Embed Size (px)

Citation preview

SAN JOSE STATE UNIVERSITY

CAMPUS VILLAGE STUDENT/FACULTY APARTMENTS

Final Report

September 6, 2006

CONSTRUCTION PROJECT EVALUATION

SAN JOSE STATE UNIVERSITY

CAMPUS VILLAGE STUDENT/FACULTY APARTMENTS

September 6, 2006

Prepared by:

KPMG LLP 801 Second Avenue, Suite 900

Seattle, WA 98104

This report and all associated analysis contained herein are based upon information made available to KPMG LLP. KPMG LLP is not responsible for incomplete or inaccurate information provided during the preparation of this report. This report only presents and summarizes factual data and does not represent an opinion or attestation to the position, approach or representation of information made by any other party involved with this evaluation.

Page 2 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONTENTS Executive Summary ……………………………..…….…………………………………... 3

Summary of Findings ……………………………………………………………… 3

Introduction ………………………………………...……………………………………… 5 Purpose ……………………………………..……………………………………… 5 Scope ………………………………………..……………………………………... 5 Methodology ..…………….………………….…………………………………….. 6 Exclusions ..………………………………….……………………………………... 6

Project Background …………………………………..………….……………………….... 7

Delivery Methodology ………………………..………………………………….... 7 Timeline ………………………………………..………………………………….. 7 Project Costs ….………………………………….………….…………………...… 8

Design Costs ………………..……………………………..…………………………...….10

Construction Bid Process …………………………..………………………………….…. 16

Construction Change Orders ………………………….…………………………….….... 17

Signature Authority ………………………………………………………………..18 Mark-up ……………………………………………………………………………19 Contractor Direct Costs …………………………………………………………....20 Change Order Report Analysis .…………….…………………………….…….... 22 Contractor Compliance - Subcontractor Practices .……….……......…………..…. 23

Construction Management Services ……………………………………..…….…….….... 24

Major Equipment / Materials Review ……………………………………..……………... 29

Close-Out Process ………………...……………………………………..………….……. 30

Liquidated Damages ………………………………………………………..…….…….... 31

Accounting …………………………………………………………………..…….……... 32

Page 3 of 32 San Jose State University

Campus Village Student/Faculty Apartments

EXECUTIVE SUMMARY Summary of Findings As a result of our evaluation of the CSU San Jose Campus Village Student/Faculty Apartments, we found areas of control or process weaknesses that could expose SJSU to unnecessary risks, if not addressed. As a result of our observations, we have identified the areas of the planning and execution process which should be improved. Our observations, associated risks and recommendations are summarized below. Examples of specific action steps are further detailed in the body of this report.

Observation Risk Recommendation 1. Additional Services

Agreements were not counter signed by the Architect and were executed SJSU letterhead instead of the Standard CSU Extra Services Agreement form.

Lack of consultant counter signatures on Extra Services Agreements may limit the enforceability of the SJSU intended to scope of work. Also, by not utilizing the standard ESA form, SJSU may compromise the intent and legal meaning of the standard ESA language.

SUAM 9210.03 should be modified to require counter signature of the service provider on Extra Service Agreements.

(Ownership: CPDC)

2. Significant work outside of the base agreement was performed and invoiced by the Architect before it was incorporated into an executed Extra Services Agreement.

Work performed without an Executed ESA and a clearly defined scope and contract terms memorialized in an executed ESA signed by the Architect may result in a dispute at a later date.

In the future, SJSU should not allow any consultant to perform and invoice any work without an executed ESA in place.

(Ownership: SJSU)

3. Neither SJSU nor NBA tracked the amounts invoiced against each contractual component separately.

By not tracking the amount charged to each item in the contractual agreement separately, the chances an individual line item would exceed the contractually agreed upon amount increases.

A better practice would be to require consultants to invoice presenting all contracted line items including the contracted amount, the amount previously billed, the current billing, and total invoiced to date for each line item. In addition, SJSU should track the invoices in a similar fashion to verify the accuracy of the billings presented by the consultant.

(Ownership: SJSU) 4. Reconciliation between

the accounting system(s) and invoices did not occur on a comprehensive and regular basis.

Without controls to prevent and detect extra amounts entered into the accounting system, SJSU is at a risk of overpaying its consultants.

Perform periodic reconciliation between the invoiced amounts and amounts paid. SJSU should consider the $6,000 overpayment in its final negotiations with NBA. (Ownership: SJSU)

5. The Architect contract was entered into without evidence of legal review.

Lack of legal review of contracts by counsel may commit SJSU to unfavorable contractual terms which may cause financial loss or other damage at a later date.

Legal review is a key factor in protecting the interests of SJSU. In the future, Spartan Shops should attempt to have design agreements receive documented legal review.

(Ownership: SJSU)

Page 4 of 32 San Jose State University

Campus Village Student/Faculty Apartments

_________________________________________________________________________ EXECUTIVE SUMMARY

Observation Risk Recommendation 6. SJSU did not

consistently obtain appropriate level of signature authority on Change Orders.

Lack of formal authorization by appropriate individuals on Change Orders may cause unnecessary cost and risk exposure to SJSU.

A better practice would require the highest level of signature authority on the face of the change order which is the contractually binding document.

(Ownership: SJSU)

7. On occasion, mark-up was calculated incorrectly on the Change Orders.

SJSU is at a risk of overpayment when mark-up is calculated incorrectly.

Change order proposal summary sheets should be checked for proper mark-up calculation prior to issuing the change order.

(Ownership: SJSU) 8. The Contractor charged

certain direct costs which by industry standards and the General Conditions should have been covered by the Change Order mark-up percentage. In addition, the General Conditions allow for ambiguous interpretation of the definition of mark-up.

SJSU is at a risk of overpayment when items which are not intended or allowed to be charged as a direct cost are permitted in the Change Orders

(a) SJSU should require the Contractor to substantiate its direct costs prior to executing a Change Order. The Contractor should be required to account for any direct costs associated with a change to facilitate an audit.

(Ownership: SJSU)

(b) The General Conditions should be modified to specify mark-up to include anything not expressly stated as an allowable change order cost of work.

(Ownership: CPDC) 9. Several agreements

were entered into without evidence of CSU legal review.

Lack of legal review of agreements may commit SJSU to unfavorable contractual terms which may cause financial loss or other damage at a later date.

Legal review is a key factor in protecting the interests of SJSU. In the future, Spartan Shops should ensure that construction management agreements receive documented legal review

(Ownership: SJSU) 10. CSU Standard

Consultant Agreement and forms were not always utilized by SJSU nor were they consistently signed by the construction manager.

Non-standard agreements and unilaterally signed contract documents may not sufficiently protect SJSU in case of a dispute or other legal event.

In the future, SJSU and Spartan Shops should utilize agreements and forms with documented legal review, and ensure that counter signatures are obtained as required. (Ownership: SJSU)

11. Work was performed by the Construction Manager prior to the formal execution of an agreement or ESA.

Allowing work to begin on a project prior to the execution of a contractual agreement puts SJSU at risk in the event of a dispute over work performed.

In the future, SJSU should not allow any consultant to perform or invoice any work without an executed ESA in place. (Ownership: SJSU)

12. Limitations in internal controls resulted in initial overpayments of $127,000 and a payment in the amount of $29,732 for which no contractual obligation existed.

A compromised internal control function over the invoice approval and payment process may result in overpayments.

SJSU should review its invoice approval and payment process and institute revised controls. In addition, SJSU should evaluate the apparent duplicate payments to JLL. (Ownership: SJSU)

Page 5 of 32 San Jose State University

Campus Village Student/Faculty Apartments

INTRODUCTION

Purpose KPMG LLP (“KPMG”) was retained by California State University’s (“CSU”) Office of the University Auditor on October 29, 2004 to perform an independent project evaluation of California State University, San Jose’s (“SJSU”) Campus Village Student/Faculty Apartments project (“the Project”). The overall objective of the construction evaluation was to assess construction management practices for the Project and to substantiate it was managed in accordance with law, Trustee policy, generally accepted business practices, and industry standards. To the extent they were uncovered as part of our work, this report provides conclusions and recommendations addressing necessary recovery of project costs and process improvements. Recommendations are listed and numbered sequentially throughout this report. Scope While the basic scope of our work matches that required by the RFP and that which KPMG has performed in years past, we also included additional items that we believe will provide value to the CSU. KPMG identified specific areas within the scope listed below that present the greatest potential for substantive loss or liability related to the Project. The various scope categories are outlined in CSU’s Request for Proposal, dated July 14, 2004 and KPMG’s Proposal, dated July 27, 2004 and contains the following sections:

• Project Background • Design Cost • Construction Bid Process • Construction Change Orders • Project Management Inspection Services • Major Equipment/Materials • Close-Out Documentation • Liquidated Damages • Accounting

Page 6 of 32 San Jose State University

Campus Village Student/Faculty Apartments

INTRODUCTION

Methodology KPMG’s approach to this engagement incorporates a work plan shared with the University Auditor’s office as outlined in our Agreement with CSU. During the course of our work we expanded on tasks related to scope sections with the greatest potential risk exposure. The work performed by KPMG was conducted in accordance with our aforementioned Methodology, but is not limited to, the following tasks:

• Examine financial records, reports, written CSU procedures, contract documents and other material related to the project and compare current practices and procedures with CSU requirements and accepted practices in the industry;

• Conduct a preliminary review to determine project emphasis; • Interview key individuals involved in the project; • Identify considerable deficiencies, if any; • Recommend changes that may result in streamlining the design/construction

process, assuring adequate project controls and reducing costs; and • Prepare a written report of our findings and recommendations.

Exclusions The services, fees and delivery schedule for this Engagement are based upon the following assumptions, representations or information supplied by CSU (“Assumptions”).

1. KPMG is not responsible for and will not make management decisions relating to this Project or any other aspect of CSU’s business. CSU shall have responsibility for making all decisions with respect to the management and administration of its real estate and capital projects.

2. CSU management accepts responsibility for the substantive outcomes of this engagement and, therefore, has a responsibility to be in a position in fact and appearance to make an informed judgment on the results of this engagement.

3. Our work under this did not include technical opinions related to engineering, operations and maintenance.

4. KPMG’s work under this engagement did not include a review, audit or evaluation of financial statements, tax services, or other services of KPMG not listed in this Statement.

5. We have, and will continue to consider the effect of this Engagement on the ongoing, planned and future audits, as required by Government Auditing Standards and have determined that this engagement will not impair KPMG’s independence.

Page 7 of 32 San Jose State University

Campus Village Student/Faculty Apartments

PROJECT BACKGROUND

The Project incorporated new student and faculty housing with a residence hall for freshmen, an apartment building for upper division students, and a faculty/staff/guest apartment building. The Project included fiber optic telecommunications, kitchens, common areas, laundry facilities, recreation areas, underground parking, a convenience store, and a computer lab and office space. During the week of February 27, 2006, KPMG conducted field work at SJSU and the General Contractor. KPMG reviewed records from the following entities involved with the project:

Architect Niles Bolton Associates (“NBA”) General Contractor (“GC”) Clark Construction Group, Inc.

(“Clark”) Construction Manager (“CM”) Jones Lang LaSalle (“JLL”) Inspector of Record (“IOR”) Construction Testing Services

(“CTS”) Project Management and Administration SJSU Department of Planning,

Design and Construction; Spartan Shops, Inc.(“Spartan Shops”)

Follow-up discussions to clarify issues and supplement supporting documentation were conducted through the completion of this report. Delivery Methodology The Project was initiated by Spartan Shops, Inc., an auxiliary organization to SJSU, as a turn-key methodology. The Project later changed to a Design-Bid-Build approach. Timeline • The Project was initiated in 2000 by Spartan Shops with the intent of obtaining outside

financing for the turn-key Project. At the time, it was SJSU’s understanding that Spartan Shops was able to issue its own debt to finance the Project and as such, the Project would not be a Public Works Project.

• In November, 2000, JLL was retained by Spartan Shops to assist with Project

development. In January 2001, the Board of Trustees granted conceptual approval of the Project with the stipulation that an actual development plan and financing mechanisms would be presented to the Board for additional approval at key points in the process.

Page 8 of 32 San Jose State University

Campus Village Student/Faculty Apartments

PROJECT BACKGROUND

• With the assistance of JLL, Spartan Shops retained a development team in April 2001

that included Trammell Crow, NBA, and McCarthy Construction. Spartan Shops had secured a revenue stream for the initial expenditures.

• The Project approach changed course in late April, 2001 as the Chancellor’s Office

became aware of the progress on the Project. The Chancellor’s Office advised SJSU and Spartan Shops that issuing its own debt as a financing mechanism was not appropriate. Instead, the Chancellor’s Office indicated the preferred financing method should be a system wide revenue bond. In addition, SJSU and Spartan Shops were informed by CSU Capital Planning, Design & Construction (“CPDC”) that the intended delivery methodology of using an outside developer was not recommended. As a result of SJSU’s discussions with the Chancellor’s Office and CSU CPDC, the Project approach was revised to a Design-Bid-Build delivery methodology financed under system wide revenue bond.

• The contracts with Trammell Crow and McCarthy were terminated in September, 2001.

NBA continued as the Architect for the remainder of the Project, as they had already completed a substantial part of the work and were familiar with the Project.

• In January, 2002, the Board of Trustees approved schematic plans of the Project. • Clark Construction was selected as the General Contractor following a normal bid

opening and evaluation procedure in late October, 2002. Notice to Proceed was issued in November 2002 and construction started in December 2002.

• The balances of JLL’s and NBA’s contracts were assumed from Spartan Shops by

SJSU’s Department of Planning Design and Construction in December, 2002. • Notice of Completion was issued to the Contractor on December 22, 2005. Project Costs Project schematic plans were approved by the Board of Trustees at $215,000,000 based on cost per square foot estimates derived from the California Construction Cost Index. Following construction bid opening and realized bid savings, the capital outlay estimate was revised to approximately $206,211,000, which included additional cost category detail. At the time of our field work, there were $205,058,554 in total approved Project commitments and a total amount paid to date of $194,535,665, as summarized in the following table:

Page 9 of 32 San Jose State University

Campus Village Student/Faculty Apartments

PROJECT BACKGROUND

Description Budget Paid Committed VarianceConstruction 145,715,000$ 150,861,311$ 159,183,660$ 13,468,660$ Furniture, Fixtures and Equipment 6,836,115 7,479,509 7,630,016 793,901 Soft Costs 23,230,344 25,967,445 26,532,745 3,302,401 Owner costs 15,714,302 10,227,400 11,712,133 (4,002,169) Contingency 14,715,000 - - (14,715,000) Total 206,210,761$ 194,535,665$ 205,058,554$ (1,152,207)$ As a result of the change from the initial turn-key Project approach to a design-bid-build approach, SJSU incurred costs in form of payments to both Trammell Crow and McCarthy. In total, SJSU paid McCarthy $534,552 and Trammell Crow $3,346,068 (excluding $960,500 for NBA, who continued on the job and whose efforts were not considered lost). Although some of these costs resulted in value for SJSU, a large portion of these payments may not have. SJSU reportedly secured competitive financing and benefited from a competitive bid climate at the time the Project was re-bid. These circumstances could not have been predicted, and may have ultimately contributed to an overall favorable financial outcome of the Project. No analysis has been completed on whether or not the Project incurred a net loss due to the change in direction of the overall Project approach.

Page 10 of 32 San Jose State University

Campus Village Student/Faculty Apartments

DESIGN COSTS Niles Bolton Associates (“NBA”) was initially selected as the Architect for the Project to serve on a team with the developer, Trammell Crow. NBA was a CSU pre-qualified Architectural firm at the time this selection was made. At the termination of the contract between Spartan Shops and Trammell Crow, SJSU decided to keep NBA as the Architect of Record, since NBA already was intimately familiar with the project and already had performed a significant portion of the design services. The initial selection process for retaining NBA was discussed with CPDC and it was agreed that the process fulfilled the requirements under SUAM for a design-bid-build public works project. Consequently, it was reported not to be in violation of Public Contract Code to continue using NBA. • NBA served under contract with Trammel Crow until the termination of Trammel Crow

on September 1, 2001, whereby Spartan Shops agreed to assume the obligation to continue paying NBA under the existing consultant agreement between NBA and Trammel Crow.

• A Letter of Intent was issued by Spartan Shops to NBA on November 8, 2001

authorizing NBA to proceed with all services under a draft agreement. • A standard CSU Architect/Engineer agreement was executed on April 22, 2002

between NBA and Spartan Shops in the amount of $11,059,800. The contract covered Basic Services, Miscellaneous Optional Services, and Reimbursable Expenses.

• A Letter of Assignment dated December 5, 2002 officially transferred the rights and

interests under the aforementioned agreement from Spartan Shops to SJSU.

• On March 10, 2003 a new standard CSU Architect/Engineer agreement was executed to transfer the remaining value of the April 22, 2002 agreement to the SJSU from Spartan Shops, pursuant to the Letter of Assignment dated December 5, 2002. The new agreement was executed for $2,618,000 and superseded NBA’s initial agreement with Spartan Shops.

• At the time of our filed visit, 16 Additional Service Agreements (“ASA”’s) had been

executed with NBA in an amount of $528,816 bringing the total value of the agreement to $11,588,616. (Note: SJSU uses the terminology Additional Services Agreement while SUAM uses the terminology Extra Services Agreement. For the purposes of this document, they are interchangeable.)

Page 11 of 32 San Jose State University

Campus Village Student/Faculty Apartments

DESIGN COSTS

The table below summarizes the agreement with NBA:

Description Date AmountTotal Basic Services 04/22/02 8,145,000$ Extra Services 04/22/02 2,899,800 Reimbursable Expenses 04/22/02 15,000 Total Base Contract 11,059,800$ ASA 1a Tunnel Service 01/15/03 37,700$ ASA 1b "Other" Services and Expenses 01/15/03 70,949 ASA 2 Expansion of Gaming Area 01/22/03 24,940 ASA 3 Mod. of security system design 02/27/04 3,740 ASA 4 Retail Space Design 03/26/04 116,190 ASA 5 Building A Entrance Revisions 03/26/04 13,572 ASA 6 Building A Mailroom Addition 03/26/04 4,177 ASA 7 Building B, 1st & 2nd Floor Revisions 06/16/04 135,973 ASA 8 Tel/Data redesign and Data Room Revisions 06/18/04 175,341 ASA 9 Building C window Revision Credit 06/17/04 (118,350) ASA 10 Café Door Redesign - Building B Tower 12/21/04 4,141 ASA 11 Added Audiovisual Design 01/03/05 33,462 ASA 12 Added Civil Engineering Support 01/31/05 10,000 ASA 13 Structural Engineering for satellite dishes 03/28/05 6,050 ASA 14 Added Civil Engineering Support 05/16/05 5,650 ASA 15 Executive Suite Design 05/01/05 3,300 ASA 16 Executive suite Design 08/12/05 1,980 Subtotal ASA's 528,816$ Total Agreement 11,588,616$

Note: The agreement uses the term “Extra Services” for miscellaneous and optional categories of work including landscape design, programming, and furniture purchasing assistance.

The ASA’s were executed on SJSU letterhead and not on the CSU Standard Extra Services Agreement form which should be utilized for this purpose. The ASA’s were not countersigned by the NBA and only in some instances could we locate a cost proposal from NBA indicating agreement to the scope of work set forth in the ASA. Although SUAM 9210.03 currently does not require counter signature of a service provider on Extra Service Agreements, obtaining the Architect’s counter signature is a standard practice. In addition, we noted several ASA’s for which work had been performed and invoiced by NBA before the ASA’s were formally executed. These include ASA’s no. 1a, 4, 5, 6, 7, 8, 10, 11, and 12, issued by SJSU Facilities Development and Operations, for a total amount of $505,281. However, none of the ASA’s were paid before they were executed.

Page 12 of 32 San Jose State University

Campus Village Student/Faculty Apartments

DESIGN COSTS Observation:

Additional Services Agreements were not counter signed by the Architect and were executed on SJSU letterhead instead of the Standard CSU Extra Services Agreement form.

Risk:

Lack of consultant counter signatures on Extra Services Agreements may limit the enforceability of the SJSU intended to scope of work. Also, by not utilizing the standard ESA form, SJSU may compromise the intent and legal meaning of the standard ESA language.

Recommendation:

1. SUAM 9210.03 should be modified to require counter signature of the service provider on Extra Service Agreements. (Ownership: CPDC)

Management Response:

1. We agree. The extra services authorization procedure was modified and posted on the CPDC web site (SUAM X, Section 9210.03 and sample letter with designer signature block in Appendix C).

Observation:

Significant work outside of the base agreement was performed and invoiced by the Architect before it was incorporated into an executed Extra Services Agreement.

Risk: Work performed without an Executed ESA and a clearly defined scope and contract terms memorialized in an executed ESA signed by the Architect may result in a dispute at a later date.

Recommendation:

2. In the future, SJSU should not allow any consultant to perform and invoice any work without an executed ESA in place.

(Ownership: SJSU)

Page 13 of 32 San Jose State University

Campus Village Student/Faculty Apartments

DESIGN COSTS

Campus Response:

2. We concur. We agree with the recommendation and will follow the SUAM protocol.

At the time of our audit, $375,548 remained to be billed under the contract with NBA. The invoices presented by NBA did not consistently utilize the above schedule of values to show what contractual component was being invoiced against, what had previously been invoiced and what value had been earned. This resulted in difficulties in determining what had been invoiced to date and what work remains outstanding on the agreement. SJSU did not keep a complete listing of all invoices and contractual agreements on the project, mainly due to Spartan Shops use of a separate accounting system from SJSU and SJSU’s own change of accounting systems during the course of the Project. As a result, no comprehensive list of invoices was maintained. JLL tracked certain cost information on behalf of the SJSU and Spartan Shops, but detail data was not available for our review, nor was it retained by SJSU. Observation:

Neither SJSU nor NBA tracked the amounts invoiced against each contractual component separately.

Risk:

By not tracking the amount charged to each separate component within the agreement separately, chances that an individual line item would exceed the contractually agreed upon amount increases. In addition, the risk for accounting irregularities and errors increases.

Recommendation:

3. A better practice would be to require consultants to invoice presenting all contracted line items including the contracted amount, the amount previously billed, the current billing, and total invoiced to date for each line item. In addition, SJSU should track the invoices in a similar fashion to verify the accuracy of the billings presented by the consultant.

(Ownership: SJSU)

Page 14 of 32 San Jose State University

Campus Village Student/Faculty Apartments

DESIGN COSTS

Campus Response:

3. We concur. We agree with the recommended practice and going forward will conform with invoicing format/forms posted by the Chancellor’s Capital Planning Design and Construction (CPDC) office. In addition, we will add the invoice format requirement to future A/E contracts.

When comparing the NBA invoices to the appropriate entries in SJSU’s accounting system, KPMG discovered that invoice number 22478 in the amount of $51,758 was incorrectly entered as $57,758 which indicates a $6,000 overpayment on that invoice. No later correction was noted. We were informed that no systematic reconciliation against the contractual agreement or the accounting systems occurred. Observation:

Reconciliation between the accounting system(s) and invoices did not occur on a comprehensive and regular basis.

Risk:

Without controls to prevent and detect extra amounts entered into the accounting system, SJSU is at a risk of overpaying its consultants.

Recommendation:

4. A periodic reconciliation between the invoiced amounts and amounts paid should occur to detect errors in data entry and correct any accidental overpayments. SJSU should consider the $6,000 overpayment in its final negotiations with NBA.

(Ownership: SJSU)

Campus Response:

4. We concur. We agree with the recommendation and will reconcile invoiced amounts before payments. The $6,000 overpayment was corrected and SJSU did not end up paying more than the contract amount.

The April 22 Standard Agreement in the amount of $11,059,800 with a modified Rider A lacked evidence of legal review, as no signature by Counsel was present. SUAM 9780.03 and 9210.01 states the requirements for review by Counsel and that and is not considered in effect until approved by CSU Office of General Counsel. Although Spartan Shops may not be subject to all requirements of CSU Contract Law, review by Counsel is a better business practice.

Page 15 of 32 San Jose State University

Campus Village Student/Faculty Apartments

DESIGN COSTS

Observation:

The Architect contract was entered into without evidence of legal review. Risk:

Lack of legal review of contracts by counsel may commit SJSU to unfavorable contractual terms which may cause financial loss or other damage at a later date.

Recommendation:

5. Legal review is a key factor in protecting the interests of SJSU. In the future, Spartan Shops should attempt to have design agreements receive documented legal review.

(Ownership: SJSU)

Campus Response:

5. We concur. In the future, Spartan Shops will have design agreements receive documented legal review.

Page 16 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION BID PROCESS Following the change in direction to Design-Bid-Build, the Project became a public works project governed by Public Contract Code including the requirement for public bid. The resulting formal bid process was administered by JLL under the direction of SJSU. Five general contractors, Clark, Hensel Phelps Construction, the Hunt Construction Group, McCarthy Building Company, and Swinerton Builders, were pre-qualified and invited to submit bids for the Project. A mandatory pre-bid meeting was held on September 19, 2002 where a completed set of specifications, general conditions and drawings were made available to the bidders. A total of six addenda were issued prior to bid opening, revising the bid opening date and modifying drawings and specifications. The Architect’s estimated cost of the Project at the time of bid was $167,600,000. Bid Opening occurred on October 22, 2002. Clark and Hensel Phelps were the only two contractors who submitted bids. A formal evaluation and ranking process occurred where Clark emerged with the lowest bid, both on the base bid and including all Alternate bid items. Clark was awarded the project with a base bid and alternates of $145,715,000 which resulted in a $21 million bid saving over the Architect’s estimate. KPMG reviewed the bid files and evaluated the pre-qualification and bid process and found SJSU in compliance with requirements related to pre-bid meeting, advertising for bids, distribution of Project plans and specifications, review of bid proposal package, addenda during bidding, pre-qualification of bidder, obtaining required documentation from the successful bidder and award of contract. When visiting with Clark, we verified that sub-contractor trades had been competitively bid. In addition to the base bid there were two major change orders which expanded on the scope of the work. The changes encompassed a significant telecom upgrade and the construction of a separate mail facility. Both these items were competitively bid separately from the base contract. Recommendation:

None

Page 17 of 32 San Jose State University

Campus Village Student/Faculty Apartments

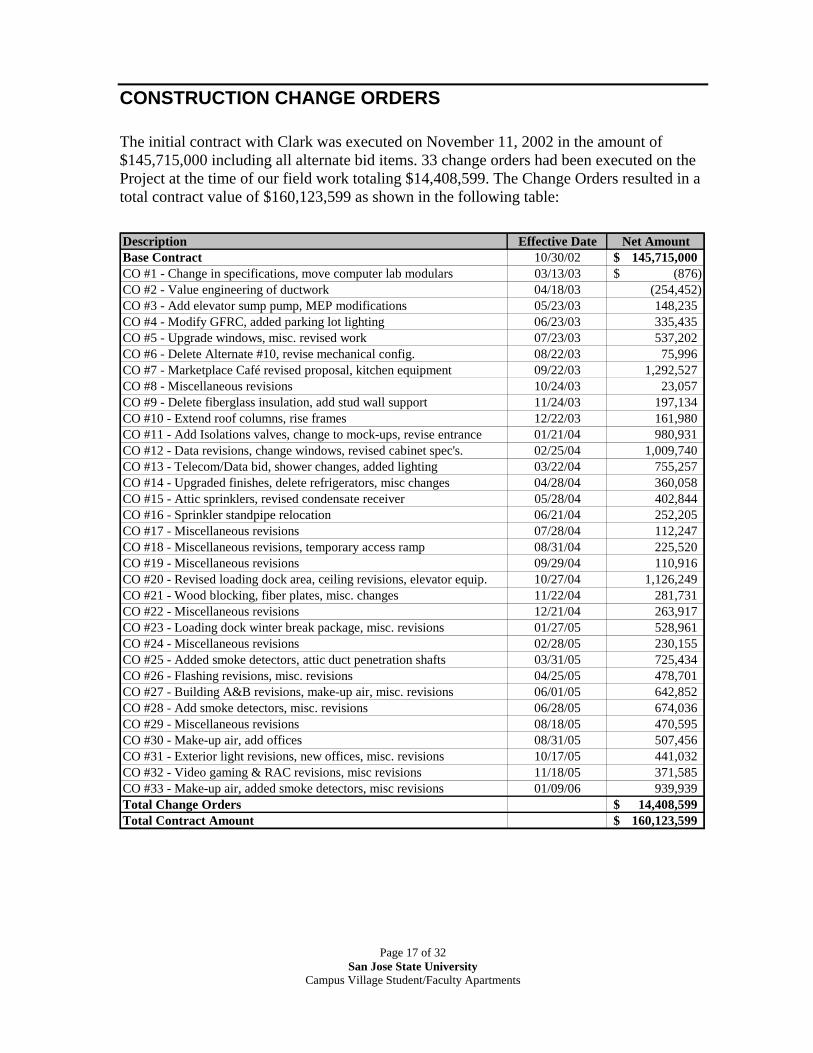

CONSTRUCTION CHANGE ORDERS

The initial contract with Clark was executed on November 11, 2002 in the amount of $145,715,000 including all alternate bid items. 33 change orders had been executed on the Project at the time of our field work totaling $14,408,599. The Change Orders resulted in a total contract value of $160,123,599 as shown in the following table: Description Effective Date Net AmountBase Contract 10/30/02 145,715,000$ CO #1 - Change in specifications, move computer lab modulars 03/13/03 (876)$ CO #2 - Value engineering of ductwork 04/18/03 (254,452) CO #3 - Add elevator sump pump, MEP modifications 05/23/03 148,235 CO #4 - Modify GFRC, added parking lot lighting 06/23/03 335,435 CO #5 - Upgrade windows, misc. revised work 07/23/03 537,202 CO #6 - Delete Alternate #10, revise mechanical config. 08/22/03 75,996 CO #7 - Marketplace Café revised proposal, kitchen equipment 09/22/03 1,292,527 CO #8 - Miscellaneous revisions 10/24/03 23,057 CO #9 - Delete fiberglass insulation, add stud wall support 11/24/03 197,134 CO #10 - Extend roof columns, rise frames 12/22/03 161,980 CO #11 - Add Isolations valves, change to mock-ups, revise entrance 01/21/04 980,931 CO #12 - Data revisions, change windows, revised cabinet spec's. 02/25/04 1,009,740 CO #13 - Telecom/Data bid, shower changes, added lighting 03/22/04 755,257 CO #14 - Upgraded finishes, delete refrigerators, misc changes 04/28/04 360,058 CO #15 - Attic sprinklers, revised condensate receiver 05/28/04 402,844 CO #16 - Sprinkler standpipe relocation 06/21/04 252,205 CO #17 - Miscellaneous revisions 07/28/04 112,247 CO #18 - Miscellaneous revisions, temporary access ramp 08/31/04 225,520 CO #19 - Miscellaneous revisions 09/29/04 110,916 CO #20 - Revised loading dock area, ceiling revisions, elevator equip. 10/27/04 1,126,249 CO #21 - Wood blocking, fiber plates, misc. changes 11/22/04 281,731 CO #22 - Miscellaneous revisions 12/21/04 263,917 CO #23 - Loading dock winter break package, misc. revisions 01/27/05 528,961 CO #24 - Miscellaneous revisions 02/28/05 230,155 CO #25 - Added smoke detectors, attic duct penetration shafts 03/31/05 725,434 CO #26 - Flashing revisions, misc. revisions 04/25/05 478,701 CO #27 - Building A&B revisions, make-up air, misc. revisions 06/01/05 642,852 CO #28 - Add smoke detectors, misc. revisions 06/28/05 674,036 CO #29 - Miscellaneous revisions 08/18/05 470,595 CO #30 - Make-up air, add offices 08/31/05 507,456 CO #31 - Exterior light revisions, new offices, misc. revisions 10/17/05 441,032 CO #32 - Video gaming & RAC revisions, misc revisions 11/18/05 371,585 CO #33 - Make-up air, added smoke detectors, misc revisions 01/09/06 939,939 Total Change Orders 14,408,599$ Total Contract Amount 160,123,599$

Page 18 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION CHANGE ORDERS

Clark and SJSU were in ongoing negotiations regarding a project time extension at the time of our field work and no extra time had been granted on any of the Change Orders. These negotiations were occurring after the Notice of Completion had been issued. SJSU provided KPMG with details of the negotiations, including initial discussions with Clark. Recommendation:

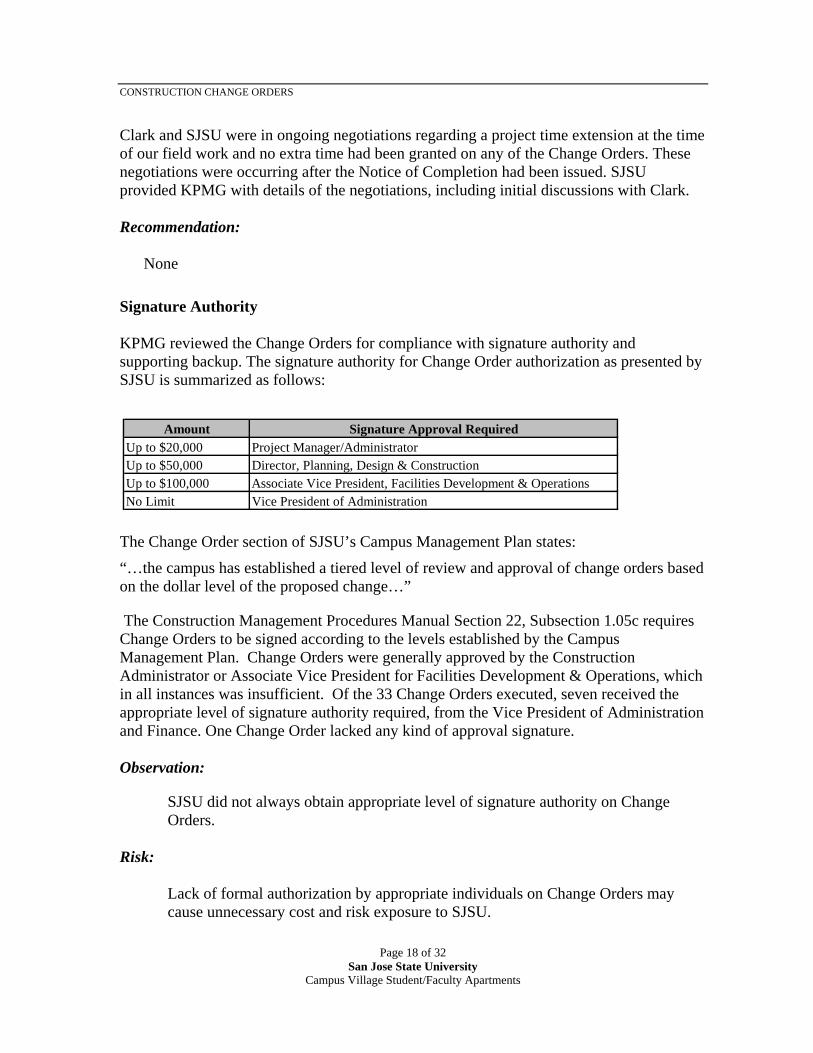

None Signature Authority KPMG reviewed the Change Orders for compliance with signature authority and supporting backup. The signature authority for Change Order authorization as presented by SJSU is summarized as follows:

Amount Signature Approval RequiredUp to $20,000 Project Manager/AdministratorUp to $50,000 Director, Planning, Design & ConstructionUp to $100,000 Associate Vice President, Facilities Development & OperationsNo Limit Vice President of Administration

The Change Order section of SJSU’s Campus Management Plan states:

“…the campus has established a tiered level of review and approval of change orders based on the dollar level of the proposed change…”

The Construction Management Procedures Manual Section 22, Subsection 1.05c requires Change Orders to be signed according to the levels established by the Campus Management Plan. Change Orders were generally approved by the Construction Administrator or Associate Vice President for Facilities Development & Operations, which in all instances was insufficient. Of the 33 Change Orders executed, seven received the appropriate level of signature authority required, from the Vice President of Administration and Finance. One Change Order lacked any kind of approval signature. Observation:

SJSU did not always obtain appropriate level of signature authority on Change Orders.

Risk:

Lack of formal authorization by appropriate individuals on Change Orders may cause unnecessary cost and risk exposure to SJSU.

Page 19 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION CHANGE ORDERS

Recommendation:

6. A better practice would require the highest level of signature authority on the face of the change order which is the contractually binding document. (Ownership: SJSU)

Campus Response:

6. We concur. We agree with the recommendation and will follow SUAM and Project Administrator protocol going forward.

Mark-Up KPMG recalculated the mark-up charged on Change Order work by Clark. The Contract General Conditions specify how mark-up is to be calculated on the various portions and types of work. KPMG sampled 11 change order line items (comprised of individual change proposals) and recalculated the mark-up based on the costs submitted by Clark Construction. We noted that on occasion, mark-up was calculated on a straight percentage basis without adjusting the percentage downward for amounts greater than $50,000 as described in the General Conditions and SUAM.

The total value of the tested change proposals included with the Change Orders was $3,583,107 for which we KPMG calculated a variance of $12,126 strictly based on adjustments to the mark-up calculation. Any cost adjustments would further modify the calculated mark-up.

The variance represents 0.31% of the total value of the total value of the Change Proposals as summarized in the table below:

CP # Value of CPRecalculated

Amount Variance114 1,141,427$ 1,139,197$ 2,230$ 185 293,009 292,971 38 189 219,044 224,776 (5,732) 190 210,557 208,615 1,942 194 307,403 298,918 8,485 201 118,350 118,376 (26) 207 270,093 264,904 5,189 216 400,953 400,953 - 231 114,404 114,404 - 246 244,739 244,739 - 505 533,128 533,128 -

Total 3,853,107$ 3,840,981$ 12,126$ Variance as percent of total CP value 0.31%

Page 20 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION CHANGE ORDERS

Observation:

On occasion, mark-up was calculated incorrectly on the Change Orders.

Risk:

SJSU is at a risk of overpayment when mark-up is calculated incorrectly. Recommendation:

7. Change order proposal summary sheets should be checked for proper mark-up calculation by the Construction Administrator prior to issuing the change order. (Ownership: SJSU)

Campus Response:

7. We concur. We agree with the recommendation and will have mark-up calculations according to Operational Plan mark-up template provided by CPDC and reviewed by at least two persons going forward.

Contractor Direct Costs Clark submitted certain recurring direct costs as part of its Change Order costs which included cost categories which by industry standards generally are categorized as general conditions costs or field overhead and as such should be covered by the Contractor’s mark-up. Examples of costs charged by Clark as direct costs include project management, supervision, quality control, temporary facilities, clean-up, and insurance. SJSU objected to the nature of these costs early on in the Project, arguing that such costs should in fact be covered by the mark-up. Due to differing interpretations of the contract definition of what mark-up should cover, SJSU eventually approved of the Change Order amounts as submitted by Clark, inclusive of all direct costs. In our discussions with the Contractor, Clark explained its interpretation of the Contract General Conditions, section 6.01.c-(4) concluding that the definition of mark-up was weak and ambiguous and allowed for their strict interpretation. Specifically mentioned by Clark was the absence of a description pertaining to work related to Change Order administration, solicitation of quotes from subcontractors and vendors as well as direct supervision. Clark did not present conclusive evidence that supported their calculation of their contractor controlled insurance program, for which they included costs in the Change Orders. Clark also indicated that any attempt by SJSU to recover any costs would result in legal action on behalf of Clark.

Page 21 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION CHANGE ORDERS Each Change Order generally consisted of 10-30 separate Change Proposals. KPMG sampled 11 Change Proposals and performed an analysis of the direct costs submitted by Clark. Amounts associated with dumpsters, temporary toilets, clean-up and insurance were subtracted. The total value of the Change Proposals included with the Change Orders was $3,583,107 of which $293,067 encompassed Contractor Direct Costs. KPMG calculated a variance of $178,261 or 4.6% of the total value of the total value of the Change Proposals as summarized in the table below:

CP # Value of CPAmount Claimed

Amount Allowed Variance

114 1,141,427$ 94,618$ 43,432$ 51,186$ 185 293,009 21,728 125 21,603 189 219,044 14,824 215 14,609 190 210,557 13,947 4,878 9,069 194 307,403 16,813 1,659 15,154 201 118,350 10,508 9,090 1,418 207 270,093 16 16 - 216 400,953 9,482 1,283 8,199 231 114,404 12,857 59 12,798 246 244,739 29,342 5,295 24,047 505 533,128 68,932 48,754 20,178

Total 3,853,107$ 293,067$ 114,806$ 178,261$

Variance as percent of total CP value 4.6% Observation:

The Contractor charged certain direct costs which by industry standards and the General Conditions should have been covered by the Change Order mark-up percentage. In addition, the General Conditions allow for ambiguous interpretation of the definition of mark-up.

Risk:

SJSU is at a risk of overpayment when items which are not intended or allowed to be charged as a direct cost are permitted in the Change Orders

Recommendation:

8.a. On future contracts, SJSU should require the Contractor to submit substantiation for its direct costs prior to executing a Change Order. SJSU should also evaluate whether any monetary recourse against the Contractor is warranted.

(Ownership: SJSU)

Page 22 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION CHANGE ORDERS

8.b. The General Conditions should be modified to specify mark-up to include

anything not expressly stated as an allowable change order cost of work. (Ownership: CPDC)

Campus Response:

8.a. We concur. We will require the Contractor to submit substantiation for its direct costs prior to executing a Change Order. We will also evaluate whether any monetary recourse against the Contractor is warranted.

Management Response:

8.b. We agree. We have modified the Contract General Conditions using the Supplementary General Conditions and posted it to the CPDC web site.

Change Order Report Analysis Trustees generally consider additional cost incurred related to Architect/Engineer errors and omissions of up to 3% of the initial award construction cost as being within the requirements of ‘standard of care’, as per the current agreement. However, the agreement as executed did not contain any language related to ‘standard of care’. The agreement stated the Architect/Engineer shall secure and maintain appropriate errors and omissions insurance of no less than $5,000,000 per occurrence, $10,000,000 annual aggregate. SJSU provided a change order log reflecting the source of each change order. However data was available through Change Order 31(of 33) only and does not reconcile to the actual executed Change Orders. The following table summarizes the data:

Amount % of Total CO

% of Original Contract

4.1 Error in or omission from the contract documents 4,161,174$ 36.05% 2.86%4.2 Unforeseeable fob site condition 351,124 3.04% 0.24%4.2 Change in the requirements of a regulatory agency 2,088,563 18.09% 1.43%4.4 Change originated by the University 4,424,118 38.32% 3.04%

4.5Changes in specified work due to the unavailability of specified materials 7,624 0.00 0.00

4.6 Other 511,090 4.43% 0.35%Total Change Orders 11,543,693 100.00% 7.92%Original Contract Amount 145,715,000$ Total 157,258,693$

Type of Change

Page 23 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION CHANGE ORDERS

Change orders attributable to Architect’s errors and omissions exceeded 36 % of the total net change order costs. In addition these errors and omissions are calculated to be 2.86% of the original contract amount. Although the total errors and omissions are less than 3% which normally fall under the CSU’s acceptable levels of ‘standard of care’, SJSU is in the process of negotiating any responsibility by NBA, as the total amount of errors and omissions exceeded $4 million. Recommendation:

None Contractor Compliance – Subcontractor Practices

There were two instances of subcontractor substitution identified on this Project, which requires specific substitution procedures to be followed. F.W. Spencer replaced Scott Co. for Mechanical work due to Scott’s inability to obtain the proper Performance or Payment bonds, and B.T. Mancini Co. Inc replaced Spectra Contract Flooring when their local store closed. Both substitutions occurred according to public contract code section 4400. Recommendation:

None

Page 24 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION MANAGEMENT SERVICES Through a competitive process, JLL was initially retained to assist with selection of a development team for the Project. As the Project progressed, JLL was competitively retained to provide construction management services for the Project throughout construction. The following bullet points summarize the timeline for the contractual arrangements with JLL: JLL was initially retained on July 7, 2000 to provide initial scoping services and to assist in the selection of a developer to provide a turn-key solution to the Project. Spartan Shops issued the initial agreement to JLL in the amount of $77,000. • On June 21, 2001 Spartan Shops entered into a second agreement with JLL to provide

development advisory services. This agreement was issued in the amount of $1,881,900.

• On April 22, 2002 Spartan Shops entered into a third agreement with JLL to expand the

development advisory services to encompass full project management and construction management services. This agreement was issued in the amount of $4,328,000 and superseded the June 21, 2001 agreement.

• A Letter of Assignment dated December 5, 2002 officially transferred the rights and

interests under the aforementioned agreement from Spartan Shops to SJSU. • On March 3, 2003 a standard CSU consultant agreement was executed to transfer the

remaining value of the April 22, 2002 to SJSU from Spartan Shops, pursuant to the Letter of Assignment dated December 5, 2002. The new agreement was executed for $2,893,000 and superseded the existing agreement with Spartan Shops.

• Three additional agreements for an operations evaluation ($112,750), selection of a

marketing firm ($21,000), and assembling an operating budget ($21,000) were agreed to in June 2003 by counter signing or otherwise agreeing to three JLL cost proposals.

• At the time of our field visit, 3 Extra Service Agreements (ESA’s) had been executed

totaling $143,750, bringing the total value of the agreement to $4,630,686. The table below summarizes the various agreements with JLL:

Page 25 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION MANAGEMENT SERVICES

Description Date Amount

Initial Development Services 07/07/02 77,000$ Expandete Developmnet and Construction Management Services 04/22/02 4,328,000 Total Base Contracts 4,405,000$ ESA #1 - Security and IT Mgmt Services 05/28/04 62,000 ESA # 2 - Dining Commons, Joe West Hall, and Village Gaming 07/13/04 74,490 ESA #3 - Miscellaneous Expanded Scope Services 07/14/05 89,196 Subtotal ESA's 225,686$ Marketing Program 06/21/03 21,000 Operating Budget 6/2/2003 10,000 Operations Evaluation Proposal 11/18/03 112,750 Subtotal Additional Agreements 143,750$ Total Agreement 4,630,686$ The JLL agreements entered into by Spartan Shops in the amounts of $77,000, $1,881,900 (superseded) and $4,328,000 did not contain any evidence of CSU legal review. Legal review becomes particularly important when non-standard agreements are utilized.

Observation:

Several JLL agreements were entered into without evidence of CSU legal review. Risk:

Lack of legal review of agreements may commit SJSU to unfavorable contractual terms which may cause financial loss or other damage at a later date.

Recommendation:

9. Legal review is a key factor in protecting the interests of SJSU. In the future, Spartan Shops should ensure that construction management agreements receive documented legal review.

(Ownership: SJSU)

Campus Response:

9. We concur. In the future, Spartan Shops will have construction management agreements receive documented legal review.

SJSU and Spartan Shops did not consistently utilize the Standard CSU consultant Agreement in contracting with JLL; (a) two of the initial agreements were developed independently by Spartan Shops, (b) the additional agreements entered into consisted of JLL proposals, bilaterally signed on JLL letterhead or, in one instance, not signed by SJSU at all, and (c) the CSU Standard Form was not utilized for the Extra Services Agreements, nor were they bilaterally signed. Although auxiliary organizations such as Spartan Shops

Page 26 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION MANAGEMENT SERVICES

may enjoy some flexibility in its contracting arrangements, it is the preference by the Chancellor’s Office that CSU contract law is adhered to. Since this Project transitioned to a SJSU Project, adherence to CSU Contract Law became a requirement. Observation:

The CSU standard consultant Agreement and standard ESA form were not always utilized by SJSU nor were they consistently signed by the construction manager.

Risk:

Non-standard agreements and unilaterally signed contract documents may not sufficiently protect SJSU in case of a dispute or other legal event.

Recommendation:

10. In the future, SJSU and Spartan Shops should utilize agreements and forms with documented legal review, and ensure that counter signatures are obtained as required.

(Ownership: SJSU)

Campus Response:

10. We concur. In matters related to Construction Management Services, Spartan Shops will utilize agreements and forms with documented legal review and obtain counter signatures as required.

The initial JLL with Spartan Shops in the amount of $1,881,900 was effective June 21, 2001. Although JLL did not present an invoice to Spartan Shops until the day after the agreement was signed into effect, this first invoice was backdated for services rendered from February 1, 2001 through May 31, 2001 totaling $185,128. Similarly, ESA #3 was invoiced and paid in full in the amount of $29,732 before the ESA was executed. Observation:

Work was performed by the Construction Manager prior to the formal execution of an agreement or ESA.

Risk:

Allowing work to begin on a project prior to the execution of a contractual agreement puts SJSU at risk in the event of a dispute over work performed.

Page 27 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION MANAGEMENT SERVICES

Recommendation:

11. In the future, SJSU should not allow any consultant to perform or invoice any

work without an executed ESA in place.

(Ownership: SJSU)

Campus Response:

11. We concur. We agree with the recommendation and will follow the SUAM protocol (this finding is the same as #2 above).

KPMG noticed two invoice processing discrepancies for JLL. The initial $185,128 invoice from Spartan Shops contained a mathematical error of $37,000; the correct amount should be $148,128. In addition, JLL invoice #29 in the amount of $90,000 was paid by both Spartan Shops and SJSU. No subsequent reversals or invoice corrections were noted. ESA #3 in the amount of $29,732 was paid before the ESA was executed.

Observation:

Limitations in internal controls over the invoice approval and payment process resulted in initial overpayments of $127,000 and a payment in the amount of $29,732 for which no contractual obligation existed.

Risk:

A compromised internal control function over the invoice approval and payment process, such as performing mathematical checks, preventing double payments of an invoice, and verification of a contractual obligation, may result in overpayments.

Recommendation:

12. SJSU should review its invoice approval and payment process and institute revised controls to prevent multiple payments on the same invoice and to help ensure invoices are checked for mathematical accuracy. In addition, SJSU should evaluate the apparent duplicate payments to JLL.

(Ownership: SJSU)

Page 28 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CONSTRUCTION MANAGEMENT SERVICES

Campus Response:

12. We concur. We agree with the recommendation and will improve controls for invoice approval and payment process. We have evaluated and reconciled all JLL payments, and after careful review and adjustments, there are no duplicate payments.

, In addition to JLL, SJSU contracted with CTS, a specialized inspection firm. A Standard Service Agreement was executed on February 12, 2003 in the amount of $708,000. As a result of added scope and increased inspection needs, change orders in the amount of $937,500 were issued resulting in a total value of the of $1,645,500. Limited review of supporting documentation was performed to evaluate reasonableness of the invoicing process. Nothing came to our attention that indicated a discrepancy.

Page 29 of 32 San Jose State University

Campus Village Student/Faculty Apartments

MAJOR EQUIPMENT/MATERIALS REVIEW The Project consisted of active housing units at the time of KPMG’s field work and as a result, equipment and materials were selected partially based on accessibility in order not to disturb the occupants. SJSU allowed full and complete access to drawings, specifications, samples and submittals which were organized and easy to locate and contained sufficient information. The equipment was verified in the field against performance specifications, submittals, and drawings available. The following equipment items and specific model data were approved and visually confirmed as installed on the project: Division Drawing No. Brand Model No./ Capacity Description15855 M0.02 Trane MCCB010VA0COVA /

7.5 HP / 5,000Air Handling Unit

15855 M0.02 Trane MCCB012UA0COUB / 7.5 HP / 5,500

Air Handling Unit

16800.200.2 SE0.01-SE5.07 Info Graphic Diamond Series Securtiy System

08800-200.0

A8.10 Kawneer 843OTL Single Hung HC-65

Glass

09680-200.0

not found Interface 1462902500 / Chenille Warp Tile Carpet

Carpet

07411-205.0

A2.13 & WW1.05 Una-Clad UC-6 18" o/c, 24 Gauge Steel Roof System

Roofing

07411-205.1

A2.13 & WW1.05 Una-Clad UC-3 16" o/c, 24 Gauge Steel Roof System

Roofing

06410- A1.06 Unspecified Unspecified Cabinets04211-200.0

A6.00 H.C. Muddox Wire Cut Medium Tumble Mountain Rose # 1230

Masonry

08210- A8.01 Lynden Door, Inc. Wood Doors

Elevator14240 A4.92 & A7.20 Fujitec Car Number 7 / 3,500 lbs

The equipment and materials observed in the field conformed to the specifications above, based on a visual inspection of equipment labeling, and comparison to samples provided. Recommendation:

None

Page 30 of 32 San Jose State University

Campus Village Student/Faculty Apartments

CLOSE-OUT PROCESS KPMG verified the project close out requirements established by the Contract General Conditions and SUAM. KPMG reviewed Notice of Completion, the Certificate of Occupancy for all five buildings, Punch List, Operating Permits, Operation & Maintenance Manuals, Warranties, As-Built Drawings, Pre-Final and Final Inspections, and other relevant project close out documentation, which was filed in an orderly fashion and retained properly at the SJSU. This project had not been fully closed out at the time of our field work and open contracts remain with Clark, NBA, and JLL. Recommendation:

None

Page 31 of 32 San Jose State University

Campus Village Student/Faculty Apartments

LIQUIDATED DAMAGES The agreement between the Trustees and Clark establishes the final completion date of August 15, 2005. The State Fire Marshal issued a Conditional Certificate of Occupancy on August 17, 2005 and a final Certificate of Occupancy on March 1, 2006. Due to the outstanding negotiations between the SJSU and Clark regarding change order time extensions, liquidated damages cannot be calculated at the present time. Recommendation:

None

Page 32 of 32 San Jose State University

Campus Village Student/Faculty Apartments

ACCOUNTING KPMG reviewed the accounting process for the Project with SJSU personnel, including invoicing and the accounts payable process. Tracking of invoices obligations and payments occurred by Spartan Shops, JLL and SJSU’s Department of Planning, Design and Construction. Four accounting systems were utilized; one by Spartan Shops and two by SJSU (who changed accounting systems shortly after the Project transitions from Spartan Shops), and one by JLL. We encountered several discrepancies and reconciliation issues between different sources of information, which in part can be attributed to the multiple accounting systems. These apparent discrepancies include: • Accounting of agreements and payments not part of this Project • No regular and comprehensive reconciliation between invoices and accounts payable • No central tracking of all obligations and payments by vendor • Double payment of invoices • Overpayment of invoices A standardized reconciliation process designed to (a) ensure the accuracy and validity of the entries in all project cost accounting systems, (b) validate that records are accurately recorded, (c) make sure unauthorized changes did not occur, and (d) resolve any discrepancies in a timely fashion, will help minimize the risk of accounting irregularities and errors go undetected. An effective reconciliation process becomes particularly important when accounting information is housed in multiple locations, as was the case with this Project. Recommendation: See previous recommendations throughout this report.