Embed Size (px)

Citation preview

Profit Strategies of Automobile Firms and China, 1980-2008

Freyssenet MichelCNRS Paris

GERPISA international network

Panel 14: International Comparison of the Chinese Auto IndustrySession II: International Experience, dealing with Environmental

Changes for Auto IndustryOrganizer(s): Institute of National Economy in Shanghai Academy of

Social Sciences, Shanghai Auto Strategy Research Centre

The 3rd World Forum on China Studies, Shanghaï, 8-9 september 2008 “The economic theories and policies toward social harmony: China and Asia's

experiences”Shanghai Academy of Social Sciences

The firsts to try, the lasts to succeed

• Renault-AMC was the first foreign carmaker to create a joint-venture with a chinese auto producer in 1983.. PSA was the first with VW to invest significantly in China in the mid of the eighties.

• After, Renault renounced to produce until now. The Dongfeng Peugeot Citroën is only the ninth cars producer today in China.

• Volkswagen (Shanghaï VW and FAW VW) is now the first with GM, a surprising lastcomer.

• The purpose of this research is to understand these divergent trajectories in China

Argument

• The constraints were the sames for Volkswagen which succeed and for PSA and Renault which failed: the bureaucratic slowness, the variations of the Chinese automobile policy, the risk of political changes…

• So the reasons given to explain the difficulties encountered insist generally on the cultural misunderstandings, the mutual lack of trust, the insufficient own government support, the errors of product policy, the lack of performant suppliers…

• But, all things considered, we can observe the cultural differences, the suspicion, the errors… are different but as important for Germans as for the Frenchs

• So we must find other and clearer explanations

Proposal

• The customary explanations presuppose that the three European carmakers were in the same internal and contextual conditions to face the difficulties. It wasn’t the case.

• So, we will try to show the necessity to take the trajectory of each carmaker and its profit strategy into account

The profit strategies of the three European

carmakers• Renault implemented the « volume and diversity » strategy since the fifties. But it wasn’t able to pursue it after the second oil crisis

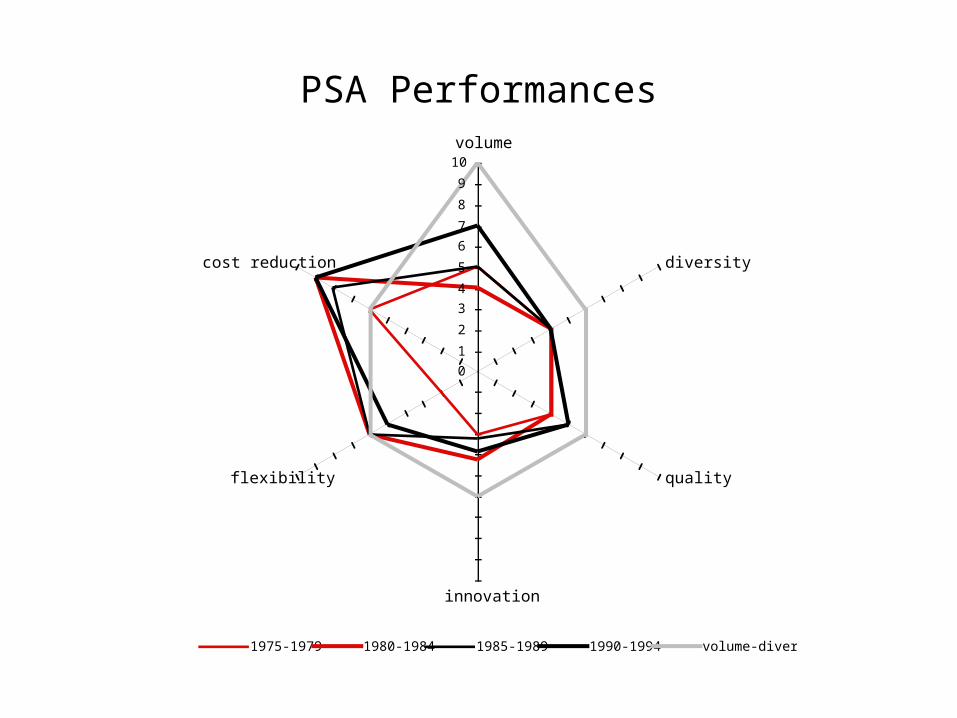

• PSA and VW adopted for the first time this profit strategy in the seventies

• PSA failed to develop it until the nineties. VW succeed to do it immediately

Why so different capabilities?

The « volume and diversity » profit strategy and its macro and

micro conditions• This strategy privileges and combines two of six

possible sources of profit: economies of scale for non-visible components and economies of scope for visible components. The other sources: quality, innovation, flexibility and permanent cost reduction are exploited also but secondarly

• This strategy, to be effectively profitable, needs a demand constantly increasing and moderatly hierarchized. It is the case when the national income distribution is « coordinated and moderatly hierarchized »

• When the market is mature, the economies of scale can be obtained sharing the platforms of more car models and brands. That was necessary after the oil shocks

The divergence of macro-conditions

• France and Germany had the same national income distribution: coordinated and moderatly hierar-chized, but the growth of France was consumer-oriented and Germany’s export-oriented

• France knew an economic crisis after the oil skocks, Germany much less strong

• The demand slowed in France and began to become more heterogenous. Much less in Germany

• So the possibility to pursue profitably the « volume and diversity » strategy became different

The micro-conditions

• To find the necessary supplementary volume, Renault took over American Motors Company in 1980 and decided to compete with the Big Three on their own market. But the structure of the North American market changed dramatically in the eighties. Heavely in debt, Renault was obliged to sale AMC in 1986 and to find a new profit strategy

• PSA purchased successively Citroën and Chrysler Europe. But it was unable to obtain rapidly a sufficient share of the platforms of these brands of which the importance was the same. Strongly in debt also, PSA was obliged to reduce the costs drasticaly during many years

• On the contrary, VW was able to create immediatly common platforms, first with Audi, constitued by little German carmakers it had purchased, after with Seat and Skoda

0

1

2

3

4

5

6

7

8

9

10

volume

diversity

quality

innovation

flexibility

cost reduction

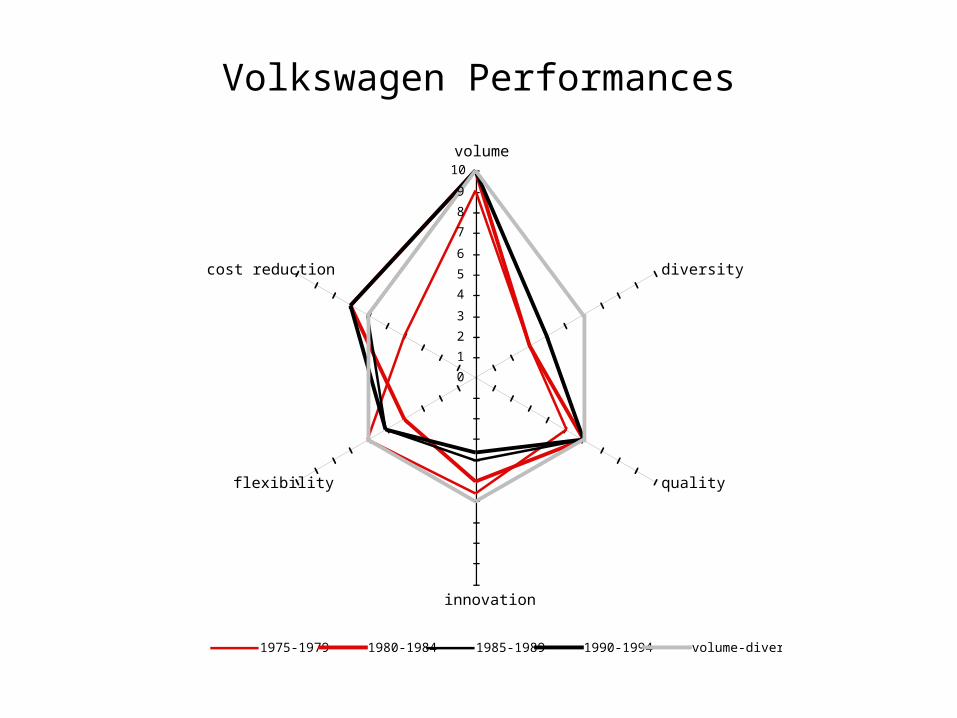

1975-1979 1980-1984 1985-1989 1990-1994 volume-diversity

Volkswagen Performances

0

1

2

3

4

5

6

7

8

9

10

volume

diversity

quality

innovation

flexibility

cost reduction

1975-1979 1980-1984 1985-1989 1990-1994 volume-diversity

PSA Performances

0

1

2

3

4

5

6

7

8

9

10

volume

diversity

quality

innovation

flexibility

cost reduction

1975-1979 1980-1984 1985-1989 1990-1994 innovation-flexibility

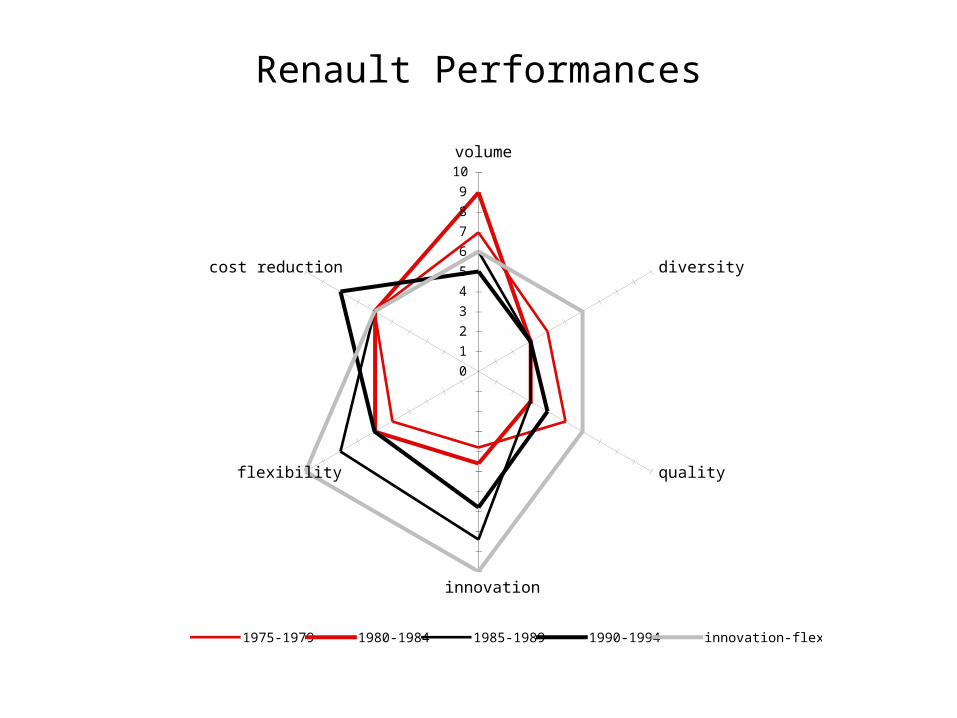

Renault Performances

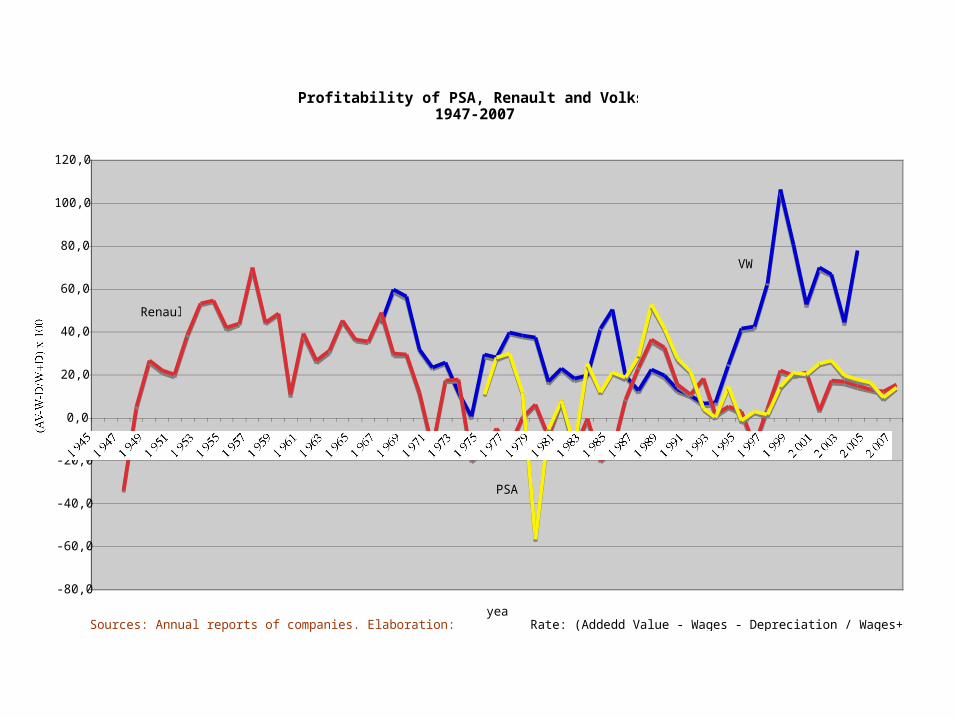

Profitability of PSA, Renault and Volkswagen Groups1947-2007

-80,0

-60,0

-40,0

-20,0

0,0

20,0

40,0

60,0

80,0

100,0

120,0

1 9451 9471 9491 9511 9531 9551 9571 9591 9611 9631 9651 9671 9691 9711 9731 9751 9771 9791 9811 9831 9851 9871 9891 9911 9931 9951 9971 9992 0012 0032 0052 007

year

(AV-W-D/W+D) x 100

VW

PSA

Renault

Sources: Annual reports of companies. Elaboration: JetinB., Freyssenet M. Rate: (Addedd Value - Wages - Depreciation / Wages+Depreciation) x 100

The financial results of these divergent conditions

• VW was constantly profitable. Renault and PSA had losses several times

• The three European carmakers were not in the same capabilities to respond to the requirements of Chinese partners

• VW was able to accept many of them and even to make losses mainwhile the developement of the demand. Renault and PSA was unable to do that

The willingness of Chinese government,

but the lack of means in the eighties

• Chinese government wanted to create quickly a car industry with the help of the foreign carmakers, as the South Koreans were able to do. The aim was to reduce the importations and to impulse a strong industrial devlopment

• But China was short of capital and above all of foreign currency

• So the requirements of Chinese government were to invest significantly for important capacities in assembly and mechanical plants, to engage at least for twenty years, to obtain avantageous loans from the government of foreign carmakers, to adapt the car models and to create specific models, to supply quickly with local parts and to export an increasing percentage of produced cars

• The counterparts for the foreign companies were the perspective of Chinese market and the preference for thus will invest first

The reactions of the foreign carmakers

• Foreign carmakers considered that forecasted plant capacities were irrealistic, being given the uncertainties concerning the level of the demand in the future

• The local suppliers weren’t able to produce parts respecting quality and delay. In these conditions, the cars could not be produced at the international standard

• So, foreign carmakers believed necessary to extend the capacities according to the effective increase of the demand and to import CKD until the local suppliers will be able to obtain the required quality

• The investments were risky. The automobile policy wasn’t completely clear. The evolution of reglementation uncertain. So it was necessary to have a minimum of sure outlets and to be not in direct competition with other foreign and local carmakers. To do that, the local partner in the joint venture must not create joint-venture with other foreign carmakers and not produce its own cars

• But after the positions diverged in the negociations

Renault: an big opportunity impossible to jump at for it

• Renault took over American Motors Company in 1980• AMC created in 1983 with Beijing Automotive Works

the first sino-foreign joint-venture of Chinese car and light truck industry: Beijing Jeep Corporation (31/69). It was a test for many people

• But the JV was decided just before the crisis of Renault and of AMC. The sale of AMC to Chrysler in 1986. The change of profit strategy of Renault

• The crisis of BJC in 1986• Ironically, one year after, Renault knew a

recovery because of the world economic boom at the end of eighties, that would permit to Renault to keep American Motors in its perimeter and to contribute to the Chinese automobile development

Volkswagen: the means to accept and to

wait

• Volkswagen created in 1984 with Shanghaï Automobile & Tractors Industries Corporation (SATIC) a first JV (at 50/50) : Shanghaï Volkswagen (SVW) to produce fleet of taxis (Santana).

• A second JV was created in 1989 with First Automobile Works: FAW-VW (60/40) to produce sedan cars in the M1 segment: Jetta, Golf, Bora…, using the machinery transplanted from the US plant of Westmoreland

• In both cases, VW accepted many Chinese requirements. In fact, the volume increased slowly and the capacities used progressively. But VW could be patient

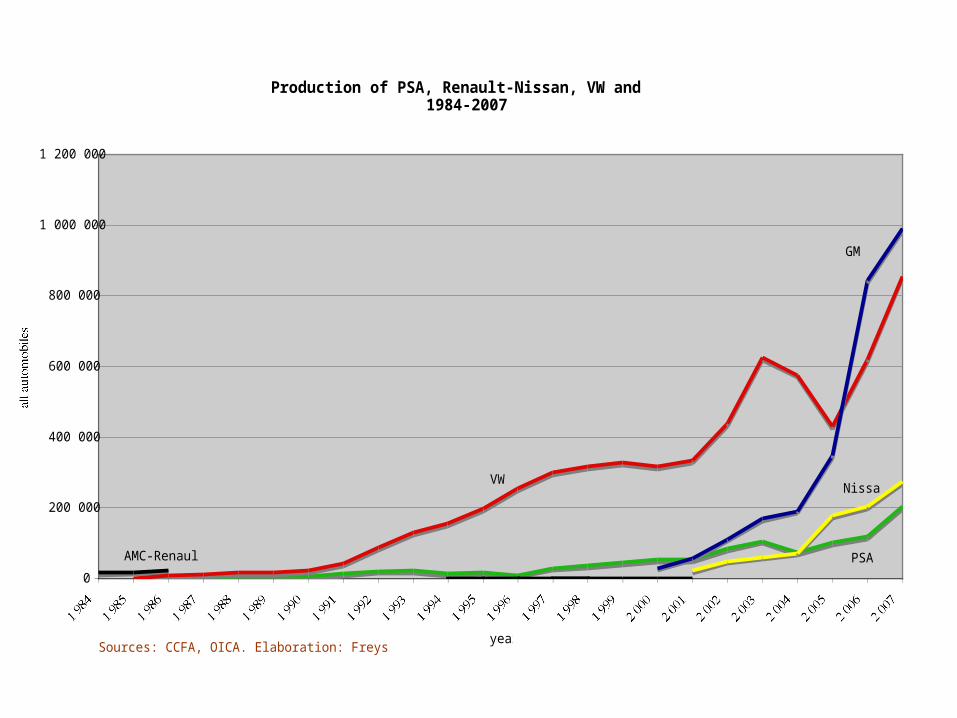

Production of PSA, Renault-Nissan, VW and GM in China1984-2007

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 984 1 985 1 986 1 987 1 988 1 989 1 990 1 991 1 992 1 993 1 994 1 995 1 996 1 997 1 998 1 999 2 000 2 001 2 002 2 003 2 004 2 005 2 006 2 007

year

all automobiles

AMC-Renault

VW

GM

PSA

Nissan

Sources: CCFA, OICA. Elaboration: Freyssenet M., 2008

PSA: against the « irrealistic » clauses

• Peugeot took over Citroën in 1976, but the two carmakers remained relatively independant until 1998 within PSA Group

• Peugot created in 1985 with Guangzhou Automobile manufactory a JV 22/78, the Guangzhou Peugeot Automobile Company, to produce pick-up and sedan cars. The JV was dissolved in 1998

• Citroën, after many abortive projects, was selected in 1988 to create a JV with Dongfeng. For the first time a foreign carmaker had proposed to launch a new model, simultaneously in Europe and in China: the ZX in the M1 segment

• But the CEO of PSA wasn’t in hurry to sign the agreement as much as the « irrealistic » clauses weren’t deleted in the contract

• PSA was just leaving a very deep crisis

PSA achieved to implement profitably the « volume and

diversity » strategy •After 1998, PSA achieved to impose common platforms to his two brands. It multiplied punctual cooperations with other carmakers to obtain new economies of scale and to complete his car models offer. The financial results improved durably•It began to have financial means to invest much more strongly in the emergings markets. Brazil and China were choised. But Brazil before. So PSA, trough DPCA, wasn’t completely ready at the beginning of Chinese market boom• DPCA lacked capacities. But now, PSA have decided to accelerate and rises its volume of production

The « innovation and flexibility » strategy of

Renault and its alliance with

Nissan •After several trials and errors, Renauly choiced to launch innovative cars and so doing to change its profit strategy•The evolution to a « competitive » mode of national income distributions was favourable to the developement of a demand of new types of vehicles •The big success of some innovatice cars of Renault have permitted it to take over Nissan, Dacia and Samsung, after the so-called Asian crisis •Whitin the Renault-Nissan Alliance, Nissan has the priority to develop its activities in China. Renault seems to wait to have attractive and distinctive products to decide an useful and profitable come back.

Volkswagen harvests the fruits of its patience

•With large capacities, FAW-VW and SVW were able to provide the car demand when it boomed in 2003

•But its offer wasn’t renewed in time

•It lost the first position in China market, passing by General Motors, a lastcomer

• The double emergence: the launch of alternative engines and cars and the boom of BRIC automobile market, is preparing a « second automobile revolution »

• What will be the alliance between new industrial actors and automobilized countries to impose a new universal standard of car?

• The battle for this have began

The second automobile revolution

0

5

10

15

20

25

30

35

1 898 1 902 1 906 1 910 1 914 1 918 1 922 1 926 1 930 1 934 1 938 1 942 1 946 1 950 1 954 1 958 1 962 1 966 1 970 1 974 1 978 1 982 1 986 1 990 1 994 1 998 2 002 2 006

year

vehicles (millions)

Americas

Europe

Asia-Oceania

Africa

China

BRIC

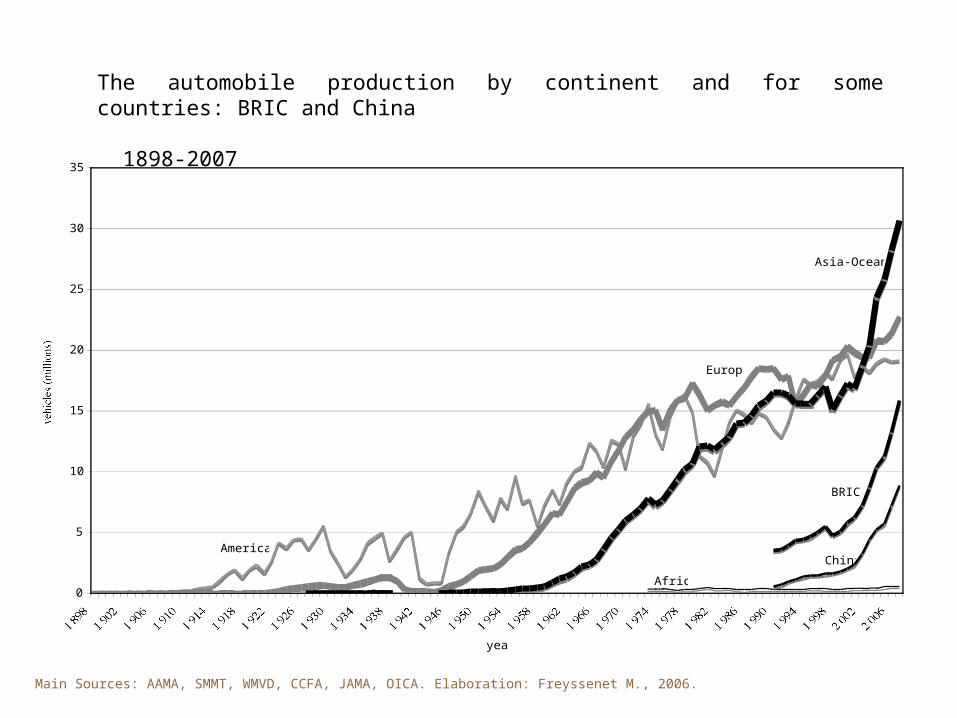

The automobile production by continent and for some countries: BRIC and China 1898-2007

Main Sources: AAMA, SMMT, WMVD, CCFA, JAMA, OICA. Elaboration: Freyssenet M., 2006.

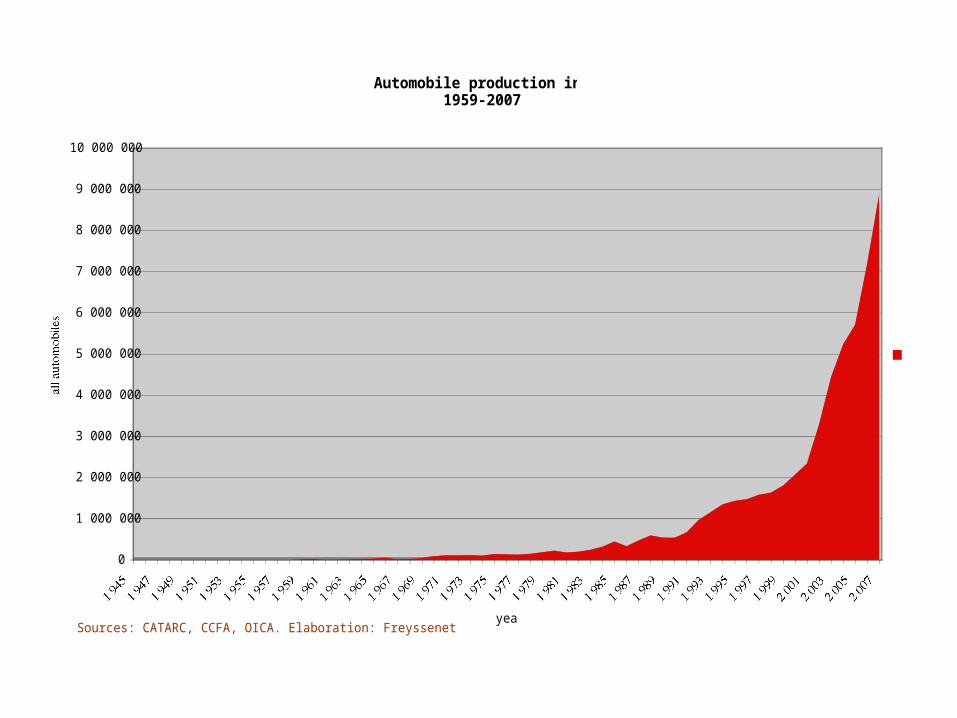

Automobile production in China1959-2007

0

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

7 000 000

8 000 000

9 000 000

10 000 000

1 9451 9471 9491 9511 9531 9551 9571 9591 9611 9631 9651 9671 9691 9711 9731 9751 9771 9791 9811 9831 9851 9871 9891 9911 9931 9951 9971 9992 0012 0032 0052 007

year

all automobiles

Sources: CATARC, CCFA, OICA. Elaboration: Freyssenet M., 2004 and after,

to more developments…

• Boyer R., Freyssenet M., The productive models. The conditions of profitability, Palgrave: London, New York, 2002

• Freyssenet M. (ed.) The second automobile revolution. The trajectories of automobile firms at the beginning of the XXIth century, Palgrave: London, New York, 2009

• http://freyssent.com• http://gerpisa.univ-evry.fr

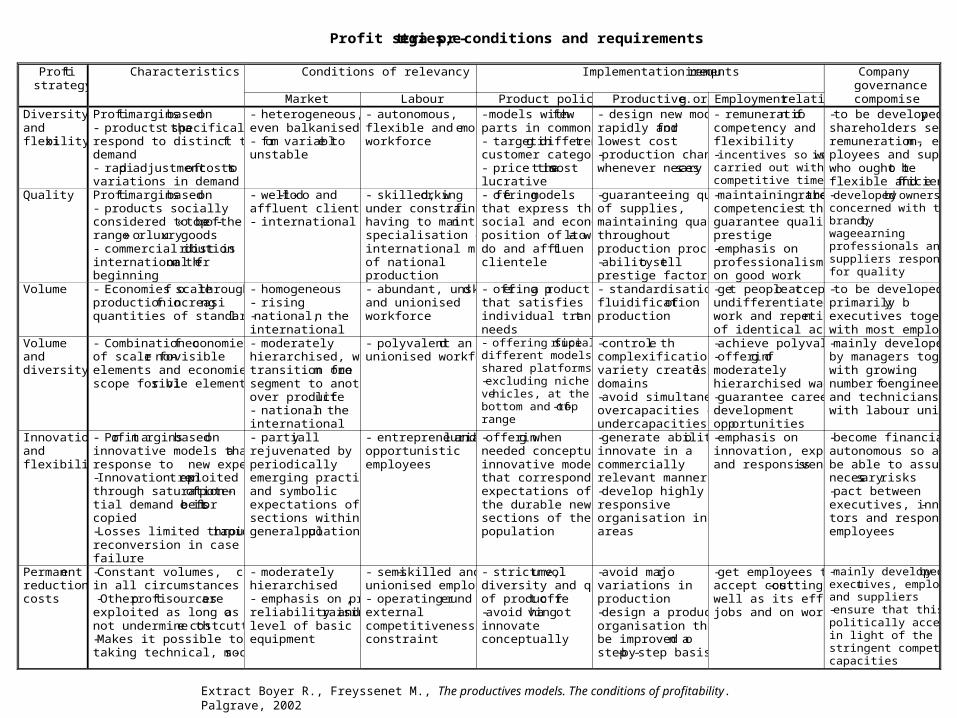

Profit strategies, pre-conditions and requirements

Profit strategy

Characteristics Conditions of relevancy Implementation requirements Company governance

Market Labour Product policy Productive org. Employment relation compomise Diversity and flexibility

Profit margins based on - products that specifically respond to distinct types of demand - rapid adjustment of costs to variations in demand

- heterogeneous, even balkanised - from variable to unstable

- autonomous, flexible and mobile workforce

- models with few parts in common - targeting different customer categories - price that is most lucrative

- design new models rapidly and for lowest cost -production changed whenever necessary

- remuneration of competency and flexibility -incentives so work is carried out within competitive timeframe

-to be developed by shareholders seeking remuneration, em-ployees and suppliers who ought to be flexible and efficient

Quality Profit margins based on - products socially considered to be « top-of-the-range » or luxury goods - commercial distribution is international from the beginning

- well-to-do and affluent clientele - international

- skilled, working under constraint of having to maintain specialisation on international markets of national production

- offering models that express the social and economic position of a well-to-do and affluent clientele

-guaranteeing quality of supplies, maintaining quality throughout production process -ability to sell prestige factor

-maintaining the rare competencies that guarantee quality and prestige -emphasis on professionalism and on good work

-developed by owners concerned with the brand, by wageearning professionals and by suppliers responsible for quality

Volume - Economies of scale through production of increasing quantities of standard model

- homogeneous - rising -national, then international

- abundant, unskilled and unionised workforce

- offering a product that satisfies basic individual transport needs

- standardisation and fluidification of production

-get people to accept undifferentiated work and repetition of identical acts

-to be developed primarily by executives together with most employees

Volume and diversity

- Combination of economies of scale for non-visible elements and economies of scope for visible elements

- moderately hierarchised, with transition from one segment to another over product life - national then international

- polyvalent and unionised workforce

- offering superficially different models with shared platforms -excluding niche vehicles, at the very bottom and top-of-range

-control the complexification variety creates in all domains -avoid simultaneous overcapacities or undercapacities

-achieve polyvalency -offering of moderately hierarchised wages -guarantee career development opportunities

-mainly developed by managers together with growing number of engineers and technicians, and with labour unions

Innovation and flexibility

- Profit margins based on innovative models that are a response to new expectations -Innovation rent exploited through saturation of poten-tial demand before it is copied -Losses limited through rapid reconversion in case of failure

- partially rejuvenated by the periodically emerging practical and symbolic expectations of new sections within the general population

- entrepreneurial and opportunistic employees

-offering when needed conceptually innovative models that correspond to expectations of those the durable new sections of the population

-generate ability to innovate in a commercially relevant manner -develop highly responsive organisation in all areas

-emphasis on innovation, expertise and responsiveness

-become financially autonomous so as to be able to assume the necessary risks -pact between executives, innova-tors and responsive employees

Permanent reduction in costs

-Constant volumes, costs cut in all circumstances -Other profit sources are exploited as long as they do not undermine the costcutting -Makes it possible to avoid taking technical, social, com-

- moderately hierarchised - emphasis on price, reliability and raising level of basic equipment

- semi-skilled and unionised employees - operating under external competitiveness constraint

- strict volume, diversity and quality of product offer -avoid having to innovate conceptually

-avoid major variations in production -design a productive organisation that can be improved on a step-by-step basis

-get employees to accept cost-cutting as well as its effects on jobs and on work

-mainly developed by executives, employees and suppliers -ensure that this is politically acceptable in light of the stringent competitive capacities

Extract Boyer R., Freyssenet M., The productives models. The conditions of profitability. Palgrave, 2002