Embed Size (px)

Citation preview

SOUTH AFRICAN NATIONAL

CREDIT REGULATOR

ACTPAKISTANI MICROFINANCE NETWORK

DELEGATION

TSHWANE, SOUTH AFRICA

Ramabaka Abel Tshimole

05 October 2010

2

South African credit market

Legislative framework before National Credit Act

There was no single unitary legislation regulating the credit market

There were different pieces of legislation such as the Usury Act & Credit

Agreements Act

Exemption Notice promulgated under the Usury Act established a regulatory body

to regulate micro lenders

Legislative framework before National

Credit Act

•There was no single unitary legislation

regulating the credit market

•There were different pieces of legislation such

as the Usury Act & Credit Agreements Act

•Exemption Notice promulgated under the Usury

Act established a regulatory body to regulate

micro lenders

Legislative framework before National Credit Act

• There was no single unitary legislation regulating the credit market

• Different pieces of legislation such as the Usury Act & Credit

Agreements Act applicable to different credit agreements

• No single reporting framework & uniform standards to monitor

compliance with legislation

3

National Credit Act in a nutshell …

National

Credit

Act

Agreements

& quotes

Enforcement &

debt collection

Credit Bureaus

National Credit Register

Interest

& fees

4

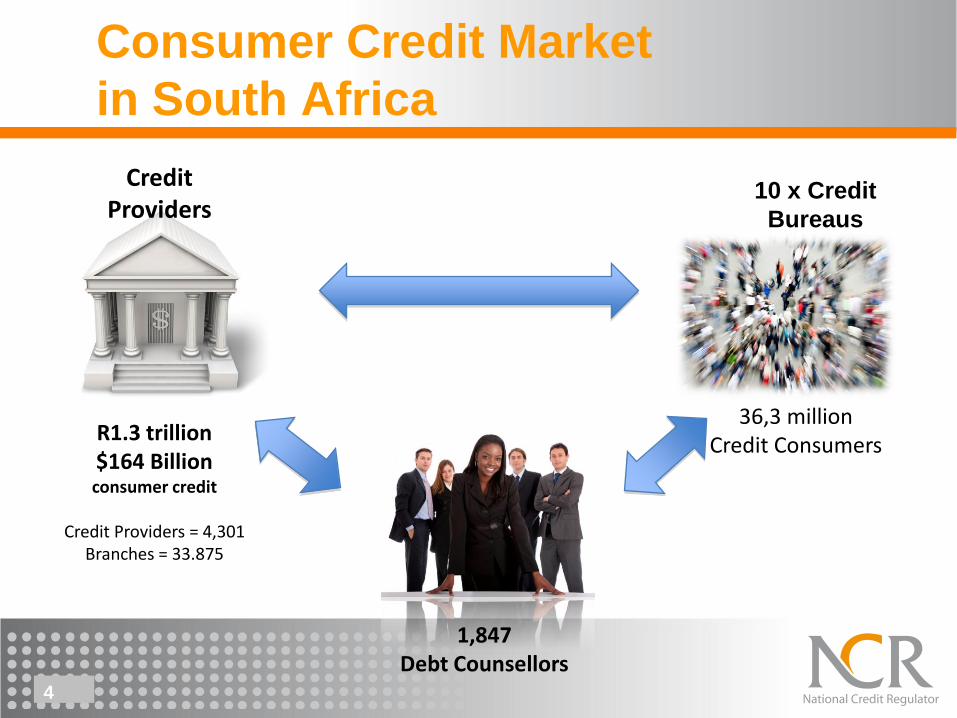

Consumer Credit Market

in South Africa

Credit Providers

36,3 millionCredit Consumers

1,847Debt Counsellors

R1.3 trillion$164 Billionconsumer credit

Credit Providers = 4,301Branches = 33.875

10 x Credit

Bureaus

5

ACHIEVEMENTS

• Unqualified (clean) Audit Report

• Registration of 4,301 entities with 33,875 branches

• Representing approximately R1.3 Trillion of credit, provided to 36,3 million credit agreements/clients

• Registered 10 credit bureaus,

• Registered 1,847 debt counsellors, arranged training, provided guidelines, accredited PDA’s 6 already

• Complaints received 9,303, calls received 349,101

• Investigations underway 39, completed 414

• Compliance notices 47, Cases referred to Tribunal 20

• Received 206,045 applications for debt review, 61,682 consumers approved and under debt review

• Awareness workshops held 1,741, radio/TV broadcasts 1,338/247, AVE R248m

6

National Credit Act

Regulatory mandate

• Registration of industry participants

• Monitoring of compliance by industry participants

• Enforcement, investigations & prosecution

• Research & publication of information

7

Registration of credit providers, credit

bureau, debt counsellors

The requirements

• Minimum requirements are set which also specify disqualification criteria

– Registration with SARS, appointment of accounting officers/auditor,

– Confirmation of registration with CIPRO, criminal/ITC check, etc

• Conditions of registration are stipulated and imposed

– General conditions

• Overall compliance with NCA & other applicable legislation

– Specific conditions

e.g for credit providers• Language policy proposals

• BBBEE

• Combating over-indebtedness of consumers

8

Debt Counselling: Update

Discussions between Credit Providers and Debt Counsellors

New rules and standardized procedures

Notifications and

financial

information

Response to Debt

Counsellors’

proposals

Restructuring rules Terminations in

terms of

Sec. 86 (10)

9

Importance & role of debt counselling

• Role of debt counselling, in the context of the lack of appropriate personal insolvency mechanisms in SA. o No appropriate “personal insolvency mechanisms”. US, UK & EU have range of different

mechanisms for personal insolvency. The mechanisms in SA are outdated and ineffective.

o As result, when debt stress occurs there is no effective mechanisms to resolve the issues, or for creating a “settlement” in which the obligations of the consumer and the demands of different credit providers are reconciled.

• Negative social impact of debt stresso No mechanism to resolve a personal financial crisis and enable an individual to get another

chance.

o Household income is permanently reduced through debt payments. Household needs not met and social welfare receipts are diverted to debt servicing.

o School fees not being paid, arrears on municipal service payments and a multitude of related areas.

10

Credit Provider Statistics

Approximately $164 billion consumer credit, provided to 17 million

consumers & consisting of 36.3 mil accounts as at March 2010

11

Compliance monitoring

Compliance Monitoring

1. Statutory Reports

Processing

1.1 Statistical Returns

2. Compliance Analysis of Statutory Reports

3. Conditions of Registration

1.2 Other Statutory

Reports (AFOR, AFS, AER, ACR)

2.1 Significant Entities (Top 20)

2.2 Remaining Significant Entities

(Biennially)

2.3 Cyclical Reactive Review (Other entities)

5. Compliance Research and

Education

3.1 Language Policy

5.1 Compliance Research

5.2 Industry Workshops

4. Market Conduct –

Flavour of the Quarter

3.2 Commit-ment to BBBEE

3.3 Combat of over

indebtedness

3.4 Review of Conditional

Registrations

12

Pro-active monitoring

• Currently we are concentrating on desk top analysis (Off-site analysis)

– Credit providers submit returns and reports

• Plans to introduce on-site analysis

– Assess the level of compliance in terms of the documents

submitted to us in comparison to what is really happening in the

companies by interviewing management team and staff

– Proactive general assessment and evaluation of business practices

and business models to identify areas of concern and aspects that

may be good for the industry (best practices in a way)

• Market conduct studies

– Focus on initial inspection before the files could be escalated to

investigations and enforcement to lessen the workload on them

– Proactive investigations

– Compliance Framework to inform the sequence, standards and

methods to use

12

13

Re-active monitoring

• Media reports

– Advertisements/ Marketing materials

• Reportable irregularities

– Following up on the non-compliance reported by IRBA on the reportable

irregularities received

• Complaints and call centre reports

– On going depending on the non-compliance received

– This will be the focus of complaints department

13

14

Statutory reporting

All registrants are required to submit reports at given times

e.g for credit providers

• Form 39 Statistical return

• Form 40 Annual Operational and Financial Return

• Annual Financial Statements

• Assurance engagement reports for both audited and non-audited credit

providers

• Annual Compliance Reports

Guidelines and workshops are provided to enlighten registrants

Consistency, accuracy, correctness, reliability, validity

• Registrants, accounting officers/auditors, compliance officers

• Systems, processes and procedures

15

Statutory reporting – credit providers

Type of document Date of submission Proposed period of extension

Compliance report Annually within 6 months after

financial year end

Not more than 2 months after due

date

Statistical Return > 15m – quarters – 15/05

15/08

15/11

15/02

<15m – 15 February for period 1

Jan to 31 Dec

Not more than 1,5 months after

due date

Annual Financial Statements 6 months after financial year end Not more than 2 months after due

date

Assurance Engagement Within 6 months after financial year

end

Not more than 2 months after due

date

Annual Financial and Operational

Return

Within 6 months after financial year

end

Not more than 2 months after due

date

16

Statutory reporting – debt counsellors

Type of document Date of submission Proposed period of extension

Compliance report 15 Feb for the period 1 Jan to 31

Dec

Not more than 2 months after due

date

Statistical Return 15 May – 1 Jan to 31 Mar

15 Aug – 1Apr to 30 Jun

15 Nov – 1 July - 30 Sep

15 Feb – 1 Oct to 31 Dec

Not more than 1 month after due

date

17

Statutory reporting – credit bureau

Type of document Date of submission Proposed period of extension

Annual compliance report 15 Mar for period 1 Jan to 31 Mar Not more than 2 months after due

date

Quarterly synoptic report 15 May – 1 Jan to 31 Mar

15 Aug – 1Apr to 30 Jun

15 Nov – 1July to 30 Sep

15 Feb – 1 Oct to 31 Dec

Not more than 2 months after due

date

18

Statutory reporting – Insurers

Type of document Date of submission Proposed date of submission

Periodic synoptic report 30 days after end of quarter

1 Jan – 31 March

1 April – 30 June

1 July – 30 September

1 October – 31 Dec

Not more than 2 months after due

date

19

Compliance reporting

• Compliance reporting by different registrants

• The reporting is standard and additional information may be

requested

• Information in the reports used to monitor market trends, market

conduct/practice

20

Enforcement Tools

• Conditions of registration

• Reports, statistics, research

• Explanatory notices, letters of undertaking

• Consumer complaints & various ombud

• Compliance notices & criminal action

• Tribunal, courts

Consultation requirement relating to enforcement action

on banks, but note does not apply to insurers

21

NCR Investigations

Present Focus and areas of concern

• Consumers losing homes due to unlawful practices

• Debt Counsellors: Receiving/distributing money & adhering to the time frames

• Debt collection practices of credit providers

• Section 73 Audits – Credit Bureaus

• Micro lenders: Adherence to interest caps and costs, card and pin, emergency loans, disclosure requirements,

• Non-registrants

• Major concern: The use of the NCA to further fraudulent activities

• Marketing and advertising

• Pre-agreement quotes and disclosure

• Right to set-off

• Priority payments

22

Investigation Statistics

Investigations Conducted 453

Debt Counselling Investigations 110

Credit Provider Investigations 328

Credit Bureau investigations 15

23

Enforcement Statistics

Instructional letters 110

Formal undertakings 20

Compliance Notices 47

Referrals to Tribunal 20

2424

Independent Professionals/ Practitioners

Independence of some of the reports

• The NCA somewhat rely on independent professionals like

auditors or accounting officers

i.e. Assurance Engagement report

25

Compliance Reporting feedback

– Reporting the outcome of the analysis of Statutory returns and others reports

• Consumer Credit Report

• Credit Bureau Monitor

• Research Reports from various research done to monitor performance and conduct of the credit industry players

– Pricing and Access Study

– Report on Over-indebtedness

– Impact of credit crisis on the consumer credit industry

• Relevant stakeholders– MRCC (Management Registrations and Compliance Committee

– MECC (Management Enforcement and Complaints Committee)

– CEO/COO

– Various government departments

– Registrants and/or associations of registrants (e.g banking association)

• NCR website

• Media release

26

Thank You !