Embed Size (px)

DESCRIPTION

Revenue Cycle

Citation preview

Accounting Information Systems,

6th

editionJames A. Hall

COPYRIGHT © 2009 South-Western, a division of Cengage Learning. Cengage Learning and South-Western are trademarks used herein under license

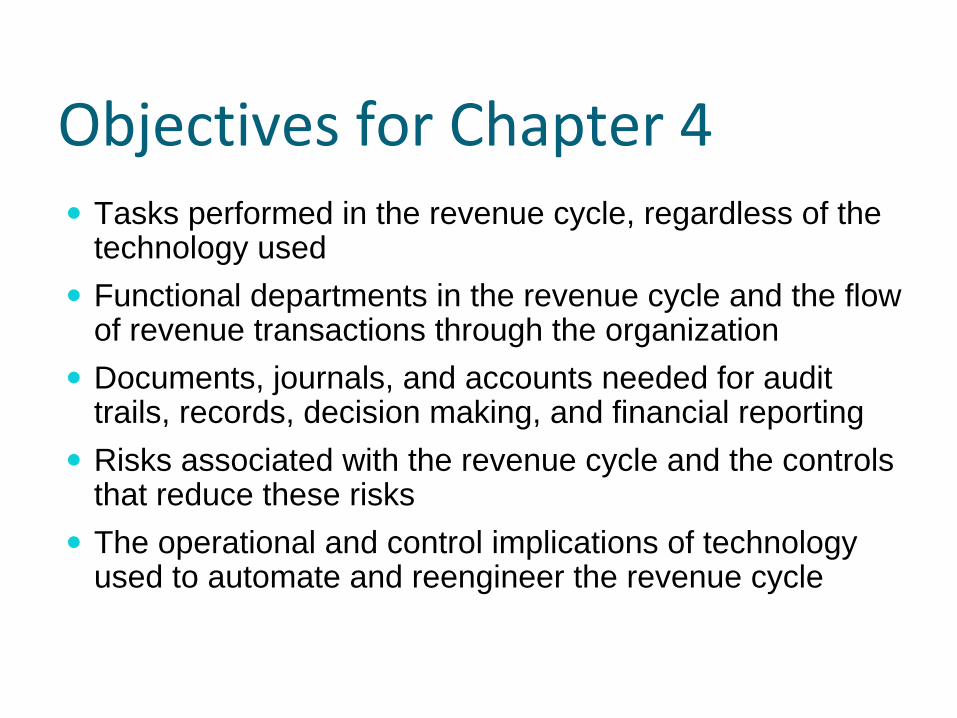

Objectives for Chapter 4Tasks performed in the revenue cycle, regardless of the technology usedFunctional departments in the revenue cycle and the flow of revenue transactions through the organizationDocuments, journals, and accounts needed for audit trails, records, decision making, and financial reportingRisks associated with the revenue cycle and the controls that reduce these risksThe operational and control implications of technology used to automate and reengineer the revenue cycle

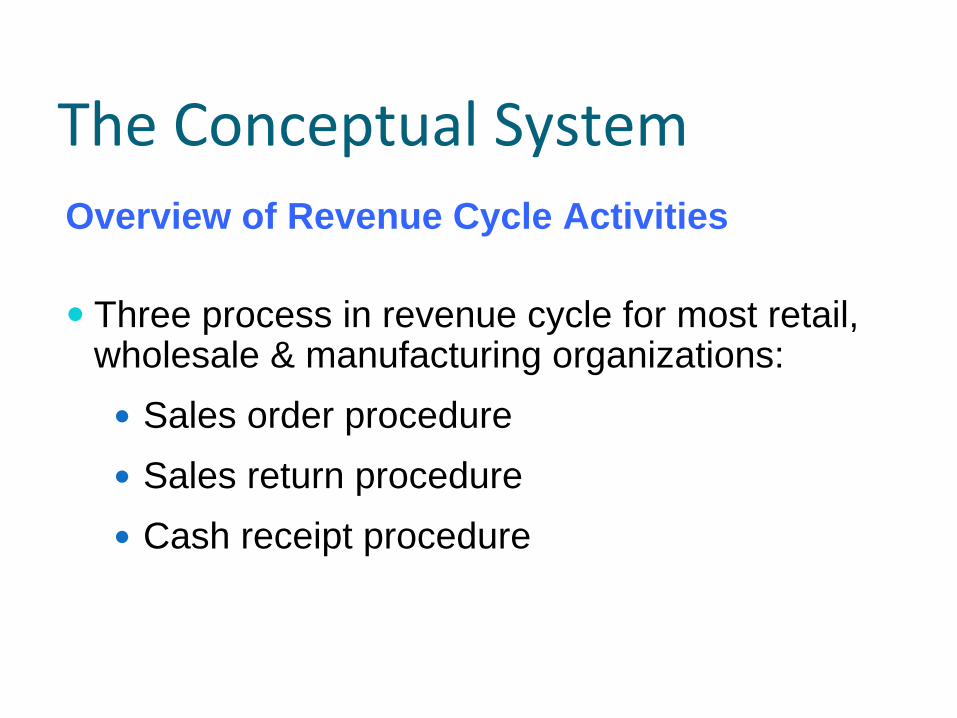

The Conceptual SystemOverview of Revenue Cycle Activities

Three process in revenue cycle for most retail, wholesale & manufacturing organizations:

Sales order procedureSales return procedureCash receipt procedure

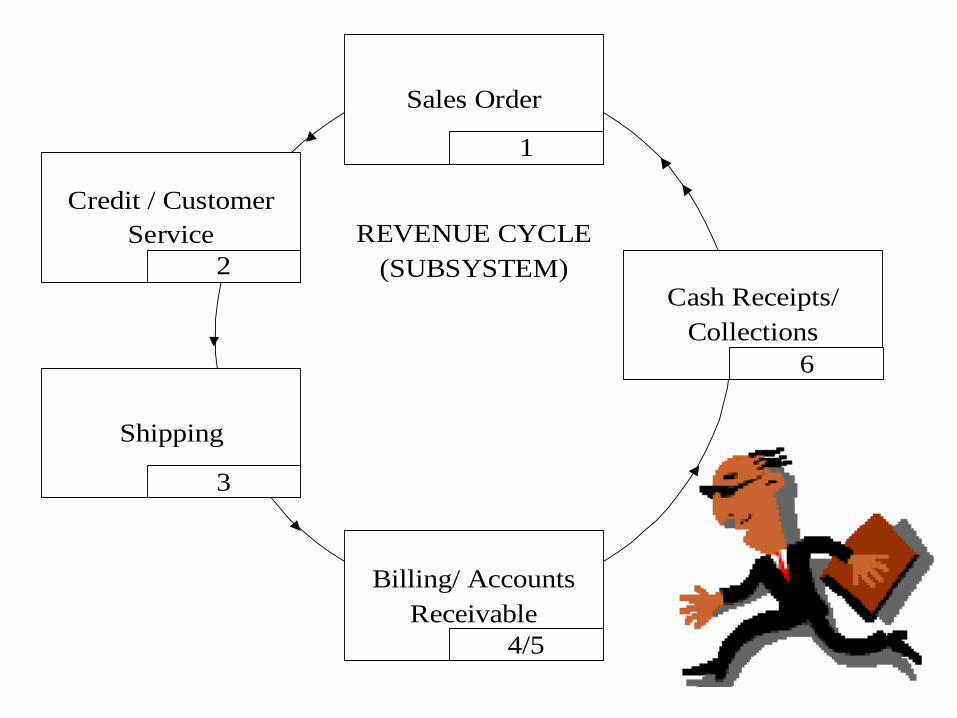

REVENUE CYCLE(SUBSYSTEM)

Sales Order

Billing/ AccountsReceivable

Cash Receipts/Collections

Shipping

1

6

4/5

3

Credit / CustomerService

2

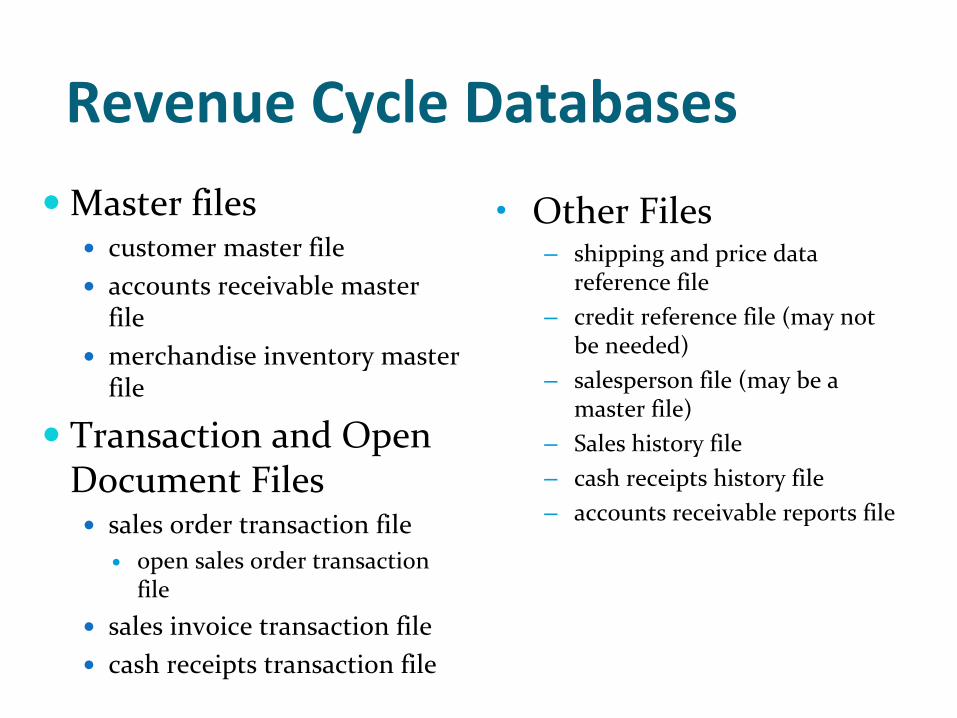

Revenue Cycle Databases

Master filescustomer master fileaccounts receivable master filemerchandise inventory master file

Transaction and Open Document Files

sales order transaction fileopen sales order transaction file

sales invoice transaction filecash receipts transaction file

•

Other Files– shipping and price data

reference file

– credit reference file (may not

be needed)

– salesperson file (may be a

master file)

– Sales history file– cash receipts history file– accounts receivable reports file

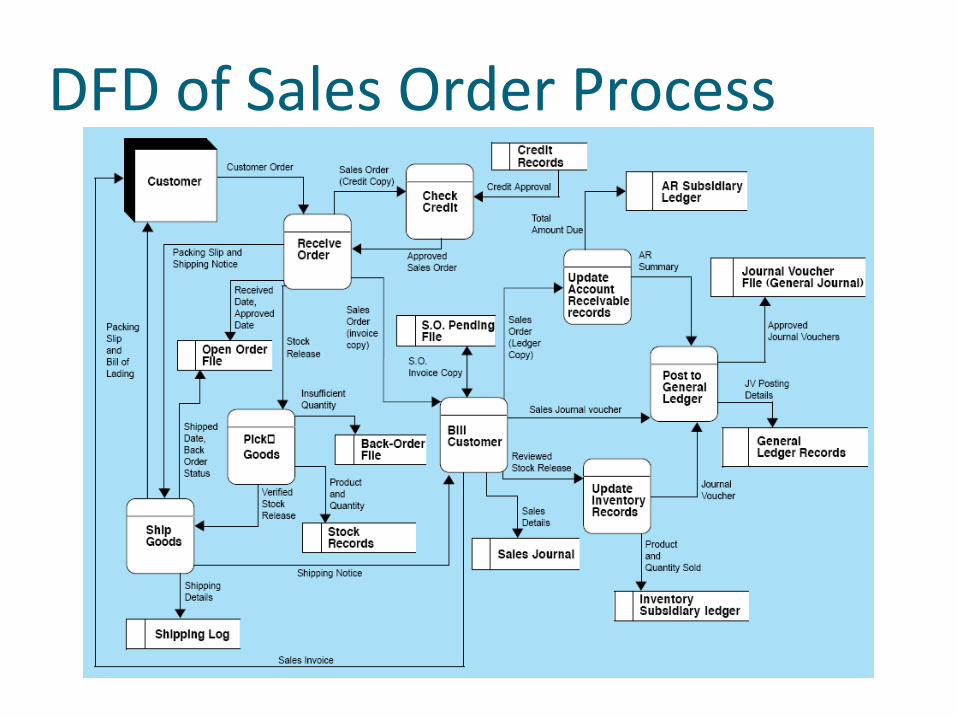

DFD of Sales Order Process

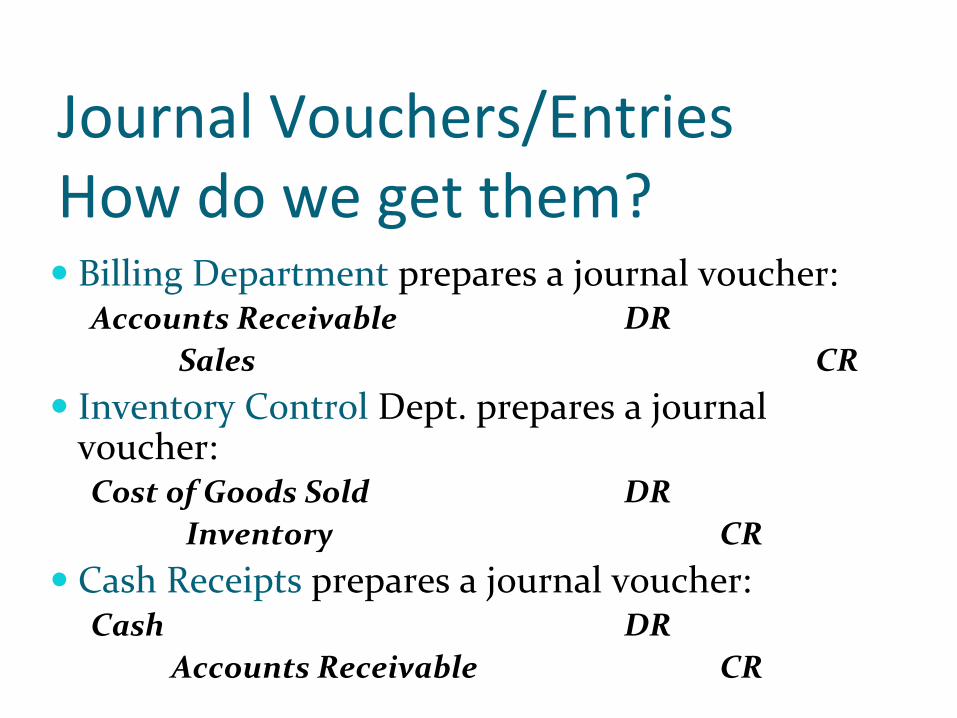

Journal Vouchers/Entries How do we get them?

Billing Department prepares a journal voucher:Accounts Receivable

DR

Sales

CRInventory Control Dept. prepares a journal voucher:Cost of Goods Sold

DR

Inventory

CRCash Receipts prepares a journal voucher:Cash

DR

Accounts Receivable

CR

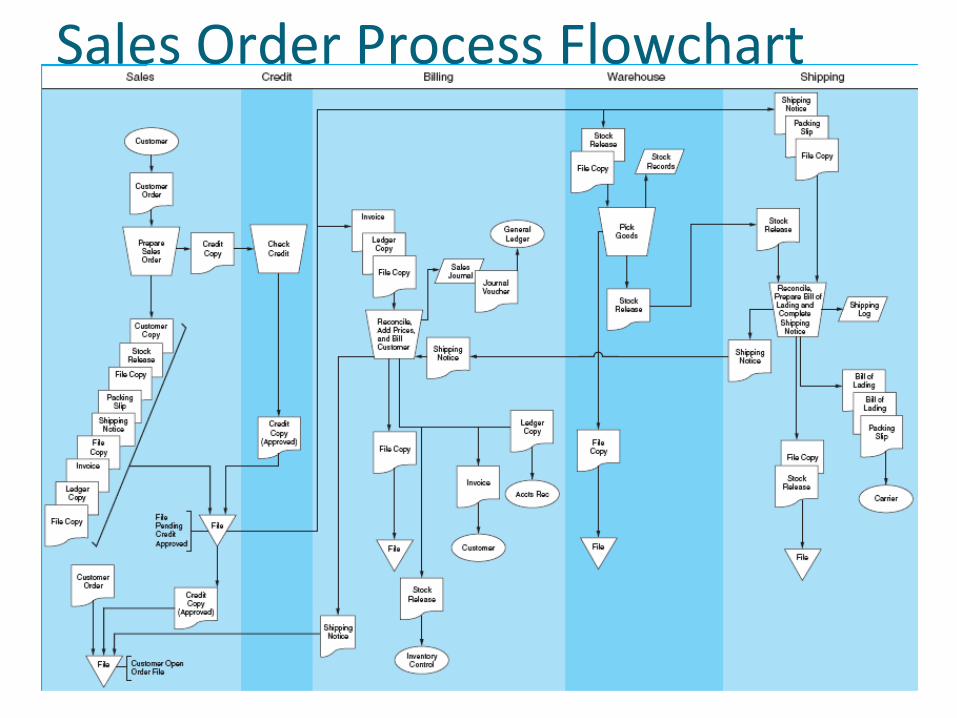

Sales Order Process Flowchart

Sales Order Process Flowchart

Manual Sales Order Processing

Begins with a customer placing an orderThe sales department captures the essential details on a sales order form.

The transaction is authorized by obtaining credit approval by the credit department.Sales information is released to:

BillingWarehouse (stock release or picking ticket)Shipping (packing slip and shipping notice)

The merchandise is picked from the Warehouse and sent to Shipping.

Stock records are adjusted.The merchandise, packing slip, and bill of lading are prepared by Shipping and sent to the customer.

Shipping reconciles the merchandise received from the Warehouse with the sales information on the packing slip.

Shipping information is sent to Billing. Billing compiles and reconciles the relevant facts and issues an invoice to the customer and updates the sales journal. Information is transferred to:

Accounts Receivable (A/R)Inventory Control

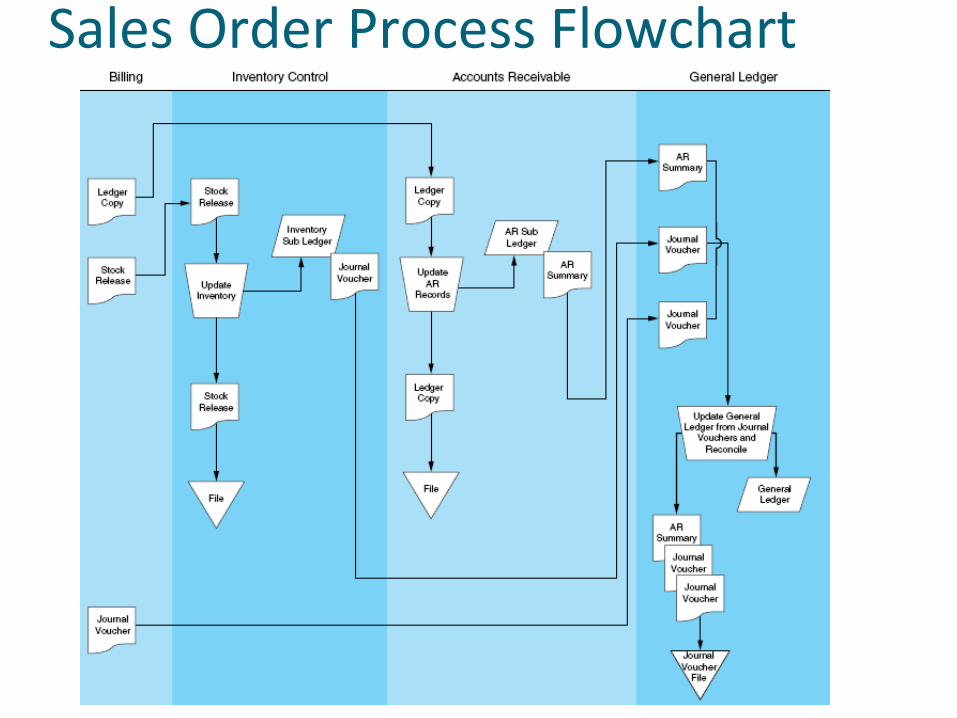

Manual Sales Order Processing

A/R records the information in the customer’s account in the accounts receivable subsidiary ledger.Inventory Control adjusts the inventory subsidiary ledger.Billing, A/R, and Inventory Control submits summary information to the General Ledger dept., which then reconciles this data and posts to the control accounts in the G/L.

Manual Sales Order Processing

The company shipped the customer the wrong merchandise.The goods were defective.The product was damage in shipment.The buyer refused delivery because the seller shipped the goods too late or they were delayed in transit.

Sales Returns Procedures

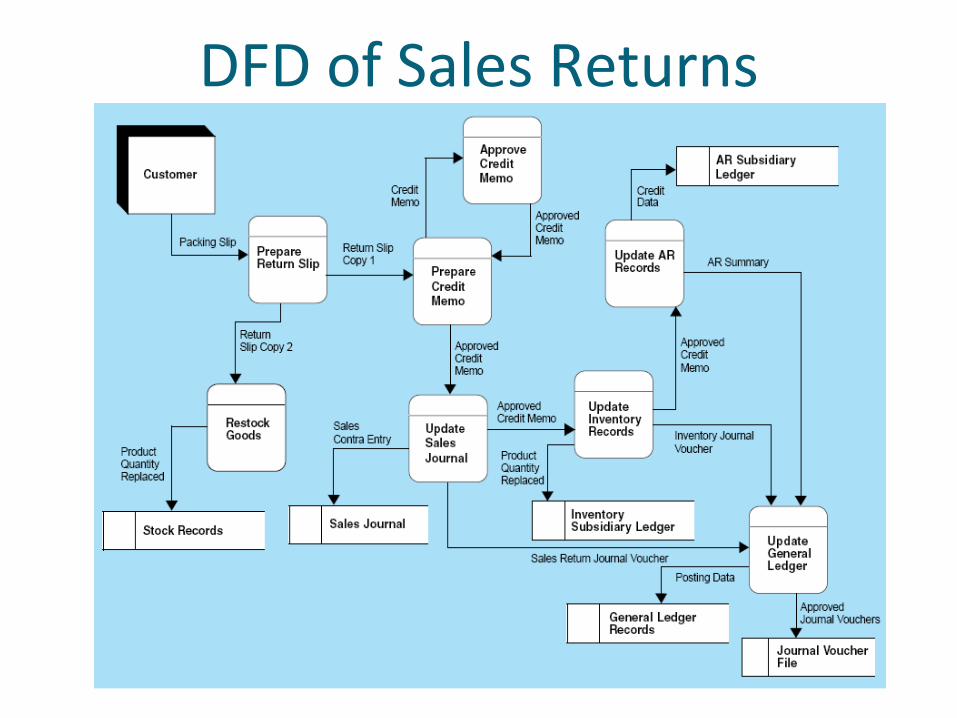

DFD of Sales Returns

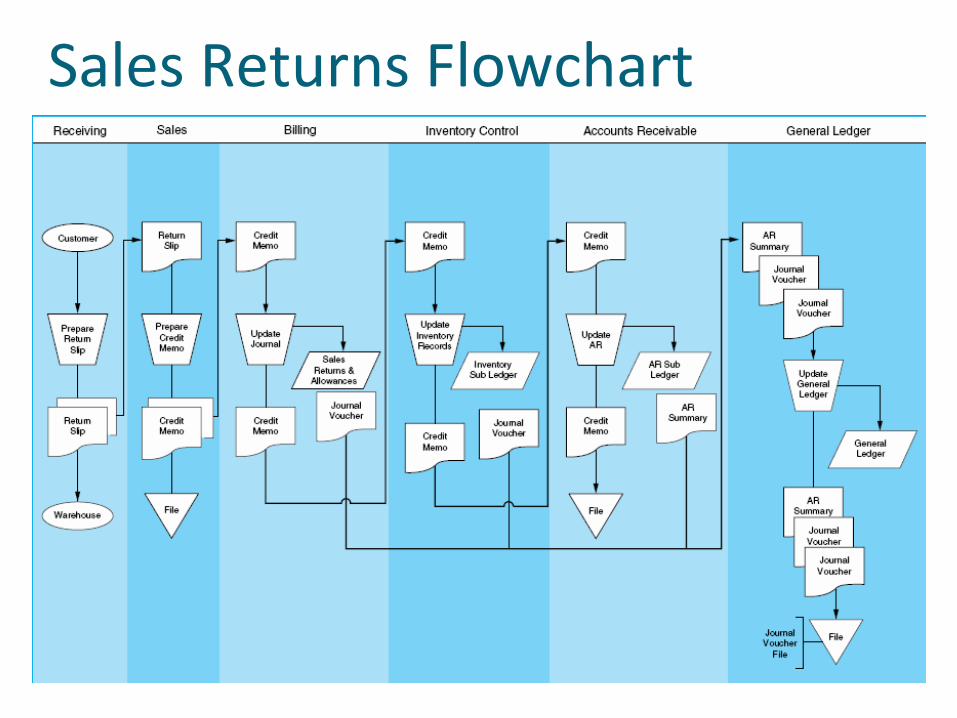

Sales Returns Flowchart

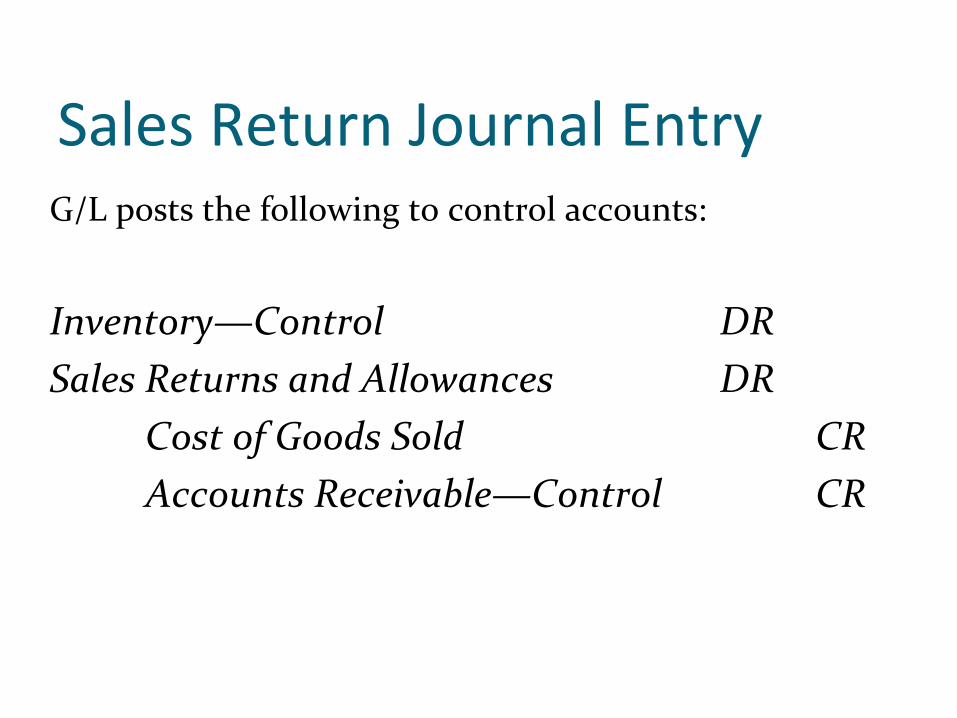

Sales Return Journal EntryG/L posts the following to control accounts:

Inventory—Control

DRSales Returns and Allowances

DR

Cost of Goods Sold

CRAccounts Receivable—Control

CR

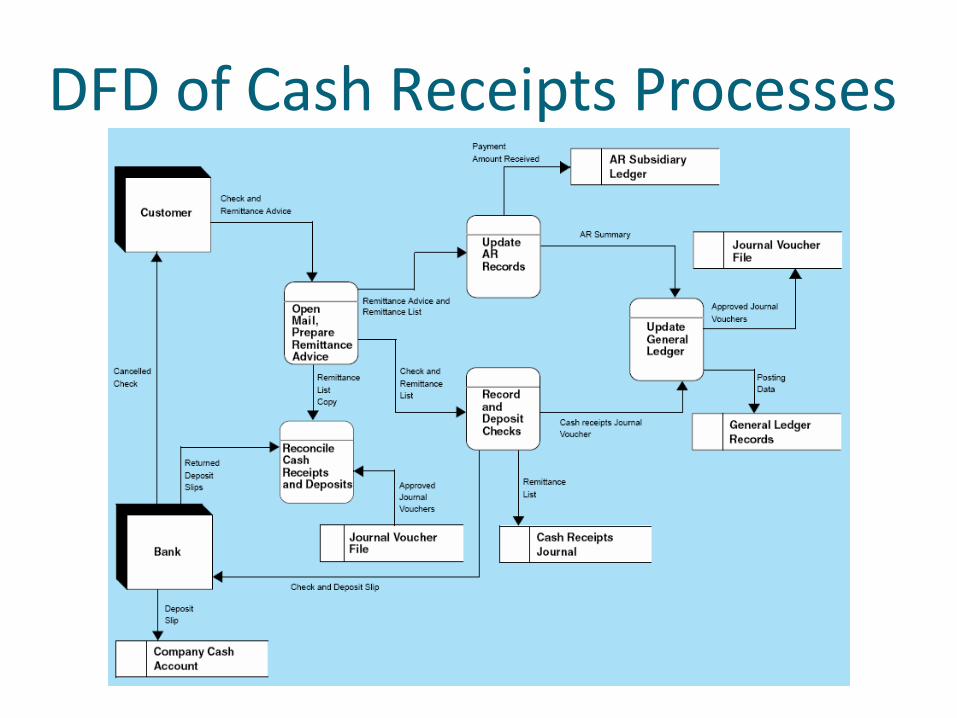

DFD of Cash Receipts Processes

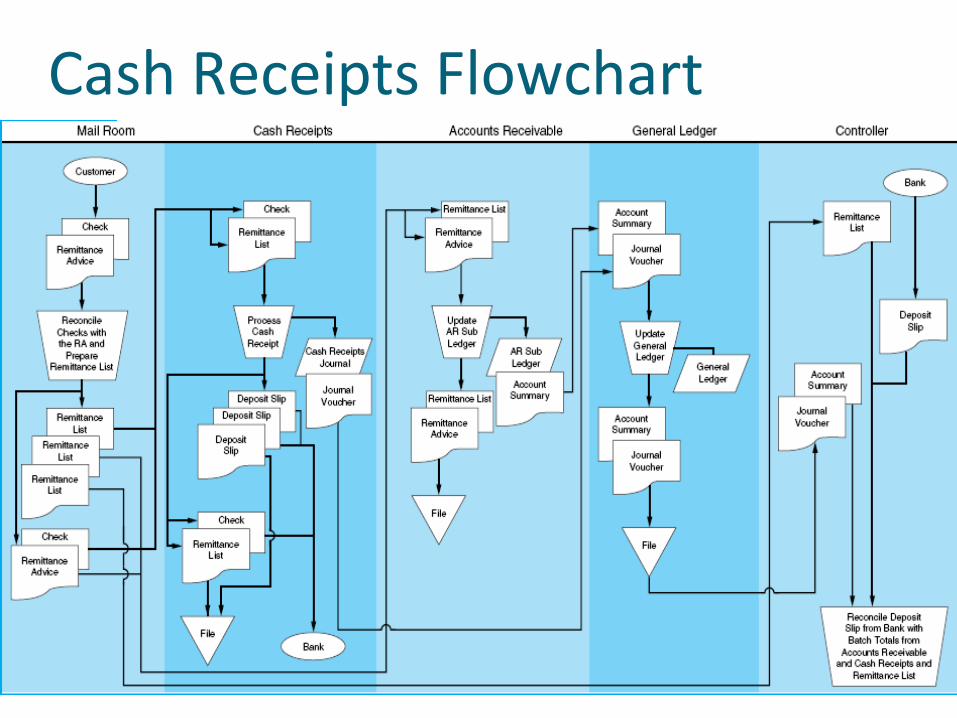

Cash Receipts Flowchart

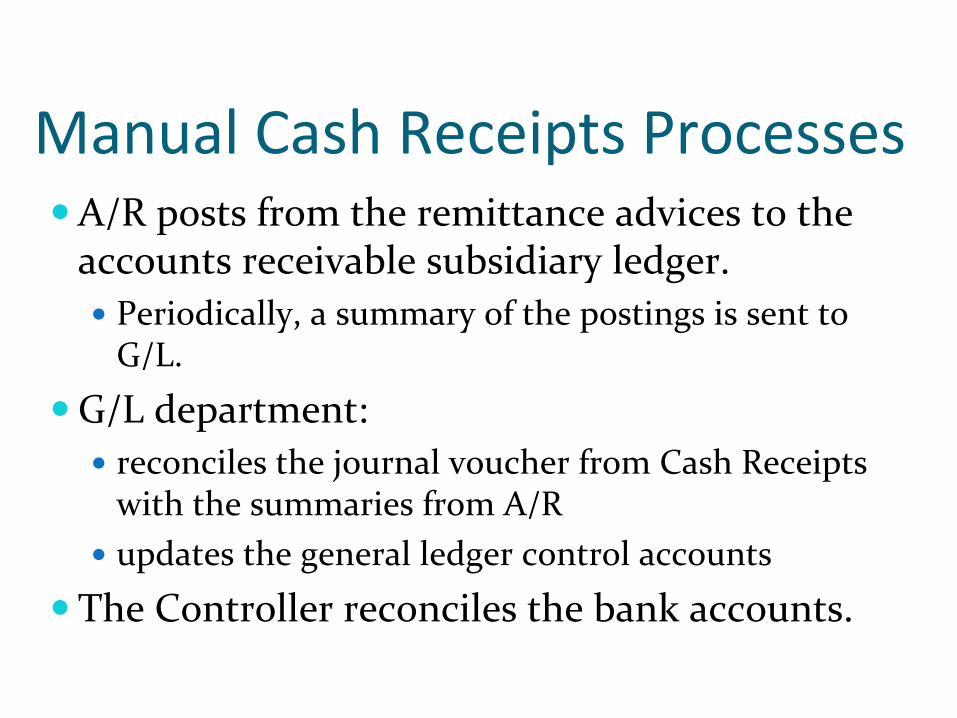

Manual Cash Receipts ProcessesCustomer checks and remittance advices are received in the Mail Room.

A mail room clerk prepares a cash prelist and sends the prelist and the checks to Cash Receipts. The cash prelist is also sent to A/R and the Controller.

Cash Receipts: verifies the accuracy and completeness of the checksupdates the cash receipts journalprepares a deposit slipprepares a journal voucher to send to G/L

A/R posts from the remittance advices to the accounts receivable subsidiary ledger.

Periodically, a summary of the postings is sent to G/L.

G/L department:reconciles the journal voucher from Cash Receipts with the summaries from A/R updates the general ledger control accounts

The Controller reconciles the bank accounts.

Manual Cash Receipts Processes

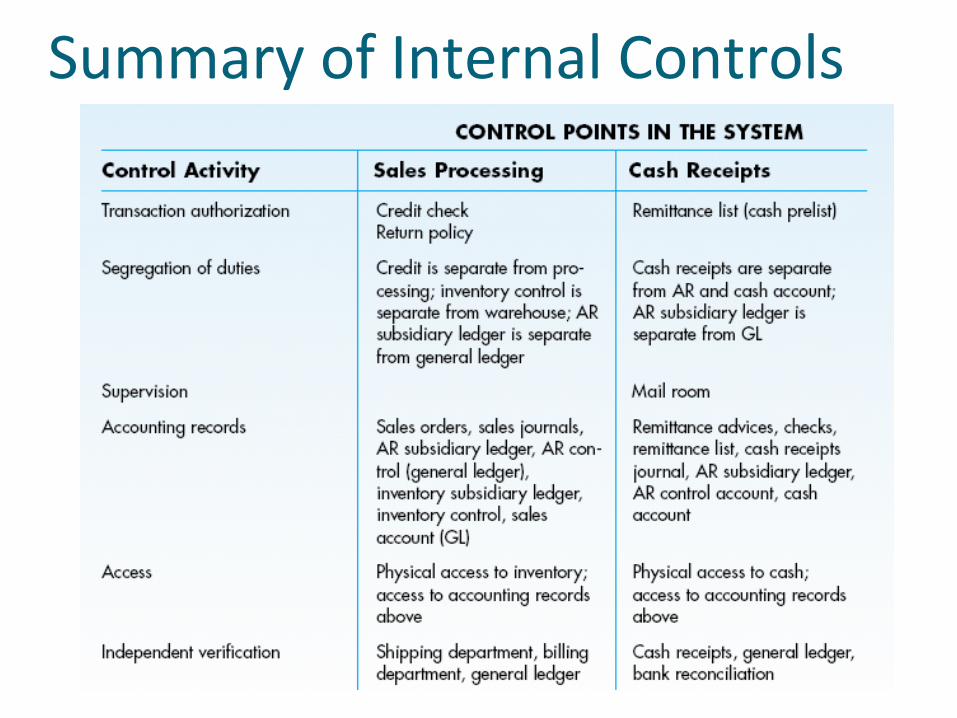

Summary of Internal Controls

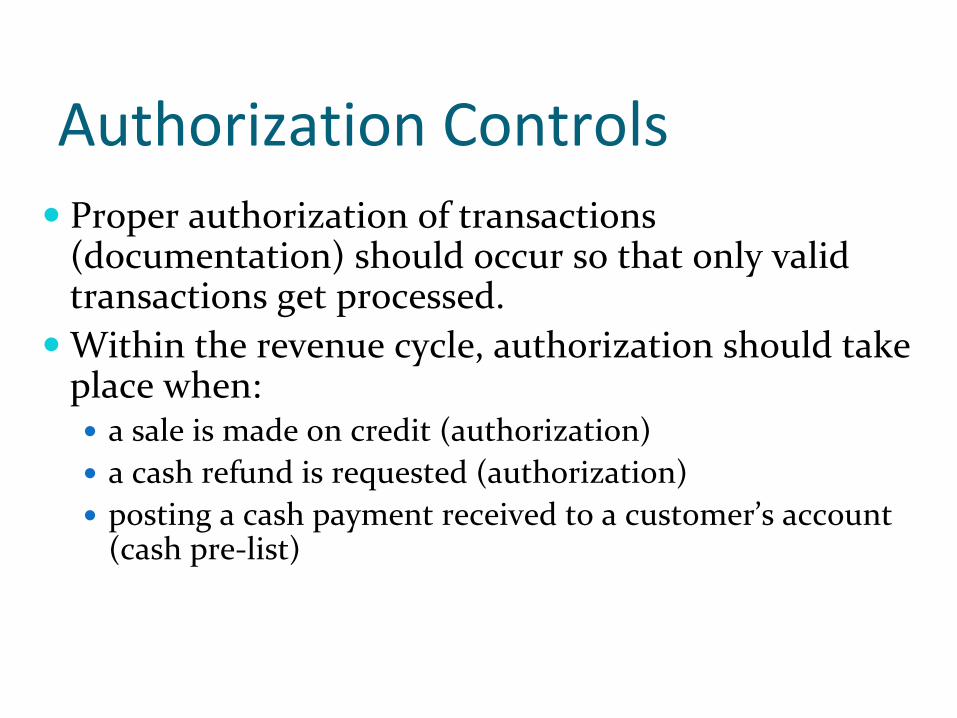

Authorization ControlsProper authorization of transactions (documentation) should occur so that only valid transactions get processed.Within the revenue cycle, authorization should take place when:

a sale is made on credit (authorization)a cash refund is requested (authorization)posting a cash payment received to a customer’s account (cash pre‐list)

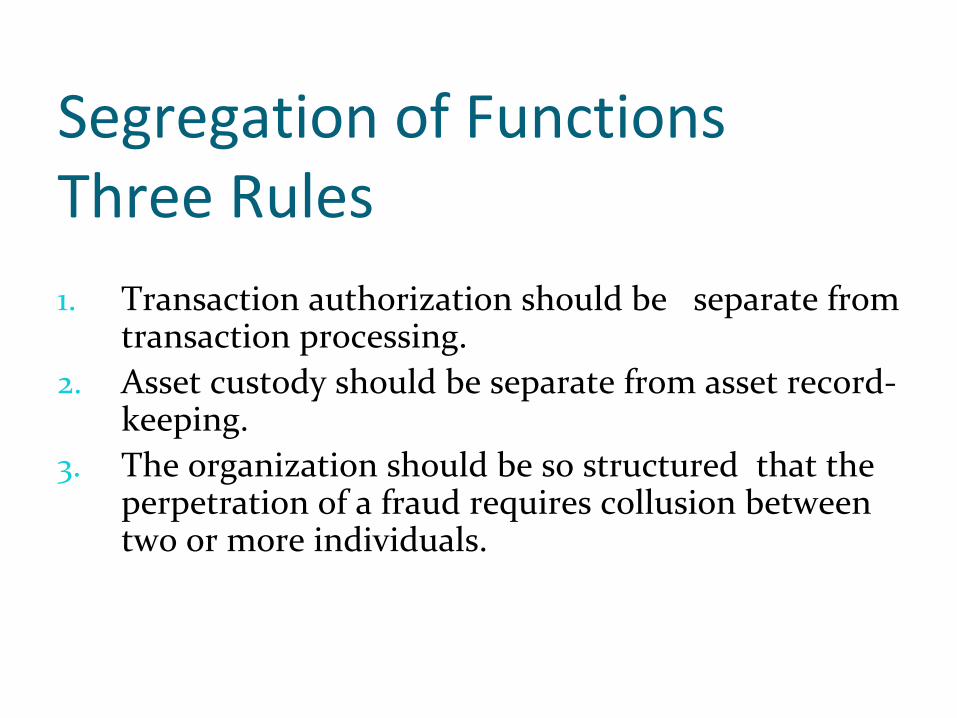

Segregation of Functions Three Rules

1. Transaction authorization should be separate from

transaction processing.2.

Asset custody should be separate from asset record‐

keeping.3.

The organization should be so structured that the

perpetration of a fraud requires collusion between two or more individuals.

Segregation of FunctionsSales Order Processing

credit authorization separate from SO processinginventory control separate from warehouseaccounts receivable sub‐ledger separate from general ledger control account

Cash Receipts Processingcash receipts separate from accounting recordsaccounts receivable sub‐ledger separate from general ledger

Supervision

Often used when unable to enact appropriate segregation of duties. Supervision of employees serves as a deterrent to dishonest acts and is particularly important in the mailroom.

Accounting Records

With a properly maintained audit trail, it is possible to track transactions through the systems and to find where and when errors were made:

pre‐numbered source documentsspecial journalssubsidiary ledgersgeneral ledgerfiles

Access Controls

Access to assets and information (accounting records) should be limited.Within the revenue cycle, the assets to protect are cash and inventories and access to records such as the accounts receivable subsidiary ledger and cash journalshould be restricted.

Independent VerificationPhysical procedures as well as record‐keeping should be independently reviewed at various points in the system to check for accuracy and completeness:

shipping verifies the goods sent from the warehouse are correct in type and quantitywarehouse reconciles the stock release document (picking slip) and packing slip billing reconciles the shipping notice with the sales invoicegeneral ledger reconciles journal vouchers from billing, inventory control, cash receipts, and accounts receivable

Automating the Revenue CycleAuthorizations and data access can be performed through computer screens. There is a decrease in the amount of paper.The manual journals and ledgers are changed to disk or tape transaction and master files. Input is still typically from a hard copy document and goes through one or more computerized processes. Processes store data in electronic files (the tape or disk) or prepare data in the form of a hardcopy report.

Automating the Revenue CycleRevenue cycle programs can include:

formatted screens for collecting data edit checks on the data entered instructions for processing and storing the datasecurity procedures (passwords or user IDs) steps for generating and displaying output

To understand files, you must consider the record design and layout. The documents and the files used as input sources must contain the data necessary to generate the output reports.

Computer‐Based Accounting Systems

CBAS technology can be viewed as a continuum with two extremes:

automation ‐ use technology to improve efficiency and effectiveness reengineering – use technology to restructure business processes and firm organization

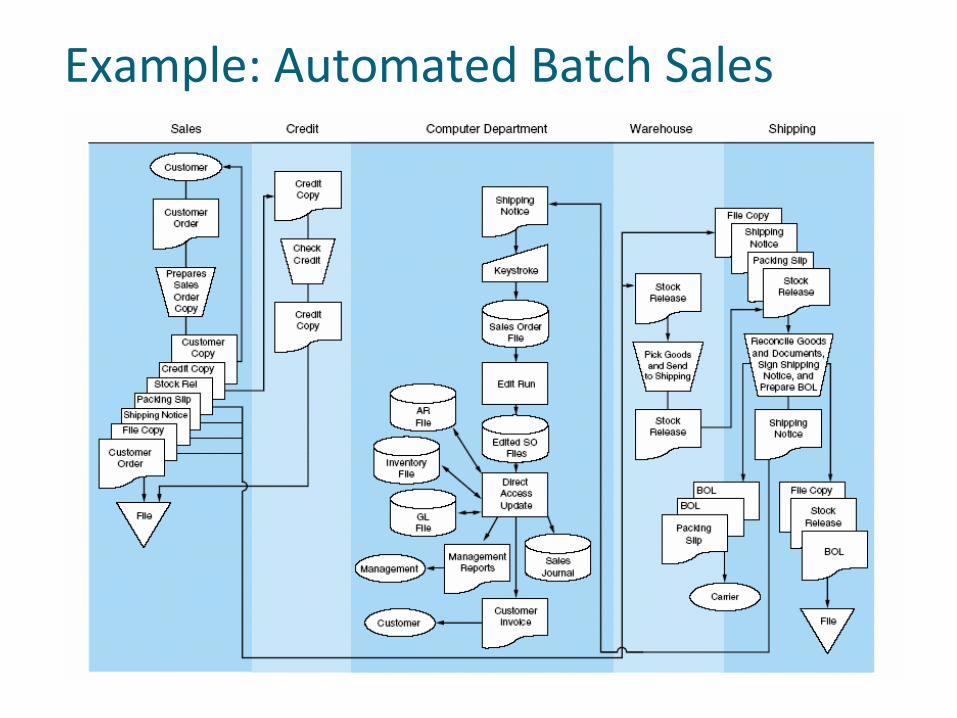

Example: Automated Batch Sales

Reengineering Sales Order Processing Using Real‐Time Technology

Manual procedures and physical documents are replaced by interactive computer terminals.Real time input and output occurs, with some master files still being updated using batches.

Real‐time ‐ entry of customer order, printout of stock release, packing slip and bill of lading; update of credit file, inventory file, and open sales orders fileBatch ‐ printout of invoice, update of closed sales order (journal), accounts receivable and general ledger control account

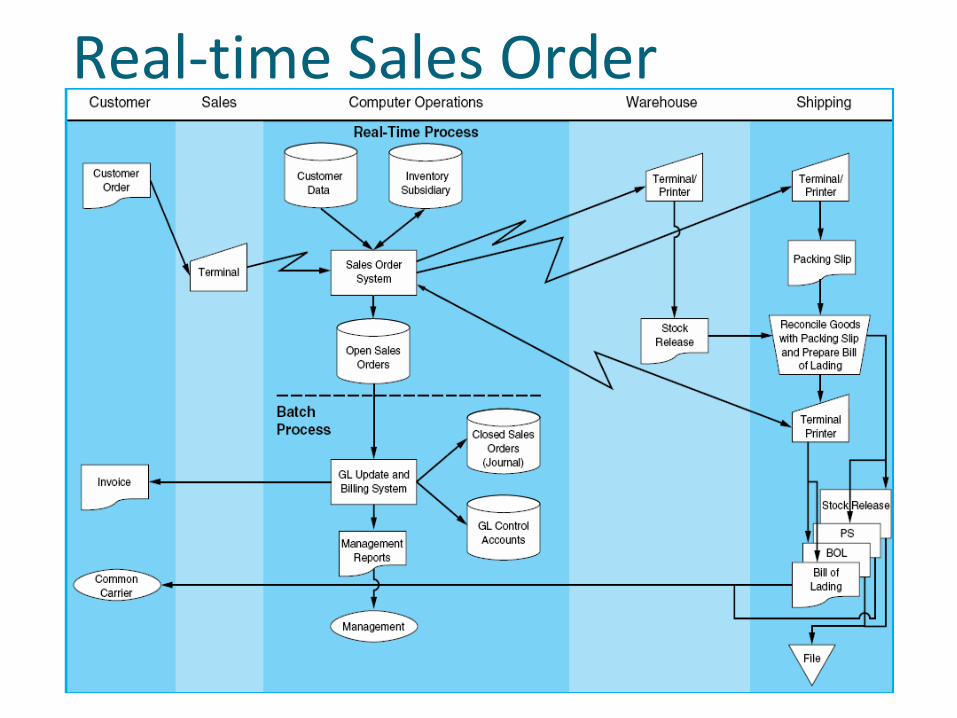

Real‐time Sales Order

Advantages of Real‐Time Processing

Shortens the cash cycle of the firm by reducing the time between the order date and billing date Better inventory management which can lead to a competitive advantageFewer clerical errors, reducing incorrect items being shipped and bill discrepanciesReduces the amount of expensive paper documents and their storage costs

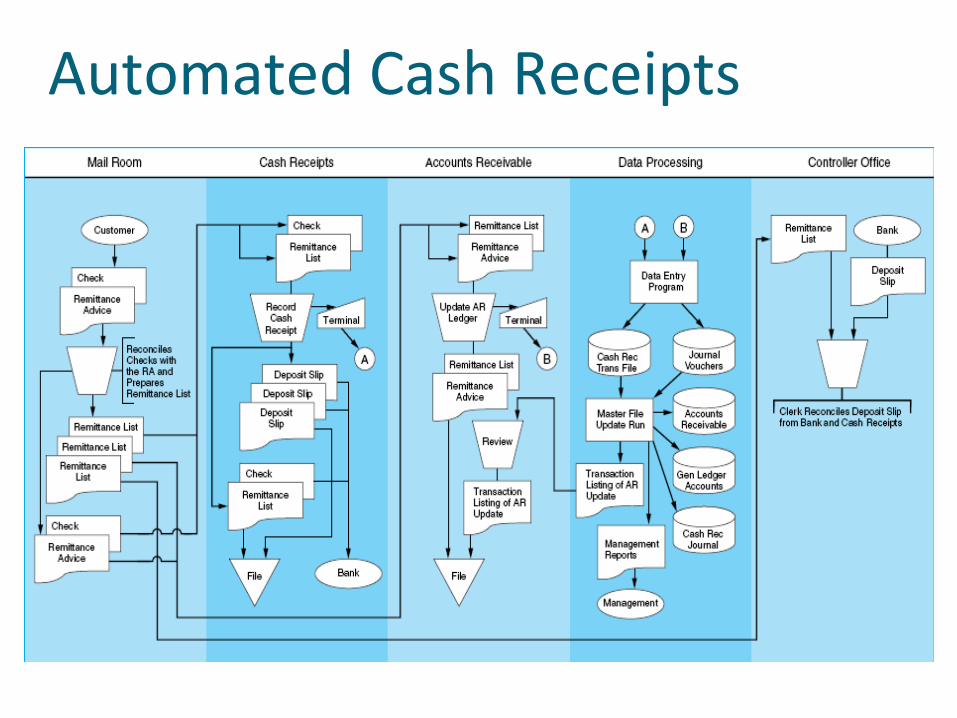

Reengineered Cash Receipts

The mail room is a frequent target for reengineering. Companies send their customers preprinted envelopes and remittance advices. Upon receipt, these envelopes are scanned to provides a control procedure against theft.Machines are open the envelopes, scan remittance advices and checks, and separate the checks.Artificial intelligence may be used to read handwriting, such as remittance amounts and signatures.

Automated Cash Receipts

Point‐of‐Sale SystemsPoint of sale systems are used extensively in retail establishments.

Customers pick the inventory from the shelves and take them to acashier.

Daily ProcedureThe clerk scans the universal product code (UPC). The POS system is connected to an inventory file, where the price and description are retrieved.

The inventory levels are updated and reorder needs can immediately be detected.

Point‐of‐Sale SystemsThe system computes the amount due. Payment is either cash, check, ATM or credit card in most cases.

No accounts receivables

If checks, ATM or credit cards are used, an on‐line link to receive approval is necessary.

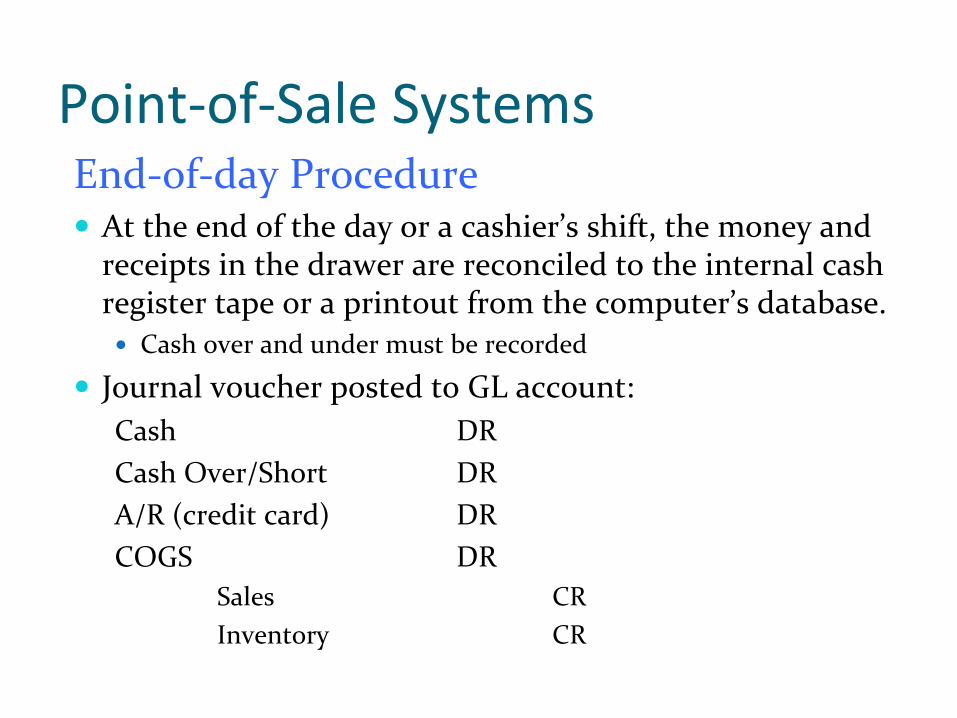

Point‐of‐Sale SystemsEnd‐of‐day ProcedureAt the end of the day or a cashier’s shift, the money and receipts in the drawer are reconciled to the internal cash register tape or a printout from the computer’s database.

Cash over and under must be recorded

Journal voucher posted to GL account:Cash

DR

Cash Over/Short

DR

A/R (credit card)

DR

COGS

DR

Sales

CRInventory

CR

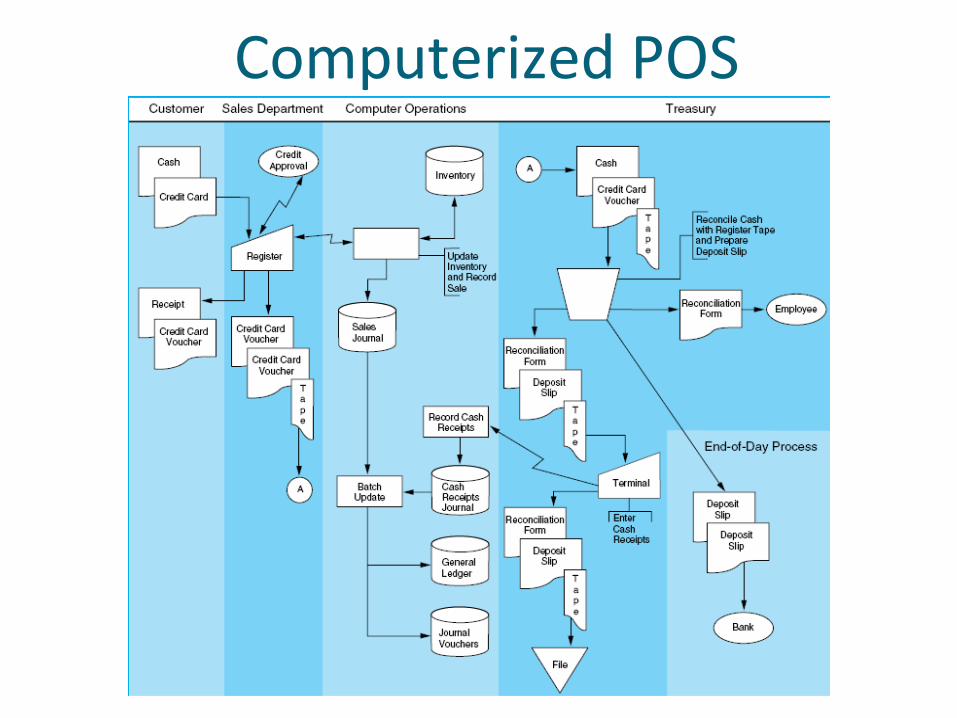

Computerized POS

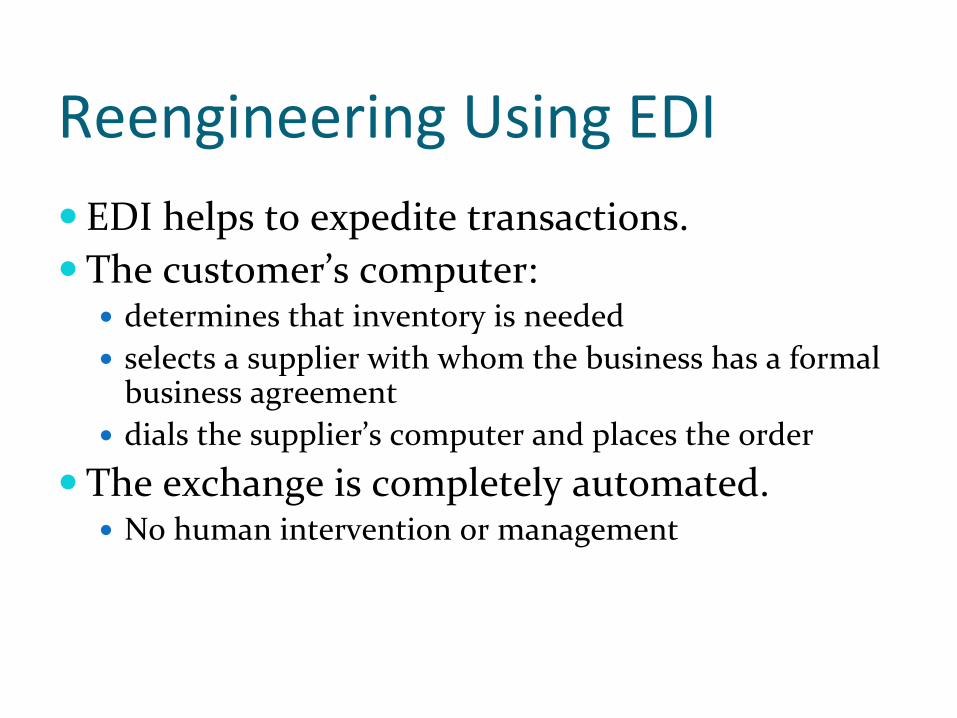

Reengineering Using EDIEDI helps to expedite transactions.The customer’s computer:

determines that inventory is neededselects a supplier with whom the business has a formal business agreementdials the supplier’s computer and places the order

The exchange is completely automated.No human intervention or management

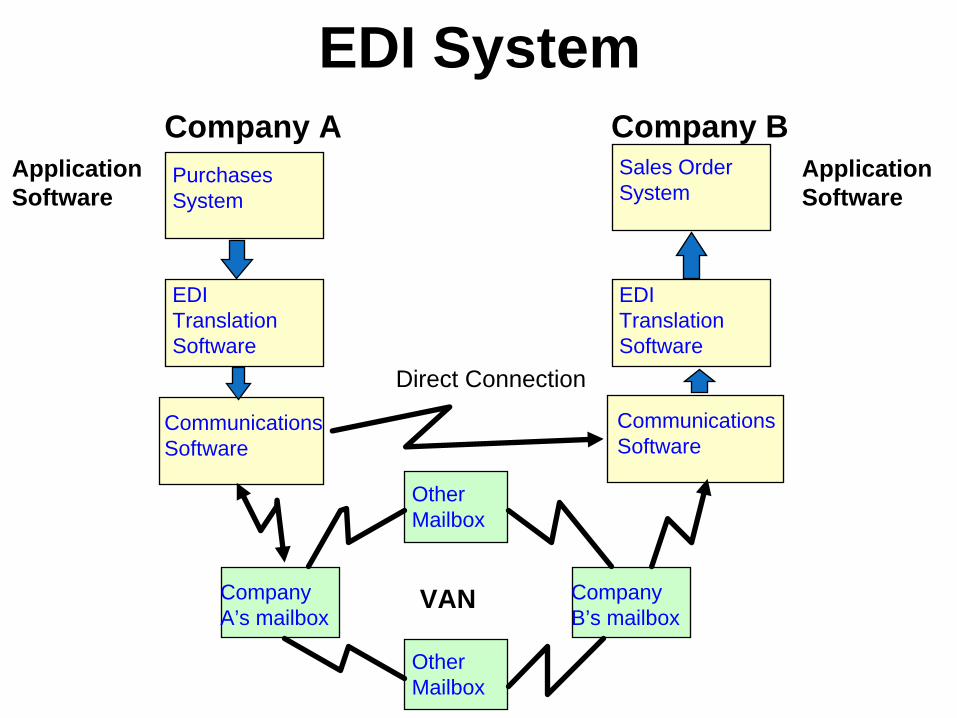

EDI System

PurchasesSystem

EDI TranslationSoftware

EDI TranslationSoftware

CommunicationsSoftware

CommunicationsSoftware

OtherMailbox

OtherMailbox

CompanyA’s mailbox

CompanyB’s mailbox

Sales OrderSystem

ApplicationSoftware

ApplicationSoftware

Direct Connection

VAN

Company A Company B

Reengineering Using the Internet

Typically, no formal business agreements exist as they do in EDI.Most orders are made with credit cards.Mainly done with e‐mail systems, and thus a turnaround time is necessary

Intelligent agents are needed to eliminate this time lag.Security and control over data is a concern with Internet transactions.

CBAS Control ConsiderationsAuthorization ‐ in real‐time systems, authorizations are automated

Programmed decision rules must be closely monitored.Segregation of Functions ‐ consolidation of tasks by the computer is common

Protect the computer programsCoding, processing, and maintenance should be separated.

Supervision ‐ in POS systems, the cash register’s internal tape or database is an added form of supervisionAccess Control ‐magnetic records are vulnerable to both authorized and unauthorized exposure and should be protected

Must have limited file accessibilityMust safeguard and monitor computer programs

CBAS Control Considerations

Accounting Records ‐ rest on reliability and security of stored digitalized data

Accountants should be skeptical about the accuracy of hard‐copy printouts.Backups ‐ the system needs to ensure that backups of all files are continuously kept

Independent Verification – consolidating accounting tasks under one computer program can remove traditional independent verification controls. To counter this problem:

perform batch control balancing after each run produce management reports and summaries for end users to review

CBAS Control Considerations

PC‐Based Accounting SystemsUsed by small firms and some large decentralized firmsAllow one or few individuals to perform entire accounting functionMost systems are divided into modules controlled by a menu‐driven program:

general ledgerinventory controlpayrollcash disbursementspurchases and accounts payablecash receiptssales order

PC Control IssuesSegregation of Duties ‐ tend to be inadequate and should be compensated for with increased supervision, detailed management reports, and frequent independent verificationAccess Control ‐ access controls to the data stored on the computer tends to be weak; methods such as encryption and disk locking devices should be usedAccounting Records ‐ computer disk failures cause data losses; external backup methods need to be implemented to allow data recovery

Internal Control

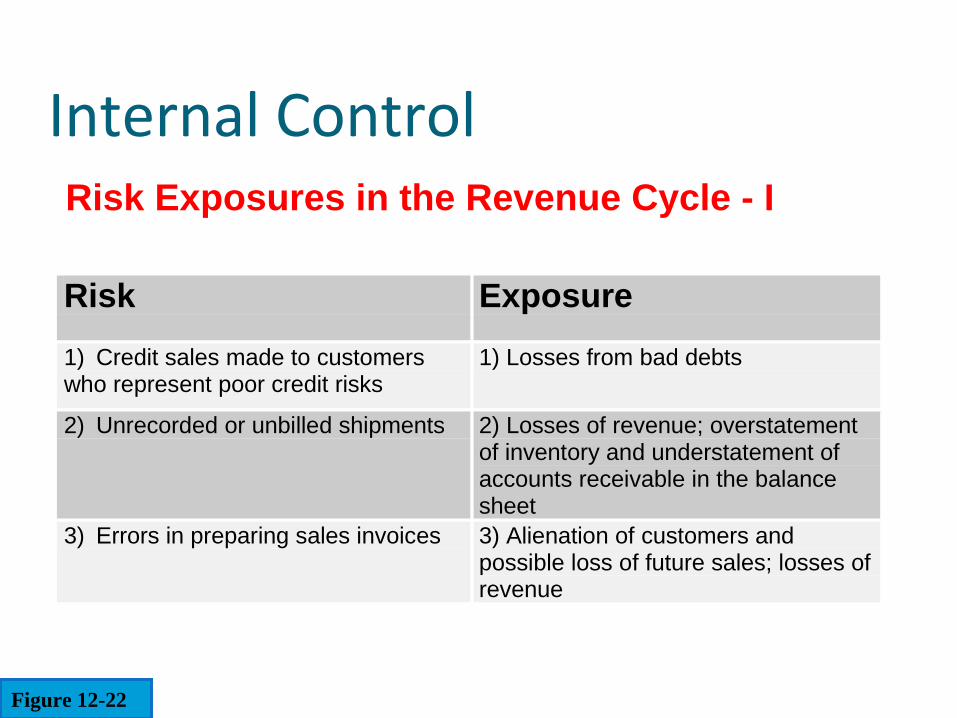

Risk Exposure 1) Credit sales made to customers who represent poor credit risks 1) Losses from bad debts 2) Unrecorded or unbilled shipments 2) Losses of revenue; overstatement

of inventory and understatement of accounts receivable in the balance sheet

3) Errors in preparing sales invoices 3) Alienation of customers and possible loss of future sales; losses of revenue

Figure 12-22

Risk Exposures in the Revenue Cycle - I

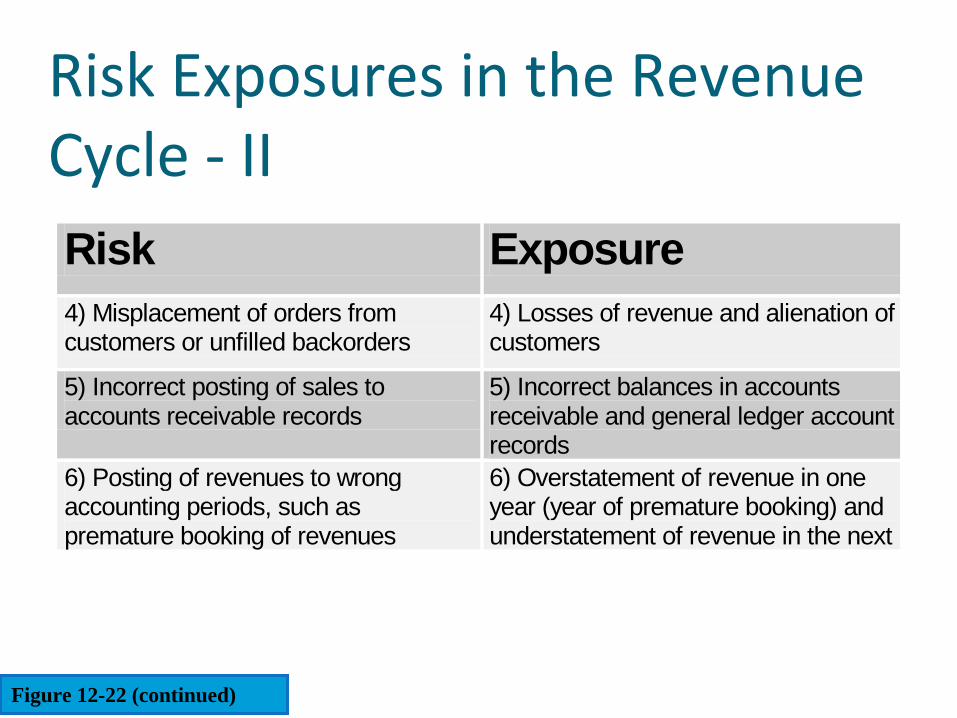

Risk Exposure 4) Misplacement of orders from customers or unfilled backorders

4) Losses of revenue and alienation of customers

5) Incorrect posting of sales to accounts receivable records

5) Incorrect balances in accounts receivable and general ledger account records

6) Posting of revenues to wrong accounting periods, such as premature booking of revenues

6) Overstatement of revenue in one year (year of premature booking) and understatement of revenue in the next

Figure 12-22 (continued)

Risk Exposures in the Revenue Cycle ‐

II

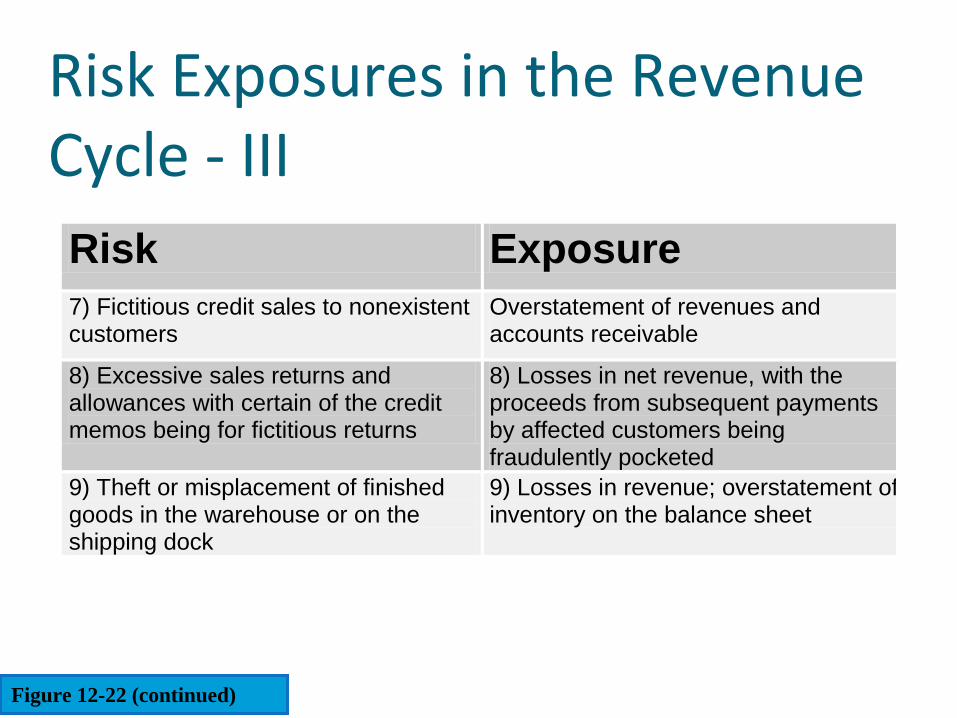

Risk Exposure 7) Fictitious credit sales to nonexistent customers

Overstatement of revenues and accounts receivable

8) Excessive sales returns and allowances with certain of the credit memos being for fictitious returns

8) Losses in net revenue, with the proceeds from subsequent payments by affected customers being fraudulently pocketed

9) Theft or misplacement of finished goods in the warehouse or on the shipping dock

9) Losses in revenue; overstatement ofinventory on the balance sheet

Figure 12-22 (continued)

Risk Exposures in the Revenue Cycle ‐

III

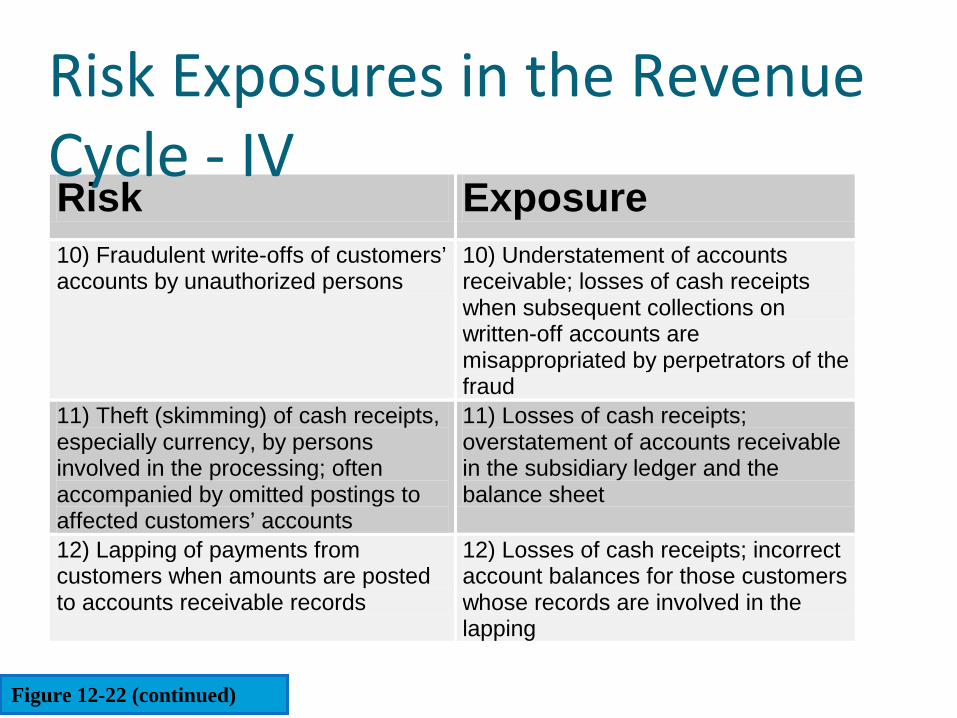

Risk Exposure 10) Fraudulent write-offs of customers’ accounts by unauthorized persons

10) Understatement of accounts receivable; losses of cash receipts when subsequent collections on written-off accounts are misappropriated by perpetrators of the fraud

11) Theft (skimming) of cash receipts, especially currency, by persons involved in the processing; often accompanied by omitted postings to affected customers’ accounts

11) Losses of cash receipts; overstatement of accounts receivable in the subsidiary ledger and the balance sheet

12) Lapping of payments from customers when amounts are posted to accounts receivable records

12) Losses of cash receipts; incorrect account balances for those customers whose records are involved in the lapping

Figure 12-22 (continued)

Risk Exposures in the Revenue Cycle ‐

IV

Risk Exposures in the Revenue Cycle ‐

V

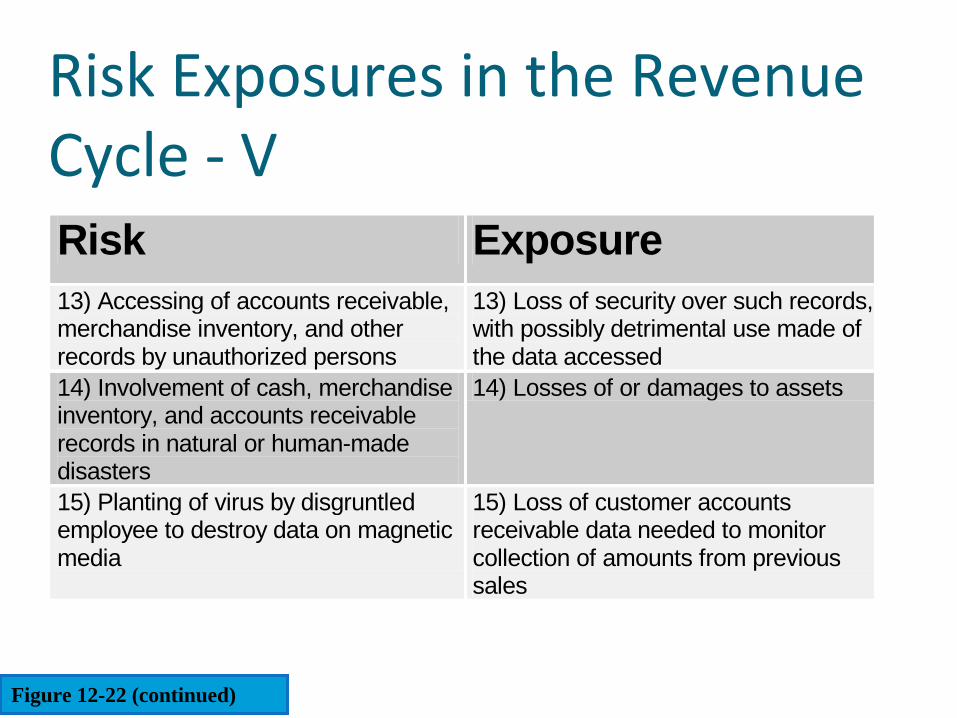

Risk Exposure 13) Accessing of accounts receivable, merchandise inventory, and other records by unauthorized persons

13) Loss of security over such records, with possibly detrimental use made of the data accessed

14) Involvement of cash, merchandise inventory, and accounts receivable records in natural or human-made disasters

14) Losses of or damages to assets

15) Planting of virus by disgruntled employee to destroy data on magnetic media

15) Loss of customer accounts receivable data needed to monitor collection of amounts from previous sales

Figure 12-22 (continued)

Risk Exposures in the Revenue Cycle ‐

VI

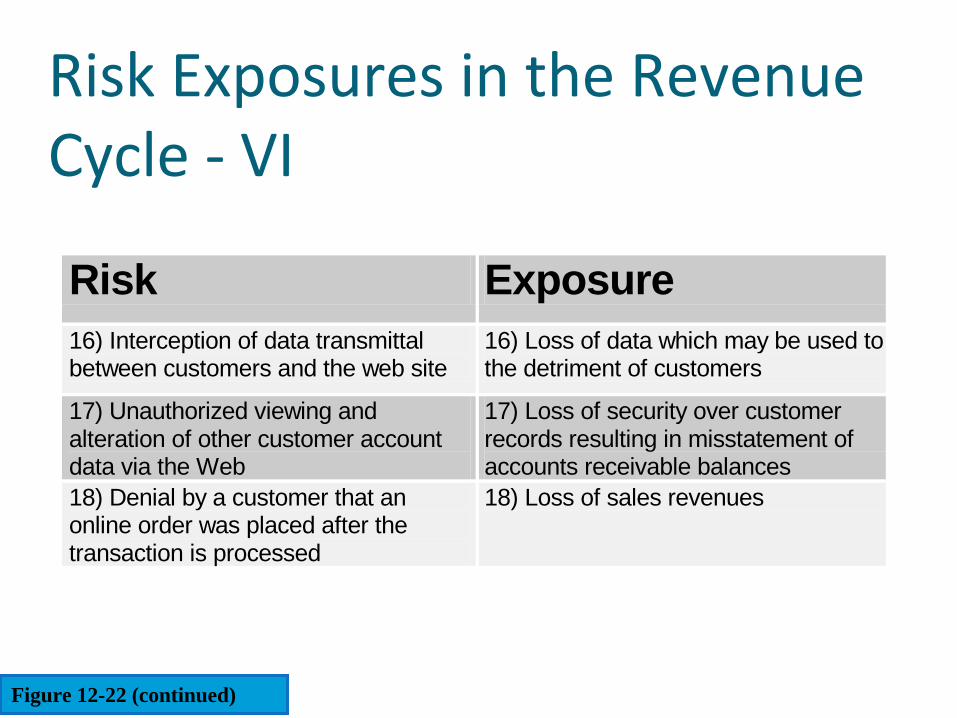

Risk Exposure 16) Interception of data transmittal between customers and the web site

16) Loss of data which may be used to the detriment of customers

17) Unauthorized viewing and alteration of other customer account data via the Web

17) Loss of security over customer records resulting in misstatement of accounts receivable balances

18) Denial by a customer that an online order was placed after the transaction is processed

18) Loss of sales revenues

Figure 12-22 (continued)

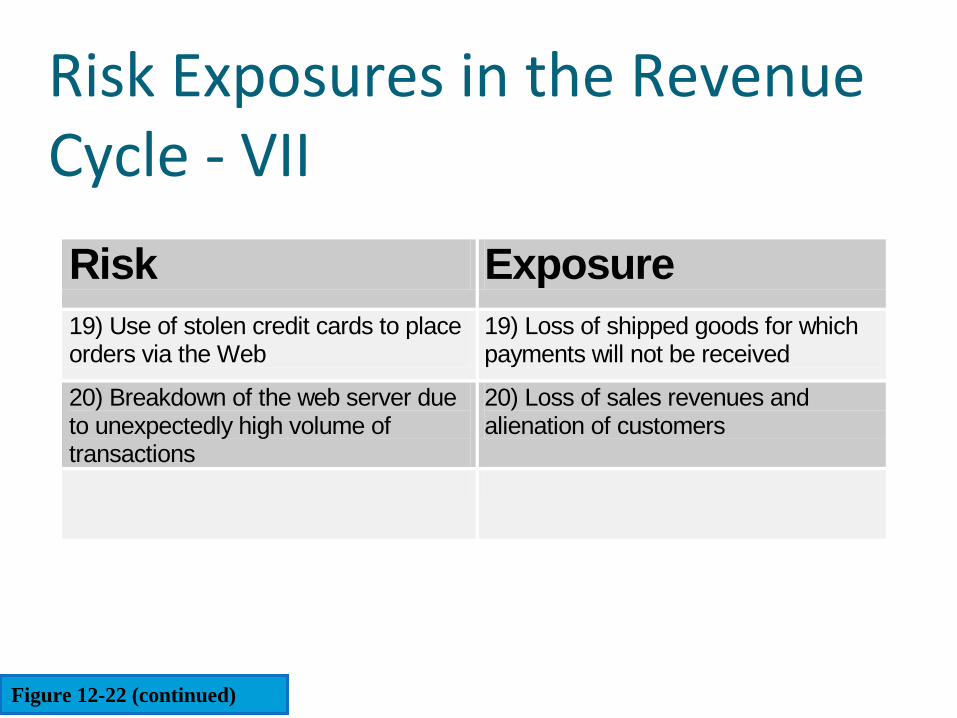

Risk Exposures in the Revenue Cycle ‐

VII

Risk Exposure 19) Use of stolen credit cards to place orders via the Web

19) Loss of shipped goods for which payments will not be received

20) Breakdown of the web server due to unexpectedly high volume of transactions

20) Loss of sales revenues and alienation of customers

Figure 12-22 (continued)

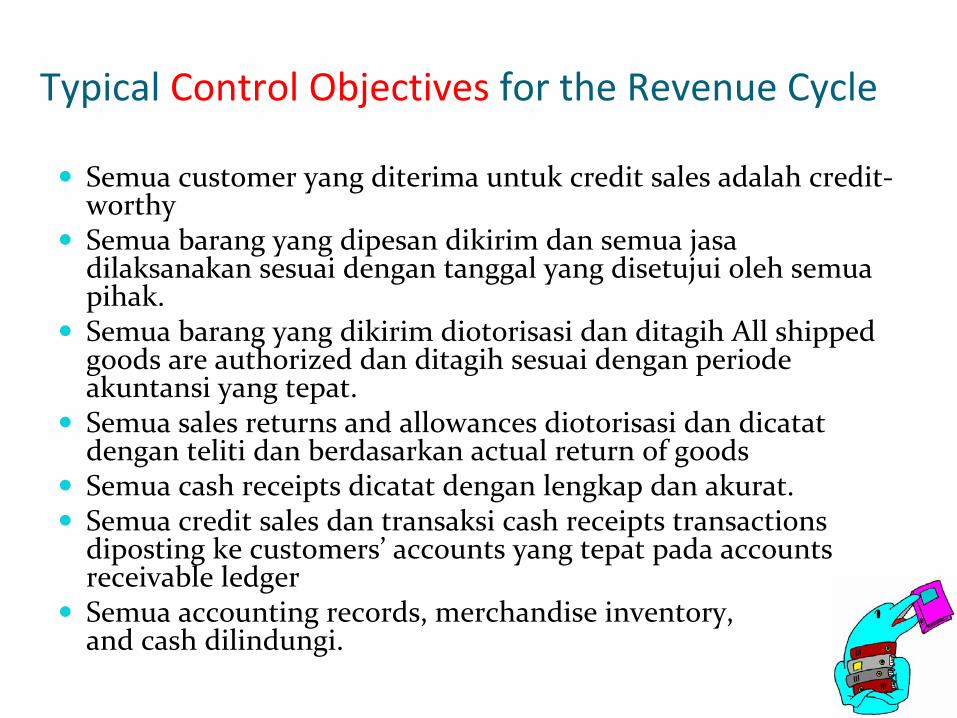

Typical Control Objectives

for the Revenue Cycle

Semua customer yang diterima untuk credit sales adalah credit‐worthySemua barang yang dipesan dikirim dan semua jasadilaksanakan sesuai dengan tanggal yang disetujui oleh semuapihak.Semua barang yang dikirim diotorisasi dan ditagih All shipped goods are authorized dan ditagih sesuai dengan periodeakuntansi yang tepat. Semua sales returns and allowances diotorisasi dan dicatatdengan teliti dan berdasarkan actual return of goodsSemua cash receipts dicatat dengan lengkap dan akurat. Semua credit sales dan transaksi cash receipts transactions diposting ke customers’ accounts yang tepat pada accounts receivable ledgerSemua accounting records, merchandise inventory,and cash dilindungi.

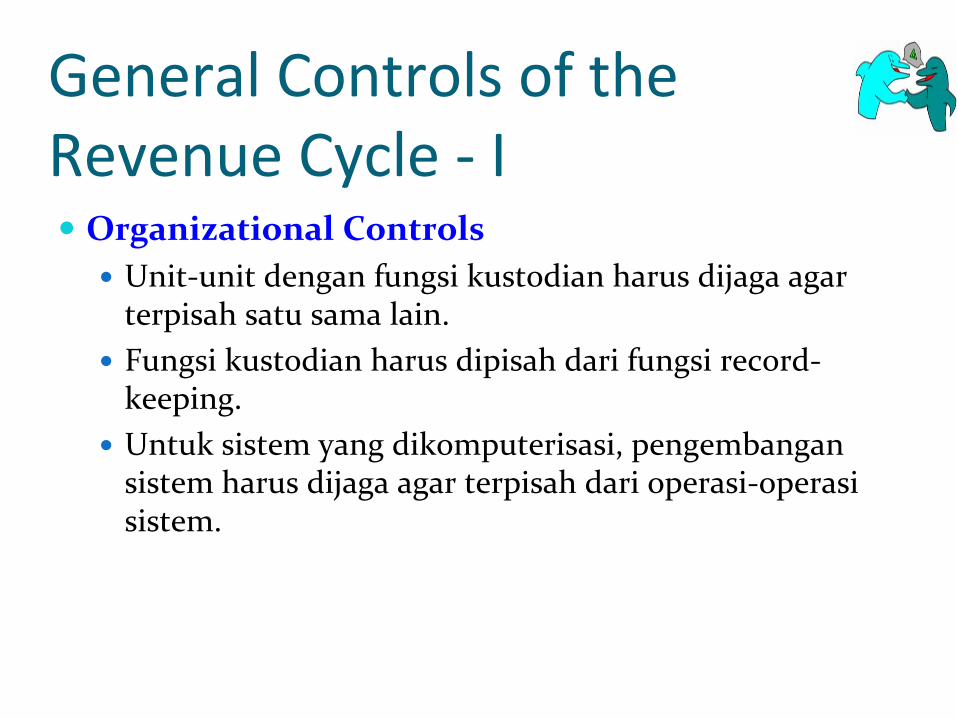

General Controls of the Revenue Cycle ‐

I

Organizational ControlsUnit‐unit dengan fungsi kustodian harus dijaga agar terpisah satu sama lain.Fungsi kustodian harus dipisah dari fungsi record‐keeping. Untuk sistem yang dikomputerisasi, pengembangansistem harus dijaga agar terpisah dari operasi‐operasisistem.

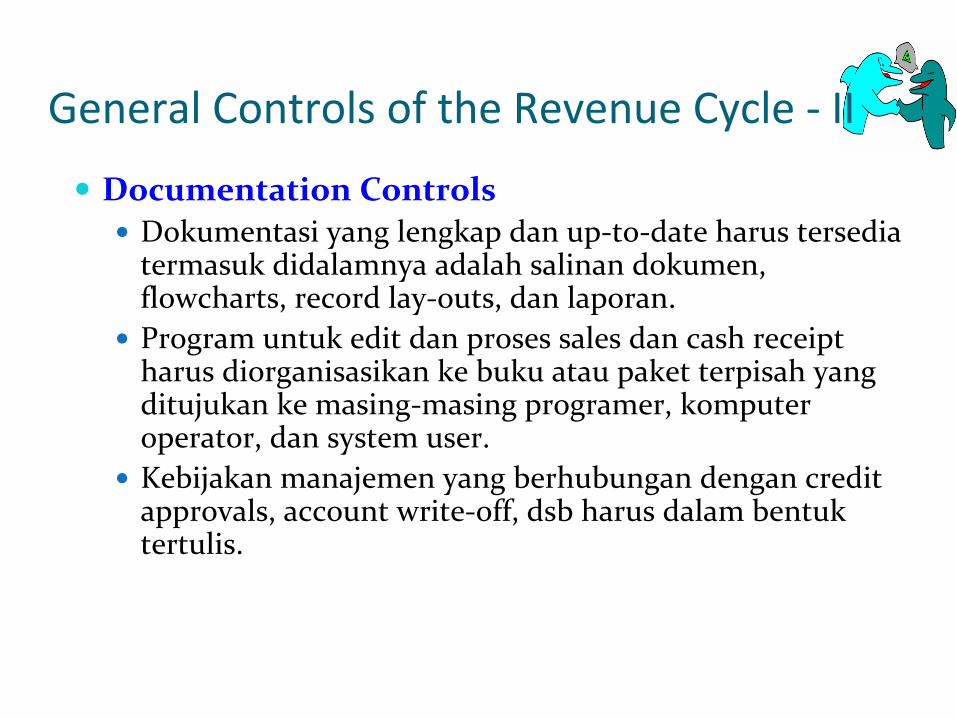

Documentation ControlsDokumentasi yang lengkap dan up‐to‐date harus tersediatermasuk didalamnya adalah salinan dokumen, flowcharts, record lay‐outs, dan laporan.Program untuk edit dan proses sales dan cash receipt harus diorganisasikan ke buku atau paket terpisah yang ditujukan ke masing‐masing programer, komputeroperator, dan system user.Kebijakan manajemen yang berhubungan dengan credit approvals, account write‐off, dsb harus dalam bentuktertulis.

General Controls of the Revenue Cycle ‐

II

Asset Accountability ControlsA/R subsidiary ledger (master file) harus sering direkonsiliasidengan A/R control account di GL.Merchandise inventory record harus dijaga pada ledger dandirekonsiliasi secara periodik ke merchandise inventory control account Bank reconciliation, harus dibandingkan balance pada bank account dengan cash account balance di GL.Petugas bagian pengiriman yang menyetujui penerimaanorder dan pengambilan barang dari gudang denganmenandatangani stock request atau shipping order.Mail room clerk yang menyiapkan daftar semua receive remittances.Customer yang mereview monthly statement dari sales danpayments untuk jumlah‐jumlah yang salah.

General Controls of the Revenue Cycle ‐

II

Management Practice ControlsKebijakan

manajemen

yang berhubungan

dengan

revenue

cycle yang harus

ditetapkan

dan

diikuti

adalah

sbb:

Pegawai (programer dan akuntan harus dilatih denganhati‐hati), pegawai yang menangani kas harus diikatdengan surat perjanjian.Perubahan dan pengembangan sistem harus melaluiprosedur yang jelas yang melibatkan prior approvals, testing, dan sign‐offs.Audit terhadap prosedur dan kebijakan sales dan cash receipt harus dilakukan.Manajer harus melakukan review periodic analyses, control summaries, dan laporan‐laporan tentang aktivitasaccount dan computer‐approved transactions.

General Controls of the Revenue Cycle ‐

II

Data Center Operations ControlsJadwal pemrosesan komputer untuk sales dan cash receipts batches harus ditetapkan dengan jelas.Sistem informasi dan pegawai bagian akuntansi harus diawasisecara aktif dan pekerjaannya direview dengan bantuancomputer processing control reports dan access logs.

Authorization ControlsSemua transaksi credit sales (atau service order) harusdiotorisasi oleh manajer kedit. Pada sistem yang dikomputerisasi otorisasi dilakukan dengan program aplikasiyang dibagun dengan aturan persetujuan kredit.Manajer tidak terlibat dalam pengolahan sales atau pada A/R.Salinan permintaan barang dari sales order harus mengotorisasipengambilan barang dari gudang dan pemindahan barang keshipping dock.

General Controls of the Revenue Cycle ‐

II

Access ControlsBerikan password pada petugas yang diberi otorisasi untukmengakses A/R dan file‐file yang berhubungan dengancustomer, untuk melaksanakan tugas‐tugas yang telahditentukan.

Batasi terminal‐terminal untuk melaksanakan fungsi‐fungsiyang berhubungan dengan transaksi sales dan cash receipts.

Catat semua transaksi sales and cash receipt ke sistem.

Sering‐seringlah mengeluarkan master file A/R danmerchandise inventory ke magnetic tape backups

Lindungi gudang dan lemari besi secara fisik.

Gunakan lockbox collection system pada situasi yang feasible.

General Controls of the Revenue Cycle ‐

III

Application Controls of the Revenue Cycle: Input ‐

I

1.

Siapkan

pre‐numbered documents dan

dokumen

yang dirancang

dengan

baik

untuk

dokumen

sales,

shipping, and cash receipts, masing‐masing

dokumen diotorisasi

oleh

orang

yang berwenang.

2.

Validasi

data sales orders dan

remittance advices seperti

data yang disiapkan

dan

dimasukkan

untuk

pengolahan. Pada

computer‐based systems, validasi harus

dilaksanakan

dengan

sarana

program edit check.

Saat

data dimasukkan

ke

computer‐readable medium, key verification

dicocokkan.

Application Controls of the Revenue Cycle: Input ‐

II

3.

Betulkan

kesalahan

yang terdeteksi

selama

data entry dan

sebelum

data diposting ke record‐record

customer dan

inventory.4.

Precompute

batch control totals yang berhubungan

dengan

data penting

pada

sales invoices (atau shipping notices) dan

remittance advices.

Precomputed

batch control totals haus

dibandingkan dengan

totals yang dihitung

selama

posting ke

accounts receivable ledger dan

setiap

kali processing run. Pada

cash receipts, total pada

remittance advices

harus

dibandingkan

dengan

total pada

deposit slips.

Application Controls of the Revenue Cycle: Processing ‐

I

1.

Pindahkan

barang

yang dipesan

dari

gudang

barang

jadi (finished goods warehouse) dan

kirim

barang‐barang

hanya

berdasarkan

otorisasi

tertulis

seperti

stock request copies2.

Invoice customers hanya

diberiahukan

oleh

bagian pengiriman

atas

jumlah

yang telah

dikirimkan.

3.

Pengeluaran

credit memos untuk

sales returns hanya

jika disertai

bukti

(seperti

receiving report) telah

diterima

bhwa

barang

memang

benar‐benar

dikembalikan.4.

Periksa

semua

perhitungan

pada

sales invoices sebelum dikirim

dan

diposting

ke

customers’

accounts yang tepat.

Bandingkan

sales invoices dengan

shipping notices and open orders, untuk

meyakinkan

nahwa

jumlah

yang dipesan

direkonsiliasi

dengan

order yang dikirim

dan

back‐ordered.

Application Controls of the Revenue Cycle: Processing ‐

II

5.

Periksa

bahwa

jumlah

total yang diposting

ke

accounts receivable accounts

dari

batch transaksi

sama dengan

precomputed

batch totals, dan

posting jumlah

total ke general ledger accounts yang tepat.

6.

Depositokan

semua

kash

yang diterima

lengkap

dengan minimum of delay, sehingga

menghilangkan

kemungkinan

cash receipts yang sedang

digunakan untuk

membayar

pegawai

atau

untuk

membayar

petty

cash funds.7.

Betulkan

kesalahan

yang dibuat

selama

tahapan pengolahan

biasanya

dengan

membalik

kesalahan

posting ke

perkiraan

dan

masukan

data yang benar. Audit trail yang berhubungan

dengan

perkiraan

yang

dikoreksi

akan

menunjukkan

kesalahan

aslinya, the reversals, and the corrections

Application Controls of the Revenue Cycle: Output

1.

Siapkan

monthly statements, yang harus

diposkan

ke semua

credit customers, terutama

jika

pendekatan

balance forward

digunakan.2.

Salinan

file dari

semua

dokumen

yang berkaitan dengan

transaksi

sales dan

cash receipts dicek

secara

periodik

dengan

urutan

nomor

pada

tiap

file untuk melihat

celah

yang ada. Jika

transaksi

tidak

didukung

dengan

preprinted documents, seperti

yang sering terjadi

pada

online computer‐based systems, tandai

nomor

transaksi

ke

transactions.3.

Siapkan

daftar

transaksi

yang dicetak

dan

account summaries pada

periodic basis untuk

menyediakan

audit trail dan

dasar

untuk

review.

Web Security ProceduresAuthentication, user identification number dan password dibutuhkan untuk akses ke private network.Authorization

Use of an Access Control ListAccountability, untuk menetapkan tanggung jawab atassegala modifikasi pada Web sites Web sercer log harusdipelihara.Data Transmission, untuk menjaga kerahasiaan danintegritas data yang dikirim via Web harus menggunakanenkripsi.Disaster Contingency & Recovery Plan,

Diperlukan prosedur backup yang cukup termasuk fault tolerance untuk meminimalkan gangguan yang tidakdiharapkan. Recovery plan direncanakan untuk meyakinkan rekonstruksidari data yang hilang.