optimistic stronglyoptimistic

Management Survey Results

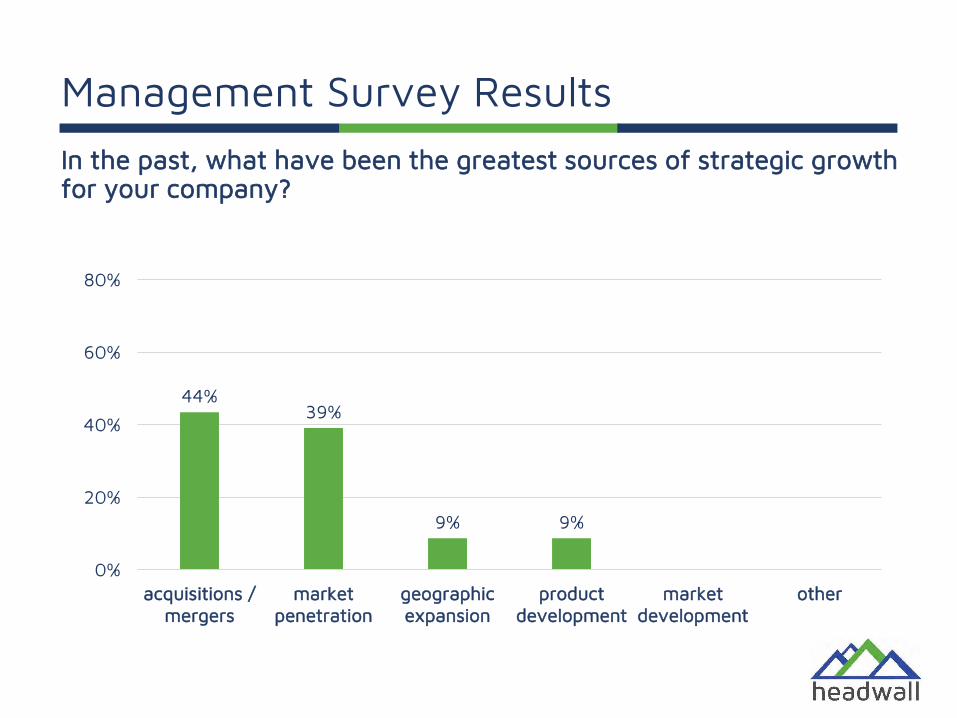

In the past, what have been the greatest sources of strategic growth for your company?

44%39%

9% 9%

0%

20%

40%

60%

80%

acquisitions /mergers

marketpenetration

geographicexpansion

productdevelopment

marketdevelopment

other

Management Survey Results

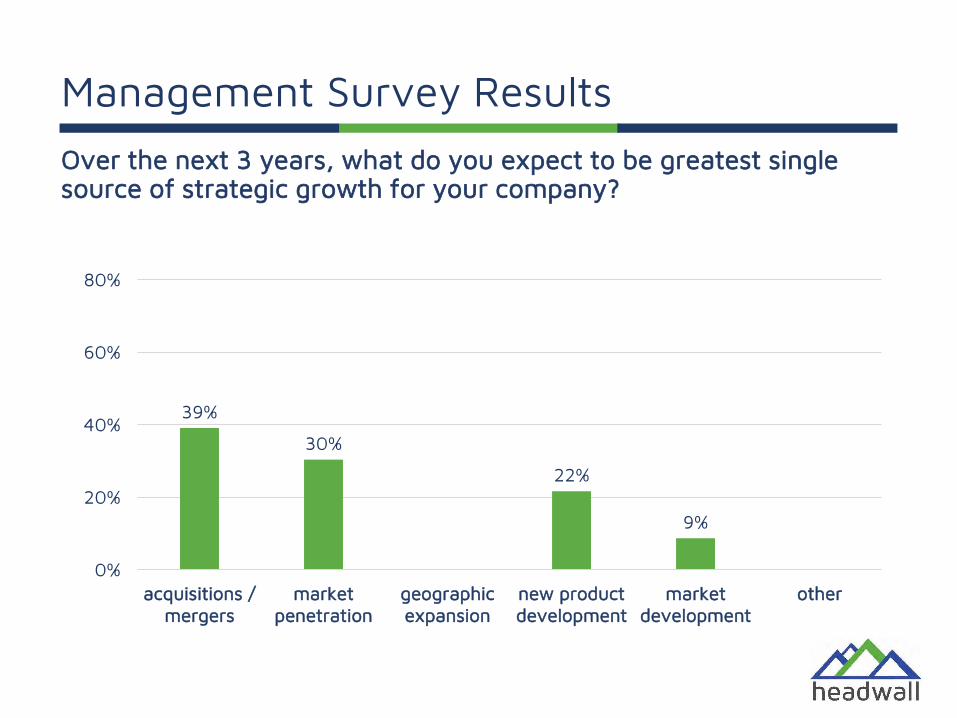

Over the next 3 years, what do you expect to be greatest single source of strategic growth for your company?

39%

30%

22%

9%

0%

20%

40%

60%

80%

acquisitions /mergers

marketpenetration

geographicexpansion

new productdevelopment

marketdevelopment

other

Management Survey Results

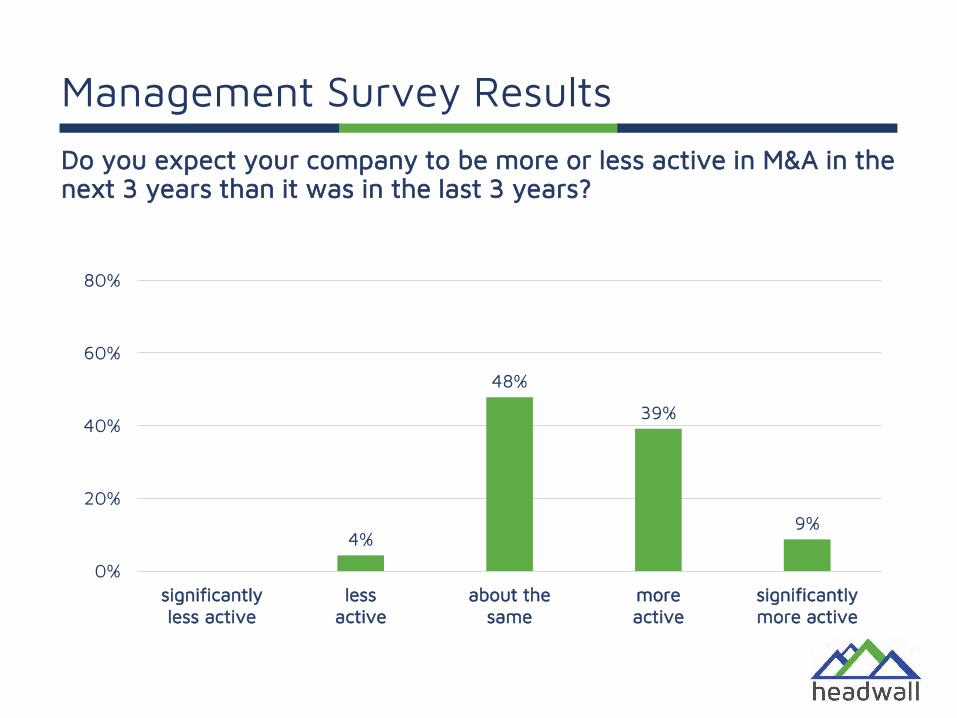

Do you expect your company to be more or less active in M&A in the next 3 years than it was in the last 3 years?

4%

48%

39%

9%

0%

20%

40%

60%

80%

significantlyless active

lessactive

about thesame

moreactive

significantlymore active

Management Survey Results

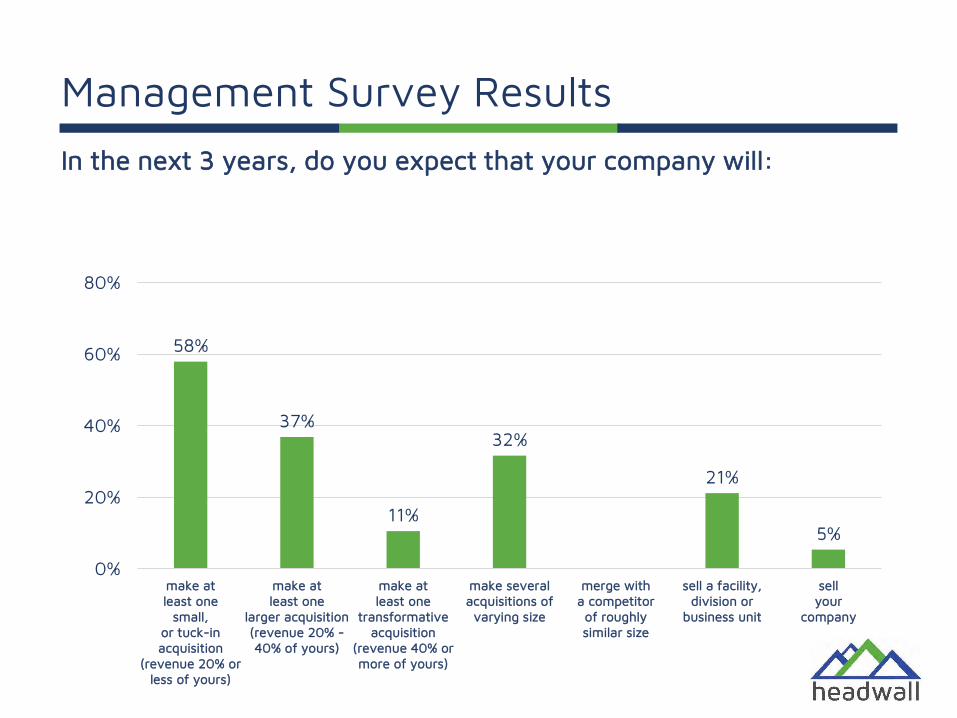

In the next 3 years, do you expect that your company will:

58%

37%

11%

32%

21%

5%

0%

20%

40%

60%

80%

make atleast one

small,or tuck-inacquisition

(revenue 20% orless of yours)

make atleast one

larger acquisition(revenue 20% -40% of yours)

make atleast one

transformativeacquisition

(revenue 40% ormore of yours)

make severalacquisitions of

varying size

merge witha competitorof roughlysimilar size

sell a facility,division or

business unit

sellyour

company

Management Survey Results

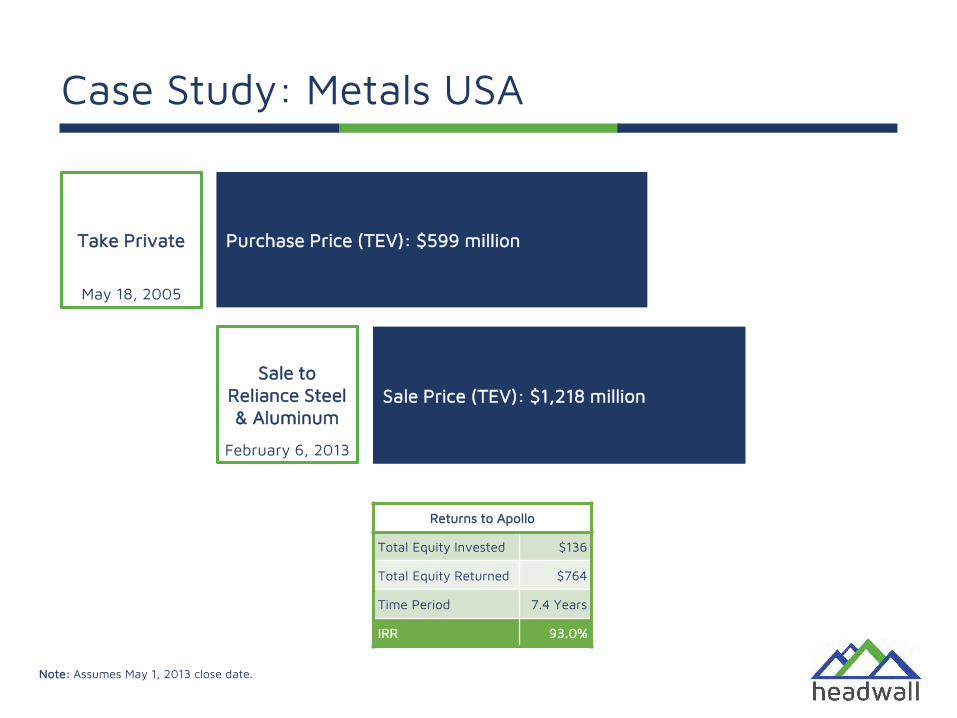

Case Study: Metals USA

Take Private

Sale to Reliance Steel & Aluminum

Purchase Price (TEV): $599 million

Sale Price (TEV): $1,218 million

May 18, 2005

February 6, 2013

Returns to Apollo

Total Equity Invested $136

Total Equity Returned $764

Time Period 7.4 Years

IRR 93.0%

Note: Assumes May 1, 2013 close date.

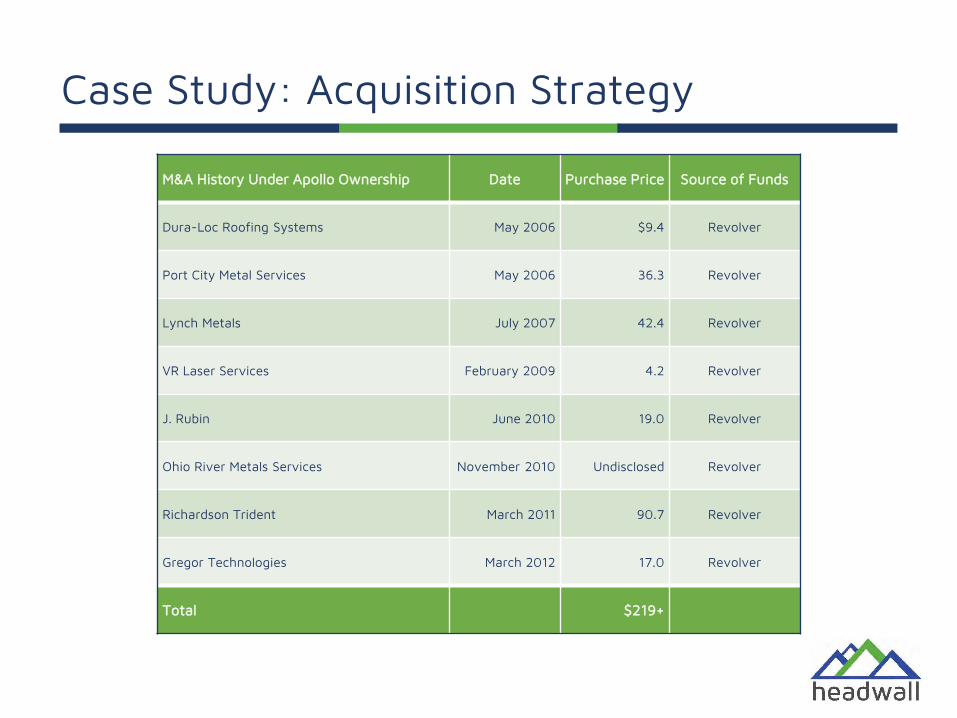

Case Study: Acquisition Strategy

M&A History Under Apollo Ownership Date Purchase Price Source of Funds

Dura-Loc Roofing Systems May 2006 $9.4 Revolver

Port City Metal Services May 2006 36.3 Revolver

Lynch Metals July 2007 42.4 Revolver

VR Laser Services February 2009 4.2 Revolver

J. Rubin June 2010 19.0 Revolver

Ohio River Metals Services November 2010 Undisclosed Revolver

Richardson Trident March 2011 90.7 Revolver

Gregor Technologies March 2012 17.0 Revolver

Total $219+

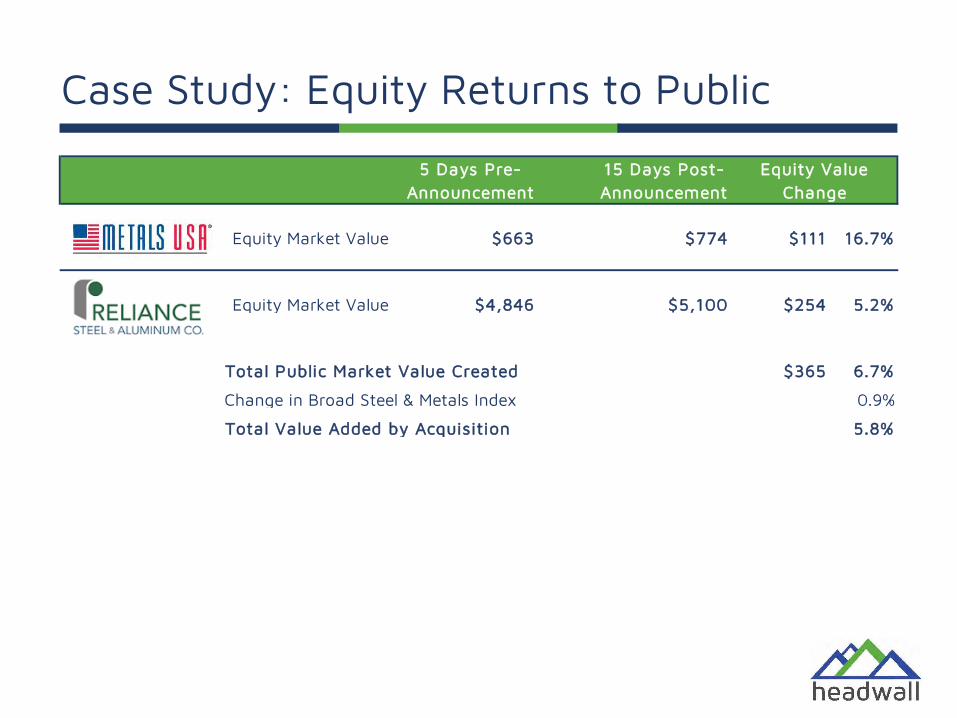

Case Study: Equity Returns to Public

5 Days Pre-Announcement

15 Days Post- Announcement

Equity Market Value $663 $774 $111 16.7%

Equity Market Value $4,846 $5,100 $254 5.2%

Total Public Market Value Created $365 6.7%

Change in Broad Steel & Metals Index 0.9%

Total Value Added by Acquisition 5.8%

Equity Value Change

Types of Acquirers

Infrequent larger acquisitionsFrequent large and small acquisitions

Infrequent smaller acquisitions Frequent smaller acquisitions

Infrequent Frequent

Larger

Smaller

Systematic

Cautious Tuck-In

Number of Transactions

<10 10+

Types of Acquirers

Infrequent Frequent

Larger

Smaller

Systematic (4)

Cautious (6) Tuck-In (6)

Larg

est

Acq

uisi

tion

as

a %

of

Mar

ket

Cap

>20

%<

20%

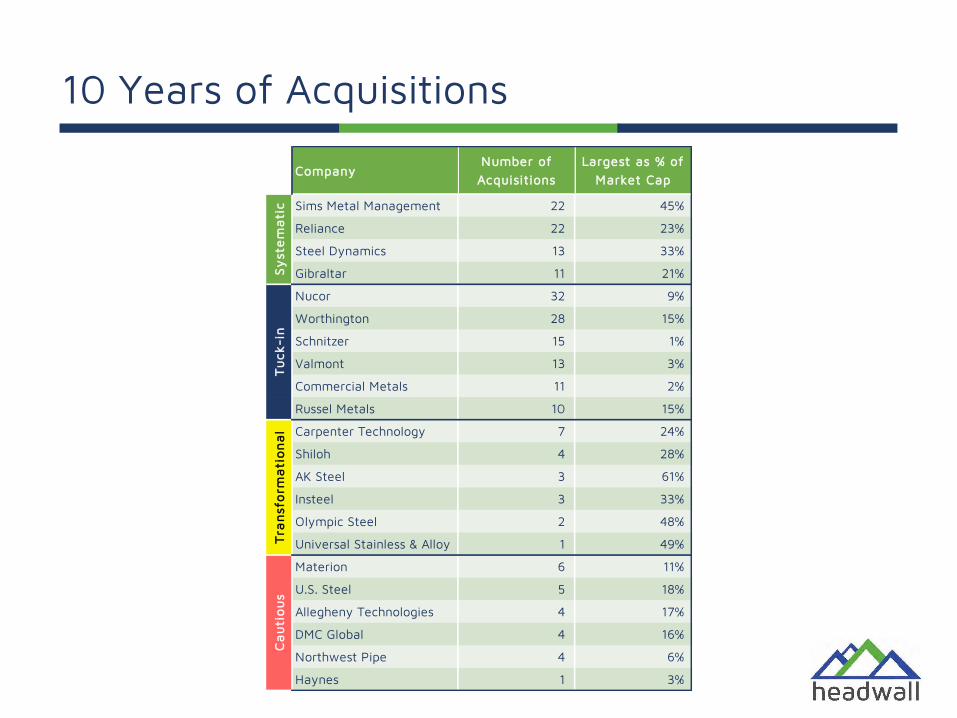

10 Years of Acquisitions

CompanyNumber of

AcquisitionsLargest as % of

Market Cap

Sims Metal Management 22 45%

Reliance 22 23%

Steel Dynamics 13 33%

Gibraltar 11 21%

Nucor 32 9%

Worthington 28 15%

Schnitzer 15 1%

Valmont 13 3%

Commercial Metals 11 2%

Russel Metals 10 15%

Carpenter Technology 7 24%

Shiloh 4 28%

AK Steel 3 61%

Insteel 3 33%

Olympic Steel 2 48%

Universal Stainless & Alloy 1 49%

Materion 6 11%

U.S. Steel 5 18%

Allegheny Technologies 4 17%

DMC Global 4 16%

Northwest Pipe 4 6%

Haynes 1 3%

Ca

uti

ou

sT

ran

sfo

rma

tio

na

lT

uck

-in

Sy

ste

ma

tic

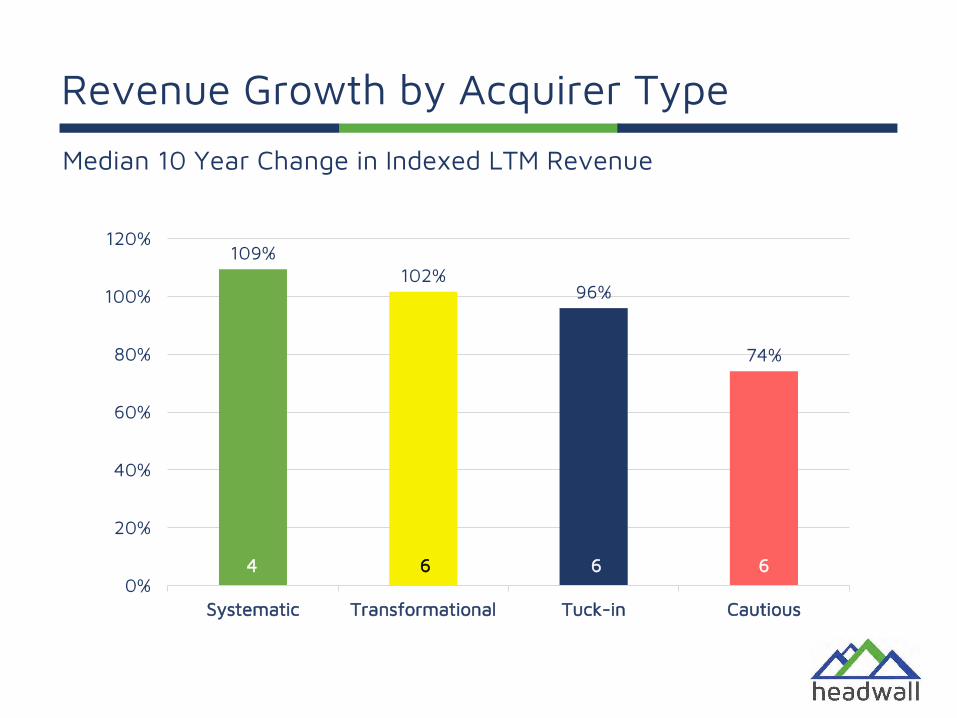

Revenue Growth by Acquirer Type

109%102%

96%

74%

0%

20%

40%

60%

80%

100%

120%

Systematic Transformational Tuck-in Cautious

Median 10 Year Change in Indexed LTM Revenue

64 66

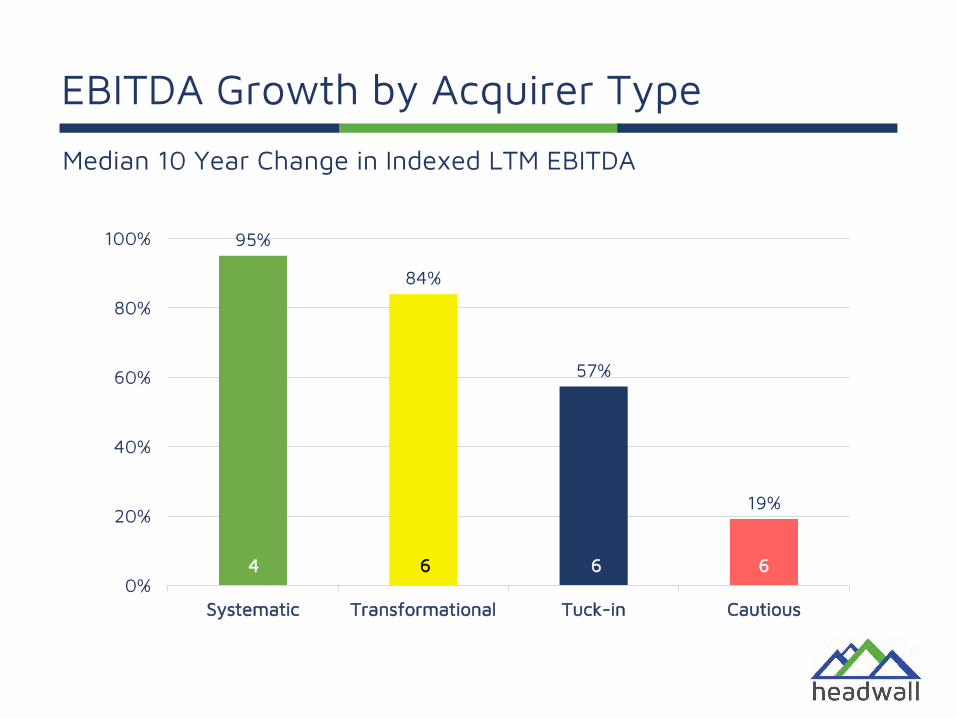

EBITDA Growth by Acquirer Type

95%

84%

57%

19%

0%

20%

40%

60%

80%

100%

Systematic Transformational Tuck-in Cautious

Median 10 Year Change in Indexed LTM EBITDA

64 66

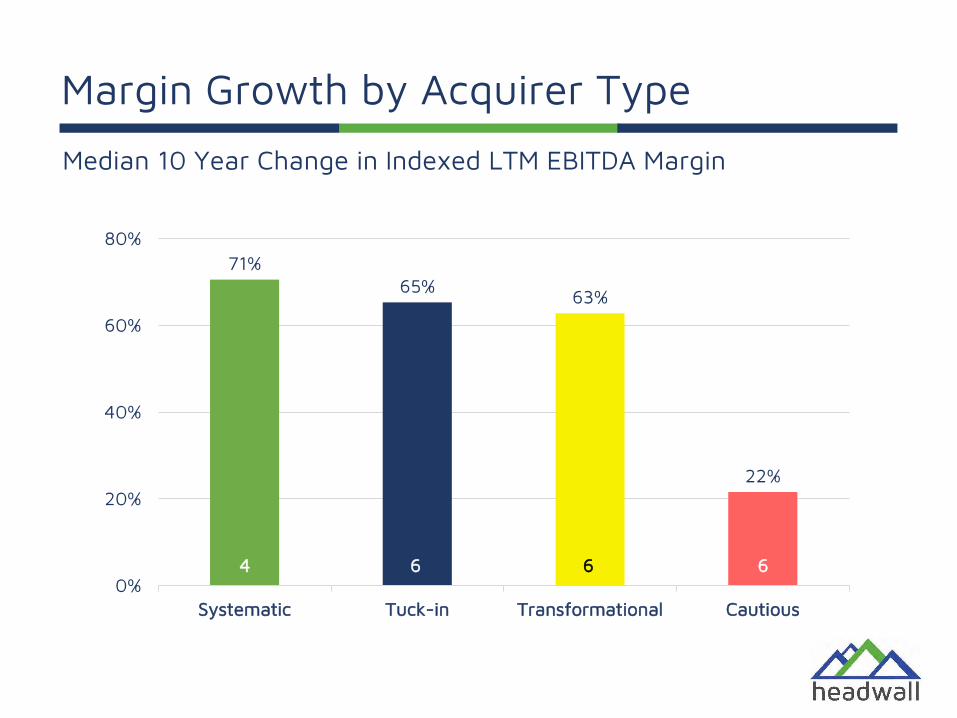

Margin Growth by Acquirer Type

71%65% 63%

22%

0%

20%

40%

60%

80%

Systematic Tuck-in Transformational Cautious

Median 10 Year Change in Indexed LTM EBITDA Margin

64 66

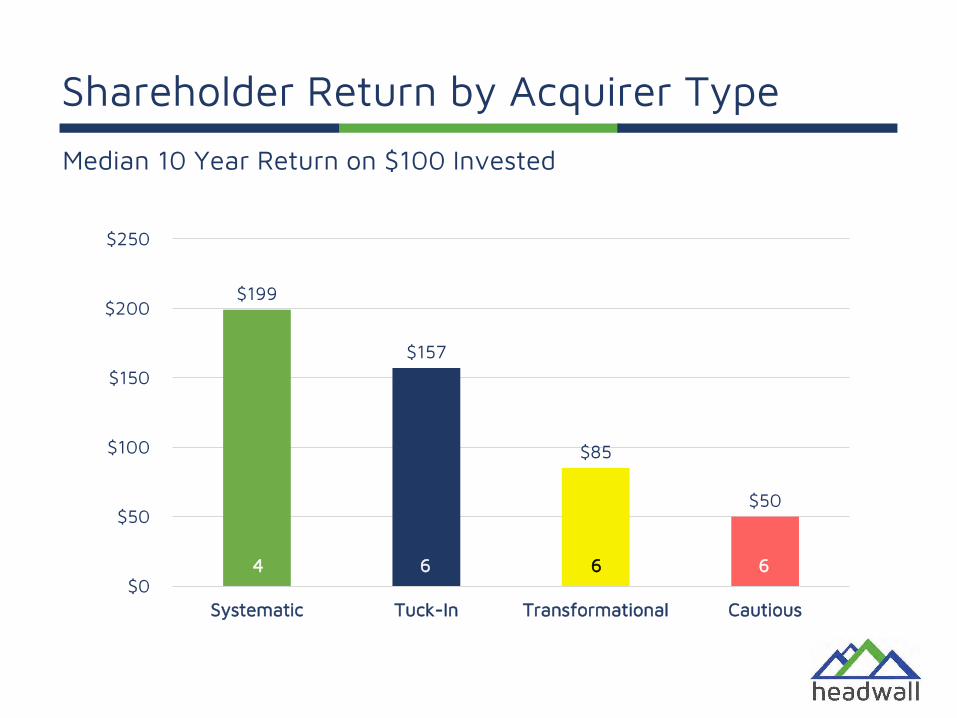

Shareholder Return by Acquirer Type

6 6 6 4

$199

$157

$85

$50

$0

$50

$100

$150

$200

$250

Systematic Tuck-In Transformational Cautious

64 66

Median 10 Year Return on $100 Invested

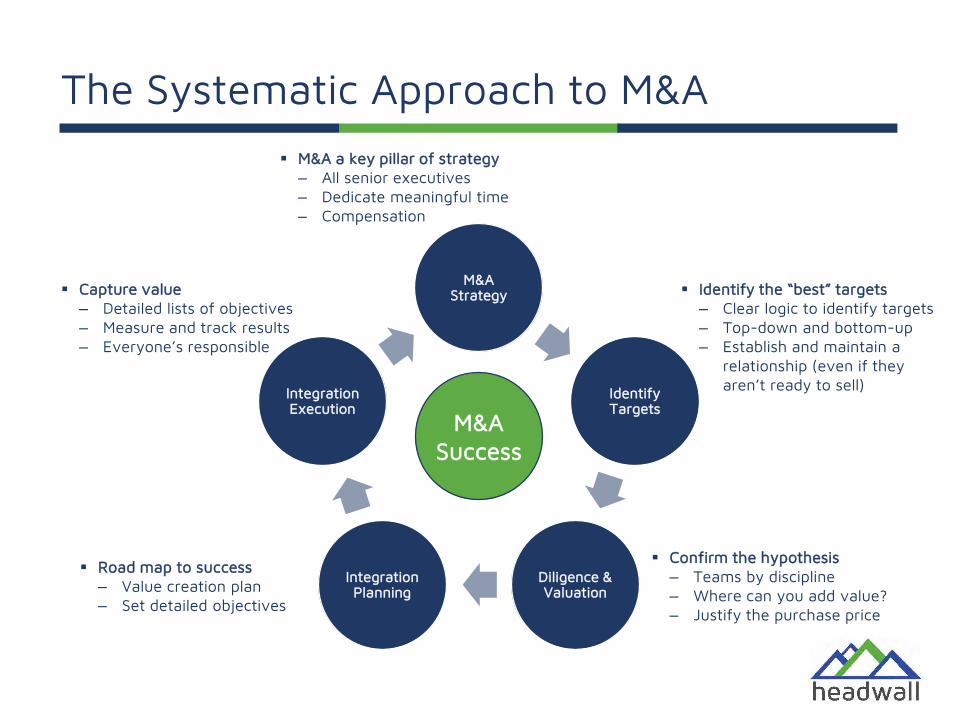

The Systematic Approach to M&A

M&A Strategy

Identify Targets

Diligence & Valuation

Integration Planning

Integration Execution

M&ASuccess

Capture value‒ Detailed lists of objectives ‒ Measure and track results ‒ Everyone’s responsible

Road map to success‒ Value creation plan‒ Set detailed objectives

Confirm the hypothesis‒ Teams by discipline‒ Where can you add value?‒ Justify the purchase price

Identify the “best” targets‒ Clear logic to identify targets‒ Top-down and bottom-up‒ Establish and maintain a

relationship (even if they aren’t ready to sell)

M&A a key pillar of strategy‒ All senior executives‒ Dedicate meaningful time‒ Compensation

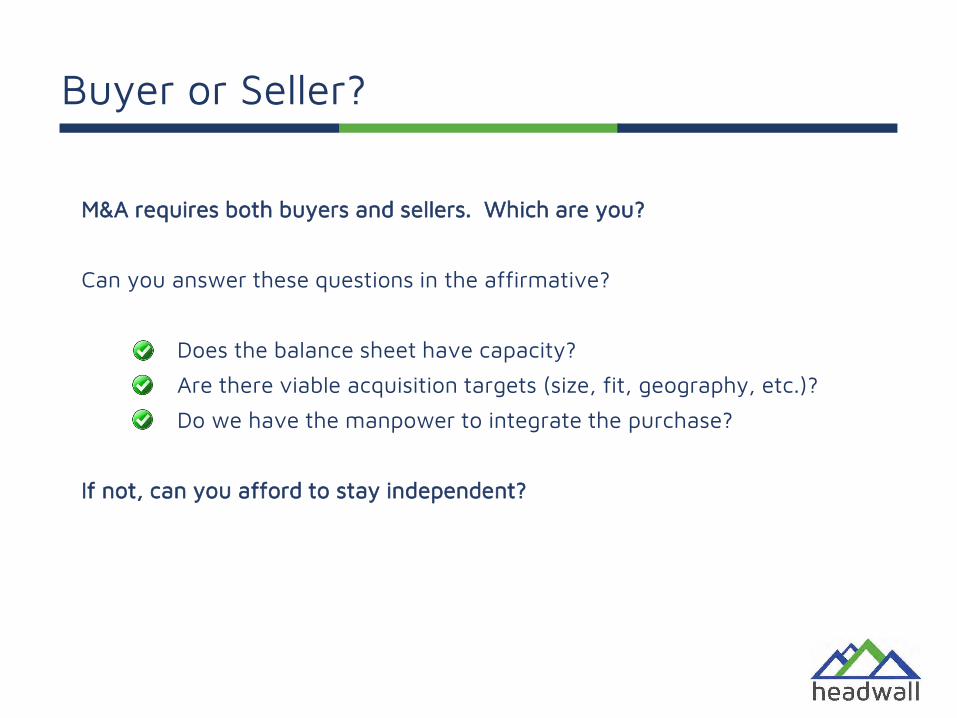

Buyer or Seller?

M&A requires both buyers and sellers. Which are you?

Can you answer these questions in the affirmative?

Does the balance sheet have capacity?

Are there viable acquisition targets (size, fit, geography, etc.)?

Do we have the manpower to integrate the purchase?

If not, can you afford to stay independent?

Conclusions

Competition in the North American steel sector bears the attributes of a zero-sum game, making traditional growth tactics less effective.

A systematic approach to acquisitions can meaningfully accelerate growth and can meaningfully add value to businesses in the steel sector. Companies that have followed this approach materiallyoutperform their peers, on average, over time.

Companies with a passive approach to M&A are more likely to underperform. These companies should consider becoming more aggressive in pursuing acquisitions or consider selling their businesses.

Headwall Partners Overview

• Boutique investment bank

• Steel & metals sector focus

• Deep industry expertise

• Broad transaction experience

• Extensive relationships with industry leaders and investors

• Senior level attention

• Product specialists through alliances

Transactions in securities are executed by a registered broker-dealer.

Steel, Metals, & Mining

80+ transactions, $30+ bn total valueSteel Metals & Mining

Selected sectors:• Mini mills• Integrated mills• Service Centers• Processors• Pipe & tube• Iron ore / scrap• Coal• Aluminum• Ferroalloys

Transactions:• Buy-side M&A• Sell-side M&A• Mergers• Divestitures• IPOs• Equity• High Yield• Term loans• ABLs• Converts• Restructuring

Transactions in securities are executed by a registered broker-dealer.

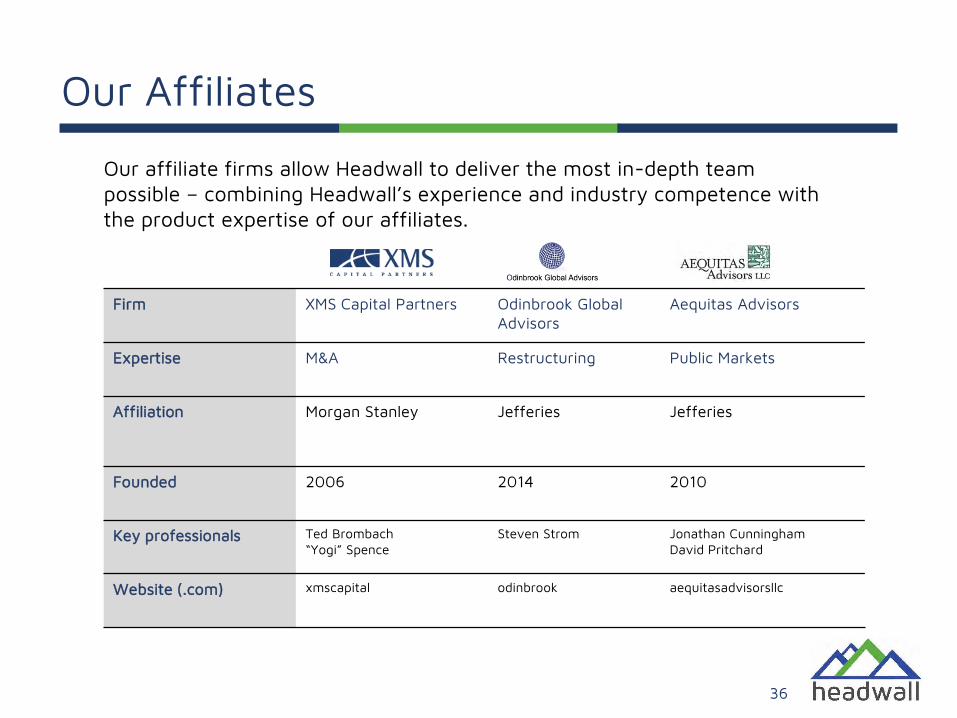

Our Affiliates

36

Firm XMS Capital Partners Odinbrook Global Advisors

Aequitas Advisors

Expertise M&A Restructuring Public Markets

Affiliation Morgan Stanley Jefferies Jefferies

Founded 2006 2014 2010

Key professionals Ted Brombach“Yogi” Spence

Steven Strom Jonathan CunninghamDavid Pritchard

Website (.com) xmscapital odinbrook aequitasadvisorsllc

Our affiliate firms allow Headwall to deliver the most in-depth team possible – combining Headwall’s experience and industry competence with the product expertise of our affiliates.

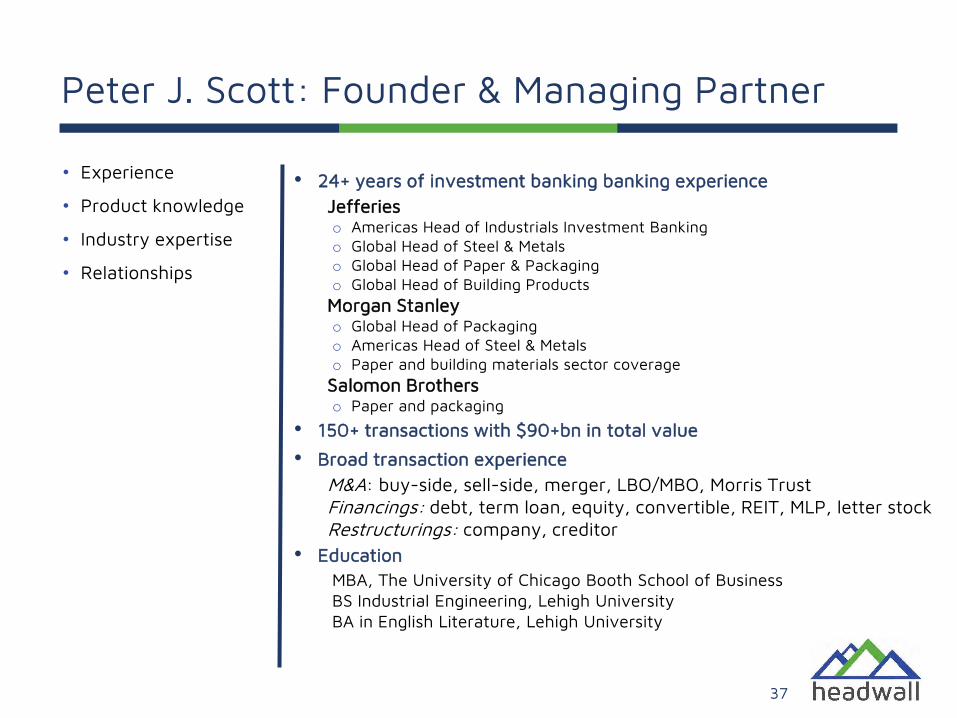

Peter J. Scott: Founder & Managing Partner

• 24+ years of investment banking banking experienceJefferieso Americas Head of Industrials Investment Bankingo Global Head of Steel & Metalso Global Head of Paper & Packagingo Global Head of Building Products Morgan Stanleyo Global Head of Packagingo Americas Head of Steel & Metalso Paper and building materials sector coverageSalomon Brotherso Paper and packaging

• 150+ transactions with $90+bn in total value

• Broad transaction experienceM&A: buy-side, sell-side, merger, LBO/MBO, Morris TrustFinancings: debt, term loan, equity, convertible, REIT, MLP, letter stockRestructurings: company, creditor

• EducationMBA, The University of Chicago Booth School of BusinessBS Industrial Engineering, Lehigh UniversityBA in English Literature, Lehigh University

37

• Experience

• Product knowledge

• Industry expertise

• Relationships