Embed Size (px)

Citation preview

Applied Mathematical Finance, M Routledge

Vol. 12. No. 2. 121-146. June 2005Taylor

Pricing Quanto Equity Swaps in aStochastic Interest Rate Economy

SAN-LIN CHUNG* & HSIAO-FEN YANG**

*Deparlmen! of Finance. National Tainan Uuiversiiy, Tapei 106. Taiwan**Depariment of Finance. Louisiana Stale University. USA

(Received 9 May 2003; in revised form 27 November 2003)

ABSTRACT This paper derives a pricing model for a quanto foreign equityldomestic floatingrate swap in which one party pays domestic floating interest rates and receives foreign stockreturns determined in the foreign currency, hut is paid in the domestic currency. We use the risk-neutral valuation technique developed hy Amin and Bodurtha to generate an arbitrage-freepricing modei A closed-form solution is obtained under further restrictions on the drift rates ofthe asset price processes. Pricing formulae show that the value of a quanto equity swap at thestart date does not depend on the foreign stock price level, but rather on the term structures ofboth countries and other parameters. However, the foreign stock price levels do affect the .swapvalue times between two payment dates. The numerical implementations indicate that thedomestic and foreign term structures, the eorrelation between the foreign interest rate and theexchange rate, and the correlation between the exchange rate and the foreign stock are moreimportant factors in pricing a quanto equity swap than other correlations.

KEY WORDS: Equity swaps, term structure of interest rates, risk-neutral valuation, arbitrage-free pricing model

Introduction

An equity swap is a transaction that allows an investor to exchange the rate of returnon an equity investment (an individual share, a basket of shares, or an index) for therate of return on another non-equity (e.g. fixed or floating rate) or equity investment.Like its currency and interest rate swap predecessors, equity swaps have been wellreceived by the financial markets, because they make it possible to achieve outcomesmore efficiently. For example, equity swaps are widely used to synthesize equity,convert the return character of fixed-income portfolios, bypass transfer andwithholding taxes, reduce transaction costs, avoid jurisdictional dilemmas, andmuch more.

Correspondence Address: San-Lin Chung. Department of Finiince. National Taiwan University, Taipei,106, Taiwan, R.O.C. Te!: 886-2-23676909. Email: [email protected]

I350-486X Print/1466-4313 Online/05/020121-26 © 2005 Taylor & Francis Ltd

DOI: 10.1080/1350486042000297261

122 S.-L Chung & H.-F. Yang

There are various types of equity swaps traded in the over-the-counter market.Among them, quanto equity swaps are common in a variety of situations forpractitioners. A typical function of a quanto equity swap is to convert a percentageequity return in a non-domestic equity into the base currency of the receiver so as toprovide currency protection.' For example, if the Japanese equity market isattractive to a US investor who owns Eurodollar deposits, he could enter into aquanto foreign equity/domestic fioating rate swap in which he agrees to make aseries of payments based on the US.$ LIBOR rate, and in return he receives thereturn of the Japanese equity market determined in Japanese Yen, but is paid inUS$.~ After the transaction, he acquires the return on Japanese equity withoutdirectly incurring an exchange rate risk.

The amount of literature on pricing and hedging equity swaps, not to mentionquanto equity swaps, is few. Marshall et al. (1992) and Rich (1995) provide pricingmodels using expectations operators. However, both of them do not providearbitrage-free valuation formulae. Jarrow and Turnbull (1996) derive a preference-free formula for the fixed rate of an equity swap at the start date only. Chance andRich (1998) use arbitrage-free replicating portfolios to derive valuation formulae fora variety of equity swaps at the start date and during the life of the swaps. They findthat the values of equity swaps generally depend on the stock price level, but at thestart date or immediately after the payment is made, the values of equity swaps areindependent of stock prices. Similar to them, our pricing formulae show that thevalue of a quanto equity swap at the start date does not depend on the foreign stockprice level.

With regard to quanto derivatives, there are some articles on the valuation ofquanto interest rate swaps (differential swaps) (Litzenberger. 1992; Jamshidian,1993; Wei, 1994), and on the valuation of quanto options (Reiner. 1992; Wei, 1995;Chung, 2002). However, to our knowledge, no pricing formulae for general quantoequity swaps have ever been published. Hence, one purpose of this paper is todevelop a pricing model for quanto equity swaps. As an illustration, we only price aquanto equity swap where a foreign equity index return is exchanged for a domesticfloating interest rate with the notional principal denominated in the domesticcurrency. However, as discussed in the following section, our results can be directlyapplied to price general type of quanto equity swaps using the building blockapproach.

The difficulty on pricing quanto equity swaps is that their payoffs are contingenton many variables.^ For example, consider a US investor enters into a two-yearquanto equity swap with a local bank. The swap agreements dictate that the investorwill pay the bank semiannually the US 6-month LIBOR rate plus (or minus) aspread, and in return will receive from the bank the FTSE 100 index return over sixmonths for two years. The notional principal is denominated in US dollars. In arealistic case, one has to consider at least four factors that directly affect the value ofthis swap: the exchange rate ($/£), the US interest rate, the UK interest rate, and theFTSE 100 index price.

In this paper we extend Amin and Bodurtha's (1995) work to value quanto equityswaps. We consider a common type of quanto equity swap in which a foreign(domestic) equity index return is exchanged for a domestic (foreign) floating interestrate with the notional principal denominated in the domestic or foreign currency.

Pricing Quanto Equity Swaps in a Stochastic Interest Rate Economy 123

Using the building block approach, we show that our pricing formulae, combiningwith existing formulae for interest rate swaps, differential swaps and/or plain vanillaequity swaps, can be used to price general structures of quanto equity swaps.

Our valuation model is of considerable complexity, because it has to deal with atleast four risk factors: the foreign asset price, the exchange rate, the domestic risk-free interest rate, and the foreign risk-free rate. The domestic and foreign interestrate dynamics are modelled here using a discrete version of the Heath et al. (1990,1992, hereafter HJM) model. Thus, as in Jarrow and Turnbull (1996) and Kijimaand Muromachi (2001), our valuation formulae are arbitrage-free. We first establishthe domestic risk-neutral measure under which the relative price of any asset(including foreign assets) to the domestic money market account follows amartingale. The swap value is then determined by taking the expected present valueof future cash flows under this measure. When the volatility and covariancefunctions are permitted to be arbitrary, our valuation model is 'path-dependent'.However, in the special case where all of the volatilities are constant or at mostfunctions of time, we obtain a closed-form solution for a quanto equity swap price.

The rest of this paper is organized as follows. The following section covers thesetting of notation and assumptions, the basic structures of quanto equity swaps,and the risk-neutral valuation relationship. The third section derives the pricingformula for a foreign equity/domestic floating rate swap with the notional principaldenominated in the domestic currency. Numerical evaluations are presented in thefourth section and conclusions in the fmal section.

The Setting

Notation and Assumptions

The following notation is employed:''

I^{t) foreign stock or index price at time ( denominated in foreigncurrency;

S(t) spot exchange rate at time / (dollars per unit of foreign currency);T maturity date of the swap;?•,{/) short rate at time t for borrowing and lending at the period from

time / to t+h, V/=J (domestic interest rate) and/(foreign interestrate);

fit. T) forward rate at time / for borrowing and lending at the period fromtime 7" to T+h,\fi=d,f

Ptj(t, T) price in domesfic currency at time / of a domestic zero-coupon bondwith maturity T a.nd unit face value;

PJ{t, T) price in foreign currency at time / of a foreign zero-coupon bondwith maturity T and unit face value.

There are four state variables relevant to the valuation of quanto equity swaps: thedomestic interest rate, the foreign interest rate, the exchange rate, and the foreignstock price. We assume that the dynamics of the domestic and foreign forward ratesfollow the HJM model, and that the exchange rate and the foreign equity price arejoint lognormally distributed. In other words, we assume that the four factors under

124 S.-L. Chung d H.-F. Yang

the domestic risk neutral ( 0 measure follow;

T)-ff{t, T)=Oir{t, T,.

(1)

(2)

In

where a,<-) and ff/(-), yi = (l.f, s, 1J-, are respectively the drift and volatility of each

variable, and the vectors of increments, X ^(x^, X/, Xs, X}-j, are multivariate

standard normal variables with the covariance matrix

Cov{X,X') =

1

Pds

1

Pu

Pds

Pfs

1

Pdi

pfl

PI:

Pdi- PI

where p,y is the correlation coefficient between / andy.We iinally assume that the market is complete and Ihere is no default risk for both

parties of the swaps. Therefore, we can price quanto equity swaps from theirexpected present values of future cash flows.

Basic Structures of Quanto Equity Swaps

Depending on the payoff specifications, quanto equity swaps can be classified intothree basic structures (Beder, 1992; Chance and Rich, 1998).

1. Quanto equitytfixed rate swaps. A foreign (domestic) equity index return isexchanged for a fixed interest rate with the notional principal denominatedin the domestic (foreign) currency. For example, in a quanto foreign equity/fixed rate swap with the notional principal denominated in the domesticcurrency, the cashfiow at time //+] for the domestic fixed-rate payer is

where NPtj is the notional principal denominated in the domestic currency andRd is the fixed rate per annual.

2.

Pricing Quanto Equity Swaps in a Stoehastic Interest Rate Economy 125

Quanto equity Ijloat ing rate swaps. A foreign (domestic) equity index returnis exchanged for a domestic (foreign) floating interest rate with the notionalprincipal denominated in the domestic or foreign currency. For example, in aquanto foreign equity/domestic floating rate swap with the notionalprincipal denominated in the domestic currency, the cashflow at time //+ifor the domestic floating-rate payer is

where qi=t,-+\ - / , , R,/(qi) is the domestic ^//-period LIBOR rate at time /, and Q isthe constant margin rate to be specified when the swap is first initiated so that thenet value of the swap is zero.3. Quanto equitylequity swaps. A domestic equity index return is exchanged for

a foreign equity index return with the notional principal denominated in thedomestic or foreign currency. For instance, in a quanto foreign equity/domestic equity swap with the notional principal denominated in thedomestic currency, the cashllow at time /,+ i for the domestic equity returnpayer is

where c',/ is the constant margin rate to be specified when the swap is firstinitiated so that the net value of the swap is zero.

Using the building block approach, it is not difficult to show that the above threebasic structures of quanto equity swaps can be created from each other by combiningwith interest rate swaps, differential swaps, and/or plain vanilla equity swaps. Forexample, if the domestic fixed-rate payer in a quanto foreign equity/fixed rate swapenters into a domestic interest rate swap in which he pays the floating rate andreceives a fixed rate (suppose the swap rate is R'd), then the cashfiow from thisinterest rate swap at time ?,+i for him is

If the market is arbitrage free, then the total cashflows from both swaps at time /•,+]for the investor must equal the cashflow at time Vi for the domestic fioating-ratepayer in a quanto foreign equity/domestic floating rate swap with the notionalprincipal denominated in the domestic currency. Therefore, the following equality issustained when the market is arbitrage free:

In conclusion., using the no-arbitrage argument and the existing results in pricinginterest rate swaps, differential swaps, and/or plain vanilla equity swaps, the

126 S.-L. Chung & H.-F. Yang

valuation of the above three basic structures of quanto equity swaps can besimplified as just the valuation of any one of them. As an illustration, we will foctison pricing a quanto foreign equity/domestic floating rate swap with the notionalprincipal denominated in the domestic currency.

Risk-neutral Valuations

In this article we apply the risk-neutral valuation technique developed by Amin andBodurtha (1995) to identify a change of measure and work directly with the risk-neutral processes of the four state variables relevant to the pricing of a quanto equityswap, hi the absence of arbitrage, there exists a probability measure, called thedomestic risk-neutral measure (denoted as ^) . under which all asset prices(denominated in the domestic currency), normalized by the domestic money marketaccount, follow martingales. Since the original probability measure governing theevolution of state variables is irrelevant to the valuation, we derive our pricing modelonly under the Q measure.

In a domestic risk-neutral world, all asset prices should be denominated in thedomestic currency. Therefore, we multiply foreign currency values by the spotexchange rate. Sit), to convert foreign asset prices to the domestic currency. Forinstance, the foreign money market account denominated in the domestic currency,B/(t), equals BJ(/) x S{t). We can hence define the relative prices of all the assets tothe domestic money market account in the economy by

5,(0

^ T)

,T) _P}{t,T)xS{t)

IJ{t)xS{t)

where Z^t), Z^t, T), Z^t, T), and Z/.(,) are the relatives prices (denominated in thedomestic currency) at time t of the foreign money market account, the domestic zero-coupon bond (with maturity T). the foreign zero-coupon bond (with maturity 7),and the foreign stock, respectively. By applying the martingale condition to Z//),Zf^t, T), Z^t, T), and Zj-i,).. one can determine the values of the drifts a^.). a/.),

as(.), and a/-(.) in Lemma 1.

Lemma 1. The prices in domestic currency of all assets relative to the domesticmoney market account are Q — martingales if and only if the following conditions are

satisfied:

T— I

Pricing Quanto Equity Snaps in a Stochastic Interest Rate Economy 127

/ T \

E, exp

Eh

I T

exp

(5)

where ^, indicates the time / conditional expectation with respect to the Q measure.

Proof See the Appendix.

Pricing Quanto Foreign Equity/Domestic Floating Rate Swaps

As discussed in the previous section, we will focus on pricing a quanto foreign equity/domestic floating rate swap with the notional principal denominated in the domesticcurrency in this paper. To the party paying the domestic floating rate and receiving aforeign equity return, the cashflow at time /,+t (CF,,^,) is

Note that the domestic ^rperiod LIBOR rate at time ti, RJ^gt), is defined by

1^ - 1

To get the present value of the cash flow Cf,,^,, we need to discount it back totime / at the domestic interest rate. Let K,, , denote the expected present value of

128 S.-L. Chung iSc H.-F. Yang

then

>\i{ih)h (6)

The term structure model (HJM model) used in this article is generally pathdependent. Thus, one needs to apply numerical methods such as the Monte Carlosimulation method (Carr and Yang, 1998) or the lattice approach (Amin and Bodurtha.1995) to evaluate equation (6). However, if the volatilities of all slate variables areconstants or at most are functions of time,^ then there exists a closed-form solution forequation (6). To facilitate the derivation of closed-form solutions, it is assumed that^

Letting h-^0 and applying Lemma I and the property of lognormally-distributedvariables.^ we can evaluate (6) and obtain the following closed-form solution'*

(7)

where.

-NP,i

_ -t)

The terms b^, b2, /'3, ^4, ^5, and b(, are meant to adjust for the effects of thecorrelation between domestic and foreign interest rates, the volatility of the foreign

Pricing Quanto Equity Swaps in a Stochastic Interest Rate Economy 129

interest rate, the correlation between the foreign interest rate and exchange rate, thecorrelation between the foreign equity price and domestic interest rate, thecorrelation between the foreign equity price and foreign interest rate, andthe correlation between the foreign equity price and exchange rate.

To the party paying the domestic floating rate and receiving a foreign equityreturn, the value of the swap is simply the summation of the present values of allfuture cash flows, i.e.

where n is the number of payment dates after / (notice that tn= T). Since the constantmargin rate (cj) is specified to let the value of the swap be zero at the initialized date,the constant margin rate at the initialized date must be

r;

So far we have derived the complete pricing formula for a quanto foreign equity/domestic floating rate swap with the notional principal denominated in the domesticcurrency. There are several points worth noting. First, at the start date orimmediately after the payment is made, the value of a quanto equity swap willmainly depend on the term structures of interest rates in both countries at each resetdate. Hence, the level of the foreign equity price is irrelevant to the valuation of aquanto equity swap."* However, the subsequent value of the swap does depend onthe level of the foreign equity price. The pricing formula of a quanto equity swap atthe subsequent date is shown in the Appendix.

Chance and Rich (1998) also find that the foreign equity price level is irrelevant forpricing other equity swaps. However, unlike them, the quanto equity swap valuedoes depend on the volatility of the equity price process, as well as its correlationswith the exchange rate and interest rates in both countries (i.e. h^ to b(, inequation (7)). Kijima and Muromachi (2001) have similar findings to ours in the caseof a plain vanilla equity swap with a variable notional principal in a stochasticinterest rate economy.

Second, when the volatility of the foreign equity price is zero (i.e. GI- =0). theforeign equity price will be equivalent to the foreign money market account. As aresult, with h^=b^=h(,=O. our pricing formula is very similar to that for a differentialswap'' (Wei. 1994; Chang et al., 2002). Moreover, if the foreign country is identicalto the domestic country (i.e. 5 = 1 , ff.v^O, kj=kf, <Sd=Of, pdf^\), then the quantoequity swap reduces to be a single-currency equity swap and the constant margin ratewill be zero in our pricing formula since b[=b2. ^4=^5. *ind bi=h(,=O. The result isconsistent with the fmding of Chance and Rich (1998) whereby the paying-float ing.

130 S.-L. Chung & H.-F. Yang

receive-equity swap is an equivalent exchange (i.e. the constant margin rate is zero).The above arguments also provide a simple way to check our complex formula.

Third, although the exchange rate itself does not appear in our pricing formula,the exchange rate volatility, the correlation with the foreign interest rate, and thecorrelation with the foreign equity price do have effects on the value of a quantoequity swap. Analogous to the discussion of Wei (1994) in the case of a differentialswap, the correlation terms here express the Tixed exchange rate effect'. That is,these terms capture the potential loss or gain due to future changes of the exchangerate. When the correlations relative to the exchange rate are zero, the swap value iscompletely independent of the exchange rate.

Fourth, it should be pointed out that the quanto equity swap described above isactually a 'quanto domestic equity/foreign floating rate swap with the notionalprincipal denominated in the foreign currency' from the viewpoint of a 'foreign'investor. Therefore, there exists a similar pricing duality to that of Chang ct al.(2002), and our pricing formula can be easily converted to the pricing formula of aquanto domestic equity/foreign floating rate swap with the notional principaldenominated in the foreign currency.'*

Finally, the valuation of a general quanto equity swap does not impose any extradifficulty. For instance, with a quanto equity swap whose periodic payments arebased on the returns of the FTSE 100 and Nikkei 225, but are denominated in USdollars, we simply have to value each leg as a foreign equity-driven floater. In thiscase, the value of a general quanto equity swap will depend on some extraparameters.

Numerical Evaluations

Our pricing formulae are applied to price a range of quanto foreign equity/domesticfloating rate swaps so as to investigate how much the swap values change whenparameters change. All analyses in this section are based on the viewpoint of aninvestor who pays domestic floating rates and receives foreign equity returns.The sensitivity analyses are divided into three parts: term structure effect, volatilityeffect, and correlation etTect. The benchmark parameters, mainly adoptedfrom Wei (1994), are as follows: (7,/=Uf=0.02, a,=0.3, ff/-=0.3, p,/y-0.3,P/i = P/7; - - 0 . 3 , pjr =p,,. = - 0 . 2 , k,/^kj=Q.\5, and NPa=$\OO.

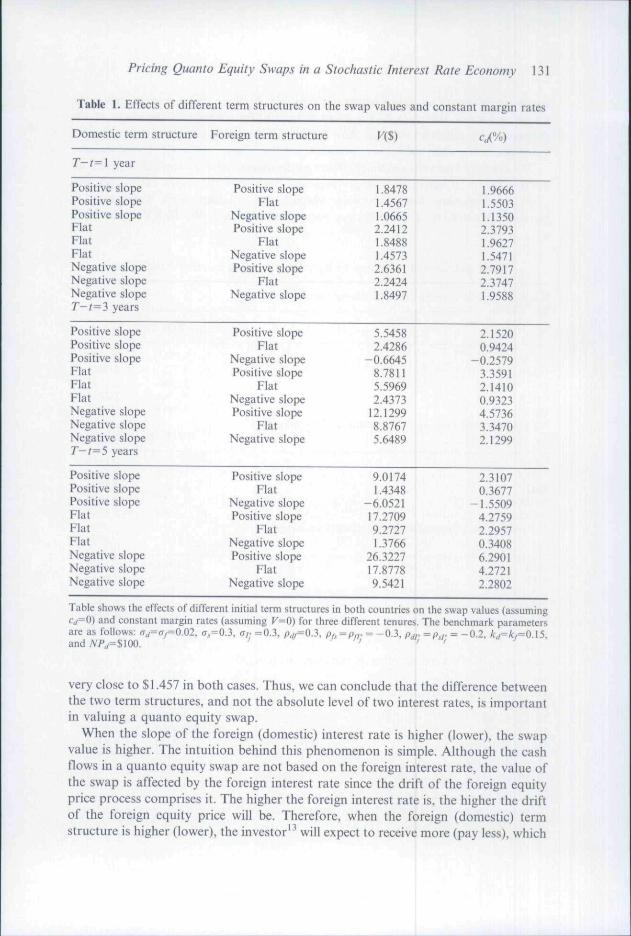

We first examine the effects of different initial term structures in both countries onthe swap values (assuming c,/=0) and constant margin rates (assuming K=0)) forthree different tenures. The term structures of both countries are classified as threekinds: positive slope, negative slope, and flat. 'Flat' means the yield is fixed at 8% forall maturities of zero-coupon bonds. 'Positive slope' ('Negative slope") represents anupward (downward) yield curve with a slope of 0.4%/year (-0.4°/i/year) starting withan instantaneous rate of 8.0%.

From Table 1, one can verify that when the differences between the two termstructures are the same, the swap values (and thus the constant margin rates) are veryclose. In the case that the tenure equals one year, the swap values are all close to$1,849 (assuming c,i=O) when both term structures have the same slope. While thedomestic term structure is 0.4%/year steeper than the foreign term structure (i.e.domestic positive foreign flat, or domestic flat foreign negative), the swap values are

Pricing Quanto Equity Swaps in a Stochastic Interest Rate Economy 131

Table 1, Efiects of different term structures on the swap values and constant margin rates

Domestic term structure

T~t=\ year

Positive slopePositive slopePositive slopeFlatFlatFlatNegative slopeNegative slopeNegative slopeT-f^3 years

Positive slopePositive slopePositive slopeFiatFlatFlatNegative slopeNegative slopeNegative slopeT-i^5 years

Positive slopePositive slopePositive slopeFlatFiatFlatNegative slopeNegative slopeNegative slope

Foreign term structure

Positive slopeFlat

Negative slopePositive slope

FlatNegative slopePositive slope

FlatNegative slope

Positive slopeFlat

Negative slopePositive slope

FlatNegative slopePositive slope

FlatNegative slope

Positive slopeFlat

Negative slopePositive slope

FlatNegative slopePositive slope

FlatNegative slope

V{S)

1.84781.45671.06652.24121.84881.45732.63612.24241.8497

5.54582.4286

-0.66458.78115.59692.4373

12.12998.87675.6489

9.01741.4348

-6.052117.27099.27271.3766

26.322717.87789.5421

1.96661.55031.13502.37931.96271.54712.79172.37471.9588

2.15200.9424

-0.25793.35912,14100.93234.57363.34702.1299

2.31070.3677

-1.55094.27592.29570.34086.29014.27212.2802

Table shows the effects of differeni initial term structures in both countries on the swap values (assumingQ=0) and constant margin rates (assuming K=0) for three dilTerent tenures. The benchmark parametersare as follows: aj=a^=0.02, a,=03, a,- =0.3, Prfy=0.3, Pf, = pn. = -0 .3 . p^,. =p,,. = -0.2. kj=k,=(i.\5,and NP,,= %\m ' •' J , J ',

very close to $1.457 in both cases. Thus, we can conclude that the difference betweenthe two term structures, and not the absolute level of two interest rates, is importantin valuing a quanto equity swap.

When the slope of the foreign (domestic) interest rate is higher (lower), the swapvalue is higher. The intuition behind this phenomenon is simple. Although the cashflows in a quanto equity swap are not based on the foreign interest rate, the value ofthe swap is affected by the foreign interest rate since the drift of the foreign equityprice process comprises it. The higher the foreign interest rate is, the higher the driftof the foreign equity price will be. Therefore, when the foreign (domestic) termstructure is higher (lower), the investor'^ will expecl to receive more (pay less), which

132 S.-L. Chung &H.'F. Yang

makes the value of a quanto equity swap higher. Tn these circumstances, when thetenure is longer, the priee of the swap is higher. By contrast, if the slope of thedomestic term structure is larger than the foreign one, then the quanto equity swapvalue decreases when the tenure increases.

We secondly study the volatility effects on the quanto equity swap values. Here weassume the swap maturity is three years and both term structures have a positiveslope. We calculate swap values by varying one volatility while keeping otherparameters constant. The results are presented in Table 2. We find that the swap

Table 2. Effects of volatilities on the swap values and constant margin rates

Varying Of while keeping other parameters unchanged

0.0100.0150.020.0250.030Varying GJ while keeping other parameters unchanged

0.0100.0150.020.0250.030Varying o-, while keeping other parameters unchanged

0.100.150.20.250.30.350.40Varying ar while keeping other parameters unchanged

O.iO0.150.20.250.30.350.40

n%)5.21685.37265.54585.73645.9445

Vi%)

5.52675.53625.54585.55535.5648

K(«

1.88012.79423.70994.62705.54586.46617.3879

m)2.31153.11833.92624.73545.54586.35747.1701

cm2.02432.08482.15202.22592.3067

a%)2.14462.14832.15202.15572.1594

cm0.72961.08431.43951.79542.15202.50912.8668

a%)0.89691.21001.52351.83752.15202.46692.7823

Table shows the volatility effects on the swap values {assuming 0 = 0 ) and constant margin rales (assumingV=Q). The benchmark parameters are as follows: (T^=(T, = 0 . 0 2 , rT, = 0.3, CT/-=0.3, /3^/=0.3,py,^^pjj. = - 0 . 3 . /),„, =p,,. = - 0 . 2 . A-,/=A-,=0.15. r - ( = 3 years, and NP,i=$\QO.

Pricing Quanto Equity Swaps in a Stochastic Interest Rate Economy 133

value is more sensitive to the volatility of the foreign interest rate than to thevolatility of the domestic interest rate. This may be explained from our pricingformula, whereby a/ appears in 6,, A2, h^. and b=,. but (TJ only appears in /J, and /14.Since the interest rate volatility is generally far less than the exchange rate volatilityand the foreign stock price volatility, the swap value and the constant margin rateare more sensitive to the latter. Moreover, the swap value increases when thevolatilities of the four state variables increase.

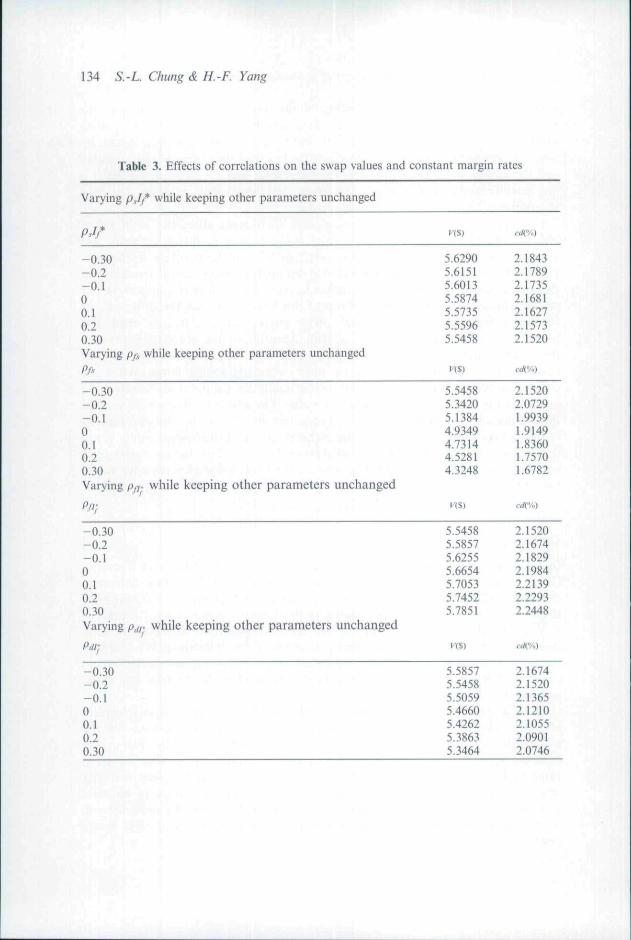

We finally investigate how the correlation coefficients affect the swap valuesand the constant margin rates. The swap maturity here is also three years. Wevary one correlation coefficient from -0.3 to 0.3 and keep others unchanged.All correlation coefficients are considered in our analyses except correlation betweenthe domestic interest rate and the exchange rate since it does not appear in ourpricing formula, i.e. equation (7). From Table 3, we find that the effect of thecorrelation between the domestic and foreign interest rate is extremely small. Theprice of a quanto equity swap is actually sensitive to the correlation betweenthe foreign interest rate and the exchange rate and the correlation between theexchange rate and the foreign equity price, especially to the latter. When thecorrelation between exchange rate and foreign equity price is positive, the value of aquanto equity swap is negative and vice versa. The above results can be veriiledby examining our pricing formula. From equation (7), it is obvious that b(,(reflecting the correlation between the exchange rate and the foreign equity price)dominates h\ to b^. because the exchange rate volatility and the foreign equity pricevolatility are generally far larger than both the domestic and the foreign interest ratevolatilities.

Conclusion

In this paper we extend the arbitrage-free pricing model of Amin and Bodurtha(1995) to derive pricing formulae for quanto equity swaps. We first determinethe drift of all asset prices in a domestic risk-neutral world such that the relative pricein domestic currency of any asset relative to the domestic money market account isa Q martingale. The pricing formulae are then obtained by discounting the cashHows of quanto equity swaps to current time under the Q measure. We find thatthe value of a quanto equity swap at the start date does not depend on the foreignstock price level, but rather on the term structures of both countries and otherparameters.

The numerical results indicate that the difference between initial term structuresof both countries will affect the swap value significantly. To the party payinga domestic interest rate and receiving a foreign equity return, the higher thedomestic term structure is (compared to the foreign one), the smaller the swapvalue is. In this circumstance the swap value will decrease as the swap maturityincreases. We also find that the swap value rises as the volatilities of all statevariables increase. Moreover, among all correlation coefficients, the swap value isthe most sensitive to the correlation between the exchange rate and the foreign equityprice.

134 S.-L Chung & H.-F. Yang

Table 3. Effects of correlations on the swap values and constant margin rates

Varying pj,* while keeping other parameters unchanged

-0.30-0.2-0.100.10.2 '0.30Varying p/,, while keeping other parameters unchangedP/s

5.62905.61515.60135.58745.57355.55965.5458

(-•(S)

5.54585.34205.13844.93494.73144.52814.3248

2.18432.17892.17352.16812.16272.15732.1520

....

2.15202.07291.99391.91491.83601.75701.6782

-0.30-0.2-0.100.10.20.30Varying

Pfi;

j . while keeping other parameters unchangedKS)

-0.30-0.2-0.100.10.20.30Varying while keeping other parameters unchanged

5.54585.58575.62555.66545.70535.74525.7851

2.15202.16742.18292.19842.21392.22932.2448

<•(«%)

-0.30-0.2-0.100.10.20.30

5.58575.54585.50595.46605.42625.38635.3464

2.16742.15202.13652.12102.10552.09012.0746

8.00425.54583.09840.6620

-1.7634-4.1779-6.5816

3.10592.15201.20230.2569

-0.6843-1.6212-2.5539

Pricing Quanto Equity Swaps in a Stochastic Interest Rate Economy !35

Table 3. (Continued.)

Varying pjf while keeping other parameters unchanged

-0 .30-0 .2-O.t0O.I0.20.30

Table shows the correlation effects on the swap values (assuming (•,/=0) and constant margin rates(assuming V=Q). The benchmark parameters are as follows: o, /=o^0.02. ^,=0.3, a;- =0.3, p , / / = 0 . 3 ,

f'fs = PjT = -0-3, Pdr^P,r = -0.2, k^-^kj^0.\5, T-t=3 years, and NP^=%\00.

In future research we can apply our valuation model to price financial derivatives,such as quanto options and quanto equity swaptions, whose payoffs depend on aforeign equity price and/or foreign risk-free rate. Moreover, our discrete time modelcan be implemented with lattice approaches to price American-style options.

Acknowled gements

The paper has benefited from discussions with Chuang-Chang Chang. MarkShacklcton. Min-Tch Yu. participants at the 15 ^ Australia Finance and BankingConference, and seminar participants at Yuan-ze University. Financial support fromthe National Science Council of Taiwan is also acknowledged.

Notes

' In this article, the 'domestic' setting is where the investor lives and receives his/her payoff. For example,to a US investor. US dollar and S&P 500 are his/her domestic currency and equity index, respectively.' In other words, the exchange rate between the US dollar and Japanese Yen during the whole life of theswap is set initially to be one.• Chance and Rich (1998) price cross-currency equity swaps in which a party pays a domestic equity returnand receives a return on a foreign index. The valuation problem considered in their paper is relativelysimple, because the foreign index returns are converted into the domestic currency using a floatingexchange rate. By contrast, we consider a fixed exchange rate (quanto) effect on the equity swap pricing inthis paper.

It should be noted that a superscript * indicates that the variable is denominated in the foreign currency.* The values of the drifts a,y((, 7",.), a^/, T,.), a/^l,.), and a/- (f,.) under the Q measure are shown in Lemma

• This assumption implies that both the domestic and foreign interest rates are normally distributed.Kijima and Muromachi (2001) make the same assumption so as to derive closed-form solutions for othertypes of equity swaps.

136 S-L Chung & K-F. Yang

' Under this assumption, the HJM model corresponds to the spot rate (extended-Vasicek) model ofHull and White (1990) with mean-reversion coefficients Av (domestic) and k, (foreign).

^ The properties of lognormally distributed variables used here are that the followings hold fornormally distributed variables .v and v:

' Please sec the Appendix for the key steps of the derivations.'° As pointed oiil by the referee, [his is a simple consequence of the fact that the payment of the equity legis defined as a 'return' over two consecutive payment dales. If it is defined in the other ways. e.g. a 'return'from the beginning date to the payment date, the results will be different.' ' The difference is due to the fact that the payment al time r, on the foreign leg is predetermined al timeti-i for a differential swap, while it is determined al time /, for an equity swap.'^ As pointed out by the referee, the pricing duality is useful only under one foreign equity case. For swapsor options written on baskets of foreign assets in many countries, the duality property becomes irrelevant.' ' Remenber thai our analyses are based on the viewpoinl of an investor who pays domestic floating ratesand receives foreign equity returns.''' It should be noted that cash flows other than the first one after time t can still be priced by equation (7)since ihe equity leg is defined as a 'return' over two conseeutive payment dates.

References

Amin, K. 1. and Bodurtha. J. N. (1995) Diserele-time valuation of American options with stochasticinterest rales. Review of Financial Stiitlie.s, 8, pp. 19.1-232.

Beder. T. S. (1992) Equity derivatives for investors. Journiil of Financial Engineering. 1(2). pp. 174-195.Carr. P. and Yang. G. (1998) Simulating American bond options in an HJM framework. Morgan Slanley

Working Paper.Chance. D. M. and Rich. D. (1998) The pricing of equity swaps and swaption. Journal of Derivatives; 5,

pp. 19-31.Chang. C. C , Chung. S. L. and Yu. M. T. (2002) Valuation and hedging of differential swaps. Journal of

Futures Market. 22(1). pp. 73-94.Chung, S. L. (2002) Pricing American options on foreign assets in a stochastic interesl rate economy.

Journal of Financial anil Quantitative .^nalv.sis. 37. pp. 667-692.Heath, D.. Jarrow. R. A. and Morton. A. (1990) Bond pricing and the term structure of interest rates: a

discrete time approximation, Journal of Financial ami Quantitative Analysis, 25, pp. 419-440.Heath, D.. Jarrow. R. A. and Morton, A. (1992) Bond pricing and the term structure of interest rates: a

new methodology for contingent claim valualion. Econonietrica. 60. pp. 77-105.Hull, J. and White. A. (1990) Pricing interest rate derivative securities. The Review of Financial Studies.. 3,

pp. 573-592.Jamshidian, F. (1993) Price differentials. Risk. 6, pp. 48-51.Jarrow, R. and Turnbull, S. (1996) Derivative Securities (Cincinnati: South-Western Publishing).Kijima, M. and Muromachi, Y. (2001) Pricing equity swaps in a stochastic interest rate economy. Journal

of Derivatives. 8, pp. 19-35.Litzenberger, R. H. (1992) Swaps: plain and fanciful. Journal of Finance. 47, pp. 831-850.

Pricing Quanto Fquity Swaps in a Stochastic Interest Rate Economy 137

Marshall. J. E.. Sorensen, E. and Tucker, A. (1992) Equity derivatives: the plain vanilla equity swap andits variants. Journal of Financial Engineering. 1, pp. 219-241.

Reiner. E. (1992) Quanto mechanics. Risk. 5. pp. 59-63.Rich, D. (1995) A note on the valuation and hedging of equity swaps. Journal of Financial Engineering, 4.

pp. 323-334.Wei, J. Z. (1994) Valuing differential swaps. Journal of Derivative.":. I. pp. 64-76.Wei, J. Z. (1995) Pricing options on foreign assets when interest rates are stochastic. Advances in

International Banking and Finance. 1, pp. 67-89.

Appendix

Proof of Lemma 1

Lemma 1 can be obtained by applying the martingale condition to Z/t). ZJt, T).Zf{t, T), and Zr{t). respectively. That is.

, T)

T)(10)

Since Amin and Bodurtha (1995) provide formulae for a,/dsit..) in their Lemma I, we will derive the formula for a/-(/,.definition of Z/'(.) and equation{10), we obtain

ih,.), oi.j{i, ih,.), andonly. Given the

E,i;{t)*s{t) (11)

In our discrete time model, the price in the domestic currency at time t of adomestic zero-coupon bond with maturity T is given by

(12)

138 S-L Chung & H.-F. Yang

The domestic money market account, BJ^t), is defined by

= cxp r,i{ih)h = exp ih, ih)h (13)

The foreign zero-coupon bond price, P^^t, T). and foreign money market account,B*f-{t), are defined in the same way as the domestic case.

Substituting equations(3), (4) and (13) into equation(11) yields

Hence, we obtain

(14)

Substituting the formula of !Xs(t,.)h into the above equation yields the desiredresult.

Deriving the Pricing Formula of a Quanto Equity Swap at the Start Date

From the definition of 9,-period LIBOR rate, the cash flow C/",,^, can be rewritten as

- - I

exp — V

'^h

The expected present values of the second and third parts of Cf,,^, are shown inChang et al. (2002). Thus we will focus on the valuation of the first part of CF,_^^.

Pricing Quanto Equity Swaps in a Stochastic Interest Rate Economy 139

Applying the lognormal property E[e'''^^']=Ele"^] Ele^e^""^"'^^ to Lemma 1, we canrewrite the drift rate of /^(/,) under the Q measure as

From the dynamic process of If(ti) and the above equation, we canexpress the expected present value of the first part of CF,.^^ as (ignoring NP^ forbrevity):

exp

exp exp r,{ih)h

(15)

— I

i:{ih..)Xn

By definition, the expectation of the first term is the domestic discount bond price^ n i.e.

exp

T

(16)

140 S.-L Chung &H.'F. Yang

The expectation of the second term can be rearranged as

E, exp

— I

l\

rf{ih)h

E,

E,

exp cov

i+\— I

fi+l

(17)

/J

where the second equality is derived by applying lognormal properties. Sincerf(ih)=ff{ih, ih), we obtain the foreign spot rate dynamics as follows:

rf{ih)h=ff{ih,ih)h

ih)h] +ff{t. ih)h(18)

ff{t, ih)h

The drift rate of the foreign forward interest rate can be rewritten as

k=J+l

Pricing Quanto Equity Swaps in a Stochastic Interest Rate Economy 14!

Substituting Lemma I into the above equation and using the lognormal propertiesyields

=j + \

Substituting (19) into (18), we obtain the dynamic process of the foreign spotinterest rate as

f - 1

/ - I

E1 - 1

i - i

J=t

Hence, we obtain

r,{jh)X,ijh +

(t. ih)h

(20)

E, exp = exp

exp.-I

h~ /-I

(21)

142 S.-L Chung iSi H.-F. Yang

Applying the lognormal properties and substituting equations (16), (17), and (21)into equation (15) yields

where

,fi

' l+l- 1

^ cov

— 1

— \

ti+\- 1

1

= cov

— COV

— 1

• - 1

b(,=7

As an illustration, we derive the formula of/)| when aj^t, T,.)=t, T,.)=Ufe\p[-kf{T-t)], and /i->0. Because rj,ih)^f,i(ih, ih), we obtain the follow

Pricing Quanta Equity Swaps in a Stochastic Interest Rate Economy 143

equation:

/ - I (-1

+fd{t, ih)h(22)

The drift rate of domestic forward interest rate can be rewritten as

/ - 1

k=j-i-\jh, kh,.)h'

Substituting Lemma 1 into the above equation and using the properties oflognormally distributed variables yields

Substituting equation (23) into equation (22) yields

(23)

k=J+l (24)

fi{t, ih)h

144 S.-L. Chung & H.-F. Yang

Therefore we have

h,

b\ =cov rd{ih)K

= hcovh i-

t t

When

Let A = j^.^^^ ^^^^^aj{kj{T-t)] into A yields

[

u)d.s. where TI^TT. Substituting cr//,

exp[-kjis-u)]dWf{u)ds

= a

= -

*f A ^ 1 1

kf J.v=

exp{-kjs)\

expikfUJ •- •'

Using the formula of integration by parts.

kf-rJs=

[exp(-

exp(

[exp(-

^{-kfi

-kfs) exp(

r1 T \ 1

i) exp(/c/i^

U W f I u Ju e x p 1 KfS I

we obtain

^V7v)df ', («) [ . , ,

1J

)dH^/-(«)- [ dWjis)Js—ii

(25)

Pricing Quanto Equity Swaps in a Stochastic Interest Rate Economy 145

and

(26)

Note that if we let B= J , ^ J ' ^ O'(/(H, s)dWti{u)ds, then B also follows formulaesimilar to equations (25) and (26). Therefore we can rewrite b\ as

fT/(«, s)dWf{u)ds

-A://,.) rill—I

'"'

where the second equality follows the definition of covariance and equations (25)and (26).

Pricing Formula of a Quanto Equity Swap at the Subsequent Date

The valuation formula in the earlier section (i.e. equation (7)) is applicable whencurrent time t is at the starting date or immediately after the payment date of theswap. However., when current time / is between two payment dates, the first paymentafter time t cannot be evaluated by equation (7) since we have known the domesticand foreign interest rates and some information of stock level from the previouspayment date to time /.'' Let /Q denote the previous payment date and i denote thenext payment date. Current time / is between /(j and ^i. The cash How received at /[becomes

CF,=NP,x

146 S-L Chung & H.-F Yang

Similar to the previous proof, one can obtain a simplified closed-form solution forthe expected present value of Cf,, at time t as

where

Obviously, equations (22) and (7) are equivalent when both t and /, equal IQ. Fromequation (22), we find that between two payment dates, the value of quanto equityswaps does depend on the stock level at time / because the value of the first payoffinvolves the stock price.