Embed Size (px)

Citation preview

Revenue Sharing and Local Public Spending: The Italian ExperienceAuthor(s): Giorgio Brosio, David N. Hyman and Walter SantagataSource: Public Choice, Vol. 35, No. 1 (1980), pp. 3-15Published by: SpringerStable URL: http://www.jstor.org/stable/30023774 .

Accessed: 16/06/2014 16:11

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Springer is collaborating with JSTOR to digitize, preserve and extend access to Public Choice.

http://www.jstor.org

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

Articles Revenue sharing and local public spending: The Italian experience

GIORGIO BROSIO, DAVID N. HYMAN and WALTER SANTAGATA*

In 1971 the Italian government enacted a radical change in its system of local finance. The principal taxes administered by local governments (the communes) were abolished. In their place was substituted a system of funding based on the yield of various taxes administered on the national level. Each local governing unit was then allocated a fixed share of the fund. In effect this established a system of 100 percent. revenue sharing. Further, since fiscal institutions in Italy had few effective restraints on local govern- ment spending, the effect of the reform was to break the link between taxing and spending decisions on the local level by no longer requiring local governments to increase taxes to finance additional expenditures.1

In this paper we test the hypothesis that the provisions of the Tax Reform of 1971 in Italy increased the real level of per capita local public expenditures over and above what one would normally have expected after adjusting for other changes affecting the demand and supply of local public services over the same period. The Italian experience with revenue sharing, while undoubtedly influenced by some of the peculiarities of Italian institutions, may nonetheless offer some insights into the impact of general revenue sharing on local public spending.2

Institutional background: the Italian tax reform of 1971 The Tax Reform of 1971 granted each local government a share of a national revenue fund beginning in 1973 based on the revenue from all sources accruing to that local government in the year immediately preceding that in which the reform went into effect. The local taxes eliminated as a result of the reform, represented 92.2 percent of all tax revenues for the Italian com- munes in 1972. The revenue sharing fund substituted for the displaced taxes was expected to increase at an annual rate of 7.5 to 10 percent and the

* Respectively, Laboratorio di Economia Politica, University of Turin; North Caro- lina State University; Laboratorio di Economia Politica, University of Turin. Research was financed, in part, by the support of the Foundation Giovanni Agnelli, Turin, Italy, and was completed during the academic year 1976-77 when Professor Hyman was Visiting Research Professor at the Laboratorio di Economia Politica of the University of Turin.

Public Choice 35 (1980) 3-15. All rights reserved. Copyright ©Martinus Ni/hoff Publishers bv, The Hague/Boston/London.

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

4 G. Brosio, D.N. Hyman and W. Santagata

share going to each local government was arbitrarily set to increase at these rates. This annual increase proved to be significantly lower than the post- 1973 inflation rates. There was no provision in the legislation to adjust the revenue sharing arrangements in response to changing economic and social conditions within particular communes. Thus, the revenue shares were com- pletely inflexible.3

The reform was passed during a period of relatively stable prices and without significant opposition. It was believed that centralization of taxing in the hands of the national government would provide a more stable source of revenue and improve the efficiency with which taxes were collected as well as offering more control of taxes as a tool of national planning. The association of local governments (Associazioni degli Enti Locali) supported the reform because they believed that the programmed rate of increase would be more than adequate to meet rising demands for local public ser- vices. These beliefs proved to be erroneous.

For a number of years labor unions had been lobbying for expansion of the social programs (e.g., education, welfare and public transport subsidies) traditionally administered by local governments in Italy. The so-called "Exit from the factory" (Uscita dalla Fabbrica) began to bear fruit after 1973 when a marked shift to the left in Italian politics began to translate the lobbying efforts of the unions into increased demands for the services of local governments. Since inflation proved to be significantly in excess of the programmed rate of increase of the sharing fund most local govern- ments found their real revenue actually declining after the reform went into effect while their citizens were demanding new programs and expansion of existing services. Thus, local administrators effectively lost their ability to raise revenue at the point when the demand for revenue began to increase rapidly.

The reform was not, however, accompanied by any significant constraints on local spending authority. That is, while local administrators lost their ability to tax their constituents, they were not limited in any effective way in their ability to supply public services. In fact, since they did not need to directly increase local taxes to finance new or expanded services, the necessity of matching the benefits of increased public services with their costs was eliminated providing incentives for administrators to increase public spending while, at the same time, reducing perceived costs of a unit of public service to voters. The method by which increased resources were allocated to the local governments is peculiar to Italy and consisted of an inflationary process fueled in part by local budget deficits.

In Italy there exist few restraints on borrowing by local governments to finance both current and capital expenditures. The only legal con- straint is that the interest burden in any one year cannot exceed 25 percent of all current income (including transfers from the central government). The reform was not accompanied by any modification in these budget

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

Revenue sharing and local public spending 5

management procedures. In fact, under political and inflationary pressures some of the pre-existing constraints applied by the central government to deficit spending and borrowing by the communes were eased.4 Local governments borrow directly from financial institutions in Italy and the result of such borrowing creates a tendency toward an increase in the money supply which, in turn, contributes to increased inflationary pressures in the economy as a whole. Most banks in Italy are either directly or in- directly controlled by the government. Loans are not always made on the basis of profitability but instead on the basis of policy. It is likely that bank reserves were increased to accommodate the enormous loan demand by governments. The loans to local governments thereby increased the money supply contributing to inflation. In 1975 the budget deficit for provincial and communal governments in Italy was 3 trillion lire or about 3.5 billion dollars amounting to 2.5 percent of GNP in that year. For the communal governments the deficit increased from 37 percent to 68 percent of total revenue making it the single most important source of funding in the aggregate for the communes.5

The implications for local government spending behavior Given the institutional framework described above it is obvious that local public spending would increase beyond the limits set by the growth in transfers and the budget constraint. Our purpose, however, is to determine whether or not such an expansion of expenditures in real terms is over and above what one would normally expect after taking account of the influence of various demographic, socioeconomic, and political variables on spending behavior. We attempt to determine the extent to which the observed behavior changes are attributable to the new revenue sharing arrangements. We have done this by including various control variables in the analysis to account for some of the social changes that have occurred since the reform went into effect. Of course, quantification of all social pressures increasing demands for public services is difficult due to the fact that some of them, such as labor union agitation for social reform, are qualitative.

To determine the influence of revenue sharing on the spending behavior of local governments we have estimated spending functions for a sample of northern and central Italian communes in one year before the provisions of the reform became effective and then compared the functions with others estimated for post-reform years. For each of these years we regressed per capita current expenditures on a group of demographic, socioeconomic, and political variables which, in past studies, have demonstrated good explana- tory power for local expenditures.6 The data for the later years (1974 and 1975) were deflated with an appropriate price index.

The parameters (the constant and the coefficients) of the estimated equations are compared to measure variations in the marginal and average

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

6 G. Brosio, D.N. Hyman and W. Santagata

propensity to spend between the two years. Further we perform a Chow test on the two vectors of coefficients to determine if a change in the structure of the empirical relationships has taken place among the years studied.

Our specific hypothesis is that both the constant and coefficients of the spending function increase after 1973. The aim of the analysis is therefore to measure the effect of revenue sharing in terms of an upward shift in the spending function. We have limited our analysis to current expenditures since the high temporal variability of capital expenditures does not allow any meaningful comparison among years.

The samples and variables Data were collected for two separate samples: a sample of thirty-nine pro- vincial capitals in the north-central regions of Italy and a sample of forty- two suburban communes around the Turin metropolitan area. We have excluded cities from the southern area since previous studies (Bondonio, 1976) have indicated that the institutional and socioeconomic factors influencing public expenditures in those regions differ significantly from those prevailing in the north so as to render the behavior of local adminis- trations in these cities not directly comparable with those of North-Central regions.

The average size of suburban Turin communes is significantly less than that of the provincial capitals. Separate analysis of this sample was therefore included to determine if any significant difference in the reaction to the reform exists between small suburban communes and the larger central cities of the provinces. In particular, most of the smaller communes lack the public transit systems present in the larger provincial capitals that many have argued run at operating losses that contribute disproportionately to the aggregate local public deficits.

The choice of independent variables was based on their availability and explanatory power as demonstrated in previous economic analysis of Italian local expenditure (Giarda, 1967; Zandano, 1972; Brosio, 1975; and Bon- donio, 1976). The first group of variables is demographic and includes population and its ten year growth rate. Population was assumed to have a positive influence on per capita expenditures while population growth was assumed to be negatively associated with the dependent variable reflecting a lag in the response of local spending to economic growth. A second group of variables is socioeconomic and includes a measure of average non- resident population (hotel and non-hotel guests per capita),' and a proxy variable for per capita income - revenue per capita (including transfers) both of which were expected to positively influence per capita expendi- tures. This measure of fiscal capacity was believed to be well correlated with per capita income and to more accurately reflect its variation than other available estimates of per capita income by city.8

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

Revenue sharing and local public spending 7

Although the inclusion of a measure of fiscal capacity in a public spend- ing function may give rise to problems of simultaneous bias we believe that this is of minimal importance in our case. Italian institutions, with heavy reliance on deficit financing and long lags in the spending process, render the interdependence between local revenue and local spending less direct than would normally be the case. Thus, we argue that inclusion of total revenue in the regression equation as a separate independent variable does not reduce the functional equation to an identity. In fact, the inclusion of this variable not only acts as a control for income effects but also allows us to estimate the lags in spending across the local governing units.

Finally, as a proxy for the preferences of local citizens for public services we used dummy variables reflecting the political composition of the giunte (city councils) of the cities in the sample.9 Per capita expenditures were hypothesized to increase with the degree of 'leftness' of the adminis- tration.

The data were used to estimate spending functions for 1971 and 1975 for the provincial capitals and 1971, 1974, and 1975, for the suburban communes of Turin.

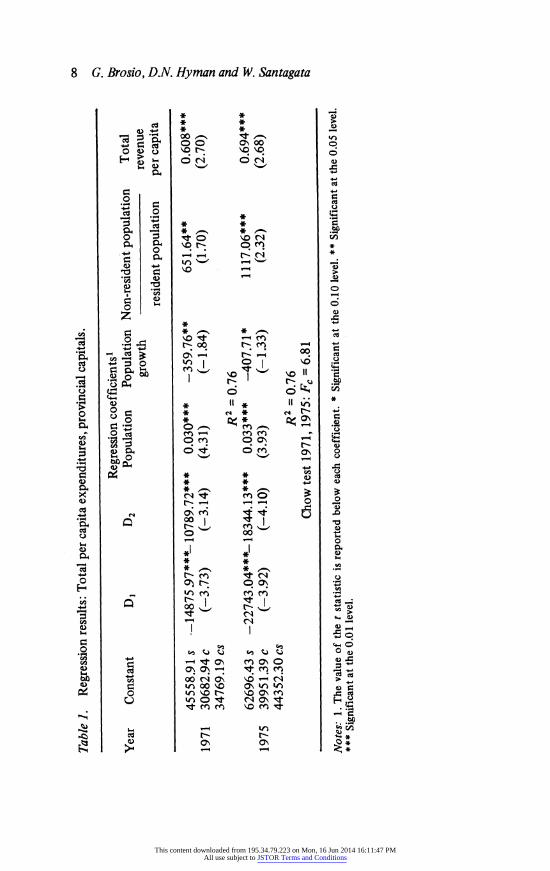

Empirical results Table I presents the results of our regression equation estimating spending functions for the provincial capitals for 1971 and 1975. The dependent variable is accrued current expenditure per capita which was deflated for the effects of inflation in 1975. Ordinary least squares regression was used to estimate the linear functions.

Comparison of the regression results for 1971 and 1975 confirm the general upward shift of the spending function we have hypothesized. Thus, we find a general increase in the propensity to spend by local governments since 1971 after adjusting for the effects of inflation and other usual in- fluences on local public expenditures. Except for population growth in 1975 all the coefficients reported in Table 1 are significant at least at the 5 percent level of confidence and have the expected signs. The model explains about three-quarters of the variation in per capita expenditures for both 1971 and 1975.

The intercept term in the estimated equations refers to the leftist (sinistra) communes and is therefore labelled with an s. The dummy vari- able D1 was set equal to one if the commune had a center (centro) adminis- tration and zero otherwise. Similarly, the dummy variable D2 was set equal to one if the commune had a center-left administration (centro-sinistra, cs) and zero otherwise. The coefficients ofD1 and D2 measure, ceteris paribus, the difference in per capita expenditures between the communes with leftist administrations and those with center and center-left administrations, respectively. Thus, the results for 1971 indicate that, on average, centrist communes spent 14,875 lire less per capita than leftist communes and

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

8 G. Brosio, D.N. Hyman and W. Santagata

Table

1.

Regression

results:

Total

per

capita

expenditures,

provincial

capitals.

Regression

coefficients'

Year

Constant

D1

D2

Population

Population

Non-resident

population

Total

growth

revenue

resident

population

per

capita

45558.91

s

-1487597***-10789.72***

0.030***

-359.76**

651.64**

0.608***

1971

30682.94

c

(-3.73)

(-3.14)

(4.31)

(-1.84)

(1.70)

(2.70)

34769.19

cs

R2

= 0.76

62696.43

s

-22743.04***-18344.13***

0.033***

-407.71*

1117.06***

0.694***

1975

39951.39

c

(-3.92)

(-4.10)

(3.93)

(-1.33)

(2.32)

(2.68)

44352.30

cs

R2

= 0.76

Chow

test

1971,

1975:

Fc = 6.81

Notes:

1. The

value

of the

t statistic

is reported

below

each

coefficient.

* Significant

at the

0.10

level.

** Significant

at the

0.05

level.

*** Significant

at the 0.01

level.

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

Revenue sharing and local public spending 9

center-left communes spent 10,789 lire less per capita than leftist communes. The coefficients of the dummy variables can be subtracted from the constant of the equation to obtain constants that would refer to the equations estimating per capita expenditures for center and center-left communes. This has been done in the table so as to allow the reader to directly compare the constants applying to all three political administrations in 1971 and 1975. The constant referring to center administrations is labelled c while that referring to center-left administrations is labelled cs.

The results show that between 1971 and 1975 the constant of the estimated spending equation increases. Further, the increase is also observed in the constants calculated for the center and center-left communes. The general increase in the constants may be interpreted as an increase in the average propensity to spend resulting from the effects of exogenous influences not reflected in the independent variables. This increase is observed for all communes irrespective of the political color of their giunte.

It is interesting to note that the upward shift in the spending function is more pronounced for the leftist administrations. For the center and center-left administrations the upward shift in the constant amounts to approximately 15 percent of average per capita expenditures in 1971 while for the leftist administrations the corresponding increase is 26 percent. Further, the equations estimate that, ceteris paribus, in 1971 the leftist administrations spent 10,000 to 15,000 lire (about ($ 11.00 to $ 16.50) more per capita than other administrations, and that this differential increased to between 18,000 to 25,000 lire ($ 20.00 to $ 28.00) after adjust- ing for the effects of inflation in 1975. For the 39 communes in the sample the mean value of current expenditures per capita increased in real terms from 66,339 lire in 1971 to 83,225 lire in 1975 - a jump of about 25 percent.

This may imply that the leftist administrations are more willing or ready to recognize opportunities to 'free-ride' by aggressively borrowing and thereby transferring tax-costs to others through their contribution to infla- tion. It may, however, be only a short-run phenomenon as center govern- ments realize they are being exploited and seek either to increase their borrowing or establish new restraints on borrowing by all governments.

The coefficient for population in the 1971 equation indicates that in that year a differential in population of 100,000 was associated with an increase in per capita expenditures of 3,000 lire. Thus, a commune with a million inhabitants tended to spend 27,000 lire more per capita than a commune of 100,000 inhabitants. In 1975 each increment in population of 100,000 was associated with a differential in per capita expenditures of 3,300 lire and the differential for a city of 100,000 and a million inhabitants had increas- ed in real terms to 29,700 lire.

Another important variable explaining local per capita expenditures is non-resident population. Given the importance of the variable as an indica-

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

10 G. Brosio, D.N. Hyman and W. Santagata

tion of tourism and commercial activity its influence reflects in part the

requirement of the communes to dimension their public services (police protection, sanitation, and other public works) for a population greater than their residents and many also indicate the influence of greater commercial activity on public expenditures. Again as observed for population, the coefficient of this variable increases markedly between 1971 and 1975.

The coefficient estimated for total revenue also increase between 1971 and 1975 from 600 to 700 for each 1000 lire differential. This coefficient tends to be less than 1000 because of the presence of 'residui.' Residui are Italian accounting measures for the public sector reflecting the difference between appropriations and actual spending. They therefore are indicative of bureaucratic lags in the spending process. A coefficient of less than 1000 implies that such lags increase with the amount of revenue which, of course, is in part indicative of the size of the commune. The increase in the coefficient between 1971 and 1975 suggests a decrease in these bureaucratic lags.

Finally, between 1971 and 1975 the coefficient associated with the ten year variation in population decreases (i.e., becomes more negative). Since the negative sign on population growth is usually interpreted as indicative of a lag in the adjustment of public expenditures to growth, the slight decrease in the coefficient estimated may imply increased rigidity of expenditures with respect to population change.

The results of the Chow test performed on the residuals of the equations estimated are also reported in Table 1. The value of the F statistic calculated confirms a significant difference in the vector of coefficients between 1971 and 1975 at the one percent level of confidence. This gives further statistical evidence of a change in the structure of the local spending function between 1971 and 1975.

We repeated our regression analysis for the sample of smaller suburban communes of the province of Torino. The results of these regression analyses are reported in Table 2. In this case, data were available for 1971, 1974, and 1975. The average 1975 population of the communes in this sample was 16,699 compared with 176,645 for our sample of provincial capitals. The suburban communes have been growing at a more rapid rate than the provincial capitals in the past five years and have therefore been subject to increased demand pressures for increased public services not reflected in the ten year growth rate of population.

The independent variables chosen, with the exception of hotel guests (which was unavailable), were the same as those used in the analysis of per capita expenditures in the provincial capitals. We were less successful in explaining expenditures in this case than we were for the provincial capitals as evidenced by the lower coefficients of determination. However, we observe the same general upward shift of the spending function after adjusting for the effects of inflation. Although there is no statistical differ-

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

Revenue sharing and local public spending 11

Table

2.

Regression

results:

Total

per

capita

expenditures,

suburban

commmunes

of Torino.

Regression

coefficients'

Year

Constant

D1

D2

Population

Population

Total

revenue

growth

per

capita

11697.35

s

-1721.51

-2036.15

0.15***

-2945.34**

0.675***

1971

-

c

(-1.12)

(-1.28)

(3.07)

(-2.18)

(5.59)

-

Cs

R2

= 0.67

29996.71

s

-7519.53***

-8134.00***

0.34***

-5569.11**

0.26**

1974

22477.18

c

(-3.40)

(-3.58)

(5.31)

(-2.12)

(1.74)

21862.71

cs

R2

= 0.69

32339.09

s

-- 10361.97***

-9216.83***

0.299***

-7048.64**

0.492***

1975

21977.12

c

(-3.59)

(-3.11)

(3.62)

(-1.97)

(3.27)

23122.26

cs

R2

= 0.66

Chow

test

1971,

1974:

Fc = 4.47

Chow

test

1971,

1975:

Fc = 6.35

Notes:

1. The

value

of the

t statistic

is reported

below

each

coefficient.

** Significant

at the

0.05

level.

***

Significant

at the

0.01

level.

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

12 G. Brosio, D.N. Hyman and W. Santagata

ence in the spending behavior according to the political color of the giunte in 1971 we do observe a significant difference in 1974 and 1975. Further the Chow test performed on the data indicates a change in the spending function between 1971 and 1974 and 1975 at a level of confidence of one percent. The response of the smaller suburban communes to the revenue sharing reform appears to be analogous to that of the larger provincial capitals. This result is of particular interest since the prevalent thesis in Italy has been that the expansion of local spending and the swelling of local debt have been primarily a phenomenon of the larger local governing units. Our analysis, however, indicates that the problem is probably much more widespread than commonly believed. In fact, just looking at our sample averages, per capita spending for the suburban communes of Torino grew from 23,690 lire in 1971 to 30,568 lire in 1975 after adjusting for inflation. This represents an increase of 29 percent or 4 percent more than the 25 percent observed in our sample of the larger provincial capitals.

Summary and conclusions Our statistical results confirm the hypothesis of a general upward shift in the spending function between 1971 and 1975. Both the constant and most coefficients of our estimated spending functions increased since 1971 indicating an increase in both the average and marginal propensity to spend. We have further determined that the political color of the local administra- tive unit has become a significant determinant of local spending with leftist administrations tending to spend more and that the leftist administrations' response to the revenue sharing reform has been more pronounced. Finally, it appears as though there has been little difference in response to the revenue sharing expansion between the large and smaller local governing units.

Our conclusions must, however, be qualified to the extent to which our spending functions do not measure all exogenous influences on public spending between 1971 and 1975. Although we have controlled for various influences on the demand for public services including political influences through the dummy variables representing the political color of the giunte, it remains possible that other exogenous influences on public spending, such as the lobbying efforts of the labor unions, have exogenously affected spending. Finally, since we use expenditure data, we cannot determine whether any observed increases in per capita spending have been translated into increased service levels. In fact, increments in per capita expenditures may be associated with any combination of increases in quantity, quality, or reduction in the level of efficiency in the productive process. We have, however, conducted some further analysis to determine whether or not the observed increase in expenditures actually constituted a response to demands for new social programs or merely an increase in the relative share of labor costs in existing programs. Decomposition of aggregate expendi-

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

Revenue sharing and local public spending 13

tures into its component parts for both our samples indicated a clear trend towards a change in the mix of programs supplied by the local governments since 1971. For both samples we observed an increase in the share of the budget going to various instructional programs including child care and public kindergartens. For the provincial capitals instructional programs' relative importance rose from 16.2 to 19.9 percent of total expenditures while for the small suburban communes of Torino, the corresponding rise was from 17.8 percent to 22.6 percent. Further, we observed a sharp drop in both samples of the share of expenditures going to general administra- tion. Much of the increased demands for public services has been concen- trated in the area of instruction so the observed change in the composition of expenditures seems to suggest that local governments have responded to the increased demands. Further, we observed an increase in the share expenditures going to public security for the provincial capitals.

Analysis of wage data for our samples indicates that increased unit labor costs were not a cause of the increase in real per capita expenditures. In fact, for the period under consideration average cost per public employee actually declined somewhat after adjusting for the effects on inflation. It seems likely, therefore, that the measured increase in per capita expendi- tures since 1971 does represent an increase in public services and a response by local governments to increased demands for particular services.

The rigidity of revenue shares built into the Italian system of local finance and their failure to keep up with inflation after the reform coupled with the lack of constraints on spending decisions has clearly contributed to the incredible growth of local public deficits since 1971. Real local per capita public expenditures in Italy since 1971 have grown over and above what one would normally expect after adjusting for the effects of various demographic, socioeconomic and political influences. We have interpreted the effects of the reform as those of providing incentives to meet increased demands for local public services without comparison of marginal costs and benefits of such increased service levels. The increase in budget deficits has contributed to increases in the rate of inflation which has served as the mechanism in Italy to reallocate resources to the local public sector.

Although the Italian experience with general revenue sharing is surely colored by the institutional peculiarities of the Italian system, especially the inflexibility of the revenue shares and the absence of effective con- straints on local public spending, one may use the Italian results to offer some insights into the possible effects of increased revenue sharing in other nations. It is clear that any revenue sharing plan must be accompanied by some sort of mechanism to allow at least minimal comparison of benefits and costs of local public services at the local level to avoid the kind of explosion of local public budgets observed in Italy since the reform. The Italian system has financed increased public services in part through infla- tion creating a situation where local governments not increasing expenditures

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

14 G. Brosio, D.N. Hyman and W. Santagata

ran the risk of paying for more than their share of public services in other localities. Although the risk of local budget deficits is minimal in, for example, the United States due to various statutory constraints, the process by which resources would be reallocated to the local public sector in the absence of spending constraints could be similar but consist of increased (and perhaps explosive) allocations to the general revenue sharing fund with- out adequate consideration of the marginal benefits of increased local expenditure.

As a concluding comment, it may be noted that there is a general con- sensus in Italy today that the reform of local finance was misguided. Local finance in Italy has recently been 're-reformed' with restraints on local bor- rowing and limits on deficit spending by local governments.

Notes

1. For an analysis of the relationship between tax sharing schemes and budgetary choices, see Wagner (1976) and Munley and Green (1978). 2. See Bradford and Oates (1971) for a discussion of revenue sharing within the context of the theory of public choice. Most empirical analysis of revenue sharing in the United States has concentrated on its impact on the composition rather than the level of local public expenditure. See Juster (1977); and Nathan and Adams (1977). 3. This is true only for the initial period of the reform which this study covers. The shar- ing formulas may be modified by the Italian government at some time in the future. The goverment recently approved a 25 percent across-the-board increase in the fund for all local governments in 1977. 4. Before the reform local governments were limited in the kinds of taxes they could claim as backing for the borrowing. The reform allowed the entire revenue sharing allocation to the commune to be used as a basis for obtaining credit which significantly eased borrowing conditions. 5. For further discussion of deficit spending by local governments in Italy, see Hyman (1977). 6. See, for example, Giarda (1967), Bahl (1969), or Brazer (1959). 7. This variable provides an indication of the demands made on public services in order to dimension them to accommodate transient residents and visitors. The inclusion of this variable in previous studies (Brosio, 1975; and Bondonio, 1976) significantly improved the explanatory power of the model. 8. No official statistics exist on per capita income by city. We did run some regressions with an estimate of per capita income. In general, the sign on income was the same as revenue per capita, but the equations with revenue per capita gave better explanatory power.

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

Revenue sharing and local public spending 15

9. Although many have argued that partisan politics is not a significant determinant of local public services in Italy, recent analysis by Brosio (1976) has provided evidence to the contrary.

References

Bahl, Roy W. Metropolitan City Expenditures. Lexington, Kentucy: University of Ken- tucky Press, 1969.

Bondonio, P.V. 'Un aspetto del dualisimo: le finance comunali del Mezzogiorno.' Rassegna Economica 6, 1976.

Bradford, D. and Oates, W. 'An Analaysis of Revenue Sharing.' Quarterly Journal of Economics, August, 1971.

Brazer, Harvey E. City Expenditures in the United States. Occasional Paper 60, Nation- al Bureau of Economic Research, 1959.

Brosio, G., 'Composizione politica e comportamento di spesa degli enti locali italiani.' Economia Pubblica, 1976.

Brosio, G., D. Hyman and W. Santagata. 'Gli Enti Locali fra Riforma Tributaria, Inflazione e Movimenti Urbani: Un Contributo all'Analisi del Dissesto della Finanza Locale,' Fondazione Agnelli Quaderno, 24, 1978.

Giarda, P. 'Un analisi statistica sui determinanti delle spese degli enti locali', in Studi sulla finanza locale. Milan: Guiffre, 1967.

Hyman, D.N. 'La Finanza Locale: Un Confronto fra Gli Stati Uniti e L'Italia,' Quad- erni Sardi di Economia, 1, 1977.

Juster, F.T. (edo The Economic and Political Impact of General Revenue Sharing. Survey Research Center, Institute for Social Research, The University of Michigan, Ann Arbor, 1977.

Munley, Vincent C. and Kenneth V. Greene. 'Fiscal illusion, the nature of public goods and operation specification.' Public Choice 31 (1), 1978.

Nathan, R.P. and C.F. Adams and Associates. Revenue Sharing: The Second Round, The Brookings Institution, Washington, DC, 1977.

Wagner, Richard. 'Revenue Structure, Fiscal Illusion, and Budgetary Choice.' Public Choice 25 (Spring) 1976.

This content downloaded from 195.34.79.223 on Mon, 16 Jun 2014 16:11:47 PMAll use subject to JSTOR Terms and Conditions

![Competitive Target Advertising and Consumer Data Sharing · target advertising spending is projected to exceed $2.6 billion in 2014 [17]. investigation by the Wall Street Journal](https://img.dokumen.tips/doc/110x75/609c87261824582e15762910/competitive-target-advertising-and-consumer-data-sharing-target-advertising-spending.jpg)