Embed Size (px)

Citation preview

By: Ashley Reeves

PEST AND INDUSTRY ANALYSIS

HISTORY Founded in 1932 by Charles and Joseph Revson, along with chemist

Charles Lachman

Products: Global color cosmetics, hair color, beauty tools, fragrances, skincare, anti-perspirant/deodorants and beauty care tools

Net Sales 2010= $1.32 Billion U.S.= 55% International= 45%

Vision: “Glamour, excitement, and innovation through high-quality products at affordable prices.”

Target market = women of all ages worldwide

Brands: Revlon Almay Age Defying ColorStay

HISTORY CONTINUED

Headquartered in New York, NY

CEO Alan Ennis as of May 2009

4,900 employees

17 manufacturing locations worldwide U.S., Canada, Europe, Latin America, and Asia

Pacific

EXTERNAL MACRO-ENVIRONMENT FACTORS

POLITICAL FACTORS

Strict FDA regulations in the U.S. and other countries

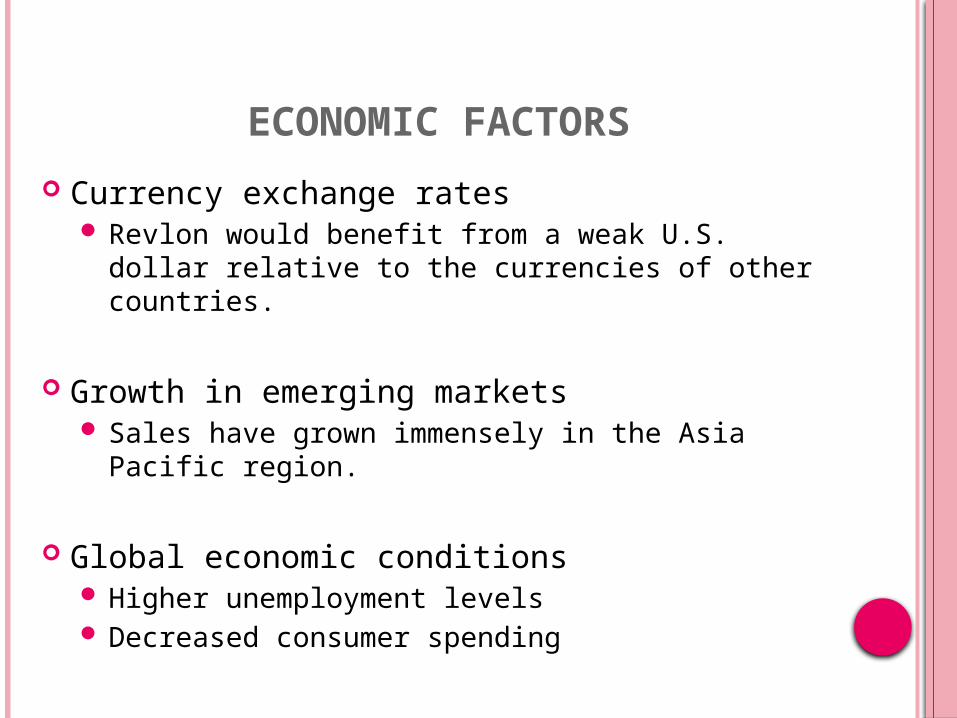

ECONOMIC FACTORS

Currency exchange rates Revlon would benefit from a weak U.S. dollar

relative to the currencies of other countries.

Growth in emerging markets Sales have grown immensely in the Asia Pacific

region.

Global economic conditions Higher unemployment levels Decreased consumer spending

SOCIAL FACTORS

Changes in consumer purchasing habits

Increased customer awareness of permanent make-up options

TECHNOLOGICAL FACTORS

E-Commerce

Use of social media

PEST ANALYSIS

Factor Trend Evaluation Impact(1=low,5=high)

Rank

PoliticalStrict FDA

regulations in the U.S. and other

countries

threat 2 4

Economic

currency exchange rates

growth in emerging markets

Global economic conditions

opportunity/threat

opportunity/threat

opportunity/threat

4

5

2

1

Social

changes in consumer

purchasing habits

Increased customer awareness of

permanent make-up options

threat

threat

3

1

2

Technological

E-Commerce

Use of social media

opportunity

opportunity

2

13

INDUSTRY ANALYSIS

Porter’s Five Forces Model

PERSONAL PRODUCTS INDUSTRY

Buyers SuppliersLarge mass volume

retailersRaw materials

Chain drug and food stores Packaging

Department and specialty stores

Competitors SubstitutesEstee Lauder Companies

Inc.Other cosmetic products

not intended for the same use

L'Oreal Permanent make-up

Procter & Gamble Co. Deciding not to purchase

THREAT OF NEW ENTRANTS Barriers to entry

Nature of Barrier Extent of Barrier

Supply-side economies of scale

High

Demand-side benefits of scale

High

Capital Requirements High

Incumbency advantages independent of size

High

Customer-switching costs Low

Unequal access to distribution channels

High

Restrictive Government Policy

Medium

POWER OF SUPPLIERS

Power Degree of Power Bargaining Power is strong if:

Switching costs Low High

Suppliers offer differentiated

products

Low High

Number of substitutes available

High Low

POWER OF BUYERS

Powers Degree of Power Bargaining Power is strong when:

Number of Buyers High High

Purchases volume Low High

Product Differentiation

High Low

Vendor Switching Costs

Low Low

Degree of backward integration

Low High

POWER OF SUBSTITUTES

Powers Degree of Power Threat is strong if:

Substitute offers attractive price-

performance trade-off

Low High

Switching Costs Low Low

INTENSITY OF RIVALRY

Power Degree of Power Rivalry is strong if:

Number of competitors

High High

Industry Growth High Low

Exit Barriers High High

NATURE OF THE FORCES

Factor Evaluation

Intensity of Rivalry Strong : several major players with similar product offerings.

Consumer Buyer Power Moderate: purchases volume, differentiation, and backward integration do not coincide with strong buyer power.

Supplier Power Benign: other supplier options are available if needed.

Threat of Substitute Products

Benign: many customers are loyal to their personal product items.

Threat of New Entrants Benign: barriers to entry are high with patents, research and development, and pricing strategies.

SUGGESTIONS FOR ADDRESSING KEY FORCES

Intensity of Rivalry Continue producing quality products, anticipating

and responding to changes in consumer demands, and educating product benefits.

PEST & INDUSTRY ANALYSIS CONCLUSIONS

Economic and social factors have the greatest affect on Revlon.

Intensity of rivalry is the greatest force for Revlon.

It is important for companies in the personal products industry to stay on top of changing consumer preferences and needs in order to stand out among the competition.

Although the cosmetics and personal products industries have fierce competition, by continuing to spend more time on research and development to create differentiated and quality products, Revlon can increase their position in the personal products industry.

COMPETITOR AND MARKET ANALYSIS

KEY COMPETITORS

"Bringing the Best to Everyone We Touch and Being the Best in Everything We Do."

“To help men and women around the world aspire to beauty and express their individual personalities to the full.”

“We will provide branded products and services of superior quality and value that improve the lives of the world’s consumers, now and for generations to come.”

Revlon L’Oreal Estee Lauder

Procter & Gamble

Net Sales(2010)

$1.32 Billion

€19.5 Billion($26

Billion)

$7.8 Billion $19.5 Billion(beauty & grooming)

Net Income $327.3 M

$3.13 B $616.4 M $12.7 B

Employees 4,900 64,600 31,000 127,000

Geographic Scope (countries)

100 130 150 180

Brands 8 23 28 32(beauty & grooming)

R&D % of Sales

1.8 3.4 1.1 2.5

Headquarters

U.S. France U.S. U.S.

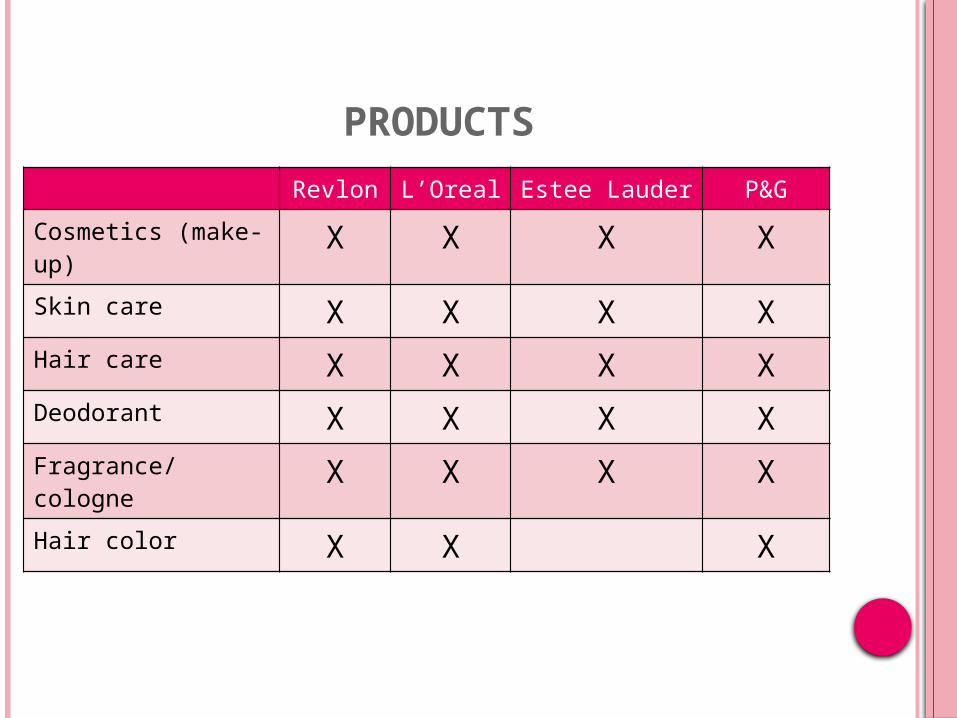

PRODUCTS

Revlon L’Oreal Estee Lauder P&G

Cosmetics (make-up)

Х Х Х Х

Skin care Х Х Х ХHair care Х Х Х ХDeodorant Х Х Х ХFragrance/cologne Х Х Х ХHair color Х Х Х

SALES BY REGION

RevlonU.S. 57%

Asia/Pacific/ 18%Africa

Europe/Canada 15%

Latin America 10%

L’OrealWestern Europe 43%

North America 23%

Asia 13%

Eastern Europe 8%

Latin America 7%

Africa/Orient/Pacific 6%

Estee Lauder

Americas 44%

Europe/Middle 37%East/Africa

Asia/Pacific 19%

Procter & GambleNorth America 42%

Western Europe 21%

Asia 15%

Central & EasternEurope, Middle East, 13%Africa

Latin America 9%

RevlonColor Cosmetics 64%

Women’s Hair Color 11%

AP/DEO 8%

Other Personal Care 7%

Fragrances 6%

Beauty Tools 4%

SALES BY SEGMENT

L’OrealSkin Care 27%

Hair Care 23%

Make-up 21%

Hair Color 15%

Perfumes 11%

Other 3%

Estee LauderSkin Care 42%

Make Up 21%

Fragrance 16%

Hair Care 5%

Procter & Gamble

Household Care 48%

Beauty 34%

Health + Well-Being 18%

TRENDS & FORCES

*Lack of research and development due to a history of losses caused by increased competition and decrease in sale of color cosmetics.*Large dependency on Wal-Mart for sales (23%)*Revlon is a lot smaller than its competition but has a more focused product offering.

*Approximately 34% of sales came from emerging markets in 2009. This presents an opportunity to increase revenues from rising income growths in those markets.

*Diverse brand names target different market niches. *Large presence in global market exposes currency fluctuation risks. More than half of their sales come from outside the U.S.

*Different product price points provide some insulation against recession. *Rises in powerful low-priced retailers negatively affect consumer product companies.* Looking to expand presence in emerging markets. They have created products designed specifically to target developing nations.

Revlon•Build their strong brands•Develop their organizational capability•Drive their company to act globally•Increase operating profits and cash flow•Improve capital structure

L’Oreal•Continue to improve products

•Find ways to promote business affordably

•Make products irresistible for distributors

•Take position early on evolving trends•Take advantage of events

•Develop the ability to continue to create innovative products

Estee Lauder•Commitment to excellent personalized service and education•Using diversified staff to create innovative products•Philanthropy•Minimize impact of products and operations on the environment•Use the latest technological advancements to develop cosmetics that provide superior aesthetics

Procter & Gamble

•Delight customers with sustainable innovations that improve the environmental profile of their products•Improve the environmental profile of their own operations•Improve children’s lives through social responsibility programs•Engage and equip employees to build sustainability thinking and practices in their work•Work with stakeholders to enable continued freedom to innovate in a responsible way

Business Strategie

s

COSMETIC INDUSTRY BCG MATRIX

Stars Question Marks

Cash Cows Dogs

Relative Market Share Position

High

Hig

h

Low

Low

Mark

et

Gro

wth

R

ate

COMPETITOR AND MARKET ANALYSIS

CONCLUSIONS

Revlon has a vast amount of competition in the personal products industry.

Being a lot smaller than the competition has caused them to fall behind in revenues and the amount of money they are able to spend on research and development.

By continuing to develop unique products and investing more money in R&D, Revlon can work their way to becoming as big as the competition.

INTERNAL AND SWOT ANALYSIS

GENERIC AND GRAND STRATEGIES

BUSINESS MODEL

Sell to a large mass-market

Cost Saving

Brand Building

Corporate Social Responsibility

Developing Organizational Capability

Increase operating profit and cash flow

Improve capital structure

Anticipating and responding to changing consumer demands

PERFORMANCE

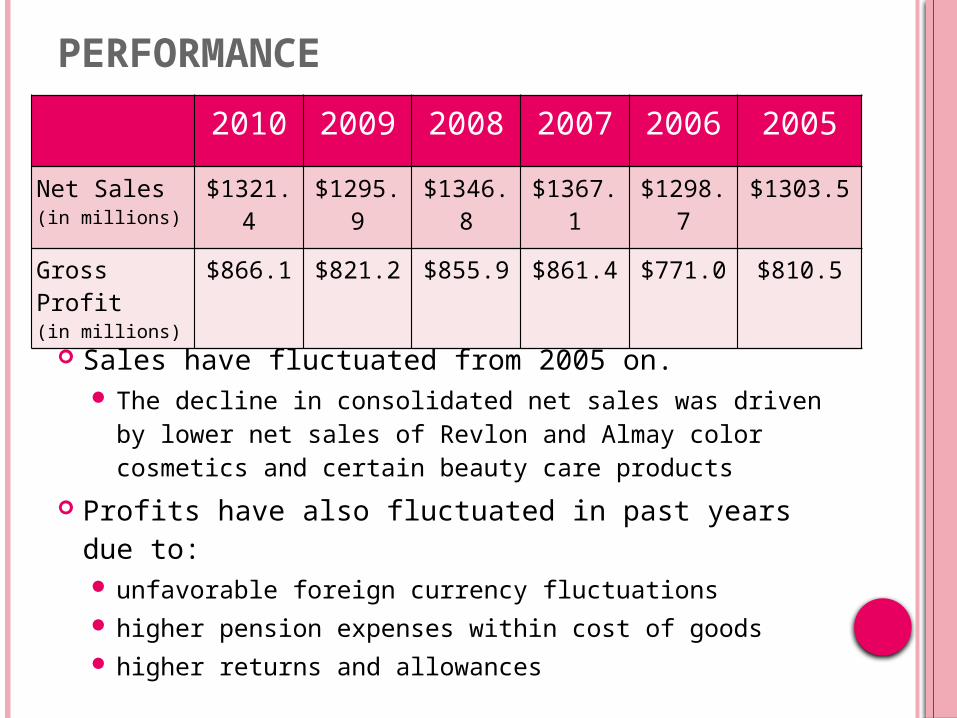

2010 2009 2008 2007 2006 2005

Net Sales(in millions)

$1321.4 $1295.9 $1346.8 $1367.1 $1298.7 $1303.5

Gross Profit(in millions)

$866.1 $821.2 $855.9 $861.4 $771.0 $810.5

Sales have fluctuated from 2005 on. The decline in consolidated net sales was driven

by lower net sales of Revlon and Almay color cosmetics and certain beauty care products

Profits have also fluctuated in past years due to: unfavorable foreign currency fluctuations higher pension expenses within cost of goods higher returns and allowances

CHANGE IN SALES BY REGION

2009 2008 2007United States $747.9 $782.6 $804.2

Asia Pacific $266.7 $265.0 $255.6

Europe $172.4 $200.8 $211.1

Latin America $108.9 $98.4 $96.2

U.S. and Europe have observed a steady decrease in sales over the past few years while Asia Pacific and Latin America have experienced a steady increase in sales. While sales have increased in Asia Pacific and

Latin America, they are not increasing at the rate in which they should, based on the growth rate of cosmetics in those regions.

CHANGE IN SALES BY REGION (CONTINUED)

• U.S. • lower net sales of Revlon and Almay color

cosmetics and Mitchum anti-perspirant deodorant.

• Europe• lower shipments of Revlon and Almay color

cosmetics in Canada• higher allowances for Revlon color cosmetics in

the U.K.• lower shipments of certain beauty care products

in France.

Sales in the U.S. and Europe have decreased due to:

• Asia Pacific• higher shipments of Revlon color cosmetics in Australia

and China and of beauty care products in South Africa.• Latin America• the impact of inflation on selling prices in Venezuela. • higher shipments of Revlon ColorSilk hair color in

Venezuela, Argentina and certain distributor markets

Sales in Asia Pacific and Latin

America have increased due

to:

U.S. SHARE % BY BRAND/PRODUCT

2009 2008

Revlon Color Cosmetics 12.7 12.7

Almay 5.4 5.9

Revlon ColorSilk Hair Color

9.7 8.3

Mitchum AP/DEO 4.6 5.0

Revlon Beauty Tools 21.0 18.8

RESOURCES

Raw materials and components used to create their products.

Most of their products are created at the company’s manufacturing facilities located around the world.

KEY ASSETS

Cash & cash

equivalents

Trade receivables

Inventories

Prepaid expenses

Property, plant, and equipment

Goodwill

BCG MATRIX

Cash Cows

Question MarksStars

Dogs

Relative Market Share Position

Market

Growth

Rate

Hig

hLo

w

High Low

*Market Share: Increase in competition causes a decrease in market share for Revlon

*Market Growth: A high growth rate is possible in global countries.

*Revlon works to expand their current products into new emerging markets where cosmetics sales are increasing.

VALUE CHAIN

Primary Activities:Inbound logistics Storing inventory and scheduling

transportation of products for distribution.

Operations Packaging and assembling products for distribution.

Outbound logistics

Distribution of products through selected channels to customers.

Marketing & Sales

Advertising and promotion of products using print, television, and internet.

Service Tips and services on company website

VALUE CHAIN (CONTINUED)

Support Activities:

Human resource management Look for energetic, success-oriented people who thrive in a dynamic environment.

Technology development Global cross-functional product development process.

Procurement Receiving raw materials from vendors.

Overall Cost Leadership Differentiation

Cost Focus Differentiation Focus

Bro

ad

Narr

ow

Differentiation

Low Cost

Competitive Advantage

Com

peti

tive

Sco

pe

GENERIC STRATEGY

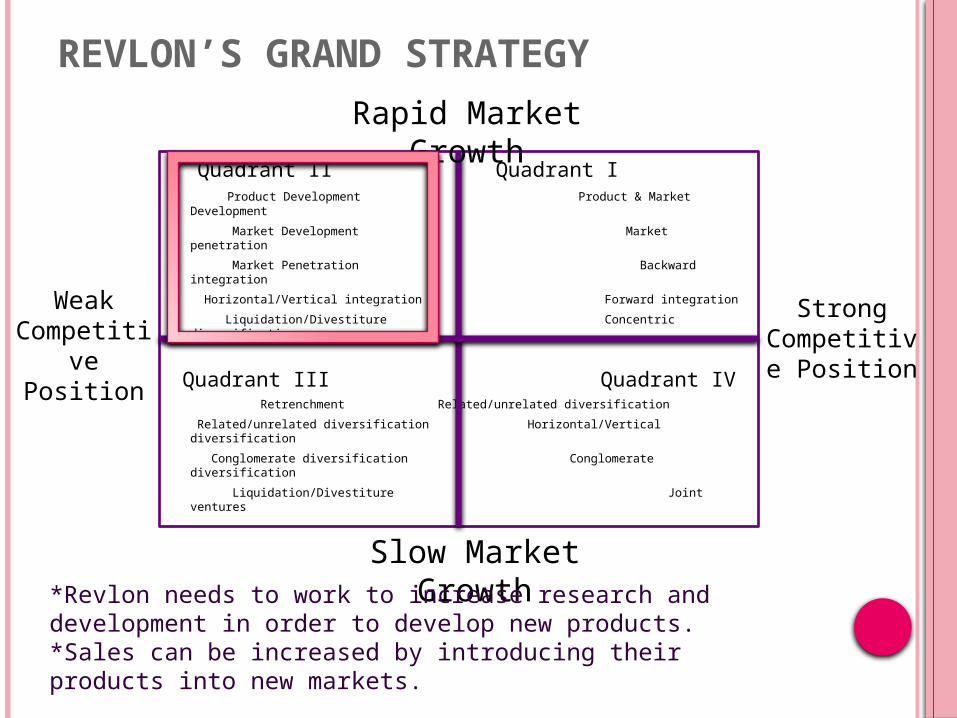

REVLON’S GRAND STRATEGY

Quadrant II Quadrant I Product Development Product & Market Development

Market Development Market penetration

Market Penetration Backward integration

Horizontal/Vertical integration Forward integration

Liquidation/Divestiture Concentric diversification

Quadrant III Quadrant IV Retrenchment Related/unrelated diversification

Related/unrelated diversification Horizontal/Vertical diversification

Conglomerate diversification Conglomerate diversification

Liquidation/Divestiture Joint ventures

Rapid Market Growth

Strong Competitive

Position

Weak Competitive Position

Slow Market Growth*Revlon needs to work to increase research and development in order to develop new products.*Sales can be increased by introducing their products into new markets.

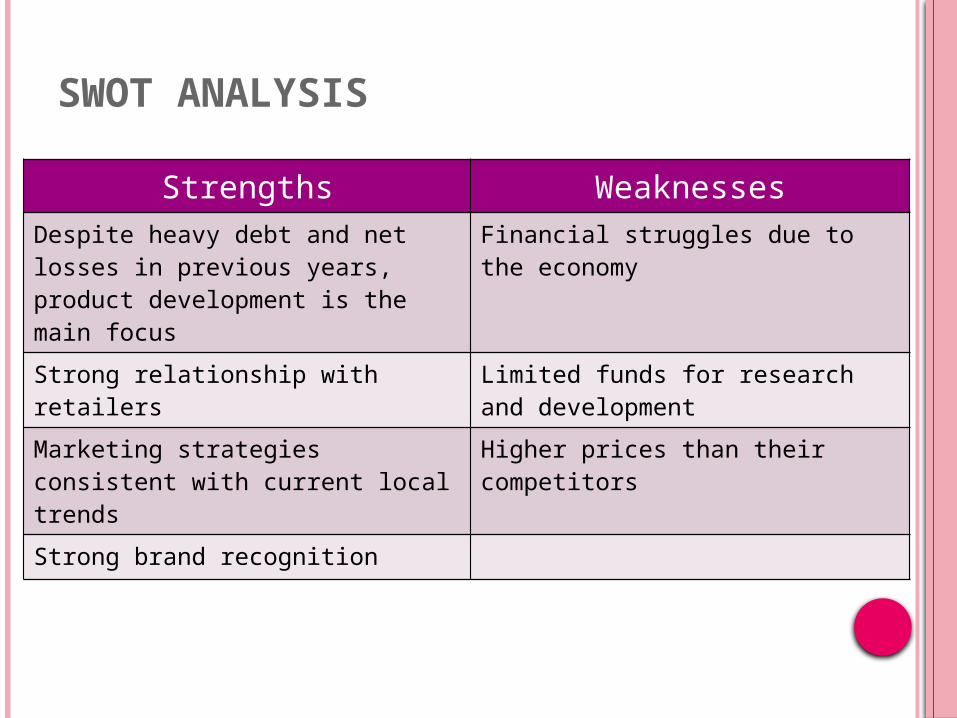

SWOT ANALYSIS

Strengths WeaknessesDespite heavy debt and net losses in previous years, product development is the main focus

Financial struggles due to the economy

Strong relationship with retailers Limited funds for research and development

Marketing strategies consistent with current local trends

Higher prices than their competitors

Strong brand recognition

SWOT ANALYSIS CONTINUED

Opportunities ThreatsE-commerce and use of social media

Changes in consumer purchasing habits

Growth in emerging markets Strict regulations in U.S. and other countries

Increase distribution Permanent make-up options

INTERNAL AND SWOT ANALYSIS

GENERIC AND GRAND STRATEGIES

CONCLUSIONS

Revlon’s sales and profits have fluctuated in the past 5 years.

Increase in consumer spending from Asia Pacific and Latin America has presented Revlon with an opportunity to expand their product market.

Increased spending on R&D will help Revlon to create better products and increase their market share against competitors.

Revlon needs to focus on market development in emerging markets to help increase sales.

![Revlon Media Kit Final[1] - Society for Women's Health ... · Revlon’“LoveIs’On”’Campaign ... Women!become!dependent!on!prescription!pain!relievers!more!quickly!than!men.!Learn!more](https://img.dokumen.tips/doc/110x75/5b408ad97f8b9a91078d5be4/revlon-media-kit-final1-society-for-womens-health-revlonloveisoncampaign.jpg)