Embed Size (px)

Citation preview

February 4, 2014

6th Auto Trade Dialogue

SIAM Society of Indian Automobile Manufacturers

SIAM SIAM

•Indian Automobile Industry

•Current market conditions

•Taxation

•Trade Agreements

•Environment Policies

•Safety

SIAM SIAM

•Indian Automobile Industry

•Current market conditions

•Taxation

•Trade Agreements

•Environment Policies

•Safety

SIAM SIAM

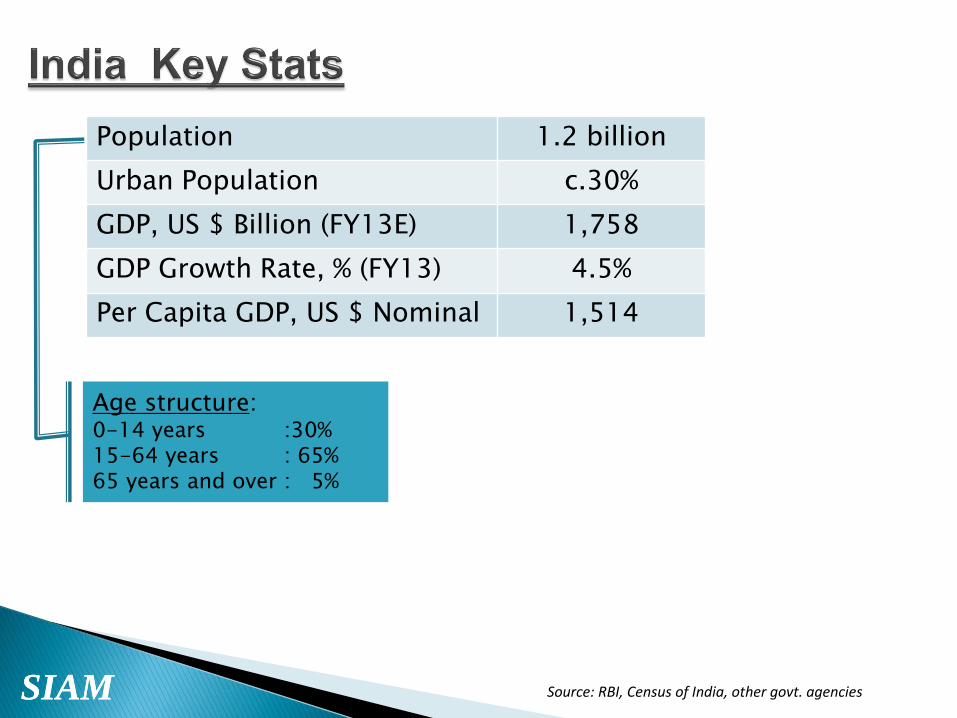

Population 1.2 billion

Urban Population c.30%

GDP, US $ Billion (FY13E) 1,758

GDP Growth Rate, % (FY13) 4.5%

Per Capita GDP, US $ Nominal 1,514

Source: RBI, Census of India, other govt. agencies

Age structure: 0-14 years :30% 15-64 years : 65% 65 years and over : 5%

SIAM SIAM

Source: CRISIL Research

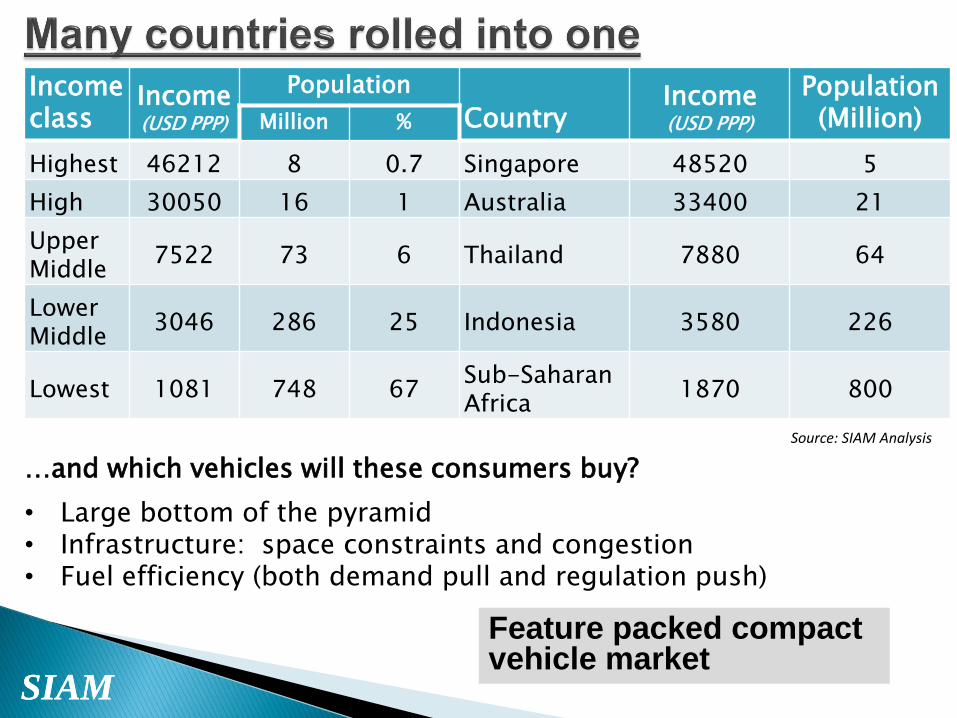

Income class

Income (USD PPP)

Population

Country Income (USD PPP)

Population (Million) Million %

Highest 46212 8 0.7 Singapore 48520 5

High 30050 16 1 Australia 33400 21

Upper Middle

7522 73 6 Thailand 7880 64

Lower Middle

3046 286 25 Indonesia 3580 226

Lowest 1081 748 67 Sub-Saharan Africa

1870 800

…and which vehicles will these consumers buy?

Feature packed compact vehicle market

• Large bottom of the pyramid • Infrastructure: space constraints and congestion • Fuel efficiency (both demand pull and regulation push)

Source: SIAM Analysis

SIAM SIAM

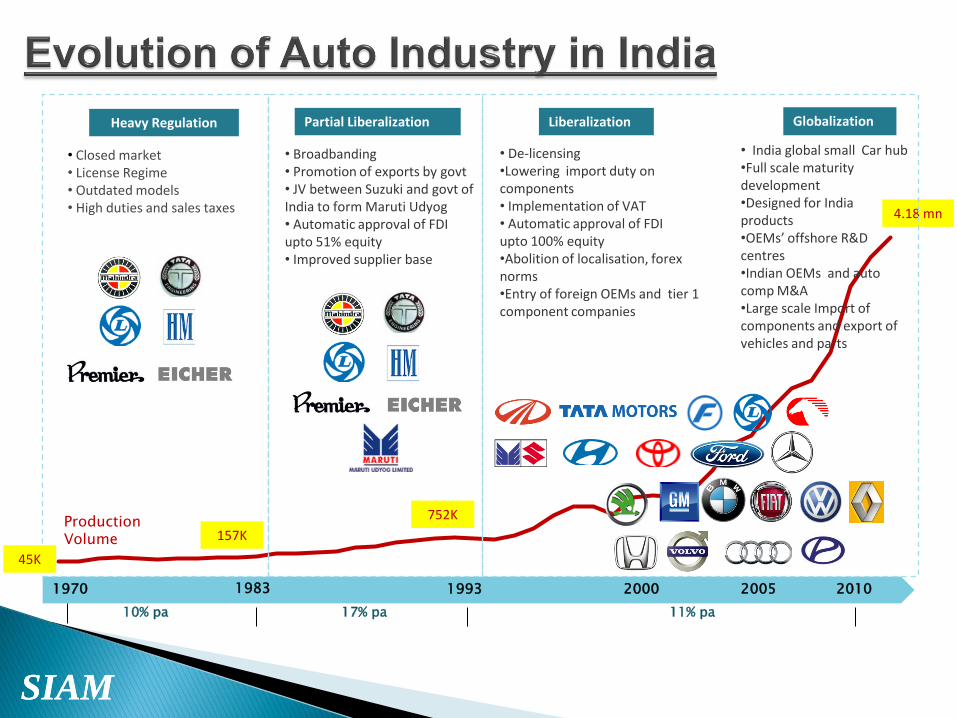

Heavy Regulation Partial Liberalization Liberalization Globalization

• Closed market • License Regime • Outdated models • High duties and sales taxes

• Broadbanding • Promotion of exports by govt • JV between Suzuki and govt of India to form Maruti Udyog • Automatic approval of FDI upto 51% equity • Improved supplier base

• India global small Car hub •Full scale maturity development •Designed for India products •OEMs’ offshore R&D centres •Indian OEMs and auto comp M&A •Large scale Import of components and export of vehicles and parts

• De-licensing •Lowering import duty on components • Implementation of VAT • Automatic approval of FDI upto 100% equity •Abolition of localisation, forex norms •Entry of foreign OEMs and tier 1 component companies

Production Volume

4.18 mn

1970 1983 1993 2000 2005 2010

45K

157K

752K

10% pa 17% pa 11% pa

SIAM

SIAM SIAM

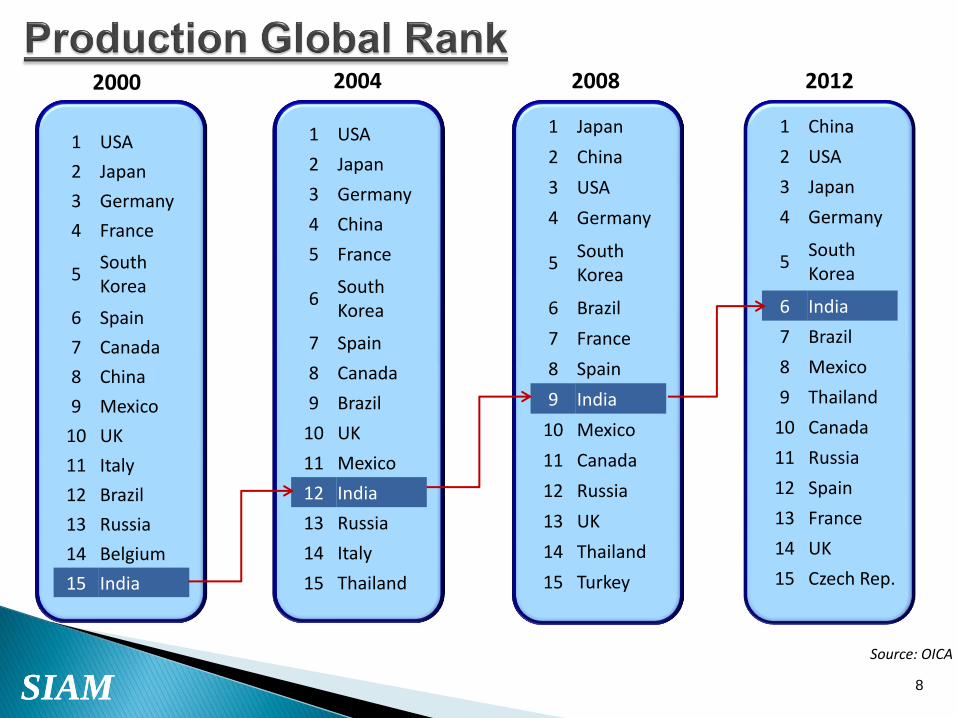

1 USA

2 Japan

3 Germany

4 China

5 France

6 South Korea

7 Spain

8 Canada

9 Brazil

10 UK

11 Mexico

12 India

13 Russia

14 Italy

15 Thailand

1 Japan

2 China

3 USA

4 Germany

5 South Korea

6 Brazil

7 France

8 Spain

9 India

10 Mexico

11 Canada

12 Russia

13 UK

14 Thailand

15 Turkey

1 China

2 USA

3 Japan

4 Germany

5 South Korea

6 India

7 Brazil

8 Mexico

9 Thailand

10 Canada

11 Russia

12 Spain

13 France

14 UK

15 Czech Rep.

8

1 USA

2 Japan

3 Germany

4 France

5 South Korea

6 Spain

7 Canada

8 China

9 Mexico

10 UK

11 Italy

12 Brazil

13 Russia

14 Belgium

15 India

2000 2004 2008 2012

Source: OICA

SIAM SIAM

Auto Policy 2002 ◦ Focus on small cars and utility

vehicles

◦ Promotion of R&D

◦ Impetus to Alternative Fuel Vehicles

◦ Lower emissions using improved vehicle technology, improved fuel quality and Parc modernisation

◦ Automatic approval for 100% FDI; no minimum investment criteria

9

Automotive Mission Plan 2006-16

◦ Infrastructure

◦ Promote brand India

◦ Favorable business environment

◦ Attract investment

◦ Promote R&D

◦ Upgrade quality standards

◦ Upgrade manufacturing technology

◦ Cost competitiveness

◦ Develop R&D capability

◦ Target overseas markets

$145 bn by FY16 &

10% of GDP

$34 bn In

FY07

SIAM

Will fall short of vision target due to implementation and slowdown

SIAM SIAM

• ~ 7% of GDP

• ~ 22% of Manufacturing GDP

Contribution to economy

• Total 1.1 mn

• 0.2mn OEMs

• 0.5mn Auto-Component Companies

• 0.4mn Service Network

Employment

• ~ USD 8 bn or Rs. 39 bn

• 4.3% of total FDI in India

FDI

(Apr-2000 to Apr-2013)

• ~USD 80bn Industry Turnover

Source: SIAM

SIAM SIAM

Countries Cars/1000

pop CVs/1000 pop 2W/1000 pop

Germany 518 36 72

Japan 457 121 98

Indonesia 45 33 216

India 16 5 85

Thailand 68 86 248

China 39 32 74

US 382 388 25

Note: India data is based on 2012, but data for other countries from Wards vehicle population data 2010.

Source: SIAM, Ward’s Auto

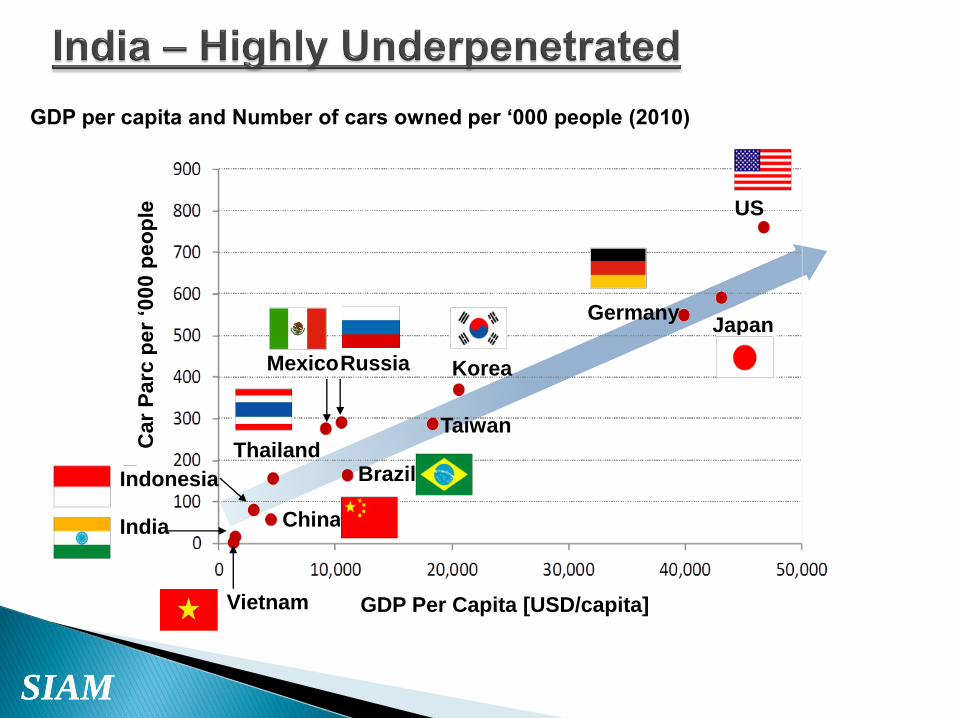

SIAM SIAM

GDP per capita and Number of cars owned per ‘000 people (2010)

Germany

US

Taiwan

Russia Mexico

Brazil Thailand

China

Indonesia

India

Vietnam

Korea

Japan

Car

Parc

per

‘000 p

eo

ple

GDP Per Capita [USD/capita]

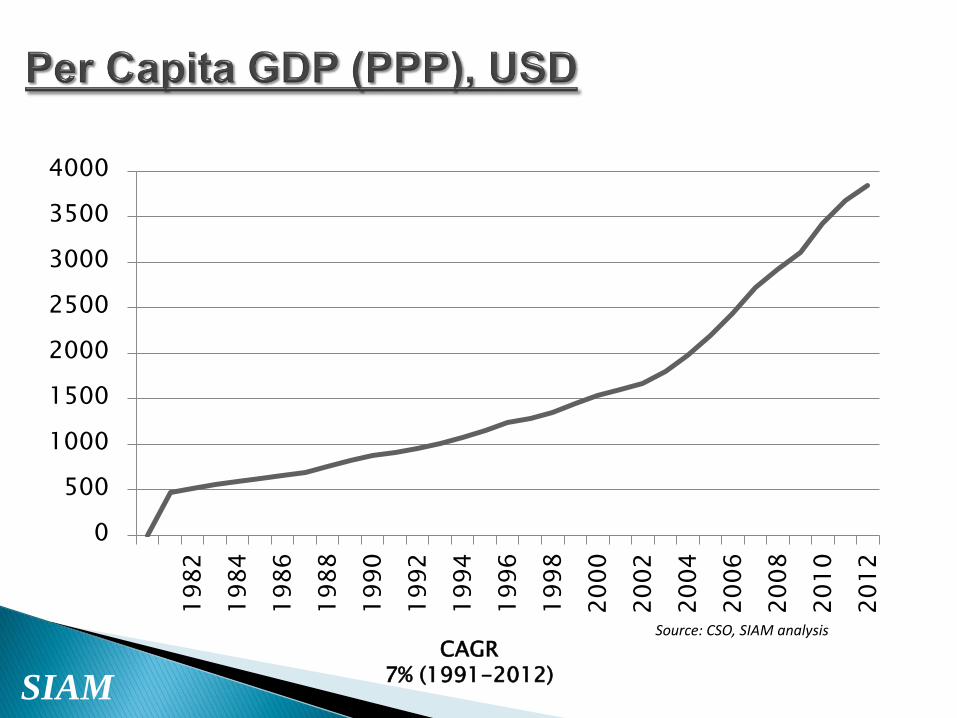

SIAM

CAGR 7% (1991-2012)

0

500

1000

1500

2000

2500

3000

3500

4000 1

98

2

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

Source: CSO, SIAM analysis

SIAM SIAM

•Indian Automobile Industry

•Current market conditions

•Taxation

•Trade Agreements

•Environment Policies

•Safety

SIAM SIAM

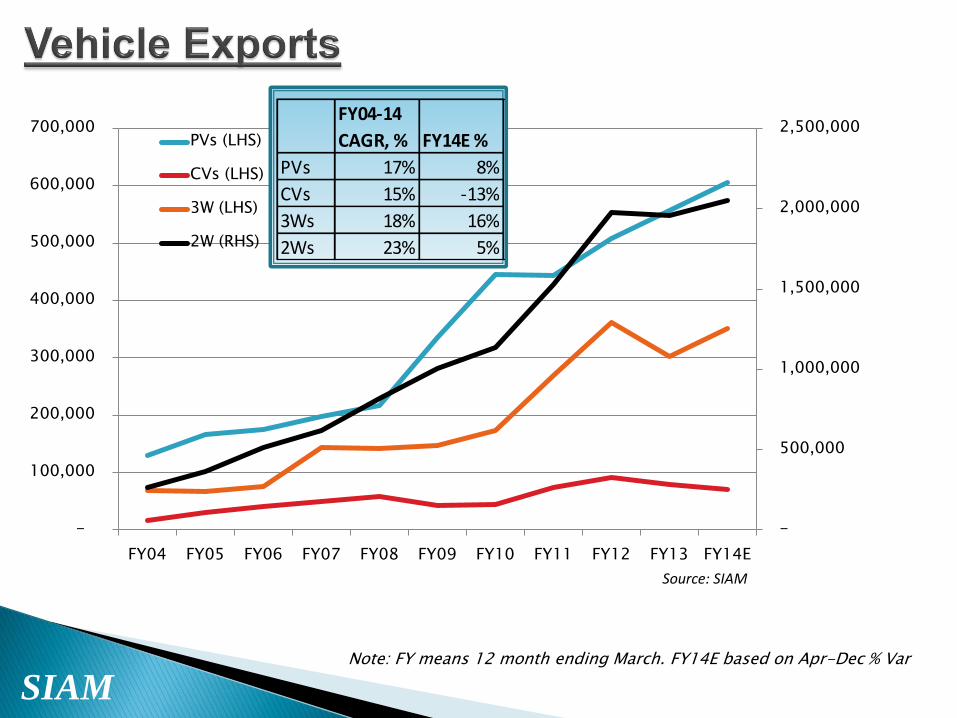

Source: SIAM, OICA

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14E

PVs (LHS)

CVs (LHS)

3W (LHS)

2W (RHS)

Note: FY means 12 month ending March. FY14E based on Apr-Dec % Var

FY04-14

CAGR, % FY14E %

Global

Rank

PVs 11% -5.8% 6

CVs 10% -18.4% 5

3Ws 6% -9.3% 1

2Ws 10% 5.4% 2

SIAM

Source: SIAM

Note: FY means 12 month ending March. FY14E based on Apr-Dec % Var

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14E

PVs (LHS)

CVs (LHS)

3W (LHS)

2W (RHS)

FY04-14

CAGR, % FY14E %

PVs 17% 8%

CVs 15% -13%

3Ws 18% 16%

2Ws 23% 5%

SIAM SIAM

% GDP growth – Showing some improvement now

7.3%

9.4%

5.3%

4.7% 4.4%

4.8%

4%

5%

6%

7%

8%

9%

10%

F10-Q

2

F10-Q

3

F10-Q

4

F11-Q

1

F11-Q

2

F11-Q

3

F11-Q

4

F12-Q

1

F12-Q

2

F12-Q

3

F12-Q

4

F13-Q

1

F13-Q

2

F13-Q

3

F13-Q

4

F14-Q

1

F14-Q

2

Source: CSO

SIAM SIAM

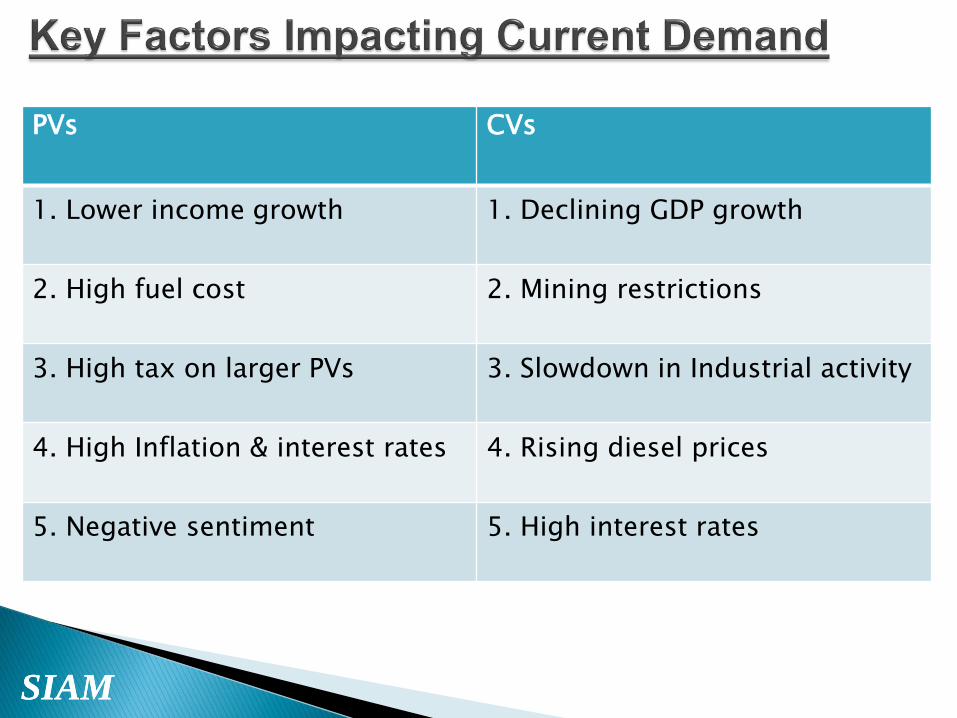

PVs CVs

1. Lower income growth

1. Declining GDP growth

2. High fuel cost

2. Mining restrictions

3. High tax on larger PVs

3. Slowdown in Industrial activity

4. High Inflation & interest rates

4. Rising diesel prices

5. Negative sentiment

5. High interest rates

SIAM SIAM

•Indian Automobile Industry

•Current market conditions

•Taxation

•Trade Agreements

•Environment Policies

•Safety

SIAM SIAM

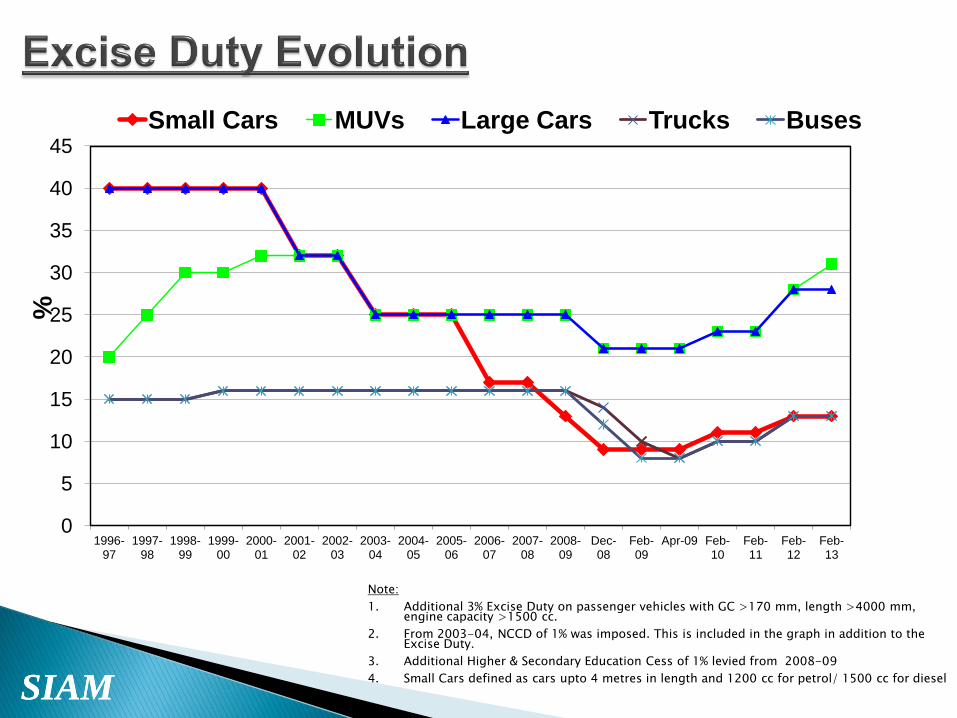

0

5

10

15

20

25

30

35

40

45

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

Dec-08

Feb-09

Apr-09 Feb-10

Feb-11

Feb-12

Feb-13

%

Small Cars MUVs Large Cars Trucks Buses

Note:

1. Additional 3% Excise Duty on passenger vehicles with GC >170 mm, length >4000 mm, engine capacity >1500 cc.

2. From 2003-04, NCCD of 1% was imposed. This is included in the graph in addition to the Excise Duty.

3. Additional Higher & Secondary Education Cess of 1% levied from 2008-09

4. Small Cars defined as cars upto 4 metres in length and 1200 cc for petrol/ 1500 cc for diesel

SIAM 21

Vehicle Category Current Excise Duty

Passenger Vehicles 12-30%

L<4m, 1.2L P, 1.5L D (Small cars ) 12%

L >4m but <1.5 L 24%

L>4m but > 1.5L 27%

MUVs/SUVs/Double Cab 30%

Hybrid cars 12%

Two wheelers 12%

Electric cars, 2W & 3W 6%

Commercial Vehicles 12%

Three wheelers 12%

SIAM SIAM

Tax Category Rate

R & D Cess 0.125%

Education Cess 3% (of excise)

National Calamity Contingent Duty 1%

Central Sales Tax (CST) for out of state

sale

2%

State Value Added Tax (VAT) 12.5%

Octroi (in one state only) 4%

State Road/Registeration Tax 4-21%

SIAM SIAM

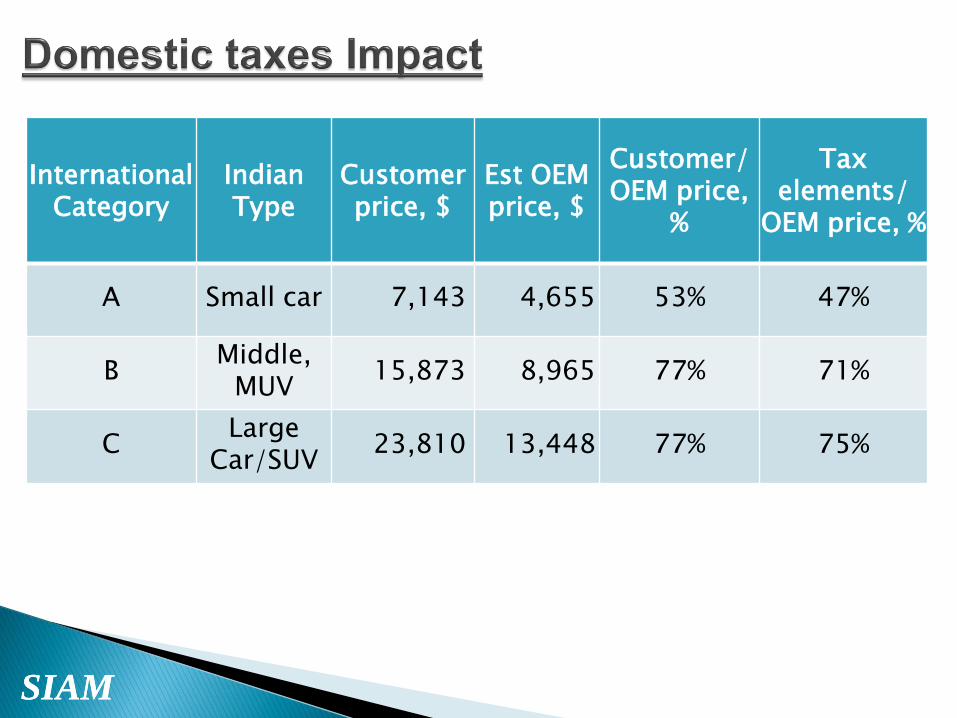

International Category

Indian Type

Customer price, $

Est OEM price, $

Customer/OEM price,

%

Tax elements/

OEM price, %

A Small car 7,143 4,655 53% 47%

B Middle,

MUV 15,873 8,965 77% 71%

C Large

Car/SUV 23,810 13,448 77% 75%

SIAM SIAM

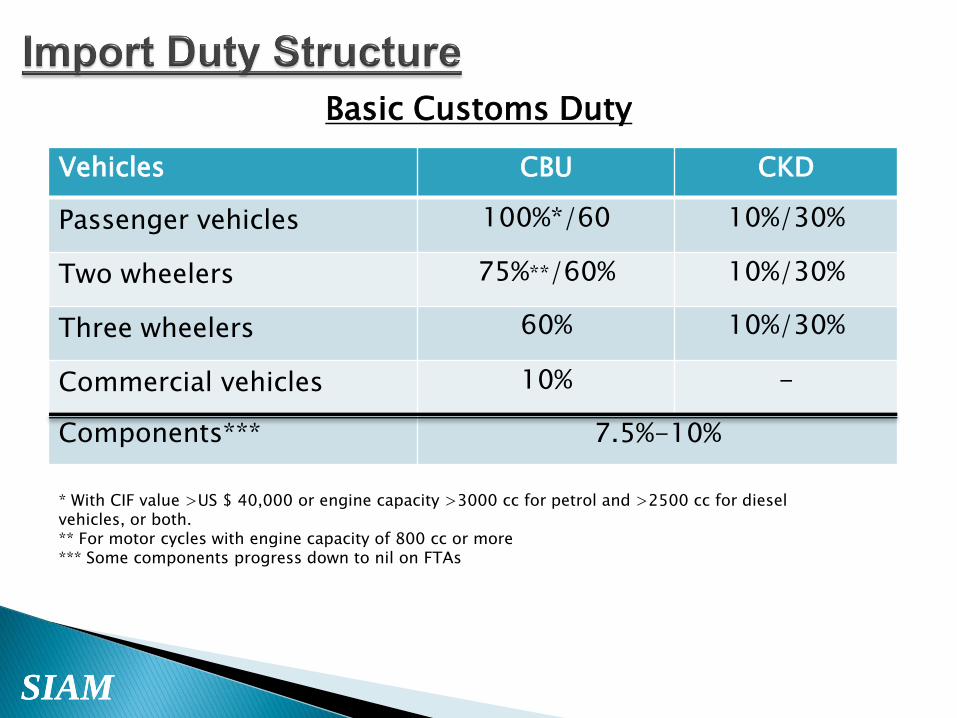

Vehicles CBU CKD

Passenger vehicles 100%*/60 10%/30%

Two wheelers 75%**/60% 10%/30%

Three wheelers 60% 10%/30%

Commercial vehicles 10% -

Components*** 7.5%-10%

Basic Customs Duty

* With CIF value >US $ 40,000 or engine capacity >3000 cc for petrol and >2500 cc for diesel vehicles, or both. ** For motor cycles with engine capacity of 800 cc or more *** Some components progress down to nil on FTAs

SIAM SIAM

Tax Category Rate

Education Cess 3% of tax

National Calamity Contingent Duty 1%

Countervailing Duty (CVD) Equivalent to excise duty

Special CVD 4%

SIAM SIAM

•Indian Automobile Industry

•Current market conditions

•Taxation

•Trade Agreements

•Environment Policies

•Safety

SIAM SIAM

WTO compliant policies

◦ No restrictions on import- no Quantitative Restrictions

◦ No localisation requirements

◦ No R&D requirement

◦ 100% FDI allowed

◦ <=10% tariffs except for PV, 2W/3W CBUs

◦ No differentiation in domestic taxation for imports

◦ Conditions of import – Emission & Safety norms as

applicable to domestic companies

Joined UN-ECE WP 29 for global standard in technology

and signed the 1998 Agreement

Increased engagements in Free Trade Agreements with

sensitivities on CBUs

SIAM

SIAM SIAM

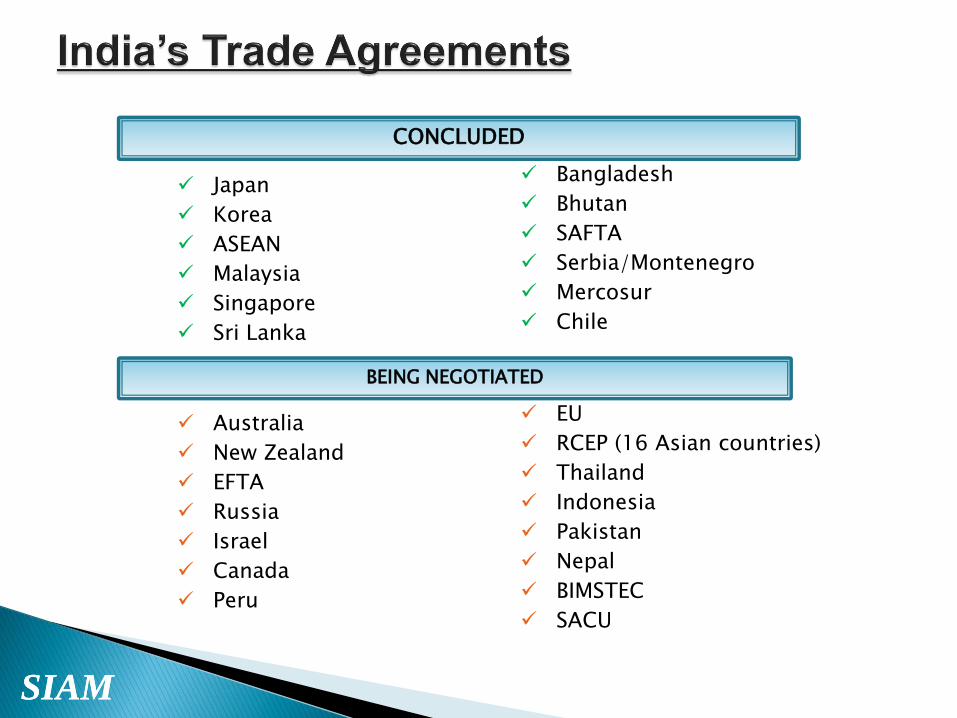

CONCLUDED

BEING NEGOTIATED

Japan

Korea

ASEAN

Malaysia

Singapore

Sri Lanka

Australia

New Zealand

EFTA

Russia

Israel

Canada

Peru

Bangladesh

Bhutan

SAFTA

Serbia/Montenegro

Mercosur

Chile

EU

RCEP (16 Asian countries)

Thailand

Indonesia

Pakistan

Nepal

BIMSTEC

SACU

SIAM SIAM

•Indian Automobile Industry

•Current market conditions

•Taxation

•Trade Agreements

•Environment Policies

•Safety

SIAM SIAM

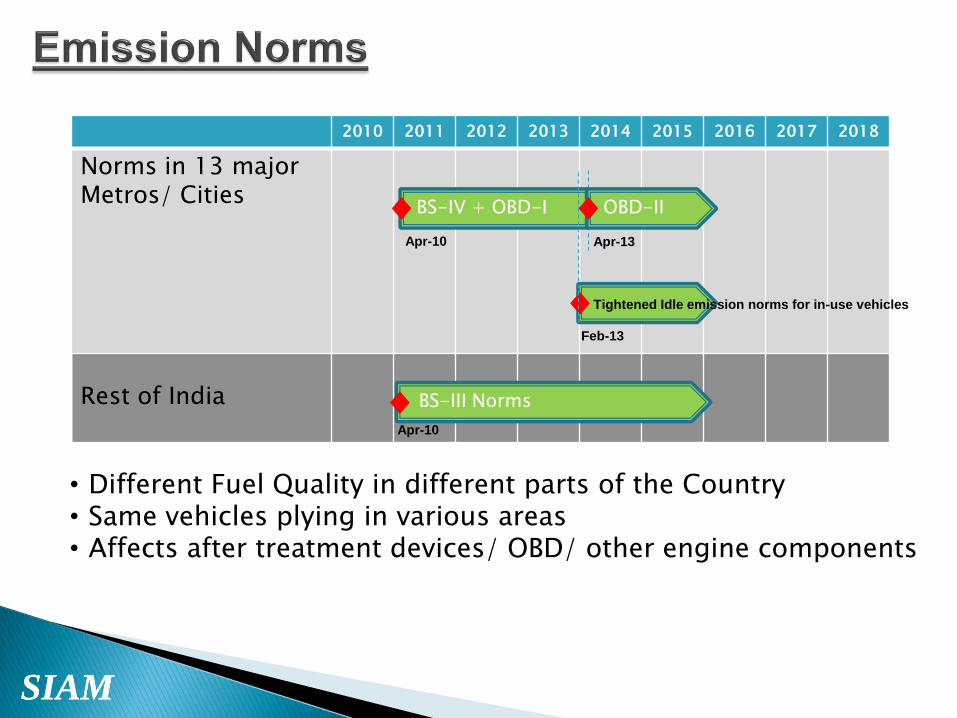

2010 2011 2012 2013 2014 2015 2016 2017 2018

Norms in 13 major Metros/ Cities

Rest of India

BS-IV + OBD-I

BS-III Norms

• Different Fuel Quality in different parts of the Country • Same vehicles plying in various areas • Affects after treatment devices/ OBD/ other engine components

OBD-II

Tightened Idle emission norms for in-use vehicles

Apr-10

Apr-10

Feb-13

Apr-13

SIAM SIAM

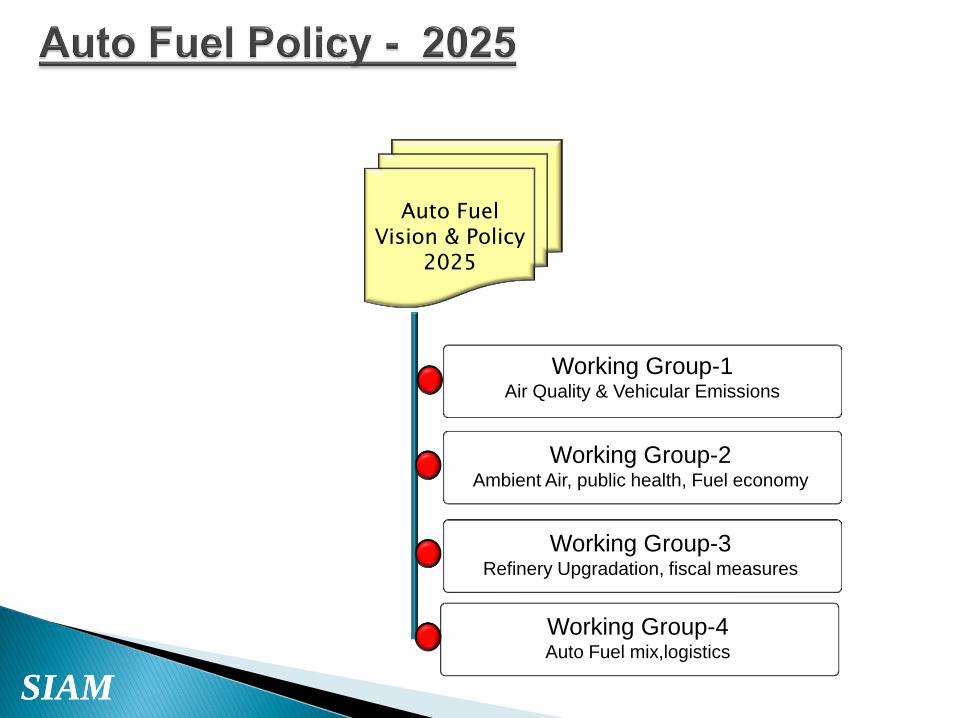

Auto Fuel Vision & Policy

2025

Working Group-1 Air Quality & Vehicular Emissions

Working Group-2 Ambient Air, public health, Fuel economy

Working Group-3 Refinery Upgradation, fiscal measures

Working Group-4 Auto Fuel mix,logistics

SIAM SIAM

•Indian Automobile Industry

•Current market conditions

•Taxation

•Trade Agreements

•Environment Policies

•Safety

SIAM SIAM

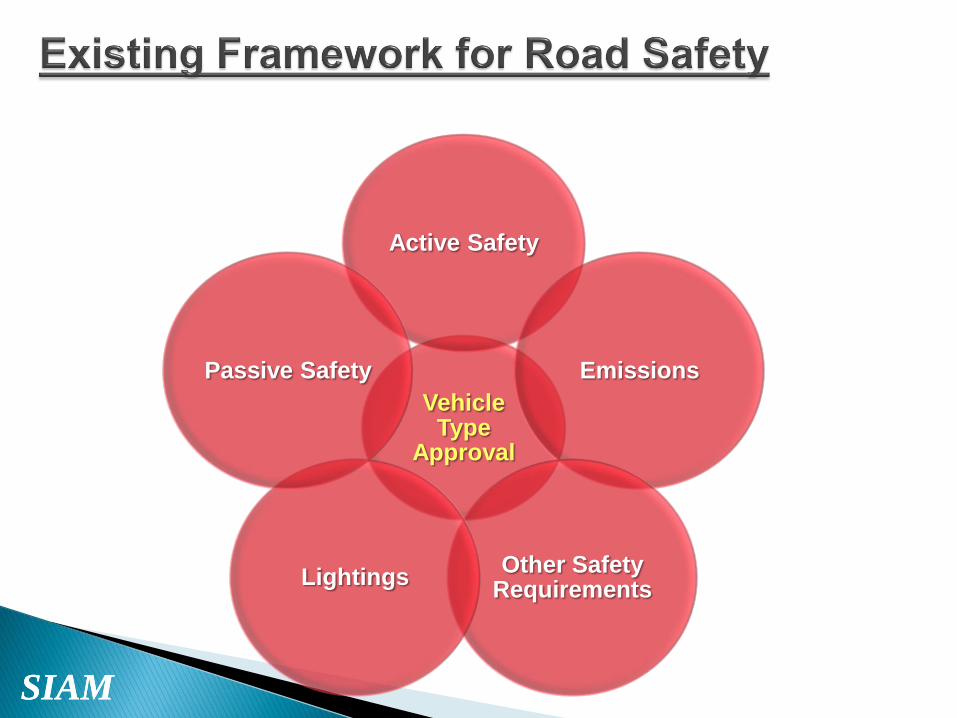

Vehicle Type

Approval

Active Safety

Emissions

Other Safety Requirements

Lightings

Passive Safety

SIAM SIAM

No of road accidents/100,000 people

No of accidents/10,000 vehicles

Source: MoRTH

SIAM SIAM

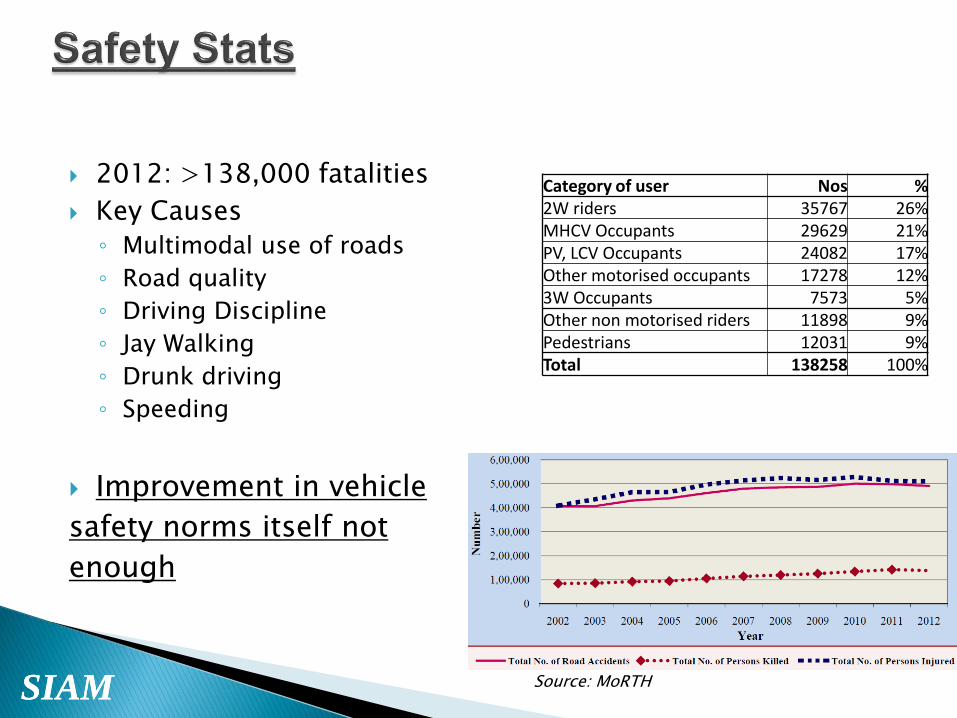

2012: >138,000 fatalities

Key Causes

◦ Multimodal use of roads

◦ Road quality

◦ Driving Discipline

◦ Jay Walking

◦ Drunk driving

◦ Speeding

Improvement in vehicle

safety norms itself not

enough

Source: MoRTH

Category of user Nos % 2W riders 35767 26% MHCV Occupants 29629 21% PV, LCV Occupants 24082 17% Other motorised occupants 17278 12% 3W Occupants 7573 5% Other non motorised riders 11898 9% Pedestrians 12031 9% Total 138258 100%

SIAM SIAM

Auto industry key component of Indian economy- both co-dependant

Notwithstanding current weakness, arguably the most promising market globally

Potential dependant on ◦ Implementation of auto policy

◦ Move to GST & rationalisation of taxation

◦ Investment in infrastructure

◦ Improvement in road safety measures & I&M regimes

SIAM SIAM