Embed Size (px)

Citation preview

Should securities regulation promote equity crowdfunding?

Lars Hornuf & Armin Schwienbacher

Accepted: 8 July 2016 /Published online: 4 April 2017# The Author(s) 2017. This article is published with open access at Springerlink.com

Abstract In this paper, we show that too strong investorprotection may harm small firms and entrepreneurial ini-tiatives, which contrasts with the traditional Blaw andfinance^ view that stronger investor protection is better.This situation is particularly relevant in equitycrowdfunding, which refers to a recent financial innova-tion originating on the Internet that targets small andinnovative firms. In many jurisdictions, securities regula-tion offers exemptions to prospectus and registration re-quirements.We provide an into-depth discussion of recentregulatory reforms in different countries and discuss howthey may impact equity crowdfunding. Building on atheoretical framework, we show that optimal regulationdepends on the availability of an alternative early-stagefinancing such as venture capital and angel finance. Fi-nally, we offer exploratory evidence fromGermany on theimpact of securities regulation on small business finance.

Keywords Equity crowdfunding . Crowdinvesting .

Small business finance . Securities regulation . Investorprotection

JEL classifications G20 . G18 . G38 . K22 . L26

1 Introduction

BWe need to have some experience with [equitycrowdfunding] before we take away the safety net… This is a new and dramatically different proce-dure with a high potential for fraud.^1

John Coffee Jr. (Columbia University)

Securities regulation is a driving policy tool for en-suring strong investor protection and, thus, stock marketdevelopment (La Porta et al. 1997, 1998; La Porta et al.2006). Traditionally, stronger securities regulationsemerged in response to the financial crises, accountingscandals, corporate governance problems, and financialinnovations. For example, the United States (US) Con-gress adopted the Securities Act of 1933 and the Ex-change Act of 1934 in response to the stock marketcrash of 1929 and the resulting Great Depression. Theseregulations were intended to mitigate the informationasymmetries between securities issuers and investors,complementing former state-level legislation in place atthe time. Similar actions were taken in other developedcountries, most recently as a response to the financialcrisis of 2008.

Securities regulation primarily concerns firms, whichseek to place large security issues to the general public.Fervent debate about reforming securities regulation hasarisen from the emergence of equity crowdfunding (alsoreferred to as investment-based crowdfunding,

Small Bus Econ (2017) 49:579–593DOI 10.1007/s11187-017-9839-9

1 Source: Wall Street Journal, 1 May 2014.

L. Hornuf (*)Max Planck Institute for Innovation and Competition,80539 Munich, Germanye-mail: [email protected]

L. HornufDepartment of Economics and Institute for Labour Law andIndustrial Relations in the European Union, University of Trier,Behringstraße 21, 54296 Trier, Germany

A. Schwienbacher (*)Department of Finance and Accounting, Université Côte d’Azur -SKEMA Business School, Avenue Willy Brandt, 59777 Euralille,Francee-mail: [email protected]

securities crowdfunding, or crowdinvesting), which de-scribes a financial innovation in securities issuance thatgives small entrepreneurs access to the general public(Ahlers et al. 2015; Hornuf and Schwienbacher 2016;Vismara 2016a, Vismara 2016b). While transactioncosts made it unlikely in the past that small amountswould be offered to the general public, the Internet nowprovides opportunities to do so. Equity crowdfundinghas therefore become a viable alternative form of exter-nal finance for entrepreneurial firms in countries thatpermit the solicitation of the general public without theissuance of a costly prospectus. In this paper, we inves-tigate the impact of securities regulation on equitycrowdfunding and whether securities regulation shouldpromote equity crowdfunding in order to offer alterna-tive source of finance to entrepreneurial firms.

Traditional research on securities regulation, such asthat by La Porta et al. (1997, 1998), who focus on theimpact of legal rules on stock markets and economicgrowth, considers measures of investor protection thatmostly apply to large and publicly traded corporations.Our approach here is different, because we concentrateon smaller firms, which are most likely to benefit fromavailable exemptions. Regarding the exemptions insecurities law, countries differ along the minimumissuance size that requires compliance with prospectusand registration requirements that define responsibilitiesand liabilities of management concerning informationdisclosure. Such differences enable us to explore theimpact of exemptions and, thus, investor protection forsmall issuances on equity crowdfunding. Therefore, ourapproach takes the perspective proposed by Acs et al.(2016) in that, it examines the impact of country-specific institutional arrangements on the pursuit ofmicro-level opportunities to create and fund newventures.

This paper aims to understand how securities regula-tion affects equity crowdfunding, in particular, the ex-emptions to prospectus and registration requirements. Ina first step, we therefore provide an overview of thelegal regime as well as regulatory reforms that haverecently taken place in different jurisdictions (Section 2).In a second step, we present a theoretical frameworkbased on small firms deciding between raising theirfunds from professional investors (venture capital funds,business angels) and launching an equity crowdfundingcampaign (Sections 3 and 4). Finally, although datacollection is limited because markets are still nascent,we offer the first evidence on how the equity

crowdfunding market is emerging and affected by theregulation in place (Section 5). Consistent with ourpredictions, our empirical analysis indicates that firmsraise inefficiently low amounts of money when theexemptions are restrictive. The German case best evi-dences these funding constraints. Finally, we discusshow the existing rules have performed so far and con-clude (Section 6).

2 Recent reforms promoting equity crowdfunding

In Europe, equity crowdfunding has challenged securi-ties regulation because it makes use of the exemptions,as defined in the national regulation of prospectus andregistration requirements. This enables firms to raiseexternal finance while avoiding incurring significantcompliance costs.2 In many countries, the capital raisedin equity crowdfunding campaigns falls under exemp-tions, most importantly with regard to the total amountof the offer. Other exemptions refer to the maximumnumber of investors to whom the offer is made, theminimum contribution imposed on investors, the mini-mum denomination of the securities offered, and wheth-er the offer is made to qualified investors only.

Recently, regulators around the world have realizedthe economic potential of equity crowdfunding andstarted easing the national securities regulation forcrowdfunding activities that take place in the Internet.At least seven jurisdictions have reformed their securi-ties regulation to suit the needs of equity crowdfundingmore effectively, while also protecting investors fromfraud up to a certain level and reducing legal uncertaintyfor issuing firms. In what follows, we investigate howlegislators have tried to unwind the inefficiency at thefirm level that will be the basis of our theoretical model.The main reforms are summarized in Table 1.

2 The initial compliance costs of a typical IPO often exceed $1,000,000because issuers must conduct a due diligence, hire a legal counsel andunderwriter, pay SEC filing fees, state securities filing fees, stockexchange or OTC registration fees, accounting fees and an increasedD&O insurance premium (Bagley and Dauchy 2003). For equitycrowdfunding, costs are lower because smaller and simpler firms thatdo not seek a public listing make offers. Still, according to DarrenWestlake, founder of the UK portal Crowdcube, costs for such pro-spectus approvals are in the range between £20,000 and £100,000 inthe UK.

580 Hornuf and Schwienbacher

Tab

le1

Overviewof

Reforms

Reform

Maxim

umissue

w/o

prospectus

Maxim

umam

ount

sold

toinvestor

Regulation

of gatekeeper

Disclosurerequirem

ents

Investor

education

Austria

Aternativfinanzierungsgesetz

(AltF

G)2015,previous

reform

ofthe

Kapitalm

arktgesetzin

2013

EUR5,000,000

(previously

€250,000,

before

that

EUR100,000)

Singleissuer

limits

10%

ofnet

investablefinancialassetsor

twicethemonthly

netincom

e;max.E

UR5000

incase

the

investor

hasanetincom

eof

EUR2500

orless

Trade authority

orsecurity

regulator

can

authorize

platform

Minim

uminform

ationdisclosure

regardingtheissuer

andfinancial

instrumentfor

issues

larger

than

EUR250,000(stocksandbonds)

andEUR1,500,000(other

investments)inform

ationdisclosure

requirem

ents(e.g.,annual

statem

ents)required

forissues

upto

EUR5,000,000simplified

prospectus

Belgium

Loi

du25

avril2

014portant

desdispositionsdiverses,

publishedattheofficial

journalM

oniteur

Belge

on7May

2014

nr.36946

EUR300,000if

noinvestor

can

investmore

than

EUR

1000;

otherw

ise,

EUR100,000

Singleissuer

limitEUR1000

for

issues

betweenEUR100,000

andEUR300,000;

nosingle

issuer

limitforissues

below

EUR100,000

France

Ordonnancenr.2014–559of

30May

2014;D

ecret

d’Applicationnr.2014–

1053

of16

Septem

ber

2014

EUR1,000,000

(previously

EUR100,000)

Securities

regulator

authorizes

platform

Obligationof

theissuersto

supply

simplifieddocumentatio

nto

the

investors,butnotsubjecttoapproval

bythesecuritiesregulator

Investorsmustu

ndergo

atest

thatdeterm

ines

theirrisk

profile,the

results

ofwhich

mustb

ein

linewith

the

risksinvolved

inequity

crow

dfunding

Germany

Kleinanlegerschutzgesetz

2015

EUR2,500,000

(previously

EUR100,000)

Singleissuer

limitEUR1000

ofinvestor

does

notw

antto

providepersonalinform

ation);

otherw

ise,twicethemonthlynet

income;max.E

UR10,000

Trade authority

authorizes

platform

Smallinformationleaflet

Italy

Decreto

Legge

n.179/2012

andDecretoLegge

n.33/

2015

EUR5,000,000

(previously

EUR

100,000)*

UK

PS14/4

2014

EUR5,000,000

(previously

EUR

5,000,000)

Aggregatelim

itof

10%

ofnet

investablefinancialassets

Securities

regulator

authorizes

platform

Retailclientsneed

toseek

financialadvice

USA

JOBSact(TitleIII)2012

USD

1,000,000

(previously

US D

0)

Aggregatelim

itof

USD

2000

toUSD

100,000annually

Securities

regulator

authorizes

Iftheoverallamount

oftheissueis

$l00,000

orless,issuersmust

providethemostrecentincom

etax

Fundingportalor

broker-

dealer

needsto

providedis-

closures,including

Should securities regulation promote equity crowdfunding? 581

Tab

le1

(contin

ued)

Reform

Maxim

umissue

w/o

prospectus

Maxim

umam

ount

sold

toinvestor

Regulation

of gatekeeper

Disclosurerequirem

ents

Investor

education

dependingon

theincomeandnet

wealth

funding

portalor

broker-

dealer

returnsandfinancialstatements,

which

mustb

ecertifiedby

the

principalexecutiv

eofficer.Fo

rissues

ofmorethan

$100,000

but

less

than

$500,000,financialstate

mustb

eprovided

andreview

edby

apublicaccountant,w

hoshould

beindependentfrom

theissuer.T

heaccountant

mustu

seprofessional

standardsandprocedures

forthe

review

.For

issues

ofmorethan

$500,000,the

issuer

mustp

rovide

auditedfinancialstatements.

disclosuresrelatedto

risks

andotherinvestor

educa-

tionmaterials.

*OnlyBinnovativestartups^andBinnovativeSME’s^eligible:[a]theincorporationandbusiness

operations

ofthefirm

should

have

takeneffect

nomorethan

48monthsago;

[b]the

managem

entislocatedin

Italy,andthemainbusiness

activ

ities

take

placethere;

[c]theannual

turnover

inthesecond

year

ofbusiness

asstated

inthelastaccountsdoes

notexceed

€5,000,000;businessactiv

ities

ofthefirm

take

placeinItaly;[d]the

firm

does

notand

didnotm

akepayoutstoshareholdersusingprevious

corporateprofits;[e]thesoleor

mainpurposeof

thefirm

istodevelop,produce,andsellinnovativ

eproductsorserviceswith

ahigh-technologicalvalue;[f]the

firm

wasnotestablishedaspartofamerger,de-m

erger,orsaleofacorporation

orcorporateentity;and;[g]thefirm

fulfillsatleastone

ofthefollo

wingconditions:(1)thefirm

investsatleast15%

ofthegreaterof

theannualproductio

ncostsor

theproductio

nvaluein

R&D;(2)

one-thirdof

theem

ployees,who

have

obtained

aPh

D,areenrolledinauniversityPhD

programor

two-thirds

oftheem

ployeeshave

obtained

anacadem

icdegree

orhave

worked

form

orethan

3yearsinaprivateor

publicresearch

institu

tion;or

(3)the

firm

owns

apatenton

anindustrial,biotech

orelectronicsemiconductor

innovatio

nor

owns

therightonasoftware,

which

isregistered

inthepubicsoftwareregister,related

tothepurposeof

thecorporation.

Article[a]does

notapplyto

BinnovativeSM

E’s^.

How

ever,theyneed

toprovidean

audited

balancesheettoinvestors.

582 Hornuf and Schwienbacher

2.1 USA

As a principal rule of the US securities law, securitiesthat are offered to the general public must be registeredwith the SEC. This is to protect investors from securitiesfraud by holding the issuer and underwriter of the secu-rity liable in case of material misstatements or omissionsof material facts. However, to account for the needs ofsmall offerings, exemptions to this rule exist. For exam-ple, accredited investors who can fend for themselves orpublic offers up to $5,000,000 have been exemptedfrom registration with the SEC. However, while theformer exemption does per definition not apply to thelarger crowd, the latter exemption was of no use forequity crowdfunding because the registration at the statelevel was still required, making a geographically dis-persed offer prohibitively expensive.

It was mainly for this reason that the US Congresspassed detailed rules specifically tailored to equitycrowdfunding. On April 5, 2012, the JOBS Act wassigned into law, amending the existing exemptions forraising capital under Section 4(6) of the Securities Act.According to Title III of the JOBS Act (also referred toas CROWDFUND Act), issuers can now raise an over-all amount of up to $1,000,000 during a 12-monthperiod without filing a registration statement with theSEC or at the state level. The legislator tied this exemp-tion, however, to three conditions: the usage of a broker-dealer or funding portal, limitations on the amount thatcan be sold to individual investors, and disclosure re-quirements for the issuers.

According to Section 4(6)(C) of the Securities Act,issuers can now offer or sell securities without a regis-tration statement if the transactions is conducted througha broker-dealer or funding portal as defined inSection 3(a)(4) and Section 3(a)(80) of the SecuritiesExchange Act. In this way, the JOBS Act de factoestablished a private gatekeeper for equi tycrowdfunding issues, which is supposed to ensure thecorrectness and completeness of the securities offered.However, the JOBS Act did not make explicit thatfunding portals would be liable for material misstate-ments or the omission of material facts by the issuer.While the JOBS Act explicitly states that equitycrowdfunding issuers will be liable for such offenses,it could be argued that the liability of the funding portalcan be derived from Rule 10b-5 of the Code of FederalRegulations (CFR) as well as the previous SupremeCourt decisions (Knight et al. 2012).

In addition, the US legislator strives to protect inves-tors through limiting the amount that an investor mayinvest in the entire market (aggregate limit). Accordingto the JOBS Act, this aggregate limit shall not exceedthe greater of either $2000 or 5% of the annual incomeor net worth of an investor if either the annual income orthe net worth of the investor is less than $100,000. If theannual income or the net worth of the investor is equal toor exceeds $100,000, the aggregate limit sold to theinvestor shall not exceed 10% of either its annual in-come or net worth, with the respectively greater valueapplying. In any case, the maximum aggregate limit soldto a single investor shall not exceed $100,000.

Finally, Section 4A(b) of the Securities Act definesthe type of information that must be disclosed to poten-tial investors. If the overall amount of the securities issueis equal to or below $100,000, issuers must provide theirmost recent income tax returns and financial statements,which must be certified by the principal executive offi-cer of the issuer. For issues of more than $100,000 butless than $500,000, financial statements must be provid-ed and reviewed by a public accountant, who should beindependent from the issuer. Furthermore, the accoun-tant must use professional standards and procedures forthe review. For issues of more than $500,000, the issuermust provide audited financial statements.

In summary, the US equity crowdfunding legislationhas not only established a maximum value for offerswithout a prospectus but also set thresholds for theamounts an individual can invest. By considering thecompliance costs associated with the provision of infor-mation, the JOBS Act further outlined a three-step ap-proach on information disclosure. These regulatorymeasures were combined with the establishment of aprivate gatekeeper.

2.2 Selected reforms in the European Union

The prospectus regulation in the EU has been harmo-nized for offers larger than €5,000,000 through direc-tives that were enacted through national implementationlaws by the respective EU member states. Therefore, itis useful to first present EU-level regulation for prospec-tus regulation before discussing the recent reforms un-dertaken by individual jurisdictions.

A main attempt to harmonize regulation on registra-tion statements was made with the Directive 2003/71/EC of 4 November 2003, which specifies when and howa prospectus must be published if securities are offered

Should securities regulation promote equity crowdfunding? 583

to the general public. More recently, it was amended bythe Directive 2010/73/EU of 24November 2010, which,among other things, modified the extent of certain ex-emptions. Exemptions to publishing a prospectus applyif at least one of the following criteria is met:

[a] The offer is addressed solely to qualified investors;[b] The offer is addressed to fewer than 150 natural or

legal persons per member state, other than quali-fied investors;

[c] Investors purchase securities for a total consider-ation of at least €100,000 per investor;

[d] The denomination per unit amounts to at least€100,000; and

[e] The offer of securities represents a total consider-ation of less than €100,000 over a 12-monthperiod.

In addition to these exemptions, Directive 2010/73/EU allows national regulators of the EU member statesto increase the amount in point [e] up to €5,000,000.

2.2.1 Italy

The Italian legislator amended the existing securitieslaw (TUF, Testo Unico della Finanza) and adoptedthe first specific equity crowdfunding legislation inEurope. On October 20, 2012, the Decreto Legge n.179/2012 went into effect. Exemptions now apply toinnovative startups and after the implementation ofDecreto Legge n. 33/2015 in 2015 also to innovativesmall and medium-sized enterprises (SMEs) thatoffer common equity shares via online portals.Innovative startups and SMEs complying with thelaw can now make offerings of up to €5,000,000without the obligation to register a prospectus. Thelegal definition of an innovative startup and SMEs isgeared to firms, which are not registered with aregulated market or a multilateral trading facilityand fulfill a lengthy catalog of criteria (see Table 1for further details). Although the Italian securitiesregulator Consob was required to set up a publicregister and define disclosure requirements forinnovative startup and SME issuers, it did not haveto define which exemptions and critical threshold forissues without a prospectus would apply for non-innovative startups and SMEs. In summary, theItalian equity crowdfunding regulation established

a very narrow exemption, which might lead to aconsiderable amount of legal uncertainty.

2.2.2 Austria

In July 2013, the Austrian legislator changed the nationalsecurities law (KMG, Kapitalmarktgesetz) and raised thecritical threshold for issues without a prospectus from€100,000 to €250,000. In October 2013, the first equitycrowdfunding was then offered to investors by the portal1000×1000, with the first issuer Woodero raising a total of€166,950 after a nearly eight-week funding period. Theamount clearly exceeded the initial value of the criticalthreshold for issues without a prospectus, indicating thatissuers would have been constrained under the earlierregulation. In 2015, Austria adopted a new regulation(Alternativfinanzierungsgesetz; see Schwienbacher 2016,for a discussion) and allows issues up to €5,000,000requesting only a very simplified prospectus from theissuer (see the Alternativfinanzierings-Informations-verordnung).

2.2.3 UK

In the UK, equity crowdfunding currently takes placeunder the general securities regulation, more preciselythe Financial Services and Markets Act 2000. In Octo-ber 2013, the Financial Conduct Authority (FCA) initi-ated a consultation on a specific equity crowdfundingregulation. The new rules were enacted in April 2014and aim to make equity crowdfunding Bmore accessibleto a wider, but restricted, audience^ of investors, whilealso ensuring that Bonly those retail investors who canunderstand and bear the various risks involved are in-vited to invest in unlisted shares or debt securities^. TheFCA only allows the brokering of securities to sophis-ticated investors, high net worth investors, corporatefinance contacts, or venture capital contacts, retail cli-ents who confirm that they will receive regulated invest-ment advice or investment management services froman authorized person, or retail clients who certify thatthey will not invest more than 10% of their net investibleassets in unlisted shares or unlisted debt securities.

2.2.4 France

As a member state of the EU, France implemented theProspectus Directive 2010/73/EU and thus applies thesame rules as other EU jurisdictions, with some

584 Hornuf and Schwienbacher

adaptations. The exemption for security offers with atotal amount of less than €100,000 holds. However, forthe range between €100,000 and €1,000,000, an addi-tional exemption applies if the total amount raised doesnot exceed 50% of the existing equity capital of the firm.For example, a firm can raise €200,000 without a pro-spectus and registration if it already possesses equitycapital of at least €400,000. This is unlikely to occur forfirms relying on equity crowdfunding, because theygenerally have little capital on the balance sheet beforea successful campaign. The French portal Anaxago doesnot use the €100,000 limit to exempt firms from theprospectus regulation but rather limits the offer to fewerthan 150 non-accredited investors. Consequently, inves-tors are required to participate with high minimumtickets, as only a subset of the solicited people mayeventually invest. The advantage is that the total amountof the equity issuance is not limited to €100,000. For theofferings successfully completed so far, the averagenumber of crowdinvestors on Anaxago is 25, with anaverage amount raised of more than €320,000.

Importantly, French portals need to obtain a licensefrom the French securities regulator AMF becausethey act as financial intermediaries and thus are sub-ject to their own rules. The former legal status andrequirements in terms of capital imposed on financialintermediaries made it costly for portals to comply.On February 14, 2014, the ministry of economicaffairs and finance announced measures to facilitateequity crowdfunding that have become effective inautumn 2014. Among other things, the new regulationcontains the following items:

[a] The creation of a special legal entity for accreditedequity crowdfunding portals, which differs fromthe one that other financial intermediaries use (so-called Conseiller en Investissement Participatif).No minimum equity capital is required for thislegal entity. However, it must comply with trans-parency rules that ensure that the crowd obtainsBfair^ and Bunbiased^ information on the offers.

[b] Investors must undergo a test that determines theirrisk profile, the results of which must be in linewith the risks involved in equity crowdfunding.Crowdinvestors must also be made aware whenregistering at the portal of the risks involved inequity crowdfunding.

[c] The threshold of exemption is increased to€1,000,000, provided the equity crowdfunding

campaign takes place on an Internet portal thathas received formal approval from the AMF.

[d] Obligation of the issuers to supply simplified doc-umentation to the investors, as described in thereform (but not subject to approval by the AMF).

2.2.5 Belgium

In 2014, Belgium introduced a reform as a way to fosterequity crowdfunding while at the same time actingcautiously to avoid a bubble. The new regulation allowsissuances up to €300,000 provided no investor isallowed to invest more than €1000 per campaign. Un-like in the USA, the Belgian regulator has defined theamount that an investor may invest in the same issuer(single issuer limit) not the overall market. The lawrequires that issuers explicitly state this single issuerlimit in the offer. If the single issuer limit is not imposed,issuers remain limited at raising no more than €100,000.However, the Belgian market remains small and mostoffers are even today below €100,000.

2.2.6 Germany

Unlike other European countries, Germany recently passeda specific legislation and for a long time followed a laissez-faire approach towards equity crowdfunding, which hadtaken place within the scope of the existing securities law.As a general rule, the German Securities Prospectus Act(WpPG, Wertpapierprospektgesetz) and the InvestmentAct (VermAnlG, Vermögensanlagengesetz) set the criticalthreshold for security and investment issues without aprospectus equal to €100,000 (Section 3 Abs. 2 Satz 1Nr. 5 WpPG). However, the definition of what constitutesan investment under the Investment Act was not all-encompassing and left out subordinated profit-participating loans. This omission left scope for the issuerseither to comply with the existing exemptions and raise upto €100,000 or to bypass the relevant laws altogether bystructuring the investment contract in a way that allowedfor offers of unlimited amounts.

On 23 April 2015, the German Parliament passed theSmall Investor Protection Act (Kleinanlegerschutzgesetz)to regulate equity crowdfundingmore specifically.Accord-ing to the new regulation, firms can offer up to €2,500,000without the obligation to register a prospectus. Similar tothe US JOBS Act, the amount sold to a single investorshall generally not exceed €1000. Investors might invest

Should securities regulation promote equity crowdfunding? 585

up to €10,000 per campaign if their wealth exceeds€100,000. If the investor does not have that amount ofassets, the limit is twice the investor’s monthly net income,but in any case not more than €10,000. Most importantly,this new rule again holds only for specific forms of invest-ments (subordinated profit-participating loans), which didpreviously not fall under the definition of an investment.For other types of investments, which are commonly usedin crowdfunding campaigns as well (silent partnershipsand non-securitized participation rights), firms will onlybe able to offer €100,000 without the obligation to registera prospectus (Klöhn et al. 2016).

3 Model description

In this section, we develop a theoretical framework thatallows us to examine the impact of exemptions to pro-spectus regulation on the fundraising decisions of smallfirms, who can decide between active, professional in-vestors (such as venture capital funds or business an-gels), and the crowd (general public). Themodel offers asetting that considers the issuance of non-listed securi-ties without a registered prospectus. It focuses on themain exemption from the prospectus regulation, namely,the total amount of the offer. The proposed analysis willhelp understand how the emergence of equitycrowdfunding as an alternative source of equity financeto professional investors affects the firm’s choice offinancing source and ultimately optimal regulation. Thisin turn may offer guidance in the question whetherregulation should promote equity crowdfunding.

To this end, we rely on a theoretical framework that isbased on managerial rent diversion (Shleifer andWolfenzon 2002). Managers divert rents away when notproperly monitored. While professional investors are as-sumed able to cope with such managerial inefficiency, thecrowd is assumed not able to adequately monitor themanagement. Further, we introduce the fact that the twotypes of investors offer adding value, either through activeparticipation in the firm by professional investors(Gompers and Lerner 2000) or wisdom of the crowd inwhich crowdinvestors offer their ideas and feedback to theentrepreneur (Hornuf and Schwienbacher 2016).3 In order

to be agnostic about the absolute size of these two forms ofadditional value, we focus on the difference between thetwo. To abstract from discounting future values and with-out loss of generality, let us assume all the parties are risk-neutral and the risk-free rate equals zero. This simplifyingassumption implied a discount rate of zero.

3.1 Issuing firms

We consider an economy populated by a continu-um of firms uniformly distributed along the capitalneeds dimension θ̃~[0;Θ], which specifies the levelof their individual investment opportunities. Firmshave a return on investment (ROI) of vi > 0 (iden-tical for all firms), with i ϵ {C,P}, up to the levelθ̃ and 0 beyond. Thus, the amount θ̃ representsexternal capital needs as well as desired invest-ment size. Subscript C corresponds to equitycrowdfunding, while P to professional investors.We consider that the type of financing affects theROI, since each type of investor may add value.

Under this setting, a firm raising and investingan amount θ ≤ θ̃ will generate a value of (1 + vi)θ, resulting in a net present value (NPV) of viθ. Ifnot adequately monitored, entrepreneurs can diverta fraction δ > 0 of the NPV so that shareholderseventually receive only a value of (1-δ)viθ. Entre-preneurs privately receive (1-x)δviθ from this di-version, where 0 ≤ x ≤ 1; the remaining fraction x(i.e., the value xδviθ) is lost so that it generates aninefficiency for all shareholders. Entrepreneurs areimpacted in two ways: as shareholders, entrepre-neurs lose value due to diversion in a similar wayas any other shareholder; as managers, they gainas they divert some value privately. Depending onthe relative size of the two opposing effects, en-trepreneurs may overall gain or lose. To restrictthe analysis to the case in which diversion isoptimal in the absence of adequate monitoring,we impose the following condition under equitycrowdfunding (the derivation is provided in thenext section):

Diversion Condition : x < 1= 1þ vcð Þ 1− fð Þ½ �

The diversion condition ensures that, in equilibrium,entrepreneurs will divert corporate resources whenever

3 The crowd may at times also enjoy other, non-financial benefits fromparticipating as shareholder in the development of startups(Belleflamme et al. 2014). We abstract from these extra benefits here,as these are more likely to be important in other forms ofcrowdfunding.

586 Hornuf and Schwienbacher

they are not constrained by shareholders or regulation. Ifthe condition is not met, then the entrepreneur will notdivert any resources even in the absence of monitoringsince he would lose more in profits as shareholder thanwhat he gets from diverting privately.

3.2 Funding choices: professional investors versusequity crowdfunding

We assume that firms have no internal funds availableand thus need to raise the entire capital externally. Forsimplicity, we assume that the entrepreneur initiallyowns 100% of the firm. When raising capital, entrepre-neurs give up a fraction (1-α) of the equity, with0 ≤ α ≤ 1. The value of α is determined so that thecrowd or professional investors are willing to investunder a take-it-or-leave-it offer, while facing an oppor-tunity cost of 0.

Professional investors can enforce internally ef-fective governance rules. They traditionally do en-force contracts, because they hold larger equitystakes and participate on the board of directors.Moreover, they generally draft tailored contractsthat enable effective intervention in case foundersdo not behave due diligently. However, interven-tion by professional investors is time-consumingand thus costly. For costs, we define them by thevariable M > 0. We regard costs M as monitoringand management costs4 that investors incur.

To derive practice-relevant implications, we in-troduce the fact that the availability of financefrom professional investors varies across countries.While venture capitalists and business angels arewell-developed and able to inject very largeamounts in startups in some countries like theUSA, these amounts tend to be smaller in othercountries especially in continental Europe. Thus,let us consider the maximum amount professionalinvestors can provide to be denoted by S. Theparameter S proxies for the development of theventure capital and business angel market in acountry. This assumption can be motivated by thefact that the size of venture capital funds variesacross countries due to a smaller supply of capital

to the venture capital markets, combined with thestandard restrictions that venture capital funds typ-ically cannot invest more than a certain amount orpercentage of total funds in a single portfoliocompany (Metrick 2007).

The second source of funding considered here isequity crowdfunding. Crowdinvestors may want toimpose similar corporate governance and disclo-sure rules that mitigate agency costs. However,even if such governance rules were included in acontract, crowdinvestors could not enforce thembecause of coordination problems that result fromfree riding. The crowd is dispersed and ratherpassive. We consider this to be a reasonable as-sumption for the market, given the type of indi-viduals participating in equity crowdfunding cam-paigns. In addition, the crowd does not sit on theboard of directors of the firms.

Portals incur costs from managing the websiteand preparing the firm for the campaign, includingdrafting investment contract and some of the basicdue diligence. In practice, these costs are passedon to the firms. We consider a percentage fee,since the bulk of the portals use such a fee struc-ture. Let us define the fee by f > 0, which ischarged to the firm after a successful campaign.

3.3 The regulator

The regulator imposes registration and ex antedisclosure requirements for any security offer tothe general public above a given threshold amountT ≥ 0, which can be larger or smaller than S. Thisview is consistent with real-world exemptions, aswe have shown in Section 2. A higher thresholdvalue of T implies a lower investor protection ingeneral, because fewer firms comply with securi-ties regulation.

Complying with these requirements leads to fixedcosts of C > 0 for the firms, which may differ frommonitoring costs M incurred by professional investors.These compliance costs may arise for different reasons;some may be incurred by filing with the regulator, whileothers may be due to the disclosure of relevant informa-tion to investors. We assume firms complying withdisclosure regulation can no longer divert value forprivate purposes. Consistent with practice, we assumethat firms can only seek compliance with the regulator iftheir capital needs are larger than T. In what follows, we

4 UnderM, we consider any costs other than B‘effort costs^’ that wouldlead to moral hazard. Thus, we assume costs M as those costs that areborne by investors by the sake of being B‘sophisticated^’. These costsinclude legal costs as well as costs incurred from running a manage-ment firm.

Should securities regulation promote equity crowdfunding? 587

assume that costs C are too high for the firms consideredin our baseline model.

We consider a benevolent regulator who maximizestotal welfare in the economy that is the sum of valuecreated by the firms seeking external finance. Thus, theregulator balances the social costs and benefits generat-ed by setting the variable T.

3.4 Time line

We consider the following time line. At time t = 0, theregulator sets T, which becomes public knowledge. Att = 1, the firm decides whether to raise funds from aprofessional investor or through equity crowdfunding. Att = 2, entrepreneurs make investment decisions, by decid-ing how much to raise and thus offer a fraction (1-α) ofownership. Finally, at t = 3 firms realize their payoffs,which are then distributed. Consistent with rational behav-ior, we solve the game by backward induction and maxi-mize firm value based on the entrepreneur’s perspective.

4Optimal choice of funding and securities regulation

4.1 Optimal outcome for the entrepreneur

In this section, we derive the optimal choice of funding.We first consider the outcome under equitycrowdfunding and professional investors separatelyand then compare them.

Case [1]: under equity crowdfunding, an entrepreneurwith given capital needs θ̃ ≤ T receives α[(1 +vc)θ̃(1 − f) − δvcθ̃(1 − f)] + (1 − x)δvcθ̃(1 − f), subject tothe crowd at least breaking even in their investment:(1 − α)[(1 + vc)θ̃(1 − f) − δvcθ̃(1 − f)] = θ̃. The first termin the first equation represents the financial gains to theentrepreneur of also being a shareholder (net of diversioncosts δvcθ̃(1 − f)), the second one (1 − x)δvcθ̃(1 − f) herprivate benefits from diversion.5 This leads to the

following gains for the entrepreneur: (1 − xδ)vcθ̃(1 − f).Any firm with θ̃ > T will not raise more than T, asotherwise the firm would need to obtain a costly prospec-tus approval; thus, gains are capped at (1-xδ)vcT(1-f). Theportal receives the total fees of fθ̃ from the firm raising θ̃.

Case [2]: under professional investor finance, theentrepreneur will raise a capital amount of θ̃ ≤ S andreceives α(1 + vp)θ̃, subject to investor at least breakingeven in the investment: (1 −α)(1 + vp)θ̃ = [θ̃ +M]. Here,only financial returns accrue to the entrepreneur, sinceno diversion takes place. Thus, the entrepreneur receivesvpθ̃ −M. Any firm with θ̃ > S will have its gains cappedat vpT − M.

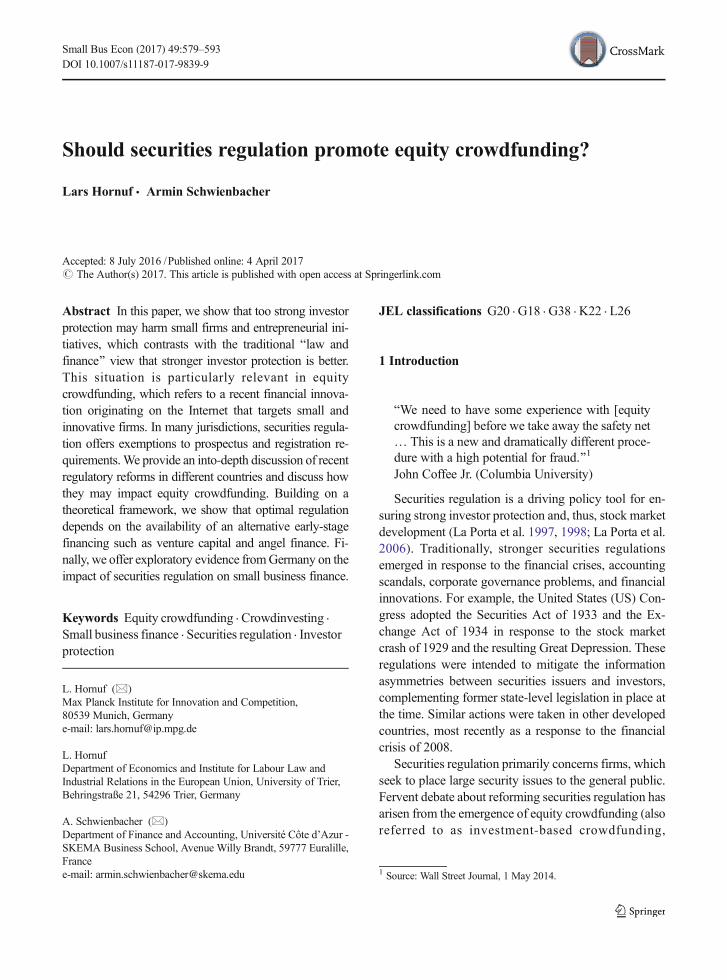

Both outcomes under [1] and [2] are depicted inFig. 1 whenever S > T. It is straightforward to derivethe threshold level of T, called Ṯ that makes equitycrowdfunding as efficient as professional investors:

T�

such that 1−xδð Þvc T�1− fð Þ ¼ vp T

�−M or :

T�¼ M=

"vp− 1−xδð Þvc 1− fð Þ

#

Therefore, equity crowdfunding is the optimal choiceof entrepreneurs seeking capital lower than Ṯ, and oth-erwise opting for professional investors is optimal.Above the amount S, professional investor can no longersupply the full amount, so that the firm needs to seekprospectus approval from the regulator. Note that feescharged by portals also affect the threshold, since feesreduce the amount left for investments and thus theoverall profitability of the firm. Higher portal fees re-duce profits under equity crowdfunding, making it lessattractive relative to professional investors. The result isa lower Ṯ. Moreover, differences in adding value be-tween the crowd (vc) and professional investors (vp) shiftthe threshold Ṯ. An increase in vc relative to vp increasesṮ, which is consistent with equity crowdfunding becom-ing more profitable and thus more attractive relative toprofessional investors.

When S < T (the venture capital and angel market ispoorly developed), a discontinuity occurs. The size ofthe discontinuity depends on the magnitude of the dif-ference between S and T, as depicted in Fig. 2. Also,there is an area (gray shaded in Fig. 2) that representsfirms with capital needs (θ̃) that are larger than thethreshold T. These firms can only raise the amount T,since raising more would lead to less profit due to thelack of larger amounts from professional investors and

5 These simple formulas allow to formally derive the Diversion Con-dition, where we need to solve the following condition α[(1 +vc)θ̃(1 − f) − δvcθ̃(1 − f)] + (1 − x)δvcθ̃(1 − f) > α[(1 + vc)θ̃(1 − f)],subject to (1 − α)(1 + vc)θ̃(1 − f) = θ̃. The left-hand side of theinequality is the entrepreneur’s profits under equity crowdfundingwhen diverting value from shareholders (as stated above); the right-hand side is her profits when not diverting; finally, the second equationgives the equilibrium financing condition for the crowd under theassumption that the entrepreneur does not divert any profits. Substitut-ing α from the second equation into the inequality leads to the Diver-sion Condition as stated above.

588 Hornuf and Schwienbacher

excessive inefficiencies under equity crowdfunding.These firms consequently forego some of their invest-ment opportunities, because there is no source of capitalavailable to (efficiently) fund them.

It is optimal for the entrepreneur to seek equitycrowdfunding below Ṯ for the same reason as above,but potentially also for larger amounts if the small offerexemption level T is large enough to make it worth-while. In the case depicted in Fig. 2, this is not happen-

ing, but would happen if Twould be as large as T . Then,larger equity crowdfunding campaigns would occur. Tcan formally be derived as the solution to the followingcondition (assuming investors under prospectus approv-al add as much value as professional investors consid-ered so far; i.e., vp):

1−xδð ÞvcT 1− fð Þ ¼ vpT−C or :

T ¼ C.

vp− 1−xδð Þvc 1− fð Þ� �

4.2 Market equilibrium under endogenous regulation

Figures 1 and 2 are helpful in deriving the optimal level ofexemption, denoted below as T*, from the perspective ofthe securities regulator. This level is affected by the degree

of development and efficiency of the venture capital andbusiness angel market. However, a note is warranted here.Our optimal outcome abstracts from effects that suchexemptions may have on the other firms seeking equityfinance. Therefore, we will consider below the lowestpossible exemption value as being the optimum, as it alsominimizes any impact on other firms in the economy.

Formally, the optimal level of exemption for equitycrowdfunding is as follows:

T* ¼ T if T < S T* ¼ T if T > S

This result yields the following empirical implica-tions. First, a more developed venture capital and busi-ness angels market enables a lower threshold Ṯ, since ithas a higher S (professional investors can finance firmswith larger capital needs as their funds are larger) andlower M (professional investors are able to do morecost-efficient contracting and monitoring).6 Thus, itdoes not require the regulator to set a higher level ofexemption. For sufficiently large venture capital and

6 Empirically, costs M may be proxied by the number of law firms andthe quality of legal institutions, as this affects legal costs of draftingcontracts and advising services for venture capital funds.

Financing Outcomes when S>TFig. 1 Financing outcomes whenS > T. INV-finance denotes theoutcome under financing withprofessional investors, ECF-finance with equitycrowdfunding. The x-axisrepresents the amount to beissued, while the y-axis theentrepreneur’s profit level. Thepoint Ṯ corresponds to thesituation where the entrepreneuris indifferent between the twofinancing alternatives

Should securities regulation promote equity crowdfunding? 589

business angel markets, the exemption level can even besubstantially reduced.

Moreover, when S > T (the more general case),the condition derived above indicates that Ṯ is de-creasing in the following, exogenous parameters:extent of managerial rent diversion (the parameterδ), the degree of losses derived from such diversion(the parameter x), and portal fees (the parameter f).For the ROI, the direction of impact depends onwhether we consider vc or vp, as discussed above.A greater rent extraction possibility creates a highercost of capital under equity crowdfunding, sincecrowdinvestors will require a higher rate of returnfor purchasing securities from the firm. Similarly,greater losses from diversion and higher portal feesmake again equity crowdfunding less valuable rela-tive to professional investors, which reduces theoptimal level of exemption.

For the opposite case where S < T (see Fig. 2), theregulator has an incentive to increase T to compensatefor shortage of professional investors. The optimal level

is T . This scenario corresponds to cases in which ven-ture capital and business angel markets are underdevel-oped. Overall, we expect regulators in countries withsmaller venture capital and business angel markets tohave incentives to set less restrictive exemptions.

4.3 Empirical implications

The parameter T can be directly interpreted as the levelof investor protection, in which a lower value of Trepresents more investor protection on average. Theconclusions of our theoretical model lead to the follow-ing empirical predictions. First, more investor protectionleads to fewer equity crowdfunding campaigns, sincethe bulk (if not all) of these campaigns take place undersecurities regulation exemptions. This may eventuallycreate a smaller equity crowdfunding market, becausemany firms will find it economically not worthwhile toseek prospectus approval by the national regulator.Others may seek financing from professional investors.In the absence of any exemptions, smaller firms may

Financing Outcomes when S<T

Fig. 2 Financing outcomes when S < T. INV-finance denotes theoutcome under financing with professional investors, ECF-financewith equity crowdfunding. The red line shows the outcome with aformal prospectus for either traditional capital markets or equitycrowdfunding campaigns above the small offerings exemption T,for which amounts of issuancesmust be larger than the threshold T.The x-axis represents the amount to be issued, while the y-axis theentrepreneur’s profit level. The point Tcorresponds to the situation

where the entrepreneur is indifferent between equity crowdfundingand financing with a formal prospectus (if the threshold wherelarge enough to allow equity crowdfunding campaigns to be largerthan , which is not the case in this figure; therefore, this range ofoutcomes is indicated in a dotted box at the top of the figure asBECF^). The dotted part of the black and red lines representspossible outcomes if the regulator changes T

590 Hornuf and Schwienbacher

even refrain from entering the market in the first place,since equity crowdfunding may be their only option interms of equity finance. The complete absence of anexemption (T = 0) leads to an exclusion of firms with thelowest capital needs, which would not be started in thefirst place. This is especially true if there is not a suffi-ciently large, professional market available as mainalternative source of seed capital.

Our main conclusion from this analysis is that regu-lation maximizing investor protection hurts small firmsand those relying on equity crowdfunding are likely tobe smaller firms seeking seed or early-stage capital. Thisis because these firms are too small to obtain fundingfrom professional investors and thus may lack alterna-tive sources of equity capital. Optimal securities regula-tion therefore has to trade off the costs of ensuringsufficient investor protection with the benefit of easieraccess to capital for startup firms, which can be animportant driver for economic growth.

The extent to which exemptions to the prospectusregulation are needed depends on the availability ofalternative sources of capital, mostly from professionalinvestors. Countries with well-developed markets ofprofessional and private investors may have fewer ex-emptions. Interestingly, the USA has a well-developedprofessional investor market, which can compensate forthe lack of exemptions needed to tap the crowd. Thiscontrasts with Europe, where the angel and venturecapital markets are smaller.

We further expect a substitution to occur away fromprofessional investors, not for firms with lower capitalneeds but with average levels. With equity crowdfunding,these firms now have an alternative source of funding. Forsome firms, the latter may economically be more interest-ing, so that they seek funding from the crowd instead ofprofessional investors. In fact, changing the level of smalloffer exemption T may have no impact on equitycrowdfunding activities in business sectors that are well-covered by professional investors, except for very smallissuances. However, other areas may be affected morewhen poorly covered by professional investors. This maybe more likely in areas with limited growth prospects.

5 Are existing exemptions too restrictive: someempirical evidence

In this section, we illustrate the impact of exemptions asdefined in national securities regulation on equity

crowdfunding campaigns. To achieve this goal, we offerevidence that restrictive exemptions may create afunding gap, where firms raise inefficiently lowamounts of capital.

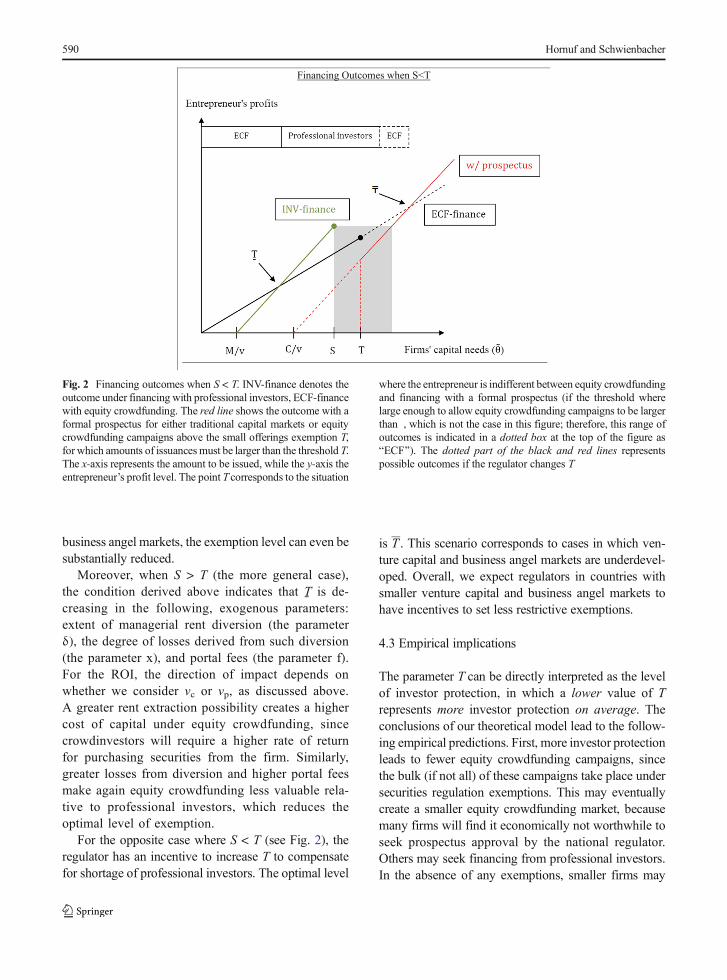

As our theoretical model predicts, firms may re-strict their fundraising goal if the small offer exemp-tion threshold is low. One good example is Germa-ny, which after the UK possesses one of the mostdeveloped equity crowdfunding market in Europe(Hornuf and Schmitt 2016) but for a long time setthe critical threshold for the small offerings exemp-tion at the lower bound of €100,000. We illustratethat this regulation created a funding gap by relyingon the cases of Seedmatch and Companisto. More-over, like many other continental European coun-tries, the German venture capital and business angelmarkets are much less-developed than in countriessuch as the USA and the UK.

The contracts that Seedmatch provided to issuerswere initially designed to comply with the GermanInves tment Act . Al l the in i t i a l 26 equi tycrowdfundings offered by Seedmatch used theexisting exemption, and a total of 24 issues had tobe terminated at the threshold of the exemption at€100,000, which indicates that issuers had highercapital needs. Moreover, as campaigns were some-times funded very quickly,7 firms’ capital needscould have easily been satisfied by the crowd andwere only constrained by the existing threshold un-der the Investment Act (see Fig. 3).

Seedmatch and other portals soon realized thelegally imposed funding constraint and tried to cir-cumvent the existing securities legislation. On No-vember 29, 2012, Seedmatch offered for the firsttime subordinated profit-participating loans, whichuntil July 10, 2015 were not classified as investmentunder the German Investment Act and thus did notrequire the registration of a prospectus. While therewas some legal uncertainty surrounding this issue,subordinated profit-participating loans allowed is-suers to raise unlimited amounts without the obliga-tion to draft and register a prospectus.

The equity crowdfunding campaigns on Companistoshow a similar trend after the portal switched contracts

7 On November 29, 2012, it took Protonet only 48 min to raise€200,000 on Seedmatch. In May 2014, the same firm raised another€1,500,000 in 10 h and 8 min, after which the founders decided tocontinue raising funds. Eventually, they raised €3,000,000 in a fewdays only.

Should securities regulation promote equity crowdfunding? 591

to subordinated profit-participating loans on February4, 2013. After the implementation of the new invest-ment contract, the funding volumes per campaignmore than sextupled on Companisto, while onSeedmatch they almost quadrupled. The largest issuefunded under this contractual design raised a total of€7,500,000 for a real estate project. A comparisonwith Innovestment, which might serve as a controlgroup because the portal has not adopted subordinatedprofit-participating loans, evidences that the increasein funding volumes does not merely reflect a generaltrend in the selection of funding campaigns. The

average funding size at Innovestment was €60,085,somewhat below the threshold of €100,000, and in-creased only slightly to €64,796 in the period whenSeedmatch adopted subordinated profit-participatingloans.

6 Discussion and concluding remarks

This study discusses recent reforms in different countriesand presents some empirical evidence based on the Ger-man experience in permitting non-accredited investors

7.5 m

Seedmatch

Companisto

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

9/1

/11

11/1

/11

1/1

/12

3/1

/12

5/1

/12

7/1

/12

9/1

/12

11/1

/12

1/1

/13

3/1

/13

5/1

/13

7/1

/13

9/1

/13

11/1

/13

1/1

/14

3/1

/14

5/1

/14

7/1

/14

9/1

/14

11/1

/14

1/1

/15

3/1

/15

5/1

/15

7/1

/15

9/1

/15

11/1

/15

1/1

/16

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

9/1

/11

11/1

/11

1/1

/12

3/1

/12

5/1

/12

7/1

/12

9/1

/12

11/1

/12

1/1

/13

3/1

/13

5/1

/13

7/1

/13

9/1

/13

11/1

/13

1/1

/14

3/1

/14

5/1

/14

7/1

/14

9/1

/14

11/1

/14

1/1

/15

3/1

/15

5/1

/15

7/1

/15

9/1

/15

11/1

/15

1/1

/16

Innovestment

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

9/1

/11

11/1

/11

1/1

/12

3/1

/12

5/1

/12

7/1

/12

9/1

/12

11

/1/1

2

1/1

/13

3/1

/13

5/1

/13

7/1

/13

9/1

/13

11

/1/1

3

1/1

/14

3/1

/14

5/1

/14

7/1

/14

9/1

/14

11/1

/14

1/1

/15

3/1

/15

5/1

/15

7/1

/15

9/1

/15

11/1

/15

1/1

/16

Fig. 3 Amounts raised in equitycrowdfunding campaigns onSeedmatch (N = 84), Companisto(N = 47), and Innovestment(N = 47) in the period fromAugust 1, 2011 to January 1,2016. The red lines separate theperiod before and aftersubordinated profit-participatingloans were used to circumvent thethreshold of the small offeringexemption as defined in theGerman securities law(T = €100,000). Before financialcontracts circumvented thethreshold, the average amountsraised were €98,048 forSeedmatch campaigns and€91,673 for Companisto cam-paigns; thereafter, the amountsrose to €391,440 and €596,827,respectively (including amountspledged in unsuccessful cam-paigns). Innovestment neverchanged its investment contract tocircumvent the threshold of theGerman securities law and ex-hibits an average funding amountof €60,085 per campaign(including amounts pledged inunsuccessful campaigns).

592 Hornuf and Schwienbacher

access to equity crowdfunding.While our analysis remainsexploratory, it contributes to the ongoing policy debate onhow to regulate the market and to examine its potentialimpact on business finance. This debate is motivated bythe fear expressed by some regulators and academics thatentrepreneurs may take advantage of the less sophisticatedcrowd, by strategically avoiding to raise capital from so-phisticated investors (Hazen 2012; Griffin 2013).

Our simple theoretical framework generates keypolicy implications in relation with alternative sourcesof entrepreneurial finance. A central implication is thatbenefits related to weaker investor protection that pro-mote equity crowdfunding markets are higher when theavailability of venture capital and angel capital is scarce.The notion that strong investor protection can be harm-ful is counter-intuitive to the traditional law and financeliterature that focuses on large firms. A tailored regula-tion may therefore be needed for equity crowdfunding,as securities regulation primarily deals with regulatinglarge issuances and therefore impose significantcompliance costs that are prohibitively high for smallfirms. Moreover, a lack of specific regulation for equitycrowdfunding may induce portals to resemble onlineangel networks and thus offer little differentiation withexisting sources of entrepreneurial finance.

Acknowledgments Open access funding provided by MaxPlanck Society. This article evolved as part of the researchproject ‘‘Crowdinvesting in Germany, England and the USA:Regulatory Perspectives and Welfare Implications of a NewFinancing Scheme,’’ which was supported by the GermanResearch Foundation (Deutsche Forschungsgemeinschaft) un-der the grant number HO 5296/1-1. We thank Jörn Block,Mariela Borell, Massimo Colombo, Douglas Cumming, SofiaJohan, Adair Morse, Casimiro Nigro, Jay Ritter, SilvioVismara, two anonymous referees as well as the participantsof the Second UC Berkeley Crowdfunding Symposium inBerkeley, the Second Crowdinvesting Symposium in Munich,the 2014 annual conference of the Canadian Law and Eco-nomics Association (CLEA) in Toronto, the 2014 annualconference of the European Association of Law and Econom-ics (EALE) in Aix-en-Provence, the 2014 Mannheim-ZEWConference on Financial Regulation and Competition, the2015 Workshop of Entrepreneurship and Innovation in Trier,and the 2016 Goethe/Penn Conference on Law and Financefor their comments.

Open Access This article is distributed under the terms of theCreative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestrict-ed use, distribution, and reproduction in any medium, providedyou give appropriate credit to the original author(s) and the source,provide a link to the Creative Commons license, and indicate ifchanges were made.

References

Acs, Z. J., Audretsch, D. B., Lehmann, E. E., & Licht, G. (2016).National systems of entrepreneurship. Small BusinessEconomics, 46(4), 527–535.

Ahlers, G. K. C., Cumming, D., Günther, C., & Schweizer, D.(2015). Signaling in equity crowdfunding. EntrepreneurshipTheory and Practice, 39(4), 955–980.

Bagley, C.E. and Dauchy, C.E. (2003) The entrepreneur’s guide tobusiness law, 3rd Edition, Thomson West.

Belleflamme, P., Lambert, T., & Schwienbacher, A. (2014).Crowdfunding: tapping the right crowd. Journal ofBusiness Venturing, 29(5), 585–609.

Gompers, P., & Lerner, J. (2000). Money chasing deals? Theimpact of fund inflows on private equity valuation. Journalof Financial Economics, 55, 281–325.

Griffin, Z. J. (2013). Crowdfunding: fleecing the Americanmasses. Case Western Reserve Journal of Law, Technology& the Internet, 4(2), 375–410.

Hazen, T. L. (2012). Crowdfunding or fraudfunding? Socialnetworks and the securities laws—why the speciallytailored exemption must be conditioned on meaningfuldisclosure. North Carolina Law Review, 90, 1735–1770.

Hornuf, L., & Schmitt, M. (2016). Success and failure in equitycrowdfunding. CESifo DICE Report, 14(2), 16–22.

Hornuf, L. and Schwienbacher, A. (2016) Crowdinvesting—angelinvesting for the masses? in: Handbook of Research onVenture Capital: Volume 3. Business Angels: Edward Elgar(Ed. C. Mason and H. Landström), 381–397.

Klöhn, L., Hornuf, L., & Schilling, T. (2016). The regulation ofcrowdfunding in the German small investor protection act:content, consequences, critique, suggestions. EuropeanCompany Law, 13(2), 56–66.

Knight, T. B., Leo, H., & Ohmer, A. (2012). A very quiet revolu-tion: a primer on securities crowdfunding and title III of theJOBS act. Michigan Journal of Private Equity & VentureCapital Law, 2, 135–153.

La Porta, R., Lopez-de-Silanes, F., & Shleifer, A. (2006). Whatworks in securities Laws? Journal of Finance, 61, 1–32.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. W.(1997). Legal determinants of external finance. Journal ofFinance, 52, 1131–1150.

La Porta, R., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. W.(1998). Law and finance. Journal of Political Economy, 106,1113–1155.

Metrick, A. (2007). Venture Capital and the Finance of Innovation.Wiley & Sons.

Schwienbacher, A. (2016) . Crowdfunding and the‘Alternativfinanzierungsgesetz’ in Austria. CESifo DICEReport, 14(2), 33–36.

Shleifer, A., & Wolfenzon, D. (2002). Investor protection andequity markets. Journal of Financial Economics, 62, 3–27.

Vismara, S. (2016a). Equity retention and social network theory inequity crowdfunding. Small Business Economics, 46(4),579–590.

Vismara, S. (2016b). Information cascades among investors inequity crowdfunding. Forthcoming: Entrepreneurship Theoryand Practice.

Should securities regulation promote equity crowdfunding? 593

![[Crowdfunding] Equity Based CrowdFunding platform _Opentrade](https://img.dokumen.tips/doc/110x75/58f9bf7e760da32f4b8b490e/crowdfunding-equity-based-crowdfunding-platform-opentrade.jpg)