Embed Size (px)

Citation preview

Page 2 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

Steel Re-Rolling Mills Association of India www.srma.co.in Email : [email protected]

Sl. No, Name

1. Shri B.M. Beriwala,

Chairman

2. Shri Jagmel Singh Matharoo,

Vice Chairman

3. Shri Ramesh Kumar Jain,

Treasurer

4. Shri Sanjay Jain

5. Shri Kailasj Goel

6. Shri G P Agarwal

7. Shri O P Agarwal

8. Shri S K Sharda

9. Shri Sandip Kumar Agarwal

10. Shri S. S. Sanganeria

11. Shri Sanjay Surekha

12. Shri R P Agarwal

13. Shri S. S. Bagaria

14. Shri Girish Agarwal

15. Shri Goutam Khanna

16. Shri Suresh Bansal

17. Shri Rajiv Jajodia

18. Shri Bhusan Agarwal

19. Shri Mahesh Agarwal

20. Shri Sita Ram Gupta

21. Shri Ashok Bardeja

Page 3 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

SRMA Steel News is a division of Steel Re-Rolling Mills Association of India and takes due care

in preparing this news. Information has been obtained by SRMA from sources, which it considers

authentic. However, SRMA does not guarantee the accuracy, adequacy or completeness of any

information and is not responsible for any errors or omissions or for the results obtained from the

use of such information. SRMA is not liable for investment decisions, which may be based on the

views expressed in the News. SRMA especially states that it has no financial liability whatsoever

to the subscribers/users/transmitters/distributors of this News. And no part of this news may be

published/reproduced in any form without SRMA’s prior written approval.

Page 4 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

Executive Summary

Present Scenario of Sponge Iron Industry

Environment & Safety Focus

Taxation News

Events

Latest Steel News

CONTENTS

Page 5 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

For the period of 2012, India maintained its ranking as the 4th largest steel producing country in the world behind

China, Japan and the US with a crude steel production of 76.7 million tonnes (MT) representing a 4.3% growth over

2011. The Indian steel industry continued to showcase trends of higher consumption of finished steel and continued

to be a net importer on account of increased demand for special grades of steel in the country. India's current per

capita finished steel consumption at 57 kg is well below the world average of 217 kg. With rising income levels

expected to make steel increasingly affordable, there is vast scope for increasing per capita consumption of steel.

The core sector of steel industry tracks the overall economic growth in the long term. Also, steel demand, being

derived from other sectors like automobiles, consumer durables and infrastructure, its fortune is dependent on the

growth of these user industries. The Indian steel sector enjoys advantages of domestic availability of raw materials

and cheap labour. Iron ore is also available in abundant quantities. This provides major cost advantage to the

domestic steel industry.

The steel industry of India is largely iron-based through the blast furnace (BF) or the direct reduced iron (DRI)

route. Indian steel industry is highly consolidated. About 60% of the crude steel capacity is resident with integrated

steel producers (ISP). But the changing ratio of hot metal to crude steel production indicates the increasing presence

of secondary steel producers (non integrated steel producers) manufacturing steel through scrap route, enhancing

their dependence on imported raw material

The New Industrial policy adopted by the Government of India has opened up the iron and steel sector for

private investment by removing it from the list of industries reserved for public sector and exempting it from

compulsory licensing. Imports of foreign technology as wall as foreign direct investments are freely permitted

up to certain under the automatic route. This, along with the other of the private sector in the steel industry.

While the existing units are being modernized/expanded , a large number of new/green—field steel plants have

also come-up in different parts of the country based on modern, cost effective, state of-the-art technologies.

The steel industry of India has recorded remarkable performance in recent years. The industry is now capable of

producing high quality materials to stringent international specifications for high end applications in sectors like

construction, engineering, automobile and infrastructure. Indian steel products have been well accepted in the global

market and the country’s export of finished steel crossed the 5 Mt mark in Fy’04 at 5.22 Mt. which was about 14.4

percent of its total domestic production.

Steel producers across the globe are grappling with low capacity use levels, resulting in a high fixed cost. Indian

steel producers’ capacity use contracted to below 80% in FY13. Any increase in the capacity use due to an uptick in

demand could be limited by significant new capacities (about 13-15 million tonnes), scheduled to start in FY15.

Domestic steel producers will have to increase their focus on cost competitiveness and efficiency of operations to

protect their margins.

Indian economy is poised to grow much faster in 2015. Development, reforms and infrastructure are perceived to be

ready to take the centre stage. With economy expected to return stronger growth, steel demand is expected to be

higher to around 5% in the year 2014-15 and potentially around 10% in 2015-16. Leading steel producers in India

expect to raise production with steel prices to remain stable in 2014 backed by moderating raw material prices.

Page 6 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

Sponge iron, also known as Direct Reduced Iron (DRI), is a product that

is produced by subjecting iron ore to a reduction process. Direct reduced

iron has a slightly higher iron content, which often makes it better suited

for use in the electric furnace route of steel making.

Though the industrial application of sponge iron started early in the

1950s, it could not fulfill industry expectations at that time in being used

as a supplementary material for feed/ alternative to blast furnaces. The

main reasons were :

The gas based sponge iron plants could operate only where

inexpensive natural gas was available.

Sponge iron furnaces could not be developed into a single entity to produce liquid metal.

Increased scrap availability that was being traded world wide as a furnace RM.

Blast furnace capacities increased from 0.7 Mt/yr in 1960s to over 4 Mt/yr. Today the largest gas based sponge iron

module available is approx. 1.0 Mt/yr. However, the environmental requirements and the capital cost required to set

up new integrated steel plants have their own draw backs. In light of this, coal based sponge iron technology now

indicates a new direction, particularly for Indian steel making conditions.

The production of sponge iron in India started about three decades ago triggered by the fact that in the mid-1970’s,

Indian mini-steel plants started examining the viability of setting up sponge iron plant. Since India has adequate coal

deposits, production of coal based sponge iron was considered a feasible option. The growth of the DRI industry till

the mid 1980 was slow largely because of restrictive licensing. It was only after de-licensing in 1985 that the

industry expanded rapidly.

Production Trend - Sponge Iron production in India witnessed a CAGR of 14.77% during the period 2004 -05 to

2009-10. However, the growth rate was volatile during that period with 2006-07 recording the highest growth rate

of around 38%. Production growth is expected to accelerate during 2011 - 13 on account of a strong demand from

the secondary steel industry, which uses sponge iron for manufacturing steel. According to CMIE, steel production

is expected to grow by 11 % and 15 %, respectively, during 2011 - 12 and 2012 - 13. As secondary steel sector

accounts for almost 55% of the total steel production, a strong growth in production of steel is expected to boost the

demand for sponge iron. Sponge iron production is expected to grow by 14 % in 2011-12 and by 18.4% in 2012-13.

INDIAN DRI PRODUCTION - FINANCIAL YEAR 2013-14 (Tons)

1nd Qtr 2nd Qtr 3nd Qtr 4nd Qtr Total

(April-June) (July - Sept) (Oct - Dec) (Jan - Mar) (April - March)

A. Gas Based 910456 529945 486113 687805 2614319

B. COAL BASED 3726841 3739841 3898000 4128223 15492905

TOTAL B 4637297 4269786 4384113 4816028 18107224

Page 7 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

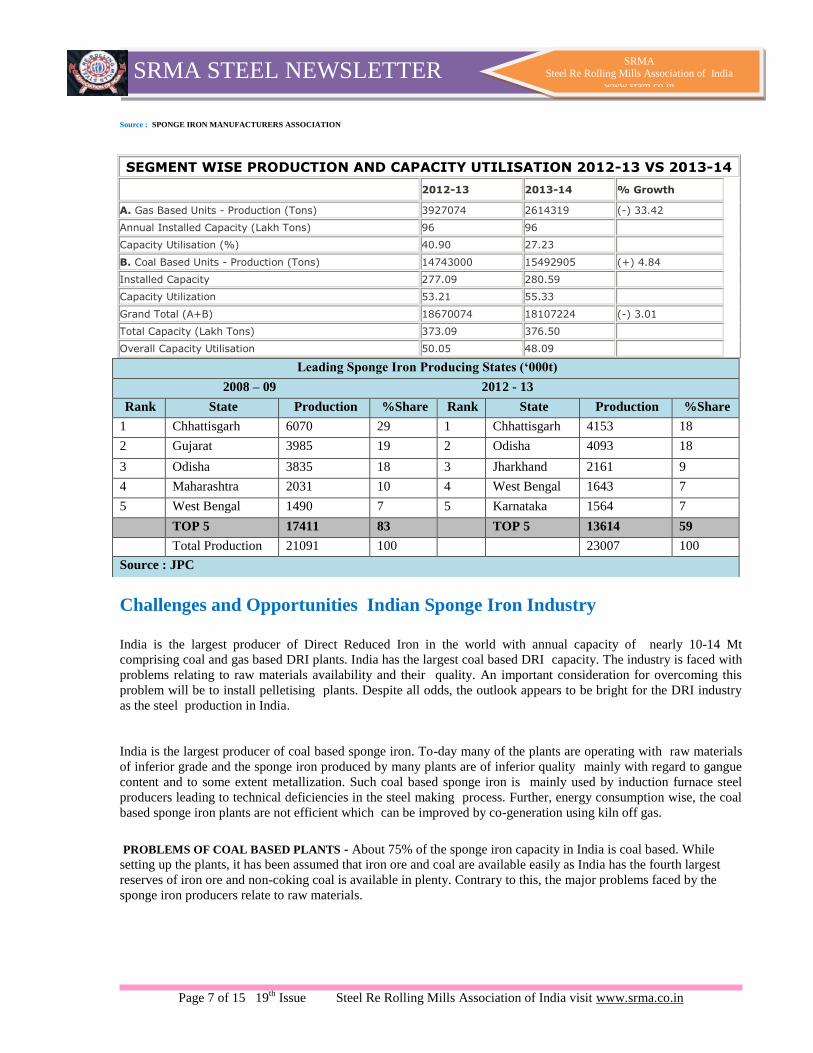

Source : SPONGE IRON MANUFACTURERS ASSOCIATION

Challenges and Opportunities Indian Sponge Iron Industry

India is the largest producer of Direct Reduced Iron in the world with annual capacity of nearly 10-14 Mt

comprising coal and gas based DRI plants. India has the largest coal based DRI capacity. The industry is faced with

problems relating to raw materials availability and their quality. An important consideration for overcoming this

problem will be to install pelletising plants. Despite all odds, the outlook appears to be bright for the DRI industry

as the steel production in India.

India is the largest producer of coal based sponge iron. To-day many of the plants are operating with raw materials

of inferior grade and the sponge iron produced by many plants are of inferior quality mainly with regard to gangue

content and to some extent metallization. Such coal based sponge iron is mainly used by induction furnace steel

producers leading to technical deficiencies in the steel making process. Further, energy consumption wise, the coal

based sponge iron plants are not efficient which can be improved by co-generation using kiln off gas.

PROBLEMS OF COAL BASED PLANTS - About 75% of the sponge iron capacity in India is coal based. While

setting up the plants, it has been assumed that iron ore and coal are available easily as India has the fourth largest

reserves of iron ore and non-coking coal is available in plenty. Contrary to this, the major problems faced by the

sponge iron producers relate to raw materials.

SEGMENT WISE PRODUCTION AND CAPACITY UTILISATION 2012-13 VS 2013-14

2012-13 2013-14 % Growth

A. Gas Based Units - Production (Tons) 3927074 2614319 (-) 33.42

Annual Installed Capacity (Lakh Tons) 96 96

Capacity Utilisation (%) 40.90 27.23

B. Coal Based Units - Production (Tons) 14743000 15492905 (+) 4.84

Installed Capacity 277.09 280.59

Capacity Utilization 53.21 55.33

Grand Total (A+B) 18670074 18107224 (-) 3.01

Total Capacity (Lakh Tons) 373.09 376.50

Overall Capacity Utilisation 50.05 48.09

Leading Sponge Iron Producing States (‘000t)

2008 – 09 2012 - 13

Rank State Production %Share Rank State Production %Share

1 Chhattisgarh 6070 29 1 Chhattisgarh 4153 18

2 Gujarat 3985 19 2 Odisha 4093 18

3 Odisha 3835 18 3 Jharkhand 2161 9

4 Maharashtra 2031 10 4 West Bengal 1643 7

5 West Bengal 1490 7 5 Karnataka 1564 7

TOP 5 17411 83 TOP 5 13614 59

Total Production 21091 100 23007 100

Source : JPC

Page 8 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

Iron Ore

Iron ore of the right quality is the basic input. The sponge iron plants are basically using lump ore. The chief quality

requirements are:

i. High Fe content with less gangue and deleterious elements like phosphorous and sulphur —preferably 65% or

higher iron content.

ii. Good handling properties - Tumbler and abrasion — preferably +85% tumbler index.

iii. Calibrated to size with less fines — preferably 6-16 mm with less than 3% fines

iv. High reducibility — (dR/d0 40% about 0.7%/minute or higher. Hematite ores generally meet the requirement

v. Low decrepitation during reduction — less than 5% fines generation

vi. Good compatibility with the reductant coal used.

The ore used in most of the coal based sponge iron plants hardly meet the above requirements. The availability of

such ore is difficult as it calls for selective mining and also the extent of such reserves are limited

Reductant

Coal is the most critical input material for rotary kiln sponge iron production. Non-coking coal is used as reductant.

The main quality requirements of coal are:

i. Low ash and high fixed carbon contents

ii. Volatile matter 23-28% desirable

iii. Low sulphur content

iv. Reactivity — desirable 2 (cm

3 CO/gC.sec)

v. Low caking index

vi. High ash fusion temperature — Initial deformation above 1200/1250 °C

vii. Swelling index less than 1.

Although India has huge reserves of non coking coal, only about 15% of such coal is suitable for rotary kiln sponge

iron process. Further, in the southern zone, Singareni being the only source, availability of linkage and coal quality

are the constraints. The sponge iron plants, therefore, are using any non coking/steam coal available to them. Many

of the sponge iron producers have switched over to imported coal usage which has superior properties compared to

local coal.

Energy Consumption

In the rotary kiln process about 6 G Cal of fuel energy is used as compared to less than half the energy required in

the gas based direct reduction processes. More than 2 G Cal of energy is let out from the kiln as waste gas. To day

some of the plants have incorporated co-generation system to utilize the energy from waste gas and producing

cheaper power. Introduction of co-generation system has improved economics of the rotary kiln /induction furnace

operation. However, the higher initial investment has slowed down the adoption of co-generation, especially at the

present situation where the sponge iron market is highly depressed.

Page 9 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

INDUSTRIAL ENVIRONMENTAL POLICY - WATER MANAGEMENT

Proper water management is part of an effective Environmental Management System. It also plays a

critical role in the viability of steel plants, especially in regions of water scarcity. Water issues and how

they are managed at specific plants vary greatly due to local aspects such as water availability, water

quality, plant configuration and legislation.

The steel industry uses saltwater, brackish water and freshwater. Water is used mainly for once through

cooling – over 81% in relation to total intake. In general, sea water is the preferred option for this process

due to availability and costs and it is returned directly to the source with no tampering in quality at all. In

much smaller volumes, water is found throughout the steelmaking process for cooling or heat transfer of

heat processing equipment. Water is also required for descaling, dust scrubbers and other processes.

A recent worldsteel member survey ( “Water management in the steel industry”) showed that average

consumption and discharge for integrated steel plants are 28.6 m3/tonne steel and 25.3 m3/tonne of steel,

respectively. For the EAF route the average is 28.1 m3/tonne steel for consumption and 26.5 m3/tonne of

steel. Water consumption and discharge are close to each other and few losses occur in the process,

indicating an overall efficient use of water. In most cases water loss is caused by evaporation.

Using advanced technologies, steel plants in areas of water scarcity are able to recycle and reuse around

98% of their water.

Biodiversity

Within the steel industry there are examples of how companies have created nature reserves for threatened species, developed reef materials based on steelmaking by-products and encouraged employees to join nature conservation initiatives.

Across the globe, extensive reclamation and afforestation and reforestation programmes are converting

mines and quarries into habitats for local wildlife. Some steel producers engage with local communities to

encourage the sustainable use of forests as a source of livelihood.

Air quality

A key aspect of steel industry environmental protection is to minimize emissions to the air. Emission

sources are mapped and monitored. Process improvements can then be identified and implemented with

the goal of reducing emissions. Control mechanisms to reduce emissions can include:

baghouse/filtration systems

chemical treatment

thermal oxidisation

scrubber systems

dust suppression.

Page 10 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

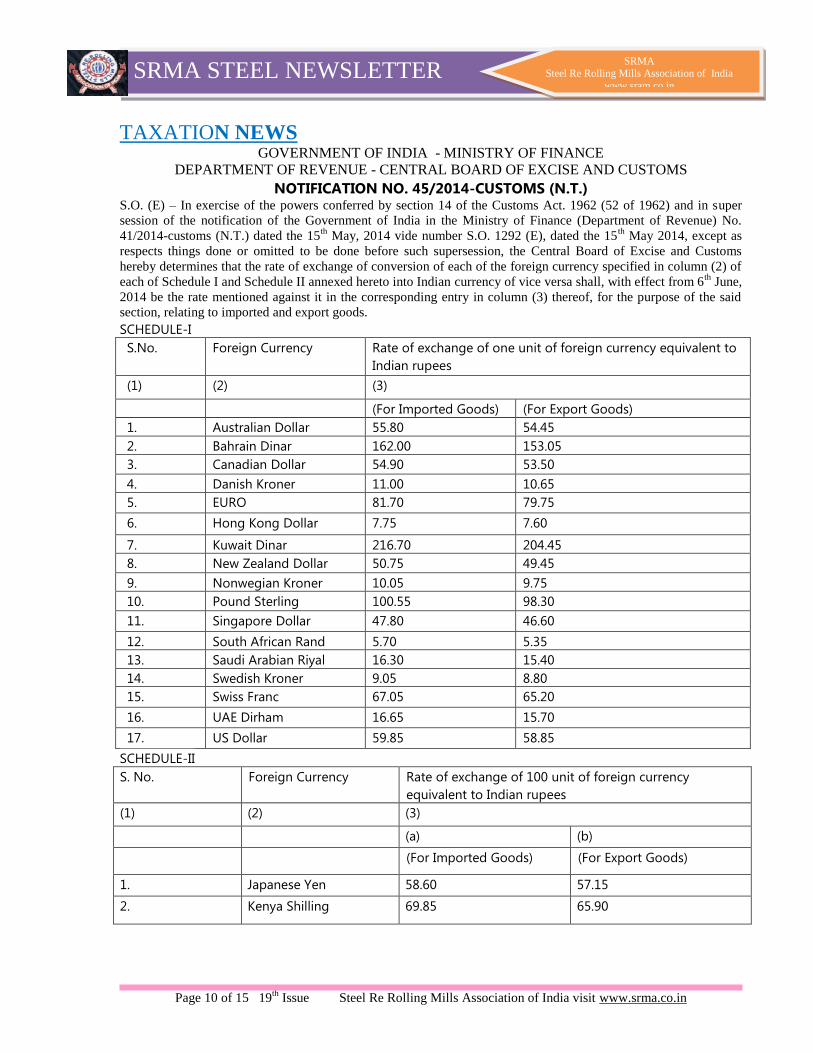

TAXATION NEWS GOVERNMENT OF INDIA - MINISTRY OF FINANCE

DEPARTMENT OF REVENUE - CENTRAL BOARD OF EXCISE AND CUSTOMS

NOTIFICATION NO. 45/2014-CUSTOMS (N.T.) S.O. (E) – In exercise of the powers conferred by section 14 of the Customs Act. 1962 (52 of 1962) and in super

session of the notification of the Government of India in the Ministry of Finance (Department of Revenue) No.

41/2014-customs (N.T.) dated the 15th

May, 2014 vide number S.O. 1292 (E), dated the 15th

May 2014, except as

respects things done or omitted to be done before such supersession, the Central Board of Excise and Customs

hereby determines that the rate of exchange of conversion of each of the foreign currency specified in column (2) of

each of Schedule I and Schedule II annexed hereto into Indian currency of vice versa shall, with effect from 6th

June,

2014 be the rate mentioned against it in the corresponding entry in column (3) thereof, for the purpose of the said

section, relating to imported and export goods.

SCHEDULE-I

S.No.

Foreign Currency

Rate of exchange of one unit of foreign currency equivalent to

Indian rupees

(1) (2) (3)

(For Imported Goods) (For Export Goods)

1. Australian Dollar 55.80 54.45

2. Bahrain Dinar 162.00 153.05

3. Canadian Dollar 54.90 53.50

4. Danish Kroner 11.00 10.65

5. EURO 81.70 79.75

6. Hong Kong Dollar 7.75 7.60

7. Kuwait Dinar 216.70 204.45

8. New Zealand Dollar 50.75 49.45

9. Nonwegian Kroner 10.05 9.75

10. Pound Sterling 100.55 98.30

11. Singapore Dollar 47.80 46.60

12. South African Rand 5.70 5.35

13. Saudi Arabian Riyal 16.30 15.40

14. Swedish Kroner 9.05 8.80

15. Swiss Franc 67.05 65.20

16. UAE Dirham 16.65 15.70

17. US Dollar 59.85 58.85

SCHEDULE-II

S. No.

Foreign Currency

Rate of exchange of 100 unit of foreign currency

equivalent to Indian rupees

(1) (2) (3)

(a) (b)

(For Imported Goods) (For Export Goods)

1. Japanese Yen 58.60 57.15

2. Kenya Shilling 69.85 65.90

Page 11 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

2nd India International DRI Summit 2014

Date: August 1, 2014

Location: Hotel Le Meridien, New Delhi

Minerals, Metals, Metallurgy & Materials (MMMM) 2014

4-7, September 2014

Pragati Maidan

New Delhi

For Booking & Enquiries

International Trade and Exhibitions India Pvt. Ltd.

1106-1107, Kailash Building, 26 K.G. Marg, New Delhi- 110001, India

Tel: +91 11 40828282

Gagan Sahni: +919810036183

Varun Sharma:+91 11 40828208

Smita Roy: +91 11 40828217

Sandeep Arora: +91 11 40828227

13th International Stainless & Special Steels 2 - 4 September 2014

Hotel InterContinental

Istanbul, Turkey

AMM 8th Steel Scrap Conference 10 - 11 September 2014

Hilton New Orleans Riverside

New Orleans, U.S.A

From 28-30 October 2014, Messe Duesseldorf India with its parent company, Messe Duesseldorf GmbH {organiser of wire and

TUBE Duesseldorf, GIFA,

METEC, THERMPROCESS and NEWCAST (GMTN)} and MESSE ESSEN GmbH (organiser of Schweissen & Schneiden),

will organise 4 leading trade fairs for the metals industry in India. They are Metallurgy India 2014, Wire & Cable India 2014,

Tube India International 2014 and INDIA ESSEN WELDING & CUTTING 2014 in halls 1, 5 and 6 at the Bombay Convention & Exhibition Center, Goregaon (East), Mumbai.

Page 12 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

STEEL NEWS

Small steelmakers hurt more than big players - Mr Verma chairman SAIL (Follow @SteelGuru on Twitter for important updates) Mr CS Verma chairman of Steel Authority of India is confident that steel demand will pick up once the projects that are held up take off. In an interview with Business Line, he spoke about smaller steel manufacturers having borne the brunt of the downturn. Excerpts: Q - India’s steel consumption grew just 0.6% in 2013 to 2014, but larger players such as SAIL reported much better volume growth. What explains this? A - You have to factor in the composition of the Indian steel industry. In the long segment, a good amount of the market is held by small units (such as sponge iron units and conversion agents) in the unorganized sector. Economies of scale will happen only in the big units. These smaller units cannot compete with big companies. Compliance with quality standards has been made mandatory for many steel products. These small units have had to either comply with these standards or face the risk of closure. Small companies have also been hit because of the absence of mining linkages. Small manufacturers have not been getting iron ore allocations. As it is they find it difficult to adhere to quality standards and emission norms. Today, free steel imports into India are free. You have to pay an import duty of 5% on long products and 7.5% on flat products. China has surplus capacity and it keeps on dumping material. All these factors taken together have hurt the smaller companies much more than the bigger ones. We have to bear in mind that five years back, we (SAIL) were getting a profit margin of 20%. We have to come out of that mind set. 20% margin is earned by companies that are monopolies. The steel industry no longer features a monopoly. So margins will be reasonable. But volumes of small players have fallen and have been grabbed by the big companies. Q - All leading steelmakers are undertaking large capacity expansions. Will this additional capacity go on stream? Will the supply be commensurate with demand which may pick up only slowly? A - India is a demand centre. We have a per capita usage of 55 kilogram per annum against the global per capita usage of 225 kilkogram. 60% of India’s population lives in rural areas where the per capita usage is 18 kilogram per annum. In the last one year or so, demand has been subdued. We have had elections in five States and at the Centre. The 12{+t}{+h} Five Year Plan outlay of USD 1 trillion to be spent on various infrastructure sectors is at 10% of GDP the highest since India started planning. But the achievement has been dismal as government projects could not take off because of elections. Now the new government is in place and there is a new agenda. We are already seeing signs of recovery. A number of projects are now getting cleared. So you will the real impact in the next five to six months when held up projects take off. That will stimulate the steel demand. Fundamentals are strong in terms of low per capita usage. That is why no steel maker in India has curtailed capacity expansion plans. Q - What are your expectations from the Budget? A - The steel industry per se is not doing well and the stainless steel market is virtually in a glut. All companies in the stainless steel segment are bleeding. The import duty on stainless steel is only 5%. So our expectation from the Budget is that the import duty on stainless steel will be put up. About a year ago, the government had imposed an ad hoc duty of 20% (over and above 5%) on imported stainless steel products from China. We, along with industry associations, have taken up this matter with the government. Import duty on carbon steel product imports must also

Page 13 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

go up. Source – The Hindu Business Line Get latest updates through Twitter – Follow @steelguru (www.steelguru.com)

160 million tonne capacity yet to come up in Eastern Region of India - Steel Ministry (Follow @SteelGuru on Twitter for important updates) Economic Times reported that Eastern region is set to push India's steel capacity with an investment of nearly INR 9 lakh crore for creating an additional 160 million tonnes per annum capacity in the next 10 to 15 years. The Steel Ministry estimates that 16 new plants are set to come up in mineral-rich eastern states adding 42 million tonnes per annum new capacity in coming five years, another 45 million tonnes per annum in next five years and further 73 million tonne per annum in about 15 years from now. In a presentation to Prime Minister Mr Narendra Modi, Steel Secretary Mr G Mohan Kumar has said six new mills could come up in Odisha, five in Jharkhand, four in Chhattisgarh and one in West Bengal with a cumulative investment of INR 8.92 lakh crore investment till 2030. Exuding confidence that India has potential to become a global leader both in production and consumption of steel, Mr Kumar said that a total of INR 12 lakh crore investment including INR 8.92 lakh crore in the east, could come up in the sector for trebling capacity to 300 MT by 2030. Sensing that funding could be a problem for the expansion of the sector, Kumar, in his presentation to Mr Modi, also sought infrastructure status for steel and pitched for indigenisation of design, manufacturing and erection of plants. He also listed out the concerns arising out of the recent developments that are impeding growth such as decline in iron ore production, low priority in coal and gas allocation, delay in statutory clearances and infrastructure bottlenecks. Source - Economic Times Get latest updates through Twitter - Follow @steelguru (www.steelguru.com)

SAIL team visits 3 sites in Telangana for possible steel plant project (Follow @SteelGuru on Twitter for important updates) Deccan Chronicle reported that serious efforts are being made by the Telangana Government to set up a steel plant in Khammam district and a team from the Steel Authority of India Limited visited Bayyaram, Paloncha and Kothagudem mandals on the request of the state government recently. As per the report, SAIL team inspected iron ore availability in the district and the feasible place to set up the steel plant. The team inspected three places Velamanuru, in Paloncha mandal, Kunaram, in Kothagudem mandal and Bayyaram for the project site. Mr Venkat Reddy an official in the mining department said that “There is every possibility to set up a steel plant by SAIL in the district. Team of SAIL that visited the district responded positively to it.” The iron ore mines are spread over 5,342 hectares in Bayyaram, Garla, Paloncha and Kothagudem mandals. The Indian Bureau of Mines has estimated the value of ore at INR 16 lakh crore. According to preliminary reports, some 18 million tonnes of iron ore would be available in these three mandals. The report added that the proposed plant also requires 750 MW Power and 1.5 tmc of water to run the plant.

Page 14 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

Source - Deccan Chronicle Get latest updates through Twitter - Follow @steelguru (www.steelguru.com)

Wazirpur steel factory workers call off strike (Follow @SteelGuru on Twitter for important updates) The Hindu Businessline reported that thousands of striking steel factory workers in Delhi’s Wazirpur industrial area called off their 22 day strike after reaching an agreement with the owners. The workers, most of whom are migrants, have been on strike since June 6. They met the factory owners at the Deputy Labour Commissioner’s office late on Friday. Garam Rolla Mazdoor Ekta Samiti, which had spearheaded the strike said that owners of all the factories have accepted to implement the eight hour workday, double the rate of overtime, minimum wages, ESI, and provident fund for the workers of Wazirpur. Mr Sunny Singh a member of the Samiti said that “Almost all the basic labour laws have been enforced in this negotiation.” The workers are engaged in ancillary units such as cold rollers, steel pickling units, shearing and machine-pressers in 23 factories in Wazirpur which make steel utensils. Last week, they held a protest at Jantar Mantar, highlighting the hazardous conditions of work, some times without protective gear, and had been demanding a wage hike, job security, reduction in work hours and health insurance, as hot rolling is a high risk job. Mr Raghuraj, another member of the Samiti said that the Deputy Labour Commissioner, had assured them that officials from the labour department would conduct surprise inspections throughout the month to ensure implementation of eight-hour workday and payment of wages. A statement by the labour department said Joint Labour Commissioner KR Verma and Deputy Labour Commissioner (North West district) UK Sinha had taken cognisance of the matter and after a prolonged conciliation proceeding, a settlement was made between the representatives of the management and the workers. Source - The Hindu Businessline Get latest updates through Twitter - Follow @steelguru (www.steelguru.com)

JLR aurge GBP 200 million investment at Halewood plant PTI reported that TATA Motors owned Jaguar Land Rover, an investment of GBP 200 million at its Halewood plant in the UK to support introduction of its upcoming SUV Discovery Sport. The company in a statement said that the Halewood plant, which is already home to the company's fastest selling model of all time - the Range Rover Evoque, has benefited from a GBP 200 million pounds investment to support the introduction of the first member of the all-new Land Rover Discovery family. It said that the latest investment takes the total amount invested in Halewood over the last 4 years to almost GBP 500 million. The company said that 250 new jobs have been created at the plant thus trebling Halewood workforce in four years.

Page 15 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

Mr Ralf Speth CEO of Jaguar Land Rover said that "The Land Rover Discovery Sport is the next in a line of exciting new products to come from Jaguar Land Rover. I am delighted that Halewood - and Liverpool - has been selected for this new investment." The new Land Rover Discovery Sport, which will go on sale in 2015, is the first member of an all-new family of Discovery vehicles, inspired by the Discovery Vision Concept which was spectacularly showcased at the New York International Auto Show. Mr Richard Else, Jaguar Land Rover Halewood Operations Director, said that "We have seen our workforce treble and production quadruple in just four years. Today we are operating three shifts, 24 hours a day to meet global demand and I am confident that the team will rise to the challenge and deliver a flawless launch of this exciting new model." Source - PTI Get latest updates through Twitter – Follow @ AutomobilesGuru (www.automobileguru.in)

Odisha government sets terms for SPVs to expedite steel projects (Follow @steelguru on Twitter for important updates) Odisha Sun Times reported that the Odisha government has given its in principle consent to be a partner in the Special Purpose Vehicle proposed by the Union Steel Ministry, which has planned to revive investor interest in the sector by creating SPVs that will acquire all government approvals required to start a steel plant and then hand them over to private companies to go ahead with project implementation. The government, however has given some suggestions before the finalisation of the Memorandum of Agreement to be signed between Odisha government, Ministry of Steel and National Mineral Development Corporation for formation of SPVs. The steel ministry has proposed that the NMDC head the SPVs, along with the state mineral development corporation that is Odisha Mining Corporation in Odisha. The ministry wants to roll out the SPV model in four mineral rich states: Karnataka, Odisha, Chhattisgarh and Jharkhand. The Odisha government in its suggestion said that the proposed holding company to oversee all the projects in the state, may not be required as such a proposal would have been advisable in case there would have been multiple projects and 2nd tier SPVs as in case of PFC for UMPPs which has multiple SPVs across the country. Therefore, it is suggested that we may have only project specific SPVs. It also said that SPVs proposed with SMDCs would be critical for establishing mining linkage for the project which would be as crucial as land and other statutory approvals. The government said that it is important to ensure that adequate mineral linkage support is provided in favour of project SPV with firm and assured supply arrangements and pricing. Absence of assured mineral linkage would not result in making the proposal attractive resulting in poor response from the market at a later stage. However, it is suggested that the project SPV may not be entrusted with the activity of arranging mineral linkage as such activity may dilute its effort for timely fulfillment of its objectives land, infrastructure and clearances. Batting for IDCO, the government said that the state PSU’S participation on behalf of the state in the project SPV should be welcomed due to its capabilities in land acquisition, infra linkages and obtaining clearances. With respect to provision in the MOA regarding allocation of water, the government suggested that the provision that state shall endeavour to unlock the water earmarked under existing MoUs which have not progressed for allocation in favour of SPV may be relooked. Source – Odisha Sun Times Get latest updates through Twitter – Follow @steelguru

Page 16 of 15 19th

Issue Steel Re Rolling Mills Association of India visit www.srma.co.in

SRMA STEEL NEWSLETTER

SRMA

Steel Re Rolling Mills Association of India

www.sram.co.in

(www.steelguru.com)

Steel Ministry reports outlines 300 million tonne capacity in India by 2025 (Follow @steelguru on Twitter for important updates) Economic Times reported that Indian Steel Ministry in a recent report has said that mega steel projects need to be set up in states like Jharkhand, Chhattisgarh and Odisha to take the country's production capacity of the metal to 300 million tonne in a decade. The Steel Ministry, prepared document said that "For realizing the national mission of having steel capacity of 300 million tonne by 2025-26, an additional steel production capacity of 176 million tonne per annum in eastern sector and about 26 million tonne in rest of India is required.” The document has projected huge direct and indirect employment opportunities to the tune of approximately 315,000 and 1,262,000, respectively, from large steel complexes, associated social infrastructure facilities and ancillary industries. It said that setting up of mega steel projects in a place give fillip to the all round development of the area and overall business and industrial climate is raised by the growth of ancillary units in both manufacturing sectors like power generation and foundry and service sectors such as consultancy, education and health. The government has also sought suggestions from various stakeholders, including industry representatives, on its report. At present, the country's crude capacity for steel production is 96 million tonnes per annum. Source - Economic Times Get latest updates through Twitter - Follow @steelguru (www.steelguru.com)