Embed Size (px)

Citation preview

© Copyright 2015 RBN Energy

Propane Winter Outlook

Kelly Van HullOctober 6, 2015

2015 Winter Energy Outlook Conference

2© Copyright 2015 RBN Energy

» Propane Market Overview Crude Oil, Natural Gas, and Natural Gas Liquids

Production

Trends – Historical and Post Crude Oil Price Collapse

» Propane Outlook Propane Supply/Demand Balance

Project Developments

Weather Sensitivities

Pricing & Price Relationships

Conclusions

3© Copyright 2015 RBN Energy

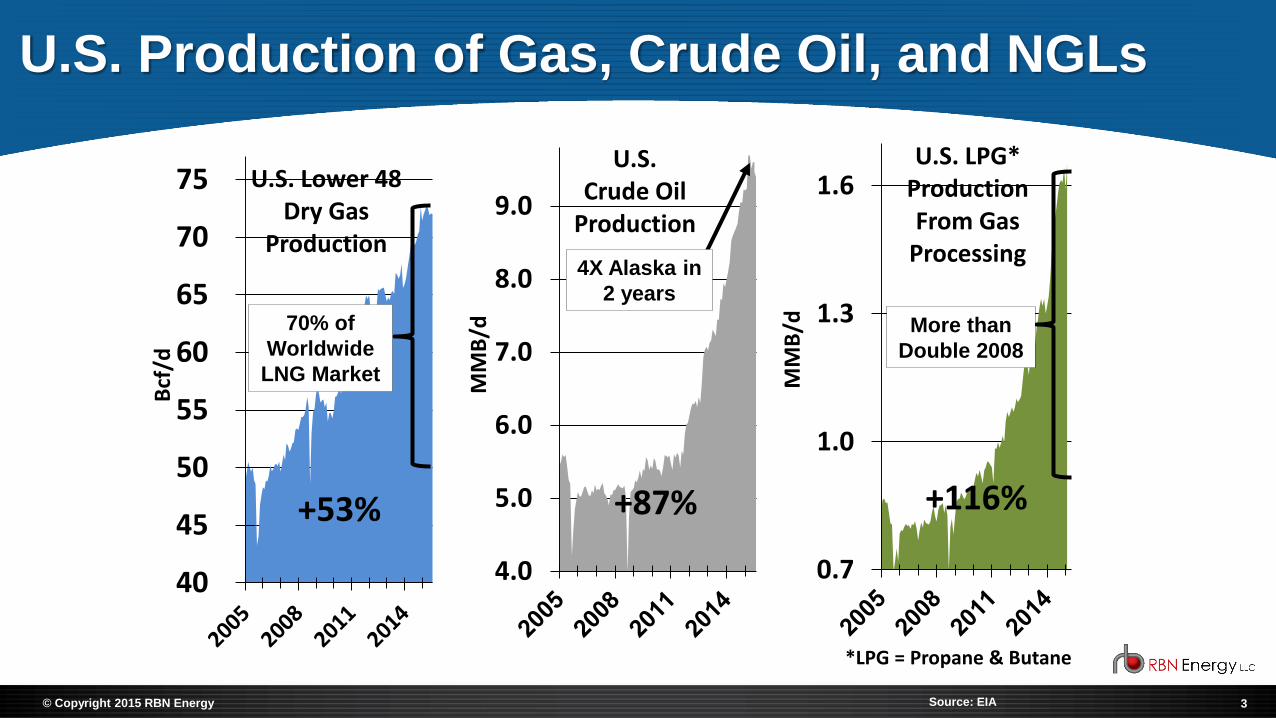

U.S. Production of Gas, Crude Oil, and NGLs

4.0

5.0

6.0

7.0

8.0

9.0

MM

B/d

U.S. Crude Oil

Production

+87%

4X Alaska in

2 years

Source: EIA

40

45

50

55

60

65

70

75B

cf/d

U.S. Lower 48 Dry Gas

Production

70% of

Worldwide

LNG Market

+53%

0.7

1.0

1.3

1.6

MM

B/d

U.S. LPG* Production From Gas

Processing

+116%

*LPG = Propane & Butane

More than

Double 2008

4© Copyright 2015 RBN Energy

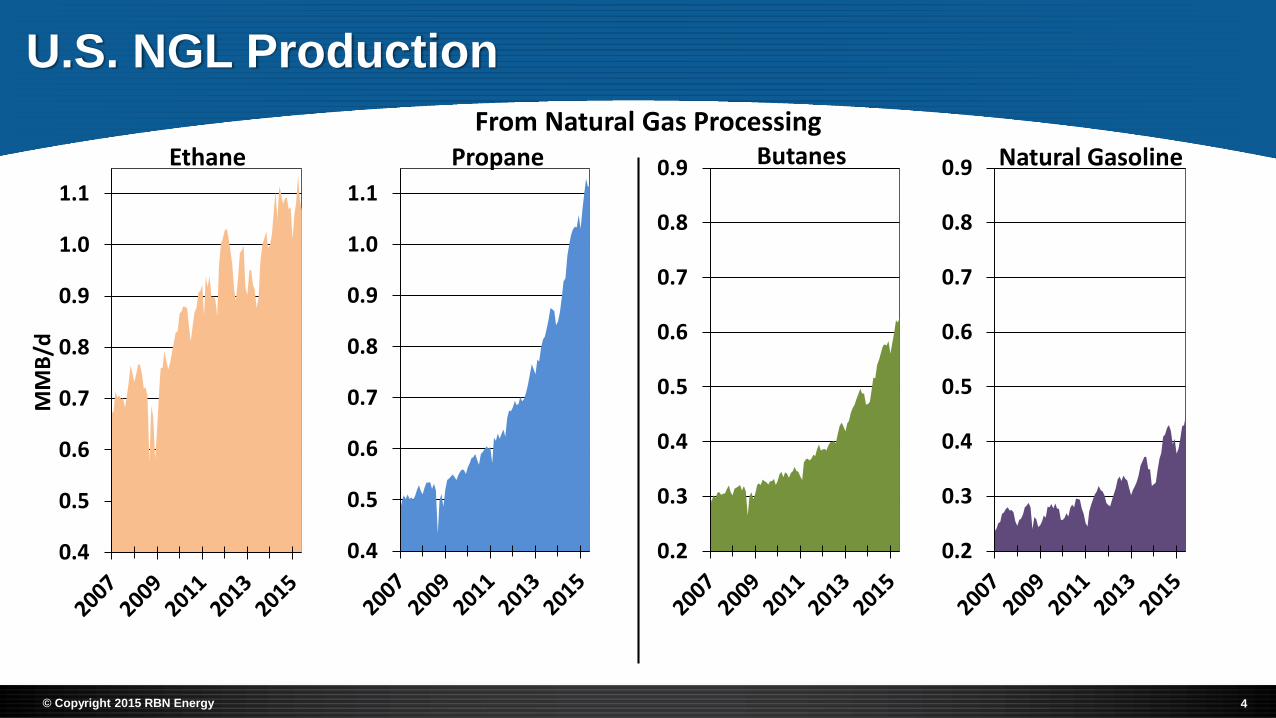

U.S. NGL Production

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9 Butanes

From Natural Gas Processing

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9 Natural Gasoline

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

Propane

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

MM

B/d

Ethane

5© Copyright 2015 RBN Energy

PADD 1 (Northeast) Gas Plant NGL Production Through June 2015

0

25

50

75

100

125

MB

/d

Ethane and Propane

Propane

Ethane

0

5

10

15

20

25

30

35

40

45

MB

/d

Butanes

Normal Butane

Isobutane

0

5

10

15

20

25

30

35

MB

/d

Pentanes+

6© Copyright 2015 RBN Energy

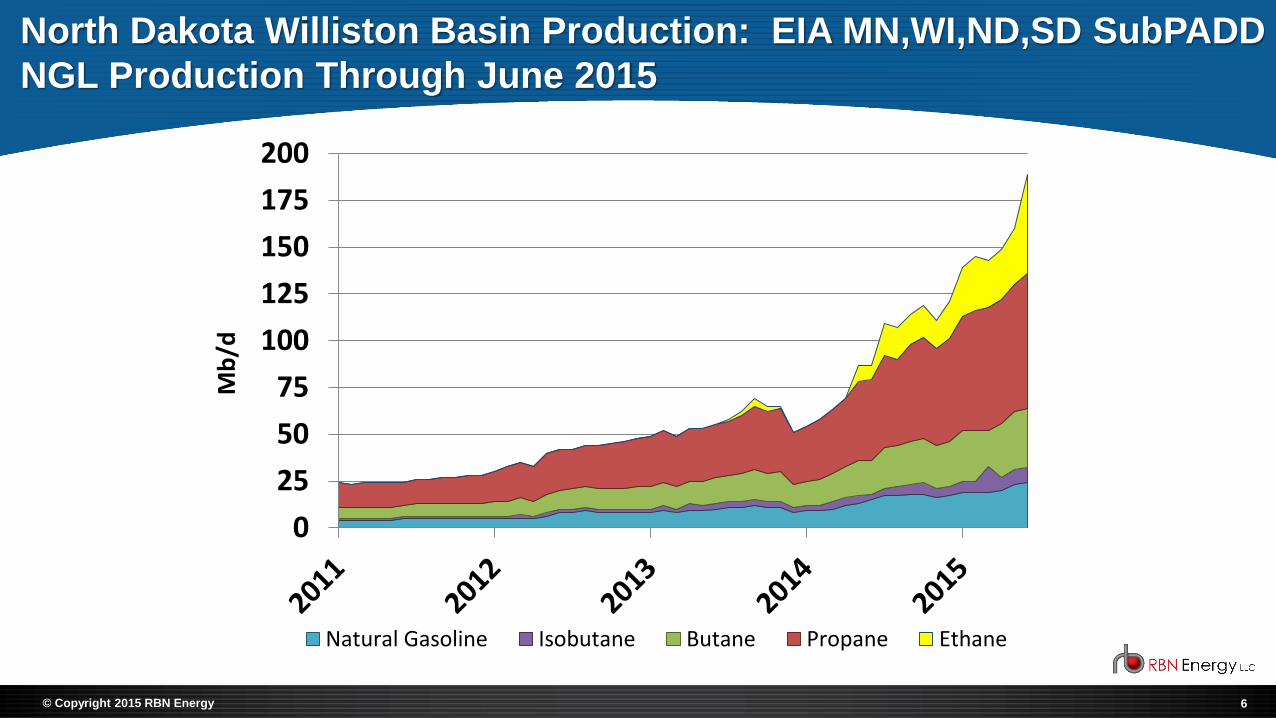

North Dakota Williston Basin Production: EIA MN,WI,ND,SD SubPADD

NGL Production Through June 2015

0

25

50

75

100

125

150

175

200

Mb

/d

Natural Gasoline Isobutane Butane Propane Ethane

7© Copyright 2015 RBN Energy

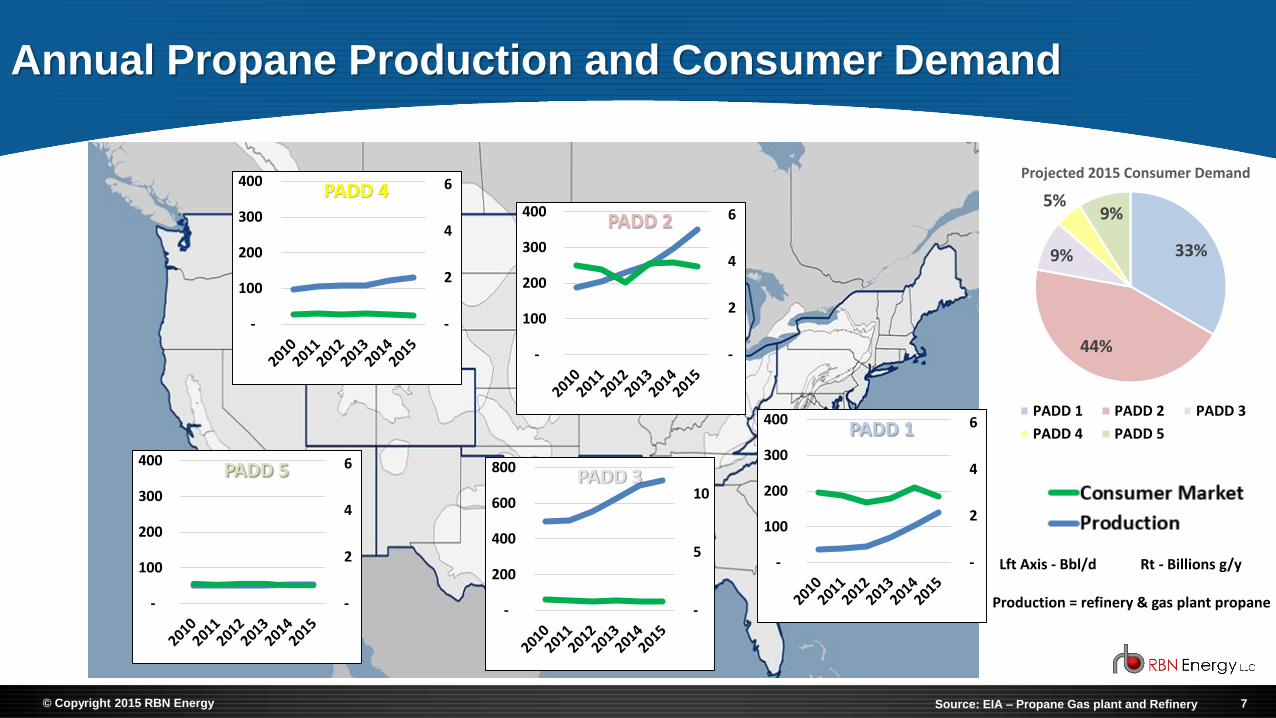

Annual Propane Production and Consumer Demand

-

2

4

6

-

100

200

300

400

Mill

ion

sPADD 1

-

2

4

6

-

100

200

300

400

Mill

ion

sPADD 2

-

5

10

-

200

400

600

800

Mill

ion

sPADD 3

-

2

4

6

-

100

200

300

400

Mill

ion

sPADD 4

-

2

4

6

-

100

200

300

400

Mill

ion

sPADD 5

33%

44%

9%

5%9%

Projected 2015 Consumer Demand

PADD 1 PADD 2 PADD 3

PADD 4 PADD 5

Lft Axis - Bbl/d Rt - Billions g/y

Source: EIA – Propane Gas plant and Refinery

Production = refinery & gas plant propane

8© Copyright 2015 RBN Energy

U.S. Gas Plant and Refinery Supply of Propane

0

200

400

600

800

1000

1200

1400

1600

Mb

/d

Gas Plants Refineries

9© Copyright 2015 RBN Energy

Mont Belvieu Propane Prices 2012-15 YTD

0

20

40

60

80

100

120

140

160

180

c/ga

l

Propane

10© Copyright 2015 RBN Energy

0

100

200

300

400

500

c/g

al

Mont Belvieu

Propane Prices 2012-15 YTD

0

100

200

300

400

500

c/g

al

Conway

11© Copyright 2015 RBN Energy

U.S. Propane Market Developments 2011 to 2014

0

200

400

600

800

1,000

1,200

1,400

1,600

Mb

/d

Petchem Demand PDH Heating Demand Exports

12© Copyright 2015 RBN Energy

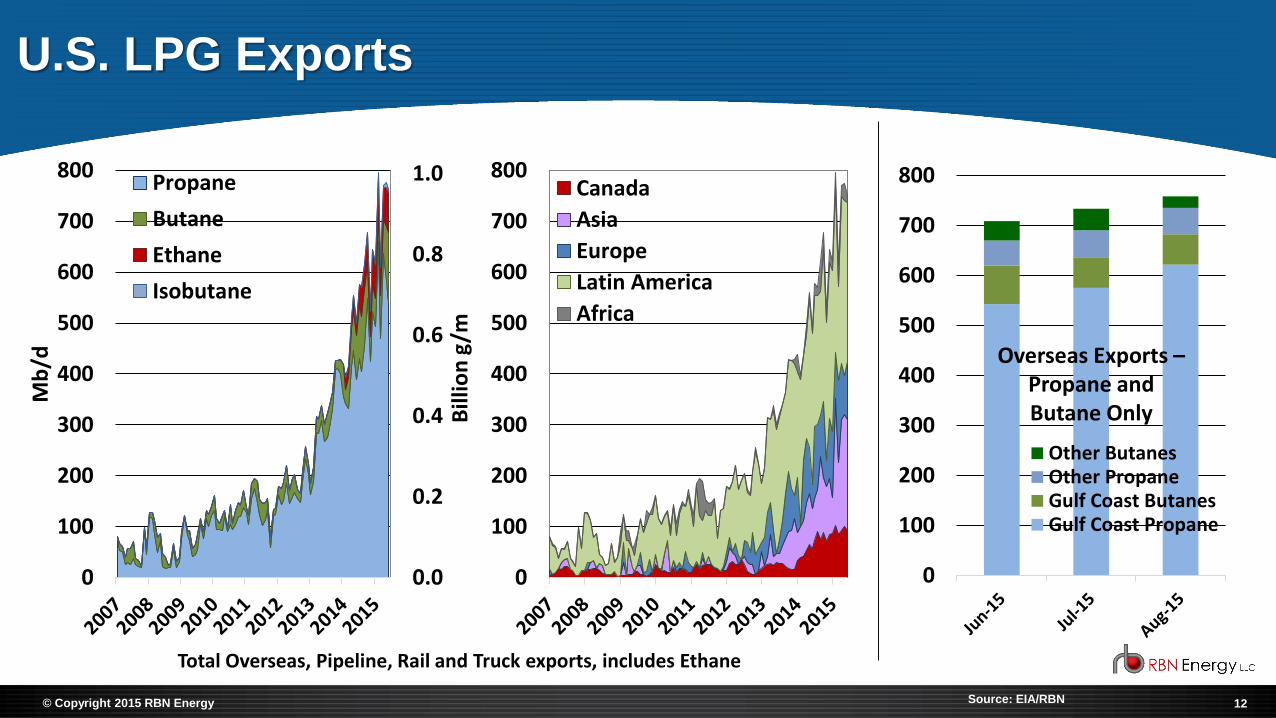

U.S. LPG Exports

Source: EIA/RBN

0

100

200

300

400

500

600

700

800Canada

Asia

Europe

Latin America

Africa

0.0

0.2

0.4

0.6

0.8

1.0

0

100

200

300

400

500

600

700

800

Mb

/d

Propane

Butane

Ethane

Isobutane

Bill

ion

g/m

0

100

200

300

400

500

600

700

800

Tho

usa

nd

s

Other ButanesOther PropaneGulf Coast ButanesGulf Coast Propane

Overseas Exports –Propane and Butane Only

Total Overseas, Pipeline, Rail and Truck exports, includes Ethane

13© Copyright 2015 RBN Energy

Petrochemical Cracker Margins 2007 - 09/2015

0

10

20

30

40

50

60

0

10

20

30

40

50

60

Cn

ts/l

b

Ethane

Propane

Butane

Natural Gasoline (Naphtha)

14© Copyright 2015 RBN Energy

Percent of U.S. Feedstocks

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Vo

l% o

f Fe

ed

U.S. Ethylene Feedstocks

Ethane Propane Butane Naphtha Gas Oil

15© Copyright 2015 RBN Energy

Flexible Steam Crackers Can Switch Feedstocks Relatively

Quickly as Market Dynamics Shift

0

200

400

600

800

1,000

Mb

/d

Ethane Propane Butane Naphtha Gas Oil

• Propane consumption fell 100 Mb/d in 3 months and nearly 200 Mb/d in 7 months in 2013

• Butane consumption has not exceeded 150 Mb/d despite being a favored feedstock most of 2015

16© Copyright 2015 RBN Energy

The Perfect Storm: Res/Com Propane Demand 2013-14

0

1

2

3

4

5

6

7

0

50

100

150

200

250

300

350

400

450

500

Bill

ion

s g

/y

Mb

/d

PADD II

Agriculture Residential and Commercial

0

1

2

3

4

5

6

7

0

50

100

150

200

250

300

350

400

450

500

Bill

ion

s g

/y

Mb

/d

PADD I

Agriculture Residential and Commercial

17© Copyright 2015 RBN Energy

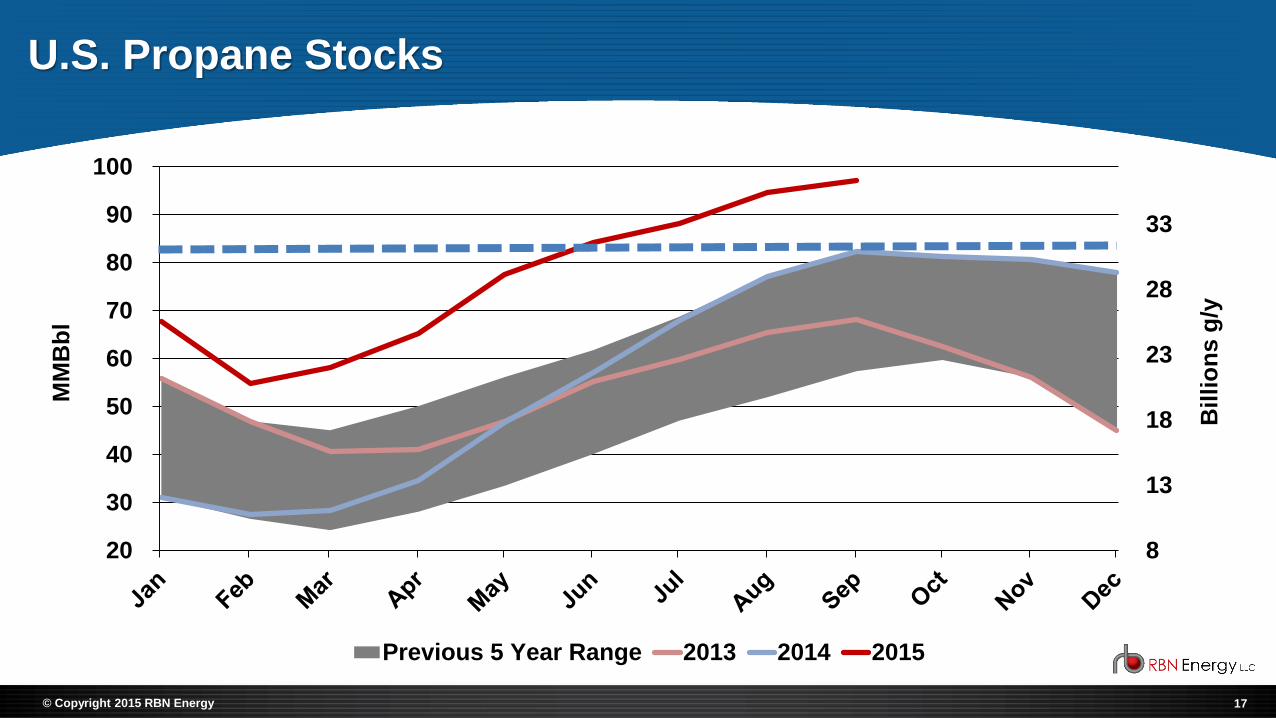

U.S. Propane Stocks

8

13

18

23

28

33

20

30

40

50

60

70

80

90

100

Billi

on

s g

/y

Previous 5 Year Range 2013 2014 2015

MM

Bb

l

18© Copyright 2015 RBN Energy

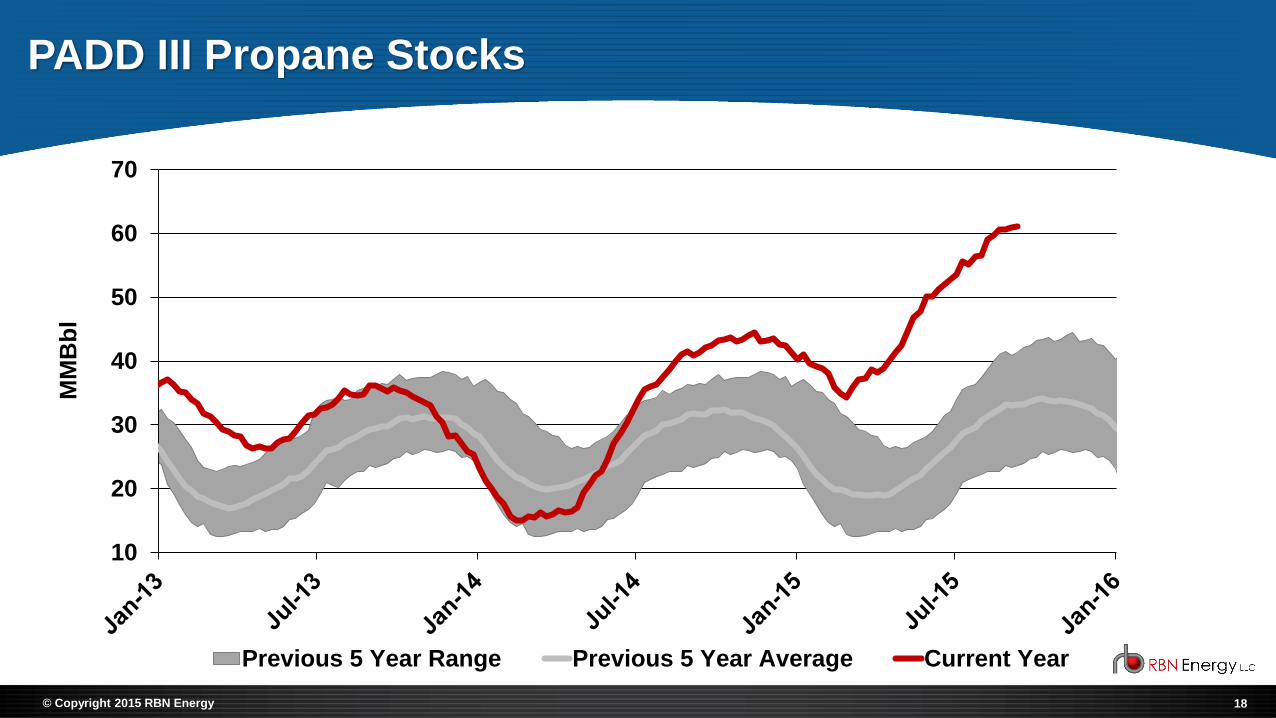

PADD III Propane Stocks

10

20

30

40

50

60

70

Previous 5 Year Range Previous 5 Year Average Current Year

MM

Bb

l

19© Copyright 2015 RBN Energy

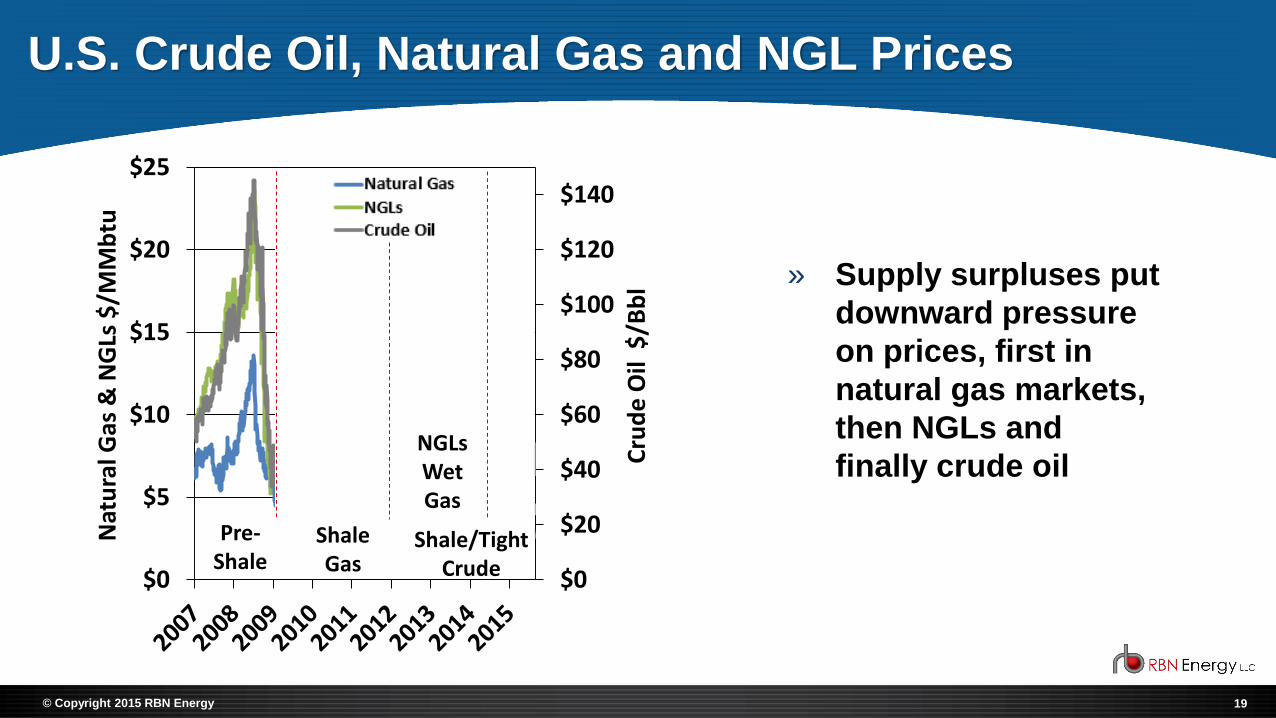

U.S. Crude Oil, Natural Gas and NGL Prices

$0

$20

$40

$60

$80

$100

$120

$140

$0

$5

$10

$15

$20

$25

Cru

de

Oil

$/B

bl

Nat

ura

l Gas

& N

GLs

$/M

Mb

tu

Natural GasNGLsCrude Oil

Pre-Shale

Shale Gas

NGLs Wet Gas

Shale/Tight Crude

» Supply surpluses put

downward pressure

on prices, first in

natural gas markets,

then NGLs and

finally crude oil

20© Copyright 2015 RBN Energy

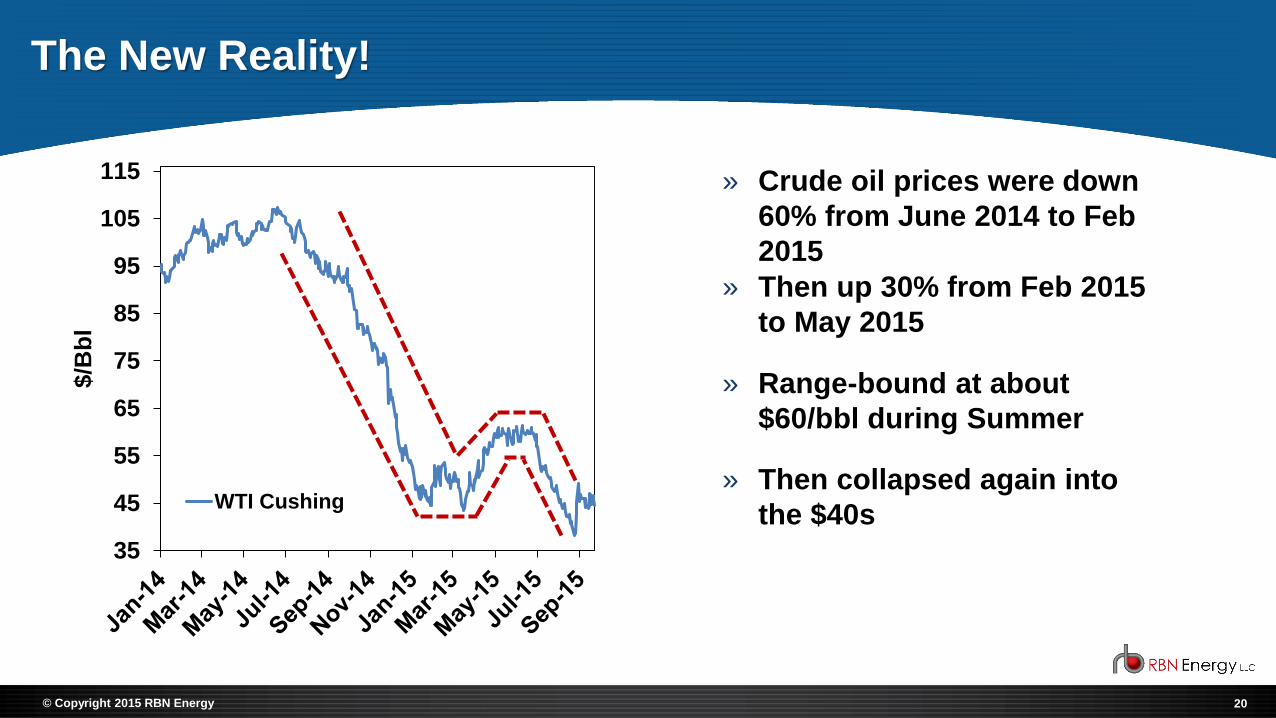

The New Reality!

35

45

55

65

75

85

95

105

115

$/B

bl

WTI Cushing

» Crude oil prices were down

60% from June 2014 to Feb

2015

» Then up 30% from Feb 2015

to May 2015

» Range-bound at about

$60/bbl during Summer

» Then collapsed again into

the $40s

21© Copyright 2015 RBN Energy

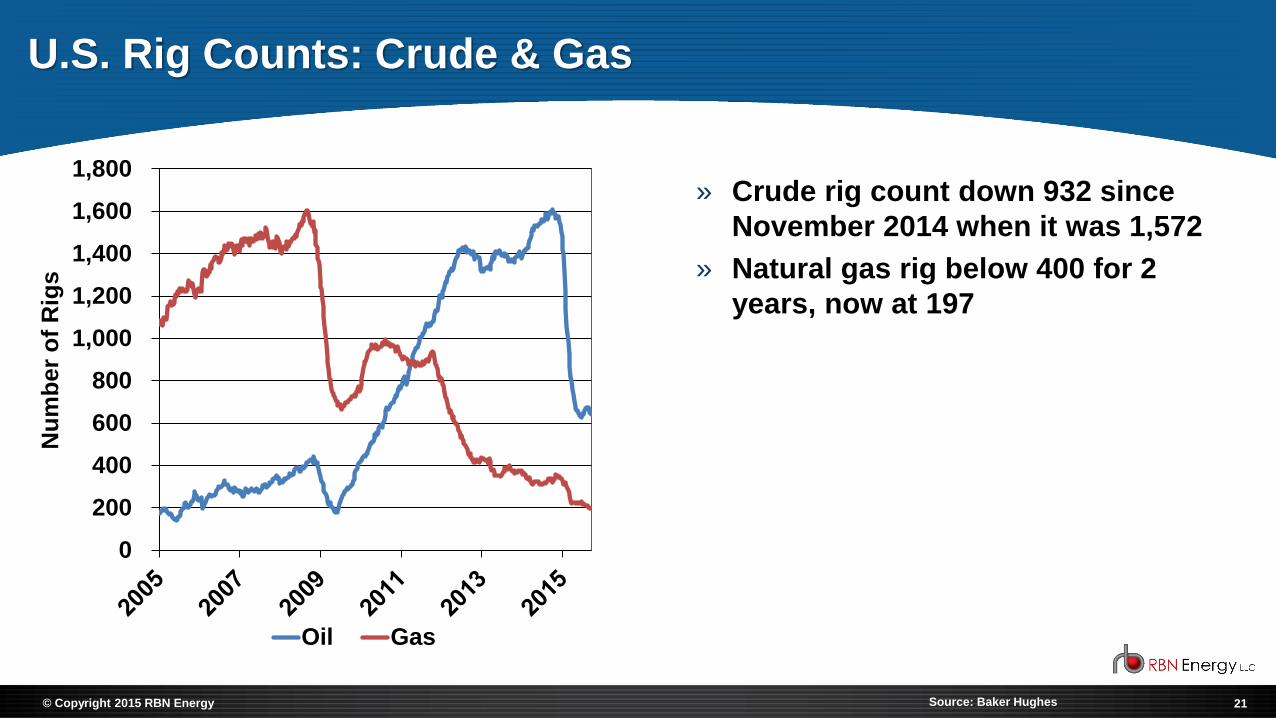

U.S. Rig Counts: Crude & Gas

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Nu

mb

er

of

Rig

s

Oil Gas

» Crude rig count down 932 since

November 2014 when it was 1,572

» Natural gas rig below 400 for 2

years, now at 197

Source: Baker Hughes

22© Copyright 2015 RBN Energy

Gas Production Added Per Rig

0.2

0.6

0.0

0.5

1.0

1.5

2.0

Bakken

+223%

1.1

1.9

0.0

0.5

1.0

1.5

2.0

Eagle Ford

0.2

0.5

0.0

0.5

1.0

1.5

2.0

Permian

4.5

5.8

0

1

2

3

4

5

6

Haynesville

+69%

+113%

+29%

1.4

7.3

0

1

2

3

4

5

6

7

MM

cf/d

Marcellus/Utica

+417%

Source: EIA

23© Copyright 2015 RBN Energy

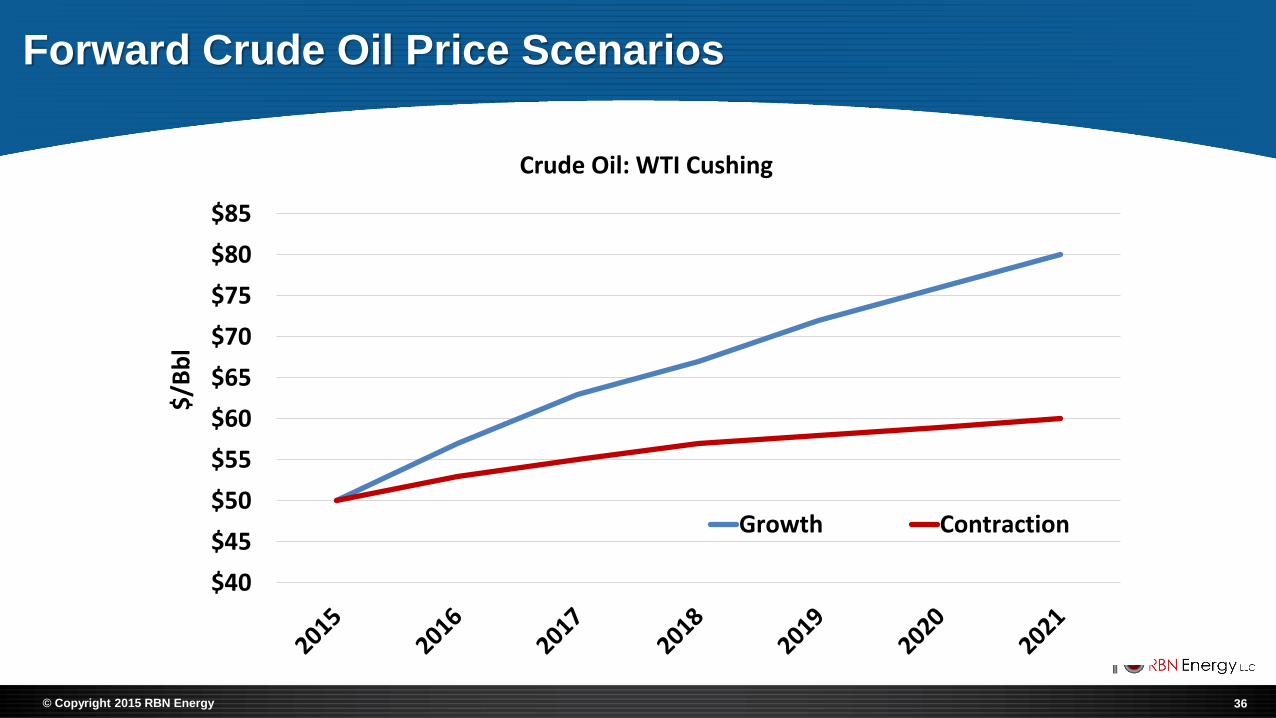

Five Year Crude and Gas Price Scenarios

» Growth Scenario -- WTI

prices return to the $80/bbl

range by 2021; Natural gas

increases to $4.00/MMbtu

» Contraction Scenario -- WTI

prices increase, but only to

average $60/bbl in 2021;

Natural gas prices flat at

$2.75/Mmbtu

» Note: These are not

forecasts; nor are they high

and low cases. They are

possible scenarios used to

understand market responses

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85

$/B

bl

Crude Oil: WTI Cushing

Growth

Contraction$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$/M

Mb

tu

Natural Gas: Henry Hub

Growth

Contraction

24© Copyright 2015 RBN Energy

U.S. Propane Market Length to be Relieved by Petrochemical Demand

and Exports

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

MM

b/d

Petchem Demand PDH Heating Demand Exports

Growth Scenario

Contraction Scenario

25© Copyright 2015 RBN Energy

Propane Dehydrogenation Capacity

0

50

100

150

200

250P

rop

ane

De

man

d M

b/d

Petrologistics Enterprise Dow Formosa REXpro Sunoco - Marcus Hook Ascend

Contraction Scenario

Growth Scenario

26© Copyright 2015 RBN Energy

Growth Case - Gulf Coast LPG Export Capacity vs. Gulf Coast

Export Volumes

0

200

400

600

800

1,000

1,200

1,400

MB

/D

Propane Butane Pre-Existing

Enterprise Targa Other

Other:• ETC Mariner South - 2015• Oxy - 2015• Phillips -2016

27© Copyright 2015 RBN Energy

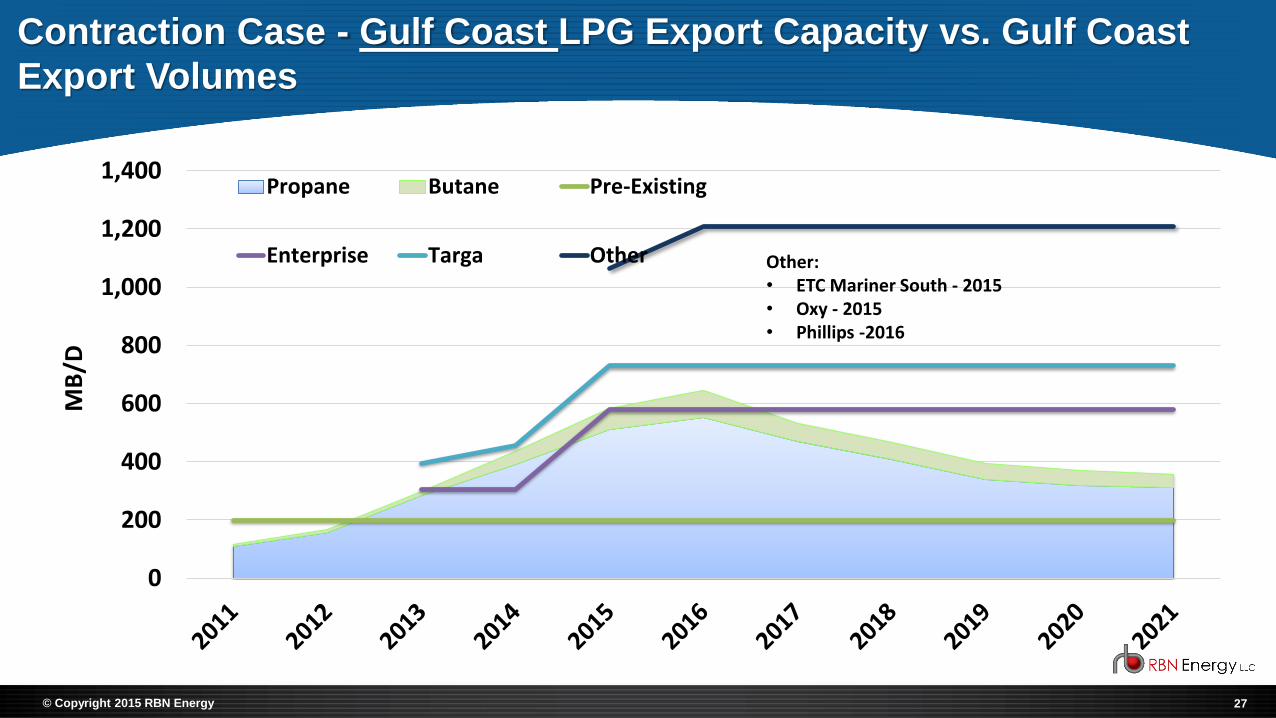

Contraction Case - Gulf Coast LPG Export Capacity vs. Gulf Coast

Export Volumes

0

200

400

600

800

1,000

1,200

1,400

MB

/D

Propane Butane Pre-Existing

Enterprise Targa Other Other:• ETC Mariner South - 2015• Oxy - 2015• Phillips -2016

28© Copyright 2015 RBN Energy

Marcus Hook LPG Export Capacity vs. Volumes - Growth

0

50

100

150

200

250

300

MB

/D

Propane

Butane

Existing Mariner East

Mariner East II Expansion

* Contracted and forecasted ethane volumes removed from capacity and volumes

29© Copyright 2015 RBN Energy

Marcus Hook LPG Export Capacity vs. Volumes - Contraction

0

50

100

150

200

250

300

MB

/D

Propane

Butane

Existing Mariner East

Mariner East II Expansion

* Contracted and forecasted ethane volumes removed from capacity and volumes

30© Copyright 2015 RBN Energy

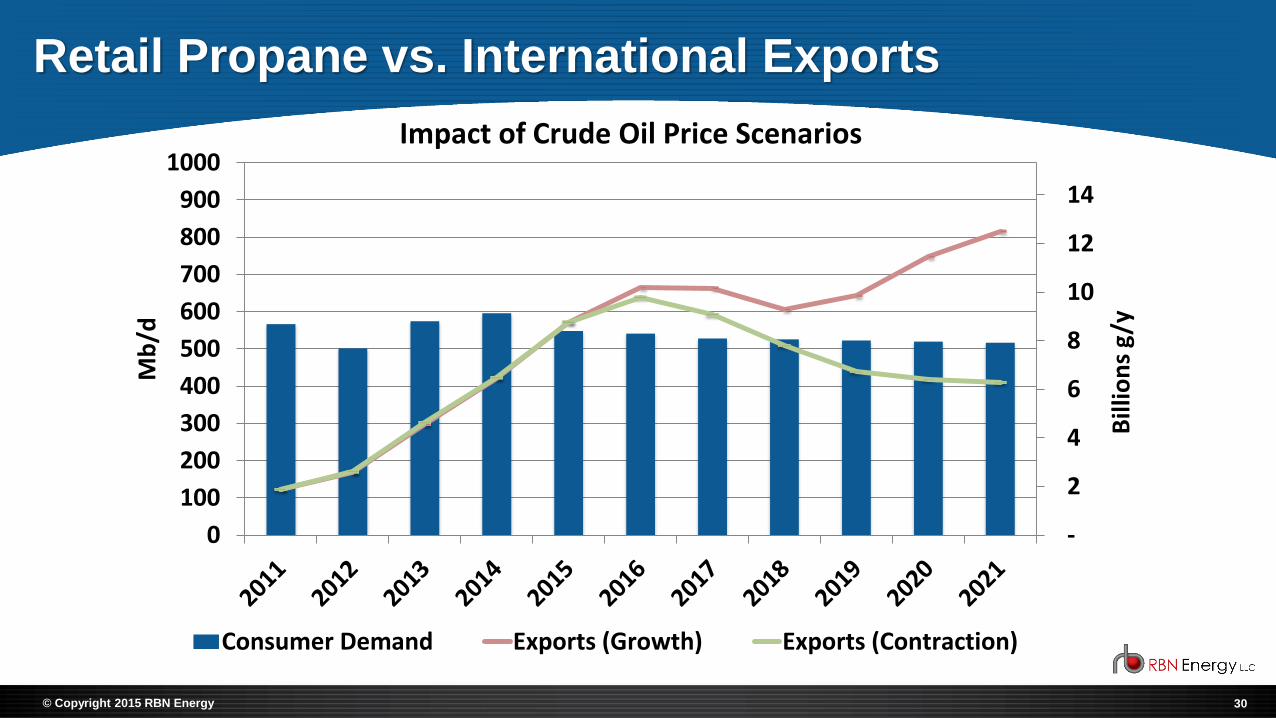

Retail Propane vs. International Exports

-

2

4

6

8

10

12

14

0

100

200

300

400

500

600

700

800

900

1000

Bill

ion

s g

/y

Mb

/d

Consumer Demand Exports (Growth) Exports (Contraction)

Impact of Crude Oil Price Scenarios

31© Copyright 2015 RBN Energy

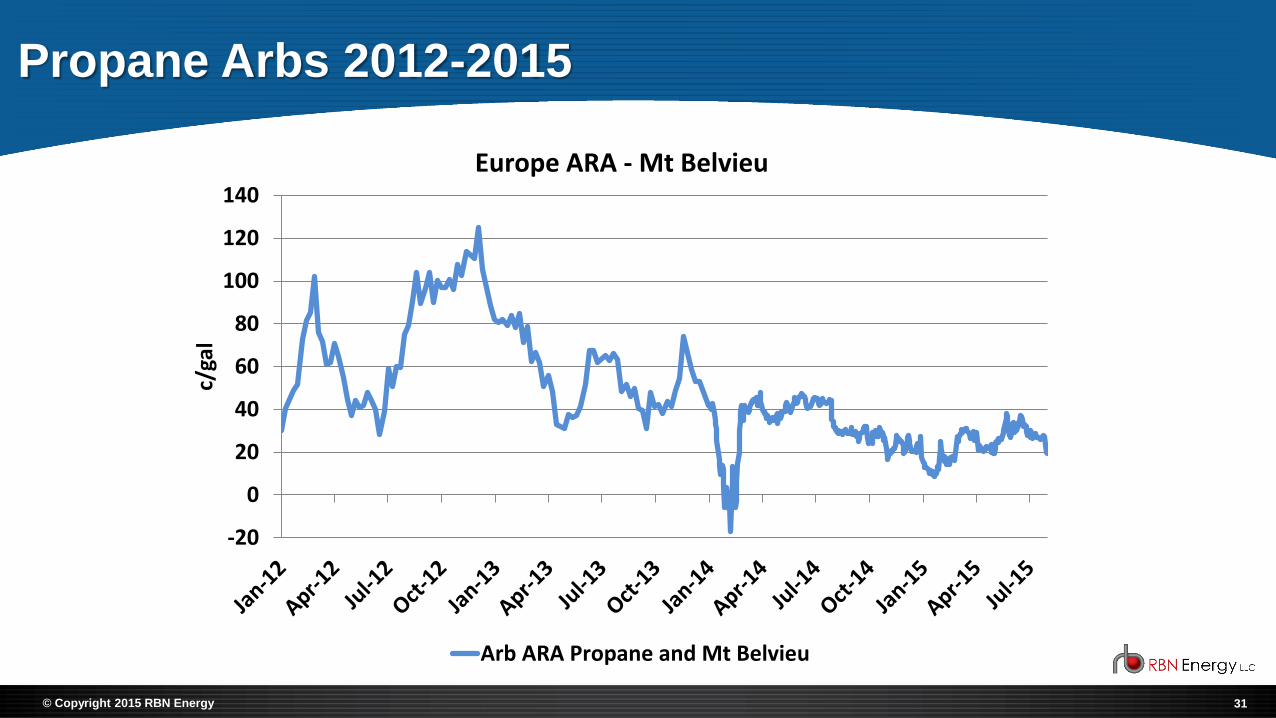

Propane Arbs 2012-2015

-20

0

20

40

60

80

100

120

140c/

gal

Europe ARA - Mt Belvieu

Arb ARA Propane and Mt Belvieu

32© Copyright 2015 RBN Energy

U.S. LPG Export Terminal Contracts

» Rates: Loading rates have varied over the last 3 years and are dependent on

market conditions when the contracts are negotiated. Long term rates at Enterprise

and Targa ranged from 14 – 20 cents per gallon for contracts negotiated before the

market decline in late 2014. Current rates are 8 – 10 cents per gallon.

» Term: LPG export terminal contracts vary in length from a minimum of 1 year

to as long as 10 years. Terms have been getting shorter; typical term today is 1-3

years. These term contracts usually have an evergreen rollover provision with a

cancellation notice period of 60-90 days.

» Commitment: Export term contracts are negotiated on a take or pay basis for

the total volume commitment. The penalties for cancellation can have a decreased

liability dependent on the time of notification before the loading window. (e.g., 45

days notice 75% penalty, 30 days notice 80% penalty, 15 days notice 90% penalty,

less than 15 days 100% of the contract).

» Seasonality: Most LPG export contracts are not affected by seasonal

demand since they are with year round end users. (ethylene crackers, PDH plants,

cooking/auto, or power generation).

» Panama Canal: The most dramatic change in LPG exports will occur in mid

2016 with the opening of the new expansion of the Panama Canal. This will allow

VLGC vessels to traverse the canal for voyages to the Far East. Currently only a

specialized Panamax vessel can go through the Panama Canal.

33© Copyright 2015 RBN Energy

VLGC Fleet (60,000-85,000 CBM)

» Fleet: 170 units

» Fleet age 25+: 4%

» Orderbook: 96 units

19%

38%15%

9%

15%

1% 3%VLGC Age Profile

0-4

5-9

10-14

15-20

21-25

26-30

30+

170

26

55

11 40246810121416

020406080

100120140160180

Mill

ion

CB

M

Nu

mb

er

VLGC Fleet and Orderbook

Number Cbm

34© Copyright 2015 RBN Energy

PADD 1 – Weather Sensitivities - Contraction

-60

-10

40

90

140

190

240

-50

0

50

100

150

200

Mill

ion

s g/

m

Mb

bl/

d

Net Receipts*

Net Receipts - Normal Weather

Net Receipts - Polar Vortex

0

1

2

3

4

5

6

7

MM

bb

l

Inventories

Last 5 year Range 13-14

14-15 15-16

16-17 PV - 16-17

* Or decreased exports

35© Copyright 2015 RBN Energy

PADD 2 – Weather Sensitivities - Contraction

50

70

90

110

130

150

170

190

210

40

60

80

100

120

140

160

180

Mill

ion

s g/

m

Mb

bl/

d

Net Deliveries

Net Deliveries - Normal Weather

Net Deliveries - Polar Vortex

0

5

10

15

20

25

30

35

MM

bb

l

Inventories

Last 5 year Range 13-14

14-15 15-16

16-17 PV - 16-17

36© Copyright 2015 RBN Energy

Forward Crude Oil Price Scenarios

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85$

/Bb

lCrude Oil: WTI Cushing

Growth Contraction

37© Copyright 2015 RBN Energy

Propane Price and Ratio to WTI

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$/G

al

Price

Growth

Contraction

20%

25%

30%

35%

40%

45%

50%

55%

60%

65%

70%Ratio to Crude Oil

Growth Contraction

38© Copyright 2015 RBN Energy

» Propane inventories are currently at historical highs, keeping

prices low

» Given the combination of winter heating demand, rising export

volumes with Enterprise’s export facility expansion coming

online, along with Dow’s PDH unit starting up in 2015 propane

inventories will draw in the coming months tightening up

propane’s price relationship to crude

» It will likely be summer 2016 before aggregate U.S. inventories

return to more normal levels

» With increasing production near demand regions, better

connectivity from both pipeline and rail, and export volumes

that can be bid away from global markets, the U.S. propane

industry is in much better position to handle a Perfect Storm of

events than it was in the Winter of 2013-14.

39© Copyright 2015 RBN Energy

Kelly Van Hull2323 South Shepherd, Suite 1010

Houston, TX, 77019www.rbnenergy.com