Embed Size (px)

Citation preview

11

2013

November 2013

Sector Report

Health Care

Economics, FI/FX & Commodities ResearchCredit Research Equity Research Cross Asset Research

“Credit Health Check”

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 2 See last pages for disclaimer.

Contents 3 Summary

4 Sector SWOT Analysis

5 Company Overview

7 Business Profiles

8 Strategy Outlook 2014

10 Investment Recommendation

16 Trading Ideas

19 Healthcare bonds: supply and outlook

21 Rating trend

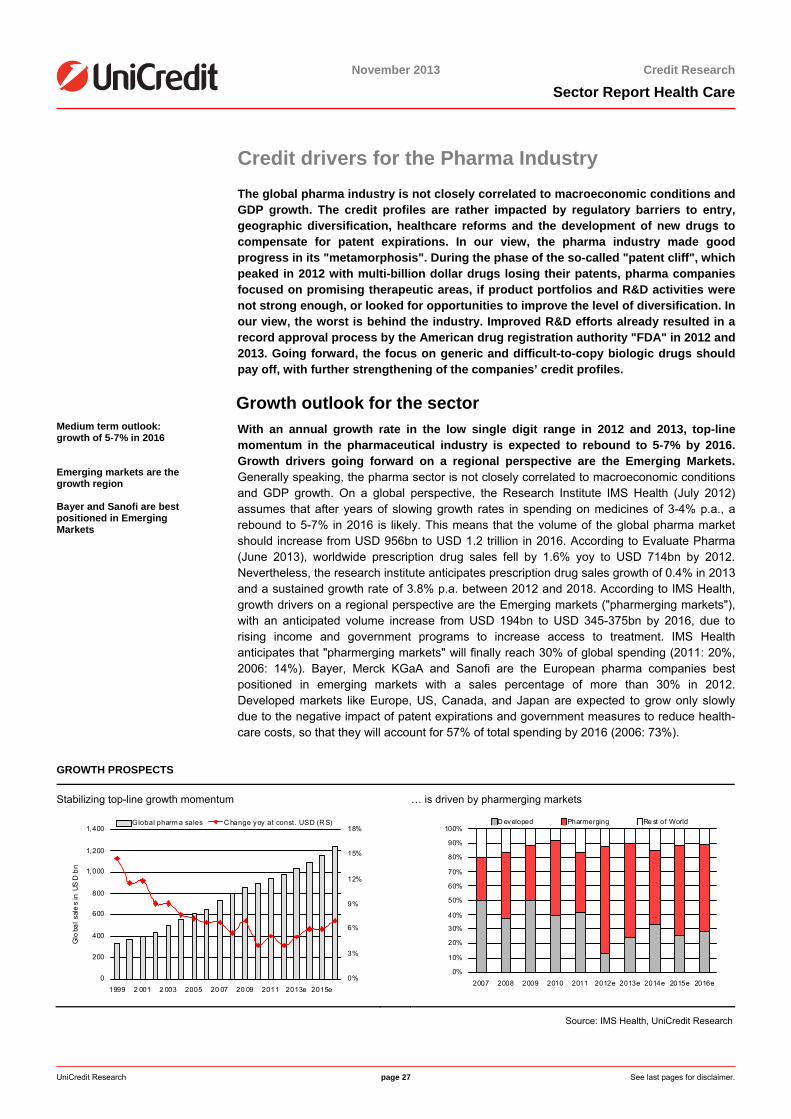

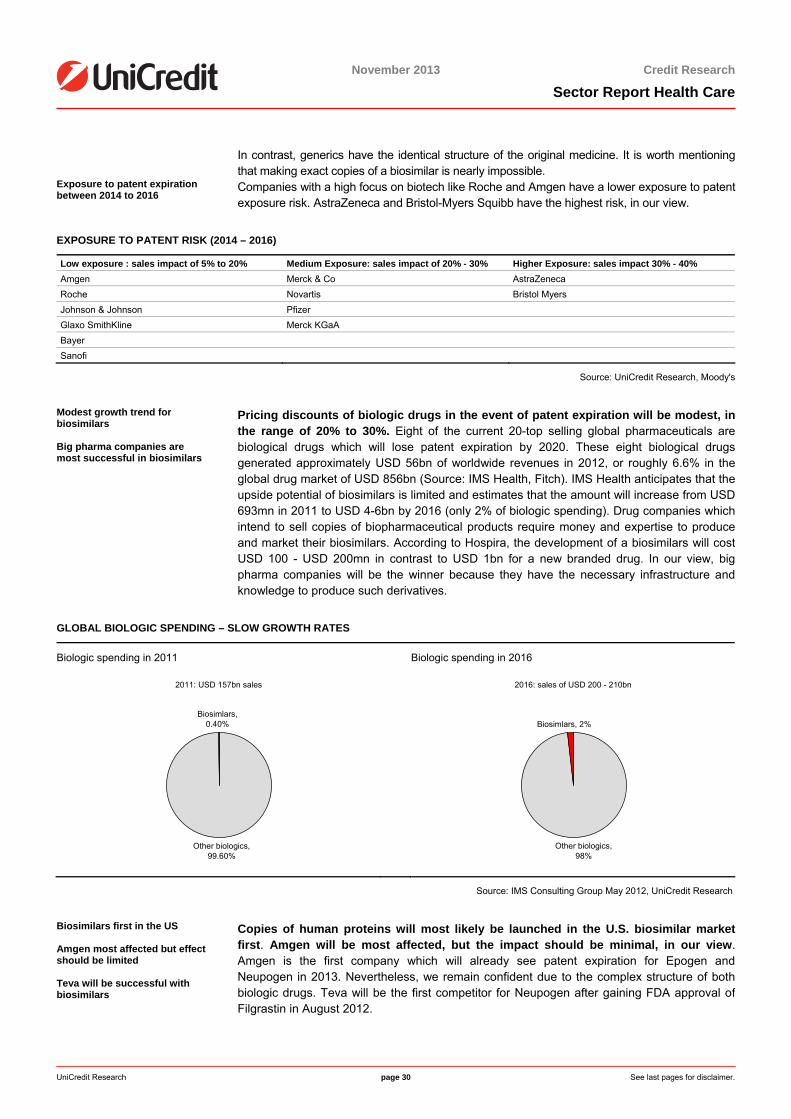

27 Credit drivers for the Pharma Industry

27 Growth outlook for the sector

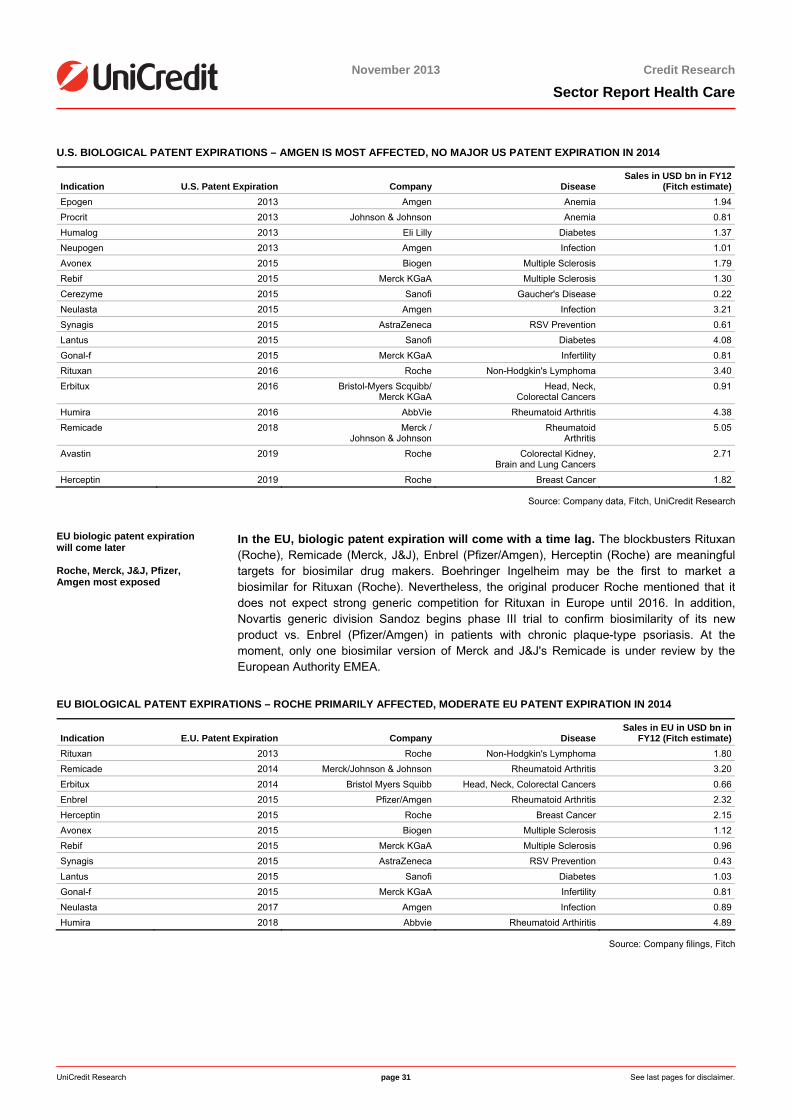

29 Patent expirations

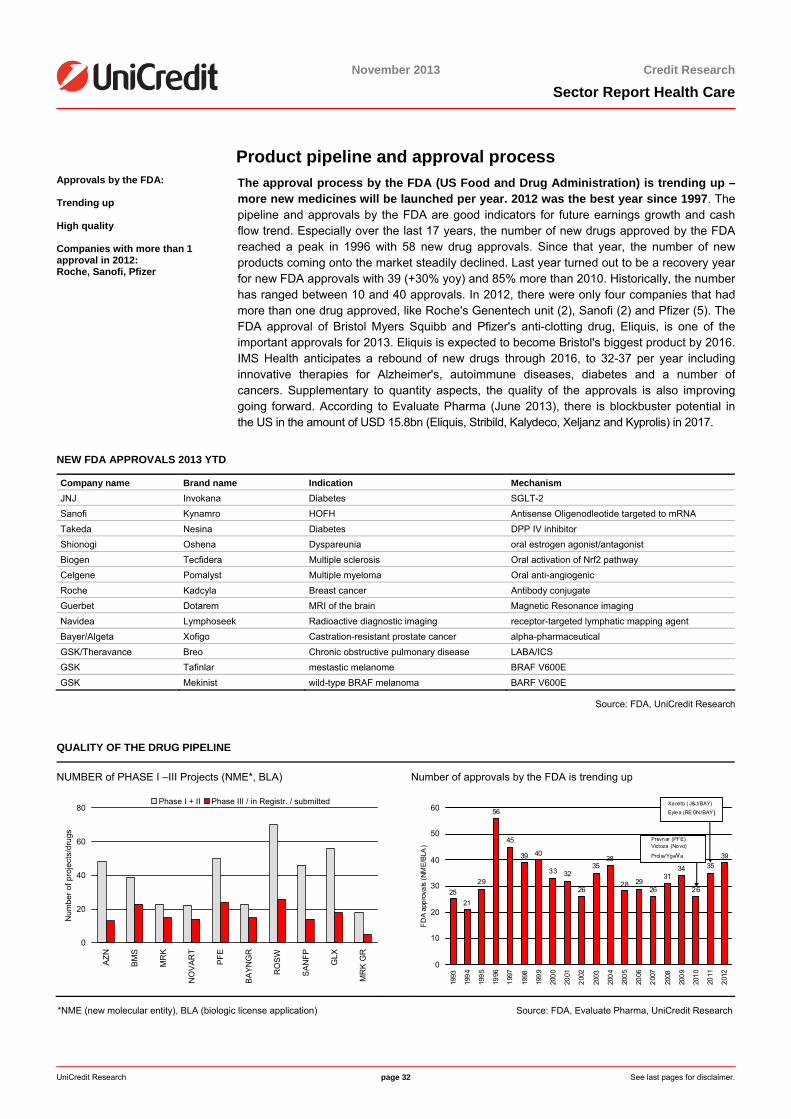

32 Product pipeline and approval process

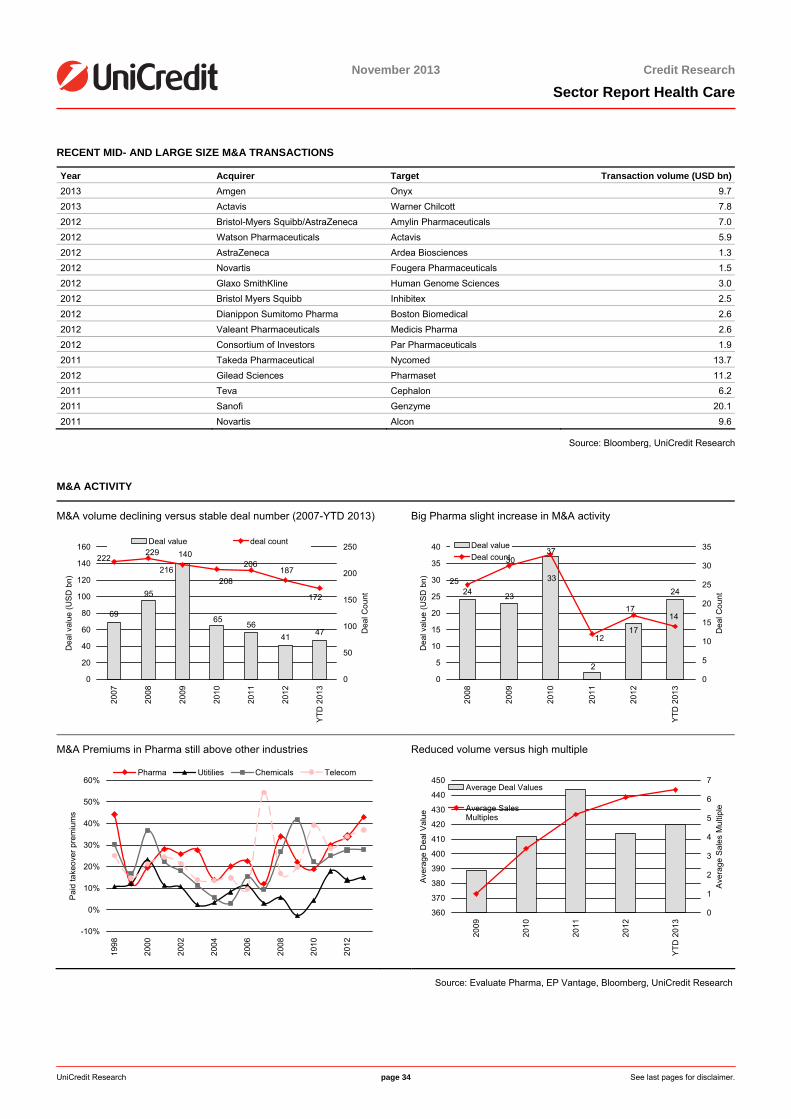

33 M&A activity

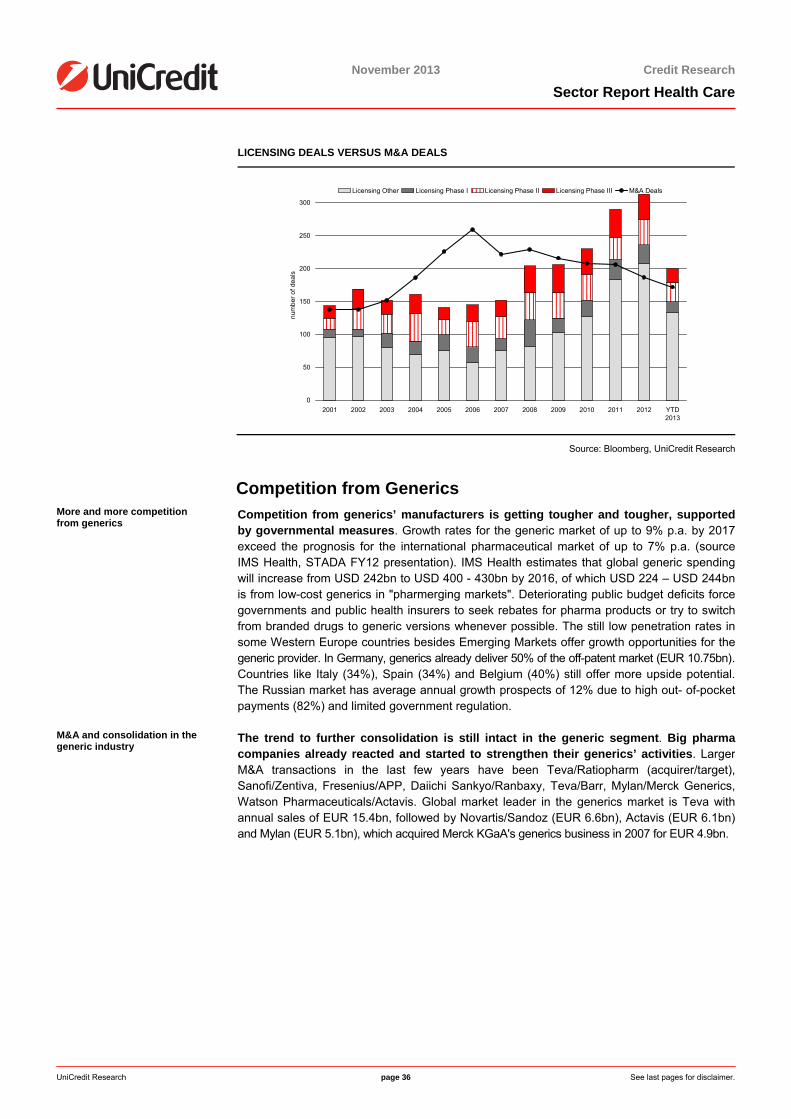

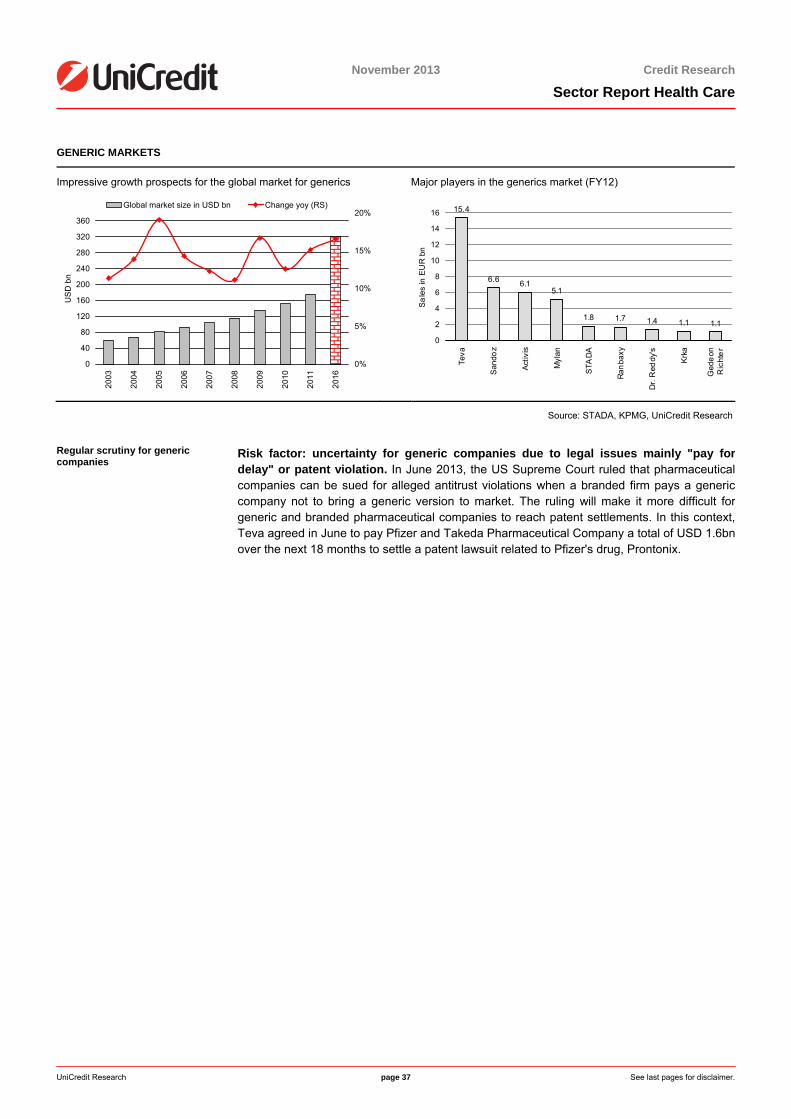

36 Competition from Generics

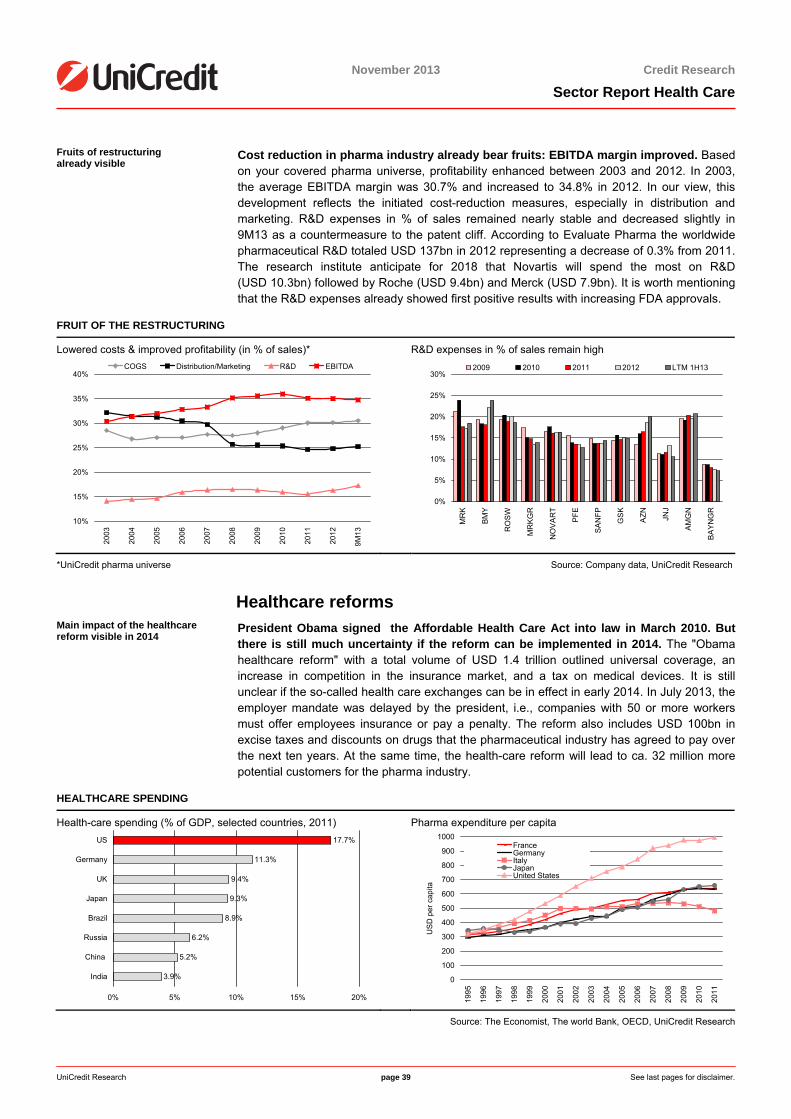

38 Cost-cutting attempts

39 Healthcare reforms

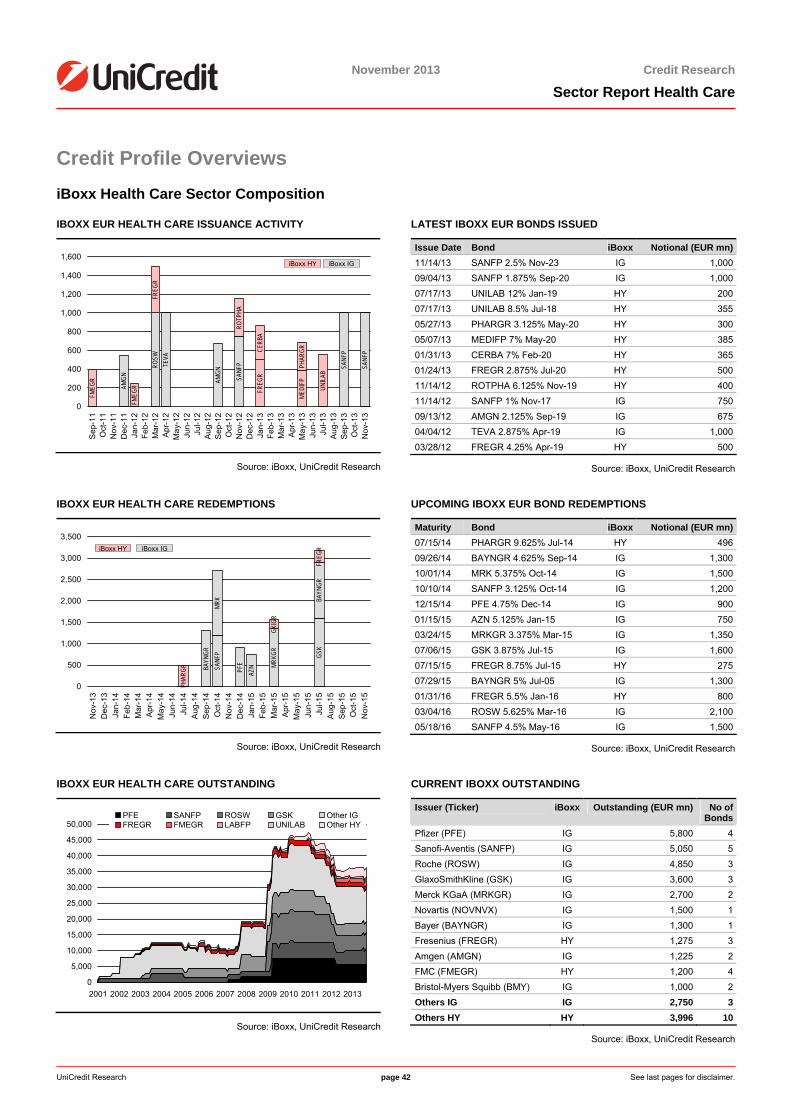

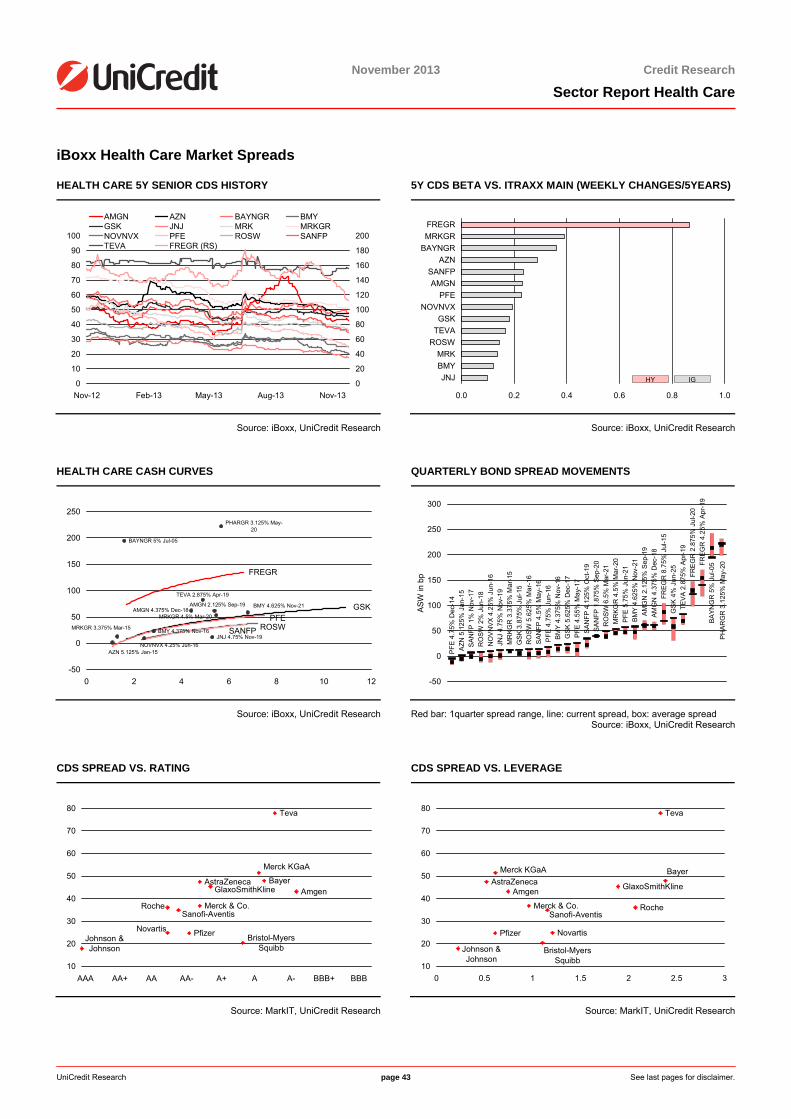

42 Credit Profile Overviews

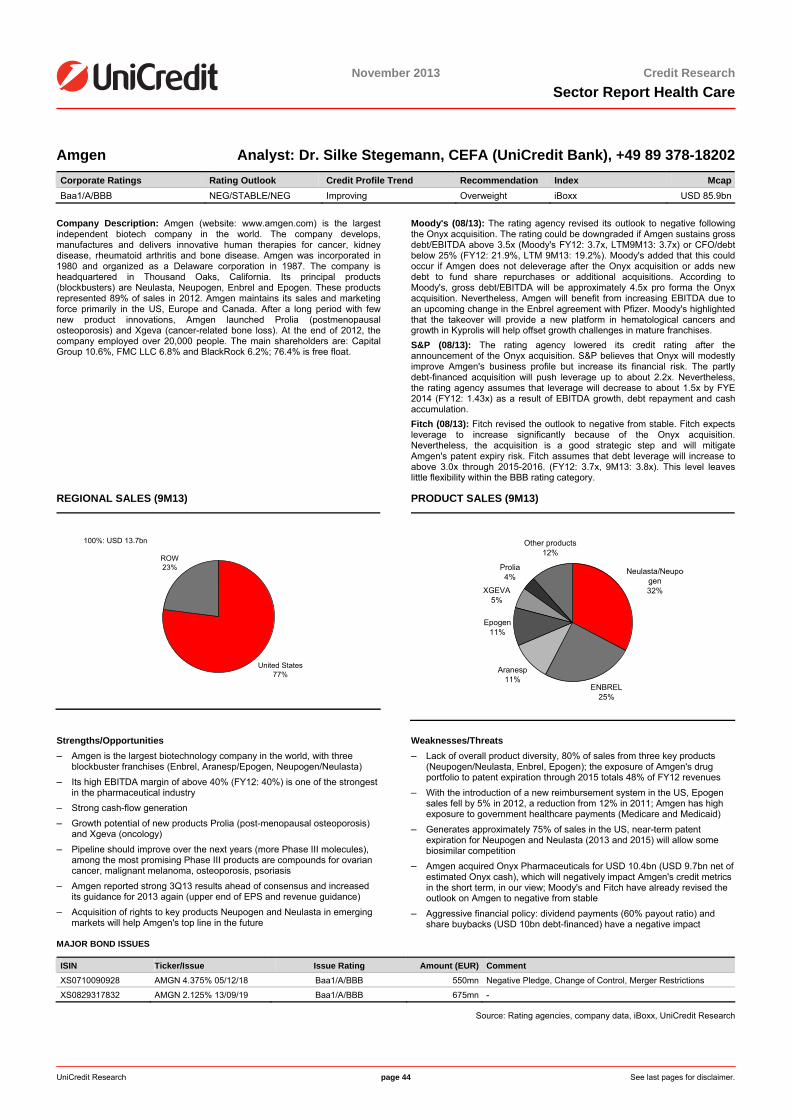

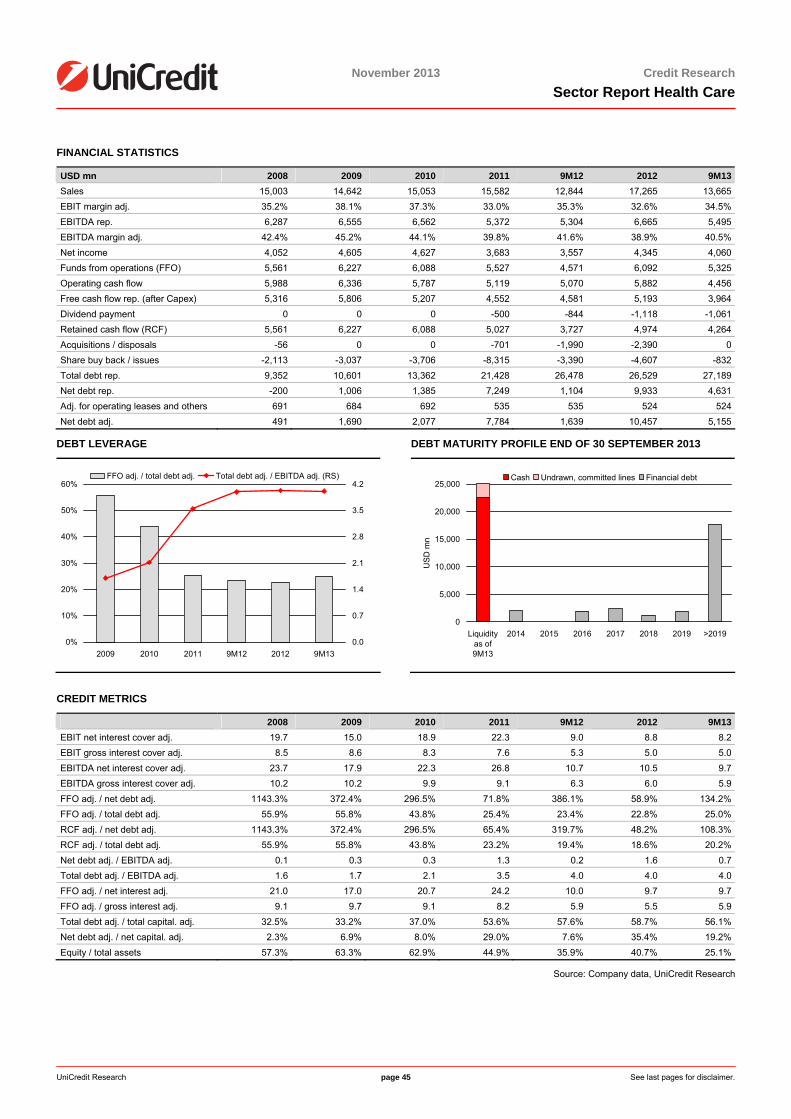

44 Amgen

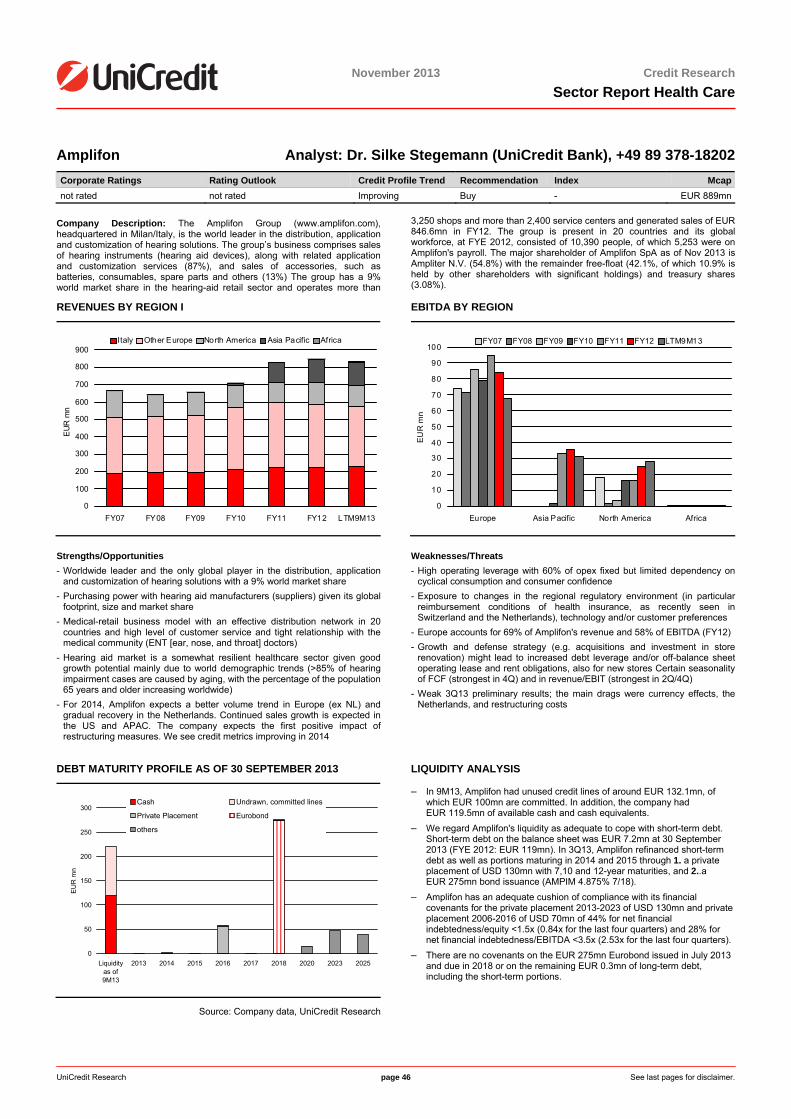

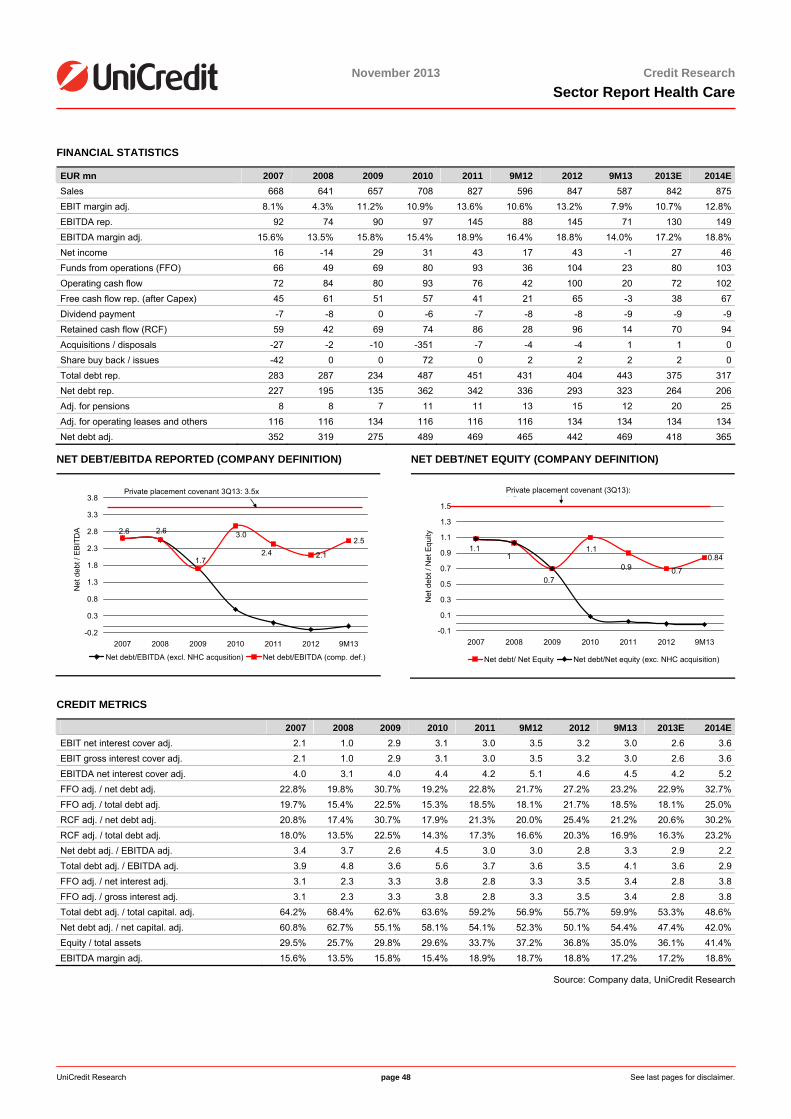

46 Amplifon

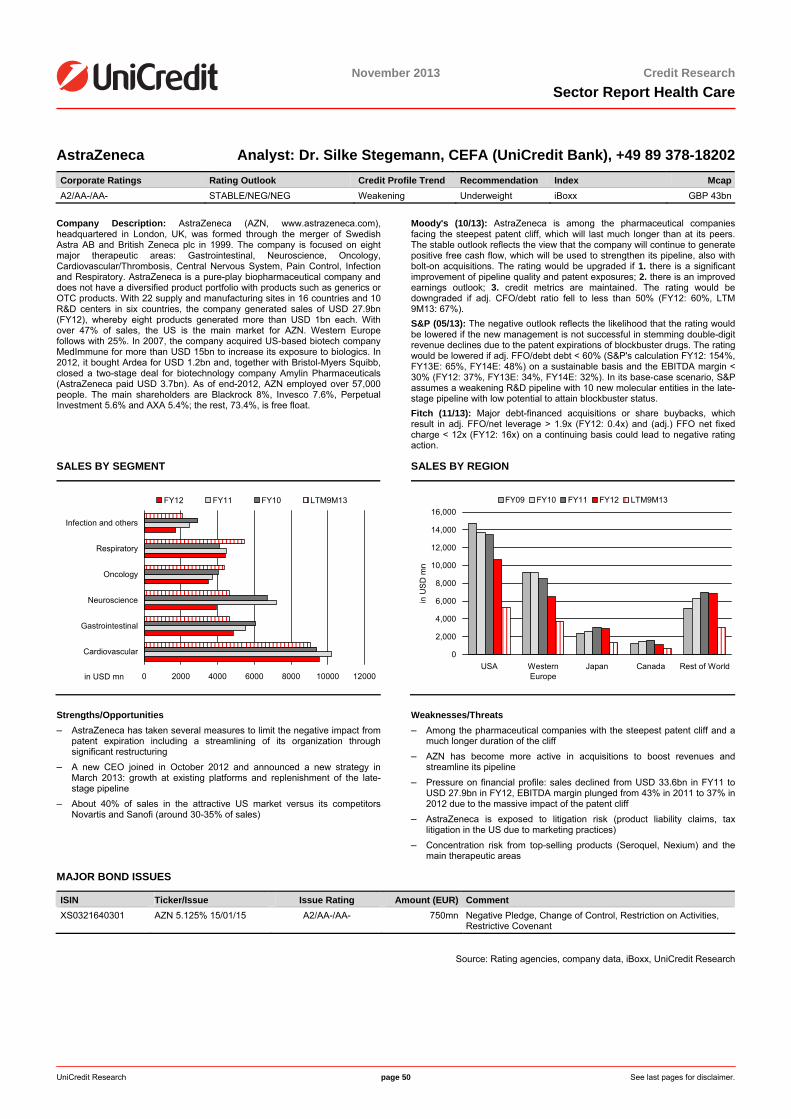

50 AstraZeneca

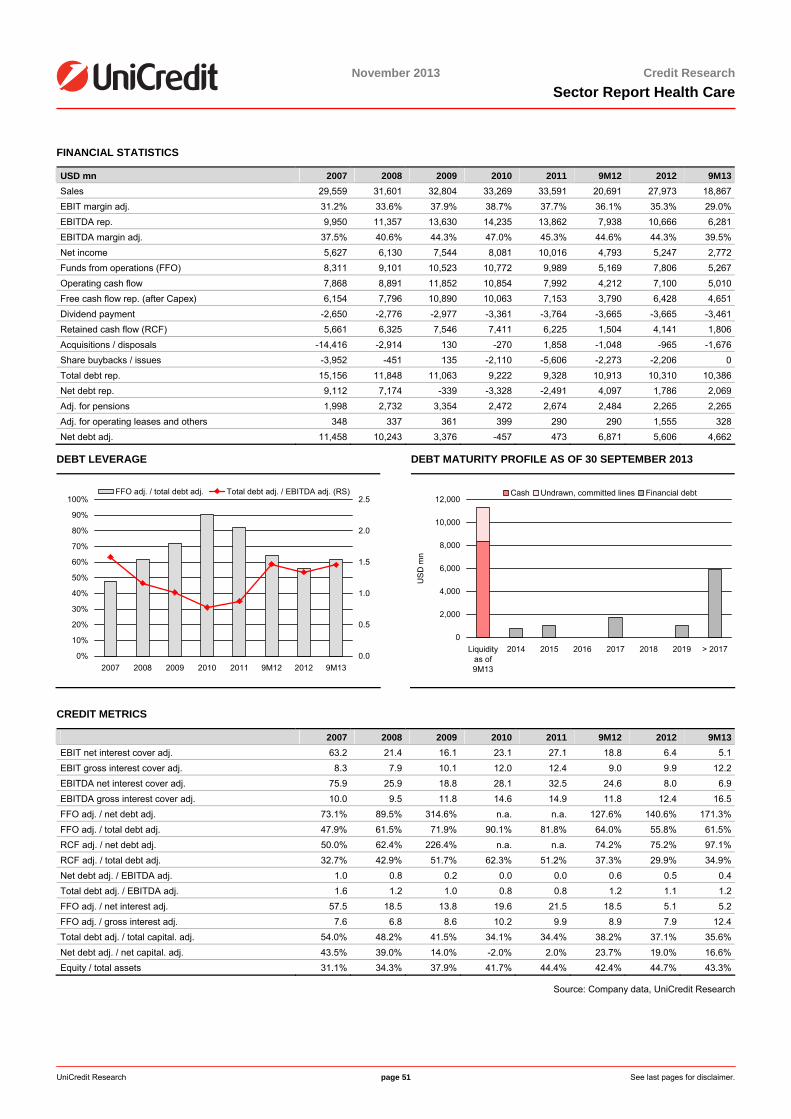

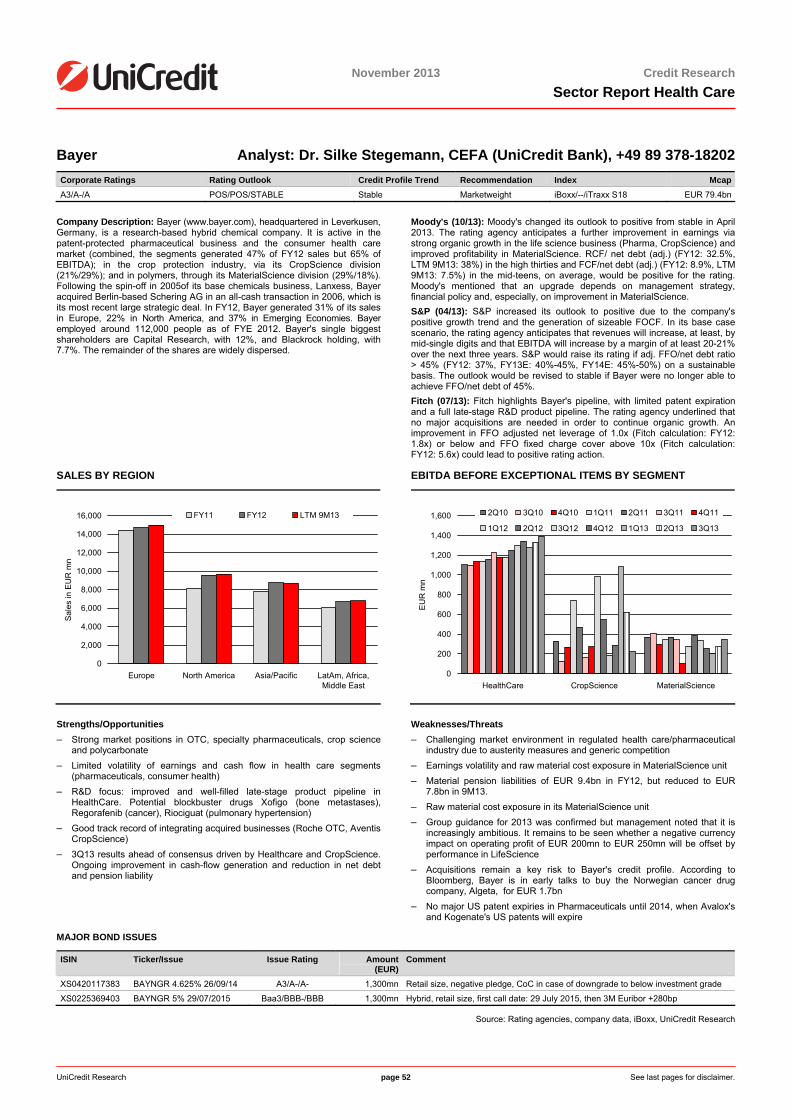

52 Bayer

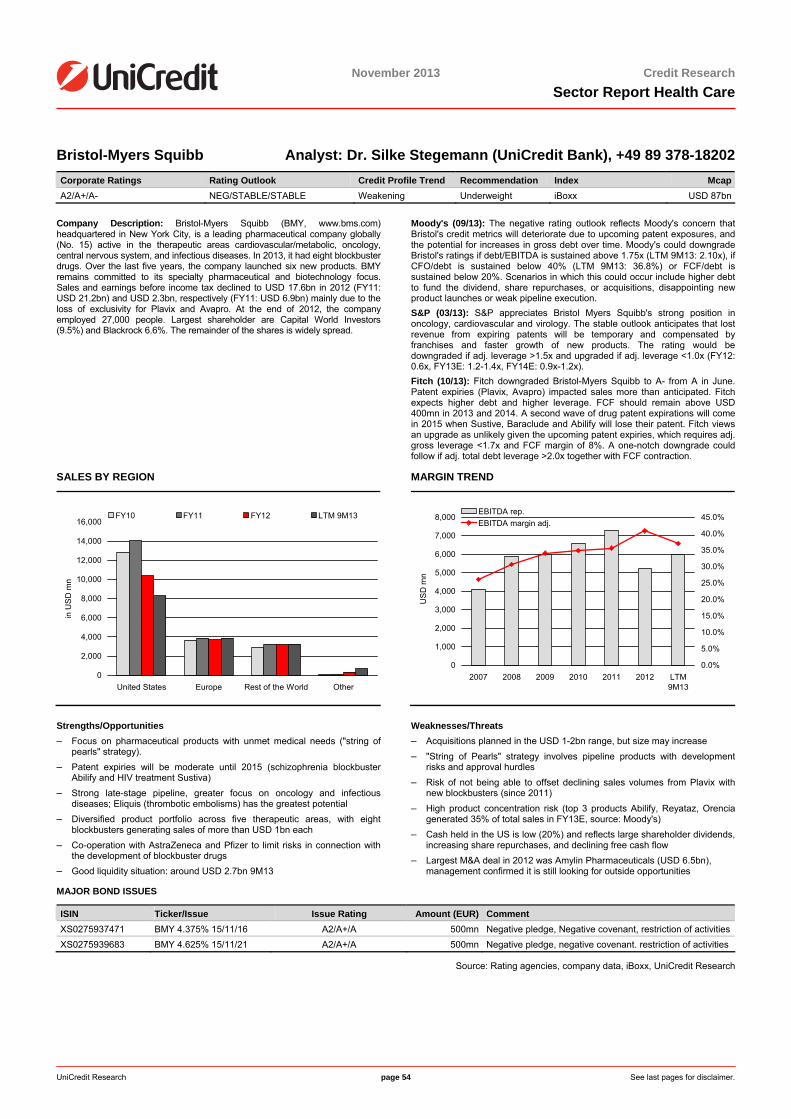

54 Bristol-Myers Squibb

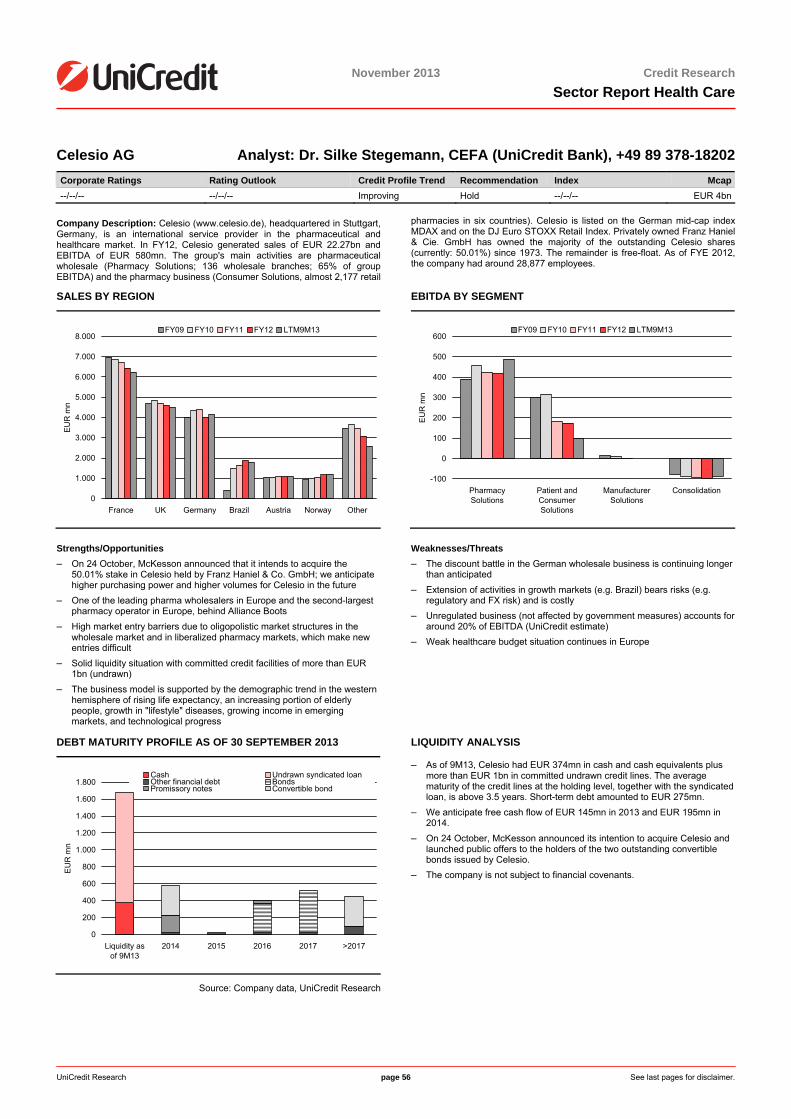

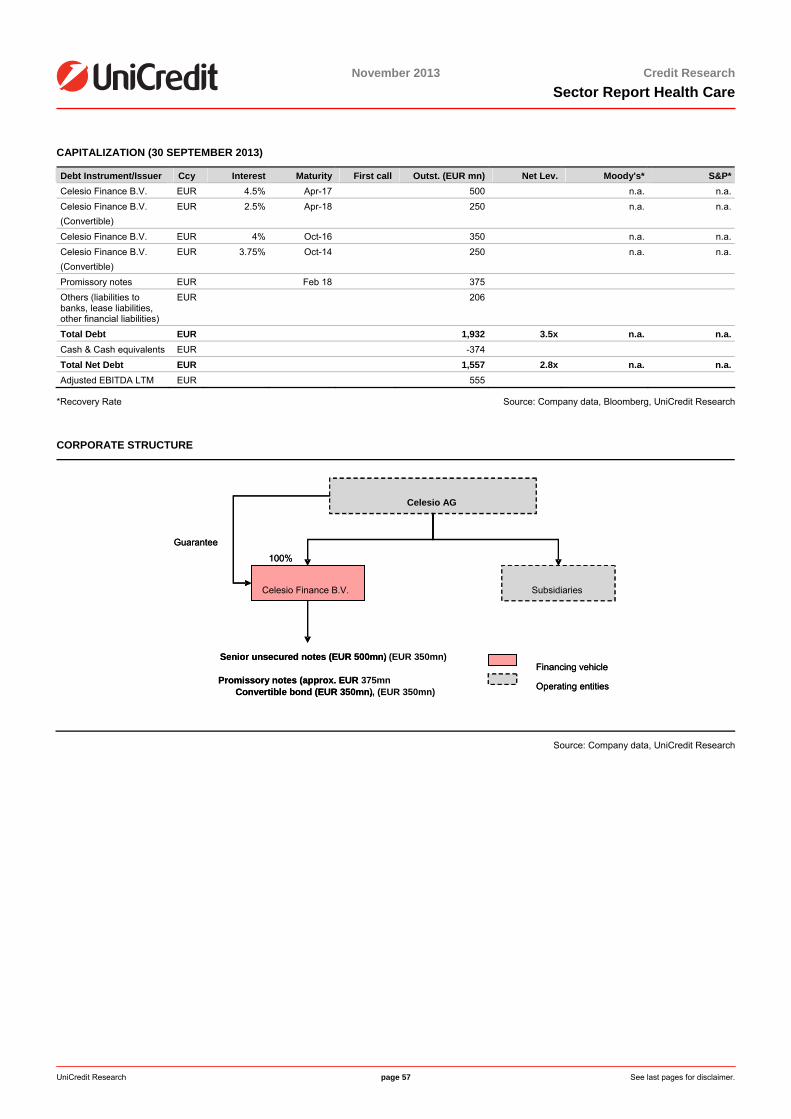

56 Celesio AG

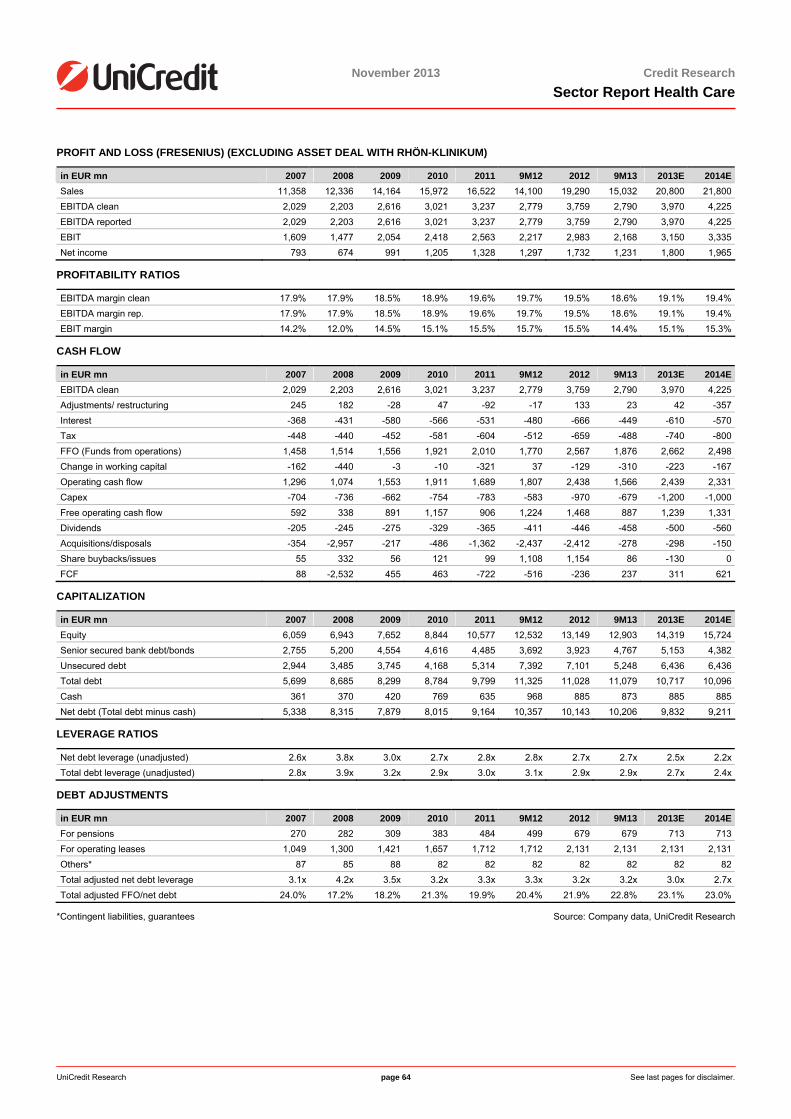

60 Fresenius

66 GlaxoSmithKline

68 Johnson & Johnson

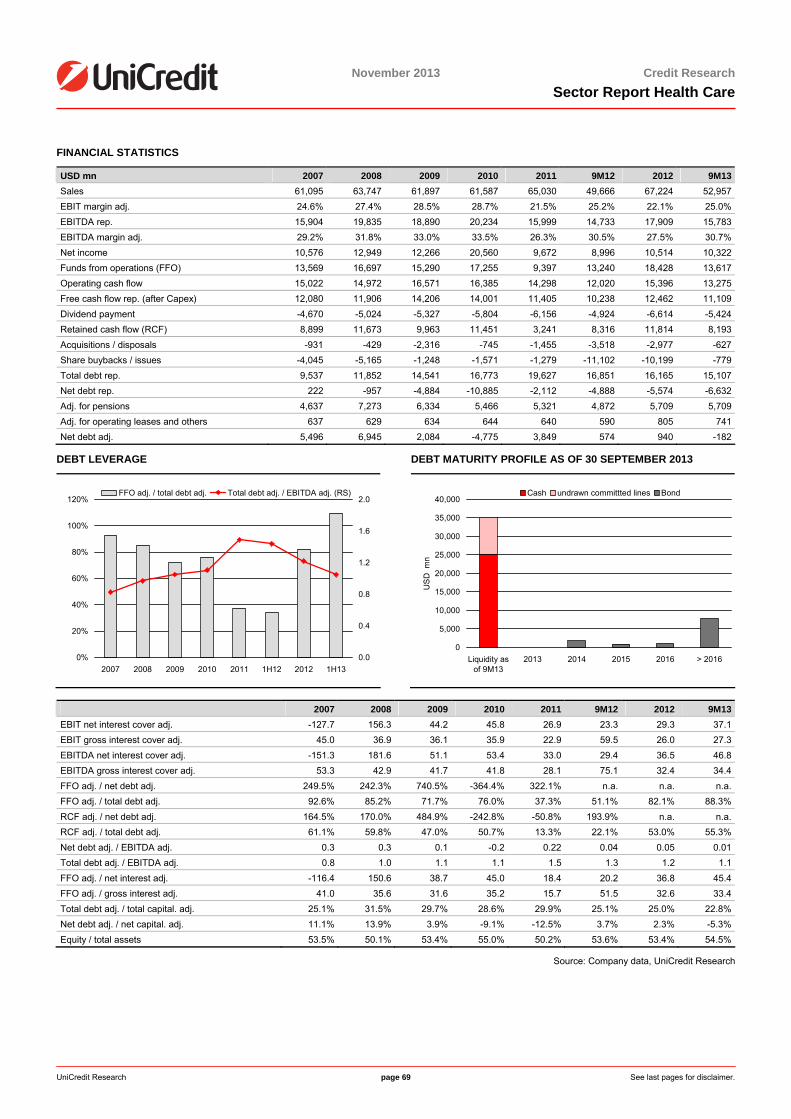

70 Merck & Co.

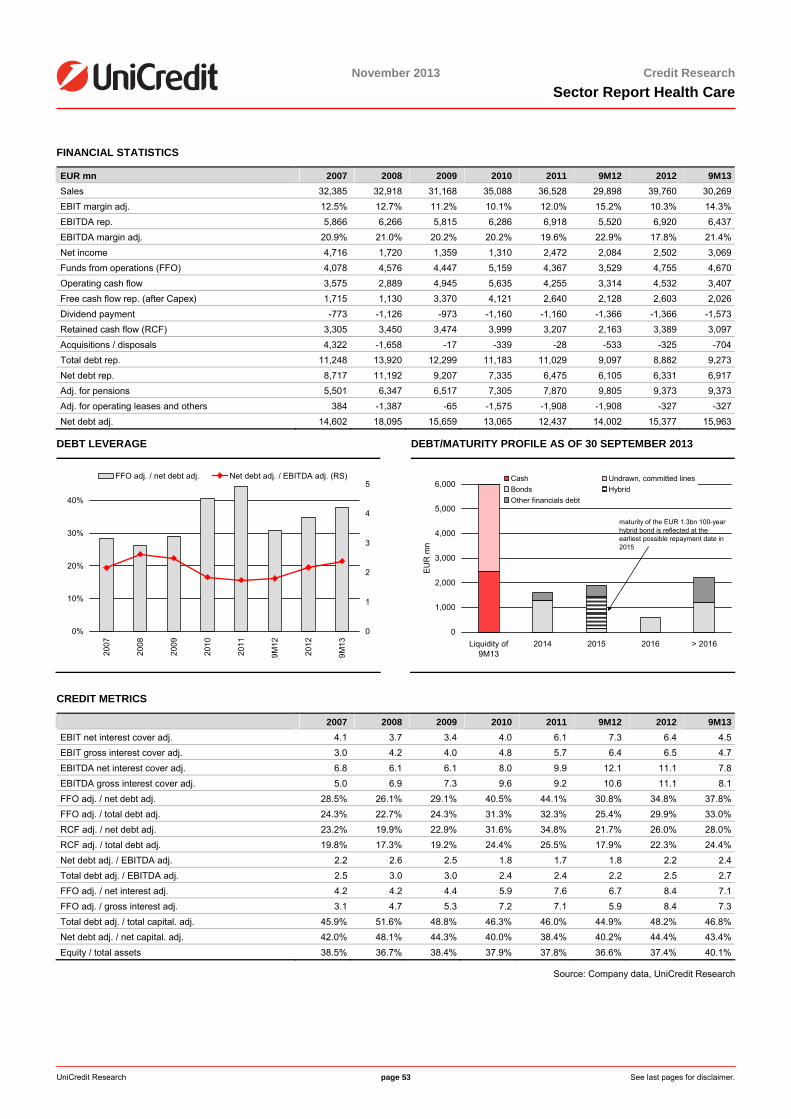

72 Merck KGaA

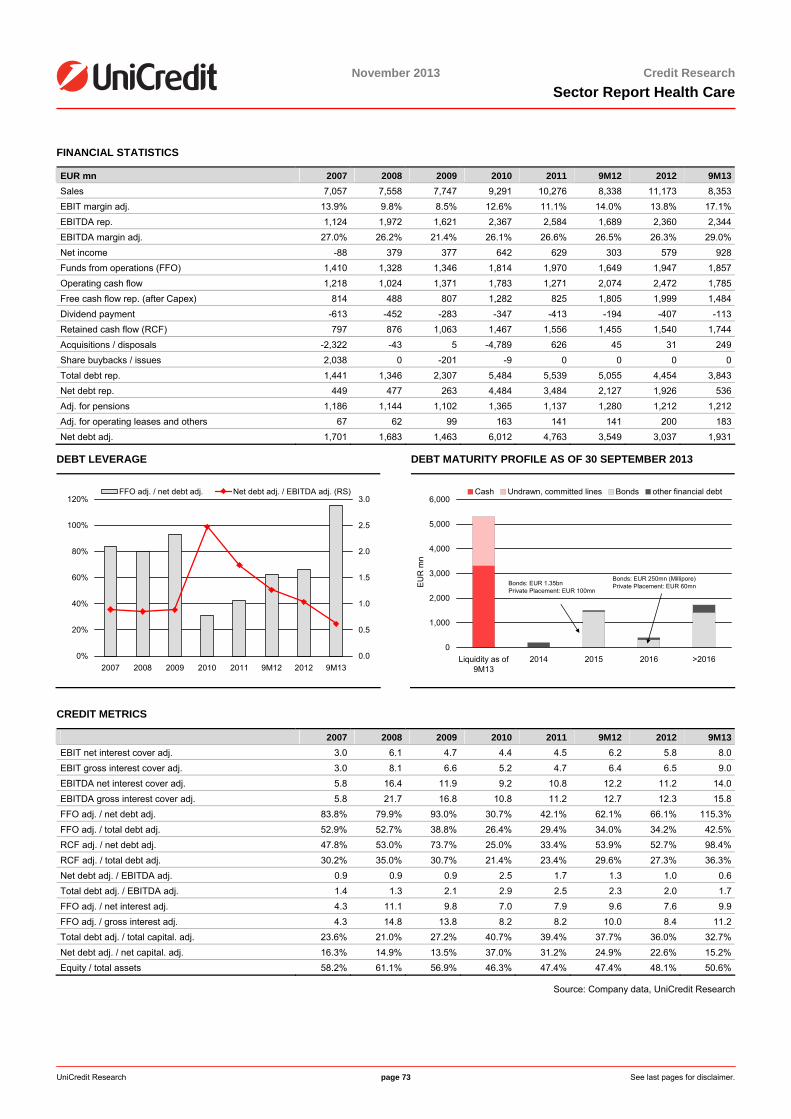

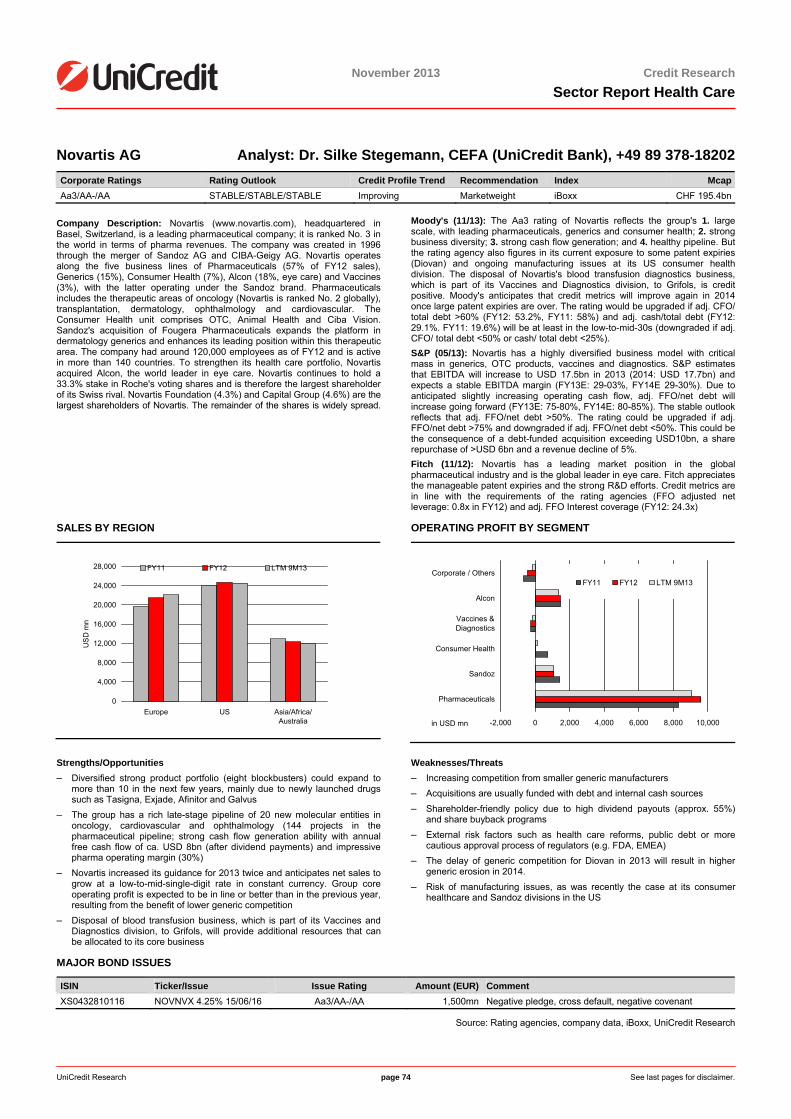

74 Novartis AG

76 Pfizer

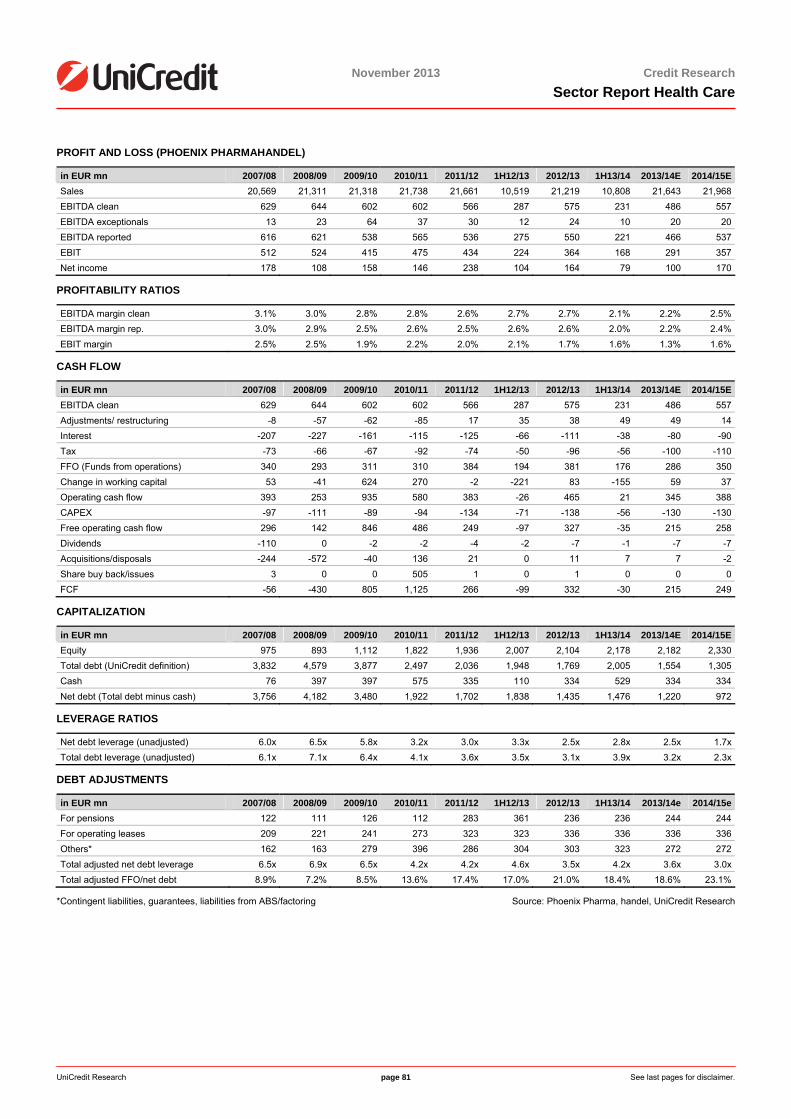

78 Phoenix Pharmahandel

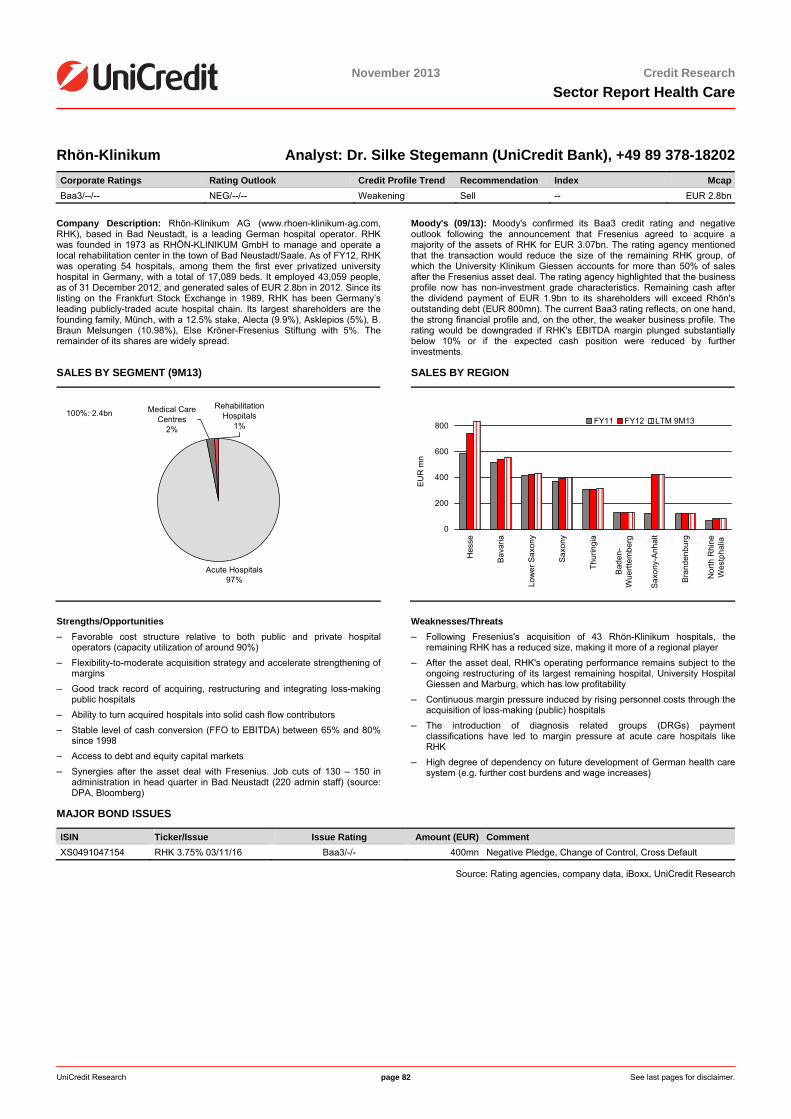

82 Rhön-Klinikum

84 Roche

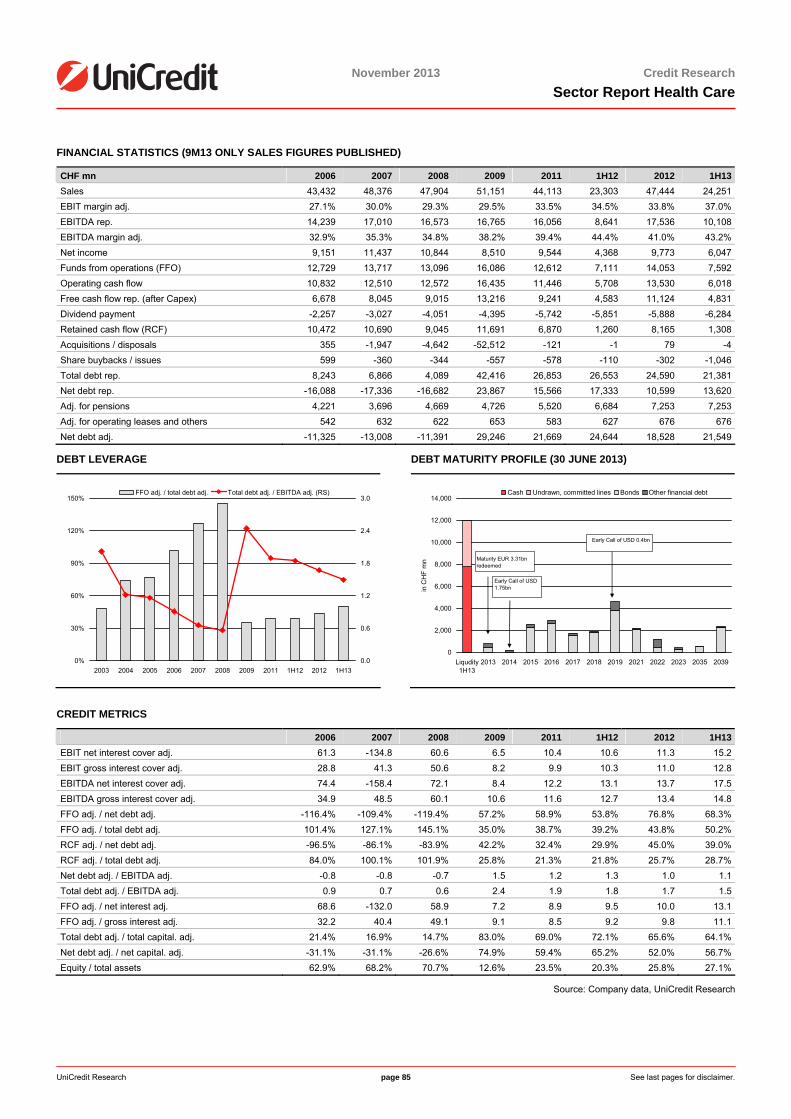

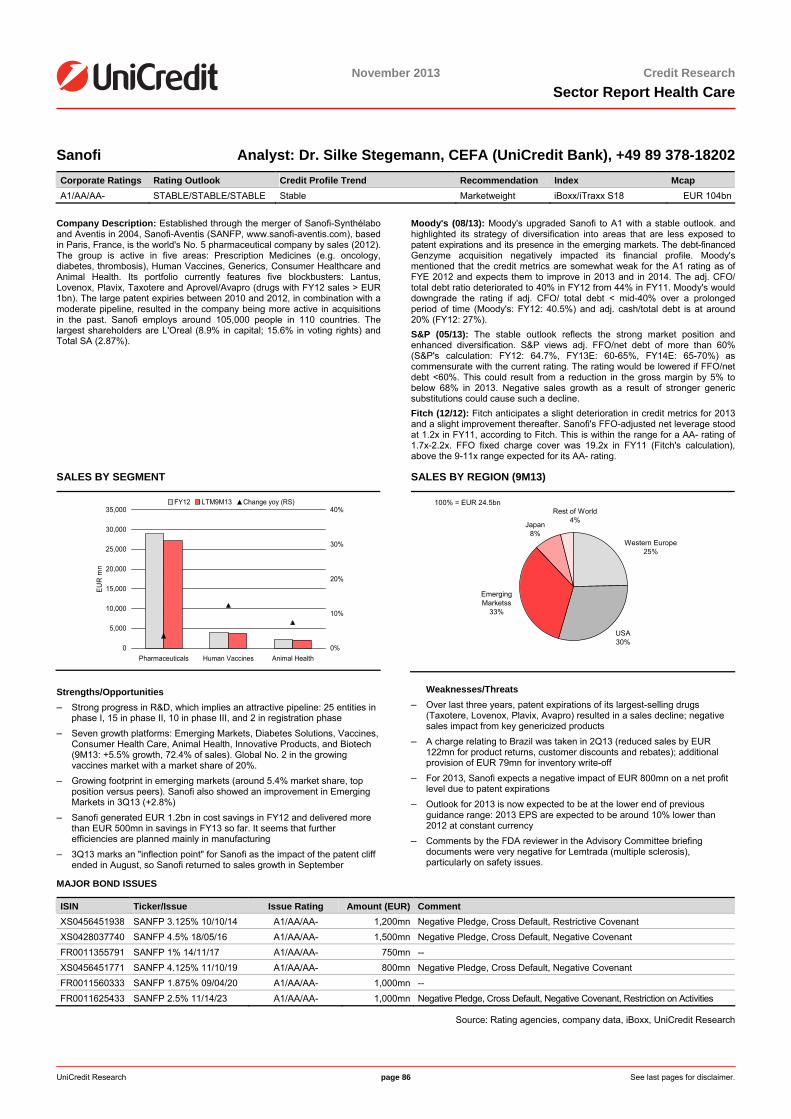

86 Sanofi

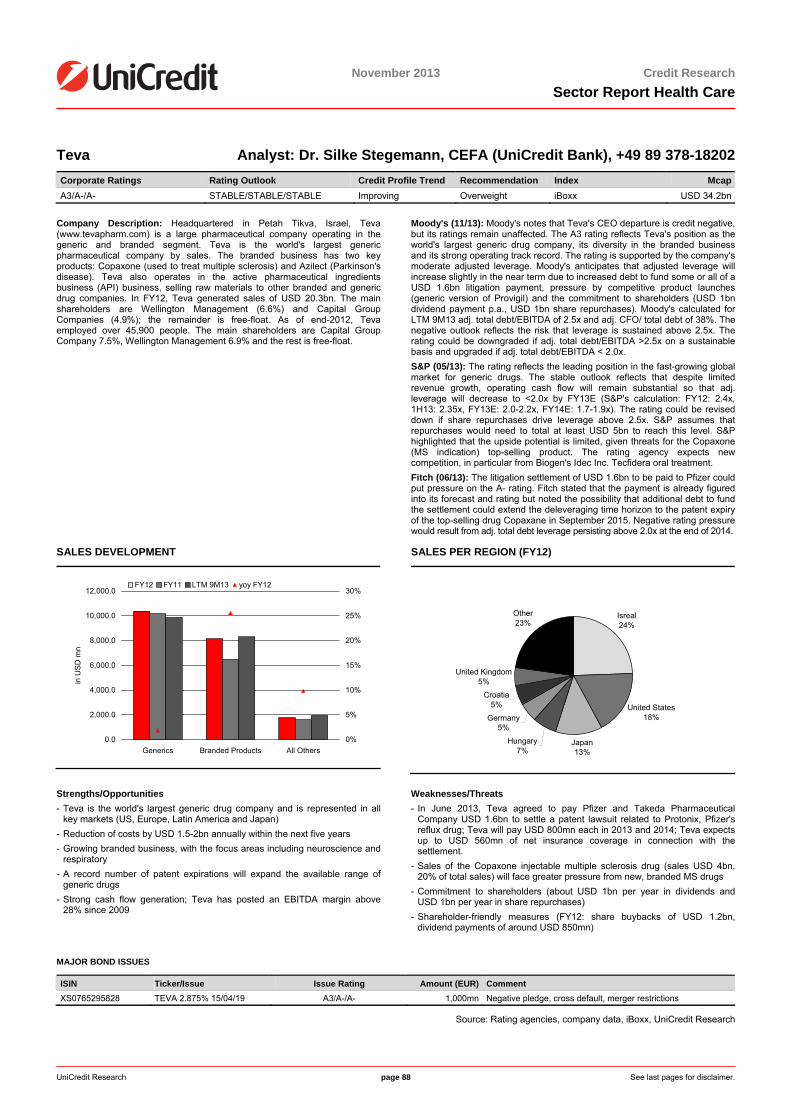

88 Teva

Coverpicture © Daniel Fuhr - Fotolia.com

<date>

UniCredit Research page 3 See last pages for disclaimer.

November 2013 Credit Research

Sector Report Health Care

Summary Sector recommendation: iBoxx Health Care sector: Underweight Top pans: Astra Zeneca Bristol-Myers Squibb Merck & Co. Rhön-Klinikum Top picks: Teva Amgen

We have an underweight recommendation on the iBoxx EUR Health Care sector. Given the relatively high average rating of the iBoxx Health Care index, bonds trade at tight levels and offer only limited potential for further tightening. Our recommendations are based on ourfundamental view on single names combined with relative value considerations. Our top picksare Teva, a generic drug company, and Amgen, the largest biotech company. Both are well-positioned in the global pharma market regarding patent expiries. Among AA rated pharma bonds, we see the best value in Roche (marketweight), highlighted by its attractive pipeline and the high percentage of biological drugs in its portfolio. We have an underweightrecommendation on Astra Zeneca, Bristol-Myers Squibb and Merck & Co due to their tight spread levels and the negative impact on sales from patent expiries.

HY Health Care sector (UniCredit): Hold Top pick: Amplifon Hold: Fresenius Celesio Phoenix Pharmahandel

We have a buy recommendation on Amplifon and a hold recommendation in our HY EUR Healthcare universe on Fresenius, Celesio and Phoenix Pharmahandel. For Amplifon, the number-one global retailer of hearing aid devices and related services, we initiate coverage with abuy recommendation. Despite remaining price pressure, we expect credit metrics to improve in2014 due to a better volume trend and operational cost savings. We like Fresenius's leading market positions in its high margin-business, as well as Phoenix's commitment to deleveraging and conservative financial policy. The main risks to their credit ratings are large M&A deals, as recentlydemonstrated by Fresenius's acquisition of the majority of Rhön-Klinikum's hospitals. The intendedtakeover of pharmaceutical wholesaler and pharmacy owner Celesio by McKesson is slightlypositive for Celesio's bondholders due to synergies and higher purchasing volumes in the future.

Rating development Still the best-rated sector in iBoxx

The pharma sector is still the best-rated in the iBoxx bond universe. In 9M13, the average rating of the iBoxx Health Care index recovered to A+, the same level seen ten years ago. Withfew exceptions, the absence of patent-loss-related downgrades during the peak of the so-called "patent cliff" in 2012 demonstrated the resilience of global pharmaceutical companies' credit.

Pharma outlook 2014: stable credit metrics Medium term: slight improvement in credit metrics

For 2014, we anticipate stable credit metrics and a slight improvement in the medium term due to the higher quality of drugs in the pipeline, fewer patent expiries and more approvals by the US Food and Drug Administration (FDA). With an annual growth rate in the low single-digit range in 2012 and 2013, top-line momentum in the pharmaceutical industry is expected to rebound to 5-7% p.a. by 2016. Looking ahead, regional growth should come from emerging markets and – from a therapeutic perspective – mainly from oncology. Nevertheless, drug companies continue to face price pressure from austerity measures in Europe and the US.

M&A volume increased in 9M13 More activity on the M&A front in 2014, but big M&A of minor focus Licensing deals of more interest Shareholder remuneration up

M&A volume in 9M13 already surpassed its level in 2012. However, the number of in-licensing deals has exceeded M&A deals since 2010. Big M&A deals pose a large risk to credit ratings in this sector. In our view, the improved quality of companies' late-stage pipelines (phase III) is a good indicator that big deals are not absolutely necessary. In FY12, drug makersfavored in-licensing deals (new ingredients from biotech companies) over M&A to improve their drug pipelines, a trend that should continue. Nevertheless, 2014 could be more active on the M&Afront, after increasing volume already in 9M13. After more debt reduction, pharma companies willagain be able to distribute more profits to shareholders via share buy-backs or dividends, in our view.

Pharma bond supply and outlook

In 2014, we expect issuance activity to more than double yoy in the iBoxx EUR Healthcare sector and increase slightly for the corresponding HY sector. This is mainly due to the companies' redemption schedules. Opportunistic M&A could increase this number further. For 2014,yield levels in EUR should remain well below those in USD; more issuance in EUR is expected. Weexpect to see issuance of EUR 5bn in the iBoxx EUR Healthcare index and EUR 2.5bn in the corresponding HY sector. Issuance activity in our HY EUR healthcare universe is supported byexpected bond issues from Fresenius after the asset deal with Rhön-Klinikum.

<date>

UniCredit Research page 4 See last pages for disclaimer.

November 2013 Credit Research

Sector Report Health Care

Sector SWOT Analysis Strengths/opportunities ■ The healthcare business is non-cyclical with stable cash-flow generation, even during the

economic crisis.

■ The iBoxx EUR Healthcare is the best-rated sector in the iBoxx universe with low leverage (average 1.6x adj. total debt/EBITDA in 9M13).

■ Business models are supported by demographic trends in the western hemisphere: rising life expectancy, an increasing proportion of elderly people, an increase in "lifestyle"diseases and technological progress.

■ Emerging markets will be the growth region over the next few years. IMS Health, a research institute, predicts that emerging markets will grow at a total annual rate of 10-13% between 2012 and 2016.

■ There are high barriers-to-entry in the healthcare sector in general. Big pharma companiesreport high R&D costs (15% of sales) and marketing costs (25% of sales). The pharmaceuticalwholesale and dialysis markets are also characterized by oligopolistic structures.

■ Restructuring programs bolstered big pharma companies' abilities to generate strong cashflows. Also, pharmaceutical wholesalers (Celesio, Phoenix Pharmahandel) have efficiencyprograms in place to improve their operating results.

■ Big pharma companies show a healthy margin trend with strong EBITDA margins between25% -40%.

■ Issuers are only headquartered in countries with a AA/AAA credit rating (Germany,Switzerland, UK, US).

Weaknesses/threats ■ Health care reforms remain an uncertainty factor in the US and many European countries.Reforms might hamper top-line growth and might burden industry margins.

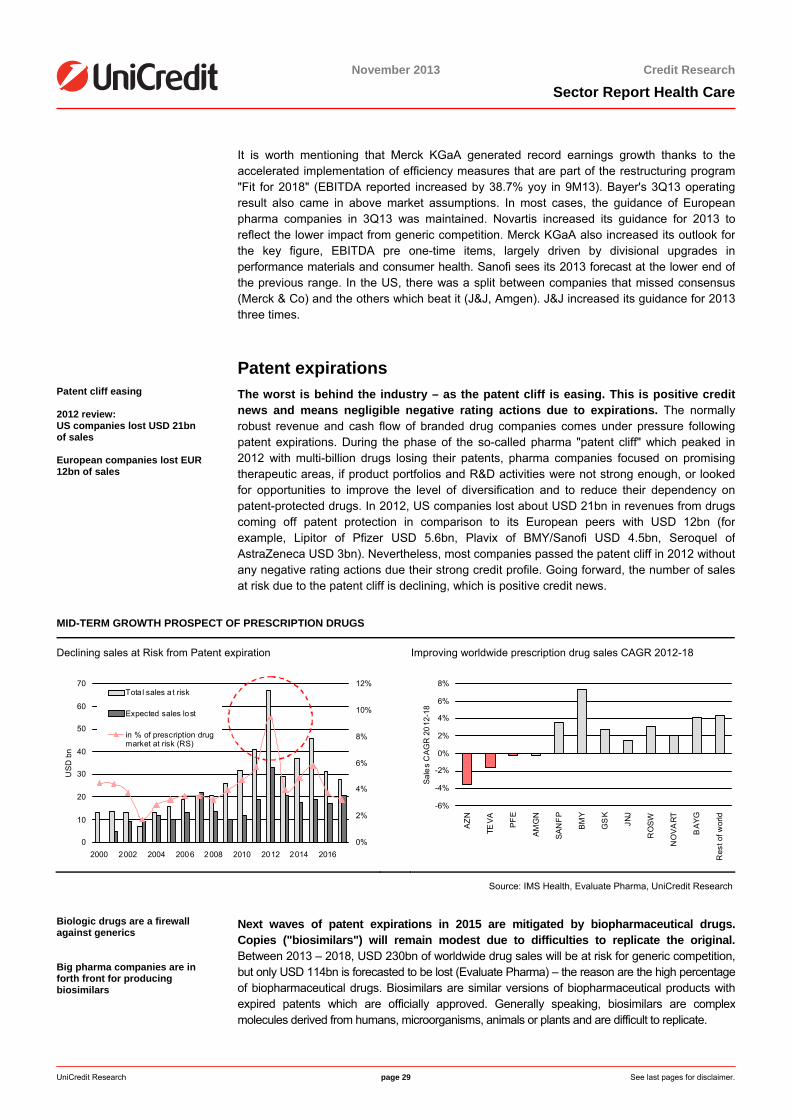

■ Globally-branded pharmaceutical companies went through a challenging period of losing their patent exclusivity ("patent cliff") on attractive drugs in 2011/2012. Nevertheless, theysaw a slight improvement in 2013. The next wave of patent expirations in 2015 will be mitigated by biopharmaceutical drugs, which are difficult to copy.

■ Approval standards and requirements for new drugs have been raised, mainly by the USFood and Drug Administration (FDA). Nevertheless, the FDA's approval process for drugs trended up in 2012, i.e. more new patented drugs will be launched per year with a positiveimpact on the cash flow of pharma companies in the future.

■ Many pharmaceutical companies have shareholder-friendly financial policies with share buy-backs and dividend increases.

■ M&A deals remain an event risk in the healthcare sector for credit investors. In 2012 and2013, big M&A deals were of minor importance for pharma companies.

■ Competition from generic drug manufacturers is getting tougher due to cost pressure from government healthcare reforms and the expiration of patents in developed markets.

■ Weakening late-stage pipelines and a low number of new drugs with blockbuster potential.

■ Uncertainty for generic drug companies prevails due to legal issues arising mainly from "pay for delay" or patent violations. In June 2013, the US Supreme Court ruled that pharmaceutical companies can be sued for antitrust violations when a branded company pays a generic company to keep a cheaper generic version of a drug off the market.

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 5 See last pages for disclaimer.

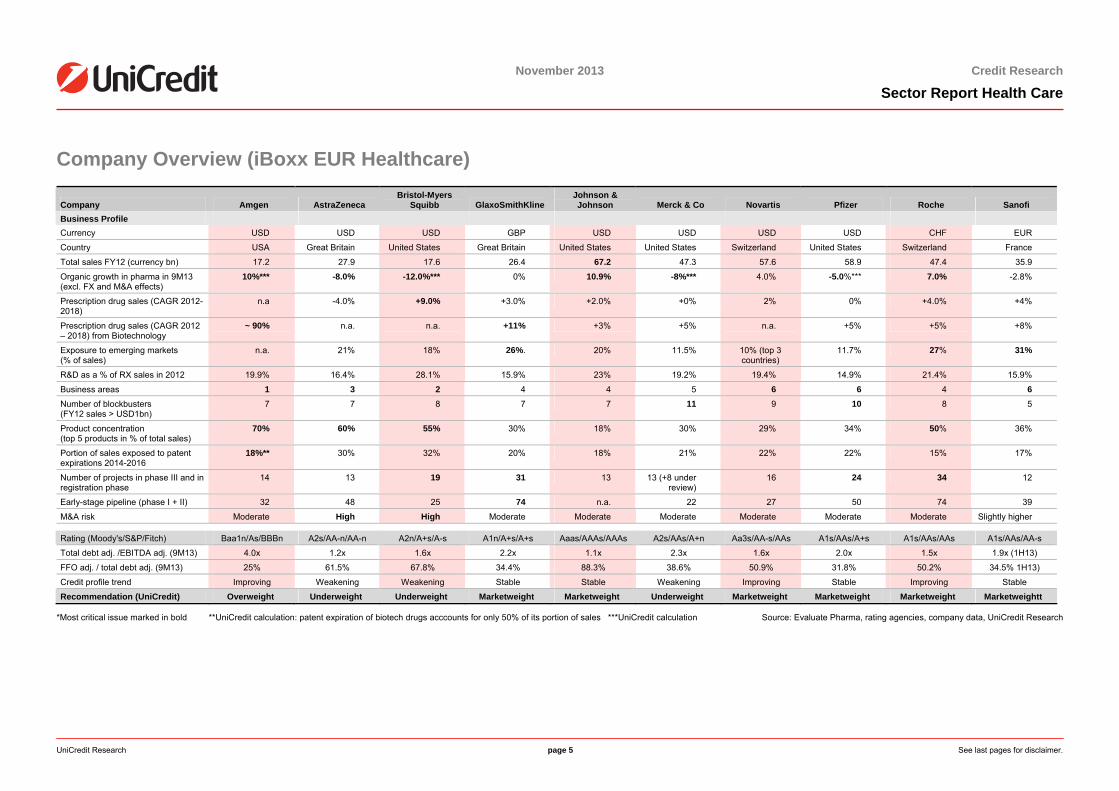

Company Overview (iBoxx EUR Healthcare)

Company Amgen AstraZeneca Bristol-Myers

Squibb GlaxoSmithKline Johnson & Johnson Merck & Co Novartis Pfizer Roche Sanofi

Business Profile Currency USD USD USD GBP USD USD USD USD CHF EUR

Country USA Great Britain United States Great Britain United States United States Switzerland United States Switzerland France

Total sales FY12 (currency bn) 17.2 27.9 17.6 26.4 67.2 47.3 57.6 58.9 47.4 35.9

Organic growth in pharma in 9M13 (excl. FX and M&A effects)

10%*** -8.0% -12.0%*** 0% 10.9% -8%*** 4.0% -5.0%*** 7.0% -2.8%

Prescription drug sales (CAGR 2012-2018)

n.a -4.0% +9.0% +3.0% +2.0% +0% 2% 0% +4.0% +4%

Prescription drug sales (CAGR 2012 – 2018) from Biotechnology

~ 90% n.a. n.a. +11% +3% +5% n.a. +5% +5% +8%

Exposure to emerging markets (% of sales)

n.a. 21% 18% 26%. 20% 11.5% 10% (top 3 countries)

11.7% 27% 31%

R&D as a % of RX sales in 2012 19.9% 16.4% 28.1% 15.9% 23% 19.2% 19.4% 14.9% 21.4% 15.9%

Business areas 1 3 2 4 4 5 6 6 4 6 Number of blockbusters (FY12 sales > USD1bn)

7 7 8 7 7 11 9 10 8 5

Product concentration (top 5 products in % of total sales)

70% 60% 55% 30% 18% 30% 29% 34% 50% 36%

Portion of sales exposed to patent expirations 2014-2016

18%** 30% 32% 20% 18% 21% 22% 22% 15% 17%

Number of projects in phase III and in registration phase

14 13 19 31 13 13 (+8 under review)

16 24 34 12

Early-stage pipeline (phase I + II) 32 48 25 74 n.a. 22 27 50 74 39

M&A risk Moderate High High Moderate Moderate Moderate Moderate Moderate Moderate Slightly higher

Rating (Moody's/S&P/Fitch) Baa1n/As/BBBn A2s/AA-n/AA-n A2n/A+s/A-s A1n/A+s/A+s Aaas/AAAs/AAAs A2s/AAs/A+n Aa3s/AA-s/AAs A1s/AAs/A+s A1s/AAs/AAs A1s/AAs/AA-s

Total debt adj. /EBITDA adj. (9M13) 4.0x 1.2x 1.6x 2.2x 1.1x 2.3x 1.6x 2.0x 1.5x 1.9x (1H13)

FFO adj. / total debt adj. (9M13) 25% 61.5% 67.8% 34.4% 88.3% 38.6% 50.9% 31.8% 50.2% 34.5% 1H13)

Credit profile trend Improving Weakening Weakening Stable Stable Weakening Improving Stable Improving Stable

Recommendation (UniCredit) Overweight Underweight Underweight Marketweight Marketweight Underweight Marketweight Marketweight Marketweight Marketweightt

*Most critical issue marked in bold **UniCredit calculation: patent expiration of biotech drugs acccounts for only 50% of its portion of sales ***UniCredit calculation Source: Evaluate Pharma, rating agencies, company data, UniCredit Research

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 6 See last pages for disclaimer.

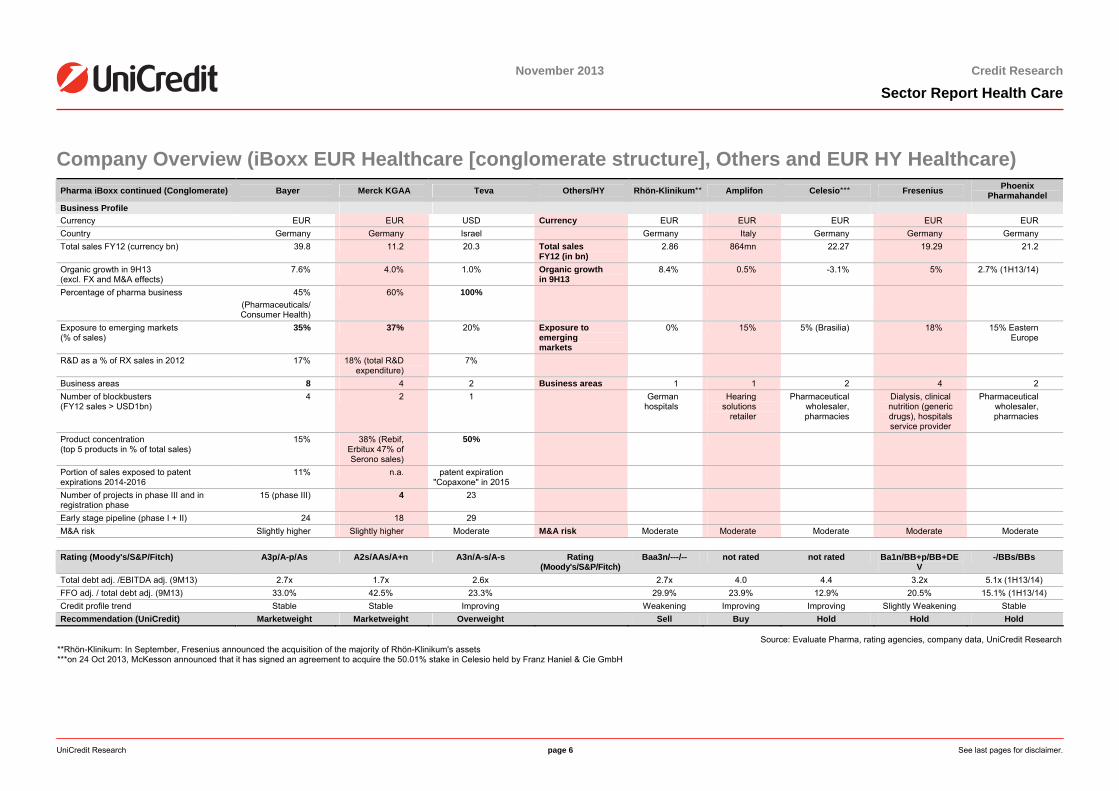

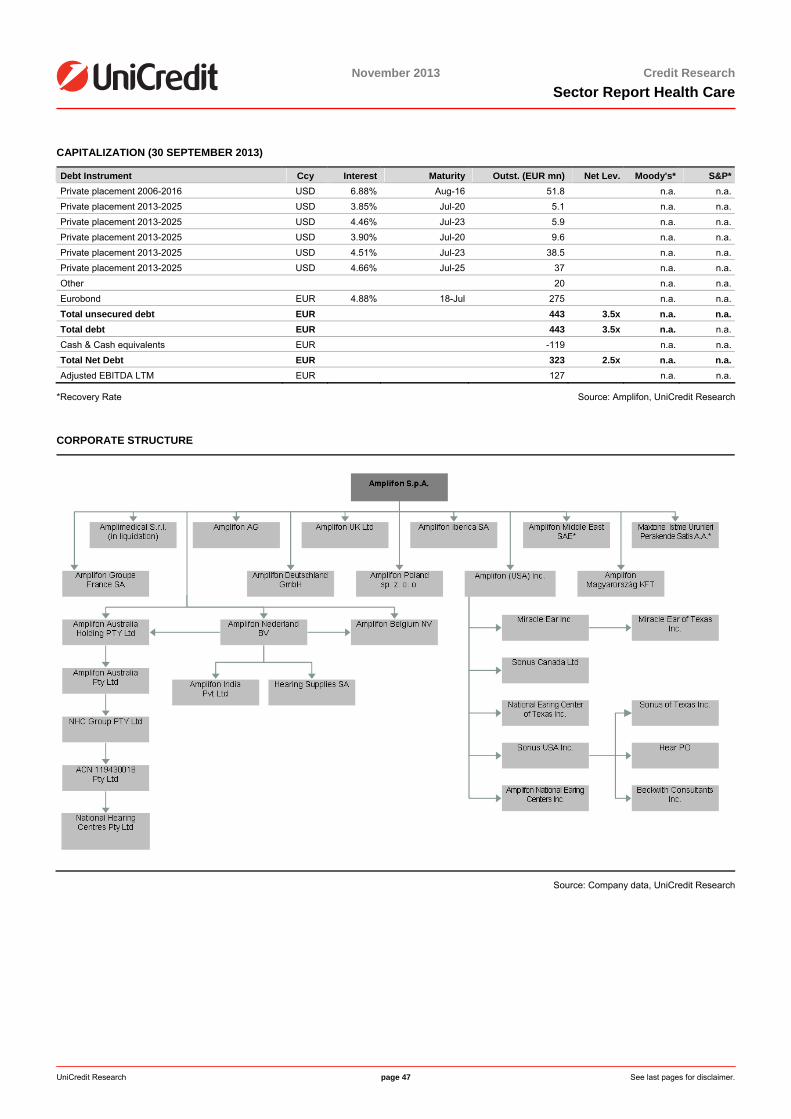

Company Overview (iBoxx EUR Healthcare [conglomerate structure], Others and EUR HY Healthcare) Pharma iBoxx continued (Conglomerate) Bayer Merck KGAA Teva Others/HY Rhön-Klinikum** Amplifon Celesio*** Fresenius Phoenix

Pharmahandel Business Profile Currency EUR EUR USD Currency EUR EUR EUR EUR EUR Country Germany Germany Israel Germany Italy Germany Germany Germany Total sales FY12 (currency bn) 39.8 11.2 20.3 Total sales

FY12 (in bn) 2.86 864mn 22.27 19.29 21.2

Organic growth in 9H13 (excl. FX and M&A effects)

7.6% 4.0% 1.0% Organic growth in 9H13

8.4% 0.5% -3.1% 5% 2.7% (1H13/14)

Percentage of pharma business 45% (Pharmaceuticals/ Consumer Health)

60% 100%

Exposure to emerging markets (% of sales)

35% 37% 20% Exposure to emerging markets

0% 15% 5% (Brasilia) 18% 15% Eastern Europe

R&D as a % of RX sales in 2012 17% 18% (total R&D expenditure)

7%

Business areas 8 4 2 Business areas 1 1 2 4 2 Number of blockbusters (FY12 sales > USD1bn)

4 2 1 German hospitals

Hearing solutions

retailer

Pharmaceutical wholesaler, pharmacies

Dialysis, clinical nutrition (generic drugs), hospitals service provider

Pharmaceutical wholesaler, pharmacies

Product concentration (top 5 products in % of total sales)

15% 38% (Rebif, Erbitux 47% of Serono sales)

50%

Portion of sales exposed to patent expirations 2014-2016

11% n.a. patent expiration "Copaxone" in 2015

Number of projects in phase III and in registration phase

15 (phase III) 4 23

Early stage pipeline (phase I + II) 24 18 29 M&A risk Slightly higher Slightly higher Moderate M&A risk Moderate Moderate Moderate Moderate Moderate Rating (Moody's/S&P/Fitch) A3p/A-p/As A2s/AAs/A+n A3n/A-s/A-s Rating

(Moody's/S&P/Fitch) Baa3n/---/-- not rated not rated Ba1n/BB+p/BB+DE

V -/BBs/BBs

Total debt adj. /EBITDA adj. (9M13) 2.7x 1.7x 2.6x 2.7x 4.0 4.4 3.2x 5.1x (1H13/14) FFO adj. / total debt adj. (9M13) 33.0% 42.5% 23.3% 29.9% 23.9% 12.9% 20.5% 15.1% (1H13/14) Credit profile trend Stable Stable Improving Weakening Improving Improving Slightly Weakening Stable Recommendation (UniCredit) Marketweight Marketweight Overweight Sell Buy Hold Hold Hold

Source: Evaluate Pharma, rating agencies, company data, UniCredit Research **Rhön-Klinikum: In September, Fresenius announced the acquisition of the majority of Rhön-Klinikum's assets ***on 24 Oct 2013, McKesson announced that it has signed an agreement to acquire the 50.01% stake in Celesio held by Franz Haniel & Cie GmbH

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 7 See last pages for disclaimer.

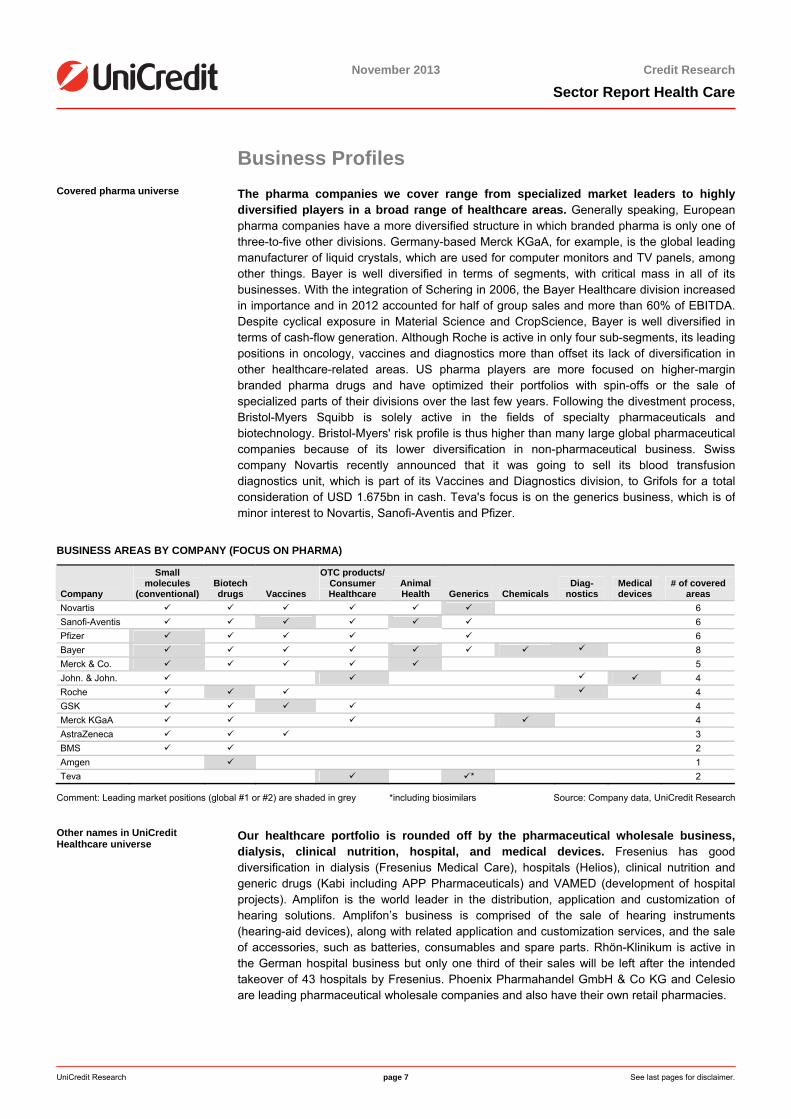

Business Profiles Covered pharma universe The pharma companies we cover range from specialized market leaders to highly

diversified players in a broad range of healthcare areas. Generally speaking, Europeanpharma companies have a more diversified structure in which branded pharma is only one ofthree-to-five other divisions. Germany-based Merck KGaA, for example, is the global leading manufacturer of liquid crystals, which are used for computer monitors and TV panels, among other things. Bayer is well diversified in terms of segments, with critical mass in all of its businesses. With the integration of Schering in 2006, the Bayer Healthcare division increasedin importance and in 2012 accounted for half of group sales and more than 60% of EBITDA.Despite cyclical exposure in Material Science and CropScience, Bayer is well diversified in terms of cash-flow generation. Although Roche is active in only four sub-segments, its leading positions in oncology, vaccines and diagnostics more than offset its lack of diversification in other healthcare-related areas. US pharma players are more focused on higher-margin branded pharma drugs and have optimized their portfolios with spin-offs or the sale of specialized parts of their divisions over the last few years. Following the divestment process, Bristol-Myers Squibb is solely active in the fields of specialty pharmaceuticals and biotechnology. Bristol-Myers' risk profile is thus higher than many large global pharmaceutical companies because of its lower diversification in non-pharmaceutical business. Swiss company Novartis recently announced that it was going to sell its blood transfusiondiagnostics unit, which is part of its Vaccines and Diagnostics division, to Grifols for a totalconsideration of USD 1.675bn in cash. Teva's focus is on the generics business, which is ofminor interest to Novartis, Sanofi-Aventis and Pfizer.

BUSINESS AREAS BY COMPANY (FOCUS ON PHARMA)

Company

Small molecules

(conventional) Biotech drugs Vaccines

OTC products/ Consumer Healthcare

Animal Health Generics Chemicals

Diag-nostics

Medical devices

# of covered areas

Novartis 6 Sanofi-Aventis 6 Pfizer 6 Bayer 8 Merck & Co. 5 John. & John. 4 Roche 4 GSK 4 Merck KGaA 4 AstraZeneca 3 BMS 2 Amgen 1 Teva * 2

Comment: Leading market positions (global #1 or #2) are shaded in grey *including biosimilars Source: Company data, UniCredit Research

Other names in UniCredit Healthcare universe

Our healthcare portfolio is rounded off by the pharmaceutical wholesale business,dialysis, clinical nutrition, hospital, and medical devices. Fresenius has good diversification in dialysis (Fresenius Medical Care), hospitals (Helios), clinical nutrition and generic drugs (Kabi including APP Pharmaceuticals) and VAMED (development of hospitalprojects). Amplifon is the world leader in the distribution, application and customization of hearing solutions. Amplifon’s business is comprised of the sale of hearing instruments (hearing-aid devices), along with related application and customization services, and the sale of accessories, such as batteries, consumables and spare parts. Rhön-Klinikum is active in the German hospital business but only one third of their sales will be left after the intendedtakeover of 43 hospitals by Fresenius. Phoenix Pharmahandel GmbH & Co KG and Celesio are leading pharmaceutical wholesale companies and also have their own retail pharmacies.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 8 See last pages for disclaimer.

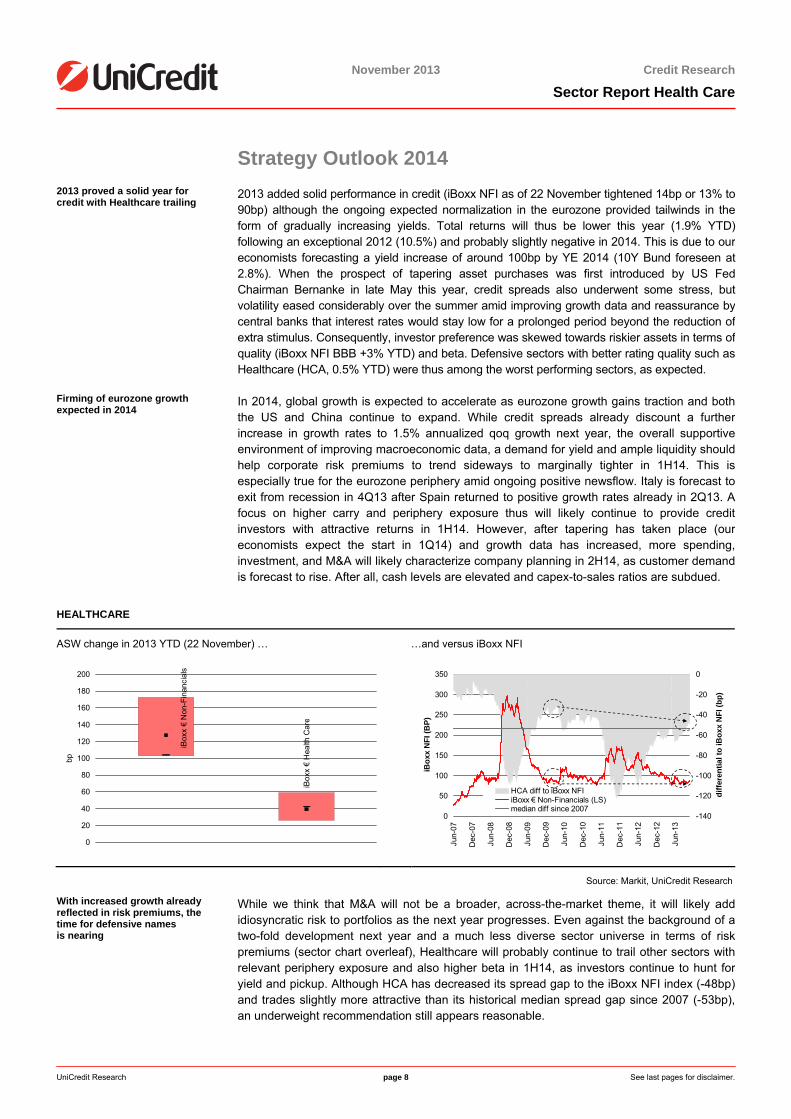

Strategy Outlook 2014 2013 proved a solid year for credit with Healthcare trailing

2013 added solid performance in credit (iBoxx NFI as of 22 November tightened 14bp or 13% to90bp) although the ongoing expected normalization in the eurozone provided tailwinds in theform of gradually increasing yields. Total returns will thus be lower this year (1.9% YTD)following an exceptional 2012 (10.5%) and probably slightly negative in 2014. This is due to oureconomists forecasting a yield increase of around 100bp by YE 2014 (10Y Bund foreseen at 2.8%). When the prospect of tapering asset purchases was first introduced by US FedChairman Bernanke in late May this year, credit spreads also underwent some stress, butvolatility eased considerably over the summer amid improving growth data and reassurance by central banks that interest rates would stay low for a prolonged period beyond the reduction ofextra stimulus. Consequently, investor preference was skewed towards riskier assets in terms ofquality (iBoxx NFI BBB +3% YTD) and beta. Defensive sectors with better rating quality such as Healthcare (HCA, 0.5% YTD) were thus among the worst performing sectors, as expected.

Firming of eurozone growth expected in 2014

In 2014, global growth is expected to accelerate as eurozone growth gains traction and both the US and China continue to expand. While credit spreads already discount a furtherincrease in growth rates to 1.5% annualized qoq growth next year, the overall supportiveenvironment of improving macroeconomic data, a demand for yield and ample liquidity should help corporate risk premiums to trend sideways to marginally tighter in 1H14. This isespecially true for the eurozone periphery amid ongoing positive newsflow. Italy is forecast toexit from recession in 4Q13 after Spain returned to positive growth rates already in 2Q13. A focus on higher carry and periphery exposure thus will likely continue to provide creditinvestors with attractive returns in 1H14. However, after tapering has taken place (oureconomists expect the start in 1Q14) and growth data has increased, more spending,investment, and M&A will likely characterize company planning in 2H14, as customer demandis forecast to rise. After all, cash levels are elevated and capex-to-sales ratios are subdued.

HEALTHCARE

ASW change in 2013 YTD (22 November) … …and versus iBoxx NFI

iBox

x €

Hea

lth C

are

iBox

x €

Non

-Fin

anci

als

0

20

40

60

80

100

120

140

160

180

200

bp

0

50

100

150

200

250

300

350

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

iBox

x N

FI (B

P)

-140

-120

-100

-80

-60

-40

-20

0

diffe

rent

ial t

o iB

oxx

NFI

(bp)

HCA diff to iBoxx NFIiBoxx € Non-Financials (LS)median diff since 2007

Source: Markit, UniCredit Research

With increased growth already reflected in risk premiums, the time for defensive names is nearing

While we think that M&A will not be a broader, across-the-market theme, it will likely addidiosyncratic risk to portfolios as the next year progresses. Even against the background of atwo-fold development next year and a much less diverse sector universe in terms of riskpremiums (sector chart overleaf), Healthcare will probably continue to trail other sectors withrelevant periphery exposure and also higher beta in 1H14, as investors continue to hunt foryield and pickup. Although HCA has decreased its spread gap to the iBoxx NFI index (-48bp) and trades slightly more attractive than its historical median spread gap since 2007 (-53bp), an underweight recommendation still appears reasonable.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 9 See last pages for disclaimer.

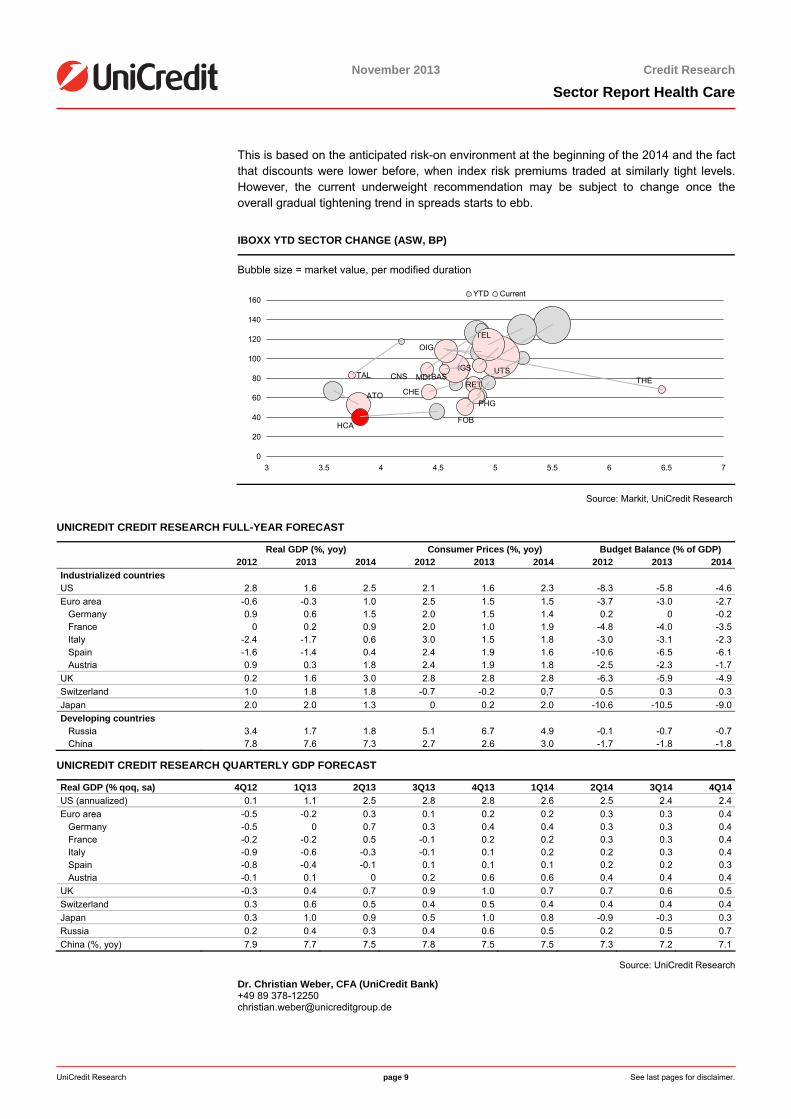

This is based on the anticipated risk-on environment at the beginning of the 2014 and the fact that discounts were lower before, when index risk premiums traded at similarly tight levels.However, the current underweight recommendation may be subject to change once theoverall gradual tightening trend in spreads starts to ebb.

IBOXX YTD SECTOR CHANGE (ASW, BP)

Bubble size = market value, per modified duration

TALTHEMDICNS BAS

CHEPHG

RET

HCAFOB

OIG

ATO

IGS

TEL

UTS

0

20

40

60

80

100

120

140

160

3 3.5 4 4.5 5 5.5 6 6.5 7

YTD Current

Source: Markit, UniCredit Research

UNICREDIT CREDIT RESEARCH FULL-YEAR FORECAST

Real GDP (%, yoy) Consumer Prices (%, yoy) Budget Balance (% of GDP) 2012 2013 2014 2012 2013 2014 2012 2013 2014Industrialized countries US 2.8 1.6 2.5 2.1 1.6 2.3 -8.3 -5.8 -4.6Euro area -0.6 -0.3 1.0 2.5 1.5 1.5 -3.7 -3.0 -2.7 Germany 0.9 0.6 1.5 2.0 1.5 1.4 0.2 0 -0.2 France 0 0.2 0.9 2.0 1.0 1.9 -4.8 -4.0 -3.5 Italy -2.4 -1.7 0.6 3.0 1.5 1.8 -3.0 -3.1 -2.3 Spain -1.6 -1.4 0.4 2.4 1.9 1.6 -10.6 -6.5 -6.1 Austria 0.9 0.3 1.8 2.4 1.9 1.8 -2.5 -2.3 -1.7UK 0.2 1.6 3.0 2.8 2.8 2.8 -6.3 -5.9 -4.9Switzerland 1.0 1.8 1.8 -0.7 -0.2 0,7 0.5 0.3 0.3Japan 2.0 2.0 1.3 0 0.2 2.0 -10.6 -10.5 -9.0Developing countries Russia 3.4 1.7 1.8 5.1 6.7 4.9 -0.1 -0.7 -0.7 China 7.8 7.6 7.3 2.7 2.6 3.0 -1.7 -1.8 -1.8

UNICREDIT CREDIT RESEARCH QUARTERLY GDP FORECAST

Real GDP (% qoq, sa) 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14US (annualized) 0.1 1.1 2.5 2.8 2.8 2.6 2.5 2.4 2.4Euro area -0.5 -0.2 0.3 0.1 0.2 0.2 0.3 0.3 0.4 Germany -0.5 0 0.7 0.3 0.4 0.4 0.3 0.3 0.4 France -0.2 -0.2 0.5 -0.1 0.2 0.2 0.3 0.3 0.4 Italy -0.9 -0.6 -0.3 -0.1 0.1 0.2 0.2 0.3 0.4 Spain -0.8 -0.4 -0.1 0.1 0.1 0.1 0.2 0.2 0.3 Austria -0.1 0.1 0 0.2 0.6 0.6 0.4 0.4 0.4UK -0.3 0.4 0.7 0.9 1.0 0.7 0.7 0.6 0.5Switzerland 0.3 0.6 0.5 0.4 0.5 0.4 0.4 0.4 0.4Japan 0.3 1.0 0.9 0.5 1.0 0.8 -0.9 -0.3 0.3Russia 0.2 0.4 0.3 0.4 0.6 0.5 0.2 0.5 0.7China (%, yoy) 7.9 7.7 7.5 7.8 7.5 7.5 7.3 7.2 7.1

Source: UniCredit Research

Dr. Christian Weber, CFA (UniCredit Bank) +49 89 378-12250 [email protected]

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 10 See last pages for disclaimer.

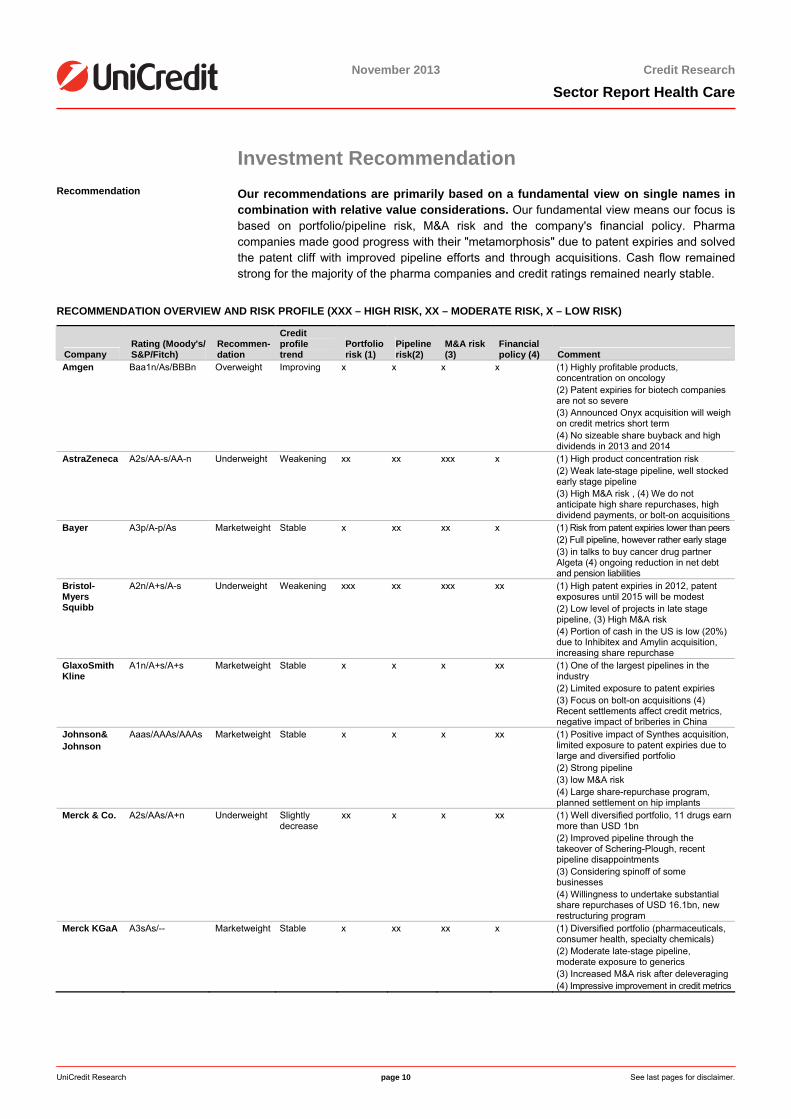

Investment Recommendation Recommendation Our recommendations are primarily based on a fundamental view on single names in

combination with relative value considerations. Our fundamental view means our focus is based on portfolio/pipeline risk, M&A risk and the company's financial policy. Pharmacompanies made good progress with their "metamorphosis" due to patent expiries and solved the patent cliff with improved pipeline efforts and through acquisitions. Cash flow remainedstrong for the majority of the pharma companies and credit ratings remained nearly stable.

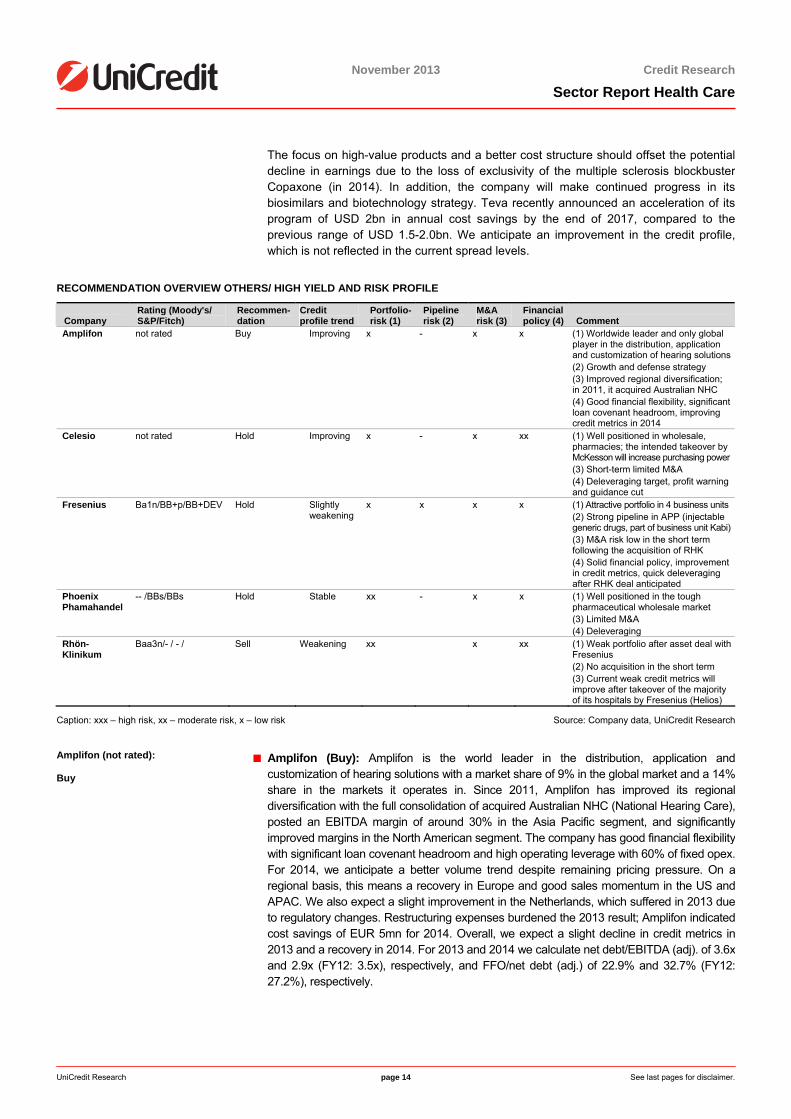

RECOMMENDATION OVERVIEW AND RISK PROFILE (XXX – HIGH RISK, XX – MODERATE RISK, X – LOW RISK)

Company Rating (Moody's/ S&P/Fitch)

Recommen- dation

Credit profile trend

Portfoliorisk (1)

Pipelinerisk(2)

M&A risk(3)

Financial policy (4) Comment

Amgen Baa1n/As/BBBn Overweight Improving x x x x (1) Highly profitable products, concentration on oncology (2) Patent expiries for biotech companies are not so severe (3) Announced Onyx acquisition will weigh on credit metrics short term (4) No sizeable share buyback and high dividends in 2013 and 2014

AstraZeneca A2s/AA-s/AA-n Underweight Weakening xx xx xxx x (1) High product concentration risk (2) Weak late-stage pipeline, well stocked early stage pipeline (3) High M&A risk , (4) We do not anticipate high share repurchases, high dividend payments, or bolt-on acquisitions

Bayer A3p/A-p/As Marketweight Stable x xx xx x (1) Risk from patent expiries lower than peers (2) Full pipeline, however rather early stage (3) in talks to buy cancer drug partner Algeta (4) ongoing reduction in net debt and pension liabilities

Bristol-Myers Squibb

A2n/A+s/A-s Underweight Weakening xxx xx xxx xx (1) High patent expiries in 2012, patent exposures until 2015 will be modest (2) Low level of projects in late stage pipeline, (3) High M&A risk (4) Portion of cash in the US is low (20%) due to Inhibitex and Amylin acquisition, increasing share repurchase

GlaxoSmithKline

A1n/A+s/A+s Marketweight Stable x x x xx (1) One of the largest pipelines in the industry (2) Limited exposure to patent expiries (3) Focus on bolt-on acquisitions (4) Recent settlements affect credit metrics, negative impact of briberies in China

Johnson& Johnson

Aaas/AAAs/AAAs Marketweight Stable x x x xx (1) Positive impact of Synthes acquisition, limited exposure to patent expiries due to large and diversified portfolio (2) Strong pipeline (3) low M&A risk (4) Large share-repurchase program, planned settlement on hip implants

Merck & Co. A2s/AAs/A+n Underweight Slightly decrease

xx x x xx (1) Well diversified portfolio, 11 drugs earn more than USD 1bn (2) Improved pipeline through the takeover of Schering-Plough, recent pipeline disappointments (3) Considering spinoff of some businesses (4) Willingness to undertake substantial share repurchases of USD 16.1bn, new restructuring program

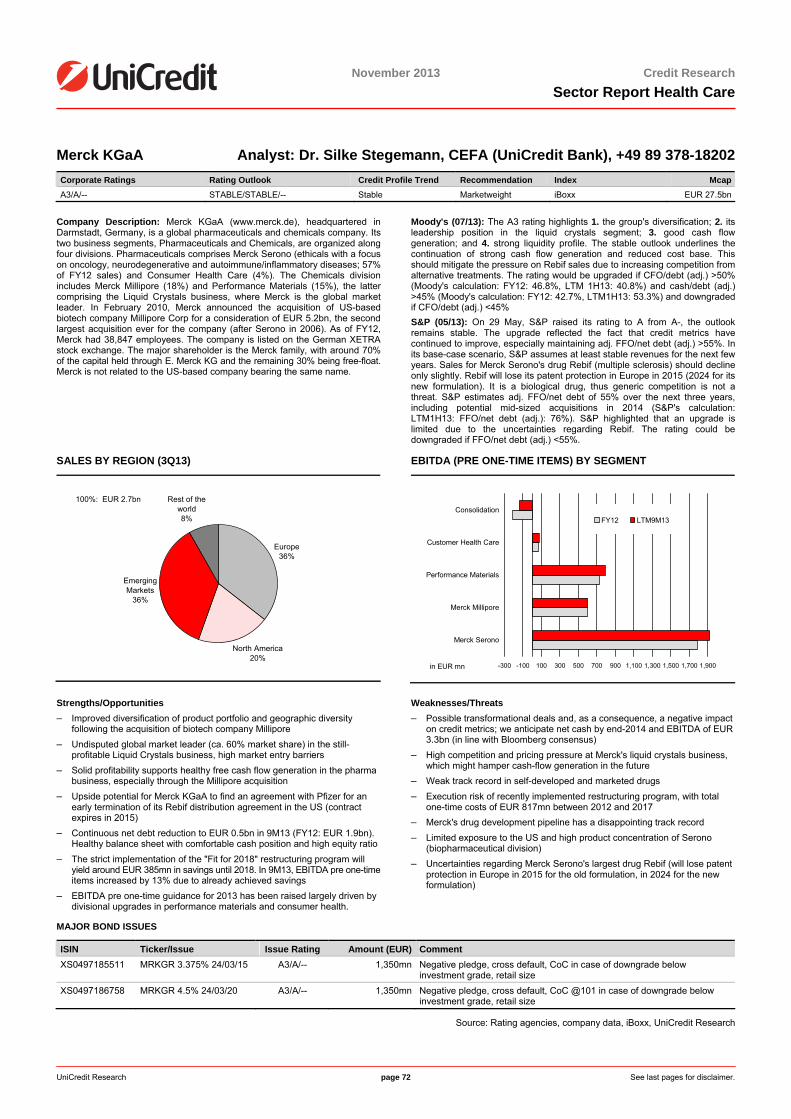

Merck KGaA A3sAs/-- Marketweight Stable x xx xx x (1) Diversified portfolio (pharmaceuticals, consumer health, specialty chemicals) (2) Moderate late-stage pipeline, moderate exposure to generics (3) Increased M&A risk after deleveraging (4) Impressive improvement in credit metrics

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 11 See last pages for disclaimer.

Company Rating (Moody's/ S&P/Fitch)

Recommen- dation

Credit profile trend

Portfoliorisk (1)

Pipelinerisk(2)

M&A risk(3)

Financial policy (4) Comment

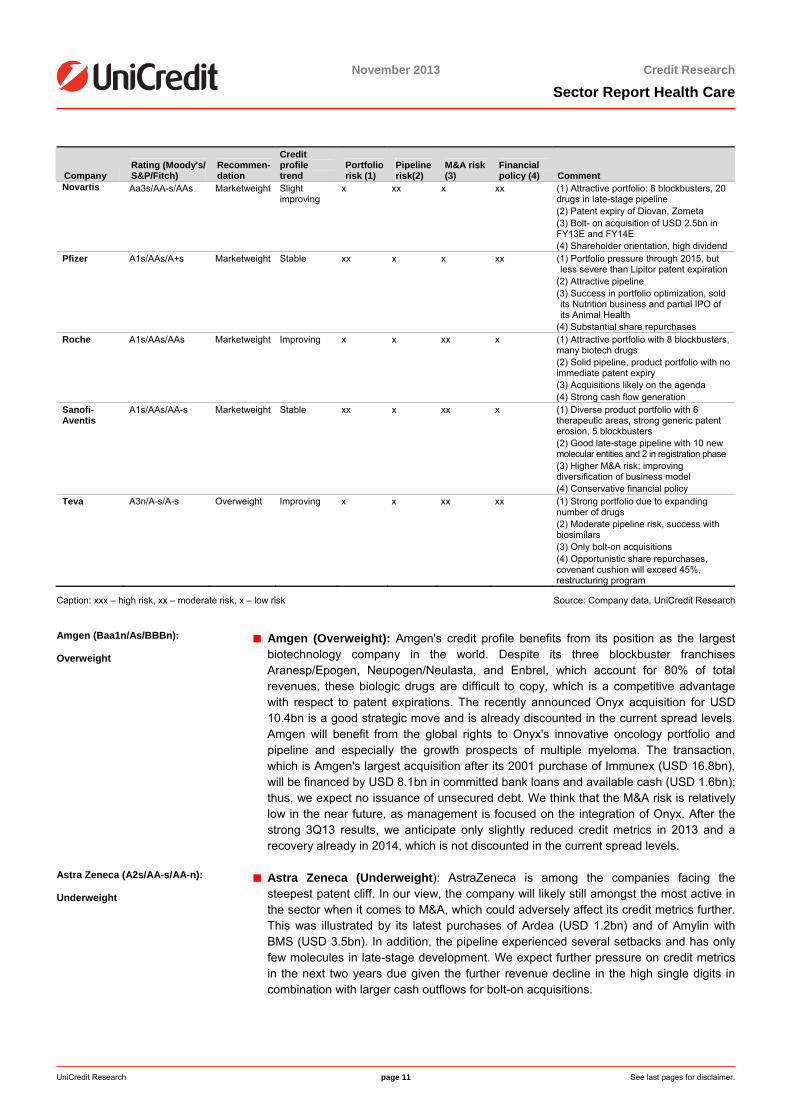

Novartis Aa3s/AA-s/AAs Marketweight Slight improving

x xx x xx (1) Attractive portfolio: 8 blockbusters, 20 drugs in late-stage pipeline (2) Patent expiry of Diovan, Zometa (3) Bolt- on acquisition of USD 2.5bn in FY13E and FY14E (4) Shareholder orientation, high dividend

Pfizer A1s/AAs/A+s Marketweight Stable xx x x xx (1) Portfolio pressure through 2015, but less severe than Lipitor patent expiration

(2) Attractive pipeline (3) Success in portfolio optimization, sold its Nutrition business and partial IPO of its Animal Health

(4) Substantial share repurchases Roche A1s/AAs/AAs Marketweight Improving x x xx x (1) Attractive portfolio with 8 blockbusters,

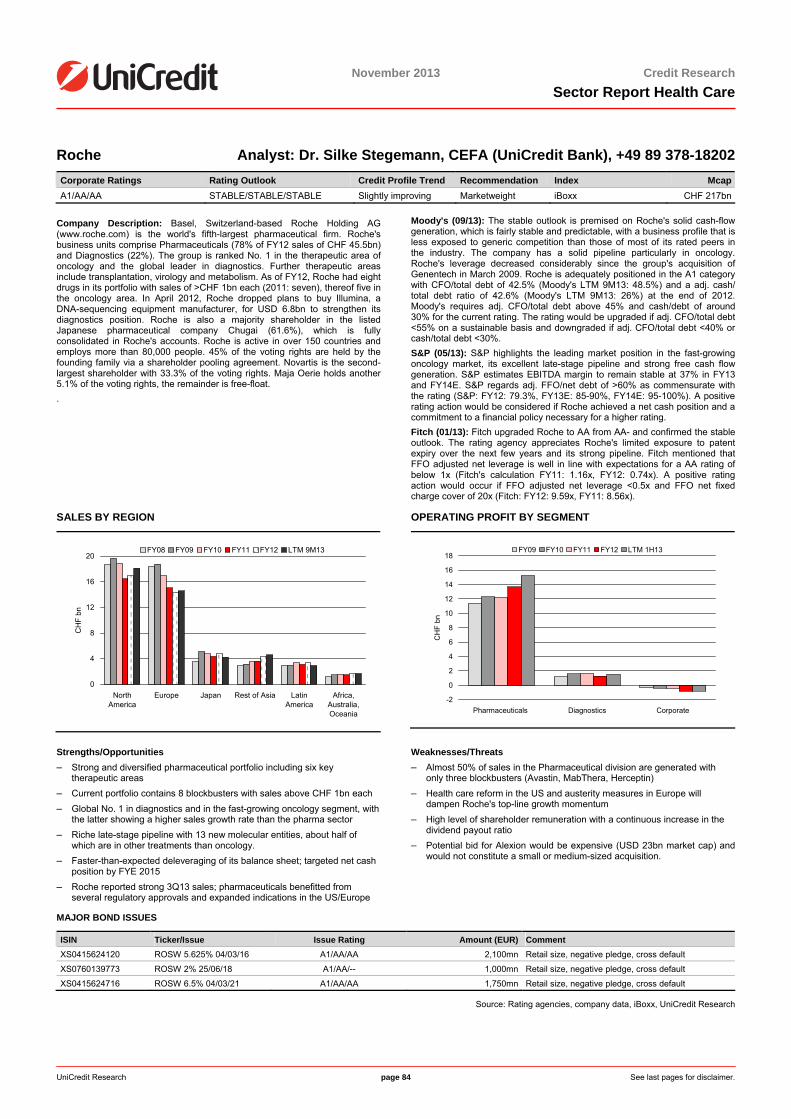

many biotech drugs (2) Solid pipeline, product portfolio with no immediate patent expiry (3) Acquisitions likely on the agenda (4) Strong cash flow generation

Sanofi-Aventis

A1s/AAs/AA-s Marketweight Stable xx x xx x (1) Diverse product portfolio with 6 therapeutic areas, strong generic patent erosion, 5 blockbusters (2) Good late-stage pipeline with 10 new molecular entities and 2 in registration phase (3) Higher M&A risk; improving diversification of business model (4) Conservative financial policy

Teva A3n/A-s/A-s Overweight Improving x x xx xx (1) Strong portfolio due to expanding number of drugs (2) Moderate pipeline risk, success with biosimilars (3) Only bolt-on acquisitions (4) Opportunistic share repurchases, covenant cushion will exceed 45%, restructuring program

Caption: xxx – high risk, xx – moderate risk, x – low risk Source: Company data, UniCredit Research

Amgen (Baa1n/As/BBBn): Overweight

■ Amgen (Overweight): Amgen's credit profile benefits from its position as the largestbiotechnology company in the world. Despite its three blockbuster franchises Aranesp/Epogen, Neupogen/Neulasta, and Enbrel, which account for 80% of totalrevenues, these biologic drugs are difficult to copy, which is a competitive advantagewith respect to patent expirations. The recently announced Onyx acquisition for USD 10.4bn is a good strategic move and is already discounted in the current spread levels.Amgen will benefit from the global rights to Onyx's innovative oncology portfolio and pipeline and especially the growth prospects of multiple myeloma. The transaction, which is Amgen's largest acquisition after its 2001 purchase of Immunex (USD 16.8bn),will be financed by USD 8.1bn in committed bank loans and available cash (USD 1.6bn);thus, we expect no issuance of unsecured debt. We think that the M&A risk is relatively low in the near future, as management is focused on the integration of Onyx. After thestrong 3Q13 results, we anticipate only slightly reduced credit metrics in 2013 and arecovery already in 2014, which is not discounted in the current spread levels.

Astra Zeneca (A2s/AA-s/AA-n): Underweight

■ Astra Zeneca (Underweight): AstraZeneca is among the companies facing the steepest patent cliff. In our view, the company will likely still amongst the most active inthe sector when it comes to M&A, which could adversely affect its credit metrics further. This was illustrated by its latest purchases of Ardea (USD 1.2bn) and of Amylin withBMS (USD 3.5bn). In addition, the pipeline experienced several setbacks and has onlyfew molecules in late-stage development. We expect further pressure on credit metrics in the next two years due given the further revenue decline in the high single digits incombination with larger cash outflows for bolt-on acquisitions.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 12 See last pages for disclaimer.

Bayer (A3p/A-p/As): Marketweight

■ Bayer (Marketweight): The company benefits from its good business diversification,which balances earnings volatility. Bayer's risk from patent expirations is relatively low inthe short term in comparison to its peers. However, its R&D pipeline in Pharmaceuticals beyond recently launched drugs remains earlier stage and therefore more speculative.There are rumors that Bayer is in early-stage talks to buy its Norwegian cancer drug partner Algeta for NOK 336 a share (EV of around USD 2.4bn, source: Bloomberg, EuroInvestor). In our view, a completely debt-financed transaction would only modestly weaken Bayer's credit metrics and would in a worst case merely pose a risk to the positive outlook shared by Moody's and S&P. In addition, Bayer is suffering from underrepresentation of sales in the US healthcare system where price levels for drugsare more attractive. The cautious view on 2013 results remains mainly due to FXeffects. Bayer expects a negative currency impact on operating profit of EUR 200-250mn. From a credit perspective, the ongoing reduction in net debt and pension liabilities is positive, but already discounted in current spread levels.

Bristol Myers (A2n/A+s/A-s) : Underweight

■ Bristol-Myers (Underweight): Bristol-Myers belongs to the companies with the highest risk of a negative impact on credit metrics due to patent expirations, i.e. Plavix and Avapro. The expected recovery of profits will be only short-lived as the next patent cliff is looming in 2015. To balance the negative impact on financials, the company spent more than USD 7.5bn on M&A in FY12. The largest pharma M&A deal in 2012 was Bristol-Myers Squibb's acquisition of Amylin Pharmaceuticals, valued at USD 6.5bn, albeit halfof the deal was paid for by Astra Zeneca. The company recently confirmed that it is still looking for outside deals, which is also credit negative.

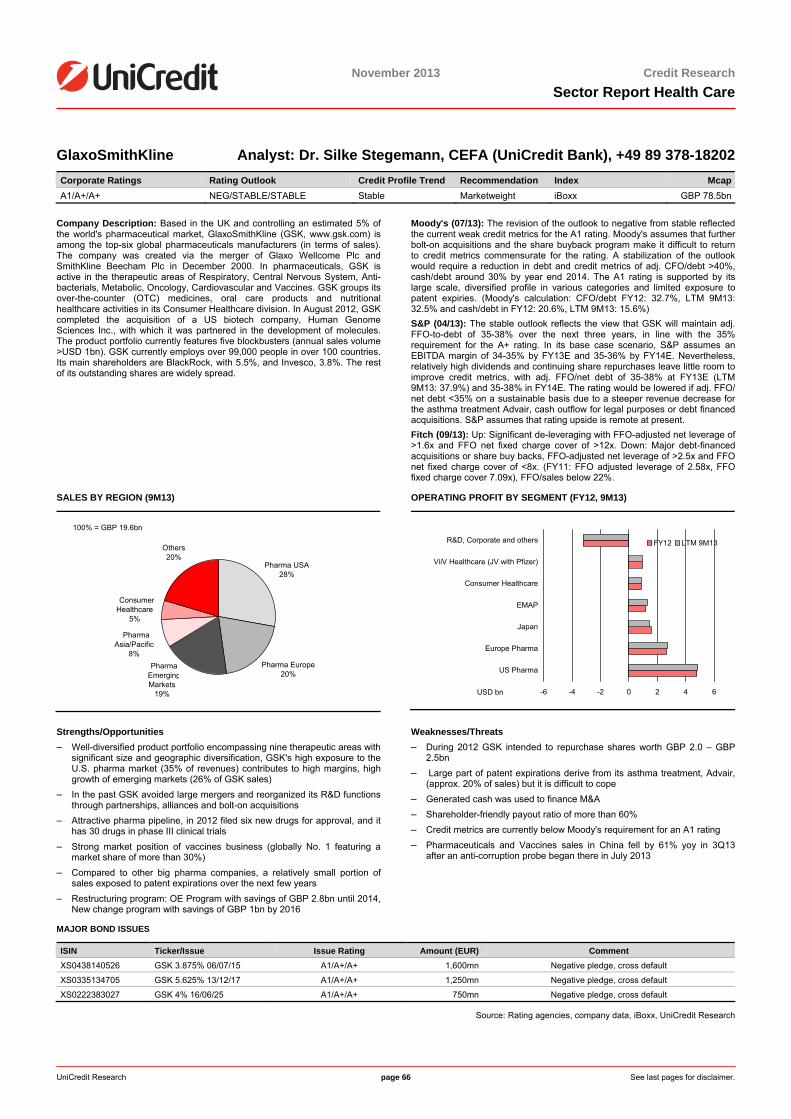

GlaxoSmithKline (A1n/A+s/A+s): Marketweight

■ GlaxoSmithKline (Marketweight): In recent years, Glaxo has increased diversification into new geographic regions and products that are less impacted by patent expiries.Nevertheless, recent bribery allegations in China are impacting GSK heavily, as alternative treatments are available (Novartis, Roche). In terms of patent expirations, the majority has already occurred, and GSK offers an attractive late-stage pipeline. Nevertheless, this is already reflected in the current tight spread levels.

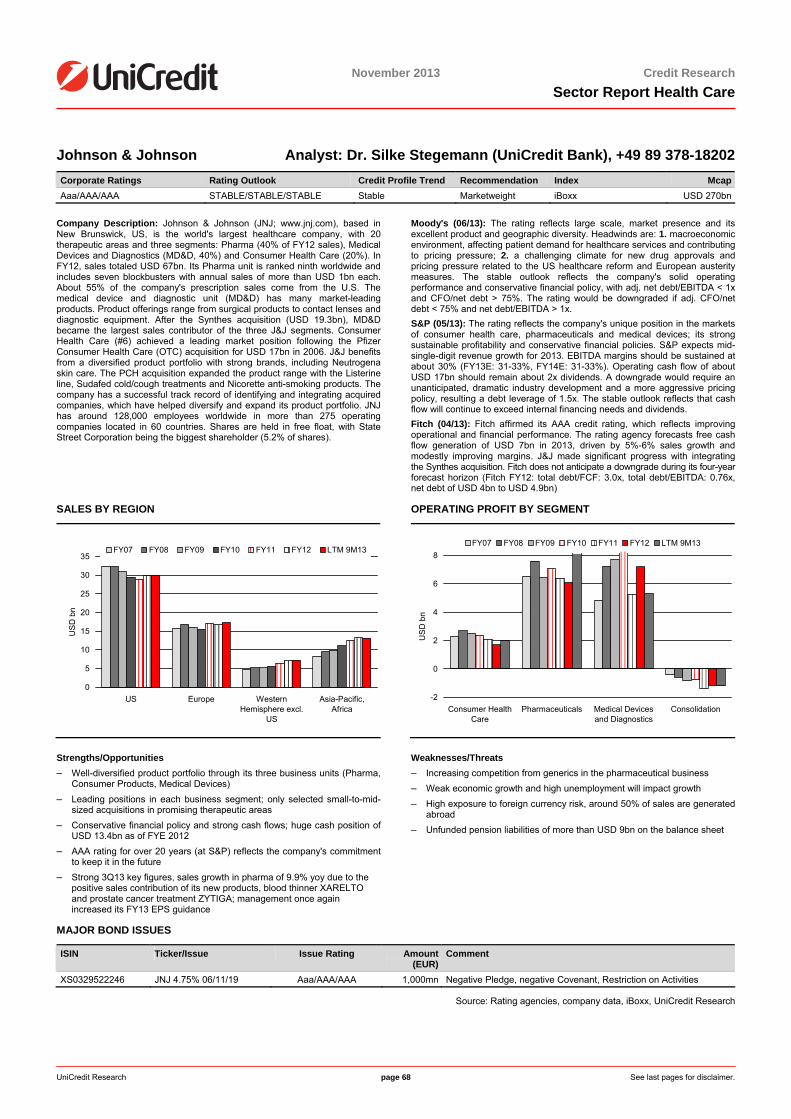

Johnson & Johnson (Aaas/AAAs/AAAs): Marketweight

■ Johnson & Johnson (Marketweight): The company benefits from its large and diversified portfolio. Big generic hits are largely behind the company, and a number ofnew product launches are being rolled out on the pharmaceutical side. The positive impact of the Synthes acquisition is already reflected in the current credit profile with a leverage ratio of 1.0x, which is required for the Aaa rating going forward. J&J increased its 2013 guidance mainly due to the gain on the sale of the equity interest in ElanCorporation. A planned settlement of more than USD 4bn aimed at resolving thousandsof lawsuits over the recalled hip implants is credit negative. Overall, we anticipate stable credit metrics going forward.

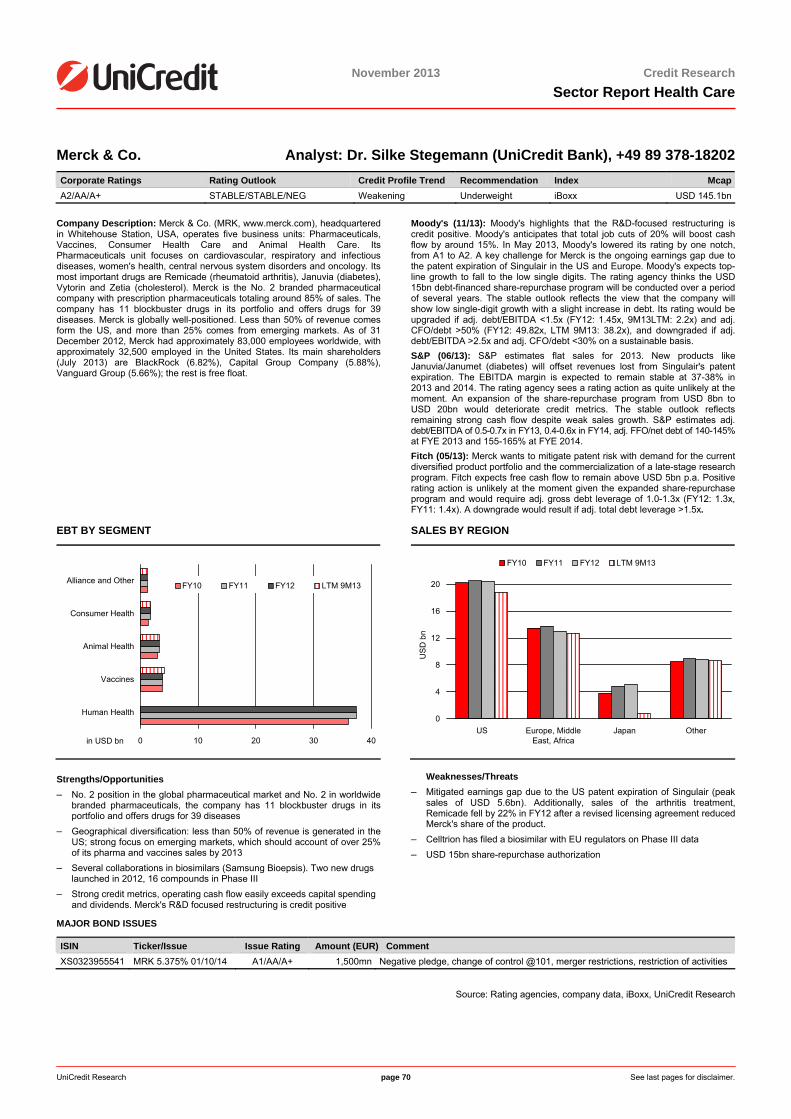

Merck & Co (A2s/AAs/A+n): Underweight

■ Merck & Co (Underweight): A key challenge will be to mitigate the ongoing earnings gap due to the US and European patent expiration of Singulair (US: August 2012, majorEuropean markets: February 2013), a once-a-day oral medicine for chronic treatment of asthma and relief of symptoms of allergic rhinitis. Even with good pipeline growth,Merck's top-line growth will fall in the low single-digits. The announcement of the company in April to extend its share repurchase program to USD 16.1bn is creditnegative. Merck intends to use debt issuances to partly repurchase USD 7.5bn worth ofshares until mid-2014. In October 2013, Merck announced a restructuring program focused on R&D, marketing and administrative expenses, to reduce annual opex byUSD 2.5bn by the end of 2015 vs. 2012 levels. However, this should compensate onlypartly for the impact of share repurchases and declining top-line growth.

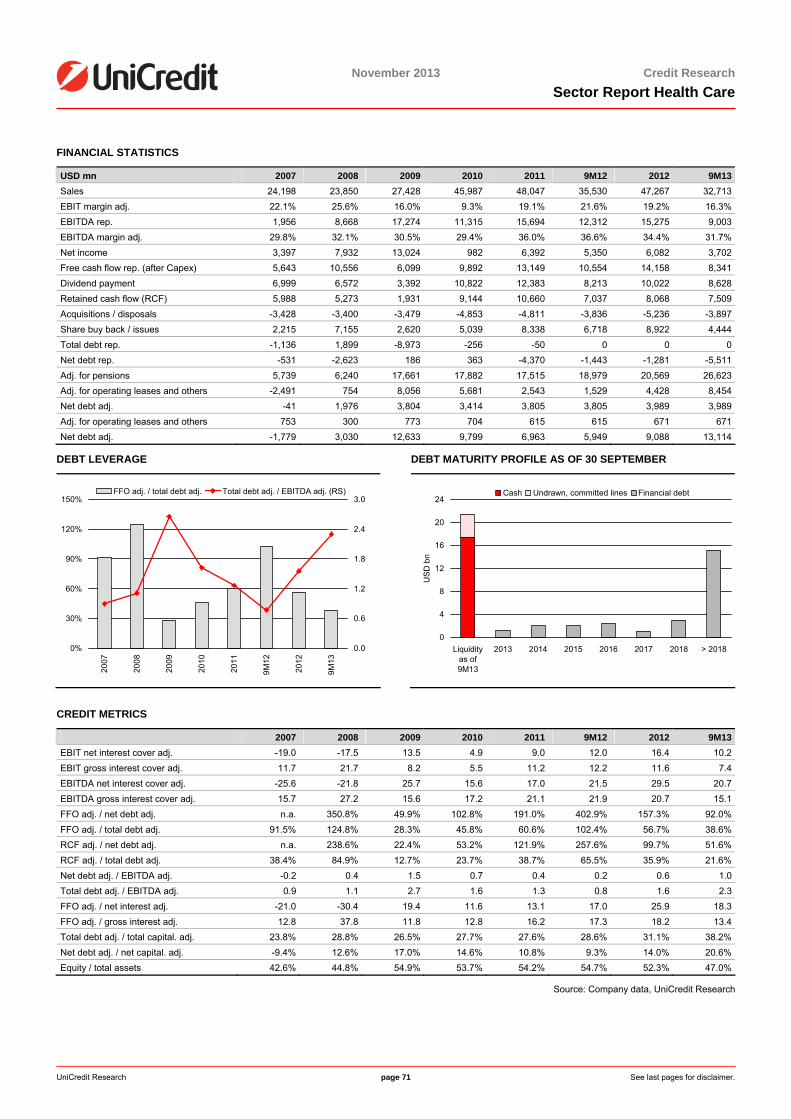

Merck KGaA (A3sAs/--): Marketweight

■ Merck KGaA (Marketweight): The company has a well-diversified portfolio, with pharmaceuticals, consumer health and specialty chemicals (liquid crystals, pigments).

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 13 See last pages for disclaimer.

Due to the focus on biological drugs, the negative impact of generics is limited. Thepipeline saw several setbacks and the potential of the late-stage pipeline is limited. Credit metrics improved after the Millipore acquisition and the company showed animpressive track record in deleveraging. Since its last capital markets day in May 2012,Merck KGaA has focused on cost savings and also indicated potential acquisitions thatmatch its portfolio for 2014. In our view, Merck KGaA has headroom to spend more than EUR 10bn on M&A, while keeping total leverage below 3x (company definition), with US acquisitions for its drug unit being the most likely scenario. The improvement in credit metrics and the risk of potential M&A is discounted in current spread levels.

Novartis (Aa3s/AA-s/AAs): Marketweight

■ Novartis (Marketweight): Novartis remains one of the more stable names in our Pharma coverage. The company has a highly diversified business model with criticalmass in the business segments. Despite the patent expiry of Diovan (hypertension, 15% of sales), Novartis will be able to compensate the loss of sales due to its new drugpipeline (16 drugs in the late-stage pipeline). Novartis is well positioned in its generic business, Sandoz, due to the ability to produce biosimilars, which are difficult to copy. The recently announced disposal of the blood transfusion diagnostics business, which ispart of the Vaccines and Diagnostics division, to Grifols, is credit positive. The company again increased its outlook for 2013 to reflect the lower impact from generic competition but all positive newsflow is already reflected in the tight spread levels.

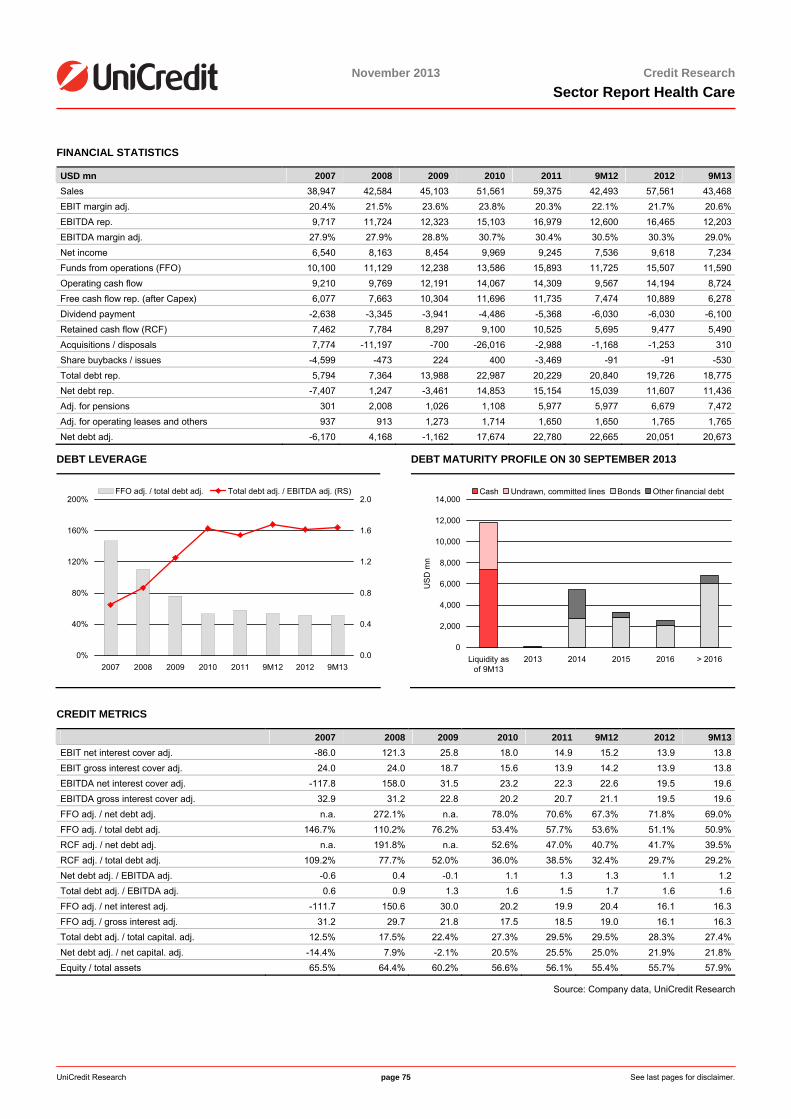

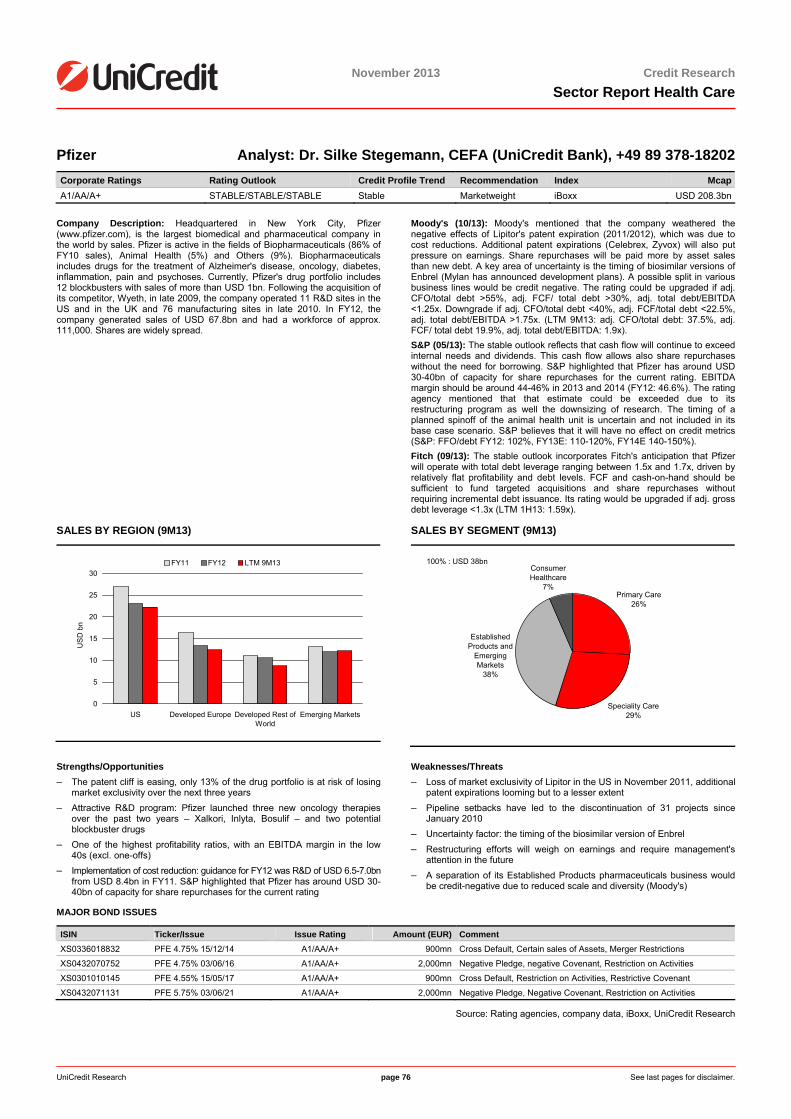

Pfizer (A1s/AAs/A+s): Marketweight

■ Pfizer (Marketweight): The company has weathered the worst effects of the 2011-2012 Lipitor patent expiration, reducing the impact with significant cost reductions. Goingforward, additional patent expirations will impact earnings but to a lesser extent. Pfizer'shigh share repurchase was mostly funded with asset sales rather than new debt. In2012, the company sold its Nutrition business and performed a partial IPO of its AnimalHealth business. A key area of uncertainty is the timing of biosimilar versions of Enbrelin its drug portfolio, thus upside spread upside potential is limited, in our view.

Roche (A1s/AAs/AAs): Marketweight

■ Roche (Marketweight): Roche is among those pharmaceutical companies that are theleast exposed to patent expiration in the next three years. The company increased itspresence in the biotech industry through Genentech in 2009, which was a good strategic step due to further protection beyond patent expiration dates. Overall, Roche has an attractive late-stage pipeline and eight blockbusters in its current portfolio. We keep our marketweight recommendation in light of the relatively tight spread levels.

Sanofi (A1s/AAs/AA-s): Marketweight

■ Sanofi (Marketweight): Sanofi benefits from its business diversification strategy ingrowth areas and from its improved late-stage pipeline. The growth platform comprises Emerging Markets, Diabetes Solutions, Vaccines, Consumer Health, Innovative Products and Biotech and generated 75% of group sales in 3Q13 and 5.5% growth yoy. Sanofi's three best-selling drugs – Lantus, Plavix and Lovenox – accounted for only around 30% of total sales. With its six therapeutic areas, Sanofi has five blockbusters in its portfolio and 10 new molecular entities in its late-stage pipeline (+2 drugs in theregistration phase), which is more or less average in comparison to its peers. Wehighlight that Sanofi has a conservative financial policy with a payout of EUR 3-3.6bn, and focuses less on share buybacks. Nevertheless, there are rumors about buying back the L'Oreal stake (Bloomberg). In this context, please note that the takeover ofGenzyme in 2011 was also financed with scrip dividend funding. We anticipate stable credit metrics for 2014. The weak 3Q13 results are already reflected in the currentspread levels.

Teva (A3n/A-s/A-s): Overweight

■ Teva (Overweight): Teva offers value versus other A-rated companies such as Pfizer and Bristol Myers due to its leading market position in generics. The record number ofpatent expirations in 2012-2014 will expand the range of generic drugs available.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 14 See last pages for disclaimer.

The focus on high-value products and a better cost structure should offset the potential decline in earnings due to the loss of exclusivity of the multiple sclerosis blockbusterCopaxone (in 2014). In addition, the company will make continued progress in its biosimilars and biotechnology strategy. Teva recently announced an acceleration of its program of USD 2bn in annual cost savings by the end of 2017, compared to theprevious range of USD 1.5-2.0bn. We anticipate an improvement in the credit profile, which is not reflected in the current spread levels.

RECOMMENDATION OVERVIEW OTHERS/ HIGH YIELD AND RISK PROFILE

Company Rating (Moody's/ S&P/Fitch)

Recommen- dation

Credit profile trend

Portfolio-risk (1)

Pipelinerisk (2)

M&A risk (3)

Financial policy (4) Comment

Amplifon not rated Buy Improving x - x x (1) Worldwide leader and only global player in the distribution, application and customization of hearing solutions(2) Growth and defense strategy (3) Improved regional diversification; in 2011, it acquired Australian NHC (4) Good financial flexibility, significant loan covenant headroom, improving credit metrics in 2014

Celesio not rated Hold Improving x - x xx (1) Well positioned in wholesale, pharmacies; the intended takeover by McKesson will increase purchasing power (3) Short-term limited M&A (4) Deleveraging target, profit warning and guidance cut

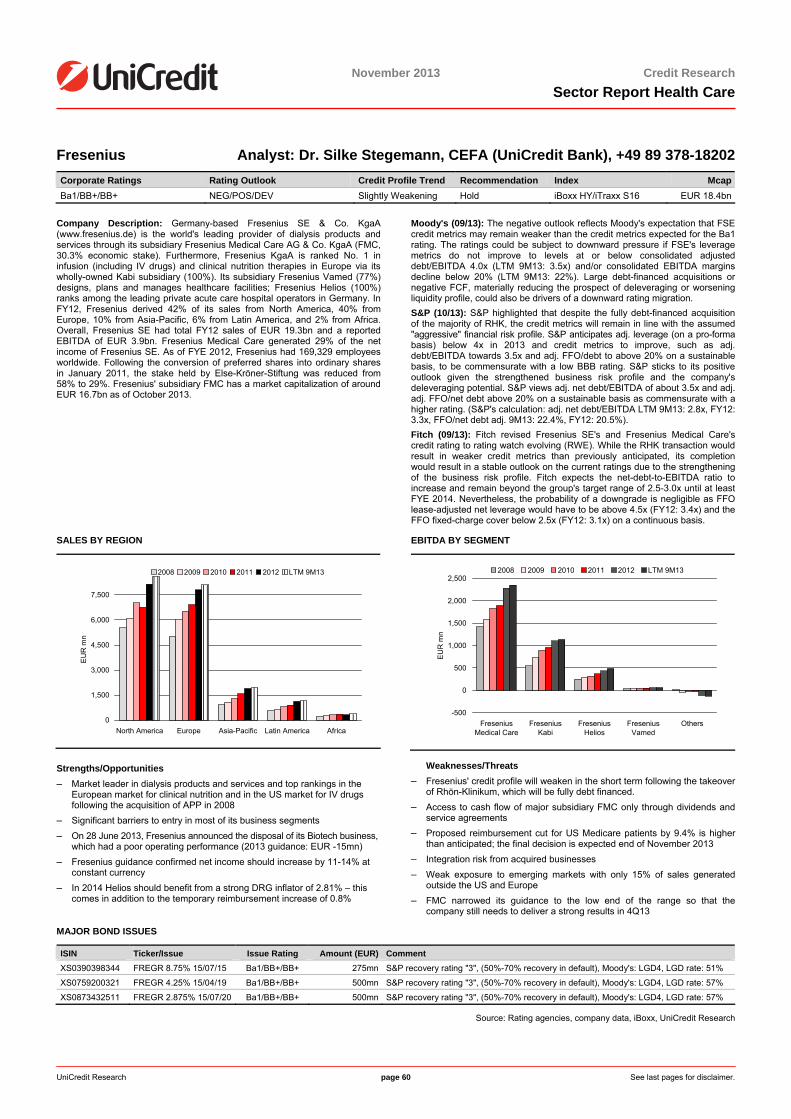

Fresenius Ba1n/BB+p/BB+DEV Hold Slightly weakening

x x x x (1) Attractive portfolio in 4 business units (2) Strong pipeline in APP (injectable generic drugs, part of business unit Kabi)(3) M&A risk low in the short term following the acquisition of RHK (4) Solid financial policy, improvement in credit metrics, quick deleveraging after RHK deal anticipated

Phoenix Phamahandel

-- /BBs/BBs Hold Stable xx - x x (1) Well positioned in the tough pharmaceutical wholesale market (3) Limited M&A (4) Deleveraging

Rhön-Klinikum

Baa3n/- / - / Sell Weakening xx x xx (1) Weak portfolio after asset deal with Fresenius (2) No acquisition in the short term (3) Current weak credit metrics will improve after takeover of the majority of its hospitals by Fresenius (Helios)

Caption: xxx – high risk, xx – moderate risk, x – low risk Source: Company data, UniCredit Research

Amplifon (not rated): Buy

■ Amplifon (Buy): Amplifon is the world leader in the distribution, application andcustomization of hearing solutions with a market share of 9% in the global market and a 14%share in the markets it operates in. Since 2011, Amplifon has improved its regionaldiversification with the full consolidation of acquired Australian NHC (National Hearing Care), posted an EBITDA margin of around 30% in the Asia Pacific segment, and significantlyimproved margins in the North American segment. The company has good financial flexibilitywith significant loan covenant headroom and high operating leverage with 60% of fixed opex. For 2014, we anticipate a better volume trend despite remaining pricing pressure. On aregional basis, this means a recovery in Europe and good sales momentum in the US andAPAC. We also expect a slight improvement in the Netherlands, which suffered in 2013 due to regulatory changes. Restructuring expenses burdened the 2013 result; Amplifon indicatedcost savings of EUR 5mn for 2014. Overall, we expect a slight decline in credit metrics in2013 and a recovery in 2014. For 2013 and 2014 we calculate net debt/EBITDA (adj). of 3.6x and 2.9x (FY12: 3.5x), respectively, and FFO/net debt (adj.) of 22.9% and 32.7% (FY12:27.2%), respectively.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 15 See last pages for disclaimer.

Celesio (not rated):

Hold

■ Celesio (Hold): Ongoing strong competition in the German wholesale market, austerity measures in many European countries and a negative currency impact weighed on operatingresults. On 24 October 2013, McKesson announced its intention to acquire a 50.01% stake inCelesio held by Franz Haniel & Cie GmbH and made a tender offer to buy the remaining publicly-listed shares and the two convertible bonds. In our view, Celesio, which is not rated, would benefit from the stronger business and financial profile and the IG rating of McKesson.The change-of-control clause of the CLSGR 10/16 and CLSGR 4/17 includes the following (summarized) conditions 1. takeover of > 50%; 2. still no rating for Celesio; 3. opportunity of repayment of the bond (at fixed nominal value), which does not seem attractive forbondholders at current levels. We confirm our hold recommendation on the CLSGR bonds, as spread levels more or less discount a successful takeover of Celesio by McKesson.

Fresenius (Ba1n/BB+p/BB+DEV): Hold

■ Fresenius (Hold) The company has a leading market position in all segments, a high-marginbusiness, a good track record of its latest acquisitions and showed successful portfoliooptimization (the Biotech unit was sold). The main risk for the credit involves potentiallylarge M&A deals, as demonstrated recently by the acquisition of the majority of Rhön Klinikum's (RHK) hospitals for EUR 3.1bn. However, we do not anticipate further big transforming deals in the short term. Fresenius indicated that the asset deal with Rhön-Klinikum will be entirely debt-financed and that it will not assume any of RHK's financial debt (UniCredit estimate: EUR 800mn). On a pro-forma basis, the transaction will be in line with Fresenius's net debt/EBITDA target of 2.5-3.0x (comp. def.) in FY14E; this means that leverage is expected to exceed temporarily 3.0x in FY13E, but will remain below 3.5x. An upgrade by the rating agencies to investment grade, which would be amajor spread driver, seems unlikely in the short term.

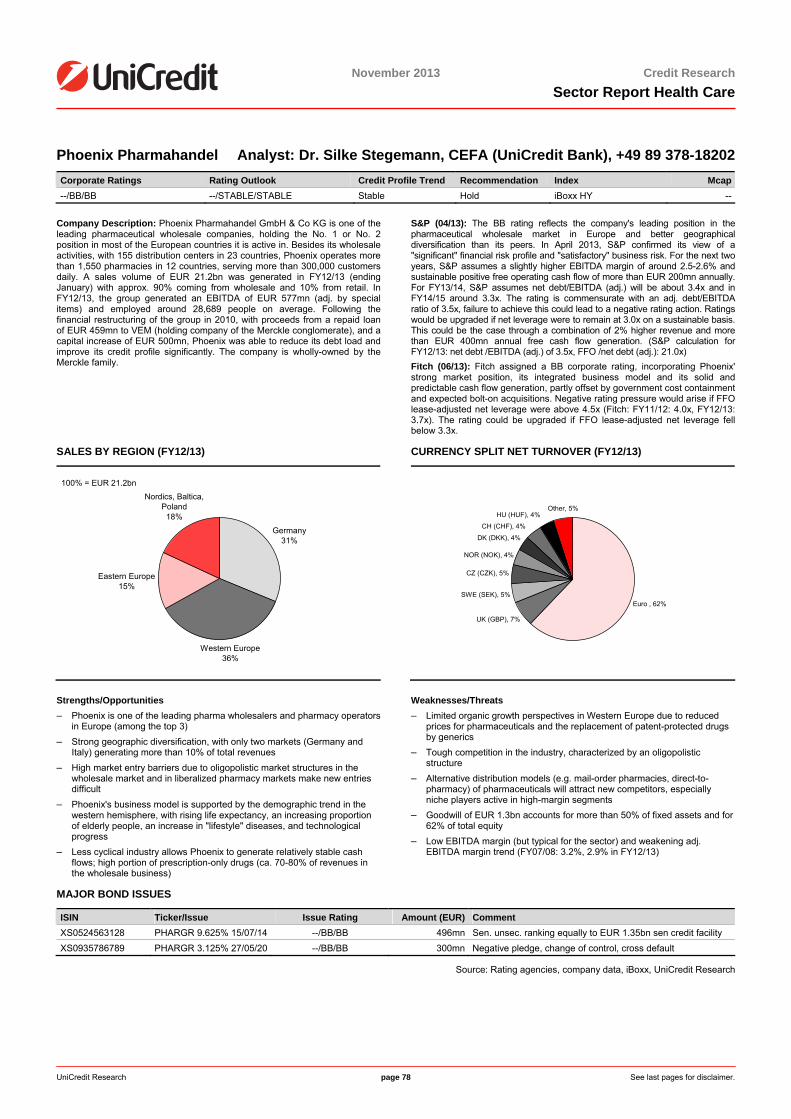

Phoenix Pharmahandel (-/BBs/BBs): Hold

■ Phoenix Pharmahandel (Hold): We confirm our hold recommendation on PHARGR issues, despite the challenging situation in the European pharmaceutical markets, givenmanagement's commitment to deleveraging, its conservative financial policy and tight M&A budget. Nevertheless, the wording of the guidance regarding EBITDA in FY13/14 seems more conservative. The company now anticipates a decline in EBITDA, which can only partly be "balanced" by a significant improvement in the financial result.Phoenix aims to compensate some of the negative market impacts by implementing internal measures based on its "PHOENIX FORWARD" program. The target is to reduce costs and increase efficiency. The positive effects from this program will mostlikely arise from fiscal year FY14/15 onwards and should result in EUR 100mn in potential savings in FY15/16. It is credit positive that management underlined that net debt is likely to further decrease due to continued cash generation and that it maintainsits general financial target of net debt to adj. EBITDA (comp. def) of around 3.0x.

Rhön-Klinikum (Baa3n/--/--): Underweight

■ Rhön-Klinikum (Underweight): The proposed transaction of Fresenius taking over 43 hospitals (65% of RHK sales) will significantly reduce RHK's size, making it more of a regional player, which would be credit negative. The operating performance remains subject to the ongoing restructuring of its largest remaining hospital, the University Hospital of Giessen and Marburg, which accounts for more than 50% of post-disposal sales. Moody's already indicated that the business profile of RHK would appear as having non-investment grade characteristics after the disposal.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 16 See last pages for disclaimer.

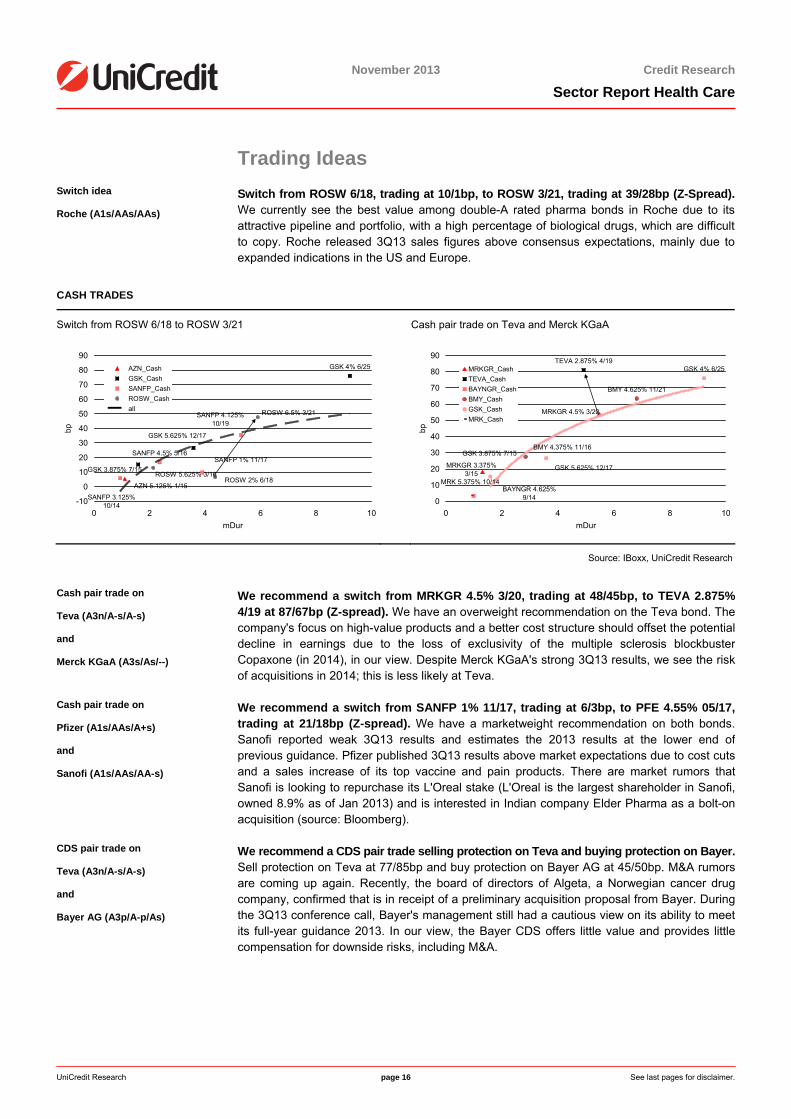

Trading Ideas Switch idea Roche (A1s/AAs/AAs)

Switch from ROSW 6/18, trading at 10/1bp, to ROSW 3/21, trading at 39/28bp (Z-Spread).We currently see the best value among double-A rated pharma bonds in Roche due to its attractive pipeline and portfolio, with a high percentage of biological drugs, which are difficultto copy. Roche released 3Q13 sales figures above consensus expectations, mainly due toexpanded indications in the US and Europe.

CASH TRADES

Switch from ROSW 6/18 to ROSW 3/21 Cash pair trade on Teva and Merck KGaA

AZN 5.125% 1/15

GSK 4% 6/25

GSK 5.625% 12/17

GSK 3.875% 7/15SANFP 1% 11/17

SANFP 4.125% 10/19

SANFP 4.5% 5/16

SANFP 3.125% 10/14

ROSW 6.5% 3/21

ROSW 2% 6/18ROSW 5.625% 3/16

-10

0

10

20

30

40

50

60

70

80

90

0 2 4 6 8 10mDur

bp

AZN_CashGSK_CashSANFP_CashROSW_Cashall

MRKGR 4.5% 3/20

MRKGR 3.375% 3/15

TEVA 2.875% 4/19

BAYNGR 4.625% 9/14

BMY 4.625% 11/21

BMY 4.375% 11/16

GSK 4% 6/25

GSK 5.625% 12/17

GSK 3.875% 7/15

MRK 5.375% 10/14

0

10

20

30

40

50

60

70

80

90

0 2 4 6 8 10mDur

bp

MRKGR_CashTEVA_CashBAYNGR_CashBMY_CashGSK_CashMRK_Cash

Source: IBoxx, UniCredit Research

Cash pair trade on Teva (A3n/A-s/A-s) and Merck KGaA (A3s/As/--)

We recommend a switch from MRKGR 4.5% 3/20, trading at 48/45bp, to TEVA 2.875% 4/19 at 87/67bp (Z-spread). We have an overweight recommendation on the Teva bond. Thecompany's focus on high-value products and a better cost structure should offset the potentialdecline in earnings due to the loss of exclusivity of the multiple sclerosis blockbusterCopaxone (in 2014), in our view. Despite Merck KGaA's strong 3Q13 results, we see the risk of acquisitions in 2014; this is less likely at Teva.

Cash pair trade on Pfizer (A1s/AAs/A+s) and Sanofi (A1s/AAs/AA-s)

We recommend a switch from SANFP 1% 11/17, trading at 6/3bp, to PFE 4.55% 05/17,trading at 21/18bp (Z-spread). We have a marketweight recommendation on both bonds. Sanofi reported weak 3Q13 results and estimates the 2013 results at the lower end of previous guidance. Pfizer published 3Q13 results above market expectations due to cost cutsand a sales increase of its top vaccine and pain products. There are market rumors thatSanofi is looking to repurchase its L'Oreal stake (L'Oreal is the largest shareholder in Sanofi, owned 8.9% as of Jan 2013) and is interested in Indian company Elder Pharma as a bolt-on acquisition (source: Bloomberg).

CDS pair trade on Teva (A3n/A-s/A-s) and Bayer AG (A3p/A-p/As)

We recommend a CDS pair trade selling protection on Teva and buying protection on Bayer.Sell protection on Teva at 77/85bp and buy protection on Bayer AG at 45/50bp. M&A rumors are coming up again. Recently, the board of directors of Algeta, a Norwegian cancer drug company, confirmed that is in receipt of a preliminary acquisition proposal from Bayer. During the 3Q13 conference call, Bayer's management still had a cautious view on its ability to meet its full-year guidance 2013. In our view, the Bayer CDS offers little value and provides little compensation for downside risks, including M&A.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 17 See last pages for disclaimer.

CASH TRADES AND PAIR TRADES

Switch from SANFP 11/17 to PFE 05/17 5Y CDS Teva vs. 5Y CDS Bayer

PFE 5.75% 6/21

PFE 4.55% 5/17

PFE 4.75% 6/16

PFE 4.75% 12/14

SANFP 1% 11/17

SANFP 4.125% 10/19

SANFP 4.5% 5/16

SANFP 3.125% 10/14

0

10

20

30

40

50

60

0 1 2 3 4 5 6 7mDur

bp

PFE_CashSANFP_Cash

40

50

60

70

80

90

Nov-12 Feb-13 May-13 Aug-13 Nov-13

bp

TEVA CDS USD SEN 5Y BAYNGR CDS EUR SEN 5Y

Source: Iboxx, UniCredit Research

Cash pair trade on Fresenius (Ba1n/BB+p/BB+DEV) and Fresenius Medical Care (Ba1s/BB+s/BB+DEV)

On the Fresenius and the Fresenius Medical Care cash curve, we prefer higher-yielding FMEGR bonds and especially the FMEGR 5.25% 2/21 bond. We recommend a switch from FREGR 2.875% 7/20 (Ba1/BB+/BB+), trading at 144/136bp, to FMEGR 5.25% 2/21 (Ba2/BB+/--), trading at 214/203bp. We see upside potential for FMC bonds after the final rulefor Medicare dialysis patients in the US was published on 22 November. The CMS (Centers for Medicare & Medicaid Services) is keeping payments unchanged for 2014, scrapping theproposed 9.4% reduction in Medicare payments to dialysis providers, which is credit positivefor Fresenius. The agency added that reductions remain a possibility over the following threeto four years.

HY CASH TRADES AND SPREAD DEVELOPMENT: FRESENIUS AND FRESENIUS MEDICAL CARE

Spread ´Development FREGR and FMEGR Cash pair trade on FREGR 7/20 and FMEGR 2/21

50

100

150

200

250

Nov-12 Feb-13 May-13 Aug-13 Nov-13

bp

FREGR 8.75% 7/15 FREGR 4.25% 4/19 FREGR 2.875% 7/20FMEGR 5.5% 7/16 FMEGR 6.5% 9/18 FMEGR 5.25% 7/19FMEGR 5.25% 2/21

FMEGR 2/21

FREGR 7/20

FREGR 2.875% 7/20

FREGR 4.25% 4/19

FREGR 8.75% 7/15

FMEGR 5.25% 2/21

FMEGR 5.25% 7/19FMEGR 6.5% 9/18

FMEGR 5.5% 7/16

50

70

90

110

130

150

170

190

210

0 1 2 3 4 5 6 7mDur

bp

FREGR FMEGR

Source: iBoxx, UniCredit Research

Cash pair trade Amplifon (not rated); Buy versus Phoenix Pharmahandel (-/BBs/BBs), Hold

We recommend a switch from PHARGR 05/20 (-/BBs/BBs) to AMPIM 7/18 (not rated). The names are active in the retail (Amplifon, Phoenix Pharmahandel) and wholesale business(Phoenix Pharmahandel) and are struggling in a challenging environment, as reflected in their weak 3Q13 results. Given McKesson's (Baa2wn/A-wn/A-wn) intention to acquire Phoenix competitor Celesio, competition in the German wholesale market will increase and Celesioitself will benefit due to expected synergies and higher purchasing volumes in the future.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 18 See last pages for disclaimer.

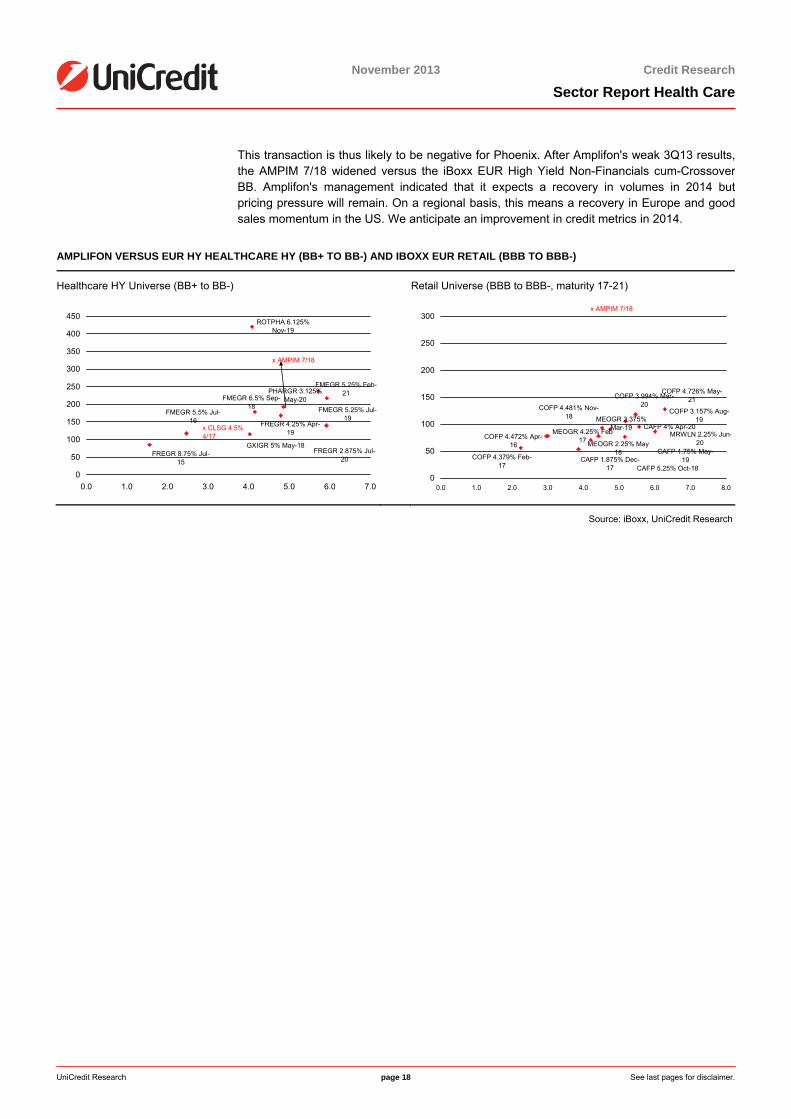

This transaction is thus likely to be negative for Phoenix. After Amplifon's weak 3Q13 results, the AMPIM 7/18 widened versus the iBoxx EUR High Yield Non-Financials cum-Crossover BB. Amplifon's management indicated that it expects a recovery in volumes in 2014 but pricing pressure will remain. On a regional basis, this means a recovery in Europe and good sales momentum in the US. We anticipate an improvement in credit metrics in 2014.

AMPLIFON VERSUS EUR HY HEALTHCARE HY (BB+ TO BB-) AND IBOXX EUR RETAIL (BBB TO BBB-)

Healthcare HY Universe (BB+ to BB-) Retail Universe (BBB to BBB-, maturity 17-21)

ROTPHA 6.125% Nov-19

PHARGR 3.125% May-20

GXIGR 5% May-18FREGR 8.75% Jul-

15

FREGR 4.25% Apr-19

FREGR 2.875% Jul-20

FMEGR 5.5% Jul-16

FMEGR 6.5% Sep-18 FMEGR 5.25% Jul-

19

FMEGR 5.25% Feb-21

0

50

100

150

200

250

300

350

400

450

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0

x CLSG 4.5% 4/17

x AMPIM 7/18

MRWLN 2.25% Jun-20

MEOGR 4.25% Feb-17 MEOGR 2.25% May-

18

MEOGR 3.375% Mar-19

COFP 4.472% Apr-16

COFP 4.379% Feb-17

COFP 4.481% Nov-18

COFP 3.157% Aug-19

COFP 3.994% Mar-20

COFP 4.726% May-21

CAFP 1.875% Dec-17 CAFP 5.25% Oct-18

CAFP 1.75% May-19

CAFP 4% Apr-20

0

50

100

150

200

250

300

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0

x AMPIM 7/18

Source: iBoxx, UniCredit Research

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 19 See last pages for disclaimer.

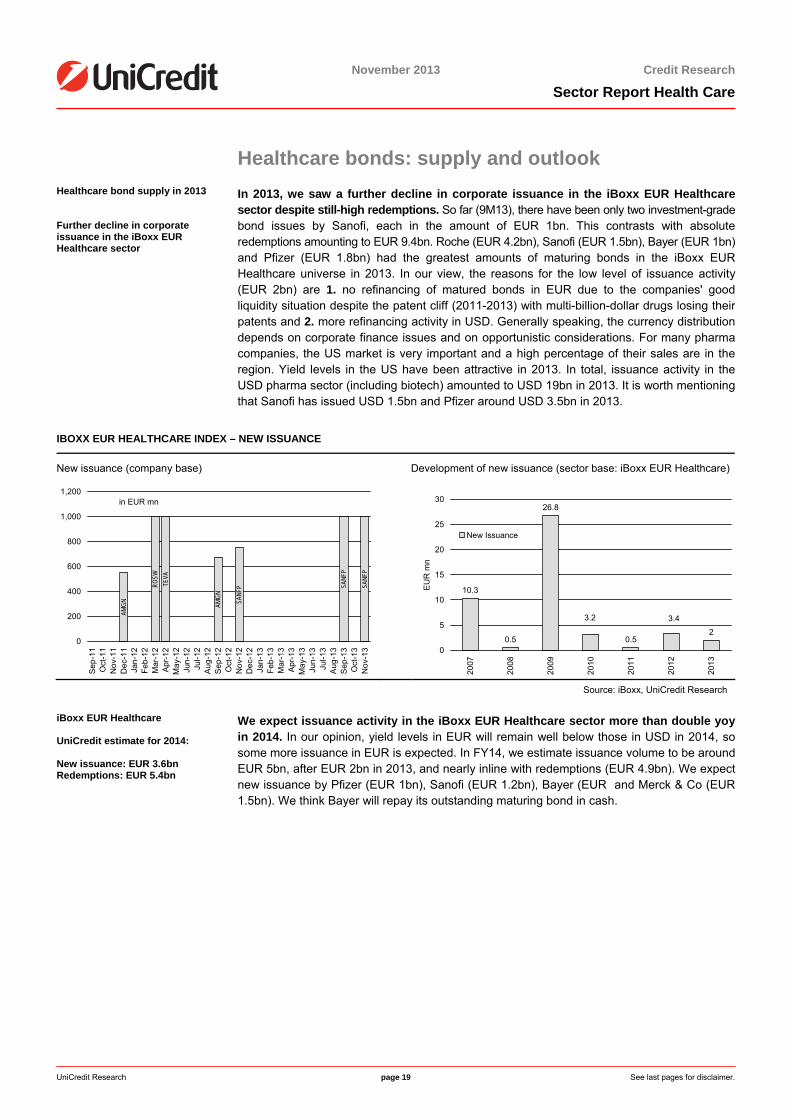

Healthcare bonds: supply and outlook Healthcare bond supply in 2013 Further decline in corporate issuance in the iBoxx EUR Healthcare sector

In 2013, we saw a further decline in corporate issuance in the iBoxx EUR Healthcaresector despite still-high redemptions. So far (9M13), there have been only two investment-gradebond issues by Sanofi, each in the amount of EUR 1bn. This contrasts with absoluteredemptions amounting to EUR 9.4bn. Roche (EUR 4.2bn), Sanofi (EUR 1.5bn), Bayer (EUR 1bn) and Pfizer (EUR 1.8bn) had the greatest amounts of maturing bonds in the iBoxx EURHealthcare universe in 2013. In our view, the reasons for the low level of issuance activity(EUR 2bn) are 1. no refinancing of matured bonds in EUR due to the companies' goodliquidity situation despite the patent cliff (2011-2013) with multi-billion-dollar drugs losing their patents and 2. more refinancing activity in USD. Generally speaking, the currency distribution depends on corporate finance issues and on opportunistic considerations. For many pharmacompanies, the US market is very important and a high percentage of their sales are in theregion. Yield levels in the US have been attractive in 2013. In total, issuance activity in the USD pharma sector (including biotech) amounted to USD 19bn in 2013. It is worth mentioning that Sanofi has issued USD 1.5bn and Pfizer around USD 3.5bn in 2013.

IBOXX EUR HEALTHCARE INDEX – NEW ISSUANCE

New issuance (company base) Development of new issuance (sector base: iBoxx EUR Healthcare)

ROSW

SANF

P

SANF

P

SANF

P

AMGN

AMGN

TEVA

0

200

400

600

800

1,000

1,200

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12Fe

b-12

Mar

-12

Apr

-12

May

-12

Jun-

12Ju

l-12

Aug

-12

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13Fe

b-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

in EUR mn

10.3

0.5 0.52

3.2 3.4

26.8

0

5

10

15

20

25

30

2007

2008

2009

2010

2011

2012

2013

EU

R m

n

New Issuance

Source: iBoxx, UniCredit Research

iBoxx EUR Healthcare UniCredit estimate for 2014: New issuance: EUR 3.6bn Redemptions: EUR 5.4bn

We expect issuance activity in the iBoxx EUR Healthcare sector more than double yoy in 2014. In our opinion, yield levels in EUR will remain well below those in USD in 2014, so some more issuance in EUR is expected. In FY14, we estimate issuance volume to be aroundEUR 5bn, after EUR 2bn in 2013, and nearly inline with redemptions (EUR 4.9bn). We expectnew issuance by Pfizer (EUR 1bn), Sanofi (EUR 1.2bn), Bayer (EUR and Merck & Co (EUR 1.5bn). We think Bayer will repay its outstanding maturing bond in cash.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 20 See last pages for disclaimer.

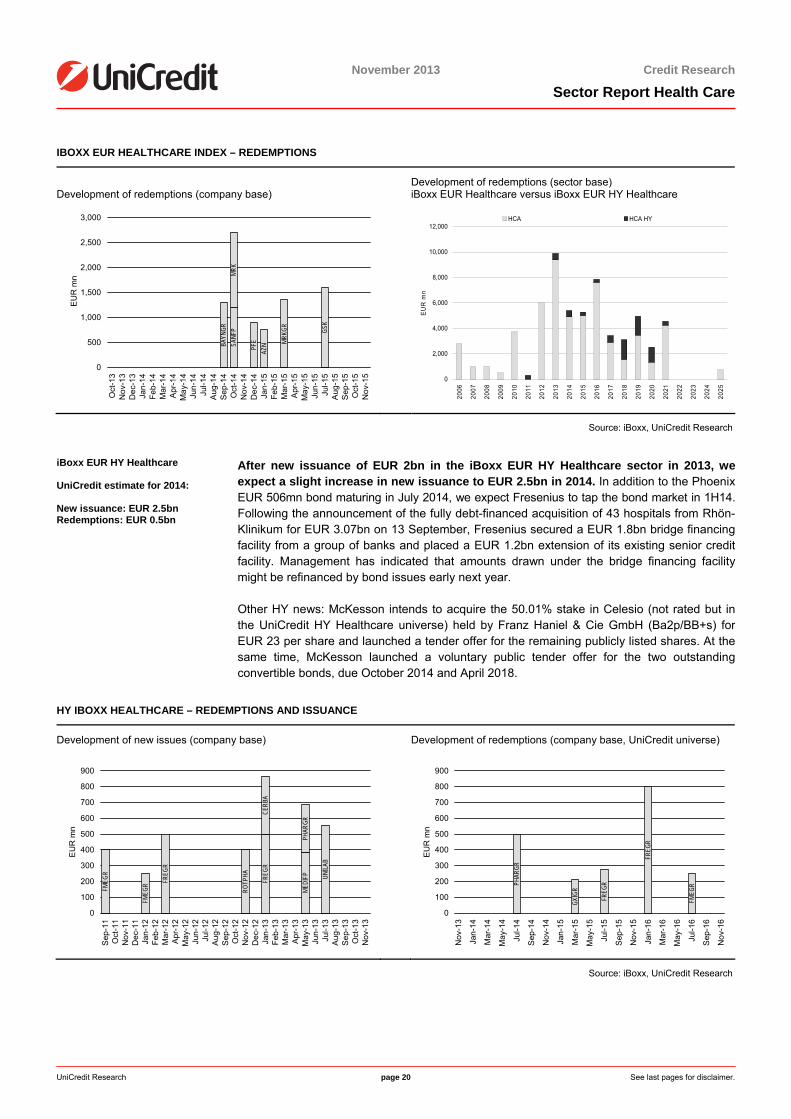

IBOXX EUR HEALTHCARE INDEX – REDEMPTIONS

Development of redemptions (company base)

Development of redemptions (sector base) iBoxx EUR Healthcare versus iBoxx EUR HY Healthcare

PFESA

NFP GS

K

MRKG

R

BAYN

GR

AZN

MRK

0

500

1,000

1,500

2,000

2,500

3,000

Oct

-13

Nov

-13

Dec

-13

Jan-

14Fe

b-14

Mar

-14

Apr

-14

May

-14

Jun-

14Ju

l-14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15Fe

b-15

Mar

-15

Apr

-15

May

-15

Jun-

15Ju

l-15

Aug

-15

Sep

-15

Oct

-15

Nov

-15

EU

R m

n

0

2,000

4,000

6,000

8,000

10,000

12,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

EU

R m

n

HCA HCA HY

Source: iBoxx, UniCredit Research

iBoxx EUR HY Healthcare UniCredit estimate for 2014: New issuance: EUR 2.5bn Redemptions: EUR 0.5bn

After new issuance of EUR 2bn in the iBoxx EUR HY Healthcare sector in 2013, we expect a slight increase in new issuance to EUR 2.5bn in 2014. In addition to the Phoenix EUR 506mn bond maturing in July 2014, we expect Fresenius to tap the bond market in 1H14. Following the announcement of the fully debt-financed acquisition of 43 hospitals from Rhön-Klinikum for EUR 3.07bn on 13 September, Fresenius secured a EUR 1.8bn bridge financing facility from a group of banks and placed a EUR 1.2bn extension of its existing senior creditfacility. Management has indicated that amounts drawn under the bridge financing facility might be refinanced by bond issues early next year.

Other HY news: McKesson intends to acquire the 50.01% stake in Celesio (not rated but inthe UniCredit HY Healthcare universe) held by Franz Haniel & Cie GmbH (Ba2p/BB+s) for EUR 23 per share and launched a tender offer for the remaining publicly listed shares. At thesame time, McKesson launched a voluntary public tender offer for the two outstandingconvertible bonds, due October 2014 and April 2018.

HY IBOXX HEALTHCARE – REDEMPTIONS AND ISSUANCE

Development of new issues (company base) Development of redemptions (company base, UniCredit universe)

FREG

R

FREG

R

FMEG

RFMEG

R UNILA

B

ROTP

HA

MEDI

FP

CERB

A

PHAR

GR

0

100

200

300

400

500

600

700

800

900

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12Fe

b-12

Mar

-12

Apr

-12

May

-12

Jun-

12Ju

l-12

Aug

-12

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13Fe

b-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

EU

R m

n

FREG

R

FREG

R

FMEG

RPHAR

GR

GXIG

R

0

100

200

300

400

500

600

700

800

900

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep

-14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep

-15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep

-16

Nov

-16

EU

R m

n

Source: iBoxx, UniCredit Research

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 21 See last pages for disclaimer.

Rating trend Pharma sector still best rated sector in iBoxx bond universe

Rating agencies became more bullish for the global pharma sector and raised the outlook to stable in 2012. Moody's and S&P already changed the outlook for the globalpharmaceutical industry to stable from negative in September and December 2012. The outlooks had been negative since 2007. In September 2013, S&P confirmed the stableoutlook, reflecting its earnings growth expectations for 2014. The rating agency estimatesaggregated EBITDA growth of 3% for 2014 after flat EBITDA in 2013. Improving pipelines, a high number of approvals by the FDA and modest patent expirations through 2014 willimprove credit profiles, the rating agencies added. Lost revenue through patent expiry shouldbe broadly offset by sales of new products. Nevertheless, cuts in government healthcare expenditures, the tendency to substitute branded drugs with generic ones and tougheconomic conditions in Southern Europe and the US are putting pressure on profitability andcash flow. The ability of global pharmaceutical companies to cope with record levels of patent expirations was the key driver for the revision of the sector outlook to stable from negative byFitch (December 2012). In addition, Fitch highlighted that the companies will strengthen theirpresence in emerging markets, where the expanding population and economy mean increased demand, particularly for affordable generic and over-the-counter medicines.

RATING TREND

Stable rating trend since 2011 Pharma sector still best-rated sector in the iBoxx

0

25

50

75

100

125

150

175

200

225

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

AS

W (b

p)

4

5

6

7iBoxx € Health Care Moody's average rating

S&P average rating

BBB+

A-

A

A+

0%

20%

40%

60%

80%

100%

HC

A

THE

CH

E

OIG

ATO

PHG

FOB

UTS IG

S

BAS TE

L

RE

T

TAL

CN

S

MD

I

0

1

2

3

4

5

BBB A AA AAA Weighted average rating

AAA

AA

A

BBB

Source: iBoxx, Moody's, S&P, UniCredit Research

Still best rated sector in iBoxx universe

The pharma sector is still the best-rated sector in the iBoxx bond universe. Within a period of 10 years, the average rating for iBoxx EUR Healthcare was again A+. It is worth mentioning that the lack of many downgrades related to patent expirations in 2012 underlinesthe credit resilience of pharmaceutical companies with low leverage, high margins and largecash cushion.

Best rating drift in iBoxx for Healthcare

In the last twelve months, Healthcare (e.g. Merck KGaA, Bayer, Sanofi) have shown themost positive rating actions due to improvements in individual company risk profiles.The Healthcare sector is the exception concerning positive rating actions; a look at rating statistics shows that the credit quality in the investment grade universe continues todeteriorate in Europe, as highlighted by negative rating migration. Basic Resources (ArcelorMittal becoming sub-investment grade), Telecoms (periphery, competitive andregulatory pressure), and Utilities (partial earnings pressure/power prices, Spanish exposure)are the three sectors featuring the most negative rating drift in the last two years.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 22 See last pages for disclaimer.

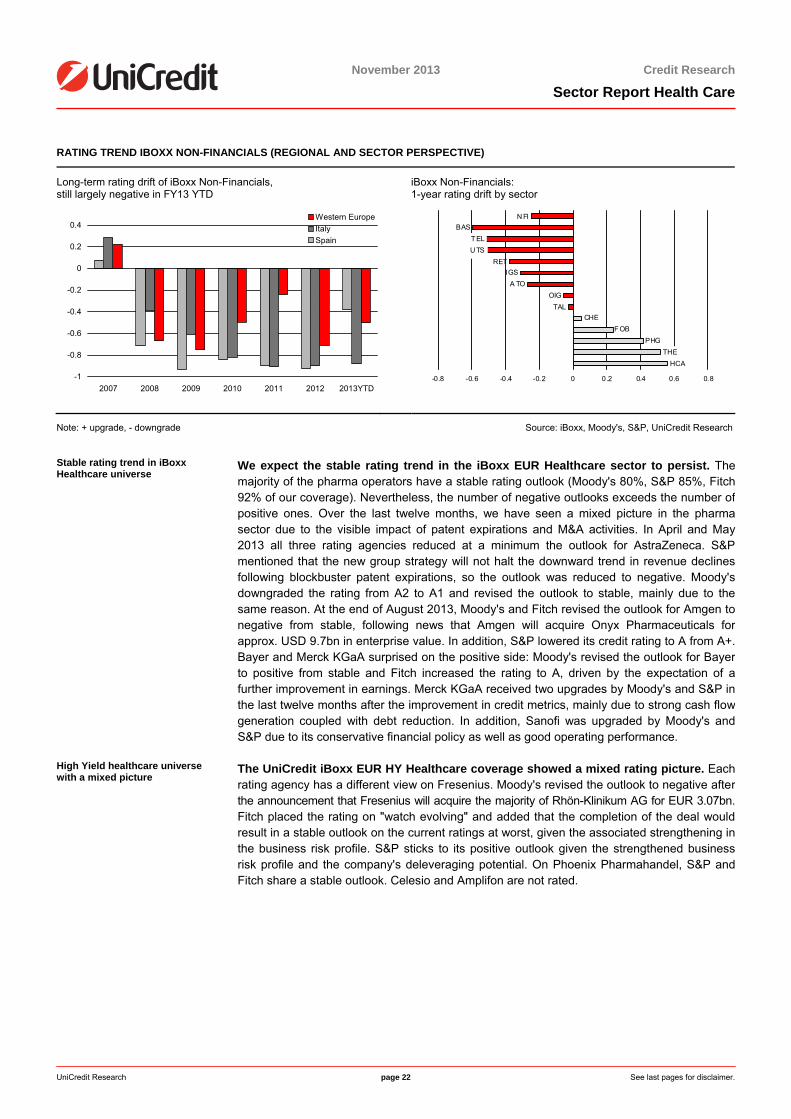

RATING TREND IBOXX NON-FINANCIALS (REGIONAL AND SECTOR PERSPECTIVE)

Long-term rating drift of iBoxx Non-Financials, still largely negative in FY13 YTD

iBoxx Non-Financials: 1-year rating drift by sector

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

2013YTD201220112010200920082007

Western EuropeItalySpain

PHGF OB

CHETAL

OIGA TO

IGSRET

BASN FI

TELU TS

THEHCA

-0.8 -0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8

Note: + upgrade, - downgrade Source: iBoxx, Moody's, S&P, UniCredit Research

Stable rating trend in iBoxx Healthcare universe

We expect the stable rating trend in the iBoxx EUR Healthcare sector to persist. The majority of the pharma operators have a stable rating outlook (Moody's 80%, S&P 85%, Fitch92% of our coverage). Nevertheless, the number of negative outlooks exceeds the number of positive ones. Over the last twelve months, we have seen a mixed picture in the pharmasector due to the visible impact of patent expirations and M&A activities. In April and May2013 all three rating agencies reduced at a minimum the outlook for AstraZeneca. S&P mentioned that the new group strategy will not halt the downward trend in revenue declinesfollowing blockbuster patent expirations, so the outlook was reduced to negative. Moody'sdowngraded the rating from A2 to A1 and revised the outlook to stable, mainly due to the same reason. At the end of August 2013, Moody's and Fitch revised the outlook for Amgen tonegative from stable, following news that Amgen will acquire Onyx Pharmaceuticals forapprox. USD 9.7bn in enterprise value. In addition, S&P lowered its credit rating to A from A+. Bayer and Merck KGaA surprised on the positive side: Moody's revised the outlook for Bayerto positive from stable and Fitch increased the rating to A, driven by the expectation of afurther improvement in earnings. Merck KGaA received two upgrades by Moody's and S&P inthe last twelve months after the improvement in credit metrics, mainly due to strong cash flowgeneration coupled with debt reduction. In addition, Sanofi was upgraded by Moody's andS&P due to its conservative financial policy as well as good operating performance.

High Yield healthcare universe with a mixed picture

The UniCredit iBoxx EUR HY Healthcare coverage showed a mixed rating picture. Each rating agency has a different view on Fresenius. Moody's revised the outlook to negative after the announcement that Fresenius will acquire the majority of Rhön-Klinikum AG for EUR 3.07bn. Fitch placed the rating on "watch evolving" and added that the completion of the deal wouldresult in a stable outlook on the current ratings at worst, given the associated strengthening inthe business risk profile. S&P sticks to its positive outlook given the strengthened businessrisk profile and the company's deleveraging potential. On Phoenix Pharmahandel, S&P and Fitch share a stable outlook. Celesio and Amplifon are not rated.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 23 See last pages for disclaimer.

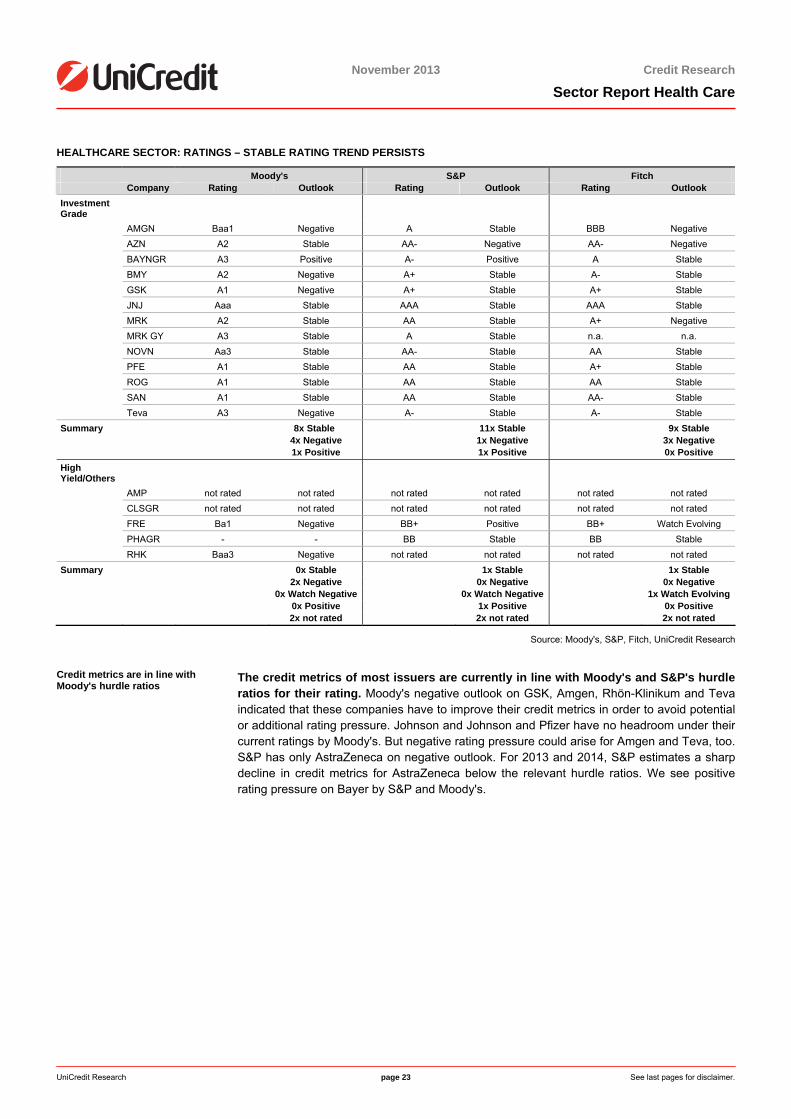

HEALTHCARE SECTOR: RATINGS – STABLE RATING TREND PERSISTS

Moody's S&P Fitch Company Rating Outlook Rating Outlook Rating Outlook Investment Grade

AMGN Baa1 Negative A Stable BBB Negative AZN A2 Stable AA- Negative AA- Negative BAYNGR A3 Positive A- Positive A Stable BMY A2 Negative A+ Stable A- Stable GSK A1 Negative A+ Stable A+ Stable JNJ Aaa Stable AAA Stable AAA Stable MRK A2 Stable AA Stable A+ Negative MRK GY A3 Stable A Stable n.a. n.a. NOVN Aa3 Stable AA- Stable AA Stable PFE A1 Stable AA Stable A+ Stable ROG A1 Stable AA Stable AA Stable SAN A1 Stable AA Stable AA- Stable Teva A3 Negative A- Stable A- Stable Summary 8x Stable 11x Stable 9x Stable 4x Negative 1x Negative 3x Negative 1x Positive 1x Positive 0x Positive High Yield/Others

AMP not rated not rated not rated not rated not rated not rated CLSGR not rated not rated not rated not rated not rated not rated FRE Ba1 Negative BB+ Positive BB+ Watch Evolving PHAGR - - BB Stable BB Stable RHK Baa3 Negative not rated not rated not rated not rated Summary 0x Stable 1x Stable 1x Stable 2x Negative 0x Negative 0x Negative 0x Watch Negative 0x Watch Negative 1x Watch Evolving 0x Positive 1x Positive 0x Positive 2x not rated 2x not rated 2x not rated

Source: Moody's, S&P, Fitch, UniCredit Research

Credit metrics are in line with Moody's hurdle ratios

The credit metrics of most issuers are currently in line with Moody's and S&P's hurdleratios for their rating. Moody's negative outlook on GSK, Amgen, Rhön-Klinikum and Teva indicated that these companies have to improve their credit metrics in order to avoid potentialor additional rating pressure. Johnson and Johnson and Pfizer have no headroom under theircurrent ratings by Moody's. But negative rating pressure could arise for Amgen and Teva, too. S&P has only AstraZeneca on negative outlook. For 2013 and 2014, S&P estimates a sharp decline in credit metrics for AstraZeneca below the relevant hurdle ratios. We see positiverating pressure on Bayer by S&P and Moody's.

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 24 See last pages for disclaimer.

REQUIRED HURDLE RATIOS* BY MOODY'S AND S&P VERSUS RECENT CALCULATED FIGURES

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

AMGN GSK PFE SAN

Adj

. CFO

to d

ebt

2012 9M13 Required CFO/total debt (adj.) ratio by Moody's

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

AMGN AZN TEVA BAYNGR

2012 9M13 Required FFO/net debt (adj.) ratio by S&P

S&P estimate:FY13E: 65%, FY14E: 48%

CFO: Cash Flow from Operations (Moody's calculation) Source: Moody's, S&P, UniCredit Research

PHARMA COMPANIES: MOODY'S CREDIT METRICS AND THRESHOLDS

Moody's hurdle ratios

Company CFO/total

debt (adj.) CFO/total debt (adj.)

FY12 (LTM 9M13) total debt/

EBITDA (adj.)

total debt/EBITDA (adj.)

FY12 (LTM 9M13) rating

pressure comment AMGN >25% 21.9% (19.2%) <3.5x 3.7x (3.7x) High Outlook was revised to negative after Onyx

takeover, potential higher debt AZN >50% 60% (67%) n.a. n.a. Limited The rating was already reduced in April 2013 from

A2 to A1 BAYNGR RCF/net

debt ~ 30% 32.4% (38%) adj. FCF/net

debt > single digits

8.9% (7.5%) High Outlook was changed to positive from stable in April, upgrade if RCF/net debt > high thirties

BMY >40% 42.1% (36.8%) <1.75x 1.6x (2.1x) Limited Moody's does not anticipate an upgrade in the near term which requires total debt/EBITDA (adj.) < 1.25x and CFO/ total debt (adj.) > 55%

GSK >40% 32.7 (32.5%) adj. cash/debt around 30%

by FY14E

20.6% (15.6%) High Revision of the outlook to negative reflects the current weak credit metrics, the disposal of its drink brands Lucozade/Ribena will improve metrics

JNJ >75% 73.9% (79.3%) <1x 0.99x (0.89x) Limited In June, the rating and outlook were confirmed MRK >30% 49.6% (38.2%) <2.5x 1.4 (2.2x) Limited Moody's lowered the rating by one notch to A2

from A1 (May) due to the challenge of patent expiration

MRK GY >45% 46.8% (1H13: 40.8%) n.a. 2.3x (2.0x) Limited In August, Moody's confirmed the rating, which would be upgraded if CFO/total debt (adj.) > 55%

NOVN >50% 53.2% (51.6%) adj. cash/debt >25%

29.1% (27.6%) Limited Short term, Moody's anticipates an increase in credit metrics.

PFE >40% 41.4% (37.5%) < .75x 1.8x (1.9x) High Additional patent expirations will weigh on earnings

ROG >40% 42.5% (1H13: 48.5%) adj. cash/debt around 30%

42% (1H13: 26%) Limited Roche is well positioned in the A1 rating category

SAN > mid of 40% 40.5% (1H13: 29.6%)* adj. cash/debt >20%

27% (1H13: 16.6%)

High In March, Moody's upgraded Sanofi to A1 with stable outlook

Teva n.a. 30.60% (38%) <2.5 2.6x (2.5x) High Negative outlook reflects the risk that leverage must be sustained < 2.5x

High Yield /Others Amplifon not rated not rated not rated not rated not rated Celesio not rated not rated not rated not rated not rated Fresenius n.a. n.a. <4.0x 3.6x (3.5x) Limited Outlook change to negative after the announcement

that it would acquire majority of assets of RHK Phoenix Pharma

not rated not rated not rated not rated not rated

RHK RCF/net debt <20%

19.2% (22.7%) <3.25 3.6x (3.2x) High Disposal of 43 hospitals is credit negative, as it will reduce the size of the remaining RHK group

* 1H13 results Source: Company data, rating agencies, UniCredit Research

<date>

November 2013 Credit Research

Sector Report Health Care

UniCredit Research page 25 See last pages for disclaimer.

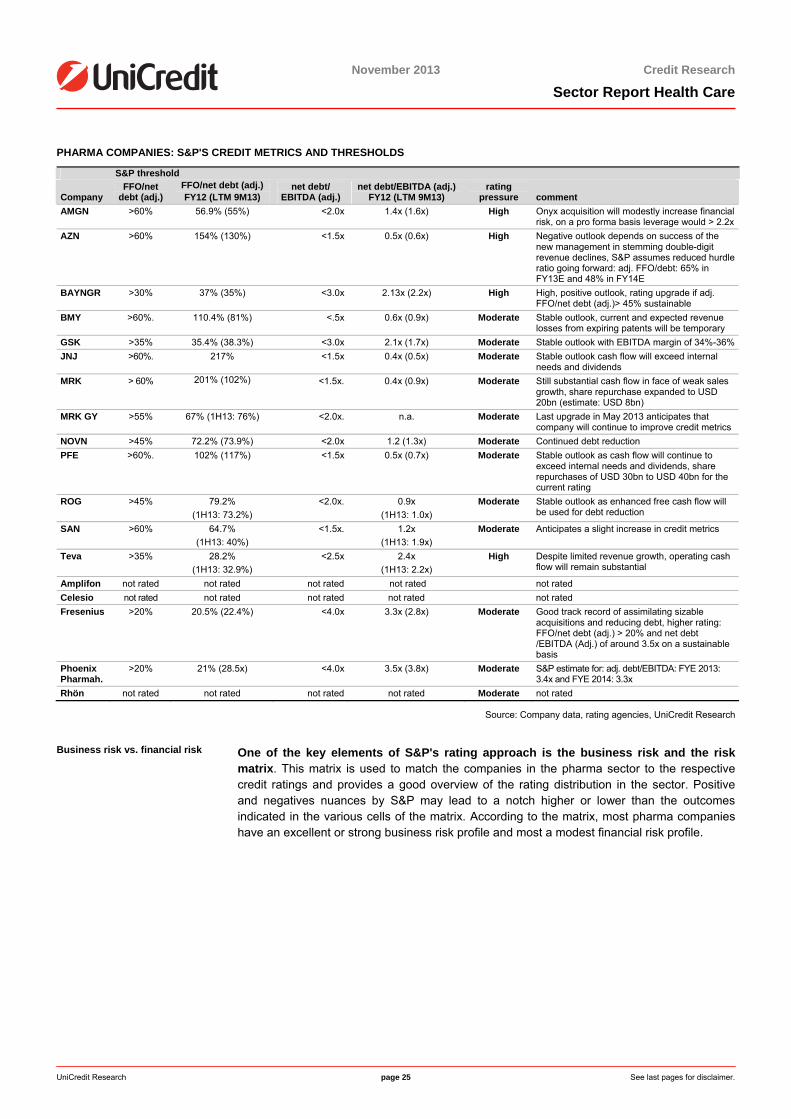

PHARMA COMPANIES: S&P'S CREDIT METRICS AND THRESHOLDS

S&P threshold

Company FFO/net

debt (adj.) FFO/net debt (adj.) FY12 (LTM 9M13)

net debt/ EBITDA (adj.)

net debt/EBITDA (adj.) FY12 (LTM 9M13)

rating pressure comment

AMGN >60% 56.9% (55%) <2.0x 1.4x (1.6x) High Onyx acquisition will modestly increase financial risk, on a pro forma basis leverage would > 2.2x

AZN >60% 154% (130%) <1.5x 0.5x (0.6x) High Negative outlook depends on success of the new management in stemming double-digit revenue declines, S&P assumes reduced hurdle ratio going forward: adj. FFO/debt: 65% in FY13E and 48% in FY14E

BAYNGR >30% 37% (35%) <3.0x 2.13x (2.2x) High High, positive outlook, rating upgrade if adj. FFO/net debt (adj.)> 45% sustainable

BMY >60%. 110.4% (81%) <.5x 0.6x (0.9x) Moderate Stable outlook, current and expected revenue losses from expiring patents will be temporary

GSK >35% 35.4% (38.3%) <3.0x 2.1x (1.7x) Moderate Stable outlook with EBITDA margin of 34%-36%JNJ >60%. 217% <1.5x 0.4x (0.5x) Moderate Stable outlook cash flow will exceed internal

needs and dividends MRK > 60% 201% (102%) <1.5x. 0.4x (0.9x) Moderate Still substantial cash flow in face of weak sales

growth, share repurchase expanded to USD 20bn (estimate: USD 8bn)

MRK GY >55% 67% (1H13: 76%) <2.0x. n.a. Moderate Last upgrade in May 2013 anticipates that company will continue to improve credit metrics

NOVN >45% 72.2% (73.9%) <2.0x 1.2 (1.3x) Moderate Continued debt reduction PFE >60%. 102% (117%) <1.5x 0.5x (0.7x) Moderate Stable outlook as cash flow will continue to

exceed internal needs and dividends, share repurchases of USD 30bn to USD 40bn for the current rating

ROG >45% 79.2% (1H13: 73.2%)

<2.0x. 0.9x (1H13: 1.0x)