Embed Size (px)

Citation preview

ww

Smart Campaign Certi�cation Standards January 2013

Client Protection Certi�cation standards describe where the micro�nance industry sets the bar in terms of client protection. To be Certi�ed, a �nancial institution (FI) needs to comply with the indicators corresponding to the following 30 adequate standards of care for client protection.

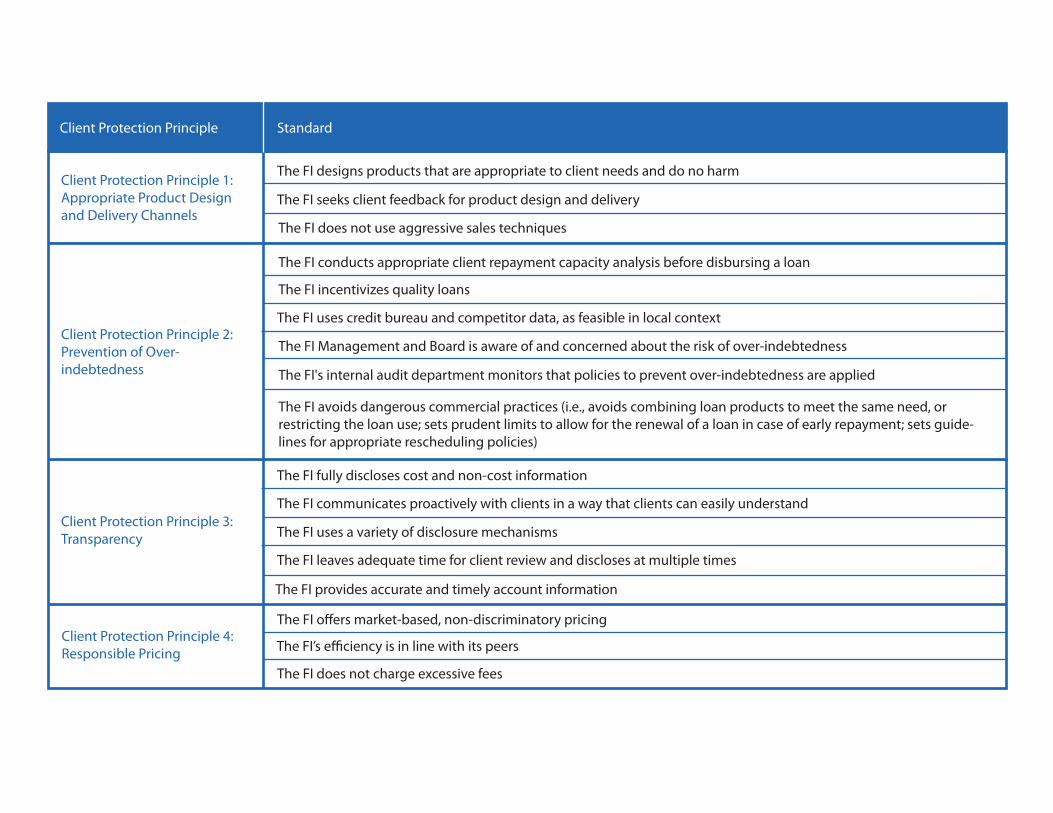

Client Protection Principle Standard

Client Protection Principle 1: Appropriate Product Design and Delivery Channels

The FI designs products that are appropriate to client needs and do no harm

The FI seeks client feedback for product design and delivery

The FI does not use aggressive sales techniques

Client Protection Principle 2: Prevention of Over-indebtedness

The FI conducts appropriate client repayment capacity analysis before disbursing a loan

The FI incentivizes quality loans

The FI uses credit bureau and competitor data, as feasible in local context

The FI Management and Board is aware of and concerned about the risk of over-indebtedness

The FI's internal audit department monitors that policies to prevent over-indebtedness are applied

The FI avoids dangerous commercial practices (i.e., avoids combining loan products to meet the same need, or restricting the loan use; sets prudent limits to allow for the renewal of a loan in case of early repayment; sets guide-lines for appropriate rescheduling policies)

Client Protection Principle 3: Transparency

The FI fully discloses cost and non-cost information

The FI communicates proactively with clients in a way that clients can easily understand

The FI uses a variety of disclosure mechanisms

The FI leaves adequate time for client review and discloses at multiple times

The FI provides accurate and timely account information

Client Protection Principle 4: Responsible Pricing

The FI o�ers market-based, non-discriminatory pricing

The FI’s e�ciency is in line with its peers

The FI does not charge excessive fees

Client Protection Principle Standard

Client Protection Principle 5: Fair and Respectful Treatment of Clients

The FI culture raises awareness and concern about fair and responsible treatment of clients

The FI has de�ned in speci�c detail what it considers to be appropriate debt collection practices

The FI's HR policies (recruitment, training) are aligned around fair and responsible treatment of clients

The FI implements policies to promote ethics and prevent fraud

In selection and treatment of clients, the FI does not discriminate inappropriately against certain categories of clients

In-house and 3rd party collections sta� are expected to follow the same practices as the FI sta�

The FI informs clients of their rights

Client Protection Principle 6: Privacy of Client Data

The FI has a privacy policy and appropriate technology systems

The FI informs clients about when and how their data is shared and gets their consent

The FI's clients are aware of how to submit complaints

The FI's sta� is trained to handle complaints

The FI's complaints resolution system is active and e�ective

The FI uses client feedback to improve practices and products

Client Protection Principle 7: Mechanisms for Complaints Resolution

Client Protection Principle 1: Appropriate Product Design and Delivery Channels

The FI designs products that are appropriate to client needs and do no harm

The FI seeks client feedback for product design and delivery

The FI does not use aggressive sales techniques

Client Protection Principle Standard

The FI designs products that are appropriate to client needs and do no harm. It does not o�er products that produce negative value for the clients.

The FI has a policy describing acceptable pledges of collateral; Has clear guidelines for how collateral is registered and valued.

The FI investigates reasons for clients drop out.

The FI uses client feedback to inform product development and improve existing products (client feedback can be informal).

The FI does not use high pressure/ aggressive sales techniques. Does not force clients to sign contracts (for credit, no forced signing of any individual borrower or group member, or any guarantor).

Client Protection Principle 2: Prevention of Over-indebtedness

The FI conducts appropriate client repayment capacity analysis before disbursing a loan

The FI incentivizes quality loans

The FI policies support good repayment capacity analysis. The loan approval does not rely solely on guarantees (whether peer guarantees, co-signers or collateral) as a substitute for good capacity analysis. [individual lending] Repayment capacity analysis is done for every loan. [group lending] The group formation and loan approval process ensure the prudent self-selection of members, with emphasis on the concept of solidarity payment.

The FI's repayment capacity policy is adequately disseminated among sta�, considering the sta� growth and turn-over.

The FI's repayment capacity policy is uniformly used in the practice.

The FI performs a repayment capacity analysis at each loan cycle, even if simpli�ed for secondary aspects at loan renewal.

For clients with informal revenues and/or non consumption loans (most cases), the repayment capacity analysis is based on a client visit (performed by the loan o�cer or delegated to the group/village members). The FI veri�es the information consistency through cross-checks. For clients with a salary asking for a consumption loan, a client visit is not required.

Regular reports on PAR and write-o�s are produced and reviewed by the FI's management.

Reasonable portfolio quality is maintained over time. If there is poor long term quality of loan portfolio, and linked to over-indebtedness, corrective measures have been put in place.

The FI's productivity targets and incentive systems value portfolio quality at least as highly as other factors, such as disbursement or client growth.

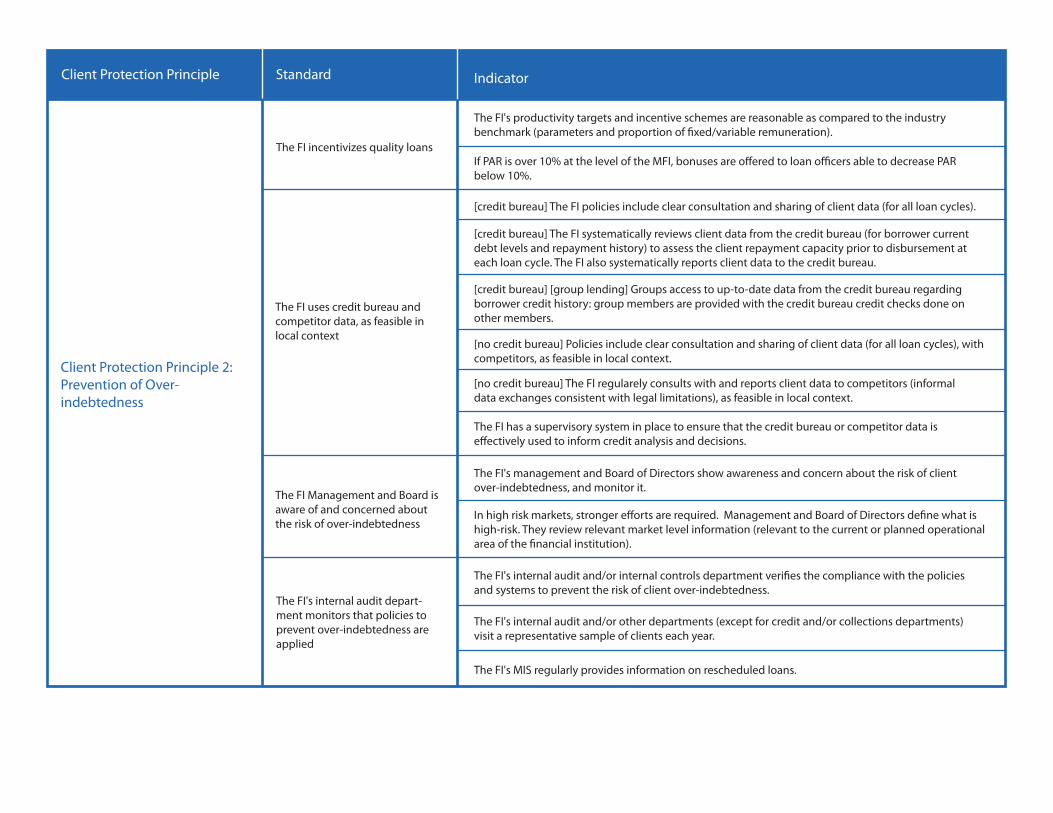

Indicator

Client Protection Principle Standard Indicator

Client Protection Principle 2: Prevention of Over-indebtedness

The FI incentivizes quality loans

The FI's productivity targets and incentive schemes are reasonable as compared to the industry benchmark (parameters and proportion of �xed/variable remuneration).

If PAR is over 10% at the level of the MFI, bonuses are o�ered to loan o�cers able to decrease PAR below 10%.

The FI uses credit bureau and competitor data, as feasible in local context

[credit bureau] The FI policies include clear consultation and sharing of client data (for all loan cycles).

[credit bureau] The FI systematically reviews client data from the credit bureau (for borrower current debt levels and repayment history) to assess the client repayment capacity prior to disbursement at each loan cycle. The FI also systematically reports client data to the credit bureau.

[credit bureau] [group lending] Groups access to up-to-date data from the credit bureau regarding borrower credit history: group members are provided with the credit bureau credit checks done on other members.

[no credit bureau] Policies include clear consultation and sharing of client data (for all loan cycles), with competitors, as feasible in local context.

[no credit bureau] The FI regularely consults with and reports client data to competitors (informal data exchanges consistent with legal limitations), as feasible in local context.

The FI has a supervisory system in place to ensure that the credit bureau or competitor data is e�ectively used to inform credit analysis and decisions.

The FI Management and Board is aware of and concerned about the risk of over-indebtedness

The FI's management and Board of Directors show awareness and concern about the risk of client over-indebtedness, and monitor it.

In high risk markets, stronger e�orts are required. Management and Board of Directors de�ne what is high-risk. They review relevant market level information (relevant to the current or planned operational area of the �nancial institution).

The FI's internal audit depart-ment monitors that policies to prevent over-indebtedness are applied

The FI's internal audit and/or internal controls department veri�es the compliance with the policies and systems to prevent the risk of client over-indebtedness.

The FI's internal audit and/or other departments (except for credit and/or collections departments) visit a representative sample of clients each year.

The FI's MIS regularly provides information on rescheduled loans.

Client Protection Principle Standard Indicator

The FI avoids dangerous commercial practices (i.e., avoids combining loan products to meet the same need, or restricting the loan use; sets prudent limits to allow for the renewal of a loan in case of early repayment; sets guidelines for appropriate rescheduling policies)

Client Protection Principle 2: Prevention of Over-indebtedness

[group lending] The FI has a policy that avoids parallel loans within the MFI (i.e., combining loan products to meet the same need, or restricting the loan use).

[group lending] The FI has prudent limits to allow for the renewal of a loan in case of early repayment.

The FI has speci�c procedures to actively work out solutions (i.e., through workout plan) for resched-uling loans/ re�nancing/ writing o� on an exceptional basis for late clients who have the “willingness” to repay but not capacity to repay, prior to seizing assets.

Client Protection Principle 3: Transparency

The FI fully discloses cost and non-cost information

The FI communicates proac-tively with clients in a way that clients can easily understand

The FI uses a variety of disclo-sure mechanisms

The FI leaves adequate time for client review and discloses at multiple times

The FI fully discloses to the clients all prices, installments, terms and conditions of all �nancial products, including all charges and fees, associated prices, penalties, linked products, 3rd party fees, and whether those can change over time.

The FI clearly presents to clients the total amount that the client pays for the product, regardless of local regulations (including in the absence of industry-wide requirements).

The FI participates in the MFTransparency project (or similar industry project, if applicable).

The FI has e�ective communication. Sta� communicates in such a manner that clients can under-stand the terms of the contract, their rights and obligations. Sta� communicates with techniques that address literacy limitations (e.g., materials available in local languages).

The FI contracts contain simple language and no �ne print (�guratively or literally). A clear facts summary page is given if the legally necessary contract is deemed too technical for the clients.

The FI avoids using pricing mechanisms that create confusion on the total costs.

The FI uses at least two di�erent communication channels for disclosing clear and accurate information about the product: written and verbal (to addredss litteracy limitatons).

The FI discloses pricing information in public domain.

The FI communicates all information related to the product (terms, conditions, etc.) to clients before signing.

The FI gives clients adequate time to review the terms and conditions of the product, ask questions and receive additional information prior to signing contracts.

The FI sta� is available to answer questions.

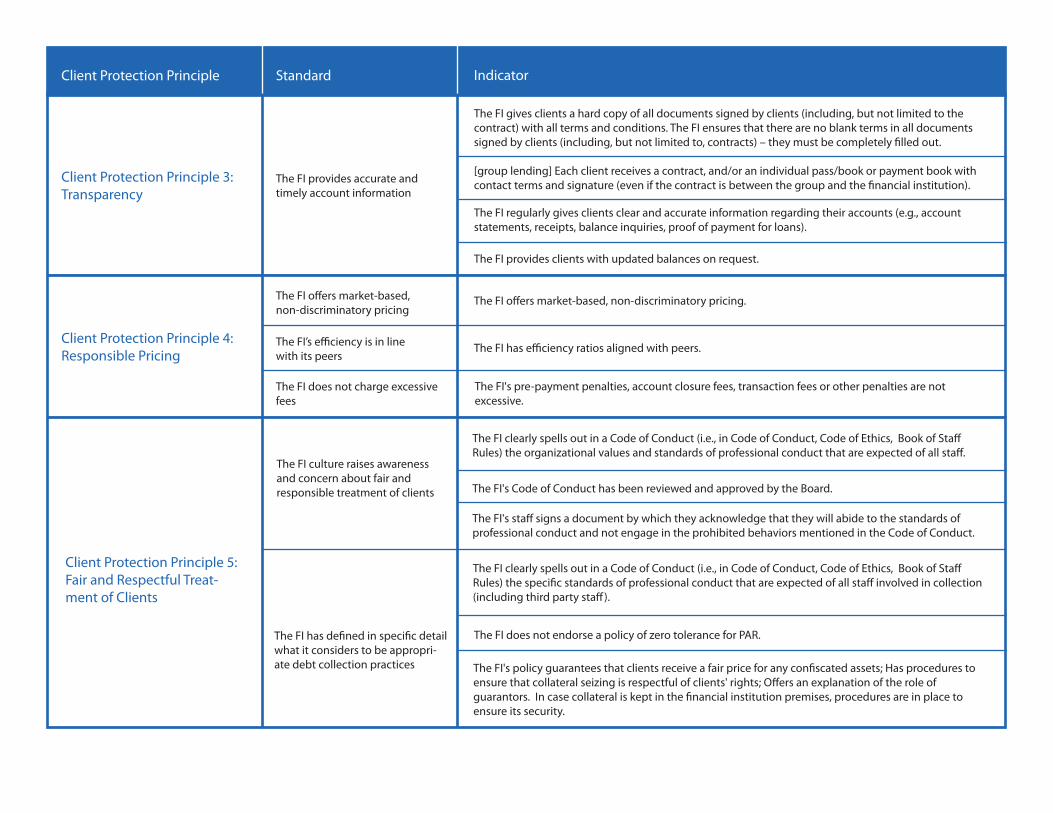

Client Protection Principle Standard Indicator

The FI provides accurate and timely account information

Client Protection Principle 3: Transparency

The FI gives clients a hard copy of all documents signed by clients (including, but not limited to the contract) with all terms and conditions. The FI ensures that there are no blank terms in all documents signed by clients (including, but not limited to, contracts) – they must be completely �lled out.

[group lending] Each client receives a contract, and/or an individual pass/book or payment book with contact terms and signature (even if the contract is between the group and the �nancial institution).

The FI regularly gives clients clear and accurate information regarding their accounts (e.g., account statements, receipts, balance inquiries, proof of payment for loans).

The FI provides clients with updated balances on request.

Client Protection Principle 4: Responsible Pricing

The FI o�ers market-based, non-discriminatory pricing

The FI’s e�ciency is in line with its peers

The FI does not charge excessive fees

The FI o�ers market-based, non-discriminatory pricing.

The FI has e�ciency ratios aligned with peers.

The FI's pre-payment penalties, account closure fees, transaction fees or other penalties are not excessive.

The FI culture raises awareness and concern about fair and responsible treatment of clients

The FI has de�ned in speci�c detail what it considers to be appropri-ate debt collection practices

The FI clearly spells out in a Code of Conduct (i.e., in Code of Conduct, Code of Ethics, Book of Sta� Rules) the organizational values and standards of professional conduct that are expected of all sta�.

The FI's Code of Conduct has been reviewed and approved by the Board.

The FI's sta� signs a document by which they acknowledge that they will abide to the standards of professional conduct and not engage in the prohibited behaviors mentioned in the Code of Conduct.

The FI clearly spells out in a Code of Conduct (i.e., in Code of Conduct, Code of Ethics, Book of Sta� Rules) the speci�c standards of professional conduct that are expected of all sta� involved in collection (including third party sta�).

The FI does not endorse a policy of zero tolerance for PAR.

The FI's policy guarantees that clients receive a fair price for any con�scated assets; Has procedures to ensure that collateral seizing is respectful of clients' rights; O�ers an explanation of the role of guarantors. In case collateral is kept in the �nancial institution premises, procedures are in place to ensure its security.

Client Protection Principle 5: Fair and Respectful Treat-ment of Clients

Client Protection Principle Standard Indicator

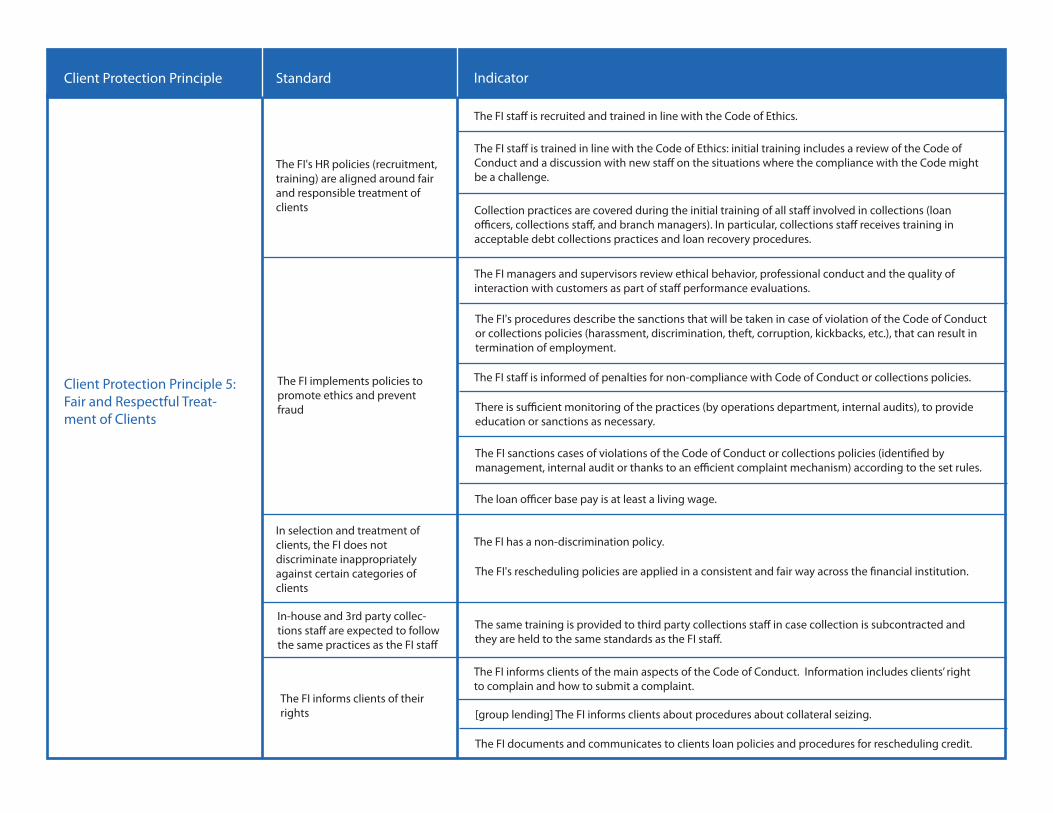

The FI's HR policies (recruitment, training) are aligned around fair and responsible treatment of clients

Client Protection Principle 5: Fair and Respectful Treat-ment of Clients

The FI sta� is recruited and trained in line with the Code of Ethics.

The FI sta� is trained in line with the Code of Ethics: initial training includes a review of the Code of Conduct and a discussion with new sta� on the situations where the compliance with the Code might be a challenge.

Collection practices are covered during the initial training of all sta� involved in collections (loan o�cers, collections sta�, and branch managers). In particular, collections sta� receives training in acceptable debt collections practices and loan recovery procedures.

The FI implements policies to promote ethics and prevent fraud

The FI managers and supervisors review ethical behavior, professional conduct and the quality of interaction with customers as part of sta� performance evaluations.

The FI's procedures describe the sanctions that will be taken in case of violation of the Code of Conduct or collections policies (harassment, discrimination, theft, corruption, kickbacks, etc.), that can result in termination of employment.

The FI sta� is informed of penalties for non-compliance with Code of Conduct or collections policies.

There is su�cient monitoring of the practices (by operations department, internal audits), to provide education or sanctions as necessary.

The FI sanctions cases of violations of the Code of Conduct or collections policies (identi�ed by management, internal audit or thanks to an e�cient complaint mechanism) according to the set rules.

The loan o�cer base pay is at least a living wage.

In selection and treatment of clients, the FI does not discriminate inappropriately against certain categories of clients

The FI has a non-discrimination policy.

The FI's rescheduling policies are applied in a consistent and fair way across the �nancial institution.

In-house and 3rd party collec-tions sta� are expected to follow the same practices as the FI sta�

The same training is provided to third party collections sta� in case collection is subcontracted and they are held to the same standards as the FI sta�.

The FI informs clients of their rights

The FI informs clients of the main aspects of the Code of Conduct. Information includes clients’ right to complain and how to submit a complaint.

[group lending] The FI informs clients about procedures about collateral seizing.

The FI documents and communicates to clients loan policies and procedures for rescheduling credit.

Client Protection Principle Standard Indicator

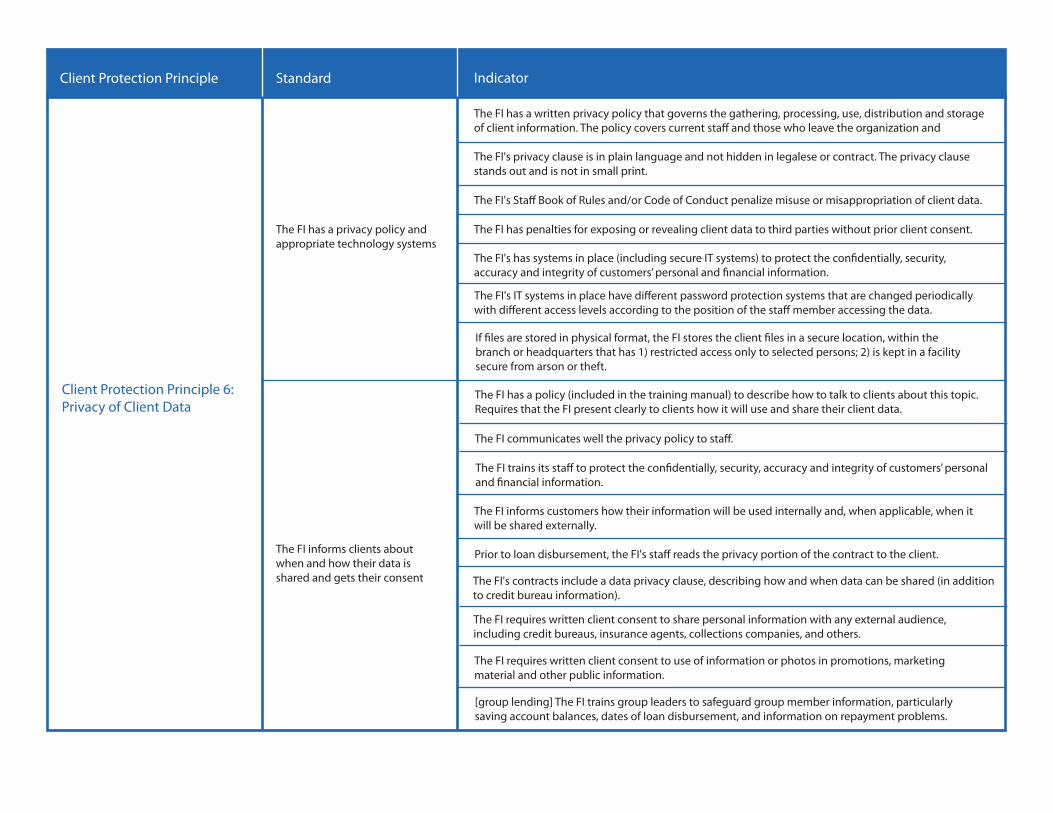

The FI has a privacy policy and appropriate technology systems

The FI has a written privacy policy that governs the gathering, processing, use, distribution and storage of client information. The policy covers current sta� and those who leave the organization and

The FI's privacy clause is in plain language and not hidden in legalese or contract. The privacy clause stands out and is not in small print.

The FI's Sta� Book of Rules and/or Code of Conduct penalize misuse or misappropriation of client data.

The FI has penalties for exposing or revealing client data to third parties without prior client consent.

The FI's has systems in place (including secure IT systems) to protect the con�dentially, security, accuracy and integrity of customers’ personal and �nancial information.

The FI's IT systems in place have di�erent password protection systems that are changed periodically with di�erent access levels according to the position of the sta� member accessing the data.

If �les are stored in physical format, the FI stores the client �les in a secure location, within the branch or headquarters that has 1) restricted access only to selected persons; 2) is kept in a facility secure from arson or theft.

Client Protection Principle 6: Privacy of Client Data

The FI informs clients about when and how their data is shared and gets their consent

The FI has a policy (included in the training manual) to describe how to talk to clients about this topic. Requires that the FI present clearly to clients how it will use and share their client data.

The FI communicates well the privacy policy to sta�.

The FI trains its sta� to protect the con�dentially, security, accuracy and integrity of customers’ personal and �nancial information.

The FI informs customers how their information will be used internally and, when applicable, when it will be shared externally.

Prior to loan disbursement, the FI's sta� reads the privacy portion of the contract to the client.

The FI's contracts include a data privacy clause, describing how and when data can be shared (in addition to credit bureau information).

The FI requires written client consent to share personal information with any external audience, including credit bureaus, insurance agents, collections companies, and others.

The FI requires written client consent to use of information or photos in promotions, marketing material and other public information.

[group lending] The FI trains group leaders to safeguard group member information, particularly saving account balances, dates of loan disbursement, and information on repayment problems.

Client Protection Principle Standard Indicator

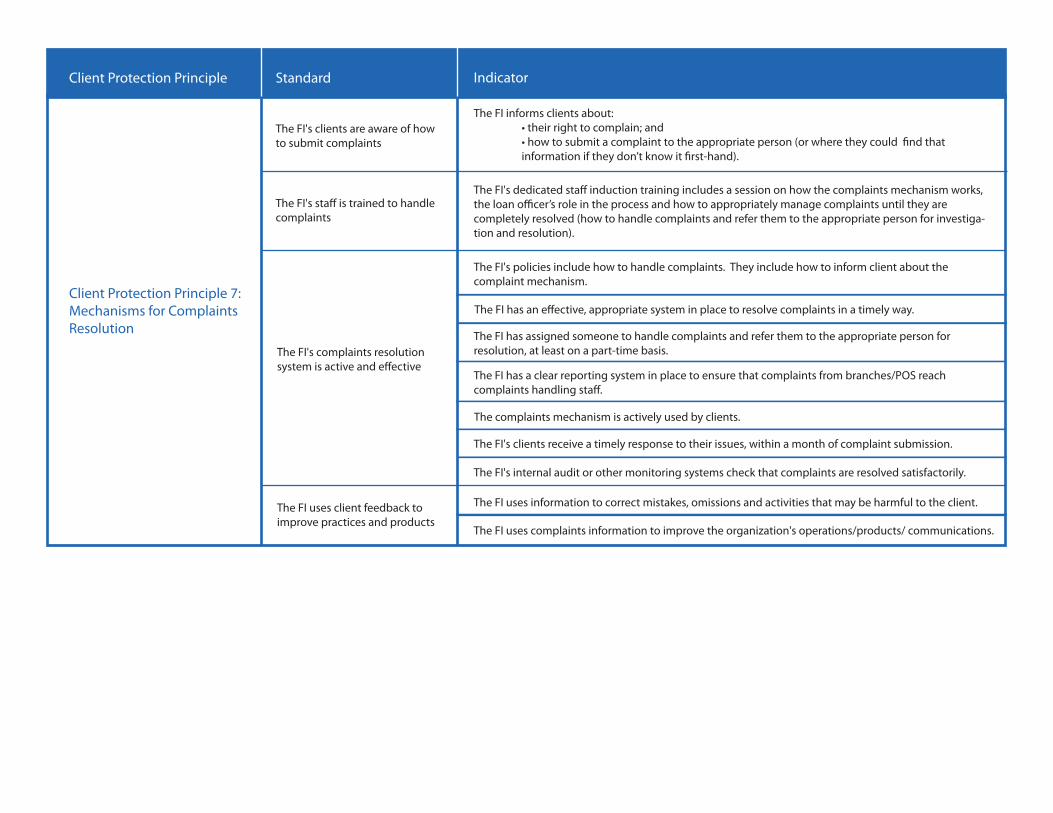

Client Protection Principle 7: Mechanisms for Complaints Resolution

The FI's clients are aware of how to submit complaints

The FI informs clients about: • their right to complain; and • how to submit a complaint to the appropriate person (or where they could find that information if they don’t know it first-hand).

The FI's sta� is trained to handle complaints

The FI's dedicated staff induction training includes a session on how the complaints mechanism works, the loan officer’s role in the process and how to appropriately manage complaints until they are completely resolved (how to handle complaints and refer them to the appropriate person for investiga-tion and resolution).

The FI's complaints resolution system is active and effective

The FI's policies include how to handle complaints. They include how to inform client about the complaint mechanism.

The FI has an effective, appropriate system in place to resolve complaints in a timely way.

The FI has assigned someone to handle complaints and refer them to the appropriate person for resolution, at least on a part-time basis.

The FI has a clear reporting system in place to ensure that complaints from branches/POS reach complaints handling staff.

The complaints mechanism is actively used by clients.

The FI's clients receive a timely response to their issues, within a month of complaint submission.

The FI's internal audit or other monitoring systems check that complaints are resolved satisfactorily.

The FI uses client feedback to improve practices and products

The FI uses information to correct mistakes, omissions and activities that may be harmful to the client.

The FI uses complaints information to improve the organization's operations/products/ communications.