Embed Size (px)

Citation preview

Private Equity co-investments: opportunities

and challenges

Elias Korosis – Partner, Hermes GPE

Private and confidential. This document should not be circulated to third parties

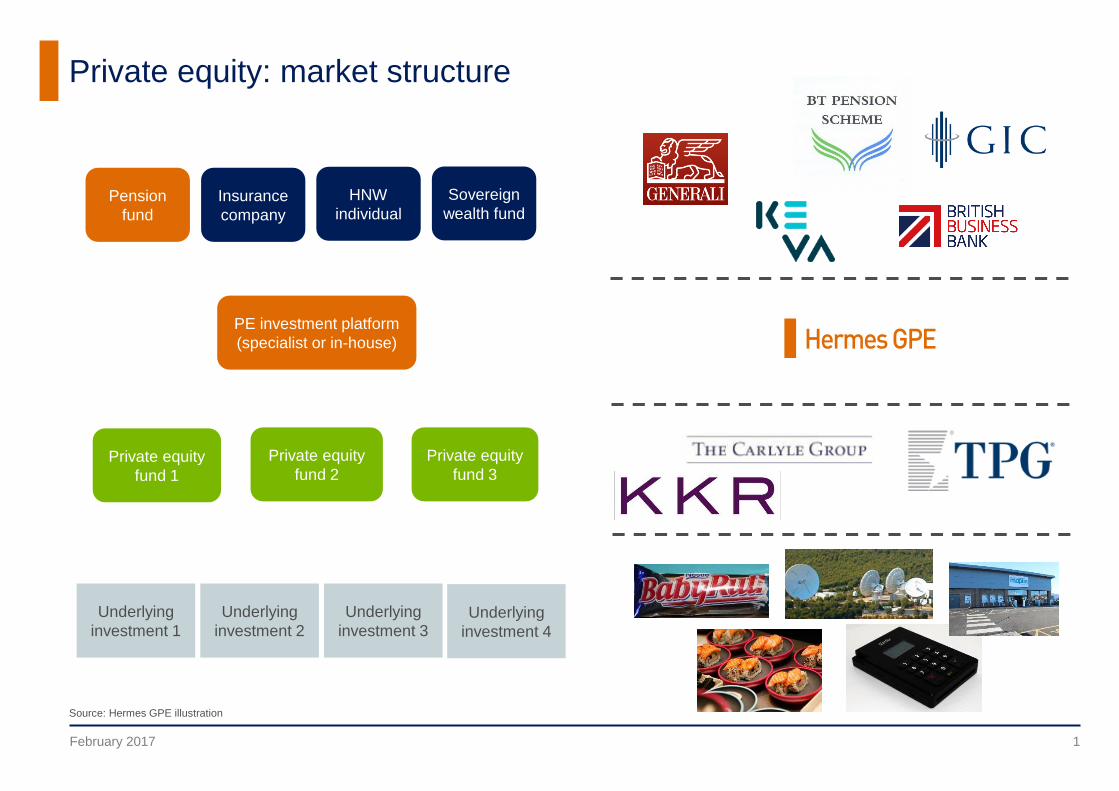

Private equity: market structure

Source: Hermes GPE illustration

1February 2017

PE investment platform

(specialist or in-house)

Pension

fund

Insurance

company

Sovereign

wealth fund

HNW

individual

Underlying

investment 1

Underlying

investment 2

Underlying

investment 3

Private equity

fund 1

Private equity

fund 2

Private equity

fund 3

Underlying

investment 4

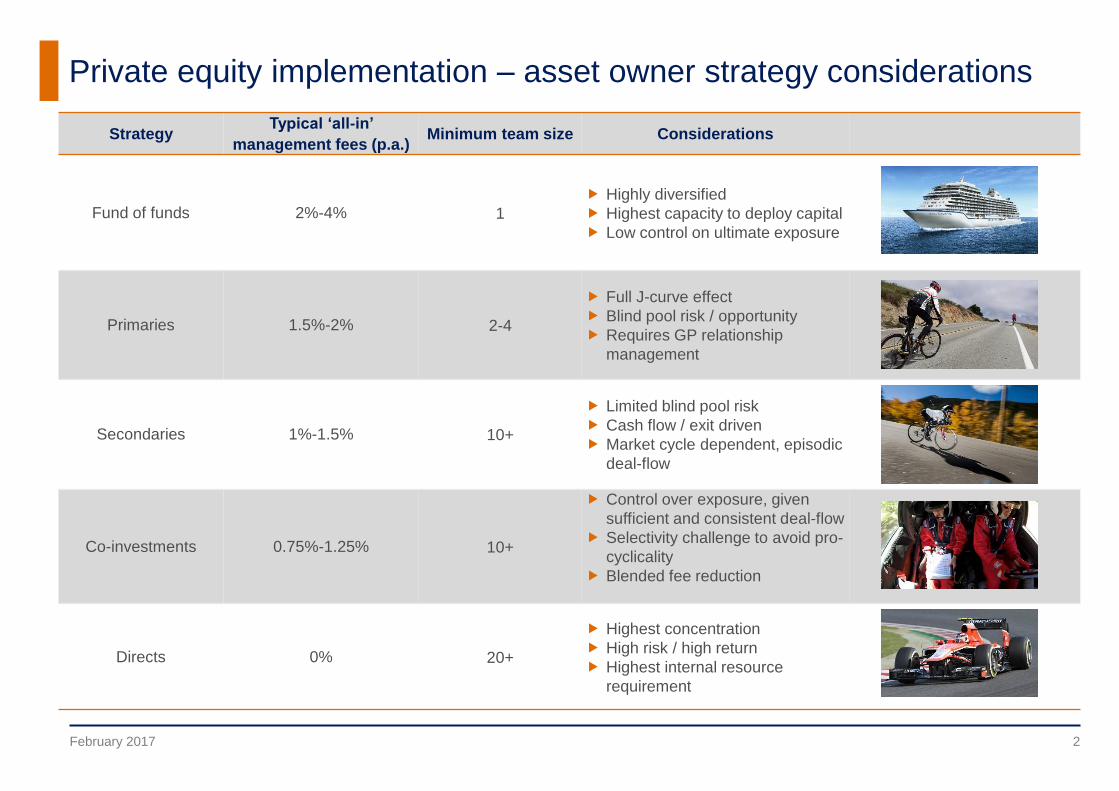

StrategyTypical ‘all-in’

management fees (p.a.)Minimum team size Considerations

Fund of funds 2%-4% 1

Highly diversified

Highest capacity to deploy capital

Low control on ultimate exposure

Primaries 1.5%-2% 2-4

Full J-curve effect

Blind pool risk / opportunity

Requires GP relationship

management

Secondaries 1%-1.5% 10+

Limited blind pool risk

Cash flow / exit driven

Market cycle dependent, episodic

deal-flow

Co-investments 0.75%-1.25% 10+

Control over exposure, given

sufficient and consistent deal-flow

Selectivity challenge to avoid pro-

cyclicality

Blended fee reduction

Directs 0% 20+

Highest concentration

High risk / high return

Highest internal resource

requirement

Private equity implementation – asset owner strategy considerations

2February 2017

Private equity implementation – asset owner strategy considerations

3February 2017

Co-investment Directs

Typical ‘all-in’

management fees (p.a.) 0.75%-1.25%

Minimum team size 10+

Considerations

Control over exposure, given

sufficient and consistent deal-

flow

Selectivity challenge to avoid

pro-cyclicality

Blended fee reduction

Typical ‘all-in’

management fees (p.a.)

0% externally

0-1% (internal costs)

Minimum team size 20+

Considerations

Highest concentration

High risk / high return potential

Highest internal resource

requirement

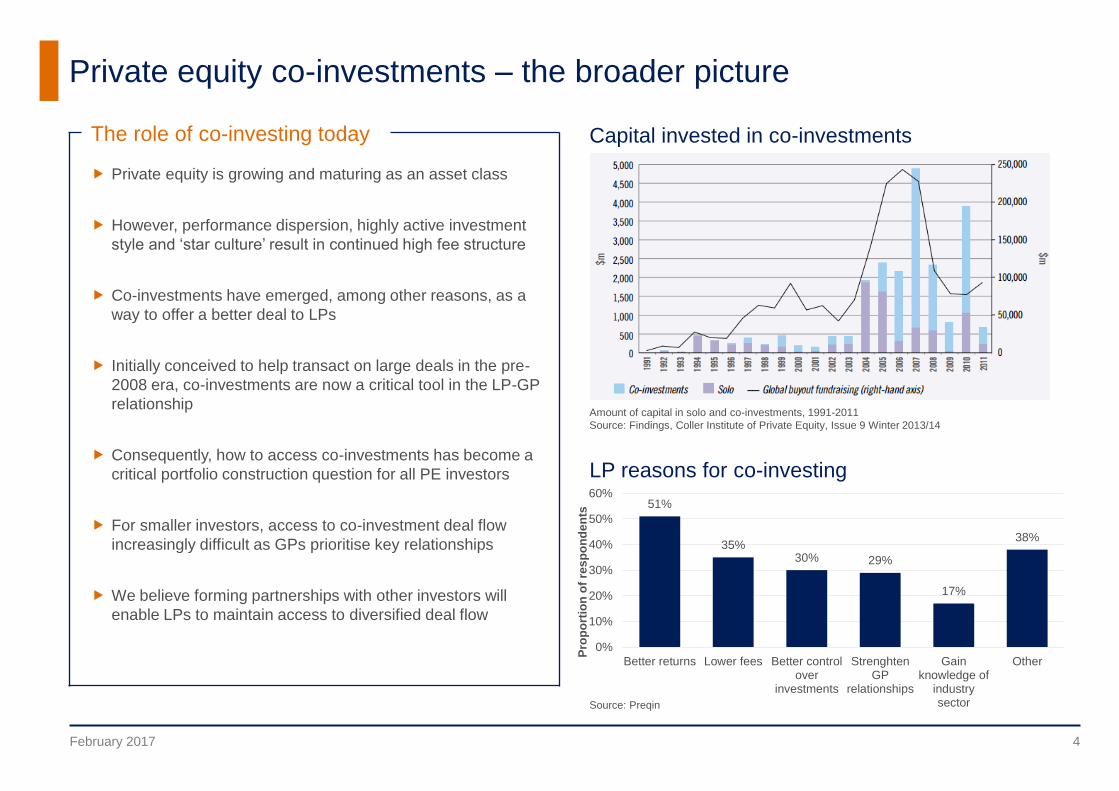

The role of co-investing today

Private equity is growing and maturing as an asset class

However, performance dispersion, highly active investment

style and ‘star culture’ result in continued high fee structure

Co-investments have emerged, among other reasons, as a

way to offer a better deal to LPs

Initially conceived to help transact on large deals in the pre-

2008 era, co-investments are now a critical tool in the LP-GP

relationship

Consequently, how to access co-investments has become a

critical portfolio construction question for all PE investors

For smaller investors, access to co-investment deal flow

increasingly difficult as GPs prioritise key relationships

We believe forming partnerships with other investors will

enable LPs to maintain access to diversified deal flow

51%

35%30% 29%

17%

38%

0%

10%

20%

30%

40%

50%

60%

Better returns Lower fees Better controlover

investments

StrenghtenGP

relationships

Gainknowledge of

industrysector

Other

Pro

po

rtio

n o

f re

sp

on

de

nts

Private equity co-investments – the broader picture

Capital invested in co-investments

LP reasons for co-investing

February 2017 4

Amount of capital in solo and co-investments, 1991-2011

Source: Findings, Coller Institute of Private Equity, Issue 9 Winter 2013/14

Source: Preqin

J-curve and fee reduction in practice: co-invest vs fund comparison

February 2017 5

0.6x

1.1x

1.6x

2.1x

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Net

TV

PI

Co-Investment Fund 50/50 Co-Investment and Funds Portfolio

2011 vintage 2001 vintage

2002 vintage

1.0x 1.0x

0.66x

0.85x

0.14x

0.03x0.20x

0.11x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

Fund Co-Invest

Total Capital Drawn Profit to LP Management Fees Carried Interest

1 Assumptions: both funds with same performance: 2.0x MoC

Buyout Fund terms: 2% fee, 20% carried interest, no hurdle

Co-Invest Fund terms: 0.6% fee, 10% carried interest , no hurdle, incl. fees and carry paid on

underlying co-investments

J-curve reduction: TVPI evolution of a co-investment fund vs the

market (2011 Vintage, Thomson VentureXpert)

Fee savings of different allocations to buyout funds and co-

investment funds (£100m portfolio)

Capital distribution – comparison of a co-investment fund and buyout

fund1 (hypothetical 2.0x gross return for each, based on actual terms)

0.91.9

2.83.8

4.7

0.7

1.4

2.2

2.9

3.6

0

2

4

6

8

10

100% Funds 90/10 Funds/Co-Invest

80/20 70/30 60/40 50/50

£m

Management Fee Savings Carried Interest Savings

Risks and challenges of co-investments

For co-invest programmes run by asset owners:

‘Large deal bias’

Challenging, resource-intensive execution

Concentration risk

Higher headline risk

GP relationship risk

Benefits of co-investments

Deployment speed and J-curve mitigation

Control over portfolio construction, strategy and pace

Potential for enhanced investment returns on selectivity basis

Blended fee reduction

Much improved fund intelligence

Manager diversification vis-à-vis single fund

Private equity co-investments – pros and cons

February 2017 6

Dealing with challenges in co-investing

February 2017 7

Risks / challenges Implementation considerations / requirements

Large deal bias Diversify deal flow as much as possible

Independent investment review and risk controls

Make quality of co-investment deal flow core to the GP relationship

Disciplined portfolio construction process

High quality and diverse deal flow

Rigorous process for follow-on investments

Concentration

risk

Disciplined ESG review as part of investment process and ongoing monitoring

Delegation to a specialist manager (fund or managed account) or ‘club’ partner

Higher headline

risk

Dedicated, experienced deal team

Rigorous investment process

Challenging

execution

GP relationship

risk

Experienced co-investment team to manage GPs throughout the process

This can improve the wider GP relationship significantly

Deals sourced

1126

In-depth review 218

IC reviewed 143

Invested

109

Concentration, selectivity and dealflow requirements

February 2017 8

Diversification and selectivity Considerations

Prudent portfolio construction

Given the high degree of business-specific risk in co-investments, to avoid over-

concentration on any particular deal, a co-investment portfolio needs to be diversified

needs to be diversified across several deals

Empirically, a sufficiently diversified portfolio requires c30–45 investments,

based on both public and private market research

Vintage diversification

Consistent investment requires a certain number of deals invested each year

Given a typical three year investment period that means c10–15 investments

need to be executed per year to build a diversified portfolio

There is strong evidence for vintage year diversification; diverting from this principle

requires high conviction on tactical allocation

Impact of selectivity

Deal-flow has to be consistent and deep enough to reliably provide attractive co-

investment opportunities

A high quality co-investment process requires high selectivity with approval ratios of

c10%–15%

This implies that a flow of c200 deals a year may be needed to provide sufficient

diversification

19%

13%

10%

1 Hermes GPE deal-flow 2010–Q4 2016

Consistent investment volume

Selectivity requires extensive deal-flow1

Portfolio risk and number of investments

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

2011 2012 2013 2014

EV

in

thousand U

SD

Date of Investment

Key investor considerations and select research issues

Select research issues / challenges

Understanding and quantifying risk in PE, including at

sub-asset class level (sector, region, stage etc)

Analyzing the systemic risk factors behind the value

creation drivers

Understanding correlation properties at the sub-asset

class level vis-à-vis different economic environments

Analytical rigour in manager selection

Cash flow modelling / forecasting

Market structure evolution (e.g. co-investment model)

Appropriate regulatory treatment

Proposed benefits

High absolute returns: Equity risk premium, illiquidity

premium, PE value creation (incl. leverage)

Strong risk-return relationship (Sharpe ratio

improvement?)

Imperfect (if material) correlation with public equities

Outperformance potential in downturns due to

structural advantages

Risks and costs

Large dispersion of performance

Cash flow timing risks

Control over investments (blind pool)

High fees

Transparency

Regulation

February 2017 9

February 2017 10

How do we do it?

An introduction to Hermes GPE

Cameron Payne |

Associate

RBC, Canaccord

Genuity,

Standard

& Poor’s

Sanjoy Sankaran |

Senior Associate

IDFC

Alternatives,

MBA

Nitin Muddana |

Associate

HGPE Sg /

London,

Doughty Hanson

Sean Yoo |

Senior Associate

Anchor Equity

Partners,

Goldman Sachs

Iesan Tsai | VP

UBS, JP Morgan,

H&Q Asia

Pacific, MBA

Elias Korosis | Partner

Previously Bridgewater, Citigroup,

Schroder Salomon Smith Barney

Sunny Chu | Partner

Previously Qatar Investment

Authority, Alpinvest, McKinsey

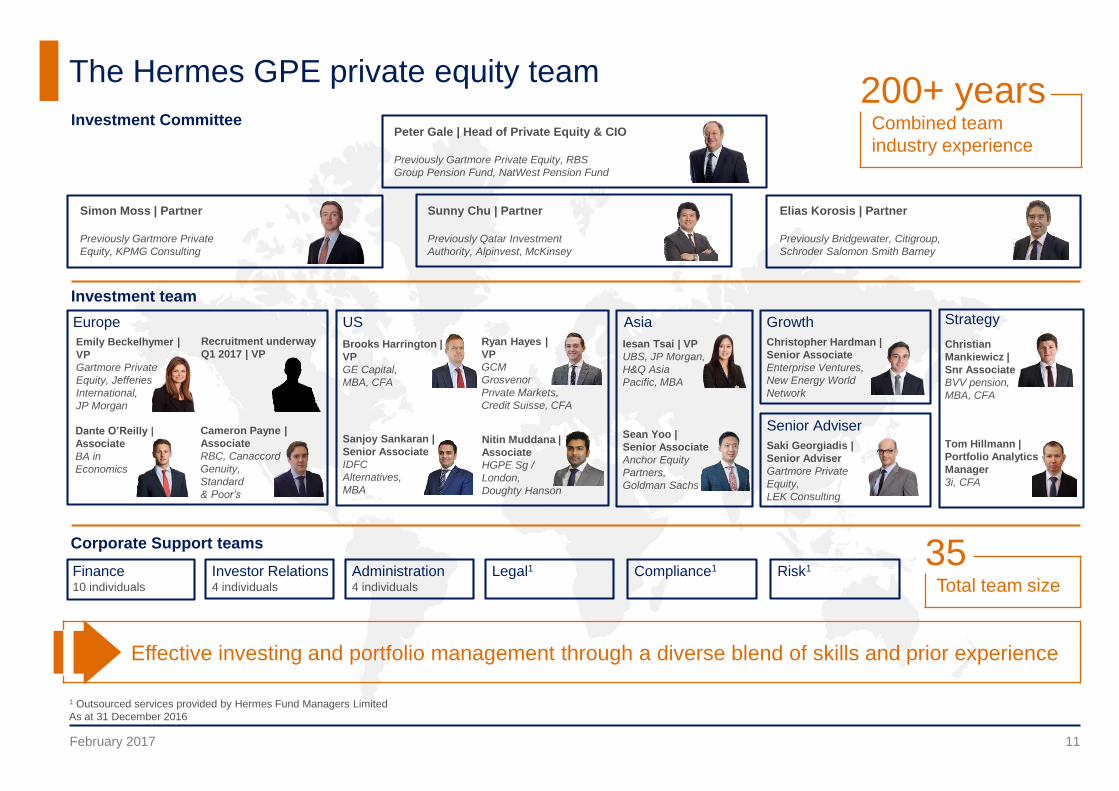

The Hermes GPE private equity team

February 2017

Investment CommitteePeter Gale | Head of Private Equity & CIO

Previously Gartmore Private Equity, RBS

Group Pension Fund, NatWest Pension Fund

Simon Moss | Partner

Previously Gartmore Private

Equity, KPMG Consulting

Investment team

GrowthEurope US Asia Strategy

Brooks Harrington |

VP

GE Capital,

MBA, CFA

Christopher Hardman |

Senior Associate

Enterprise Ventures,

New Energy World

Network

Christian

Mankiewicz |

Snr Associate

BVV pension,

MBA, CFA

Dante O’Reilly |

Associate

BA in

Economics

Tom Hillmann |

Portfolio Analytics

Manager

3i, CFA

Corporate Support teams

Finance10 individuals

Investor Relations4 individuals

Administration4 individuals

Legal1 Compliance1 Risk1

1 Outsourced services provided by Hermes Fund Managers Limited

As at 31 December 2016

Effective investing and portfolio management through a diverse blend of skills and prior experience

200+ yearsCombined team

industry experience

35Total team size

Emily Beckelhymer |

VP

Gartmore Private

Equity, Jefferies

International,

JP Morgan

Ryan Hayes |

VP

GCM

Grosvenor

Private Markets,

Credit Suisse, CFA

Senior Adviser

Saki Georgiadis |

Senior Adviser

Gartmore Private

Equity,

LEK Consulting

11

Recruitment underway

Q1 2017 | VP

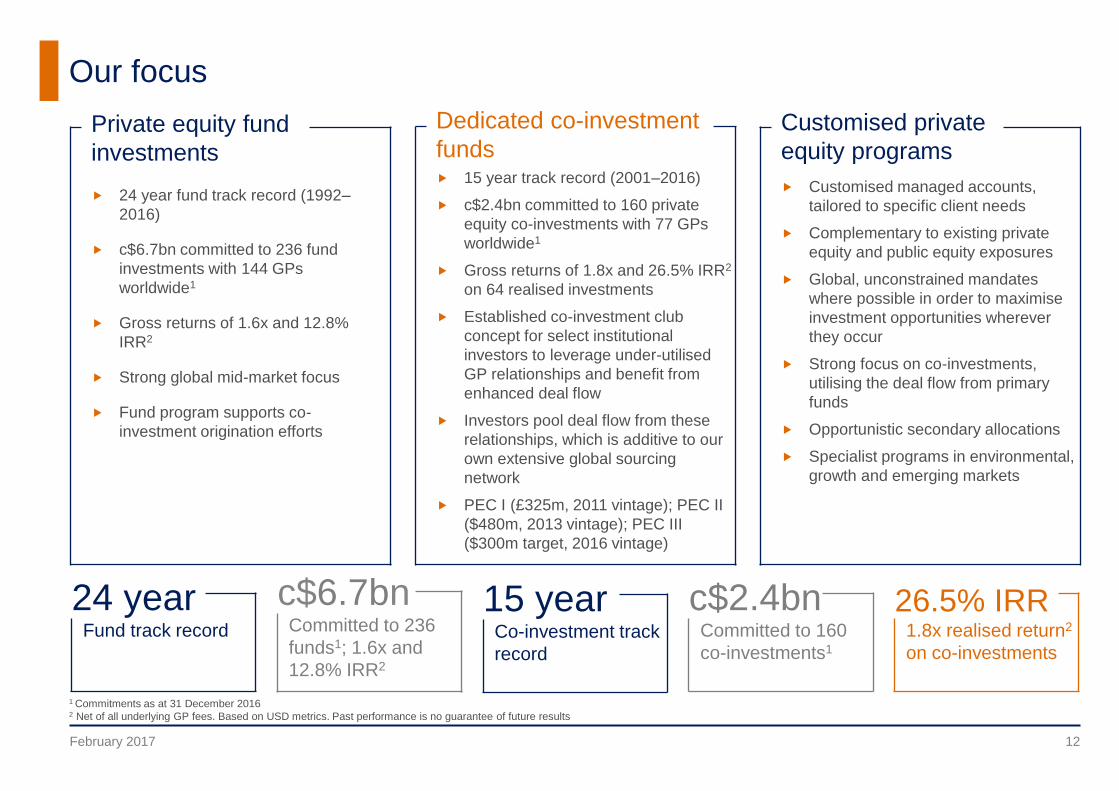

Customised private

equity programs

Customised managed accounts,

tailored to specific client needs

Complementary to existing private

equity and public equity exposures

Global, unconstrained mandates

where possible in order to maximise

investment opportunities wherever

they occur

Strong focus on co-investments,

utilising the deal flow from primary

funds

Opportunistic secondary allocations

Specialist programs in environmental,

growth and emerging markets

Private equity fund

investments

24 year fund track record (1992–

2016)

c$6.7bn committed to 236 fund

investments with 144 GPs

worldwide1

Gross returns of 1.6x and 12.8%

IRR2

Strong global mid-market focus

Fund program supports co-

investment origination efforts

1 Commitments as at 31 December 20162 Net of all underlying GP fees. Based on USD metrics. Past performance is no guarantee of future results

Our focus

February 2017

c$6.7bnCommitted to 236

funds1; 1.6x and

12.8% IRR2

24 yearFund track record

15 yearCo-investment track

record

c$2.4bnCommitted to 160

co-investments1

26.5% IRR1.8x realised return2

on co-investments

Dedicated co-investment

funds 15 year track record (2001–2016)

c$2.4bn committed to 160 private

equity co-investments with 77 GPs

worldwide1

Gross returns of 1.8x and 26.5% IRR2

on 64 realised investments

Established co-investment club

concept for select institutional

investors to leverage under-utilised

GP relationships and benefit from

enhanced deal flow

Investors pool deal flow from these

relationships, which is additive to our

own extensive global sourcing

network

PEC I (£325m, 2011 vintage); PEC II

($480m, 2013 vintage); PEC III

($300m target, 2016 vintage)

12

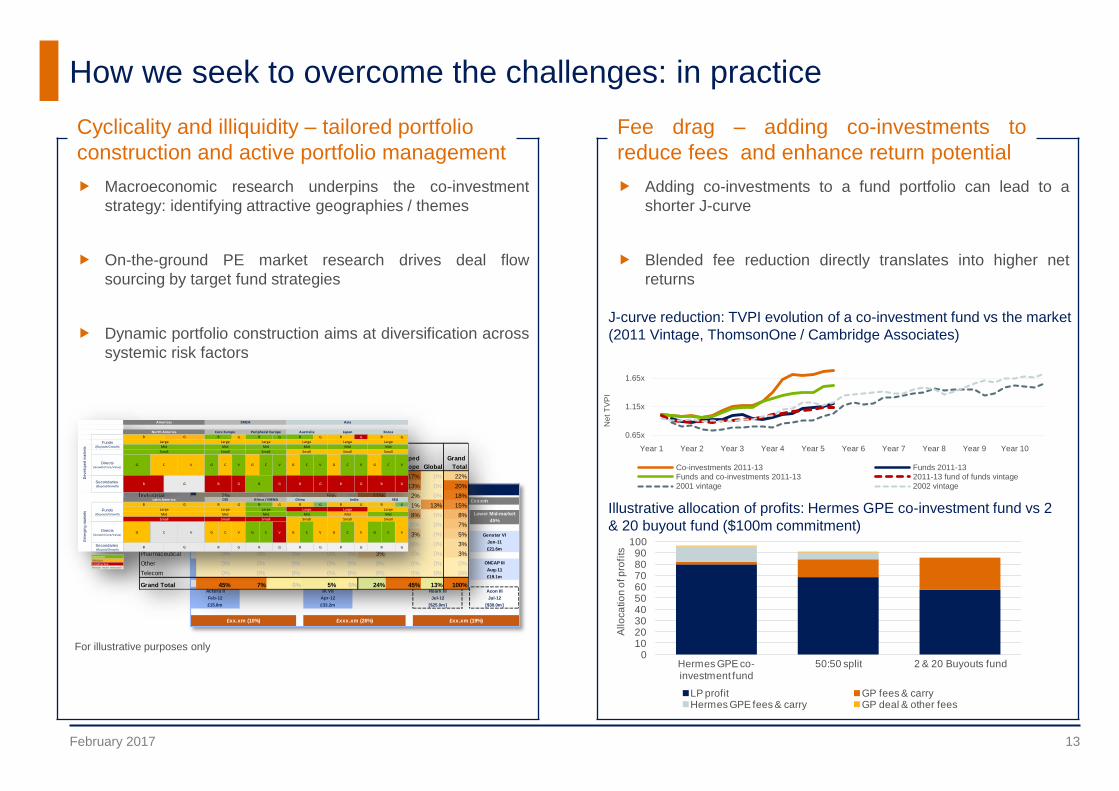

Fee drag – adding co-investments to

reduce fees and enhance return potential

Adding co-investments to a fund portfolio can lead to a

shorter J-curve

Blended fee reduction directly translates into higher net

returns

Cyclicality and illiquidity – tailored portfolio

construction and active portfolio management

Macroeconomic research underpins the co-investment

strategy: identifying attractive geographies / themes

On-the-ground PE market research drives deal flow

sourcing by target fund strategies

Dynamic portfolio construction aims at diversification across

systemic risk factors

How we seek to overcome the challenges: in practice

February 2017

For illustrative purposes only

Mid Funds Small Funds Large/Mid Funds Small Funds Upper Mid-market Lower Mid-market

50% 50% 65% 35% 55% 45%

AIF Capital IV BC Partners IX Quadriga IV GTCR X Genstar VI

Jul-11 Mar-11 May-11 Feb-11 Jun-11

£12.2m £30.2m £17.6m £21.6m £21.6m

EMPEF EQT VI Court Square III ONCAP III

Jan-12 Jul-11 May-12 Aug-11

£19.1m £36.1m £21.7m £19.1m

Actera II IK VII Roark III Acon III

Feb-12 Apr-12 Jul-12 Jul-12

£15.8m £33.2m [$25.0m] [$30.0m]

Emerging Markets: £xxm Developed Europe: £xxxm Americas: £xxxm

Hermes GPE Client Account 2011-2013 : £xxxm

£xx.xm (10%) £xxx.xm (26%) £xx.xm (19%)

Developed

Europe

Emerging

Europe

Developed

Asia

Emerging

Asia Africa

North

America

Developed

Europe Global

Grand

Total

Healthcare 17% 0% 0% 0% 0% 0% 17% 0% 22%

Retail 13% 7% 0% 0% 0% 0% 13% 0% 20%

Industrial 2% 0% 0% 5% 0% 11% 2% 0% 18%

Financial services 1% 0% 0% 0% 0% 1% 1% 13% 15%

Consumer Services 8% 0% 0% 0% 0% 0% 8% 0% 8%

Business Services 0% 0% 0% 0% 0% 7% 0% 0% 7%

Energy 3% 0% 0% 0% 0% 0% 3% 0% 5%

Consumer 0% 0% 0% 0% 0% 3% 0% 0% 3%

Pharmaceutical 0% 0% 0% 0% 0% 3% 0% 0% 3%

Other 0% 0% 0% 0% 0% 0% 0% 0% 0%

Telecom 0% 0% 0% 0% 0% 0% 0% 0% 0%

Grand Total 45% 7% 0% 5% 0% 24% 45% 13% 100%

G G G G G

Directs(Growth/Core/Value)

G C V G C V G C V G C V G C V

Secondaries (Buyout/Growth)

G G G G G

G G G G G

Directs(Growth/Core/Value)

G C V G C V G C V G C V G C V

Secondaries (Buyout/Growth)

G G G G G

Attractive

Medium

Unattractive Needs more research

Korea

Americas EMEA Asia

North America Core Europe Peripheral Europe Australia Japan

De

ve

lop

ed

ma

rke

ts

Funds(Buyouts/Growth)

B G B

Mid Mid

G C V

B G B

B B B

Large Large Large Large Large Large

B

Mid Mid Mid

Small Small Small Small Small Small

Mid

B B B

Latin America CEE Africa / MENA China India SEA

B

Em

erg

ing

ma

rke

ts

Funds(Buyouts/Growth)

B G B

Mid Mid

G C V

B G B

Small Small

B B B

Large Large Large Large Large Large

B

Mid

B

Mid Mid Mid

SmallSmall Small Small

B B B

Illustrative allocation of profits: Hermes GPE co-investment fund vs 2

& 20 buyout fund ($100m commitment)

J-curve reduction: TVPI evolution of a co-investment fund vs the market

(2011 Vintage, ThomsonOne / Cambridge Associates)

13

0.65x

1.15x

1.65x

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Net

TV

PI

Co-investments 2011-13 Funds 2011-13Funds and co-investments 2011-13 2011-13 fund of funds vintage2001 vintage 2002 vintage

0102030405060708090

100

Hermes GPE co-investment fund

50:50 split 2 & 20 Buyouts fund

Allo

ca

tio

n o

f p

rofi

ts

LP profit GP fees & carryHermes GPE fees & carry GP deal & other fees

Appendix

February 2017 14

Disclaimer

February 2017

.

For Professional Investors only. Any person who

receives this document is required to make

themselves aware of their respective jurisdictions

and observe any restrictions including exchange

control restrictions. This document does not

constitute a solicitation or offer to any person to buy

or sell any related securities or financial

instruments. It pays no regard to the investment

objectives or financial needs of any recipient. No

action should be taken or omitted to be taken based

on this document. Tax treatment depends on

personal circumstances and may change. This

document is not advice on legal, taxation or

investment matters so investors must rely on their

own examination of such matters or seek advice.

Before making any investment (new or continuous),

please consult a professional and/or investment

adviser as to its suitability. Any opinions expressed

may change. The value of investments and

income from them may go down as well as up,

and you may not get back the original amount

invested. Any investments overseas may be

affected by currency exchange rates. Past

performance is not a reliable indicator of future

results and targets are not guaranteed. All

figures, unless otherwise indicated, are sourced

from Hermes GPE LLP (‘Hermes GPE’). For more

information please read any relevant Offering

Documents or contact Hermes GPE. Issued and

approved by Hermes GPE which is authorised and

regulated by the Financial Conduct Authority.

Registered address: Lloyds Chambers, 1 Portsoken

Street, London E1 8HZ, United Kingdom. Hermes

GPE is a registered investment adviser with the

United States Securities and Exchange

Commission. Hermes GPE (Singapore) Pte Ltd is

regulated by the Monetary Authority of Singapore.

Telephone calls may be recorded for training and

monitoring purposes.

15