Embed Size (px)

Citation preview

State Benefits

Too important to leave to chance!

Things to consider – the context

• Impact on your budgeting– when will my wife’s / partner’s pension become payable?– what will be payable as a non means tested benefit?

• Basic State Pension• Additional Pension (SERPS / S2P)• Graduated Pension if you were in that scheme before 6 April 1975

– from November 2018 State Pension Age will be 65 for all– the changes to future State Pension Age

• 66 by April 2020 phased in from 2018• then planned increases to 67 and 68 might be brought forward• cannot rule out further changes

– if planning ahead what impact if any will my savings / pension have on means tested Pension Credit at 60 and 65?

Proposed changes for women

Proposed changes for women

The proposed changes to the State Pension age timetable, announced in November 2010, affect those born between 6 April 1953 and 5 April 1960. These proposed changes to the timetable are not yet law and still require the approval of Parliament.

Date of birth Date State Pension Age reached

6 April 1953 to 5 May 1953 6 July 2016

6 May 1953 to 5 June 1953 6 November 2016

6 June 1953 to 5 July 1953 6 March 2017

6 July 1953 to 5 August 1953 6 July 2017

6 August 1953 to 5 September 1953 6 November 2017

6 September 1953 to 5 October 1953 6 March 2018

6 October 1953 to 5 November 1953 6 July 2018

6 November 1953 to 5 December 1953 6 November 2018

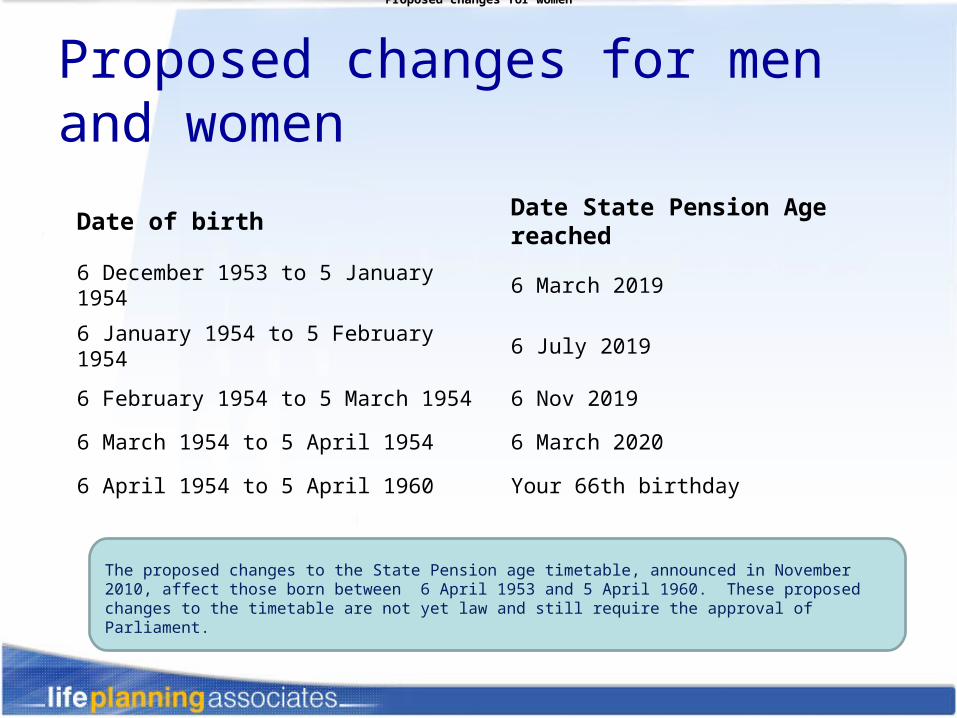

Proposed changes for men and women

Proposed changes for women

Date of birth Date State Pension Age reached

6 December 1953 to 5 January 1954 6 March 2019

6 January 1954 to 5 February 1954 6 July 2019

6 February 1954 to 5 March 1954 6 Nov 2019

6 March 1954 to 5 April 1954 6 March 2020

6 April 1954 to 5 April 1960 Your 66th birthday

The proposed changes to the State Pension age timetable, announced in November 2010, affect those born between 6 April 1953 and 5 April 1960. These proposed changes to the timetable are not yet law and still require the approval of Parliament.

Things to consider – the context

• Impact on your budgeting– how much will be paid and when will it increase?– level of inflation protection (current and from a future date)– impact on my occupational pension benefits if they are subject to

some adjustment for State benefits (State levelling or ‘claw back’)– can build up more State pension after you leave (S2P) until State

Pension date?• Earning above the Lower Earnings Limit• Carer credits• Enhanced benefits for lower earners

– if continue working, set up a business or become self-employed would it pay to defer State Retirement Pensions?

Contributory and Non-contributory benefits

Contributory benefits

• State Basic Retirement Pension

• Additional State Retirement Pension (SERPS, S2P, Graduated Pension)

• Job Seeker’s Allowance

• Employment & Support Allowance

• Maternity Allowance

• Bereavement benefits

Non- contributory benefits• Child Benefit and Guardian’s Allowance• Job Seeker’s Allowance ‘income based’• Industrial Injuries Benefit• Employment & Support Allowance ‘income based’• Working Tax Credit & Child Tax Credit• Disability Living Allowance & Severe Disablement

Allowance• Pension Credit• Attendance Allowance

Out of workJob Seeker’s Allowance

Job Seeker’s allowance (JSA)• Replaced unemployment benefit and income

support for the unemployed• Two types

– Contribution based– Income based

• Payment authorised and paid by Jobcentre Plus• Jobseeker’s agreement• Fortnightly visits to Jobcentre Plus – activity

review• Jobcentre Plus has power to stop JSA

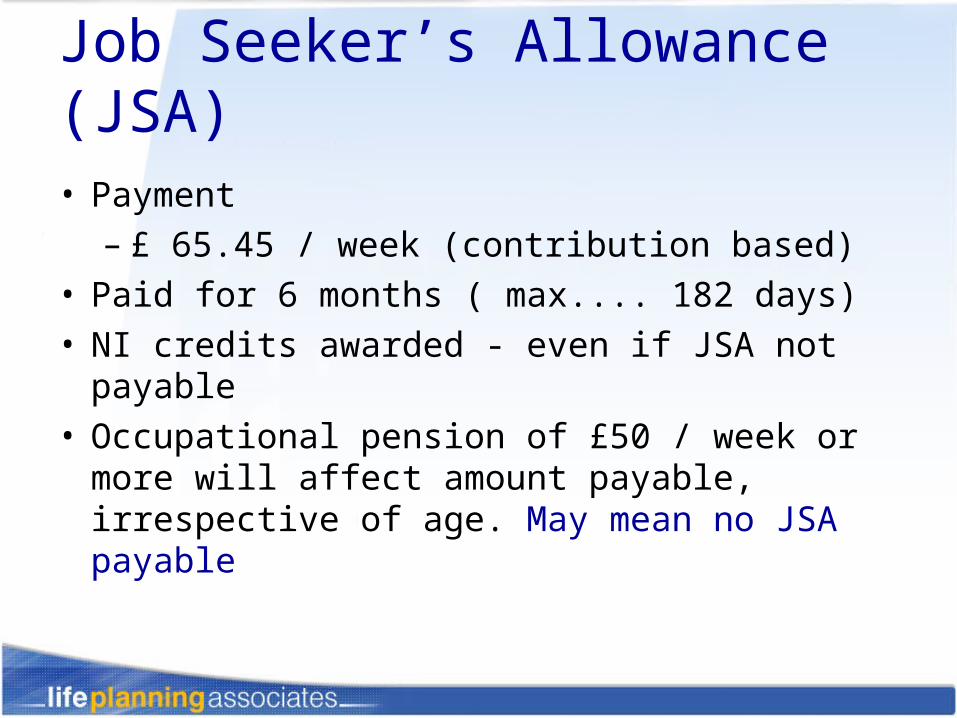

Job Seeker’s Allowance (JSA)• Payment

– £ 65.45 / week (contribution based)• Paid for 6 months ( max.... 182 days)• NI credits awarded - even if JSA not payable• Occupational pension of £50 / week or more will

affect amount payable, irrespective of age. May mean no JSA payable

Too ill to work?Employment & Support Allowance

Employment & Support Allowance

• Introduced on 27th October 2008• Replaced Incapacity Benefit for new claimants with a

focus on a can do attitude not what someone cannot do • Expected to be a temporary benefit for the vast majority

of individuals• Anyone already receiving Incapacity Benefit will be

transferred to ESA between 2009 and 2013 after a medical assessment (Work Capability Assessment)

• October 2010 Public Spending Review included announcement that the Work Related Group element of the benefit will not be paid for more than 1 year

Employment & Support Allowance

• Two phases:-– Assessment Phase of 13 weeks while decision made on

capacity for work– Main Phase from 14 weeks when an individual will be placed

into one of two categories• Work Related Group• Support Group

– Some individuals will no longer be able to claim E&SA after that assessment and will transfer to the Job Seeker’s Allowance, Income Support or Pension Credit regime

• Two types of E&SA– Contribution based Single person benefit (amount)

– Income related Rates for couples

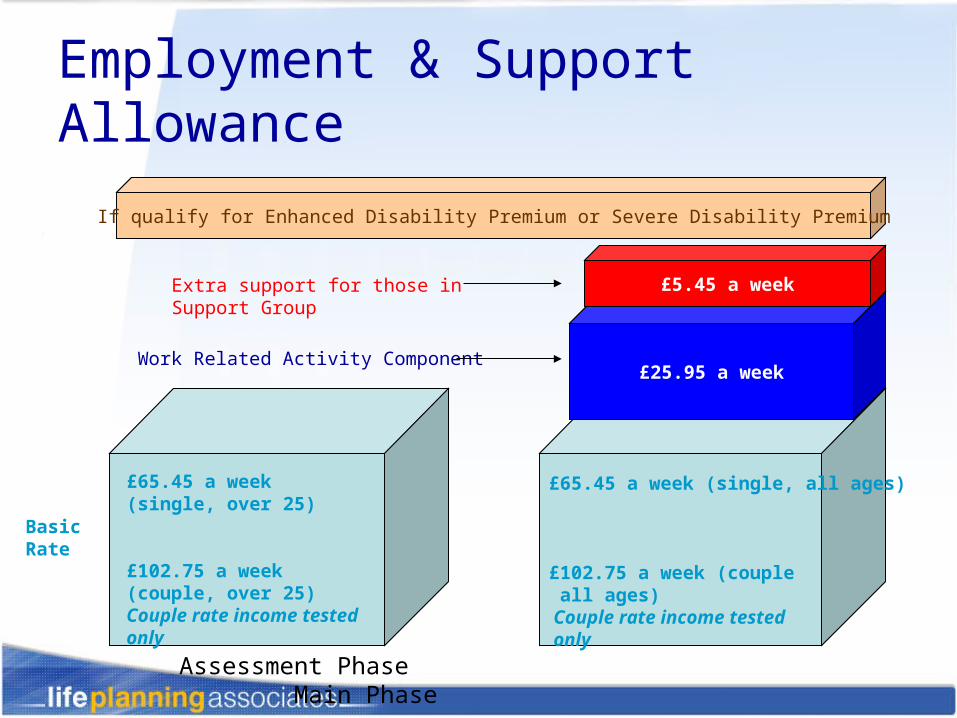

Employment & Support Allowance

£65.45 a week (single, all ages)

£102.75 a week (couple all ages) Couple rate income tested only

£25.95 a week

£5.45 a week

If qualify for Enhanced Disability Premium or Severe Disability Premium

Assessment Phase Main Phase

£65.45 a week (single, over 25)

£102.75 a week (couple, over 25)Couple rate income tested only

Work Related Activity Component

Extra support for those in Support Group

BasicRate

Employment & Support Allowance

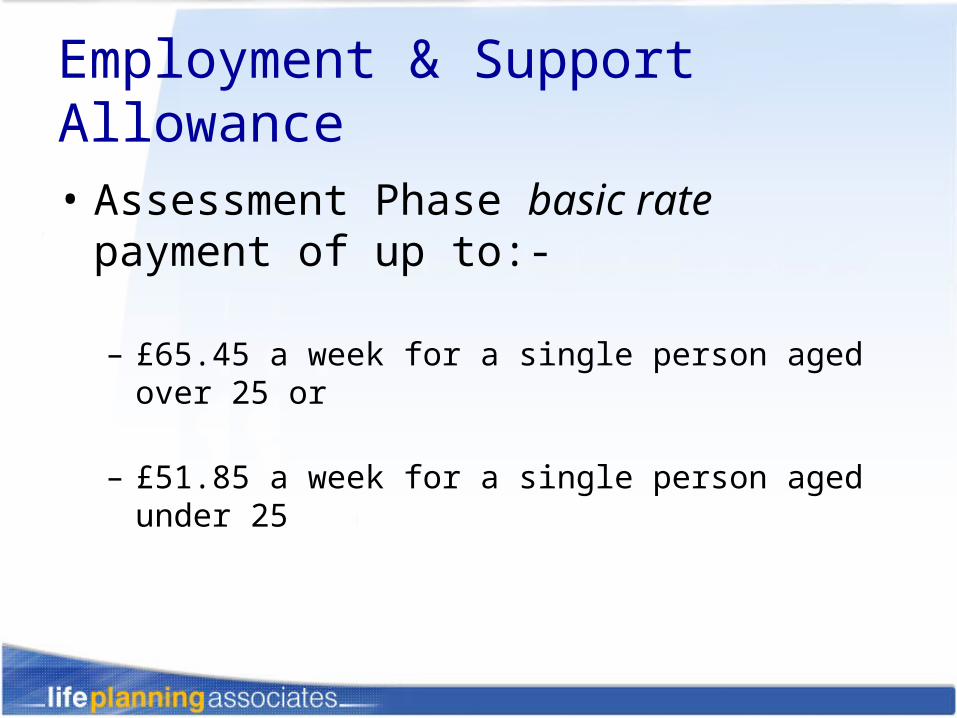

• Assessment Phase basic rate payment of up to:-

– £65.45 a week for a single person aged over 25 or

– £51.85 a week for a single person aged under 25

Employment & Support Allowance

• Main Phase categories• Work Related Activity Group – where an

individual will be expected to engage in a personalised programme of back-to-work support – the stick element in the ‘carrot and stick approach’

• Support Group – able to voluntarily participate on the programme and will receive a guarantee of a higher basic rate than anyone currently on Incapacity Benefit – the carrot element in the ‘carrot and stick approach’

Employment & Support Allowance

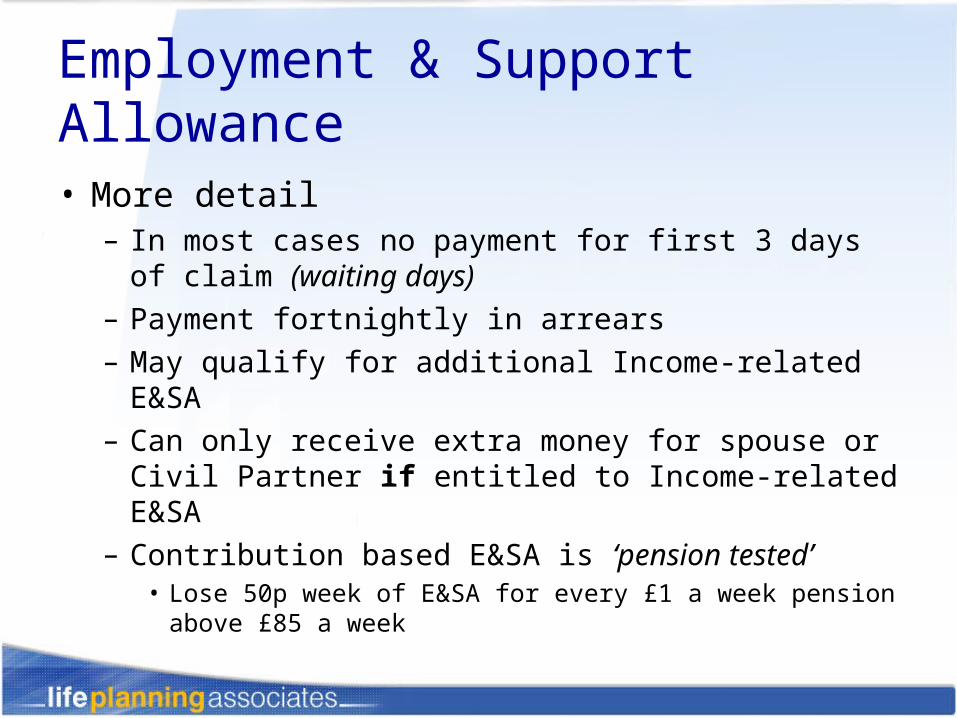

• More detail– In most cases no payment for first 3 days of claim

(waiting days)– Payment fortnightly in arrears– May qualify for additional Income-related E&SA– Can only receive extra money for spouse or Civil

Partner if entitled to Income-related E&SA– Contribution based E&SA is ‘pension tested’

• Lose 50p week of E&SA for every £1 a week pension above £85 a week

Employment & Support Allowance

• More detail– Premium Benefits payable in addition

• Enhanced disability• Severe disability• Pensioner

– Income Tax not deducted from Income-related E&SA– Income Tax may be taken from Contribution based

E&SA from week 14

Employment & Support Allowance

• Permitted work rules, you can work– For less than 16 hours a week on average with

earnings up to £93 a week for 52 weeks– For less than 16 hours a week on average with

earnings up to £93 a week if you are in the Support Group of the Main Phase of E&SA

– And earn up to £20 a week at any time for as long as you are receiving E&SA

– In ‘Supported Permitted Work’ and earn up to £93 a week as long as receiving E&SA provided you continue to satisfy the Supported Work criteria

Income that can be taken from State Pension AgeThe various types of State Retirement Income

Possible sources of State retirement income

• Basic State pension• Graduated pension• State Second Pension (previously SERPS)

• Pension Credit means tested

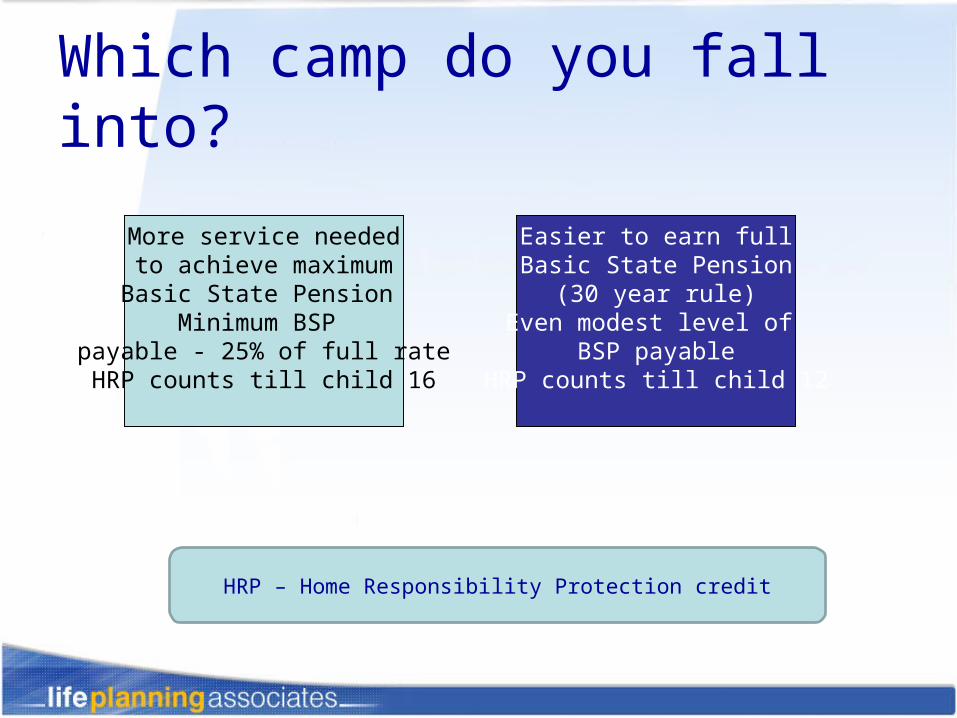

Which camp do you fall into?

Reached State Pension Age

before6 April 2010?

Reach State Pension Age on or after

6 April 2010?

Which camp do you fall into?

More service neededto achieve maximumBasic State Pension

Minimum BSP payable - 25% of full rateHRP counts till child 16

Easier to earn fullBasic State Pension

(30 year rule)Even modest level of

BSP payableHRP counts till child 12

HRP – Home Responsibility Protection credit

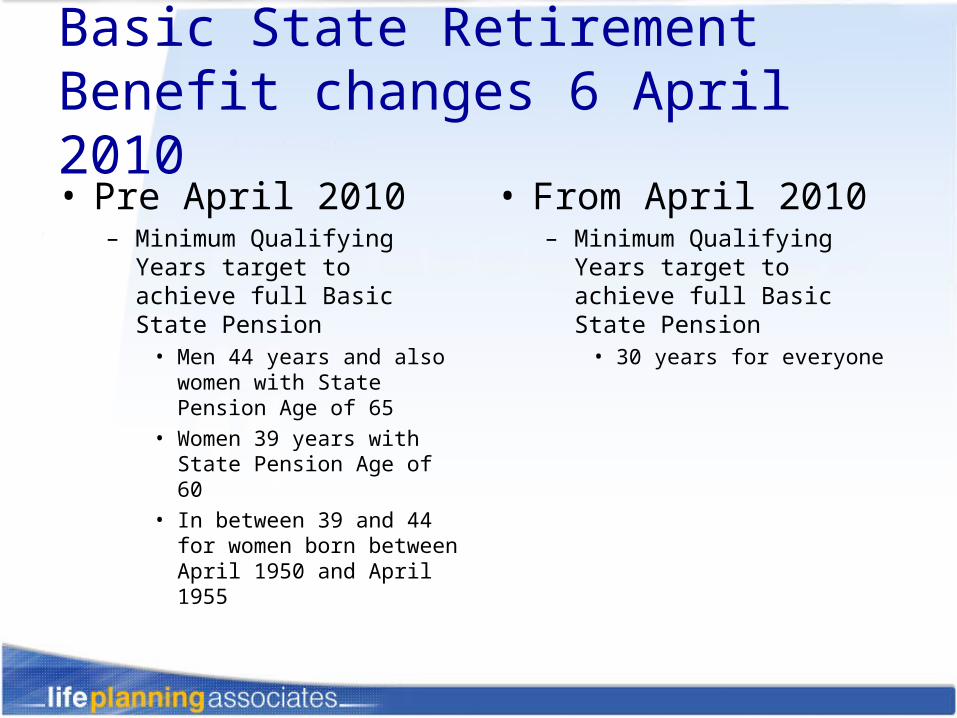

Basic State Retirement Benefit changes 6 April 2010• Pre April 2010

– Minimum Qualifying Years target to achieve full Basic State Pension

• Men 44 years and also women with State Pension Age of 65

• Women 39 years with State Pension Age of 60

• In between 39 and 44 for women born between April 1950 and April 1955

• From April 2010– Minimum Qualifying Years

target to achieve full Basic State Pension

• 30 years for everyone

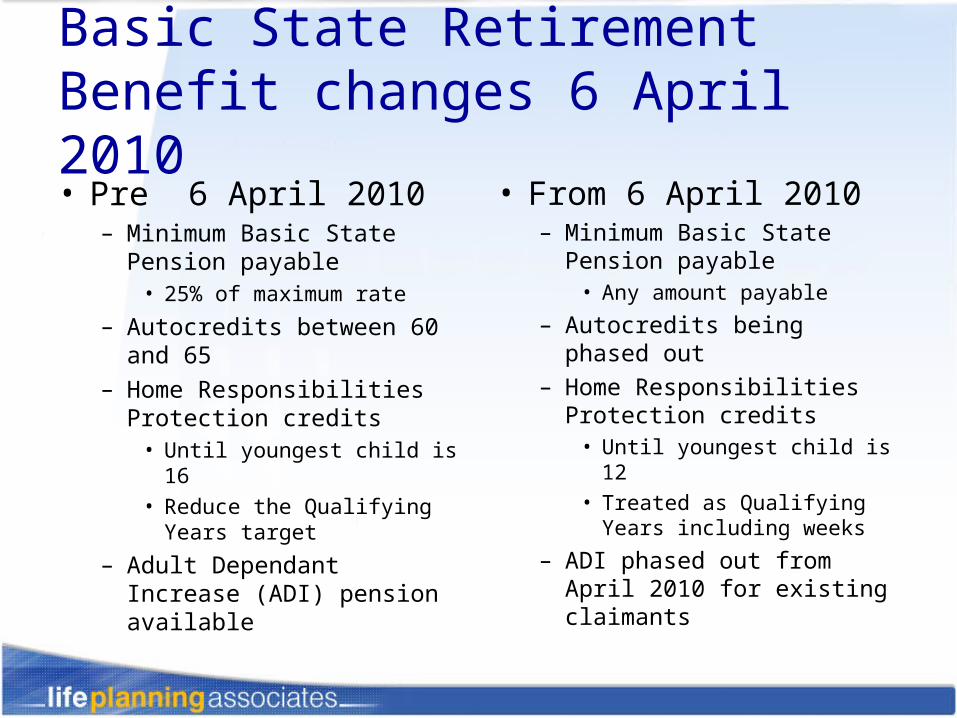

Basic State Retirement Benefit changes 6 April 2010• Pre 6 April 2010

– Minimum Basic State Pension payable

• 25% of maximum rate

– Autocredits between 60 and 65

– Home Responsibilities Protection credits

• Until youngest child is 16

• Reduce the Qualifying Years target

– Adult Dependant Increase (ADI) pension available

• From 6 April 2010– Minimum Basic State

Pension payable• Any amount payable

– Autocredits being phased out

– Home Responsibilities Protection credits

• Until youngest child is 12

• Treated as Qualifying Years including weeks

– ADI phased out from April 2010 for existing claimants

Basic State Retirement Benefit changes after 6 April 2010• Pre 6 April 2010

– Winter Fuel Allowance• Payable Winter after

reaching age 60 provided qualified in previous September

• Pension Increases until change in April 2011– Based on RPI

Annual change as reflected in September RPI index

• From 6 April 2010– Winter Fuel Allowance

• Will rise incrementally to 65 between 2010 and 2020

• Pension increases from April 2011– From 2011 restored link to

National Average Earnings for all in receipt of State Basic Pension as part of a triple lock mechanism for increases

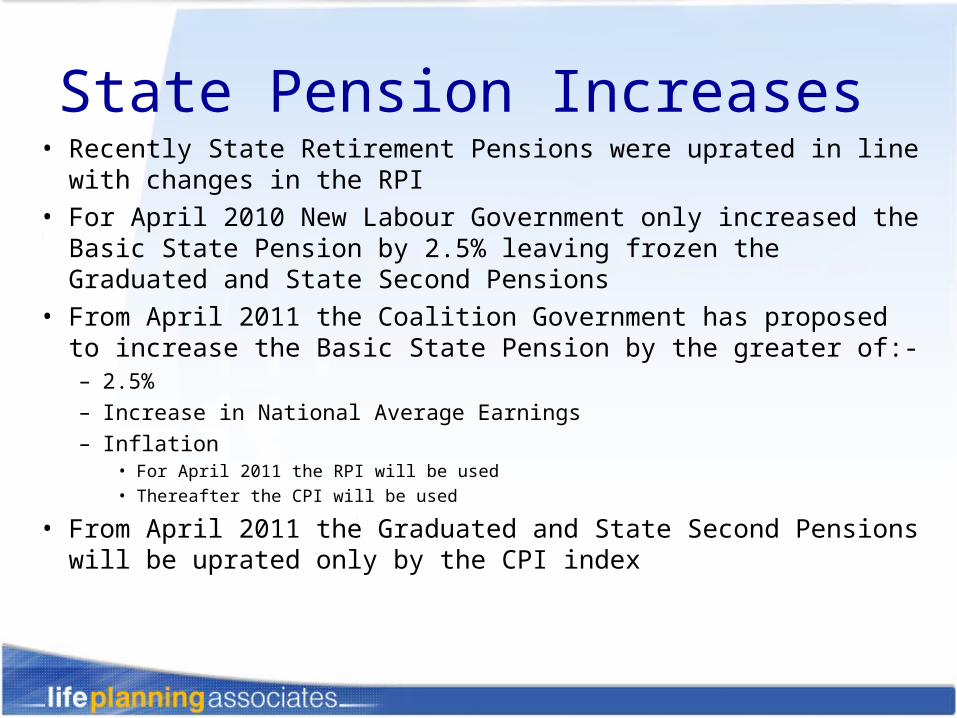

State Pension Increases• Recently State Retirement Pensions were uprated in line with

changes in the RPI

• For April 2010 New Labour Government only increased the Basic State Pension by 2.5% leaving frozen the Graduated and State Second Pensions

• From April 2011 the Coalition Government has proposed to increase the Basic State Pension by the greater of:-– 2.5%– Increase in National Average Earnings– Inflation

• For April 2011 the RPI will be used• Thereafter the CPI will be used

• From April 2011 the Graduated and State Second Pensions will be uprated only by the CPI index

Possible sources of State retirement income

• Basic State pension• Graduated pension• State Second Pension (previously SERPS)

• Pension Credit means tested

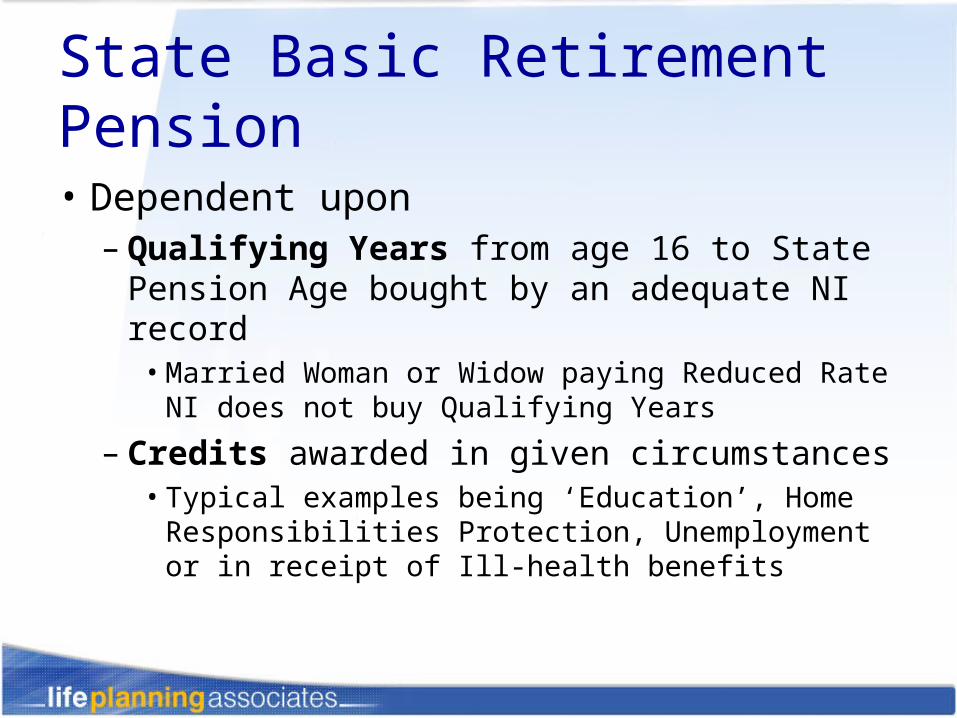

State Basic Retirement Pension

• Dependent upon– Qualifying Years from age 16 to State

Pension Age bought by an adequate NI record• Married Woman or Widow paying Reduced Rate

NI does not buy Qualifying Years

– Credits awarded in given circumstances• Typical examples being ‘Education’, Home

Responsibilities Protection, Unemployment or in receipt of Ill-health benefits

NI Credits

• Education credits for tax years when 16 / 17 / 18• If on an approved training course• While in receipt of certain benefits

– Carer’s Allowance– Job Seeker’s Allowance – Incapacity Benefit– Statutory Adoption Pay, Statutory

Maternity Pay, Maternity Allowance or Working Tax Credit

• While on Jury Service or for aperiod of wrongful imprisonment

Carer’s credit

• This new credit not a benefit is available from 6 April 2010 for Basic State Pension and State Second Pension purposes

• It also protects Bereavement Benefits for spouses and civil partners

• Applies where a carer does so for at least 20 hours a week and– the person cared for receives middle or upper care component

of Disability Living Allowance, any level of Attendance Allowance or Constant Attendance Allowance

– the person(s) have been certified by a health or social care professional as needing the level of care being provided

Carer’s credit

• Given automatically– if carer is on Income Support because they are substantially

engaged in caring – To someone with entitlement to Carer’s Allowance for certain

weeks when they cannot receive Carer’s Allowance credits

• Otherwise must be claimed using form CC1 contained in the Carer’s Credit application pack

State Basic and Graduated Pension- rates (maxima) • Basic (own right) - £ 97.65 / week

• Married woman, man* or civil partner**(on spouse’s / partner’s record) - £58.50 / week

• Graduated pension - depends upon number of units ‘earned’. Unit value 11.53p each week

* From May 2010 ** From April 2015 provided spouse or civil partner was born on / after 6 April 1950.

Married women Reduced Rate Election – 2010-11• No longer available to newly married women• Need to hold a Certificate of Election to pay

reduced rate Class 1 NI or pay no Class 3 Self-Employed NI– Class 1 Reduced Rate NI

• 4.85% compared to 11% rate if earns more than £110 a week and up to £844 a week

• On earnings above £844 a week pay 1%

• While Election in force creates gaps in NI record for contributory benefits including State Basic Retirement Pension and bereavement benefits

Married women Reduced Rate Election• Changes in status

– If widowed do not automatically lose the right and may be able to retain that right for a certain period after the husband’s death

– ‘Election’ ends if• Divorced or if marriage annulled• If for 2 consecutive tax years

– have no earnings on which Class 1 NI is payable or ‘treated as paid’– have not been self-employed

NI Enquiries Helpline Tel: 0845 302 1497

Options ( before State Pension Age) to make up a shortfall• Further employment / self employment

• Unemployment ( Job Seeker’s Allowance)

• Illness (Employment & Support Allowance / Incapacity Benefit)

• Caring role• Voluntary Class 3 NI contribution - £12.05 a

week (2010-11)

Voluntary NI contributionsClass 3• Normally within a ‘window’ of 6 years of the end of the

‘deficient’ tax year• If payment made more than 2 years after the end of the

relevant tax year the amount payable is increased • Special dispensation for tax years

– 1996-97 to 2001-02– 1993-94 to 2007-08 with incorrect credit awards if unemployed,

sick or on an approved training course

• Additional ‘6 year window’ for Class 3

Deadline dates for Class 3 NI

Tax year with gap in NI record

Voluntary Class 3 NI must be paid by

2003-04 5 April 2010

2004-05 5 April 2011

2005-06 5 April 2012

2006-07 5 April 2013

2007-08 5 April 2014

2008-09 5 April 2015

Special dispensation for Class 2 or Class 3 NI• Tax year 2005-06

– Can pay Class 2 or Class 3 NI for this tax year at the original rate of £7.35 a week provided

• Reach State Pension Age on / or after 6 April 2010• Make the payment(s) before 5 April 2012

Special dispensation for Class 2 or Class 3 NI• Tax year 2006-07

– Can pay Class 2 or Class 3 NI for this tax year at the original rate of £7.55 a week provided

• Reach State Pension Age on / after 6 April 2010• Entitled to Home Responsibilities Protection• Make the payment(s) by 5 April 2013

Special dispensation for Class 2 or Class 3 NI• Tax years 1993-94 to 2007-08

– Can pay Class 2 or Class 3 NI for these tax years at the original rates provided

• Wrongly awarded NI credits when unemployed, sick or on an approved training course

• Make the payment(s) by 5 April 2014

Home Responsibilities Protection credits• Potentially available only from 6 April 1978 for

complete tax years up to 5 April 2010 and from 6 April 2010 can be awarded for weeks

• Protects record for:-– main child benefit payees ( child under 12*)– those looking after someone receiving specified

benefits ( 35 + hours)– those receiving income support while looking after a

sick /disabled person at home

Home Responsibilities Protection• Cannot reduce qualifying years for full

Basic State pension below 20* ‘old terms’

• Cannot be given for years covered by reduced rate NI contribution election

• From April 2002 ‘carers’ and people receiving child benefit for a child under 6 can build up State Second Pension too

Home Responsibilities Protection • State Second Pension

– Until 5 April 2010• If you receive Child Benefit for a child under 6 you

automatically build up an entitlement to State Second Pension

• If you receive Child Benefit for a child aged 6 or over with a long-term illness or disability you can build up an entitlement to State Second Pension but must claim using form CF411

– From 6 April 2010• If you receive Child Benefit for a child under 12 you

automatically build up an entitlement to State Second Pension

Divorced people• Can use ex-spouse’s

contribution record if it produces a higher Basic State pension

• Cannot use if re-marriage occurs before State Pension Age

Widows / widowers / civil partners

• Entitlement to pension protected in a similar way to that of divorced people

State Graduated Pension

• Graduated pension - depends upon number of units ‘earned’. Unit value 11.53p each week 2010-11

State Pensions - rates (maxima) ‘earnings related’• State Earnings Related Pension - 25% of revalued Upper Band

Earnings before 2000 then falling away to 20%

• April 2002 State Second Pension replaced SERPS

• From 6 April 2009 Upper Earnings Limit applies to NI calculation and a lower ceiling set (Upper Accruals Point) for calculation of State Second Pension - a ‘stealth tax’ of 11% for those earning between £770 and £844 a week in 2009-10

• Pensions Act 2007 changes coming into effect in tax year 2010-11 will see further reduction in accrual rate

Subject to any deductions for periods of ‘contracted-out’ employment

State Second Pension

• From April 2010 entitlement can be built up if– Employed and earning above the Lower Earnings

Level from any one job– Looking after children under 12 years old and

claiming Child Benefit– Caring for a sick / disabled person for more than 20

hours a week and claiming Carer’s Credit– Registered foster carer and claiming Carer’s Credit– Receive certain other benefits due to illness or

disability

Some other anglesNot seeing the wood for the trees!

Pension forecast• Forecasts

– Online

– Telephone 0845 3000 168

– Submit form BR19

• Forecast will give details of– Basic State pension

– SERPS / State Second Pension

– Graduated pension

• Will indicate if Basic State pension can be increased by paying NI for past or future periods

Pension forecast / claim• If you have either live abroad or have worked

overseas then contact the International Pension Centre for any claims

• If you are living in any EEA country you should claimas follows:-– If you have worked in the

country you are now living in thenclaim through the pension institution in that country

– if you have not worked in the country you are now living in then claim your pension direct from the International Pension Centre

Claim pension

• Previously the Pension Service wrote 4 months before State Pension Date to invite someone to claim their pension

• Now they can take applications over the telephone 2 months before expected claim date

State Pension claimline 0845 300 1084

National Insurance contributionsafter State Pension Age• If employed

– You must apply for an Age Exemption Certificate (CA4140)

• Visit HMRC website (www.hmrc.gov.uk)• Telephone 0845 302 1479 (lo-call rate)

– Then pass it to your Employer

If you do not obtain the Age Exemption CertificateYour employer will continue to deduct NI!

Deferral of State Pension

• From April 2005 improved terms– no limit on the deferral period 5 years before– enhancement improved to 1% for each 5

weeks deferred (appx 10.4% for 1 year) 7 weeks before

Deferral of State Pension• From April 2005 improved terms

– new option to take a taxable lump sum at time State pension claimed with normal level of State Pension instead of enhanced pension

• deferral must be for 1 year at least• lump sum calculated using rate of interest about

2% above Bank of England Base Rate

Pension Credit

• Replaced the Minimum Income Guarantee in 2003

• Extra help to those pensioners on lower incomes

• Reward for savings or modest additional incomes

Pension Credit

• Top up to £132.60 a week ( £202.40 a week for a couple)

• Reward for savings with additional cash at an initial rate of 60p reward for every £ of savings income

• Pension credit is non-taxable

Pension Credit – savings element• Extra cash for single pensioners up to

£20.52 a week

• Extra cash for couples of up to £27.09 a week

Claim Line 0800 99 1234

Pension Credit

• Public Spending Review October 2010 announcement– maximum sum that can be awarded from the

Savings Element of Pension Credit will be frozen for 4 tax years

Additional benefits

• £10 Xmas bonus– tax free in first week of December

• Winter Fuel payment £250 (£400 if aged 80 or more Xmas 2010)*

• Free – NHS prescriptions and eye tests from 60 – local public transport nationally - 60 and

increasing – TV licence once 75

Additional benefits

• Age 80– Additional 25p weekly – Over 80 pension

• If not receiving a Basic State Pension or it is at a low level it will be topped up by the ‘married couples’ supplement (£58.50 in 2010-11)* provided

– Living in the UK when you claim– Must have lived here for 10 years or

more in any 20 year period after your 60th birthday (living in the EU counts)

Self-employment (2010-11)• Need to register as self-employed• ‘Small Earnings Exception’ if

profits under £5,075 a year• Contribution ( Class 2- flat rate

£2.40 / week)• Class 4 contributions

( really a tax)– 8% payable on profits between

£5,715 and £43,875 and 1% above £43,875

Class 1 National Insurance contribution (2010-11)• Lower Earnings Limit - £97 a week• Upper Earnings Limit - £844 a week*

• Primary Threshold - £110 a week

• Employee’s primary rate of NI– Nothing up to £110 a week– Then 11% on pay between £110.01 and £844 a week– Then 1% above £844 a week

*But for S2P benefit purposes the upper limit for eligible earnings is set at £770 a week

Bereavement benefitsWill there be anything?

Bereavement benefits

• Bereavement payment– £2,000 lump sum tax free– You must have been under State Pension Age at the date of

death, or– Your husband, wife or civil partner was not entitled to a Category

A (own right) Basic State Retirement pension when they died– You do not qualify if you

• Were divorced from your late husband / wife or the civil partnership was dissolved at the date of death

• You are living with another person as husband, wife or civil partner

• You are in prison

• Claim after more than 12 months

Bereavement benefits

• Bereavement allowance– Weekly amount, dependent upon your age at the time of death

or when Widowed Parent’s Allowance stops, paid for up to 52 weeks

– You must have been under State Pension Age at the date of death, or

– You do not qualify if you• Were under 45 years of age• You are bringing up children – Widowed Parent’s Allowance applies• Were divorced from your late husband / wife or the civil partnership

was dissolved at the date of death• You are living with another person as husband, wife or civil partner• You are in prison• Claim after more than 3 months

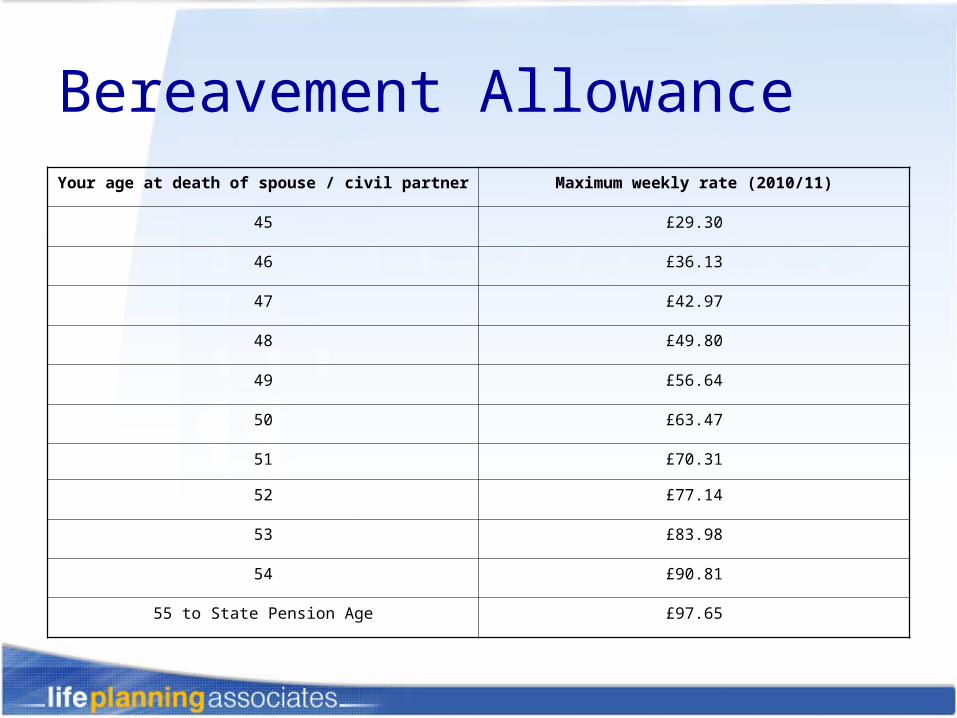

Bereavement AllowanceYour age at death of spouse / civil partner Maximum weekly rate (2010/11)

45 £29.30

46 £36.13

47 £42.97

48 £49.80

49 £56.64

50 £63.47

51 £70.31

52 £77.14

53 £83.98

54 £90.81

55 to State Pension Age £97.65

Widowed Parent’s Allowance

• Widowed Parent’s Allowance– Must be under State Pension Age to receive £97.65 a week

(2010-11) – taxable – and there may be an additional pension entitlement

– Must be a parent whose husband, wife or civil partner has died and you are entitled to Child Benefit*

– You may qualify if• You are bringing up a child or young person under 19 (or under 20

in some cases for whom you are receiving Child Benefit)

• You are expecting your late husband’s or your late Civil Partner’s baby (with whom you were pregnant from fertility treatment)

• Your husband, wife or Civil Partner died as a result of their work even if they did not pay NI

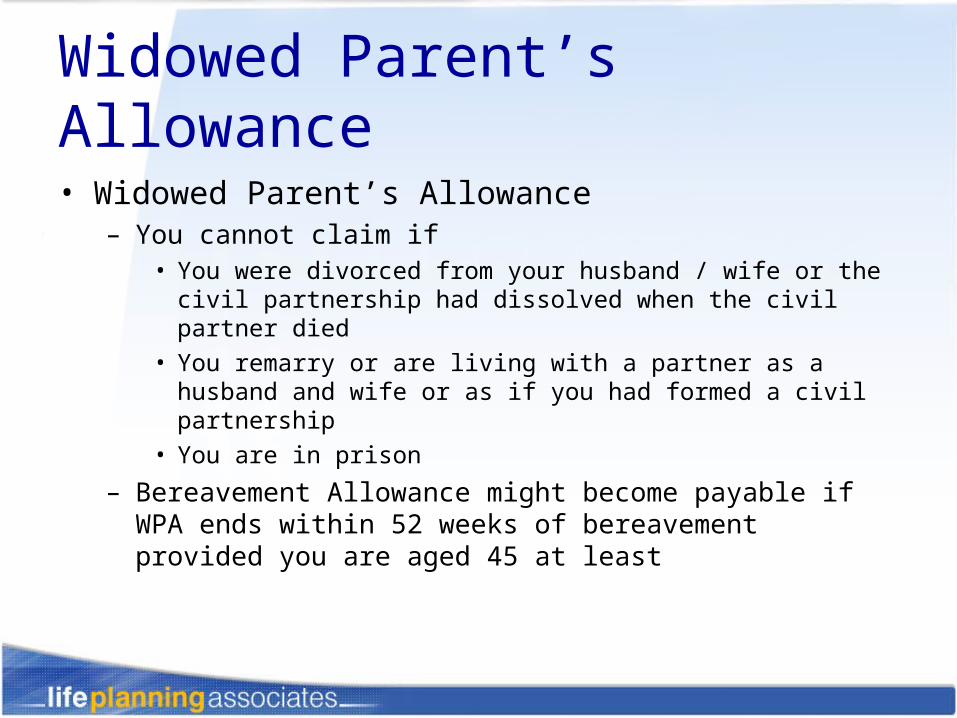

Widowed Parent’s Allowance

• Widowed Parent’s Allowance– You cannot claim if

• You were divorced from your husband / wife or the civil partnership had dissolved when the civil partner died

• You remarry or are living with a partner as a husband and wife or as if you had formed a civil partnership

• You are in prison

– Bereavement Allowance might become payable if WPA ends within 52 weeks of bereavement provided you are aged 45 at least

Basic State Pension

• Your widow / widower / civil partner may be entitled to some Basic State Pension based on your NI record if they have not already built up a full own right Basic State Pension

• They will lose this right if you die while they are under State Pension Age and before their State Pension age they – Remarry– Form a new civil partnership

• If you deferred your State Pension at State Pension Age your widow / widower / civil partner may be entitled to your extra State Pension

Additional State Pension

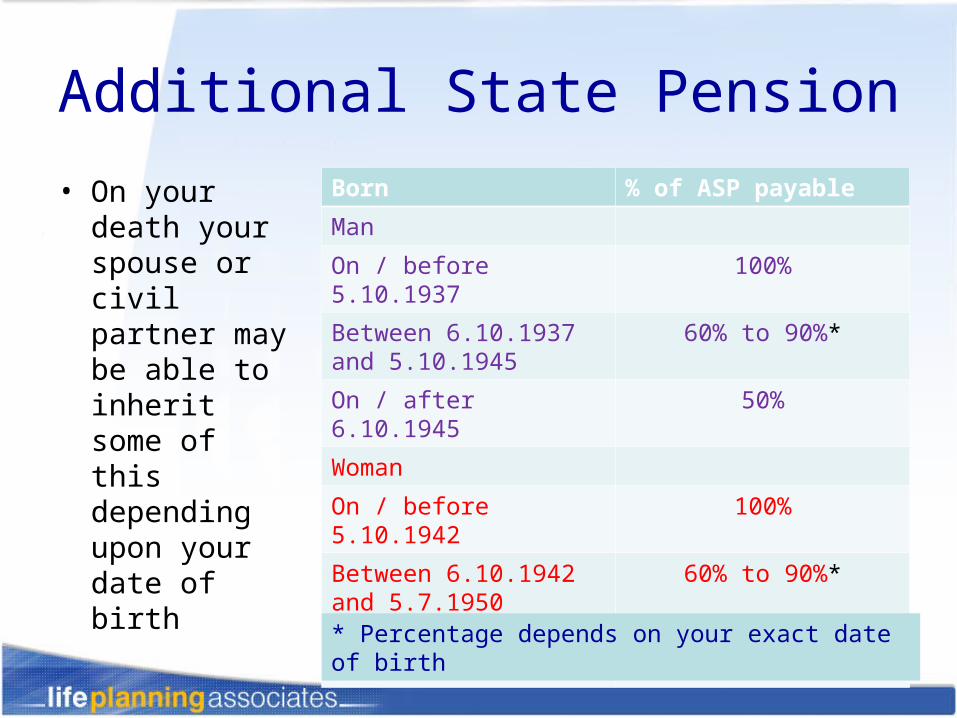

• On your death your spouse or civil partner may be able to inherit some of this depending upon your date of birth

Born % of ASP payable

Man

On / before 5.10.1937 100%

Between 6.10.1937 and 5.10.1945

60% to 90%*

On / after 6.10.1945 50%

Woman

On / before 5.10.1942 100%

Between 6.10.1942 and 5.7.1950

60% to 90%*

On / after 6 July 1950 50%

* Percentage depends on your exact date of birth

Death after deferring State PensionDeath before starting to claim

• Extra State Pension may be added to your spouse’s or civil partner’s State Pension

– A woman can benefit from her late husband’s or civil partner’s State Pension when she reaches State Pension Age provided she has not remarried or registered a new civil partnership

– From 6 April 2010 a man or surviving civil partner will not need to be over State Pension Age when the wife / civil partner dies to be able to inherit any extra State Pension or lump sum payment

Death after starting to claim

• Your widow’s, widower’s or civil partner’s pension will be increased

– For any Basic State Pension you put off claiming your widow/widower/civil partner will be entitled to the same amount as you would have received plus all or part of any Additional State Pension

– If you chose a lump-sum payment instead of extra State Pension, any amount you still have left forms part of your Estate and State Pension payments to your widow/widower/civil partner will not be increased

If you have no spouse or civil partner at death 3 months worth of the extra deferred State Pension can be claimed by your next of kin

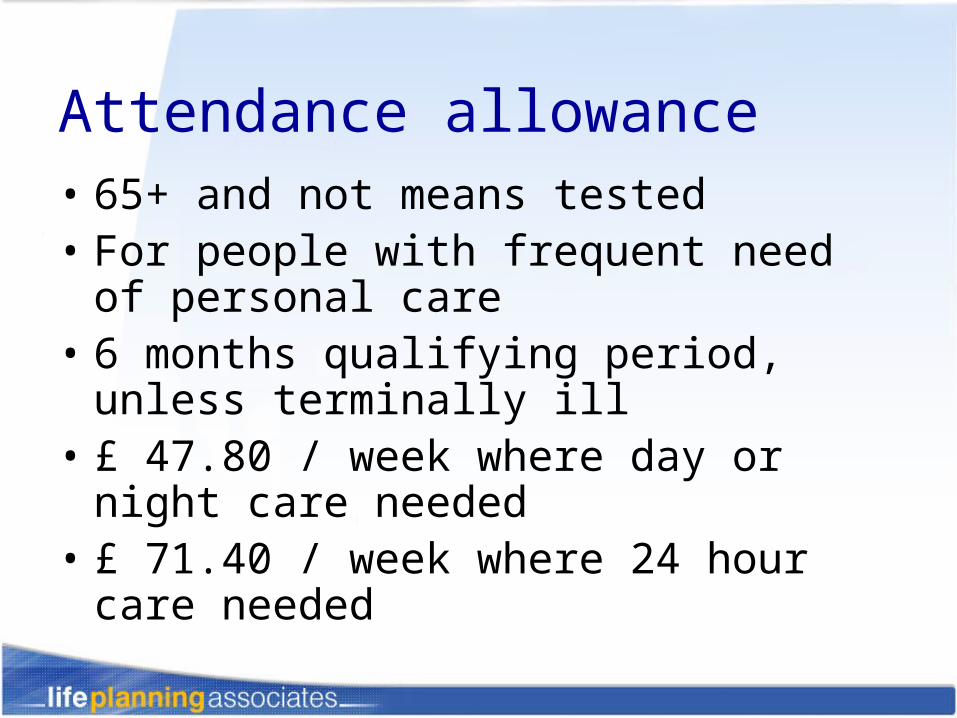

Attendance allowance• 65+ and not means tested• For people with frequent need of personal

care• 6 months qualifying period, unless

terminally ill• £ 47.80 / week where day or night care

needed• £ 71.40 / week where 24 hour care

needed

Attendance allowance

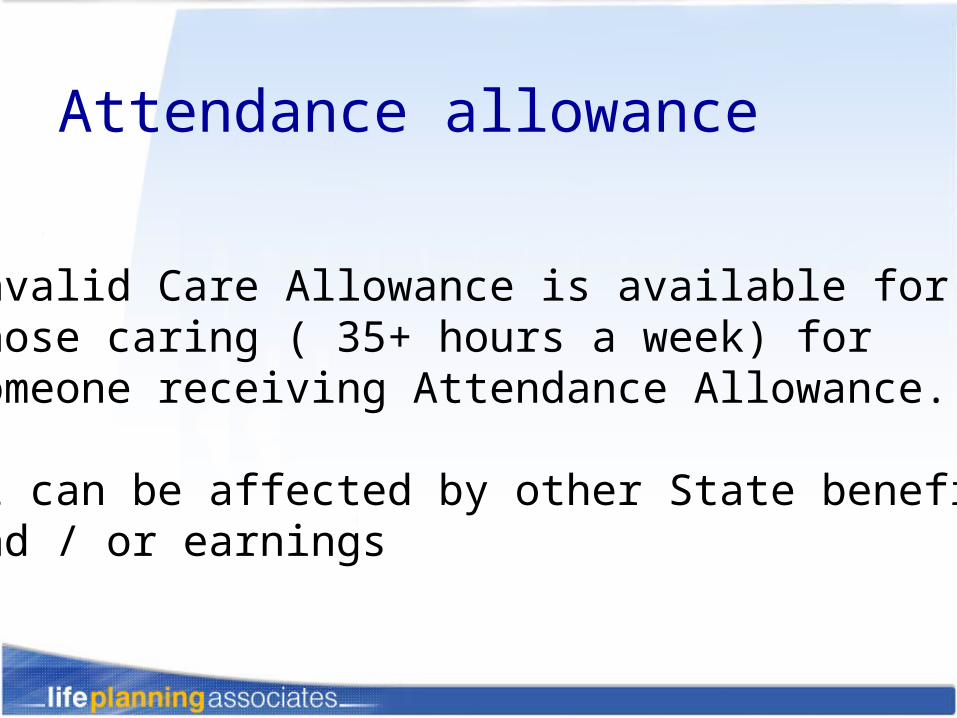

Invalid Care Allowance is available forthose caring ( 35+ hours a week) for someone receiving Attendance Allowance.

It can be affected by other State benefitsand / or earnings