Embed Size (px)

Citation preview

Economic Development Board 401 College Avenue Suite D Santa Rosa CA 95401 707.565.7170

www.sonomaedb.org

Sonoma County

Food Processing Industry

Report

2009

2009 Food Processing Industry Report

Table Of Contents

Executive Summary and Overview

Comparison of Trends: 2002 and 2008

New Trends: 2008 and 2009

Sweets

Artisan Breads

Olive Oil

Key Opportunities

Survey Results & Summary

Operations

Employment

Business Environment

Industry Specifics

Methodology and Acknowledgments

3

4

5

5

6

6

7

8

8

11

14

18

20

2 │ www.sonomaedb.org

2009 Food Processing Industry Report

3 │ www.sonomaedb.org

Executive Summary

February 2009 The Sonoma County Economic Development Board is pleased to present the 2009 Food Processing Industry Report. The survey upon which this report is based provides insight into local business activity, employment needs, job opportunities and general industry well‐being. The increased demand for organic and natural products has bolstered the food processing industry in Sonoma County, helping it to become a key regional industry. As it has grown, the relative health of the food processing industry has become an increasingly important factor in Sonoma County’s economy. While evolving into a surprisingly strong industry, changes in the local economic environment provide further opportunities for continued growth. Analysis of emerging trends and changes is included herein. The EDB conducted a survey for local food processors in order to identify issues and opportunities within the food processing industry. This report, an update of the 2002 report, presents the survey’s results and findings. Key Findings • 75% reported that the largest major industry trend was the continued increase in demand

for organic products. • 80% of respondents felt that their company was growing; 67% felt that their company’s

market share was increasing. • 70% of respondents said they plan on hiring within the next 12 months. However, 75%

indicated that they experienced difficulty in finding skilled labor. The EDB encourages interested readers to delve into these issues by contacting the agencies or organizations listed throughout this report or by visiting the EDB’s website, www.SonomaEDB.org. Ben Stone, Executive Director

2009 Food Processing Industry Report

4 │ www.sonomaedb.org

The Sonoma County Economic Development Board prepared its first report concerning the Sonoma County food processing industry in the spring of 2002. The trends that were present during 2002 can help provide a basis from which to judge the current trends and give context for the general direction of the industry. Many trends have stayed relatively stable since the last report. However, there are a few key differences that have developed since then:

• In 2002, only 48% of respondents indicated that the cost of doing business in Sonoma County was the biggest challenge to operating successfully — less than the cost of upgrading and purchasing new equipment. In 2008, 84% said the cost of doing business here was, making it by far the biggest challenge facing businesses, outweighing equipment challenges by nearly 33%.

• In 2002, 60% of respondents indicated that the increased demand for organic and natural products was a large trend. In 2008, that number rises to 74%. Similarly, only 47% of businesses carried organic products in their product lines in 2002, but in 2008, 62% of businesses carry organic products.

• In 2002, 79% of respondents reported that Sonoma County had a high or medium potential for the (then) current status and future growth of the food processing industry. In 2008, only 57% of respondents reported that Sonoma County had a high or medium potential for the current or future strength of the food processing industry.

As a whole, the trends facing the Sonoma County food processing industry are encouraging. While concerns such as the cost of doing business in Sonoma County, the difficulty of finding skilled labor for hire and the lower expectations for Sonoma County’s food processing potential, growth remains strong. A healthy number of businesses are expanding and hiring new employees. The continued growth of the organic and natural products provides an avenue that companies can utilize in order to keep business strong.

Comparison of Trends: 2002 and 2008

2009 Food Processing Industry Report

5 │ www.sonomaedb.org

In addition to the trends described on the previous page, there has been recent growth within the past year that was not present in 2002. These trends include the rise of sweets processors and retailers, artisan bakeries and the high‐quality olive oils.

Sweets

A growing number of sweet products processors and retailers have sprung in Sonoma County. Producers include Rohnert Park‐based Sonoma Toffee Works, Bert’s Desserts and Divine Delights in Petaluma, the Healdsburg Toffee Company and retailer Powell’s Sweet Shoppe in Petaluma and Windsor.

Many of the processors, such as Divine Delights and the Healdsburg Toffee Company, began as small family bakeries. The original Powell’s Sweet Shoppe in Windsor has begun to expand through locally controlled franchises throughout the Bay Area.

This investment in fine sweets may benefit the local economy: nationwide, gourmet snack sales rose 31% and candy rose 85% from 2005 to 2007, according to a 2008 specialty‐food industry report. In addition, Packaged Facts, a food and beverage market research firm, predicts that upscale chocolate sales will outperform the entire chocolate industry by five times by 2012.1

Goat Milk Sweets

In addition, Sonoma goat milk‐based sweets may gain a greater hold in 2009. Laloo’s gourmet milk ice cream company, founded in 2004, and Redwood Hill Farms, a family farm since 1968, process and distribute goat milk products.

The former, which promotes its low‐fat, low‐cal, low‐lactose, gluten‐free, hormone‐free products, will release goat milk chocolate bars and vanilla ice cream sandwiches in March. Redwood Hill Farms, the first Certified Humane Goat Dairy in the U.S., began distribution of quarts of goat milk in late 2008, and plans to add pineapple orange mango goat milk kefir to its line in spring 2009.2 1“Edible, Affordable Indulgences for 2009, ” Wall Street Journal, 17 January 2009

2“Edible, Affordable Indulgences for 2009, ” Wall Street Journal, 17 January 2009; www.redwoodhill.com and www.goatmilkicecream.com.

New Trends: 2008-2009

2009 Food Processing Industry Report

6 │ www.sonomaedb.org

Artisan Bakeries

Also expanding throughout Sonoma County and the North Bay are artisan bakeries. Sonoma County has a wealth of bakeries located throughout the region, which offer a variety of hand‐crafted, delicious and sometimes imaginative offerings. By location, a representative sample includes: Raymond’s Bakery in Cazadero; Wild Flour Bread in Freestone; Nightingale Bakery in Forestville; Costeaux French Bakery, Preston of Dry Creek and Downtown Bakery and Creamery in Healdsburg; Full Circle Bakery in Penngrove; Della Fattoria Bakery in Petaluma; Bennett Valley Bread and Pastry in Santa Rosa; Village Bakery in Sebastopol and Santa Rosa; Twofish Baking Company in Sea Ranch; and Artisan Bakers and Basque Boulangerie in Sonoma.

The bakeries have been around for various years. Some establishments, like the Costeaux French Bakery, are mature in age; others, like the Downtown Bakery and Creamery, are expanding; and the Nightingale Bakery may be the area’s newest offering, having opened in late 2008. But they all offer great loaves. For example, at Wild Flour Bread both local and out‐of‐town visitors come to enjoy fougasse, seeded french bread and sticky bun breads. At Della Fattoria one can buy anything from a baguette to Meyer lemon rosemary boule. 1

Olive Oils

Another potential area for growth in Sonoma County is olive oil. The county has an estimated 150 small‐scale olive oil producers, more than any other county in the state. While 99 percent of olive oil consumed in the United States originates abroad, the remaining percent is from California.2 Although area olive trees were originally planted in the early 1990s, the market has steadily grown. Sonoma’s olive presses include operations in Dry Creek, Glen Ellen, Hopland and Sonoma. While the cost of processing local oils is very high, the future may be in high quality artisan oils and innovative combinations. The long‐term outlook may depend on the cost of production, branding success and a strategies of local growers and harvesters.

Overall, prospects for the local food processing industry look promising. Niche marketing and an emphasis on high‐quality, specialty items that tap into new markets will help local businesses to prosper if costs of production and labor are kept reasonable.

1Of much help to this summary was “Baker’s Delight,” The Press Democrat. Food and Wine D1, D7. October 29, 2008.

2“Harvest of Hope,” The Press Democrat. A1, A9. 7 November 2008.

2009 Food Processing Industry Report

7 │ www.sonomaedb.org

Key Opportunities

• Job Creation — As the local food processing industry expands, there will be an increase in

the demand for workers, both skilled and unskilled. The Economic Development Board

could partner with local chambers of commerce, schools, job training agencies and others

to help the food processing industry meet the increased need for labor. The recent decline

in real estate prices may also have a positive impact on job creation, as the lower cost of

housing in Sonoma County may encourage potential employees to relocate to the region.

The Economic Development Board could partner with the Workforce Investment Board in

order to reach out to those individuals who are considering relocating to Sonoma for work.

• Innovation — Local food processors have relied on specialization in order to compete in a

consolidating market. In order to help the industry as a whole, a “Best Practices Guide”

could be assembled by an industry team that would highlight ways that struggling

businesses could innovate their operations successfully by documenting successful local

business practices. Successful businesses willing to share their methods of innovation can

gain recognition for their success through such a guide. Also, the creation of an annual

recognition event for the industry could help promote further innovation.

• Growth of Sector — Processors can be surveyed to determine what information might be

useful to them in order to operate effectively as changes occur over the next 10 years. This

information can be made available to both existing and start‐up businesses.

• Exhibitions — Food processors could cooperatively display their goods to the public.

Farmer’s markets could provide an opportunity to show the public available organic and

natural products, to explain their benefits, and to promote the purchase of locally

produced commodities.

• Partnerships — New partnerships created between growers and producers could prove

beneficial for both parties. Such partnerships could strengthen the ties between

processors and growers, resulting in an alliance that would help streamline both the

agriculture and processing industries. Organizations such as the Sonoma County Vintners

and Growers, the California Certified Organic Farmers, the Sonoma County Fair and Farm

Trails could prove to be useful partnerships.

2009 Food Processing Industry Report

8 │ www.sonomaedb.org

Survey Results and Summary

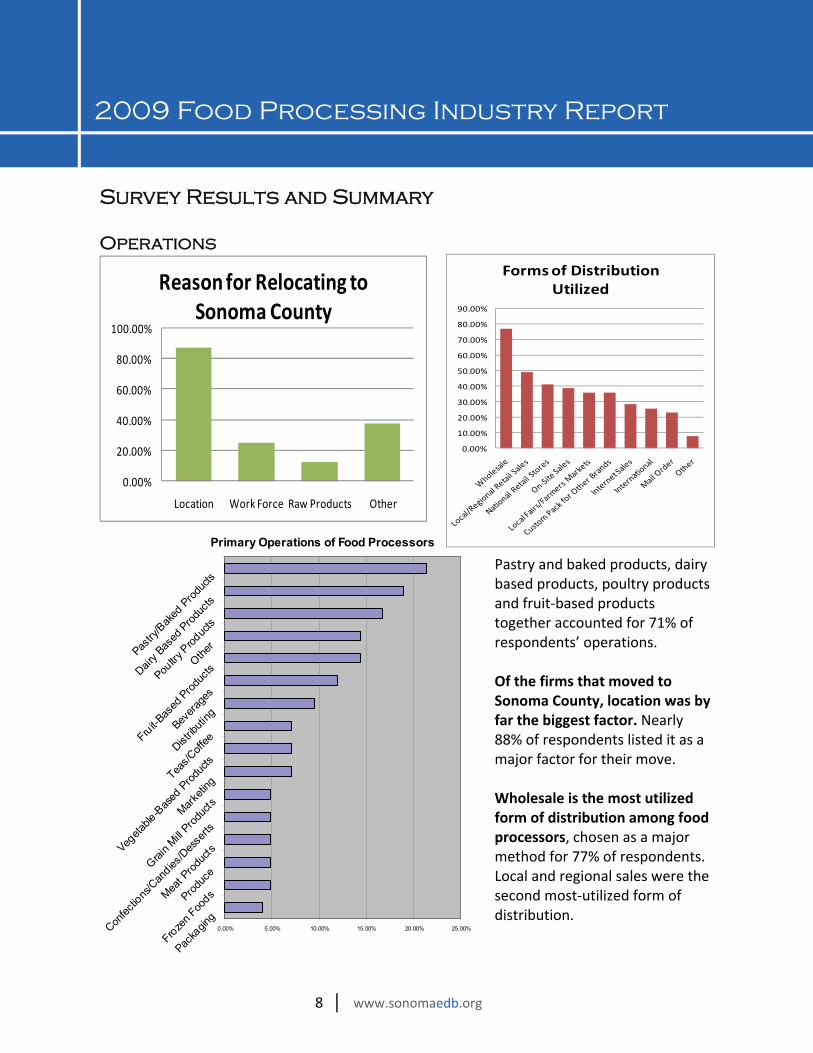

Pastry and baked products, dairy based products, poultry products and fruit‐based products together accounted for 71% of respondents’ operations. Of the firms that moved to Sonoma County, location was by far the biggest factor. Nearly 88% of respondents listed it as a major factor for their move. Wholesale is the most utilized form of distribution among food processors, chosen as a major method for 77% of respondents. Local and regional sales were the second most‐utilized form of distribution.

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

Location Work Force Raw Products Other

Reason for Relocating to Sonoma County

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

Forms of Distribution Utilized

Operations

Primary Operations of Food Processors

0.00% 5.00% 10.00% 15.00% 20.00% 25.00%

Packa

ging

Frozen F

oodsProd

uce

Meat P

roduc

ts

Confec

tions

/Can

dies/D

esse

rts

Grain M

ill Prod

uctsMark

eting

Vegeta

ble-B

ased

Prod

ucts

Teas/C

offeeDist

ributi

ngBev

erage

s

Fruit-Bas

ed Prod

ucts

Other

Poultry

Prod

ucts

Dairy B

ased

Produc

ts

Pastry

/Bak

ed P

roduc

ts

2009 Food Processing Industry Report

9 │ www.sonomaedb.org

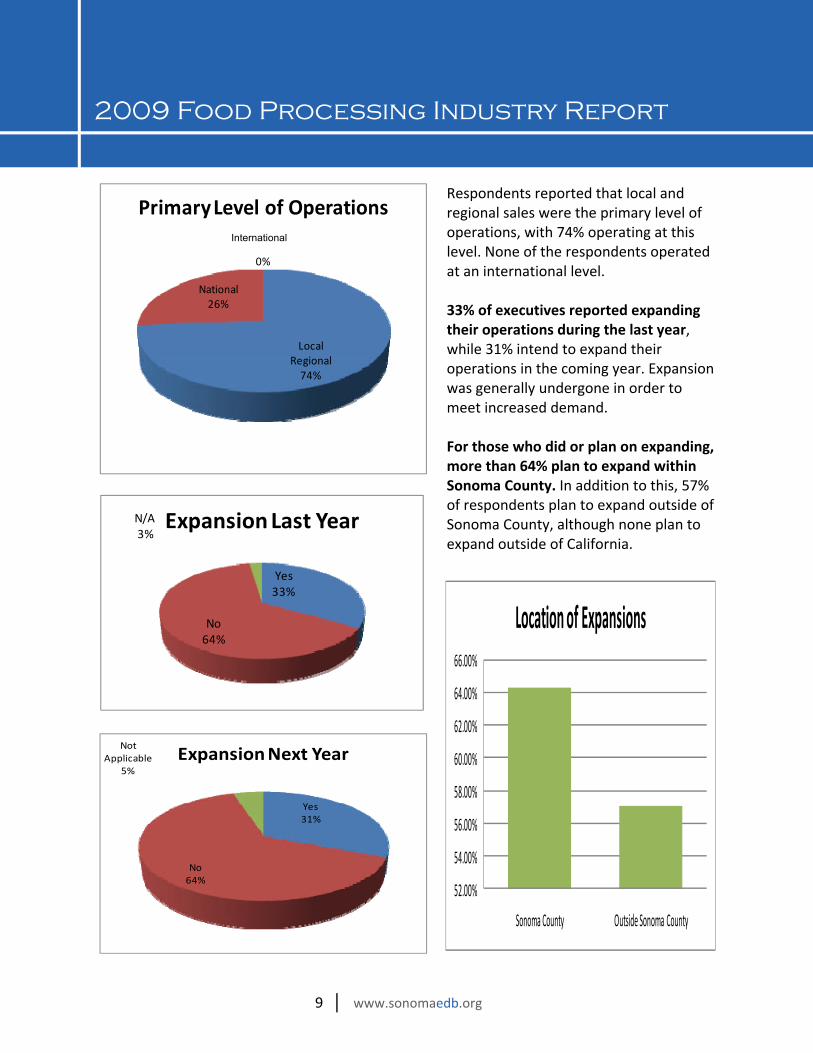

Respondents reported that local and regional sales were the primary level of operations, with 74% operating at this level. None of the respondents operated at an international level. 33% of executives reported expanding their operations during the last year, while 31% intend to expand their operations in the coming year. Expansion was generally undergone in order to meet increased demand. For those who did or plan on expanding, more than 64% plan to expand within Sonoma County. In addition to this, 57% of respondents plan to expand outside of Sonoma County, although none plan to expand outside of California.

Local Regional74%

National26%

International0%

Primary Level of Operations

Yes31%

No64%

Not Applicable

5%Expansion Next Year

52.00%

54.00%

56.00%

58.00%

60.00%

62.00%

64.00%

66.00%

Sonoma County Outside Sonoma County

Location of ExpansionsYes33%

No64%

N/A3%

Expansion Last Year

International

2009 Food Processing Industry Report

10 │ www.sonomaedb.org

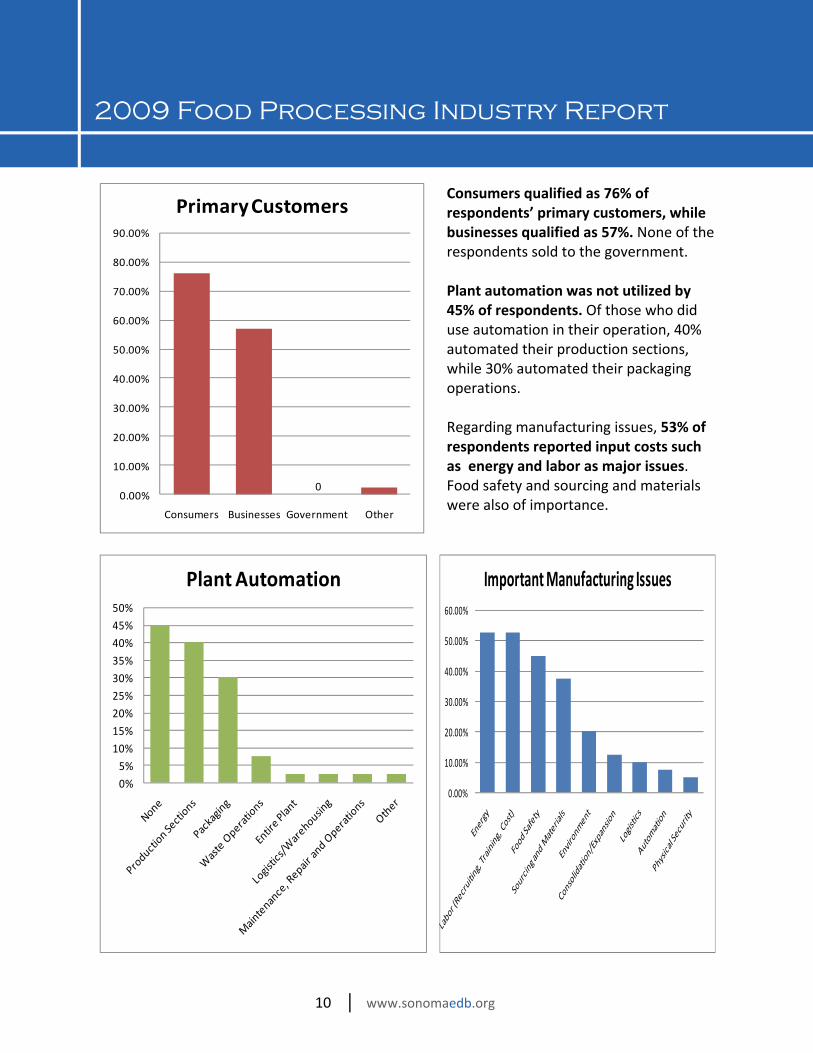

Consumers qualified as 76% of respondents’ primary customers, while businesses qualified as 57%. None of the respondents sold to the government. Plant automation was not utilized by 45% of respondents. Of those who did use automation in their operation, 40% automated their production sections, while 30% automated their packaging operations. Regarding manufacturing issues, 53% of respondents reported input costs such as energy and labor as major issues. Food safety and sourcing and materials were also of importance.

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

Consumers Businesses Government Other

Primary Customers

0%5%

10%15%

20%25%30%35%

40%45%50%

Plant Automation

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Important Manufacturing Issues

0

2009 Food Processing Industry Report

11 │ www.sonomaedb.org

Employment

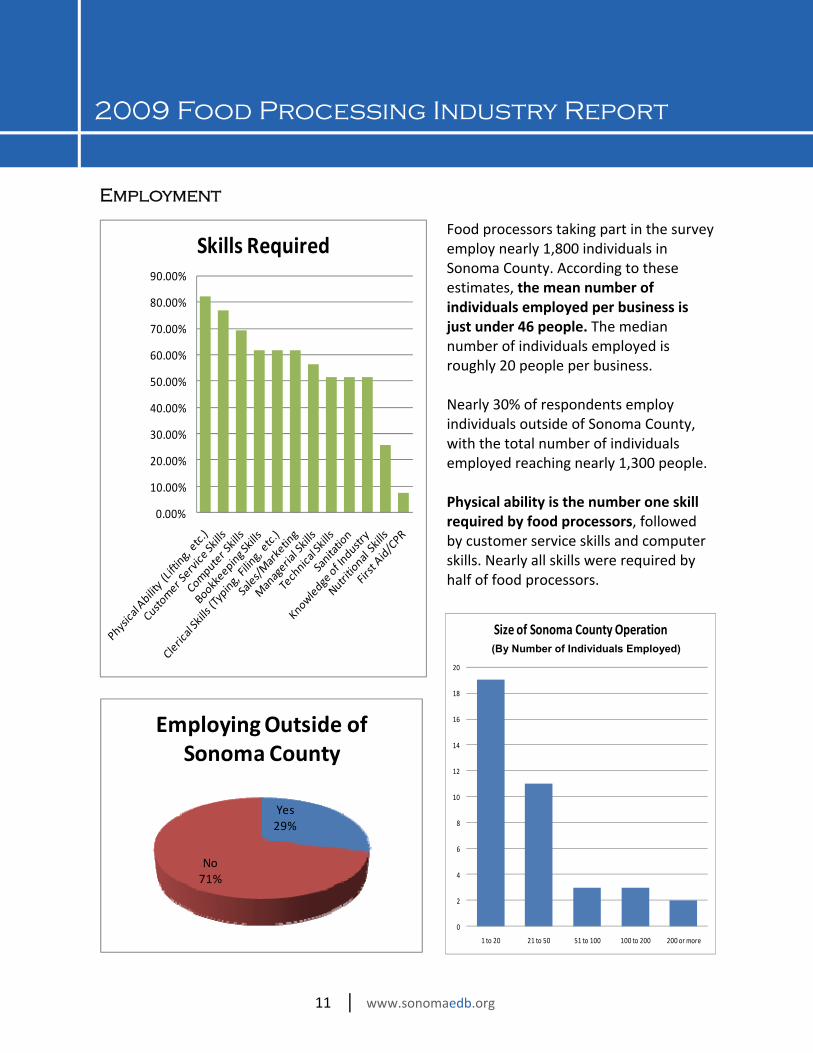

Food processors taking part in the survey employ nearly 1,800 individuals in Sonoma County. According to these estimates, the mean number of individuals employed per business is just under 46 people. The median number of individuals employed is roughly 20 people per business. Nearly 30% of respondents employ individuals outside of Sonoma County, with the total number of individuals employed reaching nearly 1,300 people. Physical ability is the number one skill required by food processors, followed by customer service skills and computer skills. Nearly all skills were required by half of food processors.

0

2

4

6

8

10

12

14

16

18

20

1 to 20 21 to 50 51 to 100 100 to 200 200 or more

Size of Sonoma County Operation (Individuals Employed)

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

Skills Required

Yes29%

No71%

Employing Outside of Sonoma County

(By Number of Individuals Employed)

2009 Food Processing Industry Report

12 │ www.sonomaedb.org

Very Difficult5% Difficult

10%

Somewhat Difficult35%

Not Really a Problem

50%

Difficulty in Finding Unskilled Labor

Skilled Employees

49%

Unskilled Employees

51%

Percentage of Skilled Employees

Difficulty in Finding Skilled Employees

Somewhat Difficult49%

Not Really a Problem13%

Very Difficult13%

Difficult25%

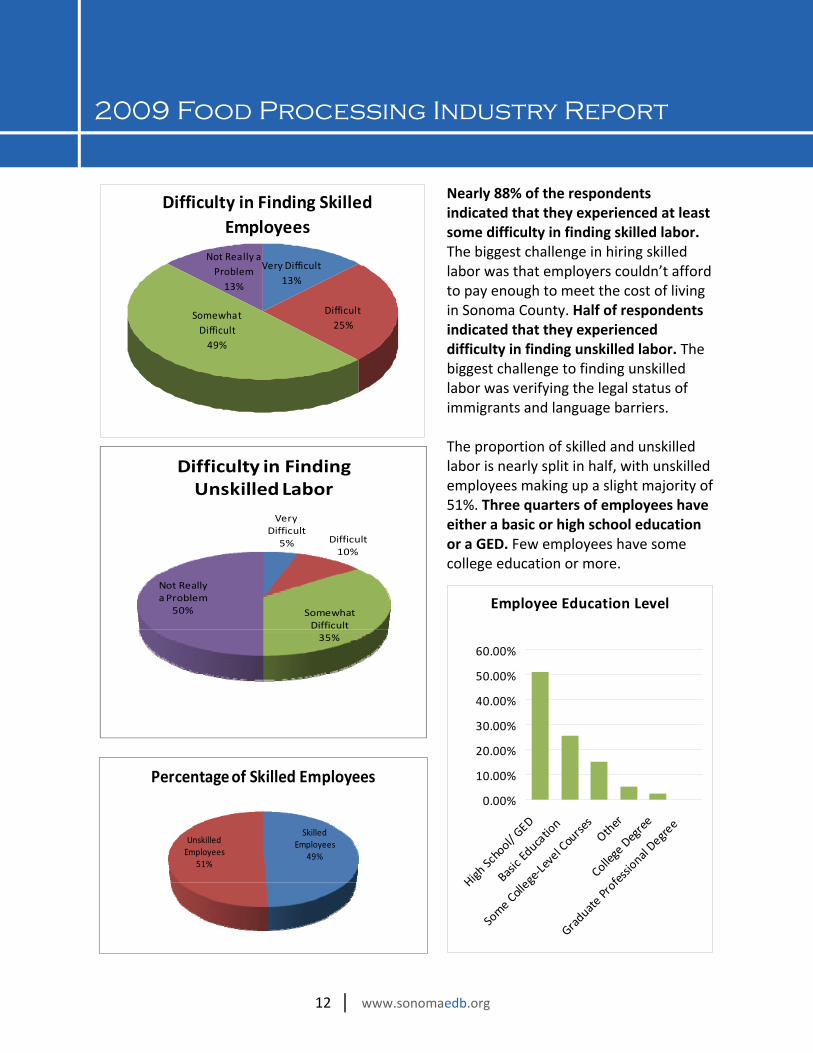

Nearly 88% of the respondents indicated that they experienced at least some difficulty in finding skilled labor. The biggest challenge in hiring skilled labor was that employers couldn’t afford to pay enough to meet the cost of living in Sonoma County. Half of respondents indicated that they experienced difficulty in finding unskilled labor. The biggest challenge to finding unskilled labor was verifying the legal status of immigrants and language barriers. The proportion of skilled and unskilled labor is nearly split in half, with unskilled employees making up a slight majority of 51%. Three quarters of employees have either a basic or high school education or a GED. Few employees have some college education or more.

Employee Education Level

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

High School/ GED

Basic Education

Some College‐Level CoursesOther

College Degree

Graduate Professional Degree

2009 Food Processing Industry Report

13 │ www.sonomaedb.org

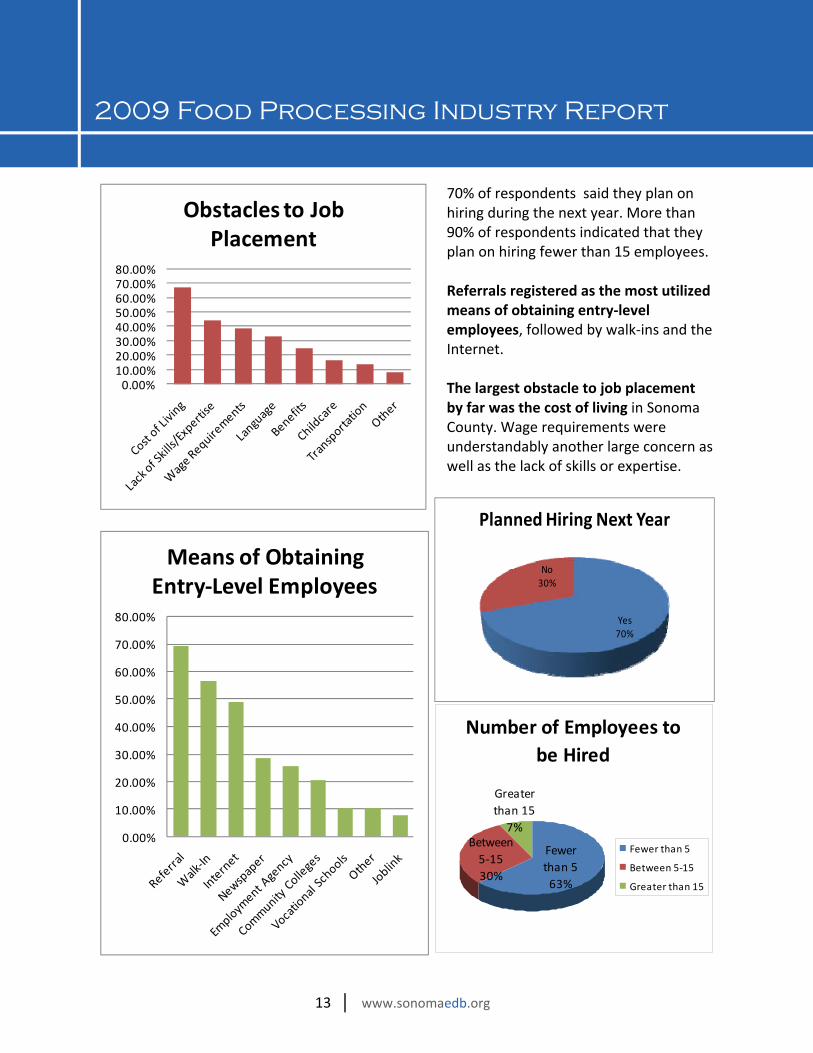

70% of respondents said they plan on hiring during the next year. More than 90% of respondents indicated that they plan on hiring fewer than 15 employees. Referrals registered as the most utilized means of obtaining entry‐level employees, followed by walk‐ins and the Internet. The largest obstacle to job placement by far was the cost of living in Sonoma County. Wage requirements were understandably another large concern as well as the lack of skills or expertise.

Yes70%

No30%

Planned Hiring Next Year

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Means of Obtaining Entry‐Level Employees

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%80.00%

Obstacles to Job Placement

Number of Employees to be Hired

Greater than 157%

Between 5‐1530%

Fewer than 563%

Fewer than 5

Between 5‐15

Greater than 15

2009 Food Processing Industry Report

14 │ www.sonomaedb.org

Business Environment

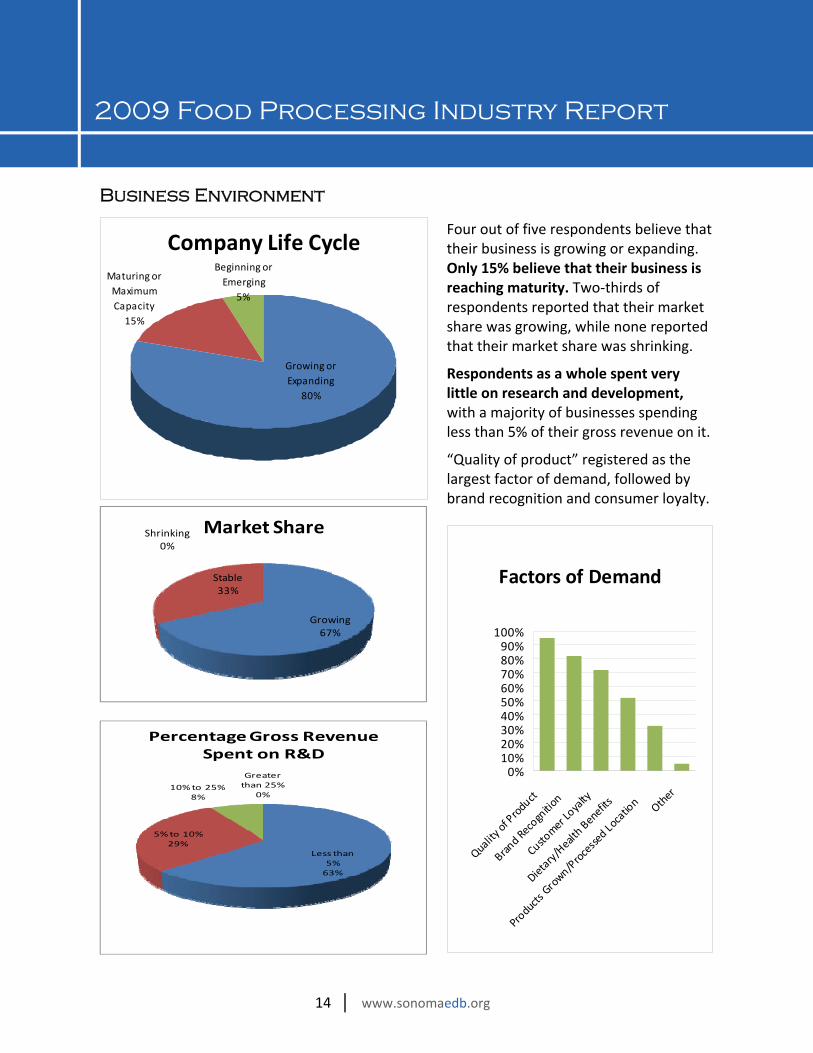

Growing67%

Stable33%

Shrinking0%

Market Share

Less than 5%63%

5% to 10%29%

10% to 25%8%

Greater than 25%

0%

Percentage Gross Revenue Spent on R&D

Four out of five respondents believe that their business is growing or expanding. Only 15% believe that their business is reaching maturity. Two‐thirds of respondents reported that their market share was growing, while none reported that their market share was shrinking.

Respondents as a whole spent very little on research and development, with a majority of businesses spending less than 5% of their gross revenue on it.

“Quality of product” registered as the largest factor of demand, followed by brand recognition and consumer loyalty.

Factors of Demand

0%10%20%30%40%50%60%70%80%90%

100%

Quality of Product

Brand Recognition

Customer Loyalty

Dietary/Health Benefits

Products Grown/Processed Location Ot

her

Company Life Cycle

Growing or Expanding

80%

Maturing or Maximum Capacity15%

Beginning or Emerging

5%

2009 Food Processing Industry Report

15 │ www.sonomaedb.org

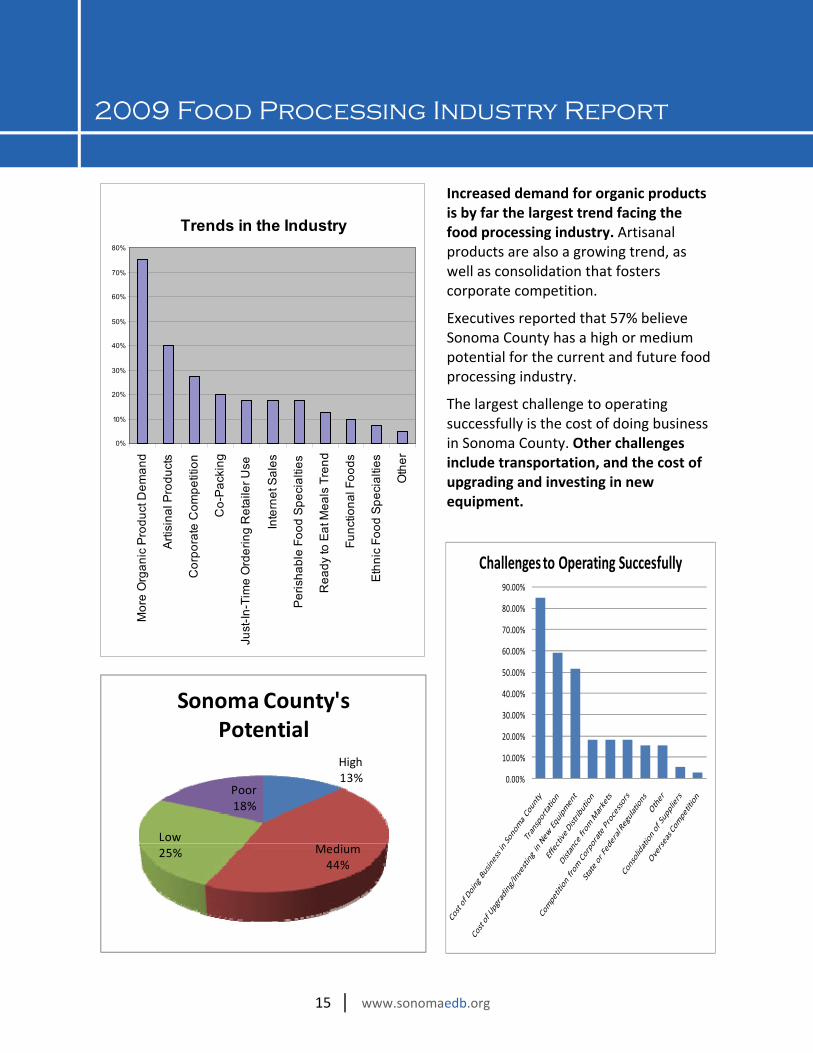

Increased demand for organic products is by far the largest trend facing the food processing industry. Artisanal products are also a growing trend, as well as consolidation that fosters corporate competition.

Executives reported that 57% believe Sonoma County has a high or medium potential for the current and future food processing industry.

The largest challenge to operating successfully is the cost of doing business in Sonoma County. Other challenges include transportation, and the cost of upgrading and investing in new equipment.

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

Challenges to Operating Succesfully

High13%

Medium44%

Low25%

Poor18%

Sonoma County's Potential

Trends in the Industry

0%

10%

20%

30%

40%

50%

60%

70%

80%

Mor

e O

rgan

ic P

rodu

ct D

eman

d

Arti

sina

l Pro

duct

s

Cor

pora

te C

ompe

titio

n

Co-

Pac

king

Just

-In-T

ime

Ord

erin

g R

etai

ler U

se

Inte

rnet

Sal

es

Per

isha

ble

Food

Spe

cial

ties

Rea

dy to

Eat

Mea

ls T

rend

Func

tiona

l Foo

ds

Eth

nic

Food

Spe

cial

ties

Oth

er

2009 Food Processing Industry Report

16 │ www.sonomaedb.org

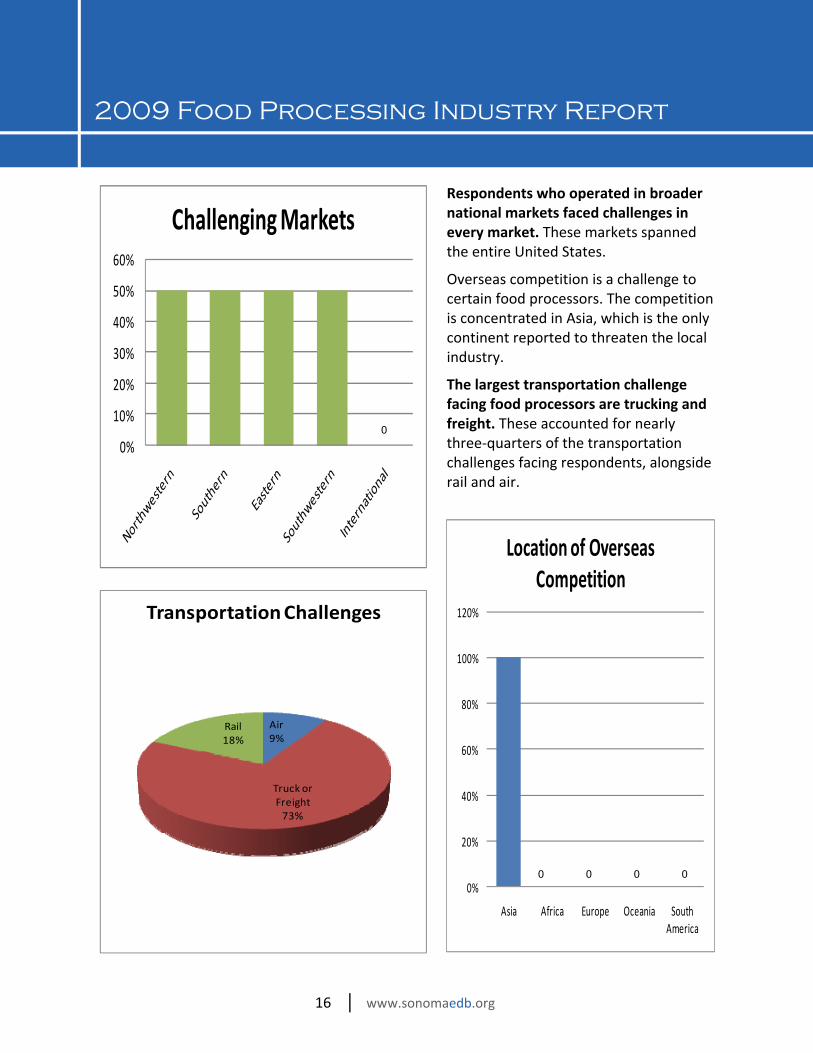

Respondents who operated in broader national markets faced challenges in every market. These markets spanned the entire United States.

Overseas competition is a challenge to certain food processors. The competition is concentrated in Asia, which is the only continent reported to threaten the local industry.

The largest transportation challenge facing food processors are trucking and freight. These accounted for nearly three‐quarters of the transportation challenges facing respondents, alongside rail and air.

0%

10%

20%

30%

40%

50%

60%

Challenging Markets

0%

20%

40%

60%

80%

100%

120%

Asia Africa Europe Oceania South America

Location of Overseas Competition

Air9%

Truck or Freight73%

Rail18%

Transportation Challenges

0 0 0 0

0

2009 Food Processing Industry Report

17 │ www.sonomaedb.org

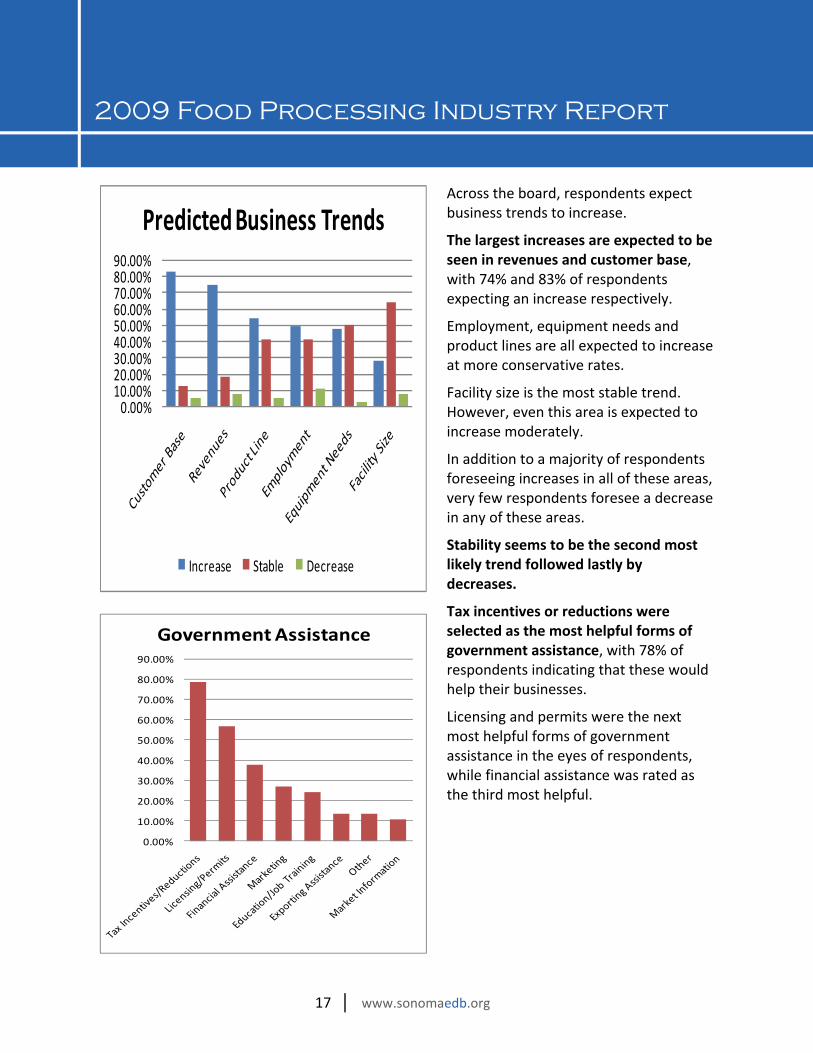

Across the board, respondents expect business trends to increase.

The largest increases are expected to be seen in revenues and customer base, with 74% and 83% of respondents expecting an increase respectively.

Employment, equipment needs and product lines are all expected to increase at more conservative rates.

Facility size is the most stable trend. However, even this area is expected to increase moderately.

In addition to a majority of respondents foreseeing increases in all of these areas, very few respondents foresee a decrease in any of these areas.

Stability seems to be the second most likely trend followed lastly by decreases.

Tax incentives or reductions were selected as the most helpful forms of government assistance, with 78% of respondents indicating that these would help their businesses.

Licensing and permits were the next most helpful forms of government assistance in the eyes of respondents, while financial assistance was rated as the third most helpful.

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

Government Assistance

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%80.00%90.00%

Predicted Business Trends

Increase Stable Decrease

2009 Food Processing Industry Report

18 │ www.sonomaedb.org

Industry Specifics

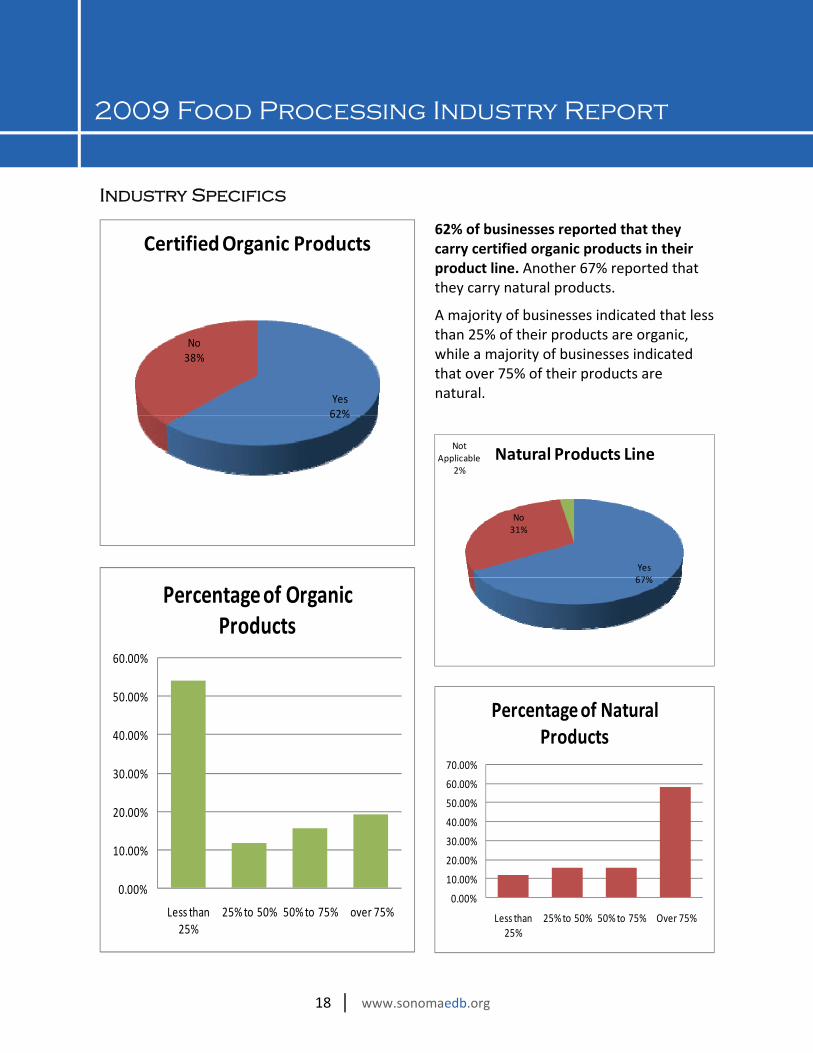

62% of businesses reported that they carry certified organic products in their product line. Another 67% reported that they carry natural products.

A majority of businesses indicated that less than 25% of their products are organic, while a majority of businesses indicated that over 75% of their products are natural. Yes

62%

No38%

Certified Organic Products

Yes67%

No31%

Not Applicable

2%Natural Products Line

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Less than 25%

25% to 50% 50% to 75% over 75%

Percentage of Organic Products

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Less than 25%

25% to 50% 50% to 75% Over 75%

Percentage of Natural Products

2009 Food Processing Industry Report

19 │ www.sonomaedb.org

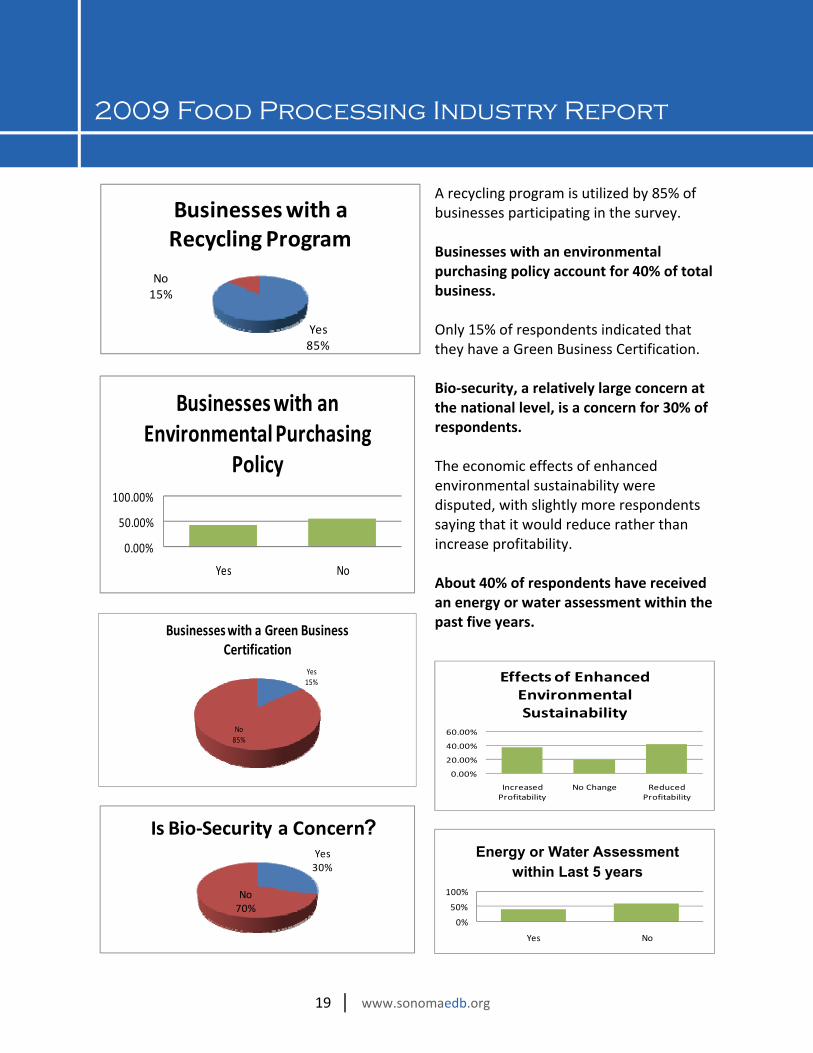

A recycling program is utilized by 85% of businesses participating in the survey. Businesses with an environmental purchasing policy account for 40% of total business. Only 15% of respondents indicated that they have a Green Business Certification. Bio‐security, a relatively large concern at the national level, is a concern for 30% of respondents. The economic effects of enhanced environmental sustainability were disputed, with slightly more respondents saying that it would reduce rather than increase profitability. About 40% of respondents have received an energy or water assessment within the past five years.

0.00%

50.00%

100.00%

Yes No

Businesses with an Environmental Purchasing

Policy

Yes15%

No85%

Businesses with a Green Business Certification

Yes30%

No70%

Is Bio‐Security a Concern

0.00%

20.00%

40.00%

60.00%

Increased Profitability

No Change Reduced Profitability

Effects of Enhanced Environmental Sustainability

0%

50%

100%

Yes No

Energy or Water Assesment Within Last 5 years

Yes85%

No15%

Businesses with a Recycling Program

? Energy or Water Assessment

within Last 5 years

2009 Food Processing Industry Report

20 │ www.sonomaedb.org

Methodology

142 surveys were distributed to food processors in Sonoma County in 2008. 43 surveys were completed, yielding a response rate of 30%. The responses were collected into a database, which provided a framework for this analysis. This report represents a snapshot of the local food processing industry. The trends discussed in this report do not exhaust the entire list of concerns facing all food processors. Certainly the trends discussed are major and deserve recognition on merit of their acknowledgement by most of the respondents surveyed. However, there exist concerns not mentioned that deserve recognition, as they greatly affect individuals within the industry. By improving communication, these issues can be recognized and addressed.

Acknowledgements

The 2009 Food Processing Report would not have been possible without the contributions of many companies, organizations and individuals. First and foremost, the local food processors that participated in the survey deserve recognition. Their responses provided the framework for this report. Mike Simanek, a summer intern for the Economic Development Board, created the report. He combined analysis of survey results with additional research to write the report. His work was outstanding and he displayed diligence and dedication in the process of writing it. The staff at the Economic Development Board contributed a significant amount of secretarial work. Staff researched the industry, created a comprehensive and relevant survey for local businesses and compiled the data for analysis. Special thanks to Colette Thomas for coordinating survey distribution and garnering its high response rate, and to Pam Gibson and K. Min Pease for editorial duties.