Embed Size (px)

DESCRIPTION

case solution ranabaxy daichi

Citation preview

Ranbaxy Daiichi Sankyo Merger

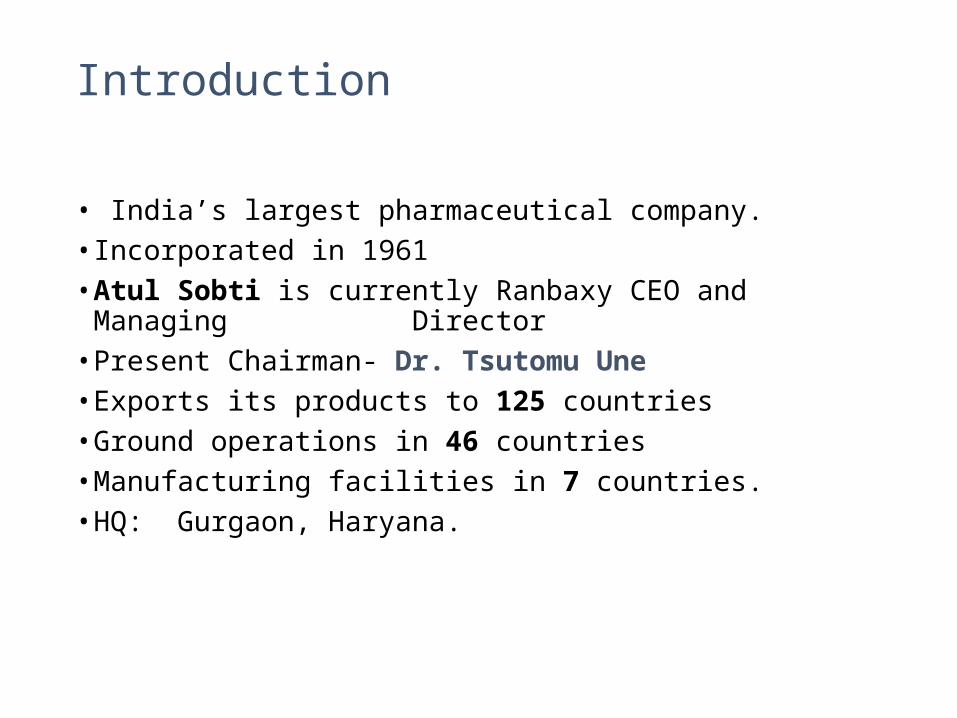

Introduction

• India’s largest pharmaceutical company.• Incorporated in 1961• Atul Sobti is currently Ranbaxy CEO and Managing Director• Present Chairman- Dr. Tsutomu Une• Exports its products to 125 countries • Ground operations in 46 countries • Manufacturing facilities in 7 countries. • HQ: Gurgaon, Haryana.

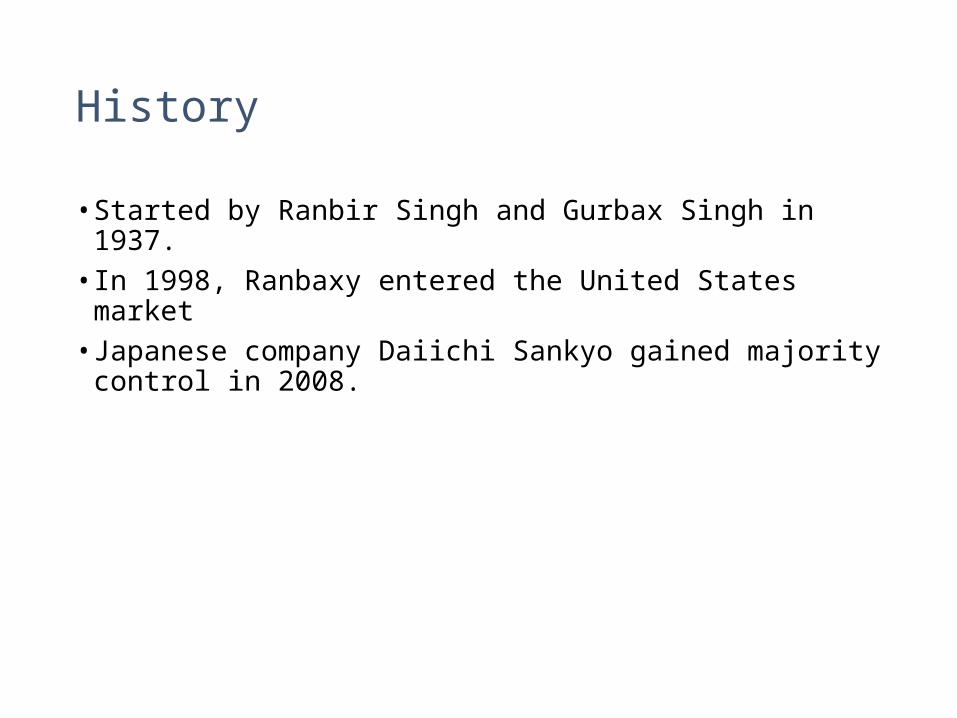

History

• Started by Ranbir Singh and Gurbax Singh in 1937.• In 1998, Ranbaxy entered the United States market• Japanese company Daiichi Sankyo gained majority control in 2008.

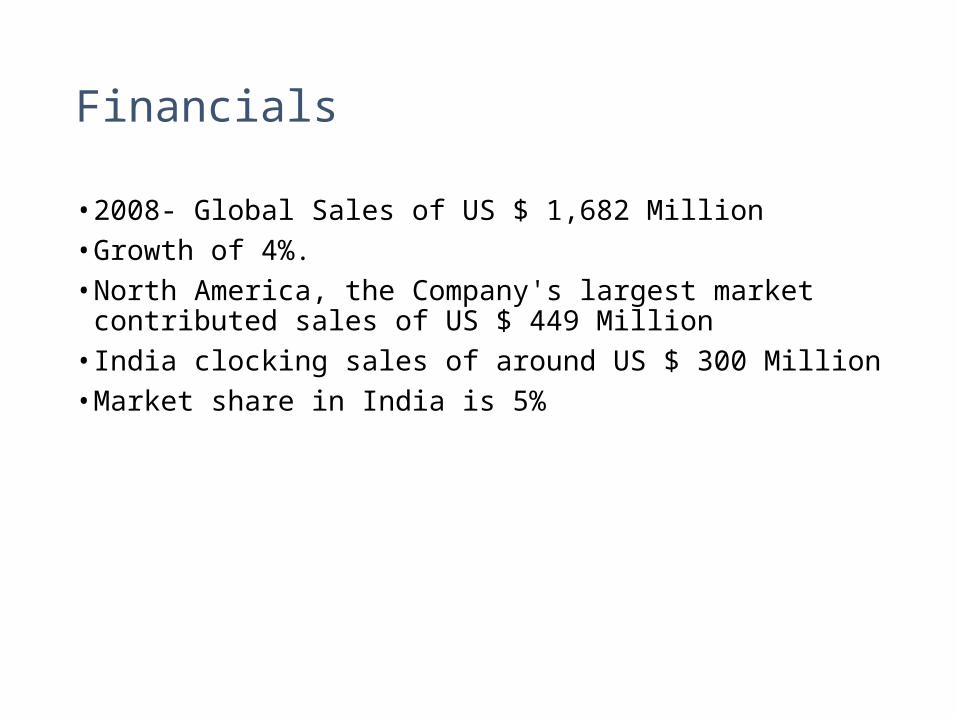

Financials

• 2008- Global Sales of US $ 1,682 Million• Growth of 4%.• North America, the Company's largest market contributed sales of US

$ 449 Million • India clocking sales of around US $ 300 Million• Market share in India is 5%

Major Setback

• December 2005, Ranbaxy's shares hit hard by a patent ruling disallowing production of its own version of Pfizer’s drug Lipitor.• September 2008, the FDA issued two Warning Letters to Ranbaxy

and an Import Alert for generic drugs produced by two manufacturing plants in India.

Product portfolio

Anti-Infectives Cardiovascular Diabetes Dermatological Neuro-Psychiatry Pain management Gastro-Intestinal Nutritional A strong player in the NDDS segment. Biological formulations such as Verorab (Rabies Vaccine) and

Vaxigrip (Flu Vaccine),

Major Alliances / Collaborations

• Drug Discovery & Clinical Development – GlaxoSmithKline• (Anti-infective and Respiratory Segments)• Drug Discovery Clinical Development – Merck • Statin molecule out licensed to PPD, USA

Introduction

• Japan based pharmaceutical company.

• Established in 2005 - merger of Sankyo Co., Ltd. and Daiichi Pharmaceutical Co., Ltd.

• Head Office – Tokyo

• Leading company in the field of cardiovascular drugs.

• Workforce - 29,272 people (as of September 30,2009) Capital - 50 billion yen

• U.S. subsidiary, Daiichi Sankyo, Inc. (DSI)

• European subsidiary, Daiichi Sankyo Europe GmbH (DSE)

History

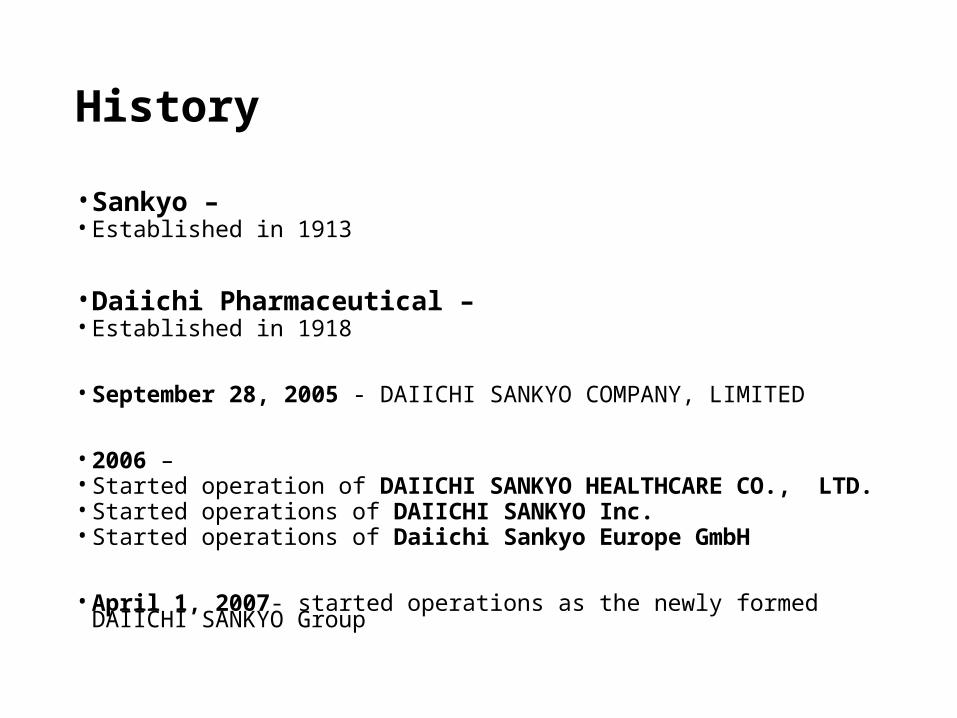

• Sankyo –• Established in 1913

• Daiichi Pharmaceutical –• Established in 1918

• September 28, 2005 - DAIICHI SANKYO COMPANY, LIMITED

• 2006 – • Started operation of DAIICHI SANKYO HEALTHCARE CO., LTD.• Started operations of DAIICHI SANKYO Inc.• Started operations of Daiichi Sankyo Europe GmbH

• April 1, 2007- started operations as the newly formed DAIICHI SANKYO Group

Research and Development

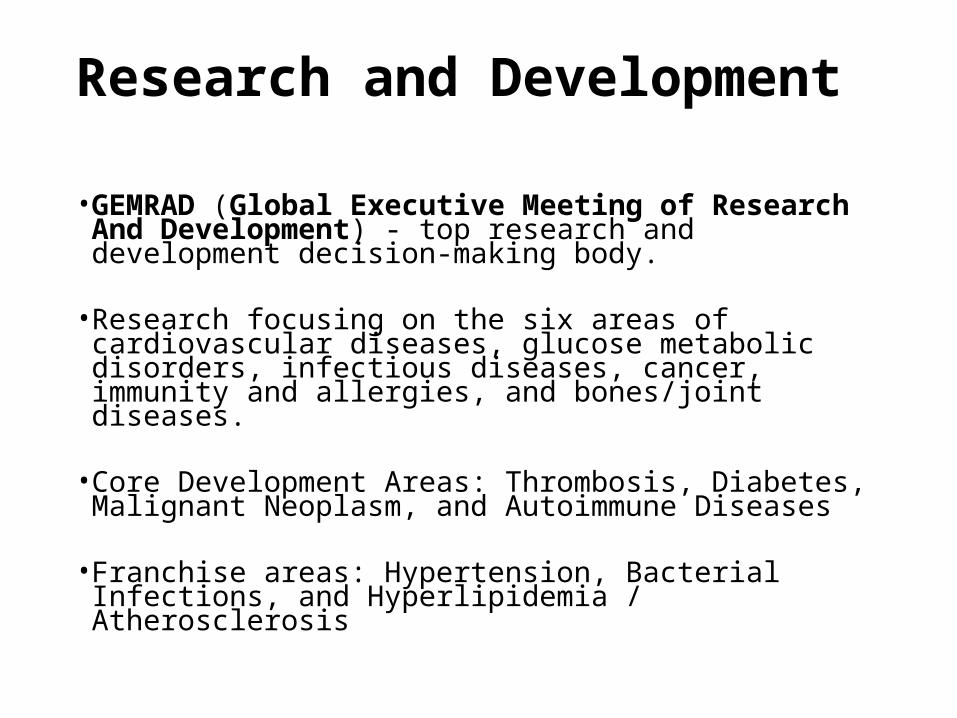

• GEMRAD (Global Executive Meeting of Research And Development) - top research and development decision-making body.

• Research focusing on the six areas of cardiovascular diseases, glucose metabolic disorders, infectious diseases, cancer, immunity and allergies, and bones/joint diseases.

• Core Development Areas: Thrombosis, Diabetes, Malignant Neoplasm, and Autoimmune Diseases

• Franchise areas: Hypertension, Bacterial Infections, and Hyperlipidemia / Atherosclerosis

Products

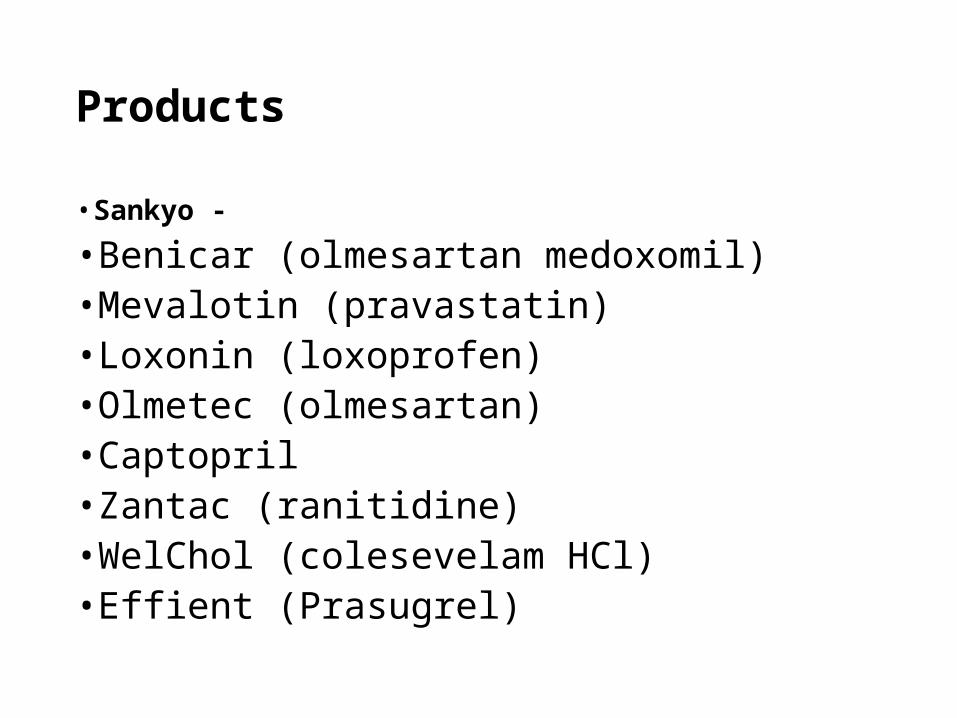

• Sankyo -

•Benicar (olmesartan medoxomil) •Mevalotin (pravastatin) • Loxonin (loxoprofen) •Olmetec (olmesartan) •Captopril •Zantac (ranitidine) •WelChol (colesevelam HCl) •Effient (Prasugrel)

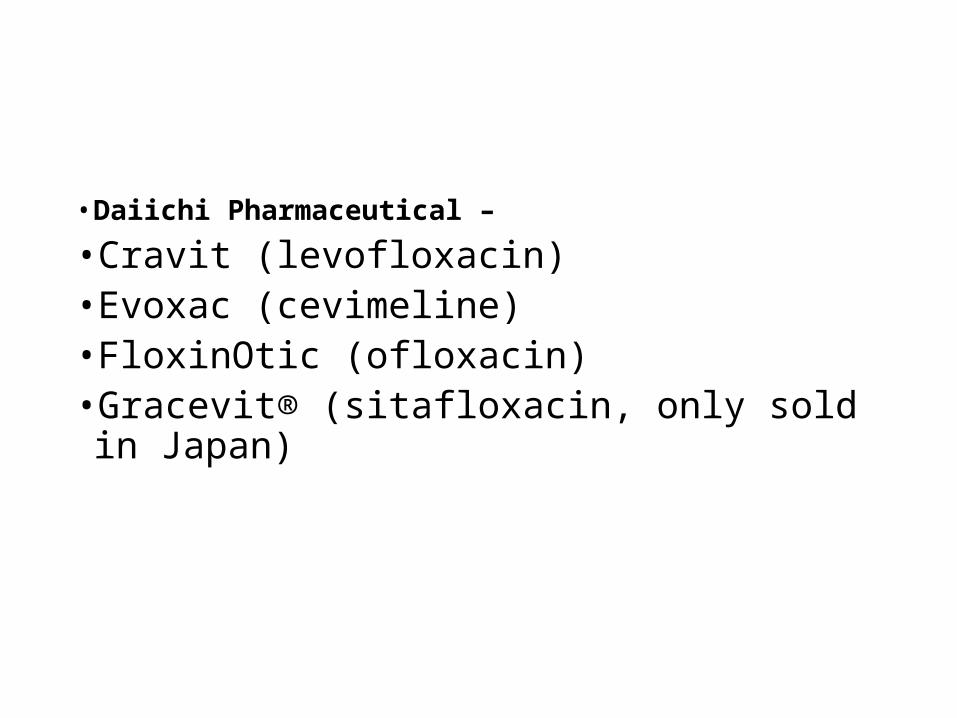

• Daiichi Pharmaceutical –

•Cravit (levofloxacin) •Evoxac (cevimeline) •FloxinOtic (ofloxacin) •Gracevit® (sitafloxacin, only sold in Japan)

RANBAXY-DAIICHI SANKYO

THE DEAL

THE DEAL

• Provide Stronger Platform for Drug Development, Manufacturing & Global Reach• Aim to be Research based International Pharmaceutical Company.

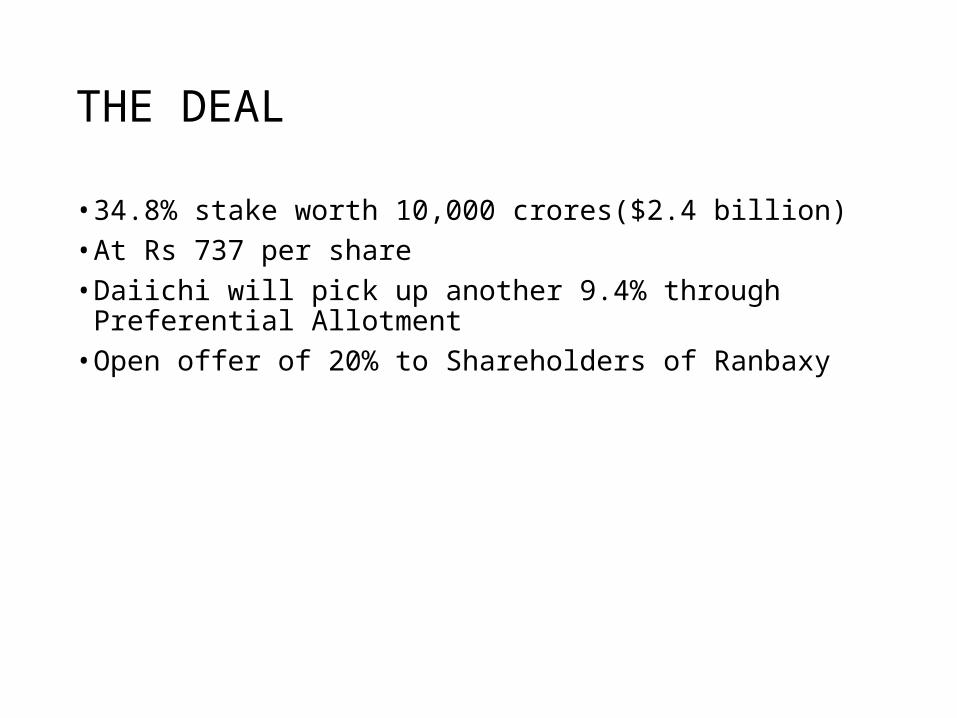

THE DEAL

• 34.8% stake worth 10,000 crores($2.4 billion)• At Rs 737 per share• Daiichi will pick up another 9.4% through Preferential Allotment• Open offer of 20% to Shareholders of Ranbaxy

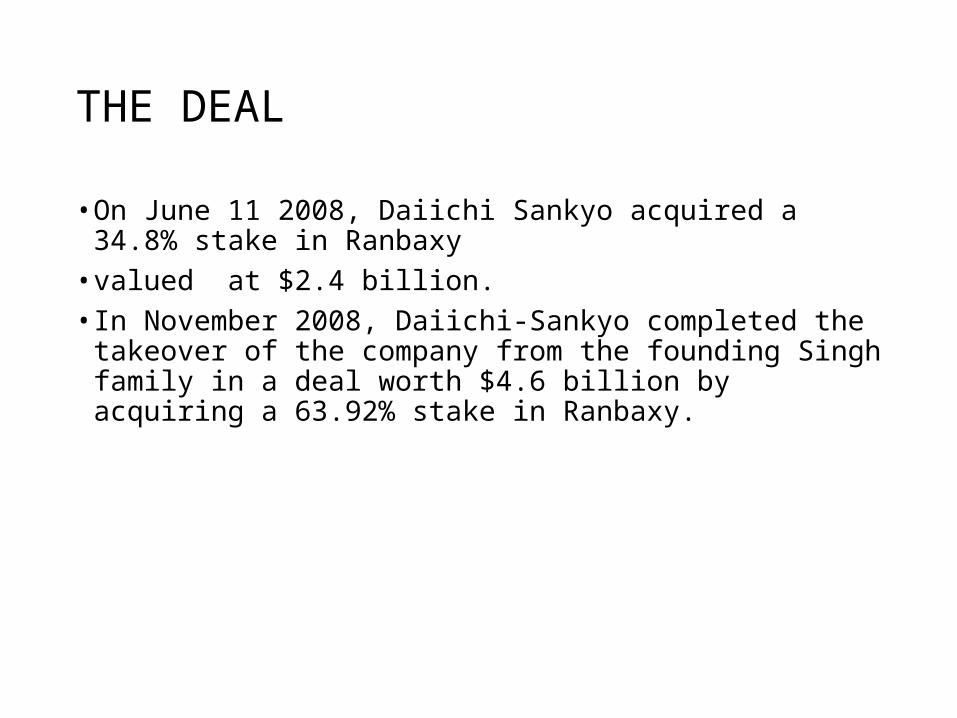

THE DEAL

• On June 11 2008, Daiichi Sankyo acquired a 34.8% stake in Ranbaxy • valued at $2.4 billion. • In November 2008, Daiichi-Sankyo completed the takeover of the

company from the founding Singh family in a deal worth $4.6 billion by acquiring a 63.92% stake in Ranbaxy.

THE DEAL

• Mr. Singh plans to Invest his $2.4 billion in:• Financial Services & Hospitals• Religare• Fortis

WHY RANBAXY DID IT ?

• A very “ intelligent” deal

• Had held share for 50 years

• But the Ranbaxy growth curve had peaked2006 – 16% growth2007 – 7% growth2009- 9% growth forecast

• Business model was struggling with high litigation costs and devaluation of the rupee against the USD

• US strategy was looking in the face of more expensive litigation

• Selling of entire stake at 30% premium

WHY DAICHI DID IT ?

• Japan has an ageing population and they needed new market

• There is growing recognition in Japan of the importance of generic drugs

• Japanese health Ministry is encouraging doctors to use generic drugs to reduce the health budget

• Acquisition of Ranbaxy gives Daiichi a low cost manufacturing base in India

• Daiichi will have a strong generics operations in India and operations in 60 different countries

• Daiichi moves from 22nd rank to 15th among world largest pharmaceutical companies

EFFECTS ON PHARMA EFFECTS ON PHARMA INDUSTRYINDUSTRY

THE EFFECTS ON RANKINGSTHE EFFECTS ON RANKINGS

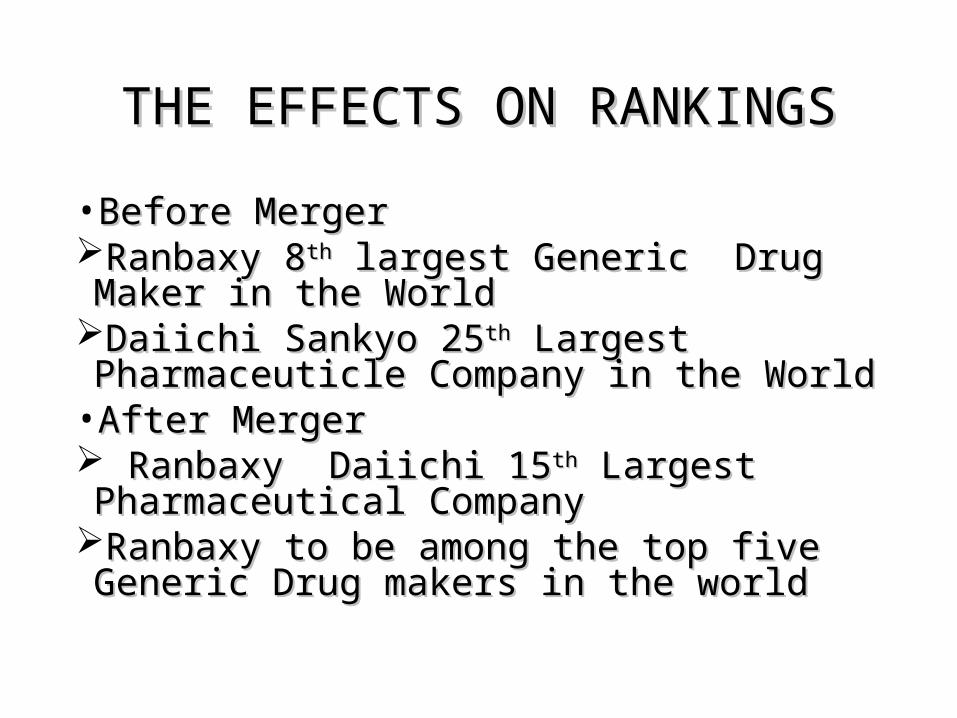

• Before MergerBefore MergerRanbaxy 8Ranbaxy 8thth largest Generic Drug Maker in the largest Generic Drug Maker in the

WorldWorldDaiichi Sankyo 25Daiichi Sankyo 25thth Largest Pharmaceuticle Largest Pharmaceuticle

Company in the WorldCompany in the World•After MergerAfter Merger Ranbaxy Daiichi 15Ranbaxy Daiichi 15thth Largest Pharmaceutical Largest Pharmaceutical

CompanyCompanyRanbaxy to be among the top five Generic Drug Ranbaxy to be among the top five Generic Drug

makers in the worldmakers in the world

The New TrendThe New Trend

• RANBAXY a Generics MakerRANBAXY a Generics Maker

• Daiichi: an Innovator Daiichi: an Innovator

• A Merger termed as the “Ardhnarishwar” ModelA Merger termed as the “Ardhnarishwar” Model

MARKET PENETRATIONMARKET PENETRATION

• Ranbaxy gets a support in the R&D Sector where it lags Ranbaxy gets a support in the R&D Sector where it lags • Daiichi forays in the Generics sector with India’s largest Generics Daiichi forays in the Generics sector with India’s largest Generics

ManufacturerManufacturer• Penetration of Ranbaxy in Japanese market made easy and same for Penetration of Ranbaxy in Japanese market made easy and same for

Daiichi in IndiaDaiichi in India

For Ranbaxy

• Significant milestone in becoming a research-based international pharmaceutical company.• Ranbaxy will gain easier access to the much-coveted Japanese

market by operating from within the Daiichi Sankyo• The immediate benefit for Ranbaxy is that the deal frees up its debt

and imparts more flexibility into its growth plans.

For Daiichi

• Easier to enter the Indian market.• Bigger goal - in securing a strong presence in the global market for

generics.• The acquisition will help Daiichi Sankyo to jump from number 22 in

the global pharmaceutical sector to number 15. • The main benefit is Ranbaxy’s low-cost manufacturing infrastructure

and supply chain strengths.

•Will be able to reduce its reliance on only branded drugs and margin risks in mature markets.•Benefit from Ranbaxy’s strengths in generics to

introduce generic versions of patent expired drugs, particularly in the Japanese market. •Additional NDAs from the US FDA on anti-

histaminics and anti-diabetics is an added advantage.

For the Joint Venture

• A complementary business combination that provides sustainable growth by diversification that spans the full spectrum of the pharmaceutical business. • An expanded global reach that enables leading market

positions in both mature and emerging markets with proprietary and non-proprietary products. • Strong growth potential by effectively managing

opportunities across the full pharmaceutical life-cycle. • Cost competitiveness by optimizing usage of R&D and

manufacturing facilities of both companies, especially in India.

• Both companies acquire a broader product base, therapeutic focus areas and well distributed risks.

Effect of deal on India as whole

1) Loss of good influencing people from pharma sector 2)Maximum use of available natural resources and not rational use.

3) Use the Indian talent in good manner at cheap rate.4)Capture of rich Indian generic store.

Common influences of merger on both Daichii and Ranbaxy

Reduced competition & choice for consumer in oligopoly market

Likelihood of job cuts

Conflict with new management

Difficulty in cultural integration

Monetory cost to the company

Happenings with Ranbaxy after merger•US regulator plan to stop reviewing any drug made at Paonta Shahib (one of the Ranbaxy Indian plant)

•Ranbaxy failed to secure the American drug regulator’s permission to market generic drug in US.(Astellas ,Flomax)

•Ban on import of around 30 generic drug by FDA US

•Financial loss

Impact of it on Daiichi

•Daichii have to face competitor of Ranbaxy•Ranbaxy acquisition puts Daiichi Sankyo in red•Price Daiichi paid for acquisition was quite high

compared to the present pricing of other Indian generic drug making companies.•Lots of government restrictions on Ranbaxy drug •Daiichi has to appoint industry experts to resolve

issues related to the USFDA

Impact of it on Daiichi

• Daiichi Sankyo's Loss Forecast The FDA's latest findings come less than a month after

Daiichi Sankyo reported a $3.7 billion loss in the October-December quarter and warned that annual earnings would swing to a loss. The Tokyo-based company now expects a net loss of $3.2 billion this fiscal year through March, instead of the previously predicted $663 million gain, largely because of the yen's recent strength and the Ranbaxy deal

The currency hedges by Ranbaxy would cost the Japanese drugmaker around $122 million this financial year

Impact of it on Daiichi

• Japan accounts for 68 per cent of Daiichi Sankyo’s sales, with North America being the second largest market contributing 20 per cent, followed by Europe with 9 per cent and other markets 3 per cent. SoThe fourth-quarter net loss of the Japanese pharma giant amounts to $390.1 million, which has been attributed to the acquisition of Ranbaxy.

• “Daiichi Sankyo might have been deceived by Ranbaxy” by

analyst Fumiyoshi Sakai. • Expiring of Ranbxy patent cutting down the royalty payment

Effect on Indian Pharmaceutical Effect on Indian Pharmaceutical IndustryIndustry

• Ranbaxy fell 3% on stock market because of low acceptance and Ranbaxy fell 3% on stock market because of low acceptance and capital gainscapital gains• Hence, proving the deal to be disadvantage to the industryHence, proving the deal to be disadvantage to the industry

![第一計器製作所 · 2016. 6. 24. · keiki seisakusho contd. daiichi t] daiichi keiki seisakusho co..ltd. _.h[ keiki seisakusho co.ltd_ daiichi keiki seisakusho sho daiichi keiki](https://img.dokumen.tips/doc/110x75/60efa82a1a6bdc50df76fed5/ceeoe-2016-6-24-keiki-seisakusho-contd-daiichi-t-daiichi.jpg)