Embed Size (px)

Citation preview

Assemblée Générale -

Algemene Vergadering

IA|BE

13/09/2018

IA|BE – General Assembly – 2 – 13/09/2018

Assemblée Générale -Algemene Vergadering

Jean-François Hannosset

IA|BE – General Assembly – 3 – 13/09/2018

Sponsors IA|BE 2018

IA|BE – General Assembly – 4 – 13/09/2018

Assemblée Générale -Algemene Vergadering

Programme - Programma

Verwelkoming – Mot de bienvenue

Nieuwe leden – Nouveaux membres

Jean-François Hannosset

Approbation révision du système CPD

Goedkeuring herziening CPD systeem

Audrey Meganck / Guy Roelandt

Exposé – Uiteenzetting:

Solvency II, two years on

Olav Jones

Night of the Actuaries 2018 Fabian de Bilderling

Conclusions – Cocktail Jean-François Hannosset

IA|BE – General Assembly – 5 – 13/09/2018

Nieuwe leden - Nouveaux membres

• Paola AGRESTA (ULB)

• Mohamed AMGHAR (ULB)

• Alexia BREULS (UCL)

• Xenia LEFEBVRE (UCL)

• Olivier SOUPART (UCL)

IA|BE – General Assembly – 6 – 13/09/2018

“Approbation révision du système CPD –Goedkeuring herziening CPD systeem”

Audrey Meganck

Jean-François Hannosset

IA|BE – General Assembly – 7 – 13/09/2018

CPD

LessonsLearned

New Syllabus

Changing World

Quality IncreaseInteraction

WHY?

IA|BE – General Assembly – 8 – 13/09/2018

HOW?

AG 13 juin High Level

presentation

Next weekdetailled ROI will be sent

out

Organisation of twoconsultation sessions

26/6 & 4/9

Final ROI has been sent out

6/9

GA 13/9 final vote new ROI

(part CPD)

ROI: limited to the CPD part

Questions: [email protected]

IA|BE – General Assembly – 9 – 13/09/2018

CPD (vanaf 1/1/2019)

Deelname aan Actuarieel Technische opleidingen

(1): IA|BE / Actuariële departementen van universiteiten (Binnenlandse & Buitenlandse) / Actuariële Alumniverenigingen

Erkende actuariële associaties / AAE, IAA, EAA, AFIR, ASTIN, EAJ, IME… Anderen, mits akkoord ComAc

1 CPD / uur –2 CPD / uur als geslaagd voor examen

Min. 20 op 60 CPD punten

(2): Werkgevers / commerciële instellingen 1 CPD / uur Max. 30 op 60 CPD punten

Geven van Actuarieel Technische opleidingen

Zie (1) bij Deelname Actuarieel Technische opleidingen 2 CPD/uur

Zie (2) bij Deelname Actuarieel Technische opleidingen 1 CPD/uur

(3) E-learning Ad hoc toekenning

IA|BE – General Assembly – 10 – 13/09/2018

CPD (vanaf 1/1/2019)

Volgen van NIET-Technische opleidingen – Max. 10 op heel de categorie

Informaticatools, management skills, kennis van de markt, kennis van relevante wetgeving, …

IA|BE 1 CPD / uur

Others 0.25 CPD / uur

Volgen van opleidingen m.b.t. professionele vaardigheden – Max 10 op heel de categorie

Kennis van ethische, deontologische en professionele normen, …

IA|BE 1 CPD / uur

Others 0.25 CPD / uur

Afleggen van een test met betrekking tot bovenstaande kennis

1 CPD / uur

IA|BE – General Assembly – 11 – 13/09/2018

CPD (vanaf 1/1/2019)

Comité’s en werkgroepen – Max 20 op heel categorie

Technische WG (IA|BE,AAE en IAA) 1 CPD/uur –

Andere technische WG (Assuralia, PensioPlus) 0,5 CPD

Comité’s IA|BE, AAE en IAA

Voorzitter van bovenstaande WG + comité’s

0,5 CPD/uur

# CPD punten x 2

Vorming Actuariële studenten – Max 20 op heel categorie

Begeleiding Bedrijfsstage student actuariaatBegeleiding Meesterproef /Dissertatie binnen onderneming (student actuariaat)Begeleiding Meesterproef/Dissertatie binnen onderneming over actuarieel relevant onderwerp (andere studenten)

5 CPD10 CPD

5 CPD

Lezer masterproeven/ dissertatie IA|BE Prijs / Erkende universitaire instellingen

Lid jury IA|BE prijs / Erkende universitaire instellingen

2 CPD

3 CPD

Andere - Max 20

Publicatie wetenschappelijk artikel Ad hoc - Max 10 CPD / artikel

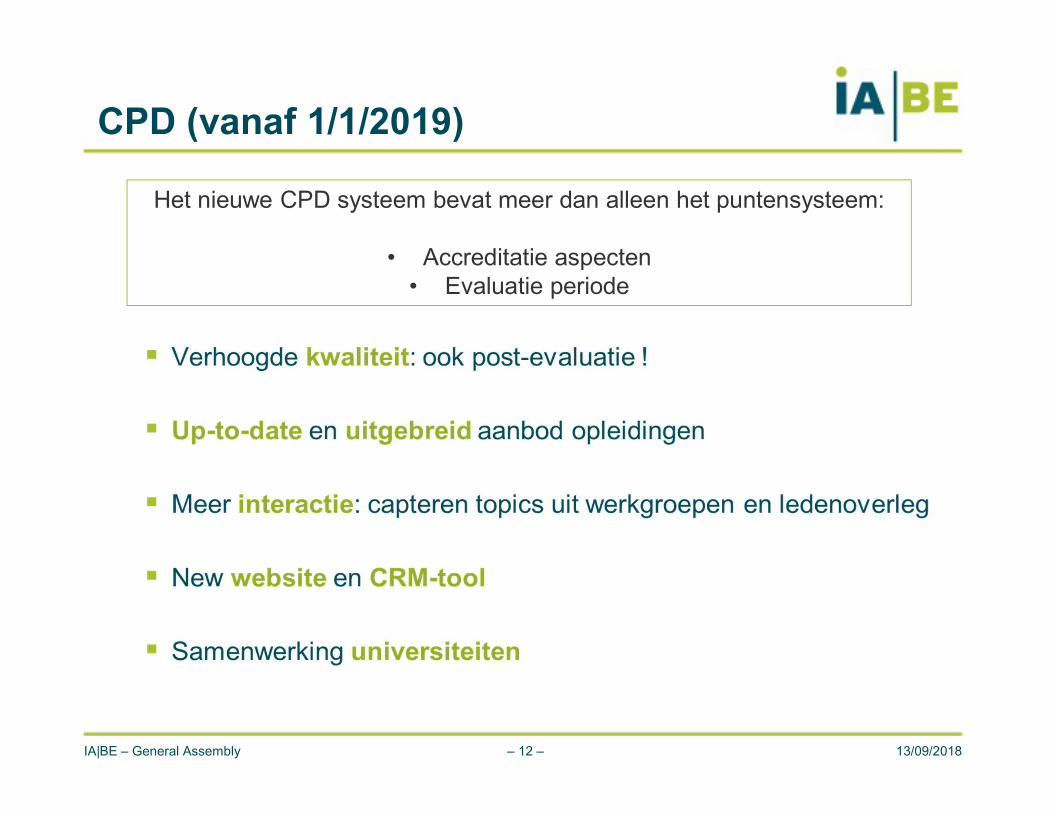

IA|BE – General Assembly – 12 – 13/09/2018

CPD (vanaf 1/1/2019)

Het nieuwe CPD systeem bevat meer dan alleen het puntensysteem:

• Accreditatie aspecten• Evaluatie periode

IA|BE – General Assembly – 13 – 13/09/2018

Olav Jones

“Solvency II, two years on”

14

General Assembly of the IA|BE

Solvency II, two years on

Presentation

Olav Jones

Deputy director general

Insurance Europe

Agenda

16

Successful launch

Impact survey

Concerns about excessive capital

Case studies

Solvency II reviews

1

2

3

4

5

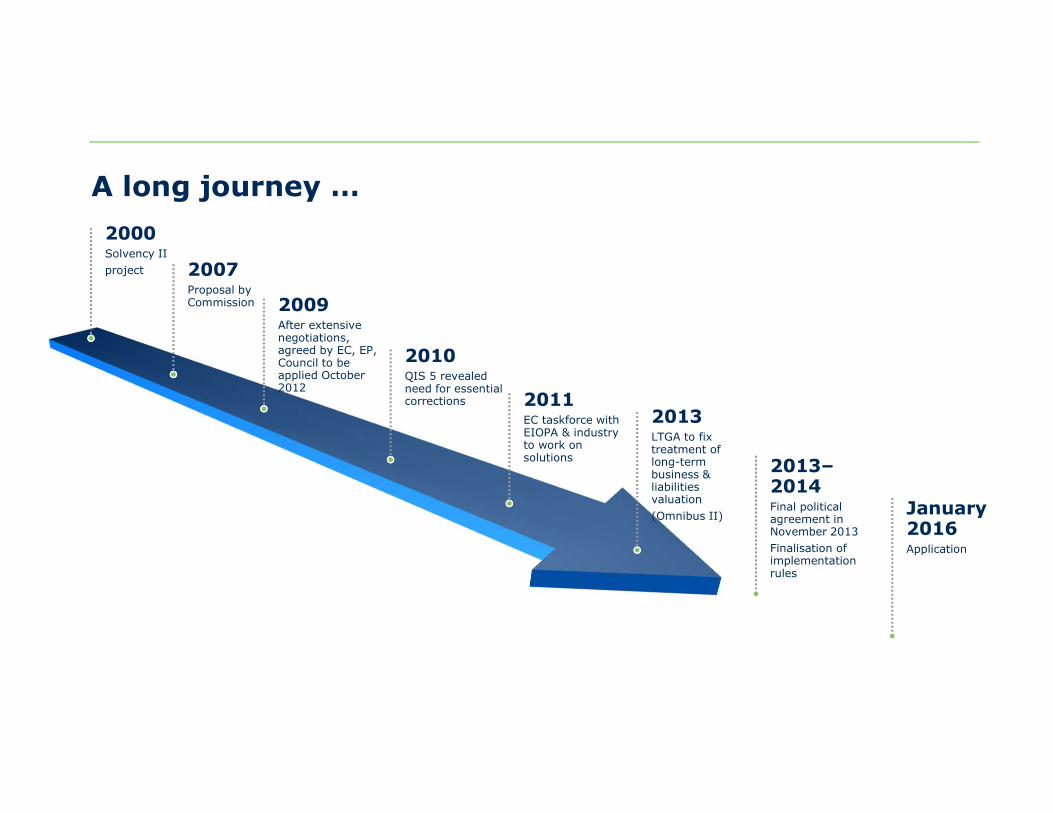

A long journey …

2000Solvency II project 2007

Proposal by Commission 2009

After extensive negotiations, agreed by EC, EP, Council to be applied October 2012

2010QIS 5 revealed need for essential corrections 2011

EC taskforce with EIOPA & industry to work on solutions

2013LTGA to fix treatment of long-term business & liabilities valuation(Omnibus II)

2013–2014Final political agreement in November 2013Finalisation of implementation rules

January 2016Application

A long journey … and it is not over yet

18

Application of Solvency II

(January 2016) Infrastructure

(April 2016)

STS securitisations

(June 2016)2018 review (Level 2)

(December 2018)EC fitness check on supervisory reporting

(December 2019) 2020 review (Levels 1+2)

(December 2020)

Huge implementation challenge

19

Revolution not evolution

3000 companies with €10trn of assets

Sophisticated modelling required even for standard formula users

3500+ pages of requirements

184 reporting templates

Successful implementation was not by chance

Industry already:

very strongly capitalised

with risk management as core focus

with widespread development of ERM & economic capital concepts

Significant preparation over many years:

helped by many QISs

very significant efforts by industry, national supervisors & EIOPA

huge investment

20

World-class frameworkThree pillars

Group & solo measures

Economic valuation of assets & liabilities

Best estimates of liabilities

All risks (28 in standard formula)

Most risks use scenario (stress test) approach

Internal models allowed

Two levels of capital (SCR & MCR) allowing early supervisory intervention

Strong & clear target level of protection: 99.5%

Significant testing & transitional measures

21

Some improvements still needed

Specific technical issues/calibrations

Proportionality

Treatment of long-term business

Agenda

23

Successful launch

Impact survey

Concerns about excessive capital

Case studies

Solvency II reviews

1

2

3

4

5

Positive impacts

24

% of respondents reporting improvements due to Solvency II

0% 20% 40% 60% 80% 100%

Any other benefits

Internal models

Harmonisation

ALM

Data quality

Risk management/governance

Unintended consequences

25

58%

“SII contributed to negative impact on guarantee business”

48%

“We invested less than optimally in real economy due to SII capital requirements”

Unintended consequences

26

“Increased SII requirements would make investment strategies for clients too conservative if they have guarantees”

“SII has led to a stronger focus on capital light products”

“The current offer of guaranteed capital products will not be sustainable … strategic plan envisages the gradual decline in the supply of guaranteed products with the growth of unit-linked products”

“We have prioritised the sales of unit-linked business with low capital requirements compared to other guaranteed products”

Agenda

27

Successful launch

Impact survey

Concerns about excessive capital

Case studies

Solvency II reviews

1

2

3

4

5

Insurers’ business model allows insurers to avoid forced sales of assets

Predictable liability portfolios, policyholders have limited ability and/or dis-incentives to surrender earlySignificant inflow of cash from premiums, dividends, rents, coupons, maturing bonds, etc creates significant liquidity

This gives insurers great deal of flexibility over IF they sell, WHEN they sell, WHICHassets they sell

Therefore insurers can reduce or even eliminate exposure to price volatility and short to medium term declines asset values

Exposure to forced-sales can and does exist but it is limited – it must be covered by the framework but it also must not be exaggerated

28

It’s all about forced-selling

Treatment of long-term business…

It is NOT about defining certain assets as long-term (e.g. asset must be of duration > 3 or 5 or 10 years, or asset must not be traded) and calibrating only these in a different way

It is about how the nature of the liabilities can allow the insurer to avoid forced-selling of the assets

Insurers can hold individual assets to maturity or long-term – but that does not mean they do or should always do in practice

There are good reasons for not doing so (changes in liability, concerns about individual performance/risks relating to individual assets or sectors, better opportunities for returns/diversification from other assets sectors)

In fact the insurer has a duty to customers/shareholders to obtain the best returns from their investments

The flexibility to choose whether to sell, what to sell and when to sell is a key benefit of the insurance business model

29

It’s all about forced-selling

Treatment of long-term business…

Three causes

30

Regulatory Technical provisions

(Amount needed to cover payment of claims and other

liabilities)

1. Liabilities exaggerated

Illustrative not to scale

Three causes

31

Amount needed to cover payment of claims and other

liabilities

Illustrative not to scale

1. Liabilities exaggerated

• Discounting close to risk free• Risk Margin

Three causes

32

Regulatory Technical provisions

(Amount needed to cover payment of claims and other

liabilities)

Company target Solvency buffer

Company surplus

1. Liabilities exaggerated• Risk Margin• Discounting close to risk free

3. Artificial volatility• Larger buffers than necessary

2. Excessive SCR requirements • Wrongly based on “trading risk”

instead of “long-term investment risk”

Total amount needed by SII

can be excessive

Regulatory SolvencyCapital

Requirement(SCR)

Illustrative not to scale

Agenda

33

Successful launch

Impact survey

Concerns about excessive capital

Case studies

Solvency II reviews

1

2

3

4

5

34

Long-term risk ≠ trading

Long-term investment ≠ trading

Importance of measuring risk correctly

35

Trader can be forced to sell entire portfolio after worst-case, 1-year price fall

Insurer can invest for 10 years and get dividends

Insurer can invest for 10 years, get dividends and use pooling/smoothing, diversifying across customers/time

1

2

3

-43%

-26%

+9%

1-in-200 outcome

Equity example

Analysis based on 100 years of US stock market data

Credit example

Importance of measuring risk correctly

36

Forced sales COULD NOT be avoided so exposure to losses was on price drops caused by spread changes which were

very high

Forced sales COULD be avoided so exposure to losses was on actual

defaults which were very low

Long-term investor losses

Short-term investor (“Trader”) losses

0.2% losses*

30% losses**

Losses during financial crisis (2007-2008)Example for AA corporate bond portfolio

* Assumes a 50% recovery rate. Actual defaults were about 0.4% in 2008** Assumes a long-term bond portfolio

Excessive capital requirements

37

Simple, long-term product with guarantee€10,000 single premiumFully matched (no interest rate risk)Standard Formula and Volatility AdjustmentOnly invested in A-rated corporate bonds Risk Margin = 40% of SCR in line with EU average for life companies

CASE STUDY

Total additional amount shareholders need to inject

Preliminary analysis

1 Risk-free rate is 0.50% Credit spread is 1.25%Volatility adjustment is 0.04% (Dec. 2017)Charges are 0.50%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Guaranteed product

Volatilitybuffer

Solvencycapitalrequirement(SCR)

Risk Margin

1

Total additional amount shareholders need to inject

Preliminary analysis

1 Risk-free rate is 0.50% Credit spread is 1.25%Volatility adjustment is 0.04%(Dec. 2017)Charges are 0.50%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Guaranteedproduct

Guaranteedproduct

(Solvency I)

Correct capitalrequirements

Volatility buffer

Solvency capitalrequirement(SCR)Risk Margin

1

Unnecessarily high capital = unnecessary impact

40

Too highsolvency capital

and/or

Higher premiums

or charges

Lower benefits paid

Fewer products available

Less optimal long-term

investmente.g. equities

Procyclical behaviour

and/or

Solvency II = shifting the risks on to individuals

41

RISK

INSURANCE COMPANY

Further work needed

42

Industry, academics, supervisors and regulators need to work together to fully understand different measures & their impact

Examine improvements:

VA/MA/dynamic VA/Country adjustments

Risk Margin

SCR for investments

Test against different products & market conditions

Agenda

43

Successful launch

Impact survey

Concerns about excessive capital

Case studies

Solvency II reviews

1

2

3

4

5

A long journey … and it is not over yet

44

Application of Solvency II

(January 2016) Infrastructure

(April 2016)

STS securitisations

(June 2016)2018 review (Level 2)

(December 2018)EC fitness check on supervisory reporting

(December 2019) 2020 review (Levels 1+2)

(December 2020)

EC action can make a difference

45

% of respondents who said EC action has had/would have positiveimpact on investment

3%

16%

29%

36%

43%

43%

0% 10% 20% 30% 40% 50%

ELTIFs

STS securitisation

Unlisted equity

Unrated debt

Infrastructure

Long-term equity

On the path to improvement

46

Solvency II doesn’t reflect long-term

business

PROBLEMSSOLUTIONSSOLUTIONS

Proportionality/

reporting

Other technical issues

Infrastructure

STS securitisations

Capital Markets Union

Equity (unlisted and listed)

Unrated debt

2018 review

Risk Margin — cost of capital

Simplifications

Address flaws/inconsistencies

Other long-term investments

2020 review

Risk Margin

Discount rates (MA, VA, etc.)

Streamlining

Address flaws/inconsistencies

IA|BE – General Assembly – 47 – 13/09/2018

Fabian de Bilderling

Night of the Actuaries 2018

IA|BE – General Assembly – 48 – 13/09/2018

Assemblée Générale -Algemene Vergadering

Jean-François Hannosset

IA|BE – General Assembly – 49 – 13/09/2018

Cocktail

![Presentatie Geothermie 12 maart 2019 .pptx [Alleen-lezen]Microsoft PowerPoint - Presentatie Geothermie 12 maart 2019_.pptx [Alleen-lezen] Author: Z026198 Created Date: 3/13/2019 2:04:07](https://img.dokumen.tips/doc/110x75/5fcefaf5cae02647b819b9d5/presentatie-geothermie-12-maart-2019-pptx-alleen-lezen-microsoft-powerpoint-.jpg)

![[MS-PPTX]: PowerPoint (.pptx) Extensions to the Office ...interoperability.blob.core.windows.net/files/MS-PPTX/[MS-PPTX... · 1 / 76 [MS-PPTX] — v20140428 PowerPoint (.pptx) Extensions](https://img.dokumen.tips/doc/110x75/5ae7f6357f8b9a6d4f8ed3b3/ms-pptx-powerpoint-pptx-extensions-to-the-office-ms-pptx1-76-ms-pptx.jpg)