Embed Size (px)

Citation preview

Reji Kumar Pillai President

India Smart Grid Forum

Introduction to India Smart Grid Forum, Smart Grid Vision and Roadmap for India,

Smart Grid Projects and India Smart Grid Week 2015

DOT

ISGF Members (partial list): Govt, Utilities, Industry, Regulators, Academia, Research etc.

NCIIPC

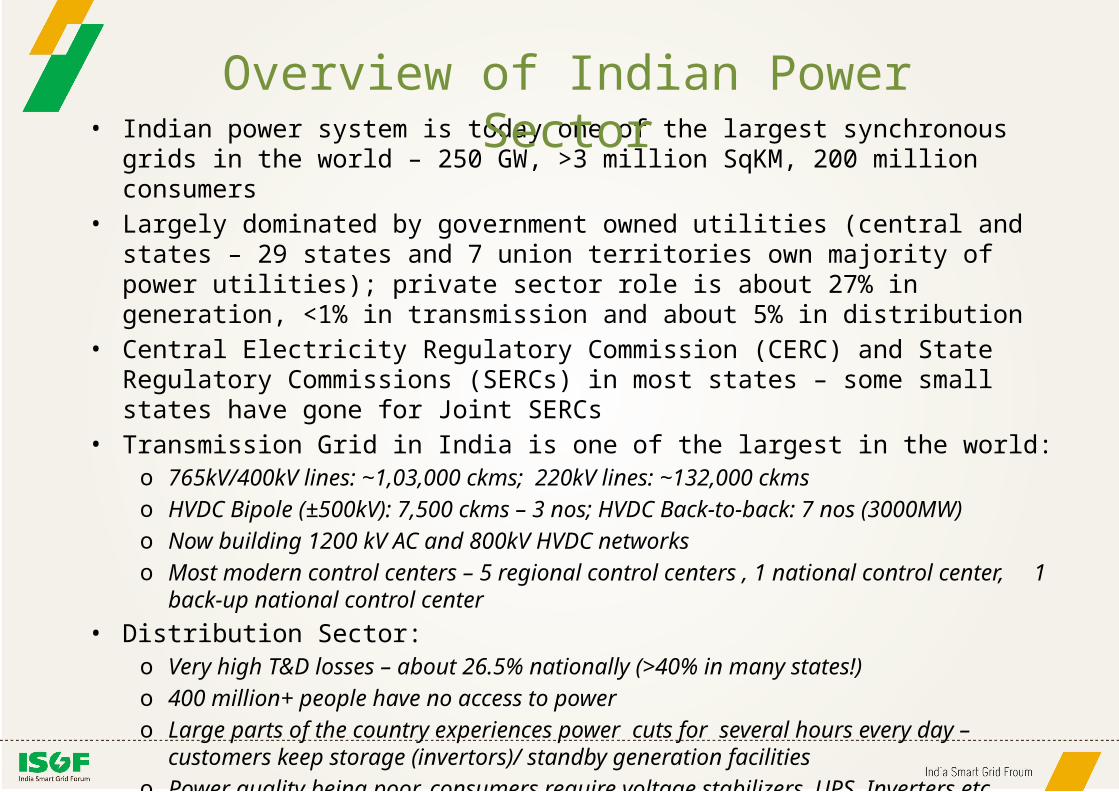

• Indian power system is today one of the largest synchronous grids in the world – 250 GW, >3 million SqKM, 200 million consumers

• Largely dominated by government owned utilities (central and states – 29 states and 7 union territories own majority of power utilities); private sector role is about 27% in generation, <1% in transmission and about 5% in distribution

• Central Electricity Regulatory Commission (CERC) and State Regulatory Commissions (SERCs) in most states – some small states have gone for Joint SERCs

• Transmission Grid in India is one of the largest in the world:o 765kV/400kV lines: ~1,03,000 ckms; 220kV lines: ~132,000 ckmso HVDC Bipole (±500kV): 7,500 ckms – 3 nos; HVDC Back-to-back: 7 nos (3000MW)o Now building 1200 kV AC and 800kV HVDC networkso Most modern control centers – 5 regional control centers , 1 national control center, 1 back-up

national control center• Distribution Sector:

o Very high T&D losses – about 26.5% nationally (>40% in many states!)o 400 million+ people have no access to power o Large parts of the country experiences power cuts for several hours every day – customers keep

storage (invertors)/ standby generation facilitieso Power quality being poor, consumers require voltage stabilizers, UPS, Inverters etc

Overview of Indian Power Sector

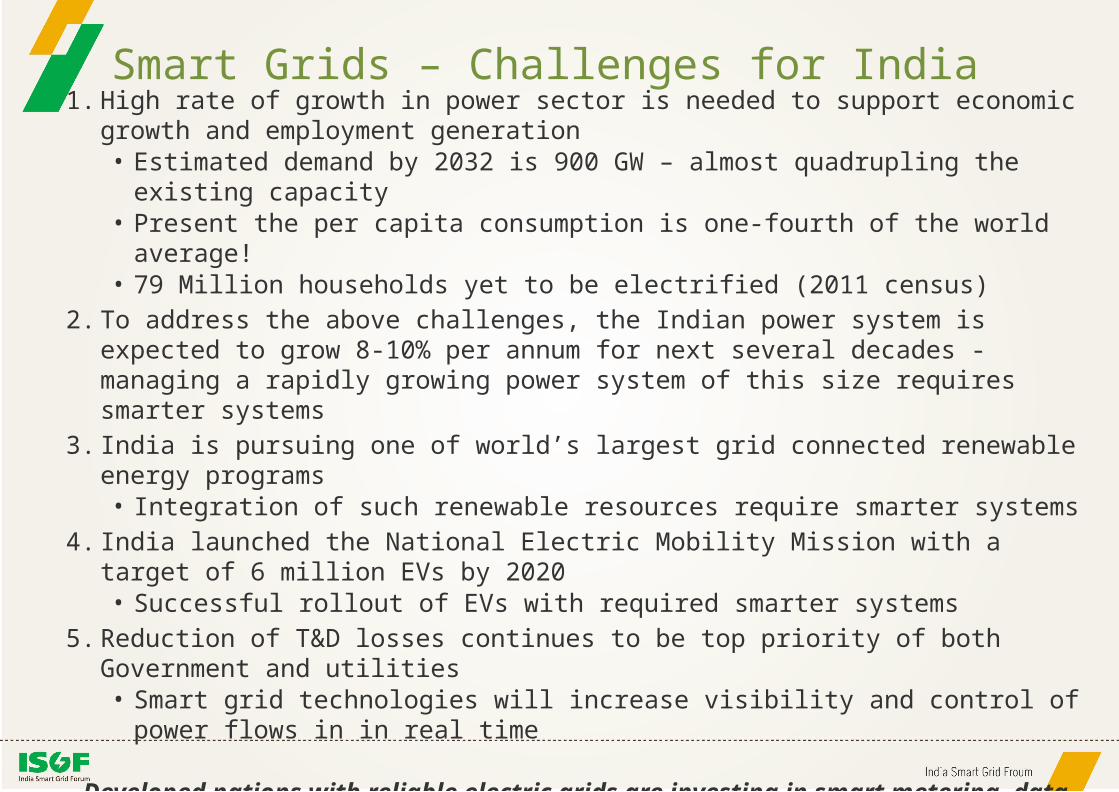

Smart Grids – Challenges for India1. High rate of growth in power sector is needed to support economic growth and employment

generation • Estimated demand by 2032 is 900 GW – almost quadrupling the existing capacity• Present the per capita consumption is one-fourth of the world average!• 79 Million households yet to be electrified (2011 census)

2. To address the above challenges, the Indian power system is expected to grow 8-10% per annum for next several decades - managing a rapidly growing power system of this size requires smarter systems

3. India is pursuing one of world’s largest grid connected renewable energy programs• Integration of such renewable resources require smarter systems

4. India launched the National Electric Mobility Mission with a target of 6 million EVs by 2020• Successful rollout of EVs with required smarter systems

5. Reduction of T&D losses continues to be top priority of both Government and utilities• Smart grid technologies will increase visibility and control of power flows in in real time

Developed nations with reliable electric grids are investing in smart metering, data communications and advanced IT systems and analytics, tools for forecasting, scheduling and

dispatching to further their smart grid journey…developing countries like India need to invest in both strengthening the electrical network as well as adding communications, IT and automation

systems to build a strong and smart grid

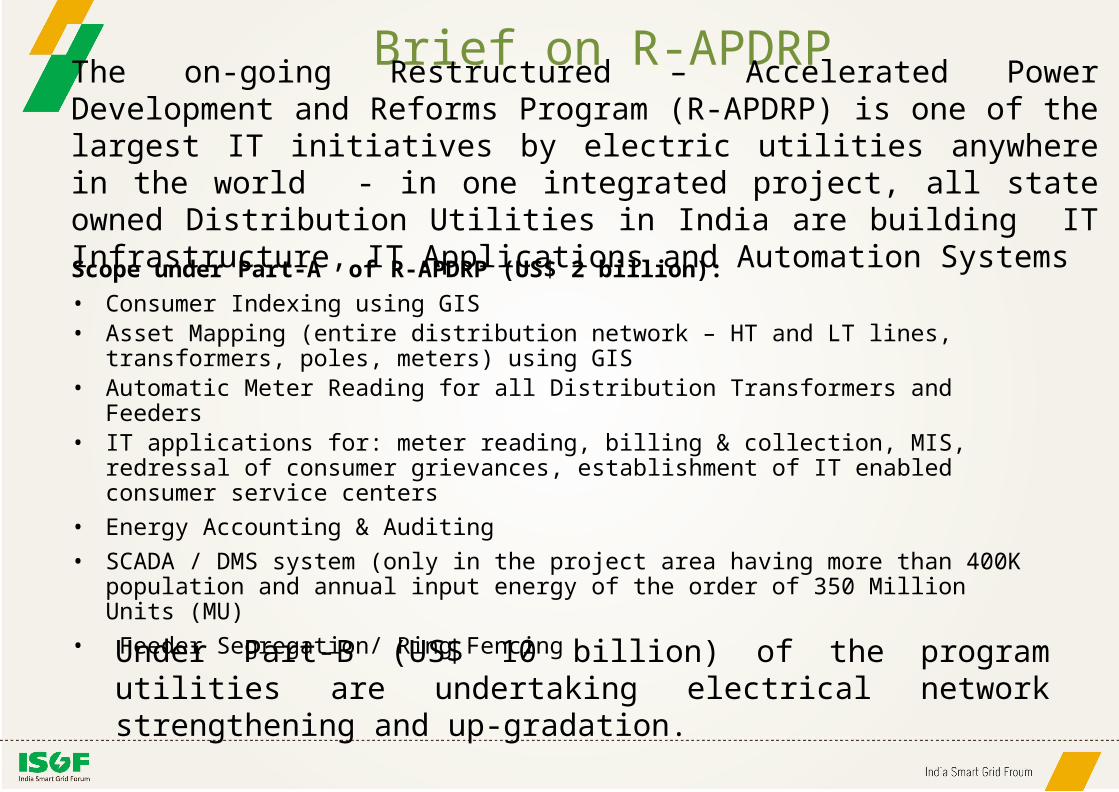

Brief on R-APDRP

Scope under Part-A of R-APDRP (US$ 2 billion):• Consumer Indexing using GIS• Asset Mapping (entire distribution network – HT and LT lines, transformers, poles,

meters) using GIS• Automatic Meter Reading for all Distribution Transformers and Feeders • IT applications for: meter reading, billing & collection, MIS, redressal of consumer

grievances, establishment of IT enabled consumer service centers • Energy Accounting & Auditing• SCADA / DMS system (only in the project area having more than 400K population and

annual input energy of the order of 350 Million Units (MU)• Feeder Segregation/ Ring Fencing

The on-going Restructured – Accelerated Power Development and Reforms Program (R-APDRP) is one of the largest IT initiatives by electric utilities anywhere in the world - in one integrated project, all state owned Distribution Utilities in India are building IT Infrastructure, IT Applications and Automation Systems

Under Part-B (US$ 10 billion) of the program utilities are undertaking electrical network strengthening and up-gradation.

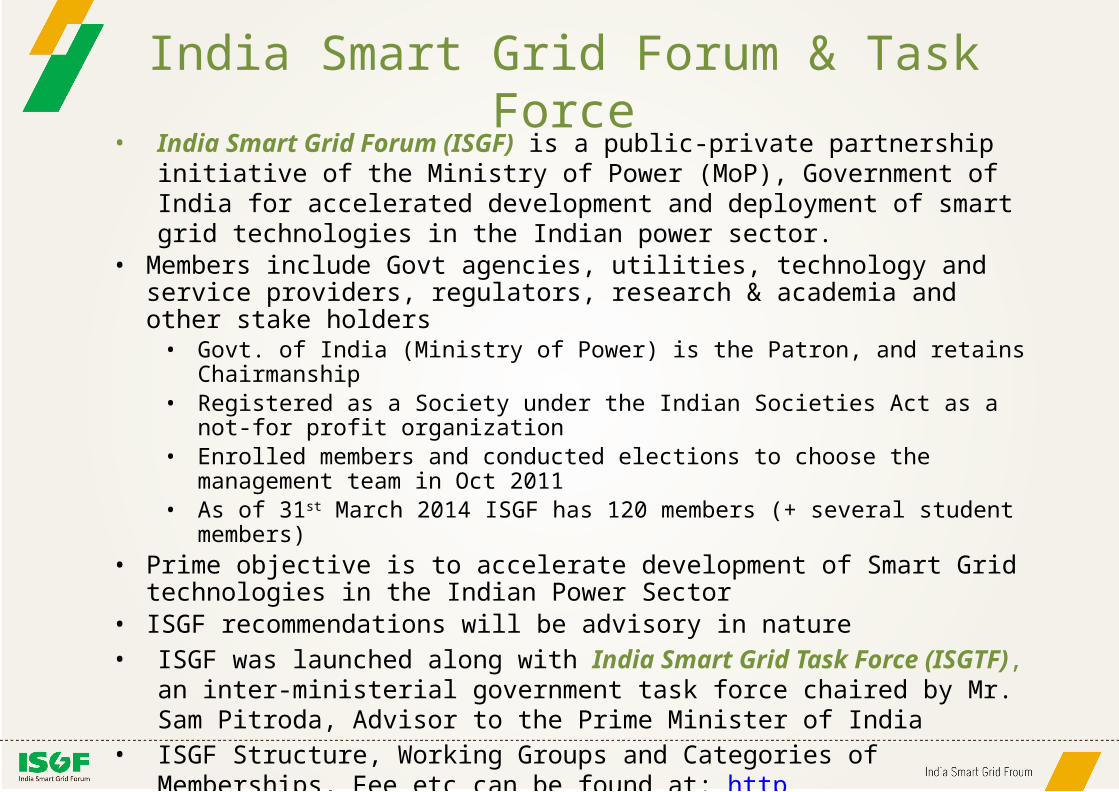

India Smart Grid Forum & Task Force• India Smart Grid Forum (ISGF) is a public-private partnership initiative of the Ministry

of Power (MoP), Government of India for accelerated development and deployment of smart grid technologies in the Indian power sector.

• Members include Govt agencies, utilities, technology and service providers, regulators, research & academia and other stake holders• Govt. of India (Ministry of Power) is the Patron, and retains Chairmanship• Registered as a Society under the Indian Societies Act as a not-for profit organization• Enrolled members and conducted elections to choose the management team in Oct 2011• As of 31st March 2014 ISGF has 120 members (+ several student members)

• Prime objective is to accelerate development of Smart Grid technologies in the Indian Power Sector

• ISGF recommendations will be advisory in nature • ISGF was launched along with India Smart Grid Task Force (ISGTF), an inter-ministerial

government task force chaired by Mr. Sam Pitroda, Advisor to the Prime Minister of India

• ISGF Structure, Working Groups and Categories of Memberships, Fee etc can be found at: http://indiasmartgrid.org/en/isgf/Pages/Membership.aspx

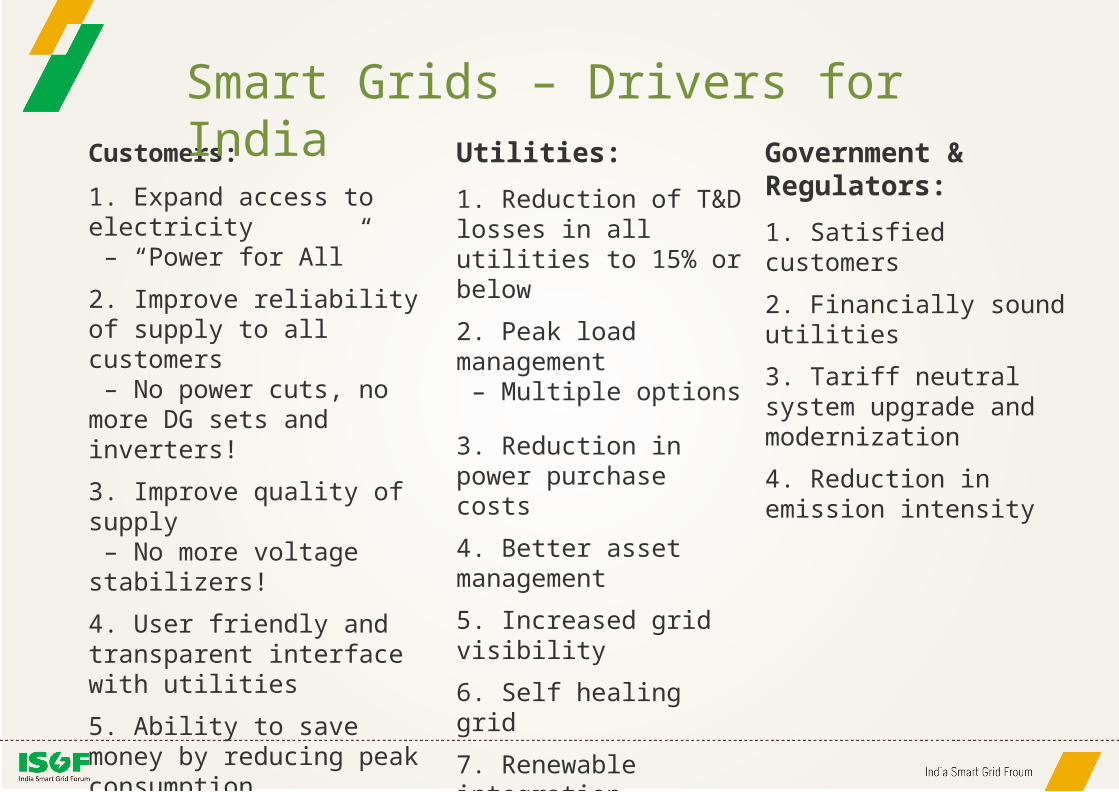

Customers:

1. Expand access to electricity – “Power for All”

2. Improve reliability of supply to all customers – No power cuts, no more DG sets and inverters!

3. Improve quality of supply – No more voltage stabilizers!

4. User friendly and transparent interface with utilities

5. Ability to save money by reducing peak consumption

6. Increased consumer engagement, also as a producer (“Prosumer”)

Smart Grids – Drivers for IndiaUtilities:

1. Reduction of T&D losses in all utilities to 15% or below

2. Peak load management – Multiple options

3. Reduction in power purchase costs

4. Better asset management

5. Increased grid visibility

6. Self healing grid

7. Renewable integration

Government & Regulators:

1. Satisfied customers

2. Financially sound utilities

3. Tariff neutral system upgrade and modernization

4. Reduction in emission intensity

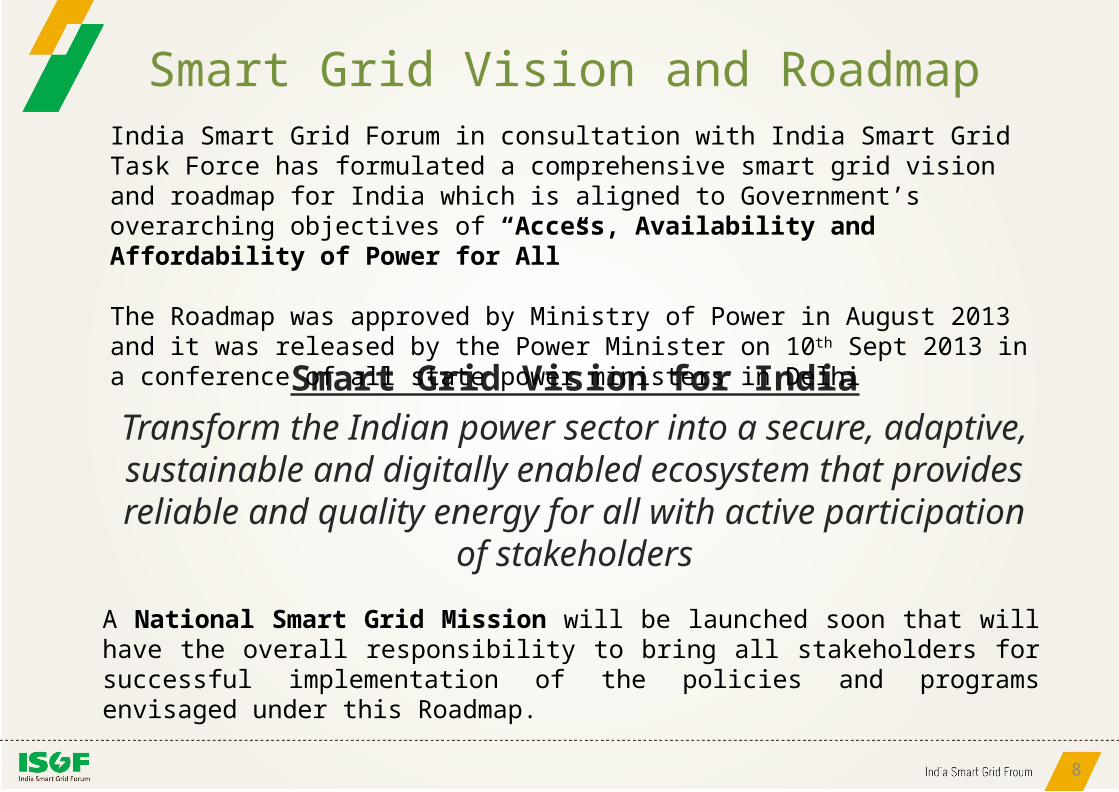

Smart Grid Vision and Roadmap

Smart Grid Vision for IndiaTransform the Indian power sector into a secure, adaptive, sustainable and digitally enabled ecosystem that provides

reliable and quality energy for all with active participation of stakeholders

8

India Smart Grid Forum in consultation with India Smart Grid Task Force has formulated a comprehensive smart grid vision and roadmap for India which is aligned to Government’s overarching objectives of “Access, Availability and Affordability of Power for All”

The Roadmap was approved by Ministry of Power in August 2013 and it was released by the Power Minister on 10th Sept 2013 in a conference of all state power ministers in Delhi

A National Smart Grid Mission will be launched soon that will have the overall responsibility to bring all stakeholders for successful implementation of the policies and programs envisaged under this Roadmap.

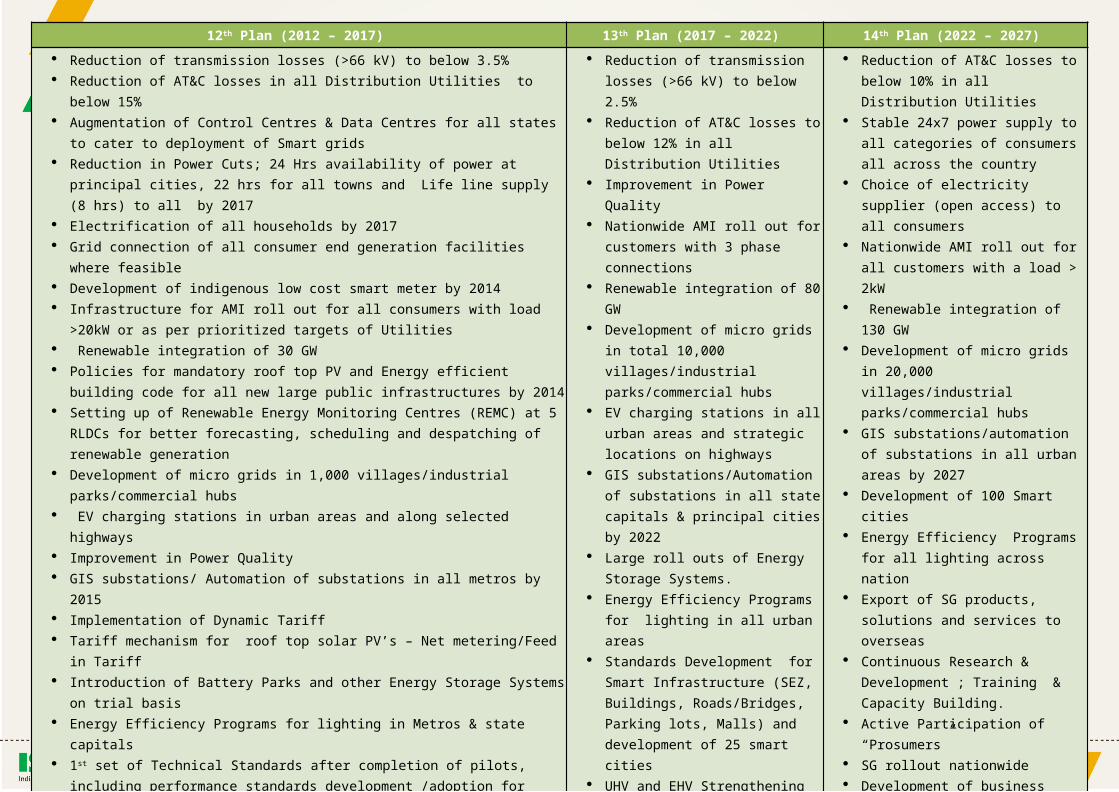

9Details of proposed activities, outcomes, and targets

12th Plan (2012 – 2017) 13th Plan (2017 – 2022) 14th Plan (2022 – 2027)

Reduction of transmission losses (>66 kV) to below 3.5% Reduction of AT&C losses in all Distribution Utilities to below 15% Augmentation of Control Centres & Data Centres for all states to cater to deployment of

Smart grids Reduction in Power Cuts; 24 Hrs availability of power at principal cities, 22 hrs for all towns

and Life line supply (8 hrs) to all by 2017 Electrification of all households by 2017 Grid connection of all consumer end generation facilities where feasible Development of indigenous low cost smart meter by 2014 Infrastructure for AMI roll out for all consumers with load >20kW or as per prioritized

targets of Utilities Renewable integration of 30 GW Policies for mandatory roof top PV and Energy efficient building code for all new large

public infrastructures by 2014 Setting up of Renewable Energy Monitoring Centres (REMC) at 5 RLDCs for better

forecasting, scheduling and despatching of renewable generation Development of micro grids in 1,000 villages/industrial parks/commercial hubs EV charging stations in urban areas and along selected highways Improvement in Power Quality GIS substations/ Automation of substations in all metros by 2015 Implementation of Dynamic Tariff Tariff mechanism for roof top solar PV’s – Net metering/Feed in Tariff Introduction of Battery Parks and other Energy Storage Systems on trial basis Energy Efficiency Programs for lighting in Metros & state capitals 1st set of Technical Standards after completion of pilots, including performance standards

development /adoption for Smart Grids including EVs and its charging infrastructure Finalization of frameworks for cyber security assessment, audit and certification of power

utilities by 2013 Strengthening of EHV/Distribution System Strengthening of optical fiber communication system along and for transmission lines and

substations 1200 kV UHV AC testing and simulation studies Research & Development, Training & Capacity Building - 10% Utility technical personnel to

be trained in Smart Grid Technologies Cost-Benefit Analysis of Smart Grid projects with inputs from pilots Customer Outreach & Participation Sustainability Initiatives SG Pilots, full SG roll out in pilot project cities Development of 5 Smart Cities Establishment of Smart Grid Test Bed by 2014 & Smart Grid Knowledge Centre by 2015

Reduction of transmission losses (>66 kV) to below 2.5%

Reduction of AT&C losses to below 12% in all Distribution Utilities

Improvement in Power Quality Nationwide AMI roll out for customers

with 3 phase connections Renewable integration of 80 GW Development of micro grids in total

10,000 villages/industrial parks/commercial hubs

EV charging stations in all urban areas and strategic locations on highways

GIS substations/Automation of substations in all state capitals & principal cities by 2022

Large roll outs of Energy Storage Systems.

Energy Efficiency Programs for lighting in all urban areas

Standards Development for Smart Infrastructure (SEZ, Buildings, Roads/Bridges, Parking lots, Malls) and development of 25 smart cities

UHV and EHV Strengthening Research & Developments; Training &

Capacity Building. 25% Utility technical personnel to be trained in Smart Grid Technologies

Export of SG products, solutions and services to overseas

Customer Outreach & Participation SG roll out in all urban areas

Reduction of AT&C losses to below 10% in all Distribution Utilities

Stable 24x7 power supply to all categories of consumers all across the country

Choice of electricity supplier (open access) to all consumers

Nationwide AMI roll out for all customers with a load > 2kW

Renewable integration of 130 GW Development of micro grids in 20,000

villages/industrial parks/commercial hubs GIS substations/automation of

substations in all urban areas by 2027 Development of 100 Smart cities Energy Efficiency Programs for all lighting

across nation Export of SG products, solutions and

services to overseas Continuous Research & Development ;

Training & Capacity Building. Active Participation of “Prosumers” SG rollout nationwide Development of business models to

create alternate revenue streams by leveraging the Smart Grid infrastructure to offer other services (security solutions, water metering, traffic solutions etc) to municipalities, state governments and other agencies

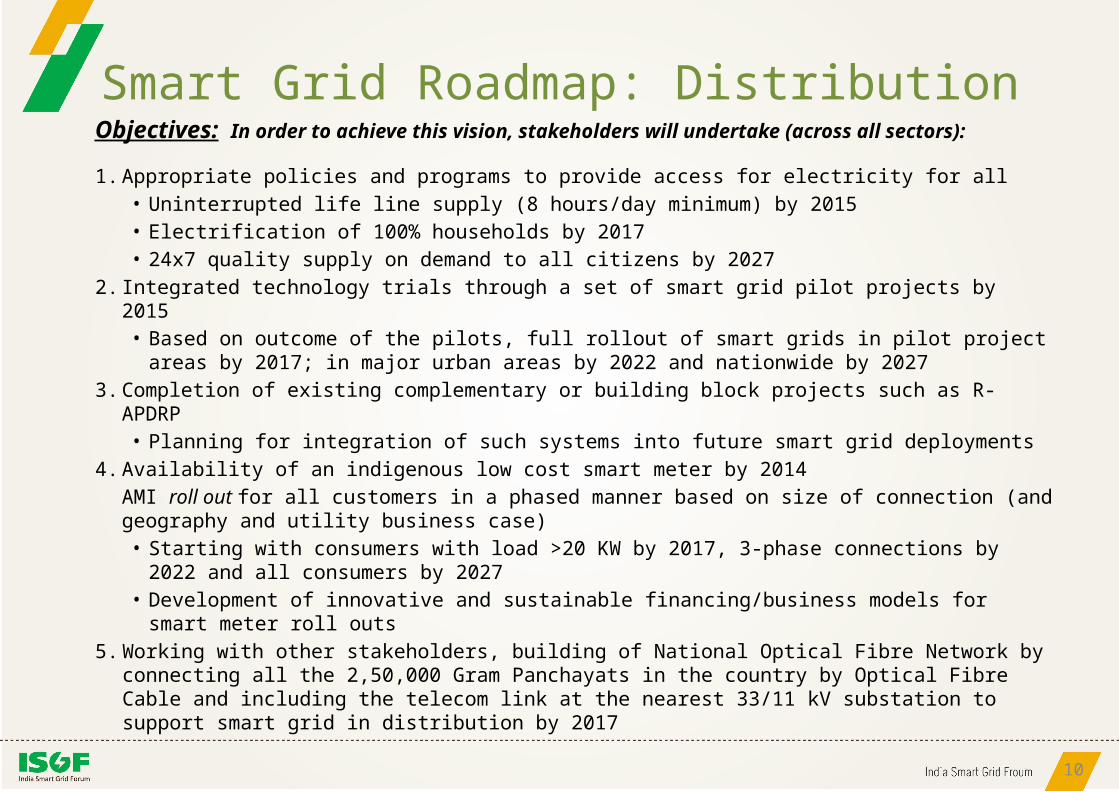

Smart Grid Roadmap: DistributionObjectives: In order to achieve this vision, stakeholders will undertake (across all sectors):

1. Appropriate policies and programs to provide access for electricity for all• Uninterrupted life line supply (8 hours/day minimum) by 2015• Electrification of 100% households by 2017 • 24x7 quality supply on demand to all citizens by 2027

2. Integrated technology trials through a set of smart grid pilot projects by 2015• Based on outcome of the pilots, full rollout of smart grids in pilot project areas by 2017; in

major urban areas by 2022 and nationwide by 20273. Completion of existing complementary or building block projects such as R-APDRP

• Planning for integration of such systems into future smart grid deployments4. Availability of an indigenous low cost smart meter by 2014

AMI roll out for all customers in a phased manner based on size of connection (and geography and utility business case)• Starting with consumers with load >20 KW by 2017, 3-phase connections by 2022 and all

consumers by 2027 • Development of innovative and sustainable financing/business models for smart meter roll

outs5. Working with other stakeholders, building of National Optical Fibre Network by connecting all

the 2,50,000 Gram Panchayats in the country by Optical Fibre Cable and including the telecom link at the nearest 33/11 kV substation to support smart grid in distribution by 2017

10

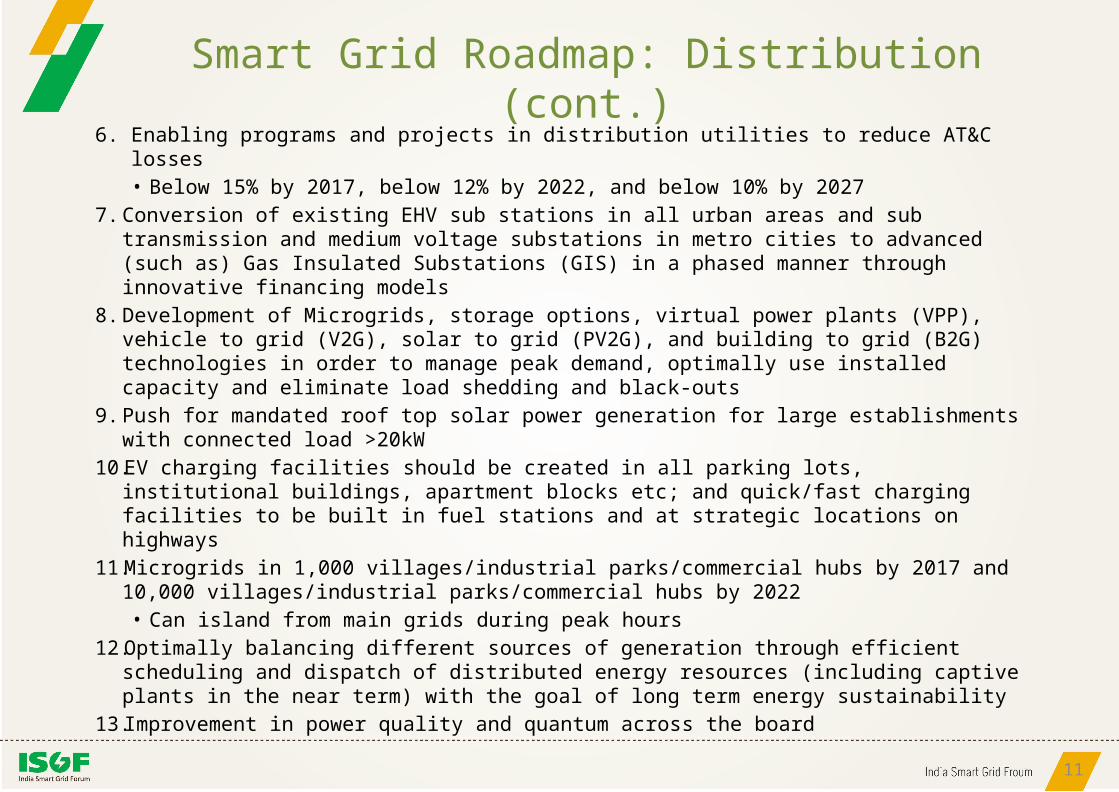

Smart Grid Roadmap: Distribution (cont.)6. Enabling programs and projects in distribution utilities to reduce AT&C losses

• Below 15% by 2017, below 12% by 2022, and below 10% by 20277. Conversion of existing EHV sub stations in all urban areas and sub transmission and medium

voltage substations in metro cities to advanced (such as) Gas Insulated Substations (GIS) in a phased manner through innovative financing models

8. Development of Microgrids, storage options, virtual power plants (VPP), vehicle to grid (V2G), solar to grid (PV2G), and building to grid (B2G) technologies in order to manage peak demand, optimally use installed capacity and eliminate load shedding and black-outs

9. Push for mandated roof top solar power generation for large establishments with connected load >20kW

10. EV charging facilities should be created in all parking lots, institutional buildings, apartment blocks etc; and quick/fast charging facilities to be built in fuel stations and at strategic locations on highways

11. Microgrids in 1,000 villages/industrial parks/commercial hubs by 2017 and 10,000 villages/industrial parks/commercial hubs by 2022 • Can island from main grids during peak hours

12. Optimally balancing different sources of generation through efficient scheduling and dispatch of distributed energy resources (including captive plants in the near term) with the goal of long term energy sustainability

13. Improvement in power quality and quantum across the board

11

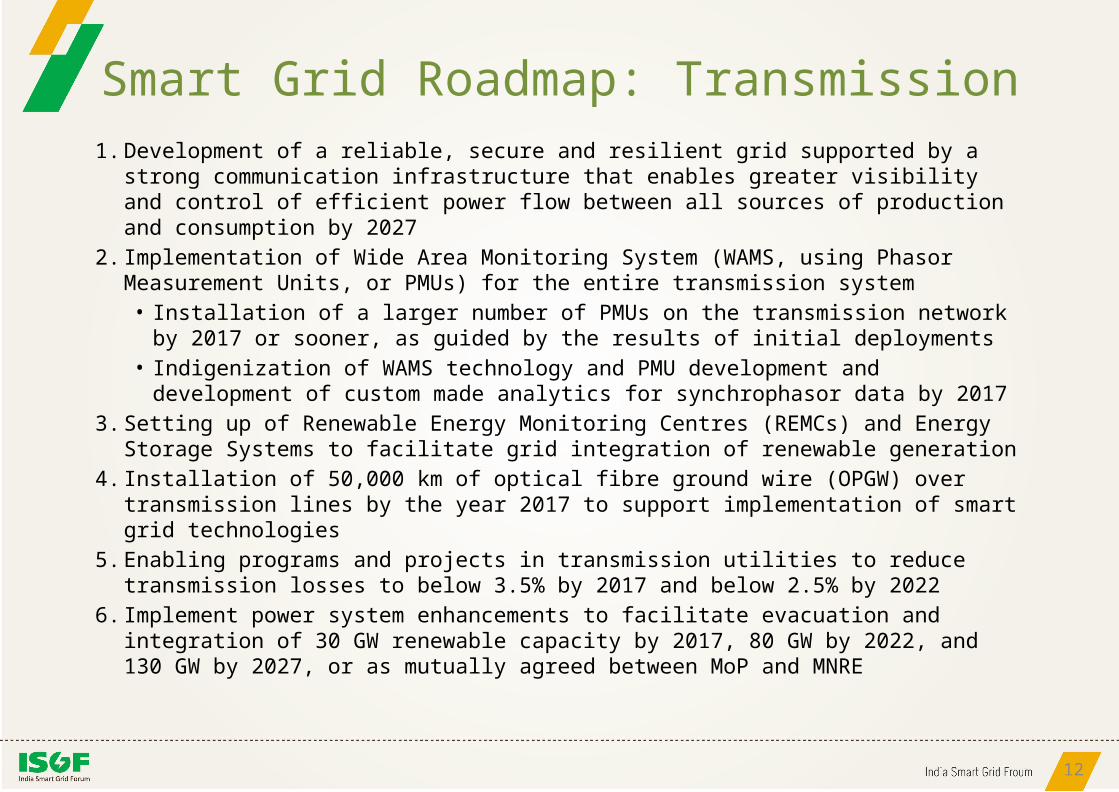

Smart Grid Roadmap: Transmission1. Development of a reliable, secure and resilient grid supported by a strong

communication infrastructure that enables greater visibility and control of efficient power flow between all sources of production and consumption by 2027

2. Implementation of Wide Area Monitoring System (WAMS, using Phasor Measurement Units, or PMUs) for the entire transmission system• Installation of a larger number of PMUs on the transmission network by 2017 or

sooner, as guided by the results of initial deployments• Indigenization of WAMS technology and PMU development and development of

custom made analytics for synchrophasor data by 20173. Setting up of Renewable Energy Monitoring Centres (REMCs) and Energy Storage

Systems to facilitate grid integration of renewable generation4. Installation of 50,000 km of optical fibre ground wire (OPGW) over transmission lines by

the year 2017 to support implementation of smart grid technologies 5. Enabling programs and projects in transmission utilities to reduce transmission losses to

below 3.5% by 2017 and below 2.5% by 20226. Implement power system enhancements to facilitate evacuation and integration of 30

GW renewable capacity by 2017, 80 GW by 2022, and 130 GW by 2027, or as mutually agreed between MoP and MNRE

12

Smart Grid Roadmap: Policy, Standards and Regulations

13

1. Formulation of effective customer outreach and communication programs2. Development of state/utility specific strategic roadmap(s) by 2014 for Smart Grid deployments • Required business process reengineering, change management and capacity building programs to

be initiated by 20143. Policies for grid-interconnection of consumer generation facilities (including renewable) where feasible• Policies for roof-top solar, net-metering/feed-in tariff as well as peaking power by 2014

4. Policies supporting improved tariffs such as dynamic tariffs, variable tariffs, etc., including demand response programs• Bulk consumers by 2014; extending to all 3-phase (or otherwise defined) consumers by 2017

5. Policies created by 2014 for implementing energy efficiency in public infrastructure and EV charging facilities starting by 2015 and Demand Response ready appliances by 2017

6. Finalization of frameworks for cyber security assessment, audit and certification of utilities by 20137. Development of business models to create alternate revenue streams by leveraging the Smart Grid

infrastructure to offer other services (security solutions, water metering, traffic solutions etc) to municipalities, state governments and other agencies

8. Build upon the results of smart grid pilot projects and recommend appropriate changes conducive to smart grid development in Acts/Plans/etc. by end of 2015

9. Development of 1st set of Indian Smart Grid Standards by 2014• Active involvement of Indian experts in international SG development bodies

Smart Grid Roadmap: Other Initiatives

14

1. Tariff mechanisms, new energy products, energy options and programs to encourage participation of customers in the energy markets that make them “prosumers” – producers and consumers – by 2017

2. Create an effective information exchange platform that can be shared by all market participants, including prosumers, in real time which will lead to the development of new and enhanced energy markets

3. Investment in research and development, training and capacity building programs for creation of adequate resource pools for developing and implementing smart grid technologies in India - can also become a global leader and exporter of smart grid know-how, products and services

Smart Grid Pilot Projects in India• 14 Smart Grid Pilot projects have been approved for different distribution

utilities last year by Ministry of Power (MoP), Govt of India (GoI). The list and project summary is available at: http://indiasmartgrid.org/en/Pages/Projects.aspx

• These projects will be part funded by MoP (50% project cost as grant from GoI). Combined cost of these projects are about US$ 80 million

• These projects will be in execution mode early 2015 – presently in RFP stage • Most projects involve 20,000 or more customers• These pilots are expected to help technology section guides and business case

developments for larger projects in the next phase• Many large utilities (in large states) could not apply for the first set of projects.

So another set of larger and more integrated projects will be formulated soon• Last mile connectivity is the major challenge in smart grid applications and

these field trials to determine the most appropriate communication solutions

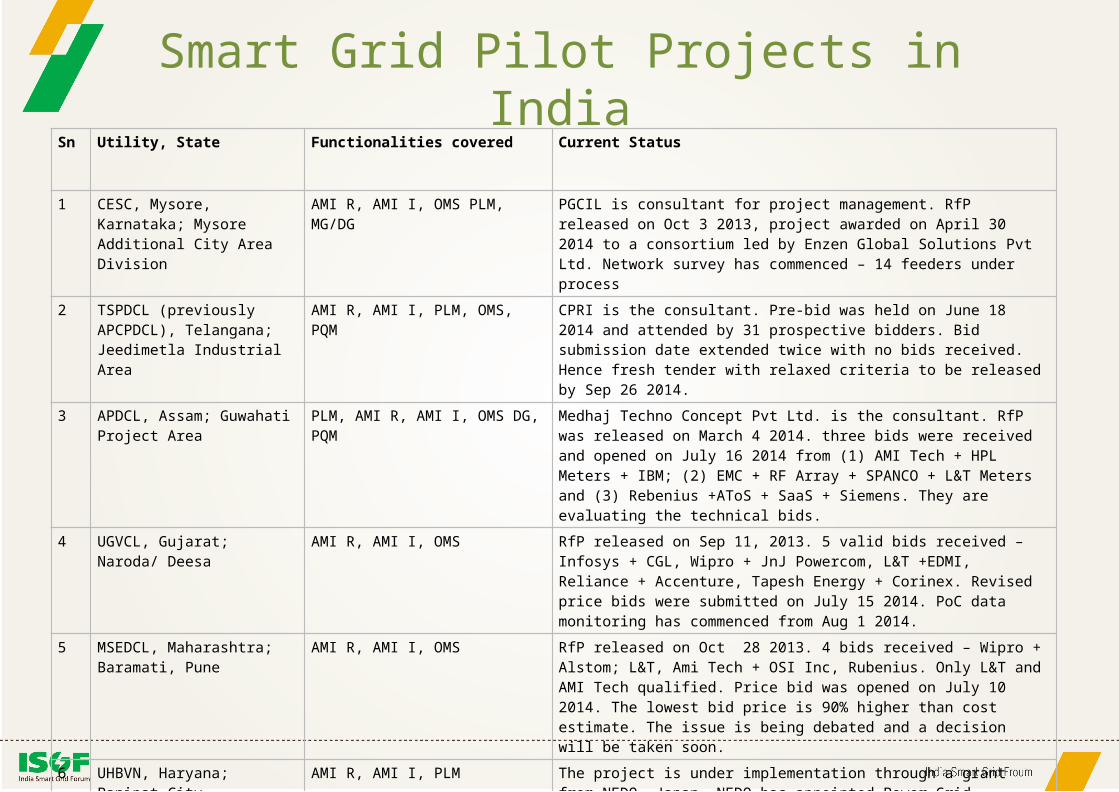

Smart Grid Pilot Projects in IndiaSn Utility, State Functionalities covered Current Status

1 CESC, Mysore, Karnataka; Mysore Additional City Area Division

AMI R, AMI I, OMS PLM, MG/DG PGCIL is consultant for project management. RfP released on Oct 3 2013, project awarded on April 30 2014 to a consortium led by Enzen Global Solutions Pvt Ltd. Network survey has commenced – 14 feeders under process

2 TSPDCL (previously APCPDCL), Telangana; Jeedimetla Industrial Area

AMI R, AMI I, PLM, OMS, PQM CPRI is the consultant. Pre-bid was held on June 18 2014 and attended by 31 prospective bidders. Bid submission date extended twice with no bids received. Hence fresh tender with relaxed criteria to be released by Sep 26 2014.

3 APDCL, Assam; Guwahati Project Area

PLM, AMI R, AMI I, OMS DG, PQM Medhaj Techno Concept Pvt Ltd. is the consultant. RfP was released on March 4 2014. three bids were received and opened on July 16 2014 from (1) AMI Tech + HPL Meters + IBM; (2) EMC + RF Array + SPANCO + L&T Meters and (3) Rebenius +AToS + SaaS + Siemens. They are evaluating the technical bids.

4 UGVCL, Gujarat; Naroda/ Deesa AMI R, AMI I, OMS RfP released on Sep 11, 2013. 5 valid bids received – Infosys + CGL, Wipro + JnJ Powercom, L&T +EDMI, Reliance + Accenture, Tapesh Energy + Corinex. Revised price bids were submitted on July 15 2014. PoC data monitoring has commenced from Aug 1 2014.

5 MSEDCL, Maharashtra; Baramati, Pune

AMI R, AMI I, OMS RfP released on Oct 28 2013. 4 bids received – Wipro + Alstom; L&T, Ami Tech + OSI Inc, Rubenius. Only L&T and AMI Tech qualified. Price bid was opened on July 10 2014. The lowest bid price is 90% higher than cost estimate. The issue is being debated and a decision will be taken soon.

6 UHBVN, Haryana; Panipat City SubDivision

AMI R, AMI I, PLM The project is under implementation through a grant from NEDO, Japan. NEDO has appointed Power Grid Solution Ltd (a JV of Tokyo electric Power Company and Hitachi), NTT Communications, Fuji Electric Company and PWC for a feasibility study, which has been completed and presented to MoP on Aug 22 2014. Once approved project feasibility and design will begin.

Smart Grid Pilot Projects in IndiaSn Utility, State Functionalities covered Current Status

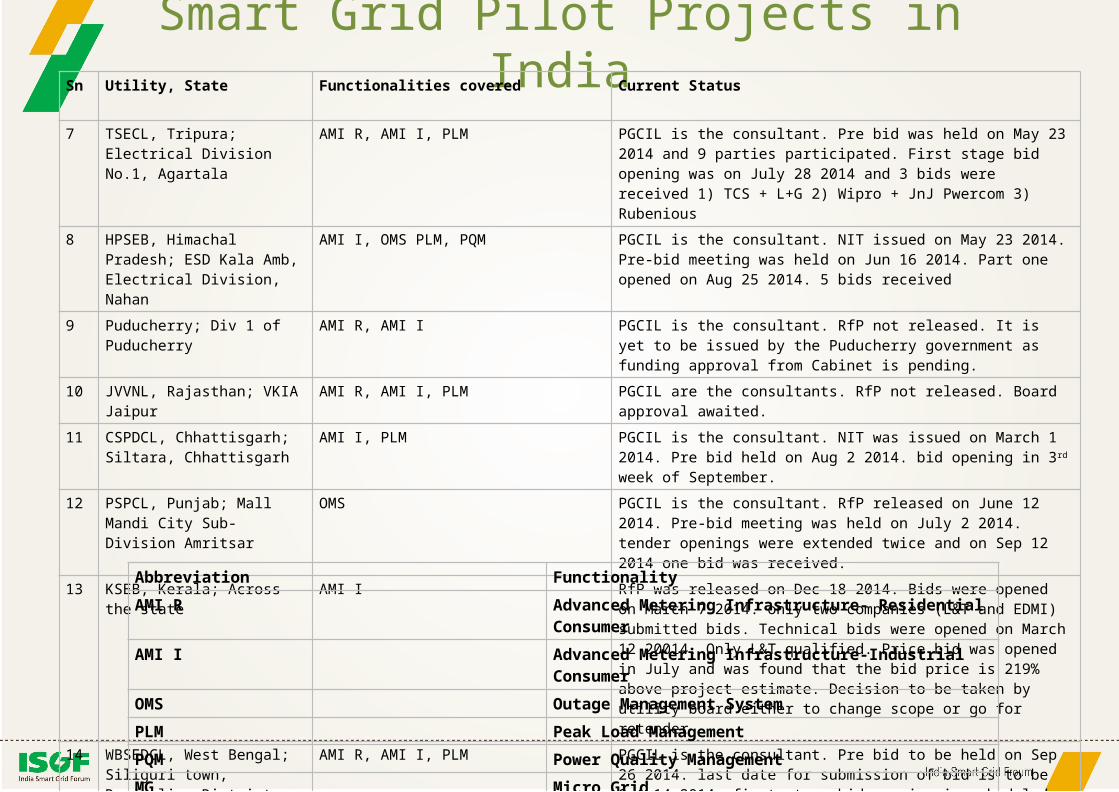

7 TSECL, Tripura; Electrical Division No.1, Agartala

AMI R, AMI I, PLM PGCIL is the consultant. Pre bid was held on May 23 2014 and 9 parties participated. First stage bid opening was on July 28 2014 and 3 bids were received 1) TCS + L+G 2) Wipro + JnJ Pwercom 3) Rubenious

8 HPSEB, Himachal Pradesh; ESD Kala Amb, Electrical Division, Nahan

AMI I, OMS PLM, PQM PGCIL is the consultant. NIT issued on May 23 2014. Pre-bid meeting was held on Jun 16 2014. Part one opened on Aug 25 2014. 5 bids received

9 Puducherry; Div 1 of Puducherry AMI R, AMI I PGCIL is the consultant. RfP not released. It is yet to be issued by the Puducherry government as funding approval from Cabinet is pending.

10 JVVNL, Rajasthan; VKIA Jaipur AMI R, AMI I, PLM PGCIL are the consultants. RfP not released. Board approval awaited.

11 CSPDCL, Chhattisgarh; Siltara, Chhattisgarh

AMI I, PLM PGCIL is the consultant. NIT was issued on March 1 2014. Pre bid held on Aug 2 2014. bid opening in 3rd week of September.

12 PSPCL, Punjab; Mall Mandi City Sub-Division Amritsar

OMS PGCIL is the consultant. RfP released on June 12 2014. Pre-bid meeting was held on July 2 2014. tender openings were extended twice and on Sep 12 2014 one bid was received.

13 KSEB, Kerala; Across the state AMI I RfP was released on Dec 18 2014. Bids were opened on March 7 2014. only two companies (L&T and EDMI) submitted bids. Technical bids were opened on March 12 20014. Only L&T qualified. Price bid was opened in July and was found that the bid price is 219% above project estimate. Decision to be taken by utility board either to change scope or go for retender

14 WBSEDCL, West Bengal; Siliguri town, Darjeeling District

AMI R, AMI I, PLM PGCIL is the consultant. Pre bid to be held on Sep 26 2014. last date for submission of bid is to be Oct 14 2014. first stage bid opening is scheduled for Oct 17 2014.

Abbreviation FunctionalityAMI R Advanced Metering Infrastructure- Residential Consumer

AMI I Advanced Metering Infrastructure-Industrial Consumer

OMS Outage Management System PLM Peak Load ManagementPQM Power Quality ManagementMG Micro GridDG Distributed Generation

Smart Grid Initiatives at State Level • Preparation of State specific/Utility specific Smart Grid Roadmaps and

Policies – all states/utilities are not at the same level• Constitution of Smart Grid Cells in States:

MAHA-SGCC in Maharashtra SMART GRID STEERING COMMITTEE in Odisha Few other states are actively considering

• Consumer Engagement Programs• Training and Capacity Building for Utilities and Industry by ISGF

Foundation Course on Smart Grid for Engineers (5 Days) Appreciation Course on Cyber Security (3 Days) Semester Course on Cyber Security for M.Tech Students R-APDRP Part-A Training for Managers, Engineers and Operators

• Training for Regulators by ISGF Foundation Course on Smart Grid for Engineers (5 days) – to start from August 2014 Regulations for Smart Grids (5 Days) – course materials under development: target Oct 2014

• State Level Smart Grid Projects – refer latest Smart Grid Bulletin

18

ISGF Smart Grid Bulletin

Smart Grid Bulletin Covers:• Message/ Interview from Senior Power Sector Officials• Smart Grid Updates:

– Policy, Regulations & Standards – Transfers & Postings in Power Sector in India– Technology & Projects– Pilot Projects in India – Other Smart Grid Projects in India

• ISGF Quarterly Progress Report• Smart Grid Capacity Building Initiatives by ISGF:

– Cyber Security for Power Systems – Smart Grid Foundation Course – Smart Grid Bootcamp

• Smart Grid Events (National & International)• SMART GRID Gyan Circulation: 2,500 printed copies to top decision makers in power sector in India and > 25,000 electronic copies to senior power sector professionals around the world.

19

National Smart Grid Mission (NSGM)In order to achieve the goals envisaged in the Smart Grid Roadmap, it is

proposed to launch a National Smart Grid Mission (NSGM)• NSGM with its own resources and funding mechanism that will bring national

level support from other Ministries, Institutions, and the State Governments • NSGM will formulate detailed blueprint that would cover specific programs and

projects in different utilities in each state and estimate the capital outlays and budgetary support

• NSGM will coordinate with state governments, utilities and other stakeholders for rollout of smart grid projects and monitor project implementation

• NSGM will coordinate development of standards, technically feasible and economically sustainable business models relevant to the Indian context

• Preparation of NSGM framework and cabinet note under progress – NSGM will have a Steering Committee chaired by the Minister of Power,

an Executive Committee chaired by Secretary- Power, a Technical Committee chaired by Chairperson of Central Electricity Authority, and a Mission Directorate. There will be NSGM PMUs in all states

20

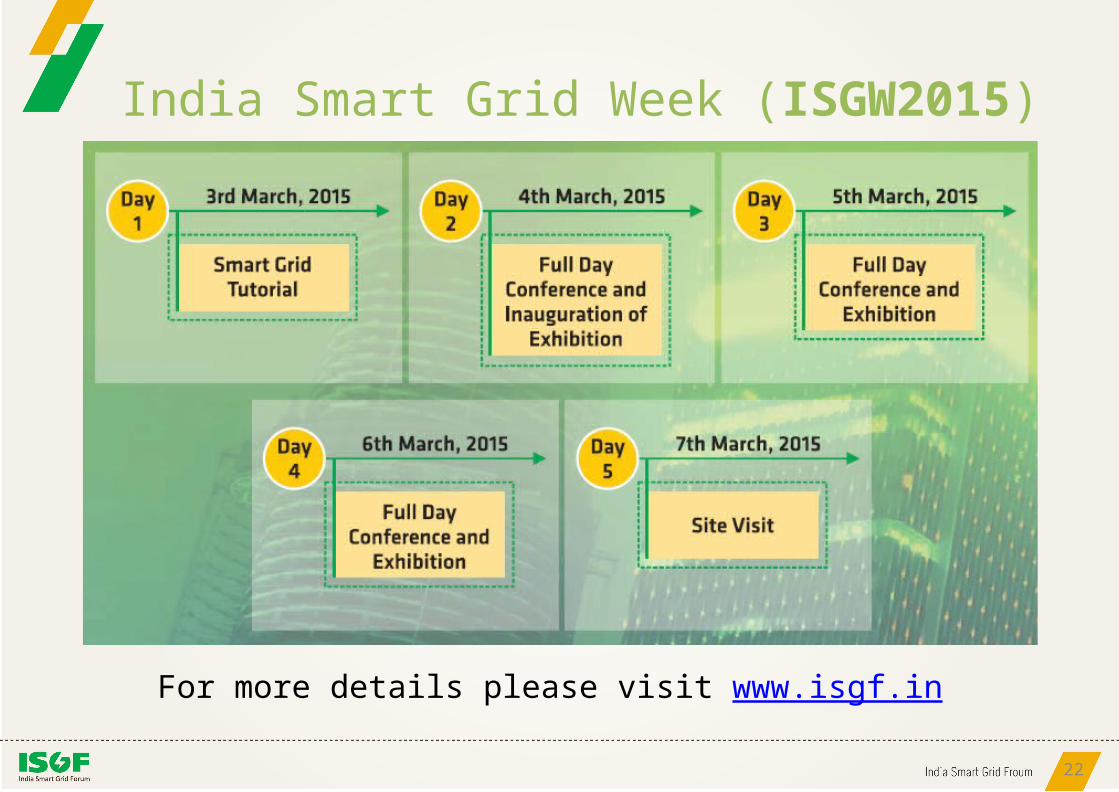

INDIA SMART GRID WEEK 2015

21

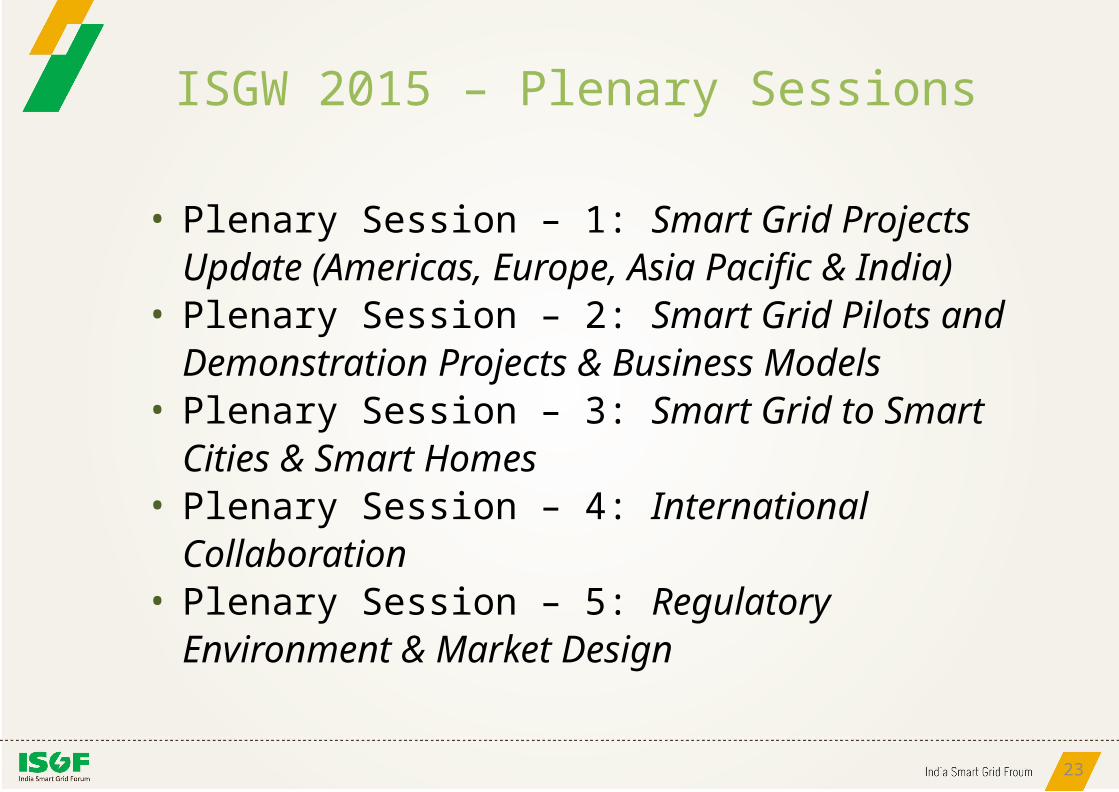

ISGW 2015 – Plenary Sessions

23

• Plenary Session – 1: Smart Grid Projects Update (Americas, Europe, Asia Pacific & India)

• Plenary Session – 2: Smart Grid Pilots and Demonstration Projects & Business Models

• Plenary Session – 3: Smart Grid to Smart Cities & Smart Homes

• Plenary Session – 4: International Collaboration• Plenary Session – 5: Regulatory Environment & Market

Design

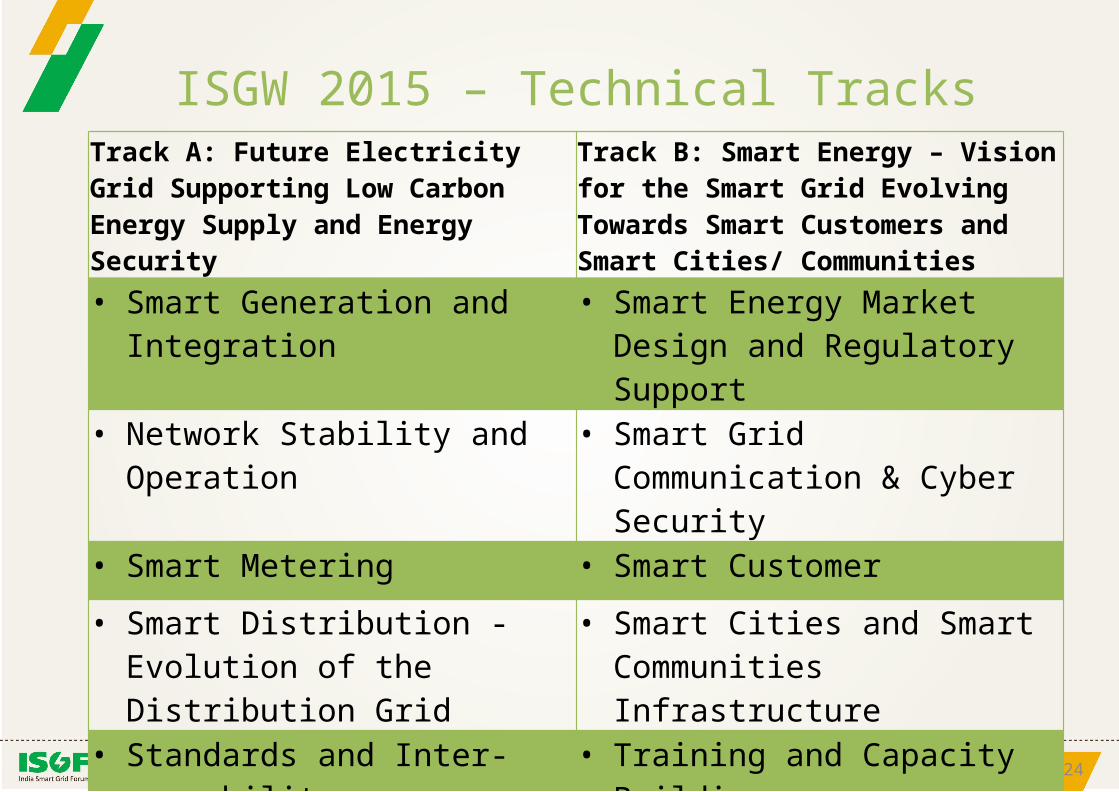

ISGW 2015 – Technical Tracks

24

Track A: Future Electricity Grid Supporting Low Carbon Energy Supply and Energy Security

Track B: Smart Energy – Vision for the Smart Grid Evolving Towards Smart Customers and Smart Cities/ Communities

• Smart Generation and Integration • Smart Energy Market Design and Regulatory Support

• Network Stability and Operation • Smart Grid Communication & Cyber Security

• Smart Metering • Smart Customer

• Smart Distribution - Evolution of the Distribution Grid

• Smart Cities and Smart Communities Infrastructure

• Standards and Inter-operability • Training and Capacity Building

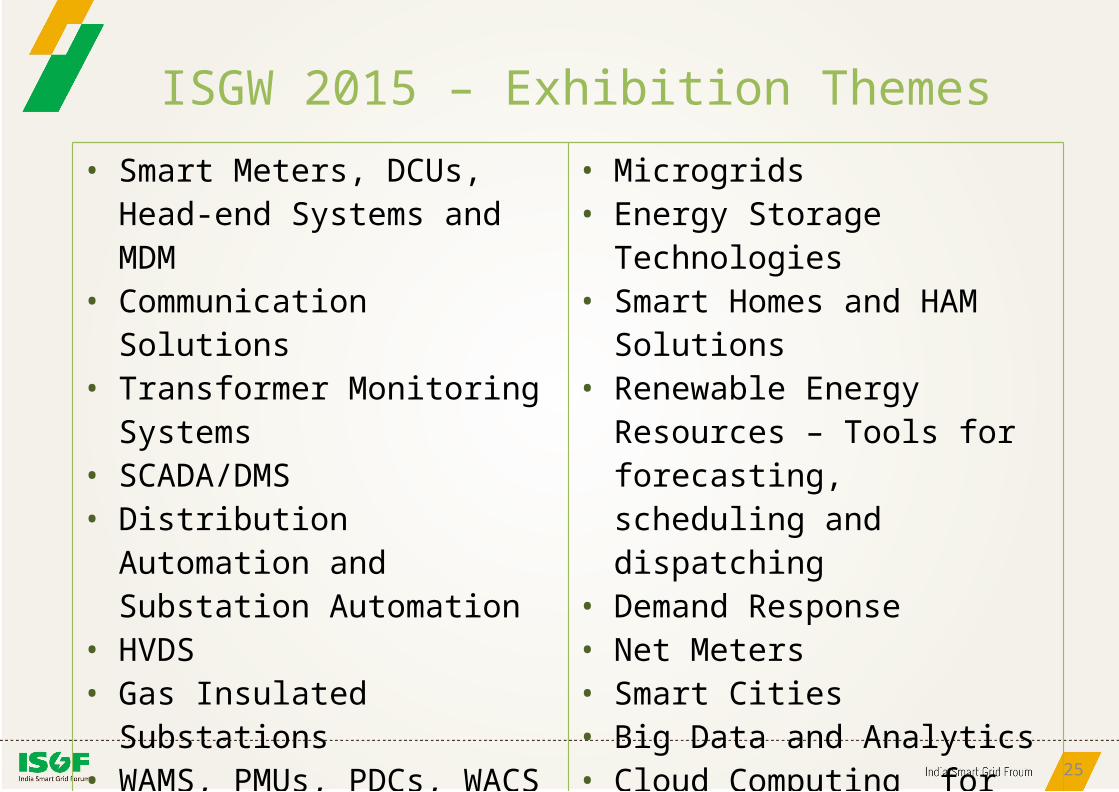

ISGW 2015 – Exhibition Themes

25

• Smart Meters, DCUs, Head-end Systems and MDM

• Communication Solutions• Transformer Monitoring Systems• SCADA/DMS• Distribution Automation and

Substation Automation• HVDS• Gas Insulated Substations• WAMS, PMUs, PDCs, WACS• EV Charging Infrastructure and

Payment Systems• V2G and B2G Technologies

• Microgrids• Energy Storage Technologies• Smart Homes and HAM Solutions• Renewable Energy Resources –

Tools for forecasting, scheduling and dispatching

• Demand Response • Net Meters• Smart Cities• Big Data and Analytics• Cloud Computing for Smart

Utilities/Smart Cities

Thank you for your kind attention!

www.indiasmartgrid.org

26