Embed Size (px)

Citation preview

RethinkingFinancial Capability

Lessons from economic psychology and behavioural finance

Mike Dixon

Sponsored by

RethinkingFinancial CapabilityLessons from economic psychology and behavioural finance

Mike Dixon

Sponsored by

About Norwich Union

Improving financial literacy is an importantprecondition for solving the long-term financialchallenges facing the UK.As a leading financialservices provider and consistently one of the mosttrusted brands, we recognise our responsibility tosupport the work of the regulator and government toimprove financial capability in the UK.

However, it is crucial that programmes designed toimprove financial skills actually deliver positive changes topeople’s financial behaviour and decision making ratherthan merely improving their awareness andunderstanding.

Delivering this behaviour change requires a greaterunderstanding of economic psychology. The debate onfinancial education must evolve in a way that ensures theapproach brings about the required change.

We are proud to have sponsored a report that hasdeepened our understanding of how people’s financialdecision making is formed and influenced, and can

therefore help us create the right products and servicesfor more informed, financially capable consumers.

Key facts• Norwich Union is the UK’s largest provider of life,

pensions and investment products and has £102billion assets under management.

• Norwich Union is the UK’s largest insurer, insuringone in seven motor vehicles with a market share ofaround 14 per cent.

• Norwich Union is part of the pan-Europeaninsurance group Aviva, the largest life and pensionprovider in Europe and the world’s sixth-largestinsurer. Its main activities are long-term savings, fundmanagement and general insurance. It has 59,000employees and 30 million customers worldwide.

Norwich UnionWellington Row,York YO90 1WRTel: +44 (0)1603 622200, Fax: +44 (0)1603 683659www.norwichunion.com

Acknowledgements vAbout the author viForeword vii

Summary 1Closing the motivation gap 2New strategies for financial capability 3Conclusion 6

Introduction 7The structure of this report 12

Section 1: Financial capability in the 21st century 13Economic trends 13The demographic context 16The cultural context 17Welfare state retrenchment 19Political context 19

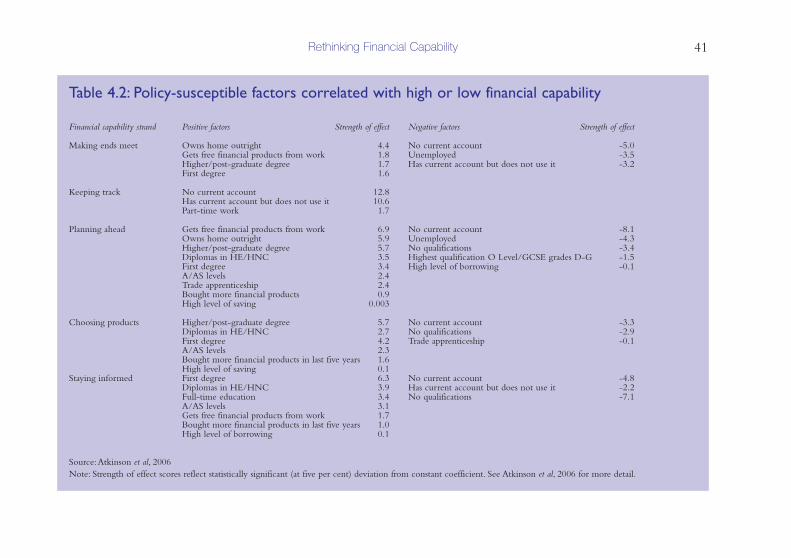

Section 2: Financial capability in 2006 21Overall levels of financial capability 22

Using the data 30

Section 3: Priorities for action and future funding 31The impact of low financial capability 31Competing priorities? 34Future funding 34Financial capability as a welfare issue 37

Section 4: Principles for action 39Demographic and socio-economic targeting 39Two approaches to financial capability 42Critical moments 42Financial advice and the motivation gap 43The role of government in changing behaviour 45

Section 5: Lessons from psychology 47Financial capability and broader notions of 48

empowermentBehavioural economics: bias and heuristics 49Using economic psychology 58

Contents

Section 6: Empowering people to change behaviour 59Empowering people to change: preparation 61Empowering people in changing 63Empowering people after change 64Financial capability and ‘consciously’ changing 65

behaviourFinancial capability and mental accounting 65Shades of Machiavelli? 67

Section 7: Explaining policy failure and success 69Does financial education really change 69

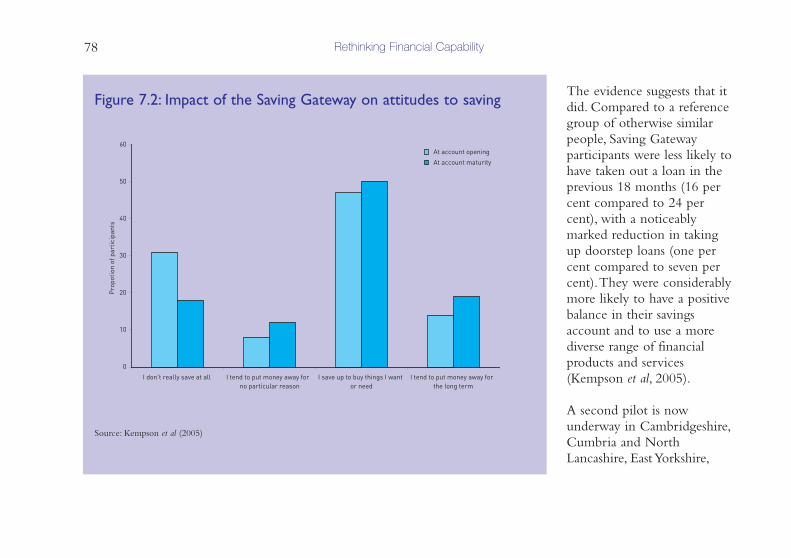

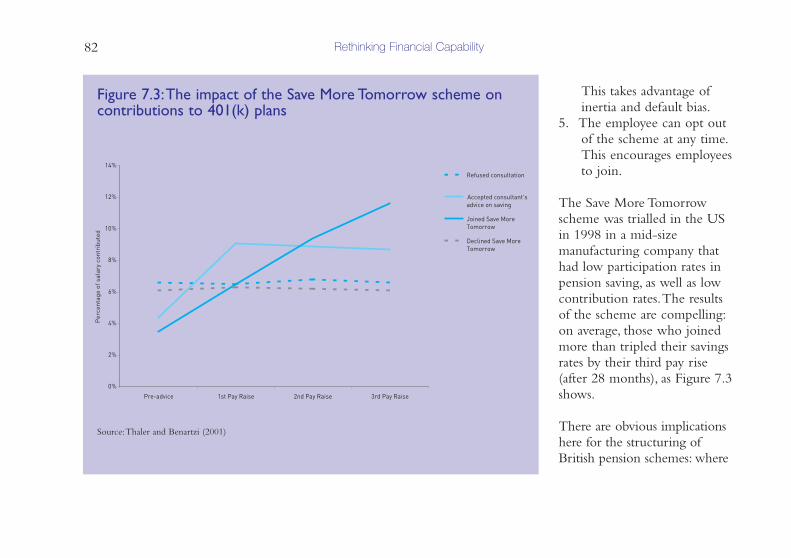

behaviour?Incentives 77Policy underpinned by economic psychology 79

and behavioural economicsTaking stock 84

Section 8: New strategies for financial capability 85Rethinking the challenge 85Tackling the motivation gap 87Responding to critical moments 89Challenging established wisdom: 90

rethinking savings hierarchiesA new model for debt management 91Empowerment through commitment 91Extending default approaches 93Using mental accounting 93Harnessing social norms and networks 94Conclusion 94

References 95

This report could not have been written withoutassistance from many people. ippr trading would liketo thank the external experts who attended aseminar at ippr in April 2006 at which ShaunMundy, Adele Atkinson and Professor Paul Webleypresented.

We would also like to thank those who generouslygave time and input in discussion with the author, orwho commented on an initial draft, including SueRegan and Patrick South at the ResolutionFoundation, Claire Coulson and Richard Cox atNorwich Union and Paul Webley.We are also verygrateful for the advice and guidance supplied bycolleagues at ippr. Particular thanks are due to MirandaLewis, Dominic Maxwell, Sonia Sodha, Ian Kearns,Howard Reed, Lula Durante and Julia Margo. Special

thanks are due to Jennifer Simms at ippr for researchsupport. However, the views expressed in this reportare solely those of the author.

This research uses data from the Financial CapabilityBaseline Survey, originally undertaken by the BritishMarket Research Bureau (BMRB) and analysed byElaine Kempson,Adele Atkinson, Stephen McKay andSharon Collard at the Personal Finance ResearchCentre, University of Bristol (Atkinson, McKay,Kempson, and Collard, 2006). It also draws on theBritish Household Panel Survey, sponsored by theEconomic and Social Research Council (ESRC); andthe Family Resources Survey, commissioned by theDepartment for Work and Pensions (DWP).These datasets were kindly supplied by the UK Data Archive andare Crown Copyright.

Acknowledgements

About the author

Mike Dixon, Research Fellow, ipprMike has written widely on a range of topics,including financial capability, labour markets,demographic change, youth transitions, globalisation,progressive renewal, political economy, crime, andpoverty and inequality. His most recent publicationsfor ippr include Population Politics (2006), CrimeShare:The unequal impact of crime (2006) and several chaptersin Social Justice: Building a fairer Britain (2005). Beforejoining ippr, Mike worked at Ogilvy and Mather,where he advised on communications strategy. Mikegraduated from St. John’s College Cambridge with afirst class BA honours degree in Philosophy.

ippr trading ltd30-32 Southampton Street,London,WC2E 7RATelephone: +44 (0)20 7470 6100

ippr trading ltd is the trading subsidiary of the Institutefor Public Policy Research (ippr), the UK’s leadingprogressive think tank (www.ippr.org).

The views expressed in this publication are those ofthe author.

We are living in a consumer-driven society. From avery early age, children are exposed to many differentmessages from an increasing range of media. Everyday,in all areas of our lives, people are making verysophisticated decisions about what to buy and how tospend their money by reaching informed and rationaldecisions based on brand, quality and price.

Indeed, anyone with children will be only too familiarwith the detailed knowledge they absorb and analyseregarding the pros and cons of mobile phones, MP3players or games consoles - making decisions bafflingto many adults.

However, despite becoming increasingly savvy aboutwhat we buy on the high street and in thesupermarket, this informed decision making has notextended to how people manage their personalfinances.When confronted with what can be equallycomplex decisions about how to manage their money,

people often take actions that are not obviouslyrational and yet to them can make perfect sense. Forexample, people may keep large amounts of cashliquid in a current account rather than investing it inshort- or medium-term savings, or they may not savefor retirement even when they can afford to and knowthey should.

A better understanding of why people act as they do iscrucial if the financial services industry and theGovernment are to successfully engage consumers andenable them to take greater personal responsibility inareas such as saving, protection and insurance.The stateis increasingly reigning back in areas where it haspreviously accepted responsibility, and Norwich Unionfeels it is important that we debate the implications ofthis for our society.

It is widely acknowledged that financial education hasa role to play in helping people take better informed

Foreword

Rethinking Financial Capabilityviii

financial decisions but it should not be assumed thatsimply having a more financially educated society willautomatically translate into people taking appropriateaction to manage their financial situation better.

There have been important and significant steps madeover the last ten years to better understand thepsychology behind the decision making process andNorwich Union is pleased to work with the Institutefor Public Policy Research to bring this analysis to anew audience beyond the academic world.

We hope that the ideas raised in this report make auseful contribution to the wider debate being led bythe Government and Financial Services Authority tocreate a more financially capable society.This is acommon goal, which if achieved successfully willreward society, government and the financial servicesindustry alike.

Mark HodgesChief Executive, Norwich Union Life

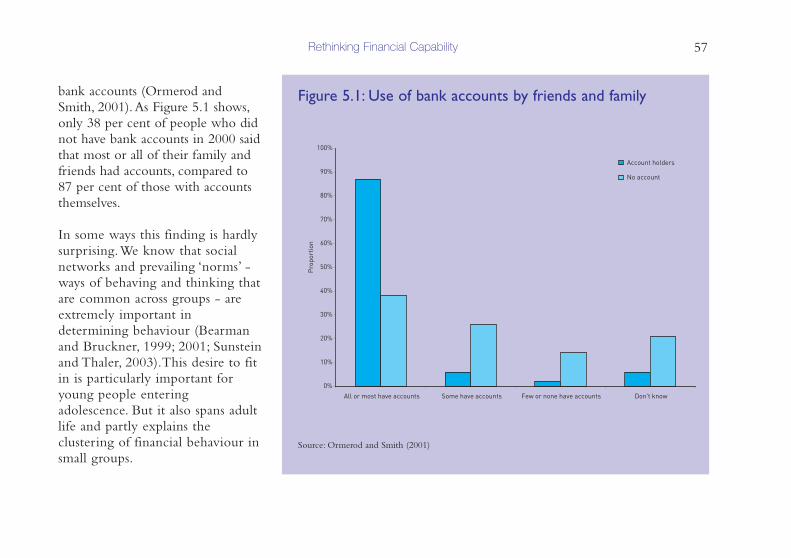

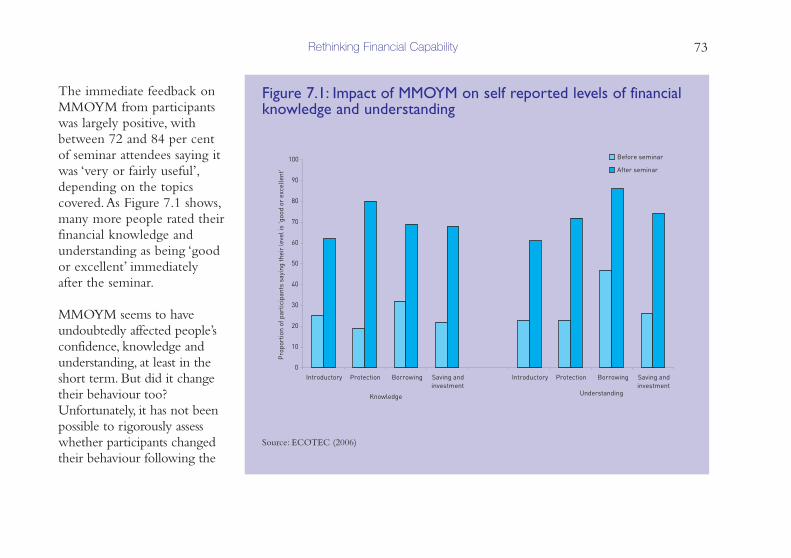

Improving the UK’s ‘financial capability’ is not an easytask. Nor is it a small one. In early 2006, although 17million adults in the UK were successfully makingends meet, keeping track, planning ahead, choosingproducts and staying informed about financialproducts, as many as 10.5 million experiencedconsiderable difficulty in one of these areas, 3.8million faced severe problems in two, 6.2 millionlacked capability in three areas, 8.6 million in four, and1.4 million were succeeding in none.

This has serious consequences for people’s well-being,the British economy, the financial services industryand future prosperity. Looking ahead, it is clear thatdeep-seated economic, demographic, cultural, policyand political trends will make financial capabilityincreasingly important in the future.

Despite the substantial progress achieved over the lastfew years, the current National Strategy for Financial

Capability is too limited in scope to achieve itsambition of significant change.A substantial increase inresources is needed. But a revitalised policy approach isalso needed that makes better use of emergingthinking from academia, and experiences from othercountries and policy areas.

There is also a clear need to determine priorities.Over the long term the best solution to financialcapability is to engender a profound cultural change,in terms of attitudes to personal responsibility,behaviour, consumption, sustainability and debt. Ifour society has moved from a ‘thrift ethic’, wherepeople limited their consumption of goods to whatthey could afford at the time, to a ‘consumptionethic’, where people buy now and pay later, we nowneed to move towards a ‘sustainability ethic’, whereboth saving and borrowing are appropriate, butwithin the context of overall financial sustainability.But in the shorter term, it is unrealistic to think that

Summary

policy can improve all elements of financial capabilityfor everyone.

The key question is where and how UK citizens’ lowlevels of financial capability are creating, and willcontinue to create, the greatest problems for society atlarge and, specifically, where - and to what extent -they affect the financial services industry.This reportargues that policy should prioritise efforts to improvepeople’s ability to plan ahead, as this has most seriousrepercussions for individuals, business, the economyand the financial services industry.

This report also sets out a case for seeing financialcapability as more of a central social welfare issue.Thiswould suggest moving responsibility for the NationalStrategy from the FSA to the government, through theDepartment for Work and Pensions (DWP) and theDepartment for Education and Skills (DfES).There areseveral key motivations for this.The first is that theDWP and DfES have considerably better access tomany practical delivery channels, through socialservices offices and education providers, than the FSA.They also have more experience in delivering large-

scale programmes, and the evaluative and researchcapacity to assess these.Also the Government hasgreater expertise in dealing with financial issues thataffect ordinary people’s lives and there are strong linksbetween the rest of its core business and financialcapability issues.

Closing the motivation gapA central challenge identified in this report is closing themotivation gap between what people say is importantand their actual behaviour. More than 80 per cent ofpeople under retirement age think that the state pensionwill not be enough to give them the standard of livingthey would like, but just 37 per cent have made someprovision for their old age (Atkinson et al, 2006).

There are two main ways to close this gap: providingthe best kind of advice and guidance to those whowant it, when they want it; and providing the bestpossible structures to make it easier for people to actin more financially capable ways, thereby becomingmore engaged and interested in improving theirfinancial capability.

Rethinking Financial Capability2

Policy has too often focused almost exclusively on thefirst of these strands, although there have beenconsiderable successes. For example, research from theUS suggests that introducing compulsory financialeducation into the curriculum could increase thewealth of UK citizens substantially by their late 40s:the average couple with no children could be betteroff by about £22,000, the average single person withno children could have £13,000 more, and the averagecouple with two children aged five and 11 could be£32,000 richer, as a result of having taken betterfinancial decisions throughout their lives. But a realchallenge remains in ensuring that the financialeducation is delivered in an engaging way and teachesthe right skills.

New strategies for financial capabilityA further key finding of this report is that economicpsychology, behavioural economics and behaviourchange theory can to help develop the second approachto improving people’s financial capability - providingthe best possible structures to make it easier for peopleto act in more financially capable ways, thereby

becoming more engaged and interested in improvingtheir financial capability. Given the right support andstructures, and a significant stake in financial products,people do take steps to become more financiallycapable. Below are some practical suggestions in whichpolicy can empower them to do so.

Improved communicationImproving the way government, the financial servicesindustry, the voluntary sector and other stakeholders talkabout financial capability, and the way thesecommunicate with people about this topic, is important.There are a range of easy, practical solutions that can beundertaken, including opening up contracts to a wider,more creative set of agencies, taking greater risks incommunication, and setting up competitions withgenerous remuneration for the best work.

Simplified products and benefitsA clear lesson from behavioural economics is thatpeople are put off making decisions by complexity anda wide range of options.This means that, for manyconsumers, it may be more appropriate to offer them asmaller range of products initially, rather than a wide

Rethinking Financial Capability 3

portfolio, even if this means that they may not haveimmediate access to the most tailored and suitableproducts.A related challenge is in simplifying the taxand benefits system.There is a difficult balance to bemade here between effective targeting and simplicity,and there are no easy answers.

Responding to critical momentsPolicy needs to identify better the key criticalmoments when people are most receptive to efforts toimprove their financial capability and, at these times, todirect them towards appropriate guidance.Thesecritical moments are sometimes related to life stages,such as becoming a new parent, but are oftenunrelated, for example, starting a new job, moving to anew city, deciding to go on an expensive holiday or tostart saving for a house.

But government, the financial services industry andother stakeholders also need to ensure that advice andguidance is available to people when they need it, in aform that does not impose any formal commitment orinformal pressure to buy specific products as a result.We support the Resolution Foundation’s call for a step

change in funding to deliver a new national financialadvice resource.

Challenging established wisdom: rethinking savingshierarchiesThe traditional model of savings hierarchies needs tobe rethought: for many people it will be moreeffective to pay off debt regularly at a slightly slowerrate and to build up a savings habit and asset at thesame time, as this could lead to better financialmanagement and cost savings over the long term. Oneclear advantage to this approach is that it would leavepeople with an asset at the end of their debt clearance,with all the benefits that asset-holding entails (Bynnerand Paxton, 2001).Another advantage is that itprovides more tangible rewards for good financialmanagement. It would also help people to developregular savings habits.

A new model for debt managementThe Government should offer people with debtproblems the option of having debt repaymentsdeducted automatically from benefit payments (up to asmall set maximum), including Working Tax Credits.

Rethinking Financial Capability4

This would effectively reduce the risk of default to zero,reducing administrative costs for both the public andprivate sector considerably. If this were combined with aplan to provide participants with the opportunity tosave for a small asset at the end of the debt-repaymentperiod - perhaps conditional on attending financialcapability training - this could have a significant impacton the UK’s financial capability, with substantial savingsfor both the public and private sector.

Empowerment through commitmentOne of the clearest lessons from behaviour changeresearch is that commitment plays a crucial role inchanging behaviour.This is because it helps to mitigateagainst hyperbolic discounting - the tendency topostpone and prevaricate indefinitely, acting againstone’s own stated long-term interests. Helping peopleto make and keep commitments is therefore animportant way of tackling the motivation gap.

There are some simple changes to current policy that canmake better use of commitment effects. Some obviousexamples include encouraging and helping people to signforms or book appointments during education seminars,

and to encourage setting small, specific and achievablefinancial behaviour goals as part of employmentprogrammes or generically provided financial advice.

Save More Tomorrow accountsA new kind of current account service could bedeveloped that makes it easier for people to commit inadvance to greater saving levels in the future.Thiswould allow people to choose to save more of any payrises that they receive.Any sustained payroll increasefrom an employer paid into the nominated accountwould automatically trigger an increased direct debitto a dedicated savings account (which could include aChild Trust Fund account).This would be up to a setmaximum, with a notification letter being sent to theaccount holder. Offering consumers the opportunityto start a direct debit into a savings account - startingif and when the customer received a pay rise - to bepaid on the same day as customers receive theirautomated pay cheque from their employer, would bea useful way to encourage greater financially capablebehaviour, at little administrative cost.

Rethinking Financial Capability 5

Extending default approachesThere is wide consensus that automatic enrolmentinto company pension schemes should be the norm.But there may also be considerable scope forextending this use of defaults into wider realms ofpolicy.

Creating new ‘mental accounts’ to encourage certainkinds of spending or savingThere seems to be potential for offering savingsaccounts with small deposits to customers who open anew basic bank account for the first time, toencourage saving.Another possible way forward wouldbe that for all schoolchildren (and perhaps adults) whotake up work experience, a small contribution couldbe made to a pension fund, linking paid work topensions saving and creating an initial pensioninvestment for children.

Harnessing social norms and networksThe importance of social norms and networks is key,and holds numerous implications for efforts topromote financial capability. It shows the importanceof promoting financial capability to the mostinfluential figures in communities with low levels offinancial capability.Word of mouth is a powerful forcein disseminating ideas and behaviour.

ConclusionThis short report has attempted an ambitious task andas such can only make a start. But it is hoped that theideas set out here will help others to move forwardwith their thinking, in developing policy approachesthat focus on empowering people to improve theirfinancial capability.

Rethinking Financial Capability6

Ten years ago, almost no one had heard of the term‘financial capability’.Today, the UK is in the secondphase of its dedicated National Strategy for FinancialCapability with combined support from the financialservices industry, the voluntary sector, theGovernment, much of the media and more than £10million in annual funding (FSA, 2006b).The aim is toimprove people in the UK’s financial capability inmaking ends meet, keeping track, planning ahead,choosing products and staying informed (Atkinson etal, 2006). But will the strategy work?

This report argues that despite the substantialprogress achieved over the last few years, the currentapproach is too limited in scope to achieve itsambition of significant change.The UK now needs asubstantial increase in resources and a revitalisedpolicy approach that makes better use of emergingthinking from academia and experiences from othercountries and policy areas.

Mid 2006 is a good time to take stock. Financialcapability is still fresh on the agenda and the NationalStrategy is in its relatively early stages. But there isnow a good opportunity to undertake a paradigm shiftin approach, in terms of both scale and content.Perhaps the most important advance so far has beenthe development of the concept of financial capabilityitself, one that is unique to the UK and internationallyadmired (SEDI, 2004; 2005).

Most other countries, including much of the US -where efforts to improve financial awareness are mostprevalent - are still working with a narrower conceptof ‘financial literacy’ (Vitt et al, 2000; 2005). So why isthinking about financial capability a step forward?

The simple answer is that financial capability is a broaderconcept, comprising five related strands that focus onbehaviour, decision making and practical skills as well asthe more traditional foci of knowledge and

Introduction

understanding.This is a more realistic encapsulation ofthe way people think about money in their everydaylives (SEDI, 2004). It is also a better focus for policyefforts because it highlights the importance of helpingpeople to change their behaviour.

If the concept of financial capability is a relativelyrecent development, so too is the emergence of realpolitical appetite for tackling it. Before the late 1990spoliticians and policymakers remained relativelysanguine about the ability of UK citizens to navigatethe financial landscape (FSA, 2000). Financialcapability was not a political priority compared torecurrent crises over Europe, year-on-year increases incrime, and an economy that appeared to swinginevitably from boom to bust and back again withnear-catastrophic implications for interest rates. Butthen two influential reports - building on agroundswell of academic research (Ford andRowlingson, 1996; Kempson and Whyley, 1999) - thefirst by the Social Exclusion Unit (SEU) in 1998(SEU, 1998) and the second in 1999 by Policy ActionTeam 14 (HM Treasury, 1999), helped change theterms of political debate.

Both of these reports focused on financial inclusion -an issue that remains central to policy debate today,with an ongoing Treasury Select Committee inquiryand a dedicated government taskforce (FinancialInclusion Taskforce, 2006).

This resurgence in political appetite was welcomed bymuch of the voluntary sector and the financial servicesindustry: both have long recognised the importance ofpeople’s financial well-being in its own right, as well asits salience for broader social policy and business goals.It is an issue that has remained central to much of thework of the Institute for Public Policy Research(ippr), notably by Sue Regan and Will Paxton (Reganand Paxton, 2003). It is also an issue that has evolvedconsiderably over the past five years.

Financial inclusion was often originally thought about ina polarised way (Kempson and Whyley, 1999): you wereeither in or you were out. But as understanding hasdeepened, there is growing consensus that this view isoverly simplistic: financial exclusion is a continuum, withpeople more or less excluded across a range of differentproducts and skills (Atkinson et al, 2006; FSA, 2006b).

Rethinking Financial Capability8

This realisation has led naturally to the development ofthe financial capability agenda, which incorporates manyof the original concerns raised in the late 1990s but seesthem as relevant to a wider audience (FSA, 2003).

A wider audience - and considerable effort - has ledto the creation of a ‘grand coalition’ for the promotionof financial capability. In 2003 the Financial ServicesAuthority (FSA), under the auspices of its new ChiefExecutive, John Tiner, convened a partnership ofleading thinkers, organisations and practitioners toestablish a ‘road map for delivering a step change inthe financial capability of the UK population’ (FSA,2003; 2006b).Three years and seven working groupslater, we now have the results of a first set of pilots,data from a comprehensive survey assessing the state ofUK citizens’ financial capability, and a range ofspecially commissioned reports covering topics as(relatively) diverse as the financial needs of youngadults (FSA, 2005) and the best way of deliveringadvice (Wallis, 2005).

The evidence base has never been better: there is nowa firmer grasp than ever of what works in promoting

financial capability.The FSA has also recentlypublished its plans for the next phase of the NationalStrategy for Financial Capability (FSA, 2006b). It is agood time to take stock and ask whether there arenew approaches and ideas to try, and to assess thestrategy against the evidence.

The time is also right to be thinking about the role ofgovernment in influencing behaviour.The business ofgovernment has always been the business of behaviourchange: from the moment the Babylonian king,Hammurabi, ordered his 282 laws to be inscribed onan eight-foot stone slab nearly four thousand yearsago, government officials have prescribed andproscribed in the interests of the common good.Regulations, taxes and subsidies, laws and punishments,information and persuasion, the provision of publicservices - all have been employed for centuries.

But in the last decade, policymakers have been spurredon by new findings in behavioural sciences andgenetics, results from longitudinal studies tracking theimpact of various kinds of behaviour on people’s laterlives, and - perhaps most importantly - a growing

Rethinking Financial Capability 9

realisation that many of the most intractable socialproblems in the UK today are the result of entrenchedbehaviour that is resistant to traditional incentives.These policymakers have now become more interestedin whether the Government should become moreinvolved in trying to influence behaviour. Proponentsof this approach variously point to the need to engagecitizens in policy efforts in a more interactive way,rather than as merely passive recipients of services; thepotential for greater cost effectiveness in achievingpolicy outcomes; and the moral and political case forgreater personal responsibility (Halpern et al, 2004).

Revealingly, this shift has not been confined to onecorner of Whitehall.Across the board politicians,researchers, practitioners and academics havesimultaneously begun to talk about these newapproaches to traditional policy questions (Halpern etal, 2004), encouraged by the deep entrenchment ofevidence-based policymaking and piloting, which hasrevealed the inadequacy of much traditional wisdom.It is no longer enough to rely on ideas alone: rightly,proof is needed of whether they work (Pearce andPaxton, 2005). From tackling obesity to encouraging

recycling, from reducing antisocial behaviour topromoting education, and from discouraging smokingto facilitating entrepreneurship, new strategies areneeded.As David Miliband MP, then Minister ofCommunities and Local Government, noted earlierthis year:

‘Across government, there is growing recognition that if we are tomove to the next stage of economic and social reform, we needmore than ‘more of the same’.To build on the foundations so farlaid, we need new relationships between different public servicesand new relationships between public services and local people.’(Miliband, 2006)

It is no coincidence that these questions have increasingresonance as our understanding of behavioural sciencesgrows. Economic psychology, behavioural economics,neuroscience, behavioural genetics, social norm theory,sociology and traditional economics (to name but a few)have seen significant advances in recent decades, partlyspurred on by technological advances that have enabledus to assess, collate and compare information faster thanever before.We also now know more than ever beforeabout how and why people make the decisions they do,

Rethinking Financial Capability10

and what affects behaviour (Kahneman, 2002).Thesedevelopments will fundamentally change the way policyis created (Dixon, 2005; Pearce and Paxton, 2005), notleast in relation to financial capability.

But these developments will also change ourperspective on the financial capability challenge, seeingit not as an isolated issue, but as one aspect of a muchbroader challenge that is deeply rooted in fundamentalcultural shifts - a challenge that will increasinglyrequire government to work harder and moreeffectively to empower people in changing theirbehaviour. Over the long term, improving financialcapability almost certainly requires a profound culturalshift, in terms of attitudes to personal responsibility,behaviour, consumption, sustainability and debt(Webley, 2006).This is an enormous challenge, whichwill not be met in the next decade. But withoutlonger-term aims that set the direction for policyefforts, lasting cultural change is unlikely.

This report aims to set out this new direction for thefinancial capability agenda, complementing anddeveloping the existing approach, and building on the

understanding gleaned and progress made so far. Itrecommends two main shifts: increasing resources andimproving the integration of academic theory andexperiences from other areas into policy.

The central focus of this new agenda should be toempower people in becoming more financiallycapable, by using the best available theories andevidence about human behaviour.The agenda mustapply the latest developments in economic psychologyand behavioural economics (the study of how peoplereally make decisions about money in their everydaylives) to the most rigorously evaluated evidence ofwhat really works in promoting financial capability.This should be combined with the best theory abouthow people change behaviour, drawn from aburgeoning specialist literature, in order to draw outlessons for future policy development.

This is an ambitious task, one in which this shortreport can only make a start. But we hope that theideas set forward here will help others to develop theirthinking further and contribute towards a morefinancially capable Britain.

Rethinking Financial Capability 11

The structure of this reportThe report is structured as follows. Section 1 sets outthe economic, demographic, cultural and politicalcontext for financial capability in the 21st century.Section 2 reviews the state of the nation’s financialcapability in 2006. Section 3 considers priorities foraction and future funding requirements andresponsibilities. Section 4 sets out principles foraction and identifies the motivation gap and the

appropriate role of advice. Section 5 provides anoverview of the latest theories from economicpsychology and behavioural economics. Section 6considers lessons from other policy areas, andstrategies that empower people to change theirbehaviour. Section 7 benchmarks current domesticand international policy success against this theory.Section 8 sets out new strategies for financialcapability, based on this analysis.

Rethinking Financial Capability12

The need for a more financially capable Britain isclear: deep-rooted social, economic, cultural andpolitical trends are changing how we live in ways thatmake financial acumen ever more important.Anypolicy response needs to be based on a firm analysis ofhow the world is evolving and what this means forpriorities. In this section we therefore provide a briefoverview of some of the most important economic,demographic, cultural, policy and political trendsshaping the UK in the 21st century, and assess theirimplications for the financial capability of UK citizens.

Economic trendsThe UK has famously experienced the longest periodof economic growth on record (HM Treasury, 2006).Following inflation targeting (and the subsequenttransfer of responsibility for interest rates to the Bankof England), interest rates and inflation have remainedconsistently low, with long-term inflationary

expectations stable at two per cent and long-terminterest rates at a 40-year low of four per cent (HMTreasury, 2006). In turn, mortgage rates, whichaveraged 11.5 per cent between 1979 and 1997, haveaveraged 6 per cent over the last eight years (HMTreasury, 2006). Employment is historically high,unemployment low and inactivity falling (HMTreasury, 2006).

This stable economic framework has provided abackdrop to ongoing structural shifts in the labourmarket, partly driven by technological change anddifferential productivity growth, partly by‘globalisation’ and international competition, andpartly by changing patterns of consumer demand(Dixon and Pearce, 2005;Wilson et al, 2006).Aspeople have become richer, they have tended tospend more of their income on services, such ashaircuts, cinemas and financial advice, and less ongoods, such as videos,TVs, washing machines and

1: Financial capability in the 21st century

even computers, as most manufactured goods havebecome more affordable so less needs to be spent onthem (Hills, 2004).

In combination with rising female employment, whichhas brought many jobs that women used to do unpaidinto the formal labour market, this has led to morepeople being employed in service industries and fewer inmanufacturing.The statistics are compelling: in 1982,33.6 per cent of total employment was in themanufacturing, construction and utilities sectors and65.4 per cent was in the service sector; by 1992 thefigures were 27.1 per cent and 72.8 per centrespectively; and by 2004 they were 20.6 per cent and79.4 per cent.This trend is expected to continue overthe next decade at least: by 2014 service-sectoremployment is projected to be 82 per cent of allemployment, with manufacturing, construction andutilities having shrunk to 18 per cent, nearly half of its1982 share (Dixon and Pearce, 2005;Wilson et al, 2006).

The implications of this shift for financial capabilityremain relatively unclear, although it is likely thatservice sector employees will require higher levels of

financial capability in their jobs. Most indicators pointto continued growth in demand for financial services(Wilson et al, 2006), a trend that will exacerbate theneed for consumers to be able to make the rightdecisions in choosing appropriate products.

More speculatively, others (FSA, 2003) have pointed totrends that make financial capability more important: apurported decline in ‘jobs for life’ and greaterflexibility in people’s careers, alternating periods oflearning or caring with paid employment.Twenty-eight per cent of people have experienced a largeunexpected drop in income in the last three yearswhile nearly half have no savings (Atkinson et al,2006).As people live more complex lives in which it isharder to plan for the long term, their need forpersonalised, tailored products to meet increasinglycomplex demands becomes more pressing.

Other trends are also important. Owner occupationhas increased rapidly - by 46 per cent between 1981and 2004, to 17.8 million dwellings (Babb et al, 2006).This has resulted in a greater need for financialcapability, as people have to take on greater financial

Rethinking Financial Capability14

and other responsibilities than when renting, and bebetter at planning ahead for large, irregularexpenditure, such as repairs or other improvements.

These trends have been reflected in the rapidlychanging nature of the financial services industry.Following the deregulatory ‘big bang’ of 1986 andsubsequent reforms, which vastly increasedcompetition in financial markets, there was a hugeexpansion in the scale, scope and range of financialservices offered to consumers. Building societiesdemutualised and raised finance through shareofferings, increasing the range of providers, andfinancial service institutions began to offer a muchwider range of products than before.Total lendingmore than doubled from £531 billion in 1993 to£1,077 billion in 2005 (prices indexed to 2004) andconsumer credit expanded even faster, by 167 per centover the same period (Babb et al, 2006).

The changes to people’s financial holdings have beenrapid, particularly in an historical context. For much ofthe twentieth century, (predominantly male) workerstook home their cash in a weekly pay packet; relatively

few had need of bank accounts.As living standardsincreased and people’s disposable income grew - partlydue to women entering the labour market, creatingdual-earner households - people began to turn tointermediaries to help secure and manage their money.But even by the standards of this unprecedenteddevelopment, the last few decades have seen a largeshift in people’s financial portfolios (FSA, 2003;Kempson and Whyley, 1999).

These trends in product offerings look set to continue.And if they do, it will become increasingly importantthat people can manage and understand the portfolioof products available to them, as many of these newproducts are relatively complex and require a greaterdegree of financial capability.

The developments have not all been on the supplyside of the financial services industry.The hugeinflationary pressures seen in the housing market, withpeople taking up 100 per cent mortgages onproperties - often relying on continued house pricegrowth - also places much greater reliance on UKcitizens’ financial capability.

Rethinking Financial Capability 15

Many people in the UK have been slow to realise thisgrowing salience, perhaps due to the relatively benigneconomic conditions of the past decade: strongeconomic conditions can hide low levels of financialcapability.Widespread negative equity is a relativelydistant memory, although still a painful one. But it isvital to remember that economic conditions change; itis unlikely that the prosperity of the last ten years willcontinue indefinitely.When things do start to shift, thebrunt is likely to fall hardest on those who are leastfinancially capable.

There are already some worrying signs.The level ofindividual insolvencies is rising rapidly: one persondeclared insolvency every 11 minutes in 2004, nearlytwice the rate of seven years before, and £4.2 billionof bad debts was written off by banks, nearly doublethe total of four years previously (DTI, 2005). Creditcard debt write-offs have risen to £1.6 billion from£0.28 billion in 1993 (Babb et al, 2006).And six percent of people - ten per cent of those aged over 85 -do not have bank accounts (DWP, 2005a), despiteconsiderable efforts to eradicate the most extremeforms of financial exclusion.All these trends suggest

that we should not slip into sanguinity: financialcapability will become ever more crucial over thecoming decade.

The demographic contextLooking even further ahead, it is clear that the UKfaces serious fiscal challenges that will have animportant bearing on the personal finances of itscitizens. Perhaps the most important of these is theinevitable ageing of the population over the next halfcentury (Dixon and Margo, 2006). Life expectancy inthe UK is longer than ever before (Dixon and Margo,2006): there were 9.5 million people aged 65 or overin the UK in 2001 but this is projected to rise to 12.8million by 2021, and to 16.7 million by 2044 - whenthere will be more than twice as many octogenarians(GAD, 2005).The picture is radically different to thatof 30 years ago and will only become more so. In2001 there were 21 per cent fewer children under theage of 16, and 23 per cent more people aged 65 orolder than in 1971; by 2044 these figures will havespiralled to 31 per cent and 56 per cent respectively(Dixon and Margo, 2006).

Rethinking Financial Capability16

These shifts in the age structure are familiar and havesome well-rehearsed implications.The number ofpeople of working age for every ‘dependent’ rose from1.6 in 1971 to 1.8 in 2001 as the ‘baby boom’generations of the late 1940s and mid 1960s entered thelabour force, but it will fall to 1.4 by 2044 as thesecohorts enter retirement (Dixon and Margo, 2006).Thiswill have a profound knock-on effect on governmentspending on a range of areas, including pensionsprovision, health spending and long-term carefinancing. Modelling by ippr earlier this year estimatedthat total public spending would have to rise by 2.6 percent of gross domestic product (GDP) by 2051 and afurther 1.6 per cent by 2074, to keep per capitaspending levels at their current rate (Dixon and Margo,2006).

The implications for financial capability are obvious: ifpeople in the UK do not save for their retirement, theywill face a considerable risk of poverty later in life.Similar implications hold true for long-term careprovision: too few people are saving for retirement(Atkinson et al, 2006; Pensions Commission, 2005). Onereason is that people simply do not believe the official

statistics: few people in the UK think that they will livelonger than the generation before - most expect theirhealth to decline from the age of 70 - which partlyexplains why there has been such strong resistance toraising the state pension age (Robinson et al, 2005).

Promoting financial capability must be an integral partof the response to an ageing population. But ageing isnot the only relevant demographic trend for thisagenda: the recent rise in solo living, increasinglydiverse family structures and divergent fertility trendsall mean that navigating the financial marketplace willcontinue to be an ever more important skill (Dixonand Margo, 2006).To take one example, people wholive alone are less able to rely on someone to supportthem in a time of financial crisis or redundancy, whichmeans that assets, insurance and savings are moreimportant for this group than many others (Bennetand Dixon, 2006; Dixon and Margo, 2006).

The cultural contextThese demographic shifts cannot be seen in isolationfrom the changing cultural milieu of modern Britain.

Rethinking Financial Capability 17

Public attitudes have inevitably evolved over a widerange of areas in the last few decades, and willcontinue to do so in the future.These changingexpectations have partly driven demographic changeand have been partly influenced in their turn by thechanging structure of the population. But they alsohold enormous importance for financial capability.

Perhaps the most profoundly relevant cultural shift ofthe past century has been a shift from a ‘thrift ethic’,where people limit their consumption of goods towhat they can afford at the time, to a ‘consumptionethic’, where people buy now and pay later (Tucker,1991;Webley, 2006). People are more willing thanever before to take on debt and use credit in returnfor more immediate gratification, and less willing tothink for the long term. Although it is difficult todisentangle cause and effect here, public policy, muchbusiness practice and economic trends have arguablyall contributed towards this shift, as well as respondedto it. For example, credit has become easier to getand use; policy has often, understandably, focused onshort-term outcomes, such as getting people into ajob rather than prioritising progression in the labour

market, and has made debt a more inevitable part oflife through the introduction of student loans inplace of grants; and many companies have focused onchildren and adolescents as an important retailmarket, effectively ‘commercialising’ childhood(Schor, 2004).

Some parts of the media have also played an importantrole here.Although the last decade has seen a rise inpersonal finance, ‘Money Matters’ or ‘Money’ sectionsof regional and national newspapers - often providingexcellent analysis and advice - these stand in markedcontrast to coverage that normalises the idea of lowfinancial capability and high debt levels.Commentators have coined new terms such as‘homeowner debt’, ‘newlywed debt’, ‘student debt’,and ‘pensioner debt’ - and characterised financialproblems as trivial or even glamorous. One recentexample is the former BBC correspondent RosieMillard, writing in the Sunday Times in 2005, proudlydetailing her private financial problems alongside largepictures of her two plush homes and four children.Her serious debt problems were reported as somehowirrelevant to her happy, successful, rich life.

Rethinking Financial Capability18

‘Am I curtailing my lifestyle? Well, I have dramatically curbedmy addiction to black cabs, but can’t live without a decent haircutevery eight weeks, vaguely designery suits, Stila makeup andThe New Yorker.As I say to my bank manager (whose mobilenumber is naturally on my direct dial), if you want to keepworking, you have to keep looking the part.’ (Millard, 2005)

Welfare state retrenchmentPolicy changes over the last two decades, particularlyunder the previous government, have made it moreimportant for UK citizens to be financially capable,although this has been partly masked in recent yearsby the strength of the economy.The scaling back ofnational insurance benefits, such as unemploymentbenefit and incapacity benefit, the breaking of the linkbetween the basic state pension and earnings (Hills,2004), and reductions in support for homeowners(Burrows and Wilcox, 2000) have meant that manymore people now have to protect themselves against illhealth, disability, unemployment and old age throughfinancial products.This places much greaterimportance on people’s ability to plan ahead and tochoose appropriate products for their needs.

Political contextThese economic, demographic, cultural and policytrends have shifted the political context in many areas.Pensions policy is a matter of urgent national debate,for example (Pensions Commission, 2005). Butlooking deeper, there are signs of a wholesale shifttowards the importance of personal responsibilityacross many areas of the Government (Halpern et al,2004), prompted by moral and political arguments asmuch as fiscal concerns. New Public Management andsubsequent shifts in thinking have led to a conceptionof citizens as active consumers of public services, inwhich personal ‘choice’ is ever more important, asboth a delivery mechanism and a valuable end in itself(Byrne et al, 2006; Pearce and Paxton, 2005).Also the‘empowerment agenda’ that is steadily gaining groundacross the Government similarly sees more activecitizens as crucial to more effective governance(Miliband, 2006).

The political concern for financial capability can beunderstood as part of this overall shift in thinking,which sees the state as playing an enabling role inproviding people with the opportunities to achieve

Rethinking Financial Capability 19

their aspirations.This thinking places personalresponsibility to the fore, but without shirking thevery real responsibility that the Government must take

in helping them to do so. But how far do we have togo? How financially capable is the UK? This questionis explored in the following section.

Rethinking Financial Capability20

The UK now leads the world in its understanding ofhow its citizens use and think about money (SEDI,2004).The initial analysis of the groundbreakingFinancial Capability Baseline Survey (FSA, 2006a),carried out by researchers at the University of Bristol(Atkinson et al, 2006), reveals for the first time the trueextent and levels of financial acumen in the UK.Asthe data is analysed further, a more detailed picturewill emerge, providing policymakers with a wealth ofdetail on which to base initiatives and developstrategies. So what does it show?

Financial capability measures a broad range of skills,behaviour and knowledge, but can broadly beunderstood as consisting of five separate strands(Atkinson et al, 2006): making ends meet, keepingtrack, planning ahead, choosing products and stayinginformed. It is crucial to realise that financial capabilityis an amorphous concept with many levels andcomponents: this means that we cannot simply say that

someone is financially capable or that they are not -people are often very capable in some areas but not inothers. For example, people on low incomes are oftenbetter at keeping track of their money than those onhigher incomes, but are not as good at choosingproducts.

Unfortunately it is not currently possible to assess levelsof financial capability in an international context. Mostother countries use measures of financial literacy that donot capture the crucial behavioural element central tofinancial capability.This section therefore focuses onoverall levels of financial capability in the UK inisolation, summarising recent work by Elaine Kempson,Adele Atkinson, Stephen McKay and Sharon Collard atthe Personal Finance Research Centre, University ofBristol (Atkinson et al, 2006).

Section 3 below uses this analysis to identify prioritygroups and key factors in determining financial

2: Financial capability in 2006

capability, and explores the ‘motivation barrier’ behindseeking financial advice and changing behaviour.

Overall levels of financial capabilityPeople in the UK are storing up trouble for the future(FSA, 2006c).Too many are failing to plan ahead forretirement or for an unexpected drop in income,despite the fact that most can afford to do so.Aroundtwo million households are living in a precariousfinancial position and could be pushed into difficultiesby a small change in their circumstances - a commonexperience.Although only a small proportion ofpeople have severe debt problems, those who do areoften very seriously affected.Too many people take oninappropriate risks - either protecting themselvesagainst risks they do not face, or failing to insurethemselves against those they do.Also too many simplychoose the first financial product that appears toroughly suit their needs, needlessly wasting substantialsums of money (Atkinson et al, 2006).

If the current situation is troubling, the prospectslooking ahead are worrying.Younger people are less

likely to be financially capable than previousgenerations, even allowing for their relativeinexperience in dealing with financial products andinstitutions.This suggests that as these groups moveinto later life, the UK will become less financiallycapable than it is today unless action is taken.This isparticularly worrying, given the analysis in Section 1,which shows that these generations are likely to have agreater need for financial capability than their parentsand grandparents.

Of course, many people have a good grasp of theirfinances and experience few difficulties, particularly inmaking ends meet and keeping track of their money.

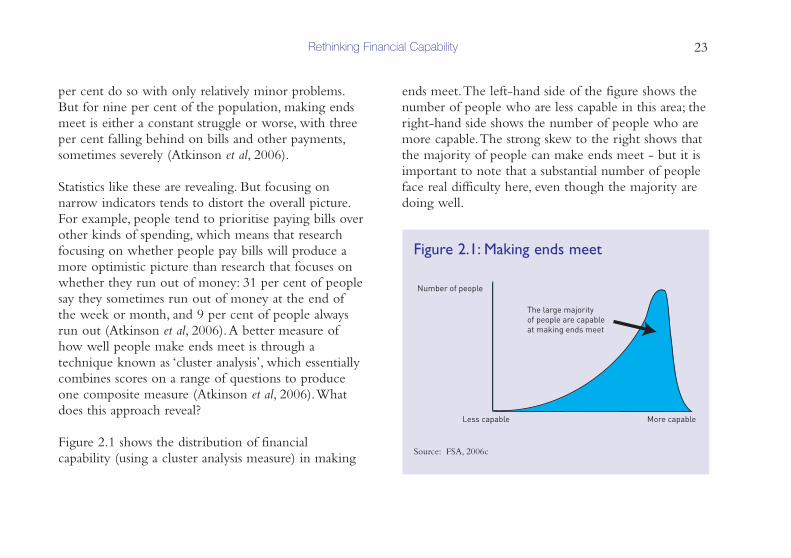

Making ends meetMaking ends meet is about how well people livewithin their means. Someone who is good at makingends meet would rarely be overdrawn or run short ofmoney, and would tend to pay off their credit card billat the end of every month.As a nation, the UK ispretty good at making ends meet. For example, 65 percent of people keep up with their bills and othercommitments without any difficulties and another 26

Rethinking Financial Capability22

per cent do so with only relatively minor problems.But for nine per cent of the population, making endsmeet is either a constant struggle or worse, with threeper cent falling behind on bills and other payments,sometimes severely (Atkinson et al, 2006).

Statistics like these are revealing. But focusing onnarrow indicators tends to distort the overall picture.For example, people tend to prioritise paying bills overother kinds of spending, which means that researchfocusing on whether people pay bills will produce amore optimistic picture than research that focuses onwhether they run out of money: 31 per cent of peoplesay they sometimes run out of money at the end ofthe week or month, and 9 per cent of people alwaysrun out (Atkinson et al, 2006).A better measure ofhow well people make ends meet is through atechnique known as ‘cluster analysis’, which essentiallycombines scores on a range of questions to produceone composite measure (Atkinson et al, 2006).Whatdoes this approach reveal?

Figure 2.1 shows the distribution of financialcapability (using a cluster analysis measure) in making

ends meet.The left-hand side of the figure shows thenumber of people who are less capable in this area; theright-hand side shows the number of people who aremore capable.The strong skew to the right shows thatthe majority of people can make ends meet - but it isimportant to note that a substantial number of peopleface real difficulty here, even though the majority aredoing well.

Rethinking Financial Capability 23

Number of people

Less capable More capable

The large majorityof people are capableat making ends meet

Figure 2.1: Making ends meet

Source: FSA, 2006c

But what differentiates those who are good at makingends meet from those who have real difficulties?Regression analysis, a statistical technique that allowsimportant factors to be isolated, reveals that olderpeople are much better at making ends meet, as arethose who own their own home, and those withhigher educational qualifications (after controlling forall other factors). Perhaps surprisingly, income makesrelatively little difference - those in the highest incomegroup are only a little more likely to say that theymake ends meet than those in the lowest (Atkinson etal, 2006).This backs up the idea that behaviour andattitudes are much more important than levels ofaffluence in financial capability.

Keeping track of financesFor some people, keeping track of finances is ofparamount importance: it can be essential to knowhow much money they have available to the nearestpound. For others, particularly those on higherincomes or with easier access to credit and savings,keeping track is much less important - a general ideaof how much money they have is all they need. Sevenper cent of people could not place their current

account balance to within £500 while 21 per cent canpinpoint it to a pound or two (Atkinson et al, 2006).This makes it difficult to say how important keepingtrack is in determining a person’s overall financialcapability, and reinforces the idea that financialcapability is best understood as a complex conceptcomposed of discrete, but related elements.

Someone who is good at keeping track of theirfinances will typically: know the amount in theiraccount to a degree that is appropriate for theirincome and outgoings, with those on higher incomesneeding to know the balance less precisely; check theamount in their current account (or in hand for cashbudgeters) frequently - 38 per cent of people do thiseach time they withdraw money while 14 per centnever check; budget to cover uneven expenditure, suchas utility bills, council tax or TV licence.

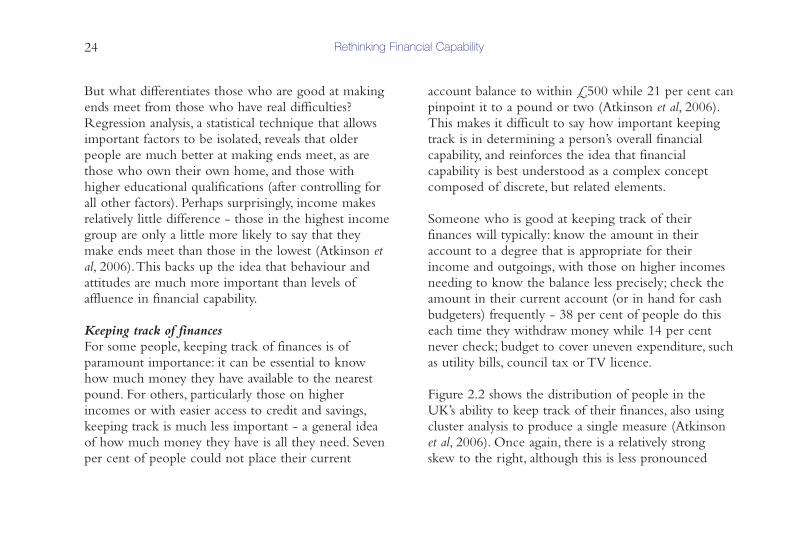

Figure 2.2 shows the distribution of people in theUK’s ability to keep track of their finances, also usingcluster analysis to produce a single measure (Atkinsonet al, 2006). Once again, there is a relatively strongskew to the right, although this is less pronounced

Rethinking Financial Capability24

than for ‘making ends meet’, suggesting a greatervariation in people’s ability to keep track. Moreworryingly, there are a far greater number of peoplewho are poor in this area: 10 per cent of people makeno provision for quarterly or annual bills, and six percent ignore bank statements completely.

Regression analysis shows that people who havedifficulty in making ends meet tend to be better than

average at keeping track of their finances.This makessense: it is more important to know exactly how muchmoney you have at any one time if you are on a tightbudget.This means that lone parents, people without acurrent account, and the unemployed tend to beparticularly capable in this area.Women are also betterthan men on average. Interestingly, age seems to makelittle difference to people’s tendency to keep track,suggesting that this is not a behaviour learned overtime, but one related to necessity (Atkinson et al,2006).

Planning aheadPeople who are good at planning ahead tend to havemade sufficient provision for an unexpected drop inincome, would be able to make ends meet for a yearor more if their income dropped unexpectedly, tend tobuy insurance and contribute to a pension (FSA,2003).These attributes are crucial determinants ofpeople’s future well-being, particularly given theeconomic, demographic, cultural and political trendsoutlined in Section 1; this component of financialcapability is arguably the most important for aprogressive government.

Rethinking Financial Capability 25

Number of people

Less capable More capable

People in the UK are reasonably capableat keeping track

Figure 2.2: Keeping track

Source: FSA, 2006c

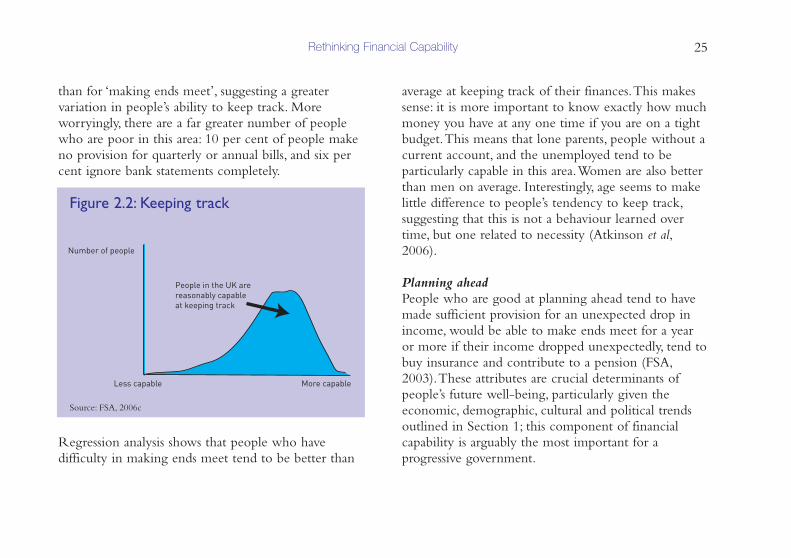

Yet worryingly, although perhaps not surprising, thestatistics show that many people in the UK are very bad atplanning ahead.Thirty-nine per cent of people in the UKsaid that they ‘live for today and let tomorrow take care ofitself ’ and just 42 per cent of those under retirement agesaid they had a personal pension (Atkinson et al, 2006).Looking at the distribution of scores in Figure 2.3 belowshows this clearly: a substantial proportion of thepopulation do not adequately plan ahead.

Looking in detail at the numbers behind this figurereveals that older people are much better at planningahead than younger people, taking all other factorssuch as income and education levels into account, asare those who perform better in making ends meet.People who do not have a current account are muchworse, as are those who live in deprived areas.Thosewho are better off are more likely to plan ahead, butincome by no means determines behaviour in thisdomain: plenty of those on very high incomes makeno provision for the future. One particularlyinteresting finding from regression analysis is thatpeople who receive free financial products from worktend to be much better at planning ahead, even whenother factors are taken into account (Atkinson et al,2006).This suggests that once people make a start inplanning ahead, this can trigger further efforts - anidea discussed in more detail in Sections 5 and 6.

Crucially, this is an area where people’s statedintentions and views do not match their behaviour.Totake two examples, three-quarters of people say theyalways make sure they have some money saved for arainy day, but in reality 70 per cent have made no

Rethinking Financial Capability26

Number of people

Less capable More capable

Nearly half of the UKpopulation appears tobe making insufficienteffort or is unable toplan ahead

Figure 2.3: Planning ahead

Source: FSA, 2006c

provision to face a drop in income and nearly halfhave no savings; and while 81 per cent of the pre-retired think that the state pension will not be enoughto give them the standard of living they would like, 37per cent have made no provision for themselves(Atkinson et al, 2006).

Choosing financial productsMany people find financial products confusing. Earlyresearch by the Financial Services Authority (FSA)revealed that two-thirds of consumers think thatfinancial matters are ‘too complicated for them’ andthat they do not know enough to choose suitablefinancial products (FSA, 2003).To take one example,forty per cent of those who own an equity IndividualSavings Account (ISA) did not know that the cashvalue of their investment depends on stock marketperformance, and 15 per cent of those who own acash ISA wrongly think that it does (Atkinson et al,2006).This often results in people buyinginappropriate or unnecessary products and missing outon ones that could meet their needs. For example,nine per cent of people renting from a private landlordhold buildings insurance, at significant expense, when

they will never see a return on their policy; and tenper cent of homeowners do not have buildingsinsurance, exposing them to enormous potential loss(Atkinson et al, 2006).

This lack of understanding means that people in theUK tend to buy financial products in a very differentway to other goods.Although many financial productsare expensive and represent a substantial outlay, peopleare often reluctant to shop around for the best deal ortake advice: 21 per cent of people take no advice at alland 42 per cent rely on friends, product information,relatives or sales staff, rather than consulting aprofessional advisor or making an active effort to findout what the best buy is.This is despite there being awealth of available information in newspapers andonline (Atkinson et al, 2006).

People also appear to pay remarkably little attention tothe price of financial products: 51 per cent of savingsaccount holders can estimate the current level ofinterest, and only 49 per cent of people choose acredit card based on the interest rate, with 11 per centsimply opting for the one that came with their current

Rethinking Financial Capability 27

account (Atkinson et al, 2006). People are alsoreluctant to change products once they have boughtone, often sticking with the same insurance policy, oreven the same mortgage, for years - even thoughother, more suitable products may be available.Thisfinding still holds true in extremely competitivemarkets, such as car insurance, where 52 per cent ofpolicy holders have not even considered switching inthe last five years.The figure for mortgages is 58 percent (Atkinson et al, 2006) - a surprisingly high figureconsidering the enormous sums of money usuallyinvolved.

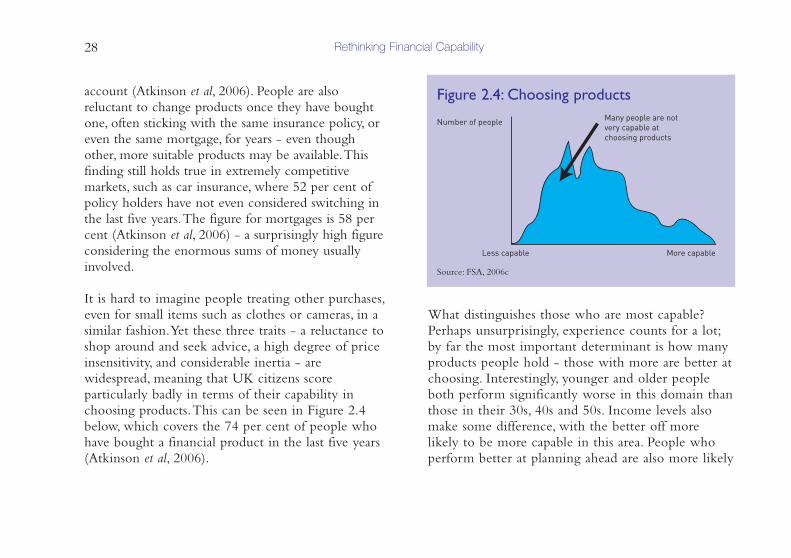

It is hard to imagine people treating other purchases,even for small items such as clothes or cameras, in asimilar fashion.Yet these three traits - a reluctance toshop around and seek advice, a high degree of priceinsensitivity, and considerable inertia - arewidespread, meaning that UK citizens scoreparticularly badly in terms of their capability inchoosing products.This can be seen in Figure 2.4below, which covers the 74 per cent of people whohave bought a financial product in the last five years(Atkinson et al, 2006).

What distinguishes those who are most capable?Perhaps unsurprisingly, experience counts for a lot;by far the most important determinant is how manyproducts people hold - those with more are better atchoosing. Interestingly, younger and older peopleboth perform significantly worse in this domain thanthose in their 30s, 40s and 50s. Income levels alsomake some difference, with the better off morelikely to be more capable in this area. People whoperform better at planning ahead are also more likely

Rethinking Financial Capability28

Number of people

Less capable More capable

Many people are not very capable atchoosing products

Figure 2.4: Choosing products

Source: FSA, 2006c

to be better at choosing products (Atkinson et al,2006).

Staying informedThe fifth component of financial capability concernswhether people stay informed about financial matters.This includes monitoring changes in key financialindicators, such as interest rates, stock marketfluctuations or the housing market; having a good levelof applied financial literacy; and thinking it isreasonably important to keep up with financial matters(FSA, 2006c).

Most people (72 per cent of people in the UK) thinkthat staying informed is important and 78 per centkeep up with at least one financial indicator. But asizeable minority are less engaged, with around a fifthof people saying they do not keep track of anyfinancial indicators at all. Perhaps unsurprisingly,people are most likely to follow the bigmacroeconomic indicators - such as interest rates,changes in the state pension or the housing market;whereas only about one in ten people claim to keepup with the best buys in financial products (Atkinson

et al, 2006). But what sources of information dopeople rely on?

Despite the growth of online financial advice sites,newspapers remain the most common source offinancial information for most UK citizens with 41per cent relying on these to stay informed. Around39 per cent glean their information from televisionand radio programmes, although 7 per cent watch orlisten to dedicated programmes such as Radio 4’sMoneybox.This suggests that most people tend toabsorb financial information without making adedicated effort to do so - they pick it up from themedia they come across as part of their everyday lives(Atkinson et al, 2006).

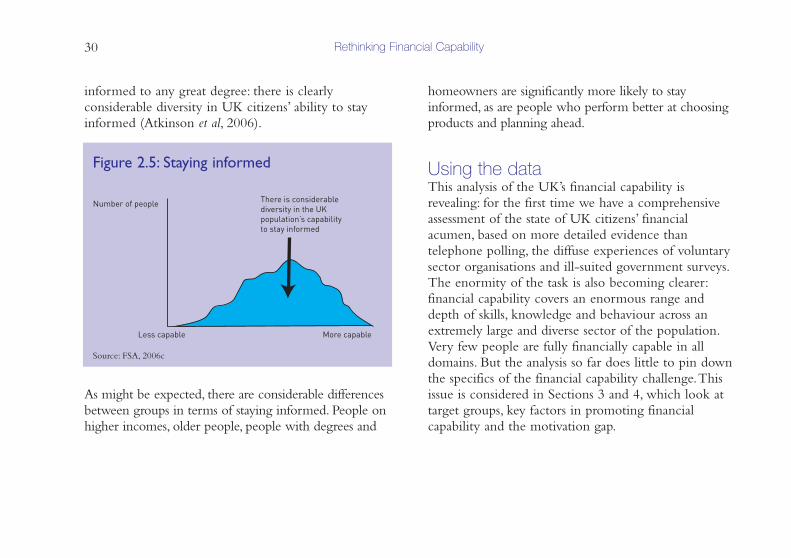

Although 72 per cent of people think that stayinginformed is important, the cluster analysis undertakenby researchers at Bristol University suggests that farfewer live up to their expectations.Twelve per cent ofthose who think it is important openly admit that theydo not really keep up to date. But the results of theFinancial Capability Baseline Survey, shown in Figure2.5, suggest that a far greater proportion do not stay

Rethinking Financial Capability 29

informed to any great degree: there is clearlyconsiderable diversity in UK citizens’ ability to stayinformed (Atkinson et al, 2006).

As might be expected, there are considerable differencesbetween groups in terms of staying informed. People onhigher incomes, older people, people with degrees and

homeowners are significantly more likely to stayinformed, as are people who perform better at choosingproducts and planning ahead.

Using the dataThis analysis of the UK’s financial capability isrevealing: for the first time we have a comprehensiveassessment of the state of UK citizens’ financialacumen, based on more detailed evidence thantelephone polling, the diffuse experiences of voluntarysector organisations and ill-suited government surveys.The enormity of the task is also becoming clearer:financial capability covers an enormous range anddepth of skills, knowledge and behaviour across anextremely large and diverse sector of the population.Very few people are fully financially capable in alldomains. But the analysis so far does little to pin downthe specifics of the financial capability challenge.Thisissue is considered in Sections 3 and 4, which look attarget groups, key factors in promoting financialcapability and the motivation gap.

Rethinking Financial Capability30

Number of people

Less capable More capable

There is considerablediversity in the UKpopulation’s capabilityto stay informed

Figure 2.5: Staying informed

Source: FSA, 2006c

Policy is often most effective when it responds tospecific, detailed needs.This makes improving the UK’sfinancial capability a particularly daunting task for twomain reasons.The first is the scale and diversity of thetarget group: just 36 per cent of people are fullyfinancial capable (Atkinson et al, 2006), which meansthat more than 30 million adults in the UKexperience difficulties in managing their finances(GAD, 2005).The second is the sheer breadth of theconcept of financial capability: it is a deliberatelyinclusive and wide-ranging idea that covers a plethoraof skills, behaviours, and generic and product-specificknowledge over several distinct domains. How shouldpolicy respond?

There is a clear need to determine priorities. It isunrealistic to think that policy can improve allelements of financial capability for everyone.The keyissue is where and how UK citizens’ low levels offinancial capability are creating, and will continue to

create, the greatest problems for society in general and,specifically, where and to what extent they affect thefinancial services industry. Resolving this issue wouldset policy priorities. It would also help determine theappropriate balance of responsibility betweengovernment, the financial services industry and otherstakeholders for funding and delivering the financialcapability agenda in the future.

The impact of low financial capabilityIn an ideal world we would be able to determinethe cost of current levels of financial capability,revealing where and how these affect the UK andthe gains to be made from policy efforts to improvethem. Unfortunately this depth of analysis remainsbeyond us for the immediate future, although efforts,led by the Resolution Foundation, are ongoing todevelop a working model.What should we expectthis to show?

3: Priorities for action and future funding

Impact on individualsLow levels of financial capability clearly harmindividuals, who are not protected against the risksthey face, experience higher costs and miss out onopportunities to save and benefit from financialproducts. Although a lack of financial capability inall the areas explored above can have negativerepercussions for individuals, perhaps the mostworrying area is people’s tendency not to planahead adequately, particularly for retirement but alsofor unanticipated income changes. Lack of financialcapability can have a considerable effect on people’swell-being: we know that financial concerns are amajor cause of stress and even ill health (FSA,2003).Yet despite these benefits it is clear thatleaving it up to individuals to improve theirfinancial capability without appropriate support willnot be enough.

Impact on the voluntary sectorThe voluntary sector as a whole would also benefitfrom improved financial capability (FSA, 2003):charities focusing on financial matters would be ableto prioritise their preventative work - which is often

more cost-effective than palliative efforts - enablingthem to make more effective use of often scarceresources.Also charities working with other clientgroups, whose problems are often exacerbated byfinancial difficulties, would see a reduction in thecomplexity of issues faced by their clients, enablingthem to provide a more effective response.

Impact on the financial services industryLow financial capability has clear costs for the financialservices industry, particularly in terms of planningahead and choosing products.A more capable Britainwould result in greater consumer confidence inmarkets and firms, and a subsequent increase indemand for financial products. Consumer vulnerabilityto mis-selling would be lower with a subsequentreduction in costs due to handling complaints and lessregulatory intervention (FSA, 2003).

There is also the possibility of growing new marketsand creating greater value from existing customers.Research by the Resolution Foundation suggests thereis a large group of people on low to median incomeswho have the capacity to save for a pension but are

Rethinking Financial Capability32

not currently doing so, representing a large under-tapped market (Resolution Foundation, 2006b).

These considerations suggest that the financial servicesindustry has a sizeable stake in improving the UK’sfinancial capability, and there are significant gains to bemade from a successful strategy.The industry, taken asa whole, also seems well placed to increase funding,given recent record profits made by many financialinstitutions, totalling £30 billion last year - althoughmuch of this was derived from overseas activities (TheGuardian, 2006).

Impact on government and society more broadlyFrom the perspective of government, there is also aclear rationale for tackling financial capability issues.From an economic point of view, improving people inthe UK’s ability to manage their money would have asignificant impact on government revenue andspending. From the revenue side, a flourishing financialservices industry is an important contributor to thepublic purse and it is in the Government’s interest toensure that people have confidence in financialproducts.

In terms of public spending, perhaps the mostimportant issue is in terms of future pensioncommitments - linked to the planning ahead aspect offinancial capability. Quite simply, if people in the UKdo not start saving more or working later, theGovernment will have to accept much higher levels ofpensioner poverty or face soaring public expenditure(Pensions Commission, 2005).This should be acompelling argument in itself. But there are manyothers. For example, there is the potential to reducesome forms of welfare spending, as people would be lesslikely to fall into serious debt problems and more likelyto have taken out insurance against the risks they face,with subsequently less reliance on the state.There is alsothe potential for existing benefit payments to have moreimpact on people’s lives - reducing the extent to whichthese payments go towards servicing existing debt ratherthan improving standards of living.There would be costsavings in other areas too, in terms of freeing upresources to focus on more effective preventativeservices rather than palliative ones.

Economic arguments such as these are importantconsiderations for the Government. But there is also a

Rethinking Financial Capability 33

compelling social case for the Government toprioritise this agenda. Lower levels of financialcapability - including the likelihood of saving for apension - are broadly correlated with disadvantage.The worst off are also likely to be more profoundlyaffected by the underlying socio-economic, culturaland political shifts outlined in Section 1.

Competing priorities?There should be no surprise that differentstakeholders are interested in different aspects offinancial capability. For example, for charities thatfocus on social exclusion, people’s capacity to makeends meet is of greater concern than their ability tochoose between financial products; whereas for afirm specialising in mortgage broking or devisingniche insurance products, people’s capacity to choosebetween financial products is of paramountimportance.While government needs to focus onthe social and moral case for financial capability, theprivate sector must see it through the lens of abusiness case. But do these really differ as much asmight be thought?

There are some good reasons to think so. Many peoplein the UK do not represent a particularly profitableopportunity for the financial services industry, certainlyin terms of providing financial advice (ResolutionFoundation, 2006b).Those on low to median incomesare often proportionately more expensive for banks andother institutions to service, for example, because theymake smaller deposits and withdrawals at counters, andare consequently less profitable.They also have less toinvest in financial products.Yet this simple analysisoverlooks considerable harmony between the aims ofthe government and the financial services industry. Onegood example is the financial behaviour of people onmoderate to low incomes who already use somefinancial services.This is a key target group for theGovernment in terms of pension saving but alsorepresents a substantial growth market for the financialservices industry, if suitable and cost-effective deliverymechanisms can be developed.

Future fundingIt is clear that individuals, the private sector andparticularly the financial services industry, the

Rethinking Financial Capability34

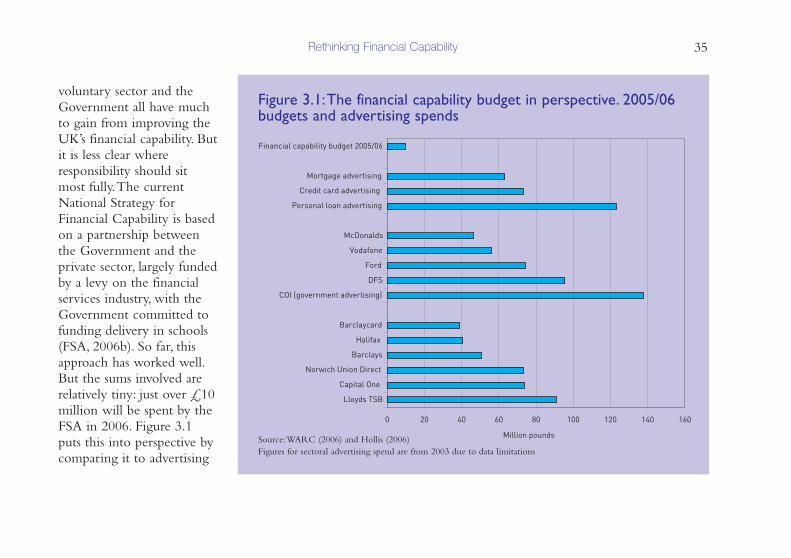

voluntary sector and theGovernment all have muchto gain from improving theUK’s financial capability. Butit is less clear whereresponsibility should sitmost fully.The currentNational Strategy forFinancial Capability is basedon a partnership betweenthe Government and theprivate sector, largely fundedby a levy on the financialservices industry, with theGovernment committed tofunding delivery in schools(FSA, 2006b). So far, thisapproach has worked well.But the sums involved arerelatively tiny: just over £10million will be spent by theFSA in 2006. Figure 3.1puts this into perspective bycomparing it to advertising

Rethinking Financial Capability 35

0 20 40 60 80 100 120 140 160

Lloyds TSB

Capital One

Norwich Union Direct

Barclays

Halifax

Barclaycard

COI (government advertising)

DFS

Ford

Vodafone

McDonalds

Personal loan advertising

Credit card advertising

Mortgage advertising

Financial capability budget 2005/06

Million pounds

Figure 3.1:The financial capability budget in perspective. 2005/06budgets and advertising spends

Source:WARC (2006) and Hollis (2006)Figures for sectoral advertising spend are from 2003 due to data limitations

spending by the financial services industry, othercompanies and the Government.

The enormous discrepancy between the fundingavailable to deliver a National Strategy and the annualadvertising spent on credit cards, personal loans andmortgages is clear. For every pound spent onpromoting financial capability, £7.30 is spentadvertising credit take-up and £12.30 on promotingpersonal loans (FSA, 2006a; Hollis, 2006;WARC,2006).

A broader comparison with other areas is revealing.Ford Motor Company spends £7.41 for every poundin the Financial Capability budget (Hollis, 2006),predominantly aiming to shift improve publicperceptions of the ‘quality’ of Ford cars. DFS spends£9.55 trying to alter people’s furniture-buying habits.The financial services industry as a whole spends£204 on advertising for every pound spent onpromoting financial capability - although of coursemuch of this advertising is aimed at encouragingsaving and other beneficial financial behaviours(Hollis, 2006).