Embed Size (px)

Citation preview

Stock Return Synchronicity and Price Informativeness:

Evidence from the Corporate Bond Market

Wei Haoa, Andrew Prevost b*, Udomsak Wongchotic

a,c School of Economics and Finance, Massey University, Palmerston North, New Zealand

b Grossman School of Business, University of Vermont, Burlington, VT 05405, USA

Abstract

Prior research reports contradictory evidence regarding the association between stock price

synchronicity and price informativeness. We contribute to this debate by examining the relation

between return synchronicity and the pricing and design of corporate debt securities. Stock price

synchronicity is negatively associated with the cost of corporate debt, and is pronounced among

bonds with lower credit quality and shorter maturity. Further analysis demonstrates that lower

stock price synchronicity is also related to a greater likelihood of bonds issued with call provisions

and a higher likelihood of split S&P and Moody’s bond ratings. These results support the view that

lower stock price synchronicity reflects greater information impairment.

Keywords: Stock return synchronicity; Information asymmetry; Corporate debt

_________________________

* Corresponding author. Email: [email protected]

1

1. Introduction

The interpretation of stock price synchronicity (or R2) as a measure of price

informativeness has been the subject of considerable debate. The conventional view (e.g. Morck,

Yeung and Yu, 2000; Durnev, Morck, Yeung and Zarowin, 2003; Durnev, Morck and Yeung, 2004)

holds that greater co-movement between stock and market returns reflects less public firm-specific

information. The underlying rationale for this interpretation is that as firm-specific information is

imputed into the stock price via the trading process, the stock return’s co-movement (or

synchronicity) with the market index decreases. However, a number of recent studies have found

contradictory evidence and have proposed that lower R2 instead captures noise regarding firm-

specific news and thus a greater level of information inefficiency (see e.g. Kelly, 2014; Dasgupta,

Gan and Gao, 2010; Rajgopal and Venkatachalam, 2010; Teoh, Yang and Zhang, 2009; Ashbaugh-

Skaife et al., 2006; Devos, Hao, Prevost, Wongchoti, 2015).1

In this study, we contribute to the debate over whether stock price synchronicity is directly

or inversely related to price informativeness by examining the role of synchronicity in the pricing

and structure of corporate bonds. While equity and debt issued by the same firm represent different

claims, they are joint claims on the same underlying assets of the firm (Kwan, 1996). Therefore,

any changes in the value of firm’s underlying assets or changes in firm’s asset return variance will

cause changes in value for both equity and debt. In other words, value-relevant information (e.g.

public firm-specific information) as reflected by stock price movements should also impact the

value of the firm’s debt. Further, Downing, Underwood and Xing (2009) and Hotchkiss and Ronen

(2002) investigate the dynamics of firm-specific information flow between the stock and bond

markets and document evidence of firm-specific information spillover from the equity market to

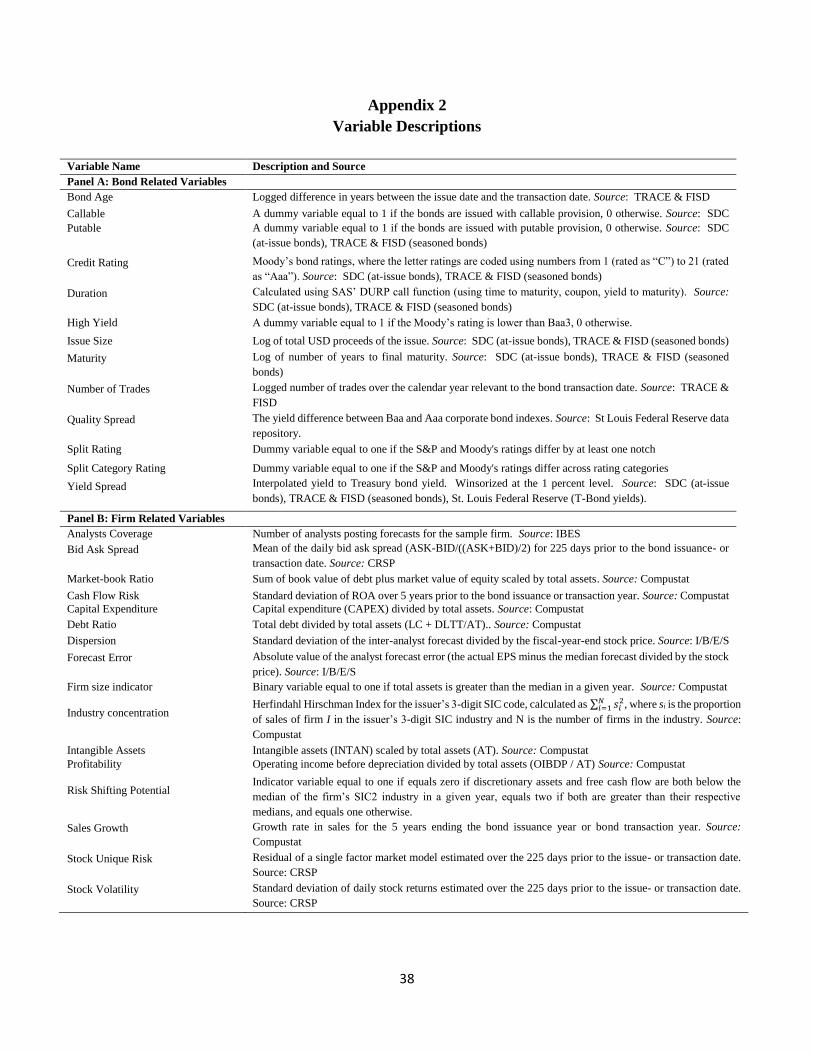

1 Appendix 1 provides a survey of these two literatures.

2

the bond market. Their findings suggest that stock price efficiency extends from the stock market

to the bond market; therefore, a measure drawn from stock price movements should be relevant to

investors of the issuer’s bonds.

Additionally, studying the relation between stock price synchronicity and price

informativeness using the structure and pricing of the firm’s debt as an experimental setting offers

several advantages. First, price movements in the bond market are less subjective to noise trading

(e.g. individual investors with behavioral biases that can move prices away from fundamentals

regardless of information quality) in comparison to those observed in the equity market. To the

extent that stock price informativeness should reflect the quality of public firm-specific

information available in the capital market, studying the impact of R2 on the pricing of the firm’s

debt allows us to reconcile ambiguous findings of previous equity-based studies which might be

partly driven by noise trading. Second, the risk premium on corporate bonds is relatively

deterministic and can be explained by components related to default, liquidity and information.

Thus, the ability of the synchronicity measure to explain risk premia on corporate bonds, apart

from controls for the default and liquidity components, implies that synchronicity represents

informational risk (e.g. uncertainty around the quality of public firm-specific information about

the issuer). In addition, the firm-specific public information explanation for synchronicity also has

connotations for the ability of market intermediaries to reach consensus on the default risk of bonds;

if synchronicity is related to the quality of the information environment, then synchronicity should

have explanatory value for the propensity of rating agencies to reach convergent opinions on the

likelihood of default for corporate borrowers. Lastly, following theoretical models by Bodie and

Taggart (1978), Barnea, Haugen and Senbet (1980), and Robbins and Schatzberg (1986), the

information explanation implies that synchronicity should have explanatory value in the design of

3

corporate debt securities to the extent that structural characteristics such as callable provisions are

a means for managers to mitigate information asymmetry with the capital market.

Based on samples of at-issue corporate bonds and secondary market bond transactions, our

preliminary univariate results show that bonds issued by firms with low stock price synchronicity

tend to have characteristics associated with greater information risk. Specifically, they receive

poorer credit ratings, provide higher yields to maturity, are more likely to receive divergent

Moody’s and S&P ratings, and are more likely to include call provisions at issuance. Further

multivariate analyses corroborate the above findings and provide additional evidence that lower

stock price synchronicity is associated with less public firm-specific information. Consistent with

the view that non-investment grade bonds are more sensitive to firm-specific information (see, e.g.,

Kwan, 1996), the negative relation between synchronicity and yield spread is stronger among high

yield bonds.

Finally, our analysis of at-issue credit ratings and the choice to include call provisions in

newly issued bonds allows us to address whether return synchronicity is driven by asymmetry

between corporate insiders and outside market participants, or by asymmetry between market

outsiders. Extant research points to an ‘insider-outsider’ explanation for divergent credit ratings

and for the use of call provisions. The ability for synchronicity to explain these characteristics

provides direct evidence that R2 can be used to measure the extent and quality of public firm-

specific information provided by companies to market participants. Overall, our results are

consistent with the view that lower synchronicity is associated with greater information

impairment.

4

The remainder of this paper is organized as follows: Section 2 reviews related literature

and develops our hypotheses. Section 3 describes data and methodology. Section 4 presents

empirical results and Section 6 concludes.

2. Literature Review and Hypotheses Development

2.1 Stock price synchronicity and price informativeness

The information-based explanation for R2 originates with Roll (1988), who calculates R2 of

large stocks using both single- and multiple factor regression models. Roll (1988) observes low R2

and little relation between R2 and public news events, suggesting that there is high firm-specific

return variation among large US stocks. Despite the growing body of literature studying R2 (or

stock price synchronicity) following Roll (1988) and the wide range of application of R2 in the

finance and accounting literature, the fundamental question of what R2 actually captures, and how

it should be interpreted, remains an open question.

The conventional view contends that R2 is inversely associated with public firm-specific

information, i.e. low R2 reflects the incorporation of a greater amount of firm-specific information

into stock prices so that low R2 represents more informative stock prices. This view was initiated

by Morck, Yeung and Yu (2000), who documented that high GDP countries, compared with low

GDP countries, experience lower stock return synchronicity. They attribute this lower

synchronicity to greater firm-specific information capitalization in high GDP countries.

Subsequent research have further expanded this view into a firm-level phenomenon. Durnev,

Morck, Yeung and Zarowin (2003) examine the relationship between firm-specific stock return

variation (i.e. 1- R2) and different accounting measures of stock price informativeness. They find

that greater firm-specific variation is associated with more informative stock prices. Also, firms

with lower R2 exhibit a greater sensitivity between current stock returns and firm-specific

5

information (represented by future earnings), suggesting that more information is incorporated into

stock returns of low R2 firms. Further, Durnev, Morck and Yeung (2004) use firm-specific return

variation as a proxy for price informativeness and find that capital investment decisions become

more efficient when stock prices are more informative. Their findings indicate that a better

information environment (e.g. less information asymmetry between corporate insiders and outsider

investors) is associated with lower stock R2. Based on the premise that R2 reflects firm-specific

information impounded in stock prices, more recent work finds that lower R2 stocks are associated

with increased information transparency (Jin and Myers, 2006), enforcement of insider trading

laws (Fernandes and Ferreira, 2009), lower board independence (Ferreira and Smith, 2006), lower

chance of stock overpricing due to investor inattention (Stowe and Xing, 2010), lower probability

of opaque financial reports and crash risk (Hutton, Marcus, and Tehranian, 2009), less analyst

forecasting activities (Piotroski and Roulstone, 2004; Chan and Hameed, 2006), and diminished

separation between control and cash flow rights (Boubaker, Mansali and Rjiba, 2014)

A developing line of research provides evidence supporting the opposite conclusion: low

R2 is associated with less public firm-specific information and stock prices with lower information

content. Using four earnings-based measures as proxies for information quality, Teoh, Yang and

Zhang (2009) show that stock prices of low R2 firms are not more reflective of its future earnings.

Li, Rajgopal and Venkatachalam (2014) and Kelly (2014) add to this view by examining various

firm and stock characteristics associated with R2, demonstrating that low R2 stocks are associated

with characteristics consistent with a noisier information environment. For example, Kelly (2014)

associates smaller, less liquid, and less followed firms with lower R2 and diminished probability

of informed trading (PIN). Hou, Peng and Xiong (2013) provide additional support for this

contention by providing evidence that investor sentiment is a key driver of low R2. At the same

6

time, Gassen, LaFond and Skaife (2014) show that illiquidity (a market friction) is the first order

determinant of R2. Additional research provides evidence for this view through information event

settings. Dasgupta, Gan and Gao (2010) examine changes in return synchronicity before and after

events that should affect stock price informativeness. In contrast to the conventional wisdom, R2

generally increases after information events such as seasoned equity issues and ADR listings.

Devos, Hao, Prevost and Wongchoti (2015) document stronger abnormal return, volume, and

volatility reactions to analyst recommendation revisions among lower R2 stocks. To the extent that

corporate outsiders such as equity analysts facilitate the interpretation of limited amount of firm-

specific information among more opaque firms, these results support the view that analysts provide

a greater role as information intermediaries for firms that are less synchronized with the market.

Finally, Chan and Chan (2014) document a negative relation between R2 and the discount of

seasoned equity offerings. To the extent that the SEO discount represents the existence of

information asymmetry between managers and investors, their findings suggest that low R2 is an

indication of greater information asymmetry among insiders and outsiders of a corporation (e.g.

the deficiency of public firm-specific information).

2.2 Stock price synchronicity and the cost of debt

We contribute to this literature by examining the relation between stock price synchronicity

and the pricing and structure of corporate bonds. Following the standard view that the risk premia

of corporate bonds are based on components related to default, liquidity, and information (e.g.

Hubbard and O’Brien, 2014), R2 should be associated with the cost of debt to the extent that it

reflects a dimension of information risk to investors. Therefore, we begin our analysis by testing

how R2 affects the cost of debt as defined by credit ratings and corporate bond yield spreads.

7

Bond credit ratings are a broad summary of the ability to repay financial commitments and

can be used as an alternative measure of cost of debt. There is evidence from previous research

that the quality of firm-specific information affects credit ratings. For example, Odders-White and

Ready (2006) find that the amount of non-public firm-specific information captured by equity-

based adverse selection measures is significantly negatively related to credit ratings. Based on the

premise that adverse selection reflects the information imbalance between corporate insiders and

outside investors, their findings indicate that firms with higher information asymmetry are

associated with lower credit ratings after controlling for other explanatory variables. In a similar

vein, Yu (2005) suggests that rating agencies specifically include the quality of information

disclosure as a determinant of corporate bonds’ credit ratings, indicating that information

asymmetry affects the rating decisions made by the rating agencies. To the extent that corporate

bonds’ credit ratings inversely measure cost of debt, then firms with lower R2 should be associated

with greater cost of debt as reflected by lower credit ratings if low R2 represents greater information

impairment:

H1: Stock price synchronicity is positively associated with credit ratings.

There is a long line of literature on the determinants of bond risk premia. Research on the

default risk component builds on the seminal work of Black and Scholes (1973) and Merton (1974).

Merton (1974) introduces a structural model that incorporates default risk into corporate bond

valuation based on the option pricing model developed by Black and Scholes (1973). Merton’s

model has been further extended in many studies. For example, Anderson and Sundaresan (1996)

incorporate insights of corporate finance research into bond valuation and find that strategic debt

service increases default risk and hence yield spread. Campbell and Taksler (2003) find that equity

volatility can explain as much yield spread changes as can credit ratings. Since debt claims can be

8

valued as a put option short position (Merton, 1973), they suggest that the value of put option

increases with the equity volatility which benefits equity holders at the expense of bond holders.

Furthermore, Collin-Dufresne and Goldstein (2001) modify the structural model to incorporate a

more complex capital structure, where firms are allowed to adjust their capital structure to reflect

changes in asset value. However, the yield spreads predicted by the traditional Merton model are

found to be far below the empirically observed corporate yield spread and corporate yield spreads

cannot be solely explained by default risk. Collin-Dufresne, Goldstein and Martin (2001) examine

the theoretical determinants of default proposed by the traditional structural model (e.g. changes

in spot rate, changes in the slope of the yield curve, leverage, volatility, etc.) and find that these

credit risk-related variables have limited ability to explain corporate yield spread. Similarly,

Huang and Huang (2012) explore how much of historically observed yield spreads can be

explained by credit risk and conclude that the risk of default explains only a small portion of yield

spread for bonds. Elton, Gruber, Agrawal and Mann (2001) find that corporate bonds paying

higher coupon rates are subject to higher tax burden and are hence less attractive to investors. Even

after taxes and default risk are both included in the corporate bond pricing model, Elton, Gruber,

Agrawal and Mann (2001) conclude that a large portion of the yield spread still remains

unexplained.

A significant determinant of yield spread missing in the early bond pricing literature is

liquidity. Longstaff, Mithal and Neis (2005) decompose corporate yield spread into default and

non-default components using credit default swap data. They find that default risk explains a large

portion of the yield spread, with the remaining component related to measures of liquidity.

Confirming the findings of Longstaff, Mithal and Neis (2005), Chen, Lesmond and Wei (2007)

establish a negative relation between bond specific liquidity and yield spread. Focusing on

9

aggregate-level liquidity risk, Lin, Wang and Wu (2011) document a positive relation between

aggregate liquidity beta and corporate bond returns. Their findings suggest that more liquidity-

sensitive bonds earn higher returns than less liquidity-sensitive bonds. Huang, Huang and Oxman

(2015) further extend the structural bond pricing model by including stock market liquidity and

provide consistent evidence that the deterioration of stock market liquidity increases bond yield

spreads.

Recent research identifies information risk as a further important determinant overlooked

in previous work. Yu (2005) finds that firms with good information disclosure quality tend to have

lower credit spreads and the negative relation between accounting transparency and yield spread

is particularly strong for short-term bonds. Mansi, Maxwell and Miller (2011) investigate the

relation between analyst forecast characteristics and the cost of debt. Given that analyst forecast

activities contribute to firm’s information environment by reducing information inefficiency, they

demonstrate that corporate bond yield spreads are reduced with increases in analyst activities.

Zhou (2010) directly incorporates liquidity and information risk into the corporate bond pricing

model. Consistent with previous findings, he finds that liquidity affects the yield spreads of risky

corporate bonds, and more importantly he also finds that information uncertainty of individual

bonds provides significant additional explanatory power to yield spread. Using various measures

to capture information uncertainty (measured by accruals quality, firm age, analyst coverage,

forecast dispersion, PIN, and order imbalances), Lu, Chen and Liao (2010) show that corporate

bond yield spreads contain a significant risk premium for investors who bear information risk.

With respect to the term structure, their results indicate that information impairment have stronger

effects for short-maturity bonds than for long-maturity bonds.

10

As discussed above, the quality of public firm-specific information surrounding the firm

should have direct impact on bond pricing due to information risk. Within a poor information

environment, bond investors only have access to limited and imprecise information about firm

value and would require a higher return for increased risk, leading to a widened yield spread2. To

the extent low R2 represents greater information impairment, low R2 firms should be associated

with greater cost of debt as indicated by greater corporate yield spread. This motivates Hypothesis

2 as follows:

H2: Stock price synchronicity is negatively associated with yield spread.

The negative relation between R2 and yield spread should be stronger for high yield (non-

investment grade) bonds with greater exposure to information risk. As Kwan (1996) demonstrates,

low rated bonds are particularly sensitive to firm-specific information. In the same vein, Mansi,

Maxwell and Miller (2011) find that the information contained in analysts’ forecasts is most

valuable when the uncertainty about firm value is the highest (i.e. for firms with high information

uncertainty). Also, Han and Zhou (2014) show that bonds that are closer to default are more

sensitive to information impairment. Compared with investment-grade bonds, these findings

suggest that investors holding high yield bonds should be more sensitive to information risk and

require a relatively higher risk premium, leading to a stronger sensitivity of yield spread to R2, as

predicted by Hypothesis 2a:

H2a: The relation between stock price synchronicity and yield spread is stronger for high yield

bonds.

2 Han and Zhou (2014) provide evidence that informed bond trading is present in US corporate bond markets,

especially for high-yield and private-firm bonds. This suggests that information risk is higher for issuers with less

public firm-specific information as better-informed traders can better exploit their informational advantage.

11

In addition, the negative relation between R2 and yield spread should be stronger for bonds

with short term maturity. Traditional structural models (such as Leland, 1994; Longstaff and

Schwartz, 1995) suggest that bond credit spread diminishes and eventually goes to zero as the

maturity approaches to zero regardless of issuing firm’s credit quality. However, Duffie and Lando

(2001) indicate that this is not true under an imperfect information environment, especially for

short term maturity bonds. Consistent with Duffie and Lando (2001), Yu (2005) and Lu, Chen and

Liao (2010) show that the impact of information risk on yield spread intensifies as bond maturity

decreases. Therefore, if low R2 represents greater information uncertainty (e.g. firm-specific noise

as a result of poor quality public firm-specific information), the negative relation between R2 and

yield spread should be pronounced for short maturity bonds than for long maturity bonds:

H2b: The relation between stock price synchronicity and yield spread is stronger for short maturity

bonds.

2.2 Stock price synchronicity and split credit ratings

A bond rating that is ‘split’ signifies divergence of opinion between Moody’s and S&P in

assessing the creditworthiness of the issuing firm; bonds issued by firms with poor firm-specific

information quality are more likely to receive split ratings between the two rating agencies because

of a greater likelihood that different conclusions will be drawn from limited relevant information

about the issuer. Existing work on the determinants of split bond ratings (see e.g. Morgan, 2002;

Livingston and Zhou, 2010) also demonstrates a strong association with the degree of information

opacity. Therefore, if low R2 represents greater information impairment, then bonds issued by

lower R2 firms should have a higher probability of receiving split Moody’s and S&P ratings as

predicted by Hypothesis H3:

H3: Stock price synchronicity is negatively associated with the incidence of split credit ratings.

12

2.3 Stock price synchronicity and callable debt

While issuing callable bonds can impose higher up-front costs of borrowing to

corporations, the theoretical models developed by Barnea, Haugen and Senbet (1980) and Robbins

and Schatzberg (1986) point out that firms do so to either preserve their ability to refinance (while

retaining private information not yet to be strategically released) or to send a credible (i.e. costly)

signal to market participants about their optimistic future prospects. These explanations are

conditional on the presence of information asymmetry between managers and corporate outsiders.

As a result, the ability to call back the bonds should be more beneficial for firms with relatively

less public firm-specific information. Banko and Zhou (2010) show that the information

asymmetry explanation of callable bonds significantly explains the decision of corporations to

issue callable bonds beyond the 1990s when interest rate became progressively lower. We employ

the information asymmetry-based explanation to the context of our study: if low R2 represents

greater information impairment, then firms with lower R2 should be more likely to issue bonds

with embedded call provisions.

H4: Stock price synchronicity is negatively related to the likelihood of embedded call options.

As noted by Banko and Zhou (2010), the landscape of the callable bond market has changed

dramatically through the years. Specifically, it has fallen in size from 80 percent of issued

corporate bonds prior to 1985 to as low as 30 percent per year in their sample (about 44 percent in

our sample). This reduction is due to a significant decrease in the issuance of investment-grade

bonds with call provisions that were motivated by higher interest rate during the 1980s. In the

more recent years, the high yield segment of the market has become the major source of callable

debt. Following prior findings, these issuers are more subject to information asymmetry problems.

13

According to the information asymmetry explanation for callable debt, the next hypothesis predicts

a pronounced sensitivity between synchronicity and the incidence of callable high yield debt:

H4: The relation between stock price synchronicity and the likelihood of embedded call option is

stronger for high yield bonds.

We investigate if there is cross-sectional variation in the impact of R2 on the choice to

include call provision in bonds. As Banko and Zhou (2010) point out, agency-related explanations

can be used to explain the motivation to issue callable debt. In addition to the information

asymmetry explanation, call provisions can be explained by agency-based theories relating to risk

shifting and underinvestment. The risk-shifting hypothesis developed by Barnea, Haugen and

Senbet (1980) illustrates that a call provision (a call option to the shareholders of the issuing

company) deteriorates in value when the issuing firm acquires riskier assets. This, in turn, reduces

the potential benefits of risk-shifting activities by shareholders. In other words, a call provision

can help mitigate agency conflicts between shareholders and bondholders. According to the

underinvestment hypothesis (Bodie and Taggart, 1978; Barnea, Haugen and Senbet, 1980),

managers of financially distressed firms pass up positive NPV projects because the gains benefit

bondholders and not shareholders. Callable debt resolves this conflict allowing managers to

refinance the outstanding debt at the time of investment at a rate that reflects the improved financial

prospects of the firm. In addition to a broader finding that issuers with lower ratings are more

likely to issue callable debt, Banko and Zhou (2010) document a significant interactive effect

between proxies for information asymmetry and underinvestment, but not between information

asymmetry and risk-shifting. Overall, they conclude that information asymmetry provides a

motivation for the issuance of callable debt, but only in the presence of underinvestment potential.

Our primary research question is if R2 is a valid proxy for public firm-specific information. In the

14

context of the findings of Banko and Zhou (2010), we explore if information asymmetry (as

proxied by R2) heightens the motive to include call provisions when there is the potential to

underinvest, and when there is the potential to shift risk to debtholders. These are summarized in

the following hypotheses:

H4a: The relation between stock price synchronicity and the likelihood of embedded call option is

stronger for companies with underinvestment potential.

H4a: The relation between stock price synchronicity and the likelihood of embedded call option is

stronger for companies with risk shifting potential.

3. Data and Methodology

Our empirical analysis is based on two samples: A broad sample of U.S. at-issue bonds

covering 1985-2013 and transaction-level price data covering 1994-2013. The two data sources

offer distinct advantages and drawbacks: the at-issue sample offers considerable cross-sectional

variation, however does not allow for a time-series of observations for a given bond. The

transaction-level dataset offers depth (time-series variation) at the bond level, at the cost of breadth.

Therefore, we employ both datasets throughout the paper according to the context. Data for at-

issue bonds are collected from SDC Platinum and pricing data for secondary market transactions

are collected from TRACE (Trade Reporting and Compliance Engine) and FISD (Fixed Income

Securities Database). Other firm-level characteristics are obtained from the I/B/E/S, Compustat,

and CRSP databases.

We estimate R2 for each firm based on the firm’s daily stock return data over the one year

period prior to the bond issuance year (for at-issue bonds) or the transaction year (for seasoned

bonds). R2 is estimated based on the four-factor model, which is defined as:

15

, (1)

where Rjt is the daily return of stock j and Rft is the daily risk-free T-Bill return; Rmt is the return

on the CRSP daily value-weighted index; SMBt is the difference between returns of equally-

weighted portfolio of small stocks and large stocks on day t; HMLt is the difference between returns

of equally-weighted portfolio of high book-to-market stocks and low book-to-market stocks on

day t, and UMDt is the difference of average returns between a high momentum portfolio and low

momentum portfolio on day t.3 Since R2 is bounded between 0 and 1, we follow the convention

in this literature (e.g. Morck, Yeung and Yu, 2000; Durnev, Morck, Yeung and Zarowin, 2003;

Durnev, Morck and Yeung, 2004) by converting R2 to the stock price synchronicity measure using

logged (R2/(1- R2)).

We begin by testing the basic association between stock price synchronicity and the cost

of debt as reflected by the credit rating (Hypothesis H1). We specify the model as:

i

i

i

i effectsYear fixedαctsfixed effe industry h Fama-Frencα

ononcentratiIndustry c αue risk Stock uniqαread Quality spαenditureexpCapital α

riskCash flow αyofitabilitPrαFirm sizeαask spreadBidαthSales growα

k ratioMarket-booαeragecovAnalyst αVolatilityαDebt ratioαDurationαPutableα

CallableαdesNumber traαBond ageαIssue sizeαitySynchronicααingCredit rat

49

20191817

1615141312

11109876

543210

(2)

We code Moody’s letter ratings into numbers from 1 (“C”) to 21 (“Aaa”). We employ three

measures to control for liquidity risk: Issue Size is related to the depth of the secondary market and

the larger the issue size the smaller the liquidity risk (Lu, Chen and Liao, 2010; Huang, Huang and

Oxman, 2015). For the sample of seasoned bonds, we also include Bond Age and Number of Trades

as additional liquidity measures. Greater Bond Age represents higher liquidity risk since older

bonds trade less frequently than younger bonds (Lu, Chen and Liao, 2010; Huang, Huang and

3 Daily data for SMH, HML and UMD data are obtained from Kenneth French’s data library, at

http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html.

jttjtjtjftmtjjftjtεUMDmHMLhSMBδ)R(RβαRR

16

Oxman, 2015). Similarly, greater Number of Trades is expected to reduce the yield spread due to

lower liquidity risk (Chuluun, Prevost and Puthenpurackal, 2014).

Information risk is also a key determinant of corporate bond yield spreads and should

provide significant explanatory power beyond default- and liquidity risk. Because proxies for firm-

specific information uncertainty are not absolutely deterministic, we include several alternative

financial- and analyst-based measures as control variables for information risk beyond stock price

synchronicity. As Clarke and Shastri (2000) argue, measures for information asymmetry generally

fall into categories based on stock analyst activity, measures of expected growth, and market

microstructure. These authors point out that each category has strengths and weaknesses and that

there is no single best measure. Therefore, our information asymmetry proxies are selected based

on these three categories including Analyst Coverage (Mansi, Maxwell and Miller, 2011 and

Chuluun, Prevost and Puthenpurackal, 2014), Book to Market Ratio and Sales Growth (Banko and

Zhou, 2010), and Bid Ask Spread (Chuluun, Prevost and Puthenpurackal, 2014).

Following related research, we include other firm- and issue-level related characteristics as

additional controls. At the bond level, Duration represents the effective maturity of bond and is

used to control for exposure to interest rate changes faced by investors. Callable and Putable are

dummy variables indicating whether the bond has embedded call or put provisions. At the firm

level, we additional dimensions of risks faced by investors that may not be fully captured by the

contemporaneous credit rating. These include Firm Size, Profitability, Cash Flow Risk, Debt Ratio,

Stock Volatility and Capital Expenditure. Because Firm size (logged total assets) and

Synchronicity are highly correlated, following the approach of Banko and Zhou (2010) we use an

indicator variable equal to one if total assets is greater than the sample median for each year.

Quality Spread is defined as the yield difference between the Baa and Aaa corporate bond indices

17

and controls for systematic credit risk exposure (e.g. Mansi, Maxwell and Miller, 2004; Klock,

Mansi and Maxwell, 2005), and we include fixed effects for year and Fama-French 49 industries.

To test H2, H2a and H2b, our strategy is to employ stock price synchronicity as a measure

of information risk in the bond valuation model while controlling for default and liquidity

components and additional bond-level control variables used in related work. Positive significance

of the Synchronicity coefficient would support the contention that R2 measures information risk

that reduces the prices of corporate bonds. Using the at-issue sample of yield spreads and, for

robustness, the seasoned bond sample, we specify the regression model as:

i

i

i

i

effectsYear fixedα

ctsfixed effe industry h Fama-FrencαononcentratiIndustry c αue risk Stock uniqαreadQuality spα

enditureexpCapital αriskCash flow αyofitabilitPrαFirm sizeαask spreadBidαthSales growα

k ratioMarket-booαeragecovAnalyst αVolatilityαDebt ratioαDurationαPutableαCallableα

desNumber traαBond ageαIssue sizeαt ratingized crediOrthogonalαitySynchronicααadYield spre

49212019

181716151413

1211109876

543210

(3)

The dependent variable Yield Spread is calculated as the difference between the yield to maturity

of sample corporate bond and the interpolated yield to maturity of Treasury corresponding to the

same time to maturity as the sample corporate bond. To calculate the interpolated yield to maturity

of Treasuries, we collect data about constant-maturity Treasury bond indices from the Federal

Reserve of St. Louis Economic Data (FRED), which provides daily yield to maturity data for

Treasury bond indices with constant maturities (e.g. 3-month, 6-month, 1-year, 2-year, 3-year, 5-

year, 7-year, 10-year and 20-year). We use linear interpolation to obtain an implied Treasury rate

for any maturity between 3 months and 20 years. For at-issue bonds, there is only one yield

observation for each bond and we merge it with other yearly data by the year of that observation.

For seasoned bonds, we aggregate multiple purchase and sale transactions occurring on the same

day into aggregated a trade-weighted daily yield to maturity based on the par amounts of each

18

transaction as weights, then use the yield observation of the closest transaction day to the fiscal

year end date to merge with other yearly data.

We use the same set of control variables are in Equation (2). To control for default risk,

our main control variable is Credit Rating using the bond’s Moody’s rating obtained from Mergent.

Since the information contained in remaining bond- and firm-level control variables is partially

captured by firms’ credit ratings (Mansi, Maxwell and Miller, 2004; Klock, Mansi and Maxwell,

2005; Mansi, Maxwell and Miller, 2011), we purge this information from ratings by creating

Orthogonalized Credit Rating, which captures only the information provided by credit ratings and

is unrelated to the information contained in the remaining control variables. Orthogonalized Credit

Rating is the residual from regressing Credit Rating on all other independent variables (including

synchronicity) included in the regression model.

Hypothesis 3 posits that greater information uncertainty, as captured by lower R2, increases

the likelihood that the rating agencies arrive at different conclusions regarding the issuer’s

creditworthiness. To investigate this prediction, we estimate the following probit model using the

at-issue- and seasoned bond samples:

i

i

i

i effectsYear fixedαctsfixed effe industry h Fama-FrencαdesNumber traα

BondageαCallable αIssue sizeαt ratingized crediOrthogonalαMaturityα

Firm sizeαenditureexpCapital αDispersionαreadBid-ask spαeragecovAnalyst α

rrorForecast eαtsgible assetanInαt ratioBook-markeαitySynchronicααngSplit rati

4915

1413121110

98765

43210

(4)

Using Moody’s and S&P ratings coded to numerical equivalents, we employ two alternative

measures of split ratings. First, we classify split ratings broadly using rating categories, where

Split category rating is equal to one if the Moody’s and S&P ratings differ across letter rating

categories, e.g. if Moody’s rating is Baa and the S&P rating is A-, and zero otherwise. Second,

we use a finer classification: Split rating equals one if the Moody’s and S&P ratings differ by one

19

notch or more, and zero otherwise. Following Livingston, Naranjo and Zhou (2007) and

Livingston and Zhou (2010), our control variables include accounting-based measures (Book

market ratio, Intangible assets, Capital expenditure), analyst opinion-based measures (Analyst

forecast error, Analysts coverage, Dispersion), liquidity measures (Bond age, Number of trades,

Issue size), market microstructure measures (Bid-ask spread) and other measures that control for

alternative dimensions of information risk (Firm size) along with additional bond-level

explanatory variables (Orthogonal credit rating, Maturity, and Callable). Consistent with

previous regression models, industry- and year fixed effects are included as additional controls.

To test Hypothesis H4, H4a and H4b we use the following probit regression model to

examine if stock price synchronicity explains the likelihood the bond contains call provisions, and

if there is significant cross-sectional variation according to higher underinvestment potential and

agency problems. Since the choice to include a call provision is made at the time of issue, we

model the call provision choice using the at-issue dataset using the following logistic regression

model:

i

i

i

i effectsYear fixedαctsfixed effe industry h Fama-Frencα

ononcentratiIndustry cαue risk Stcok uniqαIssue sizeαDurationαe slopyield curvChange in α

pe) curve sloStd.(Yieldαe slopeYield curvαDebt ratioαFirm sizeαyofitabilitPrα

yieldSynch*Highαl t potentiarinvestmenSynch*Undeαpotential shifting Synch*Riskα

High yieldαntial tment poteUnderinvesαial ing potentRisk shiftαity SynchronicααCallable

49

1716151413

12111098

765

43210

(5)

Callable is a binary variable equal to one if the bond is issued with call provision and zero

otherwise. We define a bond as callable when the SDC data item “Call Protection” is other than

“Non-life Call.” Following the findings of Banko and Zhou (2010), we expect to find significant

cross-sectional variation when underinvestment potential is higher. We also expect to find that

information uncertainty exacerbates agency problems, which Banko and Zhou (2010) broadly

define as lower rated (i.e., high yield) issuers. For comparability to Banko and Zhou’s (2010)

20

findings, we also interact R2 with a proxy for risk shifting potential. We define Risk Shifting

Potential following Banko and Zhou (2010). Defining discretionary assets as 1-(fixed assets/total

assets) and free cash flow as the ratio of operating free cash flow (operating income before

depreciation minus preferred and common dividends) divided by total asserts, Risk shifting

potential equals zero if discretionary assets and free cash flow are both below the median of the

firm’s SIC2 industry in a given year, equals two if both are greater than their respective medians,

and equals one otherwise. Aivazian, Ge and Qiu (2005) show that debt with longer maturities

significantly reduces investment for firms with high growth opportunities. To gauge

underinvestment potential, we create a binary variable equal to one if the issuer’s three-year

geometric growth in sales is greater than its industry (SIC2) median in a given year and the

maturity of the issue is ten years or greater, and zero otherwise.

In addition to the Synchronicity measure, we include additional explanatory variables to

control for other potential motivations to include a call provision. Following Banko and Zhou

(2010), we include Firm Size as additional proxy for information asymmetry and Debt Ratio as

proxy for agency conflicts. To control for the interest rate hedging explanation for call provisions,

we include the slope of the yield curve (Yield curve slope), the standard deviation of the yield

curve slope (Std. Yield curve slope) and Change in Yield Curve Slope, along with additional firm-

and bond level characteristics including Profitability, Issue Size, Duration, Stock Unique Risk and

Industry Concentration. Similar to Equations 2-4, we also include industry- and firm-level fixed

effects.

4. Empirical Results

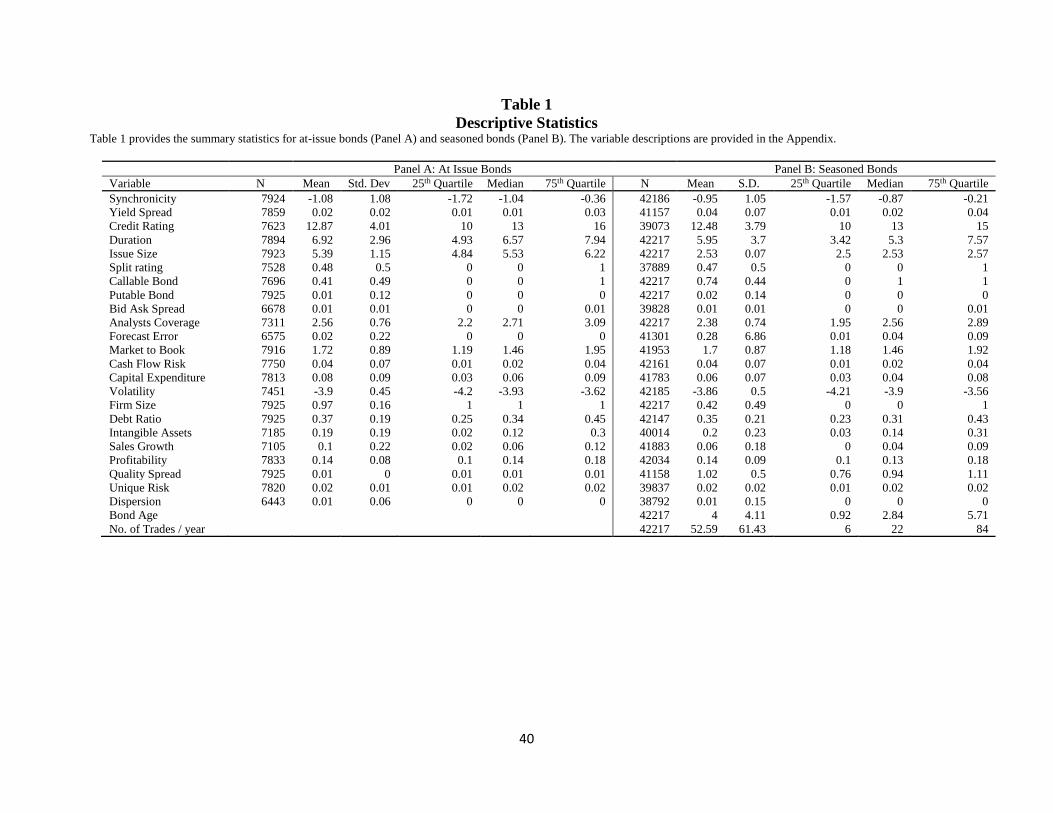

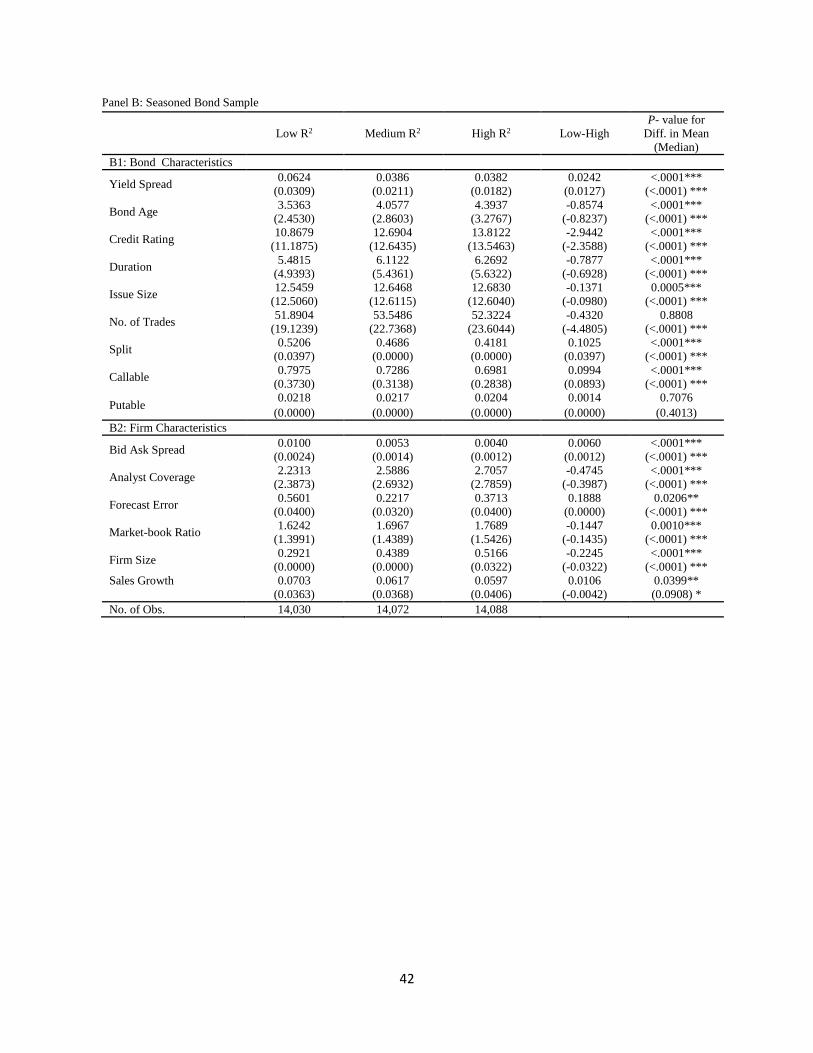

We provide summary statistics for the at-issue and seasoned bond samples in Table 1.

Most of the bond- and firm-level measures are qualitatively similar between the two samples. We

21

begin our analysis by demonstrating whether bonds issued by low R2 issuers are associated with

bond- and firm-level characteristics that are consistent with a lower or higher information

uncertainty. To address this question, we first sort sample firms according to their R2 levels within

each year and divide into terciles. We then calculate the mean (median) value of each

characteristic variable for low, medium and high R2 terciles. These results are illustrated in Table

2. We present the mean (median) results across the R2 terciles as well as the difference in mean

(median) between low and high R2 terciles for at-issue bonds in Panel A and for seasoned bonds

in Panel B.4 The mean (median) values of nearly all bond-level characteristics for both the at-

issue sample (Panel A1) and the seasoned bond sample (Panel B1) demonstrate a monotonic

pattern throughout the three R2 terciles. Specifically, bonds issued by firms with low R2 tend to

have larger Yield Spread and lower Credit Ratings, indicating low R2 bonds are perceived as riskier

by investors. Bonds issued by low R2 firms experience higher levels of split credit ratings,

suggesting that issuing firms may have less transparent firm-specific information which impedes

rating analysts from collecting accurate or relevant information, leading to conflicts in

creditworthiness opinions. In addition, bonds issued by low R2 firms have lower maturity (as

measured by Duration) and a higher incidence of embedded call provisions, features that are

consistent with a more asymmetric information environment. According to Flannery (1986),

Diamond (1991), Robbins and Schatzberg (1986), and Banko and Zhou (2010), among others, the

extent of information asymmetry plays a role in firms’ debt maturity choices and embedded

callable provision of issuance. In the presence of information impairment, firms are more likely

to issue short term maturity bonds and callable bonds in order to mitigate the adverse impact of

4 The proceeding discussion will focus on the mean value of the variables.

22

insider-outsider information asymmetry. The difference in means between low and high R2 terciles

is highly significant for all these characteristics.

Firm-level characteristics across the three R2 terciles provide further evidence that low R2

issuers are associated with a noisier and less transparent information environment. For both the at-

issue bond- (Panel A2) and seasoned bond samples (Panel B2), issuing firms with low-tercile R2

have higher Bid ask spread, lower Analyst coverage, higher Forecast error and smaller Firm size.

While low R2 issuers are associated with greater growth opportunities as measured by higher past

Sales Growth, they are valued at discount by investors as reflected by lower market-book ratios.

This is in line with Banko and Zhou’s (2010) premise that firms with high past growth and low

expected future growth are more likely to have severe underinvestment problems. The difference

in means between low and high R2 terciles is highly significant for all these measures. Viewed

collectively, our findings in Table 2 are in line with the notion that bond issuers with low stock

price synchronicity are associated with a relatively poor information environment and an impaired

supply of firm-specific information available to corporate outsiders, for which investors require a

higher yield spread as compensation.

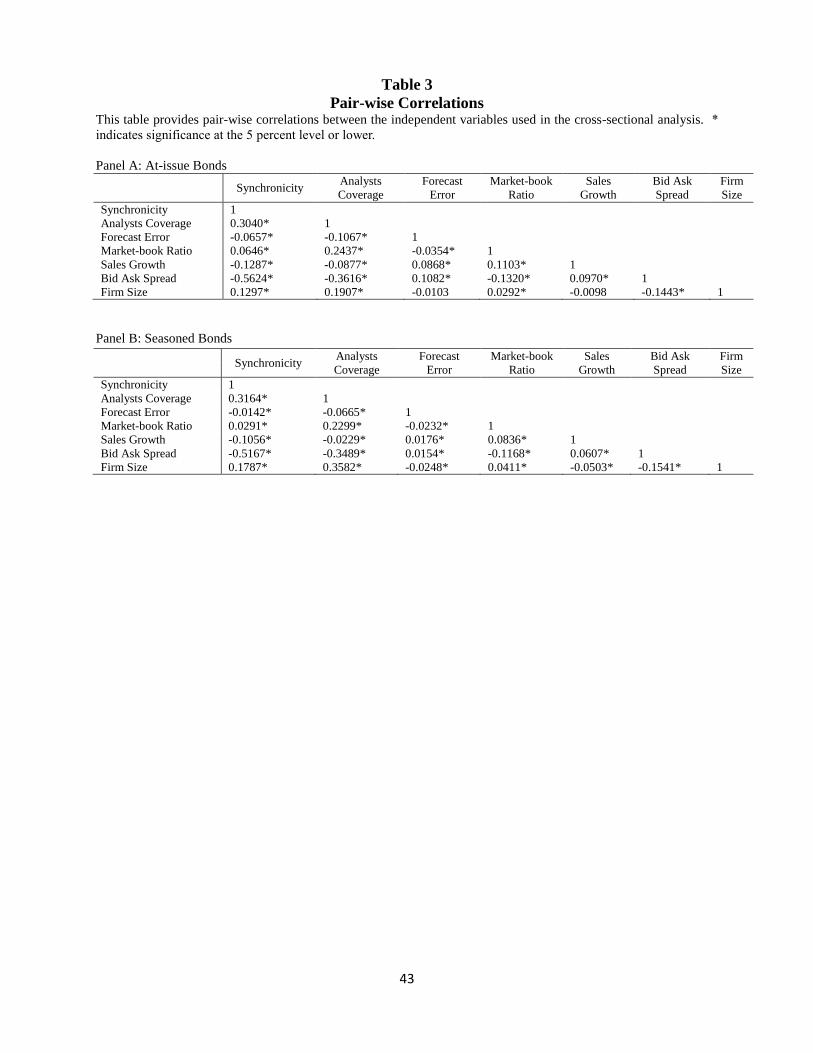

In Table 3, we provide pairwise correlations between synchronicity and alternative

information asymmetry measures. Overall, the pairwise correlations of synchronicity and

characteristic variables are consistent with our findings from the univariate comparisons reported

in Table 2. For both at-issue and seasoned bond samples, lower synchronicity issuers have strong

correlations with firm-specific characteristics that are consistent with poorer information quality.

Specifically, lower synchronicity issuers have higher Bid ask spread, lower Analyst coverage,

lower Market to book ratio, lower Analyst coverage, higher Forecast error and higher Sales

growth.

23

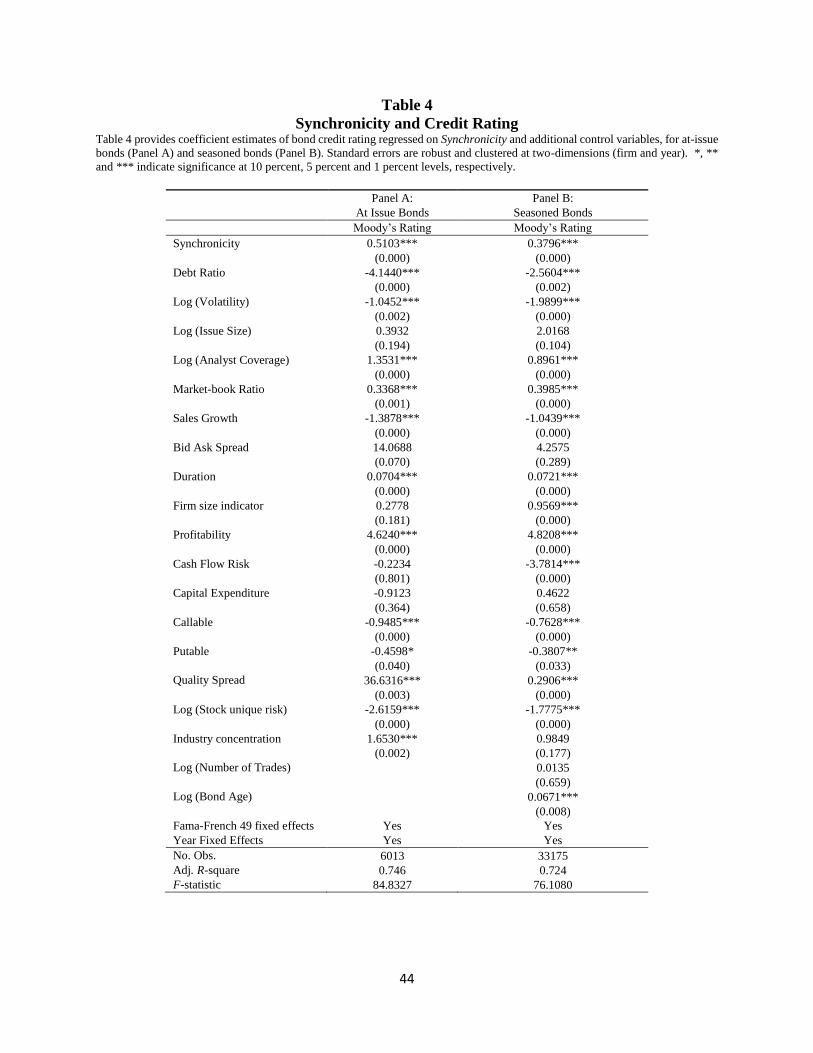

In Table 4, we investigate the association between synchronicity and the cost of debt using

Credit Rating as the dependent variable. We report the sensitivities of Credit rating to the

Synchronicity measure for the at-issue bond sample in Panel A and for the seasoned bond sample

in Panel B. Consistent the results of Table 3, Synchronicity is positive and strongly significantly

related to Credit Rating at the time of issue and over time in the secondary market. This result

supports the prediction of Hypothesis 1 and indicates that rating analysts consider firm’s

information environment as an important determinant of firm’s credit quality: bonds issued by

firms with lower Synchronicity offer less firm-specific information that is publicly available and

higher information uncertainty, and are therefore assigned lower ratings. For both at-issue- and

seasoned bond samples, the firm-level control variables associated with high probability of default

also reduce bonds’ ratings. Specifically, consistent with Adams, Burton and Hardwick (2003),

Bhojraj and Sengupta (2003) and Alali, Anandarajan and Jiang (2012), we find that Credit rating

has a strong positive relation with Profitability, Analyst coverage, Duration and negative relation

with Debt ratio, Volatility and Sales growth. Among the bond-level characteristics, the inclusion

of embedded call provisions is also associated with the perception of greater risk and lowers the

Credit rating.

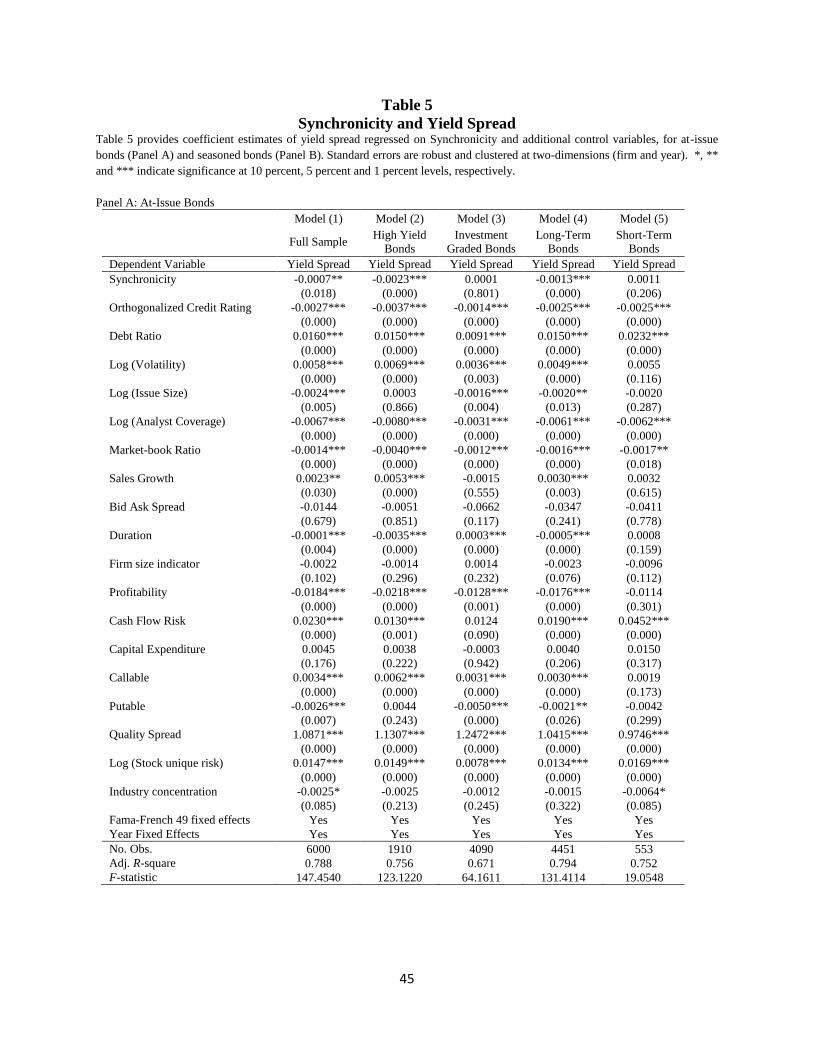

In Table 5, we present the multivariate regression results for Hypotheses 2, 2a and 2b. In

Panel A Model (1), we establish the relation between synchronicity and bond yield spread among

at-issue bonds. Using the overall at-issue sample, Synchronicity is negative but insignificantly

related to yield spread. The primary proxy of default risk (Orthogonal credit rating) is highly

significant which confirms the role of default risk as an important determinant of corporate bond

pricing. Debt Ratio, Profitability, Cash flow risk, and Stock Volatility can be viewed as alternative

indicators for default risk and are positively related to yield spread at the 1 percent levels. Analyst

24

Coverage is a control measure of the quality of the information environment and is significantly

negatively associated with yield spread at the 1 percent level. Stock unique risk has a positive

impact on yield spread and significant at the 1 percent level, indicating firms with greater unique

risk leading to more investor uncertainty about their fundamentals are associated with higher yield

spread. In general, the signs and significance of the remaining bond- and firm-level control

variables are as expected across all models.

In Table 5 Panel A, we divide the full sample of at-issue bonds into high yield- (Model 2)

and investment grade (Model 3) bonds and estimate Equation (2) for each sub-sample. In support

of Banko and Zhou’s (2010) contention that high yield issuers broadly reflect agency problems

related to information and the incentives to underinvest and take excessive risk, the Synchronicity

coefficient estimate is statistically significant in the high yield subset and becomes insignificant in

the investment grade subset. The signs and significance of the remaining control variables are

generally consistent with the results of in Model (1). These findings support Hypothesis (2a):

information risk is a relatively important risk factor to investors of bonds with a higher likelihood

of default.

Next, we divide the sample of at-issue bonds into long–term and short-term sub-samples

according to their maturity. Bonds are as classified as long-term if their time to maturity is seven

years or greater, and classified as short-term if the time to maturity is five years or lower.5 As

shown in Models (4)-(5), there is a significant negative relation between synchronicity and yield

spread among long-term bonds, but an insignificant association between synchronicity and yield

spread among short-term bonds. While not directly supportive of our Hypothesis 2b, this is

5 We follow Lu, Chen and Liao (2010) and Goyal and Wang (2013) to classify short- and long-term maturity. For both

at-issue bonds and seasoned bonds, we also classified bonds samples using alternative maturity definitions, e.g. with

maturity less than 3 years and greater than 10 years. The results are consistent with those presented in Table 5.

25

consistent with Flannery (1986), who shows that the pricing of long-term debt, at issuance, is more

sensitive to information risk. It is possible that firms with higher information risk are more likely

to issue bonds with short maturities (Flannery, 1986; Diamond, 1991; Berger, Espinosa-Vega,

Frame and Miller, 2005). Therefore, longer-term issues are penalized by a higher cost of debt

when firm-specific information is relatively scarce, as proxied by lower R2. The signs and

significance of the remaining explanatory variables are largely as expected and consistent with the

results in Model (1).

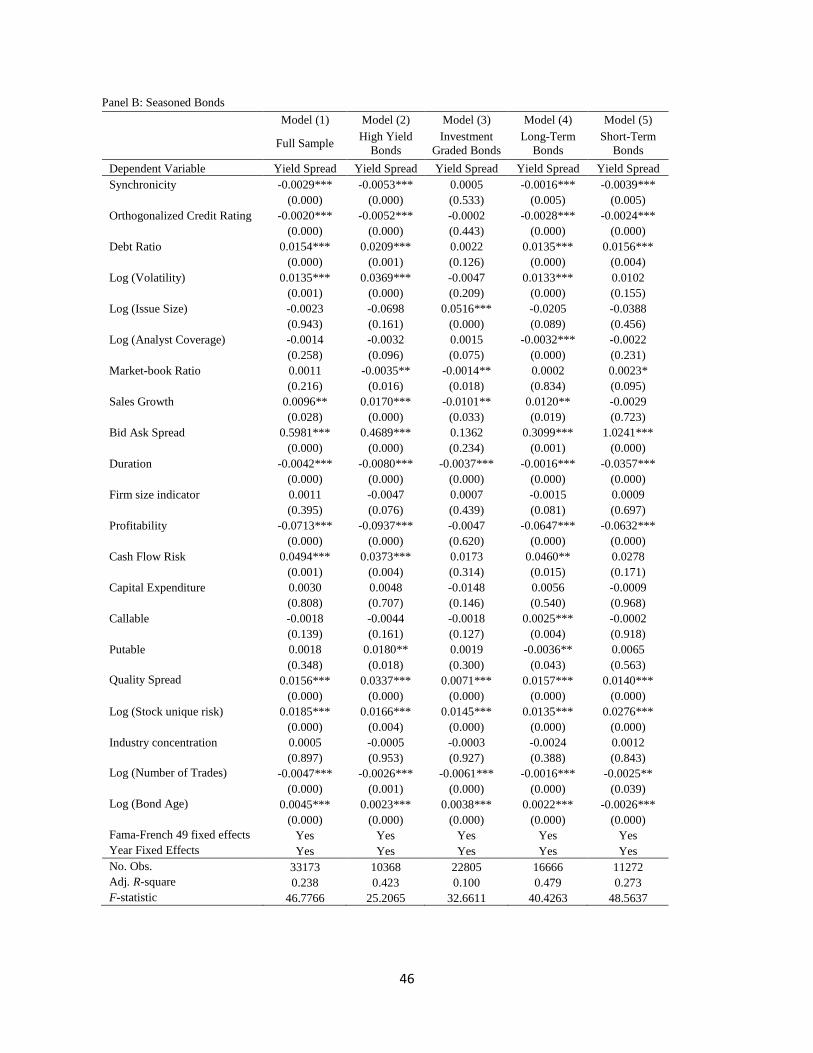

In Table 5 Panel B, we re-examine Equation (2) using the sample of seasoned bonds. In

Panel B Model (1), the Synchronicity coefficient is negative and statistically significant at the one

percent level after controlling for risks related to default, liquidity, fluctuations in macro-economic

variables along with additional firm- and bond-level factors. The main difference of this sample

to the at-issue sample bond is the role of informed bond trading (see, e.g., Han and Zhou, 2014)

that can further enhance the information uncertainty faced by uninformed bond investors. As a

result, information risk can be priced even more strongly into seasoned bonds via the trading

process, leading to a stronger impact on yield spread for seasoned bonds. In line with Han and

Zhou (2014), and in comparison to the results of Panel A, we find that lower synchronicity imposes

a significant positive effect on yield spread for the overall sample.6 Similar to our findings in

Panel A, Synchronicity has a pronounced impact on the yield spreads of high yield seasoned bonds:

the Synchronicity coefficient is significant at the 1 percent level for high yield bonds and is

insignificant for investment grade bonds. Within the seasoned bond sample, the Synchronicity

6 We also find that the magnitude of impact of synchronicity on yield spread increases with trade size. This is

consistent with the notion that informed based traders tend to avoid breaking up their trades in smaller but more

frequent transactions. As the informed traders can benefit more from the impaired information environment, our

supportive results are consistent with Han and Zhou (2014). For brevity, we do not report these results but they are

available upon request.

26

effect is approximately twice the magnitude for short- vs. long-term bonds. This supports

Hypothesis H2b and highlights the critical role of informed bond trading in debt pricing dynamics.

The control variables are largely as expected and consistent with previous findings. In addition to

Issue size, the liquidity measures Bond age is significantly positively related to yield spread and

Number of trades is significantly negatively related to yield spread across all Models. This is

consistent with the view that older bonds and less frequently traded bonds are also subject to higher

liquidity risk (Lu, Chen and Liao, 2010; Huang, Huang and Oxman, 2015). Overall, the results of

Table 5 shed further insight on the notion that low synchronicity reflects greater information

impairment for which bond investors require a higher risk premium to compensate for the higher

information risk they take. In addition, the relation is pronounced for seasoned bond prices, when

informed bond trading enhances the relative negative impact of information risk (e.g. lack of public

firm-specific information) among bond investors.

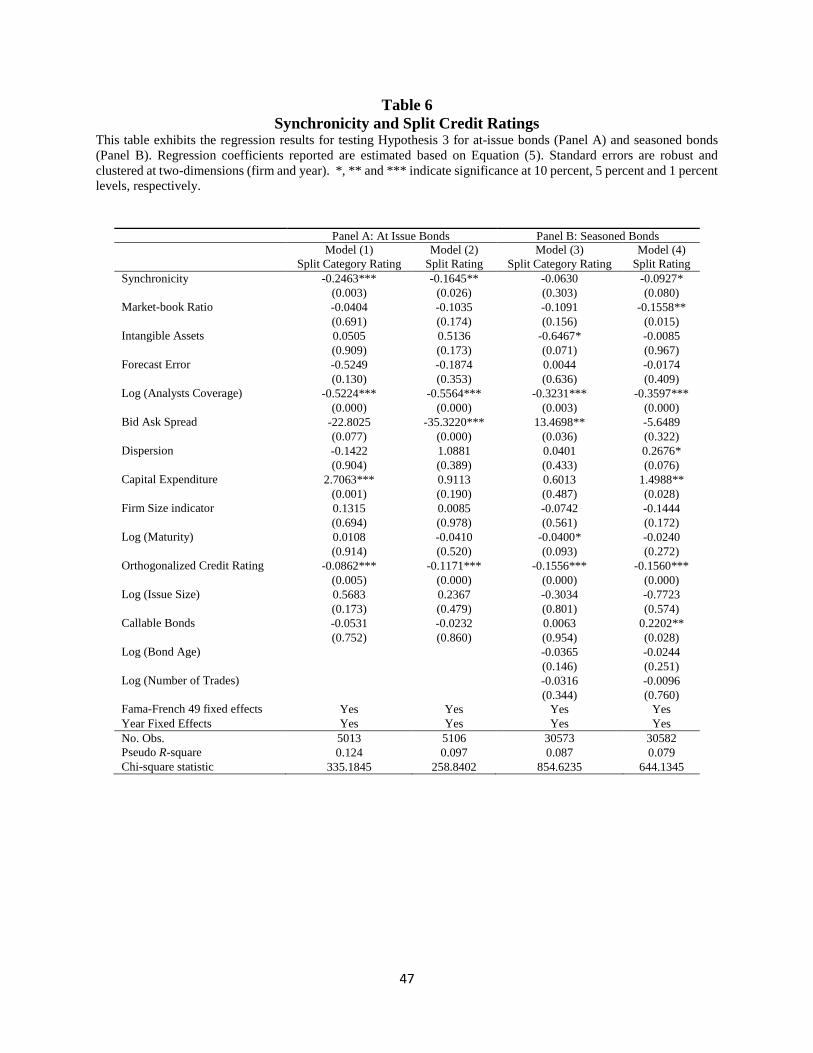

In Table 6, we report the regression results of Equation 4 where we model the likelihood

the degree that Moody’s and S&P ratings diverge. In Models (1)-(2), we report estimates using

the at-issue sample, and Models (3)-(4) we use the seasoned bond sample. Consistent with the

prediction of Hypothesis 3, we document a significant negative association between Synchronicity

and rating divergence. At the time of issue, the impact of Synchronicity on the incidence of ratings

that are split across categories is about twice as large as its predictive value on the likelihood of

split ratings of a notch or greater. The Synchronicity regression coefficient is negative and

significant at the 1 (5) percent level using Split category rating (Split rating) as the dependent

variable, respectively. Models (3)-(4) illustrate that the impact of Synchronicity on the likelihood

of a split rating lessens as bonds seasons, indicating that the rating consequences of opacity are

most severe at the time of issue. These findings further support the view that lower synchronicity

27

reflects a less transparent information environment. The signs and significance of the additional

control variables are largely consistent with the information opacity explanation for split ratings:

variables capturing a greater likelihood of information opacity, such as smaller Firm size, lower

Analyst coverage and lower Credit rating, are significantly related to Split rating for both at-issue

and seasoned bonds.7

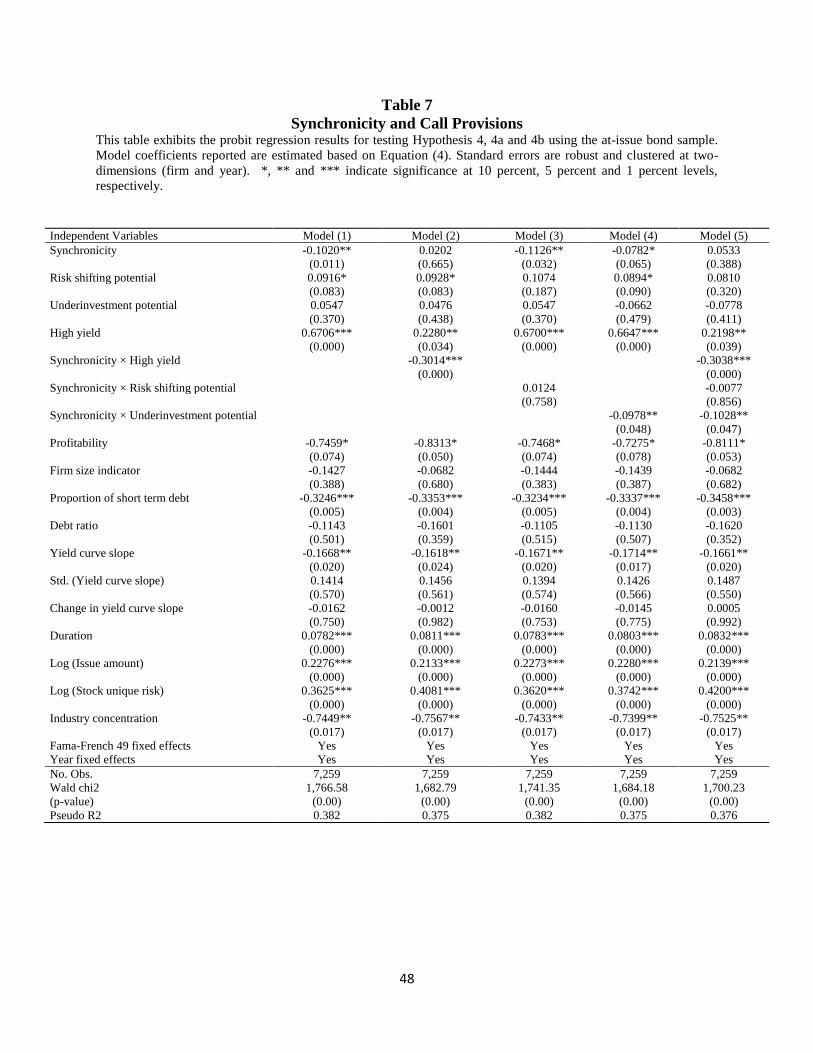

In Table 7 we investigate if Synchronicity has an association with the propensity for newly

issued bonds to contain embedded call provisions. Consistent with the general prediction of

Hypothesis 4, the Synchronicity coefficient estimate is negative and significant at the 5 percent

level, indicating that stock price synchronicity has explanatory value in the decision to include call

provisions in newly issued bonds. We also find that lower-rated firms are more likely to issue

bonds with call features; according to Banko and Zhou (2010), non-investment grade firms issue

callable bonds primarily to alleviate the agency conflicts arising from an asymmetric information

environment, while investment-grade firms issue callable bonds primarily to hedge interest rate

risk. Bonds of longer maturity and larger issue sizes are more likely to include calls, ostensibly to

hedge greater interest rate exposure. Consistent with Hypothesis 4a and the view that information

asymmetry may exacerbate the agency problems found in high yield issuers, Table 7 Model (2)

reports a strong negative interaction term between Synchronicity and High yield; the decision to

issue callable bonds is dependent on the degree of information impairment (as proxied by

Synchronicity), especially among high yield bonds, which comprise the major source of callable

issues in recent years when interest rate have been generally lower.

7 In unreported results, we find that the negative relation between split rating and R2 is stronger for credit ratings of

younger firms. To the extent that credit rating agencies are more reliant on firm-specific information revealed by

younger firms due to less chance of learning about these firms’ prospects through time, the finding is consistent with

the notion that less synchronized firms are associated with greater information impairment.

28

With the interpretation that lower R2 stocks are associated with less public firm-specific

information, the findings in Models (3) and (4) are consistent with the theoretical models by Bodie

and Taggart (1978), Barnea, Haugen and Senbet (1980), and Robbins and Schatzberg (1986)

showing that firms with severe asymmetric information problems are more likely to issue callable

bonds to mitigate the adverse impact of information inefficiency on underinvestment. Specifically,

in support of Hypothesis 4b and consistent with the findings of Banko and Zhou (2010), the

negative relation between Synchronicity and embedded call provisions is particularly strong among

firms that are prone to underinvestment problems. Also consistent with Banko and Zhou (2010),

we find no evidence that firms with information asymmetry problems have an incentive to reduce

risk-shifting problems through callable bond issuance. Finally, Model (5) shows that the

Synchronicity interactions with High yield and Underinvestment potential continue to be

significant after including all interaction terms in the model.

Viewed collectively, the multivariate regression results are consistent with the univariate

results and pairwise correlations reported in Tables 1-2 and further corroborate the view that low

synchronicity is an indication of information inefficiency, or a relative lack of public firm-specific

information. In line with the view that Synchronicity represents a priced information risk factor

from the perspective of bondholders, we find that firms with low stock price synchronicity are

associated with higher cost of debt. Synchronicity also has explanatory value in explaining the

likelihood of credit rating splits and callable bond issuance. These empirical findings provide

further evidence to in support of the view that lower stock price synchronicity proxies for

information asymmetry and an environment in which public firm-specific information is relatively

scarce.

29

6. Conclusion

Motivated by the ongoing debate of the validity of stock price synchronicity (R2) as a

measure of price informativeness, we address the question of whether low stock price

synchronicity represents a more- or less public firm-specific information. While previous studies

address this research question by examining metrics drawn from the stock market, we take a

different approach by examining the issue in the context of corporate bond market. This is

motivated by the literature that establishes the spillover of firm-specific information from the stock

market to the bond market (see e.g. Kwan, 1996; Downing, Underwood, and Xing, 2009;

Hotchkiss and Ronen, 2002). Using yield spreads and structural characteristics of corporate bonds,

we provide evidence supporting the information impairment interpretation of low synchronicity.

Based on the premise that stock price synchronicity reflects the quality of firm-specific information

surrounding the firm, we find that synchronicity has a negative relation with yield spread,

indicating that investors require greater yield premium as compensation for bearing higher

information risk when holding bonds issued by issuers with low stock price synchronicity. We

find this negative relation is pronounced when information risk is more acute, i.e. among high

yield bonds and short-maturity bonds. Using credit rating as an alternative measure of the cost of

debt, we find consistent results demonstrating that lower synchronicity is related to poorer credit

ratings. This result supports the view that firms with low synchronicity are considered by rating

agencies as firms with higher information risk. The results are robust after controlling for default

and liquidity risk embedded in these corporate bonds.

In further analysis, we directly examine the information asymmetry explanation of

synchronicity more directly by linking synchronicity to the extent of divergence in the bond’s

credit rating. The negative relation between synchronicity and split ratings offers further support

30

for the view that firms with low synchronicity are associated with a poor information quality to

outsider investors, where rating agencies are less likely to reach consensus when assigning credit

ratings based on available firm-specific information. Lastly, the examination of the corporate

decision to issue callable bonds allows us to further distinguish the information asymmetry

interpretation of lower Synchronicity from other possible explanations such as lower liquidity. We

find that firms with low synchronicity are more likely to issue bonds with embedded call features:

to the extent that firms use call features to mitigate information asymmetry problems faced by

corporate outsiders, as described in theoretical models of Barnea, Haugen and Senbet (1980) and

Robbins and Schatzberg (1986), our results further supports the view that low synchronicity firms

are associated with lower level of public firm-specific information. Overall, our findings lend

support to the alternative view that lower stock price synchronization (i.e. lower R2) actually

represents a less informative information environment.

31

References

Adams, M., Burton, B., Hardwick, P., 2003. The determinants of credit ratings in the United

Kingdom insurance industry. Journal of Business Finance and Accounting 30, 539-572.

Alali, F., Anandarajan, A., Jiang, W., 2012. The effect of corporate governance on firm’s credit

ratings: further evidence using governance score in the United States. Accounting and

Finance 52, 291-312.

Aivazian, V.A., Ge, Y., Qiu, J., 2005. Debt maturity structure and firm investment. Financial

Management 34, 107-119.

Anderson, R., Sundaresan, S., 1996. Design and valuation of debt contracts. Review of Financial

Studies 9, 37-68.

Ashbaugh-Skaife, H., Gassen, J., LaFond, R., 2006. Does stock price synchronicity represent firm-

specific information? Working paper, MIT Sloan.

Banko, J.C., Zhou, L., 2010. Callable bonds revisited. Financial Management 39, 613-641.

Barnea, A., Haugen, R. A., Senbet, L. W., 1980. A rationale for debt maturity structure and call

provisions in the agency theoretic framework. Journal of Finance 35, 1223-1234.

Berger, A. N., Espinosa-Vega, M. A., Frame, W. S., Miller, N. H., 2005. Debt maturity, risk and

asymmetric information. Journal of Finance 60, 2895-2923.

Bhojraj, S., Sengupta, P., 2003. Effect of corporate governance on bond ratings and yields: the role

of institutional investors and outside directors. The Journal of Business 76, 455-476.

Black, F., Scholes, M., 1973. The pricing of options and corporate liabilities. Journal of Political

Economy 81, 637–654.

Bodie, Z., Taggart, R.A., 1978. Future investment opportunities and the value of the call provision

on a bond. Journal of Finance 33, 1187-1200.

Boubaker, S., Mansali, H., Rjiba, H., 2014. Large controlling shareholders and stock price

synchronicity. Journal of Banking and Finance 40, 80-96.

Campbell, J. Y., Taksler, G., 2003. Equity volatility and corporate bond yields. Journal of Finance

58, 2321-2350.

Chan, k., Chan, Y., 2014. Price informativeness and stock return synchronicity: Evidence from the

pricing of seasoned equity offerings. Journal of Financial Economics 114, 36-53.

Chan, K., Hameed, A., 2006. Stock price synchronicity and analyst coverage in emerging markets.

Journal of Financial Economics 80, 115-147.

32

Chan, K., Hameed, A., Kang, W., 2013. Stock price synchronicity and liquidity. Journal of

Financial Markets 16, 414-438.

Chen, L., Lesmond, D.A., Wei, J., 2007. Corporate yield spreads and bond liquidity. Journal of

Finance 62, 119-49.

Clarke, J., Shastri, K., 2000. On information asymmetry metrics. Working paper, Georgia Institute

of Technology.

Collin-Dufresne, P., Goldstein, R., 2001. Do credit spreads reflect stationary leverage ratios?

Journal of Finance 56, 1929-1957.

Collin-Dufresne, P., Goldstein, R., Martin, J. S., 2001. The determinants of credit spread changes.

Journal of Finance 56, 2177-2207.

Chuluun, T., Prevost, A., Puthenpurackal, J., 2014. Board ties and the cost of corporate debt.

Financial Management 43, 533-568.

Dasgupta, S., Gan, J., Gao, N., 2010. Transparency, price informativeness, and stock return

synchronicity: Theory and evidence. Journal of Financial and Quantitative Analysis 45,

1189-1220.

Devos, E., Hao, W., Prevost, A.K., and Wongchoti, U., Stock return synchronicity and the

market response to analyst recommendation revisions. Journal of Banking and Finance

58, 376-389.

Diamond, D. W., 1991. Debt maturity structure and liquidity risk. Quarterly Journal of Economics

106, 709–738.

Downing, C., Underwood, S., Xing, Y., 2009. The relative informational efficiency of stocks and

bonds: An intraday analysis. Journal of Financial and Quantitative Analysis 44, 1081-1102.

Duffie, D., Lando, D., 2001. Term structure of credit spreads with incomplete accounting

information. Econometrica 69, 633–664.

Durnev, A., Morck, R., Yeung, B., 2004. Value-enhancing capital budgeting and firm-specific stock

return variation. The Journal of Finance 59, 65-105.

Durnev, A., Morck, R., Yeung, B., Zarowin, P., 2003. Does greater firm-specific return variation

mean more or less informed stock pricing? Journal of Accounting Research 41, 797-836.

Elton, E., Gruber, M., Agrawal, D., Mann, C., 2001. Explaining the rate spread on corporate bonds.

Journal of Finance 56, 247-277.

33

Fernandes, N., Ferreira, M.A., 2009. Insider trading laws and stock price informativeness. Review

of Financial Studies 22, 1845-1887.

Ferreira, E.J., Smith, S., 2006. Effect of Reg FD on information in analysts’ rating changes.

Financial Analysts Journal 62, 44-57.

Flannery, M. J., 1986. Asymmetric information and risky debt maturity choice. Journal of Finance

41, 19–37.

Gassen, J., LaFond, R., Skaife, H. A., Veenman, D., 2015. Illiquidity and R2, Working Paper,

Erasmus University Rotterdam.

Goyal, V. K., Wang, W., 2013. Debt maturity and asymmetric information: evidence from default

risk changes. Journal of Financial and Quantitative Analysis 48, 789-817.

Han, S., Zhou, X., 2014. Informed bond trading, corporate yield spreads, and corporate default

prediction. Management Science 60, 675-694.

Hotchkiss, Edith S., Tavy Ronen, 2002. The informational efficiency of the bond market: An

intraday analysis. Review of Financial Studies 15, 1325–1354.

Hou, K., Peng, L., Xiong, W., 2013. Is R2 a measure of market inefficiency? Working paper,

Princeton University.

Huang, H. H., Huang H., Oxman, J.J., 2015. Stock liquidity and corporate bond yield spreads:

Theory and Evidence. Journal of Financial Research 38, 59-91.

Huang, J., Huang, M., 2012. How much of the corporate-treasury yield spread is due to credit risk?

Review of Asset Pricing Studies, forthcoming.

Hubbard, R.G., O’Brien, A.P. Money, Banking and the Financial System. Pearson, 2nd Edition.

Hutton, A., Marcus, A., and Tehranian, H. 2009. Opaque financial reports, R2, and crash risk,

Journal of Financial Economics 94, 67-86.

Jin, L., Myers, S., 2006. R2 around the world: New theory and new tests. Journal of Financial

Economics 79, 257-292.

Klock, M., Mansi, S., Maxwell, W., 2005. Does corporate governance matter to bondholders?

Journal of Financial and Quantitative Analysis 40, 693–719.

Kwan, S. H., 1996. Firm-specific information and the correlation between individual stocks and

bonds. Journal of Financial Economics 40, 63-80.

Kelly, P., 2014. Information efficiency and firm-specific return variation. Quarterly Journal of

Finance, forthcoming.

34

Leland, H.E., 1994. Corporate debt value, bond covenants, and optimal capital structure. Journal

of Finance 49, 1213–1252.

Li, B., Rajgopal, S., Venkatachalam, M., 2014. R2 and idiosyncratic risk are not interchangeable.

Accounting Review 89, 2261-2295.

Lin, H., Wang, J., Wu, C., 2011. Liquidity risk and expected corporate bond returns. Journal of

Financial Economics 99, 628-650.

Livingston, M., Naranjo, A., Zhou, L., 2007. Asset opaqueness and split bond ratings. Financial

Management 36, 49-62.

Livingston, M., Zhou, L., 2010. Split bond ratings and information opacity premiums. Financial

Management 39, 515-552.

Longstaff, F.A., Mithal, S., Neis, E., 2005. Corporate yield spreads: default risk or liquidity? new

evidence from the credit default swap market. Journal of Finance 60, 2213-53.

Longstaff, F., Schwartz, E., 1995. Valuing risky debt: A new approach. Journal of Finance 50,

789–820.

Lu, C., Chen, T., Liao, H., 2010. Information uncertainty, information asymmetry and corporate

bond yield spreads. Journal of Banking and Finance 34, 2265-2279.

Mansi, S., Maxwell, W., Miller, D., 2004. Does auditor quality and tenure matter to investors:

Evidence from the bond market, Journal of Accounting Research 42, 755–793.

Mansi, S.A., Maxwell, W. F., Miller, D. P., 2011. Analyst forecast characteristics and the cost of

debt. Review of Account Studies 16, 116-142.

Merton, R.C., 1974. On the pricing of corporate debt: The risk structure of interest rates. Journal

of Finance 29, 449–470.

Morck, R., Yeung, B., Yu, W., 2000. The information content of stock markets: Why do emerging

markets have synchronous stock price movements? Journal of Financial Economics 58,

215-260.

Morgan, D.P., 2002. Rating banks: risk and uncertainty in an opaque industry. American Economic

Review 92, 874-888.

Odders-White, E.R., Ready, M.J., 2006. Credit ratings and stock liquidity. Review of Financial

Studies 19, 119–157.

Piotroski, J. D., Roulstone, D. T., 2004. The influence of analysts, institutional investors and

insiders on the incorporation of market, industry and firm-specific information into stock

prices. The Accounting Review 79, 1119-1151.

35

Rajgopal, S., Venkatachalam. M., 2011. Financial reporting quality and idiosyncratic return

volatility. Journal of Accounting and Economics 51, 1-20.

Robbins, E., Schatzberg, J., 1986. Callable bonds: a risk-reducing signaling mechanism. Journal

of Finance 41, 935-949.

Roll, R., 1988. R2. Journal of Finance 43, 541-566.

Stowe, J.D., Xing, X., 2011. R2: Does it matter for firm valuation? The Financial Review 46, 233-

250.

Teoh, S.H., Yang, Y., Zhang, Y., 2007. R-square: Noise or firm-specific information. Working

paper, UC- Irvine.

Yu, F., 2005. Accounting transparency and the term structure of credit spreads. Journal of

Financial Economics 75, 53–84.

Zhou, X., 2010. Information, liquidity and corporate yield spreads. Working Paper.

36

Appendix 1

Published R2 Articles

Panel A: Articles supporting the interpretation that lower R2 is more informative

Journal Article

An, H., Zhang, T., 2013. Stock price synchronicity, crash risk, and institutional investors. Journal of Corporate Finance 21,

1-5. Boubaker, S., Mansali, H., Rjiba, H., 2014. Large controlling shareholders and stock price synchronicity. Journal of Banking

and Finance 40, 80-96.

Brockman, P., Yan, X., 2009. Block ownership and firm-specific information. Journal of Banking and Finance 33, 308–316.

Brown, N., Kimbrough, M., 2011. Intangible investment and the importance of firm-specific factors in the determination of

earnings. Review of Accounting Studies 16, 539–573.

Chan, K., Hameed, A., 2006. Stock price synchronicity and analyst coverage in emerging markets. Journal of Financial

Economics 80, 115-147.

Chen, Q., Goldstein,I., W. Jiang., 2007. Price informativeness and investment sensitivity to stock price. Review of Financial

Studies 20, 619–650.

Chun, H., Kim, J., Morck, R., Yeung, B., 2008. Creative destruction and firm-specific performance heterogeneity. Journal of

Financial Economics 89, 109–135.

Crawford, S., Roulstone, D., So, E., 2012. Analyst initiations of coverage and stock return synchronicity. The Accounting

Review 87, 1527–1553.

Dong, Y., Li, Z., Lin, Y., Ni, C., 2015. Does information processing cost affect firm-sepcific information acquisition?

Evidence from XBRL adoption. Journal of Financial and Quantitative Analysis51, 435-462.

Durnev, A., Morck, R., Yeung, B., Zarowin, P., 2003. Does greater firm-specific return variation mean more or less informed

stock pricing? Journal of Accounting Research 41, 797-836.

Durnev, A., Morck, R., Yeung, B., 2004. Value-enhancing capital budgeting and firm-specific stock return variation. The

Journal of Finance 59, 65-105.

Eun, C. S., Wang, L., Xiao, S. C., 2015. Culture and R2. Journal of Financial Economics115, 283-303.

Fernandes, N., Ferreira, M., 2008. Does international cross-listing improve the information environment? Journal of Financial

Economics 88, 216–244.

Ferreira, D., Ferreira, M., Raposo, C., 2011. Board structure and price informativeness. Journal of Financial Economics 99,

523–545.

Ferreira, M., Laux, P., 2007. Corporate governance, idiosyncratic risk, and information flow. The Journal of Finance 2, 951–