Embed Size (px)

Citation preview

Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.Copyright (c) 2008 Standard & Poor’s, a division of The McGraw-Hill Companies, Inc. All rights reserved.

Thomas ConnellManaging DirectorStandard & Poor’s

FEI Canada Conference

Jasper, AlbertaJune 9-11, 2008

Reflections on Reflections on Reflections on Reflections on

the Credit Crunchthe Credit Crunchthe Credit Crunchthe Credit Crunch

2. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Reflections on the Credit Crunch

1. Global Capital Markets in Transition

2. The Credit Crunch: Aspects and Outcomes

3. Lessons from the Credit Crunch

4. Where to From Here: Current Credit Market Outlook

3. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Global Capital Markets

In Transition

4. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

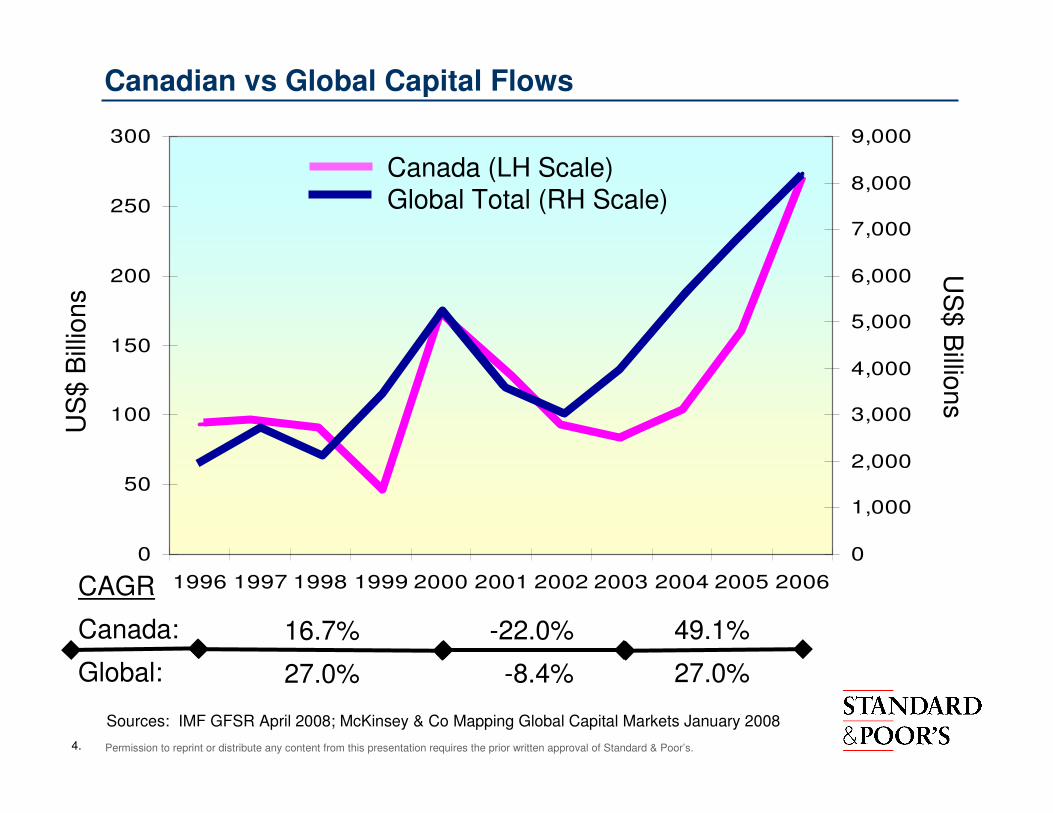

Canadian vs Global Capital Flows

0

50

100

150

200

250

300

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Canada (LH Scale)Global Total (RH Scale)

US

$ B

illio

ns

US

$ B

illion

s

16.7%

27.0%

-22.0%

-8.4%

49.1%

27.0%

CAGR

Canada:

Global:

Sources: IMF GFSR April 2008; McKinsey & Co Mapping Global Capital Markets January 2008

5. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

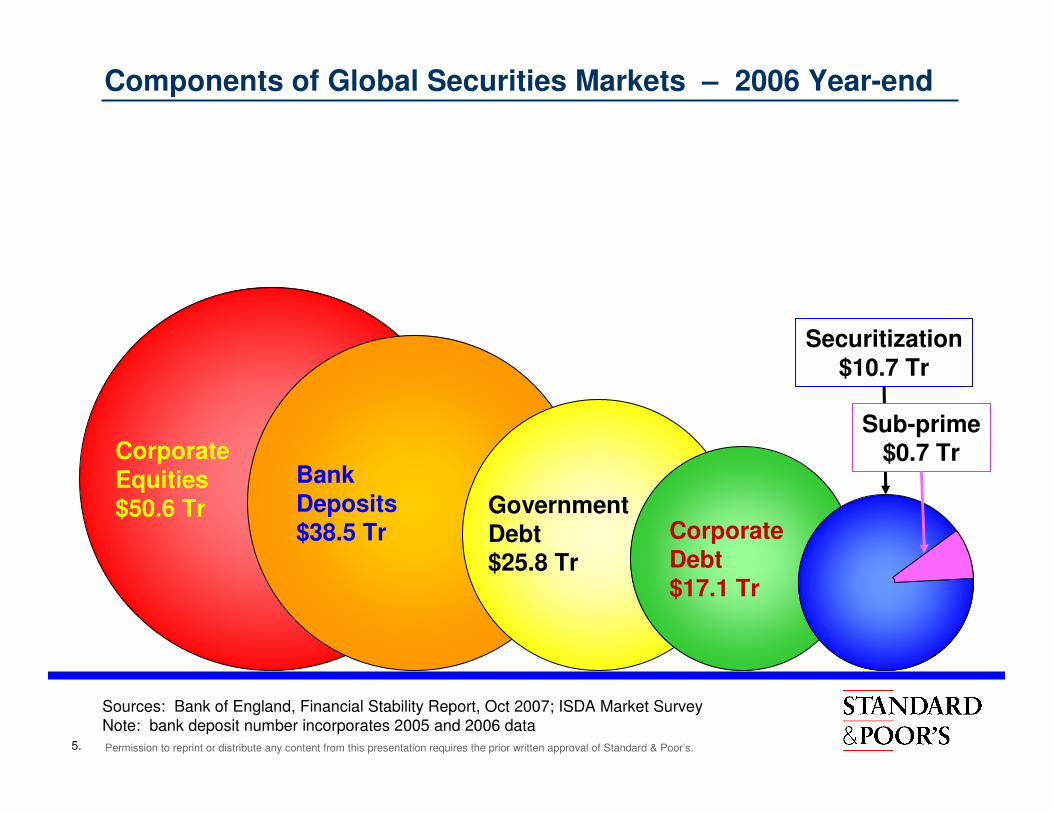

Components of Global Securities Markets – 2006 Year-end

CorporateEquities$50.6 Tr

BankDeposits$38.5 Tr

GovernmentDebt$25.8 Tr

CorporateDebt$17.1 Tr

Sub-prime$0.7 Tr

Securitization$10.7 Tr

Sources: Bank of England, Financial Stability Report, Oct 2007; ISDA Market SurveyNote: bank deposit number incorporates 2005 and 2006 data

6. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Components of Global Securities Markets – 2006 Year-end

CorporateEquities$50.6 Tr

BankDeposits$38.5 Tr

GovernmentDebt$25.8 Tr

CorporateDebt$17.1 Tr

Sub-prime$0.7 Tr

Securitization$10.7 Tr

Notional Derivatives Outstanding

2006: $327 Tr

2007: $456 Tr

Sources: Bank of England, Financial Stability Report, Oct 2007; ISDA Market SurveyNote: bank deposit number incorporates 2005 and 2006 data

CreditDerivatives Outstanding

2007$62 Tr

7. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

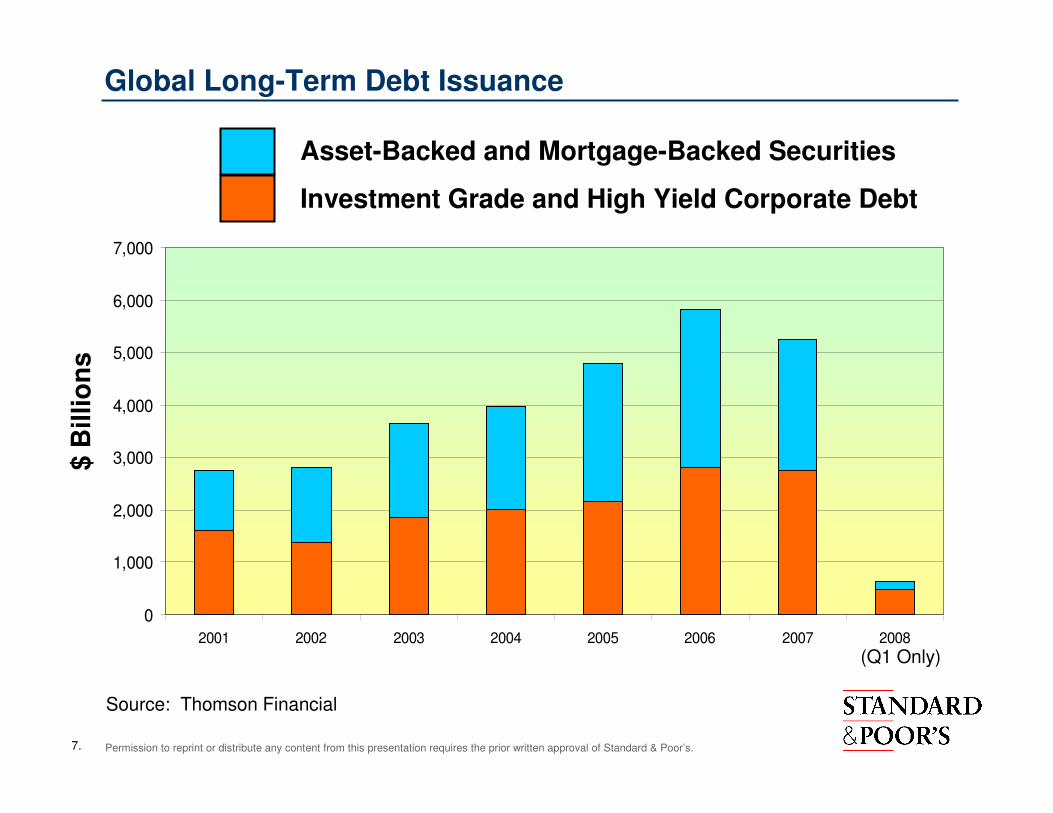

Global Long-Term Debt Issuance

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2001 2002 2003 2004 2005 2006 2007 2008

Asset-Backed and Mortgage-Backed Securities

Investment Grade and High Yield Corporate Debt

$ B

illio

ns

Source: Thomson Financial

(Q1 Only)

8. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

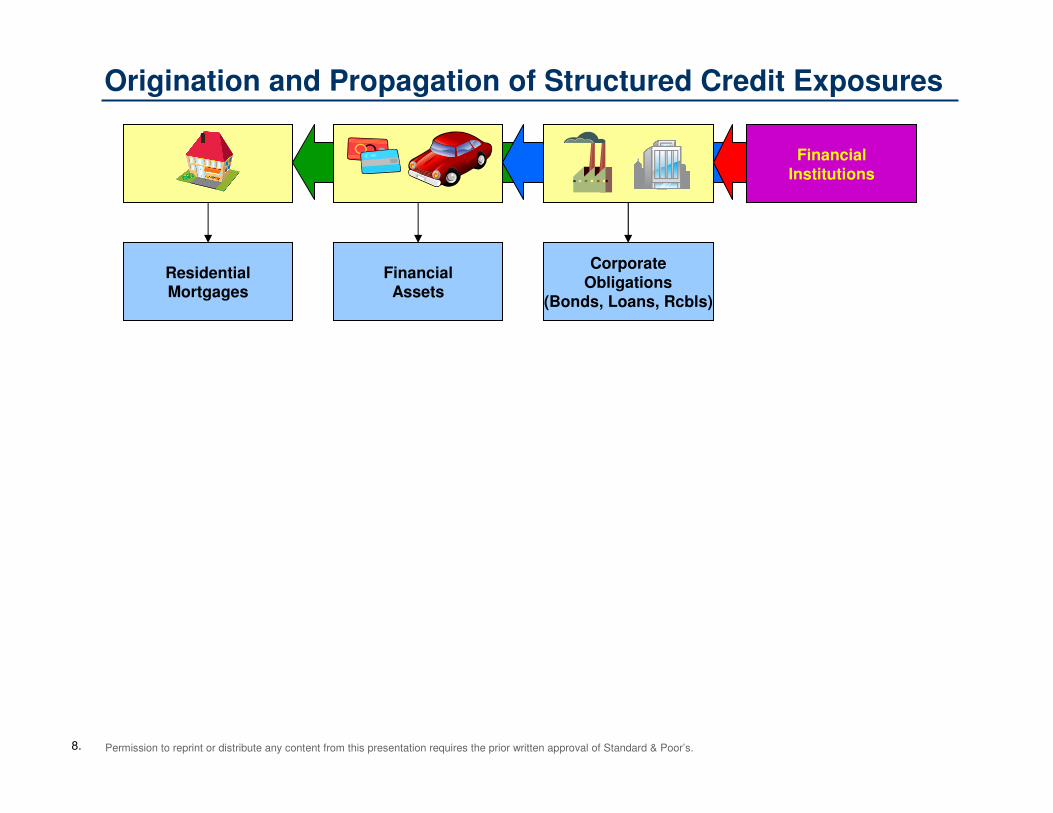

ResidentialMortgages

CorporateObligations

(Bonds, Loans, Rcbls)

FinancialAssets

FinancialInstitutions

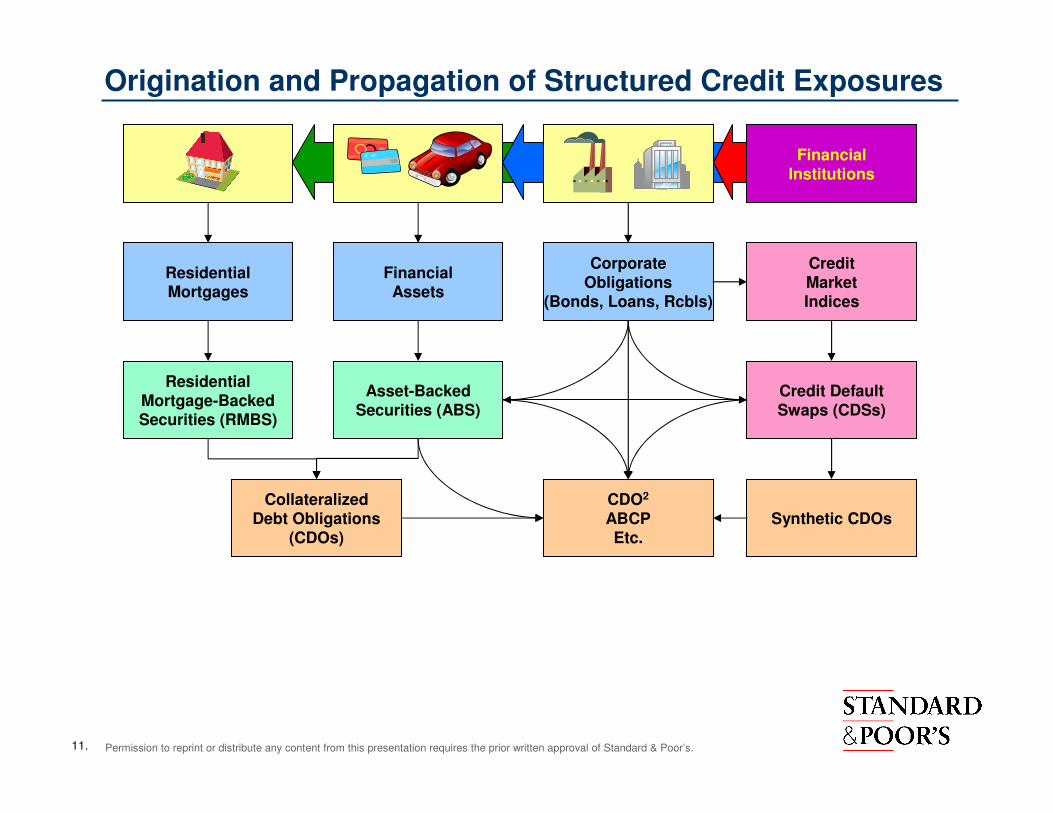

Origination and Propagation of Structured Credit Exposures

9. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

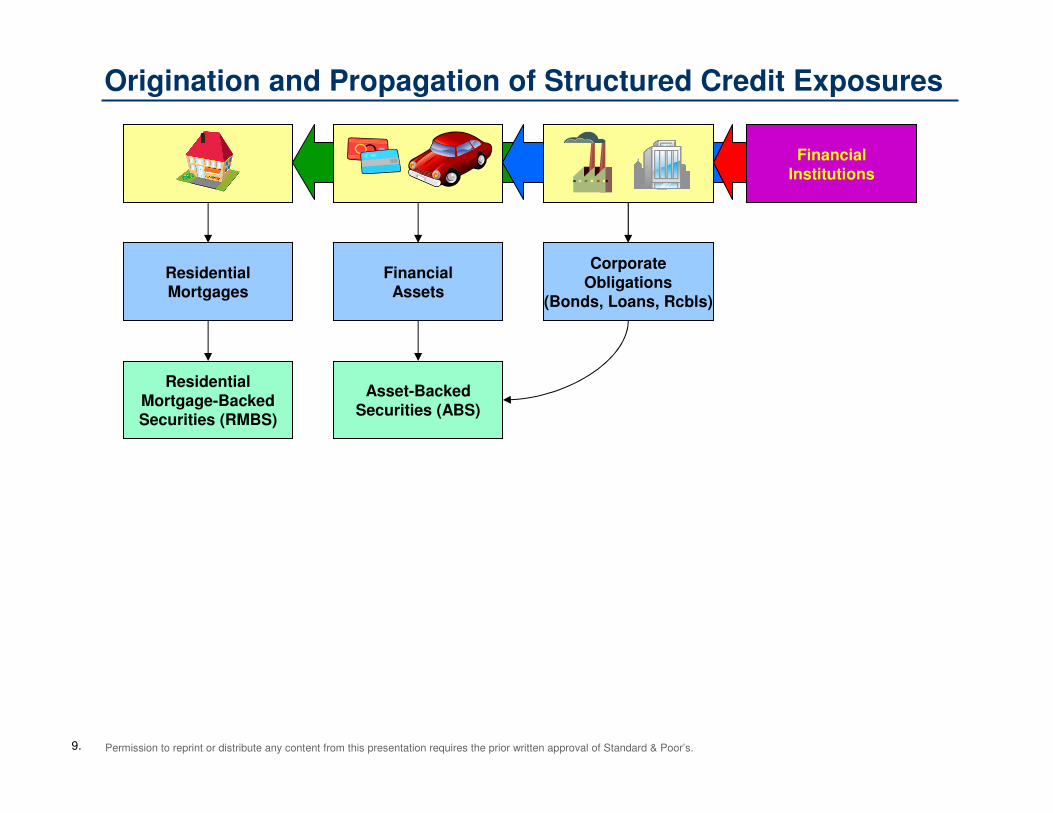

ResidentialMortgage-BackedSecurities (RMBS)

ResidentialMortgages

CorporateObligations

(Bonds, Loans, Rcbls)

Asset-BackedSecurities (ABS)

FinancialAssets

FinancialInstitutions

Origination and Propagation of Structured Credit Exposures

10. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

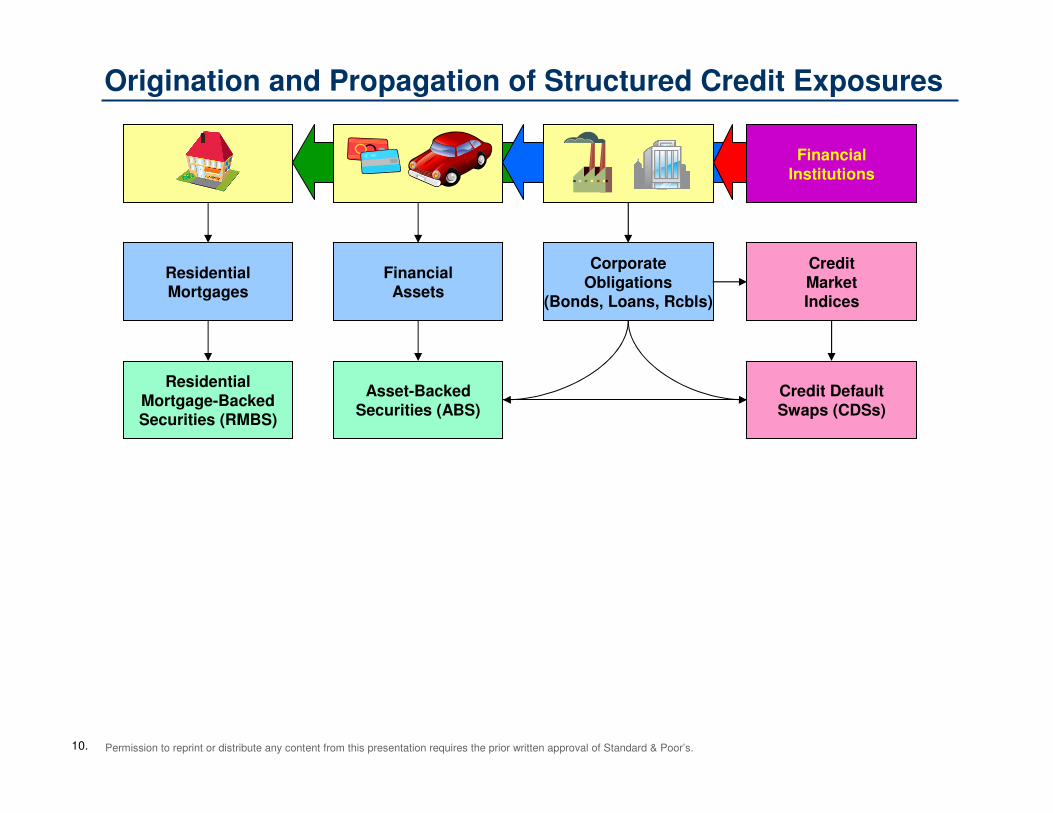

ResidentialMortgage-BackedSecurities (RMBS)

Credit DefaultSwaps (CDSs)

ResidentialMortgages

CorporateObligations

(Bonds, Loans, Rcbls)

CreditMarketIndices

Asset-BackedSecurities (ABS)

FinancialAssets

FinancialInstitutions

Origination and Propagation of Structured Credit Exposures

11. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

ResidentialMortgage-BackedSecurities (RMBS)

CollateralizedDebt Obligations

(CDOs)

Credit DefaultSwaps (CDSs)

Synthetic CDOs

ResidentialMortgages

CorporateObligations

(Bonds, Loans, Rcbls)

CreditMarketIndices

Asset-BackedSecurities (ABS)

FinancialAssets

CDO2

ABCPEtc.

FinancialInstitutions

Origination and Propagation of Structured Credit Exposures

12. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

ResidentialMortgage-BackedSecurities (RMBS)

CollateralizedDebt Obligations

(CDOs)

Credit DefaultSwaps (CDSs)

Synthetic CDOs

ResidentialMortgages

CorporateObligations

(Bonds, Loans, Rcbls)

CreditMarketIndices

Asset-BackedSecurities (ABS)

FinancialAssets

CDO2

ABCPEtc.

FinancialInstitutions

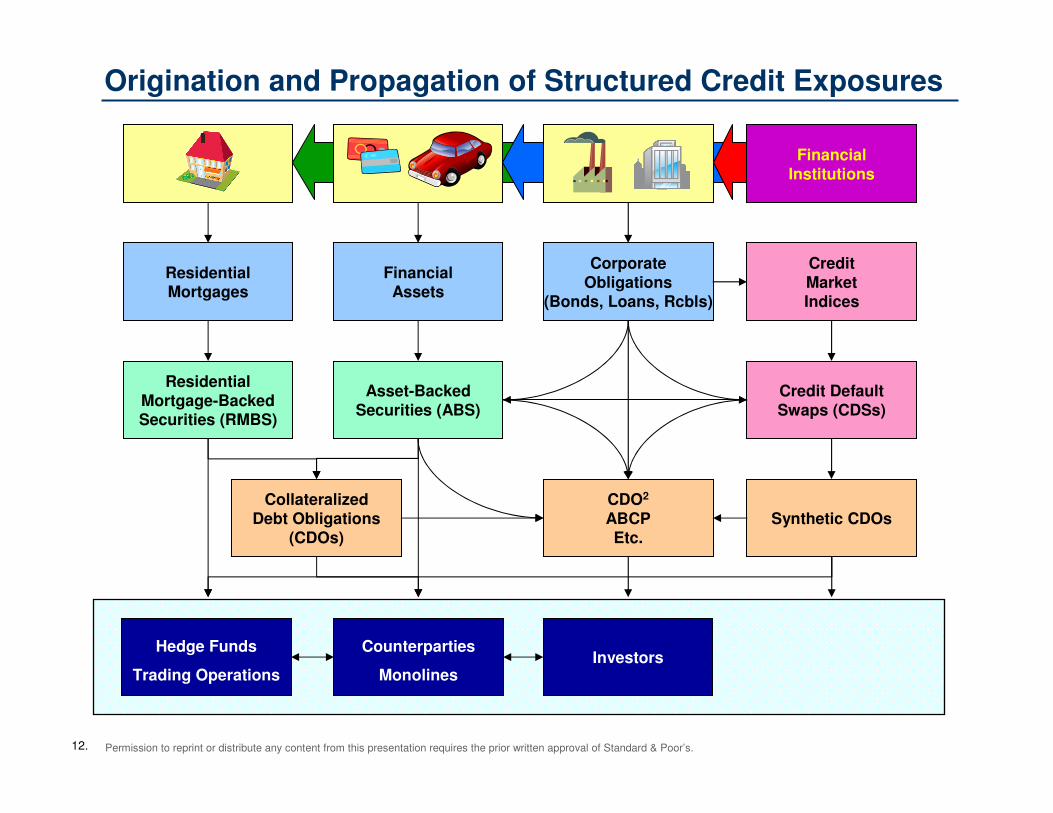

Origination and Propagation of Structured Credit Exposures

Counterparties

MonolinesInvestors

Hedge Funds

Trading Operations

13. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

ResidentialMortgage-BackedSecurities (RMBS)

CollateralizedDebt Obligations

(CDOs)

Credit DefaultSwaps (CDSs)

Synthetic CDOs

ResidentialMortgages

CorporateObligations

(Bonds, Loans, Rcbls)

CreditMarketIndices

Asset-BackedSecurities (ABS)

FinancialAssets

CDO2

ABCPEtc.

FinancialInstitutions

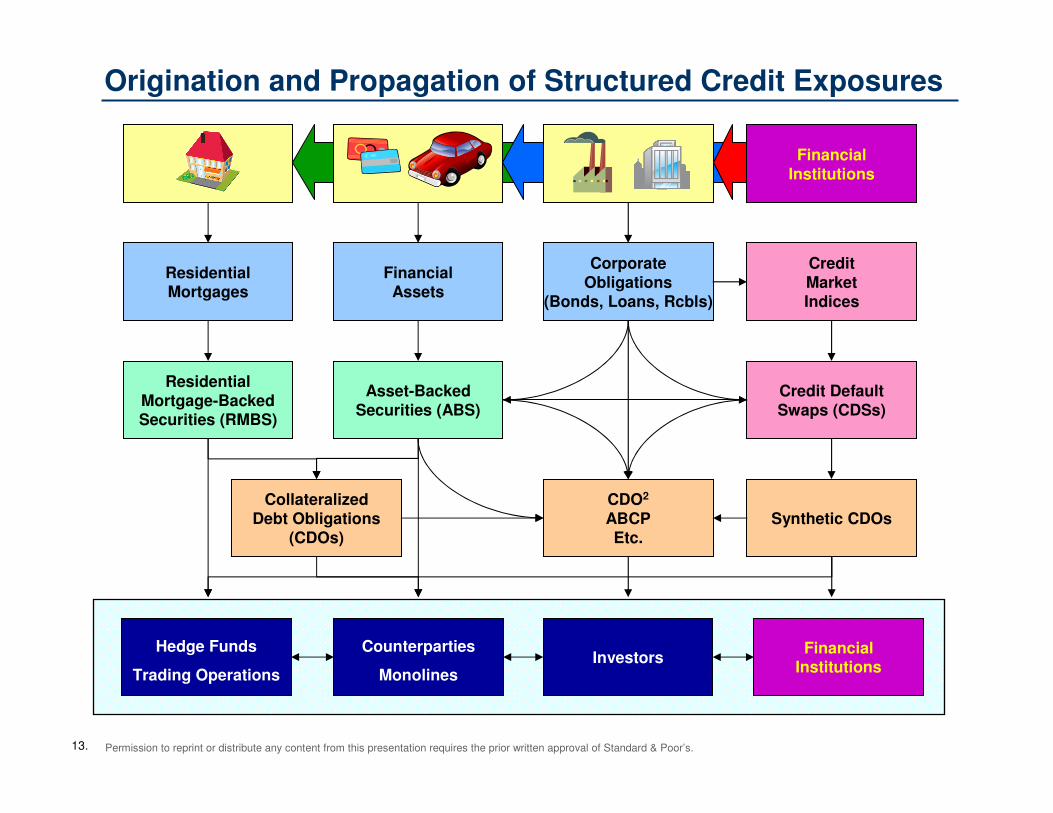

Origination and Propagation of Structured Credit Exposures

Counterparties

Monolines

FinancialInstitutions

InvestorsHedge Funds

Trading Operations

14. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

ResidentialMortgage-BackedSecurities (RMBS)

CollateralizedDebt Obligations

(CDOs)

Credit DefaultSwaps (CDSs)

Synthetic CDOs

ResidentialMortgages

CorporateObligations

(Bonds, Loans, Rcbls)

CreditMarketIndices

Asset-BackedSecurities (ABS)

FinancialAssets

CDO2

ABCPEtc.

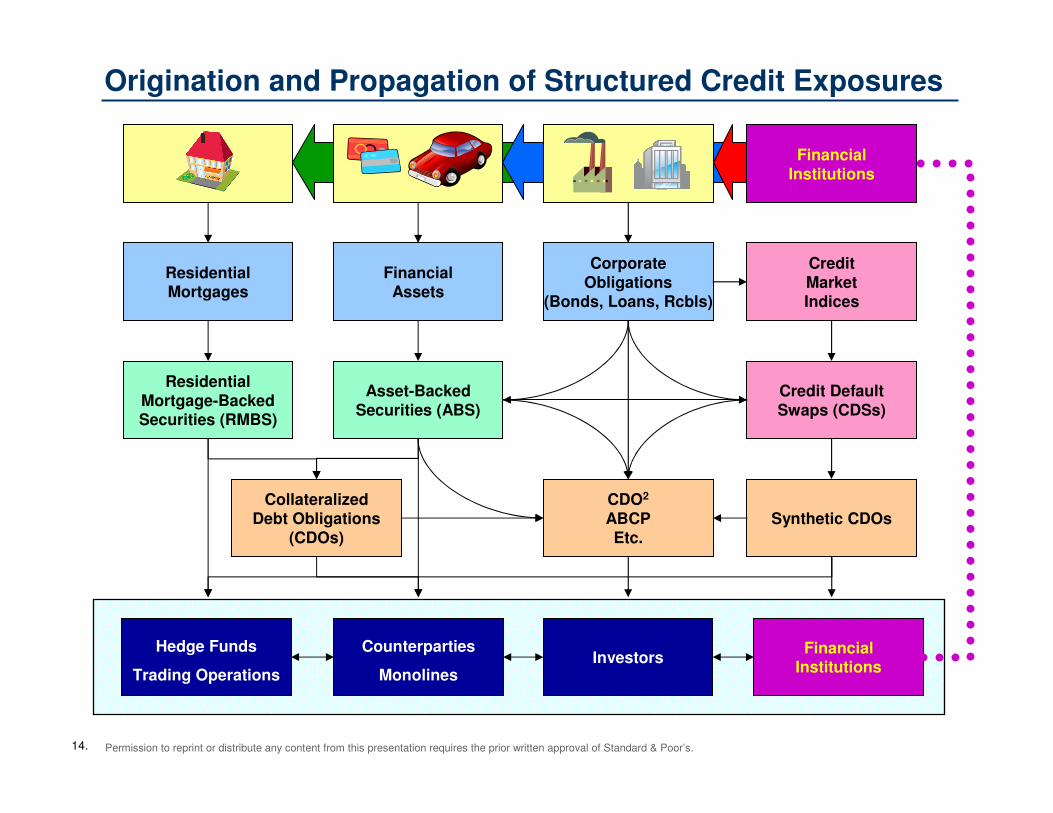

FinancialInstitutions

Origination and Propagation of Structured Credit Exposures

Counterparties

Monolines

FinancialInstitutions

InvestorsHedge Funds

Trading Operations

15. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

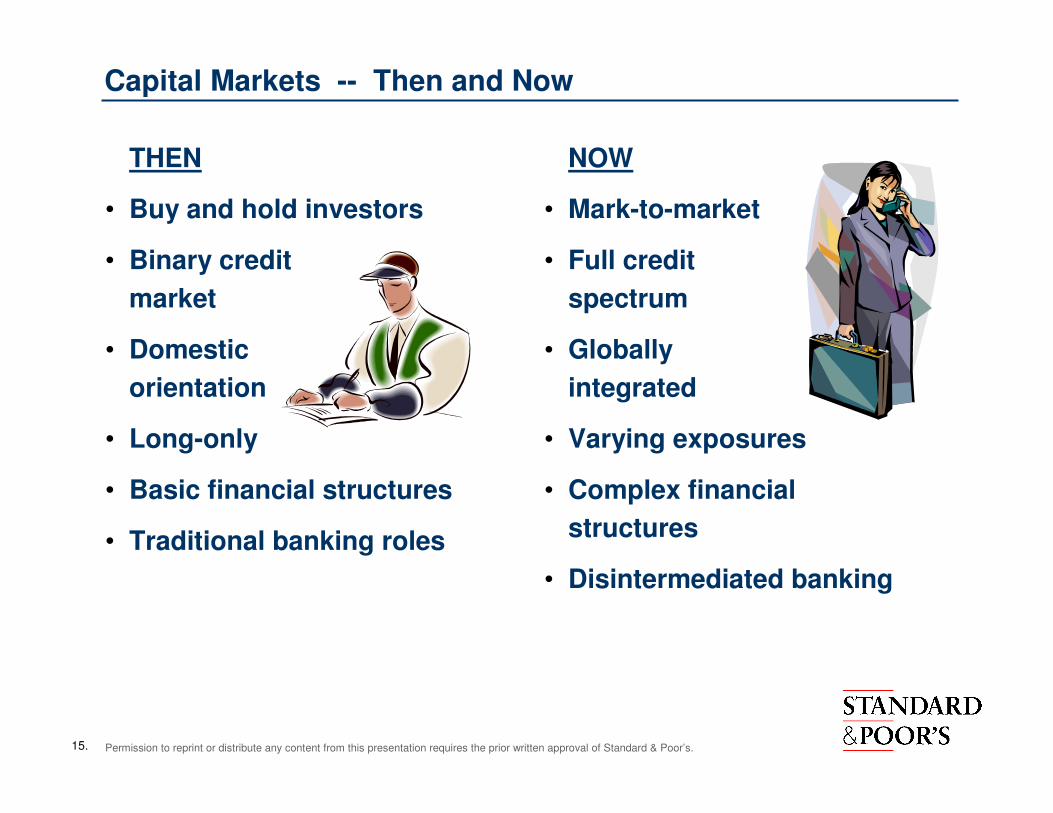

Capital Markets -- Then and Now

THEN

• Buy and hold investors

• Binary credit

market

• Domestic

orientation

• Long-only

• Basic financial structures

• Traditional banking roles

NOW

• Mark-to-market

• Full credit

spectrum

• Globally

integrated

• Varying exposures

• Complex financial

structures

• Disintermediated banking

16. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Credit Crunch: Aspects and Outcomes

17. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Global Credit Turmoil: Underlying Performance Drivers

• Overall environment: expanding market appetite for risk;

declining risk spreads (2003 through mid-2007)

• 2006/2007: sub-prime mortgage securitization performance

deterioration and rating actions

• Mid-2007: widespread reassessment of risk tolerances,

prompted by U.S. sub-prime RMBS performance

• Consequential (e.g. mark-to-market) impact on structured credit

vehicles and financial intermediaries (banks, hedge funds, bond

insurers, etc.)

• Canadian market impact: primarily ABCP, and entities with

related exposures

18. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

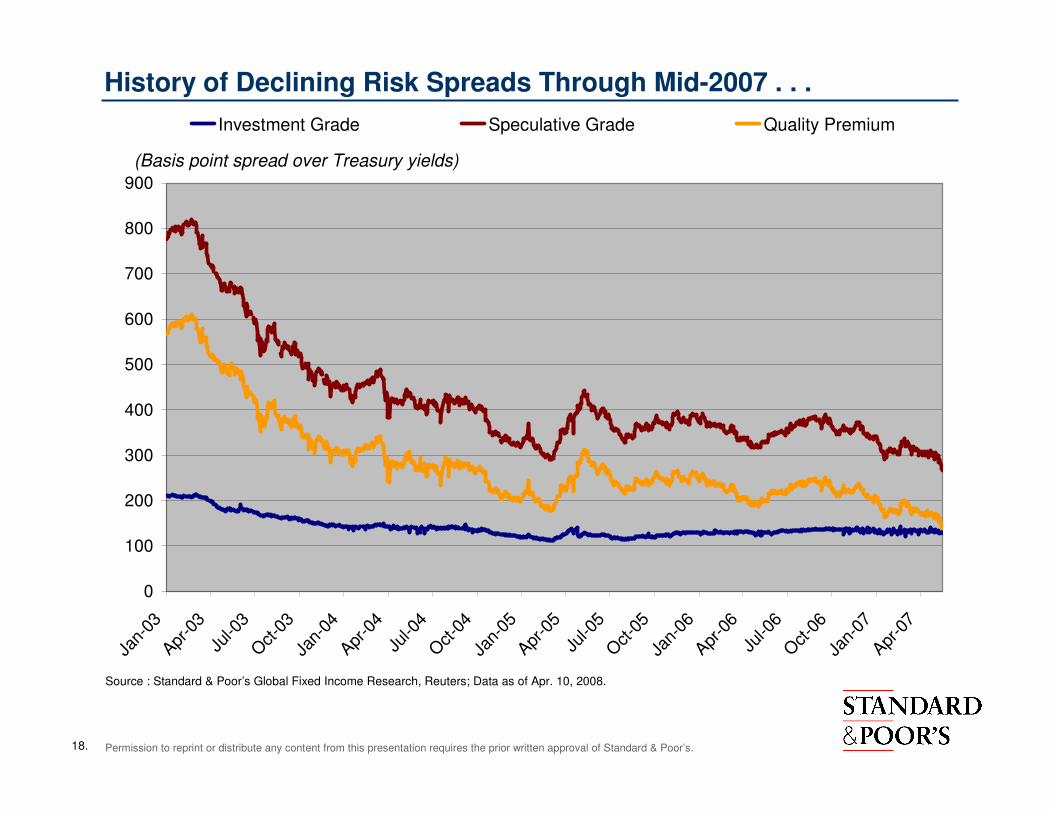

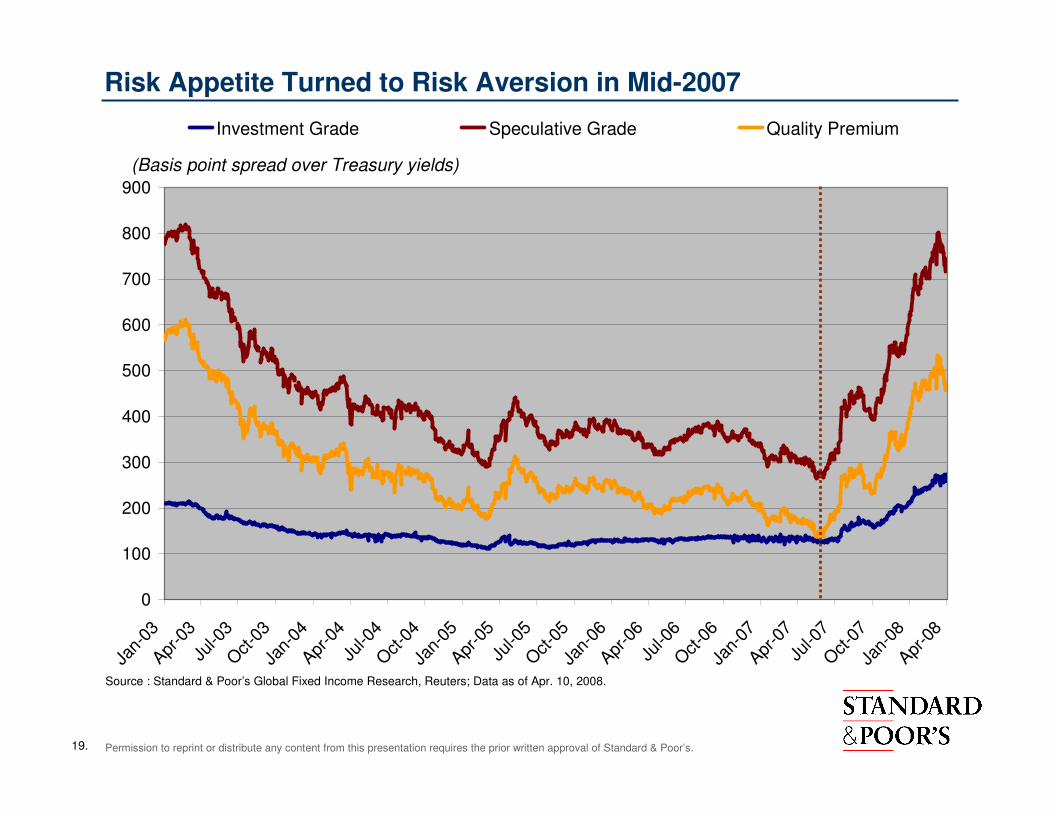

History of Declining Risk Spreads Through Mid-2007 . . .

Source : Standard & Poor’s Global Fixed Income Research, Reuters; Data as of Apr. 10, 2008.

0

100

200

300

400

500

600

700

800

900

Jan-

03Apr

-03

Jul-0

3O

ct-0

3Ja

n-04

Apr-0

4Ju

l-04

Oct

-04

Jan-

05Apr

-05

Jul-0

5O

ct-0

5Ja

n-06

Apr-0

6Ju

l-06

Oct

-06

Jan-

07Apr

-07

Investment Grade Speculative Grade Quality Premium

(Basis point spread over Treasury yields)

19. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Risk Appetite Turned to Risk Aversion in Mid-2007

Source : Standard & Poor’s Global Fixed Income Research, Reuters; Data as of Apr. 10, 2008.

0

100

200

300

400

500

600

700

800

900

Jan-

03Apr

-03

Jul-0

3O

ct-0

3Ja

n-04

Apr-0

4Ju

l-04

Oct

-04

Jan-

05Apr

-05

Jul-0

5O

ct-0

5Ja

n-06

Apr-0

6Ju

l-06

Oct

-06

Jan-

07Apr

-07

Jul-0

7O

ct-0

7Ja

n-08

Apr-0

8Investment Grade Speculative Grade Quality Premium

(Basis point spread over Treasury yields)

20. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

0

200

400

600

800

1,000

1,200

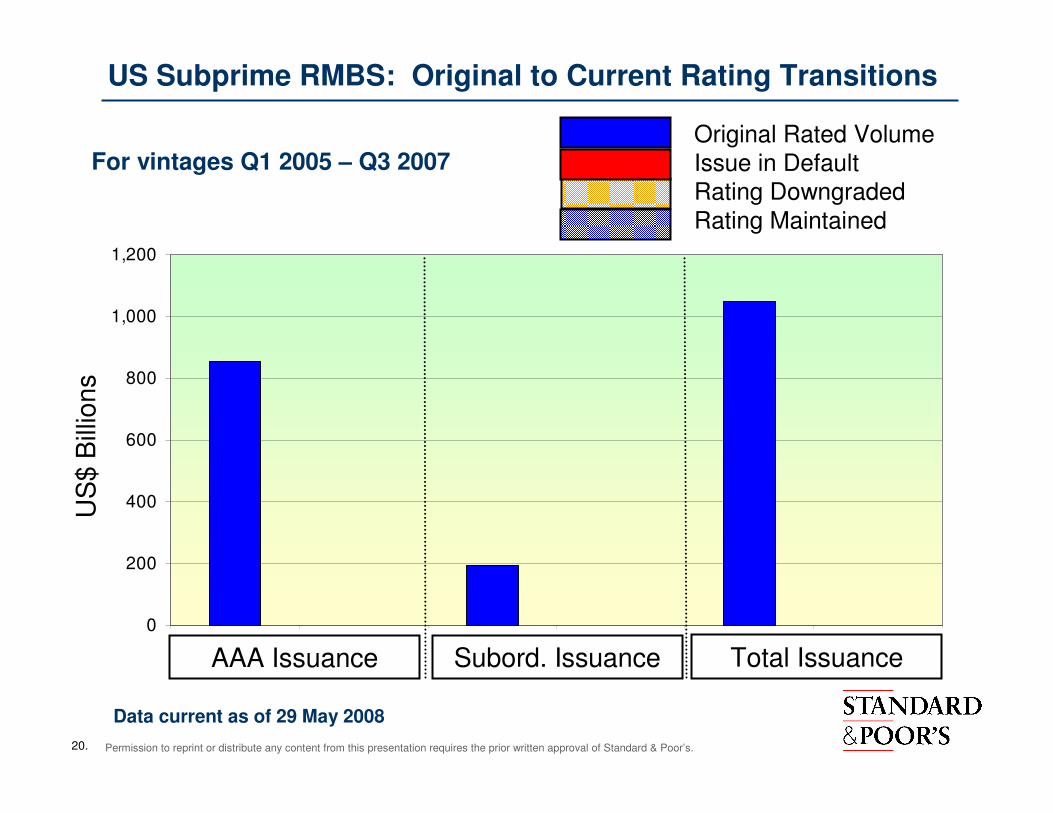

US Subprime RMBS: Original to Current Rating Transitions

For vintages Q1 2005 – Q3 2007

AAA Issuance Subord. Issuance Total Issuance

US

$ B

illio

ns

Data current as of 29 May 2008

Original Rated VolumeIssue in DefaultRating DowngradedRating Maintained

21. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

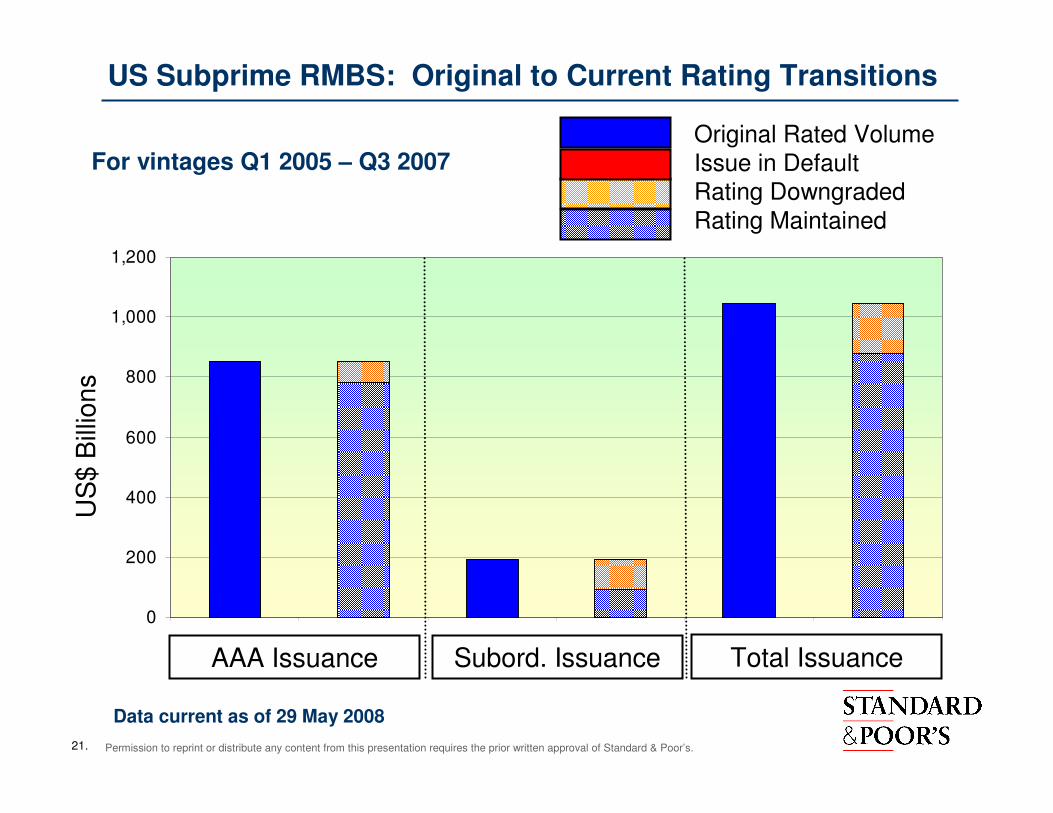

US Subprime RMBS: Original to Current Rating Transitions

0

200

400

600

800

1,000

1,200

AAA AAA' Subord Subord' Total Total'

For vintages Q1 2005 – Q3 2007Original Rated VolumeIssue in DefaultRating DowngradedRating Maintained

AAA Issuance Subord. Issuance Total Issuance

US

$ B

illio

ns

Data current as of 29 May 2008

22. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

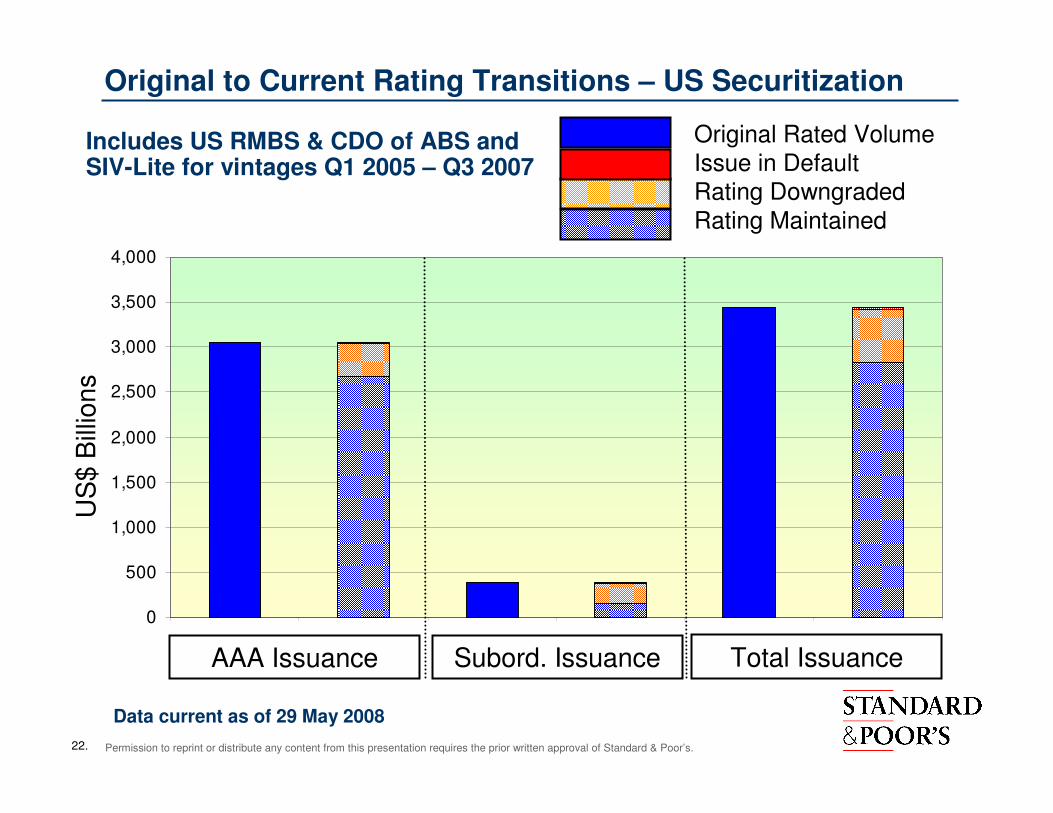

Original to Current Rating Transitions – US Securitization

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1 2 3 4 5 6

Includes US RMBS & CDO of ABS and SIV-Lite for vintages Q1 2005 – Q3 2007

US

$ B

illio

ns

AAA Issuance Subord. Issuance Total Issuance

Data current as of 29 May 2008

Original Rated VolumeIssue in DefaultRating DowngradedRating Maintained

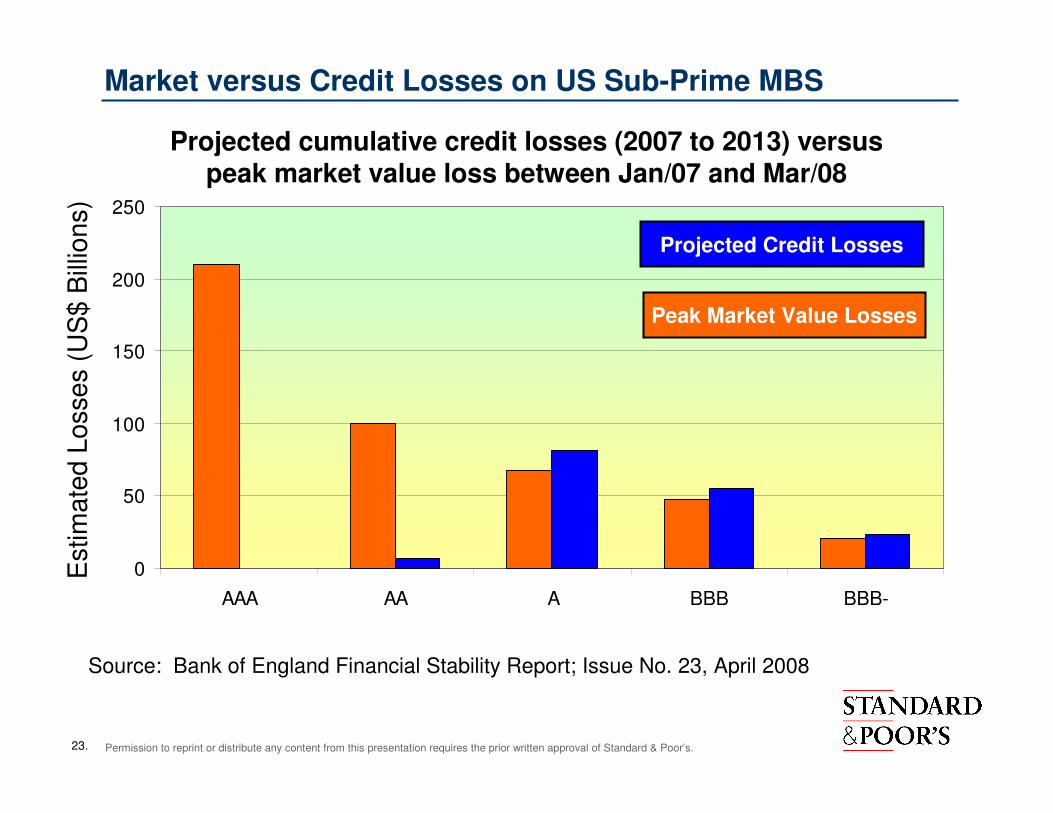

23. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Market versus Credit Losses on US Sub-Prime MBS

0

50

100

150

200

250

AAA AA A BBB BBB-

Estim

ate

d L

osse

s (

US

$ B

illio

ns)

Peak Market Value Losses

Projected Credit Losses

Source: Bank of England Financial Stability Report; Issue No. 23, April 2008

Projected cumulative credit losses (2007 to 2013) versuspeak market value loss between Jan/07 and Mar/08

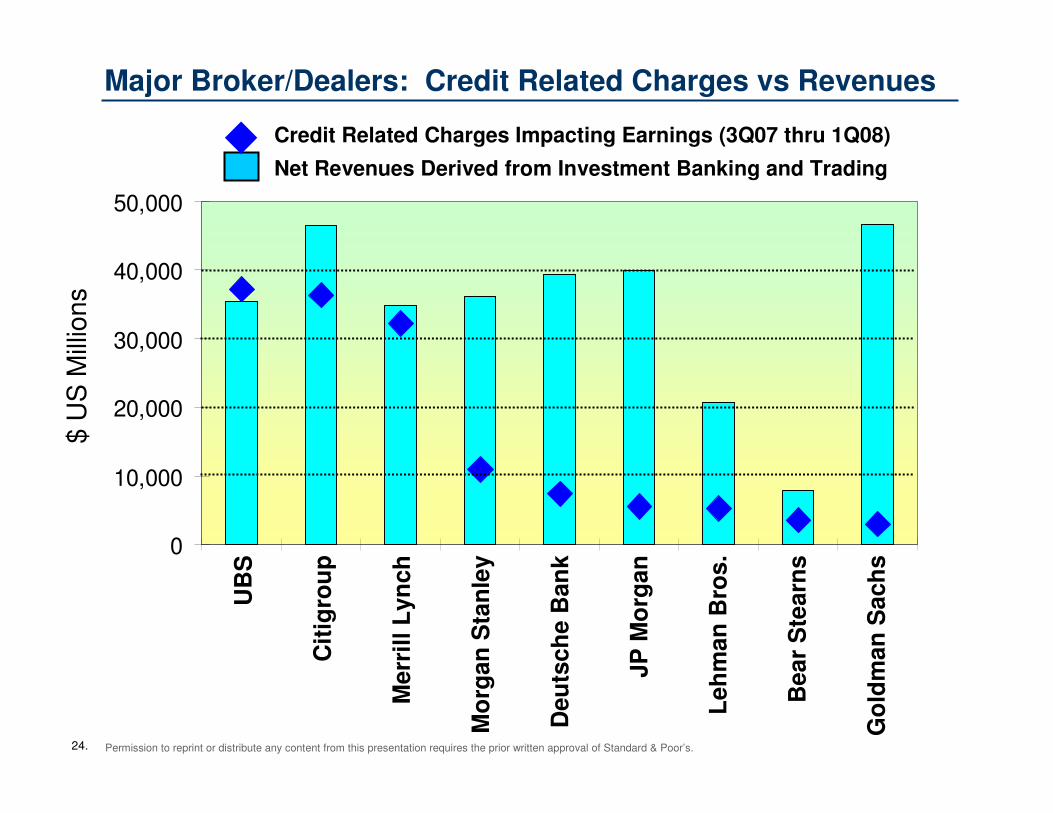

24. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Major Broker/Dealers: Credit Related Charges vs Revenues

0

10,000

20,000

30,000

40,000

50,000

UB

S

Cit

igro

up

Merr

ill

Lyn

ch

Mo

rgan

Sta

nle

y

Deu

tsch

e B

an

k

JP

Mo

rgan

Leh

man

Bro

s.

Bear

Ste

arn

s

Go

ldm

an

Sach

s

$ U

S M

illio

ns

Credit Related Charges Impacting Earnings (3Q07 thru 1Q08)

Net Revenues Derived from Investment Banking and Trading

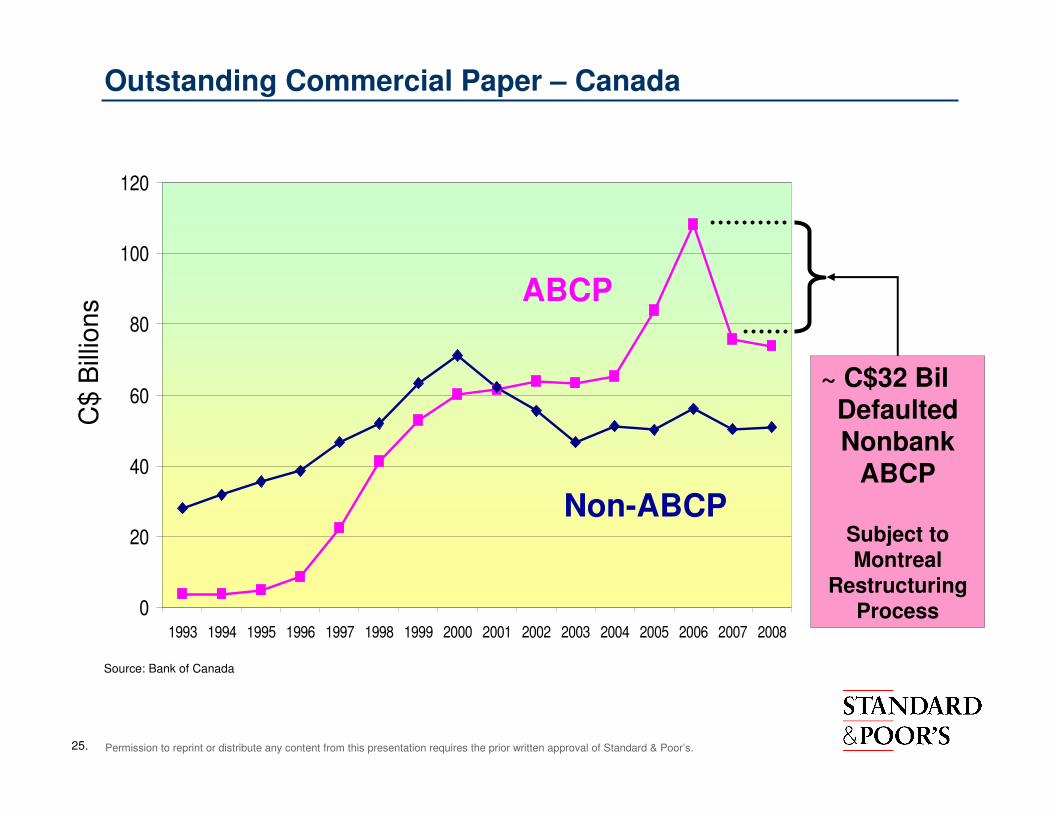

25. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Outstanding Commercial Paper – Canada

Source: Bank of Canada

0

20

40

60

80

100

120

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Non-ABCP

ABCP

C$

Bill

ion

s

~ C$32 BilDefaultedNonbank

ABCP

Subject toMontreal

RestructuringProcess

26. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Lessons from the Credit Crunch

27. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Lessons Learned: Capital Markets Overall

• Tendencies in “new” financial industry for excessive leverage and

risk creation

• Challenges of risk management practices in complex,

interdependent financial system

• Heightened emphasis on transparency

• Challenges of liquidity management in global capital markets

• Implications of fair value accounting

• Role of credit ratings and related analytics versus in-house risk

review processes

28. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

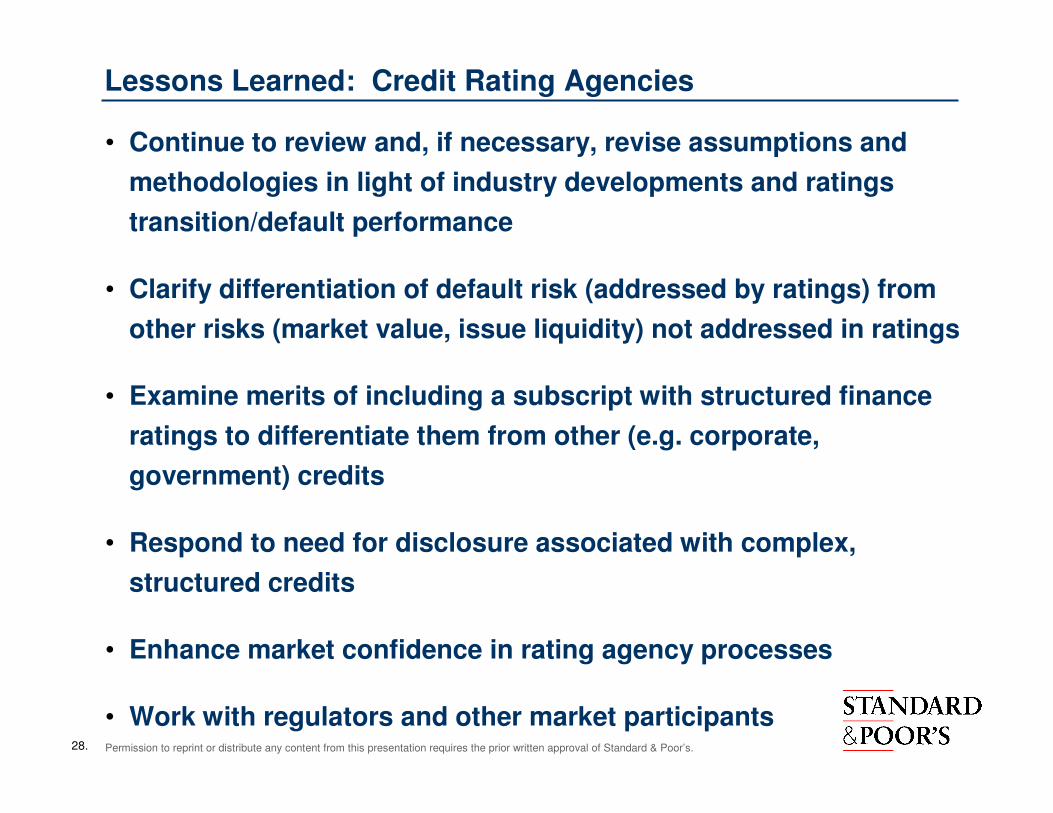

Lessons Learned: Credit Rating Agencies

• Continue to review and, if necessary, revise assumptions and

methodologies in light of industry developments and ratings

transition/default performance

• Clarify differentiation of default risk (addressed by ratings) from

other risks (market value, issue liquidity) not addressed in ratings

• Examine merits of including a subscript with structured finance

ratings to differentiate them from other (e.g. corporate,

government) credits

• Respond to need for disclosure associated with complex,

structured credits

• Enhance market confidence in rating agency processes

• Work with regulators and other market participants

29. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

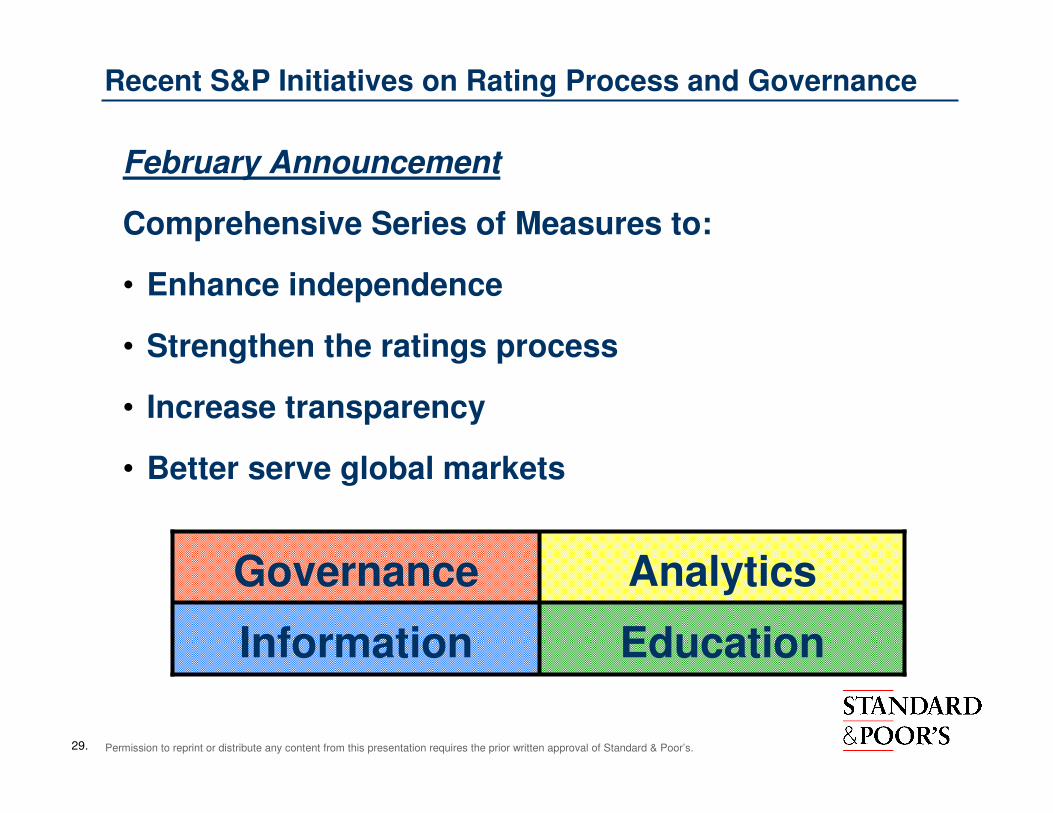

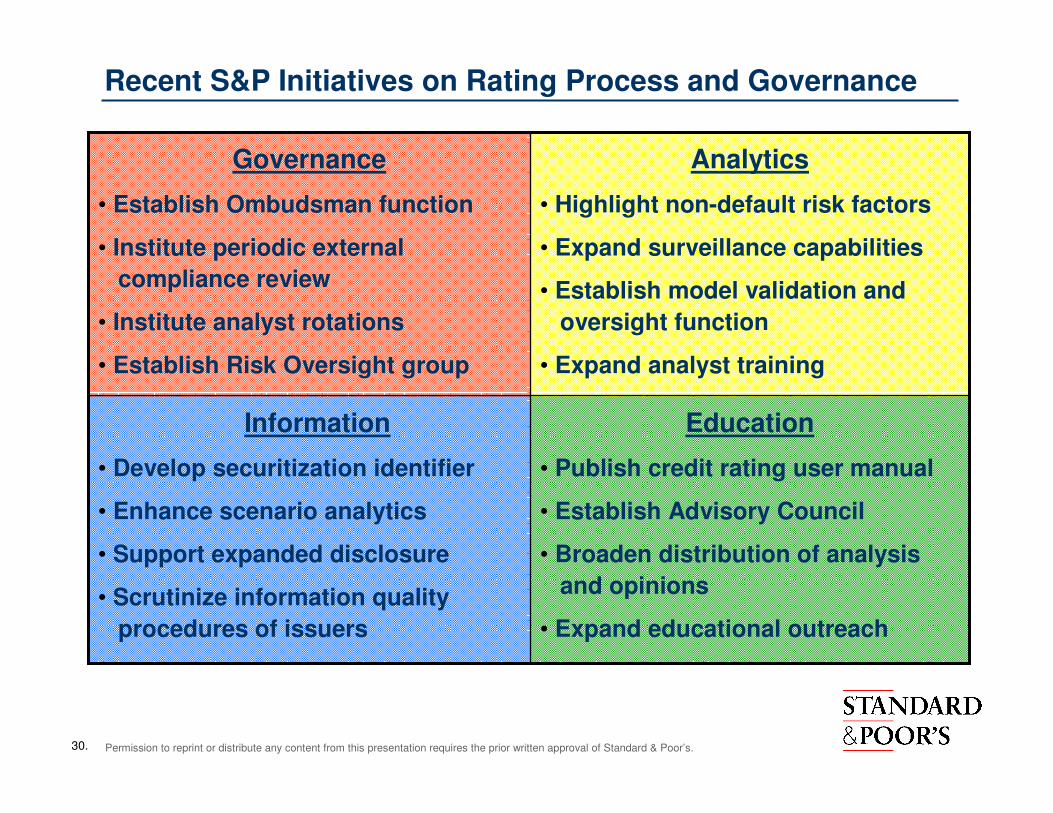

Recent S&P Initiatives on Rating Process and Governance

February Announcement

Comprehensive Series of Measures to:

• Enhance independence

• Strengthen the ratings process

• Increase transparency

• Better serve global markets

EducationInformation

AnalyticsGovernance

30. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Recent S&P Initiatives on Rating Process and Governance

Education

• Publish credit rating user manual

• Establish Advisory Council

• Broaden distribution of analysis

and opinions

• Expand educational outreach

Information

• Develop securitization identifier

• Enhance scenario analytics

• Support expanded disclosure

• Scrutinize information quality

procedures of issuers

Analytics

• Highlight non-default risk factors

• Expand surveillance capabilities

• Establish model validation and

oversight function

• Expand analyst training

Governance

• Establish Ombudsman function

• Institute periodic external

compliance review

• Institute analyst rotations

• Establish Risk Oversight group

31. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Credit Outlook

32. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

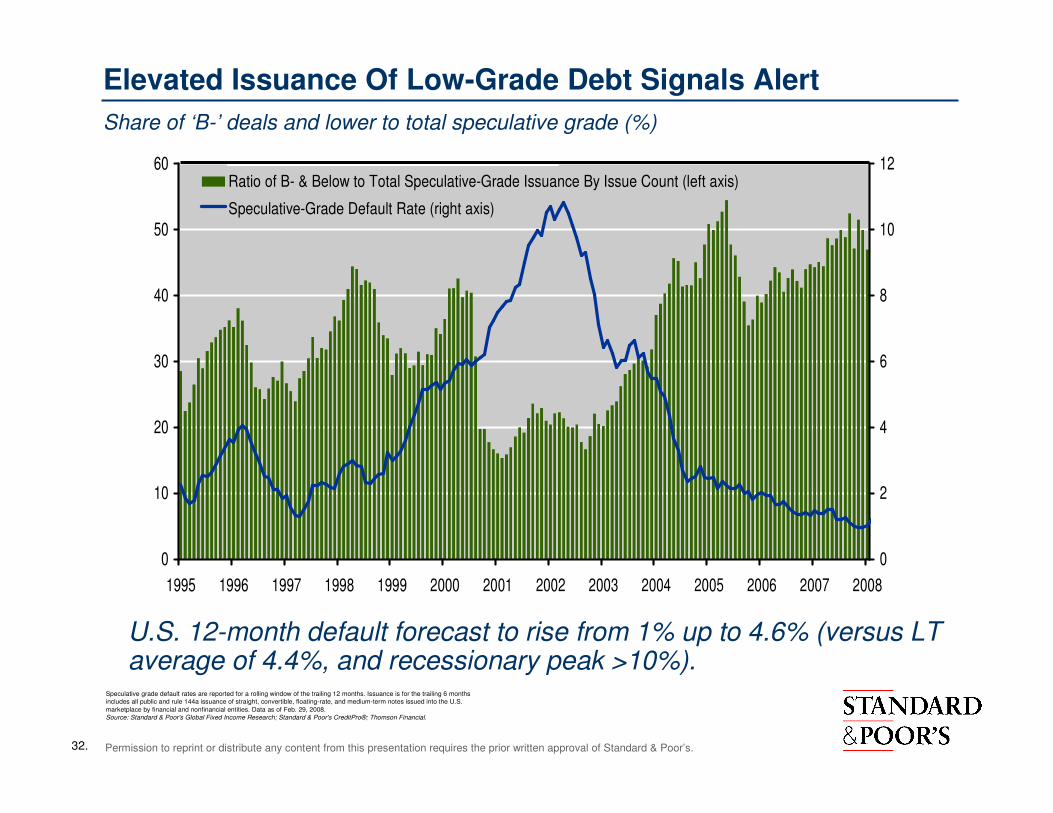

Elevated Issuance Of Low-Grade Debt Signals Alert

Share of ‘B-’ deals and lower to total speculative grade (%)

U.S. 12-month default forecast to rise from 1% up to 4.6% (versus LT average of 4.4%, and recessionary peak >10%).

0

10

20

30

40

50

60

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

0

2

4

6

8

10

12Speculative-Grade Default Rate (right axis)

Ratio of B- & Below to Total Speculative-Grade Issuance By Issue Count (left axis)

Speculative-Grade Default Rate (right axis)

Speculative grade default rates are reported for a rolling window of the trailing 12 months. Issuance is for the trailing 6 months includes all public and rule 144a issuance of straight, convertible, floating-rate, and medium-term notes issued into the U.S.

marketplace by financial and nonfinancial entities. Data as of Feb. 29, 2008.Source: Standard & Poor's Global Fixed Income Research; Standard & Poor's CreditPro®; Thomson Financial.

33. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

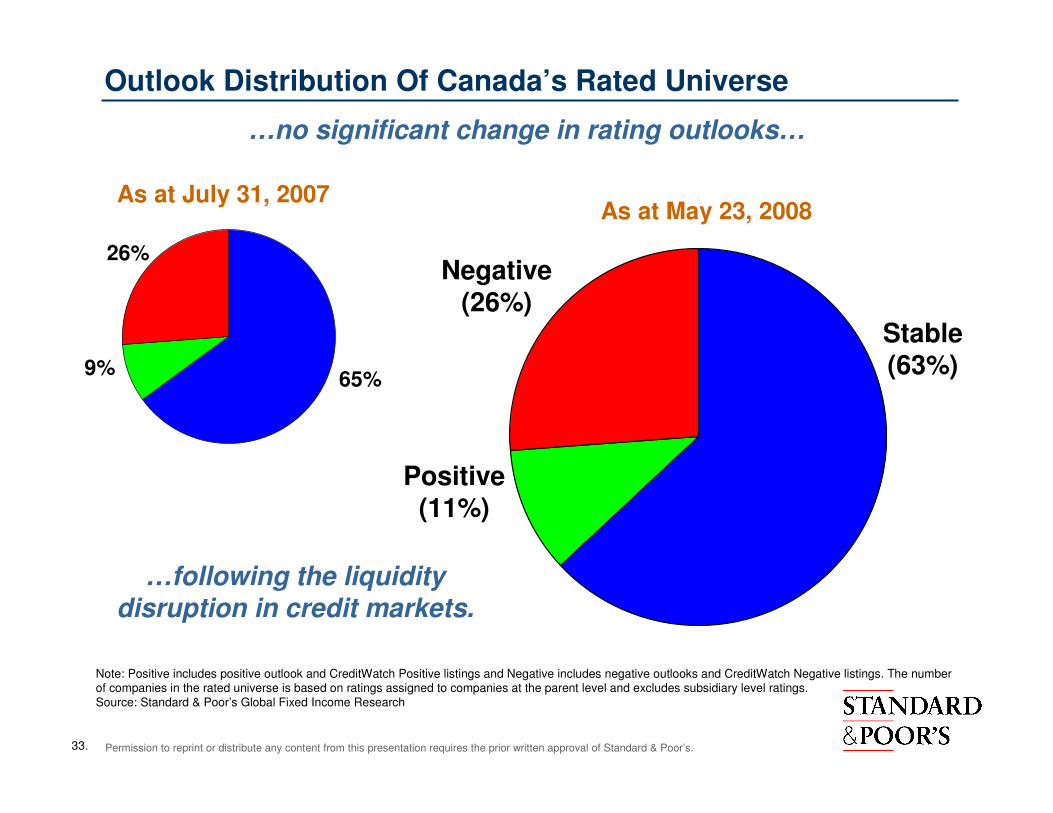

Outlook Distribution Of Canada’s Rated Universe

…no significant change in rating outlooks…

As at July 31, 2007As at May 23, 2008

…following the liquiditydisruption in credit markets.

Note: Positive includes positive outlook and CreditWatch Positive listings and Negative includes negative outlooks and CreditWatch Negative listings. The number of companies in the rated universe is based on ratings assigned to companies at the parent level and excludes subsidiary level ratings.Source: Standard & Poor’s Global Fixed Income Research

Negative(26%)

Stable(63%)

Positive(11%)

26%

9%65%

34. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

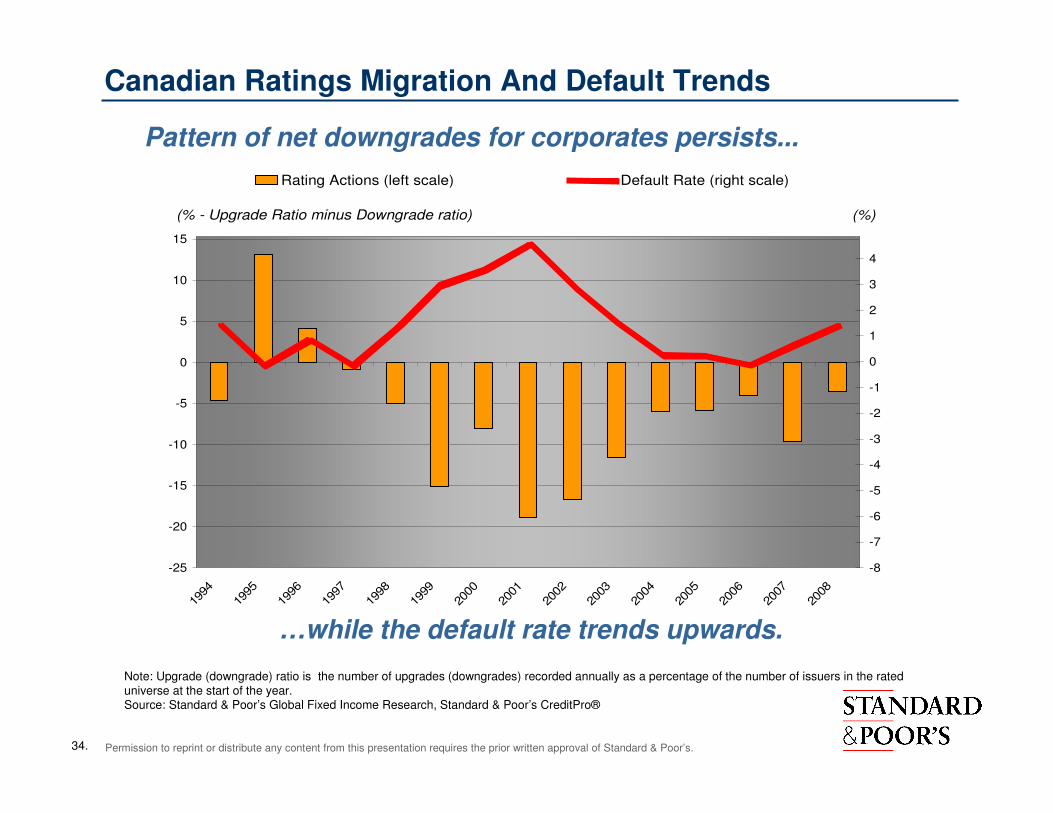

Canadian Ratings Migration And Default Trends

Note: Upgrade (downgrade) ratio is the number of upgrades (downgrades) recorded annually as a percentage of the number of issuers in the rated universe at the start of the year. Source: Standard & Poor’s Global Fixed Income Research, Standard & Poor’s CreditPro®

Pattern of net downgrades for corporates persists...

…while the default rate trends upwards.

-25

-20

-15

-10

-5

0

5

10

15

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

Rating Actions (left scale) Default Rate (right scale)

(% - Upgrade Ratio minus Downgrade ratio) (%)

35. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

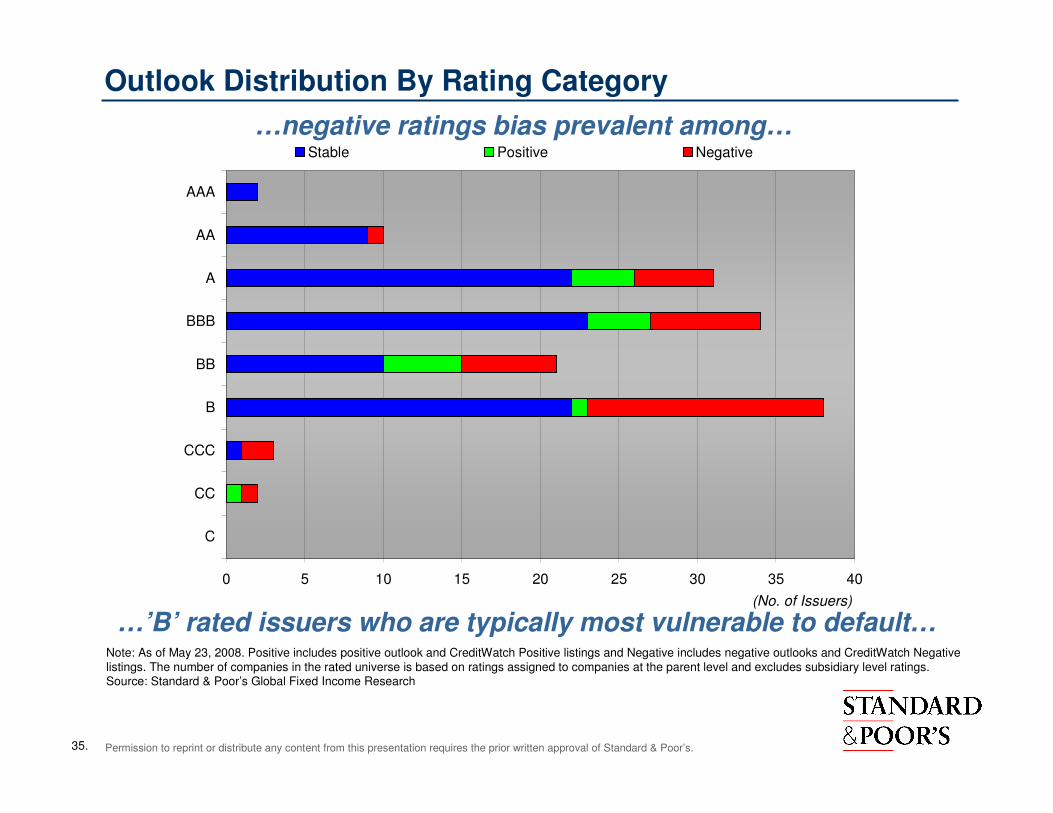

Outlook Distribution By Rating Category

…’B’ rated issuers who are typically most vulnerable to default…

…negative ratings bias prevalent among…

Note: As of May 23, 2008. Positive includes positive outlook and CreditWatch Positive listings and Negative includes negative outlooks and CreditWatch Negative listings. The number of companies in the rated universe is based on ratings assigned to companies at the parent level and excludes subsidiary level ratings.Source: Standard & Poor’s Global Fixed Income Research

0 5 10 15 20 25 30 35 40

AAA

AA

A

BBB

BB

B

CCC

CC

C

Stable Positive Negative

(No. of Issuers)

36. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

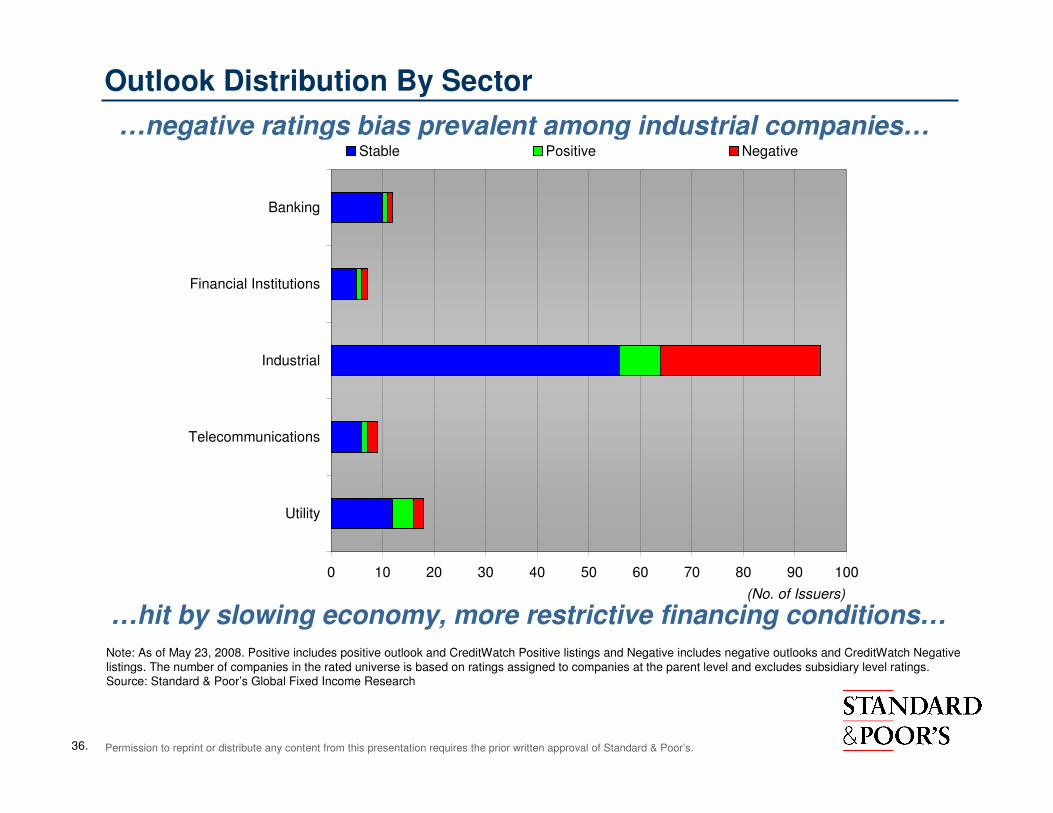

Outlook Distribution By Sector

Note: As of May 23, 2008. Positive includes positive outlook and CreditWatch Positive listings and Negative includes negative outlooks and CreditWatch Negative listings. The number of companies in the rated universe is based on ratings assigned to companies at the parent level and excludes subsidiary level ratings.Source: Standard & Poor’s Global Fixed Income Research

…negative ratings bias prevalent among industrial companies…

…hit by slowing economy, more restrictive financing conditions…

0 10 20 30 40 50 60 70 80 90 100

Banking

Financial Institutions

Industrial

Telecommunications

Utility

Stable Positive Negative

(No. of Issuers)

37. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

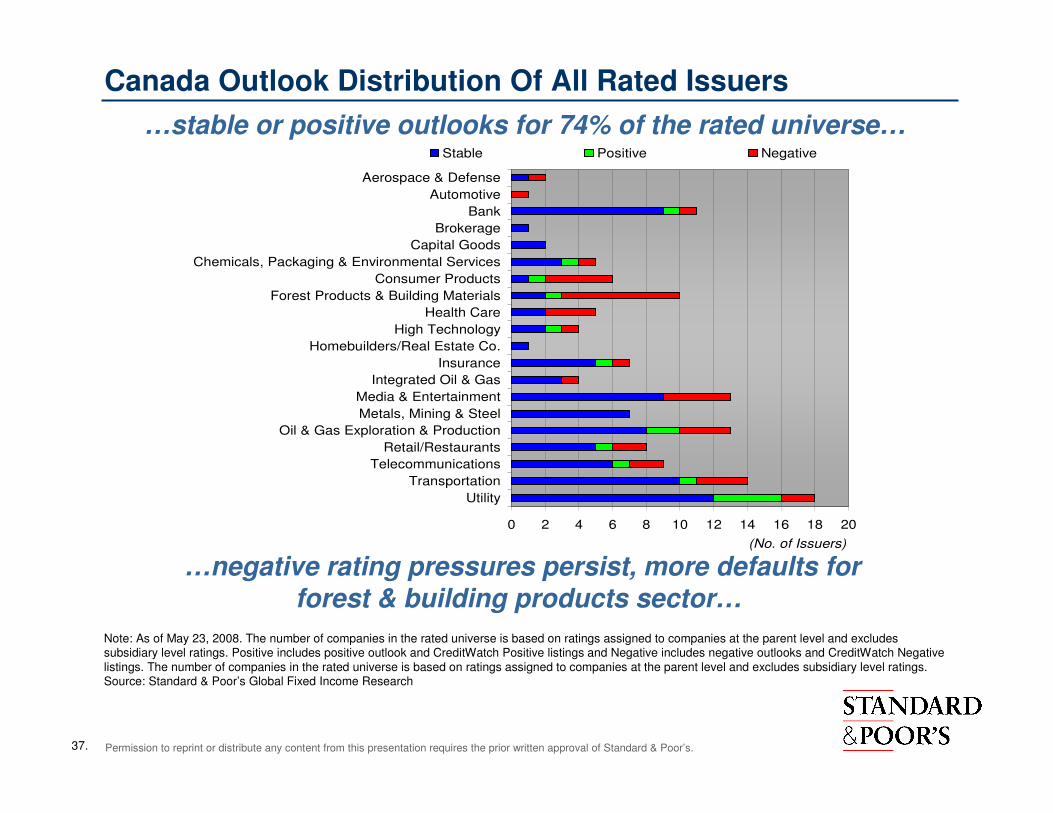

Canada Outlook Distribution Of All Rated Issuers

…stable or positive outlooks for 74% of the rated universe…

…negative rating pressures persist, more defaults for forest & building products sector…

Note: As of May 23, 2008. The number of companies in the rated universe is based on ratings assigned to companies at the parent level and excludes subsidiary level ratings. Positive includes positive outlook and CreditWatch Positive listings and Negative includes negative outlooks and CreditWatch Negative listings. The number of companies in the rated universe is based on ratings assigned to companies at the parent level and excludes subsidiary level ratings. Source: Standard & Poor’s Global Fixed Income Research

0 2 4 6 8 10 12 14 16 18 20

Aerospace & Defense

Automotive

Bank

Brokerage

Capital Goods

Chemicals, Packaging & Environmental Services

Consumer Products

Forest Products & Building Materials

Health Care

High Technology

Homebuilders/Real Estate Co.

Insurance

Integrated Oil & Gas

Media & Entertainment

Metals, Mining & Steel

Oil & Gas Exploration & Production

Retail/Restaurants

Telecommunications

Transportation

Utility

Stable Positive Negative

(No. of Issuers)

38. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

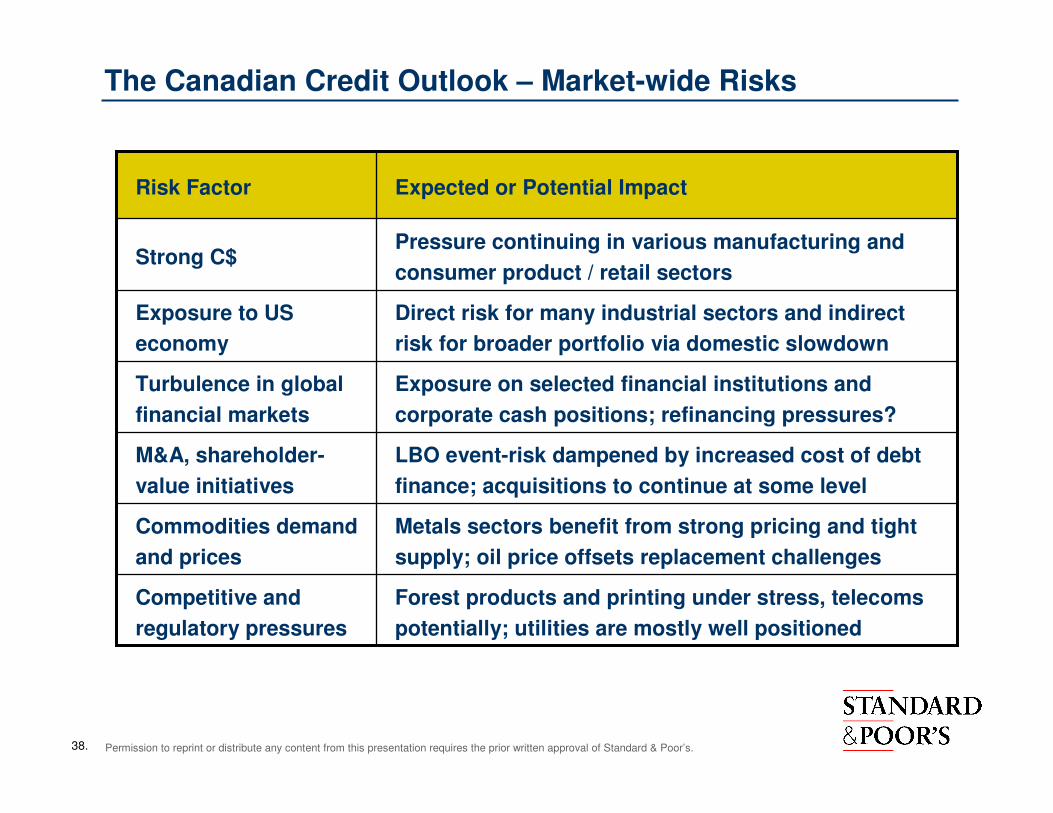

The Canadian Credit Outlook – Market-wide Risks

Direct risk for many industrial sectors and indirect

risk for broader portfolio via domestic slowdown

Exposure to US

economy

Forest products and printing under stress, telecoms

potentially; utilities are mostly well positioned

Competitive and

regulatory pressures

Metals sectors benefit from strong pricing and tight

supply; oil price offsets replacement challenges

Commodities demand

and prices

LBO event-risk dampened by increased cost of debt

finance; acquisitions to continue at some level

M&A, shareholder-

value initiatives

Exposure on selected financial institutions and

corporate cash positions; refinancing pressures?

Turbulence in global

financial markets

Pressure continuing in various manufacturing and

consumer product / retail sectorsStrong C$

Expected or Potential ImpactRisk Factor

39. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Just about finished . . .

40. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Key Take-Aways

• Recent credit turmoil reflects adaptation to the more integrated

global capital market that has rapidly embraced complex

technical tools

• Lessons learned from recent experience will strengthen

foundation of global capital markets

• Uncertain when turmoil will subside; possibly in transition to

more conventional credit downturn

• We expect future Canadian credit cycle development will reflect

US economy, among other factors

• S&P governance and process reforms designed to improve

transparency and build greater market confidence in credit

ratings coverage

41. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Analytic services and products provided by Standard & Poor’s are the result of separate activities designed to preserve the independence and objectivity of each analytic process. Standard & Poor’s has established policies and procedures to maintain the confidentiality of non-public information received during each analytic process.

www.standardandpoors.com

![Credit Crunch[1]](https://img.dokumen.tips/doc/110x75/577d22941a28ab4e1e97c86e/credit-crunch1.jpg)