Embed Size (px)

Citation preview

Research in management accounting innovations: an overview of its development

Nur Haiza Muhammad Zawawi

and

Zahirul Hoque*

Department of Accounting La Trobe University, Australia

*Corresponding author’s address: Professor Zahirul Hoque, School of Accounting, La Trobe University, Victoria, 3086 Australia; Tel (613) 9479 3433; Fax (613) 9479 2356; Email: [email protected]

Paper prepared for the Second New Zealand Management Accounting

Conference, Auckland 20-21 November 2008

1

Research in management accounting innovations: an

overview of its development

Abstract This paper reviews prior research in management accounting innovations covering the period 1926-2008. Management accounting innovations refer to the adoption of “newer” or modern forms of management accounting systems such as activity-based costing, activity-based management, time-driven activity-based costing, target costing, and balanced scorecards. Although some prior reviews, covering the period until 2000, place emphasis on modern management accounting techniques, however, we believe that the time gap between 2000 and 2008 could entail many new or innovative accounting issues. We find that research in management accounting innovations has intensified during the period 2000-2008, with the main focus has been on explaining various factors associated with the implementation and the outcome of an innovation. In addition, research in management accounting innovations indicates the dominant use of sociological-based theories and increasing use of field studies. We suggest some directions for future research pertaining to management accounting innovations.

Introduction A considerable number of scholars have conducted reviews on management accounting and control research, with particular timeframe and scope.1 The purpose of this paper is to extend these reviews, particularly by Hesford, Lee, van der Stede and Young (2007), Ittner and Larker (1998), Scapens and Bromwich (2001), Selto and Widener (2004), Shields (1997), Otley, Broadbent and Berry (1995), and Young and Selto (1991). These authors examined the topics studied, theories applied and methods used in the literature to provide understanding on the trend and development of management accounting and control research. Building upon these reviews, in this paper we focus on research in management accounting innovations to explore its recent development and to come up with some directions for future research. Table 1 summarizes the attributes of the above reviews and illustrates how the current review is different from prior reviews. As can be seen from Table 1, Young and Selto (1991) reviewed empirical research in cost management topics published prior to 1990. Their review centred on a framework that outlines several interrelated variables in order to

1 The review papers on management accounting , inter alia Elnathan, Lin and Young (1996), Hesford et al. (2007), Ittner and Larker (1998), Ittner and Larcker (2001), Langfield-Smith (2008), Otley et al. (1995), Scapens and Bromwich (2001), Selto and Widener (2004), Shields (1997) and Young and Selto (1991).

2

explain the productivity paradox. Otley et al. (1995) include research studies on management control systems covering the period between 1954 and 1995. They focused on management control literature and categorized various managerial aspects into closed or open systems and rational or natural systems perspectives. Ittner and Larcker (1998) captured the trend of innovations in performance measurement from research studies on economic value measures, non-financial measures, and performance measurement initiatives in government agencies prior to 1997. They selected articles that are mainly on surveys conducted by consulting firms and government agencies.

INSERT TABLE 1 HERE

Selto and Widener (2004) entail wider coverage but limited to articles on conventional management accounting topics and topics that are prominent in professional finance and accounting literatures. Their review involves 14 management and accounting research journals and 7 professional magazines and journals, in order to identify the divergence between management accounting research topics and practice issues. Other reviews, however, do not rely on a specific area of management accounting, for example, Shields’ (1997) review focuses on articles published by North American for the period of 1990 -1996. His review is limited only to six leading academic accounting journals.2 Scapens and Bromwich (2001) explored the articles published in Management Accounting Research journal within the period of 1990 to 1999. They also briefly compared the state of the research of those articles to the North American papers reviewed by Shields (1997). Hesford et al. (2007) analysed management accounting articles in 10 journals published during 1981 to 2000. They observed the evolution of the research in this field and examined the articles’ citations to reveal the influential individuals, topics, methods, and source of disciplines. Overall, the above reviews have provided an overview of the state of the management accounting literature and encapsulated the researches done in the past towards identifying future directions. Nevertheless, today’s business situation within which an organization must operate is rapidly changing. Up until now, there are a number of research studies that have responded to the suggestions of the above reviews. The earliest article was published in 1954, which was reviewed by Otley et al. (1995) and the latest is reviewed by Selto and Widener (2004) and Hesford et al (2007) - both concluded their reviews in 2000. The current paper seeks to address the timeline issue by including the articles published until August 2008. Although most of the above reviews place emphasis on modern management accounting techniques, however, it is believed that the time gap between 2000 and 2008 could entail many “new” or innovative accounting issues.

2They are (1) The Accounting Review, (2) Accounting, Organizations and Society, (3) Contemporary Accounting Research, (4) Journal of Accounting and Economics, (5) Journal of Accounting Research, and (6) Journal of Management Accounting Research

3

In addition, as management accounting field is a global issue, the current review features primary accounting journals from various regions. This includes journals explicit to management accounting areas (Management Accounting Research and Journal of Management Accounting Research), practitioner journals (Cost Management and Advances in Management Accounting) and other leading accounting journals listed in Table 2. The review mainly covers all publications of the journals up to the most current ones, specifically from 1926 to 2008. The focus is on the articles pertaining to management accounting innovations, with inclusion of both empiric-based studies as well as qualitative papers. As this theme involves a vast area, this paper thus sets the boundary by trying to define management accounting innovations that may best explain the articles reviewed.

Defining management accounting innovations In general, management accounting innovation in the literature has been observed by the emergence of contemporary management accounting techniques. A clear distinction between traditional and contemporary management accounting techniques is the latter are strategic-focused that combine both financial and non-financial information (Chenhall and Langfield-Smith, 1998). Recently, Chenhall (2008) recognised management accounting innovations as strategic management accounting “to connect the strategies to value chain and link activities across the organization that relates to cost objects” (p. 525). According to Chenhall (2008, p. 525), among the management accounting techniques that have these characteristics are benchmarking, activity-based costing, activity-based management, target costing, business process re-engineering, theory of constraints, balanced scorecards, total quality management, and value-chain management. Building upon this broader definition, this paper considers management accounting innovation research that primarily associated with the above contemporary management accounting techniques. Further, this paper classifies the above practices into two: management accounting and control system (MACS) and operations management (OM). According to Hansen and Mouritsen (2007), management accounting is regarded as performance number ‘at a distance’ whereas operations management is considered as ‘hands-on’ activities in operations. In addition, the literature demonstrates that tensions always exist when the management accounting system needs to keep pace with technological advancement, denoted as accounting lag by Dunk (1989) and productivity paradox by Young and Selto (1991). In light of this issue, the current review takes into account and show the division of both practices. With regard to the definition of innovation, the term is generally equated with the newness of an idea. For example, Abernethy and Bouwens (2005) perceived management accounting system innovation as either new systems or the redesign of an existing system. Within innovation studies, the term entails different interpretations particularly when referring to organisational context. An

4

innovation is perceived when it is invented or regarded as novel whether it is adopted or not (Zaltman, Duncan and Holbek, 1973), or when an idea or procedures is first or early used (Becker and Whisler, 1967), being implemented (Evan and Black, 1967) and become successful (Mohr, 1969). This has also been reflected in the diverse management accounting researches particularly pertaining to the innovation and change literature. There are different stages of the innovation and change processes attached to the studies of management accounting practices ranging from the adoption decision (e.g. Brown, Booth and Goacobbe, 2004; Malmi, 1999) to the implementation (e.g. Argyris and Kaplan, 1994; Krumwiede, 1998) and the success of the implementation (e.g. Briers and Chua, 2001; Shields, 1995).

In this paper, innovations of management accounting and control systems signify various issues related to the initiation, implementation and internalisation of contemporary management accounting and control systems and advanced operation management tools such as JIT and TQM. This includes studies that investigate management accounting innovations in general and studies on specific management accounting practices. These studies involve different levels of analysis at individual levels (Emsley, 2005; Hicks, 1978), innovation levels (Ax and Bjornenak, 2005; Bjornenak and Olson, 1999), organisational levels (Hussain and Hoque, 2002; Lin and Yu, 2002), industry-levels (Ittner and Larcker, 1998; Lapsley and Wright, 2004) and national levels (e.g. Alcouffe, Berland and Levant, 2008; Firth, 1996).

From our observations, so far, no existing reviews have built upon the development of research in management accounting innovations. Thus, this paper is envisaged to make an incremental contribution to the management accounting literature to explore the likely trend and the state of the research of management accounting and control system and operations management. It endeavours to synthesize the published researches in management accounting innovations; thereby develop a better understanding of the issue. Fruitful suggestions then could be offered for future research in this area. The rest of the paper is organized as follows. Section 2 outlines the review method used. Section 3 discusses the topics, research settings, research methods, theories and findings of the articles reviewed. Finally section 4 provides concluding remarks and suggestions for future research.

Review method As shown in Table 2, the current review involves 22 accounting journals namely ABACUS, Accounting and Business Research (ABR), Accounting, Auditing and Accountability Journal (AAAJ), Accounting and Finance (AF), Accounting Horizon (AH), Accounting, Organizations and Society (AOS), Advances in Management Accounting (AMA), Behavioral Research in Accounting (BRA), British Accounting Review (BAR), Contemporary Accounting Research (CAR), Critical Perspectives on Accounting (CPA), European Accounting Review (EAR), Journal of Accounting and Economics (JAE), Journal of Accounting and Organizational Change (JAOC), Journal of Accounting Education (JAED),

5

Journal of Accounting Literature (JAL), Journal of Accounting Research (JAR), Journal of Cost Management/Cost Management (CM), Journal of Management Accounting Research (JMAR), Management Accounting Research (MAR), Review of Accounting Studies (RAS), and The Accounting Review (TAR). The articles on management accounting innovations were searched using the term ‘management accounting innovation’. The search was targeted on the articles published on online database. However, for the purpose of the analysis, articles on financial accounting, corporate finance and research method topics, book reviews, committee reports and discussions were omitted. For organisational and employees’ performance measure, the selection was based on the use of non-financial measure or a combination of both financial and non-financial measures. Research in management accounting innovations comprises of two: first, research that focuses on management accounting innovations in general; and second, research focuses on a specific management accounting innovation such as ABC and the balanced scorecard. The result of database search is reported in Table 2. The third column of the table indicates the periods by which the search was conducted, the forth column indicates the number of articles found using keyword search of management accounting innovation and was ranked in descending order, as showed in column seven. The number of articles selected for review is reported in fifth column. As can be seen from the table, the search found 666 articles on management accounting innovations during the period between 1926 and 2008, both inclusive. From these articles, 89 were selected for further analysis, as they are widely cited articles and they are published in prestigious, internationally widely accepted ranked journals.

INSERT TABLE 2 HERE

From the ranking, large numbers of articles found from the database search are from TAR, AAAJ, JAR and EAR journals, however relatively a few were selected for the review. It is probably due to the function of search operation as described in the table’s footnotes. Meanwhile, the journals of ABACUS, ABR, BAR, JAED, JAL, RAS and CAR appear to publish very small amount of management accounting innovations research. This supports the overall idea of these journals that place emphasis on quantitative and empirical studies with less on management accounting topics. However, other generalist accounting journals like AOS, BRIA, JAOC, and AH place more equal weight on qualitative and quantitative management accounting research. They comprise of relatively large number of articles in this area with most of them reflect the scope of management accounting innovations defined earlier. With regard to the journals that pertaining to the other disciplines, AF seems to have some publications on management accounting innovations, but none in JAE. As expected, accounting journals specific to management accounting discipline comparatively constitute large number of management accounting innovations studies. From the table, JMAR publishes more articles on this area than its counterpart, MAR. Likewise, the articles from JMAR provide the largest

6

number of articles selected for the review, which tend to focus on performance measurement system and activity-based system topics. It is also found during the search, the field research methods have been discussed and encouraged in JMAR (i.e. Ahrens and James, 1998; Baxter and Chua, 1998; Kaplan, 1998) although like other US-based journals, this journal is dominated by quantitative studies. With regard to the practitioner journals, JCM publishes more research on management accounting innovations than AMA. Besides, by comparison to the other journals, the articles from JCM discuss more diverse management accounting practices, focusing on the practical insights and experiences from case studies. Appendix 1 summarises the attributes of the studies under review. The table in the appendix comprises of 9 columns on author/year, journal, article type, key issues addressed, setting, theory, research method and key findings. For the research type, the articles were categorised whether it is a case study, empirical, experimental, descriptive, conceptual, practical insight or review. Theory used by the researches was based on the classification by Shields (1997), which are economic theories, psychological theories, sociological theories, organisational behaviour theories, production and operations management theories, and strategic management theories. The classification of research methods is done following Shields (1997) and Scapens and Bromwich (2001) of mathematical analytic, survey, archival, laboratory experimentation, case/field study, literature review, and multiple research methods.

Findings This section discusses the findings from articles reviewed and briefly compares with previous reviews. The topics, research settings, theoretical frameworks, methods used, and results in the sample articles are summarised and analysed.

Topics As mentioned above, the articles for the review are categorised into two: management accounting innovations in general; and management accounting innovations as specific practices. Table 3 reports the frequency of topics in the articles which shows that 18 articles are on the management accounting practices as a whole, while 71 are specific to the 11 practices of management accounting and control system and operations management.

INSERT TABLE 3 HERE As can be seen from Table 3, the reviewed articles are dominated by the research on the innovation of management accounting and control system. Researches within this ambit concentrated on non-financial measures of

7

organisational and manufacturing performance measure (17), employees’ performance measures (11) and activity-based costing and management (ABCM) (19). Other contemporary techniques of MACS are balanced scorecards (8), strategic management accounting (3), value-based management (3), benchmarking (1), and target costing (1). The articles on operations management include total quality management (5), lean manufacturing (2) and supply-chain management (1).

As Shields (1997) found few articles on non-financial performance measures, the current review observed the increasing trend of the researches on those areas, especially on 1998 thereafter. This is consistent with Hesford et al. (2007) reported that the significant shifts of control literature from budgeting and organisational control to performance measurement and evaluation topics. We find that, in the sampled articles, studies in earlier years generally discuss the importance and performance consequences of non-financial measures. Towards recent years, researches tend to examine the way by which the non-financial measures being designed and used to improve performance. Research in ABCM received considerable attention and concentrated on implementation and contextual issues such as top management’s support and resource constraints. Our review also reveals an inconclusive debate on the mixed results in previous studies regarding the adoption of ABCM, despite its widely claimed benefits. In this light, it has been observed that the articles under review attempted to identify various variables that are associated with the adoption, use and effectiveness of ABCM. Recently, Kaplan and Anderson (2007) introduced a new innovation of ABC, namely time-driven activity-based costing to overcome the subjectivity and complexity of conventional ABC. In the revised model, time is used to drive costs directly from resources to cost objects, thus skipping the activity-definition stage and allocation of resource costs to activities as in conventional ABC (Kaplan and Anderson, 2007) In contrast to ABC, the other innovation by Kaplan and Norton (1992, 1996, 2001), the balanced scorecard (BSC) has been much less researched. Reason for this might be due to its application does not explicitly indicate the use of BSC, but the use of financial and non-financial information or, by other names. According to Malmi (2001), the determination of a measurement system as a BSC is always far from clear. The BSC has similar attributes as France’s Tableaux de Bord (Lebas, 1994) and often supplemented with other management techniques (Ax and Bjornenak, 2005). Researchers usually presume a BSC when it involves both financial and non-financial measures whereby other frameworks also constitute the same elements. The distinctive features of the BSC are that it should contain the perspectives derived from the original four; built from financial and non-financial measures; the measures are derived from organisational strategy and impose cause-and-effect relationships (Chenhall, 2005; Malmi, 2001). Overall, the current review agrees with Shields (1997) that recent research tends to extend the topics that have already been studied. Researchers incline to focus on popular tools in management accounting and control systems which could lead to lack of diversity of the topics studied. In the current review, research

8

in value-based management, benchmarking, life cycle costing, and target costing has received little attention (see also Hesford et al., 2007; Selto and Widener, 2004; Shields, 1997). Despite the continuing concern on the correspondence of management accounting practices to manufacturing technology, not much study incorporates different operations management techniques in accounting journals. TQM and JIT are common operations management techniques tested in management accounting literature, whereas lean manufacturing, supply chain management, business process reengineering, and theory of constraints are relatively rare. According to Ittner and Larcker (2001), the research on the interface of accounting and operations management has substantially reduced due to increase interest on “new” topics such as BSC, intangible assets and economic value added. This underdeveloped body of research has resulted in many research topics unexplored and conflicting results remain unresolved (Ittner and Larcker; 2001).

Settings Table 4 reports the distribution of research settings in the sampled articles. The classification of the settings is based on Scapens and Bromwich (2001) and Shields (1997). From the table, research in management accounting innovations is centered on manufacturing industry (29), comprises of production and services activities of manufacturing companies. Other setting of single industry is services (6) which comprises of retailing, banking, financial service, hotel and health care whereas specific industry (2) comprises of telecommunication and airline industries.

INSERT TABLE 4

Thirteen studies were conducted in multiple industries almost exclusively involve survey and archival methods. Six studies conducted in the public sector and nine employed generic settings.3 Researches in inter-organizational, international, and multinationals companies are very limited in this sample, consistent with Shields (1997). Nineteen studies that do not involve research settings are conceptual/practice-oriented papers. Heavy emphasis on manufacturing industry is consistent with the traditional involvement of management accounting practices (Scapens and Bromwich, 2001; Shields, 1997). Studies in manufacturing settings mainly related to the cost management and management control such as activity-based costing and activity-based management, performance measures and quality-related measures as well as operations management tools. Further, the current review shows that research in management accounting innovations places similar importance on non-manufacturing settings. The performance measurement initiatives and ABCM are widely studied in service industry and

3 Generic setting involves general, abstract or simplified setting for analytic modeling or experimental hypotheses testing (Scapens and Bromwich, 2001; Shields, 1997) .

9

public sector organisations. This indicates that innovations of management accounting are also applicable to non-manufacturing settings, which might be explained by the high intensity of competitive pressures in the service industry (Hussain and Hoque, 2002) and public sector reform (Lapsley and Wright, 2004).

Theories Table 5 provides the distribution of theories used in the articles reviewed. There are 18 articles which are based on sociological theories, 13 articles based on economics theory, 11 articles on contingency theory, and 9 articles based on organisational behaviour perspectives. Others rely on production and operations management (2), strategic management (1), psychology (1) and the combination of multiple theories (13). The other 2 articles were based on Simon’s levers of controls.

INSERT TABLE 5 HERE

Within these 89 articles, there are a number of articles that do not explicitly indicate the theory used; with most of them develop the hypotheses from the findings of previous researches. Usually, these articles using survey method and some are conceptual papers. According to Scapens and Bromwich (2001), as the theory is used implicitly in many studies, they suggested to infer the underlying theories from the content of the papers. However, as expected, 19 articles in practitioner or professional journals have not grounded on any theoretical framework. In management accounting innovations research, sociology theories are derived from institutional theory, theory of translation, actor-network theory, innovation diffusion theory, stakeholder theory, structuration theory, trust theories, and enabling vs. coercive formalisation. Economics theories mainly involve principal-agent relationship with some articles based on classical utility theory, production cost economics, and Marxian economics. Researches grounded on organisational behaviour are associated with motivational theories namely goal theory, expectancy theory and X and Y theory Researches based on production and operation management theories incorporate quality and production process layout whereas strategic management deals with strategy typologies and strategy process. Psychology theories include conflicts and social psychology. Shields (1997) documented that half of the studies from North American were built on economics theory. The current review, however, indicates that research in management accounting innovations also heavily sourced from other disciplines namely sociology, organisational behaviour, and contingency theory. As the current review is on management accounting innovations, the sociology theory such as institutional theories and innovation diffusion theories prevail. These theories are mainly used in the diffusion and adoption studies to identify the factors that influence the phenomenon. Besides that, the theories stemmed

10

from alternative management accounting stance (Baxter and Chua, 2003) has received a particular interest in the sampled articles. With regard to management accounting change, the alternative approach emphasises the research on micro context and recognises the influence of individual. Old institutional economics and new institutional sociology are notable in analysing the process especially in field studies. Nevertheless, these theories are restricted to the abstract process of stability and change (e.g. Burns and Scapens, 2000) besides the notion of isomorphism (e.g. DiMaggio and Powell, 1983; Meyer and Rowan, 1977). They appear to overlook the technical rationality and the implementation outcome. Therefore, Lounsbury (2008) highlighted the institutional rationality as a new direction for research to divert away from conventional neoinstitutionalism. The institutional frameworks further developed to embrace organisational diversity, for instance, the concept of institutional entrepreneurship that explores the roles of powerful actors that bring about change (Garud, Hardy and Maguire, 2007). However, the actor-network theory constitutes the similar element of actor, thus clear distinction is necessary to justify the theory chosen. The difference between these theories could be seen in the definition of actor and the roles of power. According to Battilana (2006), institutional entrepreneurship emphasises the role of powerful actors that have certain social position which enables them to conduct divergent organizational change despite the institutional pressures. This theory focuses on human actors that have the ability to control resources to shape new institutions or transform existing ones (Maguire, Hardy and Lawrence, 2004). On the other hand, actor-network theory does not differentiate between people and objects and it treats society, organisations, agents and machines as interactive effects (Law, 1992). These elements are embedded in heterogeneous network that influence the change. This theory is concerned with issues of power but not related to heroic or powerful individual; instead, it is affected through the production and reproduction of the network (Hassard, Law and Lee, 1999).

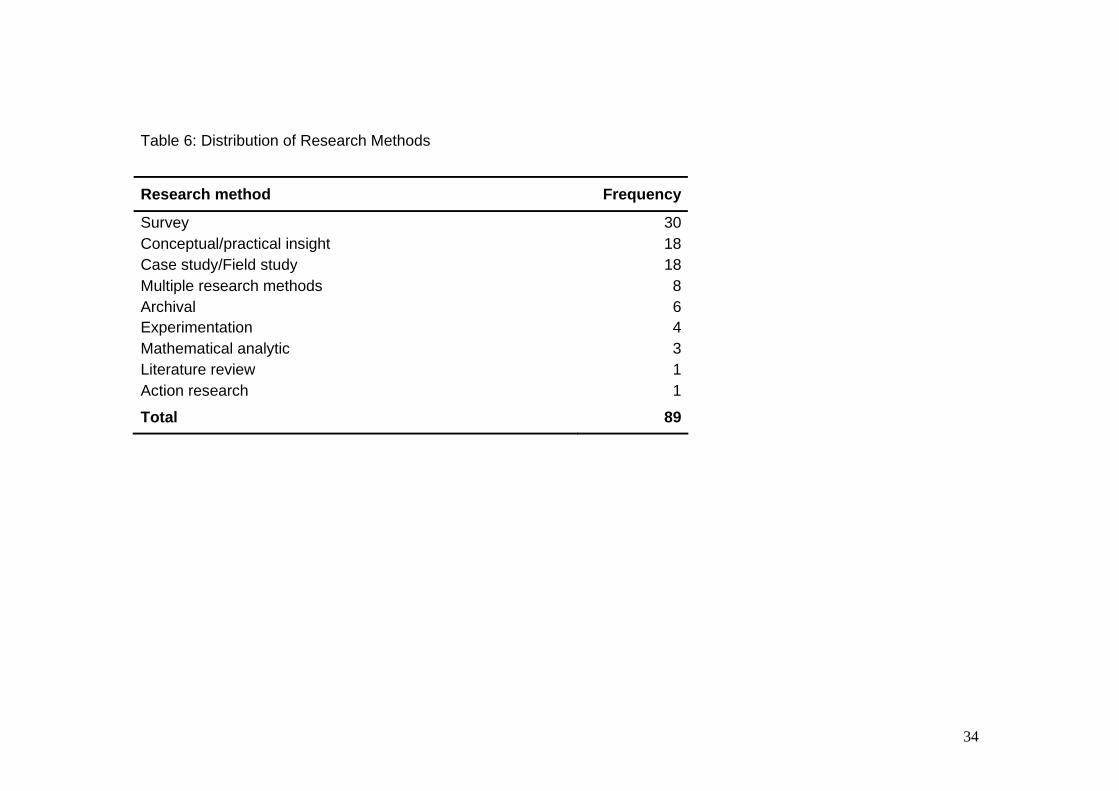

Research methods Table 6 shows the distribution of research methods used in the sampled articles. The most frequent method used is survey (30), followed by case study/field study and conceptual/practical insight, each with 18 articles, 8 articles using multiple research methods and 8 using archival. Other methods are experimentation (4), mathematical analytic (3), literature review (1), and action research (1).

INSERT TABLE 6 HERE

It appears from our review that quantitative methods of survey, experimentation and mathematical analytic are dominant in these articles. Survey method that is employed in descriptive studies particularly to identify the factors that influence the degree of adoption of management accounting practices and

11

the reason they were used, apart from the extent of financial and non-financial information was utilised. Explanatory-based studies using survey method seek to find optimal relationship engaged with the implementation of the practices with the outcome variables and contextual variables. However, survey methods often associated with the controversial of biasness, response rate, collection procedures, and inconsistency of findings with theory and previous researches. As the survey method is imperative in management accounting research, researchers need to follow the guidelines on the appropriate survey procedures (e.g. Sekaran, 2003; Neuman, 2000). For example, to improve the response rate, Dillman (1983) suggested the use of Total Design Method (TDM), which focuses on the design and the procedures of the survey. According to him, among the principles of TDM in the design of the instrument are to avoid the question in cover page and in last page, the first question applies to everyone, interesting and easy to answer and place the most-interesting and topic-related questions first, followed by potentially objectionable question and finally demographic information. For the implementation procedures, among the suggestions by Dillman (1983) are regarding the appropriate content of cover letter with printed mailing date, individual names and addresses and signed by researcher with a blue ballpoint using sufficient pressure. He suggested a postcard follow-up reminder be sent 1 week after first mailout, after 3 weeks a second cover letter and questionnaire to non-respondent and after 7 weeks another cover letter and replacement questionnaire. Mathematical analytic that primarily involves modelling was used in testing principal agent relationship associated with compensation and determination of the effect of multiple cost drivers. As opposed to the other review papers, this method is relatively rare in this review. Archival method involves the collection of quantitative and qualitative data. Quantitative data is related to firms’ financial and non-financial information retrieved from the firms’ databases and public database. Qualitative data is obtained from publications and firms’ documentations. The quantitative archival research, mathematical analytic and experimentation almost entirely coming from North American journals and the authors are affiliated mainly with North American institutions. This might hold true as due to the education system especially in research programme. The doctorate programme in the U.S. is more rigorous that consists of coursework, comprehensive examinations, internship and a thesis. For the first two years normally the students need to complete the coursework on accounting subjects, research methods and various quantitative research tools such as statistics and econometrics before commencing their research. In the U.K. and Australia, usually there is little or none course components in many universities and the programme tends to be shorter period than in the U.S. On the other hand, the qualitative analysis appears mostly in U.K. journals, AOS and MAR (Selto and Widener, 2004). In this review, the percentage of case study/field study research is increasing by comparison to Shields (1997). Case study/field study methods are paramount in understanding management accounting innovations and change. As the respond to change is unique to different organisations, these methods can explore many aspects

12

depending on the research questions and theory chosen. In the sampled articles, case study/field study research is centred on the implementation of management accounting practices, ranging from the reasons of the design and adoption, to the multiple aspects of application and implementation processes. As survey is likely to be individual perception on predetermined variables, case study primarily involve abstract and vast area of social reality (Morgan and Smircich, 1980; Yin, 1994). The reliability of data could be improved through field study whereby the information obtained from one source (e.g. interview) could be supported by other sources (e.g. documentation analysis and survey). To further enhance the external validity and reduce observer biases, Yin (1994) suggested multiple cases being studied. Normally, the pitfall of these methods is regarding the aggregation of the findings as they are fragmented to particular settings. Nevertheless, the case study/field study often exploratory in nature and present alternative perspectives (Yin, 1994) and the findings could suggest emergent variables to be tested empirically. In innovation action research, researchers are actively involved in organisations to implement the idea, with their role as change agent in creating something new (Kaplan, 1998). As opposed to the case study/field study that investigates the existing practices, innovation action researcher is experiencing the development process which may provide new insight into the literature. In this review, action research by Liu and Pan (2007) reported the implementation of ABC from technical, behavioural and organisational perspectives by which they have identified new phenomena of internal barriers to change. Conceptual papers in this review are similar to the definition of framework studies by Hesford et al. (2007). The studies involve the development of new conceptual frameworks to provide new perspectives, drew from multiple information sources and authors’ own synthesis (Hesford et al. 2007). Practical insight, on the other hand, is not associated with theoretical testing; instead, it encompasses the description of the management accounting practices that usually is based on practical experiences. This type of research normally appears in applied research and practitioner literature and adopts informal research style that does not rely on theory (Shields, 1997).

Results of prior research This section briefly discusses the results of prior research studies on management accounting innovations in general and articles on balanced scorecard, total quality management, activity-based costing and management, organisational/ manufacturing and employees’ performance measures. The review of the findings will focus on the abovementioned practices as they are relatively dominant in the sampled articles. Appendix 1 summarises the key issues addressed and the key findings of the 89 articles reviewed.

13

Management accounting innovations in general There are a number of researches on management accounting innovations that consider different management accounting practices as a whole. These articles analyse the development of management accounting practices, individual perceptions on innovation and change, accounting lag, the determinants and trends of adoption, the processes of change and the unbundling of management accounting models.

Two articles by Kaplan provide the review of the development of management accounting before and after 1984. In the article published in 1984, Kaplan concluded that the traditional cost accounting models prior to 1984 are no longer adequate for new organisations with advanced manufacturing technology and competitive business environments. Following the remarks, the ABC and BSC have been developed by which the path of the development is reported in his article published in 1994. Kaplan documented how the ABC, operational control systems and BSC by describing how these practices were initially documented, elaborated and disseminated through publications for the period of 1984 to 1994.

Similarly, Bjornenak and Olson (1999) followed the development of management accounting literature to understand the changes in the characteristics of management accounting models. They unbundled the models into scope and systems dimensions, and found that the contemporary management accounting models have experienced significant changes such as increased user-involvement and use of non-financial, external, disaggregated and ex ante data.

Studies on the determinants of management accounting innovations and change found various organizational, technical and economics factors that influence the diffusion and adoption of the practices. The prevailing factors found in the studies are the global competition and changes in technology (Waweru, Hoque and Uliana, 2004), performance gap (Lin and Yu, 2002), organisational structure (Abernethy and Bouwens, 1995; Cavaluzzo and Ittner, 2004), training and top management support (Cavaluzzo and Ittner, 2004) and the influence of government (Lapsley and Wright, 2004). Contradictory, Libby and Waterhouse (1996) found that the organizational structure, size and competition did not predict the changes in management accounting systems. Cavaluzzo and Ittner (2004) indicated that the difficulties in selecting and interpreting performance metrics inhibit the implementation of innovations of performance measurement systems in government agencies. The other factors that inhibit the innovations are related to individual attitudes (Jones, 1962; Waweru et al., 2004) and the disruptions to internal labor market (Foster and Ward, 1994). In addition, the negative perceptions on technical efficiency of administrative innovations are likely to induce accounting lag (Dunk, 1989) In international setting, Grandlund and Lukka (1998) observed the convergence of management accounting practices in the world is the results of global competition, advanced information technology and multinational institutions and consultancy firms. Similarly, Firth (1996) found that joint venture

14

with foreign firms influence more changes in management accounting systems to the local companies in China. With regard to the use of management accounting systems, Libby and Waterhouse (1996) found high rate of change in sampled organizations with the practices that support decision making and control were favoured by the organizations. Their study however does not indicate specific management accounting practices being implemented in the organizations. Szendi and Elmore (1993) drew a distinction between contemporary and traditional management accounting practices. They found that the new management accounting techniques are being adopted while traditional systems are being maintained, thus suggesting the management accounting is in a transitional stage. The inclination of organizations towards new management accounting techniques might be explained by a study of Emsley, Nevicky and Harrison (2006). They suggested that the behavior of management accountants which is innovative cognitive style is more likely to initiate radical changes to the practices of their organizations.

Balanced scorecard The articles on BSC found in this review generally focus on the design and use of BSC. A conceptual paper by Kaplan and Norton (2001) suggested the strategy map in BSC could manifest the critical elements and their linkages between organisation’s strategies. However, as discussed by Johanson, Skoog, Backlund and Almqvist (2006), the organisation adopting BSC approach might face dilemmas in the implementation and employee mobilisation, one-size-fits-all problems, the time dimension, and various organizational logics. They further suggested the organisation to maintain the balance in two aspects namely in control process by means of connectivity, regularity and stability and in BSC approach such as in perspectives, measures and individuals’ different interests. Notwithstanding, both articles agree that balanced scorecard is a holistic and balanced performance management approach, but might subject to various interpretations and modifications to adapt with different settings. This is consistent with Funck’s (2007) study which shows how the BSC is translated to equate the interest of different logics in public healthcare environment. He found that the concept of balance4 is being translated as a balance between the perspectives, the top-down control is mixed with a decentralized design and placed less importance on the cause and effect relationship. In addition to that, Ax and Bjornenak (2005) observed the BSC has been integrated with other administrative innovations to appear attractive by which they describe as a fashion-setting process. With regard to the use of BSC, Malina and Selto (2001) reported that it is an effective approach for strategy communication and management control. They found that managers respond positively to BSC measures by reorganizing resources and activities in order to improve performance on those measures. 4 Funck (2007) argued that the concept of balance between measures in Kaplan’s (1996a, 1996b) publications and the hierarchy between the four perspectives was perceived as contradictory.

15

Tuomela (2005) found, in his case company, that BSC was used for diagnostic and interactive control purposes and had specific implications for beliefs systems and boundary systems. Joseph (2008) observed that the BSC is used to implement stakeholder-based management strategy by addressing the stakeholder issues while providing long-term growth and profitability. The BSC has also been used for capital investment decision-making in a healthcare organisation through matrix approach (Lyons, Gumbus and Bellhouse, 2003). Other studies on BSC outside the domain of management accounting innovations are by Hoque and James (2000) and Davis and Albright (2004). A quasi-experimental study by Davis and Albright (2004) found that the improvement in financial performance after the implementation of BSC resulted in superior financial performance than non-BSC implementing organisations. Similarly, Hoque and James (2000) found from their survey that organizational performance increased with increased usage of BSC type measures. They also reported that the BSC adoption is positively associated with the firm size and early product life cycle stage, but not with firms’ market position. Overall, the empirical data based study on BSC is limited despite its widespread benefits (Ittner and Larcker, 1998, Malmi, 2001). In particular, Davis and Albright (2004) regarded that the research on the benefits of BSC is lacking though it is the primary research question in this area (Ittner and Larcker, 1998).

Total quality management Similar to BSC, the study on TQM in this review is relatively limited. One stream of studies is focusing on cost of quality and quality-related outcomes. Using a survey, Dunk (2002) documented that quality performance is significantly associated with product quality and environmental accounting. Emsley (2008) studied two manufacturing plants of an organisation and found the different ways the plants developed Juran’s cost of quality technique resulted in different outcomes. A descriptive study by Sjoblom (1998) indicate the widely used of non-financial quality indicators because they are good proxies for the financial impact, timelier, more reliable and more relevant. The other stream is related to the management accounting system in a TQM setting. Gurd, Smith and Swaffer (2001) suggested the factors that reduce the accounting lag following the implementation of TQM are management commitment, strong leadership, education and training programs. Second, by Ittner and Larcker (1995) documented the association between TQM and non-traditional performance measures and reward systems. Similarly, previous research reported that the changes in management accounting are necessary for manufacturing practices. For example Hoque and Alam (1999) observed that the management accounting system in the case organisation changed to become more decentralised and project-oriented to complement with TQM. However, in wider context, research on the effect of the interaction between the manufacturing practices and management accounting system on performance has mixed results. While Abernethy and Lillis (1995) found that the association between these two practices affect the performance,

16

Ittner and Larcker (1995), Perera, Harrison and Poole (1997) and Sims and Killough (1998) found no positive association with performance. Abernethy and Lillis (1995) thus suggested that the different results are due to the other factors are not tested in the study and the dynamic nature of organisations experiencing different phases of change has been overlooked.

Activity-based costing and management By and large, the ABCM research falls into 4 groups, namely descriptive study to identify the extent of ABCM adoption, the benefits of ABCM and its effect on managers’ and employees’ satisfaction, the factors influencing the adoption of ABCM and the factors affecting the successful implementation of ABCM. Studies showed that the ABCM generate the characteristics of information that superior than traditional systems (McGowan, 1998), but would be less beneficial with the present of information asymmetry (Mishra and Vaysman, 2001). The expected benefits however depending on the interaction of behavioural and cognitive conflict factors (Chenhall, 2004). The implementation of ABCM is found to improve firm performance (Banker and Potter, 1993, Ittner and Larkcer; 2002) and increased managers’ and employees’ satisfaction (Swenson, 1995; McGowan and Klemmer, 1997). Several studies attempted to investigate that factors that trigger the adoption of ABCM. Among the factors found to be common for the reasons of adoption are the institutional isomorphism (Adebayo, 2006; Malmi, 1999), technical efficiency of the system (Al-Omiri and Drury, 2007; Baird, 2007; Malmi, 1999), firm size (Baird, 2007; Brown et al., 2004; Krumwiede, 1998) as well as top management support (Brown et al., 2004). Studies found that there are variations of the level of successful implementation of ABCM in the U.S. (Shields, 1995) and in Canada, France, Germany, Italy, Japan, the U.S. and the U.K. (Bhimani, Gosselin, Ncube and Okano, 2007) The factor that mostly associated with the successful implementation of ABCM or the subsequent progression of the adoption is related to the top management support (Adebayo, 2006; Al-Omiri and Drury, 2007; Brown et al., 2004; Liu and Pan, 2007; Krumwiede, 1998; Shields, 1995) and adequate training (Al-Omiri and Drury, 2007; Krumwiede, 1998; Shields, 1995).

Organisational/manufacturing performance measures The research on organisational/manufacturing performance measures are

categorised into several prevalent issues. First, is on the performance consequences of non-financial measures. Studies found that the non-financial measures of customer satisfaction (Ittner and Larcker, 1998) and the use of both financial and non-financial measures in compensation contracts (Said, Hassab-Elnaby and Wier, 2003) as the leading indicators for financial performance.

A conceptual paper by Cote and Latham (2004) emphasized the needs to incorporate quality-related measures in performance measurement systems.

17

Using a survey, Maiga and Jacobs (2005) proved that the importance of quality-related measures in management control systems will influence quality performance and subsequently financial performance and customer satisfaction. In addition, clear definition and measurable goals are also crucial to affect quantity performance and quality performance (Verbeteen, 2007).

Second type of research is on the attributes of performance measures within manufacturing context. According to Kaplan (1983), in order for manufacturing firms to remain competitive, he suggested that the firms’ management accounting systems be able to support new manufacturing strategies. Specifically, the firms need to strengthen the measures on quality, inventory cost, productivity, new product technologies, discounted cash flows and incentive schemes. Further, based on Banker, Potter and Schroeder (1993), the firms that implement JIT, TQM and teamwork practices may need to report the manufacturing performance to the shop floor workers to improve the employees’ morale. Two articles showed that non-financial performance measures are used in tandem with manufacturing strategies. Survey by Fullerton (2003) found that the JIT firms use more non-financial performance measure and reward system as well as TQM measurement tools than non-JIT firms. Particularly, the extensive use of subjective non-financial measures within quality-based strategies firms may lead to higher performance (Van der Stede, Chow and Lin, 2006).

Third research stream is related to the design and use of non-financial measures. In banking firms, the design and use of performance measures are influenced by institutional forces of coercive, mimetic and normative aspects together with economic constraints (Hussain and Hoque, 2003).

Fourth type of research is regarding the use of non-financial measures to influence the on behaviour of managers and employees. Webb (2004) reported that the use of strategic performance measurement systems have positive impact on managerial commitment to assigned performance goals. When involving comprehensive reporting systems and incentives tied to goals, managers tend to spend more time working on non-financial measures than the financial areas (Ullrich and Tuttle, 2004). To improve employee selection and motivate the employees to provide goal-congruent effort, less distorted performance measures and higher cash bonuses must be maintained (Bouwens and van Lent, 2006). In addition, in order for the performance measurement systems to be perceived as enabling by the employees, it is need to be built on experienced and professional employees with the experimentation being allowed (Wouters and Wilderom, 2008).

Employees’ performance measures Studies of incentives systems mostly attempted to determine the optimal incentive and mechanisms that are resulted in positive outcomes. The use of non-financial measures (Banker, Potter and Srinivasan, 1998) and financial controls (Kihn, 2007) were found to be associated with improved firm performance. There is improvement of organisational trust through gain-sharing

18

system (Chenhall and Langfield-Smith, 2003) and improved creativity through emphasis of quantity measures in creativity-weighted pay scheme (Kachelmeier and Williamson, 2008). To encourage innovation, Kennedy and Schleifer (2007) proposed a team performance measurement system that balances innovation and empowerment with control. Besides, the controllability of measures (Ghosh, 2005) and job-relevant information and role ambiguity (Burney and Widener, 2007) found to have moderating effect on the relationship between performance measurement system and the outcome. The optimal contract weights in performance measures could maximise the congruity between agent’s compensation and firm’s outcome (Datar, Kulp and Lambert, 2001). According to Ittner, Larcker and Rajan (1997), the weight placed on the choice of non-financial measures over financial measures depends on the level of regulation, the implementation of innovation-oriented strategy and strategic quality initiatives. In evaluating the performance measures to be used, Merhant (2006) suggested 6 criteria namely congruent with the organization’s objectives, controllable by the manager whose behaviors are being influenced, timely, accurate, understandable, and cost effective to produce. However, in measuring general manager’s performance, he found that none of the market measures, accounting measures, and combinations of measures provides a perfect solution In conclusion, the summary of the findings on the five topics implies a likely pattern of research in the sampled articles. Although it provides only a fraction of management accounting literature, one could illuminate the debate in those topics, thus identify the gap for future research. The next section will summarise the review of the articles, discuss the management accounting literature and suggest the opportunities for future research

Future research In the current paper, most studies on management accounting innovations were published after year 2000, the period which has not been covered in prior reviews. This might indicate that the research on this area has intensified during the period. However, from the analysis of the studies, it is found that the research is experiencing a slow pace of development whereby novel idea is rather rare. A few new frameworks and techniques, for example, the measure network and time-driven activity based costing, are mostly appear in the practitioner journals. In addition, previous reviews report studies on management control topics in general and performance measurements in particular. The current review provides additional input by focusing on the studies that incorporate researches on management accounting innovations such as balanced scorecard, ABC/ABM and non-financial measures of performance, which have received increasing interest by the researchers in recent years. Further recently, research in management accounting is proliferated, as observed by Hesford et al. (2007). They found that the number of management accounting articles has increased especially after the introduction of new accounting journals. Therefore, the challenge to the researchers is to find an

19

unexamined research questions which are worth researched. The idea could be from existing literature and managers’ perceptions (Foster and Young, 1997), as well as by observing changes in the environment. The other challenge is to determine whether the research and theoretical assumptions reflect the real practice. This ever-debated issue comes into conclusion that in certain aspects the researches seems to place different emphasis from the needs of practitioners (Foster and Young, 1997; Johnson and Kaplan, 1987; Selto and Widener, 2004). The innovation in management accounting system is important particularly to the organisations prone to the globalisation. The research on this area could assist the organisation in suggesting the optimal contexts, while enhances the understanding of the real practice within theoretical domain. The following subsections attempt to identify the areas for future research pertaining to the management accounting innovations.

Environmental uncertainty In today’s global market, managers need to be responsive to the environmental change and maintain a proactive management control system. In similar vein, researchers may formulate the dynamic model of environmental uncertainty to be incorporated in management control and operations management researches. Environmental uncertainties encompass the organisation’s industrial, economic, technological, competitive, and customer environment (Gordon and Narayanan, 1984). However, now-a-days recent global issues such as oil price fluctuation, soaring commodities price, climate change, scarcity of natural resources and political and economic uncertainties may exert pressure to the business. Therefore, research could be conducted to explore how these factors will affect an organisation’s strategies as well as management control system and supply chain management.

Information technology Similarly, the advancement in information and communication technology could significantly shape the way of doing business. The practice of management control may change as various aspects of the firm could be integrated via information technology (Dechow, Grandlund and Mouritsen, 2007). Research to further investigate the changing roles of management control system could be preceded by incorporating different information technology application. It can also be suggested to conduct research on the interrelationship of different management accounting practices and information system. However, a clear boundary should be established between management accounting practices and accounting information system. This is due to the accounting software that seems to embrace the functions on management accounting practices related to cost management and management control (Grandlund and Mouritsen, 2003; Lodh and Gaffikin, 2003). It is expected that these functions might gradually diminish the visibility of particular management accounting

20

practices. Perhaps, future research is needed in this area to further investigate this issue.

Control package Extensive researches have been carried out to study the link between the management control system and organisational characteristics which were mainly based on contingency theory (Chenhall, 2003). The literature has identified the contextual factors that affect the use and usefulness of management control systems such as environmental dimensions, technology, size, strategy, and organisational structure. Researches also examined the various tools of management control system, for example, budgeting, economic value added, costing system, financial and non-financial performance measures, and the BSC. However, considering separately certain components of management control system of an organisation could lead to model underspecification (Chenhall, 2003; Dent, 1990; Langfield-Smith, 1997). The reliability of the findings could be questioned as the results might also be affected by other control systems excluded in the study. Thus, it is important for future study to incorporate the integration of broader set of control practices (Chenhall, 2003). Another area of possible research is the interface between TQM and BSC. Firms that have TQM in place need to implement BSC to identify appropriate multidimensional, non-financial and financial, to signal to managers the focus for their day-to-day work as well as to motivate and reward the employees (Hoque, 2003). However, the emphasis given on employee satisfaction in TQM (Hoque, 2003) while BSC is generally hierarchical-orientated (Modell, 2007) could be examined whether it acts as complementary or conflicting to each other. Subscribing to Hoque’s (2003) suggestion, the optimal progression of organization adopting BSC followed by TQM, or vice versa could be investigated, besides their fit with contingent factors. Other integration could be analysed is between formal and informal control systems. As formal control has been widely researched, the research of informal control practices is still lacking. Informal controls could be organizational culture (Langfield-Smith, 1997) and organisational structure (Otley, 2003). Other factors that might act as informal controls including trust to organisation and between organisation’s members and job security could be investigated. In addition, the examination of the interaction between the formal control system and other areas such as corporate governance, human resource management, internal control and financial management is also worthwhile.

Management accounting change and innovation In explaining management accounting change, the research could also take perspective from theories of innovation diffusion. Innovation diffusion approach provides different view of management accounting studies whereby it takes the perspectives of the potential adopter to show that firms will not always

21

attempt to imitate resources that produce competitive advantage (Powell, 1995). The aspects being studied using this approach are the efficiency, the characteristics of innovation and the role of propagators (Ax and Bjornenak, 2007). However, in management accounting field, this approach is relatively lacking with only brief discussion on the process of adoption and diffusion (Firth, 1996). The researcher could also consider a study using triangulation of theories to capture different dimensions of a phenomenon. Complementing different theories could provide more comprehensive understanding of the study. For example, the principles of innovation diffusion theory that emphasize on the effectiveness of innovation could be complemented by institutional theory that presumes the socials legitimisation. Besides, researchers could examine the recent management tools utilised in practice such as the financial application for problem solving. Neural networks system as well as time series analysis are started to be used for forecasting, budgeting and cost determination (Brown and Phillips, 1995; Vellido, Lisboa and Vaughan, 1999).

Concluding remarks The purpose of the review is to infer the development of research in

management accounting innovations. The innovation in this paper is signified by the advanced management accounting and control systems practices and operations management techniques. In a nutshell, research in management accounting innovations inclined to the design and implementation aspects. Within the implementation-based research, descriptive studies generally identified the extent of adoption and use of the practices. Meanwhile, empirical and field studies usually sought to explain various factors associated with the implementation and the outcome of an innovation.

This review includes the prestigious accounting journals from main continents namely North America, Europe and Australia, whereby the diversity of research methods and theoretical frameworks used is apparent. There is increasing used of field studies, while sociology theories are prevalence in the management accounting innovations researches. The sociology theories such as institutional theory and actor-network theory provide alternative perspectives to research by recognizing the individuals’ power and highlighting the transition process of the innovations.

Our review suggests a number of gaps in the literature. With regards to the evolution of these practices, it is plausible to conclude that the innovations seem stagnant, with the research tend to extend the existing ones. Certain management accounting practices such as ABCM and performance measurement systems have received considerable interest in the literature involving various technical, behavioural and sociological aspects. Therefore, comprehensive review of these studies is needed to provide overall understanding on what have been known in the literature and to reach consensus on conflicting findings.

22

On the other hand, studies on target costing, benchmarking, value-based management, and life-cycle costing are still lacking. Whether the management accounting practices are in the same pace with operations management techniques, more research is needed to conform to different techniques. What has been known, within the TQM and JIT setting, management accounting systems have been improved with more emphasis given on non-financial information.

This paper is believed to add to our understanding on the management accounting literature by providing the attributes of management accounting practices and operations management researches. The review involves a small sample size of the research papers, thus caution must be applied as the findings might not be generalized to the management accounting literature as a whole. Nevertheless, this paper has provided a number of questions to be considered for further investigation.

23

References Abernethy, M. A., & Bouwens, J. (2005). Determinants of accounting innovation

implementation. Abacus, 41(3), 217-240. Abernethy, M.A. & Lillis, A. (1995). The impact of manufacturing flexibility on

management control system design. Accounting, Organizations and Society, 20, 24-258

Adler, R., Everett, A.M. & Waldron, M. (2000). Advanced management accounting techniques in manufacturing: Utilisation, benefits, and barriers to implementation. Accounting Forum, 24, (2), 131-150.

Ahrens, T. & Dent, J. F. (1998). Accounting and organizations: Realizing the richness of field research. Journal of Management Accounting Research, 10, 1-39.

Argyris, C., & Kaplan, R. S. (1994). Implementing new knowledge: The case of activity-based costing. Accounting Horizons, 8(3), 83-105.

Atkinson, A. A., Balakrishnan, R., Booth, P., Cote, J. M., Groot, T., Malmi, T., et al. (1997). New directions in management accounting research. Journal of Management Accounting Research, 9(79-108).

Atkinson, A. A., Balakrishnan, R., Booth, P., Cote, J. M., Groot, T., Malmi, T., et al. (1997). New directions in management accounting research. Journal of Management Accounting Research, 9(79-108).

Ax, C., & Bjørnenak, T. (2005). Bundling and diffusion of management accounting innovations - the case of the balanced scorecard in Sweden. Management Accounting Research, 16, 1-20.

Ax, C., & Bjørnenak, T. (2007). Management accounting innovations: Origins and diffusion. In T. Hopper, D. Northcott & R. Scapens (Eds.), Issues in Management Accounting (pp. 45-64). Harlow, England: Pearson Education Limited.

Battilana, J. A. (2006). Agency and institutions: the enabling role of individual’s social position. Organization, 13, 5, 653-676

Baxter, J. A. & Chua, W. F. (1998). Doing field research: Practice and meta-theory in counterpoint. Journal of Management Accounting Research, 10, 69-88.

Baxter, J., & Chua, W. F. (2003). Alternative management accounting research - Whence and whither. Accounting, Organizations and Society, 28, 97-126.

Becker, S. W., & Whisler, T. L. (1967). The innovative organisation: A selective view of current theory and research. The Journal of Business, 40(4), 462-469.

Briers, M., & Chua, W. F. (2001). The role of actor-networks and boundary objects in management accounting change: A field study of an implementation of activity-based costing. Accounting, Organizations and Society, 26, 237-269.

Brown, D. A., Booth, P., & Giacobbe, F. (2004). Technological and organizational influences on the adoption of activity-based costing in Australia. Accounting and Finance, 44, 329-356.

24

Burns, J. and Scapens, R. W. (2000). Conceptualising management accounting change: An institutional framework. Management Accounting Research, 11, 1, 3-25.

Chenhall, R. H. (2005). Integrative strategic performance measurement systems, strategic alignment of manufacturing, learning and strategic outcomes: An exploratory study. Accounting, Organizations and Society, 30, 395-422.

Chenhall, R. H. (2008). Accounting for the horizontal organisation: A review essay. Accounting, Organizations and Society, 33, 517-550.

Chenhall, R., & Langfield-Smith, K. (1998). Adoption and benefits of management accounting practices: An Australian study. Management Accounting Research, 9(1-19).

Davis, S., & Albright, T. (2004). An investigation of the effect of Balanced Scorecard implementation on financial performance. Management Accounting Research, 15, 135-153.

Dechow, N., Grandlund, M., & Mouritsen, J. (2007). Managing accounting change. In T. Hopper, D. Northcott & R. Scapens (Eds.), Issues in Management Accounting (pp. 45-64). Harlow, England: Pearson Education Limited.

Dent, J. F. (1990). Strategy, organization and control: Some possibilities for accounting research. Accounting, Organizations and Society, 15(1/2), 3-25.

Dillman, D. A. (1983). Mail and Other Self-Administered Questionnaires. In P. H. Rossi, J. D. Wright & A. B. Anderson (Eds.), Handbook of Survey Research. Orlando: Academic Press.

DiMaggio, P. J. and Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational Fields. American Sociological Review, 48, 147-160.

Dunk, A. S. (1989). Management accounting lag. Abacus, 25(2), 149-155. Elnathan, D., Lin, T., & Shields, M. D. (1996). Benchmarking and management

accounting: A framework for research. Journal of Management Accounting Research, 8, 37-54.

Evan, W. M., & Black, G. (1967). Innovation in business organizations: Some factors associated with success or failure of staff proposals. The Journal of Business, 40(4), 519-530.

Foster, G., & Young, S. M. (1997). Frontiers of management accounting research. Journal of Management Accounting Research, 9, 63-77.

Garud, R., Hardy, C., & Maguire, S. (2007). Institutional entrepreneurship as embedded agency: An introduction to the special issue. Organization Studies, 28(7), 957-969.

Gordon, L. A., & Narayanan, V. K. (1984). Management accounting systems, perceived environmental uncertainty and organization structure: An empirical investigation. Accounting, Organizations and Society, 9(1), 33-47.

Gosselin, M. (2005). An empirical study of performance measurement in manufacturing firms. International Journal of Productivity and Performance Management, 54(5/6), 419-437.

25

Granlund, M. & Mouritsen, J. (2003). Special section on management control and new information technologies. European Accounting Review, 12, 1, 77-83.

Hansen, A., & Mouritsen, J. (2007). Management accounting and changing operations management. In T. Hopper, D. Northcott & R. Scapens (Eds.), Issues in Management Accounting (3 ed., pp. 3-25). Harlow, England: Pearson Education Limited.

Hassard, J., Law, J., & Lee, N. (1999). Preface. Organization, 6(3), 387-390. Hesford, J. W., Lee, S.-H., van der Stede, W. A., & Young, S. M. (2007).

Management accounting: A bibliographic study. In C. S. Chapman, A. G. Hopwood & M. D. Shields (Eds.), Handbook of Management Accounting Research (Vol. 1): Elsevier.

Hoque, Z. & Alam, M. (1999), TQM adoption, institutionalism and changes in management accounting systems: A case study. Accounting and Business Research, 29, 3, 199-210.

Hoque, Z. (2003). Total Quality Management and the Balances Scorecard approach: A critical analysis of their potential relationships and directions for future research. Critical Perspectives on Accounting, 14, 553-566.

Hoque, Z., & James, W. (2000). Linking balanced scorecard measures to size and market factors: Impact on organizational performance. Journal of Management Accounting Research, 12, 1-17.

Hussain, M. & Hoque, Z. (2002). Understanding non-financial performance measurement practices in Japanese banks: A new institutional sociological perspective. Accounting, Auditing & Accountability Journal, 15, 2, 162-83.

Ittner, C. D., & Larcker, D. F. (1995). Total Quality Management and the choice of information and reward systems. Journal of Accounting Research, 33, Supplement, 1-34.

Ittner, C. D., & Larcker, D. F. (1998). Innovations in performance measurement: Trends and research implications. Journal of Management Accounting Research, 10, 205-238.

Ittner, C. D., & Larcker, D. F. (2001). Assessing empirical research in managerial accounting: A value-based management perspective. Journal of Accounting and Economis, 32, 349-410.

Johnson, H. T., & Kaplan, R. S. (1987). Relevance Lost: The Rise and Fall of Management Accounting. Boston: Harvard Business School Press.

Kaplan, R. S. (1998). Innovation action research: Creating new management theory and practice. Journal of Management Accounting Research, 10, 89-118.

Kaplan, R. S. and D. P. Norton. 2001. Transforming the balanced scorecard from performance measurement to strategic management: Part I. Accounting Horizons, March, 87-104.

Kaplan, R. S., & Norton, D. P. (1996). The Balanced Scorecard: Translating Strategy into Action: Harvard Business School.

Kasanen, E., K. Lukka & A. Siitonen. 1993. The constructive approach in management accounting. Journal of Management Accounting Research, 5, 243-264

26

Knight, K. E. (1967). A descriptive model of the intra-firm innovation process. Journal of Business, 40(4), 478-496.

Krumwiede, K. R. (1998). The implementation stages of activity-based costing and the impact of contextual and organizational factors. Journal of Management Accounting Research, 10, 293-277.

Langfield-Smith, K. (1997). Management control systems and strategy: A critical review. Accounting, Organizations and Society, 22(2), 207-232.

Langfield-Smith, K. (2008). Strategic management accounting: How far have we come in 25 years? Accounting, Auditing and Accountability Journal, 21(2), 204-228.

Lapsley, I., & Wright, E. (2004). The diffusion of management accounting innovations in the public sector: A research agenda. Management Accounting Research, 15, 355-374.

Law, J. (1992). Notes on the theory of actor-network: Ordering, strategy, and heterogeneity. Systems Practice, 5, 4, 379-93.

Lawrence, M. (1969). Determinants of innovation in organizations. American Political Science Review, 63, 111-126.

Lebas, M. (1994). Managerial accounting in France: Overview of past tradition and current practice. The European Accounting Review, 3, 471–487.

Lodh, S. & Gaffikin, M. (2003). Implementation of an integrated accounting and cost management system using the SAP system: A field study. European Accounting Review, 12, 1, 85-121.

Lounsbury, M. (2008). Institutional rationality and practice variation: New directions in the institutional analysis of practice. Accounting, Organizations and Society, 33, 349-361.

Luft, J. L. (1997). Long-term change in management accounting: Perspectives from historical research. Journal of Management Accounting Research, 9, 163-198.

Malmi, T. (1999). Activity-based costing diffusion across organizations: An exploratory empirical analysis of Finnish firms. Accounting, Organizations and Society, 24, 649-672.

Malmi, T. (2001). Balanced scorecards in Finnish companies: A research note. Management Accounting Research, 12, 207-220.

Meyer, J. W., and Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83, 2, 340-363.

Modell, S. (2007). Bundling management control innovations: A field study of organisational experimenting with total quality management and the balanced scorecard. Paper presented at the 2007 AFAANZ Conference.

Morgan, G., & Smircich, L. (1980). The case for qualitative research. Academy of Management Review, 5, 491-500.

Neuman, W. L. (200). Social research methods: Qualitative and quantitative approaches. (4

th ed). Boston: Allyn and Bacon.

Otley, D. (2003). Management control and performance management: Whence and whither? The British Accounting Review, 35, 309-326.

27

Otley, D., Broadbent, J., & Berry, A. (1995). Research in management control: An overview of its development. British Journal of Management, 6(Special issue), 531-544.

Powell, T. C. (1995). Total quality management as competitive advantage: A review and empirical study. Strategic Management Journal, 16(1), 15-37.

Rogers, E. M. (1983). Diffusion of Innovations (3rd ed.). New York: The Free Press.

Scapens, R., & Bromwich, M. (2001). Editorial report - Management accounting research: The first decade. Management Accounting Research, 12, 245-254.

Scapens, R., & Bromwich, M. (2001). Editorial report - Management accounting research: The first decade. Management Accounting Research, 12, 245-254.

Sekaran, U. (2003). Research methods for business: A skill building approach. (4

th ed.) India: John Wiley & Sons, Inc.

Selto, F. H., & Widener, S. K. (2004). New directions in management accounting research: Insights from practice. Advances in Management Accounting, 12, 1-35.

Shields, M. D. (1997). Research in management accounting by North Americans in the 1990s. Journal of Management Accounting Research, 9, 3-61.

Smith, J. A. & Reid, G. C. (2000). The impact of contingencies on management system development. Management Accounting Research, 11, 4, 427-450.

Speckbacher, G., Bischof, J., & Pfeiffer, T. (2003). A descriptive analysis on the implementation of Balanced Scorecard in German-speaking countries. Management Accounting Research, 14, 361-387.

Sulaiman, M., Nik Ahmad, N. N., & Alwin, N. (2004). Management accounting practices in selected Asian countries: A review of the literature. Managerial Auditing Journal, 19, 493-508.

Van der Stede, W. A., Young, S. M., & Chen, C. X. (2007). Doing management accounting survey research. In C. S. Chapman, A. G. Hopwood & M. D. Shields (Eds.), Handbook of Management Accounting Research (Vol. 1, pp. 445-478): Elsevier.

Vellido, A., Lisboa, P. J. G., & Vaughan, J. (1999). Neural networks in business: A survey of applications (1992–1998). Expert Systems with Applications, 17, 51-70.

Yin, R. K. (1994). Case Study Research: Design and Methods (2nd ed.). Thousand Oaks, California: Sage.

Young, S. M., & Selto, F. H. (1991). New manufacturing practices and cost management: A review of the literature and directions for research. Journal of Accounting Literature, 10, 265-298.

Zaltman, G., Duncan, R., & Holbek, J. (1973). Innovations and Organizations. Toronto: John Wiley & Sons.

28

Table 1: Summary of selected prior reviews

Author Title Journal Scope Coverage Timeline Young & Selto (1991)

New manufacturing practices and cost management: A review of the literature and directions for research

JAL Modern cost management Empirical study Prior 1991

Otley et al. (1995)

Research in management control: An overview of its development

British Journal of Management