Embed Size (px)

Citation preview

CHAPTER VI

SERVICE QUALITY, CUSTOMER SATISFACTION AND

PROBLEMS IN INTERNET BANKING

This chapter aims at analyzing the data collected for exploring the service quality

dimensions in IB, the effect of service quality dimensions on customer satisfaction,

exploring the problems encountered during the process of service delivery and the effect

of problems on customer satisfaction. Hence the chapter is divided into three sections.

Section one (6.1) contains service quality dimensions and their effect on customer

satisfaction. Section two (6.2) contains problems and their effect on customer satisfaction

and section three (6.3) presents a discussion of the results from the chapter and their

managerial implications.

6.1 Service Quality Dimensions and their Effect on Customer

Satisfaction

This section presents a brief account of the approach of measuring service quality

used in the study, a description of service quality and customer satisfaction measures,

factor analysis and subsequent labeling of service quality dimensions, relationship and

effect of service quality dimensions on customer satisfaction.

6.1.1 Introduction to Service Quality

The concept of service quality has a journey of number of decades and aroused

attention from the part of researchers owing to lack of consensus in both defining and

measuring it. There has been continued research on the definition and measurement of

service quality concept. Quality represents the degree in which the object (entity) satisfies

user‘s requirements (Batagan et al., 2009). Due to intangible nature of services, quality

plays a pivotal role for the success of service industry. Parasuraman et al., (1985) defined

service quality as the gap between customers‘ expectations of service and their perception

of the service experience. According to Bitner and Hubert (1994) ―service quality is

consumers‘ overall impression of the relative inferiority/superiority of the organization

218

and its services‖. Service quality resides in the ability of the service provider to satisfy the

needs of customers, that is, customer satisfaction (Lewis and Brooms, 1983). Service

quality can be seen as the extent to which a service meets customers‘ needs and

expectations (Lewis and Mitchell, 1994). Traditional service quality refers to the quality

of all non-internet based customer interactions and experiences with companies

(Parasuraman et al., 1988). The advent of internet paved the way for the emergence of the

concept of e-service. E-services have two main characteristics: the service is accessible

with electronic networks and the service is consumed by a person via the internet (Batagan

et al., 2009). Internet Banking satisfies the above two characteristics and therefore service

quality in IB denotes e-service quality. Santos (2003) defined e-service quality ―as the

consumers‘ overall evaluation and judgment of excellence and quality of e-service

offerings in the virtual market place‖. Parasuraman et al., (2005) defined e-service quality

as ―the extent to which a website facilitates efficient and effective shopping, purchasing

and delivery‖.

Two schools of thought concerning the measurement of quality in relation to

services are found in the literature. One is the disconfirmation paradigm of performance-

minus-expectation and the other is performance-based paradigm of a perception only

version service quality. In disconfirmation approach (Gronroos, 1984; Parasuraman et. al.,

1985, 1988) service quality is measured on the basis of disconfirmation between consumer

expectations and perceptions. The first attempt to conceptualize service quality from the

point of view of customers was made by Gronroos and opined that the discrepancy

between expectations and perceptions decides the customers‘ service quality assessment.

Parasuraman et al., (1988) developed SERVQUAL scale and measure service quality as

the difference or disconfirmation between the customers‘ perception (P) and expectations

(E) along 22 variables divided into five dimensions. The problem of measuring

expectation was felt by many researchers in the sense that expectations change from time

to time, and they were also confronted with the problem of when to measure it, either

before or after receiving the service. SERVEQUAL scale as a measure of service quality

has been challenged by several researchers (Babakus and Booler, 1992; Cronin and

Taylor, 1992; Brown et al., 1993; Dabholkar et al., 1996).

219

Babakus and Booler (1992) and Cronin and Taylor (1992) found that perceptions

are a superior predictor of service quality than disconfirmation and subsequently Cronin

and Taylor (1994) developed SERVPERF (SERVice PERFormance) model to measure

service quality based only on customer perceptions. According to this model service

quality is evaluated by perceptions of the customers about the performance of the service

delivered. SERVPERF assumes that customers provide their ratings by automatically

comparing performance perceptions with performance expectations and that measuring

expectations directly as done in SERVQUAL is unnecessary. Many researchers (for e.g.

Jain and Gupta 2004; Andronikidis and Bellou, 2010) proved that SERVPERF is excellent

for measuring service quality and customer satisfaction. Therefore, performance based

paradigm is used in this study to measure service quality and customer satisfaction in the

internet banking context.

There are many measures which determine service quality of internet banking. The

service quality measures used in the study are set out in Table 6.1. A list of 20 statements

related to various service quality dimensions were developed by adding, deleting or

rewording items to ensure suitability for the research context from previous studies

(Nuseir et al, 2010; Khan et al, 2009; Sohail and Shaikh, 2008; Ahangar, 2011; Zarei,

2010) and respondents were asked to rate each statement on a five point likert scale from

‗Strongly agree‘ (5) to ‗Strongly disagree‘ (1).

6.1.1.1 Service Quality Measures

The mean values and standard deviations of service quality measures are given in

Table 6.1.

220

Table 6.1

Service Quality Measures with their Mean and Standard Deviations

Service Quality Measures Item

Acronym

Mean SD

The web site contains useful help facility SQ1 3.87 .753

Website design is attractive SQ2 3.68 .814

Trust in IB services presented on the bank‘s website SQ3 3.96 .612

The bank delivers IB services as promised SQ4 3.84 .756

The website is updated continuously SQ5 3.78 .789

Bank takes care of IB complaints quickly SQ6 3.48 .894

There is quick response from my bank to customer

queries SQ7 3.52 .930

Web pages load promptly SQ8 3.67 .773

Log in to IB website is fast SQ19 3.78 .808

The site provides a confirmation of the service

requested quickly SQ10 3.79 .776

Logout speed of my account is fast SQ11 3.96 .746

Finding what I need is easy and simple SQ12 3.92 .769

Easy options for canceling transactions are provided SQ13 3.48 .880

IB website of my bank always satisfy all my service

needs SQ14 3.67 .858

My personal information is secured and protected in

my bank‘s site SQ15 4.00 .718

The bank will not misuse my personal information SQ16 3.93 .779

Do not feel safe to use IB* SQ17 2.85 1.21

Worried that others may access my IB account * SQ18 3.11 1.19

IB servers may process payments incorrectly * SQ19 3.47 1.20

Banks give no compensation when errors occur* SQ20 3.12 1.19

Source: Primary data. * indicates reverse scale statements. SD– Standard Deviation

Table 6.1 indicates that all the measures except SQ17 are rated by IB users above

three which is the central value in the five point scale. Most of the values are in the

221

neighborhood of four which means that IB users have a favourable response towards the

service quality measures. The standard deviations of service quality measures range from

0.612 to 1.21. In the case of measures from SQ17 to SQ20 which are relating to security

aspects of IB, the standard deviations are comparatively high indicating that IB users‘

opinions are not uniform. This suggests that IB users need much more improved service

quality on these measures.

6.1.2 Customer Satisfaction

Customer satisfaction is a collective outcome of perception, evaluation and

psychological reactions to the consumption experience with a product/service (Yi, 1990).

In the context of IB, customer satisfaction denotes E-customer satisfaction. E-customer

satisfaction is defined as the contentment of the customer with respect to his/her prior

purchasing experience with a given electronic commerce firm (Anderson and Srinivasan,

2003). Researchers have paid much attention to the close relationships between service

quality and customer satisfaction (Parasuraman et al., 1988). Cronin and Taylor (1992, p.

65) pointed out that service quality is an antecedent of consumer satisfaction. High

perceived service quality results in higher customer satisfaction and vice versa. Empirical

studies that examined the relationship between perceived service quality and customer

satisfaction have shown that service quality determines customer satisfaction (Bloemer et

al., 1998; Yavas et al., 2004; Arasli et al., 2005; Culiberg and Rojsek, 2010). Significant

and positive relationship between perceptions of overall service quality and customer

satisfaction is also found in a study conducted by Rod et al., (2009).

The perceived performance based paradigm based on actual performance of a

product or service from customer‘s perspective is used for measuring customer

satisfaction as well. According to Churchill (1987), any single item cannot provide a

perfect representation of the concept and therefore, multi-item measures were used to

capture customer satisfaction of IB services in Kerala. Following Nuseir et al., (2010) who

measured customer satisfaction of e-service quality as a multi-item measure in the context

of commercial banks of Jordan, customer satisfaction is measured as a multi-item measure

222

to indicate the degree of customer contentment with regard to various dimensions of

internet banking service quality. A list of 6 statements as shown in Table 6.2 was used to

measure the level of customer satisfaction in respect of various IB service quality

dimensions and respondents were asked to rate each statement on a five point Likert scale

from ‗Very satisfied‘ (5) to ‗Very dissatisfied‘ (1).

6.1.2.1 Customer Satisfaction Measures

The mean values of customer satisfaction measures given in Table 6.2 indicate that

all the measures are rated above four in the five point scale. It indicates that the

respondents have favourable response towards customer satisfaction measures. Standard

deviations range from 0.643 to 0.751, which indicate that their opinions are almost

uniform.

Table 6.2

Customer Satisfaction Measures with their Mean and Standard Deviations

Customer Satisfaction Measures Item

Acronym

Mean S.D

Fulfillment of service requirements CS1 4.15 .681

Privacy/security of IB transactions CS2 4.14 .699

Reliability and confidence in your bank CS3 4.30 .643

Efficiency of bank‘s website CS4 4.25 .651

Website related to design and ease of use CS5 4.12 .668

Responsiveness of bank CS6 4.06 .751

Source: Primary data. SD – Standard Deviation

6.1.3 Exploratory Factor Analysis

Exploratory Factor Analysis is conducted on 20 measures to validate constructs

that will help analyse the questionnaire responses and explore the service quality

dimensions in IB. The 20 measures are subjected to Principal Component Analysis (PCA)

under the restriction that the Eigen value of each generated factor is more than one.

According to PCA the suitability of data for factor analysis is assessed by computing the

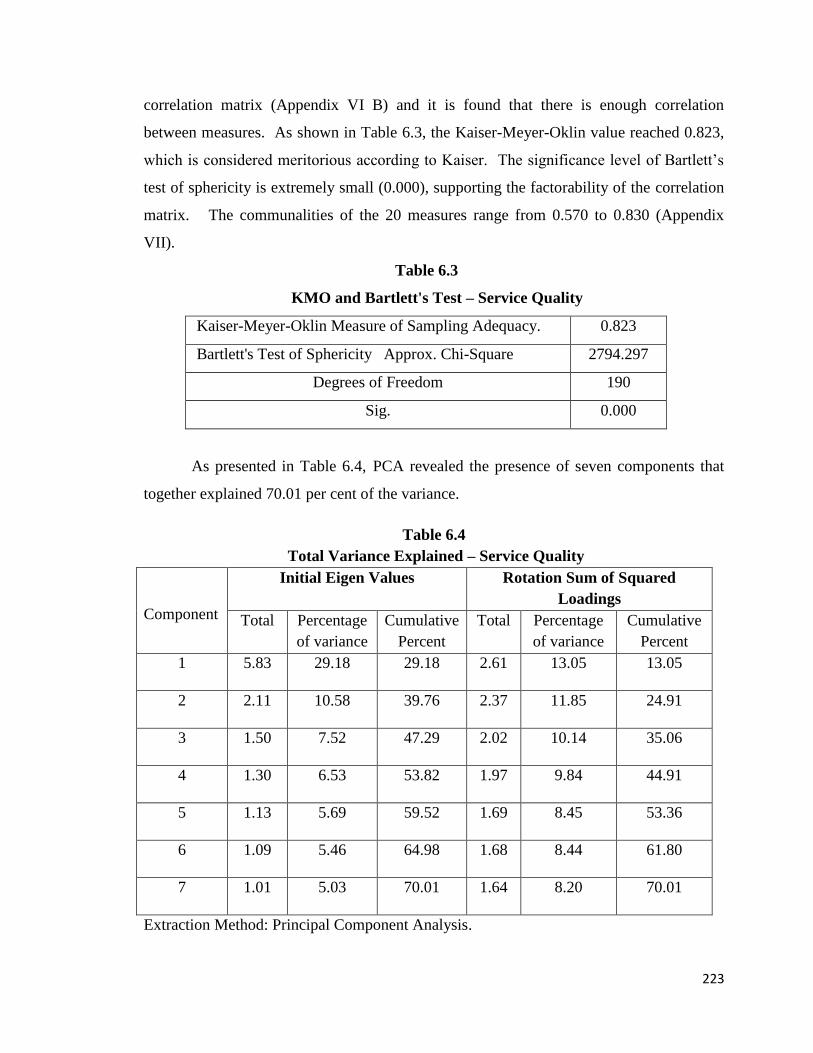

223

correlation matrix (Appendix VI B) and it is found that there is enough correlation

between measures. As shown in Table 6.3, the Kaiser-Meyer-Oklin value reached 0.823,

which is considered meritorious according to Kaiser. The significance level of Bartlett‘s

test of sphericity is extremely small (0.000), supporting the factorability of the correlation

matrix. The communalities of the 20 measures range from 0.570 to 0.830 (Appendix

VII).

Table 6.3

KMO and Bartlett's Test – Service Quality

Kaiser-Meyer-Oklin Measure of Sampling Adequacy. 0.823

Bartlett's Test of Sphericity Approx. Chi-Square 2794.297

Degrees of Freedom 190

Sig. 0.000

As presented in Table 6.4, PCA revealed the presence of seven components that

together explained 70.01 per cent of the variance.

Table 6.4

Total Variance Explained – Service Quality

Component

Initial Eigen Values Rotation Sum of Squared

Loadings

Total Percentage

of variance

Cumulative

Percent

Total Percentage

of variance

Cumulative

Percent

1 5.83 29.18 29.18 2.61 13.05 13.05

2 2.11 10.58 39.76 2.37 11.85 24.91

3 1.50 7.52 47.29 2.02 10.14 35.06

4 1.30 6.53 53.82 1.97 9.84 44.91

5 1.13 5.69 59.52 1.69 8.45 53.36

6 1.09 5.46 64.98 1.68 8.44 61.80

7 1.01 5.03 70.01 1.64 8.20 70.01

Extraction Method: Principal Component Analysis.

224

After reducing the data to seven components, a Varimax rotation is performed to

get a better overview of the seven factors. The Varimax rotated matrix presented in

Table 6.5 revealed the presence of a structure in which all components showed strong

loadings, and all items load to only one component. The rotated factors with their item

constituents and factor loadings are given in Table 6.5

Table 6.5

Rotated Component Matrixa

– Service Quality

Item

Acronym

Component

1 2 3 4 5 6 7

SQ8 .755

SQ9 .773

SQ10 .724

SQ11 .664

SQ17 .757

SQ18 .785

SQ19 .806

SQ20 .665

SQ3 .704

SQ4 .862

SQ5 .718

SQ12 .601

SQ13 .824

SQ14 .726

SQ6 .819

SQ7 .846

SQ1 .868

SQ2 .750

SQ15 .816

SQ16 .837

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization. aRotation converged in 6 iterations.

225

As seen from Table 6.5, all the measures have loadings of more than 0.60 with

most of the loadings above 0.70. Each of the seven factors is suitably labeled based on

the characteristics of its composing measures.

6.1.3.1 Factor 1 – Fulfillment

It is clear from Table 6.5 that measures SQ8, SQ9, SQ10 and SQ11 have loaded

high on factor one and this suggests that factor one is a combination of these four original

measures. The descriptions of these measures are given below.

1. Web pages load promptly (SQ8)

2. Log in to IB website is fast (SQ9)

3. The site provides a confirmation of the service requested quickly (SQ10)

4. Logout speed of my account is fast (SQ11)

Factor 1 explained the maximum variance of 29.18 per cent of the total variance

and had an Eigen value of 5.83. As this factor consists of measures pertaining to

fulfillment of the service requirements of IB users, this factor is labeled as Fulfillment. It

is defined as the extent to which the website meets the requirements of users in terms of

promptness of web page loading, speed of login and logout and confirmation of the

requested service.

6.1.3.2 Factor 2 – Security

This factor is composed of 4 measures SQ17, SQ18, SQ19 and SQ20 and the

descriptions of these measures are given below.

1. Do not feel safe to use IB (SQ17)

2. Worried that others may access my IB account (SQ18)

3. IB servers may process payments incorrectly (SQ19)

4. Banks give no compensation when errors occur (SQ20)

Factor 2 explained 10.58 per cent of the total variance and had an Eigen value of

2.11. This factor is labeled as Security since this factor is a combination of measures

226

relating to security aspect of IB. Security is defined as the extent to which a user believes

that the website is safe from intrusion and that there is very less chance for monetary loss

due to transaction error or server error. As the above measures are negative statements,

the scores are reversed for the purpose of analysis.

6.1.3.3 Factor 3 – Reliability

Three measures SQ3, SQ4 SQ5 are loaded high on this factor and they are the

following.

1. I trust IB services presented on the bank‘s website (SQ3)

2. The bank delivers IB services as promised (SQ4)

3. The website is updated continuously (SQ5)

Factor 3 explained 7.52 per cent of the total variance and had an Eigen value of 1.50.

The measures loaded on this factor are related to reliability of the services provided by

banks and therefore this factor is labeled as Reliability. It is defined as the trust of users

in IB services, delivery of IB services as promised and updating of websites.

6.1.3.4 Factor 4 – Efficiency

This factor is a combination of three measures SQ12, SQ13 and SQ14 and their

descriptions are given below.

1. Finding what I need is easy and simple (SQ12)

2. Easy options for canceling transactions are provided (SQ13)

3. IB website of my bank always satisfy all my service needs (SQ14)

Factor 4 explained 6.53 per cent of the total variance with an Eigen value of 1.30. As

the measures related to efficiency of the bank‘s website are loaded on this factor, this

factor is labeled as Efficiency. It is defined as the ease of using the site and the ability of

banks to satisfy the service needs of customers.

227

6.1.3.5 Factor 5 – Responsiveness

This factor is a combination of two measures SQ6 and SQ7 and they are;

1. Bank takes care of IB complaints quickly (SQ6)

2. There is quick response from my bank to customer queries (SQ7)

Factor 5 explained 5.69 per cent of the total variance with an Eigen value of 1.13.

Since this factor is composed of measures relating to willingness of bank employees to

help customers, this factor is labeled as Responsiveness. It is defined as the ability and

willingness of banks to provide quick response on customer queries and complaints.

6.1.3.6 Factor 6 – Website Attributes

Two measures SQ1 and SQ2 are loaded high on this factor and they are described

below.

1. The web site contains useful help facility (SQ1)

2. Website design is attractive (SQ2)

Factor 6 explained 5.46 per cent of the total variance and had an Eigen value of 1.09.

This factor is labeled as Website attributes since it is composed of measures relating to

bank websites. It is defined as the attractiveness of the website including the provision of

help facility to users.

6.1.3.7 Factor 7 – Privacy

Two measures SQ15 and SQ16 are loaded high on this factor and they are;

1. My personal information is secured and protected in my bank‘s site

(SQ15)

2. The bank will not misuse my personal information (SQ16)

228

They explained 5.03 per cent of the total variance and had the least Eigen value of

1.01. Since the measures are related to confidentiality of customer‘s personal

information, this factor is labeled as Privacy. It is defined as the extent to which a user

believes that his/her personal information is secured and protected.

EFA using Principal Component Analysis applied on six measures of customer

satisfaction indicated that all the measures are loaded on one and only factor with Eigen

value greater than one (KMO=0.847, approx. Chi-square =905.384, df – 15 p< 0.000).

The communalities of the six measures range from 0.544 to 0.671. The factor loadings

range from 0.618 to 0.819 (Appendix VII). The customer satisfaction construct explained

55.87 per cent of the total variance with an Eigen value 3.352.

The Coefficient Alpha of reliability is computed for each factor to see each

dimension‘s internal consistency. Nunnaly (1978) suggests that for any research at its

early stage, a reliable score or alpha that is 0.70 or above is sufficient. As shown in Table

6.6, Cronbach‘s Co-efficient Alpha (α) for all the factors surpassed the required minimum

and ranges from 0.760 to 0.840 and the alpha co-efficient for all the factors taken together

is 0.852. The alpha co-efficient for all the 6 customer satisfaction measures is also

computed and found to be 0.840.

229

Table 6.6

Cronbach’s Alpha for IB Service Quality and Customer Satisfaction Dimensions

IB Service Quality

Dimensions

(Constructs)

Number of

Items

Cronbach’s

Alpha

Cronbach’s

Alpha (all

Dimensions)

Fulfillment 4 0.791

0.852 (20 items)

Security 4 0.776

Reliability 3 0.760

Efficiency 3 0.731

Web site Attributes 2 0.714

Responsiveness 2 0.804

Privacy 2 0.739

Customer Satisfaction 6 0.840

6.1.4 Confirmatory Factor Analysis

The seven dimension model of service quality resulted in EFA is further validated

through Confirmatory Factor Analysis (CFA) using AMOS (Analysis of Moment

Structure).

Besides using the relative/normed Chi-square (Chi-square/ df; df=degrees of

freedom) for the assessment of the model fit, the following additional indices from the

literature are also considered for assessing the model fit. They are CFI, GFI, AGFI, NFI

and RMSEA.

The fit criteria against each index and the 7-dimension model estimated values are

depicted in Table 6.7.

230

Table 6.7

Goodness of Fit Indices – 7-Dimension Model of Service Quality

Goodness of Fit Indices Fit

Criteria

7-Dimension Model

χ2 /df (Normed Chi-square) χ

2 – 312.1, df-147 <5 2.123

GFI (Goodness of Fit Index) >0.90 0.927

AGFI (Adjusted Goodness of Fit Index) >0.80 0.896

CFI (Comparative Fit Index) >0.90 0.939

NFI (Normed Fit Index) >0.90 0.892

RMSEA (Root Mean Square Error of

Approximation)

<0.08 0.053

The model fit indices for the 7-dimension model indicates that the model fits well

in representing the dataset of 20 internet banking service quality measures.

6.1.4.1 Model Estimates

In addition to the model fit indices, standardized regression weights and Critical

Ratio (CR) estimates are also used to evaluate the 7-dimension model. Besides, the

psychometric properties of the model in terms of reliability, convergent validity and

discriminant validity are also evaluated. Reliability and convergent validity of the factors

are estimated by Composite Reliability Co-efficient (CRC) and Average Variance

Extracted (AVE) which are calculated using the formula given in page 155. The model

estimates and psychometric properties of the model are exhibited in Table 6.8

231

Table 6.8

Model Estimates and Psychometric Properties of 7-dimension Model (Service

Quality)

Constructs Indicators SRW CR P

(Sig.level) CRC AVE

Fulfillment

SQ8 0.797 12.081 ***

0.80 0.50 SQ9 0.758 11.745 ***

SQ10 0.606 9.954 ***

SQ11 0.640 *

Security

SQ17 0.597 7.248 ***

0.75 0.44 SQ18 0.823 7.466 ***

SQ19 0.702 9.048 ***

SQ20 0.470 *

Reliability

SQ3 0.689 11.688 ***

0.78 0.54 SQ4 0.800 12.704 ***

SQ5 0.718 *

Efficiency

SQ12 0.697 *

0.68 0.43 SQ13 0.632 9.494 ***

SQ14 0.614 9.270 ***

Responsiveness SQ6 0.916 *

0.82

0.69 SQ7 0.737 11.570 ***

Website

Attributes

SQ1 0.625 8.149 ***

0.71

0.56 SQ2 0.856 *

Privacy SQ15 0.774 *

0.74

0.59 SQ16 0.764 9.448 ***

SRW – Standardized Regression Weight, CR – Critical Ratio

* Unstandardised regression weights assumed as 1

AVE – Average Variance Extracted, CRC – Composite Reliability Co-efficient

***Significant at p < 0.05 level

232

As shown in Table 6.8 all standardized regression weights of indicators (measures)

in the model are greater than 0.50 except SQ 20 (0.47), with most of them close to or

above 0.70. The unstandardised regression weights are significant from the Critical Ratio

(CR) test (CR > ± 1.96, p < 0.05). The CRC of all the constructs are found above the cut

off criteria 0.70 except efficiency construct which is close to 0.70. The AVE of all the

constructs is found above the threshold of 0.50 except security and efficiency constructs.

As the standardized regression weight of SQ 20 is less than 0.50, it is dropped and the

model is re-run. The model fit indices of the final model are χ2 /df = 2.145 (Chi-square –

278.9, df – 130), GFI = 0.932, AGFI = 0.900, CFI = 0.942, NFI = 0.898 and RMSEA =

0.054 all of which indicates good model fit. The final CFA model with standardized

regression weights and correlations between the constructs are depicted in Figure 6.1

233

Figure 6.1

CFA Model of Service Quality Dimensions

234

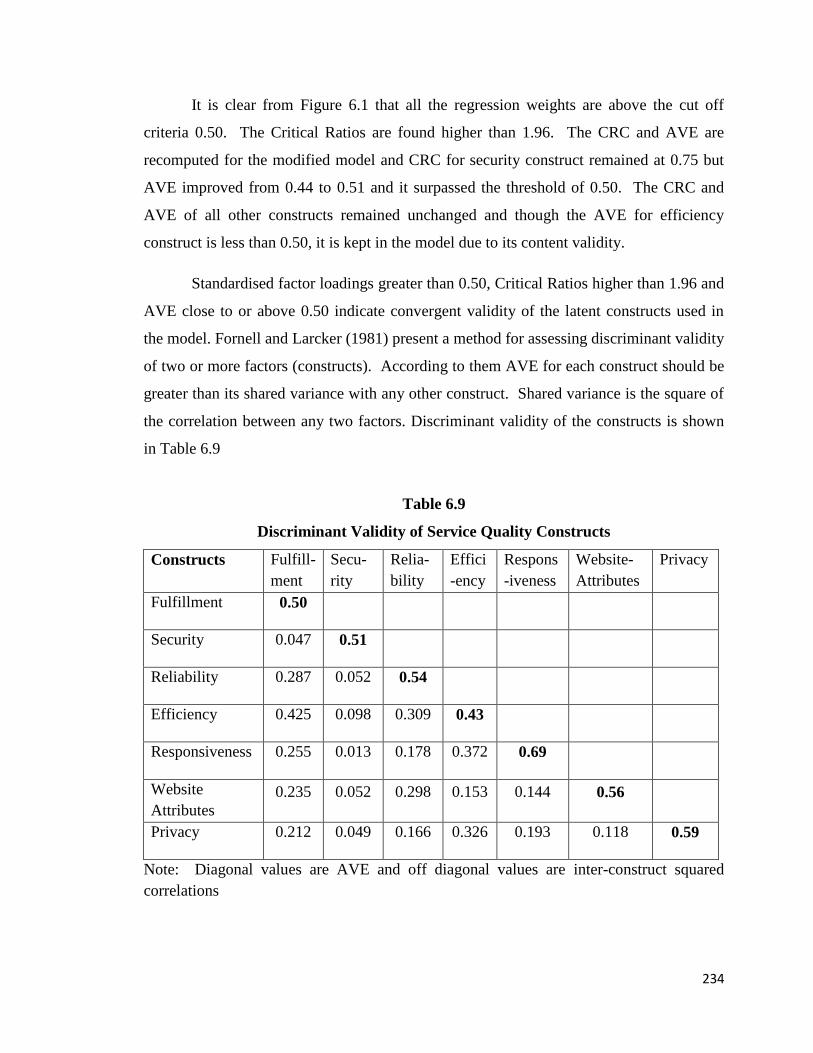

It is clear from Figure 6.1 that all the regression weights are above the cut off

criteria 0.50. The Critical Ratios are found higher than 1.96. The CRC and AVE are

recomputed for the modified model and CRC for security construct remained at 0.75 but

AVE improved from 0.44 to 0.51 and it surpassed the threshold of 0.50. The CRC and

AVE of all other constructs remained unchanged and though the AVE for efficiency

construct is less than 0.50, it is kept in the model due to its content validity.

Standardised factor loadings greater than 0.50, Critical Ratios higher than 1.96 and

AVE close to or above 0.50 indicate convergent validity of the latent constructs used in

the model. Fornell and Larcker (1981) present a method for assessing discriminant validity

of two or more factors (constructs). According to them AVE for each construct should be

greater than its shared variance with any other construct. Shared variance is the square of

the correlation between any two factors. Discriminant validity of the constructs is shown

in Table 6.9

Table 6.9

Discriminant Validity of Service Quality Constructs

Constructs Fulfill-

ment

Secu-

rity

Relia-

bility

Effici

-ency

Respons

-iveness

Website-

Attributes

Privacy

Fulfillment 0.50

Security 0.047 0.51

Reliability 0.287 0.052 0.54

Efficiency 0.425 0.098 0.309 0.43

Responsiveness 0.255 0.013 0.178 0.372 0.69

Website

Attributes

0.235 0.052 0.298 0.153 0.144 0.56

Privacy 0.212 0.049 0.166 0.326 0.193 0.118 0.59

Note: Diagonal values are AVE and off diagonal values are inter-construct squared

correlations

235

It is evident from Table 6.9 that AVE for each construct is larger than their

corresponding squared inter-construct correlations. This indicates high level of

discriminant validity of the constructs used in the model. It means that the measured

items have more in common associated with the latent construct than with other latent

constructs.

In summary, the 7-dimension model of service quality demonstrated good model

fit, adequate reliability, convergent validity and discriminant validity.

The customer satisfaction construct is also validated through CFA. The model fit

indices indicated good model fit. The χ2 /df (Normed Chi-square) χ2

– 18, df-7 is 2.578,

GFI – 0.985, AGFI – 0.956, CFI – 0.986, NFI – 0.977 and RMSEA – 0.063. However,

standardized regression weight of CS5 is 0.46 and for all other measures it is above 0.50.

Therefore CS5 is dropped and the model is re-run. The final uni-dimentional CFA model

of customer satisfaction with standardized regression weights is depicted in Figure 6.2

236

Figure 6.2

Uni-dimensional CFA Model of Customer Satisfaction

The fit indices of the modified model indicated very good model fit. The χ2 /df

(Normed Chi-square) χ2 – 9.6, df-4 is 2.410, GFI – 0.991, AGFI – 0.964, CFI – 0.991, NFI

– 0.986 and RMSEA – 0.060. As shown in Figure 6.2 all the standardized regression

237

weights are above 0.50. The unstandardised regression weights are significant from the

Critical Ratio (CR) test (CR > ± 1.96, p < 0.05). The CRC of customer satisfaction

construct is calculated as 0.82 and AVE 0.49 which is very close to 0.50. In short, the uni-

dimensional model of customer satisfaction demonstrated good model fit, adequate

reliability and convergent validity

6.1.5 Relationship between Service Quality Dimensions and Customer

Satisfaction

The relationship between service quality dimensions and customer satisfaction is

examined using correlation analysis and regression analysis. The construct score is

calculated by adding scores of individual measures in the construct which was validated

through CFA. For example, scores of measures SQ8, SQ9, SQ10 and SQ11 are added to

calculate the construct score for Fulfillment. Similarly the scores of measures CS1, CS2,

CS3, CS4 and CS6 are added to calculate the construct score of Customer Satisfaction.

6.1.5.1 Correlation Analysis

The correlation coefficients between each dimensions of service quality

(independent variables) and customer satisfaction (dependent variable) are shown in

Table 6.10. Various dimensions of service quality are the independent variables (X1…..

X7) and the dependent variable is Customer Satisfaction (Y). The independent variables

are Fulfillment (X1) Security (X2) Reliability (X3) Efficiency (X4) Website attributes (X5)

Responsiveness (X6) Privacy (X7). The dependent variable (Y) is composed of customer

satisfaction relating to Fulfillment (CS1), Privacy/Security (CS2), Reliability (CS3),

Efficiency (CS4), and Responsiveness (CS6).

238

Table 6.10

Correlation Analysis: Service Quality Dimensions and Customer Satisfaction

CS1 CS2 CS3 CS4 CS6 Y

X1 .390*

(.000)

.354*

(.000)

.337*

(.000)

.384*

(.000)

.299*

(.000)

.467*

(.000)

X2 .196*

(.000)

.206*

(.000)

.229*

(.000

.203*

(.000)

.290*

(.000)

.308*

(.000)

X3 .316*

(.000)

.337*

(.000)

.288*

(.000

.288*

(.000)

.314*

(.000)

.412*

(.000)

X4 .382*

(.000)

283*

(.000)

.308*

(.000)

.339*

(.000)

.313*

(.000)

.445*

(.000)

X5 .455*

(.000)

.237*

(.000)

199*

(.000)

.198*

(.000)

.192*

(.000)

.308*

(.000)

X6 409*

(.000)

293*

(.000)

.451*

(.000)

.325*

(.000)

.340*

(.000)

.472*

(.000)

X7 260*

(.000)

.406*

(.000)

.375*

(.000)

.287*

(.000)

.533*

(.000)

483*

(.000)

*Correlation is significant at 0.05 level (2 tailed).

Figures in parentheses indicate p value

It is seen from Table 6.10 that there is positive correlation between each

independent variable (X1….X7) and dependent variable (Y) and also between each

independent variable and each of the measures of dependent variable (CS1….. CS4 and

CS6). The correlations range from 0.192 to 0.533 and the correlations are significant at 5

per cent significance level in all cases.

The conclusion emerging from the above analysis is that there is positive

correlation between various dimensions of service quality and customer satisfaction.

6.1.5.2 Regression Analysis and Hypotheses Testing

In order to understand the effect of IB service quality dimensions on customer

satisfaction the following hypothesis is formulated and tested.

239

H0: Service quality dimensions in internet banking (fulfillment, security, reliability,

efficiency, website attributes, responsiveness and privacy) have no significant effect on

customer satisfaction.

The above hypothesis is tested using multiple regression analysis. Multiple

regression analysis examined the effect of seven dimensions of IB service quality on

customer satisfaction. Multicollinearity, the inter-correlation of independent variables, is

analysed through Tolerance and Variance Inflation Factor (VIF). As shown in Table 6.13,

Tolerance values range from 0.710 to 0.953 and VIF values range from 1.049 to 1.408

(model 5) and therefore multicollinearity is not found in this analysis. The Durbin-Watson

statistic is 1.697 which indicates independence of observations.

The output of the multiple regression analysis is used to test the hypothesis. The

regression model is formed using step-wise method. Table 6.11 shows the model summary

of the step-wise regression analysis.

Table 6.11

Model Summary of Regression Analysis – Service Quality and Customer

Satisfaction

Model R R

Square

Adjusted

R Square

Std. Error of

the Estimate Durbin-Watson

1 .515a .265 .263 .41053

1.697

2 .620b .384 .381 .37638

3 .657c .432 .427 .36185

4 .684d .468 .462 .35068

5 .699e .488 .481 .34435

a. Predictors: (Constant), Privacy

b. Predictors: (Constant), Privacy, Responsiveness

c. Predictors: (Constant), Privacy, Responsiveness, Fulfillment

d. Predictors: (Constant), Privacy, Responsiveness, Fulfillment, Security

e. Predictors: (Constant), Privacy, Responsiveness, Fulfillment, Security, Reliability

f. Dependent Variable: Customer satisfaction

240

Table 6.11 reveals that 26.3 per cent of the variations (model 1) in customer

satisfaction are explained by Privacy dimension of service quality alone. It indicates that

the most prominent independent variable which influences the dependent variable

(customer satisfaction) is ‗Privacy‘. The ANOVA table showing the regression model fit

is given in Table 6.12.

Table 6.12

ANOVA Table Showing the Regression Model Fit – Service Quality and

Customer Satisfaction

Model Sum of

Squares df

Mean

Square F Sig.

1

Regression

Residual

Total

22.908

63.538

86.446

1

377

378

22.908

.169 135.924* .000a

2

Regression

Residual

Total

33.181

53.265

86.446

2

376

378

16.590

.142 117.112* .000b

3

Regression

Residual

Total

37.346

49,100

86.446

3

375

378

12.449

.131 95.076* .000c

4

Regression

Residual

Total

40.454

45.992

86.446

4

374

378

10.113

.123 82.241* .000d

5

Regression

Residual

Total

42.216

42.229

86.446

5

373

378

8.443

.119 71.204* .000e

*Significance at 5 per cent level

241

a. Predictors: (Constant), Privacy

b. Predictors: (Constant), Privacy, Responsiveness

c. Predictors: (Constant), Privacy, Responsiveness, Fulfillment

d. Predictors: (Constant), Privacy, Responsiveness, Fulfillment, Security

e. Predictors: (Constant), Privacy, Responsiveness, Fulfillment, Security, Reliability

f. Dependent Variable: Customer satisfaction

The significance value for model 1 in the ANOVA table 0.000 is significant at 5

per cent significance level. Model 2 incorporates Responsiveness along with Privacy and

it is found that the adjusted R

2 value is increased from 26.3 per cent to 38.1 per cent.

Therefore it is clear that Privacy and Responsiveness together account for 38.1 per cent

variations in customer satisfaction. This model is significant at 5 per cent significance

level. The third model takes into account Fulfillment along with Privacy and

Responsiveness and these three dimensions together account for 42.7 per cent variations in

customer satisfaction and the model is significant at 5 per cent significance level.

Similarly when other independent variables Security and Reliability are included in the

model, the percentage of variance explained by five independent variables, such as

Privacy, Responsiveness, Fulfillment, Security and Reliability, comes up to 48.1 per cent.

All the models are significant at 5 per cent significance level.

The significance of various dimensions of service quality to customer satisfaction

is shown in Table 6.13.

242

Table 6.13

Coefficients – Significance of Service Quality Dimensions

Model Dimensions Beta t Sig Tolerance VIF

1

(Constant)

Privacy

.515

20.790*

11.659*

.000

.000

1.000

1.000

2

(Constant)

Privacy

Responsiveness

.387

.368

18.199*

8.977*

8.516*

.000

.000

.000

.880

.880

1.137

1.137

3

(Constant)

Privacy

Responsiveness

Fulfillment

.319

.292

.249

13.440*

7.387*

6.701*

5.640*

.000

.000

.000

.000

.811

.797

.776

1.233

1.255

1.288

4

(Constant)

Privacy

Responsiveness

Fulfillment

Security

.304

.287

.222

.193

12.103*

7.237*

6.797*

5.140*

5.027*

.000

.000

.000

.000

.000

.807

.797

.764

.960

1.240

1.255

1.309

1.041

5

(Constant)

Privacy

Responsiveness

Fulfillment

Security

Reliability

.278

.260

.177

.181

.163

9.850*

6.662*

6.167*

4.024*

4.772*

3.855*

.000

.000

.000

.000

.000

.000

.786

.774

.710

.953

.764

1.272

1.292

1.408

1.049

1.310

*Significance at 5 per cent level

243

Privacy dimension has the highest beta coefficients followed by Responsiveness,

Security, Fulfillment and Reliability. Out of the predictor variables the β coefficients of

all the dimensions are found to be statistically significant (p <0.05) and hence the null

hypothesis is rejected and the alternative hypothesis that Service quality dimensions in

internet banking (Privacy, Responsiveness, Security, Reliability and Fulfillment) have

significant effect on customer satisfaction is accepted.

Efficiency and Website attribute dimensions are excluded from the step-wise

regression model and they are not significant at 5 per cent significance level (Efficiency

p=0.056, Website attribute p=0.410). Therefore, the null hypothesis is accepted for

efficiency and website attribute dimensions of service quality and concluded that the effect

of these two dimensions on customer satisfaction is not statistically established.

The findings indicate that service quality dimensions Privacy, Responsiveness,

Security, Fulfillment and Reliability have a positive and significant effect on customer

satisfaction and they are the predictors of customer satisfaction.

6.2 Problems and their Effect on Customer Satisfaction

This section presents the items identified for measuring problems associated with

the use of IB, the methodology used for data analysis, factor analysis and subsequent

labeling of problems, relationship and effect of problems on customer satisfaction.

6.2.1 Problems Encountered During the Process of Service Delivery

IB users are most likely to face various problems because banking services are

availed through the medium of internet and there is no face to face contact and

communication between customers and banking personnel. Following the

recommendation of Ombati et al., (2010) that a study should be carried out to establish the

challenges encountered by the customers in the process of using electronic banking in the

service delivery, an attempt is made to identify the problems encountered by customers in

244

the process of using IB. In order to identify the problems associated with the use of IB, 27

probable problems were identified through literature review and discussions with officials

handling IB in various banks. Respondents were asked to indicate the frequency of each

of the problems faced by them on a five point scale as ‗Always‘ (5), ‗Often‘ (4),

‗Sometimes‘ (3), ‗Rarely‘ (2) and ‗Never‘ (1). The scores assigned to each response are

shown in brackets. Table 6.14 shows the list of problems along with their respective item

acronyms.

245

Table 6.14

Problems Encountered During the Process of Service Delivery

Item

Acronym

Problems

Pm-1 Money lost without my knowledge

Pm-2 Transaction failed but amount is deducted

Pm-3 For a single transaction amount is deducted more than once

Pm-4 Refund amount for cancellation of tickets etc. not received

Pm-5 Money not received into my account but deducted from sender‘s account

Pm-6 Low speed

Pm-7 Connection lost while processing transactions

Pm-8 No access to server/IB site not working

Pm-9 Account temporarily locked by bank

Pm-10 My personal information leaked out

Pm-11 Lack of training and guidance on the use of IB

Pm-12 Inadequate support from bank employees

Pm-13 Poor response from bank on complaints

Pm-14 No/delayed support from complaints redressal agencies (Ombudsman etc.)

Pm-15 Unable to login/operate the account

Pm-16 Transaction details missing

Pm-17 The service I want is not available through IB

Pm-18 The option I want is not working

Pm-19 Non delivery of cheque book/draft/passbook/ATM card etc. ordered online

Pm-20 Non delivery of tickets booked online

Pm-21 Unsuccessful transaction but service charges deducted

Pm-22 Lengthy procedure to complete transactions

Pm-23 Occurrence of transaction errors

Pm-24 Problem of forgetting username/password

Pm-25 Unable to get One Time Password (OTP)

Pm-26 Receipt of unknown e-mails that ask for ID and passwords

Pm-27 Delay in getting new password in place of password forgotten

Source: compiled by the researcher

246

6.2.2 Methodology of Analysis

To achieve the objective of identifying the problems encountered during the

process of service delivery and their influence on customer satisfaction, the following

steps are used.

Step 1: The mean values of each of the 27 problems are calculated and these mean values

are compared with the standards set out on the basis of Q1, Q2 and Q3 values calculated

using the formula mentioned in section 5.13, Precautions for the safe use of IB –

Methodology of data analysis (page 172). The standards used for comparing mean values

are given in Table 6.15.

Table 6.15

The Standards Used for Comparing the Mean Values - Problems

Mean Values Collective Opinion of

Respondents

Significantly Below Q1 (1.5) Never

Significantly not different from Q1 (1.5) or significantly

above Q1 but significantly below Q2 (3.0)

Rarely

Significantly not different from Q2 (3.0) Sometimes

Significantly above Q2 (3.0) but significantly below Q3

(4.5)

Often

Significantly not different from Q3(4.5) or significantly

Above Q3

Always

Source: Compiled by the researcher

One sample t-test with test value equal to 1.5 is used to see if the mean values are

significantly different from 1.5 (two tailed). As per the standards set out in Table 6.15,

those problems whose mean values are found significantly below 1.5 are considered as

problems ‗Never‘ faced by IB users. In other words, these may be considered as frivolous

problems which may not call for serious attention from the part of IB service providers.

247

Those problems whose mean values are not significantly different from 1.5 or

significantly above 1.5 but significantly below 3.0 are considered as problems ‗Rarely‘

faced by IB users. However, these problems may not be considered as frivolous problems

but requires attention from the part of IB service providers. Though the frequency of

occurrence of these problems is rare, efforts to further minimize their occurrence may

result in increased customer satisfaction. As the calculated mean values range from 1.2 to

2.61 (Table 6.16), the occurrence of problems associated with the use of IB fall in either of

the above two frequencies.

Step 2: Those problems whose mean values are significantly below 1.5 are dropped from

further analysis. Factor analysis is used on the remaining problems associated with the

use of IB to reduce them into fewer factors for the purpose of further analysis. The

construct score is calculated by adding scores of individual measures in the construct.

Step 3: In order to understand whether the problems associated with the use of IB have

any effect on customer satisfaction multiple regression analysis is used with customer

satisfaction as dependent variable and problems as independent variable.

6.2.3 Comparison of Mean Values with the Standards

The mean scores of each of the 27 problems along with the results of one sample t-

test are displayed in Table 6.16.

248

Table 6.16

Mean Values of Problems Encountered During Service Delivery

Item

Acronym

Mean

values

t df Sig. (2

tailed)

Mean difference

(Test Value = 1.5)

Pm - 1 1.20 -11.426* 404 .000 -.300

Pm - 2 1.68 4.193* 404 .000 .179

Pm – 3 1.31 -6.048* 404 .000 -.194

Pm – 4 1.36 -3.606* 402 .000 -.140

Pm – 5 1.34 -4.693* 404 .000 -.164

Pm – 6 2.51 21.402* 404 .000 1.011

Pm – 7 2.61 22.666* 404 .000 1.107

Pm – 8 2.39 18.272* 404 .000 .888

Pm – 9 1.54 1.044 404 .148 .043

Pm – 10 1.16 -13.598* 402 .000 -.339

Pm – 11 1.76 5.529* 402 .000 .262

Pm – 12 1.90 7.979* 404 .000 .396

Pm – 13 1.90 8.135* 404 .000 .401

Pm – 14 1.55 1.134 402 .128 .051

Pm – 15 1.84 8.221* 404 .000 .344

Pm - 16 1.35 -4.684* 404 .000 -.154

Pm – 17 1.82 7.147* 404 .000 .317

Pm – 18 1.74 5.497* 404 .000 .241

Pm – 19 1.46 -.966 401 .167 -.040

Pm – 20 1.30 -5.740* 401 .000 -.197

Pm – 21 1.47 -.764 404 .222 -.031

Pm – 22 1.84 7.337* 404 .000 .337

Pm – 23 1.87 8.348* 404 .000 .374

Pm – 24 2.14 12.056* 404 .000 .643

Pm – 25 1.82 6.070* 400 .000 .320

Pm – 26 1.82 5.714* 404 .000 .317

Pm - 27 1.83 6.249* 401 .000 .328

Source: Primary data *Significance at 5 per cent level

249

The mean scores range from 1.2 to 2.61. The mean score is lowest for Pm-1

(Money lost without my knowledge, mean 1.20) and highest for Pm-7 (Connection lost

while processing transactions, mean 2.61).

One sample t-test with test value equal to 1.5 revealed that the mean values of the

following problems are significantly below 1.5 (p<0.05). Hence these may be considered

as frivolous problems which may not call for serious attention from the part of IB service

providers. These problems are, therefore, dropped from further analysis.

1. Money lost without my knowledge (Pm-1)

2. For a single transaction amount is deducted more than once (Pm-3)

3. Refund amount for cancellation of tickets etc. not received (Pm-4)

4. Money not received into my account but deducted from sender‘s account

(Pm-5)

5. My personal information leaked out (Pm-10)

6. Transaction details missing (Pm-16)

7. Non-delivery of tickets booked online(Pm-20)

One sample t-test with test value equal to 1.5 revealed that the mean values of the

following problems are not significantly different from 1.5 (p>0.05). Though the

occurrence of these problems is rare, these may not be considered as frivolous problems

but requires attention from the part of IB service providers.

1. Account temporarily locked by bank (Pm-9)

2. No/delayed support from complaints redressal agencies (Pm-14)

3. Non-delivery of cheque book/draft/passbook/ATM card etc. ordered online (Pm-

19)

4. Unsuccessful transaction but service charges deducted (Pm-21)

One sample t-test with test value equal to 1.5 revealed that the mean values of the

following problems are significantly above 1.5 (p<0.05). These problems require

attention from the part of IB service providers.

250

1. Transaction failed but amount is deducted(Pm-2)

2. Low speed (Pm-6)

3. Connection lost while processing transactions (Pm-7)

4. No access to server/IB site not working (Pm-8)

5. Lack of training and guidance on the use of IB (Pm-11)

6. Inadequate support from bank employees (Pm-12)

7. Poor response from bank on complaints (Pm-13)

8. Unable to login/operate the account (Pm-15)

9. The service I want is not available through IB (Pm-17)

10. The option I want is not working (Pm-18)

11. Lengthy procedure to complete transactions (Pm-22)

12. Occurrence of transaction errors (Pm-23)

13. Problem of forgetting username/password (Pm-24)

14. Unable to get One Time Password (OTP) (Pm-25)

15. Receipt of unknown e-mails that ask for ID and passwords (Pm-26)

16. Delay in getting new password in place of password forgotten (Pm-27)

6.2.4 Exploratory Factor Analysis

Exploratory Factor Analysis is used in order to reduce the 20 problems (whose

mean values are either significantly not different from 1.5 or significantly above 1.5)

associated with the use of IB into fewer factors, which explain much of the original data

more economically. To check whether the data is suitable for factor analysis, the following

steps are taken.

1. The correlation matrices are computed and given in Appendix VI C and it is

found that there is enough correlation between measures to go ahead for factor

analysis.

2. Kaiser-Meyer-Olkin Measure of Sampling Adequacy is 0.887 as shown in

Table 6.17. According to Kaiser, a measure greater than 0.80 is meritorious

(Darren & Paul, 2011), and therefore the sample is big enough to do factor

analysis.

251

3. The significance value of Bartlett‘s test of sphericity 0.000 is less than 0.05

and therefore the data do not produce an identity matrix and are thus

approximately multivariate normal and acceptable for factor analysis.

Table 6.17

KMO and Bartlett's Test - Problems Kaiser-Meyer-Olkin Measure of Sampling

Adequacy

.887

Bartlett's Test of

Sphericity

Approx. Chi-Square 2814.713

df 190

Sig. .000

After the standards indicate that the data is suitable for factor analysis, Principal

Components Analysis is employed for extracting the factors, their Eigen values and the

cumulative percentage of variance. It is seen from Table 6.18 that four factors with

Eigen values greater than one is extracted which together account for 54.17 per cent of

the total variance. After the four factors are extracted, the communalities of the 20

original variables range from 0.443 to 0.736 (Appendix VII) which indicate that the

variance of the original values is captured fairly well by these four factors.

252

Table 6.18

Total Variance Explained - Problems

Initial Eigen values Rotation sum of squared

loadings

Component Total % of

variance

Cumulative

%

Total % of

variance

Cumulative

%

1 6.564 32.822 32.822 3.044 15.222 15.222

2 1.673 8.364 41.186 2.853 14.263 29.485

3 1.448 7.240 48.426 2.717 13.587 43.071

4 1.149 5.743 54.169 2.219 11.097 54.169

Extraction Method: Principal Component Analysis.

Since the extraction technique suggested that there are four factors, the extracted

factors are then rotated using the widely used Varimax rotation method and the rotated

factor matrix is exhibited in Table 6.19. The rotated factor matrix gives the loadings of

each measure on each of the extracted factors. The factor loadings range from 0.460 to

0.818 with most of the factor loadings greater than 0.60.

253

Table 6.19

Rotated Component Matrix - Problems

Item

Acronym

Components

1 2 3 4

Pm – 11 .499

Pm – 12 .818

Pm – 13 .790

Pm – 14 .661

Pm – 2 .480

Pm – 17 .735

Pm – 18 .649

Pm – 19 .525

Pm – 21 .582

Pm – 22 .426

Pm – 23 .573

Pm – 6 .674

Pm – 7 .792

Pm – 8 .779

Pm – 9 .454

Pm-15 .507

Pm – 24 .773

Pm – 25 .700

Pm – 26 .460

Pm – 27 .751

Extraction Method: Principal Component Analysis

Rotation Method: Varimax with Kaiser Normalization

a.Rotation converged in 15 iterations

Each of the six factors is suitably labeled based on the characteristics of its

composing measures.

254

6.2.4.1 Factor 1 – Customer Support Problems

This factor is composed of the following 4 problems.

1. Lack of training and guidance on the use of IB (Pm-11)

2. Inadequate support from bank employees (Pm-12)

3. Poor response from bank on complaints (Pm-13)

4. No/delayed support from complaints redressal agencies (Pm-14)

Factor 1 explained 32.82 per cent of the total variance and had an Eigen value of

6.564. This factor is labeled as Customer support problems since this factor is a

combination of measures relating to customer support aspect of IB from the service

providers and grievance redressal agencies like banking ombudsman.

6.2.4.2 Factor 2 –Service Problems

Factor 2 consists of the following 7 problems.

1. Transaction failed but amount is deducted (Pm-2)

2. The service I want is not available through IB (Pm-17)

3. The option I want is not working (Pm-18)

4. Non delivery of cheque book/draft/passbook/ATM card etc. ordered online (Pm-19)

5. Unsuccessful transaction but service charges deducted (Pm-21)

6. Lengthy procedure to complete transactions (Pm-22)

7. Occurrence of transaction errors (Pm-23)

Factor 2 explained the maximum variance of 8.36 per cent of the total variance and

had an Eigen value of 1.67. This factor is labeled as Service problems because this factor

is composed of problems relating to IB service aspects.

6.2.4.3 Factor 3 – Web based Problems

Five measures are loaded on this factor 3. They are;

1. Low speed (Pm-6)

2. Connection lost while processing transactions (Pm-7)

255

3. No access to server/IB site not working (Pm-8)

4. Account temporarily locked by bank (Pm-9)

5. Unable to login/operate the account (Pm-15)

Factor 3 explained 7.24 per cent of the total variance and had an Eigen value of

1.448. This factor is labeled as Web based problems because this factor consists of

problems relating to the website of banks.

6.2.4.4 Factor 4 – Password Problems

This factor is a combination of the following four measures.

1. Problem of forgetting username/password (Pm-24)

2. Unable to get One Time Password (Pm-25)

3. Receipt of unknown e-mails that ask for ID and passwords (Pm-26)

4. Delay in getting new password in place of password forgotten (Pm-27)

This factor explained 5.74 per cent of the total variance with an Eigen value of

1.149. This factor is labeled as Password problems because problems relating to

password are loaded on this factor.

The Coefficient Alpha of reliability is computed for each factor to see the internal

consistency of each factor. As shown in Table 6.20, Cronbach‘s Co-efficient Alphas (α)

for all the factors are above 0.70 and range from 0.701 to 0.799. The Alpha Co-efficient

for all the factors taken together is 0.888.

256

Table 6.20

Cronbach’s Co-efficent Alpha – Problems

Factors (Constructs) Number

of Items

Cronbach’s

Alpha

Cronbach’s

Alpha (All

Factors)

Customer support problems 4 0.792

0.888 (20

items)

Service problems 7 0.799

Web based problems 5 0.743

Password problems 4 0.701

The construct score is calculated by adding scores of individual measures in the

construct. The percentage scores ({Construct score ÷ Maximum possible score} x 100) of

each construct are calculated and the mean of the percentage scores is shown in Figure 6.3

Figure 6.3

Mean of Percentage Scores of Problem Constructs

35.55

33.96

43.58

38.08

0 10 20 30 40 50

Customer support problems

Service problems

Web based problems

Password problems

Mean Percentage Score (%)

257

The mean percentage score is highest for web based problems (43.58 per cent)

followed by password problems (38.08 per cent), customer support problems (35.55 per

cent) and service problems (33.96 per cent).

The conclusions emerging from the above analysis is that, four problems are

associated with the use of IB as perceived by IB users in Kerala. They are web based

problems, password problems, customer support problems and service problems. But IB

users perceive these problems on a lesser gravity.

6.2.5 Effect of Problems on Customer Satisfaction

The problems associated with the use of IB identified through factor analysis are

used as independent variables to understand their effect on customer satisfaction, the

dependent variable. The following null hypothesis is formulated for this purpose.

H0: Problems encountered during internet banking service delivery (web based problems,

password problems, customer support problems and service problems) have no significant

effect on customer satisfaction.

6.2.5.1 Correlation Analysis

Before testing the above hypothesis, it is felt necessary to see the correlation

between dependent variable (Y) and independent variables (X1, X2, X3, X4) and also

between each of the components of dependent variables such as CS1, CS2, CS3, CS4, CS6

and independent variables. The dependent variable, customer satisfaction (Y) and the

measures of customer satisfaction (CS1 ……CS4 and CS6) have been discussed in section

6.1.2.1 (page 222) and validated using CFA (page 236). The independent variables are

Customer Support Problems (X1), Service Problems (X2), Web based Problems (X3) and

Password Problems (X4). The correlations between the variables are shown in Table 6.21.

258

Table 6.21

Correlation Analysis: Problems and Customer Satisfaction

CS1 CS2 CS3 CS4 CS6 Y

X1 -.315*

(.000)

.349*

(.000)

-.374*

(.000)

-.352*

(.000)

-.294*

(.000)

-.444*

(.000)

X2 -.206*

(.000)

-.238*

(.000)

-.277*

(.000

-.316*

(.000)

-.286*

(.000)

-.377*

(.000)

X3 .-234*

(.000)

.-236*

(.000)

.-305*

(.000

.-253*

(.000)

.-194*

(.000)

.-331*

(.000)

X4 .-173*

(.000)

.-171*

(.000)

.-163*

(.000)

.-232*

(.000)

.-140*

(.000)

.-232*

(.000)

*Correlation is significant at 0.05 level (2 tailed).

Figures in parentheses indicate p value

The correlations range from -0.140 to -0.444 and the correlations are significant at 5 per

cent significance level in all cases.

The conclusion emerging from the above analysis is that there is negative

correlation between problems associated with the use of IB and customer satisfaction.

6.2.5.2 Regression Analysis and Hypotheses Testing

In order to understand the variation in customer satisfaction based on problems

associated with the use of IB, multiple regression analysis is used. The output of the

multiple regression analysis is used to test the hypothesis. The regression model is formed

using step-wise method. Table 6.22 shows the model summary of the step-wise regression

analysis.

259

Table 6.22

Model Summary of Regression Analysis – Problems and Customer Satisfaction

Model R R

Square

Adjusted

R Square

Std. Error of

the Estimate

Durbin-Watson

1 .442a .196 .194 .45891

2.01 2 .469b .220 .216 .45248

a. Predictors: (Constant), Customer support problems

b. Predictors: (Constant), Customer support problems, Web based problems

Dependent variable – Customer Satisfaction

Table 6.22 reveals that 19.4 per cent of the variation (model 1) in customer

satisfaction is explained by customer support problems alone. It indicates that the most

prominent independent variable which influences the dependent variable (customer

satisfaction) is customer support problems. The ANOVA table showing the regression

model fit is given in Table 6.23.

Table 6.23

ANOVA Table Showing the Regression Model Fit –Problems and Customer

Satisfaction

Model Sum of

Squares df

Mean

Square F Sig.

1

Regression

Residual

Total

20.375

83.819

104.94

1

398

399

20.375

.211

96.746*

.000a

2

Regression

Residual

Total

22.193

81.281

104.194

2

397

399

11.457

.205

55.958*

.000b

*Significance at 5 per cent level

a. Predictors: (Constant), Customer support problems

b. Predictors: (Constant), Customer support problems, Web based problems

Dependent variable: Customer satisfaction

260

The significance value for model 1 in the ANOVA table 0.000 is significant at 5

per cent significance level. Model 2 incorporates web based problems along with customer

support problems and it is found that web based problems have a nominal impact on the

R2 and the adjusted

R

2 value is increased from 19.4 per cent to only 21.6 per cent. The

model is significant at 5 per cent significance level. Multicollinearity is examined through

Tolerance and Variance Inflation Factor (VIF). As shown in Table 6.24 Tolerance values

and VIF values are .817, 1.224 respectively for both independent variables and therefore

the presence of multicollinearity is not found. The Durbin-Watson statistic 2.01 indicates

independence of observations.

The significance of customer support problems and web based problems to

customer satisfaction is shown in Table 6.24.

Table 6.24

Coefficients – Significance of Problems to Customer Satisfaction

Model Dimensions Beta t Sig Tolerance VIF

1

(Constant)

Customer support problems

-.442

79.851*

-9.836*

.000

.000

1.000

1.000

2

(Constant)

Customer support problems

Web based problems

-.368

-.173

60.164*

-7.508*

-3.521*

.000

.000

.000

.817

.817

1.224

1.224

* Significance at 5 per cent level

Customer support problems have the highest beta coefficient (β = -.368) than web

based problems (β = -.173). It indicates that customer support problems have greater

negative effect on customer satisfaction than web based problems. Out of the

independent variables the β coefficients of both problems are found to be statistically

significant (p <0.05) and hence the null hypothesis is rejected and the alternative

hypothesis that Problems encountered during internet banking service delivery

261

(Customer support problems, Web based problems) have significant effect on customer

satisfaction is accepted.

Service problems and Password problems are excluded from the step-wise

regression model and they are not significant at 5 per cent significance level (Service

problems p=0.090, Password problems p=0.891). Therefore the null hypothesis is

accepted for service problems and password problems and concluded that the effect of

these two problems on customer satisfaction is not statistically established.

6.3 Discussion of the Results and their Implications

Factor analysis segmented 20 IB service quality variables into seven dimensions

labeled Fulfillment, Security, Reliability, Efficiency, Responsiveness, Website attributes

and Privacy. Significant positive correlations were found between various dimensions of

service quality and customer satisfaction. Multiple regression analysis unfolded the

effect of service quality dimensions on customer satisfaction. Privacy dimension

followed by Responsiveness, Security, Fulfillment and Reliability were found to be

predictors of customer satisfaction. However, the effect of Efficiency and Website

attribute dimensions on customer satisfaction was not statistically established.

Among the dimensions, Privacy was the one having the strongest impact followed

by Responsiveness and Security. This finding, combined with the fact that customers

perceived the measures of Security and Responsiveness dimensions as the lowest amid

the measures of various service quality dimensions, may pose a major threat to the wider

embracing of IB in Kerala. Therefore, banks should closely look at how they can

improve the perception of IB users regarding the Security and Responsiveness

dimensions of service quality.

The government and the RBI are taking efforts to bring down the usage of cash in

the society by giving more emphasis on Information and Communication Technology

(ICT) solutions such as mobile and online banking, core banking and electronic fund

transfers (Press Trust of India, 2012, Sept.13). In such a context banks cannot afford to

262

underestimate the importance of any of the above mentioned dimensions that affect

customer satisfaction in IB and should continuously aim to improve them especially at a

time when the usage of IB services are gaining acceptance among the banking customers

in Kerala.

The findings that customer support problems and web based problems have

significant negative effect on customer satisfaction indicate that these factors hinder

customer satisfaction in the use of IB. The finding, that customer support problem exert

comparatively strong negative effect on customer satisfaction than web based problems,

cross validates the finding that responsiveness of bank employees is one of the strongest

predictors of customer satisfaction. The essence of this finding is that IB users in Kerala

may be satisfied about IB services in general but may not be satisfied about specific

dimensions of service quality, for example, responsiveness. In order to maximize

customer satisfaction, banks in Kerala should pay high attention to responsiveness

dimension of service quality so that customer support problems are minimized. The

negative significant correlation between responsiveness dimension of service quality and

customer support problems ( r = -.295, p = 0.000) underscores the above statement.

To create a highly responsive bank for IB services, a bank should have accessible

and responsive employees who can respond to all customers‘ requirements and complaints

quickly and professionally. Skilful and experienced staff who can also handle problems

associated with the use of IB may be devoted for this purpose. In order to provide hands

on training to potential IB users on how to use IB, banks may arrange live demos at

branch offices when the customers approach the banks for IB facility. Though the website

of some of the banks provide demos, demos in the presence of experienced bank staff may

be more beneficial from the point of view of customers.

Most of the web based problems such as low speed, connection lost while

processing transactions etc. may not be within the reach of banks and they may not have

much to solve these problems. However, for problem of ‗account temporarily locked by

bank‘, the bank can make the customers aware that their account will be temporarily

263

locked if they make multiple incorrect password entry, to ensure security. What the banks

can do in this regard is to advice users to choose passwords which are easy to remember

for them but difficult to be guessed by others.

![6. Performance Testing of Bellows - INFLIBNETshodhganga.inflibnet.ac.in/bitstream/10603/40881/15/15_chapter6.pdf · 6. Performance Testing of Bellows ... EJMA.[20] A minimum of ten](https://img.dokumen.tips/doc/110x75/5b2f87bd7f8b9a594c8e6159/6-performance-testing-of-bellows-6-performance-testing-of-bellows-ejma20.jpg)