Embed Size (px)

Citation preview

rics.org/standards

rics.org

RICS HQ

Parliament Square London SW1P 3ADUnited Kingdom

Worldwide mediaenquiries:

e pressoffi [email protected]

Contact Centre:

e [email protected] +44 (0)870 333 1600f +44 (0)20 7334 3811

Advancing standards in land, property and construction.

RICS is the world’s leading qualifi cation when it comes to professional standards in land, property and construction.

In a world where more and more people, governments, banks and commercial organisations demand greater certainty of professional standards and ethics, attaining RICS status is the recognised mark of property professionalism.

Over 100 000 property professionals working in the major established and emerging economies of the world have already recognised the importance of securing RICS status by becoming members.

RICS is an independent professional body originally established in the UK by Royal Charter. Since 1868, RICS has been committed to setting and upholding the highest standards of excellence and integrity – providing impartial, authoritative advice on key issues affecting businesses and society.

RICS is a regulator of both its individual members and fi rms enabling it to maintain the highest standards and providing the basis for unparalleled client confi dence in the sector.

RICS has a worldwide network. For further information simply contact the relevant RICS offi ce or our Contact Centre.

AsiaRoom 2203Hopewell Centre183 Queen’s Road EastWanchaiHong Kong

t +852 2537 7117f +852 2537 [email protected]

AmericasOne Grand Central Place60 East 42nd StreetSuite 2810New York 10165 – 2811USA

t +1 212 847 7400f +1 212 847 [email protected]

OceaniaSuite 2, Level 161 Castlereagh StreetSydney, NSW 2000Australia

t +61 2 9216 2333f +61 2 9232 [email protected]

Europe (excluding United Kingdom and Ireland)Rue Ducale 671000 BrusselsBelgium

t +32 2 733 10 19f +32 2 742 97 [email protected]

AfricaPO Box 3400Witkoppen 2068South Africa

t +27 11 467 2857 f +27 86 514 0655 [email protected]

Middle EastOffi ce G14, Block 3Knowledge VillageDubaiUnited Arab Emirates

t +971 4 375 3074f +971 4 427 [email protected]

India48 & 49 Centrum Plaza Sector RoadSector 53, Gurgaon – 122002India

t +91 124 459 5400f +91 124 459 [email protected]

United KingdomParliament SquareLondon SW1P 3ADUnited Kingdom

t +44 (0)870 333 1600f +44 (0)207 334 [email protected]

Ireland 38 Merrion SquareDublin 2Ireland

t +353 1 644 5500f +353 1 661 [email protected]

RICS Professional Guidance, England

1st edition, guidance note

Financial viability in planning

GN 94/2012

Financial viability in planningRICS guidance note

1st edition (GN 94/2012)

Published by the Royal Institution of Chartered Surveyors (RICS)

Surveyor Court

Westwood Business Park

Coventry CV4 8JE

UK

www.ricsbooks.com

No responsibility for loss or damage caused to any person acting or refraining from action as a result of the material included in thispublication can be accepted by the authors or RICS.

Produced by the Planning and Development Professional Group of the Royal Institution of Chartered Surveyors.

ISBN 978 1 84219 801 8

Royal Institution of Chartered Surveyors (RICS) August 2012. Copyright in all or part of this publication rests with RICS. No part of thiswork may be reproduced or used in any form or by any means including graphic, electronic, or mechanical, including photocopying,recording, taping or Web distribution, without the written permission of the Royal Institution of Chartered Surveyors or in line with the rulesof an existing license.

Typeset in Great Britain by Columns Design XML Ltd, Reading, Berks

Printed in Great Britain by Page Bros, Norwich

Contents

Acknowledgments ivRICS guidance notes 1Statement from Chair of Working Group 2Executive Summary 41 Introduction 6

1.1 Overview......................................................................................................................... 61.2 Viability in national planning policy context................................................................... 71.3 National Planning Policy Framework ............................................................................. 71.4 Community Infrastructure Levy Regulations.................................................................. 81.5 The use of viability appraisals in planning..................................................................... 8

2 Key features of a development viability assessment 102.1 Why are viability assessments important in planning? ................................................. 102.2 Appraisal framework ...................................................................................................... 112.3 Definition of Site value ................................................................................................... 122.4 Using a viability assessment to arrive at a professional judgment............................... 122.5 Indicative outline of what to include in a viability assessment ..................................... 13

3 Viability and Site Value benchmarks 153.1 Overview......................................................................................................................... 153.2 Model and approach...................................................................................................... 153.3 Developer’s return approach (where Site Value is a cost of development) .................. 153.4 Site Value approach (including an allowance for developer’s return as a cost of

development)..................................................................................................................17

3.5 Date of assessment ....................................................................................................... 193.6 Other material issues ..................................................................................................... 19

4 Further professional advice 234.1 Planning and viability ..................................................................................................... 234.2 Viability appraisals and evidence................................................................................... 234.3 Confidentiality................................................................................................................. 244.4 Mediation, expert determination and arbitration ........................................................... 244.5 Preparing and scrutinising a viability assessment......................................................... 25

Appendix A: Relevance of viability to planning 26Appendix B: Property market context overview 30Appendix C: Indicative outline of what to include in a viability assessment 32Appendix D: Refinements to viability methodology 34Appendix E: Application of underlying concepts within the guidance 37Appendix F: Glossary of terms 43Appendix G: FAQs for users of viability assessments 50References 55

FINANCIAL VIABILITY IN PLANNING | iii

Acknowledgments

This guidance was produced by the WorkingGroup supported by a consultant team.

Core Working Group

Simon Radford (Chair), Lothbury InvestmentManagement

Robert Fourt, Gerald Eve

Bruce Duncan, Huggins Edwards & Sharp

Nigel Jones, Chesterton Humberts

Charles Solomon, DVS

Jeremy Edge, Edge Planning and Development

Tony Mulhall, RICS

Consultants to the Working Group

GVA: Jacob Kut, Lorraine Hughes, StuartMorley

University of Reading: Neil Crosby, Peter Wyatt

Extended Working Group

Alan Gray, Planning Inspector

Simon Greenwood, Savills

Ben Hudson, Greenhill Brownfield

Georgiana Hibberd, RICS

In producing this guidance RICS hasundertaken extensive consultation with theplanning and development community in boththe public and the private sectors. A widerange of views was expressed and the workinggroup considered comments and submissionsfrom the following individuals and bodies.

We would like to express our thanks to all whoparticipated and state that inclusion in this listdoes not imply agreement with all aspects ofthe final guidance.

Arthur Whatling, RICS Red Book Editor;Graham Chase (Past President RICS); RobinPurchas QC; Homes and Communities Agency;Association of Chief Estates Surveyors; LawSociety; Royal Town Planning Institute; NationalHousing Federation; Planning Officers Society;Greater London Authority; Planning AdvisoryService; British Property Federation; PlanningInspectorate; Home Builders Federation;English Heritage; House Builders Association;Richard Asher, Jones Lang LaSalle; JamesBrown, Strutt & Parker; David Henry, Savills;Andrew Martinelli, Nottingham Trent University;Stephen Ashworth, SNR Denton; Tim Smith,Berwin Leighton Paisner; Michael Gallimore,Hogan Lovells; Simon Ricketts, SJ Berwin;Hugh Bullock, Gerald Eve; Yvonne Rydin,University College London; Michael Beaman,Michael Beaman Ltd.; Janet Montgomery,Brimble, Lea & Partners; Janice Morphet,University College London; Dominic Williams,Hewdon Consulting; Lawrence Chadwick; PeterMail, Land Securities; John Oldham,Countryside Properties; Kathleen Dunmore, 3Dragons; Anthony Lee, BNP Paribas RealEstate; Richard Wickins, Savills; AndrewGolland, Three Dragons (AG) Ltd; ChrisCobbold, DTZ; Keith Thomas, AECOM; GeraldHarford, Chesterton Humberts; Nicholas Falk,Urbed; Nigel Hawkey, Quintain.

iv | FINANCIAL VIABILITY IN PLANNING

RICS guidance notes

This is a guidance note. Whererecommendations are made for specificprofessional tasks, these are intended torepresent ‘best practice’, i.e.recommendations which in the opinion ofRICS meet a high standard of professionalcompetence.

Although members are not required to followthe recommendations contained in the note,they should take into account the followingpoints.

When an allegation of professional negligenceis made against a surveyor, a court or tribunalmay take account of the contents of anyrelevant guidance notes published by RICS indeciding whether or not the member had actedwith reasonable competence.

In the opinion of RICS, a member conformingto the practices recommended in this noteshould have at least a partial defence to anallegation of negligence if they have followedthose practices. However, members have theresponsibility of deciding when it isinappropriate to follow the guidance.

It is for each surveyor to decide on theappropriate procedure to follow in anyprofessional task. However, where members donot comply with the practice recommended inthis note, they should do so only for a goodreason. In the event of a legal dispute, a courtor tribunal may require them to explain whythey decided not to adopt the recommendedpractice. Also, if members have not followedthis guidance, and their actions are questionedin an RICS disciplinary case, they will be askedto explain the actions they did take and thismay be taken into account by the Panel.

In addition, guidance notes are relevant toprofessional competence in that each membershould be up to date and should haveknowledge of guidance notes within areasonable time of their coming into effect.

Document status defined

RICS produces a range of standards products.These have been defined in the table below.This document is a guidance note.

Type of document Definition StatusRICS practice statement Document that provides members with

mandatory requirements under Rule 4 of theRules of Conduct for members

Mandatory

RICS code of practice Standard approved by RICS, and endorsedby another professional body that providesusers with recommendations for acceptedgood practice as followed by conscientiouspractitioners

Mandatory orrecommended goodpractice (will beconfirmed in thedocument itself)

RICS guidance note Document that provides users withrecommendations for accepted goodpractice as followed by competent andconscientious practitioners

Recommended goodpractice

RICS information paper Practice based information that providesusers with the latest information and/orresearch

Information and/orexplanatorycommentary

FINANCIAL VIABILITY IN PLANNING | 1

Statement from Chair of Working Group

Financial viability has become an increasinglyimportant material consideration in the planningsystem. While the fundamental purpose ofgood planning extends well beyond financialviability, the capacity to deliver essentialdevelopment and associated infrastructure isinextricably linked to the delivery of land andviable development.

The Government’s recent National PlanningPolicy Framework (NPPF) emphasisesdeliverability and the provision of competitivereturns to willing land owners and developersto enable sustainable development to comeforward. This guidance note seeks to elaborateon how this can be achieved.

RICS acknowledges that the planning authorityis responsible for promoting policies forsustainable development and for decisiontaking on schemes based on their compliancewith sustainable development policies. We alsorecognise that where development proposalscan not be made to comply with sustainabledevelopment policies, the planning authoritymay refuse planning permission.

The NPPF sets out to achieve growth throughattracting investment and implementing plans.This guidance note starts from the premise thatthe private sector will continue to be reliedupon to deliver the majority of commercial,residential and mixed-use developments,together with consequential planningobligations. It further recognises thatdevelopment for which there is no plausiblebusiness case, on viability grounds or for otherreasons, will not take place which is clearlyrecognised in the NPPF. A sharedunderstanding of development viability forplanning purposes by all those involved is,therefore, essential to achieve consistency inboth approach and assessment.

Throughout the guidance we refer to themarket value which is a key benchmark to

investors in all areas of land transactions,development and investment. Whetherinvestors are using their own funds or arerelying on borrowings, their assessment ofviability will be based on obtaining a marketrisk adjusted return having regard to prevailingmarket conditions. Plan implementation andplanning objectives are delivered throughdevelopment projects which in turn need toachieve a competitive return. In this way planviability and delivery are closely linked to themarket.

The purpose of this guidance note is to enableall participants in the planning process to havea more objective and transparent basis forunderstanding and evaluating financial viabilityin a planning context. Arriving at an outcomewhich is satisfactory for all should be mucheasier where there is an agreed framework andbasis for evaluation. It is acknowledged thatthe market is constantly moving, however theprinciples set out in the guidance should beapplicable in all states of the economy andproperty sector.

While this guidance note provides practitionerswith advice in undertaking and assessingviability appraisals for planning purposes, it willalso be helpful to users of these assessments,be they planners, developers, investors,landowners, interested parties, individuals orcommunity groups.

Financial viability assessments for planningpurposes should be approached on anobjective and best practice basis to the extentthat the conclusions are capable of unbiasedobjective scrutiny. This may occur during allstages of the development managementprocess, including to an appeal at a publicinquiry, or, in the case of policy making,through to an examination in public.

The guidance note sets out a methodologyframework and set of principles for financial

2 | FINANCIAL VIABILITY IN PLANNING

viability in planning. These have beenformulated mainly for developmentmanagement purposes at a scheme-specificlevel but the principles apply equally to planmaking and to the viability testing thatunderpins Community Infrastructure Levy (CIL)charging schedules (area wide viability studies).

We have consulted widely within the industry inproducing the guidance note. It isfundamentally grounded in the statutory andregulatory planning regime as it should operatein England. We have deliberately avoidedreference to planning appeals and case lawwhere viability has been an issue, given thelack of previous guidance in this area fordecision makers to refer to and rely upon informulating their views. It will, however, beapparent that elements of the guidance closelyreflect certain decisions as financial viability inplanning has evolved.

The guidance note, for the first time, definesfinancial viability for planning purposes;separating the key functions of development,being land delivery and viable development (inaccordance with the NPPF). It highlights theresidual appraisal methodology; defines SiteValue for both scheme-specific and area-widetesting in a market rather than hypotheticalcontext; indicates what to include in viabilityassessments; defines terminology andsuggested protocols, and explains the uses offinancial viability assessments in planning.

The guidance note is also consistent with andhas regard to the recently released NPPF.

Importantly the guidance note does not seek tointroduce new approaches to such matters asSite Value, for example. Well understood andrecognised terminology and definitions arehighlighted and clarification provided within thecontext of the guidance.

This guidance note is divided into varioussections to assist both practitioners and users.Sections 1 and 2 and accompanyingappendices A, B, C, F and G should assistusers of viability assessments, but alsocontains important guidance for practitioners.Section 3 and accompanying appendices Dand E are principally aimed at practitioners.Section 4 provides further professional advice

on the production of viability assessments forboth users and practitioners. Appendix Gprovides a summary of FAQs together withreferences to various parts of the guidance.The guidance note proper starts with anexecutive summary which follows thisstatement and highlights a number of its keyaspects.

The working party wishes to highlight that it isnot the purpose of this guidance note to tellpractitioners how to carry out a financialviability assessment. This will inevitably vary ineach instance. The guidance, however,provides a framework, methodology andprinciples to apply, without seeking to beprescriptive. The guidance note, for example,does not suggest a particular financial model,ranges of input/benchmark outcomes, etc. It isup to the practitioners to advise accordingly ineach case. It is also intended that a ‘ViabilityCommunity’ will be established online by RICSto facilitate continued debate in this importantarea.

It is stressed that this guidance noteencourages practitioners at all times to bereasonable and objective in their approach,whether undertaking viability assessments orscrutinising them, and, where possible, to seekto resolve differences of opinion in order toassist the planning process where it is relyingon financial viability as a material consideration.

Finally, I would like to thank the consultants tothe working group, GVA and the University ofReading; my fellow members of the workinggroup and all those who contributed andprovided comments in producing this guidancenote.

Simon Radford, ChairRICS Working GroupFinancial Viability in Planning

FINANCIAL VIABILITY IN PLANNING | 3

Executive Summary

The guidance note provides all those involvedin financial viability in planning and relatedmatters with a definitive and objectivemethodology framework and set of principlesthat can be applied mainly to developmentmanagement. The principles are howeverapplicable to the plan making and CIL (area-wide) viability testing.

The National Planning Policy Framework(NPPF) sets out to achieve growth throughattracting investment and development. RICSacknowledges that the planning authority isresponsible for promoting policies forsustainable development. We also recognisethat where development proposals can not bemade to comply with sustainable developmentpolicies the planning authority may be obligedto refuse planning permission.

The guidance note is grounded in the statutoryand regulatory planning regime that currentlyoperates in England. It is consistent with theLocalism Act 2011, the NPPF and CommunityInfrastructure Levy (CIL) Regulations 2010.

The most common uses for financial viabilityassessments as set out in this guidance noteare for development management (includingaffordable housing, enabling development, landuse, Section 106 Agreement planningobligations) and plan making (policy and CILviability testing).

Financial viability for planning purposes isdefined by this guidance as follows:

An objective financial viability test of theability of a development project to meet itscosts including the cost of planningobligations, while ensuring an appropriateSite Value for the landowner and a marketrisk adjusted return to the developer indelivering that project.

(Where viability is being used to test andinform planning policy it will be necessaryto substitute ‘a development project’ intothe wider context)

The guidance note separates the two keycomponents of development: land delivery andviable development. This is in accordance withthe NPPF. Fundability is also an intrinsicelement of both.

The residual appraisal methodology for financialviability testing is highlighted where either thelevel of return or residual Site Value can be aninput and the consequential output (either aresidual land value or return respectively) canbe compared to a benchmark to assess theimpact of planning obligations or policyimplications on viability.

The guidance note does not recommend anyparticular financial model (bespoke orotherwise) or provide indications as to inputs oroutputs commonly used. It is up to thepractitioner in each case to adopt and justify asappropriate.

Site Value, either as an input into a scheme-specific appraisal or as a benchmark, isdefined in the guidance note as follows:

Site Value should equate to the marketvalue1 subject to the following assumption:that the value has regard to developmentplan policies and all other materialplanning considerations and disregardsthat which is contrary to the developmentplan.

When undertaking Local Plan or CIL (area-wide)viability testing, a second assumption needs tobe applied to the Site Value definition:

The Site Value (as defined above) mayneed to be further adjusted to reflect theemerging policy/CIL charging level. The

4 | FINANCIAL VIABILITY IN PLANNING

level of the adjustment assumes that sitedelivery would not be prejudiced. Wherean adjustment is made, the practitionershould set out their professional opinionunderlying the assumptions adopted.These include, as a minimum, commentson the state of the market and deliverytargets as at the date of assessment.

The guidance note encourages practitioners tobe reasonable, transparent and fair inobjectively undertaking or reviewing financialviability assessments. Where possible,practitioners should seek to resolve differencesof opinion.

In undertaking scheme-specific viabilityassessments, the nature of the applicantshould normally be disregarded, as shouldbenefits or disbenefits that are unique to theapplicant. The aim should be to reflect industrybenchmarks in both development managementand plan making viability testing.

Viability assessments will usually be datedwhen an application is submitted, or when aCIL charging schedule or local plan ispublished in draft; exceptions to this may bepre-application submissions and appeals.Viability assessments may occasionally need tobe updated due to market movements duringthe planning process.

The guidance note highlights where re-appraisals, i.e. viability reviews prior to schemeor phase implementation, or projection (growth)models may be appropriate as an alternative tocurrent day methodologies. It is assumed thatfor CIL charging schedules and local plantesting this will be undertaken on a current daybasis, subject to suitable margins/buffers.

It is strongly recommended that financialappraisals are sensitivity tested as a minimum,and with more complex schemes furtherscenario/simulation analysis should also beundertaken. This is to ensure that a soundjudgment can be formulated on viability.

The guidance note sets out what shouldusually be included in viability assessments,common terminology and definitions, togetherwith additional technical guidance forpractitioners.

Confidentiality protocols and suggested non-binding mediation/arbitration mechanisms forresolving disputes are set out in the guidancenote.

FINANCIAL VIABILITY IN PLANNING | 5

1 Introduction

Key issues: purpose of the guidance note;viability context in national and localplanning policy; use of viability appraisals inplanning, and an effective framework forviability testing.

1.1 Overview1.1.1 This guidance note provides all thoseinvolved in financial viability in planning andrelated matters with a definitive and objectivemethodology framework and set of principlesfor application to development management.

Box 1: Purpose of the guidance noteThe guidance note provides all thoseinvolved in financial viability in planning andrelated matters with a definitive andobjective methodology framework and set ofprinciples primarily for application todevelopment management.

1.1.2 The motivation for undertaking thisguidance note arose from the gap (partly as aresult of a lack of clear published guidance)that often occurs between what local planningauthorities consider viable to provide, and whatdevelopment proposals are actually capable ofsupporting financially, in terms of planningobligations, while seeking to meet policyrequirements. This does not just relate to the‘development management’ stage of theplanning process where section 106agreements are negotiated, but also to thebeginning of the spatial planning processwhere policy is formulated in local developmentplan documents. Viability is also relevant tolocal planning authorities when draftingCommunity Infrastructure Levy (CIL) chargingschedules. The Local Housing Delivery Grouprecently published advice on area-wide viabilitytesting entitled ‘Viability Testing Local Plans’.Both this and the RICS guidance can be seenas complementary. The RICS provides

significantly more technical guidance (seesection 3 of this guidance) on arriving at SiteValue and therefore meeting NPPF compliance,with regard to this matter, than the LHDGadvice which focuses more on policy andprocess.

1.1.3 The importance of enabling sustainabledevelopment has been underlined in theNational Planning Policy Framework. This RICSguidance recognises the role of the planningauthority in achieving sustainable developmentand supports the implementation ofdevelopment plans. The guidance does notseek to determine policy. It sets out to bringclarity to the decision making by facilitatingevaluation of the critical elements that mayimpact on viability and therefore delivery in anopen and explicit way.

1.1.4 The guidance aims to satisfy thefollowing requirements:

+ outline the statutory/regulatory/policybackground in considering viabilityassessments in a town planning context

+ clearly define terminology in a way that isconsistent with existing RICS usage

+ clearly define financial viability in thecontext of planning and development

+ enable an objective evaluation of financialviability to be made

+ set down the parameters within whichissues of financial viability are to beconsidered

+ establish the principles upon which thesewill be evaluated

+ be applicable at all stages in the economiccycle; and

+ be applicable to all scales of site whethergreenfield or urban.

1.1.5 The intention of this guidance note is toprovide local planning authorities, developers,investors, land owners, interested parties,

6 | FINANCIAL VIABILITY IN PLANNING

individuals or community groups and allprofessionals, including chartered surveyors,with definitive and impartial objective guidanceon viability in a development management andplan making context. In respect of developmentmanagement, this includes evaluating theimpact of planning obligations, includingaffordable housing and other section 106requirements, CIL including the application oftariffs/levies, and planning policy, on thefinancial viability of a proposed development.While the focus of this guidance is on thedevelopment management stage, dealing withsite specific applications, the principles can beapplied equally to area-wide viability in respectof local plans and CIL charging schedules.

1.2 Viability in nationalplanning policy context1.2.1 While always central in the developmentprocess, viability has become an increasinglyimportant consideration in town planning.Whether preparing policy or considering aspecific proposal scheme, viability is inherentlylinked to the ability to satisfy planning policy,and to deliver regeneration objectives andeconomic development. The significance ofviability has increased during periods ofeconomic downturn when the delivery of newdevelopment has been threatened and therelative burden of planning obligations andpolicy requirements on developers andlandowners has increased. Striking the rightbalance to deliver development in the rightplace at the right time is, therefore, essential.

1.2.2 In undertaking development, the privatesector is often called upon by local planningauthorities (LPAs) to deliver and/or contributetowards the provision of infrastructure andmitigate potential harm arising from a proposeddevelopment. Scheme viability is a materialconsideration in deciding the appropriate levelof contribution. It is important, therefore, forLPAs to have a greater understanding ofviability as it is relevant to planning in both theformulation of planning policy, as well as in thedetermination of planning applications. In theformer, the emphasis is upon deliverability ofan authority’s vision/infrastructure or

community requirements during the planperiod; the latter relates to an authority’swillingness to allow a scheme to proceed afterrelaxation of policy and/or planning obligationsin the context of viability. A full assessment ofthe implications for planning is provided inAppendix A and a summary is provided in 1.3.

1.2.3 Reference is made throughout thisguidance note to national planning guidanceset out in the NPPF, the CIL Regulations andother relevant national policy.

1.3 National Planning PolicyFramework1.3.1 In the context of achieving sustainabledevelopment the Draft NPPF refers to ensuringviability and deliverability at sections 173–177.

… To ensure viability, the costs of anyrequirement likely to be applied todevelopment, such as requirements foraffordable housing, standards, infrastructurecontributions or other requirements should,when taking into account of the normal costof development and mitigation, providecompetitive returns to a willing land ownerand willing developer to enable thedevelopment to be deliverable

(NPPF, 2012, paragraph 173)

1.3.2 The NPPF also refers to the use ofplanning conditions and obligations at sections203–206 and advises that where obligations arebeing sought:

…local planning authorities should takeaccount of changes in market conditionsover time and, wherever appropriate, besufficiently flexible to prevent planneddevelopment being stalled.

(NPPF, 2012, paragraph 205)

1.3.3 This RICS guidance fully recognises thewider role of the planning authority in achievingsustainable development and that the planningauthority may refuse planning permission inorder to achieve its objectives.

FINANCIAL VIABILITY IN PLANNING | 7

1.4 Community InfrastructureLevy Regulations1.4.1 Since April 2010, the tests fordetermining the lawfulness of planningobligations are set out in regulation 122 of theCommunity Infrastructure Levy Regulations2010. The 2010 Regulations provide that aplanning obligation may only constitute areason for granting planning permission if it is:(a) necessary to make the developmentacceptable in planning terms; (b) directlyrelated to the development; and (c) fairly andreasonably related in scale and kind to thedevelopment. These three prerequisites are thesame as three of the five policy tests forplanning obligations in Annex B to Circular 05/2005.

1.4.2 CIL should be set at a level that assumesthe development plan requirements are beingdelivered and not prejudiced. Also, in setting anappropriate CIL, a local authority as thedecision maker may conclude it is acceptablethat some development will not be viable.Further background information on the CILRegulations and other relevant planningconsiderations upon which this guidance notehas been based are set out in Appendix A.

Box 2: Legal and policy basisThe guidance note is grounded in thestatutory and regulatory planning regime thatcurrently operates in England. It is consistentwith the Localism Act 2011, NationalPlanning Policy Framework of 2012 andCommunity Infrastructure Levy (CIL)Regulations 2010.

1.5 The use of viabilityappraisals in planning1.5.1 Viability appraisals may be used inconnection with a number of planning-relatedissues in respect of both policy assessmentand development control. It is usual to apply a‘reasonableness’ test in development control;this may take the form, for example, of themaximum reasonable amount of affordablehousing in terms of the economic viability of adevelopment. Reasonableness should be

considered of utmost importance in allinstances where viability appraisals areundertaken. In certain instances, financialviability may also be relevant in the context ofseeking to depart from planning policy. This isemphasised in paragraph 187 of the NPPF.

1.5.2 The most common uses of viabilityappraisals include:

+ assessing the nature and level of planningobligation contributions/requirements

+ establishing the level of affordable housing

+ identifying the split between affordablehousing tenures

+ establishing off-site affordable housinglevels including the quantification ofoverprovision and affordable housingcredits

+ assessing contributions in lieu payments foraffordable housing

+ the timing of planning obligationscontributions and affordable housingdelivery

+ applications incorporating enablingdevelopment

+ assessing the bulk, scale and massing (andspecification relative to cost and value) of aproposed scheme

+ reviewing land uses

+ assessing continuing existing uses in termsof obsolescence and depreciation

+ dealing with heritage assets andconservation issues

+ formulating planning policy through localdevelopment plans; and

+ consideration by local authorities whendrafting and viability testing CIL chargingschedules.

8 | FINANCIAL VIABILITY IN PLANNING

Box 3: Uses of viability assessmentsThe most common uses for financial viabilityassessments as set out in the guidance noteare for development management (includingaffordable housing, enabling development,land use, section 106 Agreement planningobligations) and plan making (policy and CILviability testing). The guidance note has aparticular focus on developmentmanagement (scheme specific assessments)although the principles set out are equallyapplicable to plan making and CIL (area-wide) viability testing.

1.5.3 In many instances a viability assessmentwill have regard to not just single policyimpacts but a cumulative impact of policy andplanning obligations as illustrated in figure 1.

1.5.4 This guidance note is intended to providean effective framework within which financialviability may be assessed, having regard to theregulatory regime in place and at whateverstage of the economic cycle the evaluation isbeing carried out (Appendix B provides aproperty market context overview). It seeks toprovide a rigorous approach to evaluatingfinancial viability and reaching an appropriateprofessional judgment in the context ofassessing the introduction of planningobligations, formulating planning policy andestablishing CIL charging schedules.

Figure 1: Cumulative impact of policy and planning obligations

FINANCIAL VIABILITY IN PLANNING | 9

2 Key features of a development viabilityassessment

Key issues: definition of viability for planningpurposes; an appraisal framework; definitionof Site Value for scheme specific appraisalsand area wide studies; using a viabilityassessment to arrive at a professionaljudgment; and indicative outline of what toinclude in a viability assessment.

2.1 Why are viabilityassessments important inplanning?2.1.1 Viability, in the context of undertakingappraisals of financial viability for the purposesof town planning decisions, can be defined as:

An objective financial viability test of theability of a development project to meet itscosts including the cost of planningobligations, while ensuring an appropriateSite Value for the landowner and a marketrisk adjusted return to the developer indelivering that project.

(Where viability is being used to test and informplanning policies or CIL charging schedules, itwill be necessary to substitute ‘project’ in tothe wider context of development for whichviability is being assessed).

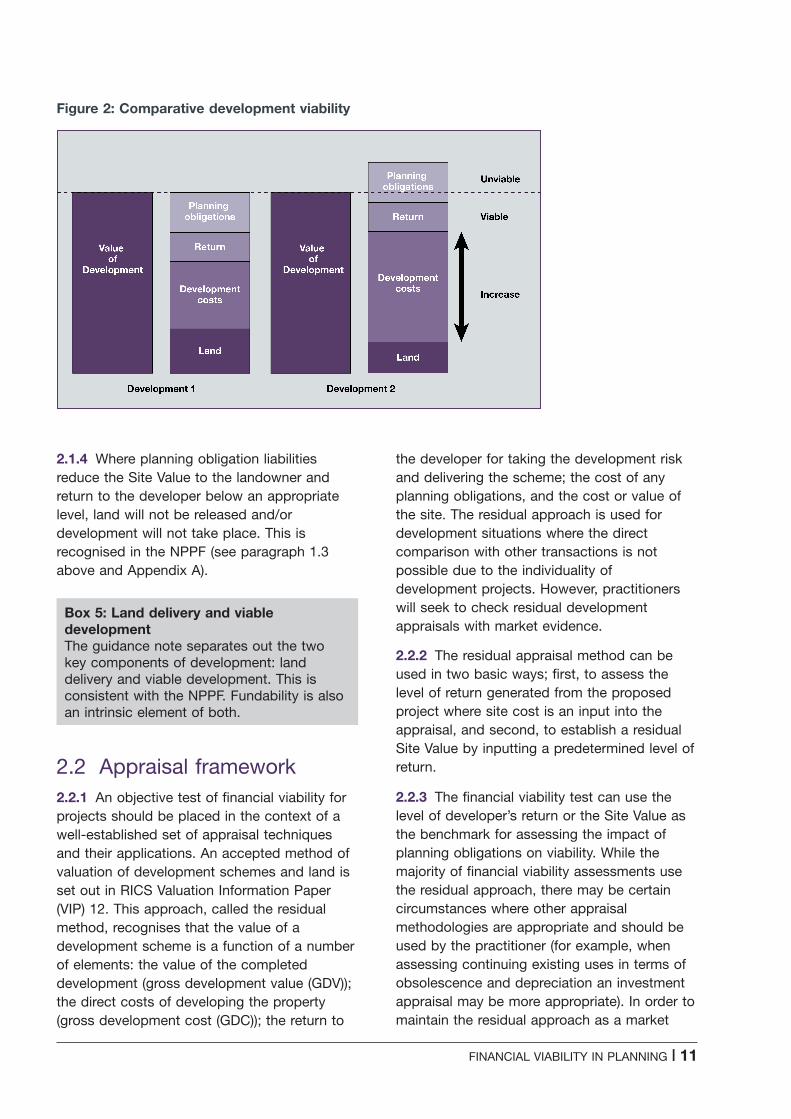

2.1.2 The fundamental issue in consideringviability assessments in a town planningcontext is whether an otherwise viabledevelopment is made unviable by the extent ofplanning obligations or other requirements. Thisis illustrated in figure 2 (opposite) in terms ofcomparative development viability. As can beseen, the development economics of Scenario1 is such that policy can be met in deliveringall planning obligations while meeting a SiteValue for the land, all other development costsand a market risk adjusted return for thedevelopment. In this case it is unlikely a

financial viability assessment would berequired. Under Scenario 2, costs haveincreased, while development values haveremained static. In arriving at Site Value, thedevelopment return, and the ability to meet theplanning obligations, a financial viabilityassessment would be required to objectivelyresolve what could viably deliver thedevelopment while meeting the viabilitydefinition in 2.1.1. It follows, for example, thatland value is flexible and not a fixed figure tothe extent that Site Value has to be determinedas part of the viability assessment.

Box 4: Financial viability definitionFinancial viability for planning purposes isdefined as follows:‘An objective financial viability test of theability of a development project to meet itscosts including the cost of planningobligations, while ensuring an appropriateSite Value for the landowner and a marketrisk adjusted return to the developer indelivering that project.’2

2.1.3 A proper understanding of financialviability is essential in ensuring that:

+ land is willingly released for developmentby landowners

+ developers are capable of obtaining anappropriate market risk adjusted return fordelivering the proposed development

+ the proposed development is capable ofsecuring funding

+ assumptions about the quantum ofdevelopment that can be viably deliveredover the course of the plan period arerobust; and

+ CIL charging schedules are set at anappropriate level.

10 | FINANCIAL VIABILITY IN PLANNING

Figure 2: Comparative development viability

2.1.4 Where planning obligation liabilitiesreduce the Site Value to the landowner andreturn to the developer below an appropriatelevel, land will not be released and/ordevelopment will not take place. This isrecognised in the NPPF (see paragraph 1.3above and Appendix A).

Box 5: Land delivery and viabledevelopmentThe guidance note separates out the twokey components of development: landdelivery and viable development. This isconsistent with the NPPF. Fundability is alsoan intrinsic element of both.

2.2 Appraisal framework2.2.1 An objective test of financial viability forprojects should be placed in the context of awell-established set of appraisal techniquesand their applications. An accepted method ofvaluation of development schemes and land isset out in RICS Valuation Information Paper(VIP) 12. This approach, called the residualmethod, recognises that the value of adevelopment scheme is a function of a numberof elements: the value of the completeddevelopment (gross development value (GDV));the direct costs of developing the property(gross development cost (GDC)); the return to

the developer for taking the development riskand delivering the scheme; the cost of anyplanning obligations, and the cost or value ofthe site. The residual approach is used fordevelopment situations where the directcomparison with other transactions is notpossible due to the individuality ofdevelopment projects. However, practitionerswill seek to check residual developmentappraisals with market evidence.

2.2.2 The residual appraisal method can beused in two basic ways; first, to assess thelevel of return generated from the proposedproject where site cost is an input into theappraisal, and second, to establish a residualSite Value by inputting a predetermined level ofreturn.

2.2.3 The financial viability test can use thelevel of developer’s return or the Site Value asthe benchmark for assessing the impact ofplanning obligations on viability. While themajority of financial viability assessments usethe residual approach, there may be certaincircumstances where other appraisalmethodologies are appropriate and should beused by the practitioner (for example, whenassessing continuing existing uses in terms ofobsolescence and depreciation an investmentappraisal may be more appropriate). In order tomaintain the residual approach as a market

FINANCIAL VIABILITY IN PLANNING | 11

based exercise, as the NPPF also advocatesthrough seeking a competitive return, it will beimportant to both benchmark and have regardto the available comparable market basedevidence. The practitioner may have to analyseand form a judgment on this evidence asappropriate to the circumstances.

Box 6: Residual appraisalThe residual appraisal methodology forfinancial viability testing is normally used,where either the level of return or Site Valuecan be an input and the consequentialoutput (either a residual land value or returnrespectively) can be compared to abenchmark having regard to the market inorder to assess the impact of planningobligations or policy implications on viability.

2.3 Definition of Site Value2.3.1 Site Value either as an input into ascheme-specific appraisal or as a benchmarkis defined as follows:

Site Value should equate to the marketvalue3 subject to the following assumption:that the value has regard to developmentplan polices and all other material planningconsiderations and disregards that which iscontrary to the development plan.

2.3.2 Any assessment of Site Value, however,will have regard to prospective planningobligations and the point of the viabilityappraisal is to assess the extent of theseobligations while also having regard to theprevailing property market. This point isdiscussed further in Section 3.

Box 7: Site Value definitionSite Value either as an input into a schemespecific appraisal or as a benchmark isdefined in the guidance note as follows:‘Site Value should equate to the marketvalue4 subject to the following assumption:that the value has regard to developmentplan policies and all other material planningconsiderations and disregards that which iscontrary to the development plan.’

2.3.3 When undertaking Local Plan or CIL(area-wide) viability testing, a secondassumption needs to be applied to thedefinition of Site Value in 2.3.1:

Site Value (as defined above) may need tobe further adjusted to reflect the emergingpolicy/CIL charging level. The level of theadjustment assumes that site delivery wouldnot be prejudiced. Where an adjustment ismade, the practitioner should set out theirprofessional opinion underlying theassumptions adopted. These include, as aminimum, comments on the state of themarket and delivery targets as at the date ofassessment.

Box 8: Site Value – area-wideassessmentsWhen undertaking Local Plan or CIL (area-wide) viability testing, a second assumptionneeds to be applied to the above:‘Site Value (as defined above) may need tobe further adjusted to reflect the emergingpolicy / CIL charging level. The level of theadjustment assumes that site delivery wouldnot be prejudiced. Where an adjustment ismade, the practitioner should set out theirprofessional opinion underlying theassumptions adopted. These include, as aminimum, comments on the state of themarket and delivery targets as at the date ofassessment.’

2.4 Using a viabilityassessment to arrive at aprofessional judgment2.4.1 Valuation and formulating appropriatejudgments is an intrinsic part of appraisals thatcontain a significant number of variables. Thesevariables may change over time and will reflectthe movement in the property market generally(see Appendix B). The appraisal date shouldtherefore be clearly stated and inevitableuncertainty addressed through sensitivity orsimilar analysis. It is for the practitioner todecide in each specific case if the advicebeing provided falls within the ambit of theRICS Valuation – Professional Standards(Red Book) or its exceptions.

12 | FINANCIAL VIABILITY IN PLANNING

2.4.2 The residual approach can be appliedwith differing levels of information andsophistication and it is for the practitioner todecide upon the most appropriate applicationof any financial model, bespoke or otherwise.

2.4.3 The basic residual concept isstraightforward, but difficulties can arise, notonly in the method itself, but also in estimatingthe values of the many variables that go intothe appraisal. The residual answer can also besensitive to small changes in some variables. Itis appropriate and strongly recommended,therefore, for some form of sensitivity (scenarioand/or simulation) analysis to be undertaken.This would examine the effect of changes inthe level of individual variables on the residualland value (or developer’s return) to test the keyassumptions in order to ensure that they aresoundly based, before a judgment is finalisedand the residual land value (or return required)is finally determined and a full picture ofdevelopment viability ascertained. As explainedin 2.2.3 the residual approach should bemarket based as envisaged by the NPPF inundertaking viability assessments.

Box 9: Sensitivity testingIt is strongly recommended that financialappraisals are sensitivity tested, as aminimum, and with more complex schemes,further scenario/simulation analysis shouldalso be undertaken. This is to ensure that asound judgment can be formulated onviability.

2.4.4 It is also recommended that additionalchecks are undertaken on the estimatedresidual land value when this is the purpose ofthe calculation. These checks should includecomparison with the sale price of land forsimilar development, where such evidenceexists, based on land value per hectare or perunit of development, particularly for greenfielddevelopment, and calculation of the ratio of theresidual land value to the capital value of thescheme and how this ratio compares to otherevidence of similar transactions.

2.4.5 The value of development land (forestablishing Site Value) has regard to what canbe developed on that land and the value, costand timing of that development. Furthermore,

the value of that development is not directlyrelated to its cost, but is created by theinterplay of market forces. These market forcesinclude the supply of and demand fordevelopment properties and land in the market(see also Appendix E, figure 5 and paragraphE.1.13). This, in turn, is influenced by theplanning system, the availability of fundingthrough the financial system, residential andoccupier demand, and the property investmentand capital markets.

2.4.6 Where the residual appraisal method hasassessed the level of return, it will benecessary to form a professional judgment asto that return’s acceptability in respect of theproposed development. This will have regard toboth market forces as described above and theintrinsic risks associated with the schemebeing appraised (see also Appendix E,paragraph E.3.2.1). A market risk adjustedreturn may fall within a prescribed range ormay be required to seek to achieve a minimumtarget level for a proposed development. Thejudgment formulated will, in practice, need tobe justified having regard to 2.4.3 and 2.4.4.

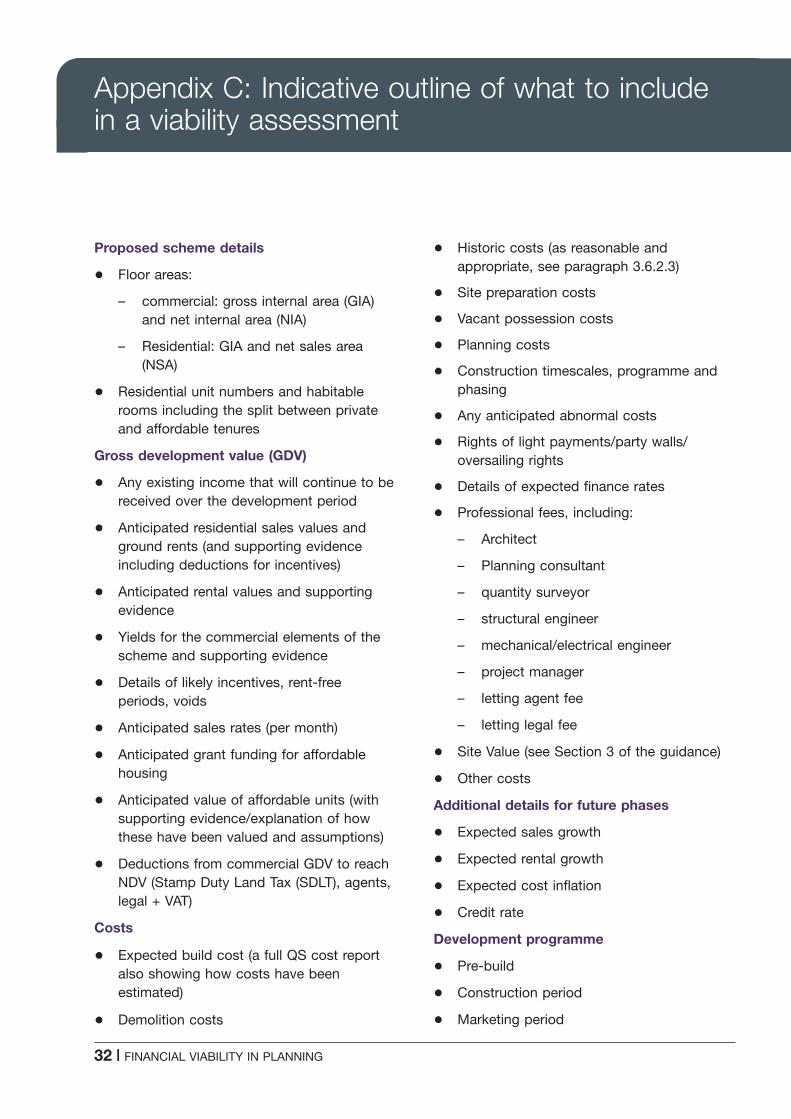

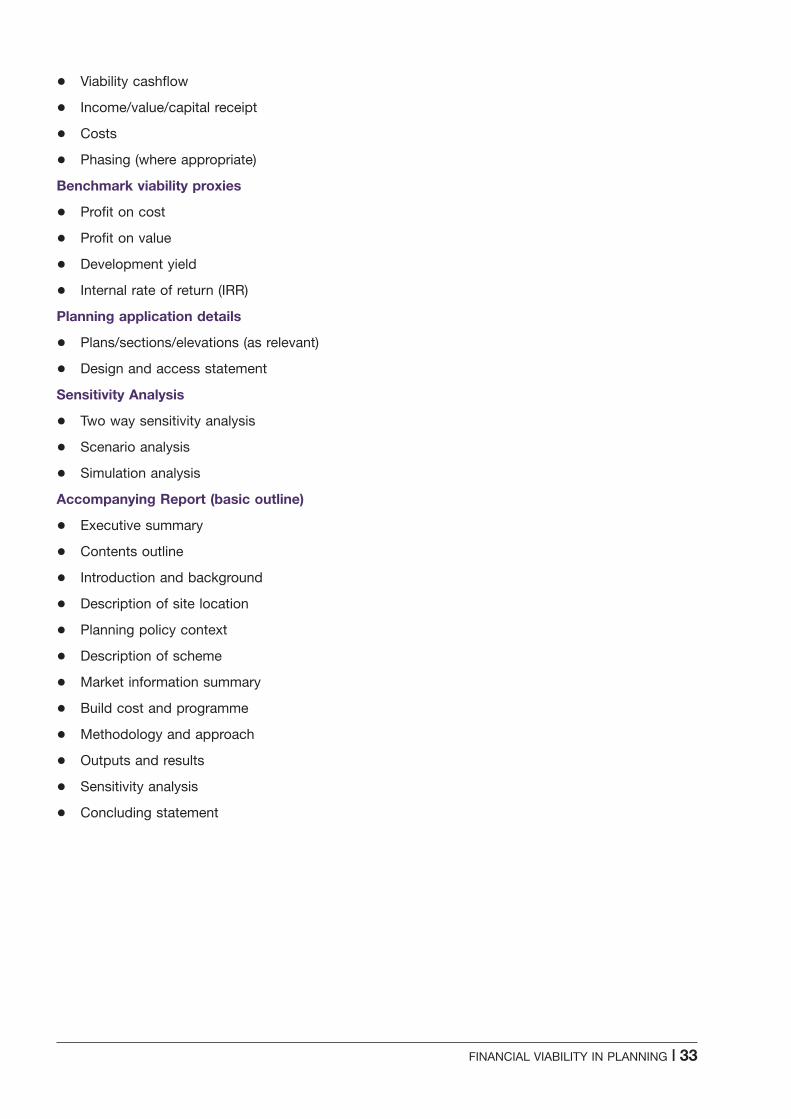

2.5 Indicative outline of whatto include in a viabilityassessment2.5.1 As an illustration of what a viabilityassessment should comprise, Appendix Cprovides a checklist. It is stressed that the leveland detail of information forming the viabilityassessment will vary considerably from schemeto scheme, and in the case of plan making andCIL charging schedules. It is up to thepractitioner to submit what they believe isreasonable and appropriate in the particularcircumstances and for the local authority ortheir advisers to agree whether this is sufficientfor them to undertake an objective review.

2.5.2 When determining planning applications,LPAs are concerned with the merits of theparticular scheme in question. They shoulddisregard who is the applicant, except inexceptional circumstances such as personalplanning permissions, as planning permissionsrun with the land. It follows that in formulating

FINANCIAL VIABILITY IN PLANNING | 13

information and inputs into viability appraisals,these should disregard either benefits ordisbenefits that are unique to the applicant,whether landowner, developer or both; forexample, internal financing arrangements. Theaim should be to reflect industry benchmarksas applied to the particular site in question fora planning application or as appropriate for thewider area in the context of the preparation ofpolicy or the setting of the CIL chargingschedules. Clearly, there must be consistencyin viability principles and application acrossthese interrelated planning matters.

Box 10: Industry benchmarksIn undertaking scheme specific viabilityassessments, the nature of the applicantshould normally be disregarded as shouldbenefits or disbenefits that are unique to theapplicant. The aim should be to reflectindustry benchmarks having regard to theparticular circumstances in bothdevelopment management and plan makingviability testing.

2.5.3 This guidance note does not recommendany particular financial model (bespoke orotherwise) or provide indications as to inputs oroutputs commonly used. It is up to thepractitioner in each case to adopt and justify asappropriate.

2.5.4 While this section has outlined the basicapproach to assessing development viabilitythat is commonly used in practice, Appendix Dcontains refinements to the basic residualmethod of assessing development viability. Thisincludes cash flows and DCF analysis (internalrate of return (IRR) and net present value (NPV)approaches) and the effects of inflation andforecasting are set out. Section 3 provides adetailed consideration of development viabilityand Site Value benchmarks to determinewhether the scheme, or planning policy, isviable or not, and therefore the level ofplanning obligations that can be afforded orcompliance with policy met.

2.5.5 Appendix E, sections E.2 and E.3 providedetails of the types of developer and theconstituent parts of the development appraisalmodel.

14 | FINANCIAL VIABILITY IN PLANNING

3 Viability and Site Value benchmarks

Key issues: principles that practitionersshould take into account; model andapproach; developer’s return approach; SiteValue approach; date of assessment; actualpurchase price; holding costs; third partyinterests; vacant possession and relocationcosts; reappraisals, and projection models.

3.1 Overview3.1.1 This section is intended to provide amore detailed consideration of financial viabilityassessments for the purposes of thepractitioner. It provides an approach toassessing viability, rather than specifying aprescriptive tool or financial model. It thereforedoes not remove the need for developers, localplanning authorities and other interested partiesto seek advice from appropriately qualifiedprofessionals when undertaking or reviewingviability assessments.

3.1.2 This guidance follows the usual approachof setting down a set of principles thatpractitioners should take into account. It doesnot give specific examples but leaves thisdiscretion to the professionals in providingsuitably appropriate advice.

3.1.3 As part of providing a viability frameworkit is necessary to set out clear guidance on SiteValue to be used in viability assessments.Much of this section is focused on schemespecific decision taking but the principles areequally applicable to area-wide viability testing.Appendix D sets out further refinements toviability methodology having regard tocashflow, inflation in costs and values andmore complex developments.

3.1.4 While the guidance does not specify aprescriptive tool or financial model it doesemphasise the importance of using marketevidence as the best indicator of the behaviour

of willing buyers and willing sellers in themarket. It will be necessary for practitioners toexamine the available evidence, analyseaccordingly and form an appropriate judgment.

3.2 Model and approach3.2.1 In assessing the impact of planningobligations on the viability of the developmentprocess, it is accepted practice that a residualvaluation model is most often used. Thisapproach uses various inputs to establish aGDV from which GDC is deducted. GDC caninclude a Site Value as a fixed figure resultingin the developer’s residual profit (return)becoming the output, which is then consideredagainst a benchmark to assess viability.Alternatively, the developer’s return (profit) is anadopted input to GDC, leaving a residual landvalue as the output from which to benchmarkviability, i.e. being greater or less than whatwould be considered an acceptable Site Value.

3.3 Developer’s returnapproach (where Site Value isa cost of development)3.3.1 When a developer’s return is adopted asthe benchmark variable, a scheme should beconsidered viable, as long as the costimplications of planning obligations are not setat a level at which the developer’s return (afterallowing for all development costs includingSite Value) falls below that which is acceptablein the market for the risk in undertaking thedevelopment scheme. If the cost implicationsof the obligations erode a developer’s returnbelow an acceptable market level for thescheme being assessed, the extent of thoseobligations will be deemed to make a

FINANCIAL VIABILITY IN PLANNING | 15

development unviable as the developer wouldnot proceed on that basis (see figure 2).

3.3.2 The benchmark return, which is reflectedin a developer’s profit allowance, should be ata level reflective of the market at the time ofthe assessment being undertaken. It willinclude the risks attached to the specificscheme. This will include both property-specificrisk, i.e. the direct development risks within thescheme being considered, and also broadermarket risk issues, such as the strength of theeconomy and occupational demand, the levelof rents and capital values, the level of interestrates and availability of finance. The level ofprofit required will vary from scheme toscheme, given different risk profiles as well asthe stage in the economic cycle. For example,a small scheme constructed over a shortertimeframe may be considered relatively lessrisky and therefore attract a lower profit margin,given the exit position is more certain, than alarge redevelopment spanning a number ofyears where the outturn is considerably moreuncertain. A development project will only beconsidered economically viable if a market riskadjusted return is met or exceeds a benchmarkrisk-adjusted market return.

3.3.3 When considering what Site Value toinclude, the relevant value should also be inaccordance with the definition of viability forplanning purposes in 2.1, which is defined asfollows:

Site Value should equate to the marketvalue subject to the following assumption;that the value has regard to developmentplan polices and all other material planningconsiderations and disregards that which iscontrary to the development plan.

3.3.4 In arriving at a Site Value based on thedefinition in 3.3.3, regard should be given toprospective planning obligations. The purposeof the viability appraisal is, of course, to assessthe extent of these obligations while alsohaving regard to the prevailing property market.This point is discussed further in 3.4 below.

3.3.5 When undertaking Local Plan or CIL(area-wide) viability testing, a secondassumption, as outlined in 2.3.3 needs to beapplied to the definition of Site Value above.

Site Value (as defined above) may need tobe further adjusted to reflect the emergingpolicy/CIL charging level. The level of theadjustment assumes that site delivery wouldnot be prejudiced. Where an adjustment ismade, the practitioner should set out theirprofessional opinion underlying theassumptions adopted. These include, as aminimum, comments on the state of themarket and delivery targets as at the date ofassessment.

3.3.6 The amendment to market value for CILor Local Plan viability testing has not yethappened in the market, i.e. the effect on themarket value of land of the new policy (orchanges to existing) or the burden of CILcharge. There is of course a spectrum rangingfrom CIL testing where there is no planningpolicy change through to a whole-scale policychange within the local Plan. It follows that ifthe latter end of the spectrum is being tested,the first assumption in the definition of SiteValue would fall away, whereas with the former,it would be necessary to retain thisassumption. There must, however, be a‘boundary’ placed on the effect on land, toreflect new policy or the burden of CIL charge,in terms of restricting any reduction so that itdoes not go below what land would willinglytransact at in order to provide a competitivereturn to a willing landowner.5

3.3.7 The above definition is therefore notprescriptive and leaves the practitioner to makean appropriate judgment which must bereasonable, having regard to the workings ofthe property market (see also 3.4.1 below).Clearly, if sites are not willingly delivered atcompetitive returns to the market, developmentwill not take place, i.e. it will not be deliverable.

16 | FINANCIAL VIABILITY IN PLANNING

Box 11: Site Value definitionSite Value either as an input into a schemespecific appraisal or as a benchmark isdefined in the guidance note as follows:‘Site Value should equate to the marketvalue6 subject to the following assumption:that the value has regard to developmentplan policies and all other material planningconsiderations and disregards that which iscontrary to the development plan.’

Box 12: Site Value – area-wideassessmentsWhen undertaking Local Plan or CIL (area-wide) viability testing, a second assumptionneeds to be applied to the above:‘Site Value (as defined above) may need tobe further adjusted to reflect the emergingpolicy/CIL charging level. The level of theadjustment assumes that site delivery wouldnot be prejudiced. Where an adjustment ismade, the practitioner should set out theirprofessional opinion underlying theassumptions adopted. These include, as aminimum, comments on the state of themarket and delivery targets as at the date ofassessment.’

3.4 Site Value approach(including an allowance fordeveloper’s return as a cost ofdevelopment)3.4.1 To date, in the absence of any guidance,a variety of practices have evolved, which areused by practitioners to benchmark land value.One approach has been to exclusively adoptcurrent use value (CUV) plus a margin or avariant of this, i.e. existing use value (EUV) plusa premium. The problem with this singularapproach is that it does not reflect theworkings of the market as land is not releasedat CUV or CUV plus a margin (EUV plus).

The margin mark-up is also arbitrary and ofteninconsistently applied in practical application asa result. Figure 3 (overleaf) illustrates how EUVplus a premium can over-value and under-valuesites compared to market value with anassumption, and the resultant impact onplanning obligations that can be viablyafforded. Appendix E sets out further detail onwhy a CUV approach is not recommended. It isof course possible to show how Site Value (asdefined in the guidance), when it has beenestablished, can be disaggregated andexpressed in terms of ‘CUV plus a premium’.This guidance recognises that somepractitioners and users may find this helpful aspart of the decision taking process. AgainAppendix E comments upon this further.

3.4.2 In a market without planning obligations,the maximum value of a developmentopportunity would be the residual value of thesite with the proposed planning permissionafter development profit and all developmentexpenses have been deducted from the GDV ofthe proposed scheme. In this situation, if thisvalue was above the CUV (defined in AppendixF, Glossary of terms) of the site, landowners aremore likely to deliver a site for development.The level of uplift arising, which would result inland being released for development, couldvary considerably between individual sites.

3.4.3 The residual land value (ignoring anyplanning obligations and assuming planningpermission is in place) and current use valuerepresent the parameters within which toassess the level of any planning obligations.Any planning obligations imposed will need tobe paid out of this uplift but cannot use up thewhole of this difference, other than inexceptional circumstances, as that wouldremove the likelihood of the land beingreleased for development.

FINANCIAL VIABILITY IN PLANNING | 17

Figure 3: Market value (with assumption) v existing use (plus)

3.4.4 For a development to be financiallyviable, any uplift from current use value toresidual land value that arises when planningpermission is granted should be able to meetthe cost of planning obligations while ensuringan appropriate Site Value for the landownerand a market risk adjusted return to thedeveloper in delivering that project (the NPPFrefers to this as ‘competitive returns’respectively). The return to the landowner willbe in the form of a land value in excess ofcurrent use value but it would be inappropriateto assume an uplift based on set percentagesas detailed above and in Appendix E, given thediversity of individual development sites.

3.4.5 The Site Value will be based on marketvalue, which will be risk-adjusted, so it willnormally be less than current market prices fordevelopment land for which planningpermission has been secured and planningobligation requirements are known. Thepractitioner will have regard to current usevalue, alternative use value, market/transactional evidence (including the propertyitself if that has recently been subject to adisposal/acquisition), and all materialconsiderations including planning policy inderiving the Site Value.

3.4.6 The assessment of Site Value in thesecircumstances is not straightforward, but it will

be, by definition, at a level at which alandowner would be willing to sell which isrecognised by the NPPF.

3.4.7 Sale prices of comparable developmentsites may provide an indication of the landvalue that a landowner might expect, but it isimportant to note that, depending on theplanning status of the land, the market pricewill include risk-adjusted expectations of thenature of the permission and associatedplanning obligations. If these market prices areused in the negotiation of planning obligationsthen account should be taken of anyexpectation of planning obligations that areembedded in the market price, or valuation inthe absence of a price. In many cases, relevantand up-to-date comparable evidence may notbe available, or the diversity of developmentsites requires an approach not based on directcomparison. The importance, however, ofcomparable evidence cannot be over-emphasised, even if the supporting evidence isvery limited, as seen in court and land tribunaldecisions.

3.4.8 This guidance has sought to reflect moreappropriately the workings of the market. Witha definition of viability established, it has beenconsidered appropriate to look at terms theindustry is familiar with, rather than invent newones. Accordingly, the well understood

18 | FINANCIAL VIABILITY IN PLANNING

definition of market value has been adopted asthe appropriate basis to assess Site Value,subject to planning policy as set out above inboth site specific and area wide assessments.

3.4.9 It has become very common forpractitioners to look at alternative use value(AUV) as a land value benchmark. This willcome with its own set of planning obligationsand requirements. Reviewing alternative uses isvery much part of the process of assessing themarket value of land and it is not unusual toconsider a range of scenarios for certainproperties. Where an alternative use can bereadily identified as generating a higher value,the value for this alternative use would be themarket value. Again, comparable evidence mayprovide information to assist in arriving at anAUV. Accordingly, in assessing the marketvalue of the land there may well be a range ofpossible market values for different uses, whichcould be applicable to the land and buildings,from current use through to a number ofalternative use options, each having its ownplanning obligation requirements. These will beused to derive the ‘market value withassumption’ (the option with highest valuebeing the Site Value) for input into a viabilityassessment.

Box 13: Site Value and comparableevidenceThe assessment of Site Value withassumption is not straightforward but must,by definition, be at a level which makes alandowner willing to sell, as recognised bythe NPPF. Appropriate comparable evidence,even where this is limited, is important inestablishing Site Value for scheme specificas well as area wide assessments.

3.5 Date of assessment3.5.1 The date upon which the planningauthority, or the Secretary of State, (see below)resolves to grant or refuse a planningapplication is the date upon which all relevantinformation is considered. In practical terms,reports and supporting documentation areprepared well in advance of this date. It followsthat the ‘appraisal date’ should be carefullyconsidered and agreed. If the viability

assessment is provided pre-application, thenthe date of the assessment will clearly be priorto the submission of an application. Theviability assessment may subsequently requireupdating when the application is submitted. Ifthe viability assessment is submitted with aplanning application, the date of the application(not the date of registration) may be theappropriate date but it is important to note thatthe decision of the LPA on a planningapplication needs to be based on the materialconsiderations at the date of determination,hence the conclusions of a viability assessmentundertaken at the date of application will stillhold good at the date of decision. Viabilityassessments may, therefore, occasionally needto be updated to market movements during theplanning process.

3.5.2 There are occasions where the appraisalswill require revisions. In certain circumstances,as a result of, for example, fundamental marketchanges or changes in density of the scheme,between submission of the viabilityassessment, application and consideration bythe planning authority, it will be necessary toreview and update the appraisal. This should,however, relate to changes in the market, orchanges specific to the scheme, that would nothave been known at the time of the originalsubmission. Where there is a planning appeal,the date should be agreed between the partiesor taken as the date of the hearing/writtenrepresentations.

Box 14: Date of assessmentViability assessments will usually be datedwhen an application is submitted (or when aCIL charging schedule or Local Plan ispublished in draft). Exceptions to this maybe pre-application submissions and appeals.Viability assessments may occasionally needto be updated due to market movements orif schemes are amended during the planningprocess.

3.6 Other material issues

3.6.1 Actual purchase price

3.6.1.1 Site purchase price may or may not bematerial in arriving at a Site Value for the

FINANCIAL VIABILITY IN PLANNING | 19

assessment of financial viability. In somecircumstances, the use of actual purchaseprice should be treated as a special case. Thefollowing points should be considered.

+ A viability appraisal is taken at a point intime, taking account of costs and values atthat date. A site may be purchased sometime before a viability assessment takesplace and circumstances might change.This is part of the developer’s risk. Landvalues can go up or down between thedate of purchase and a viability assessmenttaking place; in a rising market developersbenefit, in a falling market they may loseout.

+ A developer may make unreasonable/over-optimistic assumptions regarding the typeand density of development or the extent ofplanning obligations, which means that ithas overpaid for the site.

+ Where plots have been acquired to formthe site of the proposed development,without the benefit of a compulsorypurchase order, this should be reflectedeither in the level of Site Value incorporatedin the appraisal or in the developmentreturn. In some instances, site assemblymay result in synergistic value arising.

+ The Site Value should always be reviewedat the date of assessment and comparedwith the purchase price and associatedholding costs and the specificcircumstances in each case.

3.6.1.2 It is for the practitioner to consider therelevance or otherwise of the actual purchaseprice, and whether any weight should beattached to it, having regard to the date ofassessment and the Site Value definition setout in this guidance.

Box 15: Purchase price and historic costsIt is for the practitioner to consider therelevance or otherwise of the actualpurchase price, and whether any weightshould be attached to it, having regard tothe date of assessment and the Site Valuedefinition as set out in this guidance. Wherehistoric costs (for example remediationworks) are stated it is important that theseare not reflected in the Site Value (i.e. doublecounted).

3.6.2 Holding costs

3.6.2.1 The site will be valued at the date ofassessment. Holding costs attributable to thepurchase of the site should, therefore, notnormally be allowed, as the Site Value will beupdated. In phased schemes where land isvalued at the beginning of the developmentand land is drawn down for each phase, it maybe appropriate to apply holding costs. Also,where plots of land have been assembled andsubject to assessment, it may also beappropriate to include related holding costs.Where holding costs are applicable they shouldbe offset by any income received from theproperty.

3.6.2.2 Other relevant costs subsequent topurchase, including professional fees and othercosts incurred in bringing the applicationforward, and holding the site includingremediation measures, should be reflected inthe development appraisal as appropriate andreasonable.

3.6.2.3 Where there has been historicexpenditure on a development site prior toreceiving planning permission, these can beincluded in a development appraisal. This ishighly relevant with certain regeneration sites,where cost is not reflected in Site Value. Care,however, must be taken in arriving at a SiteValue that the effect of this expenditure shouldbe ignored. In many instances the practitionerwill note the expenditure as being reflected inthe Site Value arrived at and therefore thehistoric cost (for example remediation works)will not appear explicitly in the appraisal.Clearly, the objective is that there should be nodouble counting.

3.6.3 Third party interests, vacantpossession and relocation costs

3.6.3.1 Often, in the case of development andsite assembly, various interests need to beacquired or negotiated in order to be able toimplement a project. These may include:buying in leases of existing occupiers or payingcompensation; negotiating rights of light claimsand payments; party wall agreements,oversailing rights, ransom strips/rights,agreeing arrangements with utility companies;

20 | FINANCIAL VIABILITY IN PLANNING

temporary/facilitating works, etc. These are allrelevant development costs that should betaken into account in viability assessments. Forexample, it is appropriate to include rights oflight payments as it is a real cost to thedeveloper in terms of compensation for loss ofrights of light to neighbouring properties. Thisis often not reflected in Site Value given thedifferent views on how a site can bedeveloped.

3.6.4 Re-appraisals (viability reviews)

3.6.4.1 The re-appraisal approach, which maybe more applicable to certain schemes, allowsfor planning applications to be determined butleaving, for example, the level of affordablehousing to be fixed prior to implementation ofthe scheme. Such re-appraisals are generallysuited to phased schemes over the longer termrather than a single phase scheme to beimplemented immediately, which requirescertainty.

3.6.4.2 Where long life planning permissionsare granted (five years plus) reappraisals mayalso be appropriate. As such re-appraisalmechanisms should only be considered inexceptional cases. These appraisals wouldusually be undertaken during the reservedmatters application stage. Careful considerationwould need to be given as to how this is setout in a section 106 agreement, although it willbe important to the LPA and applicant toexpress a range for the assessment, i.e. for theapplicant to state the level of obligation abovewhich they would not be expected to exceedand for the LPA to state the level of obligationbelow which the development will beunacceptable, regardless of the benefits thatarise from it.

3.6.4.3 The methodology may include, forexample, specifying: the process involved, thebasis of model, inputs, basis of return, and SiteValue. It is stressed that the re-appraisal shouldalways be undertaken prior to theimplementation of a scheme or phase in orderto fully account at the time for the risk thedeveloper is undertaking, and, therefore, theappropriate return. From a technicalperspective, so-called ‘overage’ arrangements(post-development appraisals) are not

considered appropriate, as development risk atthe time of implementation cannot beaccounted in respect of the inevitableuncertainty of undertaking a development orindividual phase. It also undermines the basisof a competitive return as envisaged by theNPPF by introducing uncertainty post theimplementation of the development. This maymake funding the scheme difficult or unlikely inmany cases.

3.6.4.4 It is important to ensure that thedrafting of re-appraisal provisions do not resultin the earlier phases becoming uncertain as tothe amount of development to be provided onsite. This would have the unfortunate effect ofstifling development. Each phase requiressufficient certainty to be able to provide therequired returns and secure developmentfunding.

Box 16: Re-appraisalsRe-appraisals may be appropriate for longerterm/multi phased schemes and should beundertaken prior to the implementation of ascheme or phase.

3.6.5 Validity of projection models forcapturing future market growth

3.6.5.1 An alternative approach to the re-appraisal approach (and current day appraisals)is the use of projection models. In more volatilemarket conditions, many planning applicationsmay not be viable for the schemes proposedusing present-day values and costs. Thisreflects a variety of factors that would includethe relationship of likely end values to the costsof building the scheme. Inevitably, when suchschemes go forward for discussion with theLPA, applicants may look at growth models(see Appendix D) and the likelihood of theproposed development becoming viable overthe short to medium term, with the acceptancethat it may not be currently viable. This isnormally more relevant to large schemes to bebuilt over the medium to longer term than forshort term projects.

3.6.5.2 Current day methodologies, for largeschemes of a medium to longer term build outduration, may at times give the LPA cause forconcern as the case is made that the site is

FINANCIAL VIABILITY IN PLANNING | 21

not currently viable. As a result they may notachieve the desired outturn in terms ofplanning obligations, etc. The principle andapplication of projection models is for sites thatare non-viable today but where the likelihood isthat development would occur at some futuredate in the life of a planning permission, orwhere the development is likely to be over asufficiently long period of time during which themarket conditions may vary.

3.6.5.3 It is important to distinguish in caseswhere projection modelling is used betweenmarket value growth and site regenerativegrowth when preparing appraisals. Largerschemes may be subject to intrinsic/internalvalue growth as a result of development,achieving a critical mass that may or may notbe reflected in the broader market.

3.6.5.4 Projection models are valid in terms ofassessing the viability of the site. Advisers forboth applicant and local authority should putthemselves in the position of looking at thepotential of the site in the future and assessthe likely obligations and commitments that aparticular site can make based on thoseforecasts, rather than on current dayassessments. Such an approach might enablethe LPA to achieve a number of its objectivesby adopting the ‘looking forward’ approach,and for both the LPA and applicant to achievecertainty over the level of planning obligationsattached to the planning permission. AppendixD provides further information on the effects ofinflation and forecasting.

Box 17: Projection modelsProjection (growth) models are an alternativeto current day and reappraisal approachesfor assessing the viability of a site. A ‘lookingforward’ approach for the LPA and applicantcan provide certainty in terms of definingplanning obligations for both at the time ofgranting a planning permission.

3.6.6 Sensitivity testingCounterfactuals

3.6.6.1 As highlighted in section 2 it is stronglyrecommended that financial appraisals aresensitivity tested (including where appropriatescenario and simulation analysis) in order to