Embed Size (px)

Citation preview

STATE OF MICHIGAN

OAKLAND COUNTY CIRCUIT COURT

ALAN POLAND, Individually and on Behalf of All Others Similarly Situated, and Derivatively on Behalf of ITC HOLDINGS CORP.,

Case No. 2016-151852-CB Hon. Alexander

O) CLASS ACTION CO

Plaintiff, AMENDED COMPLAINT FOR BREACH OF FIDUCIARY DUTIES

O

vs. CL 00 FORTIS INC., FORTISUS INC., ELEMENT

ACQUISITION SUB INC., JOSEPH L. WELCH, ALBERT ERNST, CHRISTOPHER H. FRANKLIN, EDWARD G. JEPSEN, DAVE R. LOPEZ, HAZEL R. O'LEARY, THOMAS G. STEPHENS, G. BENNETT STEWART III and LEE C. STEWART,

O CT CL < CD

O CNJ j*:

Defendants, CD

O and

c ITC HOLDINGS CORP., a Michigan 3 corporation, O

O Nominal Party. •O c DEMAND FOR JURY TRIAL / cc

THE MILLER LAW FIRM, P.C. E. POWELL MILLER (P39487) MARC L. NEWMAN (P51393) RICHARD L. BRAUN (P26408) 950 W. University Drive, Suite 300 Rochester, MI 48307 Telephone: 248/841-2200 248/652-2852 (fax)

ROBBINS GELLER RUDMAN & DOWD LLP

DAVID T. WISSBROECKER EDWARD M. GERGOSIAN (P35322) 655 West Broadway, Suite 1900 San Diego, CA 92101 Telephone: 619/231-1058 619/231-7423 (fax)

ro O

CT>

C

LL

O

T3 <D > CD O CD

CE

SUMMARY OF THE ACTION

This is a shareholder action brought by plaintiff: (i) derivatively on behalf of ITC

Holdings Corp. ("ITC" or the "Company"); and (ii) individually and on behalf of all other similarly

situated shareholders of ITC, against the members of ITC's Board of Directors (the "Board"), Fortis

Inc., FortisUS Inc., a Delaware corporation ("Parent"), and Element Acquisition Sub Inc., a

Michigan corporation and a direct wholly owned subsidiary of Parent ("Merger Sub" and with Fortis

Inc. and Parent, "Fortis") , for breaches of fiduciary duty and/or the aiding and abetting such

breaches of fiduciary duty, arising out of the proposed sale of ITC to Fortis (the "Proposed

Acquisition").

O) CO

o

CL 00 o cr CL < ITC is headquartered in Novi, Michigan, and is the largest independent electric

transmission company in the United States. On February 9, 2016, ITC and Fortis announced that

they had entered into an Agreement and Plan of Merger (the "Merger Agreement"). Pursuant to the

Merger Agreement, Fortis will acquire ITC by purchasing all of the Company's outstanding shares at

a purchase price of just $22.57 in cash and 0.7520 of a Fortis share for each share of ITC common

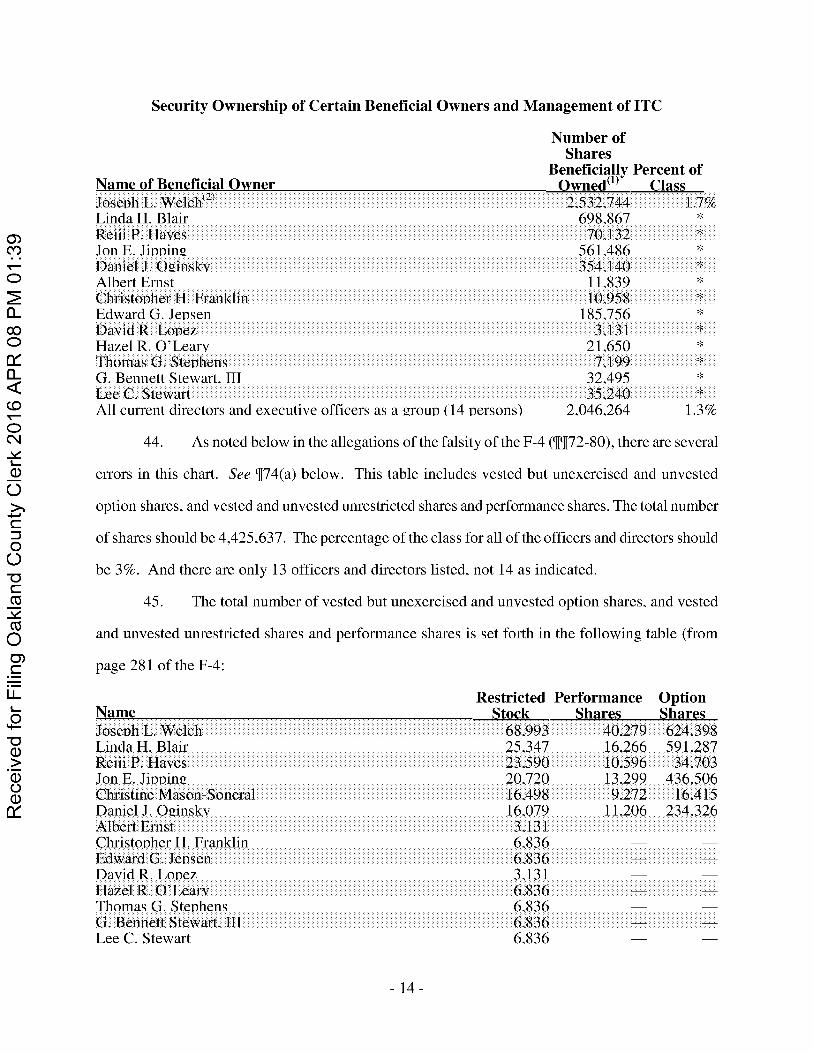

stock owned. Following the consummation of the Proposed Acquisition, ITC will become a

subsidiary of Fortis and approximately 27% of the common shares of Fortis will be held by ITC

shareholders.

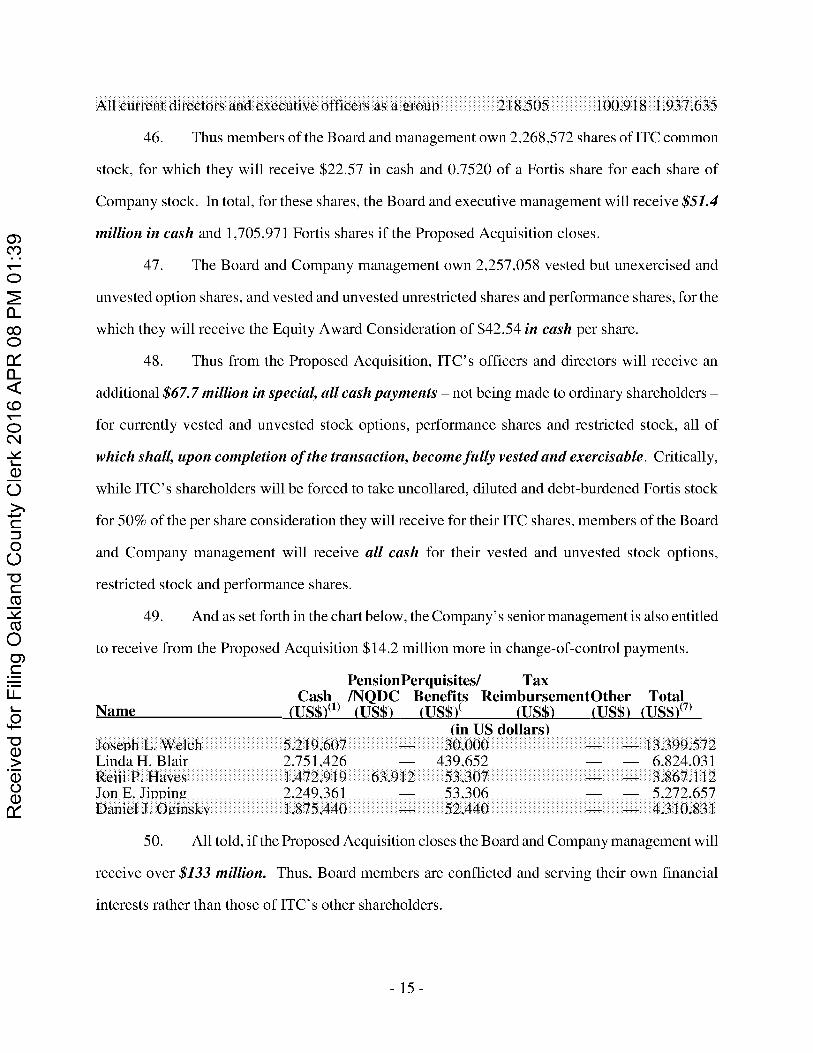

CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O The Proposed Acquisition is the product of a hopelessly flawed process that is

designed to ensure the sale of ITC to Fortis on terms preferential to defendants and other ITC

insiders and to subvert the interests of plaintiff and the other public stockholders of the Company.

The Proposed Acquisition is being driven by the Company's current Board and management, who

collectively hold 3% of ITC's outstanding shares (over 4.5 million shares and including vested and

unvested stock options, restricted stock and performance shares). The Board and other Company

insiders seek liquidity for their illiquid holdings in ITC stock, and the Proposed Acquisition offers

significant liquidity for their illiquid ITC shares. If the Proposed Acquisition closes, the Board and

Company management will receive over $5/ million from the sale of shares owned as of the date of

the Merger Agreement.

CT>

C

LL

O

T3 <D > CD O CD 01

4. From the Proposed Acquisition, ITC' s officers and directors will receive an additional

$67.7 million in special payments - not being made to ordinary shareholders - for currently

unvested stock options, performance shares and restricted stock, all of which shall, upon completion

of the transaction, become fully vested and exercisable. Critically, while ITC's shareholders will

be forced to take uncollared, diluted and debt-burdened Fortis stock for 50% of the per share

consideration they will receive for their ITC shares, members of the Board and Company

management will receive all cash for their vested and unvested stock options, restricted stock and

performance shares. The Company's senior management is also entitled to receive from the

Proposed Acquisition $14.2 million more in change-of-control payments. All told, if the Proposed

Acquisition closes the Board and Company management will receive over $133 million. Thus,

Board members are conflicted and serving their own financial interests rather than those of ITC's

other shareholders.

O) CO

O

CL 00 o

CL < CD

O CNJ j*: CD

As a result of these unresolved conflicts, the process leading to the Proposed

Acquisition was flawed and favored the interests of Fortis and the Board and Company management.

For example, on January 11, 2016, Fortis offered to acquire all of ITC's outstanding shares for

$44.25 in cash. But later the same day, Fortis withdrew the all cash offer because it had received an

unfavorable report from a national debt rating agency service with respect to the proposed

transaction, and thus Fortis could not afford to pay all cash to acquire ITC. In the face of this

stunning revelation, the Board did not tell Fortis to take a hike but instead continued to negotiate

with Fortis, which now had one hand tied behind its back in terms of what it could offer to acquire

ITC. Ultimately, the Board agreed to sell ITC to Fortis for just $22.57 in cash and 0.7520 of a Fortis

share for each share of ITC common stock. The Board members did, however, make sure they and

ITC management will be paid all cash for their vested and unvested stock options, restricted stock

and performance shares.

o c o O •O c ro

ro O

CT>

C

LL

O

T3 <D > CD O CD

QL

This flawed and conflicted process resulted in an unfair price for ITC's public

shareholders. The Proposed Acquisition consideration drastically undervalues the Company and its

prospects. First, based on the closing price of Fortis stock the day before the Proposed Acquisition

6.

was announced ($29.71), the Proposed Acquisition consideration was valued at just $44.91 per ITC

But defendants failed to obtain a collar on the Fortis stock portion of the Proposed

Acquisition consideration, and on the day the deal was announced, Fortis common closed down

sharply at $26.97, reducing the value of the Proposed Acquisition consideration to $42.85. This

represents a premium of just 8.8% to ITC's closing price the day before the deal was announced, and

is lower than an analyst's high price target of $45.00 per ITC share.

Second, rather than demanding an all-cash offer for all ITC shares, the Board

accepted an offer that included a substantial amount of Fortis stock for ITC's public shareholders

(and again without a collar). Fortis, however, intends to sell up 20% of the value of ITC to an

infrastructure fund in order to finance the deal. This will further dilute the value of the stock portion

of the Proposed Acquisition consideration. Third, the Proposed Acquisition will lift Fortis's debt

burden to more than $15 billion from its current $9.1 billion.

share.

O) CO

o

CL 00 o cr CL < CD

O CNJ j*: CD

On the other hand, the Board and the members of management treated themselves

differently and better than ITC's public shareholders are being treated. For each of ITC's 2,257,058

vested or unvested stock options, performance shares and restricted shares that they own, the

members of ITC's Board and executive management will receive $42.54 per share in cash, or as

noted above, over $67.7 million in cash. Unlike ITC's other shareholders, who will only receive

$22.57 in cash and 0.7520 of a Fortis share for each share of ITC common stock owned, the Board

g o c o O •O c ro

ro O

CT>

C and management will not be harmed by the lack of a collar, the dilution from Fortis' plan to sell 20%

of ITC's equity, or Fortis' dramatically increased debt burden following the Merger.

Motivated by the prospect of receiving over $133 million in cash from a deal with

Fortis, defendants agreed to the Proposed Acquisition, in breach of their fiduciary duties to ITC's

public shareholders, through an unfair sales process. Rather than undertake a full and fair sales

process designed to maximize shareholder value as their fiduciary duties require, the Board catered

to their liquidity goals, as well as to Fortis.

To protect against the threat of alternate bidders out-bidding Fortis after the

announcement, plaintiff alleges on information and belief that defendants implemented preclusive

LL

O

T3 9 <D > CD O CD 01

10.

deal protection devices to guarantee that Fortis would not lose its preferred position. On information

and belief, plaintiff alleges that those deal protection devices will preclude a fair sales process for the

Company and lock out competing bidders, and include:

(a) a "no-solicitation" or "no-shop" provision that precludes ITC from providing

confidential Company information to, or even communicating with, potential competing bidders for

the Company except under very limited circumstances;

(b) an illusory "fiduciary out" for the no-shop provision that requires the

Company to provide Fortis with advance notice before providing any competing bidder with any

confidential Company information, even after the Board has determined that the competing bid is

reasonably likely to lead to a superior proposal and that the Board is breaching its fiduciary duties by

not providing the competing bidder with confidential Company information;

(c) an "information rights" provision that requires the Company to provide Fortis

with confidential, non-public information about competing proposals which Fortis can then use to

formulate a matching bid;

O) CO

O

CL 00 o cr CL < CD

O CNJ j*: CD

O

c 3 o (d) a "matching rights" provision that requires ITC to provide Fortis with the

opportunity to match any competing proposal; and

(e) a termination and expense fee provision that requires the Company to pay

Fortis a $245 million penalty if the Proposed Acquisition is terminated in favor of a superior

proposal.

o •o c ro

ro O

CT>

C

LL 11. Thus, the Board compounded its breaches by, inter alia, agreeing to these

unreasonable deal protection devices that preclude other bidders from making a successful

competing offer for the Company. The support agreements and the deal protection devices prelude a

fair sales process for ITC s shareholders and make the Proposed Acquisition a virtual fait accompli.

12. To make matters worse, and in an attempt to secure shareholder support for the unfair

Proposed Acquisition, on March 17,2016, defendants caused Fortis to file a Form F-4 Registration

Statement ("F-4"). The F-4 included ITC's Preliminary Proxy Statement, which recommends that

ITC stockholders vote in favor of the Proposed Acquisition, omits and/or misrepresents material

O

T3 <D > CD O CD

QL

- 4 -

information about the unfair sales process for the Company, conflicts of interest that corrupted the

sales process, the unfair consideration offered in the Proposed Acquisition, ITC s inherent value, and

data and assumptions underlying the fairness analyses performed by ITC's three financial advisors.

See below at (][(][72-80. Significantly the F-4provides no information about when or why the Board

members decided that they and ITC management - unlike ITC's public shareholders - will be paid

all cash (over $67.7 million) for their vested and unvested stock options, restricted stock and

performance shares.

13. In pursuing the unlawful plan to sell ITC, each of the defendants violated applicable

law by directly breaching and/or aiding and abetting the other defendants' breaches of their fiduciary

duties of loyalty, due care, candor, independence, good faith and fair dealing.

14. Instead of attempting to obtain the highest price reasonably available for ITC for its

shareholders, defendants tailored the terms of the Proposed Acquisition to meet the specific needs of

Company insiders and Fortis. In essence, the Proposed Acquisition is the product of a hopelessly

flawed process that was designed to ensure the sale of ITC to Fortis and Fortis only, on terms

preferential to Fortis and to aggrandize the financial interests of Company insiders at the expense of

plaintiff and ITC's public stockholders.

15. Plaintiff seeks to enjoin the Proposed Acquisition.

O) CO

O

CL 00 o

CL < CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O JURISDICTION AND VENUE

CT>

C 16. This Court has jurisdiction over ITC because ITC conducts business in Michigan, is a

citizen of Michigan and is incorporated in Michigan. ITC has its principal place of business at LL

O

T3 27175 Energy Way, Novi, Michigan. <D > Venue is proper in this Court under MCL §600.1621(a) because at least one

defendant resides and/or has a place of business in this County.

17. CD O CD 01

THE PARTIES

18. Plaintiff Alan Poland is, and at all times relevant hereto was, a shareholder of ITC.

19. Nominal party ITC is a Michigan corporation headquartered in Novi, Michigan.

20. Defendant Fortis Inc. is an international diversified electric utility holding company

headquartered in St. John's, Newfoundland, and a party to the Merger Agreement. Defendant Fortis

is sued herein as an aider and abettor.

21. Defendant Parent is a Delaware corporation and a party to the Merger Agreement.

Defendant Parent is sued herein as an aider and abettor. O) CO

22. Defendant Merger Sub is a Michigan corporation, a party to the Merger Agreement

and a direct wholly owned subsidiary of Parent. Defendant Merger Sub is sued herein as an aider

and abettor.

O

CL 00 o cr 23. Defendant Joseph L. Welch is and has been at all relevant times ITC's Chairman, CL < President and CEO, and a member of the Board. CD

24. Defendant Albert Ernst is and has been at all relevant times a member of the Board. O CNJ j*: 25. Defendant Christopher H. Franklin is and has been at all relevant times a member of CD

the Board. o 26. Defendant Edward G. Jepsen is and has been at all relevant times a member of the c

o Board. o •o 27. Defendant Dave R. Lopez is and has been at all relevant times a member of the c TO

Board. CC O 28. Defendant Hazel R. O'Leary is and has been at all relevant times a member of the

CT> c Board.

LL 29. Defendant Thomas G. Stephens is and has been at all relevant times a member of the O

T3 Board. <D > 30. Defendant G. Bennett Stewart III is and has been at all relevant times a member of the CD

O CD Board. CE

31. Defendant Lee C. Stewart is and has been at all relevant times a member of the

Board.

32. The defendants named above in (][(][23-31 are sometimes collectively referred to herein

as the "Individual Defendants."

- 6 -

THE PROPOSED ACQUISITION

Background

33. Headquartered in Novi, Michigan, ITC is the largest independent electric

transmission company in the United States. ITC invests in the electric transmission grid to improve

reliability, expand access to markets, allow new generating resources to interconnect to its

transmission systems and lower the overall cost of delivered energy. Through its regulated operating

subsidiaries ITC Transmission, Michigan Electric Transmission Company, ITC Midwest and ITC

Great Plains, ITC owns and operates high-voltage transmission facilities in Michigan, Iowa,

Minnesota, Illinois, Missouri, Kansas and Oklahoma, serving a combined peak load exceeding

26,000 megawatts along approximately 15,600 circuit miles of transmission line. ITC's grid

development focus includes growth through regulated infrastructure investment as well as domestic

and international expansion through merchant and other commercial development opportunities.

34. Fortis is a leader in the North American electric and gas utility business, with total

assets of approximately C$28.6 billion as at September 30,2015, and revenue totaling approximately

C$6.7 billion for the twelve-month period ended September 30, 2015. Its regulated utilities serve

more than three million customers across Canada and in the United States and the Caribbean. Fortis

O) CO

O

CL 00 o cr CL < CD

O CNJ j*: CD O

c 3 o O -O c

CO also owns long-term contracted hydroelectric generation assets in British Columbia and Belize.

The Company's Ongoing and Growing Success

35. Over the last several years, ITC has reported significant financial performance,

signaling excellent prospects for growth. As set forth in the chart below, over the last five years,

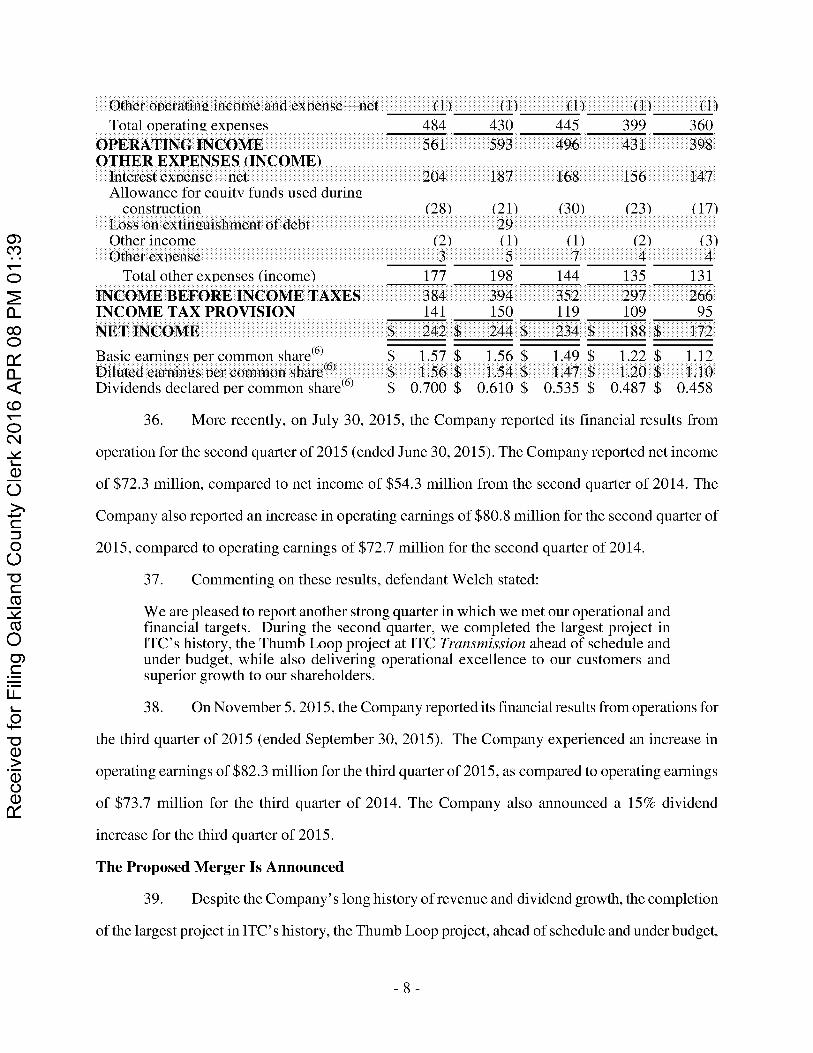

ITC has reported increasing revenues and dividends:

03 O O) c LL

£ TJ 0 >

ITC and Subsidiaries CD O Year Ended December 31.

2015 2014 2013 2012 2011 CD a:

(in millions of US dollars, except per share amounts)

WfliWS)® S 1.045 S 1.023 S 'Ml S 831 S 757 OPKRATINC; RKVKNTKS OPERATING EXPENSES

122 129 112 113 113 Oneration and maintenance General and administrative 1 Vmvcialion ami amorli/alion Taxes other than income taxes

(4X5) 149 112 83 145 115 1 1 9 95 128 107 145 66 60 53 82 77

( 1 ) (1) ( 1 ) Olhcr o ivml in« j i nco i i K ' ; I IH I CMVIISC nc l

Total oncralinc expenses ( 1 ) ( 1 )

360 399 445 484 430 398 431 496 OI'KRATINC INCOMK

OTHER EXPENSES (INCOME) 561

147 156 168 204 187 In le ivs l expense ne l Allowance for eauitv funds used durins

construction Loss on exliivjuishmenl of dehl Other income Other expense

(17) (23) (30) (28) (21) 29

(3) (2) ( 1 ) a> (2) ( 1 ) CO 4 4 1

131 135 144 Total other expenses (income) 198 177 O 266 297 "2 384 m INCOME BEFORE INCOME TAXES

INCOME TAX PROVISION NET INCOME

95 109 119 141 150 Q_

$ TJ/ $ n56 $ L49 $ 1.22 $ 1.12 $ 1.56 $ 1.54 $ 1.47 $ 1.20 S 1.1.0 $ 0.700 $ 0.610 $ 0.535 $ 0.487 $ 0.458

00 o (6) Basic eamines per common share Diluted earnings per common shaiv"" Dividends declared per common share

CL (6) < CO

36. More recently, on July 30, 2015, the Company reported its financial results from

operation for the second quarter of 2015 (ended June 30,2015). The Company reported net income

of $72.3 million, compared to net income of $54.3 million from the second quarter of 2014. The

Company also reported an increase in operating earnings of $80.8 million for the second quarter of

2015, compared to operating earnings of $72.7 million for the second quarter of 2014.

37. Commenting on these results, defendant Welch stated:

We are pleased to report another strong quarter in which we met our operational and financial targets. During the second quarter, we completed the largest project in ITC's history, the Thumb Loop project at ITC Transmission ahead of schedule and under budget, while also delivering operational excellence to our customers and superior growth to our shareholders.

38. On November 5,2015, the Company reported its financial results from operations for

the third quarter of 2015 (ended September 30, 2015). The Company experienced an increase in

operating earnings of $82.3 million for the third quarter of 2015, as compared to operating earnings

of $73.7 million for the third quarter of 2014. The Company also announced a 15% dividend

increase for the third quarter of 2015.

The Proposed Merger Is Announced

39. Despite the Company's long history of revenue and dividend growth, the completion

of the largest project in ITC s history, the Thumb Loop project, ahead of schedule and under budget.

O CM J*

0 o c 3 o O •O c ro

ro O O) c LL

£ ~o 0) > 0) o CD

g

and delivering operational excellence to our customers and superior growth to our shareholders, the

Board decided to sell the Company.

40. On February 9,2016, ITC and Fortis announced that they had entered into the Merger

Agreement. Pursuant to the Merger Agreement Fortis will acquire ITC by purchasing all of the

Company's outstanding shares at a purchase price of just $22.57 in cash and 0.7520 Fortis shares for

each share of ITC common stock. Following the consummation of the Proposed Acquisition, ITC

will become a subsidiary of Fortis and just 27% of the common shares of Fortis will be held by ITC

shareholders.

O) CO

o

CL 00 o cr 41. The press release announcing the Proposed Acquisition states in pertinent part: CL < FORTIS INC. TO ACQUIRE ITC HOLDINGS CORP.

FOR US$11.3 BILLION CD

O CNJ Fortis to increase its 2016 consolidated mid year rate base to approximately

C$26 billion (US$18 billion) with acquisition of the largest independent transmission utility in the United States

j*: CD

O Highlights

c The acquisition aligns with Fortis' financial objectives by providing approximately 5% earnings per common share accretion in the first full year following closing, excluding one-time acquisition-related expenses. Fortis continues to target 6% average annual dividend growth through 2020.

O O •O c ro

ITC owns and operates high-voltage transmission facilities in Michigan, Iowa, Minnesota, Illinois, Missouri, Kansas and Oklahoma, serving a combined peak load exceeding 26,000 megawatts along approximately 15,600 miles of transmission line.

ro O

CT>

C

LL Fortis will become one of the top 15 North American public utilities ranked by enterprise value. O

T3 ITC's FFRC regulated operations, with substantial rate base growth and robust investment opportunities, add a new growth platform. <D >

CD O Following the acquisition, ITC will continue as a stand-alone transmission

company, retaining its focus on growth and operational excellence while benefiting from a broader platform that will support its mission to modernize electrical infrastructure in the U.S.

CD 01

ITC's average rate base and CWIP is expected to grow at a compounded average annual rate of approximately 7.5% through 2018.

Fortis intends on retaining all of ITC's employees and maintaining the corporate headquarters in Novi, Michigan.

- 9 -

The per share consideration of cash and Fortis stock payable to ITC shareholders of US$44.90 represents a 33% premium to the unaffected closing share price on November 27,2015 and a 37% premium to the 30-day average unaffected share price prior to November 27,2015. Pro forma, upon closing of the transaction, ITC shareholders will own approximately 27% of the combined company and will receive a meaningful increase in their dividend per share.

In connection with the acquisition, Fortis will apply to list its common shares O) on the NYSE. CO

o Fortis Inc. ("Fortis") and ITC Holdings Corp. ("ITC") announced today that they have entered into an agreement and plan of merger pursuant to which Fortis will acquire ITC in a transaction (the "Acquisition") valued at approximately US$11.3 billion. Under the terms of the transaction ITC shareholders will receive US$22.57 in cash and 0.7520 Fortis shares per ITC share. At yesterday's closing price for Fortis common shares and the US$/C$ exchange rate, the per share consideration represents a premium of 33% over ITC's unaffected closing share price on November 27,2015 and a 37% premium to the unaffected average closing price over the 30 day period prior to November 27, 2015.

Following the Acquisition, Fortis will be one of the top 15 North American public utilities ranked by enterprise value, with an estimated enterprise value of C$42 billion (US$30 billion). On a pro forma basis, the consolidated mid year 2016 rate base of Fortis would increase by approximately C$8 billion (US$6 billion) to approximately C$26 billion (US$18 billion), as a result of the Acquisition.

"Fortis has grown its business through strategic acquisitions that have contributed to strong organic growth over the past decade. Our performance in 2015 is a clear demonstration of the success of this strategy," says Mr. Barry Perry, President and Chief Executive Officer of Fortis. "The acquisition of ITC - a premier pure-play transmission utility - is a continuation of this growth strategy. ITC not only further strengthens and diversifies our business, but it also accelerates our growth."

cl 00 o

cl < CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O

CT> Under the terms of the Acquisition, which has been approved by the boards of directors of both companies, ITC shareholders will receive approximately US$6.9 billion in Fortis common shares and cash at closing and Fortis will assume approximately US$4.4 billion of consolidated ITC indebtedness. Upon completion of the Acquisition, ITC will become a subsidiary of Fortis and approximately 27% of the common shares of Fortis will be held by ITC shareholders. Fortis will apply to list its common shares on the New York Stock Exchange ("NYSE") in connection with the Acquisition and will continue to have its shares listed on the Toronto Stock

c LL

O

T3 <D > CD O Exchange ("TSX"). CD

QL "From the very beginning of ITC, we have been focused on creating

meaningful value for all stakeholders, including customers, investors and employees, by becoming the leading electric transmission company in the U.S.," says Joseph L. Welch, Chairman, President and CEO of ITC. "Fortis is an outstanding company with a proven track record of successfully acquiring and managing U.S. based utilities in a decentralized manner. This transaction accomplishes our objectives by better positioning the company to have a higher level of focus on pursuing our long-term strategy of investing in transmission opportunities to improve reliability, expand

- 1 0 -

access to power markets and allow new generating resources to interconnect to transmission systems and lower the overall cost of delivered energy for customers.

"I am forever grateful for the hard work of the ITC employees in building this great company and look forward to a bright future of continued operational excellence supported by the Fortis platform," says Mr. Welch. "We also very much appreciate the longstanding support of our investors who will receive an attractive premium for their investment and will also benefit from the opportunity to participate in the upside of the combination, including future value creation and a growing dividend program."

In addition to the necessary state approvals, the closing of the Acquisition is subject to ITC and Fortis shareholder approvals, the satisfaction of other customary closing conditions, and certain regulatory and federal approvals including, among others, those of the Federal Energy Regulatory Commission ("FFRC"), the Committee on Foreign Investment in the United States, and the United States Federal Trade Commission/Department of Justice under the Hart-Scott-Rodino Antitrust Improvement Act. The closing of the Acquisition is expected to occur in late 2016.

A joint conference call and webcast is scheduled for Tuesday February 9, 2016 beginning at 8:30 a.m. Eastern Time (details provided below).

Entry into FERC Regulated Transmission

By acquiring ITC, Fortis is acquiring the largest independent pure-play electric transmission company in the United States. ITC owns and operates high-voltage transmission facilities in Michigan, Iowa, Minnesota, Illinois, Missouri, Kansas and Oklahoma, serving a combined peak load exceeding 26,000 megawatts along approximately 15,600 miles of transmission line. In addition, ITC is a public utility and independent transmission owner in Wisconsin. ITC has grown its average rate base at a compounded average annual rate of approximately 16% over the last three years and, as of September 30, 2015, ITC had assets of US$7.4 billion.

"The acquisition of ITC is in alignment with our business model and acquisition strategy, providing meaningful accretion, and creating a unique, highly diversified, low-risk regulated energy transportation platform," explains Mr. Perry. "The predictable returns of a transmission business, with no commodity or fuel exposure, are very compelling.

O) CO

o

cl 00 o

cl < CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

O "We take a very disciplined approach to acquisitions and are focused on businesses that have experienced management teams, provide geographic diversity in favorable economic regions, and possess significant growth prospects," concludes

T3 <D >

Mr. Perry. CD O CD Strategic Rationale

The strategic rationale underlying the transaction includes:

QL

The Acquisition aligns with Fortis' financial objectives by providing approximately 5% earnings per common share accretion in the first full year following closing, excluding one-time Acquisition-related expenses. Fortis continues to target 6% average annual dividend growth through

Accretive Transaction

2020.

- 1 1 -

Increases Diversification opportunity for Fortis to significantly diversify its business in terms of regulatory jurisdictions, business risk profile and regional economic mix. Based on the twelve months ended September 30, 2015, pro forma the Acquisition, ITC is expected to represent almost 40% of the consolidated regulated operating earnings of Fortis. The Acquisition will increase the regional economic diversity of Fortis from its current operations in five Canadian provinces, the U.S. states of New York and Arizona, and three Caribbean countries, to include a presence in eight additional U.S. states.

Supportive FERC Regulation - ITC's tariff rates are regulated by FFRC, which has been one of the most consistently supportive utility regulators in North America providing reasonable returns and equity ratios. Rates are set using a forward-looking rate-setting mechanism with an annual true-up, which provides timely cost recovery and reduces regulatory lag.

Long-Term Rate Base Growth Prospects - There is a significant need for capital investment in the aging U.S. electric transmission sector to improve reliability, expand access to power markets, allow new generating resources to interconnect to the transmission system and lower the overall cost of energy delivery. Based on ITC's planned capital expenditure program, ITC's average rate base and construction work in progress ("CWIP") is expected to increase at a compounded average annual rate of approximately 7.5% through 2018.

Clean energy policies in the United States, including renewable portfolio standards, are driving the need for new transmission investment to facilitate the delivery of electricity from renewable energy resources to load-serving entities. In particular, the Clean Power Plan ("CPP") is expected to drive investment in renewables and the retirement of coal-fired generation in the U.S. With its economies of scale and geographic footprint, ITC is favourably positioned to participate in the significant transmission investment opportunity fostered by the CPP.

Management Expertise - The ITC management team has a proven track record of strong EPS growth, total shareholder return, cash flow from operations and operational efficiencies. From its initial public offering in 2005 through November 2015, ITC has delivered more than double the annual shareholder returns of the S&P 500 Utilities Sector Index. ITC's experienced and execution-focused management team will continue to operate independently under the ownership structure of Fortis.

Transaction Details

The Acquisition represents a singular

O) CO

o

cl 00 o

cl < CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

O

T3 The agreement and plan of merger relating to the Acquisition includes customary provisions.

In connection with the Acquisition, Fortis will become a registrant with the United States Securities and Exchange Commission (the "SEC") and will apply to list its common shares on the NYSE.

<D > CD O CD 01

Each of the ITC board of directors and Fortis board of directors has approved the Acquisition and has determined that the Acquisition is in the best interest of its shareholders. Each of the ITC board and Fortis board recommend that its shareholders vote in favour of the proposed Acquisition.

In accordance with the requirements of the TSX, Fortis will seek shareholder approval of the issuance of common shares representing 40% of the outstanding

- 1 2 -

common shares of Fortis (on a pre-Acquisition, non-diluted basis) as partial consideration for the Acquisition at an upcoming shareholders' meeting. The resolution is required to be approved by a majority of Fortis shareholders represented in person or by proxy at the meeting. A proxy circular describing the Acquisition in more detail will be mailed to Fortis shareholders in advance of the meeting.

Acquisition Financing

The financing of the Acquisition has been structured to allow Fortis to maintain a solid investment-grade credit rating and is consistent with Fortis's existing capital structure. Financing for the cash portion of the Acquisition will be achieved primarily through the issuance of approximately US$2 billion of Fortis debt and the sale of up to 19.9% of ITC to one or more infrastructure-focused minority investors.

O) CO

o

CL 00 o Advisors cr •_ Goldman Sachs and Scotiabank served as financial advisors to Fortis and

provided committed financing. White & Case LLP and Davies Ward Phillips & Vineberg LLP acted as legal advisors to Fortis.

Barclays and Morgan Stanley acted as financial advisors to ITC. Simpson Thacher & Bartlett LLP acted as legal advisor to ITC. Lazard served as financial advisor and Jones Day acted as legal advisor to ITC's board of directors.

Disabling Conflicts Infect the Process

42. The Proposed Acquisition is the product of a hopelessly flawed process that is

designed to ensure the sale of ITC to Fortis on terms preferential to defendants and other ITC

insiders and to subvert the interests of plaintiff and the other public stockholders of the Company.

The Proposed Acquisition is being driven by the Company's current Board and management, who

collectively hold 3% of ITC's outstanding shares (over 4.5 million shares and including vested and

unvested stock options, restricted stock and performance shares). The Board and other Company

insiders seek liquidity for their illiquid holdings in ITC stock, and the Proposed Acquisition offers

significant liquidity for their illiquid ITC shares. If the Proposed Acquisition closes, the Board and

Company management will receive over $5/ million from the sale of shares owned as of the date of

the Merger Agreement.

43. The ITC shareholdings of the Board and management are set forth in the following

< CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

O

T3 <D > CD O CD 01

table from page 280 of the F-4:

- 13 -

Security Ownership of Certain Beneficial Owners and Management of ITC

Number of Shares

Beneficially Percent of Owned" Class Name of Beneficial Owner

m Joseph L. Welch Linda H. Blair Reiii P. Haves Jon E. Jippine Daniel J. ()«jinsk\ Albert Ernst C'hi'isiopher 11. I 'lanklin Edward G. Jepsen l)a\ ill R. I .ope/ Hazel R. O'Leary Thomas (i. Slephens G. Bennett Stewart. Ill I .ec Slew art All current directors and executive officers as a group (14 persons)

698.867 70.1^2

561.486 .^4.140

11.839 KWSS

185.756 3.131

21.650 7.IW

32.495 35.240

2,046,264

I

O) C O

>{<

o

CL >j< 00 o

0̂ CL < >j<

CD 1.3% O CNJ 44. As noted below in the allegations of the falsity of the F-4 ((][(][72-80j. there are several

errors in this chart. See 1174(a) below. This table includes vested but unexercised and unvested j*:

CD

O option shares, and vested and unvested unrestricted shares and performance shares. The total number

of shares should be 4,425,637. The percentage of the class for all of the officers and directors should

be 3%. And there are only 13 officers and directors listed, not 14 as indicated.

45. The total number of vested but unexercised and unvested option shares, and vested

and unvested unrestricted shares and performance shares is set forth in the following table (from

c o O •O c ro

ro O

CT> page 281 of the F-4: c LL Restricted Performance Option

Shares Shares Name Stock O Joseph L. Welch Linda H. Blair Reiii 1'. I laws Jon E. Jippine C'hi'isline Mason-Soneral Daniel J. Oeinskv Alherl Mm si Christopher H. Franklin l-ilwaiil G. Jepsen David R. Lopez I la/el R. ()T.eai \ Thomas G. Stephens Ci. Bennell Sleuarl. Ill Lee C. Stewart

6S.W3 25.347 23.5l)() 20.720 16.4l)S 16.079 3.131 6.836 6.S36 3.131 6.S36 6.836 6.S36 6,836

40.27') 16.266 l0.5Wr 13.299

l).272 11.206

624.398 591.287

34.703 436.506

16.415 234.326

T3 <D > CD O CD 01

- 1 4 -

All L i i n v n l I M I V L I O I S ami c\ L V i i l i \c oflkvrs ;is ;i moiin J I S . S O S 100,918 1,937,635

46. Thus members of the Board and management own 2,268,572 shares of ITC common

stock, for which they will receive $22.57 in cash and 0.7520 of a Fortis share for each share of

Company stock. In total, for these shares, the Board and executive management will receive $51.4

million in cash and 1,705,971 Fortis shares if the Proposed Acquisition closes.

47. The Board and Company management own 2,257,058 vested but unexercised and

unvested option shares, and vested and unvested unrestricted shares and performance shares, for the

which they will receive the Equity Award Consideration of $42.54 in cash per share.

48. Thus from the Proposed Acquisition, ITC's officers and directors will receive an

additional $67.7 million in special, all cash payments - not being made to ordinary shareholders -

for currently vested and unvested stock options, performance shares and restricted stock, all of

which shall, upon completion of the transaction, become fully vested and exercisable. Critically,

while ITC's shareholders will be forced to take uncollared, diluted and debt-burdened Fortis stock

O) C O

O

CL 00 o

CL < CD

O CNJ j*:

CD

O for 50% of the per share consideration they will receive for their ITC shares, members of the Board

and Company management will receive all cash for their vested and unvested stock options,

restricted stock and performance shares.

And as set forth in the chart below, the Company's senior management is also entitled

to receive from the Proposed Acquisition $14.2 million more in change-of-control payments.

c o O •O c ro

49. ro O

CT>

C PensionPerquisites/ Tax

Benefits Reimbursement Other Total (TISfr) (TISft')

LL Cash /NQDC (TISft') ( Name (US$) o

(in US dollars) M U M )

— 439.652 63.l)i: 53.307

— 53.306 52.440

T3 Jnscnh I.. W elch Linda H. Blair Rciii I'. I laws Jon E. Jinninc Daniel .1. Ouinskv

5.:il).607 2.751.426 1.472.911) 2.249.361 1.875.440

13.399.572 6.824.031 3.867.112 5.272.657 4.310.831

<D > CD O CD 01

50. All told, if the Proposed Acquisition closes the Board and Company management will

receive over $133 million. Thus, Board members are conflicted and serving their own financial

interests rather than those of ITC's other shareholders.

- 1 5 -

51. In addition to "cashing in" their illiquid holdings, members of the Board and

Company management appear to be staying on board after the transaction. As it says in the

announcement of the Proposed Acquisition, "ITC's experienced and execution-focused management

team will continue to operate independently under the ownership structure of Fortis."

52. Furthermore, the Board retained three financial advisors, without explaining why

there was a need for more than one. The terms of the engagement of Barclays Financial Capital, Inc.

("Barclays") to serve as ITC's financial advisor conflict it. Barclays is to be paid $20.7 million for

its service as a financial advisor, even though the Board concluded that Barclays was not

independent. While the F-4 indicates that Barclays was paid $1 million for its fairness opinion, the

remainder of the fee is to be paid out in unspecified installments upon the announcement of the

merger, the approval of the merger by ITC's shareholders, and the consummation of the merger.

53. Similarly, the terms of the engagement of Morgan Stanley & Co. LLC ("Morgan

Stanley") to serve as ITC's financial advisor conflict it. Morgan Stanley is also to be paid $20.7

million for its service as a financial advisor, even though the Board concluded that Morgan Stanley

was not independent. The F-4 indicates that Morgan Stanley was paid $2.1 million shortly after the

execution of the merger agreement, $4.1 million is contingent upon shareholder approval, and the

remainder is contingent upon the consummation of the merger. Furthermore, in the last two years,

Morgan Stanley has received fees of $900,000 for services rendered to ITC, and fees of $ 1.7 million

from services rendered to Fortis or its subsidiaries.

O) CO

O

CL 00 o

CL < CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

54. Finally, the Board hired Lazard Freres & Co. LLC ("Lazard") which the Board

considered independent, even though Lazard has received fees of $1.2 million from Fortis in

connection with the sale of a subsidiary of a company that was acquired by Fortis before the

subsidiary sale was completed. Furthermore, Lazard has been paid $2.5 million for its opinion, and

may receive up to an additional $2 million, solely in the discretion of ITC's Board.

The Unresolved Conflicts Led to an Unfair Process

O

T3 <D > CD O CD

QL

55. The conflicts described above resulted in a process that led to: (i) the Board agreeing

to sell the Company, rather than continuing to operate ITC as a growing and successful standalone

- 1 6 -

business; (ii) a final price for ITC that was no better (and in fact worse) than Fortis' opening bid; (iii)

the Board accepting 50% of the consideration in Fortis stock; (iv) the Board not obtaining or even

seeking a collar on the stock portion of the consideration offered to ITC shareholders; (v) the Board

agreeing that Fortis could sell 20% of the value of ITC at the closing, further diluting the Fortis

shares that ITC stockholders will receive; and (vi) the Board obtaining for itself and ITC's executive

management special, all cash consideration for its vested and unvested stock options, restricted

stock and performance shares.

56. The process leading to the Proposed Acquisition was flawed and favored the interests

of Fortis and the Board and Company management. For example, according to the F-4, on

November 15,2015 Fortis provided ITC with an initial indication of interest to acquire the Company

for $44.25 per share in cash. On January 11, 2016, Fortis submitted a formal proposal to acquire

ITC for $44.25 per share in cash. The January 11, 2016 proposal also included executed financing

commitments. But later the same day, Fortis withdrew the all cash offer because it had received an

unfavorable report from a national debt rating agency service with respect to the proposed

transaction, and thus Fortis could not afford to pay all cash to acquire ITC. In the face of this

stunning revelation, the Board did not tell Fortis to take a hike but instead continued to negotiate

with Fortis, which now had one hand tied behind its back in terms of what it could offer to acquire

ITC. Ultimately, the Board agreed to sell ITC to Fortis for just $22.57 in cash and 0.7520 of a Fortis

share for each share of ITC common stock. The Board members did, however, make sure they and

ITC management will be paid all cash for their vested and unvested stock options, restricted stock

and performance shares.

57. On January 15, 2016, Fortis submitted a revised proposal to acquire ITC for just

$41.00 per share in a cash and stock transaction consisting of 54% cash ($22.14) and 46% stock

(valued at $18.86). During the week of January 18, 2016, the Board asked Fortis to increase both the

value of its proposal and the cash portion.

58. On February 3, Fortis submitted another revised proposal to ITC. This time Fortis

proposed to acquire the Company for $22.57 in cash (an increase of $.43) and 0.7250 of a Fortis

O) CO

o

cl 00 o

cl < CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

O

T3 <D > CD O CD q:

- 1 7 -

share for each ITC common share. The total value of this proposal was $44.86, based on the closing

price of Fortis common stock of $40.86 and an exchange ratio of 0.712504 Canadian dollars per U.S.

dollar as of February 2, 2016. While the cash portion of this proposal increased slightly, the value

attributed to the Fortis stock increased much more, making this a 50/50 cash/stock proposal,

meaning the percentage of cash in the deal actually went down from Fortis' January 15, 2016

proposal.

O) CO

O 59. The February 3, 2016 value of Fortis' proposal was only $.61 per share higher than

Fortis' original all cash proposal, and it was half stock. Given the information Fortis had revealed

about the unfavorable debt rating report it had received, it was a breach of defendants' duties not to

insist upon a collar on the stock portion (which as alleged above, would protect ITC stockholders in

the event of a decline in the market price of Fortis common stock. This breach was especially

egregious given the Board's decision to self-deal in order to receive all cash consideration for the

Board's and management's stock options, restricted stock and performance shares.

60. The F-4 reveals nothing about the Board's decision to self-deal. All it says is that on

February 8,2016, while considering Fortis' February 3,2016 cash and stock offer, the ITC board of

directors held a telephonic meeting during which ITC's counsel reviewed the interests of directors

in the possible transaction that were in addition to or different from the interests of shareholders

generally. There is nothing in the F-4 about why or when the Board decided to insist upon all cash

for the stock options, restricted stock and performance shares held by members of the Board and

Company management.

61. In light of the Board's efforts to pursue all cash consideration for the equity awards of

the Board and management, and with the absence of a collar on the stock portion, it was a breach of

the Board's duties not to insist on an all cash deal (as the Board was getting for its stock options,

restricted stock and performance shares). Failing to get either a collar on the deal or all cash, the

Board should have rejected Fortis' February 3, 2016 proposal, and continued to operate ITC as a

valuable and growing standalone business.

CL 00 o

CL < CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

O

T3 <D > CD O CD

QL

- 1 8 -

But the Board accepted Fortis' February 3, 2016 proposal, and things got worse.

First, the Board agreed that while giving ITC shareholders Fortis stock as 50% of the consideration

for their ITC shares, Fortis could further dilute the value of those shares by selling up to 20% of the

value of ITC to one or more infrastructure-focused minority investors. Second, the Board ignored

the impact on ITC shareholders receiving uncollared Fortis stock of the increased foreign exchange

risks and Fortis' increased debt load as a result of the deal. But why would the Board care - they

were receiving all cash for their stock options, restricted stock and performance shares.

The Conflicted and Unfair Process Led to an Unfair Price

62.

O) CO

o

CL 00 o cr CL 63. The Proposed Acquisition consideration drastically undervalues the Company and its

prospects. First, based on the closing price of Fortis stock the day before the Proposed Acquisition

was announced ($29.71), the Proposed Acquisition consideration was valued at just $44.91 per ITC

share. But defendants failed to obtain a collar on the Fortis stock portion of the Proposed

Acquisition consideration. A collar would protect ITC shareholders in the event - as has happened -

that the market price of Fortis common stock declines between now and the closing of the Proposed

Acquisition. On the day the deal was announced, Fortis common closed down sharply at $26.97,

reducing the value of the Proposed Acquisition consideration to $42.85. This represents a premium

of just 8.8% to ITC's closing price the day before the deal was announced, and is lower than an

analyst's high price target of $45.00 per ITC share.

64. Second, rather than demanding an all-cash offer, the Board accepted an offer that

included a substantial amount of Fortis stock (and again without a collar). Fortis, however, intends

to sell up 20% of the value of ITC to an infrastructure fund in order to finance the deal. This will

further dilute the value of the stock portion of the Proposed Acquisition consideration. Third, the

Proposed Acquisition will lift Fortis's debt burden to more than $15 billion from its current $9.1

billion.

< CD

O CNJ j*: CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

O

T3 <D > CD O CD

CE

- 1 9 -

65. Third, another potential concern for investors is that, with the majority of its earnings

coming from the United States, Fortis will face greater exchange rate risk. The Canadian dollar

has moved sharply lower against the U.S. currency since 2013.

66. Fourth, the Company continues to report positive and growing financial results. On

February 25,2016, ITC announced its financial results from operations for the fourth quarter and full

fiscal year ended December 31, 2015. For the fourth quarter, the Company reported operating

earnings of $87.6 million, compared to operating earnings of $75.9 million for the same period in

2014. For the full year 2015, the Company reported operating earnings of $323.8 million, compared

to operating earnings of $292 million for the prior year.

67. Defendant Welch commented on ITC's fourth quarter and full year results, stating:

From a financial perspective, we had another strong year with 2015 operating earnings of $2.08 per diluted share, which was well within our guidance range and marks the ninth consecutive year of double-digit annual operating earnings growth. To that end, we continue to see double-digit earnings growth in the years to come as evidenced by our revised capital investment forecast through 2018 at our regulated operating companies .... On the value return front, we continue to honor our commitments to shareholders by increasing the dividend by approximately 15% in August of 2015 and concluding our $115 million accelerated share repurchase program in November. Effectively using the remaining capacity of Board authorized share repurchases. Together, these efforts highlight the operational and financial strength of the business, which we believe will continue to yield long-term benefits for our customers and investors.

O) CO

O

CL 00 o

CL < CD

O CNJ j*:

CD

O

c 3 o O •O c ro

ro 68. So if the Proposed Acquisition closes, ITC stockholders will be stripped of their

equity for an unfair price that includes uncollared, diluted and debt burdened Fortis shares. But the

Board and the members of management treated themselves differently and better than ITC s public

shareholders are being treated. For each of ITC's 2,257,058 vested or unvested stock options,

performance shares and restricted shares that they own, the members of ITC's Board and executive

management will receive $42.54 per share in cash, or as noted above, over $67.7 million in cash.

Unlike ITC's other shareholders, who will only receive $22.57 in cash and 0.7520 of a Fortis share

for each share of ITC common stock owned, the Board and management will not be harmed by the

lack of a collar, the dilution from Fortis' plan to sell 20% of ITC's equity, or Fortis' dramatically

increased debt burden following the Merger.

o CT> c

LL

O

T3 <D > CD O CD 01

- 2 0 -

69. Motivated by the prospect of receiving over $133 million in cash from a deal with

Fortis, defendants agreed to the Proposed Acquisition in breach of their fiduciary duties to ITC's

public shareholders, which they brought about through an unfair sales process. Rather than

undertake a full and fair sales process designed to maximize shareholder value as their fiduciary

duties require, the Board catered to their own liquidity goals, as well as to Fortis.

70. To protect against the threat of alternate bidders out-bidding Fortis after the

announcement, plaintiff alleges on information and belief that defendants implemented preclusive

deal protection devices to guarantee that Fortis will not lose its preferred position, and which

effectively preclude any competing bids for ITC. Those deal protection devices will preclude a fair

sales process for the Company and lock out competing bidders, and include:

(a) a "no-solicitation" or "no-shop" provision that precludes ITC from providing

confidential Company information to, or even communicating with, potential competing bidders for

the Company except under very limited circumstances;

(b) an illusory "fiduciary out" for the no-shop provision that requires the

Company to provide Fortis with advance notice before providing any competing bidder with any

confidential Company information, even after the Board has determined that the competing bid is

reasonably likely to lead to a superior proposal and that the Board is breaching its fiduciary duties by

not providing the competing bidder with confidential Company information;

(c) an "information rights" provision that requires the Company to provide Fortis

with confidential, non-public information about competing proposals which Fortis can then use to

formulate a matching bid;

O) CO

O

CL 00 o

CL < CD

O CNJ j*:

CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

O

T3 <D >

(d) a "matching rights" provision that requires ITC to provide Fortis with the

opportunity to match any competing proposal; and

(e) a termination and expense fee provision that requires the Company to pay

Fortis $245 million if the Proposed Acquisition is terminated in favor of a superior proposal.

71. Thus, the Board compounded its breaches by, inter alia, agreeing to these

unreasonable deal protection devices that preclude other bidders from making a successful

CD O CD

QL

- 2 1 -

competing offer for the Company. The support agreements and the deal protection devices prelude a

fair sales process for ITC s shareholders and make the Proposed Acquisition a virtual fait accompli.

The False and Misleading F-4

72. To make matters worse, defendants have withheld material information about the

Merger from ITC s public shareholders. This information is necessary for shareholders to make an

informed decision about whether to vote in favor of the Merger. The F-4 contains numerous

material misstatements and otherwise fails to disclose material information about the flawed sales

O) CO

O

CL process, including: 00

o (a) the specific strategic alternatives reviewed by Morgan Stanley between July

CL < 27, 2015 and August 4, 2015; CD

(b) the resulting valuations of ITC under each strategic alternative as reviewed by O CNJ j*: Morgan Stanley; and CD

(c) the specific strategic alternatives reviewed by Barclays with defendant Welch o on September 23, 2015. c

o 73. As defendants are seeking shareholder approval of the Merger, defendants have a

duty to disclose fully and fairly all material details of the sales process, including those set forth in

the previous paragraph. Shareholders are entitled to know, before deciding whether to vote for or

against the Proposed Acquisition, the details that led to the Board's decision to sell the Company for

an unfair price.

o •o c ro

ro O

CT>

C

LL 74. The F-4 also made numerous material misstatements and otherwise failed to disclose O

T3 material information about conflicts of interests that burdened the Board, Company management and

their advisors, including:

<D > CD O CD (a) the errors in the chart in the F-4 at page 280, including the total number of

shares owned, the percentage of all shares owned and the number of officers and directors in the

chart;

QL

(b) any discussions that any members of the Board or Company management had,

when, and with whom, about the consideration that the members of Board and Company

- 2 2 -

management would receive for their vested and unvested options, restricted stock and performance

shares;

(c) the reasons the Board decided to allow the members of Board and Company

management to receive different and more valuable consideration for their vested and unvested

options, restricted stock and performance shares than the ITC's public shareholders will receive for

their shares;

O) CO

o (d) the bases for the Board's conclusion that neither Barclays nor Morgan Stanley

CL was independent; 00

o cr (e) the bases for the Board's decision to engage Barclays, given that the Board

concluded it was not independent;

(f) the bases for the Board's decision to engage Morgan Stanley, given that the

Board concluded it was not independent;

(g) the bases for the Board's conclusion that Lazard was independent;

(h) the reasons the Board retained both Barclays and Morgan Stanley; and

(i) the specific amounts Barclays is to be paid at each of the milestones listed in

CL < CD

O CNJ j*:

CD

O

c 3 o O •O the F-4 at page 92. c TO

75. In order for there to be an informed shareholder vote on the Merger, defendants are

required to disclose even potential conflicts of interest. Here the conflicts were more than potential,

as ITC's Board, financial advisors, and management were all conflicted. Shareholders are entitled to

know if their fiduciaries have interests in the transaction that are even potentially in conflict with the

shareholders' interest in maximized value. This information is material because shareholders must

ro O

CT>

C

LL

O

T3 <D >

be told of all potential and actual conflicts of interests that bear on a director's ability to objectively

assess merger transactions.

CD O CD

CE 76. Defendants also made material misstatements and otherwise failed to disclose

material information in the F-4 about the Company's intrinsic value and prospects going forward,

including the financial projections provided by ITC management and Fortis' standalone financial

- 2 3 -

projections, and relied upon by Barclays, Morgan Stanley and Lazard for purposes of their analysis,

including:

(a) the ITC Holdings Corp. standalone financial projections (for the whole

company, and for projects in Puerto Rico and Mexico separately) provided by ITC management and

relied upon by Lazard, Barclays, and Morgan Stanley for purposes of their analyses, for years 2016 -

2020, for the following items:

O) CO

o (i) EBIT (or D&A);

CL (ii) Taxes (or tax rate); 00

o cr (iii) Changes in net working capital;

Stock-based compensation expense;

Unlevered free cash flow;

CL < (iv) CD

(v) O CNJ j*: (vi) Dividends; and CD

(vii)

in $US or $C currency;

whether the financial forecasts for ITC presented in the F-4 are stated o c o (b) the Fortis standalone financial projections relied upon by Lazard, Barclays,

and Morgan Stanley for purposes of their analyses, for years 2016-2020, for the following items:

(i) Revenue;

o •o c ro

ro O (ii) EBIT (or D&A);

CT> c (iii) Taxes (or tax rate);

LL (iv) Capital expenditures;

Changes in net working capital;

Stock-based compensation expense;

Any other adjustments to unlevered free cash flow;

Unlevered free cash flow; and

O

T3 (v) <D > (vi) CD

O CD (vii) CE

(viii)

(ix) whether the financial forecasts for Fortis presented in the F-4 are stated

in $US or $C currency.

- 2 4 -

77. In order to determine whether to vote for or against a transaction like the one at the

heart of this case, it is critical that shareholders receive the material information underlying or

supporting the Company's inherent value. Without this information, shareholders cannot evaluate

whether to vote in favor of or against the Merger.

78. In the F-4 defendants also made several material misleading statements or otherwise

failed to disclose material information about critical data and inputs underlying the financial analyses

supporting the fairness opinions of the Board's three financial advisors Barclays, Morgan Stanley

and Lazard, including:

O) CO

O

CL 00 o cr (a) with respect to Lazard's Selected Comparable Company Multiples Analysis: CL < (i) the 2016 P/E, 2017 P/E, 2018 P/E, and Enterprise Value / 2017E CD

EBITDA multiples for each of the selected companies observed by Lazard in its analysis;

(ii) the average depreciable life of asset base for each of the selected

companies observed by Lazard in its analysis;

(iii) whether Lazard performed any type of benchmarking analysis for ITC

or Eortis in relation the selected companies; and

O CNJ j*:

CD

O

c 3 o O •O the direction and magnitude of the adjustment Lazard made to

"equalize the depreciable life of ITC s asset base" to the comparable companies;

(b) with respect to Lazard's Discounted Cash Flow Analysis:

the implied perpetuity growth rates for each of ITC and Eortis as

(iv) c ro

ro O

CT>

C (i)

LL calculated by Lazard in its analysis; and O

T3 (ii) whether Lazard treated stock-based compensation as a cash or non-<D > cash expense; CD

O CD (c) with respect to Lazard's Selected Precedent transactions Multiples Analysis:

the EY+l P/E and FY+2 P/E multiples for each of the selected

01

(i)

transactions observed by Lazard in its analysis; and

- 2 5 -

whether Lazard made a similar equalization adjustment to the

depreciable life of ITC's asset base as it did in the Selected Comparable Company Multiples

Analysis above;

(ii)

(d) with respect to Lazard's Infrastructure Returns Analysis, the illustrative

required range of equity returns expected by long-term infrastructure investors for assets similar to

ITC's assets;

O) CO

O (e) with respect to Lazard's Discounted Cash Flow Sensitivity Analysis:

(i) the basis for Lazard separating out the unlevered free cash flows

associated with ITC s projects in Puerto Rico and Mexico into a separate analysis and not including

them as part of its primary Discounted Cash Flow Analysis; and

(ii) the specific risks, if any, that Lazard associated with ITC's projects in

Puerto Rico and Mexico that required the unlevered free cash flows to be measured at 10%, 25% and

CL 00 o

CL < CD

O CNJ j*:

CD

100%; O (f) with respect to Barclays' ITC Selected Comparable Company Analysis: c

o (i) the LTM P/E, 2016E P/E and Market Price to book value multiples for o •o each of the selected companies observed by Barclays in its analysis; and

(ii) whether Barclays performed any type of benchmarking analysis for

c TO

ro O ITC in relation the selected companies;

(g) with respect to Barclays' ITC Selected Precedent Transaction Analysis, the

EYl P/E, EW Rate Base, and P/B multiples for each of the selected transactions observed by

Barclays in its analysis;

CT>

C

LL

O

T3 <D >

(h) with respect to Barclays' ITC Discounted Cash Flow Analysis:

(i) the implied perpetuity growth rates as calculated by Barclays in its

CD O CD

QL

analysis; and

(ii) whether Barclays treated stock-based compensation as a cash or non

cash expense;

(i) with respect to Barclays' Fortis Selected Comparable Company Analysis:

- 2 6 -

(i) the LTM P/E, 2016E P/E and Market Price to book value multiples for

each of the selected companies observed by Barclays in its analysis; and

(ii) whether Barclays performed any type of benchmarking analysis for

Fortis in relation the selected companies;

(j) with respect to Barclays' Fortis Discounted Cash Flow Analysis:

(i) the implied perpetuity growth rates as calculated by Barclays in its

O) CO

o analysis; and

CL (ii) whether Barclays treated stock-based compensation as a cash or non-00

o cash expense;

CL < (k) with respect to Morgan Stanley's ITC Comparable Public Companies CD

Analysis: O CNJ j*: (i) the stock price to 2016 estimated unadjusted EPS, stock price to 2016

estimated adjusted EPS, and stock price to 2016 estimated EPS multiples for each of the selected

companies observed by Morgan Stanley in its analysis;

CD

O

c 3 o (ii) whether Morgan Stanley performed any type of benchmarking analysis o •o for ITC in relation the selected companies; and

(iii) the specific adjustments made to 2016 estimated EPS according to

c TO

ro O guidance from ITC's management;

(1) with respect to Morgan Stanley's ITC Discounted Cash Flow Analysis:

(i) the implied perpetuity growth rates as calculated by Morgan Stanley

CT>

C

LL

O

T3 in its analysis; and <D > (ii) whether Morgan Stanley treated stock-based compensation as a cash or CD

O CD non-cash expense; QL

(m) with respect to Morgan Stanley's ITC Analysis of Selected Precedent

Transactions and Premiums Paid, the price to 2016E earnings multiples for each of the selected

transactions observed by Morgan Stanley in its analysis;

- 2 7 -

(n) with respect to Morgan Stanley's Fortis Comparable Public Companies

Analysis, whether Morgan Stanley performed any type of benchmarking analysis for Fortis in

relation to the selected companies; and

(o) with respect to Morgan Stanley's Fortis Discounted Cash Flow Analysis:

(i) the implied perpetuity growth rates as calculated by Morgan Stanley in O) CO

its analysis; and O

(ii) whether Morgan Stanley treated stock-based compensation as a cash or CL

non-cash expense. 00 o

There is no more material information to shareholders in a merger than the

information underlying or supporting the purported "fair value" of their shares. Shareholders are

entitled to the information necessary to inform a decision as to the adequacy of the merger

consideration, which includes the underlying data (including management's projections) the

investment bankers relied upon, the key assumptions that the financial advisors used in performing

valuation analyses, and the range of values that resulted from those analyses. Here the analyses of

ITC's three financial advisors incorporated certain critical assumptions that significantly affect the

output (valuation) of the analyses. Without this material information, shareholders have no basis on

which to judge the adequacy of Fortis' offer.

Without full and fair disclosure of the material information set forth above,

79. CL < CD

O CNJ j*:

CD

O

c 3 o O •O c ro

ro O 80.

CT>

C shareholders should not be asked to vote on the Merger.

81. Because defendants dominate and control the business and corporate affairs of ITC

and are in possession of private corporate information concerning ITC's assets, business and future

prospects, there exists an imbalance and disparity of knowledge and economic power between them

and the public shareholders of ITC, which makes it inherently unfair for them to pursue any

proposed transaction wherein they will reap disproportionate benefits to the exclusion of maximizing

stockholder value.

LL

O

T3 <D > CD O CD

QL

- 2 8 -

82. In pursuing the unlawful plan to sell ITC, each of the defendants violated applicable

law by directly breaching and/or aiding and abetting the other defendants' breaches of their fiduciary

duties of loyalty, due care, candor, independence, good faith and fair dealing.

83. Instead of attempting to obtain the highest price reasonably available for ITC for its

shareholders, defendants tailored the terms of the Proposed Acquisition to meet the specific needs of

Company insiders and Fortis. In essence, the Proposed Acquisition is the product of a hopelessly

flawed process that was designed to ensure the sale of ITC to Fortis and Fortis only, on terms

preferential to Fortis and to aggrandize the financial interests of Company insiders at the expense of

plaintiff and ITC's public stockholders.

84. Plaintiff seeks to enjoin the Proposed Acquisition.

O) CO

O

CL 00 o cr CL < CD

CLASS ACTION ALLEGATIONS O CNJ j*: 85. Plaintiff brings this action individually and as a class action on behalf of all holders of

ITC stock who are being and will be harmed by defendants' actions described below (the "Class").

Excluded from the Class are defendants herein and any person, firm, trust, corporation, or other

entity related to or affiliated with any defendant.

86. This action is properly maintainable as a class action and is not removable.

87. The Class is so numerous that joinder of all members is impracticable. According to

ITC's SEC filings, as of October 30,2015 there are more than 153.4 million shares of ITC common

stock outstanding, held by hundreds if not thousands of shareholders geographically dispersed across

the country.

CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

O

T3 There are questions of law and fact that are common to the Class and that

predominate over questions affecting any individual Class member. The common questions include,

inter alia, the following:

88. <D > CD O CD

QL

(a) whether the Individual Defendants have breached their fiduciary duties of

undivided loyalty, independence, or due care with respect to plaintiff and the other members of the

Class in connection with the Proposed Acquisition;

- 2 9 -

(b) whether defendants are engaging in self-dealing in connection with the

Proposed Acquisition;

(c) whether defendants are unjustly enriching themselves and other insiders or

affiliates of ITC;

(d) whether the Individual Defendants have breached any of their other fiduciary

duties to plaintiff and the other members of the Class in connection with the Proposed Acquisition,

including the duties of good faith, diligence, honesty and fair dealing;

(e) whether the defendants, in bad faith and for improper motives, have impeded

or erected barriers to discourage other offers for the Company or its assets;

(f) whether the defendants failed to disclose material information to shareholders

O) CO

O

cl 00 o cr cl < CD

in connection with the potential transaction, or aided and abetted therein; and

(g) whether plaintiff and the other members of the Class will suffer irreparable

injury unless defendants' conduct is enjoined.

89. Plaintiff's claims are typical of the claims of the other members of the Class and

plaintiff does not have any interests adverse to the Class.

90. Plaintiff is an adequate representative of the Class, has retained competent counsel

experienced in litigation of this nature, and will fairly and adequately protect the interests of the

Class.

O CNJ j*:

CD

O

c 3 o O •O c ro

ro O

CT>

C 91. The prosecution of separate actions by individual members of the Class would create

a risk of inconsistent or varying adjudications with respect to individual members of the Class,

which would establish incompatible standards of conduct for the parties opposing the Class.

92. Plaintiff anticipates that there will be no difficulty in the management of this

litigation. A class action is superior to other available methods for the fair and efficient adjudication

of this controversy.

93. Defendants have acted on grounds generally applicable to the Class with respect to

the matters complained of herein, thereby making appropriate the relief sought herein with respect to

the Class as a whole.

LL

O

T3 <D > CD O CD

CE

- 3 0 -

DEFENDANTS' FIDUCIARY DUTIES AND THE "ENTIRE FAIRNESS" STANDARD

94. Under applicable law, in any situation where the directors of a publicly traded

corporation undertake a transaction that will result in either (i) a change in corporate control, or (ii) a

break-up of the corporation's assets, the directors have an affirmative fiduciary obligation to obtain

the highest value reasonably available for the corporation's shareholders, and if such transaction will

result in a change of corporate control, the shareholders are entitled to receive a significant premium.

To diligently comply with these duties, the directors may not take any action that: (a) adversely

affects the value provided to the corporation's shareholders; (b) will discourage or inhibit alternative

offers to purchase control of the corporation or its assets; (c) contractually prohibits them from

complying with their fiduciary duties; (d) will otherwise adversely affect their duty to search and

secure the best value reasonably available under the circumstances for the corporation's

shareholders; and/or (e) will provide the directors with preferential treatment at the expense of, or

separate from, the public shareholders.

95. In accordance with their duties of loyalty and good faith, the Individual Defendants,

as directors and/or officers of ITC, are obligated to refrain from: (a) participating in any transaction

where the directors' or officers' loyalties are divided; (b) participating in any transaction where the

directors or officers receive or are entitled to receive a personal financial benefit not equally shared

by the public shareholders of the corporation; and/or (c) unjustly enriching themselves at the expense

or to the detriment of the public shareholders.

96. The concept of fair dealing embraces questions of when the transaction was timed,

how it was initiated, structured, negotiated, disclosed to the directors, and how the approvals of the

directors and the stockholders were obtained. The concept of fair price relates to the economic and

financial considerations of the proposed merger, including all relevant factors: assets, market value,

earnings, future prospects, and any other elements that affect the intrinsic or inherent value of a

company's stock.

O) CO

o

cl 00 o cr cl < CD

O CNJ j*:

CD

O

c 3 o O •O c ro

ro O

CT>

C

LL

O

T3 <D > CD O CD

CE

- 3 1 -

97. The test for fairness is not a bifurcated one as between fair dealing and price. All

aspects of the issue must be examined as a whole since the question is one of entire fairness.

98. To demonstrate entire fairness, the defendants must present evidence of the

cumulative manner by which they discharged all of their fiduciary duties. An entire fairness analysis

then requires the Court to consider carefully how the Board discharged all of its fiduciary duties with

regard to each aspect of the non-bifurcated components of entire fairness: fair dealing and fair price.

Because the Company's officers and directors hold significantly divergent interests from the

minority shareholders, the burden to prove the entire fairness of the Proposed Acquisition will

remain with defendants.

O) CO

O

cl 00 o cr cl < CONSPIRACY, AIDING AND ABETTING,

AND CONCERTED ACTION CD

O CNJ 99. In committing the wrongful acts alleged herein, defendants have pursued, or joined in