Embed Size (px)

Citation preview

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 1/22

IMPACT OF

PRIVATISATION

ON

LIC

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 2/22

INDEX

Sr

No. Particulars1) Introduction

2) Introduction To LIC3) LIC OF INDIA: History and position after

privatization.

4) STATUS AND POSITION OF INDIAN LIFE

INSURANCE INDUSTRY IN THE PRE LPG ERA

5) Comparison of LIC as an today and at the

time of Nationalization

6) Causes and effects of privatization oninsurance firm.

7) Objectives of LIC

8) PROGRESS OF INDIAN LIFE INSURANCE

INDUSTRY IN THE POST LPG ERA

9) SETTING-UP OF IRDA, AND THE ENTRY OF

PRIVATE INSURANCE COMPANIES

10) Lic in new era11) LIC OF INDIA: STILL AT THE TOP

12) Conclusion

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 3/22

INTRODUCTION

The new millennium has exposed the insurance sector to new challenges ofcompetition and struggle for survival. The era of liberalization, privatization and

globalisation has ended the monopolistic tendency in this sector. It has been over four

years since the Indian insurance market has opened up and the new entrants into the

market have set up their shops throughout the country.

Until the late nineties, the Indian insurance industry was under State control with no

private participation. In April 1993 the Government of India appointed the Malhotra

Committee to evaluate the insurance industry and to suggest its future direction. The

Committee submitted its report in 1994, strongly recommending private participation inthe industry. The discussion and efforts to open up the insurance market continued for

about six years. The policymakers were in a „Catch 22‟ situation. On the one hand,

they wanted competition for the development and growth of the insurance sector, and

on the other, they feared that the insurance premium would seep out of the country.

Thus they adopted a cautious approach towards opening up the sector to foreign

participation. Ultimately, the Insurance Regulatory and Development Act (IRDA) was

passed in December 1999 and with this the globalisation of the Indian insurance

sector became a reality. Certainly, these developments were bound to have an impact

on Life Insurance Corporation (LIC) of India too. The present paper tries to review the

current status of LIC in the changed competitive scenario of the insurance industry.

INTRODUCTION TO LIC

The Life Insurance Corporation of India (LIC) (Hindi: भारतीय जीवन बीमा नगम ) is the

largest state-owned life insurance company in India, and also the country's largest

investor. It is fully owned by the Government of India. It also funds close to 24.6% of

the Indian Government's expenses. It has assets estimated of 9.31 trillion

(US$207.61 billion).[1] It was founded in 1956 with the merger of more than 200

insurance companies and provident societies.[2]

Headquartered in Mumbai, financial and commercial capital of India,[3] the Life

Insurance Corporation of India currently has 8 zonal Offices and 101 divisional offices

located in different parts of India, at least 2048 branches located in different cities and

towns of India along with satellite Offices attached to about some 50 Branches, and

has a network of around 1.2 million agents for soliciting life insurance business from

the public.

The slogan of LIC is "Zindagi ke saath bhi,Zindagi ke baad bhi" (Hindi: ़दगी के साथ

भी , ़दगी के बाद भी ) which means "during life and after life".

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 4/22

LIC OF INDIA: HISTORY AND POSITION AFTER PRIVATISATION

Life insurance in its present form came to India from England in the year 1818, when

the Oriental Insurance Company, the first corporate entity in India offering lifeinsurance cover was established in Calcutta. From then onwards, for the next 138

years, several companies and societies were formed for providing life insurance cover.

The period was marked by a turbulent economic backdrop, sometimes also

interspersed with periods of relative economic stability. The period witnessed India‟s

First War of Independence, adverse effects of the World War I and World War II on the

economy of India, and in between them the period of worldwide economic crises

triggered by the Great Depression of 1929-30. The aggregate effect of these events

led to a high rate of bankruptcies and liquidation of life insurance companies in India.

This had adversely affected the faith of the general public in the utility of obtaining life

cover. Against this background, the Parliament of India passed the Life Insurance ofIndia Act on 19th June 1956, and the Life Insurance Corporation of India came into

existence on 1st September, 1956, by consolidating the life insurance business of 245

life insurers and other entities offering life insurance services.

the Bombay Mutua l L i fe Assurance Soc ie ty , fo rmed in 1870, wasth e fi rs t na ti ve insurance provider. Others insurance companiesestablished in the pre -independence are included:

Bharat Insurance Company (1896)

United India (1906)

National Indian (1906)

National Insurance (1906)

Co-operative Assurance (1906)

Hindustan Co-operatives (1907)

Indian Mercantile

General Assurance

Swadeshi Life (later Bombay Life)

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 5/22

The first 150 years were marked mostly by turbulent economiccond i t i ons . I t w i tnessed Ind ia ‟s Fi rs t War o f Independence, adverseeffects of the World War I and World War II on the economy of India, and inbetween them the period of world wide economic crises triggered by the GreatDepress ion . The f i r s t ha l f o f the 20 th ce nt ur y al so sa w a heightened

struggle for India‟s Independence. The aggregate effect of t hese eventsled to a high rate of bankruptcies and l iquidat ion of l i fe Insurancecompanies in adversely affected the faith of the general public in the utility of obtaininglife cover. The Life Insurance Act and the Provident Fund Act were passed in 1912,providing the first regulatory mechanism in the Life Insurance industry. T he Ind ianInsura nce Co mpanies Act of 1928 autho r ized t he govt . to obtainstatistical information from companies operating in both life and non-life insuranceareas. The subsequent Insurance Act of 1938 brought stricter state control overan insurance that had seen several financially unsound ventures fail.A bill was also introduced in the Legislative Assembly in 1944 to nationalize the

insurance industry.

STATUS AND POSITION OF INDIAN LIFE INSURANCE INDUSTRY INTHE PRE LPG ERAThe process of insurance has been evolved to safeguard the interests of people fromuncertainty by providing certainty of payment at a given contingency. Life insurance inits modern form came to India from England in 1818 with the formation of Oriental LifeInsurance Company (OLIC) in Calcutta mainly by Europeans to help widows of theirkin. Later, due to persuasion by one of its directors (Shri Babu Muttyal Seal), Indianswere also covered by the company. By 1868, 285 companies were doing business ofinsurance in India. Earlier these companies were governed by Indian company act

1866. By 1870, 174 companies ceased to exist, when British parliament enactedinsurance Act 1870. These companies were however, insuring European lives. ThoseIndians who were offered insurance cover were treated as sub-standard lives andwere accepted with an extra premium of 15% to 20%

Some Areas of Future Growth (before privatization the expectationsfor future growth) :-

Life Insurance The traditional life insurance business for the LIC has been a little more than a savings

policy. Term life (where the insurance company pays a predetermined amount if thepolicyholder dies within a given time but it pays nothing if the policyholder does notdie) has accounted for less than 2% of the insurance premium of the LIC (Mitra andNayak, 2001). For the new life insurance companies, term life policies would be themain line of business.

Health Insurance Health insurance expenditure in India is roughly 6% of GDP, much higher than mostother countries with the same level of economic development. Of that, 4.7% is privateand the rest is public. What is even more striking is that 4.5% are out of pocketexpenditure (Berman, 1996). There has been an almost total failure of the public

health care system in India. This creates an opportunity for the new insurancecompanies.

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 6/22

Thus, private insurance companies will be able to sell health insurance to a vastnumber of families who would like to have health care cover but do not have it

Pension The pension system in India is in its infancy. There are generally three forms of plans:provident funds, gratuities and pension funds. Most of the pension schemes are

confined to government employees (and some large companies). The vast majority ofworkers are in the informal sector. As a result, most workers do not have anyretirement benefits to fall back on after retirement. Total assets of all the pension plansin India amount to less than USD 40 billion.Therefore, there is a huge scope for the development of pension funds in India. Thefinance minister of India has repeatedly asserted that a Latin American style reform ofthe privatized pension system in India would be welcome (Roy, 1997). Given all thepros and cons, it is not clear whether such a wholesale privatization would reallybenefit India or not (Sinha, 2000).

First Indian Company

Pioneering efforts of reformers and social workers like Raja Ram mohan Ray,Dwarakanath Tagore, Ramatam Lahiri, Rustomji Cowasji and other led to entry of

Indians in insurance business. First Indian insurance company under the name

“Bombay Life Insurance Society” started its operation in 1870, and started covering

Indian lives at standard rates. Later “Oriental Government Security Life Insurance

Company”, was established in 1874, with Sir Phirozshah Mehta as one of its founder

directors and later emerged as a leading Indian insurance company under the name

“Bombay Life Assurance Society” started its operations in 1870.

PRE-INDEPENDENCE SCENARIO

With the patriotic fervour of Non-Corporation Movement (1919) and Civil Disobedience

Movement (1929), number of Indian companies entered the insurance arena. Eminent

figures in political area like Mahatma Gandhi and Pandit Nehru openly encouraged

Indians to enter the fray. In 1914 there were only 44 companies, by 1940 this number

grew to 195. Business in force during this period grew from Rs.22.44 crores to

Rs.304.03 crores (1628381 polices). Life fund steadily grew from Rs.6.36 crores to

Rs.62.41 crores. In 1938, the insurance business was heavily regulated by enactment

of insurance Act 1938(based on draft bill presented by Sir N.N.Sarcar in LegislativeAssembly in January 1937). From here onwards the growth of life insurance was quite

steady except for a setback in 1947-48 due to aftermath of partition of Indian. In 1948,

there were 209 insurances, with 712.76 crores business in force under 3,016, 000

policies. The life fund by then grew to 150.39 crores.

After completing the arduous task of integration of about 250 life insurance

companies, the LIC of India gave an exemplary performance in achieving various

objectives of nationalization. The following table shows the achievements of LIC in 40

odd years of its existence

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 7/22

NATIONALISATION OF LIFE INSURANCE (1956)

Despite the mushroom growth of many insurance companies per capita insurance in

Indian was merely Rs.8.00 in 1944(against Rs.2, 000 in US and Rs.600 in UK),

besides some companies were indulging in malpractices, and a number of companies

went into liquidation. Big industry houses were controlling the insurance and banking

business resulting in inter looking of funds between banks and insurance companies.

This shook the faith of insuring public in insurance companies as custodians of their

savings and security. The nation under the leadership of Pandit Jawarberlal Nehru

was moving towards socialistic pattern of society with the main aim of spreading of life

insurance to rural areas and to channelise huge funds accumulated by life insurance

companies to nation building activities. The Government of India nationalized the life

insurance industry in January 1956 by merging about 250 life insurance companies

and forming Life Insurance Corporation of India (LIC), which started functioning from

01.09.1956.

After completing the arduous task of integration of about 250 life insurance

companies, the LIC of India gave an exemplary performance in achieving various

objectives of nationalization. The following table shows the achievements of LIC in 40

odd years of its existence

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 8/22

Growth ofLIC between1959 and1999 S.No.

Particulars 1957 1999

1 AnnualBusiness:Sum AssuredPolicies Firstyear premium

336.3 crores8,00,000 14crores

75606 crores148570004171 crores

2 Business inforce: SumAssuredPoliciesRenewal

premium

1477 crores5686000 74crores

459201 crores9172600016136crores

3 GroupBusiness inforce: SumAssured No.of Lives

5.29 crores - 69558 crores21671000

4 Life Fund: 41040 crores 127389.06crores

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 9/22

COMPARISON OF LIC AS ON TODAY AND AT THE TIME OF

NATIONALIZATION

LIC had 5 zonal offices, 33 divisional offices and 212 branch offices, apart from itscorporate office in the year 1956. Since life insurance contracts are long term contractsand during the currency of the policy it requires a variety of services need was felt in thelater years to expand the operations and place a branch office at each districtheadquarter. Re-organization of LIC took place and large numbers of new branchoffices were opened. As a result of re-organisation servicing functions were transferredto the branches, and branches were made accounting units. It worked wonders with theperformance of the corporation. It may be seen that from about 200.00 crores of NewBusiness in 1957 the corporation crossed 1000.00 crores only in the year 1969-70, andit took another 10 years for LIC to cross 2000.00 crore mark of new business. But withre-organisation happening in the early eighties, by 1985-86 LIC had already crossed7000.00 crore Sum Assured on new policies.

Today LIC functions with 2048 fully computerized branch offices, 109 divisional offices,8 zonal offices, 992 satallite offices and the Corporate office. LIC‟s Wide Area Networkcovers 109 divisional offices and connects all the branches through a Metro AreaNetwork. LIC has tied up with some Banks and Service providers to offer on-linepremium collection facility in selected cities. LIC‟s ECS and ATM premium paymentfacility is an addition to customer convenience. Apart from on-line Kiosks and IVRS, InfoCentres have been commissioned at Mumbai, Ahmedabad, Bangalore, Chennai,Hyderabad, Kolkata, New Delhi, Pune and many other cities. With a vision of providingeasy access to its policyholders, LIC has launched its SATELLITE SAMPARK offices.The satellite offices are smaller, leaner and closer to the customer. The digitalizedrecords of the satellite offices will facilitate anywhere servicing and many other

conveniences in the future.

LIC continues to be the dominant life insurer even in the liberalized scenario of Indianinsurance and is moving fast on a new growth trajectory surpassing its own pastrecords. LIC has issued over one crore policies during the current year. It has crossedthe milestone of issuing 1,01,32,955 new policies by 15th Oct, 2005, posting a healthygrowth rate of 16.67% over the corresponding period of the previous year.

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 10/22

THE OBJECTIVES OF LIC:

(i) “Spreading life insurance much more widely and in particular to the rural areas and to

the socially and economically backward classes, with a view to reach all insurable persons

in the country and provide them adequate financial coverage against death at a reasonable

cost.

(ii) Maximizing mobilization of people savings by making insurance linked savings

adequately attractive.

(iii) Investing funds to the best advantage of the investors as well as the community as a

whole, keeping in view national priorities and obligations of attractive return, and

(iv) Meeting the various life insurance needs of the community that would arise in the

changing social and economic environment through its Family Schemes and Group

Insurance Schemes.

(v) The above objectives are framed by the LIC at the time of its establishment and it istrying to materialise its objectives over the subsequent years. However, the Indian Life

Insurance Industry is facing several challenges and issues throughout its career and

establishes meaningful strategies to overcome these challenges and issues from time to

time. Since the date of its establishment it has earmarked a steady growth; but many

factors affected its abnormal growth and progress.”3 They are as follows:

a. The mega illiteracy percentage

b. Improper awareness among the general public regarding the savings

c. Least percentage of employment opportunities

d. Lowest wage and salary pattern etc.,

When compared with the developed foreign countries the Indian life insurance industry has

achieved only a little, because of no quality strategies adopted by the LIC, as well as our

standard of education and awareness about savings, per capita income, and employment

opportunities are comparatively not up to the mark.

Soon after the introduction of new economic policy (LPG) in the year 1991, the shape of the

Indian life insurance industry has been changing and it has geared up. Soon after then

many private players have entered into this industry, who pose challenges and threat to its

competitors. These new challenges forced the industry.

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 11/22

WHAT ARE THE CAUSES FOR PRIVATISATION OF INSURANCESECTOR IN IN INDIA?

when we critically examine the opportunities which were available before theglobalization of Indian market, it can be said that LIC failed to cash it. one of the main

reasons for the low insurance penetration in India was the ineffective distribution andmarketing strategies adopted by LIC. The company reportedly never had any strategicmarketing game plan, and due to its monopolistic nature the need for serious marketingefforts was never felt. The advertising initiatives were limited to some print andelectronic media advertisements, which typically talked about LIC's products being greattax saving tool for salaried individuals who came under the income-tax bracket. Despiteall this, LIC was synonymous with insurance in India and it had established an enviablebrand image for itself, especially in the rural areas and small towns. However, with theentry of new players, the insurance market changed almost overnight. the privateinsurers seemed all set to make the industry marketing-driven, wherein technical andservice excellence would be the key factors of success. The private companies, in a bid

to make their presence felt and their brand noticed, initiated a series of aggressivemarketing and promotion initiatives, something that buyers of insurance were notaccustomed to.lic had made Indian insurance industry a sellers market, where customerhad no option other than to buy its (LIC's) product . LIC had also not tried to explore themarket but were happy what they were getting effortlessly.

WHAT ARE THE EFFECTS OF PRIVATISATION IN INSURANCESECTOR IN INDIA?

There's another dimension to the insurance numbers game. While the private insurancecompanies have attained 13 to 14 per cent share of the overall insurance market, their

share in the key metros (Mumbai and Delhi) is as high as 30 to 40 per cent.

"We have to struggle to complete a deal in the metros now, because policyholders arecomparing products and asking for better deals," says S B Mathur, chairman of the LifeInsurance Corporation of India.

Private insurance companies are essentially joint ventures with global insurancecompanies holding a maximum of 26 per cent stake. The foreign partners are investingheavily in the Indian market and, thereby, driving sales, because they see Indiaemerging as one of the biggest markets in the Asian region.

"India will become the biggest market for us in the next three to four years," predictsDan Bardin, Prudential Corporation Asia managing director south Asia and greaterChina.

Private players have certainly done their bit to increase the penetration levels ofinsurance, mainly by creating alternative distribution channels--such as associationswith banks, brokers and corporate agents.

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 12/22

PROGRESS OF INDIAN LIFE INSURANCE INDUSTRY IN THE POSTLPG ERA

In the post LPG period, the Life Insurance Industry of India witnessed a marvelous

growth and touched its historical height. So many factors have collectively contributed

for this remarkable achievement. In this tenure, the LIC of India introduced many

phenomenal business strategies by way of offering colorful schemes and products. The

reason for these kinds of extraordinary effect was only because of the stiff competition

emerging by the private insurance players. The private insurance companies are

offering plenty of new attractive schemes and products to get meaningful share in the

insurance market. However, the LIC of India has the powerful network and it is

launching attractive advertisements in the regular interval to create great awareness

among the general public. Simultaneously, the private life insurance companies are also

taking much pain to cover-up the major populations (inventors) under their boundary, for

that they are sponsoring series of effective awareness programmes through manyattractive advertisements. This healthy competition motivated the general public to go in

favour of more investments in insurance. While comparing the efficiency and

progressiveness of life insurance business in pre and post LPG arena, the Indian Life

Insurance Industries are achieving a magnificent growth.

Impact of Privatisation and Performance presents an indepth analysis of LIC's

performance in respect of various indicators since the policy of liberalisation was

itnroduced in the country. The productivity analysis of the corporation has been carried

out using different parameters. The portfolio management of the corporation has been

studied in detail in respect of loans and investments. The impact of privatisation on the

performance of LIC has been evaluated in terms of its market share in various

parameters of insurance vis-a-vis the private players. The book also identifies key

determinants of the performance of LIC and makes recommednations for improving it.

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 13/22

MONOPOLY RAJ

The nationalization of life insurance was justified mainly on three counts.

(1) It was perceived that private companies would not promote insurance in rural areas.

(2) The Government would be in a better position to channel resources for saving and

investment by taking over the business of life insurance.

(3) Bankruptcies of life insurance companies had become a big problem (at the time of

takeover, 25 insurance companies were already bankrupt and another 25 were on the

verge of bankruptcy). The experience of the next four decades would temper these

views. 5Life Story of the Life Insurance Corporation. The life insurance industry was

nationalized under the Life Insurance Corporation (LIC) Act of India. In some ways, the

LIC has become very successful.

(1) Despite being a monopoly, it has some 60-70 million policyholders. Given that theIndian middle-class is around 250-300 million, the LIC has managed to capture some 30

odd percent of it.

(2) The level of customer satisfaction is high for the LIC (one of the findings of the

Malhotra Committee, see below). This is somewhat surprising given the frequent

delays in claim settlement.

(3) Market penetration in the rural areas has grown substantially. Around 48% of the

customers of the LIC are from rural and semi-urban areas. This probably would not

have happened had the charter of the LIC not specifically set out the goal of serving therural areas.

One exogenous factor has helped the LIC to grow rapidly in recent years: a high saving

rate in India. Even though the saving rate is high in India (compared with other

countries with a similar level of development), Indians exhibit high degree of risk

aversion. Thus, nearly half of the investments are in physical assets (like property and

gold). Around twenty three percent are in (low yielding but safe) bank deposits. In

addition, some 1.3- percent of the GDP are in life insurance related savings vehicles.

This figure has doubled between 1985 and 1995.

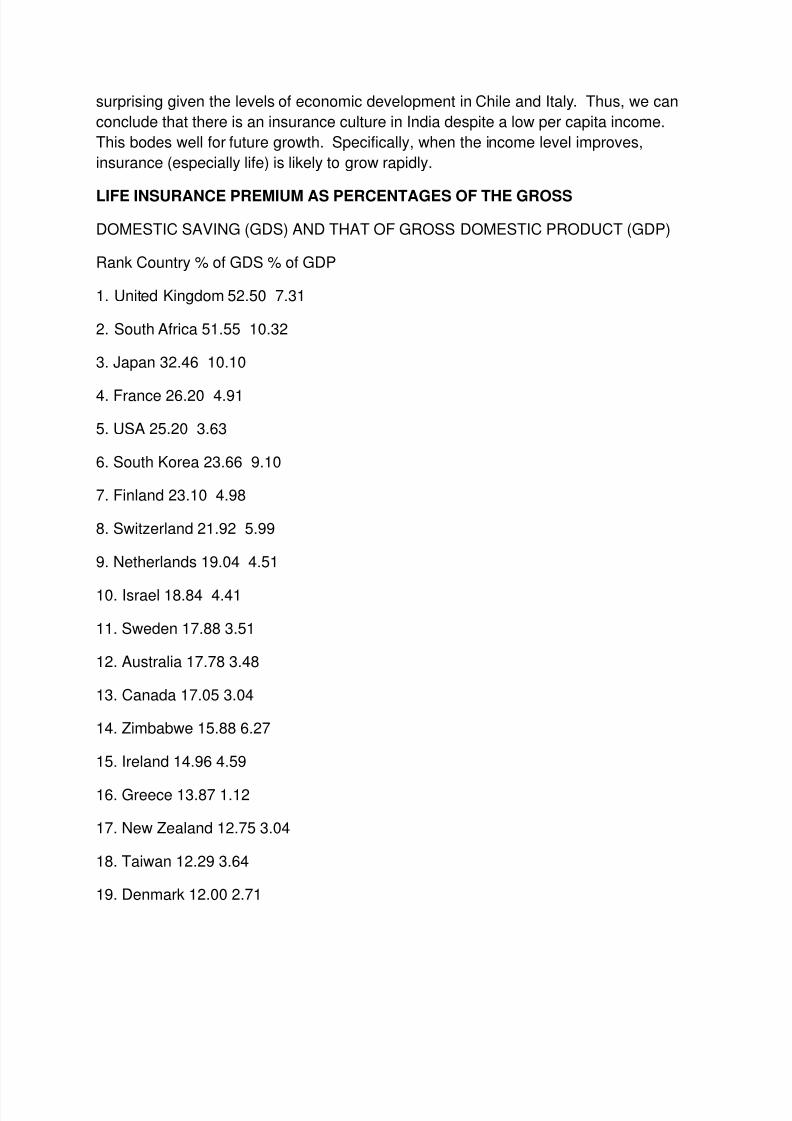

Life Insurance in India:

A World Perspective In many countries, insurance has been a form of savings. Table 2

shows that in many developed countries, a significant fraction of domestic saving is in

the form of (endowment) insurance plans. This is not surprising. The prominence of

some developing countries is more surprising. For example, South Africa features at

the 6 number two spot. India is nestled between Chile and Italy. This is even more

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 14/22

surprising given the levels of economic development in Chile and Italy. Thus, we can

conclude that there is an insurance culture in India despite a low per capita income.

This bodes well for future growth. Specifically, when the income level improves,

insurance (especially life) is likely to grow rapidly.

LIFE INSURANCE PREMIUM AS PERCENTAGES OF THE GROSS

DOMESTIC SAVING (GDS) AND THAT OF GROSS DOMESTIC PRODUCT (GDP)

Rank Country % of GDS % of GDP

1. United Kingdom 52.50 7.31

2. South Africa 51.55 10.32

3. Japan 32.46 10.10

4. France 26.20 4.91

5. USA 25.20 3.63

6. South Korea 23.66 9.10

7. Finland 23.10 4.98

8. Switzerland 21.92 5.99

9. Netherlands 19.04 4.51

10. Israel 18.84 4.41

11. Sweden 17.88 3.51

12. Australia 17.78 3.48

13. Canada 17.05 3.04

14. Zimbabwe 15.88 6.27

15. Ireland 14.96 4.59

16. Greece 13.87 1.12

17. New Zealand 12.75 3.04

18. Taiwan 12.29 3.64

19. Denmark 12.00 2.71

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 15/22

20. Spain 11.68 2.23

21. Germany 11.40 2.80

22. Norway 9.57 2.33

23. Belgium 9.13 2.38

24. Portugal 8.76 1.65

25. Austria 6.96 2.10

26. Chile 6.96 1.95

27. India 5.95 1.29

28. Italy 5.60 1.13

29. Malaysia 5.35 2.30

30. Singapore 4.72 2.73

SETTING-UP OF IRDA, AND THE ENTRY OF PRIVATE INSURANCE

COMPANIES

In spite of phenomenal progress of LIC of India, especially in the 80s, the government

and public at large were not quite satisfied with it. By signing GATT accord, thegovernment of India committed to opening of insurance sector to private sector – to

local and global operators. A committee under the chairmanship of late R.N.Malhotra

(Ex- governor of KBI) was appointed by the government to look into all the aspects of

insurance industry in India. The committee too, opined that in its about 40 years of

existence, LIC had been able to insure only 22 percentage of the insurable population.

A moot reason may be the lack of competition. Further, the monopoly has resulted in

lack of sensitivity to the policy holders. There is a greater scope for product innovation

and service improvement. The committee recommended a number of measures to

revamp LIC of India, GIC of India and its four subsidiaries. It also recommended to allow

outside insurance companies to operate in India with an Indian partner. After a greatdeal of discussion, finally the Lok Sabha has enacted the Insurance Regulatory and

Development Authority Act, 1999. In terms of the act, the Insurance Regulatory and

Development Authority is being set-up to regulate and develop the insurance industry

by opening it up to the private sector. Foreign insurance companies can enter into the

insurance sector in India only with an Indian partner, as a joint-venture, with a capital

contribution up to a maximum of 26 percentage of the capital in the joint-venture.

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 16/22

LIC IN NEW ERA

Change in attitude of people: people changed their attitude towards insurance.Earlier insurance was taken as tool of tax saving but people thinks as a shieldaround their families as well. Now, people are quite aware about both, the risk

coverage and the investment part of insurance.

Open and transparent environment: insurance sector got financially strongand willingly waiting for returns like customers their confidence boosted becauseof open and transparent policy guidelines.

Well established distribution network: distribution refers to the arrangementby which the product after manufacture is moved till it reaches the customer.There are various intermediaries in every business that do this job. Insurancebusiness is sold through agents. Recently banks also linked with insurance firms.

Known as bancassurance. Public sector banks which have huge branch networkbecause of their long existence, plays a very crucial role in this direction.

Trained professionals: in the past, insurance agents were consideres to be thebest salesman for insurance products but now privatization and globalizationmore professionalism has been seen.

Rational approach to the investment criteria: the guidelines issued by IRDAfor investment pattern has been adopted so as meet the obligations. LIC followedthese guidelines and kept in mind that more the people insured, the better therevenue, the better the security and ultimately better morale and productivity.

Stringent accounting practices: the insurer has mobilized the hard earnedmoney of the masses. The failure for any reason had disastrous effects. Toprevent such a possibility, imperative insurers follow stringent accountingpractices.

Advertising and publicity: In the present age of competition, any organization

can be successful only if it is able to convince customers about the quality and

effectiveness of its products. LIC did a wonderful job in this regard. But to

improve its performance it started giving importance to advertising its productsusinga wide range of advertising methods such as print and electronic

media,sponsoring events, road shows,etc

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 17/22

CURRENT STATUS

Over its existence of around 50 years, Life Insurance Corporation of India, which

commanded a monopoly of soliciting and selling life insurance in India, created huge

surpluses, and contributed around 7 % of India's GDP in 2006.

The Corporation, which started its business with around 300 offices, 5.6 million policies

and a corpus of INR 459 million (US$ 92 million as per the 1959 exchange rate of

roughly Rs. 5 for a US $ [4], has grown to 25000 servicing around 350 million policies

and a corpus of over 8 trillion (US$178.4 billion)

RESEARCH OBJECTIVE

The report gives the brief background of the sector and proceeds toh i g h l i g h t t h e s h o r t c o m i n g s o f t h e e x i s t i n g s e t u p a n d p l a y e r s .T h e benefits of liberalized sector are enumerated. The report also tries to identify themarket potential for insurance products and the strategy that we employed to exploit thesame. The stress is also given on knowing the awareness level of general public.

First and foremost objective is to find out the reasons for using of Different Productsof LIC.

To find out the services that other insurance companies are giving to theircustomers.

To build the relationship with the customers and to follow up them, make sure thatthey are satisfied with the product.

To maintain good relationships with the corporate employees.

To get more references from the customers and generate new leads by following achain process.

To place LIC Products ahead of the competitors.

To find out the customer awareness on booming Advance Product market and tofind out the using patterns of the people.

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 18/22

LIC OF INDIA: STILL AT THE TOP

Although it is now almost seven years since the insurance sector of India was opened

up for FDI, LIC of India is still at the top. This is very clear from the following facts

a. In 2004-05, LIC brought in a First Premium Income of Rs.15840.67 crore as against

the first premium income of Rs.12179 crore during 2003-04, posting a momentous

growth rate of 30 percent during the year. Out of this, Rs.12174.11 crore came from the

individual business, posting an impressive growth rate of 42.1 percent as against the

targeted growth rate of 35 percent. This was possible because of the sale of more than

1 crore policies during the year 2004-05. Thus the LIC has continued to retain its

position as dominant market leader in life insurance in India. During the year 2004-05,

the Corporation‟s Pension & Group Business contributed Rs.3666.56 crore.

b. The segment of Individual Pension Plans also posted an astronomical growth rate of462 percent in First Premium income and 337 percent in policies. The Single Premium

plans and Bima Nivesh have also done extremely well, posting a growth rate of 132

percent.

c. In the segment of Pension and Group Business also, LIC has achieved a growth rate

of 42 percent in the number of lives covered. In spite of the intensifying competition, the

market share of LIC‟s Pension and Group Business has shown an increasing trend and

is expected to go up further.

d. LIC‟s Total Income (provisional) for the year 2004-05 amounts to Rs.106540 crore(growth rate – 14.45 percent) and the Total Assets as on March 2005 stand at

Rs.462000 crore (growth rate of 25.76 percent). LIC has settled 1.073 crore of Total

Claims during the year 2004-05 (Maturity Claims – 1.034 crore and Death Claims – 0.39

crore) taking forward the spirit on the servicing front as well. LIC in recent times has

made rapid strides towards customer service, leveraging technology to offer quicker and

better services to its customer base (more than 16 crore customers).

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 19/22

e. LIC is on a new growth trajectory surpassing its own past records. LIC has issued

over one crore policies during the current year. It has crossed the milestone of issuing

1,01,32,955 new policies by 15th October 2005, posting a healthy growth rate of 16.67

percent over the corresponding period of previous year.

Mr. A.K. Shukla, Chairman, LIC has expressed his gratitude to the policyholders and

complimented them for their overwhelming response and continued trust in the

Corporation during the Golden Jubilee Year. He assured the public that LIC would

reciprocate this faith reposed by providing even more value added services to the

customers.

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 20/22

CONCLUSION

The data was analyzed using method of least squares. It was found that thebusinesses in India, the business outside India as well as the total business ofLIC are always in an increasing trend. The collected and analyzed data prove that

the LPG is incorporating a positive influence on LIC of India and its performance."Life Insurance Corporation of India : Impact of Privatisation and Performancepresents an in-depth analysis of LIC's performance in respect of variousindicators since the policy of liberalisation was introduced in the country. Theproductivity analysis of the corporation has been carried out using differentparameters. The portfolio management of the corporation has been studied indetail in respect of loans and investments. The impact of privatisation on theperformance of LIC has been evaluated in terms of its market share in variousparameters of insurance vis-a-vis the private players. The book also identifies keydeterminants of the performance of LIC and makes recommendations forimproving it. After privatization LIC still maintained its level on top. LIC had a

tremendous change in its policy, products,schemes. The impact of privatizationon insurance sector was very gud since it brought many new insurancecompanies in market.India is not unique among the developing countries where the insurance

business has been opened up to foreign competitors.we observe that theopenness of the market did not mean a takeover by foreign companies even in adecade. Thus, it is unlikely that the same will happen in India, especially when theforeign insurers cannot have a majority shareholding in any company

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 21/22

BIBLIOGRAPHY:-

infibean.com

Business Today. "The Monitory Group Study on Insurance I and

II."

www.licindia.in

and other information from newspaper and net.

8/4/2019 shreya lic (1)

http://slidepdf.com/reader/full/shreya-lic-1 22/22