Embed Size (px)

DESCRIPTION

Citation preview

Corporate Presenta,on February 22, 2011

2

The information in this document has been prepared as of February 9, 2011. Certain statements contained in this document constitute “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and forward looking information under the provisions of Canadian provincial securities laws. When used in this document, the words “anticipate”, “expect”, “estimate”, “forecast”, “will”, “planned”, and similar expressions are intended to identify forward-looking statements or information. Specifically, this presentation contains forward looking statements regarding the results and projections contained in the February 2011 technical report of the Haile Gold project, including the expected mine life, recovery, capital costs, cash operating costs and other costs and anticipated production of the described open pit mine, the projected internal rate of return, the projected payback period, the availability of capital for development, sensitivity to metal prices, ore grade, the reserve and resource estimates on the project, the financial analysis, the timing for completion of the revised feasibility study on the Haile Gold project, the timing and amount of future production, the timing of construction of the proposed mine and process facilities, capital and operating expenditures, the timing of the receipt of permits, rights and authorizations, communications with local stakeholders and community relations, availability of financing and any and all other timing, development, operational, financial, economic, legal, regulatory and political factors that may influence future events or conditions and expected drilling activities. In addition, this presentation also contains updated resource estimates contained in the February 2011 technical reports. Scientific and technical information referred herein has been extracted from and are hereby qualified in their entirety by reference to the aforementioned technical reports (“Technical Reports”). Joshua Snider, P.E., Thomas L. Drielick, P.E., Lee “Pat” Gochnour, M.M.S.A., John Marek, P.E. and Derek Wittwer, P.E. are responsible for preparing the Technical Reports. Each of the above referenced persons is a “qualified person” as defined in National Instrument 43-101 — Standards of Disclosure for Mineral Projects. Such forward‐looking statements are based on a number of material factors and assumptions, including, but not limited in any manner, those disclosed in any aother of Romarco’s public filings, and include the ultimate determination of mineral reserves and resources, availability and final receipt of required approvals, licenses and permits, sufficient working capital to develop and operate the proposed mine, access to adequate services and supplies, economic conditions, commodity prices, foreign currency exchange rates, interest rates, access to capital and debt markets and associated cost of funds, availability of a qualified work force, lack of social opposition and legal challenges, and the ultimate ability to mine, process and sell mineral products on economically favorable terms. While Romarco considers these assumptions to be reasonable based on information currently available to it, they may prove to be incorrect. Actual results may vary from such forward‐looking information for a variety of reasons, including but not limited to risks and uncertainties disclosed in other Romarco filings at www.sedar.com. Forward‐looking statements are based upon management’s beliefs, estimate and opinions on the date the statements are made and, other than as required by law, Romarco does not intend, and undertakes no obligation to update any forward‐looking information to reflect, among other things, new information or future events Cautionary Note to United States Investors Concerning Estimates of Measured, Indicated and Inferred Resources: Certain tables may use the terms “Measured”, “Indicated” and “Inferred” Resources. United States investors are advised that while such terms are recognized and required by Canadian regulations, however, the United States Securities and Exchange Commission does not recognize them. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or other economic studies. United States investors are cautioned not to assume that all or any part of Measured or Indicated Mineral Resources will ever be converted into Mineral Reserves. United States investors are also cautioned not to assume that all or any part of a Mineral Resource is economically or legally mineable.

All figures are US$ unless otherwise indicated

Cau,onary Statement

3

Introduc,on to the Haile Gold Mine Project

FEBRUARY 2011 § Feasibility completed

$275 million § One of lowest capital cost projects in industry

$379/oz ($347/oz first 5 years) § One of lowest operating cost projects in industry

2.06 g/t § One of highest grade open-pit projects in industry

4

Romarco – Company Overview

§ Romarco is a gold development company focused on produc,on primarily in the U.S.

§ The Company’s flagship project is the Haile Gold Mine in South Carolina ê Feasibility study completed ê Permits Pending ê System remains open in all direc6ons at depth

§ Experienced board, management & technical team

Company Descrip,on

Exchange/ Symbol TSX:R

Share Price(1) C$2.35

Shares Outstanding (Basic)(2) 483.5M

FD Shares Outstanding (TSM)(2) 516.5M

Market Capitaliza6on(1) C$1.14B

52 Week High / Low C$2.88 / C$1.53

Cash Balance (January 31, 2011) C$99.6M (1) As at close on February 22, 2011 (2) Calculated using treasury stock method. Includes 18.1 mm warrants and 15.0 mm opCons at

average strike price of C$0.60 and C$1.04 respecCvely as of January 31, 2011

Capitaliza,on Summary

Project Loca,on

181 Bay St. Suite 3630, Toronto, ON, M5J 2T3 │Email: [email protected] │Office: 416.367.5500 │Fax: 416.367.5505 │Website: www.romarco.com

Atlantic Ocean

SOUTH CAROLINA

GEORGIA

NORTH CAROLINA Charlotte

Myrtle Beach Columbia

Haile Mine

5

Mining Friendly Jurisdic,on with Excellent Infrastructure

§ South Carolina is a mining friendly state with a history of gold mining ê Loca6on of 1st gold rush (before California) ê Carolinas led U.S. gold produc6on un6l 1848 ê 2nd U.S. Mint in CharloUe, North Carolina ê Original 49ers came from east coast ê Significant gold produc6on in 80s – 90s ê Mining part of local history/community ê 500 ac6ve mines in South Carolina

§ Romarco controls 8,000+ acres of 100% private land ê Surface, mineral and water rights

Haile Project Loca,on

Tennessee

Kentucky West Virginia

North Carolina

Georgia

South Carolina

Russell Mine

Reed Mine

Howie Mine Brewer Mine

Ridgeway Mine Dorn Mine

Bante Mine Tathom Mine

Columbia Mine

Magruder Mine

Haile Mine

6

Investment Highlights

§ Near term, low cost gold producer with strong project economics

§ Located in a mining friendly jurisdic6on with excellent infrastructure

§ Large resource with significant remaining explora6on upside poten6al

§ Strong board, management and technical team

§ Clear plan to bring Haile into produc6on

§ Solid cash posi6on (~US$100 million), no debt – as of January 31, 2011

§ 11 drill rigs -‐ 172,000 meters drilling scheduled for 2011 (~US$30 million)

§ Haile system remains open in all direc6ons at depth

7

Resource Summary

Project Resource Gold Name Category Tonnes Grade Contained

000’s Mt g/t M oz Haile P&P(1) 30.509 2.06 2.018

M&I(2)(3) 53.378 1.82 3.123

Inferred(2) 24.944 1.34 1.072 (1) As per press release dated February 9, 2011; at US$950 gold (2) As per Technical Report dated December 14, 2010; at US$1200 gold (3) Includes Proven & Probable Reserve

In-‐Shell Resource / Reserve

$1200 Resource Shell

$950 Pit Feasibility

N$950 Pit area accounts for less than 10% of the Haile property.

601

Champion

Small

Chase Hill Ledbeher

South

Snake

Horseshoe

8

US$950 Gold -‐ Reserve Pits

§ Mineraliza,on exists outside & below US$950 reserve pits

§ Feasibility does not include ê Horseshoe ê Snake Deep ê West LedbeUer ê West South Pit ê 601

9

Near Term, Low Cost Gold Producer

§ Posi,ve feasibility study on Haile announced on Feb. 9, 2011

§ Strong project economics with robust IRR and NPV at conserva,ve gold prices ê Low cash cost opera6on ê Manageable, low cost capital requirements

§ Posi,ve feasibility study does not include ê Horseshoe zone ê Snake Deep ê West LedbeUer ê West South Pit ê 601 ê Inferred resources within US $950 Pit

§ Open all direc,ons and at depth § 2011 economic studies

ê Underground at Horseshoe ê Expansion ê Trade off

Summary of Haile Feasibility Study (US$950 Gold)

2 P Gold Reserves (‘000 oz) 2,018 Recovery Rate (%) 83.7 Net Recoverable Gold (‘000 oz) 1,681 Annual Mill Throughput (‘000 t) 2,555 Daily Mill Throughput (tpd) 7,000 Mine Life (years) 13.25 Overall Strip Ra6o (waste:ore) 7.2:1 Average Feed Grade to Mill (LOM) (g/t) 2.06 Average Produc6on (year 1) (‘000 oz) 172 Average Produc6on (years 1 -‐ 5) (‘000 oz) 150

Cash Costs (year 1-‐5) (US$/oz) 347 Cash Costs (LOM) (US$/oz) 379 Ini6al Capital Expenditures (US$M) 275.5 Sustaining Capital Expenditures (US$M) 119.2 Net Present Value (5% discount)

Pre-‐Tax (US$M) 279 Internal Rate of Return

Pre-‐Tax (%) 19.6

10

NPV & IRR Sensi,vity to Gold Price

Gold Price Per oz.

NPV @0% NPV @ 5% NPV @ 10% IRR % PAYBACK YEARS

$1500 $1,426 $930 $621 47.0% 2.0

$1400 $1,259 $811 $534 42.3% 2.2

$1300 $1,092 $693 $447 37.6% 2.4

$1200 $925 $575 $359 32.7% 2.7

$1100 $758 $457 $272 27.6% 3.1

$1000 $591 $339 $185 22.3% 3.8

$950 $507 $279 $141 19.6% 4.2

$800 $257 $102 $10 10.7% 7.6

$700 $90 -‐$16 -‐$77 4.0% 9.4

Pre-‐tax NPV and IRR Sensi,vity to Gold Price

($ Millions, except gold price)

11

Favourable Posi,on on the Cash Cost Curve

§ Haile life of mine cash costs of US$379/oz § Compares favourably with industry average

cash costs of US$572/oz in Q3 2010(1)

§ Posi,ons Romarco within the lowest quar,le on the cash cost curve

Industry Average Q3 2010 (1)

ROMARCO LOM Average (2)

Lowest Quar6le Average Q3 2010 (1)

(1) Source: GFMS presentation, Gold Survey 2010 Update

Average Cash Cost lowest quartile Q3 2010 (1)

(2) Announced February 9, 2011

12

Clear Plan to Bring Haile Into Produc,on

Design Overflow & Process Descrip,on

§ Conven,onal opera,on § Simple flowsheet § Off-‐the-‐shelf

technology § Ability to expand

project scale to include addi,onal resource discoveries

Design Overflow Process Descrip,on

§ Robust “Simple” Flowsheet Crush Æ Grind Æ Flota,on

§ Proven Technologies Regrind Flot Con Æ Leach Con

§ Flexible, Expandable Leach Flot Tail Æ Recover both

§ Non-‐Refractory CN Detox Æ Tail Storage Facility

§ Off-‐The-‐Shelf Technology Standard Carbon Elu,ons, EW

§ No Long Lead Time Units

13

Processing Plant (conceptual)

14

Site Layout

US$950 Pits

Overburden

Tailings Facility

Mill Site

15

Located in Mining Friendly Jurisdic,on

§ Strong State and local support for Haile ê Drill permits received in <2 weeks (650 holes)

ê No Federal, State or local opposi6on to date ê State offered tax incen6ves

• $3M in annual savings • Tax reduc6on from 10% to 4%

§ Permiung ê Federal (404) -‐ SUBMITTED

• Wetlands ê State (South Carolina)

• Mining / opera6ng permit – SUBMITTED - Water treatment permit - Storm water permit - Air permit

• Water (401) – SUBMITTED

Strong Community Rela,ons (July 4, 2010 Parade)

From leW to right: Diane GarreZ (CEO, Romarco), John SpraZ (South Carolina Congressman), Mick Mulvaney (South Carolina State Senator), Jack Estridge (City Counsel)

16

Located in Mining Friendly Jurisdic,on

§ Romarco con,nues to build strong local rela,onships and support ê High local unemployment ê Romarco hires locally

• 94 employees + 50 contractors ê $1 million/month spent locally

§ Outstanding Business Award (2010)

Ongoing Community Involvement Strong Community Support

17

Resource / Reserve Growth

§ Track record of con,nuing to grow resource base, con,nuity, and quality of ounces § 2010 Explora,on Highlights

ê Discovered Horseshoe, con6nuity between Snake & Horseshoe, high-‐grade Snake Deep, high-‐grade West LedbeUer, high-‐grade Mill Zone – extension of South Pit

§ Haile remains open in all direc,ons and at depth § 2011 – largest drill program to date

Note: All ounces stated in the table 3 above are contained ounces (1) Non 43-101 Historical Reserve in technical report filed July 17, 2007

* 2010 Resources are within a US$1200 Shell

(1)

Poten,al Mineral Deposits

18

Zone Scenario A

Tonnes x 1000 Scenario B

Tonnes x 1000 Case A g/t

Case B g/t

Horseshoe 16,511 13,956 3.39 2.09

LedbeUer 21,772 17,582 2.37 0.86

Snake 3,966 3,426 1.99 1.17

Chase Hill 1,633 1,515 1.06 0.93

Mill Zone 1,814 1,573 1.47 1.30

Small 5,039 4,149 0.65 0.62

601 Area 6,666 5,416 0.89 0.82

Champion 6,654 4,968 0.96 0.82

TOTAL 64,056 52,585 2.11 1.18

Poten,al Mineral Deposits (1)

(1) The resulting potential ranges of quantities and grades listed below are conceptual in nature based on geologic knowledge, interpretation and wireframes. There has been insufficient exploration to define a mineral resource and it is uncertain if further exploration will result in any of the targeted areas being delineated as a mineral resource. The Company currently plans to focus on further exploration drilling within these potential mineral deposits during 2011 and beyond.

§ Drill targets for 2011

Poten,al Mineral Deposits

19

601

Champion

Small

South

Snake

Ledbeher

Chase Hill

Horseshoe

PMD

PMD

PMD

PMD

PMD

PMD

Poten6al Mineral Deposits (PMD)

Surface

Mineraliza6on based on drilling

PMD

PMD

Significant Remaining Explora,on Upside Poten,al

§ 2010 drill program of 108,000m confirmed resource at Haile remains open along strike and at depth ê 40% of 2010 drilling focused on condemna6on drilling to locate suitable tailings site

2010 Highlights

§ M&I resources increased 44% § M&I grade increased 21% (to 1.82 g/t) § M&I tonnes increased 20% § Inferred resources declined 46%

ê Conversion to indicated § Inferred grade increased 33% (to 1.34 g/t) § 2P reserves increased 54%

2008 2009 2010 2011

20

21

Significant Remaining Explora,on Upside Poten,al

§ Large district land package with numerous untested zones along Haile gold trend

Haile Long Sec,on – Mineraliza,on based on drill data through September 30th 2010 US$950 GOLD

601 Champion Small South Ledbeher Snake Horseshoe

Snake Horseshoe

22

Significant Remaining Explora,on Upside Poten,al

§ Large district land package with numerous untested zones along Haile gold trend

Snake / Horseshoe Long Sec,on

US$950 PIT

US$1200 SHELL

Horseshoe Resource within US$1200 Shell

Measured & Indicated Inferred

380Koz 180Koz

23

Significant Remaining Explora,on Upside Poten,al

Upside From Mineraliza,on Not Captured

Deep Horseshoe Zone

§ Zone not yet drill defined along strike and down dip

§ Potential new zone may exist south of main Horseshoe/Snake trend

Snake Deep Zone

§ Mineralization encountered in down dip extensions of Snake deposit

§ Areas lie beneath the resource shell § Additional drilling is planned

West Ledbetter

§ Drill hole intercepts lie below the resource shell

§ Additional drilling is planned

West South Pit

§ Strike extends beyond the resource shell § Step-out drilling is planned to test extent

2010 Explora,on Findings

Horseshoe Discovery

§ Confirms underground potential § Highest grade § Underground economic study (2011)

South Pit § Extending to west and south § Higher grades encountered

Ledbetter § Extending to west and at depth § Higher grades

Snake § Extending at depth § Higher grades

Haile Corridor

§ Remains open § Connecting Horseshoe

24

Strong Board, Management and Technical Team § Proven gold mine development, finance, permiung and opera,ons experience

ê Romarco has the team in place to bring Haile into produc6on

Experienced Board of Directors Strong Management & Technical Team

Edward A. van Ginkel, Chairman § Consultant, former Noranda, Dayton Mining Diane R. Garreh § Former Dayton Mining, US Global Investors James R. Arnold § Former Freeport, Gold Fields – Richards Award Winner Leendert Krol § Former Brazuro, Newmont Don MacDonald § CFO QuadraFNX, former NovaGold, DeBeers, Dayton Mining John Marsden § Consultant, former Freeport – Richards Award Winner Patrick Michaels § Porqolio Manager – Zuri-‐invest, Switzerland Robert van Doorn § Former Mundoro, Rio Narcea, Morgan Stanley

Diane R. Garreh, Ph.D., President & CEO § Former Dayton Mining, US Global Investors James R. Arnold, Sr. VP, COO § Former Freeport, Gold Fields – Richards Award Winner Stan Rideout, Sr. VP, CFO § Former Phelps Dodge James Berry, Chief Geologist § Former Barrick Brent Anderson, Mine Manager § Former Quadra, Freeport Kevin Russel, Regional Geologist § Former Barrick Jim Wickens, Mill Manager § Former Barrick Oh Jackson, Health & Safety § Former Freeport Johnny Pappas, Environmental Manager § Former Freeport Ramona Schneider, Environmental Manager § Former Kinross Dan Symons, Manager Investor Rela,ons § Former Renmark Financial

25

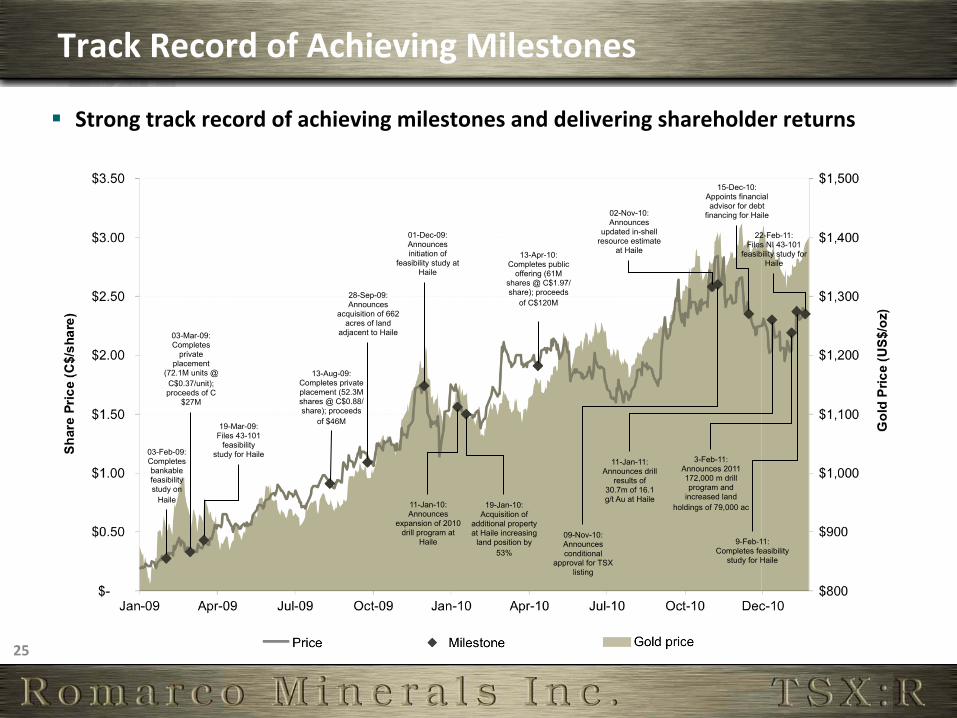

§ Strong track record of achieving milestones and delivering shareholder returns

Track Record of Achieving Milestones

03-Feb-09: Completes bankable feasibility study on

Haile

03-Mar-09: Completes

private placement

(72.1M units @ C$0.37/unit); proceeds of C

$27M

19-Mar-09: Files 43-101

feasibility study for Haile

13-Aug-09: Completes private placement (52.3M shares @ C$0.88/share); proceeds

of $46M

28-Sep-09: Announces

acquisition of 662 acres of land

adjacent to Haile

01-Dec-09: Announces initiation of

feasibility study at Haile

11-Jan-10: Announces

expansion of 2010 drill program at

Haile

19-Jan-10: Acquisition of

additional property at Haile increasing

land position by 53%

13-Apr-10: Completes public

offering (61M shares @ C$1.97/share); proceeds

of C$120M

02-Nov-10: Announces

updated in-shell resource estimate

at Haile

09-Nov-10: Announces conditional

approval for TSX listing

15-Dec-10: Appoints financial advisor for debt

financing for Haile

11-Jan-11: Announces drill

results of 30.7m of 16.1 g/t Au at Haile

3-Feb-11: Announces 2011 172,000 m drill program and

increased land holdings of 79,000 ac

22-Feb-11: Files NI 43-101

feasibility study for Haile

9-Feb-11: Completes feasibility

study for Haile

26

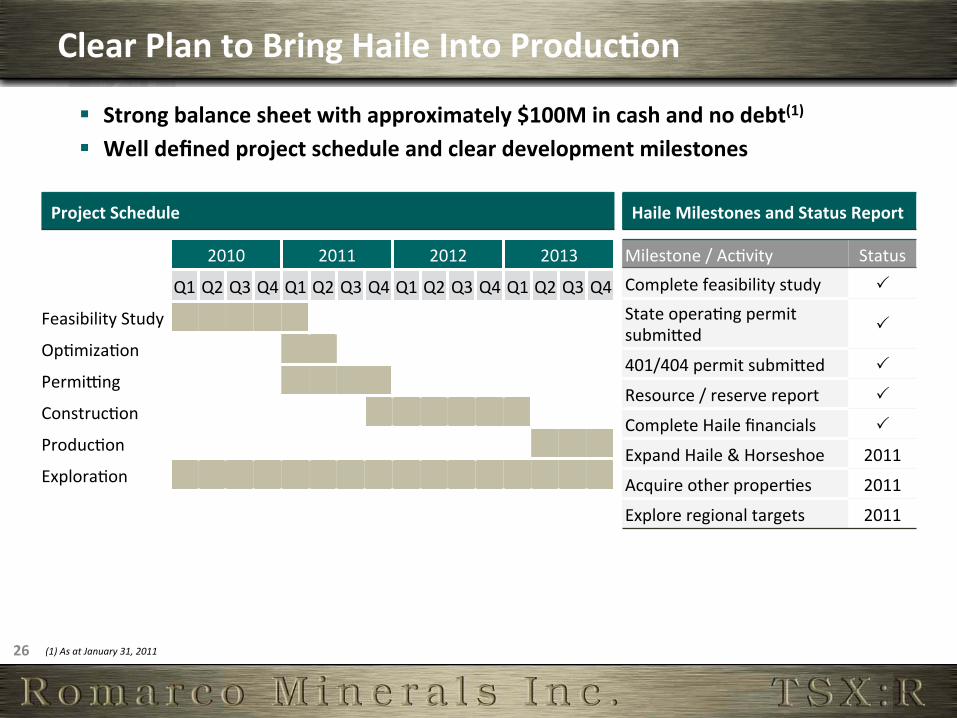

Clear Plan to Bring Haile Into Produc,on

§ Strong balance sheet with approximately $100M in cash and no debt(1)

§ Well defined project schedule and clear development milestones

Project Schedule Haile Milestones and Status Report

Milestone / Ac6vity Status Complete feasibility study State opera6ng permit submiUed

401/404 permit submiUed

Resource / reserve report

Complete Haile financials

Expand Haile & Horseshoe 2011

Acquire other proper6es 2011

Explore regional targets 2011

2010 2011 2012 2013

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Feasibility Study

Op6miza6on

Permirng

Construc6on

Produc6on

Explora6on

(1) As at January 31, 2011

27

Well-‐Posi,oned in Peer Group

§ Romarco trades at a discount to its developer peers on a P/NAV basis(1)

R-T

(1) Source: Wellington West Capital Markets

28

Volta

Vior

US Gold Corp

TemexRye Patch

Riverstone

Premier

Goldstone

Orezone

Northern FreegoldMidway

Coral

Keegan

Victoria

Grayd

Exeter

Cassidy

Belo Sun

Amarillo

Northern Gold

Andina

Osisko

Romarco

Rainy River

Detour

$0

$50

$100

$150

$200

$250

$300

0.0 0.5 1.0 1.5 2.0Gold Grade (g/t)

AMC / oz (U

S$/oz)

Well-‐Posi,oned in Peer Group

§ Romarco trades at a strong AMC(1)/oz mul,ple reflec,ng ê Large resource base at higher than average grade ê Rela6vely advanced stage of development with con6nued evidence of upside poten6al

Total Resources

25 Mozs

15 Mozs

5 Mozs

050100

150

200 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Gol

d G

rade

(g/t)

AMC / Oz (US$/oz)

1 Mozs

Peers

Selected Peers

AmarilloBelo Sun

CassidyExeter

Fronteer

Goldstone

Grayd

Int. Tower Hill

Keegan

Luna

Coral

Midway

Northern Freegold

Northern Gold

Orezone

PedimentPMI

Riverstone ResourcesRye Patch

Temex

US Gold Corp

Victoria

Vior

Volta Resources

Rainy River

Romarco

Detour

Osisko

Andina

$0

$50

$100

$150

$200

$250

$300

0.3 0.8 1.3 1.8 2.3Gold Grade (g/t)

EV /

Oz

(US$

/oz)

AmarilloBelo Sun

CassidyExeter

Fronteer

Goldstone

Grayd

Int. Tower Hill

Keegan

Luna

Coral

Midway

Northern Freegold

Northern Gold

Orezone

PedimentPMI

Riverstone ResourcesRye Patch

Temex

US Gold Corp

Victoria

Vior

Volta Resources

Rainy River

Romarco

Detour

Osisko

Andina

$0

$50

$100

$150

$200

$250

$300

0.3 0.8 1.3 1.8 2.3Gold Grade (g/t)

EV /

Oz

(US$

/oz)

Geography

West Africa, Australia, Mexico

North America, Chile, Brazil

050100

150

200 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Gol

d G

rade

(g/t)

AMC / Oz (US$/oz)

050100

150

200 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Gol

d G

rade

(g/t)

AMC / Oz (US$/oz)

050100

150

200 0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Gol

d G

rade

(g/t)

AMC / Oz (US$/oz)

Gold Explorers Compe,,ve Landscape

Source: RBC Equity Research, as of February 8, 2011 (1) Represents Adjusted Market CapitalizaCon (“AMC”) = Market CapitalizaCon plus Long-‐term Debt minus Working Capital

Torex

Queenston

PMI

Klondex

Guyana GF

2.0 6.0 10.0

Weighted Average Gold Grade: 1.38 g/t

Weighted Average: US$167/oz

29

Analyst Coverage

§ 6 Analysts Covering Romarco

ANALYSTS

Paradigm Capital $3.40

BMO Capital Markets $3.25

GMP Securi6es $3.10

RBC Capital Markets $3.00

Wellington West Capital Markets $2.90

CIBC World Markets $2.50

12 Month Target Price

Opportuni,es – Strip Ra,o

§ Current strip ra,o is 7.2:1 § If 5mt (1.1 g/t) of inferred within US$950 Pit is processed strip ra,o reduces to 6:1

§ Further reduc,ons are possible through: ê Remaining saddles between deposits through addi6onal drilling

ê Connec6ng mineraliza6on at depth between deposits

30

Wheel Loader

Hydraulic Front Shovel Haultruck

Opportuni,es – Expansion § 7000 tpd is PHASE 1 of Developing Haile § Expansion can come from:

ê Expansion of current reserves ê Underground ê Open-‐pit and underground ê New deposit ê One of our other regional proper6es

§ Tailings & Plant Site are designed to scale opera,ons from 7,000 to 20,000 tpd

SCALED FOR EXPANSION PHASE 1

7,000 tpd

10,000 tpd requires minimal modifica,ons

§ addi,onal crusher § flota,on cells

20,000 tpd mirror design of

10,000 tpd opera,on 14,000 tpd

mirror design of 7,000 tpd opera,on

31

32

Summary

§ Near term, low cost gold producer with strong project economics

§ Located in a mining friendly jurisdic6on with excellent infrastructure

§ Large resource with significant remaining explora6on upside poten6al

§ Expansion studies underway

§ Underground economic studies underway

§ Solid cash posi6on (~ US$100 million), no debt – as of January 31, 2011

§ 11 drill rigs – 172,000 meters drilling scheduled for 2011 (~US$30 million)

§ Permits submiUed and pending

33

Romarco Minerals Inc. Brookfield Place

181 Bay Street, Suite 3630 Toronto, Ontario M5J 2T3

Tel: 416.367.5500 Fax: 416.367.5505

Email: [email protected] Website: www.romarco.com

Dan Symons Manager, Investor Rela6ons [email protected]

Contact Informa,on Head Office Informa,on