Embed Size (px)

DESCRIPTION

Primary Agent - July 2009 - DE Edition

Citation preview

INTHISISSUE_______________Value proposition: your mealticket to an amazing career

Customer service slumps and solutions

When the back office is half a world away

Berkley Mid-Atlantic Grouplooks beyond soft market,hard economic times

DELAWARE

G10029_Covers.qxd:July09Primary 6/15/09 2:45 AM Page 1

Progressive Preferred is a new rewards program for independent agents in Pennsylvania.*

To qualify, sell an average of one policy per week to preferred customers. That’s someone

who owns a home, has a good driving record, and has continuous insurance with no lapse.

HIGHER COMMISSION IS ONLY THE BEGINNING

Signature Agents are rewarded with numerous special benefits including:

15/12 commission on preferred personal auto

A $2,000 annual marketing allowance for exclusive Signature AgentSM goods and services

An appointment to sell the Progressive Home Advantage and Personal Umbrella – both offer 15/12 commission

Increased opportunity to put Progressive’s marketing power to work for your agency

BECOME A SIGNATURE AGENT

Ready to learn more? Contact your Progressive account sales representative.

*This program is currently available only to Progressive agents in Pennsylvania and Colorado.

More Commission. More Rewards.

More Reasons to Prefer Progressive.

Earn higher commission and put Progressive’s marketing power to work

for your agency with the Progressive Preferred program

P R O G R E S S I V E

G10029_IFC-IBC-OBCJuly09.qxd:July09Primary 6/15/09 2:41 AM Page 1

One-Stop Insurance ShoppingSecure, Competitively

Priced Protection

For employees

For vehicles and fleets

Workers’ Comp

Commercial Auto

in PA and NJ

More States

in 2009

For property and liability

Businessowners’ Policy

in PA and NJ

COMING SOON

For added protection

Commercial Umbrella

in PA and NJ

Our GUARD Business Shield is a comprehensive insurance solution that offers the multiple lines of

coverage typically needed by small- to mid-sized businesses. As the current soft market begins to

draw to a close, GUARD’s history as a stable and secure carrier through both good times and bad will

become even more important!

A- (”EXCELLENT”) A.M. Best Rating

To learn more, visit

www.guard.com/apply

OR call 800-673-2465, ext 4567.

�

� Coverage extensions

Increased limits �

�

Price discounts

Good income potential

Ask About Our:

G10029_01-13.qxd:July09Primary 6/15/09 1:49 AM Page 1

Value proposition: your meal ticket to an amazing careerHow do you create value? This apparently simple question may well be themost important one you will ever be asked. Your ability to clearly articulateyour value proposition will separate you from the pack, elevate yourperformance and offer direction as you move ahead with your career.

Page 14

Customer service slumps and solutionsCustomer service is more than icing on the cake. It’s the bread and butter of anagency’s livelihood. A little training can go a long way toward addressingcommon concerns and improving service.

Page 18

When the back office is half a world awayWhen the sheer amount of data entry began to slow down his agency, JerryO’Donovan found help — a half a world away.

Page 20

Berkley Mid-Atlantic Group looks beyond soft market, hardeconomic timesBerkley Mid-Atlantic Group representatives recently met with the IA&B Boardof Directors to discuss the company’s differentiation points, commitment toaddressing agents’ technology needs and plans for growth despite the softmarket and hard economic times.

Page 24

14

18

20

24

ContentsP R I M A R Y A G E N T M A G A Z I N E

Copyright 2009. All rights reserved. No material may be reproduced in whole or in part without written consent of the publisher. The information in this publication is general in nature and is not intended to serve as legal, accounting, financial,insurance, investment advisory or other professional advice as to any reader’s particular situation. Users are encouraged to consult withcompetent legal, financial, insurance, investment advisory and or other professional advisors concerning specific matters before makingany decisions and we disclaim any responsibility for any decisions or actions by readers. Statements of fact and opinion in PrimaryAgent are the responsibility of the authors alone and do not imply an opinion on the part of the officers or the members of the IA&B.Participation in IA&B events, activities and/or publications is available on a non-discriminatory basis and does not reflect IA&Bendorsement of the products and/or services.

Subscriptions: Non-member price: $2.25 per copy or $15 per year.

All communications for publications, including news, features, advertising copy, cuts, etc., must reach the editor by 1st of month two monthsprior to publication. Advertising rates furnished upon request.

Address inquiries to:Primary Agent EditorPO Box 2023Mechanicsburg, PA 17055-0763Phone (800) 998-9644 or (717) 795-9100 Fax (717) 795-8347

Periodical postage paid at Mechanicsburg, Pa. and additional entry post office.

Postmaster: Send address changes to above address.Primary Agent (ISSN 1543-3110), Permit # 638-620, Issue # 2009-7) is published monthly by IA&B Service Group Inc., a subsidiary of IA&B.

4 Chairman of the Board’s Message6 State News7 New Members8 Preventing Errors & Omissions10 Coverage Corner12 Glance at Events

13 Member FAQ29 IA&B Partners30 Technology Update32 Advertisers Index32 Classified Ads

In every issue

Mission StatementPrimary Agent delivers ideas to helpInsurance Agents & Brokers’ membersnegotiate their unique position asguardians of trust between insuranceconsumers and companies whilefacing the challenges of maintaining a small business. Primary Agent also supports IA&B’s mission topreserve and advocate the AmericanAgency System.

G10029_01-13.qxd:July09Primary 6/15/09 1:50 AM Page 2

generalcasualty.com

General Casualty is a registered service mark of General Casualty Company of Wisconsin.QBE and the links logo are registered service marks of QBE Insurance Group Limited.All coverages underwritten by member companies of QBE. © 2009 QBE Holdings, Inc.

GLOBAL SOLUTIONSMEETLOCAL SUPPORT.

We’re General Casualty®.

We’re the regional insurer you already know, always there

to help independent agents with expert field support that

understands local needs. Now that support is stronger

than ever—because we’re stronger than ever. General

Casualty has joined QBE®, providing local hands with the

international reach needed to solve even your most

complex challenges.

We are now QBE Americas Division.

And we’re working for you.

G10029_01-13.qxd:July09Primary 6/15/09 1:51 AM Page 3

OfficersRobert J. “Buc” Cawley, AAI

ChairmanWexford, Pa.

Kathleen M. Glattly, ChFC, CLU, CPCUVice ChairwomanFactoryville, Pa.

G. Kevin Nemith, CICImmediate Past ChairmanDover, Del.

MembersNorman F. Basso, CPCU

York, Pa.

Vincent D. “Chip” Boylan Jr., CPCURockville, Md.

Timothy P. BurrisThompsontown, Pa.

M. Scott Clemens, CIC, CPCU, CLU, ChFC Souderton, Pa.

John T. “Chip” Colwell Jr., CICCorry, Pa.

Robert B. Hall, CPCU, CLU, ChFC, ARM, ARM-PWest Chester, Pa.

Denise M. Kozel, CPCUNewark, Del.

Linda A. McCann, AAI, CPCU, CPIWSalisbury, Md.

Thomas G. McElhaney State College, Pa.

Michael F. McGroarty Sr.Pittsburgh, Pa.

Scott C. Rogers, CPIAYork, Pa.

David Rosenkilde, CICReisterstown, Md.

Susan A. Sallada, CIC**Ft. Washington, Pa.

William D. Schneider, CPCU, ARM*Pittsburgh, Pa.

Robert A. Walbeck, CICHomer City, Pa.

David B. Wasson Sr., CICState College, Pa.

James M. Watkins*Dover, Del.

King W. “Kip” White, LUTCFFallston, Md.

John S. Yasik, CICNewark, Del.

* IIABA National Director** PIA National Director

Board of Directors

Reading material for your summertime escape

The dog days of summer have arrived. If you haven’talready, I hope that you take an opportunity to escapefrom the daily hustle and bustle and enjoy some quiet timeto recharge your work batteries. And in the event thatsome work-related reading material ends up in yoursuitcase, this issue of Primary Agent, which is dedicated tocustomer service, will be worth the read….

Customer service is crucial to maintaining an agency’sprofitability. Just ask industry expert and instructor, Rita Hollada. She makes her case for taking serviceseriously — and for committing resources to honing staff’s skills — on page 18.

This issue includes other customer-service considerationsas well. On page 14, IA&B member and industry coach,Scott Addis, explores the importance of communicatingyour value to customers. And on page 20, IA&B memberJerry O’Donovan shares his back-office secret that allowshis agency to exceed his customers’ time expectations.

Best wishes for a summer filled with time for family,relaxation and fresh ideas for the fall.

[ 4 ]

ROBERT J. “BUC” CAWLEYAAI

ChairmanO F T H E B O A R D ’ S M E S S A G E

G10029_01-13.qxd:July09Primary 6/15/09 1:51 AM Page 4

©S

IAA

2005

YourBridge to

Success!THE ALTERNATIVE

The Strategic Independent Agents Alliance (SIAA) is the future of insurancedistribution…NOW. Since 1983, SIAA and our Master Agencies have made a business out of

helping local independent agencies stay independent, while helping Captive Agents, DirectWriters, Producers, and Life and Financial Service Agents become independent.

GET INSTANTLY BIGAs soon as you join an SIAA Master Agency, you become instantly BIG by accessing the

companies that you need in order to compete with and win against any agency. Your agency’sincome and value will increase beyond any amount that you can generate on your own.

Over 2,100 agencies like yours have increased their income and value by joining SIAA. Find out more by visiting our website at www.siaa4u.net.

Trouble Get t ing Mar ket s?

Now over 50 agencies

in Pennsylvania

G10029_01-13.qxd:July09Primary 6/15/09 1:56 AM Page 5

State NewsPrimary Agent | July 2009

Delaware addressesemployeemisclassificationFollowing a national trend, Delaware haslegislation pending that would help curtailthe problem of fraudulent employersclassifying their workers as independentcontractors, as opposed to employees — a move made to avoid costly workers’compensation (WC) insurance and other benefits.

HB129, which follows on the heels ofsignificant WC and independent contractorclassification reform from several sessionsago, pertains only to the constructionindustry and imposes substantial penalties(fines, terms of imprisonment, loss ofbusiness licenses) on employers whoimproperly classify their employees.

DAIAB again will work to ensure thatagents will not be held liable for themisclassification of clients’ employees.However, members are reminded notassist clients in the classification process oftheir employees, which exposes producersto unnecessary liability risks.

New MembersW E L C O M E

Cambridge Broyhill Chambers LLCLewes, Del.

[ 6 ]

G10029_DE06-07.qxd:Layout 1 6/15/09 2:34 AM Page 2

[ 7 ]

Maryland condoclarificationAs a reminder to those withcondominium-owner or condoassociation clients in Maryland,legislation to address condominiumlaw went into effect June 1.

The IA&B of Maryland lead a coalitionthat pushed for the legislation, whichrequires condominium associations toinsure individual units exclusive ofbetterments or improvements. Theowner of the unit where damageoriginated still is responsible for theassociation’s deductible up to $5,000.However, the ability of the associationto assess the unit owner for the $5,000is now automatic, rather than requiringinclusion in the association’s bylaws.

Need for the legislative clarificationcame after an April 2008 MarylandCourt of Appeals decision which heldthat the Maryland Condominium Actdid not require the master insurancepolicy of the condominium associationto cover damage to an individual unit.

Members can read a recap of the issue— as well as access a webinar thatexplains the new coverage conditions —by visiting iabgroup.com/md, selectingIndustry & Legal Affairs from the left-hand navigation bar and then clickingthe Industry link.

In addition to the health care reformmovement, several bills have beenintroduced in Washington, D.C., thatcould impact members. IA&B’s nationalaffiliates are advocating on behalf ofmembers, and IA&B will provideupdates via Agent Headlines e-newsletter in the coming months.

The Homeowners’ Defense ActThe Homeowners’ Defense Act (HR 2555) would address the financialrepercussions of natural disasters. Thebill would create four programs to helpstabilize the private insurance marketand prevent potential insolvencies, allwith an end goal of increasing theavailability of catastrophe insurance.

The Insurance Information ActThis bill (HR 2609) calls for the creationof an Office of Insurance Informationwithin the Treasury Department. Thebill first surfaced last year as part ofthen Treasury Secretary HenryPaulson’s Blueprint on FinancialModernization. Some worry that thelegislation would serve as a precursorto an optional federal charter, but billsponsor Paul Kanjorksi (D-Pa.) toldIA&B last summer that the proposal isintended solely to help the federalgovernment address “insurance policy issues.”

The National Association ofRegistered Agents andBrokers Reform ActKnown as NARAB II (HR 2554), thislegislation would establish a private,non-profit entity to coordinate licenseissuance and renewal. Membershipwould be voluntary and benefitproducers who write in multiple states.The bill, which would allow states tomaintain regulation of the industry, issupported by IA&B.

The National InsuranceConsumer Protection ActThe National Insurance ConsumerProtection Act (HR 1880) would createan optional federal charter (OFC) as analternative to state-based insuranceregulation. An OFC would provideregulation similar to the dual-chartering system that controls thebanking industry. While many largeinsurers favor this bill, IA&B and itsnational affiliates do not.

The Non-admitted andReinsurance Reform ActThe Non-admitted and ReinsuranceReform Act (HR 2571) wouldstandardize state regulation of thesurplus-lines market and reinsurance.The legislation would unify surplus-lines premium tax allocation andremittance and multi-state surplus-lines risks.

Legislative news on the national front

G10029_DE06-07.qxd:Layout 1 6/15/09 2:35 AM Page 3

I remember back in 1987asking Ron Anderson and JimHarrison, two of the trueexperts on the Agents E&Oclass of business, what thekey was for an agent toavoid/minimize E&O claims.Their response was clear:document, document,document. Having just beenprovided with theresponsibility of managing the

Utica program, I thought thisseemed too simple; there hadto be more to it. Now over 20years later, while there are anumber of steps that can betaken to reduce the potentialfor an E&O claim, a key factorin whether a claim is evenbrought and if it is whatdirection it takes, deals withthe matter of documentation.

Take this recent claim: You aresuccessful in securing a newaccount, and the client initiallyasks you to just duplicatewhat he currently has. Soundssimple. As you get intosecuring proposals, the clientadvises you (verbally) thatdue to economics, he is notinterested in continuing hisumbrella coverage. As aresult, you proceed withplacing the remainder of thecoverage. After you get theother lines placed, one of hisvehicles is in a seriousaccident resulting in thefatality of one of the othercar’s passengers – definitely aloss that would exceed theunderlying limits and hit theumbrella layer.

Guess what his story is now?He is advising you that hewanted his prior coveragereplaced exactly as expiring,no exceptions. The issue?There is nothing in writing,nothing documented. It is tooearly to know where thisclaim is going to go, butwithout the necessarydocumentation, the defenseof the agent is definitely not

PreventingE R R O R S A N D O M I S S I O N S

[ 8 ]

CURTIS M. PEARSALL,CPCU, AIAF, CPIA

Curtis M. Pearsall

is vice president of E&O

for Utica Mutual Insurance

Company in Utica, N.Y.

Insurance Agents & Brokers

Service Group Inc. is the

exclusive agent for the Utica

E&O program in Delaware,

Maryland and Pennsylvania.

For questions regarding this

article or your Errors &

Omissions coverage, contact

IA&B at (800) 998-9644 or by

e-mail at [email protected].

DOCUMENTATION — WHAT IS YOUR AGENCY’S EXPECTATION?

Primary Agent | July 2009

G10029_01-13.qxd:July09Primary 6/15/09 1:53 AM Page 8

as strong. In retrospect, one could faultthe agency for not having full andcomplete documentation in the file.For example, a letter to the clientrecapping the conversation that theumbrella was not wanted would havebeen appropriate. So would have beenproviding the client with an umbrellaproposal anyway and then getting hissignoff that he didn’t want it. Sure,these would take time, but I wouldhope that everyone would agree that itis time well spent.

Could this claim occur in your agency?Is there a clear and concise positionfrom management to the CSRs andproducers how they would expect the above matter to be handled/documented? Is the documentationexpectation actually documented?

Unfortunately, there are many moreclaims like the one above where asolid trail of documentation wouldmake the difference. Imagine in theclaim above what would happen ifthere was solid documentation.Chances are the claim would not haveeven become a claim when the clientrealized that he put in writing that hedid not want the umbrella policy.

There are many scenarios where thedegree of documentation would play akey role in the defense of the agency.Whether you are dealing with policychanges (either additions or deletions)or moving accounts from onecompany to another where thecoverage may be different, soliddocumentation is key. The preferencewould be to get something from thecustomer in writing, but if this isn’tpractical, sending the customer aletter/e-mail detailing what you believethat he is asking for is a goodalternative. Also, ensuring that theright person is doing the documenting

can play a big role. If the producerspoke with the customer, then theproducer should be the one handlingthe documentation. To ask a CSR tohandle that when they were not evenpart of the conversation is notappropriate and certainly not fair to the CSR.

Also be certain that the documentationin your system is handled promptlyand without a lot of abbreviations. Youdefinitely want to keep the commentsprofessional as notes in your systemcan be discovered in the event that aclaim develops on that file.

Good solid documentation takes time,and there is no doubt that while strongdocumentation is key, it is easier saidthan done. It would be appropriate to

talk this through with your staffmembers to see if you can collectivelyidentify some efficiencies that willenable them to have the time to dothe necessary documentation.

If you are serious about makingchanges that will reduce the potentialfor an E&O claim being made againstyour agency, documentation is a greatstarting point. There is no doubt thattaking the time to the proper job ofdocumenting will pay major benefitsfor your agency.

[ 9 ]

G10029_01-13.qxd:July09Primary 6/16/09 9:35 AM Page 9

CoverageC O R N E R

[ 10 ]

JERRY MILTON, CIC

Jerry M. Milton teaches

and consults on industry

issues. The legal profession

recognizes him as an

expert on insurance

coverages. He is also the

education consultant for

IA&B, working with CISR,

CIC and continuing

education programs.

FIRST, KVAERNER METALS; NEXT, GAMBONEBROTHERS; NOW, NO COMPLETED OPERATIONSCOVERAGE FOR CONTRACTORS

Primary Agent | July 2009

The Commercial GeneralLiability (CGL) policy hasalways excluded damage to“your product” or “your work”arising out of that product orwork including any part of it.These are considered“business risk” exclusions. Ifyou made a faulty product ordid faulty work, you should beresponsible for replacing thatproduct or work.

However, for many, manyyears there has been anexception to the “damage toyour work” exclusion if thework was done bysubcontractors. Prior to 1986,this exception was added byendorsement and was called“broad form propertydamage.” Since 1986, thisexception has beenincorporated in the languageof the ISO CGL policy.

Exclusion l. under Coverage Aof the CGL policy states:

Damage To Your Work

“Property damage” to “yourwork” arising out of it or anypart of it and included in the“products-completedoperations hazard.” Thisexclusion does not apply if thedamaged work or the workout of which the damagearises was performed on yourbehalf by a subcontractor.

Because of this exception,general contractors havehistorically been coveredunder the CGL policy fordamage to buildings theyconstructed if that damagewas caused by asubcontractor’s faulty work.

On October 25, 2006, thePennsylvania Supreme Courtchanged all of this in theirKvaerner Metals Division ofKvaerner U.S., Inc. v.Commercial Union InsuranceCo. decision. In the Kvaernercase, the PennsylvaniaSupreme Court eliminatedcoverage for a general

G10029_01-13.qxd:July09Primary 6/15/09 1:53 AM Page 10

[ 11 ]

contractor for damage to a buildingcaused by the faulty workmanship of asubcontractor. In its decision, the courtdetermined that faulty work is not anaccident, and therefore, does notconstitute an “occurrence” under theCGL policy.

In June of 1997, Bethlehem SteelCorporation filed a complaint againstKvaerner Metals and other relatedcompanies for breach of contract andbreach of warranty in the design andconstruction of a coke oven battery.Kvaerner sought coverage from itsinsurer, Commercial Union, based onthe fact that the damage was caused bywork done by a subcontractor.

Commercial Union denied the claim onthe basis that faulty workmanship is notan “occurrence,” and the trial courtagreed. On appeal, the trial court’sdecision was reversed by the SuperiorCourt. Commercial Union appealed,and the Pennsylvania Supreme Courtoverturned the Superior Court’sdecision. The court determined that thefaulty work that caused the damagewas not an accident and thus not an“occurrence” under the CGL policy. Thecourt further determined that damagefrom faulty construction work should beexpected and therefore is no accident.

In reaching its decision, thePennsylvania Supreme Court relied onsimilar cases in New Hampshire andSouth Carolina. However, most otherstates have not agreed withPennsylvania. For example, in 2007 theFlorida Supreme court stated thefollowing in a case similar to Kvaerner:

The insurance and policyholdercommunities agreed that the CGLpolicy should provide coveragefor defective construction claimsso long as the allegedly defectivework had been performed by asubcontractor rather than thepolicyholder itself. This resultedboth because of the demands of

the policyholder community(which wanted this sort ofcoverage) and the view ofinsurers that the CGL was a more attractive product thatcould be better sold if itcontained this coverage.

The Superior Court of Pennsylvaniarecently reinforced the Kvaernerdecision in Millers Capital Insurance Co.v. Gambone Brothers Development Co.Gambone constructed several housesthat had various faulty constructionissues, including faulty exterior stucco,which led to water damage to thehomes. Because the stucco work wasdone by a subcontractor, Gambonesubmitted the claims to Millers Capital.

Millers denied the claims, and the trialcourt agreed. Again, not an“occurrence.” Gambone appealed thedecision to the Superior Court. Relyingon the Kvaerner decision, the SuperiorCourt rejected all of Gambone’sarguments. The court stated in part:

The grant of coverage states that“property damage” will only becovered if caused by an“occurrence,” which is, in turn,defined as an “accident.”Inasmuch as the claims arepremised on allegations of faultyworkmanship, Gambone arguesthat the exception to the “yourwork” exclusion allows coverageto lie for claims based on faultyworkmanship by a subcontractor.Yet, claims predicated on faultyworkmanship cannot beconsidered “occurrences” forpurposes of an occurrence CGLpolicy as a matter of plainlanguage and judicialconstruction. Gambone does notoffer us any manner in which torectify this seeminglyinsurmountable contradiction.

Unfortunately the court’s ruling inGambone goes even further than

Kvaerner. The effect of the Gambonedecision could be that not only is anydamage to the work itself excluded, butany third party damage or injury is alsoexcluded. In other words, the practicaleffect of the Gambone decision will beto exclude coverage under Pennsylvanialaw for any consequential damages thatare caused by faulty workmanship.

If this is the case, then contractors inPennsylvania will have no coveragewhatsoever for any injuries or damagesarising out of their completedoperations. If this decision is upheld andstrictly interpreted, why does acontractor need a CGL?

In reaching their decisions, some of thecourts have stipulated that faultyworkmanship should be addressed by aperformance bond. A bond is notinsurance. The surety has the right ofrecovery if any payment is made.Furthermore, the statute of repose forcontractors in Pennsylvania is 12 years.How many sureties are willing to extendtheir bond period following completionfor 12 years? I can answer that one.None!

The good news, if there is any, is thatseveral insurers have developedendorsements to address this problemby redefining “occurrence.” Thoseinsurers are to be congratulated andthanked. Hopefully these endorsementswill remedy the problem we now havein Pennsylvania. If you have not doneso already, talk to your insurers and askthem how they plan to solve this issue.

Until then, my advice to a contractor inPennsylvania is, “Don’t build anything!”Pennsylvania is now one of the most, ifnot the most, restrictive states in thecountry for construction defect claims.

Remember when the license plates inPennsylvania stated, “You’ve got afriend in Pennsylvania?” Well,contractors don’t!

Y’all take care!

G10029_01-13.qxd:July09Primary 6/15/09 1:53 AM Page 11

[ 12 ]

Glance at EventsDate Topic Location

7 CISR Commercial Casualty Allentown, Pa.

Mistakes That Lead to E&O Claims seminar Allentown, Pa.

8 CISR Commercial Casualty Mechanicsburg, Pa.

William T. Hold seminar (Personal Lines) Philadelphia, Pa.

Insuring Contractors Newark, Del.

9 CISR Commercial Property Lancaster, Pa.

William T. Hold seminar (Commercial Lines) Salisbury, Md.

Insuring Contractors Philadelphia, Pa.

14 William T. Hold seminar Baltimore, Md.

10 Ways to Get Sued (Sources of E&O Claims) seminar Mechanicsburg, Pa.

20 CIC Commercial Casualty Philadelphia, Pa.

21 CIC Commercial Casualty Philadelphia, Pa.

CISR Commercial Casualty Erie, Pa.

22 CIC Commercial Casualty Philadelphia, Pa.

CISR Agency Operations Baltimore, Md.

CISR Commercial Casualty Pittsburgh, Pa.

23 CIC Commercial Casualty Philadelphia, Pa.

William T. Hold seminar (Personal Lines) Pittsburgh, Pa.

28 Compliance Pitfalls—How to Avoid Costly Fines & Penalties seminar Pittsburgh, Pa.

29 Compliance Pitfalls—How to Avoid Costly Fines & Penalties seminar Mechanicsburg, Pa.

Don’t wait for a CISR course to come to you — access it from your desktop! CISR OnLine is an excellent way tocomplete a course you need that may not be scheduled in your area in the timeframe you need it. You can alsomix and match the CISR OnLine course with classroom courses so you can still maximize the benefit ofnetworking and face time with the instructor. Register for courses online at iabgroup.com.

J U L Y C A L E N D A R

G10029_01-13.qxd:July09Primary 6/15/09 1:54 AM Page 12

?ANSWER:No, but it’s not always that simple. We have alreadyaddressed this issue in the past, but an update is neededbased on recent developments. In all cases, the answer willdepend on:

w the state where the practice occurs and

w the type of financial institution and/or loan.

First of all, our three states now all have language prohibitingthe practice of requiring more than the replacement value ofthe buildings. It is important to remember that thisprohibition applies to state-chartered banks.

Delaware: The Delaware Code specifically addresses theamount of property insurance in connection with the loan atChapter 21. Mortgages on Real Estate, section 2119 Insurancerequirements for mortgages. It states, in relevant part, thatthe lender may not require more than “the value placed onthe improvements,” which by definition excludes the value ofthe land.

Maryland: The Maryland Code is replete with protection forconsumers, prohibiting state-chartered lenders fromrequiring a borrower to obtain coverage beyond thereplacement cost of the real property. Members who areconfronted with this situation can refer the lender toCommercial Law/ Credit regulations § section 12-124 (for afirst mortgage or first deed of trust). Substantially similarlanguage is also available at § 12-410 for secondarymortgages, § 12-312 (e) for consumer loans, § 12-909 (e) forrevolving-credit transactions, and at § 12-1007 (f) for closed-end-credit transactions.

Pennsylvania: IA&B spearheaded the Mortgage PropertyInsurance Coverage Act (Act 51 of 2008), which applies toowner-occupied residential property. The new law prohibits

lenders from requiring a borrower to obtain propertyinsurance coverage which exceeds the replacement value ofbuildings and structures situated on the land. The borrowermay not be required to insure the value of the land.

Fannie Mae / Freddie Mac: Fannie Mae and Freddie Macpurchase mortgages and convert them for resale to investors.Both institutions have specific guidelines that also prohibitthe practice of asking more than the replacement cost. If theissue you run into involves any one of these institutions, thelender should be referred to:

w the Fannie Mae Selling Guide - Single Family (Part B,Chapter B7-3, Hazard and Flood Insurance) or

w the Freddie Mac Single Family Seller/Servicer Guide(Volume 2, Chapter 58, Section 58.2).

Flood policies: if the situation involves a flood policy, youmay refer the lender to the NFIP publication entitledMandatory Purchase of Flood Insurance Guidelines, availableat fema.gov/pdf/nfip/mandpur1.pdf. A similar prohibition isalso clearly stated.

The main stumbling block remains national banks (whichhave the word “national” in their name or “N.A.” after theirname). National banks are regulated by the Office of theComptroller of the Currency (OCC). The OCC does notcurrently provide any guidance for lenders on this issue.Producers can still encourage individuals to file a complaintwith the Office of the Comptroller of the Currency, but thereis no legal or regulatory leverage to speak of.

IA&B has developed a state-specific resource on the issue ofloan value. It is accessible at iabgroup.com under AgencyManagement/Coverage Issues/Homeowners. Any questionscan be directed to IA&B’s Member Service Center toll free at(800) 998-9644 or locally at (717) 795-9100, option 0, or bye-mailing [email protected].

QUESTION:

A mortgage lender is requiring my insured to cover the home for the full loan value rather than the replacement

cost. Is this an acceptable practice?

DO YOU HAVE A QUESTION? E-mail it to us at [email protected]. Please use “Primary Agent FAQ” in the subject line of your message. You can also fax yourquestion to (717) 795-8347. We look forward to answering your questions!

Member FAQ

[ 13 ]

G10029_01-13.qxd:July09Primary 6/15/09 1:54 AM Page 13

CUSTOMER SERVICE

How do you create value?This apparently simplequestion may well be themost important one youwill ever be asked. Yourability to clearly articulateyour value proposition willseparate you from thepack, elevate yourperformance and offerdirection as you moveahead with your career.

Value proposition: your meal ticket to anamazing career

G10029_14-19.qxd:July09Primary 6/15/09 2:01 AM Page 14

[ 15 ]

Primary Agent | July 2009

Your value proposition is the reason for yourprofessional existence. It describes how youcreate value for others. It makes you stand out ina crowded marketplace. Without a compellingvalue proposition, you are ordinary anddisposable — a commodity. With a distinguished

value proposition, you are unique and indispensable.

A value proposition statement summarizes the reason why apotential customer should buy your particular product orservice, how it exceeds that of your competition and why it isworthy of the price they must pay. The ideal value propositionis concise and appeals to the customer’s strongest decision-making drivers. It is an irresistible offer, an invitation that isso compelling and attractive that the customer would be outof his or her mind to refuse your offer. The million dollarquestion is how to make your value proposition seductive.

Research indicates that most professionals do not have avalue proposition in the form of a clear and concise statement that explains the tangible results their customerswill receive, the unique benefits they bring to bear that otherscannot. A differentiated value proposition goes beyondfunctional product or service descriptions to express theresults a consumer can expect to achieve. Most peopleattempt to sell a product or service without focusing oncustomer benefits or outcomes.

Let’s take a look at two well-known value propositionstatements from FedEx and M&M.

“When your package absolutely, positively has to get there overnight.”

FedEx became the leading overnight courier in the world withthe help of this value proposition by identifying that thecustomer did not just want fast delivery but also valued arock-solid guarantee of urgent delivery.

“The milk chocolate melts in your mouth, not in your hand.”

M&M’s powerful value proposition made customers realizethat chocolate did not have to make a mess. This statementmade a particular impact with children.

Which of the following value proposition statements wouldyou be most likely to respond to:

w “We offer one-stop shopping. My company can offer you a full range of products and services to meet yourevery need!”

w “After going through our unique process, one client saw a 30 percent reduction in claim frequency and a

A powerful value proposition is

not about you. It is not about

the products, services and

resources of your firm. It is all

about the customer. Your ability

to articulate how you are

uniquely qualified to help the

customer will distinguish you

from others in the marketplace.

YG10029_14-19.qxd:July09Primary 6/15/09 2:01 AM Page 15

25 percent decrease ininsurance costs.Through the utilizationof my diagnosticsystem, you willrealize significantimpact to your bottom line.”

Earlier this year, I had thepleasure of meeting Kelly ata Beyond Insurance®

workshop. Kelly is asuccessful agency principalwho cares deeply abouteach and every member ofher 50 person firm. Duringthe workshop, Kellyconfided in me that she wasperplexed about theperformance of Ryan andChase — two of her seniorproducers.

Kelly stated, “Both men arepolished, passionate andextremely professional.They are team players whoeffectively utilize theagency’s value-addedservices and resources.However, I cannotcomprehend why Chaselags so far behind Ryan inbusiness-developmentperformance.”

It was obvious that Kelly cared about Ryan and Chase. She truly hadtheir best interests at heart. Yet, she was painedby the fact that Chase’sbook of business washovering around $500,000in revenue after 10 yearswith the firm, while Ryanboasted a $2,000,000 book of business.

“Chase has an amazingwork ethic,” said Kelly. “Heis personable, attractive andtechnical. He is adored byour staff and thecommunity. I don’t get it.”

After carefully listening toKelly agonize over theperformance gap betweenRyan and Chase, Isuggested that Kellyaccompany both individualsto a handful of first-meetingprospect interviews to studyeach individual’s valueproposition. Kelly loved theidea. She created ascorecard to evaluate bothindividual’s valueproposition in the followingthree areas:

1. The ability of Ryan andChase to articulatehow they create value.

2. The consumers’ abilityto understand andappreciate eachindividual’s valueproposition.

3. The degree to whicheach person’s valueproposition wasdifferentiated fromothers in themarketplace.

Two weeks after leaving theBeyond Insurance®

workshop, I received anenthusiastic phone call from Kelly.

“I figured it out,” she said.“The only differencebetween Ryan and Chase isthe quality of their value

[ 16 ]

CUSTOMER SERVICE

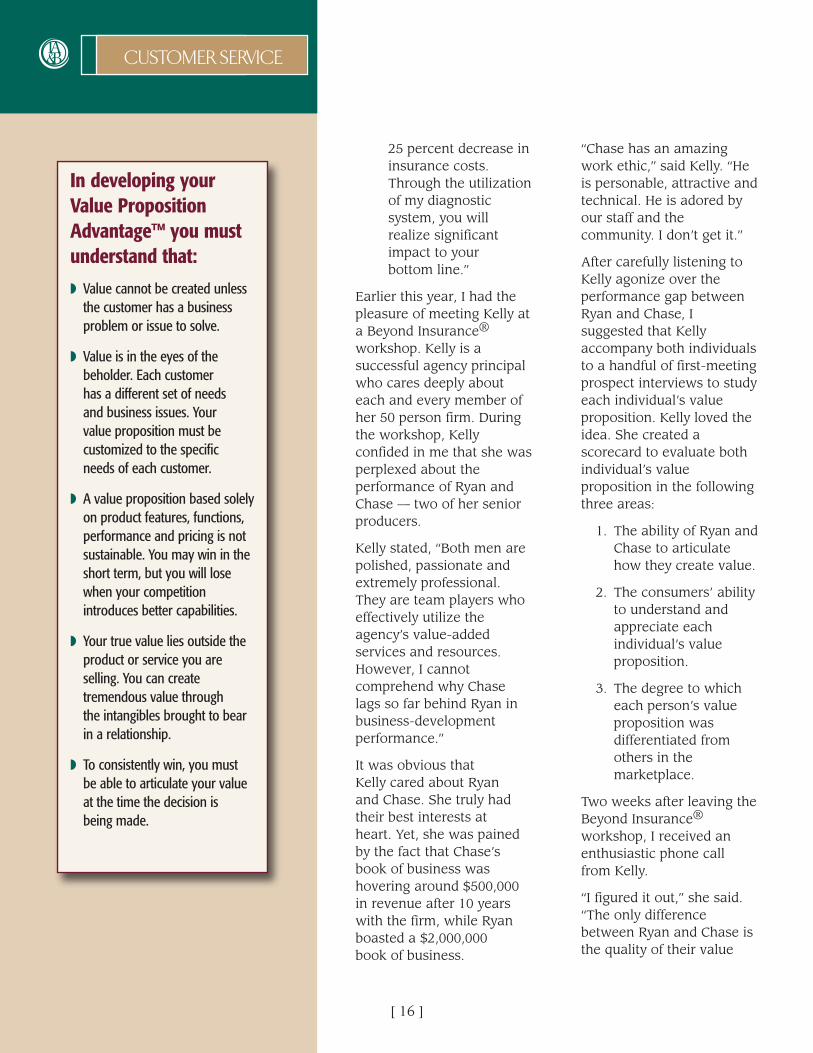

In developing yourValue PropositionAdvantage™ you mustunderstand that:

w Value cannot be created unlessthe customer has a businessproblem or issue to solve.

w Value is in the eyes of thebeholder. Each customer has a different set of needs and business issues. Your value proposition must becustomized to the specific needs of each customer.

w A value proposition based solelyon product features, functions,performance and pricing is notsustainable. You may win in theshort term, but you will losewhen your competitionintroduces better capabilities.

w Your true value lies outside theproduct or service you areselling. You can createtremendous value through the intangibles brought to bearin a relationship.

w To consistently win, you must be able to articulate your valueat the time the decision is being made.

G10029_14-19.qxd:July09Primary 6/15/09 2:02 AM Page 16

[ 17 ]

proposition statements. Ryan’s is clear and concise.The consumer is able tounderstand and easily identify with how he createsvalue. On the other hand,Chase is missing the mark. Hespeaks eloquently about theagency’s unique process andservices, yet does notdemonstrate the impact to thecustomer. He uses too muchinsurance jargon.”

Kelly had uncovered acommon flaw in many well-intentioned producers. They do not reach theirperformance potential as theylack a compelling andattractive value proposition.

Over the next month, I workedwith Kelly to repackageChase’s value proposition.Before Kelly and I could helpChase formulate his valueproposition, we asked him to answer the followingquestions:

1. What do you believe theconsumer values?

2. What are the biggestchallenges facing theconsumer as they relateto insurance and riskmanagement?

3. What unique abilities doyou possess to assist theconsumer with thesechallenges?

4. Who is your competitionand what are theydelivering?

5. What can you providethat your competitorscannot?

6. What will be the outcomeif you can help thecustomer with thesechallenges?

Accompanying the fivequestions listed above, I sent Chase a document to be posted in his office which stated, “A powerfulvalue proposition is not aboutyou. It is not about theproducts, services andresources of your firm. It is all about the customer. Your ability to articulate howyou are uniquely qualified tohelp the customer willdistinguish you from others in the marketplace.”

With guidance and inspirationfrom Kelly, Chase retooled his value propositionstatement. He boiled down the complexities of how hecreates value into somethingthat the customer could easilygrasp, identify with andremember. Chase’s new,irresistible value propositionstatement was all abouthelping the customer discoverissues and create solutions. It was also aboutdifferentiation. Chase realizedthat to be successful, his value proposition had to bedifferentiated and superior to all others.

In a recent conversation,Chase informed me that he is having the best year of his career.

He said, “I now have a clearerpicture of who I am and myrole in serving the customer. I had no idea of theimportance of my valueproposition statement. My new value propositionpinpoints my ability to uncoverthe customers’ issues anddeliver solutions to addressthese problems. The shift in my thinking about how I create value has impacted my confidence, attitude and results.”

How do you create value? Your answer to this questionhas unparalleled implicationsin determining your futuresuccess.

______________________________

The author, Scott Addis, is thepresident and CEO of The AddisGroup and Addis IntellectualCapital, LLC (AIC). AIC is acoaching and consultingcompany with the purpose oftransforming the process thatinsurance agents, brokers andcarriers use when working withtheir clients. Scott is recognizedas an industry leader havingbeen named Inc Magazine’s“Entrepreneur of the Year” as well as one of the 25 MostInnovative Agents in America. He can be reached [email protected] or 610-945-1019.

G10029_14-19.qxd:July09Primary 6/15/09 2:02 AM Page 17

CUSTOMER SERVICE

Customer service is more than icing on the cake.It’s the bread and butter of an agency’s livelihood.

“Getting people-skillstraining is the easiestchange agencies canmake to improve theircustomer service.”

Rita Hollada,Customer Service

Consultant &IA&B Instructor

Customer service slumpsand solutions

G10029_14-19.qxd:July09Primary 6/15/09 2:02 AM Page 18

[ 19 ]

Primary Agent | July 2009

The only stable source of income an agency has is itsexisting customers,” says Rita Hollada, an IA&Binstructor and customer-service consultant for theinsurance industry. “Keeping customers happy is asource of profitability through continued growth andnew referrals.”

Hollada cites a study that found agencies require up to four yearsto overcome the costs associated with the loss of an account.

“Going out to get new customers is far more expensive than anagency may know,” she says.

Industry professionals may be surprised by the value customersplace on service as well.

“Assuming that price is all that matters is a mistake,” says Hollada,pointing to another study. “Of the top 10 things that customers findmost important when dealing with their insurance agent, priceranks sixth, while customer service is first.”

Service challengesThe economic downturn undoubtedly has affected the day-to-dayoperations of insurance agencies, and one of the strains is oncustomer service.

“One challenge is doing more with less,” explains Hollada, “lesspremium but not less work or fewer customers.”

In response to reduced income, some agencies are implementingvoluntary furloughs and foregoing the replacement of retiredemployees. And those personnel changes can have a negativeeffect by disrupting hard-earned relationships between clients andtheir agency contacts.

Additional challenges stem from technology. First there arecarriers’ various delivery systems and degrees of automation.

“The learning curve is phenomenal,” says Hollada.

Then there are the new sources of insurance information — much ofit misinformation – that insureds can easily find on the Internet. Thatcreates situations when agency staff must re-educate customers,many of whom are confused and some of whom are angry.

Training solutionsA little training can go a long way toward addressing these issuesand improving service. IA&B offers Dynamics of Service andAgency Operations courses – both through the CISR designationprogram — that cover people, listening and communication skills.

“Getting people-skills training is the easiest change agencies canmake to improve their customer service,” says Hollada. “It’s not agiven that employees know the importance of building rapport.”

In addition to the CISR courses, IA&B offers in-house, customer-service trainings that can be customized to an agency’s specific needs.

“The industry offers lots of technical training but needs to do morewith relationships,” offers Hollada.

To register for CISR seminars,

including Dynamics of Service

and Agency Operations, visit

iabgroup.com and select

Education from the left-hand

navigation bar.

For more information on

customized, in-house programs,

call IA&B’s Member Service

Center toll free at

(800) 998-9644 or locally at

(717) 795-9100, option 0.

See page 27 for details on

Dynamics of Service and

Agency Operations seminars

offered through IA&B.

T“G10029_14-19.qxd:July09Primary 6/15/09 2:03 AM Page 19

AGENCY MANAGEMENT

When the sheer amount of data entry began to slow down his agency, Jerry O’Donovan foundhelp — a half a world away.

When the back office ishalf a world away

G10029_20-27.qxd:July09Primary 6/15/09 2:14 AM Page 20

[ 21 ]

Primary Agent | July 2009

When the soft market of the late ‘80s andearly ‘90s hit, Jerry O’Donovan searchedfor a better way to position his agency,O’Donovan & Associates Inc., and in 1995he created TimberSure. The niche programpositioned him to insure subagents’

logging contractors throughout the country.

Early on, carriers oversaw policy issuance, but through theyears, they began requiring O’Donovan’s staff to handle it.

“Now we process just about everything but claims,” explainsO’Donovan, as he rattles off the list of duties. “We haveunderwriting authority, and the tradeoff in order to get the penand function of the program is that the carrier has feweroverhead costs.”

How it all beganAround the same time, New York-based insurance wholesalerThe Distinguished Programs Group developed a uniquesolution to their own staffing needs.

When an insurer pulled out and left them with theoverwhelming task of reissuing thousands of habitationpolicies, the agency principal’s son, who was in Chinateaching English, offered that a few of his college studentsmight pick up the work on the side.

_________________________________________________________

“We couldn’t find anyone to handle the work,”

says O’Donovan. “Everyone right out of high

school expected to make $45,000 a year, and then

we had to worry if they would show up or not.”

_________________________________________________________

With six students in Qingdao, China on the case, the backlogthat would have taken The Distinguished Programs Groupfour to six months to complete took only three weeks.

And from there, the insurance-processing company ReSourcePro was born. Today nearly 600 Chinese students work forinsurance-related agencies and companies throughout theUnited States, O’Donovan & Associates included.

Why it’s neededBack in Glenelg, MD, the sheer amount of data entry wasweighing — and slowing — down O’Donovan’s agency.

“We couldn’t find anyone to handle the work,” saysO’Donovan. “Everyone right out of high school expected tomake $45,000 a year, and then we had to worry if they wouldshow up or not.”

W

Q. What is remote staffing?

A. Remote staffing offers some

of the benefits of outsourcing

(lower costs, processing

expertise) but is different

in that it does not require

agencies to migrate their

agency management

system or data to an

external provider.

Adapted from resourcepro.com

G10029_20-27.qxd:July09Primary 6/15/09 2:15 AM Page 21

After learning about ReSource Pro ata Target Markets annual meeting,O’Donovan contracted withthem in January 2008. Theoriginal contract covered theoutsourcing of data entry toone employee. Today O’Donovanworks with five and may add a sixth.

How it worksO’Donovan and his 11 on-site staff developedhow-to manuals for their Chinesecounterparts and now communicate withthem via e-mail and telephone. Each nightO’Donovan’s staff places work in an electronicoutbox. Then the ReSource Pro employeescomplete it overnight — which, of course, isthe next workday in China.

“We write auto, CL and property,” explainsO’Donovan. “That means we have a numberof ACORD applications, MVRs, loss runs, etc.These guys enter the data into the system for us.”

In fact, the ReSource Pro employees are soefficient and detail-oriented that O’Donovanhas expanded their duties to include quotingthrough the rating system.

“They have helped us with efficiency andprocessing time,” he continues. “It used totake us 60 days to process an endorsement.Now it’s done in two days.”

O’Donovan points to another benefit: Lesshuman resources work.

“I don’t have to worry about employeeissues,” he says. “No taxes, no benefits.There’s just one flat fee per year. And theyhave made us money because of an increasein production.”

For O’Donovan, who keeps a photo of hisChinese team on his desk, a back office that works a day ahead presents the perfectstate of affairs.

[ 22 ]

Each night O’Donovan’s staff places workin an electronic outbox. Then theReSource Pro employees complete itovernight — which, of course, is the nextworkday in China.

AGENCY MANAGEMENT

800-523-6422, 215-885-7300, 215-886-2482 Fax

Home Office Contacts:Etty Herzig ext. 139 [email protected] or

Janet Barton, ext. 128 [email protected]

COVERAGES TO HELPYOUR BUSINESS GROW

at Insurance Innovators, Inc.

TREE PRUNERS

LANDSCAPERS

DEBRIS REMOVAL

GARDEN CENTER/NURSERIES

SWIMMING POOL INSTALLATION

www.iiigroup.com

G10029_20-27.qxd:July09Primary 6/15/09 2:15 AM Page 22

Bond excuses you’ll never hear

from Commonwealth:

“Sorry, the contractor’s

too small and doesn’t have

enough working capital.”

Relax, Commonwealth writes bondsRelax, Commonwealth writes bondsRelax, Commonwealth writes bondsRelax, Commonwealth writes bondsRelax, Commonwealth writes bonds

for small short-on-capital companies.for small short-on-capital companies.for small short-on-capital companies.for small short-on-capital companies.for small short-on-capital companies.

Now, whenever you need to place a bond for a small

contractor who’s short on cash, you can count on Com-

monwealth Insurance. With our innovative approval pro-

cess, we can write bonds for just about anyone with quick

approval. Which means one less headache for you

--and faster profits, too.

Quick, no hassle bonds

make bonding a snap.

With more than a decade of serving insurance agents,

Commonwealth knows how fast you need answers, so

we give you quick approval with NO cash collateral

and NO letter of credit in most cases. 90% of our bonds

are for small and mid-sized companies.

Express service

makes life easier.

Fast turnaround with no runaround is why brokers

depend on Commonwealth Insurance. In most cases,

we can provide the bond you need in 24 hours or less.

Call us for your next bond and learn how easy it is to

place bonds with a minimum of paperwork--and earn

a big commission on every Commonwealth bond.

COMMONWEALTH

INSURANCE

The No-Excuses Bond CompanyThe No-Excuses Bond CompanyThe No-Excuses Bond CompanyThe No-Excuses Bond CompanyThe No-Excuses Bond Company

CALL TOLL FREE: 1-800-886-7760 FAX TOLL FREE:1-800-566-7761

G10029_20-27.qxd:July09Primary 6/15/09 2:23 AM Page 23

INDUSTRY NEWS

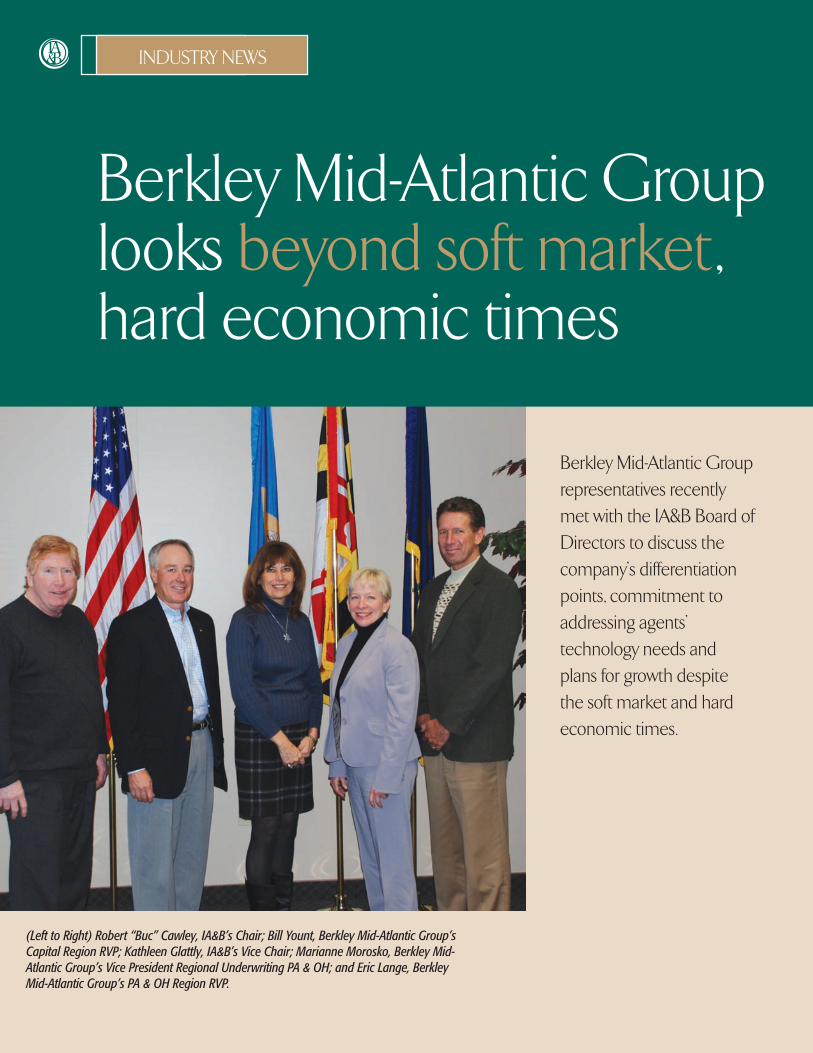

Berkley Mid-Atlantic Grouprepresentatives recentlymet with the IA&B Board ofDirectors to discuss thecompany’s differentiationpoints, commitment toaddressing agents’technology needs andplans for growth despitethe soft market and hardeconomic times.

Berkley Mid-Atlantic Grouplooks beyond soft market,hard economic times

(Left to Right) Robert “Buc” Cawley, IA&B’s Chair; Bill Yount, Berkley Mid-Atlantic Group’sCapital Region RVP; Kathleen Glattly, IA&B’s Vice Chair; Marianne Morosko, Berkley Mid-Atlantic Group’s Vice President Regional Underwriting PA & OH; and Eric Lange, BerkleyMid-Atlantic Group’s PA & OH Region RVP.

G10029_20-27.qxd:July09Primary 6/15/09 2:15 AM Page 24

[ 25 ]

Primary Agent | July 2009

The March IA&B Board of Directors meetingincluded a presentation by three Berkley Mid-Atlantic Group (BMAG) representatives — J. Eric Lange, Regional Vice President for thePennsylvania and Ohio Region; Marianne M.Morosko, Vice President of Agency Relations

and Marketing; and William E. Yount, Regional Vice Presidentof the Capital Region. IA&B invited them to enhance theassociation’s relationship with the carrier, learn more aboutthe company’s market position and strategic direction, review topics of interest to the association and explore areasof common ground.

Strengths“We’ve been blessed with an outstanding claims staff from thebeginning,” shared Yount, when recounting the company’sstrengths, “and our underwriters are very experienced.”

He also pointed to the company’s structure as a differentiationpoint: “We have significant autonomy as an independentoperating unit. We can react to market conditions much,much faster than certain national companies with the typicalhierarchal structure where you have to run it up the flagpoleand get permission and by the time you get the permission it’s too late.”

What’s more, the companies are run with integrity. Accordingto Yount, founder Bill Berkley, who serves as chairman of theboard and CEO, expects his senior management to be “goodcorporate citizens” in addition to delivering a high return oninvestment each year.

GrowthThe soft market, combined with the recession, has hit theindustry hard, so the BMAG representatives were asked howthey can expect to grow in such a challenging environment.

“We have implemented a few steps to penetrate certain areaswhere Berkley Mid-Atlantic Group didn’t really have apresence,” said Yount, who observed that last fall they didn’tanticipate just how drastic the economic downturn would be.“We think there are growth opportunities, not in price per se,but from additional representation, adding policy count. Weanticipate pressure on price to dissipate through the year. Theproblem is that we can achieve small rate increases but stilllose premium because of the economic conditions.”

Lange expanded on growth opportunities and discussed hisdesire to expand in southeastern Pennsylvania along with thecompany’s new areas of focus, including manufacturing andwholesale distribution and alternative energy businesses. Thecarrier has also made its way into the non-profit and socialservice markets by offering professional liability coverage and,as a result, anticipates adding premium this year.

TA history of Berkley Mid-Atlantic Group, LLC

Berkley Mid-Atlantic Group, LLC is aregional insurance operation offeringcommercial property and casualtycoverages in Delaware, the District ofColumbia, Maryland, North Carolina, Ohio,Pennsylvania, South Carolina and Virginia,with a focus on middle-market commercialaccounts. The company, which writesexclusively through independent insuranceagents, was created in 1999 through thecombination of operations of four regionalunits – Firemen’s Insurance Company ofWashington, D.C.; Presque Isle InsuranceDivision of Firemen’s Insurance Company of Washington, D.C.; Chesapeake BayProperty and Casualty Insurance Company; and Berkley Insurance Companyof the Carolinas.

Berkley Mid-Atlantic Group is part of the W. R. Berkley Corporation. Founded in 1967, the W. R. Berkley Corporation is aninsurance holding company with $4 billion in written premium and along-term strategy of decentralizedoperations. It is among the largestcommercial-lines writers in the UnitedStates and operates in five segments ofthe property/casualty-insurance business:specialty insurance, regionalproperty/casualty insurance, alternativemarkets, reinsurance and international.

G10029_20-27.qxd:July09Primary 6/15/09 2:15 AM Page 25

TechnologyBerkley Mid-Atlantic Groupis working to improve itsperformance in thetechnology segment ofIA&B’s most recent CompanySatisfaction Index survey.Company representativesoffered that they take thoseresults seriously and aremaking improvements as a result.

One way that the company isaddressing the issue is via itsreal-time, automated system,Berkley Link, which willconnect agency managementsystems with the carrier’srating system.

“We’re getting ready to do avery slow rollout of BerkleyLink, and we’re starting inPennsylvania with fouragents,” said Morosko.

At first the technology will beutilized for business owners’,auto and workers’compensation policies.Eventually, the carrier willuse it for all lines.

“We’re not looking at it as a rating quote system toget small business,”explained Morosko, whoexpressed interest inincreasing the averageaccount size of businessowners’ policies. “We’relooking at it as an easier wayfor agents to get business tous and to prevent re-keyingerrors which generateendorsement requests.”

OpportunitiesBerkley Mid-Atlantic Groupis looking for newappointments with agenciesthat can meet the company’sobjectives, includingreaching a profit-sharingpremium eligibility thresholdof $500,000 within the firstfew years.

“We’re looking for agentswith capabilities andstrategic plans for organicgrowth, agents whoarticulate a true need for a company like Berkley Mid-Atlantic Group, as wellas the member companies ofthe W.R. BerkleyCorporation,” said Lange.

According to Yount, therelationship those agents willfind is one of consistencyand mutual trust.

“For the foreseeable future,we plan to deal exclusivelywith independent agents asour sole source ofdistribution,” he said. “Wedepend on a tightrelationship with ouragencies, and where wehave trust, we have success,and it’s mutually profitable.”

Additional information aboutBMAG is available atwrbmag.com.

[ 26 ]

INDUSTRY NEWS

“We depend on a tight

relationship with our agencies,

and where we have trust,

we have success, and it’s

mutually profitable.”

G10029_20-27.qxd:July09Primary 6/15/09 2:16 AM Page 26

[ 27 ]

The Certified Insurance ServiceRepresentatives (CISR) designation is intended for agency personnelinterested in improving their customer service.

The completion of five, one-daycourses, along with correspondingexams, is required within three years ofstarting the program. Designees leavewith a thorough understanding of risks,coverages and exposures, which makesthe program ideal for newer agentsand agency personnel.

Dynamics of Service and AgencyOperations are two of the seminarsparticularly geared to customer service.

Dynamics of ServiceThe Dynamics of Service coursefocuses on customer service skills.Designed for customer servicepersonnel, the one-day programteaches mediation skills, behaviorstyles and communication techniquesto improve dealings with difficultpersonalities. The goal? Tactful yetdecisive customer service.

Topics:

w Integrating service from the saleonward

w Targeting common “peopleissues”

w Learning people skills

w Improving listening andcommunication skills

Agency OperationsThe Agency Operations course coversinsurance agencies’ dynamics andoperations. Designed for agency andcompany personnel, the seminarfocuses on the basics of riskmanagement, financial-statementanalysis, due diligence, accountmanagement and claims processing.

Topics:

w Understanding agency functionsand systems

w Meeting ethics and legalobligations

w Insuring commercial casualty

w Analyzing general liability,workers’ compensation,commercial auto endorsements

w Qualifying risk and analyzing risk exposures

To register for CISR seminars, includingDynamics of Service and AgencyOperations, visit iabgroup.com and select Education from the left-handnavigation bar.

CISR OnLineSeveral CISR courses,

including Agency Operations,

are now available on

demand. Participants have

30 days after registering to

take the course. It is accessible

any time of the day or night

and can be stopped and

restarted as needed.

Customer serviceby the books

G10029_20-27.qxd:July09Primary 6/15/09 2:16 AM Page 27

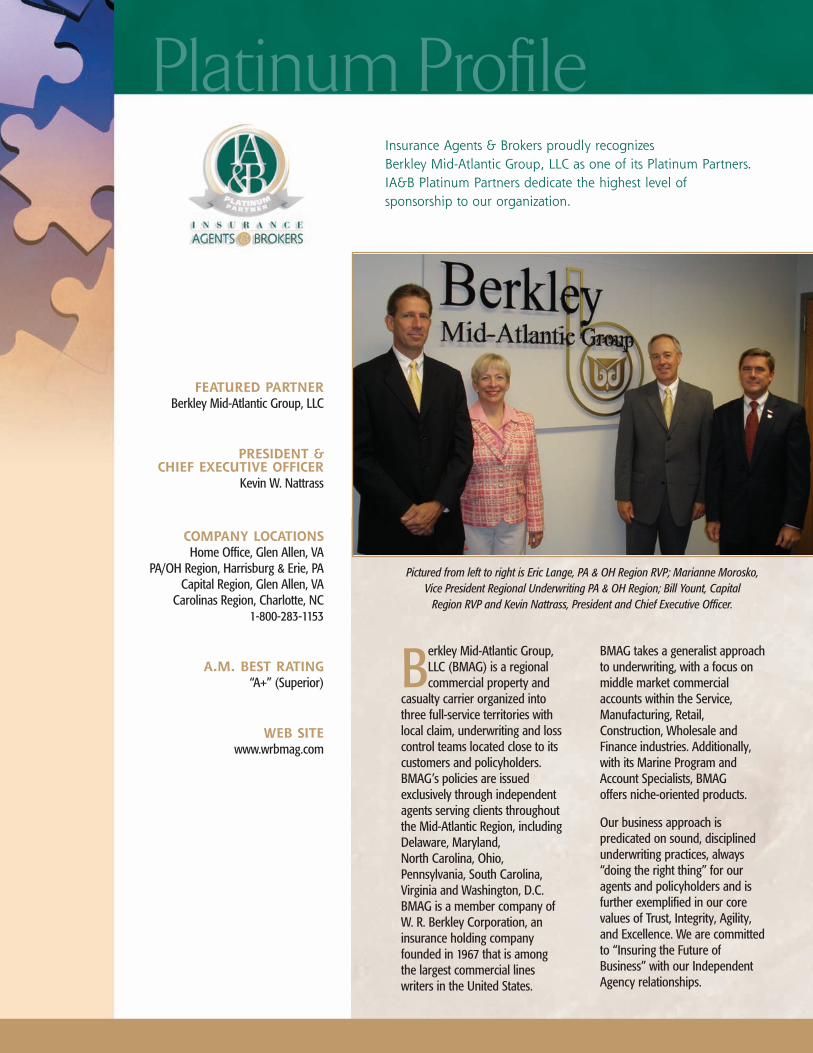

Platinum ProfileInsurance Agents & Brokers proudly recognizes Berkley Mid-Atlantic Group, LLC as one of its Platinum Partners.IA&B Platinum Partners dedicate the highest level ofsponsorship to our organization.

FEATURED PARTNERBerkley Mid-Atlantic Group, LLC

PRESIDENT & CHIEF EXECUTIVE OFFICER

Kevin W. Nattrass

COMPANY LOCATIONSHome Office, Glen Allen, VA

PA/OH Region, Harrisburg & Erie, PACapital Region, Glen Allen, VA

Carolinas Region, Charlotte, NC1-800-283-1153

A.M. BEST RATING “A+” (Superior)

WEB SITEwww.wrbmag.com

Berkley Mid-Atlantic Group,LLC (BMAG) is a regionalcommercial property and

casualty carrier organized intothree full-service territories withlocal claim, underwriting and losscontrol teams located close to itscustomers and policyholders.BMAG’s policies are issuedexclusively through independentagents serving clients throughoutthe Mid-Atlantic Region, includingDelaware, Maryland, North Carolina, Ohio,Pennsylvania, South Carolina,Virginia and Washington, D.C.BMAG is a member company ofW. R. Berkley Corporation, aninsurance holding companyfounded in 1967 that is among the largest commercial lineswriters in the United States.

BMAG takes a generalist approachto underwriting, with a focus onmiddle market commercialaccounts within the Service,Manufacturing, Retail,Construction, Wholesale andFinance industries. Additionally,with its Marine Program andAccount Specialists, BMAG offers niche-oriented products.

Our business approach ispredicated on sound, disciplinedunderwriting practices, always“doing the right thing” for ouragents and policyholders and isfurther exemplified in our corevalues of Trust, Integrity, Agility,and Excellence. We are committedto “Insuring the Future ofBusiness” with our IndependentAgency relationships.

Pictured from left to right is Eric Lange, PA & OH Region RVP; Marianne Morosko,Vice President Regional Underwriting PA & OH Region; Bill Yount, Capital

Region RVP and Kevin Nattrass, President and Chief Executive Officer.

G10029_28-32.qxd:July09Primary 6/15/09 2:30 AM Page 28

WHAT IS IA&BPARTNERS?The IA&B Partners

program gives company

and allied businesses

the opportunity to

demonstrate their

commitment of support

to independent agents

and receive maximum

market exposure. As an

IA&B Partner, you will

also realize the benefits

of IA&B membership to

help you succeed in

the insurance industry.

DO YOU SEEYOUR NAME?To become an IA&B Partner,

choose the sponsorship

package that matches your

commitment of support.

Contact the Member Sales

Center at (800) 998-9644,

(717) 795-9100 or visit us

online at www.iabgroup.com

to get started.

Listed below are those companies that strongly support the independent agency

system and Insurance Agents & Brokers.Thank you for your continued sponsorship.

PLATINUM LEVELBerkley Mid-Atlantic GroupErie Insurance GroupHarleysville InsuranceInsurance Agents & BrokersService Group IncMillers Mutual GroupMillville Mutual Insurance CoMutual Benefit GroupPenn National InsuranceSelective Swiss ReThe Main Street America GroupTravelersUtica National Insurance Group

GOLD LEVELOhio CasualtyProgressive

SILVER LEVELAegis Security Insurance CoAmerican Mining Insurance CoCumberland Insurance GroupFrederick Mutual Insurance CoHarford Mutual Insurance CoJuniata Mutual Insurance CoMMG Insurance CompanyPrivate Client GroupPSBA Insurance TrustThe Motorists Insurance GroupWestfield InsuranceZenith Insurance

BRONZE LEVELAAA Insurance

Agency Insurance Company

Allied Insurance

Briar Creek Mutual Insurance Company

Builders Insurance Group

Capitol Insurance Company

Chubb Group of Insurance Companies

Companion Property & Casualty Group

Countryway Insurance Company

Encompass Insurance

Foremost Insurance Group

Friends Cove Mutual Ins Company

Goodville Mutual Casualty Company

Grange Insurance Companies

Hanover Fire & Casualty Insurance Company

Insurance Alliance of Central PA Inc

Insurance Placement Facility of PA

Keystone Insurers Group Inc

Lebanon Mutual Insurance Company

Mercer Insurance Group

Merchants Insurance Group

Mercury Casualty

Penn Millers Insurance Company

Penn Prime Municipal Insurance

PMSLIC Insurance Company

Reamstown Mutual Insurance Company

Rhoads & Sinon LLP

Rockwood Casualty Insurance

State Auto Mutual Insurance Company

TAPCO Underwriters Inc

The Brethren Mutual Insurance Company

The Mutual Service Office Inc

The Philadelphia Insurance Companies

Tuscarora Wayne Mutual Insurance Company

UPAC Insurance Finance

Primary Agent July 2009

G10029_28-32.qxd:July09Primary 6/15/09 2:30 AM Page 29

JEFF YATES, ACTEXECUTIVE DIRECTOR

Jeff Yates is executive director of

the Agents Council for

Technology (ACT) which is part

of the Independent Insurance

Agents & Brokers of America.

Jeff can be reached at

[email protected]. ACT

has posted further information

on many of the subjects

discussed above at

www.independentagent.com/act.

This article reflects the views of

the author and should not be

construed as an official

statement by ACT.

Primary Agent | July 2009 TechnologyU P D A T E

[ 30 ]

Independent agents certainlyhave a lot of challenges rightnow. We are dealing with aproperty-casualty market thatis not growing. Many of ourcommercial-lines clients havehad to scale back or haveclosed their doorspermanently. Our investmentshave taken a severe hit. Weare understandably concernedabout whether independentagents will continue to have arole in the health insurancemarket as national health careproposals are beingdeveloped.

Focusing on theopportunitiesDuring this time of challenge,it is easy to become fixatedupon the problems and to

overlook the hugeopportunities that are staringus in the face. As I have gonearound the country talkingwith agents, what hasimpressed me is the numberof agencies that are continuingto grow even in this toughmarket. I run into agencieswhich have been able todouble their premium volumewith the same number ofemployees. How are theseagencies doing it?

A common thread I have seenamong these agencies is adetermined focus to takeadvantage of the newtechnologies available toenhance their productivity.This focus is driven by theagency principals, and they

are using the time and costsavings they achieve to buildtheir sales power. Theseagency leaders understandthat technology has finallyimproved to the point that itcan deliver significant benefitsto them far outweighing thecosts, provided they fully usethe technology’s capabilities.Carrier reps have told me thatthey are finding thetechnology-savvy agenciesrunning disciplined shops tobe their best business partnersand performers.

Technology-driventransformationConsider this quote fromDaniel Burrus, the author ofTechnotrends, who is knownfor his forward thinking and

POSITIONING YOUR AGENCY TO PROSPER IN A TOUGH MARKET

G10029_28-32.qxd:July09Primary 6/15/09 2:31 AM Page 30

[ 31 ]

ability to identify significant trends and opportunities:

We are now at the dawn of aprofound technology-driventransformation that will make thechanges we have experiencedover the past 25 years seemsmall and slow…. We are aboutto transform how we sell, market,communicate, collaborate,innovate, watch TV, learn and asyou might guess, much more….This is a once-in-a lifetimeopportunity for you personally,and for your organization. Don’tmiss it! (January 2009Technotrends Newsletter)

So how are these agencies usingtechnology to enhance their productivityand how is it benefiting them? Theseagencies are moving to an electronicmodel as completely as they can,eliminating paper wherever possible.Their agency management systemsprovide the hub for their information,and their other systems, if needed,integrate with their management systemas much as possible. These agencies areactive in their user groups, takingadvantage of the excellent classes andonline services provided by thesegroups to help them get maximumbenefit out of their systems. They alsodrive continued improvements in theirsoftware from their vendors throughthese user groups.

Productivity-minded agencies providetheir servicing and processingemployees with at least two monitors,and sometimes three. The additionalmonitors pay for themselves in addedproductivity in well under one year. Thecapability of their systems to generateautomated letters to clients is used tothe maximum extent possible. Theobjective is to automate processingwherever possible, so that employeescan concentrate on more productiveservicing and sales activities. Employeesare trained on written procedures andworkflows that are implemented

consistently throughout the agency, andcompliance with the procedures areconsistently monitored. E&O exposuresare reduced as a result.

Real Time – a givenThese best-practices agencies haveimplemented Real Time inquiries(billing, policy view, claims),endorsements and quoting throughtheir agency management systems andcomparative raters. Real Time enablesagents to work with multiple carriers ina consistent way through their ownsystems; it handles log-ons andpasswords to carrier systems and Websites automatically; and it eliminateshaving to re-enter data that is already inthe agency management system. It is a“no brainer” for these agencies to turnon their Real Time capability because itis usually provided by their agencymanagement system at no cost.

In the 2008 IIABA Future One AgencyUniverse Survey, agencies ranked RealTime billing, claims and policy inquiry asthe technology having the greatestimpact on their productivity. And it is nowonder. In the January 2009 Real TimeCampaign Agency Survey, the agentsusing Real Time (inquiries,endorsements and/or quoting) reportedsaving 10 hours a month per employeeon average.

Real Time is fast becoming thepredominant workflow used by agentsto perform transactions with carriers,supplanting carrier-proprietary Websites. That same 2009 Real TimeCampaign Survey indicated that 54percent of the agencies with agencymanagement systems are doing RealTime inquiries and endorsements. Forty-three percent of agents are usingpersonal-lines, real-time rating throughthe agency management system orcomparative rater; and 18 percent areperforming commercial- lines, real-timerating. I expect the amount of real-timequoting in both personal andcommercial lines to grow significantly in2009 because of the tremendous time

savings agent users of this functionalityare deriving. Another very positive signis that 180 carriers and carrier groupsare now offering at least some real-timefunctionality. That’s a 58 percentincrease in two years.

Download – more criticaltodayDownload has become even moreimportant in the world of the electronicagent because the agency depends onhaving accurate data in its system toadvise clients; create certificates, auto idcards and other client documents;generate reports and marketingcampaigns; and transmit data back tocarriers in subsequent real-timetransactions. Best-practices agents notonly have implemented personal-linesdownload; they have implementedcommercial-lines download particularlyfor their small commercial business. Thecarriers, vendors and user groups havedone a lot of work to improve thequality of commercial-lines downloadsin recent years and continuedrefinements are ongoing today. Carrierswill work with agents to start with a fewcommercial policies to see how thedownload impacts their data. To besuccessful with commercial-linesdownload, it is critical that the agency’semployees take a disciplined approachto place data only in the field for whichit was intended so that important data isnot over-written.

Agencies report saving significantprocessing staff time by automating theentry of commission-statementinformation into their systems usingDirect Bill Commission Download.Agents are also taking advantage ofClaims Download where available to getback into the claims loop and toautomate the entry of claims data intotheir systems.

Going “paperless” rocksI am also seeing agents derive greatbenefit from going “paperless.”Agencies typically implement back-endscanning first where the CSRs scan the

G10029_28-32.qxd:July09Primary 6/15/09 2:31 AM Page 31

[ 32 ]

important documents they want to keep.Moving to electronic files allows thosefiles to be more easily shared amongemployees and offices, reduces thenumber of searches for misplaced filesand protects that information shouldthere be a disaster, provided theelectronic information has been properlybacked up.

More and more agencies are now takingthe next step to front-end scanning wheredocuments are scanned as they comeinto the agency and are trackedcontinuously as they make their waythrough the agency, so that processingtime can be monitored and employeeworkloads managed.

The social Web is transformingmarketingSavvy agents are also starting to enhancetheir Internet presence by using social-networking tools. These agentsunderstand that the Web is in the midstof a profound transformation from onewhere static information is presented(Web 1.0) to one where the participantsare actively engaged in contributingcomment and spreading messages (Web2.0). Web 2.0 is creating exciting newopportunities in marketing where agentscan participate in online communitiesand expand their reach considerably, justas previous generations have doneparticipating in civic and othercommunity organizations.

Even more exciting, the Social Web isputting the person back into the Internet,rather than having it dominated by bigcompanies. This bodes very well forindependent agents who excel in buildingpersonal relationships based upon trust.

By developing their personal and agencybrands in these online communities,agents are developing “fans” who want

to learn more about them and theiragencies and visit the agent’s Web site.These fans often help extend the agent’sreach even further by spreading theagent’s message to all of their owncontacts in a viral fashion. Agents arefinding that by participating in acombination of social media – blogs,Facebook, Twitter, and LinkedIn being themost commonly used – they areincreasing the traffic to their Web site,improving their Web site’s position onsearch engines, developing newprospects and establishing theircredentials as an insurance expert to awider audience.

Importance of continuedinvestment and innovationSuccessful businesses continue to investand innovate in tough markets permittingthem to emerge as even more dominantplayers when the clouds clear away andthe sun returns. It is wonderful to see somany independent agencies takingadvantage of this period ofunprecedented opportunity to employproductive technologies, implement newmarketing strategies and transform theirstaffs’ focus from processing to moreproactive service and sales. These agentsrealize that this is absolutely the best timeto be an independent agent because oftheir unique ability to provide theircustomers with choices; their ability toengender trust; and their agility to makechanges to adjust to new marketconditions and take advantage of newopportunities.

TECHNOLOGY UPDATE

Commonwealth Insurance Co . . . . . . . . . . . . .23

General Casualty . . . . . . . . . . . . . . . . . . . . . . . . .3

Guard Insurance Group . . . . . . . . . . . . . . . . . . .1

IA&B Series Ads . . . . . . . . . . . . . . . . . . . . . . . .IBC

IA&B Partners Program . . . . . . . . . . . . . . . . . . .29

Insurance Innovators . . . . . . . . . . . . . . . . . . . .22

Interstate Insurance Mngmnt. . . . . . . . . . . . .OBC

KnightBrook Insurance Co . . . . . . . . . . . . . . .IBC

Preferred Property Program . . . . . . . . . . . . . . . .9

Progressive . . . . . . . . . . . . . . . . . . . . . . . . . . . .IFC

Susquehanna Ins Agents Alliance . . . . . . . . . . . .5

ClassifiedA D V E R T I S E M E N T S

Ad Index

SOUTHEAST PA PRODUCERS & AGENCIES

Professional agency located inFeasterville, Bucks County, Pa. Call for confidential information and a review of our services. Contact Ray Reinard at (215) 375-8600, Ext. 119.

If you would like to place a

Classified Advertisement, simply

fax your ad on company letterhead

to (717) 795-8347, and we will take

care of the rest.

G10029_28-32.qxd:July09Primary 6/15/09 2:31 AM Page 32

A-Rated Carrier Now AppointingNew Producers in Pennsylvania,

Maryland & Delaware! (More states to be added in the near future.)

� Business Insurance—CPP, BOP Monoline Fire, GL

� Competitive pricing—All LinesMSO rates and policy forms

� Personal lines roll overs will be considered

� Commercial auto for artisan contractors, retailers and wholesalers

� Contractor’s policy rated on number of employees, not payroll

� Internet rating system

� No minimum premium requirement forour producers

� Fast and friendly service for our customersfrom company staff

Knightbrook Insurance Company

P.O. Box 686, 927 West Main Street

Valley View, PA 17983

Office: 215-249-1394

Cell: 215-272-1442

Fax: 215-249-1395

E-mail: [email protected]

To get started, please contact Dick Riddle, CPCU

G10029_IFC-IBC-OBCJuly09.qxd:July09Primary 6/15/09 2:42 AM Page 2

Let Interstate help you reap the abundance of summer opportunities.

Ripe For the Picking

Your clients with outdoor businesses need extra protection for the unique risks that the summer season brings. Interstate can cover: