Embed Size (px)

Citation preview

Copyright © 2011, Oracle and/or its affiliates. All rights reserved.

Solvency II

September 2011

What is Solvency II?

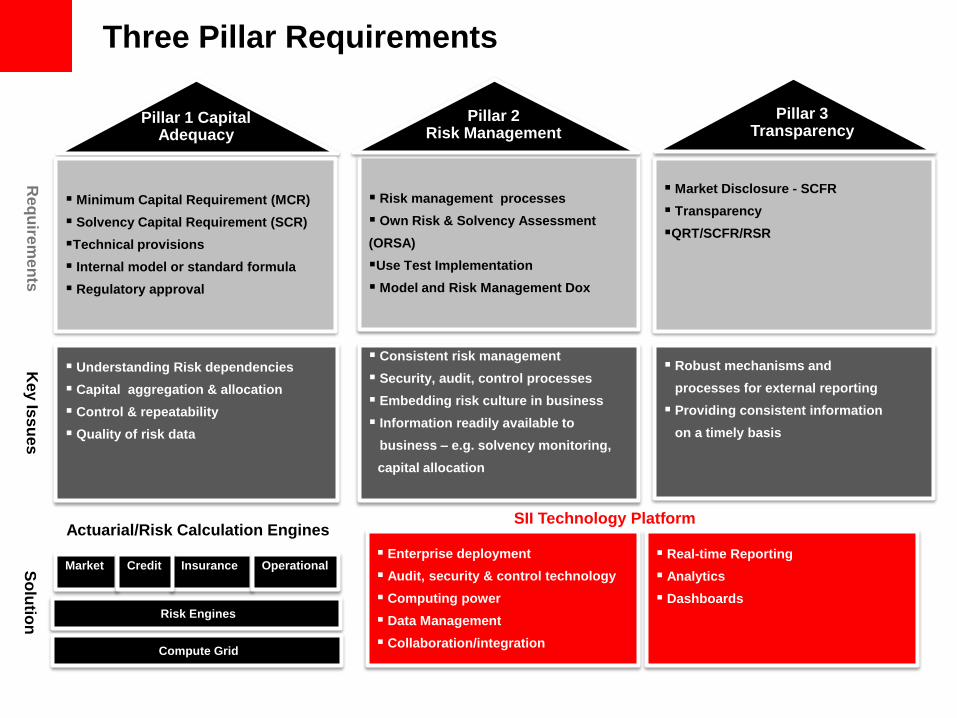

Three Pillars of Solvency II

SII Technology Platform Actuarial/Risk Calculation Engines

Req

uire

me

nts

S

olu

tion

K

ey Is

su

es

Minimum Capital Requirement (MCR)

Solvency Capital Requirement (SCR)

Technical provisions

Internal model or standard formula

Regulatory approval

Risk management processes

Own Risk & Solvency Assessment

(ORSA)

Use Test Implementation

Model and Risk Management Dox

Market Disclosure - SCFR

Transparency

QRT/SCFR/RSR

Understanding Risk dependencies

Capital aggregation & allocation

Control & repeatability

Quality of risk data

Consistent risk management

Security, audit, control processes

Embedding risk culture in business

Information readily available to

business – e.g. solvency monitoring,

capital allocation

Robust mechanisms and

processes for external reporting

Providing consistent information

on a timely basis

Enterprise deployment

Audit, security & control technology

Computing power

Data Management

Collaboration/integration

Real-time Reporting

Analytics

Dashboards

Three Pillar Requirements

Pillar 1 Capital Adequacy

Pillar 2 Risk Management

Pillar 3 Transparency

Risk Engines

Market Insurance Credit Operational

Compute Grid

4

Chief Actuary

Faster production of information in real

time

Graphical and analytical reports for the

regulators and the business

Sensitivity and what if analysis

Centralised and consistent modelling

platform for all actuarial users

Automated modeling processes

Audit & security controls for Models

and associated data

Chief Risk Officer

Internal model approval

Understanding of key assumptions

Risk calculations to accurately reflect

the underlying risk profile

Enterprise-wide consistent risk

management standards

Auditable and transparent modelling

and risk processes

Graphical and analytical reports for

the regulators and the business –

SCFR/RSR/QRT/ORSA

Chief Information Officer

Robust IT governance

Power to run complex models

Centralised modeling platform

based on enterprise technologies

Deployment across the enterprise

Seamless integration with other

enterprise systems and Automated

data extraction/ transformation

Centralised SII Database for

enterprise access

Chief Financial Officer

Consistency of external reporting

(e.g. IFRS, SII, MCEV)

Financial Consolidation - QRTs

Faster, controlled production of

accounting reports – e.g. inputs to

IFRS statements

Graphical and analytical reports for

the regulators and the business

Faster financial close

CA

CRO

CIO

CFO

CEO

Solvency II Programme

Enhanced business performance

through improved risk-based

decision making

Internal Stakeholder Requirements

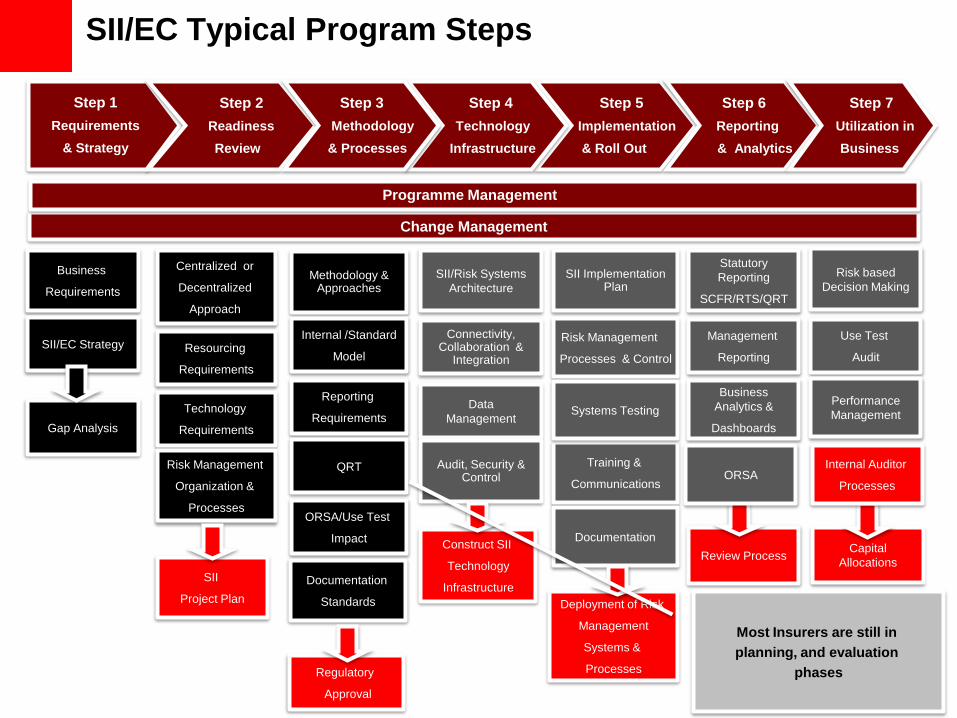

SII/EC Typical Program Steps

Business

Requirements

SII/EC Strategy

Gap Analysis

Centralized or

Decentralized

Approach

Resourcing

Requirements

Technology

Requirements

Risk Management

Organization &

Processes

SII

Project Plan

SII/Risk Systems

Architecture

Connectivity, Collaboration &

Integration

Data

Management

Audit, Security & Control

Construct SII

Technology

Infrastructure

SII Implementation Plan

Risk Management

Processes & Control

Deployment of Risk

Management

Systems &

Processes

Training &

Communications

Statutory

Reporting

SCFR/RTS/QRT

Management

Reporting

Business

Analytics &

Dashboards

Review Process

Methodology & Approaches

Internal /Standard

Model

Reporting

Requirements

ORSA/Use Test

Impact

Documentation

Standards

Risk based

Decision Making

Use Test

Audit

Performance

Management

Capital

Allocations

Step 5

Implementation

& Roll Out

Step 1

Requirements

& Strategy

Step 2

Readiness

Review

Step 4

Technology

Infrastructure

Step 6

Reporting

& Analytics

Step 3

Methodology

& Processes

Step 7

Utilization in

Business

Systems Testing

Documentation

Change Management

Programme Management

Regulatory

Approval

QRT Internal Auditor

Processes

Most Insurers are still in

planning, and evaluation

phases

ORSA

6 6

SII Programs – Key Issues with our Clients

QRT Process – Insurers have completed their QIS5 exercise and now the focus is

on the QRT Reporting Process and the associated SFCR/RSR processes. Key

focus on Regulatory Reporting

Data Quality – how do we ensure that the input data is consolidated, accurate and

validated ? Can we trust the data!

Use Test/ORSA Implementation – is the internal model genuinely important to the

business? Is it widely used in decision making? How do we demonstrate to the

regulators we are using the capital/risk information in business decision

making?

Actuarial/Risk Management Processes - do we actually have defined, controlled

and documented processes? How do we demonstrate full audit trail?

Spread Sheets - How do you reduce the dependency on Spread Sheets –

Insurers can have 100s of spread sheets that are difficult to audit & control

Auditability & Transparency - how do we audit, track and control our actuarial

and risk management processes? Particularly as most of the existing systems

are Desktop based

Documentation Standards – is there a proper documentation to describe the

models, the supporting processes and how is it kept up to date? Documentation is

a real issue

Pilla

r I P

illar s

II & III

Pilla

r s II/III

SII Program Phases

Pillar 1 Capital

Numbers &

Processes

IMAP Process

QRT/SFCR/RSR

Processes

Report Production

Regulatory Reporting/

IMAP Process

Phase 1 QRT/SFRC/RSR

Data Sources

Data ETL

Staging/Manual Input

Data Quality

Data Validation

Data Reconciliation

Data Quality to

support Pillar 1 &

Pillars II/III

Phase 2

Data Quality

SII Reporting Data

Risk Data

Finance Data

Actuarial Data

SII Data Mart

Phase 3

SII Mart

Capital/Risk

Information

Use Test Process

ORSA Process

Utilisation within the

Business

Phase 4

Use Test/ORSA

Fully Integrated Risk,

Finance and Actuarial

Data Warehouse

Solvency II Plus

Phase 5 Fully Integrated Repository

An Integrated Risk Repository will

typically be developed in stages

Pillar 1

Pillars 2/3

Actuarial

Operational Risk Finance Risk Management Process

Change Management Business Processes

Roles/Responsibilities Culture

Current Solvency II technology landscape

Traditional actuarial and risk systems are desktop oriented and

supplemented heavily with manual controls

Often insurers have multiple risk systems as a result of

multinational structures or M&A activity

These systems tend to lack enterprise capabilities making

security, auditability and control difficult

Risk data is collected from multiple sources and generally lacks

consistency, quality and controls

Reporting is split across multiple systems making it difficult to

aggregate risk information

Desktop computing power inhibits the ability to undertake frequent

and ever more complex actuarial/risk models

9

Case study of Actuarial Spaghetti!

Solvency II Projects

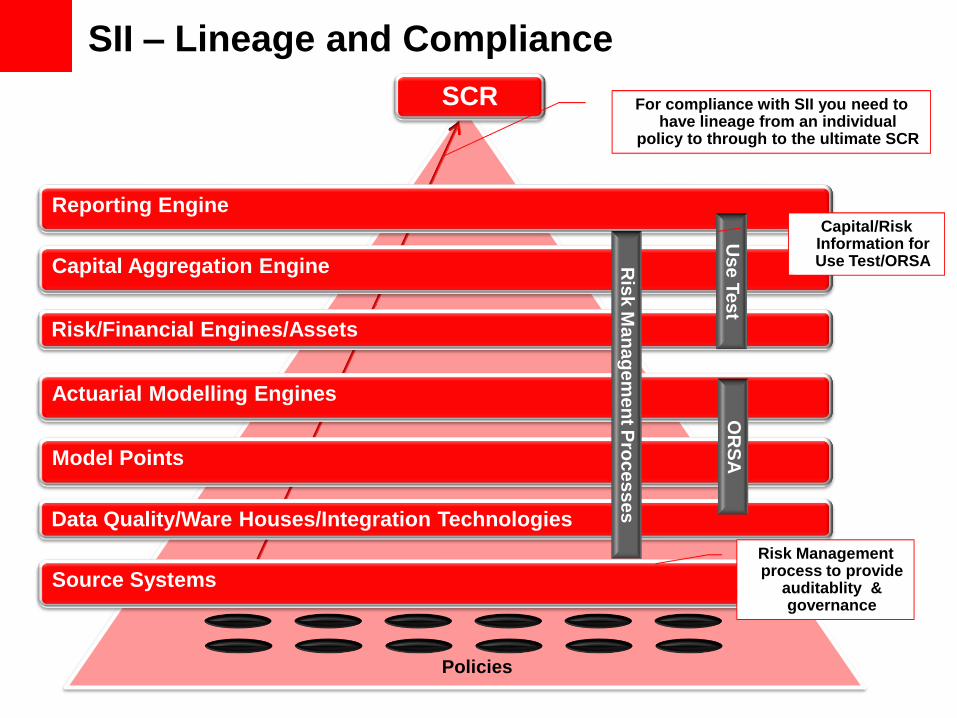

SII – Lineage and Compliance

SCR

Policies

For compliance with SII you need to have lineage from an individual

policy to through to the ultimate SCR

Reporting Engine

Capital Aggregation Engine

Actuarial Modelling Engines

Model Points

Risk/Financial Engines/Assets

Data Quality/Ware Houses/Integration Technologies

Source Systems

Ris

k M

an

ag

em

en

t Pro

ce

ss

es

Us

e T

es

t Capital/Risk

Information for Use Test/ORSA

OR

SA

Risk Management process to provide

auditablity & governance

Secrets of Success

There is no one-size fits all solution to Solvency II - no vendor has

one and no insurer would buy one!

Insurers already have a number of existing SII related components -

these will have to be integrated into any strategic SII framework

Plan strategically but implement in a phased manner delivering

defined functionality in other words identify a number of quick wins

Components must be capable of meeting both today's and

tomorrows requirements – they must be flexible – data model,

warehouse, reporting engine etc....

IT must work closely with Actuarial , Risk and Finance to

understand the business requirements

Ultimately business benefits have to be derived from a SII program

so plan for SII plus and finally ................................

IT represents 50% upwards of total SII Budget

<Insert Picture Here>

1. Stable, repeatable and robust technology platform for risk management

2. Full audit, security and control around risk systems

3. Version control and change management around risk models and process

4. Full documentation of risk models and associated risk management process

Wider CEIOPs Requirements

Oracle Solution

Typical SII Architecture

Repository

ETL/MDM

Source

Operational Data

Warehouses

Policy/Assets Data

Actuarial tables

External Data

Financial Data

Cash flow projection output

QIS5/QRT/SII Data

Aggregation, Analyses

Reconciliation

Policy Admin Systems

Claims

Asset Data

Risk

Bloomberg

3. Data Staging Area

4. SII Repository

ETL

2 . Manual

Data Entry

Data Quality

Process Flow

Automation

1. 1. Source

2. Systems

GLs

Reporting

BI Reporting & Analysis

7. Analytics

Monthly KPIs

Business Dashboards

Risk/Management

Regulatory

6. Pillar II Compliance

ORSA

Use Test

Calculation/Validation

Balance Sheet Forecasting

Financial Consolidation

Annual Reporting - QRTs

8. Actuarial Engines

Assets

LIFE

ALM

Economic Capital

5. Validation Engine

9. Financial Consolidation Engine

P&C

Operational Risk

10. Governance Risk & Compliance Systems – Risk Management Processes/Controls

Typical SII Architecture

Repository

ETL/MDM

Source

Operational Data

Warehouses

Policy/Assets Data

Actuarial tables

External Data

Financial Data

Cash flow projection output

QIS5/QRT/SII Data

Aggregation, Analyses

Reconciliation

Policy Admin Systems

Claims

Asset Data

Risk

Bloomberg

3. Data Staging Area

4. SII Repository

ETL

2 . Manual

Data Entry

Data Quality

Process Flow

Automation

1. 1. Source

2. Systems

GLs

Reporting

BI Reporting & Analysis

7. Analytics

Monthly KPIs

Business Dashboards

Risk/Management

Regulatory

6. Pillar II Compliance

ORSA

Use Test

Calculation/Validation

Balance Sheet Forecasting

Financial Consolidation

Annual Reporting

8. Actuarial Engines

Assets

LIFE

ALM

Economic Capital

5. Validation Engine

9. Financial Consolidation Engine

P&C

Operational Risk

10. Governance Risk & Compliance Systems – Risk Management Processes/Controls

2. Oracle HFM

Financial Consolidation

SII Reporting

XBRL

Audit & Security

Process Flows

1. Oracle OFFSA

Data Quality

Data ETL

Data Staging &Validation

Data Repository

Process Flows

Calculations & Aggregation

3. Oracle Analytics

SII Reporting

Dash Boards

KPIs

Integrated Risk, Actuarial

& Finance

Solvency II Plus

4. Oracle GRC

Risk Process definition

Risk Process flows & controls

Risk Reporting

QMR (SII Regulatory) Reporting Application

Using the HFM platform

What is QMR for SII? (Quantitative Management Reporting)

18

“Out of the Box” solution for SII reporting – QRTs, SFCR, RSR

Based on the existing Oracle financial consolidation engine – Hyperion Financial Management (HFM)

HFM comprises:

Powerful Financial Consolidation Engine with process flow controls (HFM)

Data Quality and Integration Tool (FDQM)

Reporting (Disclosure Management)

QMR is a dedicated application that operates with the HFM environment to specifically provide for QRT, SFCR,RSR functionality.

The QMR application will be maintained and developed by Oracle to keep pace with EIOPA regulations

All insurers need to capture QRT information from all their legal entities, reporting entities, branches or any other organisational structure of the respective insurer.

This is could be a violation of upcoming Solvency II reporting requirements (Pillar II) and will impose future liabilities regarding insurers filling Solvency II (based on further developments of QRT principles)

Many insurers are using manual Excel procedures to capture and consolidate information

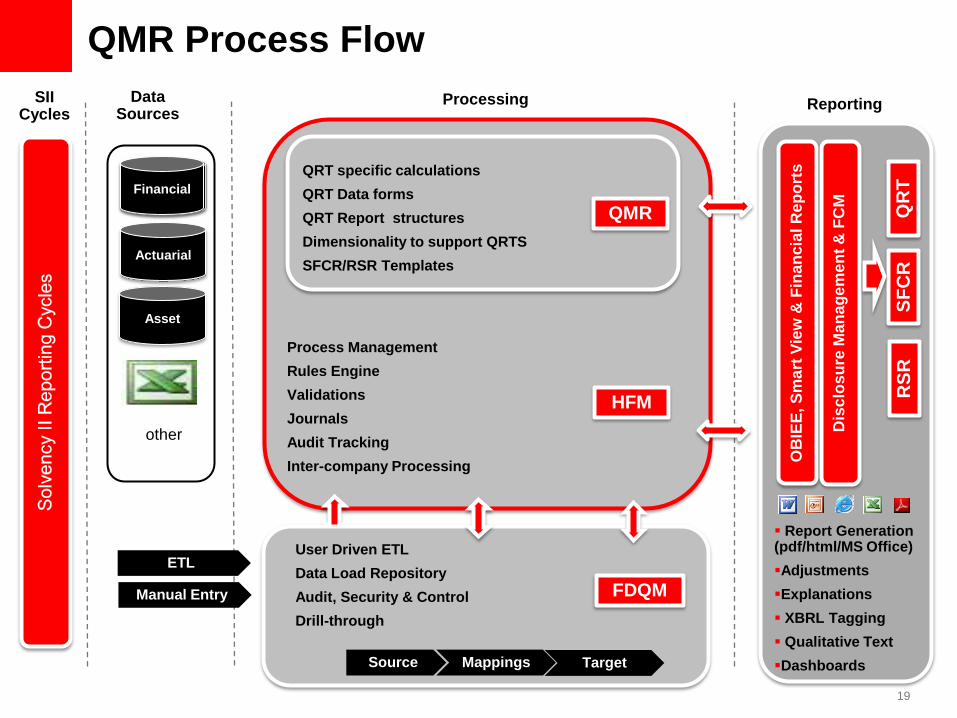

QMR Process Flow

19

Reporting

Financial

Actuarial

Asset

Financial

Data Sources

SII Cycles

Process Management

Rules Engine

Validations

Journals

Audit Tracking

Inter-company Processing

HFM

QRT specific calculations

QRT Data forms

QRT Report structures

Dimensionality to support QRTS

SFCR/RSR Templates

QMR

User Driven ETL

Data Load Repository

Audit, Security & Control

Drill-through

FDQM

Source Mappings Target

Processing

Manual Entry

ETL

Report Generation (pdf/html/MS Office)

Adjustments

Explanations

XBRL Tagging

Qualitative Text

Dashboards

OB

IEE

, S

ma

rt V

iew

& F

ina

ncia

l R

ep

ort

s

Dis

clo

su

re M

an

ag

em

en

t &

FC

M

QR

T

SF

CR

R

SR

other

QMR Application within HFM

Pre-Built application that supports (both independently and in conjunction with

Oracle S-II Repository) the generation of the QRT reporting requirements as

prescribed by the European Insurance regulators (EIOPA) for both for solo

and group reporting

Incorporates calculations for SCR/MCR and Diversification calculations

Our approach and release management will support future upgrades in the

underlying platform (HFM) and future regulations – e.g. QRTs/

SFCRs/RSRs….

QMR supports both Life, Non-life business and composite Insurers

Capability for the customisation of QRT templates (for local regulator

requirements) and generation of user specific templates

QRT specific calculations

QRT Data forms

QRT Reports

Dimensionality to support QRTS

SFCR/RSR Templates

QMR

XBRL Taxonomy

21

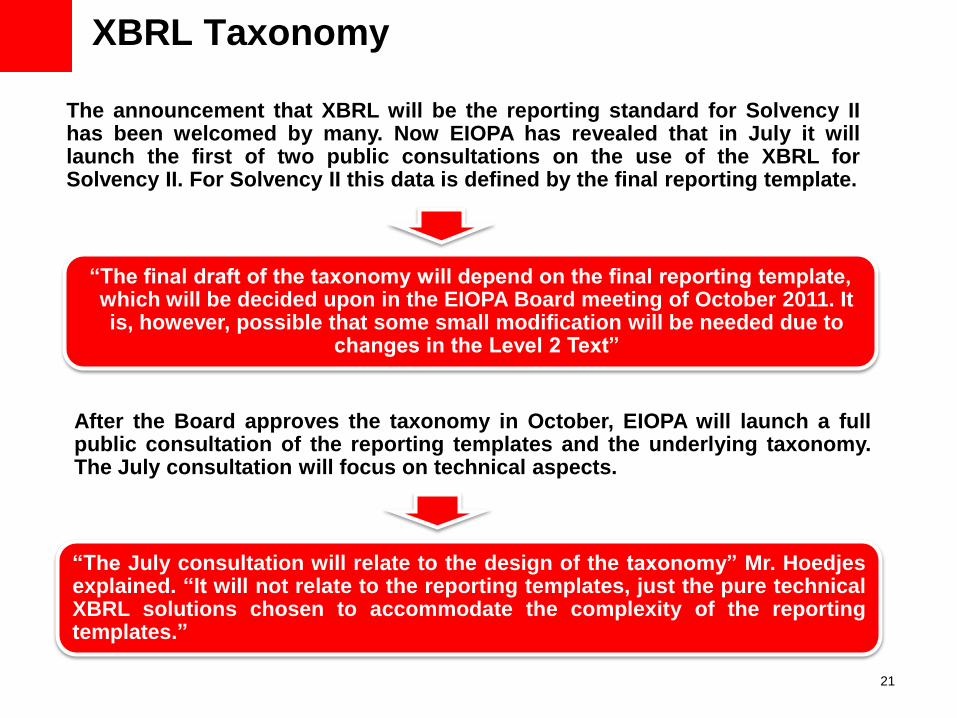

The announcement that XBRL will be the reporting standard for Solvency II has been welcomed by many. Now EIOPA has revealed that in July it will launch the first of two public consultations on the use of the XBRL for Solvency II. For Solvency II this data is defined by the final reporting template.

After the Board approves the taxonomy in October, EIOPA will launch a full public consultation of the reporting templates and the underlying taxonomy. The July consultation will focus on technical aspects.

“The final draft of the taxonomy will depend on the final reporting template, which will be decided upon in the EIOPA Board meeting of October 2011. It is, however, possible that some small modification will be needed due to

changes in the Level 2 Text”

“The July consultation will relate to the design of the taxonomy” Mr. Hoedjes explained. “It will not relate to the reporting templates, just the pure technical XBRL solutions chosen to accommodate the complexity of the reporting templates.”

Benefits of QMR

HFM/QMR

5. More than just a reporting solution – it provides essential capabilities for Pillar 2/3 SII controls:

Data Quality, Auditabilty, ETL

Validations and Calculation capabilities

Embedded process flows with inbuilt approvals and signs-off procedures

Support for Internal and Standard Models

2. Fully supported and maintained by Oracle with a discounted “bundled price” for SII reporting

1. “Out of the Box” solution for QRT- Specially bundled package of HFM/QMR for SII reporting

3. Fully customisable to an insurers specific legal structures, regulatory environment and internal requirements

4. Relatively quick implementation process – estimated 3-4 months to support SII reporting - can be quicker in a existing HFM client

EIOPA QRT Templates

23

Template

Content

S G QS IAG DS DG

BS - C1 Balance sheet X X Tbd Tbd X X

BS - C1B Off-balance sheet items X X X X X X

BS - C1D Assets and liabilities by currency X X

OF - B1A Own funds - Annual X X X X

OF - B1Q Own funds - Quarterly X X X X

SCR - B2A Solvency capital requirement (for undertaking on standard formula or partial internal model)

X X X X SCR - B2B Solvency capital requirement (for undertakings on partial internal models)

SCR - B2C Solvency capital requirement (for undertaking on full internal models)

SCR - B3A Solvency capital requirement - market risk X X

SCR - B3B Solvency capital requirement - counterparty risk5 X X

SCR - B3C Solvency capital requirement - life underwriting risk5 X X

SCR - B3D Solvency capital requirement - health underwriting risk5 X X

SCR - B3E Solvency capital requirement - non-life underwriting risk5 X X

SCR - B3F Solvency capital requirement - non-life catastrophe risk5 X X

SCR - B3G Solvency capital requirement - operational risk5 X X

MCR - B4A Minimum capital requirement (except for composite undertakings)

X X X

MCR - B4B Minimum capital requirement (for composite insurance undertakings)

Oracle - SII Reporting Pack

Solvency II – Repository

Asset Data

External Data

Reporting Data

Financial Data

Portfolio, Asset Types, Duration ,QRT inputs etc

Balance Sheet, P&L, IFRS, GAAP

ESG files, Catastrophe Models, Reuters, Bloomberg etc

QRTs, SFCR, RSR, MVEV, IFRS etc...

Capital Aggregation Inputs/Results

(Algo- Risk, Ortec)

Actuarial Results Files, Risk Factors, Asset Data (super-set). Results – Curve Fitting, Replicating Portfolios

Actuarial Modelling Input Data

(MoSes, Profit, Igloo, ReMetrica, Mo.Net)

Actuarial Modelling Results Data

(MoSes, Profit, Igloo, ReMetrica, Mo.Net)

Assumptions Tables, Yield Tables, Mortality Tables, Run Parameters, Policy Data

Results Files, Cash Flows etc..........

SCR

Solvency II – Reporting

Statutory/SII

SCR

QIS5, QRT, SFCR, RSR ORSA, Use Test

Management Reports/Dashboards

Executive

Management/Business Information

SCR Projection/SCR Breaches/SCR Breakdown

Risk Management Risk Factors/Capital/Risk Analysis/Geographies

Asset Management Asset Mix/Asset Durations/Intangible Assets

Actuarial Shocks/SCR Scenarios/Sensitivity Analyses

Finance

Ad Hoc Reports

Operating Expenses/Income, Claims Analysis, Liquidity, Key Ratios, Capital Adequacy etc

Executive Economic Capital/KPIs/SCR

Executive Reports

Risk Adjusted Return on Capital

Group SCR

Reconciliation of ECaR

SCR by Line of Business

Examples Solvency II

Dashboards

Executive

Dashboards Answers More Products

Settings

Log Out

Executive Reports

SCR Development

Key Indicators

SCR Minimum Values

SCR Decomposition

Examples Solvency II

Dashboards

Executive

Dashboards Answers More Products

Settings

Log Out

0,00

50,00

100,00

150,00

2010 2011 212 2013

Tier 3

0

10

20

30

40

50

60

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

2010 2011 212 2013

TIer1

tier3

Tier 2

Tier 1 scr req (1/3)

scr

0,00

0,50

1,00

1,50

2,00

2,50

2009 2010 2011 2012 Goal

tier2+tier3/tier1

min 2

0,00

0,10

0,20

0,30

0,40

0,50

0,60

2009 2010 2011 2012 Goal

tier 3/ tier

1+ tier 2

breach .5

0

1000

2000

3000

4000

5000

0

1

2

3

4

5

6

7

8

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

SCR

Yield

Linear (SCR)

Linear (Yield)

Risk Reports

SCR by Region

SCR Breach Level

Risk Factors over Time

MCR Breach Level

Examples Solvency II

Dashboards

Executive

Dashboards Answers More Products

Settings

Log Out

Actuarial Reports

SCR Killer Scenarios

Impact of the 26 EIOPA Shocks

Internal v Standard Models

Impact of the 26 EIOPA Shocks – Projected Forward

Examples Solvency II

Dashboards

Executive

Dashboards Answers More Products

Settings

Log Out

SII is spreading around the globe

South Africa is adopting a SII

regime by 2014

Australia is also considering an

SII regime

USA currently has Principal Based

Approach regulation but

likely to move to SII regime in a few

years

Japan is adopting an SII

type regime

Israel is considering SII

type regime Mexico is adopting SII

Equivalence for 2012

32

Rating Agencies have similar requirements…

“All insurers will need to have at a strong enterprise risk

management assessment before we will consider

undertaking an Economic Capital Review”

These insurers will have demonstrated to us that their

Economic Capital Model (e.g. Internal Model) is an integral

part of the way in which they manage their business and

thus will tend to have better and more robust models

It is important that management relies on the ECM as a

key management tool and not just as a determinate of

capital adequacy

Source S&P