Embed Size (px)

Citation preview

Sailing away the winter blues with ISFAA …

2015 Winter Conference

Financial Literacy “ROI”

Constructing Measurable Financial Literacy Initiatives

2

Contact Info

Michele Wedel, Adjunct Instructor Kelley School of Business, IUPUI(317) [email protected]

Sara Wilson, USA Funds(317) [email protected]

3

Agenda

• Building The Program• Evaluating The Program• Discussion/Question & Answer

4

Session Outcomes• By the end of the this session, you will be able to:

– Cite the importance of involving all stakeholders in the planning and implementation processes

– List the top financial literacy topics for the student audience

– Describe how to make financial literacy sessions interesting and relevant for students

– Use national datasets to develop an assessment plan to measure the impact of the financial literacy initiatives

5

Why is financial literacy needed• Student loan debt over $1.1 trillion. Compared

to:– Credit card debt = $854 billion. – Auto loan debt = $877 billion.

• Average student loan debt is approx. $30,000.• Financial stress is one of the top reasons for

students leaving college prior to completing their education.

• CDR change from 2-year rate to a 3-year rate.

BUILDING THE PROGRAM

7

Who needs to Be Involved• Implementing alone can be difficult• Identify the key stakeholders

– Who/what areas benefit from financial education• Or suffer from a lack of it

– Stakeholders will vary from campus to campus• Look for overlapping areas – the sweet spot

Students

Alumni Office

Financial Aid Office

Student Loan Indebtedness

8

Potential key stakeholders• Admissions• Enrollment/Retention• Orientation/First-Year

Experience• Financial Aid• Academics/Academic

Services – Course curriculum,

academic advising, Higher Education Opportunity Programs, summer bridge

• Career Development/Services

• Administration– President’s office,

business office

• Support Services – TRIO, Upward Bound,

EOPS

• Alumni Services• Accrediting Organizations

9

What is needed on my campus• Ways to determine the

most important financial literacy issues on your campus– Check with student-led

organizations– Talk with other

departments like financial aid, housing, advising, alumni and retention

– Survey students directly

10

Create a Hub or Single Point of Contact

• For example, IUPUI Financial Wellness Committee– Led by Marvin Smith, Director of Student Financial Services– Representation by numerous stakeholder offices

• Financial aid• Student advising• Student housing• Student government• Undergraduate and graduate programs• Faculty• Office of Financial Literacy

– Significantly reduces silos/stovepipes; the barriers to communicating across the institution

11

Start Small, Build Up

• Focus on the most important outcome(s)• Focus on what will impact the most number of

stakeholders

Students

Alumni Office

Financial Aid

Office

Student Loan Indebtedness

12

How can I apply this?• Assess the need

– all stakeholders, instructional need• Clearly and specifically define the goals and

objectives of the lesson, course, presentation…– Start with goals, then assessment and finally methods

• Remember the learners’ perspective– What is driving them, make it relevant

• Design, implement, evaluate, repeat….

13

Classes, Workshops, Forums, Oh My!

• Biggest lesson learned – Just because you build it, doesn’t mean they’ll come.

• Choose delivery methods that work best for you and your students.

• Variety is key – Meets the needs of different types of learners

14

Classes, Workshops, Forums, Oh My!

• Formal admissions process• Freshman orientation

programs• First year experience

courses• Individual course work/

assignments• Incorporated into program

of study• Financial aid application

process• SAP appeals• Peer mentor programs• Electronic newsletter/

targeted emails• Group presentations/

workshops• Summer bridge programs

for high school students• Student Success Programs

15

Classes, Workshops, Forums, Oh My!• Office of Financial Literacy

– Phil Schuman, Director– Money$marts web site

• FWC & SFS Leadership• For credit class

– Hybrid & Online– Same design

• Except for in-class portion

– Pre/post-Tests– End of course survey– Launched Fall 2013– FWC key to promoting– 306 so far, 88 started 1/12/15

• Silos reduced or removed!

16

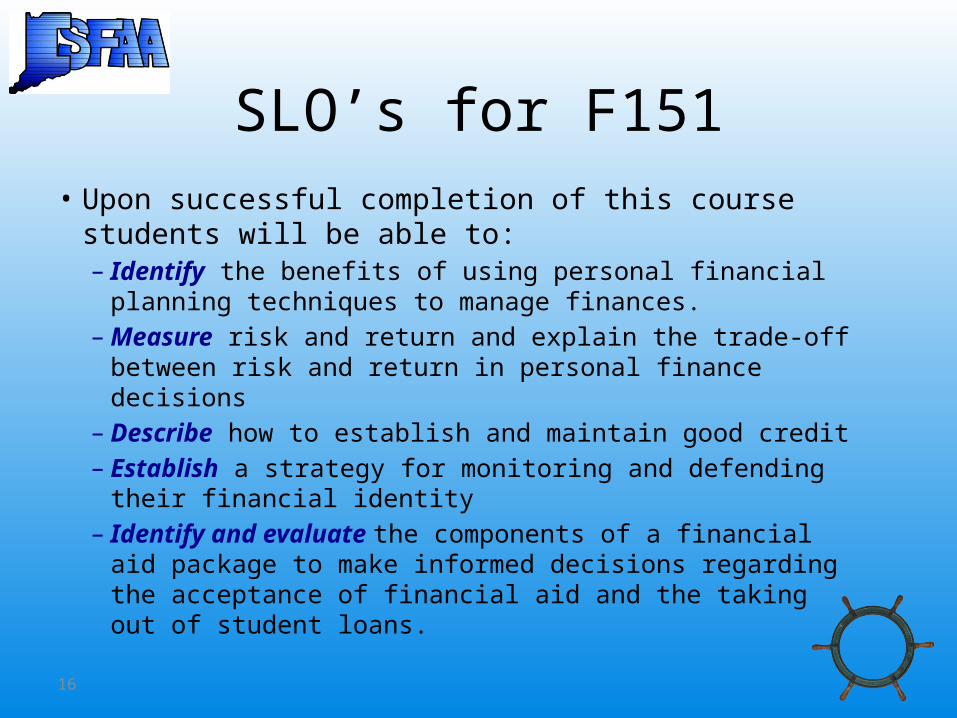

SLO’s for F151• Upon successful completion of this course students will

be able to:– Identify the benefits of using personal financial planning

techniques to manage finances. – Measure risk and return and explain the trade-off between

risk and return in personal finance decisions– Describe how to establish and maintain good credit– Establish a strategy for monitoring and defending their

financial identity – Identify and evaluate the components of a financial aid

package to make informed decisions regarding the acceptance of financial aid and the taking out of student loans.

17

Make It Relevant • Topics of interest according to research

– Saving and investing for the future– Getting ahead financially after graduation– Avoiding credit problems and ID theft– Budgeting income and expenses– Financial aid and student loans

18

Make It Relevant • Find ways to relate training to topics that matter

to students– Ways to save money on campus– Skills needed to make financial decisions students

are being asked to make• loans, food, housing, transportation

• Teach the concept, show an example and then have the students apply– Exercises can be simple and still teach life long

financial management and problem solving skills

EVALUATING THE PROGRAM/IMPACT

20

Why Measure• Track progress towards goal(s) identified when

building the program• Assess effectiveness of program and make

improvements• Challenges:

– “Doing no harm” does not equal “doing good”– Difficult to prove scientifically (attribution vs.

contribution)• Solution: look for leading indicators — knowledge,

attitudes and behaviors

21

What to Measure• What have others done? — Use national datasets

– Numerous school and program specific research studies– Some nationwide research on the state of financial literacy– Very few nationwide research on effectiveness

• What can you do? — Learning value chain – Input: volume and exposure– Reaction: satisfaction– Learning: knowledge and ability– Attitude: planned actions– Application: changes in behavior

22

Kirkpatrick’s Four Levels of Evaluation

Kirkpatrick, D. L. & James D. Kirkpatrick. (2006). Evaluating training programs: The four levels, 3rd ed. San Franciso: Berrett-Koehler

23

The Learning Value Chain - SimplifiedLevel Measurement Focus Key Questions

Input - 0Volume and exposure to materials

How many participants? What topics were presented?

Reaction - 1Satisfaction with program

Was the program relevant, important and useful at this time?

Learning - 2Knowledge and ability to apply newly learned skills

Did participants increase or enhance knowledge, skills or perceptions and have confidence to use them?

Attitude and Planned Action - 2

Participant planned actions

What’s one thing you plan to do differently related to managing your finances after receiving this training?

Application - 3 Changes in behaviorWhat did you do differently after related to managing your finances after receiving the training?

Impact - 4 ImpactDid it impact the bottom line? Did you meet your ultimate goal?

24

What to Measure• Leading indicator examples:

– Number of borrowers and borrowed amounts.• Indiana University – 12% decrease in borrowing from 2012-13

to 2013-14.

– Number of SAP appeals (repeat vs. new).– Number of students retained from year to year.

• Discussion– What data might you have at your disposal that contains

leading indicators?– What new data could you collect? Remember to make it

measurable!

25

How to Measure• Again, review the SLO’s identified when building the

program– Implement assessment methods that will measure

whether or not the SLO’s were met• Pre-test and post-test• End of course survey

– Self reported data, but is still a good way to measure

• Student surveys at set times after the course, workshop or other training/teaching event

• Grades

– Information can also be used to fine tune the instructional methods

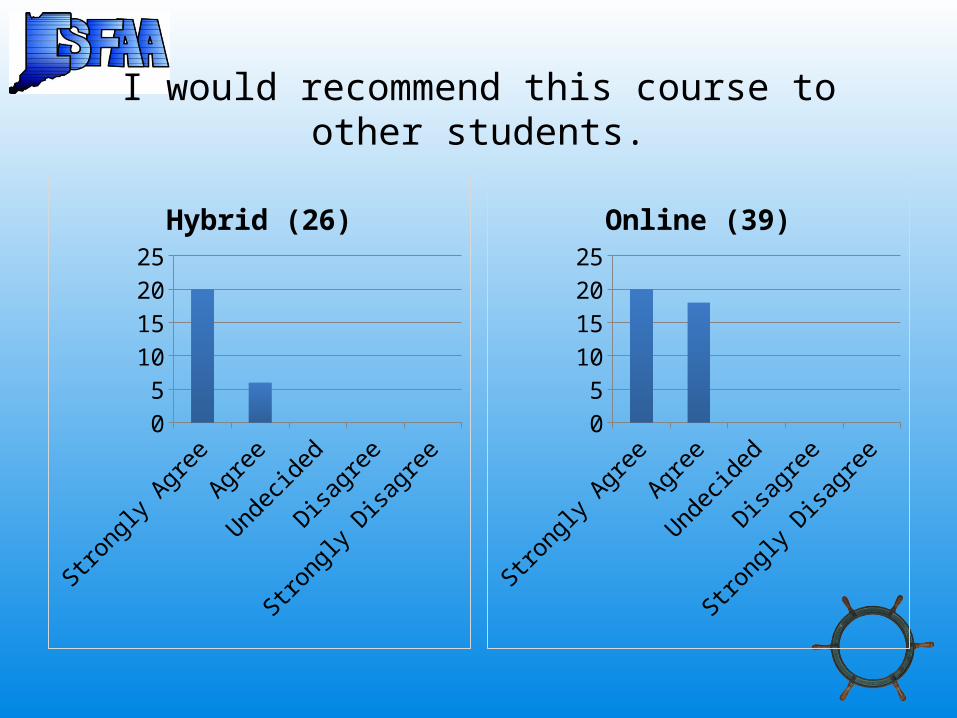

I would recommend this course to other students.

Strongly

Agree

Agree

Undecided

Disagre

e

Strongly

Disagre

e0

5

10

15

20

25

Hybrid (26)

Strongly

Agree

Agree

Undecided

Disagre

e

Strongly

Disagre

e0

5

10

15

20

25

Online (39)

Because of this course I am better able to manage my personal finances.

Strongly

Agree

Agree

Undecided

Disagre

e

Strongly

Disagre

e02468

101214

Hybrid (26)

Strongly

Agree

Agree

Undecided

Disagre

e

Strongly

Disagre

e0

5

10

15

20

25

Online (39)

I can develop and use a budget to plan for and keep track of my income vs. expenses.

Strongly

Agree

Agree

Undecided

Disagre

e

Strongly

Disagre

e02468

10121416

Hybrid (26)

Strongly

Agree

Agree

Undecided

Disagre

e

Strongly

Disagre

e0

5

10

15

20

25

Online (39)

I understand my student loan repayment options and how to select one that fits my financial situation.

Strongly

Agree

Agree

Undecided

Disagre

e

Strongly

Disagre

e02468

10121416

Hybrid (26)

Strongly

Agree

Agree

Undecided

Disagre

e

Strongly

Disagre

e0

4

8

12

16

20

Online (39)

30

Example Results: Life Skills• Nearly 728,000 courses completed by more than

214,000 students.• Average post-course assessment score: 88%• Immediate post-course survey (approx. 104,000

surveys):– Average student rating for usability, relevance and

satisfaction: 4.2 out of 5– Average knowledge before: 3.4– Average knowledge after: 4.4– Intent to change behavior: 94%

31

Example Results: Life Skills• Follow-up survey (approx. 13,300 surveys):

– 90% reported making a positive change in behavior• Top behavior changes reported:

– I consider if an item is a need or want before purchasing it and spend less on wants.

– I established educational, financial and/or career goals.– I researched and understand the requirements to complete my

program of study.– I avoid taking on additional debt unless I am sure I can afford

the payments.– I spend more time on activities that help me achieve my

educational, financial and career goals.

DISCUSSION/Q&A

33

Contact Info

Michele Wedel, Adjunct Instructor Kelley School of Business, IUPUI(317) [email protected]

Sara Wilson, USA Funds(317) [email protected]