Embed Size (px)

Citation preview

1

May 29, 2013

Quantitative Strategy

Joseph J. Mezrich

1-212-310-4241

Instinet, LLC

1095 Avenue of the Americas

New York, N.Y. 10036

2

The opportunity for quants in a

world of diminished alpha

Tulip Mania to Twitter Media

3

Tulip Mania to Twitter Media

No market bubbles before media – tulip mania of 1630’s needed

newspapers. The twenties bubble needed the telephone. Media

and communication can dramatically impact investor behavior.

Government regulation and industry standardization over a

decade ago have played an important role in data, with

unintended harm to investment performance.

This has led to shifts in asset flows, the growing importance of

alternative beta, and a new opportunity for quants.

4

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400

500

Ap

r-0

3

Oct

-03

Ap

r-0

4

Oct

-04

Ap

r-0

5

Oct

-05

Ap

r-0

6

Oct

-06

Ap

r-0

7

Oct

-07

Ap

r-0

8

Oct

-08

Ap

r-0

9

Oct

-09

Ap

r-1

0

Oct

-10

Ap

r-1

1

Oct

-11

Ap

r-1

2

Oct

-12

Cu

mu

lati

ve f

un

d f

low

(b

illio

n $

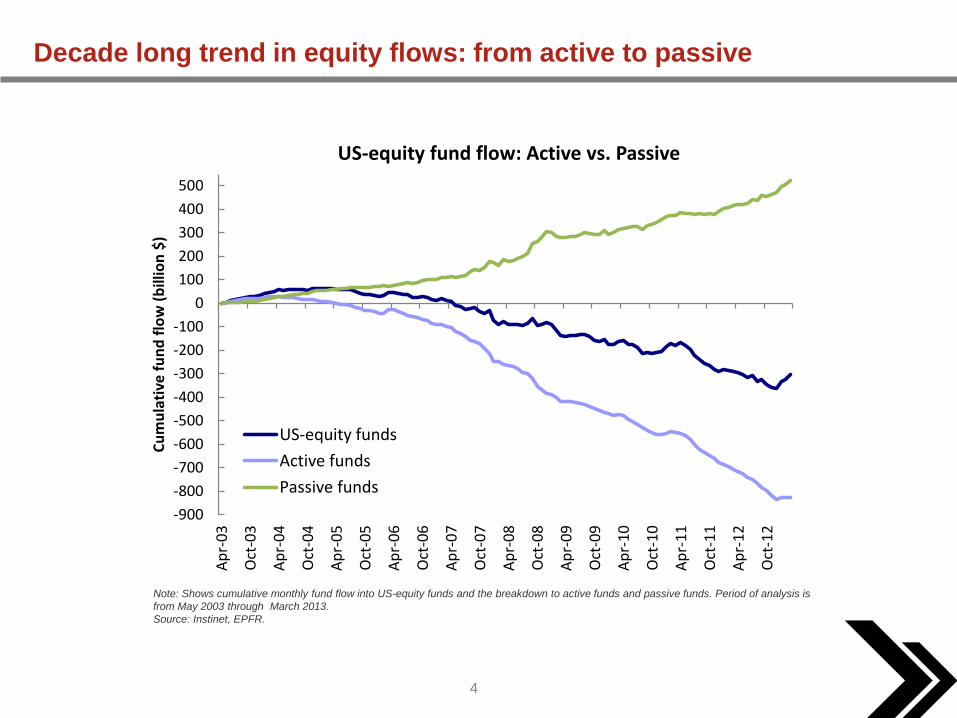

)US-equity fund flow: Active vs. Passive

US-equity funds

Active funds

Passive funds

Decade long trend in equity flows: from active to passive

Note: Shows cumulative monthly fund flow into US-equity funds and the breakdown to active funds and passive funds. Period of analysis is

from May 2003 through March 2013.

Source: Instinet, EPFR.

5

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13

Cu

mu

lati

ve e

xce

ss r

etu

rn (

%)

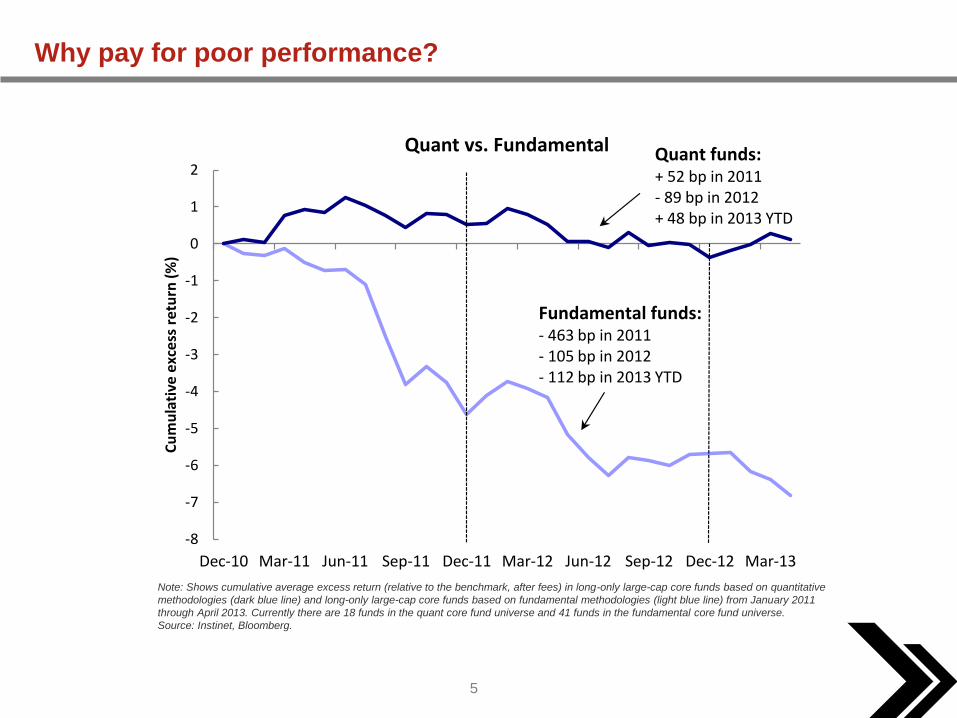

Quant vs. Fundamental Quant funds:+ 52 bp in 2011- 89 bp in 2012+ 48 bp in 2013 YTD

Fundamental funds:- 463 bp in 2011- 105 bp in 2012- 112 bp in 2013 YTD

Why pay for poor performance?

Note: Shows cumulative average excess return (relative to the benchmark, after fees) in long-only large-cap core funds based on quantitative

methodologies (dark blue line) and long-only large-cap core funds based on fundamental methodologies (light blue line) from January 2011

through April 2013. Currently there are 18 funds in the quant core fund universe and 41 funds in the fundamental core fund universe.

Source: Instinet, Bloomberg.

6

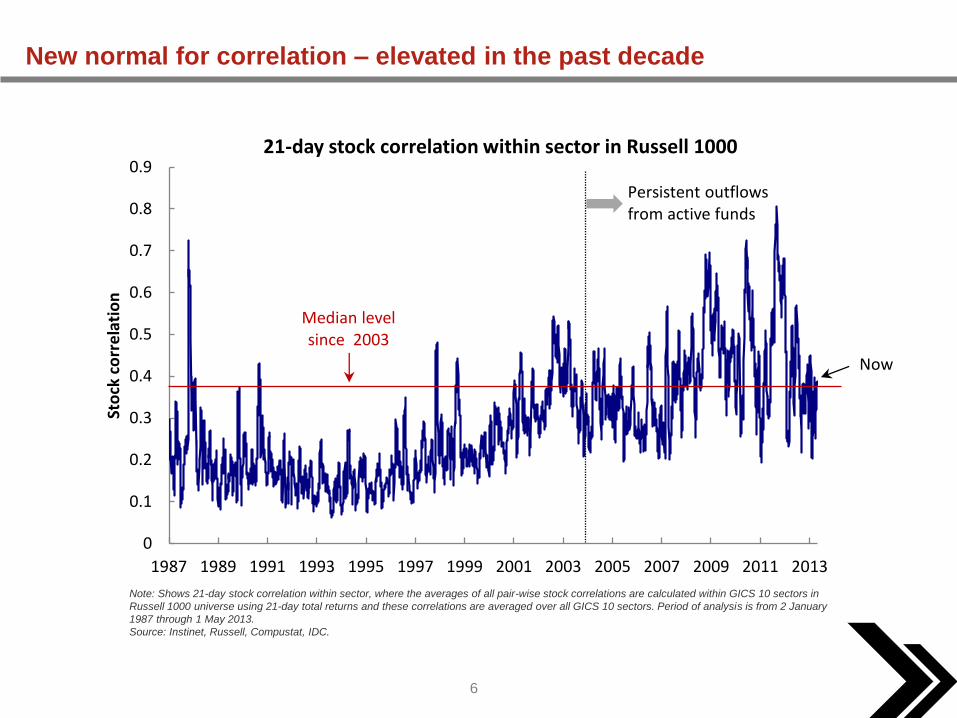

New normal for correlation – elevated in the past decade

Note: Shows 21-day stock correlation within sector, where the averages of all pair-wise stock correlations are calculated within GICS 10 sectors in

Russell 1000 universe using 21-day total returns and these correlations are averaged over all GICS 10 sectors. Period of analysis is from 2 January

1987 through 1 May 2013.

Source: Instinet, Russell, Compustat, IDC.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Sto

ck c

orr

ela

tio

n

21-day stock correlation within sector in Russell 1000

Median level since 2003

Persistent outflows from active funds

Now

7

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0

10

20

30

40

50

60

70

80

901

98

7

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Stock co

rrelation

with

in secto

r

Vo

lati

lity

of

Ru

ssel

l 10

00

ind

ex (

%)

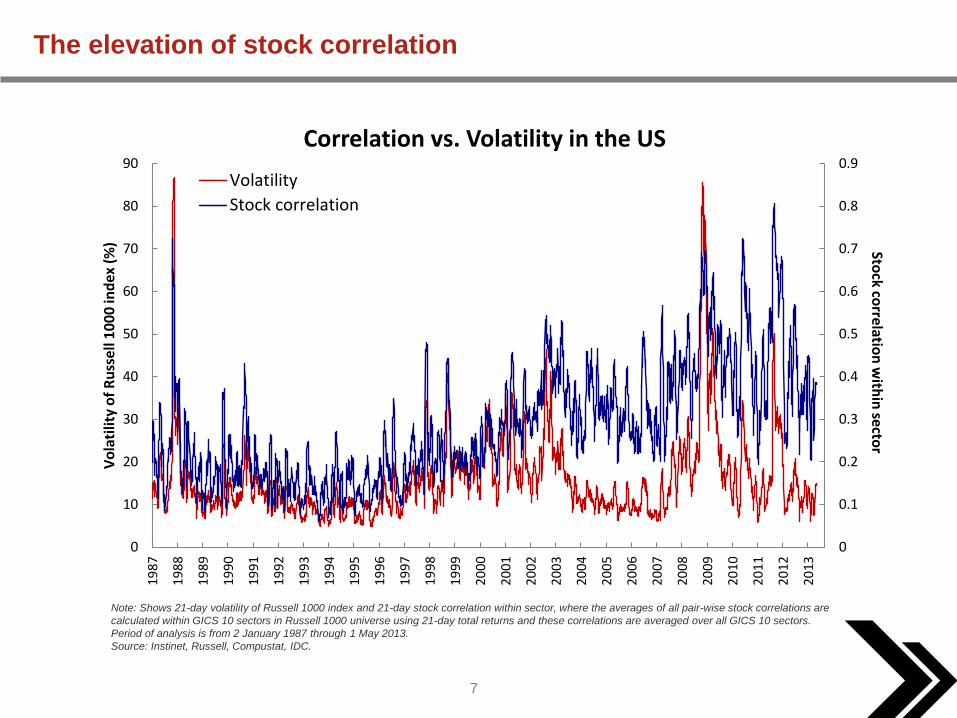

Correlation vs. Volatility in the US

Volatility

Stock correlation

The elevation of stock correlation

Note: Shows 21-day volatility of Russell 1000 index and 21-day stock correlation within sector, where the averages of all pair-wise stock correlations are

calculated within GICS 10 sectors in Russell 1000 universe using 21-day total returns and these correlations are averaged over all GICS 10 sectors.

Period of analysis is from 2 January 1987 through 1 May 2013.

Source: Instinet, Russell, Compustat, IDC.

8

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.451

98

7

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Sto

ck c

orr

elat

ion

-V

ola

tilit

ySpread between stock correlation and market volatility

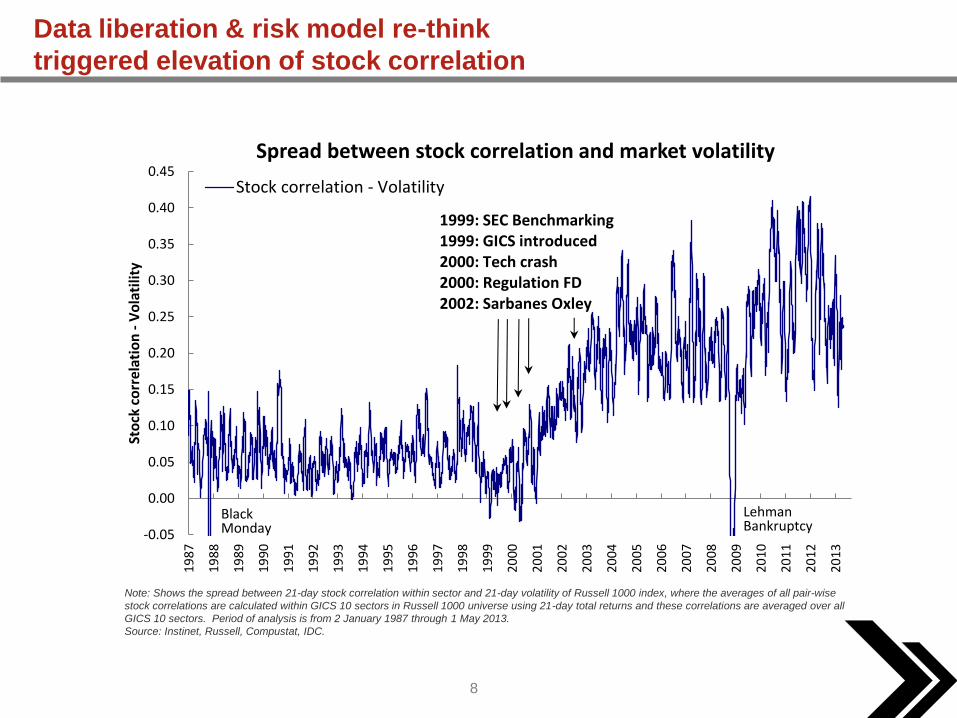

Stock correlation - Volatility

Lehman Bankruptcy

BlackMonday

1999: SEC Benchmarking1999: GICS introduced2000: Tech crash2000: Regulation FD2002: Sarbanes Oxley

Data liberation & risk model re-think

triggered elevation of stock correlation

Note: Shows the spread between 21-day stock correlation within sector and 21-day volatility of Russell 1000 index, where the averages of all pair-wise

stock correlations are calculated within GICS 10 sectors in Russell 1000 universe using 21-day total returns and these correlations are averaged over all

GICS 10 sectors. Period of analysis is from 2 January 1987 through 1 May 2013.

Source: Instinet, Russell, Compustat, IDC.

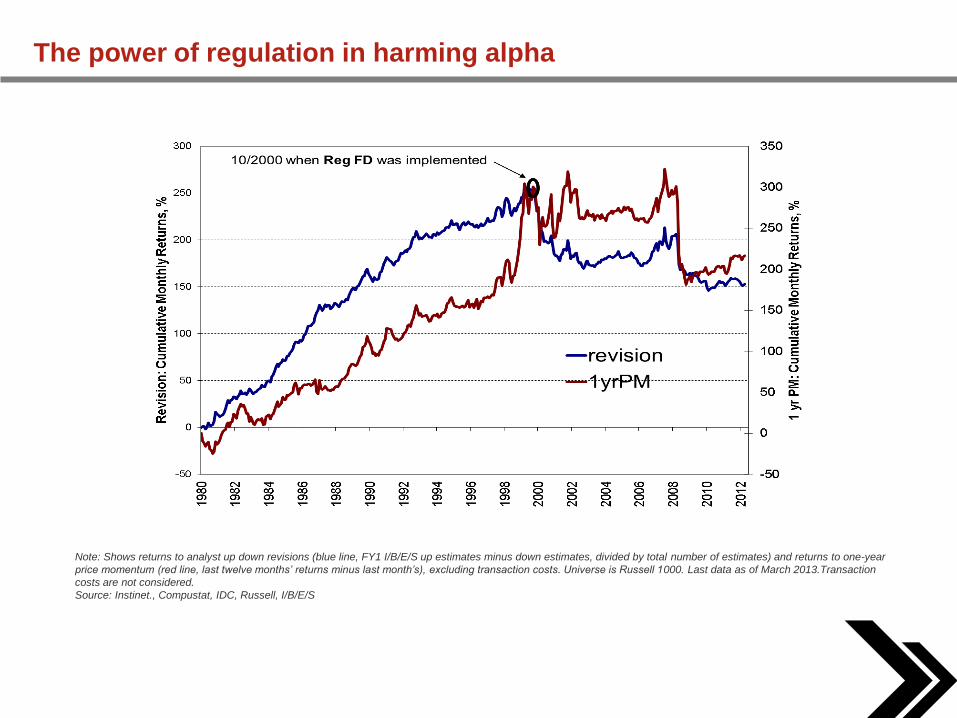

The power of regulation in harming alpha

Note: Shows returns to analyst up down revisions (blue line, FY1 I/B/E/S up estimates minus down estimates, divided by total number of estimates) and returns to one-year

price momentum (red line, last twelve months’ returns minus last month’s), excluding transaction costs. Universe is Russell 1000. Last data as of March 2013.Transaction

costs are not considered.

Source: Instinet., Compustat, IDC, Russell, I/B/E/S

10

0

50

100

150

200

250

300

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Cu

mu

lati

ve r

etu

rn (

%)

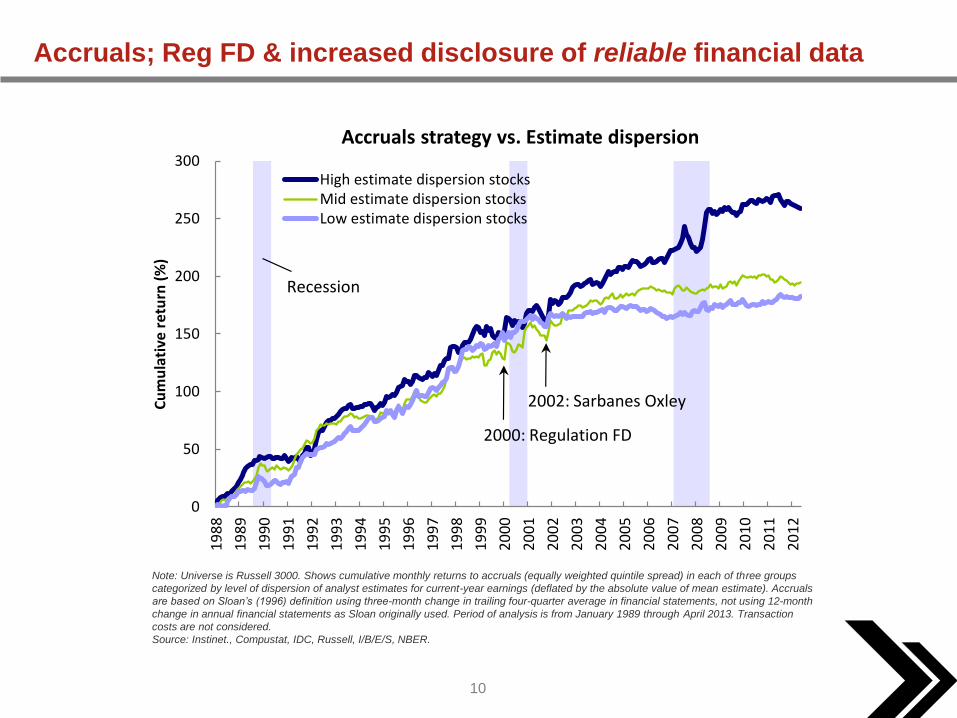

Accruals strategy vs. Estimate dispersion

High estimate dispersion stocksMid estimate dispersion stocksLow estimate dispersion stocks

2000: Regulation FD

Recession

2002: Sarbanes Oxley

Accruals; Reg FD & increased disclosure of reliable financial data

Note: Universe is Russell 3000. Shows cumulative monthly returns to accruals (equally weighted quintile spread) in each of three groups

categorized by level of dispersion of analyst estimates for current-year earnings (deflated by the absolute value of mean estimate). Accruals

are based on Sloan’s (1996) definition using three-month change in trailing four-quarter average in financial statements, not using 12-month

change in annual financial statements as Sloan originally used. Period of analysis is from January 1989 through April 2013. Transaction

costs are not considered.

Source: Instinet., Compustat, IDC, Russell, I/B/E/S, NBER.

11

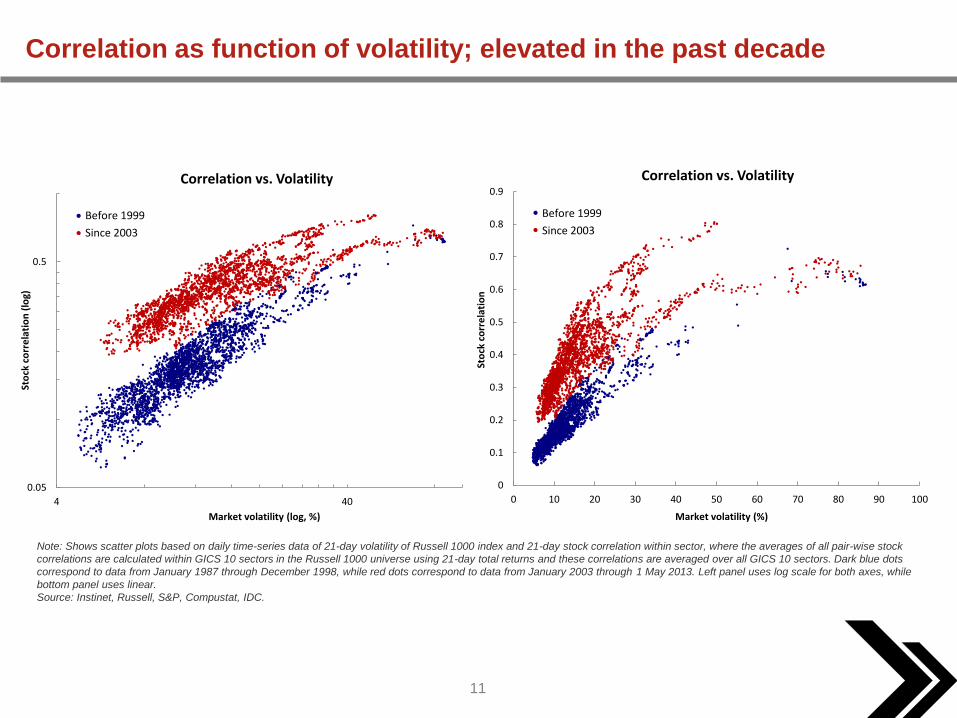

Correlation as function of volatility; elevated in the past decade

Note: Shows scatter plots based on daily time-series data of 21-day volatility of Russell 1000 index and 21-day stock correlation within sector, where the averages of all pair-wise stock

correlations are calculated within GICS 10 sectors in the Russell 1000 universe using 21-day total returns and these correlations are averaged over all GICS 10 sectors. Dark blue dots

correspond to data from January 1987 through December 1998, while red dots correspond to data from January 2003 through 1 May 2013. Left panel uses log scale for both axes, while

bottom panel uses linear.

Source: Instinet, Russell, S&P, Compustat, IDC.

0.05

0.5

4 40

Sto

ck c

orr

ela

tio

n (

log)

Market volatility (log, %)

Correlation vs. Volatility

Before 1999

Since 2003

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0 10 20 30 40 50 60 70 80 90 100

Sto

ck c

orr

ela

tio

n

Market volatility (%)

Correlation vs. Volatility

Before 1999

Since 2003

12 Joseph Mezrich, 212.310.4241, [email protected]

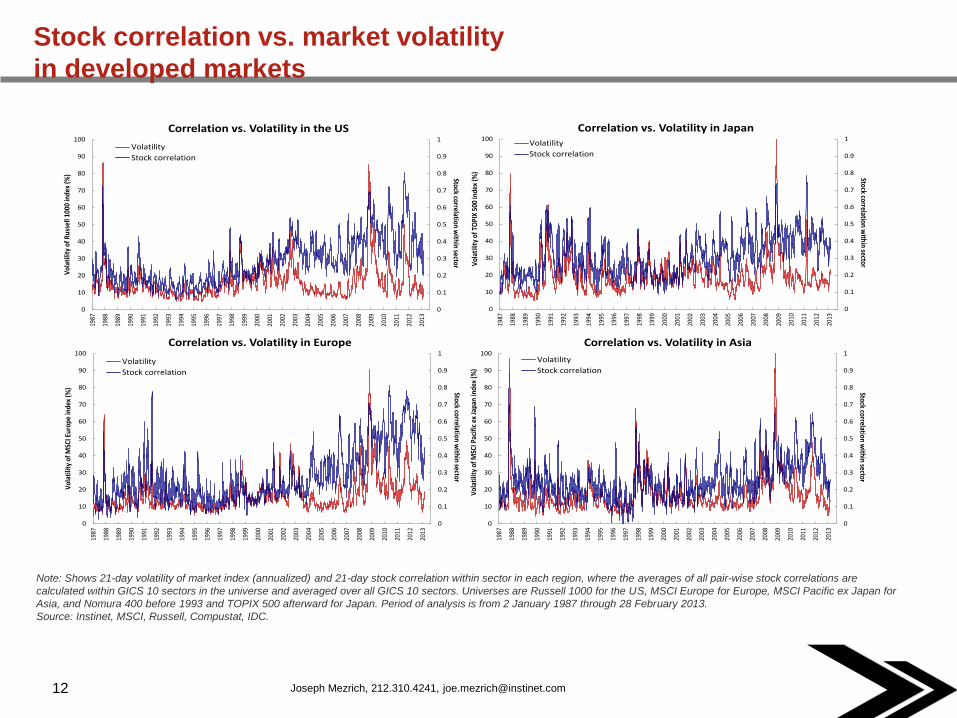

Stock correlation vs. market volatility

in developed markets

Note: Shows 21-day volatility of market index (annualized) and 21-day stock correlation within sector in each region, where the averages of all pair-wise stock correlations are

calculated within GICS 10 sectors in the universe and averaged over all GICS 10 sectors. Universes are Russell 1000 for the US, MSCI Europe for Europe, MSCI Pacific ex Japan for

Asia, and Nomura 400 before 1993 and TOPIX 500 afterward for Japan. Period of analysis is from 2 January 1987 through 28 February 2013.

Source: Instinet, MSCI, Russell, Compustat, IDC.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0

10

20

30

40

50

60

70

80

90

100

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Stock correlation within sector

Vol

atili

ty o

f Rus

sell

1000

inde

x (%

)

Correlation vs. Volatility in the US

Volatility

Stock correlation

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0

10

20

30

40

50

60

70

80

90

100

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Stock correlation within sector

Vol

atili

ty o

f MSC

I Eur

ope

inde

x (%

)

Correlation vs. Volatility in Europe

Volatility

Stock correlation

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0

10

20

30

40

50

60

70

80

90

100

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Stock correlation within sectorV

olat

ility

of T

OPI

X 50

0 in

dex

(%)

Correlation vs. Volatility in JapanVolatility

Stock correlation

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0

10

20

30

40

50

60

70

80

90

100

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Stock correlation within sector

Vol

atili

ty o

f MSC

I Pac

ific

ex

Japa

n in

dex

(%)

Correlation vs. Volatility in Asia

Volatility

Stock correlation

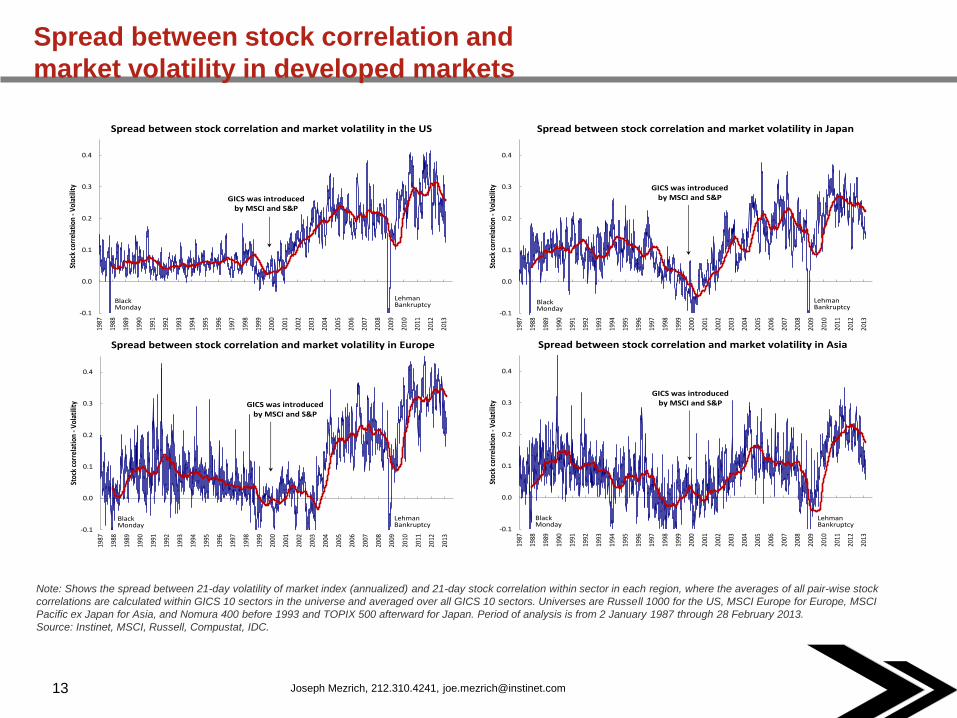

13 Joseph Mezrich, 212.310.4241, [email protected]

Spread between stock correlation and

market volatility in developed markets

Note: Shows the spread between 21-day volatility of market index (annualized) and 21-day stock correlation within sector in each region, where the averages of all pair-wise stock

correlations are calculated within GICS 10 sectors in the universe and averaged over all GICS 10 sectors. Universes are Russell 1000 for the US, MSCI Europe for Europe, MSCI

Pacific ex Japan for Asia, and Nomura 400 before 1993 and TOPIX 500 afterward for Japan. Period of analysis is from 2 January 1987 through 28 February 2013.

Source: Instinet, MSCI, Russell, Compustat, IDC.

-0.1

0.0

0.1

0.2

0.3

0.4

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Stoc

k co

rrel

atio

n -V

olat

ility

Spread between stock correlation and market volatility in the US

Lehman Bankruptcy

BlackMonday

GICS was introducedby MSCI and S&P

Spread between stock correlation and market volatility in the US

-0.1

0.0

0.1

0.2

0.3

0.4

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Stoc

k co

rrel

atio

n -V

olat

ility

Spread between stock correlation and market volatility in Europe

Lehman Bankruptcy

BlackMonday

GICS was introducedby MSCI and S&P

Spread between stock correlation and market volatility in Europe

-0.1

0.0

0.1

0.2

0.3

0.4

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Stoc

k co

rrel

atio

n -V

olat

ility

Spread between stock correlation and market volatility in Japan

Lehman Bankruptcy

BlackMonday

GICS was introducedby MSCI and S&P

Spread between stock correlation and market volatility in Japan

-0.1

0.0

0.1

0.2

0.3

0.4

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Stoc

k co

rrel

atio

n -V

olat

ility

Spread between stock correlation and market volatility in Asia

Lehman Bankruptcy

BlackMonday

GICS was introducedby MSCI and S&P

Spread between stock correlation and market volatility in Asia

14 Joseph Mezrich, 212.310.4241, [email protected]

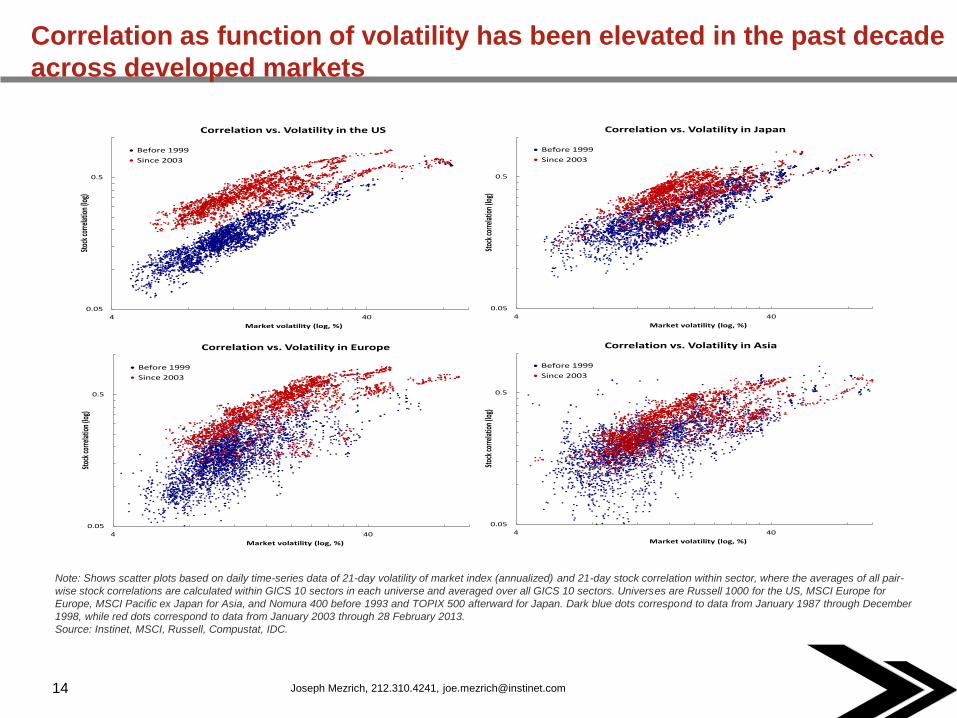

Correlation as function of volatility has been elevated in the past decade

across developed markets

Note: Shows scatter plots based on daily time-series data of 21-day volatility of market index (annualized) and 21-day stock correlation within sector, where the averages of all pair-

wise stock correlations are calculated within GICS 10 sectors in each universe and averaged over all GICS 10 sectors. Universes are Russell 1000 for the US, MSCI Europe for

Europe, MSCI Pacific ex Japan for Asia, and Nomura 400 before 1993 and TOPIX 500 afterward for Japan. Dark blue dots correspond to data from January 1987 through December

1998, while red dots correspond to data from January 2003 through 28 February 2013.

Source: Instinet, MSCI, Russell, Compustat, IDC.

0.05

0.5

4 40

Stoc

k cor

relat

ion

(log)

Market volatility (log, %)

Correlation vs. Volatility in Europe

Before 1999

Since 2003

0.05

0.5

4 40

Stoc

k cor

relat

ion

(log)

Market volatility (log, %)

Correlation vs. Volatility in Japan

Before 1999

Since 2003

0.05

0.5

4 40

Stoc

k cor

relat

ion

(log)

Market volatility (log, %)

Correlation vs. Volatility in the US

Before 1999

Since 2003

0.05

0.5

4 40

Stoc

k cor

relat

ion

(log)

Market volatility (log, %)

Correlation vs. Volatility in Asia

Before 1999

Since 2003

15

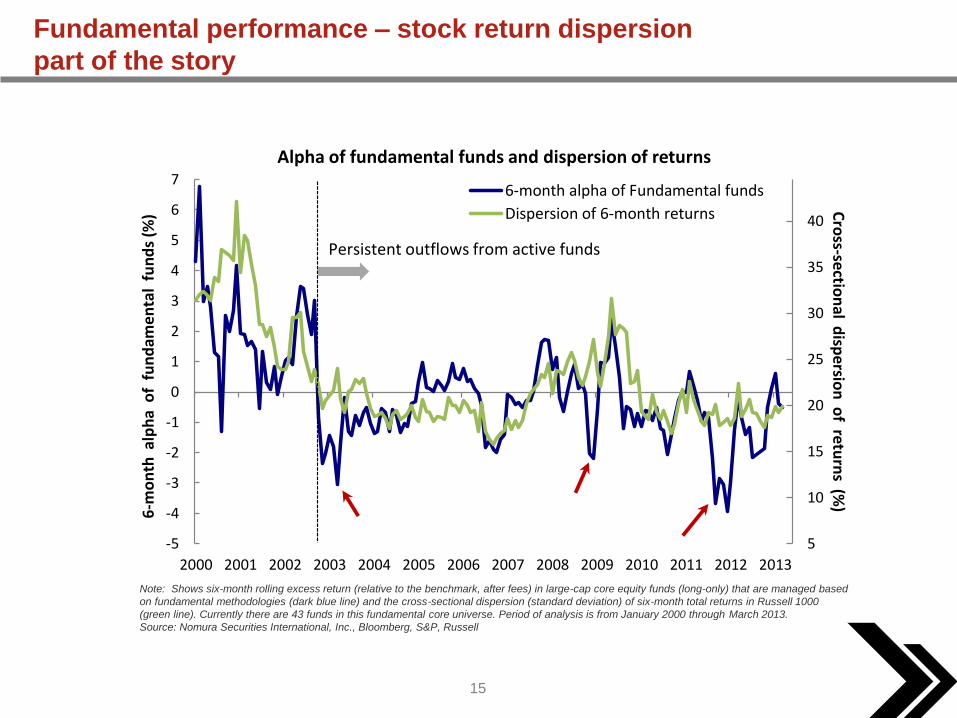

Fundamental performance – stock return dispersion

part of the story

Note: Shows six-month rolling excess return (relative to the benchmark, after fees) in large-cap core equity funds (long-only) that are managed based

on fundamental methodologies (dark blue line) and the cross-sectional dispersion (standard deviation) of six-month total returns in Russell 1000

(green line). Currently there are 43 funds in this fundamental core universe. Period of analysis is from January 2000 through March 2013.

Source: Nomura Securities International, Inc., Bloomberg, S&P, Russell

5

10

15

20

25

30

35

40

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Cro

ss-section

al disp

ersion

of retu

rns (%

)

6-m

on

th a

lph

a o

f f

un

dam

enta

l fu

nd

s (%

)Alpha of fundamental funds and dispersion of returns

6-month alpha of Fundamental funds

Dispersion of 6-month returns

Persistent outflows from active funds

16

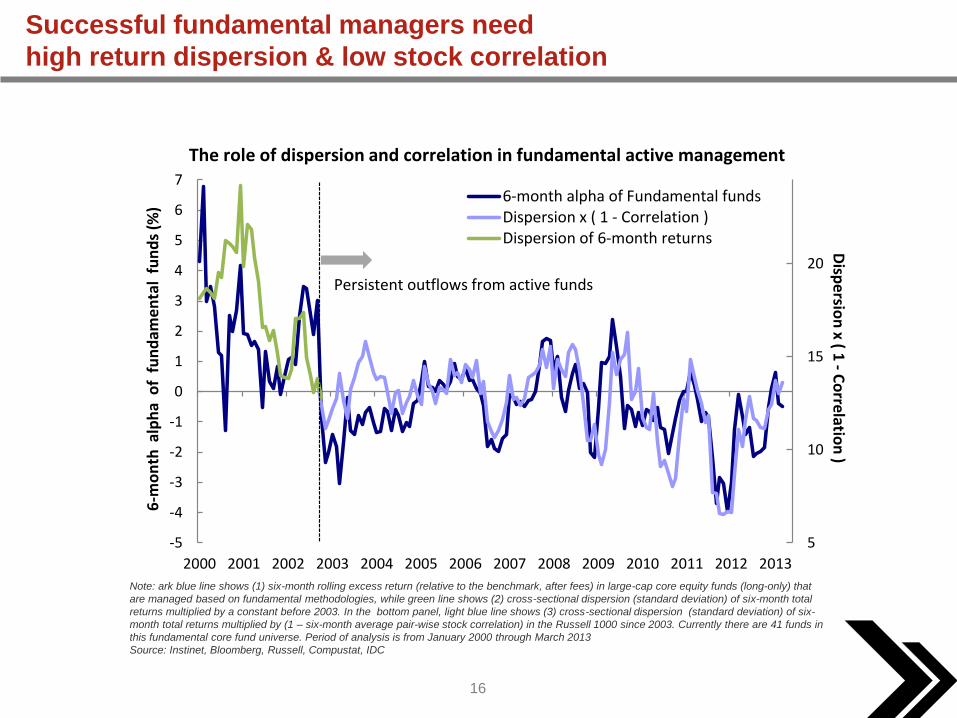

Successful fundamental managers need

high return dispersion & low stock correlation

Note: ark blue line shows (1) six-month rolling excess return (relative to the benchmark, after fees) in large-cap core equity funds (long-only) that

are managed based on fundamental methodologies, while green line shows (2) cross-sectional dispersion (standard deviation) of six-month total

returns multiplied by a constant before 2003. In the bottom panel, light blue line shows (3) cross-sectional dispersion (standard deviation) of six-

month total returns multiplied by (1 – six-month average pair-wise stock correlation) in the Russell 1000 since 2003. Currently there are 41 funds in

this fundamental core fund universe. Period of analysis is from January 2000 through March 2013

Source: Instinet, Bloomberg, Russell, Compustat, IDC

5

10

15

20

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Disp

ersio

n x ( 1

-C

orrelatio

n )

6-m

on

th a

lph

a o

f f

un

dam

en

tal

fun

ds

(%)

6-month alpha of Fundamental fundsDispersion x ( 1 - Correlation )Dispersion of 6-month returns

Persistent outflows from active funds

The role of dispersion and correlation in fundamental active management

17

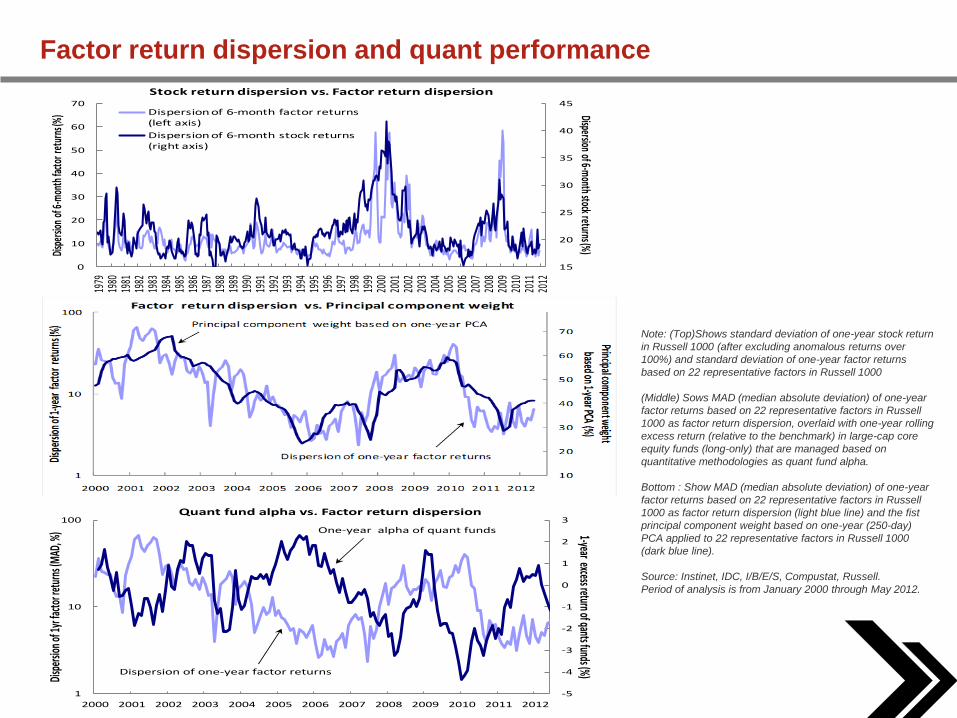

Factor return dispersion and quant performance

Note: (Top)Shows standard deviation of one-year stock return

in Russell 1000 (after excluding anomalous returns over

100%) and standard deviation of one-year factor returns

based on 22 representative factors in Russell 1000

(Middle) Sows MAD (median absolute deviation) of one-year

factor returns based on 22 representative factors in Russell

1000 as factor return dispersion, overlaid with one-year rolling

excess return (relative to the benchmark) in large-cap core

equity funds (long-only) that are managed based on

quantitative methodologies as quant fund alpha.

Bottom : Show MAD (median absolute deviation) of one-year

factor returns based on 22 representative factors in Russell

1000 as factor return dispersion (light blue line) and the fist

principal component weight based on one-year (250-day)

PCA applied to 22 representative factors in Russell 1000

(dark blue line).

Source: Instinet, IDC, I/B/E/S, Compustat, Russell.

Period of analysis is from January 2000 through May 2012.

15

20

25

30

35

40

45

0

10

20

30

40

50

60

7019

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12

Dispersion of 6-month stock returns (%)Di

sper

sion

of 6-

mon

th fa

ctor r

etur

ns (%

)

Stock return dispersion vs. Factor return dispersion

Dispersion of 6-month factor returns (left axis)

Dispersion of 6-month stock returns (right axis)

-5

-4

-3

-2

-1

0

1

2

3

1

10

100

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

1-year excess return of qants funds (%)Disp

ersio

n of 1

yr fa

ctor r

etur

ns (M

AD, %

)

Quant fund alpha vs. Factor return dispersion

One-year alpha of quant funds

Dispersion of one-year factor returns

18

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0

10

20

30

40

50

60

70

80

901

99

3

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Factor m

agnitu

de co

rrelation

Wei

ght

of

1st

pri

nci

pal

co

mp

on

ent

(%)

Magnitude of factor correlation vs. Principal component weight

1st principal component weight based on PCA

Magnitude of factor correlation

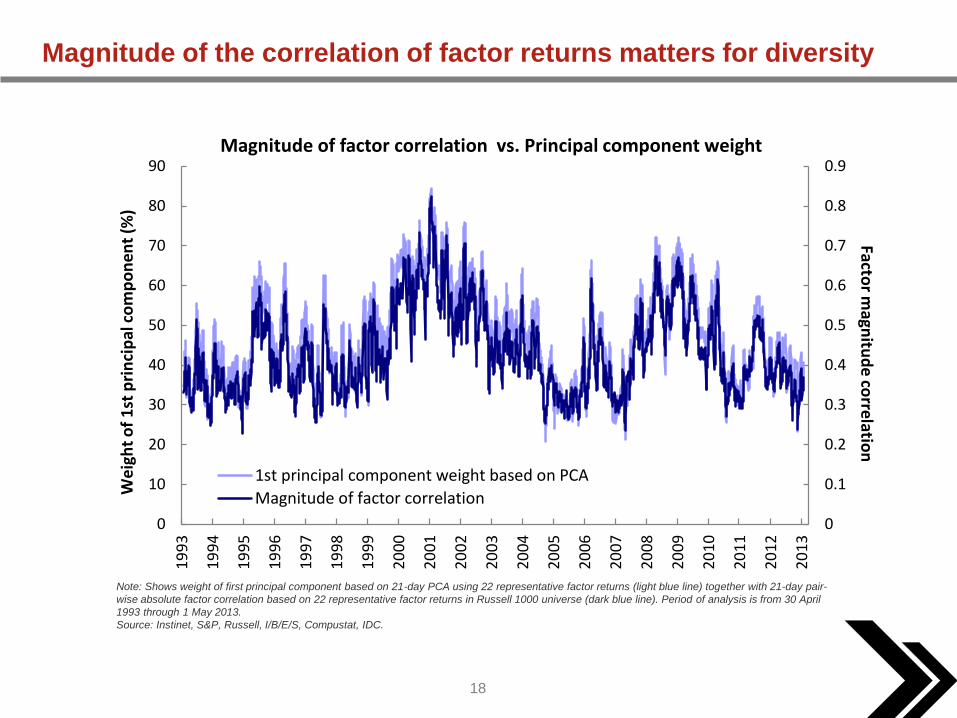

Magnitude of the correlation of factor returns matters for diversity

Note: Shows weight of first principal component based on 21-day PCA using 22 representative factor returns (light blue line) together with 21-day pair-

wise absolute factor correlation based on 22 representative factor returns in Russell 1000 universe (dark blue line). Period of analysis is from 30 April

1993 through 1 May 2013.

Source: Instinet, S&P, Russell, I/B/E/S, Compustat, IDC.

19

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

21

-day

co

rrel

atio

nStock correlation vs. Magnitude of factor correlation

Stock correlation

Magnitude of factor correlation

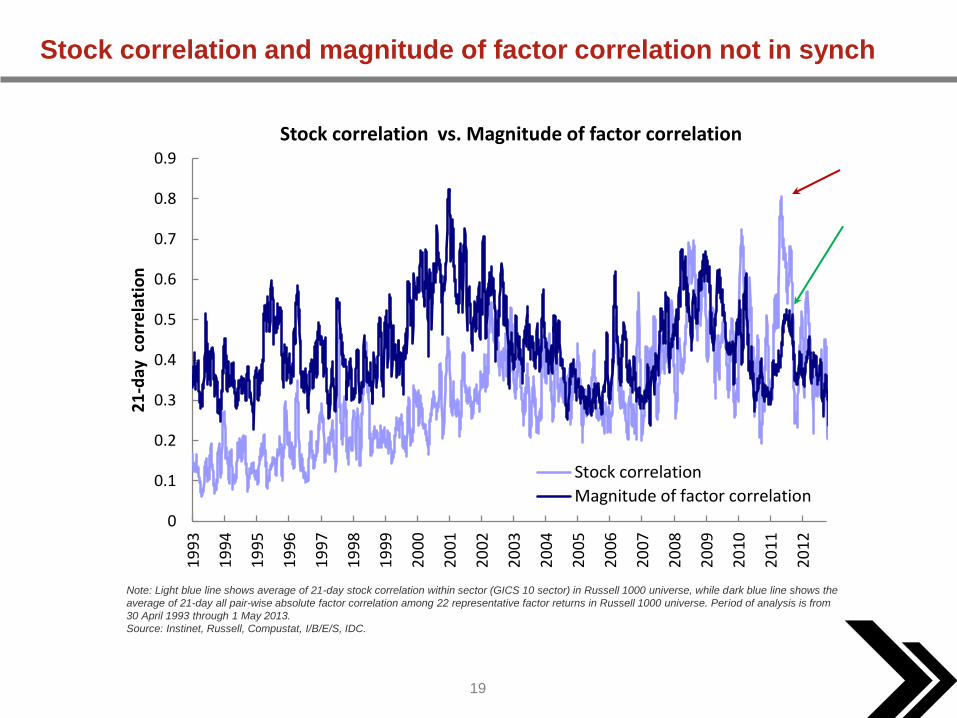

Stock correlation and magnitude of factor correlation not in synch

Note: Light blue line shows average of 21-day stock correlation within sector (GICS 10 sector) in Russell 1000 universe, while dark blue line shows the

average of 21-day all pair-wise absolute factor correlation among 22 representative factor returns in Russell 1000 universe. Period of analysis is from

30 April 1993 through 1 May 2013.

Source: Instinet, Russell, Compustat, I/B/E/S, IDC.

20

The market has many ways to pay

Fundamental investors & quant investors reap

different payoffs from the market

- Fundamental managers find idiosyncratic

opportunity to accrue alpha

- Quant managers harvest factor premium

21

-5

0

5

10

15

201

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

5-y

ear

ro

llin

g o

f fa

cto

r re

turn

(%

, an

nu

aliz

ed

)5-year rolling factor premium in the US market

8%

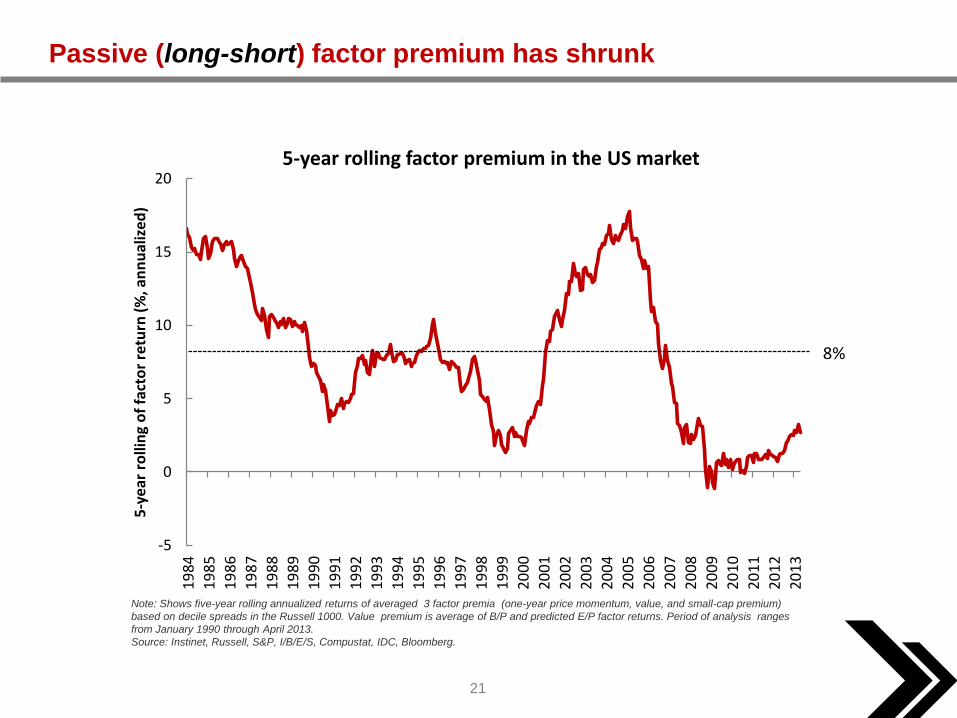

Passive (long-short) factor premium has shrunk

Note: Shows five-year rolling annualized returns of averaged 3 factor premia (one-year price momentum, value, and small-cap premium)

based on decile spreads in the Russell 1000. Value premium is average of B/P and predicted E/P factor returns. Period of analysis ranges

from January 1990 through April 2013.

Source: Instinet, Russell, S&P, I/B/E/S, Compustat, IDC, Bloomberg.

22

-20

-10

0

10

20

30

40

19

84

19

85

19

86

19

87

19

88

19

89

19

91

19

92

19

93

19

94

19

95

19

96

19

98

19

99

20

00

20

01

20

02

20

03

20

05

20

06

20

07

20

08

20

09

20

10

20

12

20

13

5-y

ear

ro

llin

g re

turn

(%

, an

nu

aliz

ed

)5-year rolling factor premium in the US

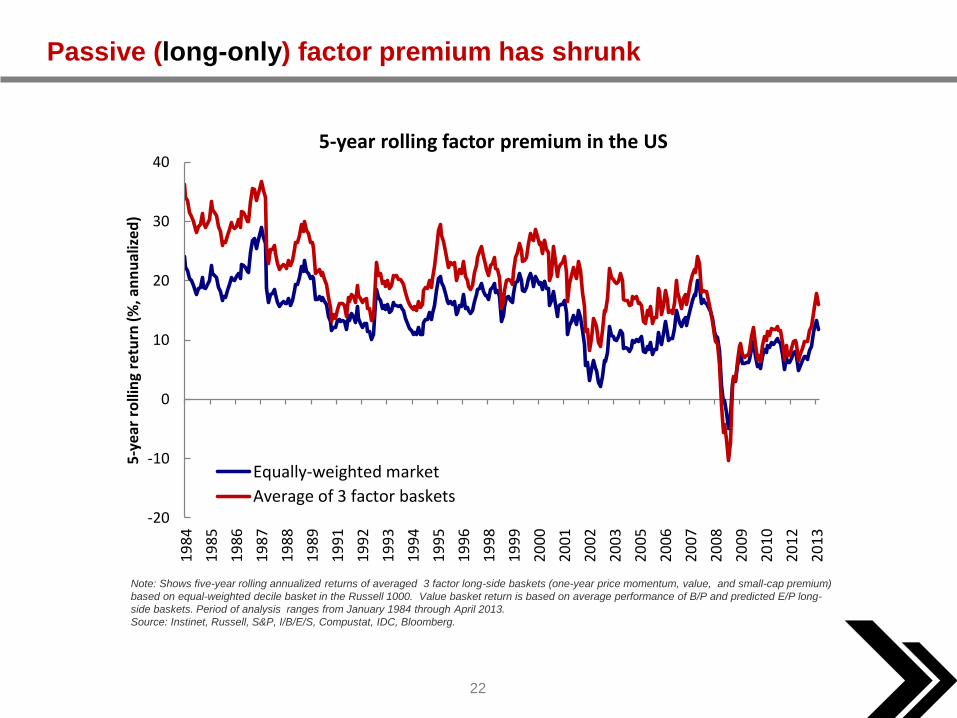

Equally-weighted market

Average of 3 factor baskets

Passive (long-only) factor premium has shrunk

Note: Shows five-year rolling annualized returns of averaged 3 factor long-side baskets (one-year price momentum, value, and small-cap premium)

based on equal-weighted decile basket in the Russell 1000. Value basket return is based on average performance of B/P and predicted E/P long-

side baskets. Period of analysis ranges from January 1984 through April 2013.

Source: Instinet, Russell, S&P, I/B/E/S, Compustat, IDC, Bloomberg.

23

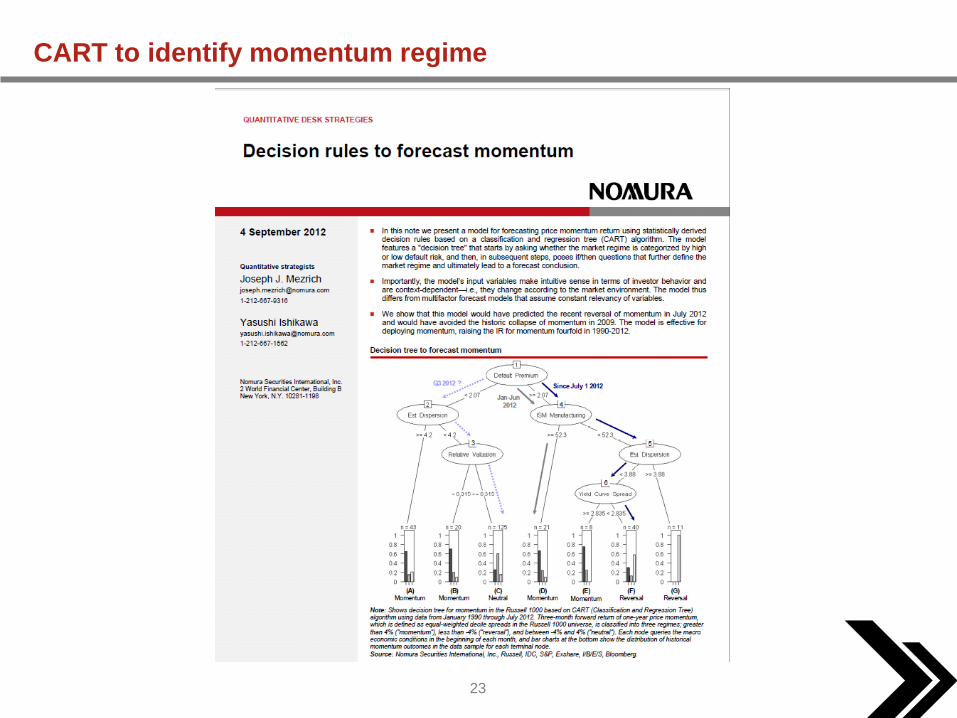

CART to identify momentum regime

24

-50

50

150

250

350

450

550

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Cu

mu

lati

ve r

etu

rn (

%)

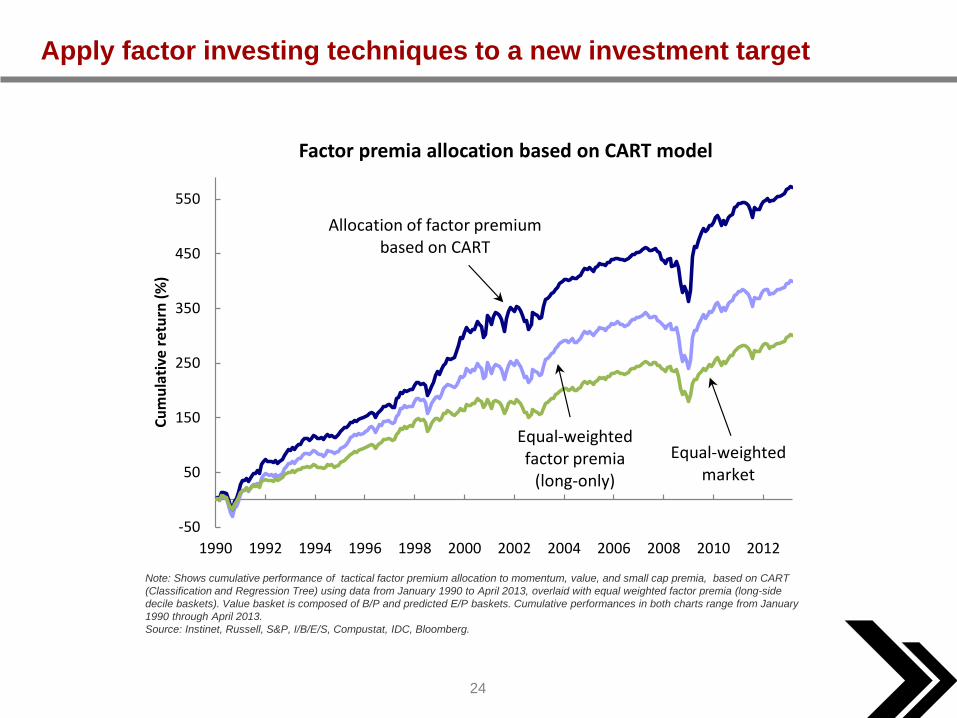

Factor premia allocation based on CART model

Allocation of factor premiumbased on CART

Equal-weightedfactor premia

(long-only)

Equal-weightedmarket

Apply factor investing techniques to a new investment target

Note: Shows cumulative performance of tactical factor premium allocation to momentum, value, and small cap premia, based on CART

(Classification and Regression Tree) using data from January 1990 to April 2013, overlaid with equal weighted factor premia (long-side

decile baskets). Value basket is composed of B/P and predicted E/P baskets. Cumulative performances in both charts range from January

1990 through April 2013.

Source: Instinet, Russell, S&P, I/B/E/S, Compustat, IDC, Bloomberg.

25

The institutional investment paradigm is in motion

26

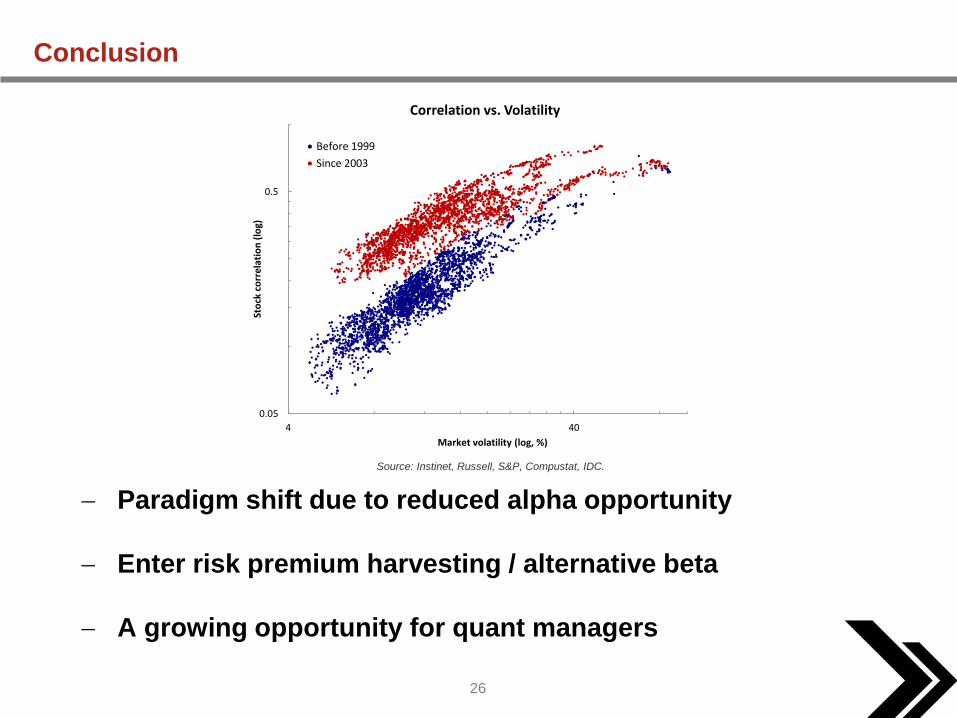

Conclusion

Paradigm shift due to reduced alpha opportunity

Enter risk premium harvesting / alternative beta

A growing opportunity for quant managers

Source: Instinet, Russell, S&P, Compustat, IDC.

0.05

0.5

4 40

Sto

ck c

orr

ela

tio

n (

log)

Market volatility (log, %)

Correlation vs. Volatility

Before 1999

Since 2003

27

Disclaimer

©2013, Instinet Incorporated and its subsidiaries. All rights reserved. INSTINET is a registered trademark in the United States and other countries throughout the world. This material is

provided for informational purposes only and does not constitute an offer, solicitation, or recommendation with respect to the purchase or sale of any security. It does not take into

account the particular investment objectives, financial situation or needs of individual clients. Approved for distribution: in Australia by Instinet Australia Pty Limited (ACN: 131 253 686

AFSL No: 327834), which is regulated by the Australian Securities & Investments Commission; in Canada by Instinet Canada Limited and Instinet Canada Cross Limited, members

IIROC/CIPF; in Europe by Instinet Europe Limited, which is authorized and regulated by the Financial Services Authority; in Hong Kong by Instinet Pacific Limited, which is authorized

and regulated by the Securities and Futures Commission of Hong Kong; in Singapore by Instinet Singapore Services Private Limited, which is regulated by the Monetary Authority of

Singapore, a trading member of The Singapore Exchange Securities Trading Private Limited and a clearing member of The Central Depository (Pte) Limited; and in the US by Instinet,

LLC, member SIPC. For institutional investor use only.